FINA 522: Project Finance and Risk Analysis Lecture 12 Updated: 19 May 2007.

24

FINA 522: Project Finance and Risk Analysis Lecture 12 Updated: 19 May 2007

-

Upload

claud-morgan -

Category

Documents

-

view

223 -

download

0

Transcript of FINA 522: Project Finance and Risk Analysis Lecture 12 Updated: 19 May 2007.

FINA 522: Project Finance and Risk

Analysis

Lecture 12

Updated: 19 May 2007

Real Options in Theory and Practice

Real Options

• Use of Net Present Value (NPV) rule• Often does not capture management decisions

to change and revise operations in response to new information or conditions.

• DCF approach assumes a commitment to an operating strategy to end of project’s useful life.

• In reality the realized cash flows will be different from what management expected at the beginning.

Managerial Operating Flexibility

• As new information becomes available and uncertainty is reduced, management may alter the operating strategy to:– Reduce loses– Take advantage of favorable opportunities as

they arise

• Managerial flexibility is similar to financial option– Call option on an asset (with current value v) gives

the right, with no obligation to buy the underlying asset by paying the prescribed price- the exercise price.

– Put Option gives the right to sell the underlying asset and receive the exercise price.

– The asymmetry from having the right, but not the obligation to exercise the option gives the option its value.

– To properly evaluate an investment opportunity need to combine the evaluating of NPV of distinct cash flows with option value of operating flexibility and strategic interactions.

Common Real Options

1. Options to defer– Firm has an option to buy land for future

development of a mine.

2. Staged investments– Making a series of outlays creates the option

to abandon the enterprise mid stream.

3. Options to alter scale, to expand, to shut down

– If market conditions change then firm can adapt.

Common Real Options4. Options to abandon

− If market conditions decline badly then firm can abandon current operations.

5. Options to switch outputs or inputs− If prices or demand changes management can

change the output mix or use different inputs.

6. Growth options− An early investment e.g. oil exploration, Research

and Development project is a prerequisite or a link to future development and growth.

Comparison of Evaluation Techniques

• Discounted Cash Flow- – evaluates the net present value (NPV) of

specific investment and operating strategies.– These techniques may under value

investment opportunities.

• Real Options– Evaluates the value of having managerial

flexibility to optimize the activity over time.– Japanese firms managed to incorporate real

options into the manufacturing systems.

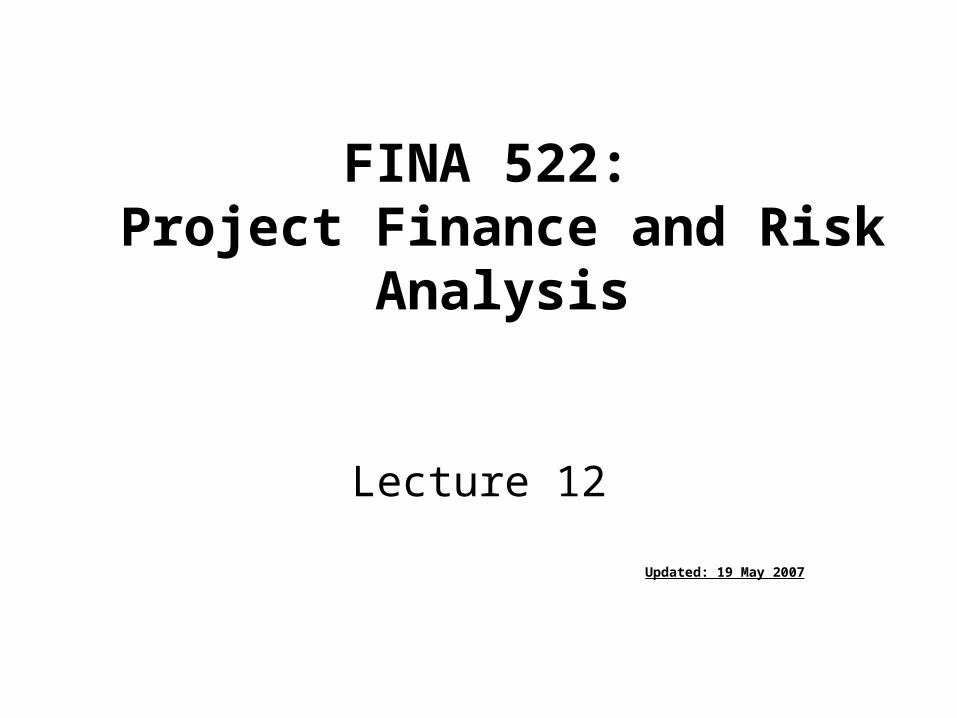

Example of Jyoti Spinning Mills

• Rup Jyoti decision in 1980s which choosing types of machines for making yarn

1. Could buy cheaper equipment that would produce lower quality yarn that could only be sold in Nepal. At that time, Nepal market was closed to international trade and very inactive.

2. Could buy more expensive equipment that would allow production of yarn of different qualities. This would allow Jyoti Mills to sell around the world if Nepal market was not good.

Example of Jyoti Spinning Mills

• Results– He purchased higher quality machines.– In early years after the firm opened, the government

opened the Nepal market to imports of higher quality yarns at lower prices.

– The market for low quality yarn in Nepal disappeared– Jyoti Mills was able to sell their yarn abroad in places

like Hong Kong, Sri Lanka, and the UK.– They survived to change in market conditions while

many of their competitors were closed down.

Real Options over time Build or investment stage Time 0 3 5 7 15 (years)

Option to expand by 50%

Option to switch use or abandon for salvage

Options to delay building for T years

Option to contract size of operation of 25% by not building last unit

Option to abandon if implementation going poorly or initial results show poor prospects

Evaluation Techniques for Real Options

1. Those that approximate the underlying stochastic process directly Include:I. Monte Carlo Simulation

II. Lattice methods

III. Log transformation binomial approach

2. Techniques that approximate the underlying differential equationsI. Numerical integration

II. Implicitly or explicit finite-differential schemes

Real Option Approach to Project Decision Making

• Building manufacturing capacity to make computer chassis

• Feasibility study- cost US$ 800,000– Options for size

• Major expansions- cost US$ 6 million• Moderate expansion- cost US$ 4 million• Minor expansion- cost US$2 million

– Market opportunities• High volume of sales US$ 6.5 million• Lower volume sales US$ 2.5 million

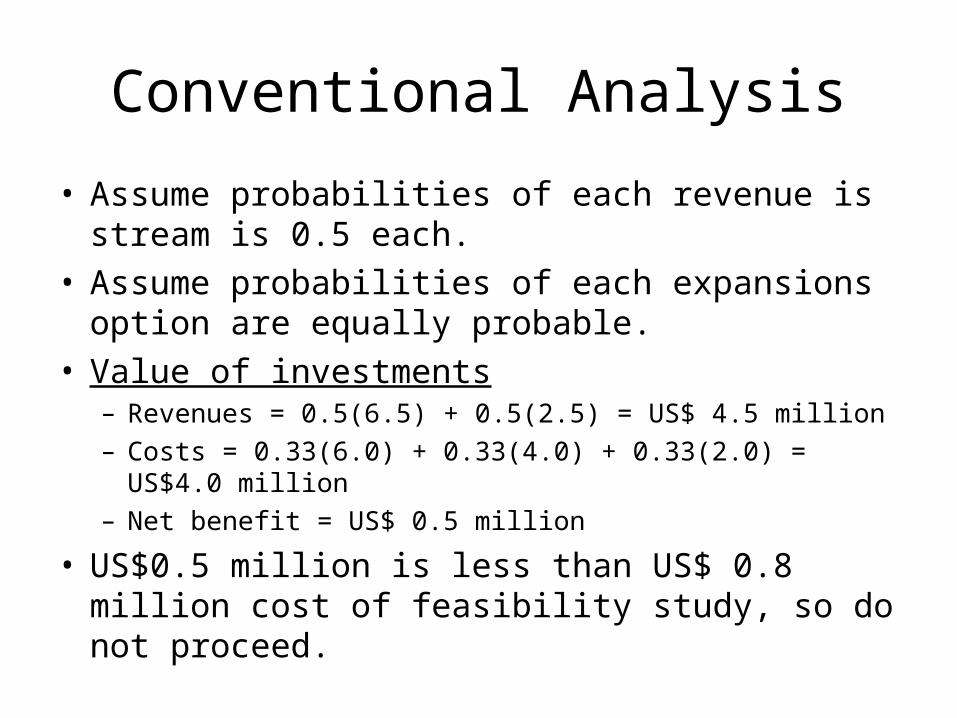

Conventional Analysis

• Assume probabilities of each revenue is stream is 0.5 each.

• Assume probabilities of each expansions option are equally probable.

• Value of investments– Revenues = 0.5(6.5) + 0.5(2.5) = US$ 4.5 million

– Costs = 0.33(6.0) + 0.33(4.0) + 0.33(2.0) = US$4.0 million

– Net benefit = US$ 0.5 million

• US$0.5 million is less than US$ 0.8 million cost of feasibility study, so do not proceed.

Real Options ApproachConductFeasibility study

US$ 0.8 m

Low: $2.5mPr = 0.5

Low: $2.5 mPr = 0.5

High: $6.5mPr = 0.5

Low:$2.5 mPr = 0.5

High: $6.5 mPr = 0.5

Minor: $2 mPr = 0.33

Moderate: $4 mPr = 0.33

Cost Revenue

Major: $6 mPr = 0.33

High: $6.5 mPr = 0.5

Real Options Approach

• We take a multi-step approach to decision making.

• During each step we incorporate newly gained information into the decision analysis.

• Beginning by estimating the profitability associated with each of the investment scenarios.

Scenario A: Major Expansion

• Expected Profit/major expansion=e (Revenue) – e Cost/Major Expansion

=US$4.5 m – US$6.0 m = -US$1.5 m

• We will never carry out a major expansion because we would expect to lose money. Better to make zero profit.

Scenario B: Moderate Expansion

• Expected Profit/moderate expansion=e (Revenue) – e Cost/moderate Expansion

=US$4.5 m – US$4.0 m = US$0.5 m

Profit = US$0.5 million

Scenario C: Minor Expansion

• Expected Profit/minor expansion=e (Revenue) – e Cost/Minor Expansion

=US$4.5 m – US$2.0 m = US$2.5 m

Profit = US$2.5 million

Overall Profitability

• E (profitability) = 0.33 (0 m) + 0.33(0.5 m) + 0.33(2.5 m) = US$1.0 million

• Expected profit is greater than cost of feasibility study of US$ 0.8 million.

• To see which scenario should be undertaken.

Second Round of Real Option Thinking

• Assume firm goes ahead with feasibility study.• Recommends that the moderate facility be built.• Marketing department starts to carry out a

careful market research to determine which of the two revenue scenarios are most likely to arise.

• Question? Should company begin to build the new facilities or wait until better market information is available.

Traditional Approach

• Expected Profit/moderate expansion=e (Revenue) – e Cost/moderate Expansion

=US$4.5 m – US$4.0 m = US$0.5 m

Profit = US$0.5 million

Real Option ApproachScenario 1: High Revenue• Expected Profit/moderate expansion and high

revenue=e (Revenue/moderate) – e Cost/moderate Expansion=US$6.5 m – US$4.0 m = US$2.5 m

Scenario 2: Low Revenue• Expected Profit/moderate expansion and low

revenue=e (Revenue/moderate) – e Cost/moderate Expansion=US$2.5 m – US$4.0 m = -US$1.5 m

• If this happens the lose US$1.5 m, if abandon idea of project then expected revenue = 0 million

Overall profitability

• If we assume that high revenue and low revenue scenarios are equal to probability = 0.5 each,

• Expected profit= e (profit) = 0.5(2.5m) + 0.5(0m) = US$1.25 m

• The profit of US$1.25 is larger than the US$0.5 computed using the tradition approach.

• Hence, worthwhile to wait until the marketing study is complete to determine anticipated revenue.

Other Considerations• Every number used when employing real option

approach is a guess.• Need to use best information available.• The probabilities of different payoffs or probabilities

of costs will not be equal.• Unlike financial options, real options are not traded.• The timing of exercising the real option is uncertain.

Some wait 2, 3, 4 months for marketing study - information improves over time.

Note:• More than 50% of the value of a real option analysis

is thinking about them before making decisions on the initial investments.

• It is a guide to decision making.