Fscal Transparency - Richard Adorjan, Hungary (English)

15

1 The Role Of Institutions In Hungary In Budget Making Process 9th Annual Meeting of MENA-SBO 12-13 October, Kuwait City Richárd Adorján Dr. Deputy State Secretary

-

Upload

oecd-governance -

Category

Government & Nonprofit

-

view

75 -

download

1

Transcript of Fscal Transparency - Richard Adorjan, Hungary (English)

1

The Role Of Institutions In Hungary In Budget Making Process

9th Annual Meeting of MENA-SBO

12-13 October, Kuwait City

Richárd Adorján Dr. Deputy State Secretary

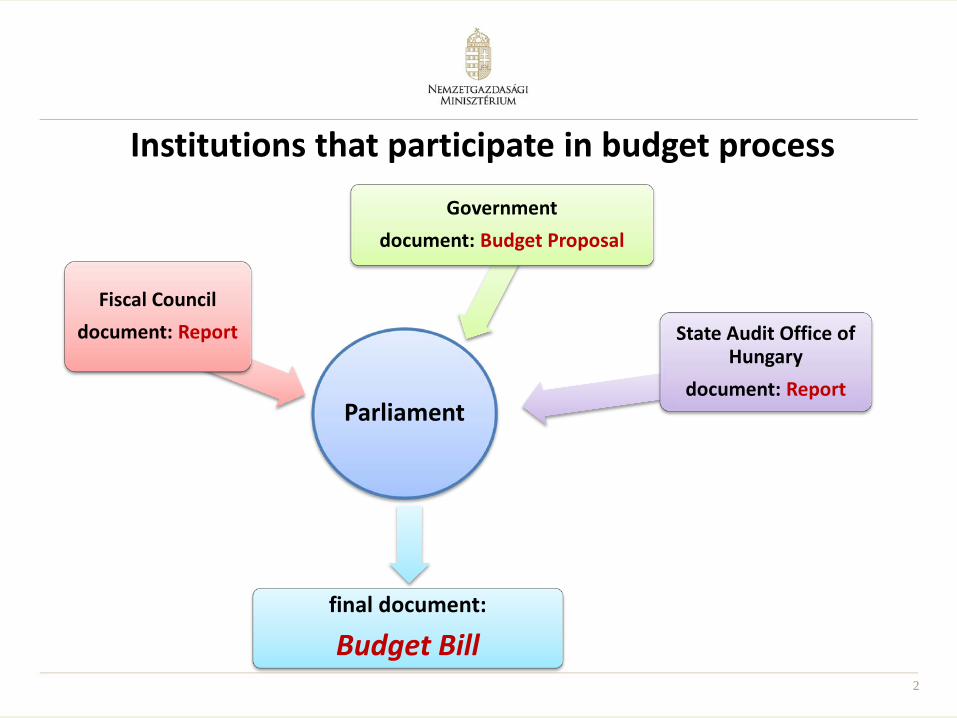

2

Institutions that participate in budget process

Parliament

Fiscal Council document: Report

Government document: Budget Proposal

State Audit Office of Hungary

document: Report

final document:

Budget Bill

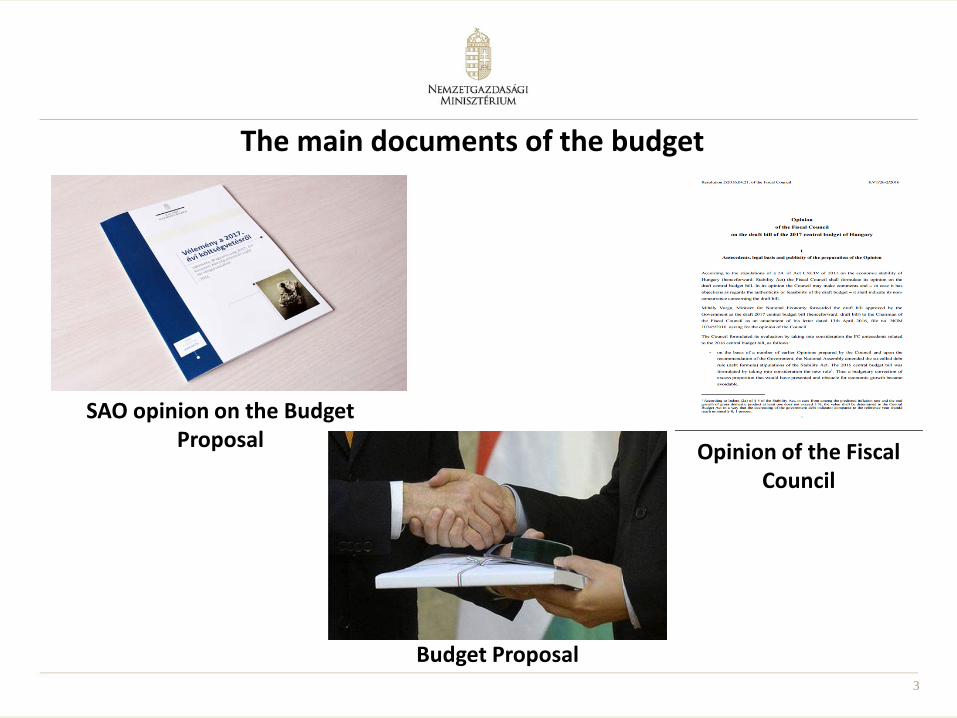

3

The main documents of the budget

Budget Proposal

SAO opinion on the Budget Proposal Opinion of the Fiscal

Council

4

Role of Government

• the Government is the most important body of executive power

• the primary director of public administration

• it implements decisions made by Parliament, as the legislative organ,

• it pursues realization of the goals laid out in the Government’s programme.

• the Government responsibilities and competences shall include all matters not expressly delegated by the Fundamental Law or other legislation to the responsibilities and competences of another body.

• the Hungarian Government comprises the Prime Minister and government ministers.

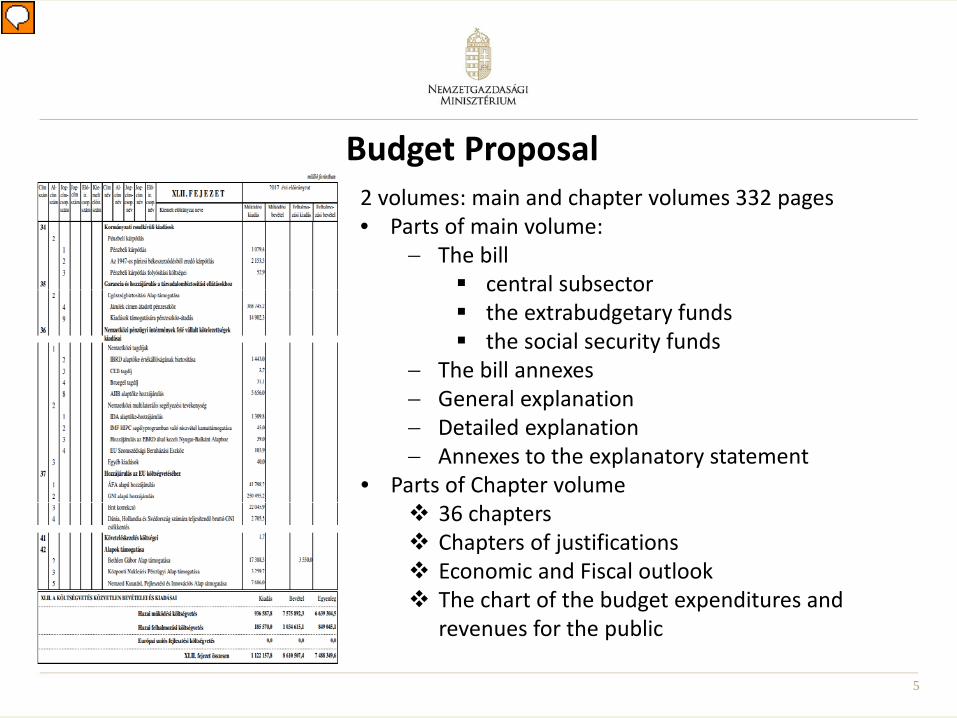

5

Budget Proposal 2 volumes: main and chapter volumes 332 pages • Parts of main volume:

− The bill central subsector the extrabudgetary funds the social security funds

− The bill annexes − General explanation − Detailed explanation − Annexes to the explanatory statement

• Parts of Chapter volume 36 chapters Chapters of justifications Economic and Fiscal outlook The chart of the budget expenditures and

revenues for the public

Presenter

Presentation Notes

The Bill contains: Balance and the revenues and expenditures gross sum The amount of balance The debt The provisions relating to state assets Special powers rights of the Minister for Public Finances and managing chapter of the head of departments Relationship between the local government and central government Rules on the use of EU funds The Bill annexes (9 pieces): The central government expenditure and revenue appropriations EU appropriations for the 2014-2020 programming period Normatives for some social, performing public duties child protection institutions providing personal care General explanation: Economic and fiscal policy major measures Detailed explanation: Explanation to the budget bill Annexes to the explanatory statement: The main features of economic development The main characteristics of the general government (cash basis), economic balance sheet, consolidated expenditures, functional balance sheet Financial relations to European Union the general government deficit and debt of the European Union methodology Explanation for chapters Budget of budgetary institutions; chapter-managed appropriations for sectoral programmes and other programmes under the discretion of the chapter head (minister); EU projects managed by the chapter; centrally managed appropriations, mainly entitlement programmes, transfers to the extrabudgetary funds, to the social security funds and to local government, special larger investment projects and interest payments; and Medium term projection for the budget, central revenues, including tax and non-tax revenues

6

Role of Fiscal Council • imakes comments on the planning and execution of the

budget, the use of public funds and the state of public finances

• makes comments on any issues related to the planning and execution of the budget or the use of public funds

• evaluates the state budget and its execution and developments of government debt

• supports Parliament’s legislative activities

• the acceptance of budget bill is dependent on the approval of the Fiscal Council, thus it has veto power over budget laws

• the State President could dissolve Parliament if it fails to pass a budget law by the end of March (for any reason), so there is time pressure to get the approval of the Fiscal Council (two out of three council members is needed for approval)

7

Opinion of the Fiscal Council on the draft bill of the 2017 central budget of Hungary

• 13 pages • Contents:

I. Antecedents, legal basis and publicity of the preparation of the Opinion

II. The Council’s Resolution III. Justification

o The Authenticity of the Draft o The Expected Implementation of Budget 2015

and 2016 o Evaluation of the Goals and Conditions of

Budget 2017 Expected Macroeconomic Indicators Revenues and Expenditures of the Central

Budget Public Finance Deficit Government Debt

o Other

Presenter

Presentation Notes

FC resolution Budget 2017: „The Council’s Resolution At its meeting held on 21st April 2016 – on the basis of the documents submitted by the Government about the draft bill of year 2017 central budget – the Council formulated the following Opinion: As regards the authenticity and feasibility of the draft of the 2017 central budget bill the Council has no such fundamental objections that would justify the indication of nonconcurrence concerning the document submitted for formulating and opinion. According to the Council’s judgement the draft bill is based on a well-established macroeconomic forecast. Following the dynamism of economic growth since 2013 – the annual 2, 9 percent in year 2015 – the 2016 economic growth might be around 2, 5 percent. The 2017 budget is built on a 3, 1 percent economic growth that – considering the expected increase of incoming EU funds and other growth factors, primarily that of consumption – can be regarded as solidly founded. The revenue and expenditure appropriations are basically in harmony with the macroeconomic forecast, the preliminary implementation of year 2015 and the expected trends of 2016 as well as with the governmental actions listed in the draft bill. However, even with these considerations the increase of the VAT and personal income tax appropriation – compared to the preceding year – can be regarded as stretched and the further increase of the efficiency of tax collection is necessary to ensure the implementation of the increased appropriations. On the basis of the macroeconomic course and the budget appropriations the Council establishes that the 2, 4 percent GDP proportionate targeted deficit for 2017 – calculated by EU methodology – is in harmony with the economic processes described by the draft budget bill and the planned revenue and expenditure appropriations. The targeted public finance deficit is in harmony with the correction arm of the fiscal regulations of the European Union and Point b) Indent (2) of § 3/A of the Stability Act. However, with the increase of the targeted deficit the structural deficit shall also increase. Hence, the Council considers it justified that in the justification part of the bill the Government should present that the targeted deficit according to the budget bill meets the criteria of the EU concerning the structural deficit as well as the requirement stipulated by Point a) Indent (2) . § 3/A of the Stability Act arising from the above regulation. The Council considers it positive that the central budget separates the operational and accumulation budgets as well as that of the EU developments, as this contributes to the transparency of the processes and the separation of costs laying the foundations for long-term growth from current expenditures. The Council finds that the trends of the year 2016 debt indicator (73, 5 percent of the GDP) and of the year 2017 debt indicator (71, 9 % of the GDP) calculated at unchanged rate and according to the stipulations of the Stability Act, are in harmony with the economic and budgetary processes expected for year 2016 and those planned for year 2017. This means that the debt rule stipulated by the Basic Law of Hungary shall be met. The planned and expected measure of the debt-rate decrease is in harmony also with the stipulation of the European Union as regards government debt. The Council deems it necessary that the draft budget bill provided three types of reserve systems for unforeseen tasks, expenditures or possible arrears if revenues - i.e. beyond the HUF 120 billion reserved for Extraordinary Governmental Measures, the HUF 50 billion reserved for the Country Protection Fund and the chapters - shall create stability reserves as well, similarly to the practice introduced in 2016. Apart from this, from the aspect of government debt rule implementation, the planned decrease of the government debt indicator means an implicit reserve as it is higher by 1, 5 percent that the 0, 1 percent stipulated by the Stability Act. According to the Council, from the aspect of the 2017 targeted deficit it is not the prescription of Point b) Indent (2) § 3/A about the 3 percent ceiling of the GDP but the requirement according to Point a), Ident (2) of § 3/A that has the stricter stipulations as regards the determination of the mid-range budgetary goal. Thus the Council would deem it practical if in the Justification section of the bill the Government presented, with regard to what type and measure of risks had it planned the reserves. The Council hereby shall authorise its Chairman to publish its Opinion as regards the draft budget bill and present the Opinion before the National Assembly, with regards to its relations concerning the submitted draft bill.”

8

Role of State Audit Office of Hungary

• the State Audit Office of Hungary is the supreme financial and economic audit institution of the National Assembly

• the State Audit Office is the only non-governmental body that has an oversight of the budget from January to December

• the SAO also prepares analyses on budgetary processes of the current year and the year preceding the current year

• It has a comprehensive and objective view on the final accounts bill, the reliability of data in the budget

• it enforces the provisions of the Fundamental Law pertaining to public debt and it monitors the calculations underlying the planned public debt figure

• it provides an opinion on the budget proposal, and also prepares analyses for the Fiscal Council

9

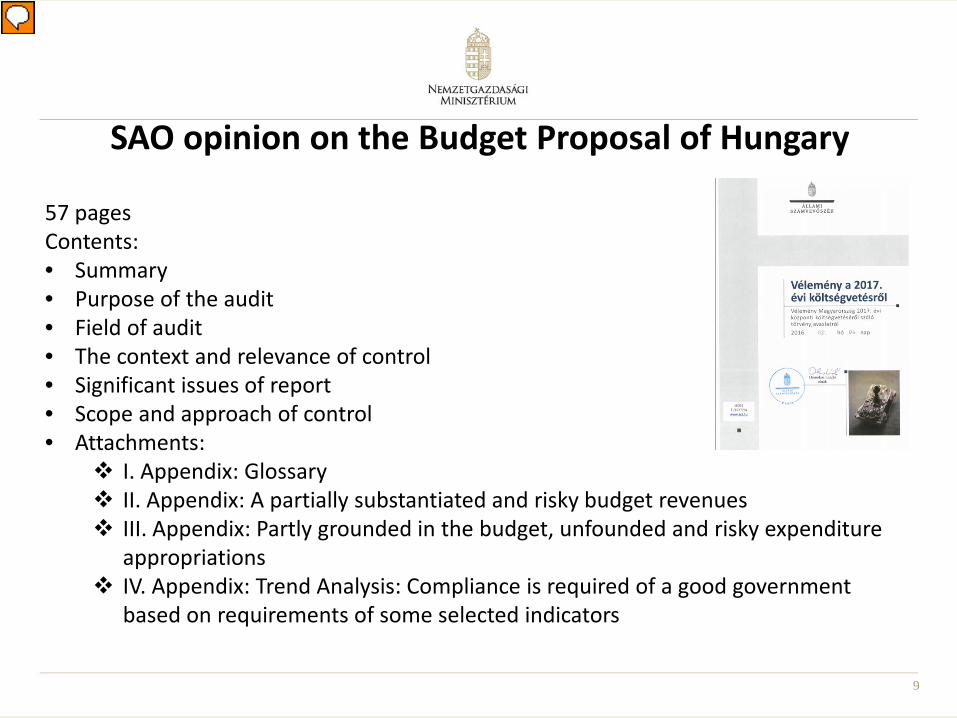

SAO opinion on the Budget Proposal of Hungary

57 pages Contents: • Summary • Purpose of the audit • Field of audit • The context and relevance of control • Significant issues of report • Scope and approach of control • Attachments:

I. Appendix: Glossary II. Appendix: A partially substantiated and risky budget revenues III. Appendix: Partly grounded in the budget, unfounded and risky expenditure

appropriations IV. Appendix: Trend Analysis: Compliance is required of a good government

based on requirements of some selected indicators

Presenter

Presentation Notes

The 2017 budget appropriation bill is substantiated, in case of the realization of the macroeconomic forecasts taken into account while planning the budget the revenue appropriation is feasible – concluded the State Audit Office of Hungary. The appropriation bill on Hungary’s 2016 central budget is in accordance with the public debt requirement set down in the Fundamental Law and also with the requirements of the legislation governing public finances with the exception of one provision. In its opinion the SAO draws the attention to that the multi-element system of budgetary reserves, as well as the expansion of opportunities for budget restructuring improved the security and flexibility of budget implementation, the management of the risks revealed, as well as that the triple grouping of the incomes and revenues further enhances the transparency of the budget. In fulfilment of its statutory duty, the SAO has prepared its opinion on the appropriation bill on Hungary’s 2017 central budget. The opinion of the SAO is about a given status of the drafting the budget. SAO audit is aiming at to contribute to the adoption of a substantiated budget capable of managing risks arising realistically through enacting the missing legal regulations and adopting the amendment proposals. The SAO qualified the 99.9 per cent of the audited revenue appropriations as substantiated, 0.1 per cent of them as partly substantiated, the 99.2 per cent of the expenditure appropriations as substantiated, 0.5 per cent of expenditure appropriations as partly substantiated and 0.3 per cent of them as unsubstantiated. The audit considers risky the realization of revenue appropriations amounting to EUR 5.6 billion and noted the risk that certain expenditures with a total of £ 62.7 billion exceeds the amount of the proposed appropriations, though the reserves provide opportunity to the treatment thereof. In its opinion, the SAO draws the attention to that in terms of meeting the budgetary target it is an overall risk that 53.3% of the expenditure appropriations is of the so-called top open that can be exceeded without a change in the law. Based on substantive testing of all appropriations, the SAO found that four of these were drafted without due substantiation. The SAO found, that the preparation of the budget appropriation bill, its compilation, structure and content was in line with the prescriptions of the relevant legal regulations. A new element enhancing the transparency of the budget is included in the bill, i.e. the triple grouping of revenue and expenditure appropriations (operational, domestic accumulation, EU development revenues and expenditures) The 2017 budget appropriation bill sets out HUF 1166.4 billion deficit of the central subsystem, which is composed - in addition to the planned break-even operating budget – the planned deficit of the accumulation budget of HUF 472.4 billion and the EU development budget is HUF 694.0 billion. According to the EU methodology this corresponds to a 2.4% deficit. Based on the date of the budget appropriation bill the national debt to GDP ratio will decline to 71.9% by the end of 2017, showing a 1.6 percentage point decrease compared to the expected 73.5% in the last day of the year 2016. Accordingly, the budget appropriation bill meets the public debt rule set out in the Fundamental Law. In its opinion the SAO points out that at the same time the structural balance of the general government rate is less favourable than the medium-term fiscal deficit target, which is not in accordance with the realization of the medium-term budgetary objective despite of what is stated in the stability law, but this does not pose a risk in terms of the execution of the budget. �

10

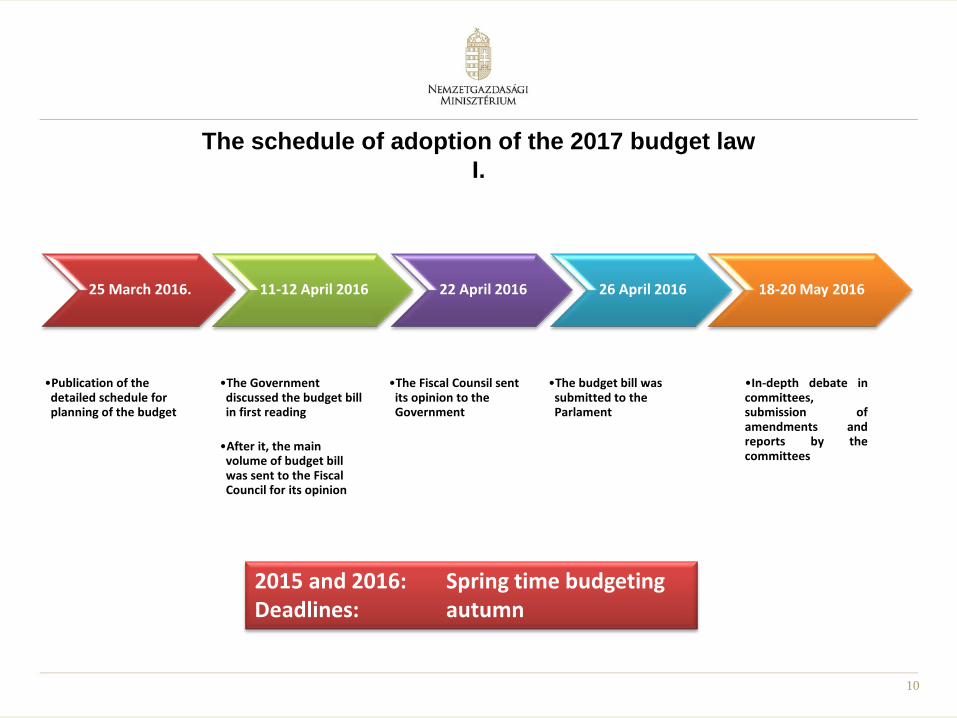

The schedule of adoption of the 2017 budget law I.

25 March 2016.

•Publication of the

detailed schedule for planning of the budget

11-12 April 2016

•The Government

discussed the budget bill in first reading

•After it, the main volume of budget bill was sent to the Fiscal Council for its opinion

22 April 2016

•The Fiscal Counsil sent

its opinion to the Government

26 April 2016

•The budget bill was

submitted to the Parlament

18-20 May 2016

•In-depth debate in committees, submission of amendments and reports by the committees

2015 and 2016: Spring time budgeting Deadlines: autumn

11

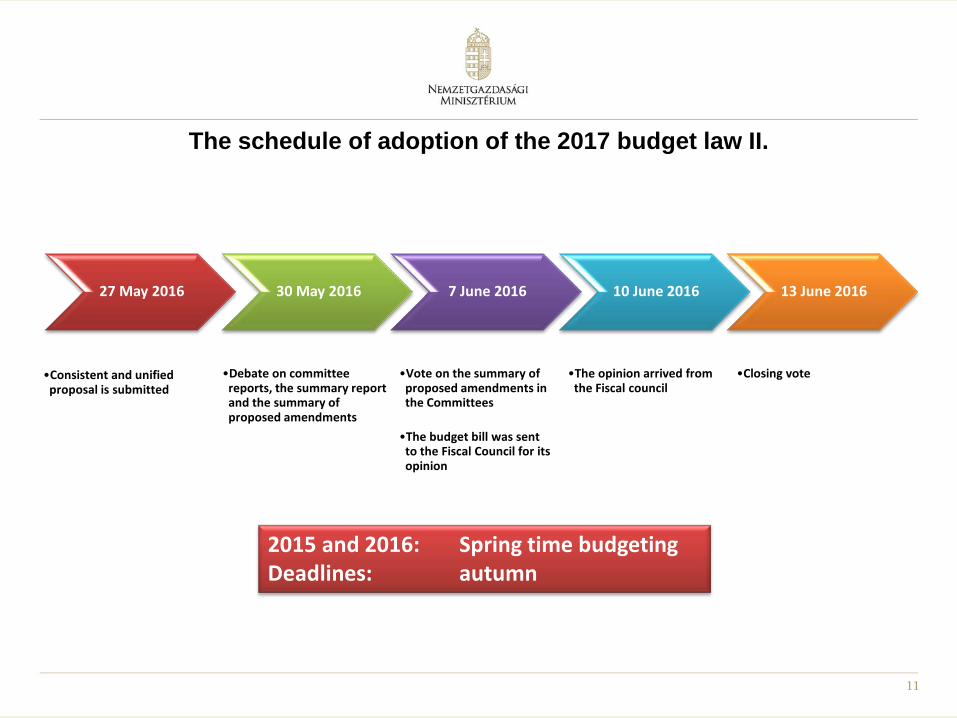

The schedule of adoption of the 2017 budget law II.

27 May 2016

•Consistent and unified proposal is submitted

30 May 2016

•Debate on committee reports, the summary report and the summary of proposed amendments

7 June 2016

•Vote on the summary of proposed amendments in the Committees

•The budget bill was sent to the Fiscal Council for its opinion

10 June 2016

•The opinion arrived from the Fiscal council

13 June 2016

•Closing vote

2015 and 2016: Spring time budgeting Deadlines: autumn

12

Fiscal Councils in EU Country name Name of the Fiscal Council Start of activity (Year)

Austria Fiscal Advisory Council 2002 Belgium Federal Planning Bureau 1994 Croatia Fiscal Policy Commission 2013 Cyprus Fiscal Council 2014 Denmark Danish Economic Council 1962 Estonia Fiscal Council 2014 Finland National Audit Office of Finland 2013 France High Council of Public Finance 2013 Germany German Council of Economic Experts 1963 Greece Parliamentary Budget Office 2010 Hungary Fiscal Council 2009 Ireland Irish Fiscal Advisory Council 2011 Italy Parliamentary Budget Office 2014 Latvia Fiscal Council 2014 Lithuania Budget Policy Control Institution 2015 Luxembourg Conseil national des finances publiques 2014 Netherlands Netherlands Bureau for Economic Policy Analysis 1945 Portugal Portuguese Public Finance Council 2012 Romania Fiscal Council 2010 Serbia Fiscal Council 2011 Slovak Republic Council for Budget Responsibility 2011 Slovenia Fiscal Council 2009 Spain Independent Authority of Fiscal Responsibility 2014 Sweden Swedish Fiscal Policy Council 2007 United Kingdom Office for Budget Responsibility 2010

Source: Strengthening Post-Crisis Fiscal Credibility: Fiscal Councils on the Rise—A New Dataset; Xavier Debrun and Tidiane Kinda

13

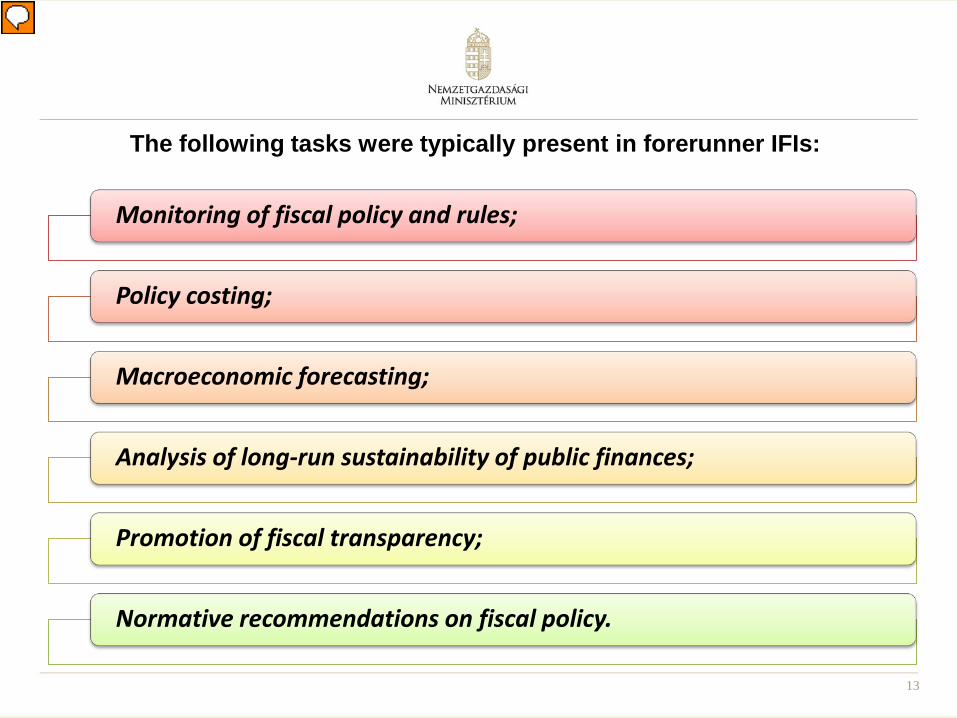

The following tasks were typically present in forerunner IFIs:

Monitoring of fiscal policy and rules;

Policy costing;

Macroeconomic forecasting;

Analysis of long-run sustainability of public finances;

Promotion of fiscal transparency;

Normative recommendations on fiscal policy.

Presenter

Presentation Notes

IFI = Independent fiscal institutions

14

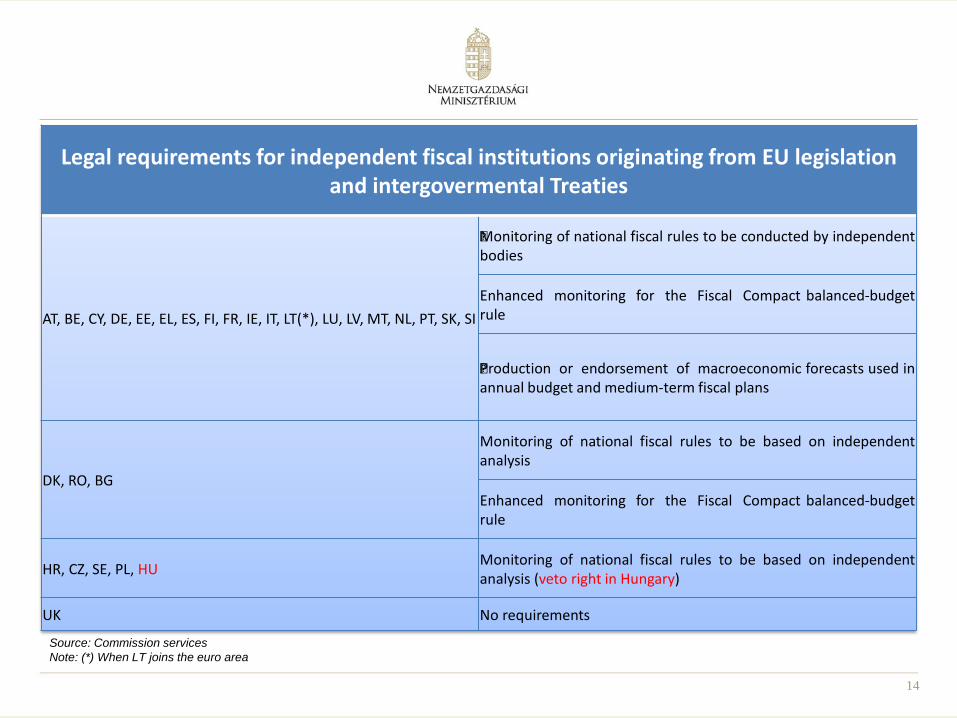

Legal requirements for independent fiscal institutions originating from EU legislation and intergovermental Treaties

AT, BE, CY, DE, EE, EL, ES, FI, FR, IE, IT, LT(*), LU, LV, MT, NL, PT, SK, SI

�Monitoring of national fiscal rules to be conducted by independent bodies

Enhanced monitoring for the Fiscal Compact balanced-budget rule

�Production or endorsement of macroeconomic forecasts used in annual budget and medium-term fiscal plans

DK, RO, BG

Monitoring of national fiscal rules to be based on independent analysis

Enhanced monitoring for the Fiscal Compact balanced-budget rule

HR, CZ, SE, PL, HU Monitoring of national fiscal rules to be based on independent analysis (veto right in Hungary)

UK No requirements

Source: Commission services Note: (*) When LT joins the euro area

15

THANK YOU FOR YOUR ATTENTION!