First Horizon National Corporation -...

41

1 First Horizon National Corporation Barclays Global Financial Services Conference September 16, 2009

Transcript of First Horizon National Corporation -...

1

First Horizon National Corporation

Barclays Global Financial Services ConferenceSeptember 16, 2009

2

Portions of this presentation use non-GAAP financial information. Each of those

portions is so noted, and a reconciliation of that non-GAAP information to comparable

GAAP information is provided in a footnote or in the appendix at the end of this

presentation.

This presentation contains forward-looking statements, which may include guidance,

involving significant risks and uncertainties which will be identified by words such as

“believe” “expect” “anticipate” “intend” “estimate” “should” “is likely” “will” “going

forward” and other expressions that indicate future events and trends and may be

followed by or reference cautionary statements. A number of factors could cause

actual results to differ materially from those in the forward-looking

information. These factors are outlined in our recent earnings and other press

releases and in more detail in the most current 10-Q and 10-K. First Horizon

disclaims any obligation to update any of the forward-looking statements that are

made from time to time to reflect future events or developments.

3

Back to the Future: Repositioning FHN on Track

Winding down national lending businesses

Returning company to sustained profitability

Driving shareholder returns over the long-term

4

Strategic Actions Since December 2007

Attractive Growth

Opportunities

Industry-Leading Strengths

Ceased national originations in Jan 2008Sold national mortgage platform in Sept 2008Shrunk balance sheet by 22% Retired $8B in debt through balance sheet reduction and growth in core deposits

AbilityTo

Execute

Raised $690mm common equity in May 2008TARP CPP of $866mm in Nov 2008Tier 1 ratio has improved from 8.1% to 15.6%TCE / TA up from 5.1% to 7.3%

Leading JD Power Ranking in Tennessee2

Hired talent to grow market share in TNImplemented line of business structure to enhance performance and profitability

Strong Capital Position1

Strong Regional Banking Franchise

Focused Capital Markets Business Distribution platform and low balance sheet usage drives higher risk-adjusted returnsCurrent market conditions demonstrate counter-cyclical nature of businessesHigher market share from competitive disruption and new hires

1Tier 1 Common, TCE, & TA are non-GAAP numbers, and a reconciliation is provided in the appendix. 2Power 2009 Retail Banking Satisfaction Study: Customer Satisfaction Index, Southeast Region. Rankings. First Tennessee ranked #2 in overall study.

Reducing Risk

Proactive on Asset Quality Reserve coverage ratio up from 1.55% to 4.91%Early identification of problems loans driving recent NPA slow down

5

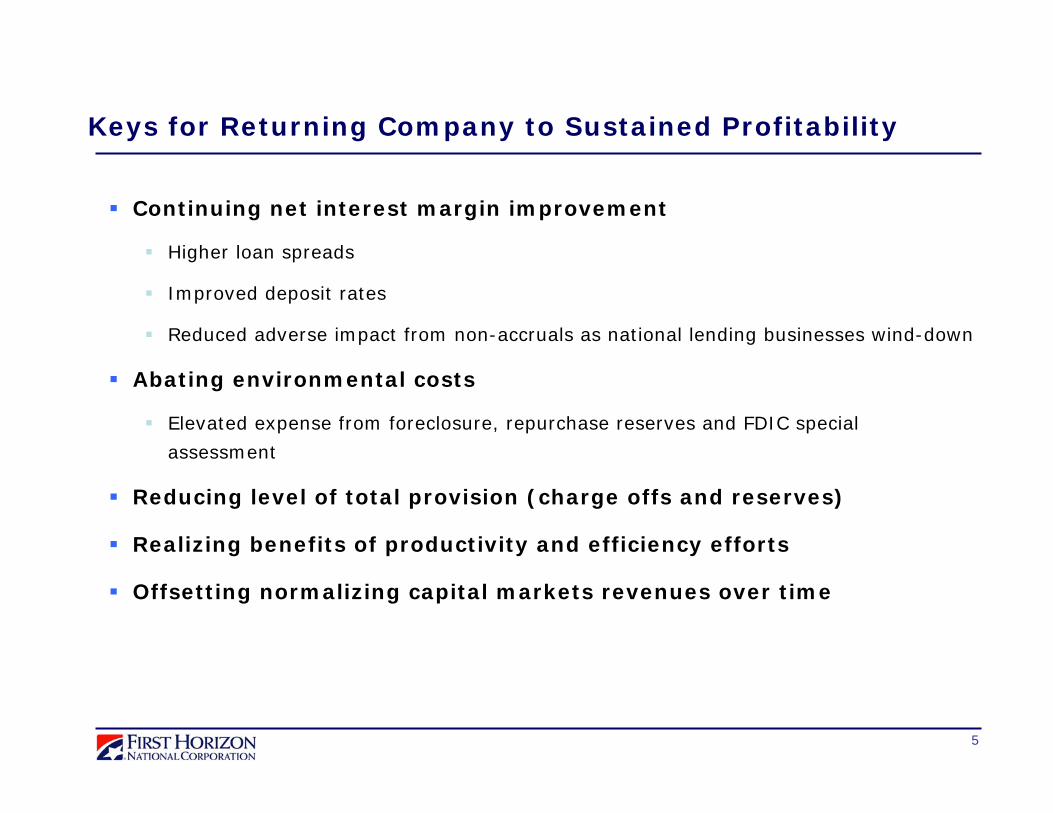

Keys for Returning Company to Sustained Profitability

Continuing net interest margin improvement

Higher loan spreads

Improved deposit rates

Reduced adverse impact from non-accruals as national lending businesses wind-down

Abating environmental costs

Elevated expense from foreclosure, repurchase reserves and FDIC special

assessment

Reducing level of total provision (charge offs and reserves)

Realizing benefits of productivity and efficiency efforts

Offsetting normalizing capital markets revenues over time

6

$0

$200

$400

$600

$800

$1,000

$1,200

$1,400

1Q08 2Q08 3Q08 4Q08 1Q09 2Q09

$ M

illio

ns

NPLs ORE

Asset Quality Overview

Proactive management of credit quality remains top priority

Wind-down of national portfolios remains on track

65% of NPLs from OTC & National CRE in 2Q09

Home equity delinquency trends stabilizing

Income CRE and C&I softening as expected

Reserve increases in Income CRE and C&I in 2Q09

128155

191 208239

92

185 8992 20

2.59%

3.52%

3.99%

4.57%4.91%

0

50

100

150

200

250

300

350

400

2Q08 3Q08 4Q08 1Q09 2Q09

$ M

illio

ns

0.00%

0.50%

1.00%

1.50%

2.00%

2.50%

3.00%

3.50%

4.00%

4.50%

5.00%

Net Charge-Offs Reserve Increase Reserve % of Loans (right axis)

Reserves Strong, Growth SlowingNon-Performing Assets Flattening

43%

16%

14%8% (2)%

7

First Half 2009Trends generally consistent with previously communicated expectations2Q09: Total charge-offs in line; reserve build driven by C&I, Income CRE, Perm Mortgage

Second Half 2009Expectations generally consistent with prior viewsWind-down of national specialty portfolio should drive sequentially lower charge-offs and reservesContinued stress anticipated in Income CRE and C&I, particularly bank-related exposures

Credit Expectations and Risks Summary

1Other includes permanent mortgage, other consumer, and credit card. Expectations as of 7/17/09.

Balance

Portfolio6/30/09

($B)4Q08

(Actual)1Q09 Actual

2Q09 Actual

2H09 Expected

4Q08(Actual)

1Q09 Actual

2Q09 Actual

2H09 Expected

Residential CRE $1.0 $55 $56 $46 $106 $97 $97

One-Time Close 0.6 40 47 51 201 183 164

Home Equity 7.4 35 46 56 182 233 223

Commercial 7.4 41 30 27 192 228 251

Income CRE 1.9 14 17 31 94 101 108

Other1 1.4 6 13 28 74 99 118

Total $191 $208 $239 $849 $941 $961

2H09 expectations are relative to 2Q09 actual levels.

Net Charge-Offs ($mm) Allowance

8

Regional Banking

9

Strong Tennessee Franchise in Diverse Economy

Strategy emphasizes competitive advantages in Convenience, Advice, and Service

180 financial centers

$10B loans / $11B deposits1

GAALMS

AR

MOKY

NC

SC

TENNESSEEMid-South(#1)

Middle(#5)

Southeast(#2)

East(#1)

Northeast(#1)

Customer Service-TN Competitors2

734

735

746

746

746

756

767

788

700 725 750 775 800

Bank A

Bank B

SE Region Avg.

Bank C

Bank D

Bank E

Bank F

First Tennessee

1At 6/30/09 2JD Power 2009 Retail Banking Satisfaction Study: Customer Satisfaction Index, Southeast Region. Rankings. First Tennessee ranked #2 in overall study.

Top 3 TN Competitors

Deposit growth

Pricing Management

Productivity/Process Improvement

Efficiency

Asset quality

Leading Customer Market Share in Tennessee

Regional Banking Priorities

10

Regional Banking Restructure Improves Focus on Customers, Productivity, and Profitability

Retail

Business Banking

Commercial

Private Client/Wealth Management

Mid-South

Middle

TN

Southeast

TN

East

TN

Northeast

TN

Customer Relationships Go to Market ExecutionManagement of sales forceP&L Responsibility

Market

LOB StrategySales/Service EffectivenessGoals & IncentivesDelivery/TechnologyProduct OfferingsP&L Responsibility

Line of Business

Corporate

Improved performance disciplineConsistent execution across geographiesScalability to potential new markets

Commercial Real Estate

11

Capital Markets

12

Capital Markets Demonstrates Value to FHN Strategy

27%33%

41%

24%

83%

69%80%

20%

40%

60%

80%

100%

120%

4Q07

1Q08

2Q08

3Q08

4Q08

1Q09

2Q09

1Capital Markets return on capital excludes correspondent banking, a non-GAAP number; a reconciliation is provided in the appendix. .

Capital Markets: High Return on Capital1

High normalized return on equity

Counter-cyclical to regional banking business

Significant contributor to fee income as a percent of total revenue

$0.0

$0.5

$1.0

$1.5

$2.0

$2.5

$3.0

$3.5

1Q052Q053Q054Q051Q062Q063Q064Q061Q072Q073Q074Q071Q082Q083Q084Q081Q092Q09

4.00%

4.20%

4.40%

4.60%

4.80%

5.00%

5.20%

5.40%Regional Bank NIM (right axis)Fixed Income Correlation = -86%

Fixed Income Average Daily Revenue (left axis)

Fixed Income’s Counter-Cyclicality to Regional Banking

13

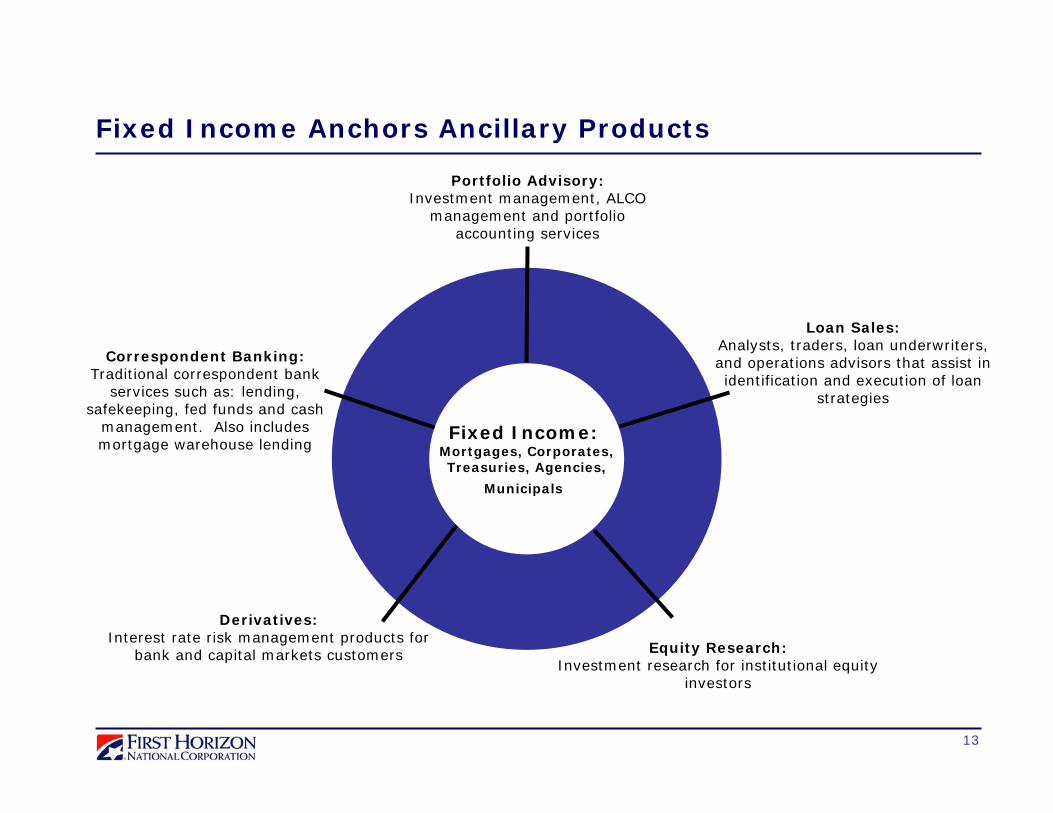

Fixed Income Anchors Ancillary Products

Equity Research:Investment research for institutional equity

investors

Loan Sales:Analysts, traders, loan underwriters, and operations advisors that assist in identification and execution of loan

strategies

Correspondent Banking:Traditional correspondent bank

services such as: lending, safekeeping, fed funds and cash

management. Also includes mortgage warehouse lending

Fixed Income: Mortgages, Corporates,Treasuries, Agencies,

Municipals

Derivatives:Interest rate risk management products for

bank and capital markets customers

Portfolio Advisory:Investment management, ALCO

management and portfolio accounting services

14

Capital Markets’ Diverse Client Base

Depositories40%

Non-Depositories1

60%

1 Non-Depositories includes Money Managers, Insurance Companies, Public Funds and Other Customer Types.

Geographic Distribution of Domestic Clients Revenue by Customer Type at 2Q09

FTN Financial does business with more than one-third of all banks in the U.S.

15

Significant Opportunities For More Focused First Horizon

16

Key Areas of Focus for FHN

Gaining market share in Middle TN

Leverage existing infrastructure to grow deposits

Targeting affluent market

Migration of affluent branch customers to private client network to maximize

profitability

Improving efficiency and productivity

Company-wide effort to operate more efficiently through expense control

Process transformation to improve productivity

17

Key Area of Focus: Middle TN Market

50 branch Locations

Opportunity to develop branch network for higher customer share

25 branches built since 2003

Leverage de novo delivery system

Key new hires to expand relationships

Attractive market demographics

FT 10%

$34

$63

$50

$24.0

$32.0

$40.0

$48.0

$56.0

$64.0

FTB Branch FTB MatureBranch

CompetitorMature Branch

$m

m

Middle TN Average Deposits Per Branch1

First Tennessee Branch Share

First Tennessee Customer Share

FT 16%

First Tennessee FDIC Deposit Share

FT 7%

.1 FDIC data as of June 30, 2008. Mature branch represents branch older than 5 years in Middle TN.

18

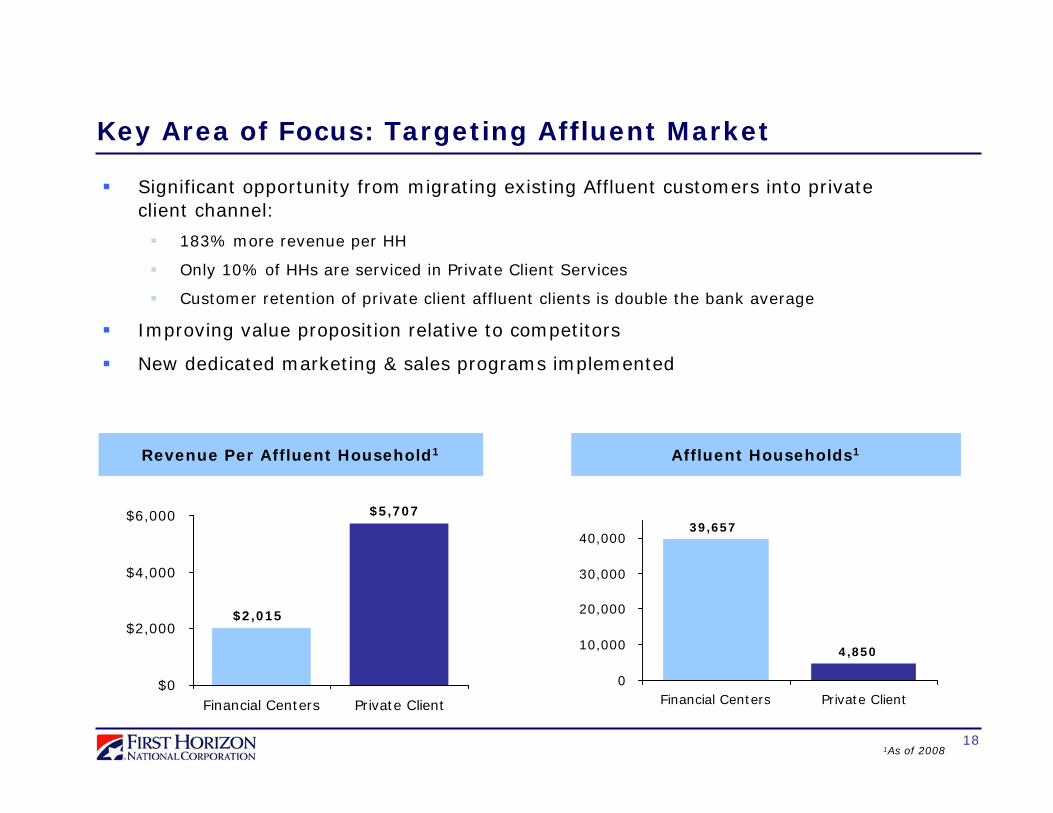

Significant opportunity from migrating existing Affluent customers into private client channel:

183% more revenue per HH

Only 10% of HHs are serviced in Private Client Services

Customer retention of private client affluent clients is double the bank average

Improving value proposition relative to competitors

New dedicated marketing & sales programs implemented

Key Area of Focus: Targeting Affluent Market

$5,707

$2,015

$0

$2,000

$4,000

$6,000

Financial Centers Private Client

4,850

39,657

0

10,000

20,000

30,000

40,000

Financial Centers Private Client

1As of 2008

Revenue Per Affluent Household1 Affluent Households1

19

Company-wide effort to operate more efficiently through expense control

Environmental costs should be significantly reduced over long-term and wind-down costs should be eliminated

Targeting approximately $50mm-$75mm in efficiency initiatives to reduce core run rate, in addition to reduced environmental costs

Key Area of Focus: Improving Efficiency

40%

50%

60%

70%

80%

90%

100%

2Q09Efficiency

Ratio

EnvironmentalCosts

Wind-DownBusinesses

NormalizedNIM

NormalizedFees

EfficiencyInitiaitves

TargetEfficiency

Ratio

84%

60-65%

Impact to Efficiency Ratio:

20

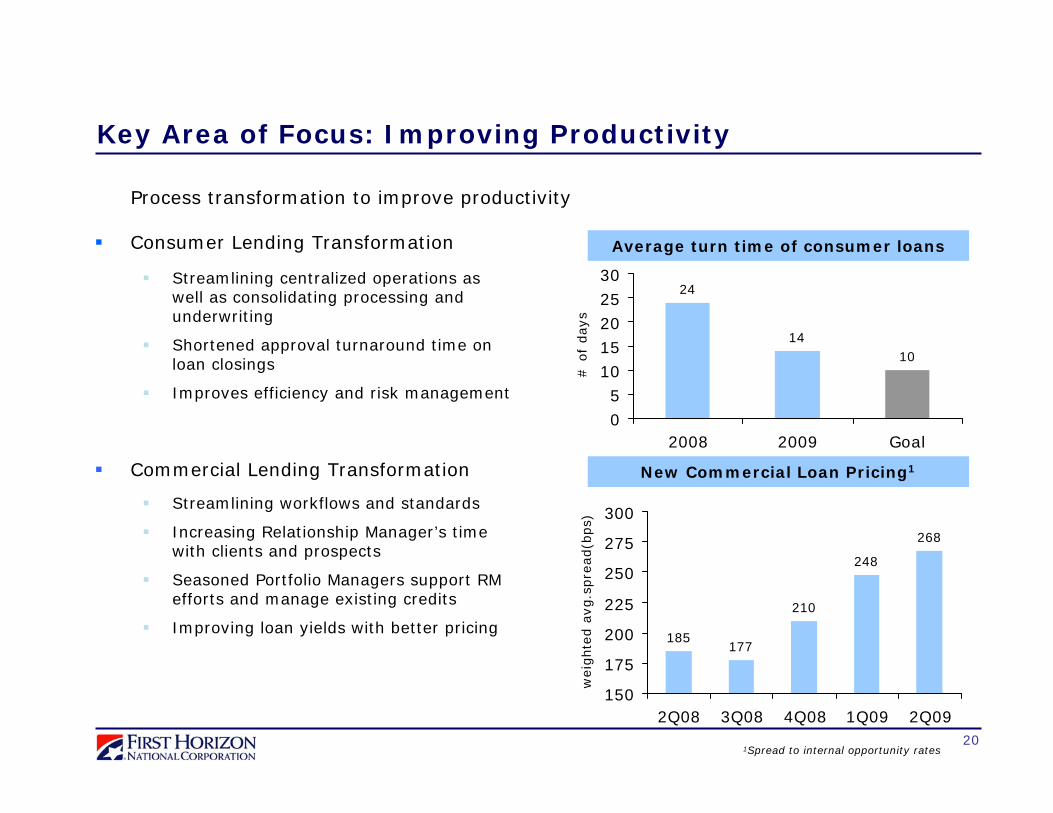

185177

210

248

268

150

175

200

225

250

275

300

2Q08 3Q08 4Q08 1Q09 2Q09

weig

hte

d a

vg.s

pre

ad(b

ps)

24

1410

05

1015202530

2008 2009 Goal

# o

f days

1Spread to internal opportunity rates

Average turn time of consumer loans

New Commercial Loan Pricing1

Consumer Lending Transformation

Streamlining centralized operations as well as consolidating processing and underwriting

Shortened approval turnaround time on loan closings

Improves efficiency and risk management

Key Area of Focus: Improving Productivity

Process transformation to improve productivity

Commercial Lending Transformation

Streamlining workflows and standards

Increasing Relationship Manager’s time with clients and prospects

Seasoned Portfolio Managers support RM efforts and manage existing credits

Improving loan yields with better pricing

21

Alternatives for Deploying Excess Capital for Optimal Return

Internal Investors External

Deployable Capital

Risk appropriate loan growth

Product development in capital markets

Technology infrastructure

Branch expansion

Repay TARP CPP Preferred

Reinstitute cash dividend on common

Share buyback

FDIC-assisted transactions of distressed franchises

Proactive strategic acquisitions

Complementary lines of business

22

Path to Driving Long-Term Returns & Profitability

Total Assets Earning Assets

Return on Assets Pre-tax Income 1.25% - 1.45% Net Interest Margin

3.50% - 4.00%

Tax Rate

Annualized Net Charge-Offs0.3% - 0.7%

Return on Equity15% - 20%

% Fee Income40% - 50%

Equity / Assets TCE / TA6% - 7%

Efficiency Ratio60% - 65%

Risk Adjusted Margin

23

Appendix

All financials in Appendix are as of 6/30/09, unless otherwise noted.

24

Segment Structure Reflects Strategic Focus

FIRST HORIZON NATIONAL CORPORATION

RegionalBanking

RetailOrigination

Servicing

CorrespondentBanking

Fixed Income

Other Products

Commercial

CorporateFunctions

InvestmentPortfolio

RiskManagement

ConsumerLending

ConstructionLending

CapitalMarkets

CorporateNationalSpecialtyLending

MortgageBanking

Core Business Wind-Down / Liquidating Businesses

Business Banking

PC/Wealth Management

Corporate

CRE

25

Actual Actual Actual Hypothetical4Q08 1Q09 2Q09 4Q10

Tier 1 15.0% 15.0% 15.6% 14.6%

Tier 1 Common 9.6% 9.4% 9.6% 8.6%

TCE/TA 7.3% 7.1% 7.3% 6.6%

TCE/RWA 8.8% 8.6% 8.7% 7.9%

Capital Analysis Demonstrates Balance Sheet Strength

Loan Loss AssumptionsAssumptions

Capital Ratios3

Illustrates expected strong 2010 year-end capital ratios based on severe economic conditions Pre-tax, pre-provision income at current broker estimates2

Loan losses at reported SCAP median rates by category under more adverse scenario$2.5B asset reduction (wind-down), assumes RWA decline by $1.8B from 4Q08Ending ALLL at 2.00% of loansTax rate of 35%

Tier 1 Common Roll-Forward

8.5%9.6%

3.5

1.1

0.8 (0.6)

(5.7)

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

9.0%

10.0%

4Q08 Loan Losses PTPPEarnings

ReserveRelease

B/SShrinkage

Dividends /Warrant

4Q10

1Source: Federal Reserve SCAP: Overview of Results. 2PTPP assumptions based on ThomsonOne broker estimates; average of BAC-ML, FBR, Credit Suisse, FIG, Fox-Pitt, Sterne Agee, Stifel Nicolaus, SunTrust RH, & Wunderlich as of 7/9/09. FHN does not provide earnings estimates & has not endorsed these or any other broker estimates.

3Tier 1 Common, TCE, and TA are non-GAAP numbers, and a reconciliation is provided on page 39 of the Appendix.

Hypothetical Illustration

12/31/2008 2009-10Loans ($mm) Loss Rate1

C&I 7,806 5.8%Income CRE 1,988 10.6%Res CRE 1,288 16.5%Home Equity 7,749 13.3%OTC 981 16.5%Permanent Mortgage 1,127 8.0%Other 339 22.3%

Total 21,278 10.5%

26

2Q09Peer

4Q08 1Q09 2Q09 Median

Total Capital 15.2% 20.2% 20.8% 14.0%

Tier 1 Capital 15.0% 15.0% 15.6% 11.6%

TCE/TA 7.3% 7.1% 7.3% 5.9%

TCE/RWA 8.8% 8.6% 8.7% 7.3%

Liquidity and Capital Remain Strong

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

4Q08 1Q09 2Q09 2Q09 PeerMedian

Tangible Common Equity Reserves

Numbers may not add to total due to rounding.1Peer median includes Top 50 banks at 2Q09 as of 8/10/09. TCE and TA are considered non-GAAP, and a reconciliation is provided at the end of this presentation

2Excluding Securities Sold Repos, Trading Liabilities, and sub-debt and other collateralized borrowings of $4.0B.

TCE + Reserves / RWA1

12.3% 12.6% 13.1%

9.8%

Liquidity

Wholesale Funding2 — P/E Balances ($B) Capital Ratios1

Continued core deposit growth

Asset reductions, deposit growth offsetting debt maturities

Retired ~$700mm of debt in 2Q09

Wholesale funding in non-credit sensitive sources

2Q08 1Q09 2Q09Fed Funds Purchased $1.4 $1.4 $1.4Street CDs Long Term 1.0 0.5 0.5 Bank Notes 3.0 1.8 1.0 X-Notes 1.3 - - Insured Network Deposits 1.2 1.1 1.4 CDARs - - 0.1 Borrowing from FRB (TAF) 2.4 3.5 2.4 Borrowing from FHLB 3.0 - - Other 0.0 0.1 0.1

$13.3 $8.4 $6.9

27

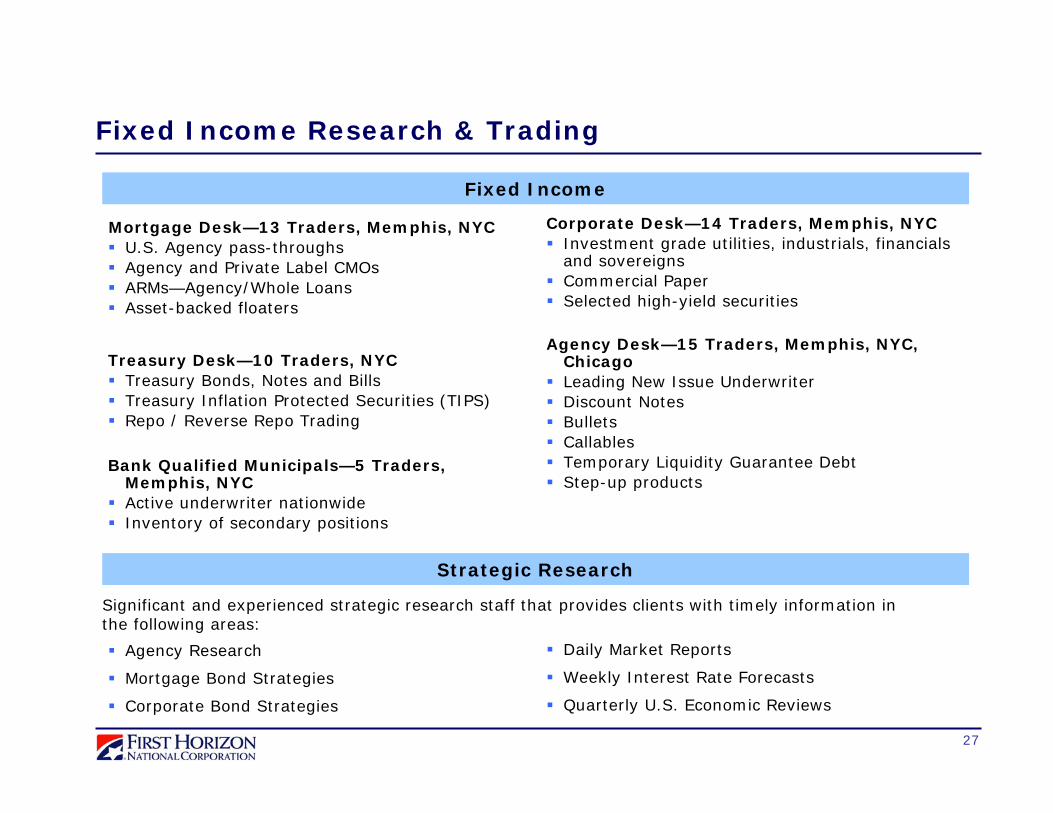

Fixed Income Research & Trading

Fixed Income

Strategic Research

Significant and experienced strategic research staff that provides clients with timely information in the following areas:

Daily Market Reports

Weekly Interest Rate Forecasts

Quarterly U.S. Economic Reviews

Agency Research

Mortgage Bond Strategies

Corporate Bond Strategies

Treasury Desk—10 Traders, NYCTreasury Bonds, Notes and BillsTreasury Inflation Protected Securities (TIPS)Repo / Reverse Repo Trading

Agency Desk—15 Traders, Memphis, NYC, ChicagoLeading New Issue UnderwriterDiscount NotesBulletsCallablesTemporary Liquidity Guarantee DebtStep-up products

Mortgage Desk—13 Traders, Memphis, NYCU.S. Agency pass-throughsAgency and Private Label CMOsARMs—Agency/Whole LoansAsset-backed floaters

Corporate Desk—14 Traders, Memphis, NYCInvestment grade utilities, industrials, financials and sovereignsCommercial PaperSelected high-yield securities

Bank Qualified Municipals—5 Traders, Memphis, NYCActive underwriter nationwideInventory of secondary positions

28

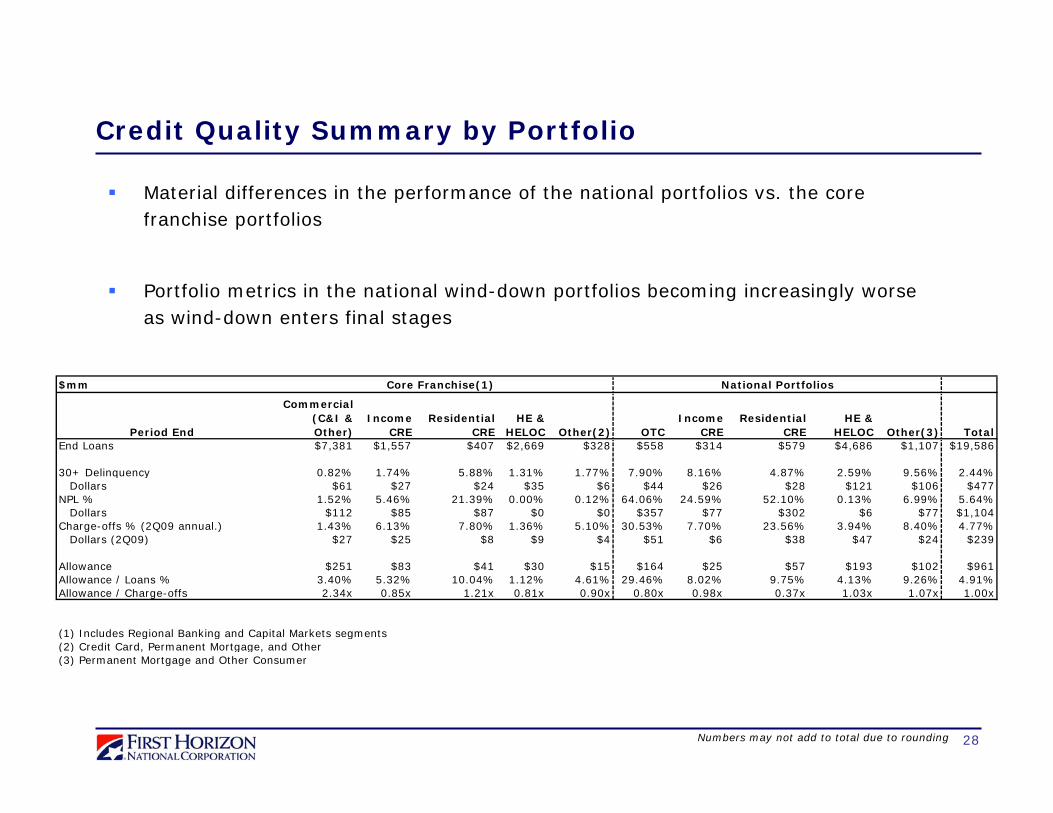

Credit Quality Summary by Portfolio

Numbers may not add to total due to rounding

Material differences in the performance of the national portfolios vs. the core franchise portfolios

Portfolio metrics in the national wind-down portfolios becoming increasingly worse as wind-down enters final stages

$mm

Period End

Commercial (C&I & Other)

IncomeCRE

Residential CRE

HE &HELOC Other(2) OTC

IncomeCRE

Residential CRE

HE &HELOC Other(3) Total

End Loans $7,381 $1,557 $407 $2,669 $328 $558 $314 $579 $4,686 $1,107 $19,586

30+ Delinquency 0.82% 1.74% 5.88% 1.31% 1.77% 7.90% 8.16% 4.87% 2.59% 9.56% 2.44%Dollars $61 $27 $24 $35 $6 $44 $26 $28 $121 $106 $477

NPL % 1.52% 5.46% 21.39% 0.00% 0.12% 64.06% 24.59% 52.10% 0.13% 6.99% 5.64%Dollars $112 $85 $87 $0 $0 $357 $77 $302 $6 $77 $1,104

Charge-offs % (2Q09 annual.) 1.43% 6.13% 7.80% 1.36% 5.10% 30.53% 7.70% 23.56% 3.94% 8.40% 4.77%Dollars (2Q09) $27 $25 $8 $9 $4 $51 $6 $38 $47 $24 $239

Allowance $251 $83 $41 $30 $15 $164 $25 $57 $193 $102 $961Allowance / Loans % 3.40% 5.32% 10.04% 1.12% 4.61% 29.46% 8.02% 9.75% 4.13% 9.26% 4.91%Allowance / Charge-offs 2.34x 0.85x 1.21x 0.81x 0.90x 0.80x 0.98x 0.37x 1.03x 1.07x 1.00x

(1) Includes Regional Banking and Capital Markets segments(2) Credit Card, Permanent Mortgage, and Other(3) Permanent Mortgage and Other Consumer

Core Franchise(1) National Portfolios

29

($ mm) 4Q08 1Q09 2Q09

Beginning ORE $115 $104 $119

+ Additions $22 $45 $39

- Dispositions ($33) ($30) ($52)

Ending ORE $104 $119 $106

NPAs declined 2% linked-quarter

Problem loan outflows increased while inflows decreased

Reduced ORE inventory partially via small bulk sales

Individual sales at approximate carrying values

Losses taken on bulk sales to move aging inventory

Active re-valuation of inventory resulted in increased foreclosure expense

Problem Loans – Inflows Declining, Resolutions Rising

ORE: Proactive Disposition Efforts3

1Includes Commercial & One-Time Close Portfolios only 2Commercial loan grade migration reflects pass to non-pass

3ORE excludes foreclosed real estate from GNMA loans. Includes fair value adjustments

NPLs: Slower Inflows, More Resolutions1

($ mm) 4Q08 1Q09 2Q09

Beginning NPLs $854 $998 $1,064

+ Additions $395 $317 $232

+ Principal Increase $6 $13 $19

- Payments ($83) ($81) ($113)

- Charge-Offs ($150) ($149) ($155)

- Transfer to ORE ($18) ($33) ($25)

- Upgrade to Accrual ($6) ($1) ($1)

Ending NPLs $998 $1,064 $1,021

30

Proactive Approach to Credit Quality Indicated as Problem Loans Slowing

Median 16%

FHN4.9%

1Peers include Top 50 banks at 2Q09 as of 8/10/09. 2Commercial Loan grade migration reflects pass to non-pass.

FHN(2)%

Reserves at $961 million or 4.9% of loans, well above peers

NPA’s declined 2% from 1Q09 to 2Q09, one of the few declines in the industry

Commercial loan deterioration slowing as downward loan grade migration continues to decline in 2Q09

Median 2.4%

Coverage Ratio1

NPA Growth1 from 1Q09 to 2Q09 Commercial Loan Downgrades2

$200

$400

$600

$800

$1,000

$1,200

2Q08 3Q08 4Q08 1Q09 2Q09

Bal

ance

s in

$M

illio

ns

31

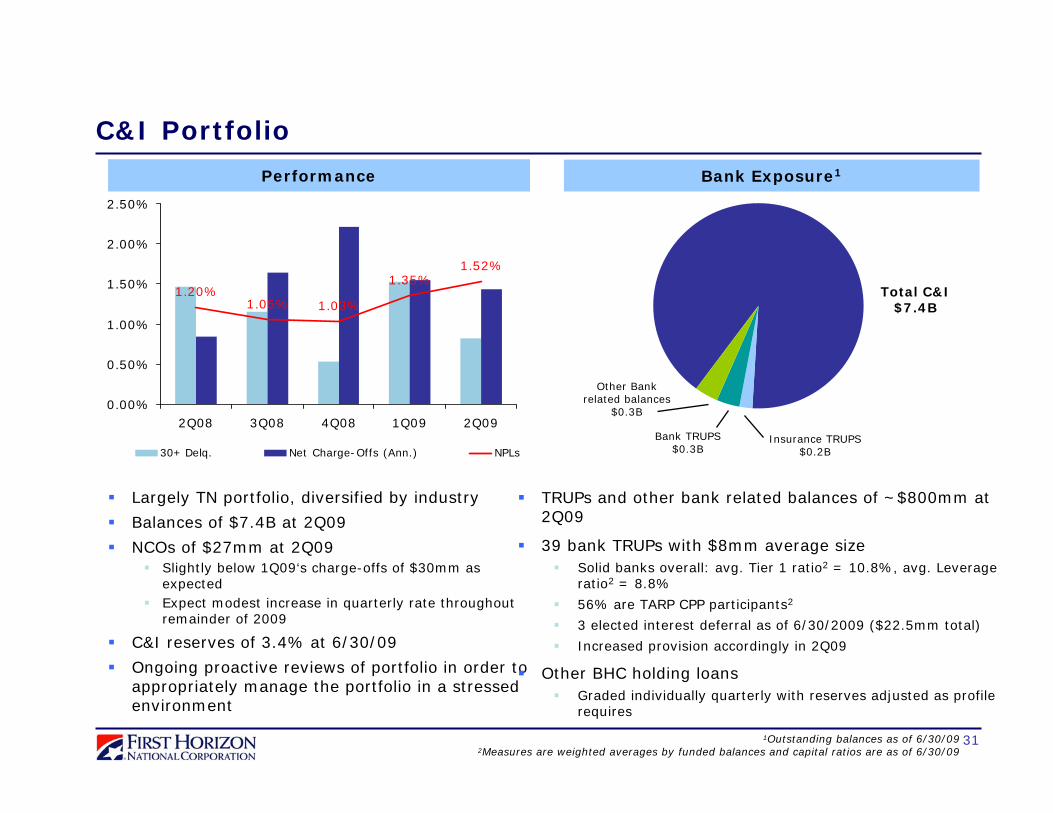

C&I Portfolio

Performance Bank Exposure1

1.52%

1.20%1.05% 1.03%

1.35%

0.00%

0.50%

1.00%

1.50%

2.00%

2.50%

2Q08 3Q08 4Q08 1Q09 2Q09

30+ Delq. Net Charge-Offs (Ann.) NPLs

Largely TN portfolio, diversified by industry

Balances of $7.4B at 2Q09

NCOs of $27mm at 2Q09Slightly below 1Q09‘s charge-offs of $30mm as expectedExpect modest increase in quarterly rate throughout remainder of 2009

C&I reserves of 3.4% at 6/30/09

Ongoing proactive reviews of portfolio in order to appropriately manage the portfolio in a stressed environment

TRUPs and other bank related balances of ~$800mm at 2Q09

39 bank TRUPs with $8mm average size Solid banks overall: avg. Tier 1 ratio2 = 10.8%, avg. Leverage ratio2 = 8.8%

56% are TARP CPP participants2

3 elected interest deferral as of 6/30/2009 ($22.5mm total)

Increased provision accordingly in 2Q09

Other BHC holding loansGraded individually quarterly with reserves adjusted as profile requires

Total C&I $7.4B

Insurance TRUPS $0.2B

Bank TRUPS$0.3B

Other Bank related balances

$0.3B

1Outstanding balances as of 6/30/092Measures are weighted averages by funded balances and capital ratios are as of 6/30/09

32

Income CRE Portfolio

Traditional commercial real estate construction and mini-permanent loans

Balances of ~$2 billion at 2Q09

Three-fourths managed in regional banking

Market conditions impacting portfolio performanceRecession increasing vacancy and rental rates (NOI)Lack of real estate financing in the market increasing cap rates

Reserves of 5.8% at 6/30/09

Multi-Family19%

Office14%

Land14%

Other12%

Industrial 10%

Hospitality7%

Retail24%

Portfolio Characteristics Performance

Collateral Type1Loan Type1

3.54% 3.72%

6.30%

8.67%

5.02%

0.00%1.00%2.00%3.00%4.00%5.00%

6.00%7.00%8.00%9.00%

10.00%

2Q08 3Q08 4Q08 1Q09 2Q09

30+ Delq. Net Charge-Offs (ann.) NPLs

1As of 6/30/09

Construction21%

Land14%%

Mini-Perm/Construction

65%

NPLs by Product Type1

Product Type 1Q09 2Q09

Raw Land 33.2% 41.3%Land Development 12.5% 24.2%Multi-Family 7.8% 11.2%Developed Land 4.3% 7.2%Retail 2.2% 6.5%Other 5.9% 5.5%Office 3.9% 5.2%Industrial 3.0% 3.5%Hospitality 0.0% 0.0%

33

Home Equity Portfolio

30+ Delinquency: National vs. Regional1 Net-Charge Offs2

3.94%

1.50%

0.81%

1.23%1.45% 1.36%

2.88%

2.10%1.91%1.70%

0.00%

1.00%

2.00%

3.00%

4.00%

5.00%

2Q08 3Q08 4Q08 1Q09 2Q09

Regional Banking National Specialty

Vintage Mix

15%17%

11%9%

15%

4,400

4,600

4,800

5,000

5,200

5,400

2Q08 3Q08 4Q08 1Q09 2Q09

$ M

illio

ns

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

Period End Balance Constant Pre-Payment Rate (right axis)

National Portfolio Run-Off

1.28%

2.62%

0.00%

1.00%

2.00%

3.00%

Jun-

08

Jul-0

8

Aug-

08

Sep-

08

Oct-08

Nov-0

8

Dec-0

8

Jan-

09

Feb-

09

Mar-0

9

Apr-0

9

May-0

9

Jun-

09

Regional Banking National Specialty

Industry = 13.20%

1Source: McDash industry data as of April 2009. FHN data excludes FHB.2Net Charge-Offs are annualized

Balance ($B) W/AVintage 6/30/2009 1Q09 2Q09 Age (mo.)

pre-2002 0.4 2.0% 1.4% 932003 0.7 1.3% 1.3% 722004 0.9 2.1% 1.8% 592005 1.6 3.1% 4.3% 472006 1.3 3.5% 4.3% 362007 1.5 2.5% 4.0% 242008 0.7 1.7% 2.3% 132009 0.3 0.0% 0.0% 3

Total 7.4 2.4% 3.0%

NCOs QTD Ann.

34

Portfolio Characteristics

Home Equity - Differentiated Portfolio Characteristics

Other 37%

WA4%

VA 4%

MD3%

FL 3%

CA 15%

TN 34%

30+ Delinquency: Key Drivers

FICO Score Channel Lien Position

Geographic Distribution

% of portfolio

86% 14%

1.34%

2.44%

0%

2%

4%

6%

1st Lien 2nd Lien

% of portfolio

28% 72%

% of portfolio

1.02%

2.59%3.23% 2.97%

4.68%

0%

2%

4%

6%

>=740 720-739 700-719 660-699 <660

50% 14% 13% 15% 9%

1.81%

4.09%

0%

2%

4%

6%

Retail Wholesale/Other

First Second Total

Balance $2.1B $5.3B $7.3B

Original FICO 734 736 735

Original CLTV 70% 80% 78%

Full Doc 78% 69% 71%

Owner Occupied 85% 96% 93%

HELOCs $0.8B $3.6B $4.4B

Weighted Avg. HELOC Utilization

50% 59% 57%

35

Home Equity - Cumulative Charge-Offs

0.00%

0.50%

1.00%

1.50%

2.00%

2.50%

3.00%

3.50%

4.00%

1 3 5 7 9 11 13 15 17 19 21 23 25 27 29 31 33 35 37 39 41 43 45 47 49 51 53 55 57 59

Cu

mu

lati

ve C

harg

e-O

ff P

erc

en

t

Older vintage performance benefiting from home price appreciation

Portfolio weighted average cumulative losses expected at 3-6%

Regional Banking cumulative losses expected at 2-5%

National Specialty cumulative losses expected at 3-6%

Age (months)

2007

2006

2005

2004

20022003

2000

2001

Cum loss rate represents charge-off amount over origination volume

$ Balance (mm)

Balance %

Pre-2002 441 6%2003 736 10%2004 956 13%2005 1,471 20%2006 1,251 17%2007 1,471 20%2008 736 10%2009 294 4%

36

National Wind-Down Portfolios: OTC, Perm Mortgage, & Res CRE

0.0

0.5

1.0

1.5

2.0

2.5

3.0

4Q07 2Q08 3Q08 4Q08 1Q09 2Q09

$ B

illio

ns

OTC Balances Unfunded Commitments

$0.0

$0.4

$0.8

$1.2

$1.6

$2.0

$2.4

4Q07 2Q08 3Q08 4Q08 1Q09 2Q09

$ B

illio

ns

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

Nat'l Res CRE Balances Nat'l Res CRE Unfunded Commitments

NPLs as % of portfolio 30+day Del.

79%

One-Time Close

Permanent Mortgage1

National portfolios on track for wind-downOTC balances down 28% to $558mm from 1Q09

Completed loans paid off, modified to perm mortgage, or managed as problem assetsOTC reserves of 29.5% at 6/30/09

Perm portfolio is heterogeneous; performance varies by pool

Delinquency and severity driving higher reserves and lossesReserve growth also from available LOCOM depletion Perm mortgage reserves of 8.9% at 2Q09

Res CRE national balances down 15% to $579mm at 2Q09

Res CRE national reserves of 9.8% at 6/30/09

National Res CRE

$500

$700

$900

$1,100

$1,300

$1,500

2Q08 3Q08 4Q08 1Q09 2Q09

$ M

illio

ns

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

Perm Mortgage Balances 30+Del. Charge-Offs Ann.

1Perm Mortgage reflects consolidated asset quality trends

70%

37

Reserves/($ mm) Reserves Loans Loans

FAS114 Impaired Loans w/o Reserves

$0 $522 0.00%

FAS114 Impaired Loans w/ Reserves

$9 $26 33.67%

Other Commercial Loans $448 $9,691 4.62%

Total $456 $10,238 4.46%

$0

$100

$200

$300

$400

$500

$600

$700

$800

$900

AppraisedValue

Pre-ChargeDown Balance

CumulativeCharge Down

Book Balance(6/30/09)

$ M

illio

ns

Problem Loans Written Down to Realizable Values, Reserves Largely for Performing Credits

FAS 114 Charge-Downs2Commercial Loan Reserves

837

785522

34% write-down

(263)

1Refers to Individually Impaired Loans, ASC 310. 2Approximation based on most recent appraised value, which can be impacted by changing market conditions and asset disposition.

Generally, classified non-accrual loans over $1mm are assessed for impairment in accordance with FAS-1141

Commercial loans typically charged-down to net realizable value rather than holding reserves

38

Reconciliation to GAAP Financials

Slides in this presentation use non-GAAP information of capital markets’ return on capital. That information is not presented according to generally accepted accounting principles (GAAP), and is reconciled to GAAP information below.

4Q07 1Q08 2Q08 3Q08 4Q08 1Q09 2Q09Capital Markets Net Income Correspondent Banking 5,828 (1,435) (4,310) (16,836) 1,783 482 (5,242) Capital Markets 13,505 15,818 19,599 11,956 44,701 46,171 54,534 Total Capital Markets 19,333 14,383 15,289 (4,880) 46,484 46,653 49,292

Capital Markets Capital Correspondent Banking 89,008 93,005 103,716 108,333 126,907 137,870 145,895 Capital Markets 198,004 192,192 191,466 201,658 215,780 265,868 272,327 Total Capital Markets 287,012 285,197 295,182 309,991 342,687 403,738 418,223

Capital Markets Return on Capital excluding correspondent banking capital 27% 33% 41% 24% 83% 69% 80%Total Capital Markets Return on Capital 27% 20% 21% -6% 54% 46% 47%

Return on equity is calculated by annualizing quarterly net income divided by capital.

39

Reconciliation to GAAP FinancialsSlides in this presentation use non-GAAP information of pre-tax, pre-provision earnings. That information is not presented according to generally accepted accounting principles (GAAP), and is reconciled to GAAP information below.

($ Millions)Regional Banking 2Q09 1Q09 2Q08

Pre-Tax, Pre-Provision Earnings/(Loss) $ 38 $ 31 $ 72Provision (51) (98) (89)Reported Pre-Tax Earnings/(Loss) (13) (67) (17)

National Specialty Lending

Pre-Tax, Pre-Provision Earnings/(Loss) (19) (5) 10Provision (176) (189) (108)Reported Pre-Tax Earnings/(Loss) (195) (194) (98)

Mortgage Banking

Pre-Tax, Pre-Provision Earnings/(Loss) (33) 85 72Provision (12) (0) (4)Reported Pre-Tax Earnings/(Loss) (45) 85 68

Capital Markets

Pre-Tax, Pre-Provision Earnings/(Loss) 100 89 43Provision (21) (14) (19)Reported Pre-Tax Earnings/(Loss) 79 75 24

Corporate

Pre-Tax, Pre-Provision Earnings/(Loss) (7) (12) (22)Provision - - -Reported Pre-Tax Earnings/(Loss) (7) (12) (22)

Total Consolidated

Pre-Tax, Pre-Provision Earnings/(Loss) 79 187 175Provision (260) (300) (220)Reported Pre-Tax Earnings/(Loss) $ (181) $ (113) $ (45)

40

Reconciliation to GAAP FinancialsSlides in this presentation use non-GAAP information of TCE, TA, and Tier 1 Common. That information is not presented according to generally accepted accounting principles (GAAP), and is reconciled to GAAP information below.

1Includes goodwill and other intangible assets, net of amortization

($ Millions) 2Q09 1Q09 4Q08

Tangible Common Equity (Non-GAAP)Total equity (GAAP) $ 3,394.0 $ 3,507.7 $ 3,574.6Less: Preferred stock capital surplus - CPP 790.6 786.6 785.7Less: Noncontrolling interest 295.2 295.2 295.2Total common equity 2,308.2 2,425.9 2,493.7Less: Intangible assets (GAAP)1 234.3 235.9 237.5Tangible common equity (Non-GAAP) 2,073.9 2,190.0 2,256.2Less: Unrealized gains on AFS securities, net of tax 59.2 57.4 42.3Adjusted tangible common equity (Non-GAAP) 2,014.7 2,132.6 2,213.9

Tangible Assets (Non-GAAP)Total assets (GAAP) $ 28,758.9 $ 31,208.0 $ 31,022.0Less: Intangible assets (GAAP)1 234.3 235.9 237.5Tangible assets (Non-GAAP) 28,524.6 30,972.1 30,784.5

Tier 1 Common (Non-GAAP)Tier 1 capital $ 3,596.3 $ 3,709.0 $ 3,784.2Less: Preferred stock capital surplus - CPP 790.6 786.6 782.7 Less: Noncontrolling interest 295.2 295.2 295.2 Less: Trust preferred 300.0 300.0 300.0 Tier 1 common (Non-GAAP) 2,210.5 2,327.2 2,406.3

Risk Weighted AssetsRisk weighted assets $ 23,123.4 $ 24,771.8 $ 25,185.4

RatiosTangible common equity to tangible assets (TCE/TA) (Non-GAAP) 7.27% 7.07% 7.34%Total equity to total assets (GAAP) 11.80% 11.24% 11.52%Tier 1 common ratio (Non-GAAP) 9.56% 9.40% 9.56%Tier 1 capital to total assets (GAAP) 12.50% 11.88% 12.20%Adjusted tangible common equity to risk weighted assets (TCE/RWA) (Non-GAAP) 8.71% 8.61% 8.80%Total equity to total assets (GAAP) 11.80% 11.24% 11.52%Tangible common equity plus reserves to risk weighted assets (TCE/RWA) (Non-GAAP) 13.13% 12.64% 12.33%Total equity plus reserves to total assets (GAAP) 15.14% 14.25% 14.26%

41

FHN Investor Relations Contact Information

Dave Miller, Corporate Strategy & Investor Relations165 Madison Ave, Memphis, TN 38103(901) [email protected]

Aarti Bowman, Investor Relations165 Madison Ave, Memphis, TN 38103(901) [email protected]