For personal use only - ASX · 2016 2021 ion Bank Debt Senior Notes 1,158 (29) 55 1,184 0 500 1,000...

30

© 2011 Boart Longyear. All rights reserved. TM 1 © 2009 Boart Longyear. All rights reserved. BOART LONGYEAR – 1H 2011 PERFORMING TO PLAN AUGUST 2011 © 2011 Boart Longyear. All rights reserved. Craig Kipp - CEO Joe Ragan - CFO Jay Clement - IR For personal use only

Transcript of For personal use only - ASX · 2016 2021 ion Bank Debt Senior Notes 1,158 (29) 55 1,184 0 500 1,000...

© 2011 Boart Longyear. All rights reserved.

TM

1

© 2009 Boart Longyear. All rights reserved.

BOART LONGYEAR – 1H 2011

PERFORMING TO PLAN

AUGUST 2011 © 2011 Boart Longyear. All rights reserved.

Craig Kipp - CEO Joe Ragan - CFO Jay Clement - IR

For

per

sona

l use

onl

y

TM

© 2011 Boart Longyear. All rights reserved.

2

IMPORTANT NOTICE AND DISCLAIMER

• This presentation has been prepared by Boart Longyear Limited, ABN 49 123 052 728 (Boart Longyear or the

Company). It contains general information about the Company’s activities as at the date of the presentation. It is

information given in summary form and does not purport to be complete. The distribution of this presentation in

jurisdictions outside Australia may be restricted by law, and you should observe any such restrictions.

• This presentation is not, and nothing in it should be construed as, an offer, invitation or recommendation in respect of

securities, or an offer, invitation or recommendation to sell, or a solicitation of an offer to buy, securities in any

jurisdiction. Neither this document nor anything in it shall form the basis of any contract or commitment. This

presentation is not intended to be relied upon as advice to investors or potential investors and does not take into

account the investment objectives, financial situation or needs of any investor. All investors should consider such

factors in consultation with a professional advisor of their choosing when deciding if an investment is appropriate.

• The Company has prepared this presentation based on information available to it, including information derived from

public sources that have not been independently verified. No representation or warranty, express or implied, is

provided in relation to the fairness, accuracy, correctness, completeness or reliability of the information, opinions or

conclusions expressed herein.

• This presentation includes forward-looking statements within the meaning of securities laws. Any forward-looking

statements involve known and unknown risks and uncertainties, many of which are outside the control of the Company

and its representatives. Forward-looking statements may also be based on estimates and assumptions with respect to

future business decisions, which are subject to change. Any statements, assumptions, opinions or conclusions as to

future matters may prove to be incorrect, and actual results, performance or achievement may vary materially from any

projections and forward-looking statements.

• Due care and attention should be undertaken when considering and analysing the financial performance of the

Company.

• All references to dollars are to United States currency unless otherwise stated.

For

per

sona

l use

onl

y

© 2011 Boart Longyear. All rights reserved.

TM

3

33

74

0

50

100

1H 2010 1H 2011

98

165

0

100

200

1H 2010 1H 2011

685

959

0

500

1000

1H 2010 1H 2011

• 40% Global Growth: Both businesses, all regions

• New Products: Market share increases

1H 2011 - RESULTS SUMMARY (US $M)

Revenue

EBITDA

• Pricing and margin recovery

• Excellent cost control – Lower SG&A percentage

• Increased dividend by 129%: 2.1 to 4.8 cents

• 13.5% ROE1

Net Profit After Tax (NPAT)

12% 16%

1. Average 1H Equity

5% 8%

14% 17%

For

per

sona

l use

onl

y

© 2011 Boart Longyear. All rights reserved.

TM

4

TECHNOLOGY LEADERSHIP

• Technology and safety upgrades

• More metres per person

• In front of expected demand through 2012:

• Rigs

• Labour

1H 2011 • 55 new rigs

• 29 decom. rigs

26 net adds

7UMX & 9UMX

Diamond Bits

Patents

Awarded Trademarks Patent

Applications

1H 2011

Roller Latch

Underground Head

Assembly

Surface Rock Drill &

Blast Rods

Reverse Circulation Rig

Rock Drill &

Blast Bits

Rod Lifter

Split Tube Loader

FY 2011 Est. • 80 new rigs

• 53 decom. rigs

27 net adds

For

per

sona

l use

onl

y

© 2011 Boart Longyear. All rights reserved.

TM

5

50

101

0

25

50

75

100

125

1H 2010 1H 2011

250 300

0

100

200

300

400

2016 2021U

S$ m

illio

n

Bank Debt Senior Notes

1,158 (29) 55 1,184

0

500

1,000

1,500

Dec2010

Decoms Adds Jun 2011

0%

50%

100%

150%

200%

1H 2010 1H 2011

EXECUTING GROWTH STRATEGY

Manufacturing: Capacity

Rig Upgrades: Capacity & Productivity

CAPEX: Supporting Growth

Through the Cycle Capital Structure

Rig Count

Rod Capacity (Indexed to 2010)

Debt Maturity

CAPEX

US

$ m

illio

n

For

per

sona

l use

onl

y

TM Company confidential – unauthorized use or distribution prohibited

© 2011 Boart Longyear. All rights reserved.

6

Mine Site - Northern Canada

FINANCIAL OVERVIEW

© 2011 Boart Longyear. All rights reserved.

For

per

sona

l use

onl

y

© 2011 Boart Longyear. All rights reserved.

TM

7

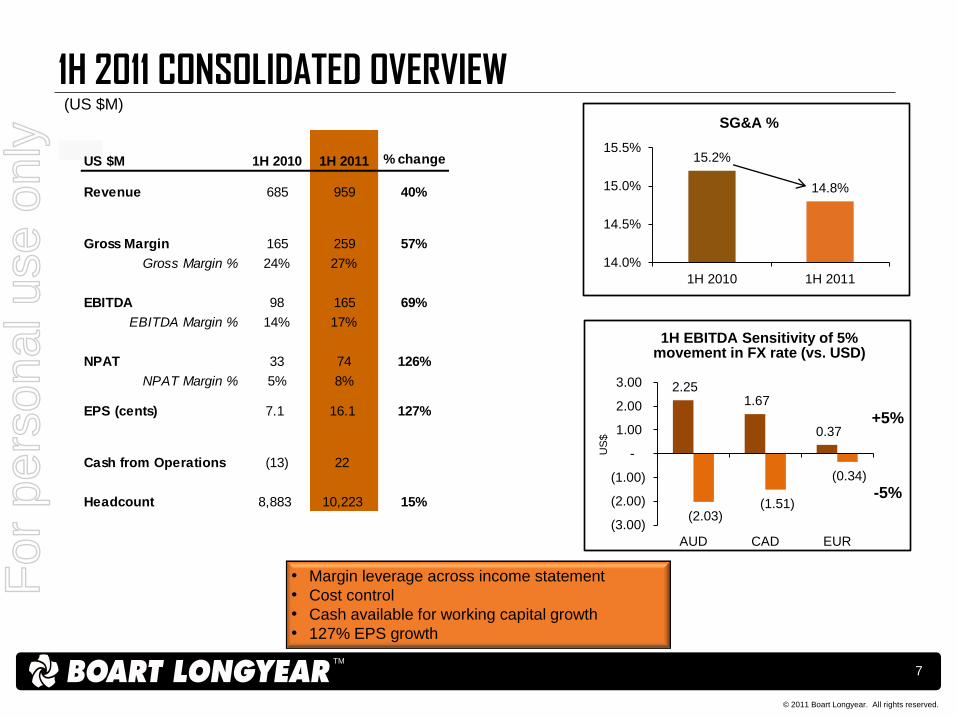

• Margin leverage across income statement

• Cost control

• Cash available for working capital growth

• 127% EPS growth

1H 2011 CONSOLIDATED OVERVIEW (US $M)

US $M 1H 2010 1H 2011 % change

Revenue 685 959 40%

Gross Margin 165 259 57%

Gross Margin % 24% 27%

EBITDA 98 165 69%

EBITDA Margin % 14% 17%

NPAT 33 74 126%

NPAT Margin % 5% 8%

EPS (cents) 7.1 16.1 127%

Cash from Operations (13) 22

Headcount 8,883 10,223 15%

15.2%

14.8%

14.0%

14.5%

15.0%

15.5%

1H 2010 1H 2011

SG&A %

1H EBITDA Sensitivity of 5% movement in FX rate (vs. USD)

+5%

-5%

2.25 1.67

0.37

(2.03) (1.51)

(0.34)

(3.00)

(2.00)

(1.00)

-

1.00

2.00

3.00

AUD CAD EUR

US

$

For

per

sona

l use

onl

y

TM Company confidential – unauthorized use or distribution prohibited

© 2011 Boart Longyear. All rights reserved.

8

685

165 59 49

959

1H 2010 Volume / Mix Price FX 1H 2011

Revenue Bridge (US $M)

1H 2011 CONSOLIDATED OVERVIEW

98

59

59 (32)

(35)

9 7

165

1H 2010 Volume / Mix Price SG&A Material / LabourInflation

FX Other 1H 2011

EBITDA Bridge

For

per

sona

l use

onl

y

© 2011 Boart Longyear. All rights reserved.

TM

9

• Positives: Pricing and Productivity

• Challenges: Some inflation margin erosion and labour availability

• Selective on Pricing, Terms, and Locations

• Ramp up costs continue

DRILLING SERVICES

Drilling Services

US $M 1H 2010 1H 2011 % change

Revenue 511 682 33%

EBITDA 91 129 42%

EBITDA Margin % 18% 19%

91

54 24 (31)

(15) 6

129

1H 2010 Pricing Volume / Mix Material /LabourInflation

SG&A Fx 1H 2011

(US

$ M

)

(US $M)

For

per

sona

l use

onl

y

© 2011 Boart Longyear. All rights reserved.

TM

10

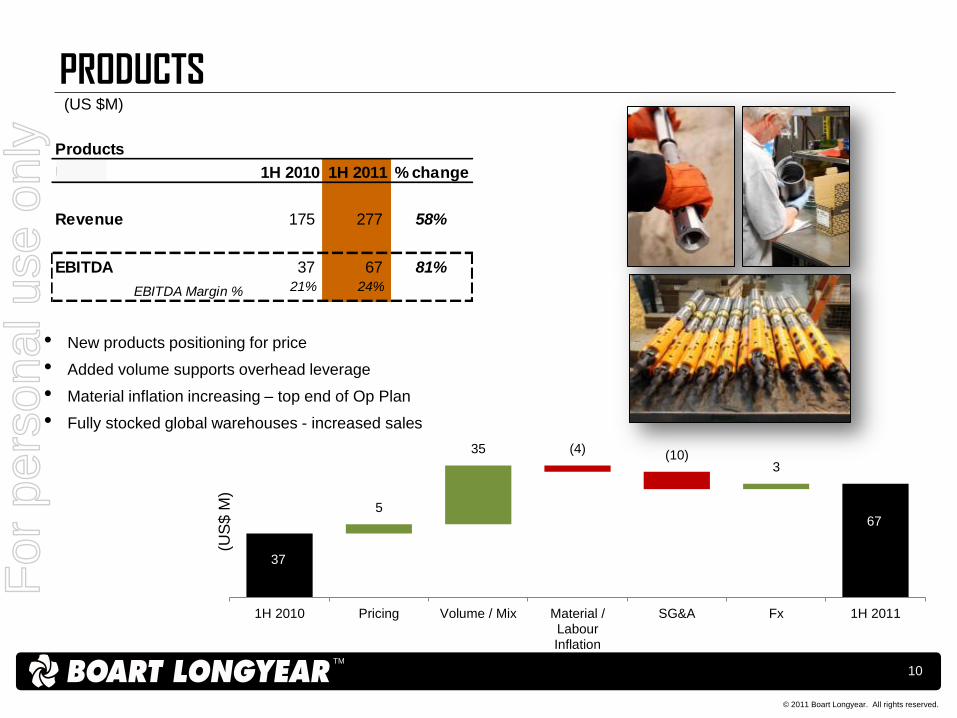

PRODUCTS

Products

US $M 1H 2010 1H 2011 % change

Revenue 175 277 58%

EBITDA 37 67 81%

EBITDA Margin % 21% 24%

• New products positioning for price

• Added volume supports overhead leverage

• Material inflation increasing – top end of Op Plan

• Fully stocked global warehouses - increased sales

37

5

35 (4) (10) 3

67

1H 2010 Pricing Volume / Mix Material /LabourInflation

SG&A Fx 1H 2011

(US

$ M

)

(US $M)

For

per

sona

l use

onl

y

© 2011 Boart Longyear. All rights reserved.

TM

11

1H 2011: CASH AND DEBT

1H 2011 Net Debt Bridge

1H 2011 Cash Flow Cash flow and capital

structure supporting growth

(US $M)

95

85

152 (130)

(101)

(16) (16)

69

0

50

100

150

200

250

300

350

Cash BalanceDec 2010

Net Borrowings Cash from Operations(before WC)

Working Capital CAPEX Dividends Other Cash BalanceJun 2011

154

267 (165) 130

10 8

101 16

13

-

50

100

150

200

250

300

Net DebtDec 2010

WorkingCapitalChange

EBITDA Net CashInterest

Cash Tax CAPEX Dividends Other Net DebtJun 2011

For

per

sona

l use

onl

y

© 2011 Boart Longyear. All rights reserved.

TM

12

1.2x

0.0x

0.5x

1.0x

1.5x

2.0x

2.5x

3.0x

3.5x

4.0x

1

Gro

ss D

eb

t /

EBIT

DA

16.4x

0.0x

2.0x

4.0x

6.0x

8.0x

10.0x

12.0x

14.0x

16.0x

18.0x

1

EBIT

DA

/ In

tere

st

250 300

0

50

100

150

200

250

300

350

2012 …… 2016 …… 2021

DEBT (PRO-FORMA JUNE 2011)

Revolver Covenant

Compliance

3.5x Max.

Leverage

Interest Cover

3.0x Min.

Interest Cover

Through the Cycle Capital Structure

Senior Notes

(New – March 2011)

Debt Maturity – New 2011 Capital Structure

Bank Debt

(New - July 2011)

1. 2X Trough EBITDA, assumes $50M cash

(US $M)

• Over US$200M undrawn • Staggered maturities • All IPO debt facilities now retired

For

per

sona

l use

onl

y

© 2011 Boart Longyear. All rights reserved.

TM

13

2011 GROWTH “ORGANIC” SPEND

17%

21%

13%

49%

0%

20%

40%

60%

80%

100%

120%

2011 - $210 million

New Rigs & Upgrades

Rig Rebuilds

Technology

Mfg. Capacity

Fleet Optimisation • More metres per shift • More metres per rig, per person • Safety upgrades

Drive ROI Performance • New drilling technologies driving productivity • New geographies – Products & Services • Adding manufacturing and drilling capacity

Drilling Services

Products and

Corporate

Technology • New product development (R&D) • Global IT systems

Rebuild • Rebuild rigs after ~ 5 years

Mfg. capacity • Manufacturing, outsourcing,

warehousing and distribution

(US $M)

For

per

sona

l use

onl

y

© 2011 Boart Longyear. All rights reserved.

TM

14

74

22

0

10

20

30

40

50

60

70

80

NPAT Dividend

DIVIDEND PAYMENT

30% Payout Ratio

35% Franked

1H 2011 (US $M)

Record Date: 9 September 2011

Payment Date: 7 October 2011

2.1

3.4

4.8

1H 2010 2H 2010 1H 2011

Dividend History (US cents)

For

per

sona

l use

onl

y

TM Company confidential – unauthorized use or distribution prohibited

© 2011 Boart Longyear. All rights reserved.

15

© 2011 Boart Longyear. All rights reserved.

MARKET OVERVIEW

© 2011 Boart Longyear. All rights reserved.

For

per

sona

l use

onl

y

© 2011 Boart Longyear. All rights reserved.

TM

16

Air Quality • Replacing Solvent-based paints • Reducing emissions

Energy Efficiency • Installed high efficiency compressors • Rigs utilizing Tier 3 & 4 Diesel Engines

Waste Minimization • Waste tracking programs • Recycling carbon & scrap metal waste

40%

45%

50%

55%

60%

65%

70%

75%

80%

OPERATIONS – STRONG UNDERLYING TRENDS

Products: • Capacity available through 2012 • Higher inventory levels in warehouse: Readiness to serve • Backlog stabilising: Faster delivery times (orders = shipments) Services: • Controlled growth:

• Allowing proper driller training (safety) • Optimising contracts: Key clients, larger sites, terms • 2011 forecast: 75% to 80% rig utilisation

• Expanding to meet demand through 2012 – rigs & labour

0%

50%

100%

150%

200%

250%

300%

350%

Drilling Products Order Backlog (Indexed to Jan-09)

Products Services M&E1 Drilling Services Rig Utilisation2

1. Minerals & Energy (M&E) 2. Rig utilisation is defined as % of total fleet either operating or assigned

• Backlog up 27% vs. Dec 2010 • Strong utilisation throughout 1H 2011

75% - 80%

Environmental Sustainability (1H 2011 Focus)

For

per

sona

l use

onl

y

© 2011 Boart Longyear. All rights reserved.

TM

17

1.8 2.4 3.2 4.2 4.9

3.5 5.4

- - - - - - - -

1.0 1.5

2.4

3.6

5.2

2.6

3.5

- - - - - - -

0.8

1.2

1.7

3.2

3.7

- - - - -

3.6

5.0

7.3

11.0

13.9

8.0

11.5

14.0

19.0

20.4 19.3

17.1 18.0

20.8

22.5

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

Gold Exploration Spend Base Metal Exploration Spend Other Exploration Spend Future Projections

Equity raisings by Juniors**

OUTLOOK - 2011

*Source: 2004 – 2010 Metals Economics Group; 2011 – 2018 McKinsey Analysis

Total worldwide nonferrous exploration spend ($ Billions)*

• Potential record 2011 exploration spend • YTD 2011 utilisation rates: As planned • Inflation challenges:

• Labor & material • High end of 2011 op plan

• Junior capital raising in 1H 2011: Very strong • YTD price increases: As planned • Focused on shareholder value: Not utilisation

GFC

*

**Source: Thomson ONE. Junior Miners are defined as mining sector companies with market cap of less than US$500mm at the time of raising.

Exploration spend rising as expected

Juniors entering markets as expected

$-

$500

$1,000

$1,500

$2,000

$2,500

$3,000

$3,500

$4,000

$4,500

$5,000

Dec-0

4

Ma

r-05

Jun

-05

Se

p-0

5

Dec-0

5

Ma

r-06

Jun

-06

Se

p-0

6

Dec-0

6

Ma

r-07

Jun

-07

Se

p-0

7

Dec-0

7

Ma

r-08

Jun

-08

Se

p-0

8

Dec-0

8

Ma

r-09

Jun

-09

Se

p-0

9

Dec-0

9

Ma

r-10

Jun

-10

Se

p-1

0

Dec-1

0

Ma

r-11

Jun

-11

(in

mil

lio

ns

US

D)

ASX TSX-V TSX London AIM OTC Other

For

per

sona

l use

onl

y

© 2011 Boart Longyear. All rights reserved.

TM

18

GOLD: PRODUCTION VS. RESOURCES

*Sources: Metals Economics Group, Kitco

Continued drilling anticipated – gold reserves not being replenished

$-

$200

$400

$600

$800

$1,000

$1,200

$1,400

$1,600

$1,800

-

20

40

60

80

100

120

140

160

180

200

1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

Ave

rag

e p

ric

e o

f g

old

(U

SD

/ o

z.)

Go

ld m

ine

d a

nd

dis

co

ve

red

(m

illi

on

oz.)

World mine production Resources in discoveries 3-year average Gold price

Data not

Available

For

per

sona

l use

onl

y

© 2011 Boart Longyear. All rights reserved.

TM

19

Exploration Products

23%

Surface Core Drilling 39%

Rotary Drilling 17%

Production 46%

Exploration 26%

Development 20%

Non-Mining

8%

Gold 40%

Copper 21%

Nickel 8%

Iron 8%

Other Metals 6%

Energy 1%

Environmental 5% Other

11%

Major 80%

Junior 12%

Non-Mining

8%

Total Company 1H 2011 Revenue - Products and Services

1H 2011 Drilling Service Revenue by Stage

1H 2011 Drilling Service Revenue by Commodity

DIVERSIFIED END MARKET EXPOSURE – 1H 2011

Over 20% of total revenue comes from

non-exploration

Gold, Copper, Nickel, and

Iron: >75% of revenue

Production mining is almost 50% of drilling

service revenue

1H 2011 Drilling Service Revenue by Customer Type

Focused on key clients

Percussive Products

6%

Percussive Drilling 2%

Underground Drilling

8% Non-Mining Drilling

5%

For

per

sona

l use

onl

y

TM

© 2011 Boart Longyear. All rights reserved.

20

INCREASING GLOBAL ENFORCEMENT

USA Foreign

Corrupt

Practices Act

UK Bribery Act

Canada

Corruption of

Foreign Public

Officials Act

Australia

Criminal Code

Registered to do

Business

Pay All Taxes

Ethical Business Partners

Proper Import

Procedures

No Improper Payments

Visas and Work

Permits

Investing resources to ensure…

For

per

sona

l use

onl

y

TM

© 2011 Boart Longyear. All rights reserved.

21

2H 2011 – KEY METRICS Total Company Pricing (indexed to 2H 2008)

Total Company Inflation vs. Op Plan

100% -5%

-5%

-3% 2%

6% 95%

80%

85%

90%

95%

100%

105%

2H 2008 1H 2009 2H 2009 1H 2010 2H 2010 1H 2011 Current

2011Op Plan

Labour Material Mitigation 2011Forecast

Starting second year of re-pricing

Ge

ne

ric

BL

Y T

ren

ds

For

per

sona

l use

onl

y

© 2011 Boart Longyear. All rights reserved.

TM

22

2011 GUIDANCE

*Note: Guidance assumes normal seasonality in November and December and constant fx.

Upside to Guidance:

• Pricing and margins continue

to accelerate?

• Global rig demand?

• On-going exploration demand?

• Commodity pricing?

• New product adaption?

Risk to Guidance:

• Global economic disruption?

• Fx (Stronger US$)?

• China slowdown?

• Inflation (labour, material)?

• Labour availability?

US $M 2010 ActualPrevious

GuidanceNEW

GuidanceYOY %

change

Revenue 1,476 1,750 1,900 29%

EBITDA 222 300 330 49%EBITDA Margin % 15% 17% 17%

200 50%CAPEX 140 210

(US $M)

For

per

sona

l use

onl

y

© 2011 Boart Longyear. All rights reserved.

TM

23

2012 – PLANNING FOR THE FUTURE

*Source: 2011 – 2018 McKinsey Analysis

“Through the Cycle” Capital Structure

Expand: New Geographies, Drilling Types, and Products

Invest in Global Compliance

Hire and Train New Employees

14.0

19.0 20.4

2011 2012 2013

Projected Future M.E.G. Spend*

(in billions USD)

Remaining flexible –

maintaining variable structure For

per

sona

l use

onl

y

TM Company confidential – unauthorized use or distribution prohibited

© 2011 Boart Longyear. All rights reserved.

24

© 2009 Boart Longyear. All rights reserved.

Pilbara – Western Australia

APPENDIX

© 2011 Boart Longyear. All rights reserved.

For

per

sona

l use

onl

y

TM Company confidential – unauthorized use or distribution prohibited

© 2011 Boart Longyear. All rights reserved.

25

BASIS OF PREPERATION

• Financial information has been extracted from underlying financial report data which

has been prepared in accordance with A-IFRS

• All financial figures are reported in US$

• Earnings per share computations reflect the weighted average number of fully paid

ordinary shares issued by Boart Longyear and outstanding as at 30 June 2011

(455,958,822 shares) and 30 June 2010 (458,449,150 shares)

For

per

sona

l use

onl

y

TM Company confidential – unauthorized use or distribution prohibited

© 2011 Boart Longyear. All rights reserved.

26

INCOME STATEMENT Extract from the Boart Longyear 1H 2011 Report – periods ended 30 June

Half-year Half-year

ended ended

30 June 2011 30 June 2010

Note US$'000 US$'000

Continuing operations

Revenue 958,765 685,411

Cost of goods sold (699,827) (520,645)

Gross margin 258,938 164,766

Other income 4 3,111 1,498

General and administrative expenses (115,763) (84,956)

Selling and marketing expenses (25,955) (19,417)

Other expenses 4 (7,653) (11,337)

Operating profit 112,678 50,554

Interest income 2,410 1,626

Finance costs 5 (9,375) (4,416)

Profit before taxation 105,713 47,764

Income tax expense (31,630) (15,053)

Profit for the period attributable

to equity holders of the parent 74,083 32,711

Earnings per share

Basic earnings per share 16.2 cents 7.1 cents

Diluted earnings per share 16.2 cents 7.1 cents

Other comprehensive income (loss)

Profit for the period attributable to equity holders of the parent 74,083 32,711

Exchange differences arising on translation of foreign operations 26,624 (22,985)

Gains on cash f low hedges recorded in equity 193 272

Transfer to profit or loss on cash f low hedges 137 -

Income tax on income and expense recognised directly through equity (71) (96)

Other comprehensive income (loss) for the period, net of tax 26,883 (22,809)

Total comprehensive income for the period attributable

to equity holders of the parent 100,966 9,902

For

per

sona

l use

onl

y

TM Company confidential – unauthorized use or distribution prohibited

© 2011 Boart Longyear. All rights reserved.

27

BALANCE SHEET - ASSETS Extract from the Boart Longyear 1H 2011 Report – periods ended 30 June

30 June 31 December

2011 2010

Note US$'000 US$'000

Current assets

Cash and cash equivalents 68,631 94,944

Trade and other receivables 6 399,367 276,836

Inventories 376,668 283,115

Current tax receivable 17,724 21,705

Prepaid expenses and other assets 25,600 17,965

Defined benefit plan asset 7 20,373 -

Total current assets 908,363 694,565

Non-current assets

Property, plant and equipment 482,615 439,446

Goodw ill 8 302,310 297,408

Other intangible assets 8 112,293 106,295

Deferred tax assets 149,886 147,322

Other assets 1,090 1,918

Defined benefit plan asset 7 - 20,335

Total non-current assets 1,048,194 1,012,724

Total assets 1,956,557 1,707,289

Current liabilities

Trade and other payables 323,257 260,038

Provisions 10 22,264 18,398

Other f inancial liabilities 11 2,522 7,272

Current tax payable 60,648 46,338

Loans and borrow ings 9 40,959 979

Total current liabilities 449,650 333,025

Non-current liabilities

Loans and borrow ings 9 294,483 247,490

Deferred tax liabilities 15,890 11,468

Provisions 10 56,380 55,337

Total non-current liabilities 366,753 314,295

Total liabilities 816,403 647,320

Net assets 1,140,154 1,059,969

Equity

Issued capital 1,128,562 1,132,051

Reserves 109,848 84,577

Other equity (137,182) (137,182)

Accumulated profit (losses) 38,926 (19,477)

Total equity 1,140,154 1,059,969

For

per

sona

l use

onl

y

TM Company confidential – unauthorized use or distribution prohibited

© 2011 Boart Longyear. All rights reserved.

28

Extract from the Boart Longyear 1H 2011 Report – periods ended 30 June

30 June 31 December

2011 2010

Note US$'000 US$'000

Current assets

Cash and cash equivalents 68,631 94,944

Trade and other receivables 6 399,367 276,836

Inventories 376,668 283,115

Current tax receivable 17,724 21,705

Prepaid expenses and other assets 25,600 17,965

Defined benefit plan asset 7 20,373 -

Total current assets 908,363 694,565

Non-current assets

Property, plant and equipment 482,615 439,446

Goodw ill 8 302,310 297,408

Other intangible assets 8 112,293 106,295

Deferred tax assets 149,886 147,322

Other assets 1,090 1,918

Defined benefit plan asset 7 - 20,335

Total non-current assets 1,048,194 1,012,724

Total assets 1,956,557 1,707,289

Current liabilities

Trade and other payables 323,257 260,038

Provisions 10 22,264 18,398

Other f inancial liabilities 11 2,522 7,272

Current tax payable 60,648 46,338

Loans and borrow ings 9 40,959 979

Total current liabilities 449,650 333,025

Non-current liabilities

Loans and borrow ings 9 294,483 247,490

Deferred tax liabilities 15,890 11,468

Provisions 10 56,380 55,337

Total non-current liabilities 366,753 314,295

Total liabilities 816,403 647,320

Net assets 1,140,154 1,059,969

Equity

Issued capital 1,128,562 1,132,051

Reserves 109,848 84,577

Other equity (137,182) (137,182)

Accumulated profit (losses) 38,926 (19,477)

Total equity 1,140,154 1,059,969

BALANCE SHEET – LIABILITY & EQUITY F

or p

erso

nal u

se o

nly

TM Company confidential – unauthorized use or distribution prohibited

© 2011 Boart Longyear. All rights reserved.

29

CASH FLOW (1 of 2) Extract from the Boart Longyear 1H 2011 Report – periods ended 30 June

Half-year Half-year

ended ended

30 June 2011 30 June 2010

Note US$'000 US$'000

Cash flows from operating activities

Profit for the year 74,083 32,711

Adjustments provided by operating activities:

Income tax expense recognised in profit 31,630 15,053

Finance costs recognised in profit 5 9,375 4,416

Investment revenue recognised in profit (2,410) (1,626)

(Gain) Loss on disposal of non-current assets (619) 700

Impairment of current and non-current assets - 177

Depreciation and amortisation 52,219 47,198

Foreign exchange loss on intercompany balances 1,114 1,267

Share-based compensation 3,231 2,001

Long-term compensation - cash rights 1,330 619

Changes in net assets and liabilities, net of effects

from acquisition and disposal of businesses:

Increase in assets:

Trade and other receivables (110,333) (86,239)

Inventories (81,502) (49,039)

Other assets (6,294) (2,340)

Increase in liabilities:

Trade and other payables 67,066 42,135

Provisions 1,145 178

Cash generated from operations 40,035 7,211

Interest paid (12,867) (8,553)

Interest received 2,410 1,626

Income taxes paid (7,777) (13,222)

Net cash flow s provided by (used in) operating activities 21,801 (12,938)

For

per

sona

l use

onl

y

TM Company confidential – unauthorized use or distribution prohibited

© 2011 Boart Longyear. All rights reserved.

30

Extract from the Boart Longyear 1H 2011 Report – periods ended 30 June

Half-year Half-year

ended ended

30 June 2011 30 June 2010

Note US$'000 US$'000

Cash flows from investing activities

Purchase of property, plant and equipment (83,820) (36,775)

Purchase of rods and casings (1,587) (2,203)

Proceeds from sale of property, plant and equipment 1,731 450

Intangible and development costs paid (15,987) (11,229)

Net cash flow s used in investing activities (99,663) (49,757)

Cash flows from financing activities

Purchase shares for LTIP 14 (8,332) (5,768)

Proceeds from borrow ings 478,077 125,000

Repayment of borrow ings (387,405) (55,078)

Payments for debt issuance costs (6,098) -

Dividends paid 13 (15,680) -

Net cash flow s provided by f inancing activities 60,562 64,154

Net (decrease) increase in cash and cash equivalents (17,300) 1,459

Cash and cash equivalents at the beginning of the period 94,944 87,557

Effects of exchange rate changes on the balance of cash held in

foreign currencies (9,013) 3,063

Cash and cash equivalents at the end of the period 68,631 92,079

CASH FLOW (2 of 2) F

or p

erso

nal u

se o

nly