Fairchild Semiconductor International,...

65

www.fairchildsemi.com 1 Fairchild Semiconductor International, Inc. January 2010 Investor Presentation

Transcript of Fairchild Semiconductor International,...

www.fairchildsemi.com

1

Fairchild Semiconductor

International, Inc.

January 2010

Investor Presentation

www.fairchildsemi.com2

Notes on Forward Looking Statements

and Non-GAAP Measures

• Comments in this presentation other than statements of historical fact may constitute forward looking statements and are based on Fairchild’s management’s estimates and projections and are subject to various risks and uncertainties

• These risks and uncertainties are described in the Company’s periodic reports and other filings with the Securities and Exchange Commission (see the Risk Factors section) and are available at http://sec.gov and investor.fairchildsemi.com

• Actual results may differ materially from those projected in the forward looking statements

• Some data in this presentation may include non-GAAP measures that we believe provide useful information about the operating performance of our businesses that should be considered by investors in conjunction with GAAP measures that we also provide. You can find a reconciliation of non-GAAP to comparable GAAP measures at the Investor Relations section of our web site at http://investor.fairchildsemi.com

Recent additions to our website at http://investor.fairchildsemi.com

Updated Financials (through 2009 Q4, with segment revenue/gross margin breakouts)

• Quarterly Fact Sheet with 2009 Q4 highlights

• This investor presentation

www.fairchildsemi.com3

Sales were $355m, up 7% QoQ and 11% YoY... Solid performance in what is typically at flat sales quarter

Demand was higher across a broad range of end markets and regions

Under-shipped POS to reduce channel inventory 7% QoQ or >1 week to record low 8.3 weeks supply

Internal inventory decreased 3 days to 69 DOI…higher sales more than offset the $7m increase

Generated $43m in free cash flow (cash from operation – capex) due to significant cost reductions, aggressive

AR control, lower capex and strong asset management…FCF for all of 2009 is a record level $129m

Adjusted gross margin was 30.3%, up >3 points QoQ, due to better mix for new products and our focus on

higher value sockets as well as firmer pricing, lower costs and higher factory loadings

Pricing moderated to down <1% QoQ as customers are increasingly focused on product availability

Lead times extended to the low teens providing us excellent demand visibility

Analog switches, HF regulators, SPMs, HV MOSFETs along with analog power conversion products

recorded the strongest sales driven by market share gains in analog and strength in PCs, industrial and

consumer

Highlights of the Quarter – Q4 2009

www.fairchildsemi.com4

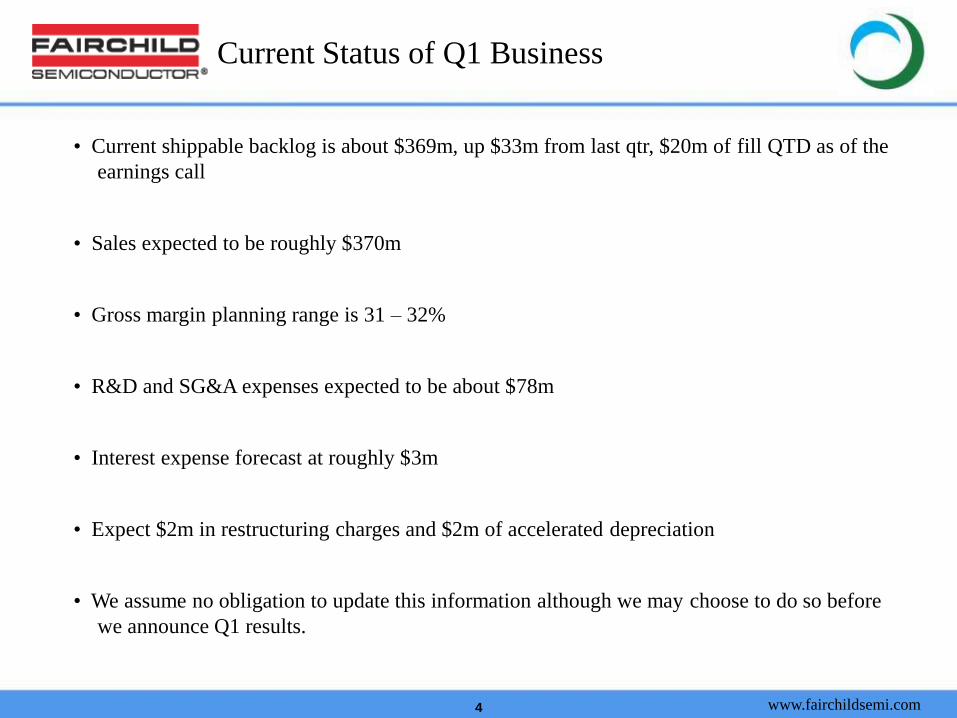

Current Status of Q1 Business

• Current shippable backlog is about $369m, up $33m from last qtr, $20m of fill QTD as of the

earnings call

• Sales expected to be roughly $370m

• Gross margin planning range is 31 – 32%

• R&D and SG&A expenses expected to be about $78m

• Interest expense forecast at roughly $3m

• Expect $2m in restructuring charges and $2m of accelerated depreciation

• We assume no obligation to update this information although we may choose to do so before

we announce Q1 results.

www.fairchildsemi.com

5

Fairchild Overview

www.fairchildsemi.com6

• Wireless Convergence and Energy

Efficiency mega-trends

• Power silicon content grows

faster than end market sales –

premium paid for efficiency

• Segment structure increases our

apps knowledge and ability to

sell solutions

• Large customers dominate these

markets and align well with

Fairchild’s strengths in SCM,

global presence and wide product

breadth

Markets That Drive Our Business

www.fairchildsemi.com7

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2007 2008 2009 2010 2011 2012

M U

nit

s

0

500

1,000

1,500

2,000

2,500

3,000

3,500

M $

Handset Units (LHS) Voltage Regulator/Reference Sales (RHS)

Power Silicon Content GrowthHandsets

• Handset growth slows gradually as market hits 1.6B units in 2012

• Voltage regulator CAGR of 13% reflects greater power management value in the handset to support new features, better resolution displays and 3G/4G

Source: iSuppli, July 2008

6% Handset Unit CAGR

13% Voltage Reg Sales CAGR

Handset Units vs Handset Voltage Reg Sales

www.fairchildsemi.com8

Power Silicon Content Growth Notebook PC

• Notebook unit growth projected to be very strong through 2012

• Power transistor/FET sales growth inline with unit sales as advances in power management drive value through improved battery life

Source: iSuppli, July 2008

0

50,000

100,000

150,000

200,000

250,000

2007 2008 2009 2010 2011 2012

M U

nit

s

0

200

400

600

800

1,000

1,200

M $

Notebook Units (LHS) Power Transistor/FET (RHS)

18% Notebook Unit CAGR

17% Pwr Trans/FET Sales CAGR

Notebook Units vs Power Transistor/FET Sales

www.fairchildsemi.com9

Power Silicon Content GrowthAppliances

• Appliance sales growth projected to grow at 7% CAGR through 2012

• Power analog & transistor sales CAGR of 10% in the same time reflects greater content of power management silicon as manufacturers adopt variable speed motors for greater efficiency and longer service life

Source: iSuppli, July 2008

0

20,000

40,000

60,000

80,000

100,000

120,000

2007 2008 2009 2010 2011 2012

M $

0

200

400

600

800

1,000

1,200

M $

Appliance Sales (LHS) Pwr Analog & Trans Sales (RHS)

7% Appliance Sales CAGR

10% Pwr Analog & Trans Sales CAGR

Consumer Appliance Sales vs Pwr Analog & Trans Sales

www.fairchildsemi.com10

Power Silicon Content GrowthLCD TV

• LCD TVs expected to continue strong growth

• Power analog & transistor sales forecasted to grow even faster as screen resolution and backlighting requirements advance and concern over energy efficiency of these devices increases

Source: iSuppli, July 2008

0

50,000

100,000

150,000

200,000

250,000

2007 2008 2009 2010 2011 2012

M U

nit

s

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

M $

LCD TV Units (LHS) Pwr Analog & Trans Sales (RHS)

22% LCD TV Unit CAGR25% Pwr Analog & Trans Sales CAGR

LCD TV Units vs Pwr Analog & Trans Sales

www.fairchildsemi.com11

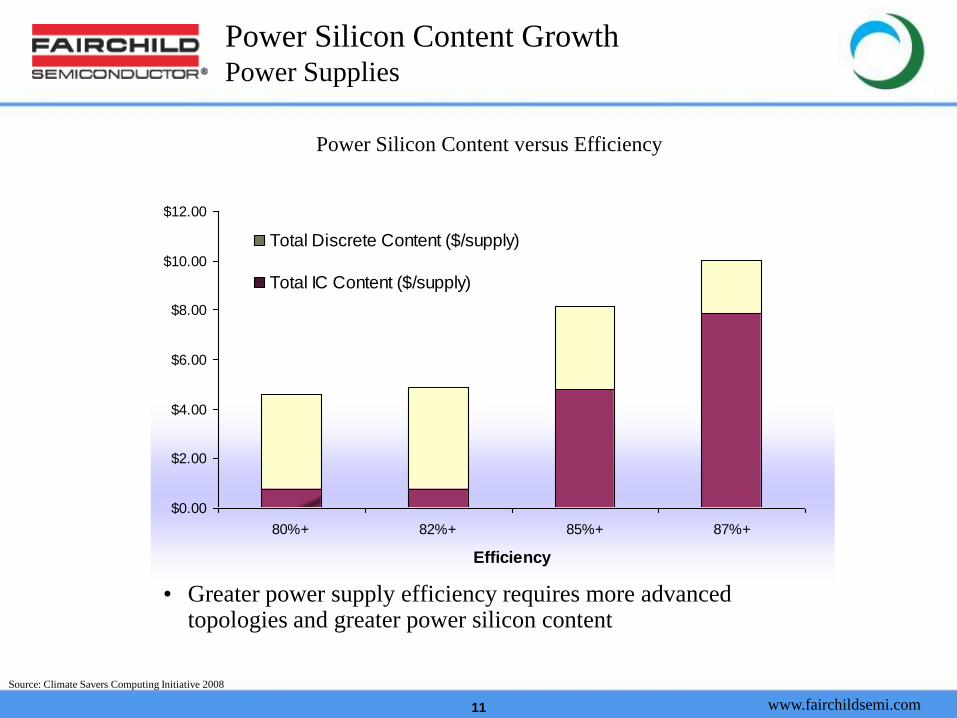

Power Silicon Content GrowthPower Supplies

• Greater power supply efficiency requires more advanced topologies and greater power silicon content

Source: Climate Savers Computing Initiative 2008

$0.00

$2.00

$4.00

$6.00

$8.00

$10.00

$12.00

80%+ 82%+ 85%+ 87%+

Efficiency

Total Discrete Content ($/supply)

Total IC Content ($/supply)

Power Silicon Content versus Efficiency

www.fairchildsemi.com12

Capitalizing on these Market Trends

• Engage with industry-leading customers in key markets to build our

applications expertise (ex. Handsets, power supplies)

• Leverage our technology leadership in analog switches, µSerDes™ and now

HF Voltage Regs to expand content and increase integration level in

handsets & ultra-portable apps

• Maintain/achieve silicon-based technology leadership in power MOSFETs

and IGBTs to deliver industry-leading margins

• Expand SPM business beyond Japan to support transition to variable speed

motors in appliances

• Greater package in-sourcing for better control and higher margins

www.fairchildsemi.com13

Acquisition Landscape

Small Privates

Carve outs

<$1B Public

Large Public

Combination

Technology/IP, Key

Personnel Talents,

Emerging Products

Easy path to profitability,

Complementary Products

Change Competitive

Structure

Enter new markets

Financial Leverage, Cost

reduction possibilities,

Complementary Products

Low, mostly around

keeping talent

Low to High, very

situation dependent

Med to High. Mgmt &

change of control issues.

Risks of culture clash

High, if priced right and

strategy fits

Pricing power elusive.

Must have strategic

synergies

Banks/sponsors and

investors who flip shares

will make the most

Reason to Pursue Integration Risk

Likelihood of Value to

FCS Shareholders

Med to High. Mgmt &

change of control issues.

Risks of culture clash

High, if priced right and

integration is crisp. Needs

strategic value beyond

beating DCF

Increasing Focus

www.fairchildsemi.com14

Fairchild Semiconductor Solid Progress, Exciting Potential

• Transition to a higher value company is well underway

• Tier 1 customer sales growing at highest rate in the company

• HF Voltage Regulators ramping rapidly

• Analog Switches growing strongly as we leverage leadership

technology

• Ramping new silicon-based MOSFET & IGBT technologies

• Segment focus drives greater application and customer intimacy –

Enables us to become a more important supplier

• Package cost reductions & tight spending controls increase confidence

in ability to achieve target model

www.fairchildsemi.com

15

Mobile, Computing, Consumer &

Communications (MCCC) Group

Overview

www.fairchildsemi.com16

MCCC Strategy Summary

Package

Technology

Leadership

Dedicated

Field

Marketing and

Applications

Teams

High Quality,

Low Cost

Manufacturing

and SCM

Focused

Product Line

Teams

Building Capabilties to enable profitable growth

Foundation

Focus

Areas

Anticipating Customer and Global Trends

MobileAnalog

Smart & Feature

Phones

ComputingMOSFET

Notebook

ConsumerMOSFET & Analog

Display

Set top Box

Networking

Focus on Mobile and

Power Efficiency

Process

Technology

Leadership

www.fairchildsemi.com17

MCCC Mobile ProductsExtend Battery Life, Enable Greater Functionality

• MOSFET

• IntelliMAX™

• Building Block Regulators

• ASSP Regulators

• Analog Switches

• USB

• µSerDes™

• Mixed Signal ASSP

Base Band and

Application Processor

PMIC

Memory

Display

Sub Display

LMU

Camera

Audio DataVideo

Display &

Camera

“uSerDes

Signal Path

Subsystems

GPSPower

SubsystemsLMU

DC:DC

RF

SD cardHDMI

Camera

DC:DC

Microphone

Power

PM

IC

www.fairchildsemi.com18

Growing Our Content in Mobile

6,000

7,000

8,000

9,000

10,000

11,000

12,000

13,000

14,000

15,000

2005 2006 2007 2008 2009 2010 2011

($M

)

$0.00

$1.00

$2.00

$3.00

$4.00

$5.00

$6.00

$7.00

2005 2006 2007 2008 2009

Addressable Content Has

Doubled in 3 years

• Signal Path

• Power Management

•Tier 1, Tier 2, China

Smart + Feature Phone SAM 15% CAGR*

Lots of room for SOM expansion

Source: iSuppli Q108

Product SAM

Smart and Feature Phone – Fairchild SAM

www.fairchildsemi.com19

Smarter Phones More Functions

• Feature & smart phone=

Fairchild opportunity

• 60% going to 80% (2011)

of phones are upgrades.

• Additional Functions are

being constrained by power

requirements.

• Top five suppliers have

>80% market share

-

200

400

600

800

1,000

1,200

2005 2006 2007 2008 2009 2010 2011

Un

its

M

Smartphone

Feature Phone

Entry Level

ULCH

PC Card

-

200

400

600

800

1,000

1,200

1,400

1,600

2005 2006 2007 2008 2009 2010 2011

Un

its

M

Music Playback

FM Radio

GPS

Application Software

Video Playback/ Streaming

Video Calling

TV Reception

Source: iSuppli Q108

><

Handset Category

Multimedia Functions

www.fairchildsemi.com20

Increasing Power Consumption

3G 3.5G Pre 4G 4G2.75G2G

GPRS

UMTS

WCDMA

TD-SCDMA

HSDPA

HSPAGSM

WiMax / WiFi

WiBroLTEEDGE

70M172M

14Mbps

384K180k56k9.6k

DATA RATE (bps)

VOICE

SMS

Internet

Browsing

Video call

Video Download

Interactive Gaming

Video Conference

Video Broadcast

VOIP

HDTV

Multiview Video

Digital TV

10hr 5hr 2:30hr 1:00hr ?hr

Talk / Connection time

www.fairchildsemi.com21

USB Switch

WLAN

Module

Mobile Handset Targeted Subsystems

Audio

Connectors

Distributed Architecture Drivers :

• Dissimilar Process Technology

• Dissimilar IC lifecycles

• Optimized power consumption/efficiency

• Improved Time to Market (modularity)

• Differentiation (feature sets and user experience)

FAIRCHILD FOCUS: Distributed Signal Path

Subsystems and Power

OVPT

X

MU

S

Bluetooth

Module

SDIO

SwitchDACCodecADCAMPAMP AMP

Application

ProcessorPMIC

Broadband

ProcessorRF Power

Chipset

LCDBacklight

Driver

DisplayGPS

Mobile TV

FeaturesMP3

Other

P

P

P1

PN

P

www.fairchildsemi.com22

Mobile Power Solutions

We strive for excellence in electrical performance:

• Ultra Low standby current

• Highest Efficiency

• Fast transient response

• Low EMI

• High precision regulation

• Digital control

www.fairchildsemi.com23

IP migrated from consumer Applications

Second generation portable video filter

• 3 Channel Video Filter / Driver

• Ideal for handsets, Personal media players (PMP), and other mobile platforms

Low power / small size

• 30% lower power than existing solutions

• Utilizes FCS SOI process

• <2mm2 Chip Scale Package

Supports (SD) and (ED) Enhanced Definition

(up to 480p)

Composite and Component outputs

Ultra-Portable Video Filter Driver

www.fairchildsemi.com24

USB Opportunity

USB is the standardized Data and Power Interface for Mobile

•Data: 1.5Mb/s, 12Mb/s, 480Mb/s, 4.8Gb/s

•Power: 500mA 5V

USB is the wired Interface for Mobile products

•85% of handsets today support USB

What’s changing?

•Mechanical standardization

•System repartitioning

•Migration from 2.0 to OTG and USB 3.0

The Opportunity?

•FSC provides a complete USB solution (less the integrated controller)

•Leverages the our power and signal capabilities

•Improve our ASP per port

•Integrated and Block Solutions

Micro

Mini

www.fairchildsemi.com25

Intellimax™: Features at a Glance

Under Voltage Lock

Out

Thermal Shutdown

At 140C with Hysteresis

Current Limit

w/ Fast Response Time(Polyfuse Competition Acts in

Tenths of Seconds to Seconds)

Error Flag

Current Limit

UVLO

Thermal

Switch

ESD

Protection at Electronic Speed

(response time)

3 to 5 µS For Over-current

20 ns For Hard Shorts

PowerGood

Slew rate contol and output

discharge

www.fairchildsemi.com26

2002 2003 2004 2005 2006 2007 2008 E

Mobile Strategy Drivers

1) More Functionality Power & Signal Path Optimization

2) Distributed Architecture

3) Manufacturing and Supply Chain Strengths

4) Business Model

5 yr CAGR: UP IC 38%

Mobile Customer MixMobile Revenue

LV UP MOSFET UP IC

www.fairchildsemi.com27

LV MOSFET Strategy

• Process Technology Leadership

• Package Technology Leadership

• Target Market Segments

www.fairchildsemi.com28

Technology Driven Cost Reduction

1998 2000 2002 2003 2005 2006 2007 2008 2009 2010 2011

• Process technology learning curve

rejuvenated

• Scale learning curve resumed

• Move to next-gen packages lower

costs and improves performance

• Technology leverage is greater

than scale leverage

$-

$10

$20

$30

$40

$50

$60

$70

0 1 2 3 4 5 6 7Volume Scenario

Pa

cka

ge

Co

st

Next Gen

Current Pkg

Current Pkg

Next Gen

Next Gen

Long Term Die Cost Trends

Relative Package Cost Curve

www.fairchildsemi.com29

Summary

• Our focused investment in Analog for mobile is working

• LV MOSFET is a great EPS growth driver

www.fairchildsemi.com

30

Power Conversion,

Industrial & Auto (PCIA)

Group Overview

www.fairchildsemi.com31

What Drives our Business?

“Green Power” needs will fuel future growth

FCS provides key technology solutions to both convert and save energy

• PFC, PWM IC’s, Low Resistivity MOSFET’s, and IGBT’s improve conversion efficiency in power supplies

• PSR controllers minimize standby energy consumption of small chargers

• LED power supplies and electronic ballast controllers drive Solid State and Compact Florescent Lighting

• Controllers, Modules and MOSFET’s/IGBT’s spin Brushless DC Motors

• IGBT’s and High Voltage Drivers invert power

• IGBT’s start a car and Modules steer it

We are a complete solutions provider in the segments that we serve

• Full family of products: discrete switches, and IC’s

• Leverage our packaging expertise to sell integrated modules (SPM, FPS, EZ family)

US Residential Energy Consumption per capita, 1990-2030,

source: EIA, Annual Energy Outlook 2008

(index, 1990 = 1)

0.800

0.850

0.900

0.950

1.000

1.050

1.100

1990 2000 2010 2020 20302006

Projected consumption with

2008 technology

Projected consumption with

improved technology

Historical consumption

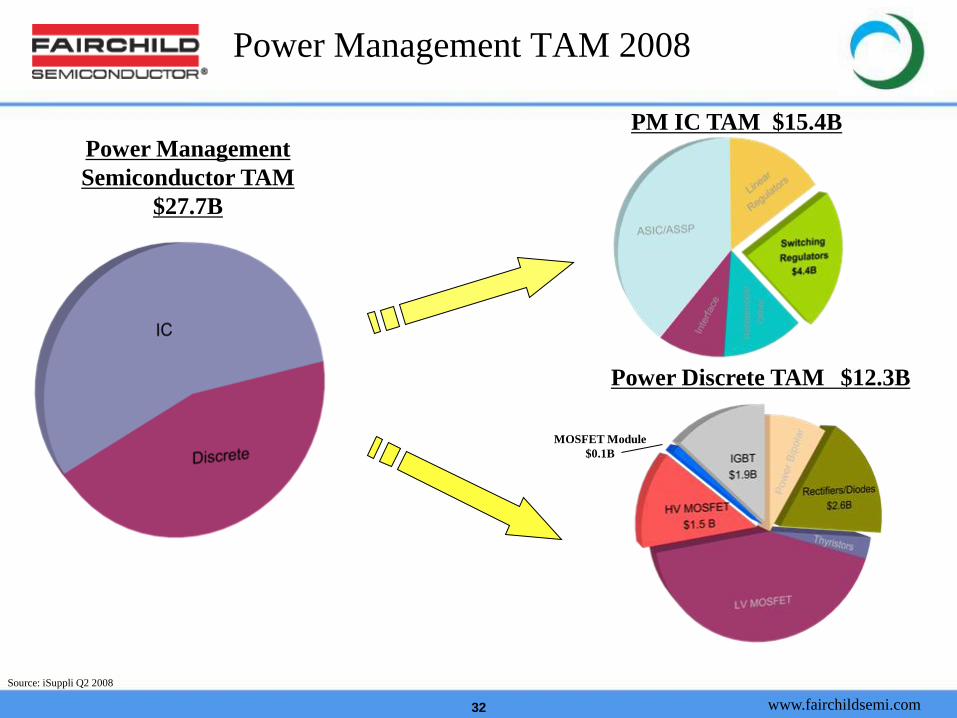

www.fairchildsemi.com32

Power Management TAM 2008

Source: iSuppli Q2 2008

MOSFET Module

$0.1B

Power Management

Semiconductor TAM

$27.7B

PM IC TAM $15.4B

Power Discrete TAM $12.3B

www.fairchildsemi.com33

PCIA SAM by Segment

2008 = $7.6B

2011 = $9.8B

CAGR = 9%

• Great combination of markets where there is synergy between the product lines

• Energy efficiency will drive growth

– IGBT, SPM markets expected to have double digit CAGR over next 4 years

– Computing power supply IC CAGR expected to be >20% even though units will only

grow by 8.5%Source: iSuppli, IMS, Displaybank, Dataquest, Fuji Chimera Institute, Darnell, Fairchild

www.fairchildsemi.com34

PCIA Snapshot

Estimated 2008 PCIA

Revenue by Region

Estimated 2008 PCIA

Revenue by Segment

www.fairchildsemi.com35

Product Line Focus

HV Discretes

• Focus on margins has driven significant improvements

• Margin and revenue growth will be driven by new products and operating leverage

Automotive

• Capitalize on other FCS technology developments

Power Conversion

• System General gaining momentum

• Significant cost reduction opportunities

• New products and applications knowledge driving increased value

Transition to a segment based structure while retaining product line expertise

• Sales aligning to this structure

• Common customer and application base

www.fairchildsemi.com36

Energy Efficiency Will Fuel

Our Growth

• In desktop computing total units are projected to be flat, but more demanding efficiency

requirements (80+ 82+ 85+ 87+) drive newer technology and increased content

• For lighting, LED’s and CFL’s are expected to grow substantially, while more traditional

technologies will shrink or maintain share

LED Incandescent Halogen CFL LF

Lighting efficiency

(lm/W)59 10 20 50 75

Efficiency of

lighting equip (%)80~90 30~50 30~50 50~60 50~70

Total efficiency

(lm/W)42 4 8 23 38

Life expectancy

(Hr)10K~50K 1k 3k 10k 15k

(Source : LEDs Magazine, 2007 May)

LED Incandescent Halogen CFL LF

Lighting efficiency

(lm/W)59 10 20 50 75

Efficiency of

lighting equip (%)80~90 30~50 30~50 50~60 50~70

Total efficiency

(lm/W)42 4 8 23 38

Life expectancy

(Hr)10K~50K 1k 3k 10k 15k

(Source : LEDs Magazine, 2007 May)

Efficiency (%) 80+ 82+ 85+ (1) 85+ (2) 87+

Total IC ($/set) 0.78 0.78 1.43 4.80 7.90

Total Discrete ($/set) 3.85 4.09 6.13 3.35 2.15

www.fairchildsemi.com37

Improving Efficiency Through SiliconPC Power Supply Example

Fairchild is positioned to provide the total solution

+12VAC Input

+3.3V

+5V

PFC +

PWM

SR + MOS

SR + MOS

AHB

+

MOS

Buck +

MOSx2

Integrated Synchronous Rectifier (SR) IC

improves efficiency +2% over traditional

Schottky diodes

Integrated DC/DC Buck regulator IC

improves efficiency +1.5% efficiency

over traditional (Mag Amplifier + Diode)

Integrated

Asymmetrical Half

Bridge (AHB) IC

improve efficiency

+1.2% over

traditional Double

Forward topology

PFC+PWM combo IC

improves efficiency

+1% at light load

condition

Total efficiency improvement = +5.7%

+5VStandby

Innovative FPS IC reduces standby

power below 100mW with no load

www.fairchildsemi.com38

Complexity Increases with PowerWe Provide Solutions Across this Range

watts

100

500

1000

50

10

Induction

Heating

Complexity

Desk Top

PC

Game

Console

Server/

Telecom

Air-Con/

Inverters &

Indus system

Cell Phone

Chargers

DVD/STB

Consumer

CFL

Lighting

LFL

Lighting

LED

Lighting

HID

Lighting

LCDTV

(> 46”)

PDP TVWashing

Machine

Note PC,

LCDTV

(< 45”)

Flyback QR Flyback /

Forward

Resonant

LLC

Soft

Switching

Multi-phase

Bridge

Hig

h E

fficiency

So

lutio

ns -

5W

to K

Ws

www.fairchildsemi.com39

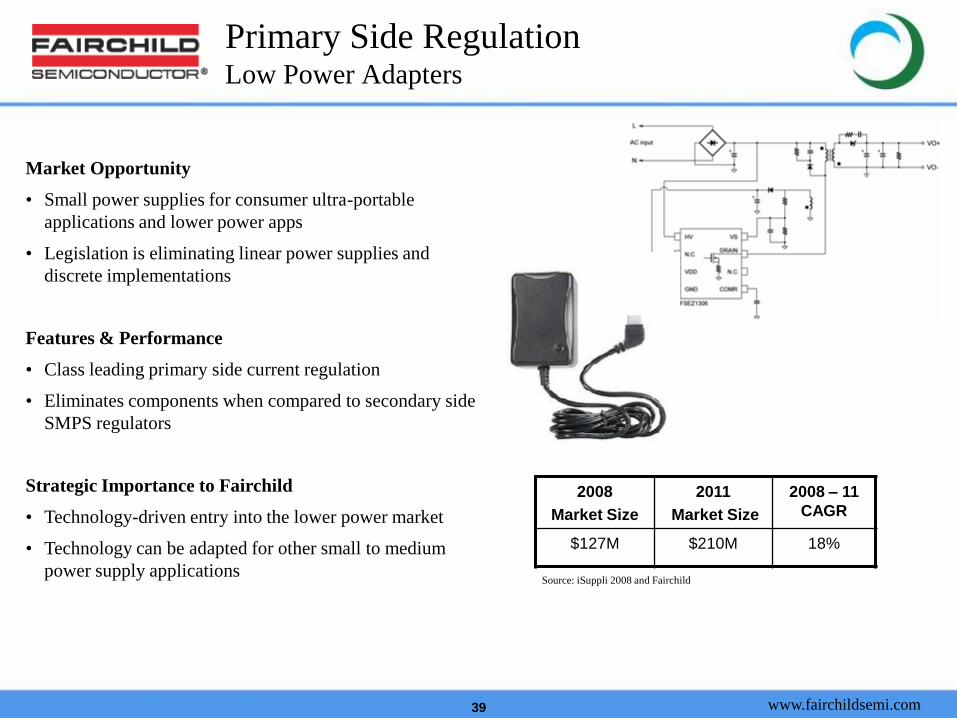

Primary Side RegulationLow Power Adapters

2008

Market Size

2011

Market Size

2008 – 11

CAGR

$127M $210M 18%

Market Opportunity

• Small power supplies for consumer ultra-portable

applications and lower power apps

• Legislation is eliminating linear power supplies and

discrete implementations

Features & Performance

• Class leading primary side current regulation

• Eliminates components when compared to secondary side

SMPS regulators

Strategic Importance to Fairchild

• Technology-driven entry into the lower power market

• Technology can be adapted for other small to medium

power supply applicationsSource: iSuppli 2008 and Fairchild

www.fairchildsemi.com40

LCD TV

FPS ($0.50-$1.50)

T-series & E-series

PFC IC ($0.20-$0.50)

CRM/CCM PFC IC

Interleaved PFC IC

BACKLIGHT IC ($0.30-$0.90)

CCFL PP/PN/NN Half bridge

CCFL PN Full bridge

LED Backlight control IC

BACKLIGHT MOSFET ($0.40-$0.90)

HV Ultra FRFET™ & FRFET®

LV MOSFET

PFC DIODE ($0.15-$0.30)

Hyperfast II & Stealth II

Total FSC Content $1.85-$5.10

PFC MOSFET ($0.30-$1.00)

SupreMOS™, SuperFET™

& UniFET™

SAM: $257M in 2008

$335M in 2011

CAGR: 9%

Source: Displaybank, Dataquest, Fuji Chimera Institute

www.fairchildsemi.com41

HV MOSFET – SupreMOSTM

PFC Switching

Source: iSuppli 2008

2008

Market Size

2011

Market Size

2008 – 11

CAGR

117M units 208M units 21%

AC Input

PFC

HV BLU

Switch

DC-DC

HV BLU

Driver

& FB

[LCD TV PSU & BLU board]

Market Opportunity

• Address the PFC switching needs in the LCD

TV market and other high power/efficiency

applications such as Servers

Features and Performance

• World-class deep Trench Super-junction

technology

Strategic Importance to Fairchild

• Next generation super-junction MOSFET

improves both cost and performance

www.fairchildsemi.com42

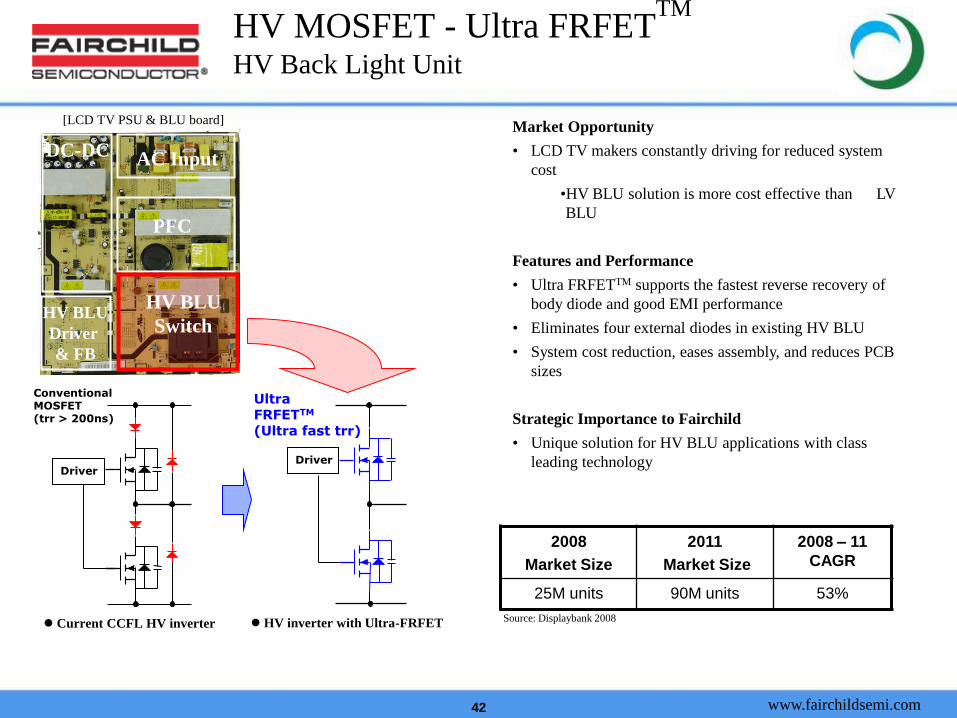

HV MOSFET - Ultra FRFETTM

HV Back Light Unit

Source: Displaybank 2008

2008

Market Size

2011

Market Size

2008 – 11

CAGR

25M units 90M units 53%

ConventionalMOSFET(trr > 200ns)

UltraFRFETTM

(Ultra fast trr)

AC Input

HV inverter with Ultra-FRFET Current CCFL HV inverter

DriverDriver

PFC

HV BLU

Switch

DC-DC

HV BLU

Driver

& FB

[LCD TV PSU & BLU board]Market Opportunity

• LCD TV makers constantly driving for reduced system

cost

•HV BLU solution is more cost effective than LV

BLU

Features and Performance

• Ultra FRFETTM supports the fastest reverse recovery of

body diode and good EMI performance

• Eliminates four external diodes in existing HV BLU

• System cost reduction, eases assembly, and reduces PCB

sizes

Strategic Importance to Fairchild

• Unique solution for HV BLU applications with class

leading technology

AC Input

www.fairchildsemi.com43

Advanced Packaging Solutions

Extend Our Reach

www.fairchildsemi.com44

BLDC Fan Motor

Drive

Compressor

Drive

Motion-SPM™

Market Opportunity

• Home appliance market is rapidly adopting inverter

technology to improve efficiency

Features and Performance

• Simple to Design

–Optimized footprint

–Built-in protection functions

–Matched component performance

• Simple to Assemble

–Reduced components

–Increases productivity and reliability

–Eliminates additional insulation material

Strategic Importance to Fairchild

• Key component in an inverter system

• Value solutions

• Growth driver for HV organization

2008

Market Size

2011

Market Size

2008 – 11

CAGR

$238M $408M 20%

Source: IMS, Fuji Chimera Institute, Fairchild

www.fairchildsemi.com45

Smart Power Integrated ModuleSystem Air Conditioning

Market Opportunity

• New energy regulations driving rapid increase

in variable speed drives

Features and Performance

• 3 phase IGBT inverter using HVIC reduces

auxiliary power parts

• Higher reliability

• Advanced IGBT technology

• Built-in sensing

Strategic Importance to Fairchild

• Increased functionality evolution of SPM

• Flexible structure easily modified

2008

Market Size

2011

Market Size

2008 – 11

CAGR

$42M $97M 32%

Source: IMS, Fuji Chimera Institute, Fairchild

www.fairchildsemi.com46

Engine Control

Ignition

Fuel Injection

Glow Plug

BLDC Motor Control

EPS

Cooling

Pumps

Body Load Control

HID

PTC-Heater

HEV

Full Hybrid

Mild Hybrid

Micro Hybrid (Start/Stop)

Transmission Control

Engine Control

Ignition

Fuel Injection

Glow Plug

BLDC Motor Control

EPS

Cooling

Pumps

Body Load Control

HID

PTC-Heater

HEV

Full Hybrid

Mild Hybrid

Micro Hybrid (Start/Stop)

Transmission Control

Automotive

Power Modules ($8.00 – $14.28)

• EPS/EHPS Modules

• Auxiliary VSD’s

Discrete Power($0.07 – $0.35)

• Low Voltage MOSFET’s

• Mid Voltage MOSFET’s

• High Efficiency Diode

Ignition ($0.30 – $4.00)

• Current Limit IGBTs

• Smart IGBT

SAM: $2.1B in 2008

$2.8B in 2011

CAGR: 10%

Functional Drivers ($0.30 – $2.15)

• Smart Switches

• Gate Drivers

• Motor Controls

Source: IMS Research 2007, Fairchild

2003 2004 2005 2006 2007 2008 YTD

Total Revenue Gross Profit%

www.fairchildsemi.com47

Advanced Automotive Power ModulesElectric Power Steering (EPS/EHPS) Modules

2008

Market Size

2011

Market Size

2008 – 11

CAGR

$71.1M $118.2M 19%

Source: IMS Research, 2007

Market Opportunity

• Automotive auxiliaries are being electrified for

improved MPG and CO2 emissions

Features & Performance

• Inverter module with enhanced electrical and thermal

characteristics enabling higher power handling and

improved EMI

• Compact design, integrating MOSFET’s, filters and

sensors

• EPS module enables customer to provide higher

torque output, expanding the field of application of

their EPS systems.

Strategic Importance to Fairchild

• EPS use increasing and moving into heavier vehicles,

requiring module functionality

• Leverage SPM® technology where its added value is

the highest

www.fairchildsemi.com48

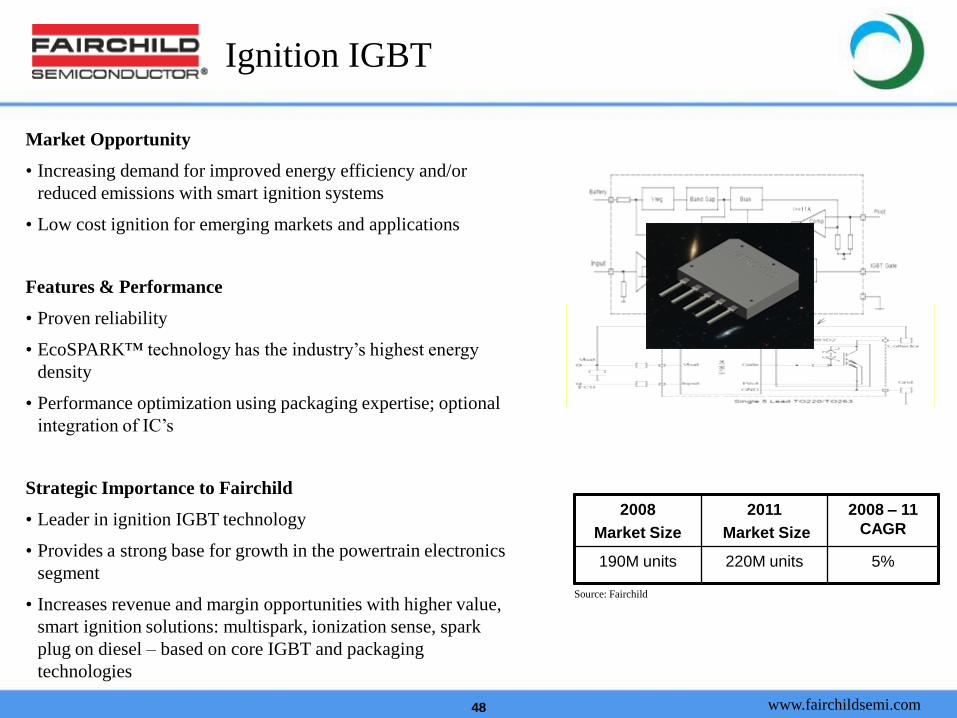

Ignition IGBT

Market Opportunity

• Increasing demand for improved energy efficiency and/or

reduced emissions with smart ignition systems

• Low cost ignition for emerging markets and applications

Features & Performance

• Proven reliability

• EcoSPARK™ technology has the industry’s highest energy

density

• Performance optimization using packaging expertise; optional

integration of IC’s

Strategic Importance to Fairchild

• Leader in ignition IGBT technology

• Provides a strong base for growth in the powertrain electronics

segment

• Increases revenue and margin opportunities with higher value,

smart ignition solutions: multispark, ionization sense, spark

plug on diesel – based on core IGBT and packaging

technologies

2008

Market Size

2011

Market Size

2008 – 11

CAGR

190M units 220M units 5%

Source: Fairchild

www.fairchildsemi.com49

Improving Margins Through TechnologyHV MOSFET Area x RDS(on) Trend

• 5% annual resistivity reduction

in planar devices

• Significant change with

introduction of charge balance

devices

• Costs roughly scale with Area x

RDS(on)

Charge Balance

Technology

Planar

Technology1995 1997 1999 2001 2003 2005 2007 2009

Introduction Year

Planar

Charge Balance

www.fairchildsemi.com50

Summary

• Energy efficiency demands will drive demand for our products

• The new segment based structure is optimized to capitalize on these

opportunities at our power supply customers

• Revenue and margin progression will occur through a combination

of new product/technology introductions and cost reductions

• Automotive is positioned for profitable growth

www.fairchildsemi.com

51

Finance Overview

www.fairchildsemi.com52

Financial Highlights

• Focus on asset management, cash generation and maintaining a lean

cost structure

• Adj GM at high end of guidance range at 30.3%

• 80% fall through of incremental sales to gross profit

• Internal inventory decreased 3 days QoQ to 69 DOI…higher sales

more than offset $7m increase

• Channel inventory decreased 7% QoQ, record low 8.3 weeks

• Other working capital reductions and aggressive cost controls

enabled $43m in FCF in Q4 and a record $129m in 2009

www.fairchildsemi.com53

Adjusted Revenue & GM%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

200.0

250.0

300.0

350.0

400.0

450.0

500.0

Gro

ss M

argi

n %

Re

ven

ue

(M$

)

www.fairchildsemi.com54

8 Qtr Rolling Adj. Revenue & GM%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

200.0

250.0

300.0

350.0

400.0

450.0

500.0

8 Q

tr R

olli

ng

Gro

ss M

argi

n %

8 Q

tr R

olli

ng

Re

ven

ue

(M

$)

www.fairchildsemi.com55Note : Includes Equity Comp

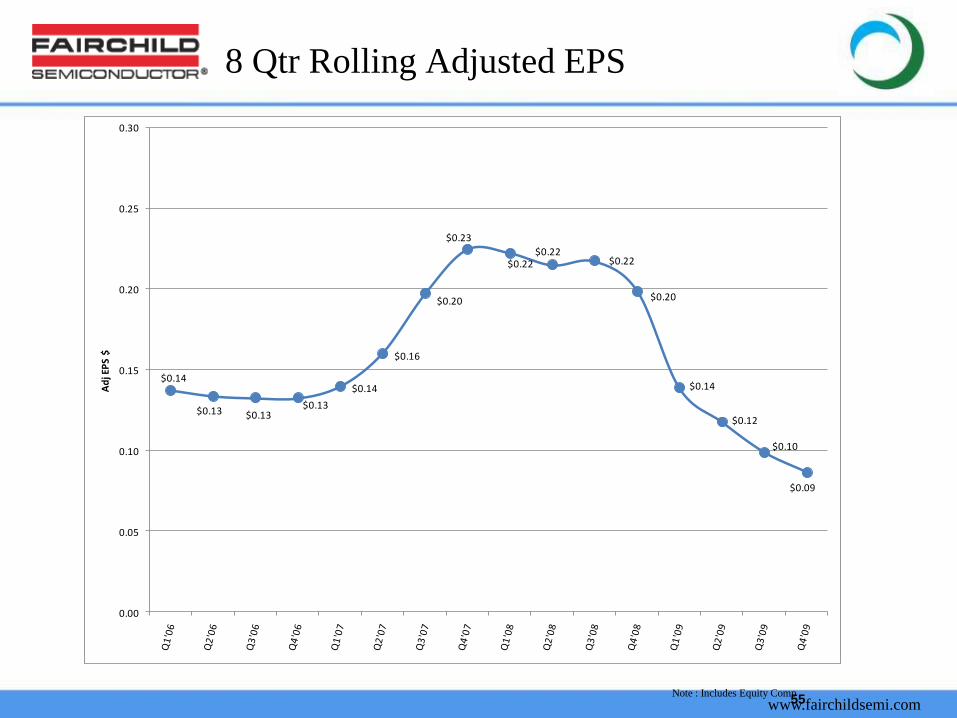

8 Qtr Rolling Adjusted EPS

$0.14

$0.13 $0.13 $0.13

$0.14

$0.16

$0.20

$0.23

$0.22 $0.22 $0.22

$0.20

$0.14

$0.12

$0.10

$0.09

0.00

0.05

0.10

0.15

0.20

0.25

0.30

Ad

j EP

S $

www.fairchildsemi.com

56

Increasing Gross Margins

www.fairchildsemi.com57

Gross Margin ImprovementKey Drivers

Growth of new product families with higher margins

• µSerDes™, Analog Switches, HF Voltage Regulators, System General, SupreMOS, integrated power systems (SPM), IntelliMAX™, DrMOS, Digital Power

Divest / Reduce low margin business

• Divest = Motor ICs, LEDs, RF

• Reduce = Planar MOSFETs, small signal and bipolar transistors

Manufacturing cost reductions and product redesigns

• Package in-sourcing

• 8” upgrade in Maine

• Fab process upgrades/shrinks for HV & LV MOSFETs, IGBTs and Power Conversion

www.fairchildsemi.com58

Margin Drivers

Growing Profitable New Product Families

MCCC Growth Drivers

-Switches USB and multimedia applications

-High Frequency Voltage Regulators Highly efficient regulators for handsets

-Power Trench Technology Potentially best figure of merit for low

voltage applications

-µSerDes™ Proliferation to top 5 cell phone suppliers

-Digital Power Flexible power mgmt for high-end POL and

power supply applications

PCIA

-Power Conversion System General acquisition, driver for

energy efficiency

-SupreMOS/FS IGBT Potentially best figure of merit for high

voltage applications

-HF Voltage Regulators New high performance platform addresses

emerging needs

-SPM Highly efficient package-level integrated

power management solutions

www.fairchildsemi.com59

$0

$200

< 0 0 > 10 10 > 20 20 > 30 30 > 40 40 > 50 50 >

Mil

lio

ns $

0%

40%

% o

f T

ota

l

Margin Drivers

Shifting Our Margin Profile

Decrease Population I

• Minimize through lead time

• Obsolete / exit / divest

• Cost reductions / product

redesigns

Manage Population II

• Cost reduction

• Pricing

• Technology migrations

Grow Population III

• New product design wins

• Responsive supply chains

Low Margin Average Margin High Margin

www.fairchildsemi.com60

Margin DriversProcess Upgrades will Drive Front End Savings

• Maine 8” conversion will increase die capacity by ~70% with

minimal impact to fixed and variable overhead

• Migration of System General and other Bucheon processes to

Maine fab on 0.5µm or lower will increase Power Conversion

margins by ~600 bps

• SupreMOS and FS Trench IGBT processes in Bucheon drive

30% to 40% die shrink while maintaining RDS on performance

• PT7 & PT9 processes in Salt Lake to increase die per wafer by

30% to 45%

www.fairchildsemi.com

61

Strong Cash Flow and Balance Sheet

www.fairchildsemi.com62

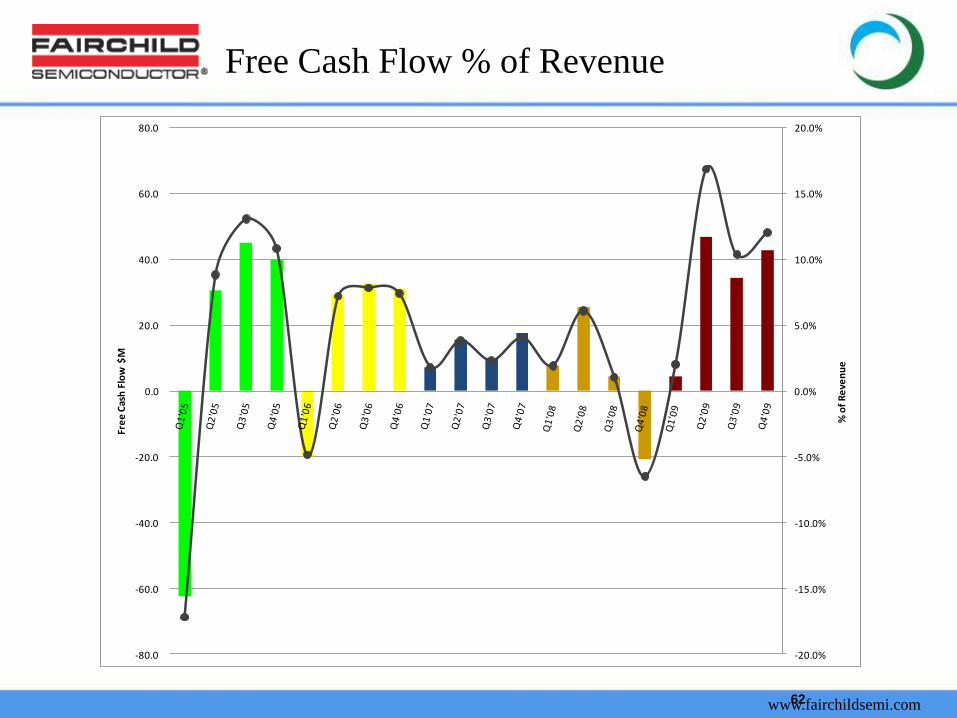

Free Cash Flow % of Revenue

-20.0%

-15.0%

-10.0%

-5.0%

0.0%

5.0%

10.0%

15.0%

20.0%

-80.0

-60.0

-40.0

-20.0

0.0

20.0

40.0

60.0

80.0

% o

f R

eve

nu

e

Fre

e C

ash

Flo

w $

M

www.fairchildsemi.com63

8 Qtr Rolling Free Cash Flow

-10.0

-5.0

0.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

40.0

8Q

tr R

olli

ng

Fre

e C

ash

Flo

w M

illio

ns

$

www.fairchildsemi.com64

Fairchild: The Power Franchise®

• Better cycle management has enabled rapid inventory correction and solid asset management results through a very challenging macro-economic environment

• Top priority going forward is margin growth through:

• Profitable sales growth in analog and functional power products

• Better mix of products due to more new products and reduction/divestiture of low margin business

• Product cost reduction driven by increased A&T in-sourcing, fab shrinks, fab consolidation and new processes

• Reduced D&A due to consolidations and long term lower CAPEX spending

• Structural changes to reduce OPEX and improve earnings

• Expect improved cash flow as we improve EBIT and maintain low CAPEX

We’re making solid progress at transitioning Fairchild to be a premier power management company…not only in sales but also profitability!

www.fairchildsemi.com

Follow us on Twitter twitter.com/fairchildSemi

View product and company videos, listen to podcasts and comment on our blog @ www.fairchildsemi.com/engineeringconnections

Visit us on Facebook @ www.facebook.com/FairchildSemiconductor