Pacific Horizon Investment Trust PLC -...

52

Annual Report and Financial Statements 31 July 2011 Pacific Horizon Investment Trust PLC

Transcript of Pacific Horizon Investment Trust PLC -...

Annual Report and Financial Statements 31 July 2011Pacific Horizon Investment Trust PLC

1 Company Summary 2 Year’s Summary 3 Five Year Summary 4 Chairman’s Statement 6 Managers’ Overview 8 Distribution of Portfolio 8 Thirty Largest Equity Holdings 9 Classification of Investments 10 Managers’ Portfolio Review12 Review of Investments14 List of Investments16 Ten Year Record17 Directors and Managers18 Directors’ Report25 Directors’ Remuneration Report

27 Statement of Directors’ Responsibilities28 Independent Auditor’s Report29 Income Statement30 Balance Sheet31 Reconciliation of Movements in

Shareholders’ Funds 32 Cash Flow Statement33 Notes to the Financial Statements42 Notice of Annual General Meeting45 Further Shareholder Information46 Analysis of Shareholders47 Cost-effective Ways to Buy and Hold

Shares in Pacific Horizon49 Communicating with Shareholders

Contents

THIS DOCUMENT IS IMPORTANT AND REQUIRES YOUR IMMEDIATE ATTENTION. If you are in any doubt as to the action you should take you should consult your stockbroker, bank manager, solicitor, accountant or other independent financial adviser authorised under the Financial Services and Markets Act 2000 if you are in the United Kingdom or, if not, from another appropriately authorised financial adviser.

If you have sold or otherwise transferred all of your ordinary shares in Pacific Horizon Investment Trust PLC, please forward this document, together with any accompanying documents,as soon as possible to the purchaser or transferee, or to the stockbroker, bank or other agent through whom the sale or transfer was or is being effected for delivery to the purchaser or transferee.

Excluding Japan, the Trust invests throughout the Asia-Pacific region including the Indian Sub-continent.

PACIFIC HORIZON INVESTMENT TRUST PLC 1

ComPany summary

Company data at 31 July 2011

Shareholders’ funds Market capitalisation

£137m £127m

Company Summary

Investment Policy Pacific Horizon’s objective is to invest in the stockmarkets of the Asia-Pacific region (excluding Japan) and in the stockmarkets of the Indian Sub-continent in order to achieve capital growth.

The Company is prepared to move freely between the markets of the region as opportunities for growth vary. The portfolio will normally consist entirely of quoted securities.

Further details of the Company’s investment policy are given in the Directors’ Report.

Comparative Index For the year to 31 July 2011 the principal index against which performance is measured is the MSCI All Country Far East ex Japan Index (in sterling terms). From the 1 August 2011 the comparative index will be the MSCI All Country Asia ex Japan Index (in sterling terms).

Management Details Baillie Gifford & Co are appointed as investment managers and secretaries to the Company. The Managers may terminate the Management Agreement on six months’ notice and the Company may terminate on three months’ notice.

Management Fee Baillie Gifford & Co’s annual remuneration is 1.0% of total assets less current liabilities, calculated on a quarterly basis.

Capital Structure At the year end the Company’s share capital consisted of 76,932,002 ordinary shares of 10p each which are issued and fully paid. The Company currently has powers to buy back a limited number of its own ordinary shares for cancellation at a discount to net asset value per share (NAV) as well as to issue shares at a premium to NAV. The Directors are seeking to renew these authorities at the forthcoming Annual General Meeting.

Savings Vehicles Pacific Horizon shares can be held through a variety of savings vehicles (see page 47).

AIC The Company is a member of the Association of Investment Companies.

Duration of the CompanyAt the Annual General Meeting of the Company held on 24 October 2006, the shareholders approved the resolution postponing until the date of the Annual General Meeting of the Company to be held in 2011 or 30 November 2011, whichever is earlier, or such later date as the shareholders may resolve, the obligation of the Directors to convene an Extraordinary General Meeting at which a resolution will be proposed pursuant to section 84 of the Insolvency Act 1986 to wind the Company up voluntarily.

The Directors are proposing a resolution at this year’s Annual General Meeting to postpone the obligation of the Directors to convene such a meeting for a further five years.

Notes None of the views expressed in this document should be construed as advice to buy or sell a particular investment.

Investment trusts are UK public listed companies and as such comply with requirements of the UK Listing Authority. They are not authorised or regulated by the Financial Services Authority.

Pacific Horizon’s objective is to invest in the stockmarkets of the Asia-Pacific region (excluding Japan) and in the stockmarkets of the Indian Sub-continent in order to achieve capital growth.

2 ANNUAL REPORT 2011

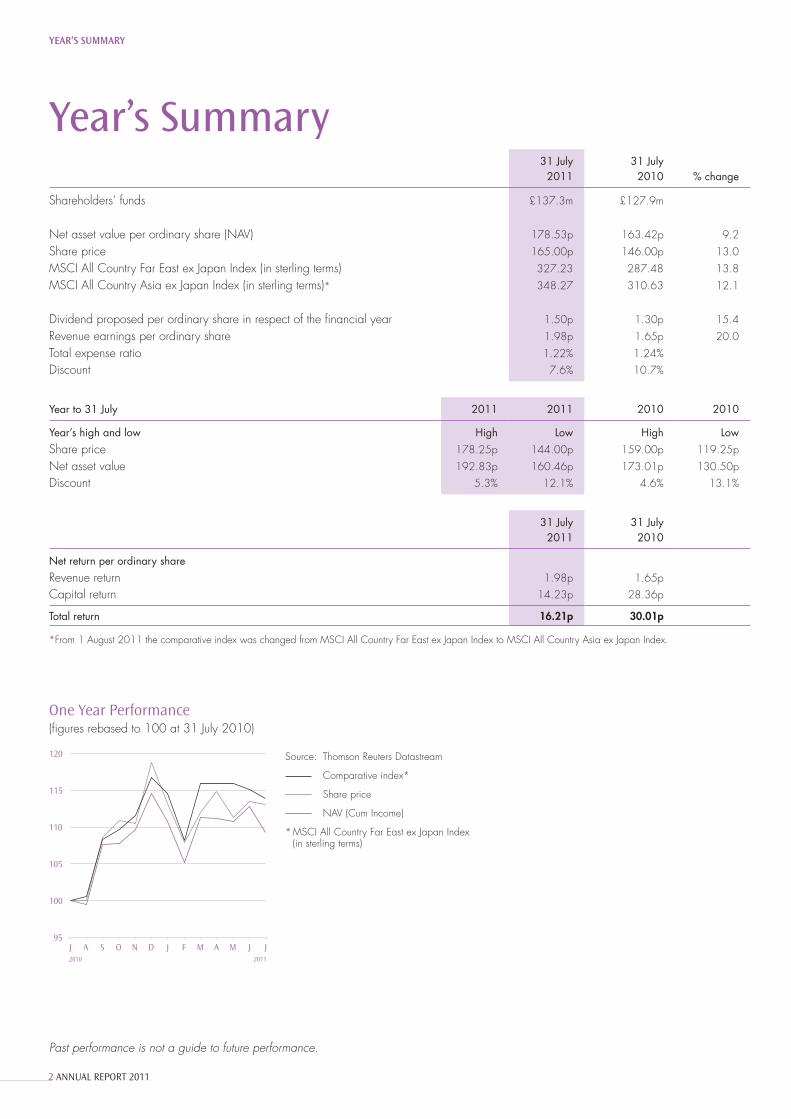

yEar’s summary

Year’s Summary31 July 2011

31 July 2010 % change

Shareholders’ funds £137.3m £127.9m

Net asset value per ordinary share (NAV) 178.53p 163.42p 9.2

Share price 165.00p 146.00p 13.0

MSCI All Country Far East ex Japan Index (in sterling terms) 327.23 287.48 13.8

MSCI All Country Asia ex Japan Index (in sterling terms)* 348.27 310.63 12.1

Dividend proposed per ordinary share in respect of the financial year 1.50p 1.30p 15.4

Revenue earnings per ordinary share 1.98p 1.65p 20.0

Total expense ratio 1.22% 1.24%Discount 7.6% 10.7%

Year to 31 July 2011 2011 2010 2010

Year’s high and low High Low High LowShare price 178.25p 144.00p 159.00p 119.25p

Net asset value 192.83p 160.46p 173.01p 130.50pDiscount 5.3% 12.1% 4.6% 13.1%

31 July 2011

31 July2010

Net return per ordinary shareRevenue return 1.98p 1.65pCapital return 14.23p 28.36p

Total return 16.21p 30.01p

*From 1 August 2011 the comparative index was changed from MSCI All Country Far East ex Japan Index to MSCI All Country Asia ex Japan Index.

Past performance is not a guide to future performance.

Source: Thomson Reuters Datastream

Comparative index*

Share price

NAV (Cum Income)

* MSCI All Country Far East ex Japan Index(in sterling terms)

105

110

115

120

100

95

2011

J A S O N D J F M A M J J2010

One Year Performance(figures rebased to 100 at 31 July 2010)

PACIFIC HORIZON INVESTMENT TRUST PLC 3

FIVE yEar summary

Five Year SummaryThe following charts indicate how Pacific Horizon has performed relative to its comparative index (MSCI All Country Far East ex Japan Index (in sterling terms)) and the relationship between share price and net asset value over the five year period to 31 July 2011.

5 Year Total Return Performance Share Price, Net Asset Value and Index(figures rebased to 100 at 31 July 2006)

Annual Share Price Total Return and NAV Total Return

(Discount)/Premium to Net Asset Value(figures plotted on a monthly basis)

Annual Share Price Total Return and NAV Total Return(compared to the MSCI All Country Far East ex Japan Index total return (in sterling terms))

Past performance is not a guide to future performance.

Source: Thomson Reuters DatastreamDividends are reinvested

Comparative index total return

NAV total return

Share price total return

CUMULATIVE TO 31 JULY

100

2006 2007 2008 2009 2010 2011

220

140

60

180

Source: Thomson Reuters Datastream

Pacific Horizon (discount)/premium

The (discount)/premium is the difference betweenPacific Horizon’s quoted share price and its underlyingnet asset value.

YEARS TO 31 JULY2006 2008 2009 2010 2011

(20%)

(10%)

(5%)

0%

5%

10%

2007

(15%)

Source: Thomson Reuters DatastreamDividends are reinvested

NAV total return

Share price total return

YEARS TO 31 JULY

2007 2008 2009 2010 2011(40%)

(20%)

0%

20%

40%

60%

80%

Source: Thomson Reuters DatastreamDividends are reinvested

NAV total return compared to thetotal return on the comparative index

Share price total return compared to thetotal return on the comparative index

YEARS TO 31 JULY

2011(20%)

(10%)

0%

10%

20%

30%

20102007 2008 2009

4 ANNUAL REPORT 2011

CHaIrman’s sTaTEmEnT

Past performance is not a guide to future performance.

Chairman’s Statement

PerformanceIn the year to 31 July 2011 net asset value per share increased by 9.2%, compared to a 13.8% rise in the MSCI All Country Far East ex Japan Index (in sterling terms). The share price rose by 13.0% and the discount narrowed from 10.7% to 7.6%. Some of our top ten holdings performed strongly over the period, including Hyundai Mobis, a Korean auto parts supplier for the Hyundai Motor Group, and Baidu, a Chinese internet search business. Other strong performers included China National Building Material, a Chinese cement producer, China Life Insurance (Taiwan), a Taiwanese life insurer, and Bank Negara Indonesia, an Indonesian bank. All of these stocks rose by over 50% in sterling terms over the course of the Company’s year. Most of the underperformance against the comparative index occurred in the first half of the year, caused by weakness in holdings in India and some industrial companies as well as a low weighting in the markets of Korea and Taiwan, which were both strong performers. The Managers’ Report on page 6 and pages 10 and 11 contains a more detailed explanation, together with a summary of the performance of the principal markets in which the Company is invested and the Managers’ comments on them.

There was no gearing during the year and at the year end net current assets were equal to 1.1% of shareholders’ funds.

Earnings per share rose by 20% to 1.98p from 1.65p for the previous year. The Board is recommending that a dividend of 1.50p should be paid.

Comparative IndexUntil 1 August 2011the principal index against which performance was measured was the MSCI All Country Far East ex Japan Index (in sterling terms). From1 August 2011, the comparative index will be the MSCI All Country Asia ex Japan Index (in sterling terms). The change was made to reflect better the Company’s investible universe.

Continuation of the CompanyAt this year’s Annual General Meeting (‘AGM’) the Directors are proposing, in accordance with the Articles, that the life of the Company be extended for a further five years. If the continuation vote were not to be approved, the Directors would convene a meeting, to be held on or around 30 November 2011, at which a further resolution would be proposed to wind up the Company voluntarily and to appoint a liquidator following which the Company’s portfolio would be realised, with shareholders being entitled, in proportion to their respective holdings, to the net proceeds of the liquidation. At this meeting, in accordance with the Articles, every shareholder present in person or by proxy and entitled to vote should be obliged to vote in favour of the resolution to wind up the Company and any votes proposed to be cast against that resolution should not be counted as valid votes.

Your Directors are aware that performance in the volatile markets which have followed the financial crisis of 2008/9 has been disappointing. However, we are also aware that since Baillie Gifford were appointed Managers of the Company in 1992 performance has generally been good, and having conducted a thorough review of the Managers’ approach and resources we judge them to have the right team to manage a portfolio in what we still consider to be a region with outstanding long term prospects for investment.

Your Directors therefore believe that it is desirable to extend the Company’s life and recommend that shareholders vote in favour of the extension for a further period of five years.

Share buy backs During the year the Company bought back a total of 1,355,000 ordinary shares, representing 1.7% of the issued share capital as at 31 July 2010, at a cost of £2,213,000. We shall be asking shareholders to renew the mandate to repurchase up to 14.99% of the outstanding shares at the forthcoming AGM.

PACIFIC HORIZON INVESTMENT TRUST PLC 5

CHaIrman’s sTaTEmEnT

The Board is aware that one shareholder would like the Company to undertake a tender offer and some would like the Company to announce a stated discount level at which it would buy back stock for cancellation. Having heard the views of other shareholders, and considered market turbulence along with the Company’s current size and liquidity, the Board is of the view that it would be in the best interest of shareholders overall to commit to buying back shares in an opportunistic fashion based on the Company’s relative and absolute level of discount, rather than commit to a formula for redemptions.

Changes to the BoardPeter Mackay, my predecessor as Chairman, retired from the Board at last year’s AGM and Michael Morrison, a Director since 2002, retired in March this year. Gerald Smith will not be standing for re-election at the coming AGM following his appointment as Baillie Gifford’s Chief Investment Officer, but will continue to be accessible to us in his new role. I should like to thank all three for their service to the Company, and in particular Peter Mackay for his wise leadership of the Board. I am pleased to welcome to the Board Elisabeth Scott, who brings with her extensive experience of investment management in South East Asia. Shareholders will be asked to confirm her appointment at the AGM.

Annual General MeetingThis year’s AGM will take place on 17 October 2011 at the offices of Baillie Gifford & Co in Edinburgh at 10.45am. Mike Gush, who manages your portfolio, will make a presentation and, along with the Board, will answer any questions. I hope to see as many of you as possible there.

OutlookDespite the problems of debt and slow growth currently faced by the developed world the Board and Managers consider that the attractions of investing in the regions of the Asia-Pacific and Indian sub-continent remain strong. Continued urbanisation, industrialisation, the building of infrastructure, the emerging consumer class and generally sound fiscal management suggest continued growth in excess of that within the capacity of the developed world, and shareholders have the opportunity to take advantage of these trends by investing through a portfolio of companies with sound managements and strong competitive positions.

JEAN MATTERSON 9 September 2011

6 ANNUAL REPORT 2011

managErs’ oVErVIEw

Managers’ Overview

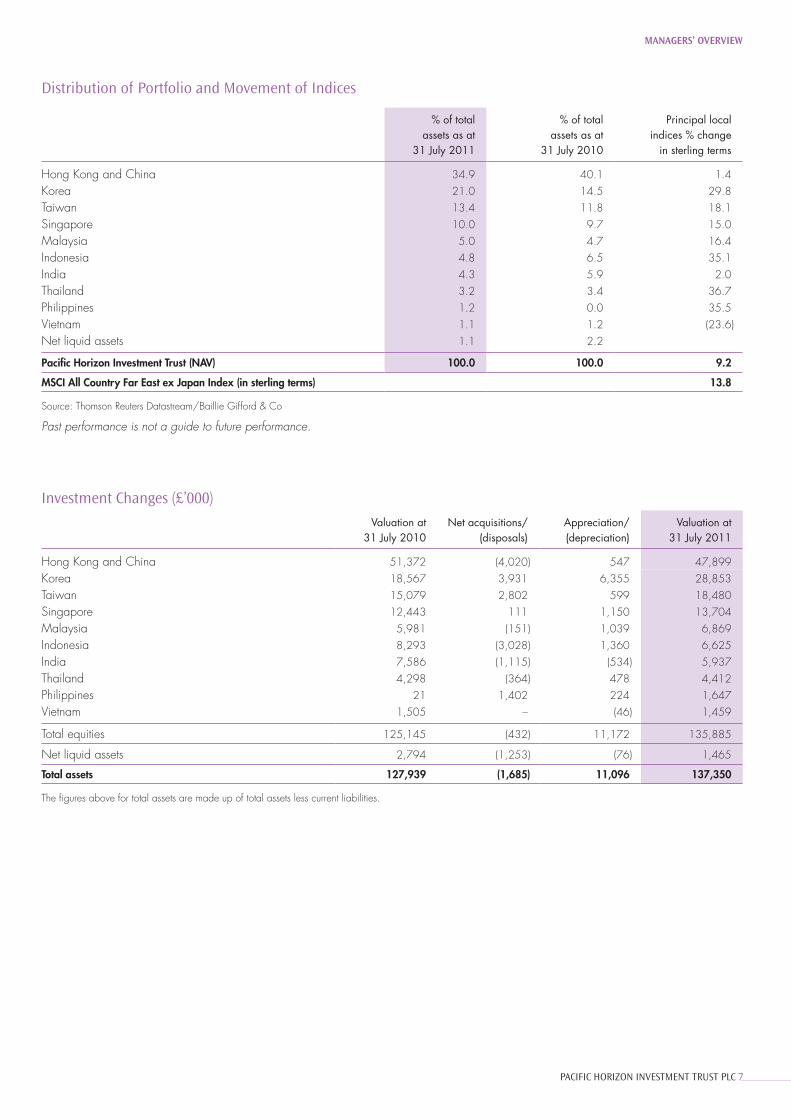

In the year to 31 July 2011 markets in the region have performed well, especially for sterling based investors. The best performing markets in sterling terms were Thailand, the Philippines and Indonesia, all up over 35%. The poorest performing markets in sterling terms were Vietnam, Hong Kong and India. A geographical review can be found under the ‘Managers’ Portfolio Review’ on pages 10 and 11.

The most notable change to the distribution of the Company’s assets by geography has been a large increase in Korea. This is a result of the number and quality of opportunities we are finding for investment, relative to those elsewhere, rather than an asset allocation decision. Small increases have also been made to Taiwan, the Philippines, and Singapore. These changes have been funded mainly through reductions in Hong Kong and China, India and Indonesia. In terms of industrial sector, changes in the portfolio have been minor. The largest increases have been in the Financials and Industrials sectors, with reductions principally in the Consumer Staples, Health Care and Telecommunication Services sectors. In accordance with our investment policy, which remains unchanged, these changes are driven by the merits of individual stocks and not an overarching top down view.

Over the course of the Company’s year the most significant developments across the world occurred in regions outside those in which we invest, such as the debt problems of the developed world,

the instability of the euro and the tragic earthquake and subsequent tsunami in Japan. Despite these external events, most Asian economies have enjoyed robust economic performance, with domestic demand remaining firm. During the second half of the period, inflationary concerns mounted and central banks responded by tightening monetary conditions through interest rate hikes and bank reserve requirement increases. These should be seen as sensible and proactive measures to prevent significant economic imbalances emerging and, in the absence of further exogenous shocks, should serve to make future growth all the more sustainable. Corporate governance has also been a topic of note, with first India and then China being the subject of investor scrutiny. Whilst such problems do come to the fore from time to time, we believe standards in the aggregate continue to improve with minority shareholders continuing to benefit as a result. Overall, we continue to consider that the markets in which we invest present an attractive prospect for shareholders in Pacific Horizon.

Over the past year we have continued to invest in companies with strong growth prospects and sustainable competitive advantages and which trade at low valuations relative to their prospects. We maintained a near fully invested position throughout the year and at the end of the year the cash balance was 1.1% of shareholders’ funds.

PACIFIC HORIZON INVESTMENT TRUST PLC 7

Investment Changes (£’000)

Valuation at 31 July 2010

Net acquisitions/(disposals)

Appreciation/(depreciation)

Valuation at 31 July 2011

Hong Kong and China 51,372 (4,020) 547 47,899Korea 18,567 3,931 6,355 28,853Taiwan 15,079 2,802 599 18,480Singapore 12,443 111 1,150 13,704Malaysia 5,981 (151) 1,039 6,869Indonesia 8,293 (3,028) 1,360 6,625India 7,586 (1,115) (534) 5,937Thailand 4,298 (364) 478 4,412Philippines 21 1,402 224 1,647Vietnam 1,505 – (46) 1,459

Total equities 125,145 (432) 11,172 135,885

Net liquid assets 2,794 (1,253) (76) 1,465

Total assets 127,939 (1,685) 11,096 137,350

The figures above for total assets are made up of total assets less current liabilities.

Distribution of Portfolio and Movement of Indices

% of total assets as at

31 July 2011

% of total assets as at

31 July 2010

Principal local indices % change

in sterling terms

Hong Kong and China 34.9 40.1 1.4Korea 21.0 14.5 29.8Taiwan 13.4 11.8 18.1Singapore 10.0 9.7 15.0Malaysia 5.0 4.7 16.4Indonesia 4.8 6.5 35.1India 4.3 5.9 2.0Thailand 3.2 3.4 36.7Philippines 1.2 0.0 35.5Vietnam 1.1 1.2 (23.6)Net liquid assets 1.1 2.2

Pacific Horizon Investment Trust (NAV) 100.0 100.0 9.2

MSCI All Country Far East ex Japan Index (in sterling terms) 13.8

Source: Thomson Reuters Datastream/Baillie Gifford & Co

Past performance is not a guide to future performance.

managErs’ oVErVIEw

8 ANNUAL REPORT 2011

Thirty Largest Equity Holdings at 31 July

Name Country Business

2011Value

£’000

2011 % of total assets *

Samsung Electronics Korea Semiconductor manufacturer 7,063 5.1Hyundai Mobis Korea Automotive parts producer 5,555 4.0Kunlun Energy Company HK/China Oil and gas exploration and production 4,718 3.4Taiwan Semiconductor Manufacturing Taiwan Semiconductor manufacturer 4,643 3.4Baidu HK/China Internet search provider 4,210 3.1CNOOC HK/China Oil and gas exploration and production 3,415 2.5Ping An Insurance HK/China Life insurance provider 3,324 2.4China Life Insurance (Taiwan) Taiwan Life insurance provider 3,199 2.3Hyundai Marine and Fire Insurance Korea Non-life insurance provider 2,967 2.2Singapore Exchange Singapore Stock exchange 2,805 2.0Hon Hai Precision Industries Taiwan Electronic manufacturing services company 2,699 2.0Hyundai Glovis Korea Logistics company 2,678 1.9Sembcorp Marine Singapore Shipbuilder 2,490 1.8ASM Pacific Technology HK/China Semiconductor equipment manufacturer 2,417 1.8Samsung Fire & Marine Korea Non-life insurance provider 2,398 1.7Kuala Lumpur Kepong Malaysia Palm oil producer and refiner 2,290 1.7Parkson Holdings Malaysia Department store owner and operator 2,250 1.6Li & Fung HK/China Supply chain management 2,189 1.6MediaTek Taiwan Integrated circuit design house 2,182 1.6LG Corporation Korea Holding company for the LG Group 2,072 1.5SATS Limited Singapore Airport services provider 2,023 1.5Ports Design HK/China Apparel retailer 1,874 1.4China Petroleum & Chemical Corporation HK/China Integrated oil and gas producer 1,784 1.3CapitaMall Trust Singapore Real estate investment trust 1,782 1.3Orion Korea Consumer conglomerate 1,745 1.3China National Building Material HK/China Building materials manufacturer 1,677 1.2ZTE HK/China Telecommunications equipment provider 1,668 1.2Security Bank Philippines Commercial bank 1,625 1.2Bank Negara Indonesia Indonesia Commercial bank 1,624 1.2PT Telekomunikasi Indonesia Diversified telecommunications provider 1,618 1.2

82,984 60.4

HK/China denotes Hong Kong and China.Details of the ten largest investments are given on pages 12 and 13 along with comparative valuations.*Total assets less current liabilities.

Net Liquid Assets 1.1% (2.2%)

Hong Kongand China34.9% (40.1%)

Philippines 1.2% (0.0%)

Thailand 3.2% (3.4%)

Indonesia 4.8% (6.5%)

Vietnam 1.1% (1.2%)

Taiwan13.4% (11.8%)

Singapore10.0% (9.7%)

Korea 21.0% (14.5%)

Malaysia5.0% (4.7%)

India 4.3% (5.9%)

Financials26.7% (24.8%)

Materials4.2% (3.6%)

Energy 9.7% (10.3%)

ConsumerDiscretionary12.7% (12.6%)

Net Liquid Assets 1.1% (2.2%)TelecommunicationServices 5.1% (5.9%)

Industrials12.8% (11.0%)

InformationTechnology23.4% (24.3%)

Consumer Staples 2.8% (2.9%)

Utilities 1.5% (1.5%)

Health Care Nil (0.9%)

Distribution of Portfolio

Geographical 2011 (2010)

dIsTrIbuTIon oF PorTFoLIo and THIrTy LargEsT EquITy HoLdIngs

Sectoral 2011 (2010)

PACIFIC HORIZON INVESTMENT TRUST PLC 9

CLassIFICaTIon oF InVEsTmEnTs

Classification of Investments

Classification

Hong Kongand China

%Korea

%Taiwan

%Singapore

%Malaysia

%

OtherCountries

%

2011Total

%

2010Total

%

Equities:Energy 8.3 – – – – 1.4 9.7 10.3

Energy 8.3 – – – – 1.4 9.7 10.3

Materials 3.3 – 0.9 – – – 4.2 3.6

Materials 3.3 – 0.9 – – – 4.2 3.6

Capital goods 2.2 4.5 – 1.8 – – 8.5 7.0 Transportation 0.9 1.9 – 1.5 – – 4.3 4.0

Industrials 3.1 6.4 – 3.3 – – 12.8 11.0

Automobiles and components 0.8 4.0 – – – 1.0 5.8 4.8 Consumer durables and apparel 2.2 – – – – – 2.2 1.0 Media 1.0 – – – – – 1.0 – Retailing 1.6 0.5 – – 1.6 – 3.7 6.8

Consumer Discretionary 5.6 4.5 – – 1.6 1.0 12.7 12.6

Food and staples retailing – 1.1 – – – – 1.1 1.3

Food beverage and tobacco – – – – 1.7 – 1.7 1.6

Consumer Staples – 1.1 – – 1.7 – 2.8 2.9

Health care equipment and services – – – – – – – 0.9

Health Care – – – – – – – 0.9

Banks – – – – 1.0 7.2 8.2 6.8 Diversified financials 1.4 – 1.0 2.0 – 2.3 6.7 7.3 Insurance 2.4 3.9 2.3 – – – 8.6 5.6

Real estate 0.8 – – 2.4 – – 3.2 5.1

Financials 4.6 3.9 3.3 4.4 1.0 9.5 26.7 24.8

Software and services 3.9 – – – – – 3.9 4.6 Technology hardware and equipment 2.2 – 3.2 1.2 – – 6.6 6.4 Semiconductors and semiconductor equipment 1.8 5.1 6.0 – – – 12.9 13.3

Information Technology 7.9 5.1 9.2 1.2 – – 23.4 24.3

Telecommunication services 2.1 – – 1.1 0.7 1.2 5.1 5.9

Telecommunication Services 2.1 – – 1.1 0.7 1.2 5.1 5.9

Utilities – – – – – 1.5 1.5 1.5

Utilities – – – – – 1.5 1.5 1.5

Total Equities 34.9 21.0 13.4 10.0 5.0 14.6 98.9

Total Equities – 2010 40.1 14.5 11.8 9.7 4.7 17.0 97.8 Net Liquid Assets 0.9 – 0.3 0.1 – (0.2) 1.1 2.2

Shareholders’ Funds 35.8 21.0 13.7 10.1 5.0 14.4 100.0

Shareholders’ Funds – 2010 42.1 14.5 12.0 9.8 4.7 16.9 100.0

Number of equity investments 28 12 9 8 4 18 79 81

Note:

The Classification of Investments has been based this year on the Global Industry Classification Standard (GICS) and the comparatives restated. The previous classification had been based on the FTSE Industry Classification Benchmark.

10 ANNUAL REPORT 2011

managErs’ PorTFoLIo rEVIEw

Managers’ Portfolio Review

Hong Kong and ChinaChina’s economic progress remains strong, with a proactive government looking to absorb excess liquidity and curb speculative exuberance. Inflationary concerns persist, although with monetary growth under control and trending lower we are relatively relaxed. Initial market focus was on the prospect of overheating, turning more recently to whether or not the tightening measures undertaken have been too aggressive. We believe that the government has exhibited sensible macroeconomic management to date, which should enable sustainable growth to be achieved. Indeed, unlike a number of countries around the world, China is firmly in control of her own destiny with enough financial firepower to counteract any slowdown should it be required.

Despite the undoubted potential of both the Chinese economy and her companies, stockmarket performance was lacklustre over the period. Aside from the short term worries surrounding economic performance, there have been questions raised over both the funding of Local Government Financing Vehicles and the standards of corporate governance at Chinese companies. On this latter point, Real Gold Mining, a holding taken earlier in the year, remains suspended following a press article questioning the accuracy of its accounts and we have written down its value accordingly. Despite this disappointment, our belief in the prospects for our Chinese holdings has never been stronger. We continue to invest in a wide range of companies sporting excellent growth prospects, sustainable competitive advantages and attractive financial characteristics. Valuations look reasonable, giving an opportunity to invest at a level that should deliver meaningful returns.

Over the period, Hong Kong (‘HK’) was the second worst performing market in which we invest. Given the large influence the mainland has over the stockmarket much of the relative weakness was due to short term worries about China’s economic performance. This aside, HK remains a premier beneficiary of continued Chinese growth, while also having a notable role to play in the further internationalisation of the Renminbi.

There were a number of new purchases made during the year in HK and China. These included Ping An Insurance, a leading financial business in China, Ports Design, a high end fashion retailer expanding in the mainland, VTech, a niche electronics manufacturer based in HK and Angang Steel, a leading Chinese steel producer. Few themes can be identified amongst the sales, although concern over the situation in HK has contributed in part to sales of Hang Seng Bank, a leading HK bank, and New World Development, a HK property company.

KoreaKorea performed well over the period, with sterling returns of almost 30%. Relations with North Korea appear stable for now after a potentially difficult time following the shelling of a South Korean island by the North. Regional tensions are an area of concern, although one that international pressures should be able to keep in check. We made substantial additions to the Korean holdings over the course of the year. Additions to Hyundai Mobis, an auto parts company, have made it into one of the largest holdings and more recently we have also purchased a holding in Hyundai Glovis, a logistic business. Both companies are part of the Hyundai Motor Group and are key beneficiaries of the Hyundai and Kia marques’ success. Other new buys included LG Corp, the holding company for the LG Group, and LS Corp, where we believe the growth potential from transmission network upgrades is being underpriced by the market. Sales of Mirae Asset Securities, a domestic stockbroker, Hyundai Development, a property company, and SK Telecom, a mobile phone operator, partially funded the new buys.

PACIFIC HORIZON INVESTMENT TRUST PLC 11

TaiwanTaiwan posted a good performance in both local and sterling currency terms. We remain upbeat regarding the prospects of closer ties with the mainland, with a number of our holdings such as China Life Insurance (Taiwan) set to be potential beneficiaries. Changes to the Taiwanese holdings over the year have been limited. We have made a recent new purchase of China Steel, the leading Taiwanese steel manufacturer, and a complete sale of Vanguard International Semiconductor, a niche semiconductor manufacturer. We have also been adding to MediaTek, an integrated circuit design house, where we feel that short term concerns are offering an attractive entry point.

SingaporeThe performance of Singapore has been good, albeit improved by a significant boost in sterling terms by the strength of its currency. Despite being one of the most open economies in which the Company invests, in times of uncertainty the Singaporean Dollar remains a safe haven currency. Limited changes have been made to the Singapore holdings with only one new purchase and one sale. Venture Corp, a niche electronic manufacturing services business, has been added given the potential for the business to improve margins as its product mix changes and KS Energy, an offshore services business, has been sold as a result of concerns over the future financing of the business.

MalaysiaDespite traditionally being one of the more defensive markets, Malaysia has posted a good performance in both local and sterling currency terms over the year. Economic performance continues to be good and the Economic Transformation Programme, a key initiative to deliver sustained growth and raise the standards of living, is progressing well. We made some small reductions to existing holdings to fund more exciting ideas elsewhere and took a new holding in CIMB, a leading Malaysian bank.

IndonesiaBenefiting from strong growth and a largely stable political environment, Indonesia has been one of the strongest performers over the Company’s year, both in local and sterling currency terms. However, inflationary pressures persist and with the Central Bank perhaps somewhat slow to react there is a risk that from here a more difficult environment will evolve. We would raise a flag of caution regarding the political environment, with some developments in the background perhaps being the first straws in the wind that the elections in 2014 may not be as smooth as the market expects. Given the strong performance and almost universal belief that Indonesia has finally put its problems behind it, we have used our Indonesian holdings as a source of funds, reducing our banking holdings and selling Bakrie and Brothers, an Indonesian conglomerate.

IndiaStockmarket returns in India were disappointing over the year as the country struggled in the face of rapid inflation, a rising oil price and corporate scandals. Reform remains a much needed step; however, despite the positive election result noted in this report last year, progress has been slow. Significant changes to the portfolio over the Company’s year included a new purchase of GAIL (India), a gas utility business, and sales of Patni Computer Systems, an IT services business, and Jain Irrigation, an industrial company with a focus on micro-irrigation units.

ThailandThailand was the best performing equity market in sterling terms over the period. With strong economic performance delivered and with political unrest in check for the time being, investors have returned to what had become a very lowly rated market. The landslide win in July for the opposition PT party was taken very well with markets performing strongly towards the Company’s year end. We made a new purchase of Bangkok Bank, a leading Thai bank, on expectations that in a better macroeconomic environment corporate spending may increase following years of underinvestment. We sold holdings in Esso Thailand, a refiner, and Thoresen Thai, a shipping company, as better investment opportunities have arisen.

PhilippinesLike many other ASEAN markets, the Philippines was a strong performer in both local and sterling currency terms. Economic growth was strong with inflation under control and remittances continuing to flow in. Following the peaceful election last year, reforms have been slow to materialise. We made one new purchase during the year; Security Bank, a well run bank with strong growth prospects and an attractive valuation.

VietnamVietnam was the weakest performing market over the financial year, posting a significant decline in local and sterling currency terms. Inflationary pressures remain fierce and the Central Bank has little latitude to intervene. The currency has been under pressure with further devaluations and concerns regarding the debt levels, balance of payments and credit quality. We remain optimistic regarding the long term outlook for the economy given the attractive structural features such as the demographic profile and geographic proximity to China, and valuations remain low. We retain two pooled holdings there.

managErs’ PorTFoLIo rEVIEw

12 ANNUAL REPORT 2011

rEVIEw oF InVEsTmEnTs

Review of InvestmentsA review of the Company’s ten largest investments as at 31 July 2011 is given below and on the following page.

Samsung ElectronicsSamsung Electronics is one of the leading electronics companies in the world. Its principal products include memory chips for computers, LCD panels for computer monitors and TVs and mobile phones. We are firm believers in the value of the Samsung brand and the benefits that scale delivers in this industry. With a strong balance sheet and stable management team the company should be able to continue to generate returns well in excess of its cost of capital for many years to come.

Country KoreaValuation £7,063,000% of total assets 5.1%(Valuation at 31 July 2010 £6,339,000)

Hyundai MobisHyundai Mobis is a leading auto parts and module supplier to Hyundai Motor and Kia, and is also starting to win contracts from other auto companies. It is a direct beneficiary of the continued success of the Hyundai and Kia marques and in addition is a key asset within the Hyundai Motor Group and therefore likely to be treated favourably as and when the group restructures. In the meantime the business should continue to generate decent returns on capital and strong cash flow.

Country KoreaValuation £5,555,000% of total assets 4.0%(Valuation at 31 July 2010 £2,373,000)

Kunlun Energy Company Kunlun Energy Company has two main divisions: the oil and gas E&P assets and the increasingly important natural gas business. The immature downstream gas market in China remains an attractive industry in which to operate, especially for Kunlun Energy given the strong relationship with CNPC, one of China’s leading state controlled oil and gas companies. In addition, we believe that through continued gas asset injections from the parent company the company will continue to deliver strong growth whilst being able to deploy capital at favourable rates of return.

Country Hong Kong and ChinaValuation £4,718,000% of total assets 3.4%(Valuation at 31 July 2010 £3,850,000)

Taiwan Semiconductor Manufacturing (‘TSMC’)TSMC is the largest foundry company in the world, manufacturing semiconductor chips for some of the world’s largest design companies. The company is benefiting from competitive advantages derived from technology leadership, scale and efficiency which enable it to lower costs faster than its competitors. TSMC operates in a cyclical industry, though its business model and the continued outsourcing of semiconductor manufacturing should enable the company to achieve good returns and growth through the cycle.

Country TaiwanValuation £4,643,000% of total assets 3.4%(Valuation at 31 July 2010 £3,788,000)

BaiduBaidu is the leading internet search platform in China. It benefits from a rapidly expanding internet community and customer base that are likely to exhibit strong growth for many years to come. The company is the clear leader in its market, with attractive financial characteristics and the ability to reinvest capital at very high incremental rates of return.

Country Hong Kong and ChinaValuation £4,210,000% of total assets 3.1%(Valuation at 31 July 2010 £2,287,000)

CNOOCChina National Offshore Oil Corporation (CNOOC) engages in the exploration, development and production of crude oil and natural gas in offshore regions in China and overseas. The group boasts a strengthening reserve and production profile in both oil and gas after a number of successful new finds and has a privileged position in offshore China, a largely underexplored region. Further overseas acquisitions could also provide meaningful upside.

Country Hong Kong and ChinaValuation £3,415,000% of total assets 2.5%(Valuation at 31 July 2010 £2,696,000)

PACIFIC HORIZON INVESTMENT TRUST PLC 13

Ping An InsurancePing An Insurance is one of the leading life insurance companies in China and also has growing banking, general insurance and asset management arms. The insurance market in China should be a beneficiary of a number of attractive themes such as increasing wealth, increasing levels of sophistication and the aging society. We believe the company is ideally placed to deliver on this opportunity with a strong market position, well incentivised employees, an entrepreneurial management team and a strong financial position.

Country Hong Kong and ChinaValuation £3,324,000% of total assets 2.4%(Valuation at 31 July 2010 £Nil)

China Life Insurance (Taiwan)China Life Insurance (Taiwan) is a dynamic insurance company operating in a largely mature and stable industry. The key attraction is the professional management team, who have been behind the success of the company since their appointment in 2003. The recent tie up with China Construction Bank could also prove to be a very shrewd deal.

Country TaiwanValuation £3,199,000% of total assets 2.3%(Valuation at 31 July 2010 £1,651,000)

Hyundai Marine and Fire InsuranceHyundai Marine and Fire Insurance is a leading non-life insurer in South Korea, with a mid-teens share of premiums written. The company benefits from a privileged position as insurer of choice for the Hyundai companies leading to very high levels of profitability as well as a lowly valued quasi-life insurance book.

Country KoreaValuation £2,967,000% of total assets 2.2%(Valuation at 31 July 2010 £1,992,000)

Singapore ExchangeSingapore Exchange is Singapore’s listed stock exchange. Continued liquidity flows into Asia and the significant increase in the number of companies looking to list provides a strong operating background. It is highly leveraged to this given its fixed cost base and should continue to benefit from the structural drivers of investment into Asia. The company is also likely to play a role in the future consolidation of the sector.

Country SingaporeValuation £2,805,000% of total assets 2.0%(Valuation at 31 July 2010 £3,033,000)

rEVIEw oF InVEsTmEnTs

14 ANNUAL REPORT 2011

Name BusinessValue

£’000% of total

assets

Hong Kong and China

Alibaba.com B2B e-commerce 1,074Angang Steel Steel maker 1,320ASM Pacific Technology Semiconductor equipment manufacturer 2,417Baidu Internet search provider 4,210Bosideng International Holdings Apparel retailer 1,146China Mobile Wireless telecommunications provider 1,546China National Building Material Building materials manufacturer 1,677China Petroleum & Chemical Corporation Integrated oil and gas producer 1,784China Railway Construction Construction company 989China Shenhua Energy Coal producer 1,469China Unicom Diversified telecommunications provider 1,383CNOOC Oil and gas exploration and production 3,415Dongfang Electric Power equipment manufacturer 1,471Focus Media Out of home media company 1,364Geely Automobile Automobile manufacturer 1,105Great Eagle Property investment company 1,072Hong Kong Exchanges and Clearing Stock exchange 1,562Kunlun Energy Company Oil and gas exploration and production 4,718Li & Fung Supply chain management 2,189Pacific Basin Shipping Shipping company 1,184Ping An Insurance Life insurance provider 3,324Ports Design Apparel retailer 1,874Real Gold Mining Gold mining 312SouthGobi Resources Coal producer 1,257Sun Hung Kai & Company Brokerage 420VTech Holdings Electronic product manufacturer 1,413Xinjiang Goldwin Science & Technology Wind power generation equipment 536ZTE Telecommunications equipment provider 1,668

47,899 34.9

Korea

E-Mart Discount store chain 1,471Hyundai Engineering & Construction Construction company 789Hyundai Glovis Logistics company 2,678Hyundai Marine and Fire Insurance Non-life insurance provider 2,967Hyundai Mobis Automotive parts producer 5,555Hyunjin Materials Industrial machinery manufacturer 828LG Corporation Holding company for the LG Group 2,072LS Corporation Holding company for the LS Group 664Orion Consumer conglomerate 1,745Samsung Electronics Semiconductor manufacturer 7,063Samsung Fire & Marine Non-life insurance provider 2,398Shinsegae General retailer 623

28,853 21.0

Taiwan

Asustek Computer Computer manufacturer 784China Life Insurance (Taiwan) Life insurance provider 3,199China Steel Steel maker 1,265Hon Hai Precision Industries Electronic manufacturing services company 2,699MediaTek Integrated circuit design house 2,182Phison Electronics Semiconductor products 1,397Taiwan Semiconductor Manufacturing Semiconductor manufacturer 4,643Wah Lee Industrial Corp Chemicals and materials distributor 908Yuanta Financial Financial holding company 1,403

18,480 13.4

LIsT oF InVEsTmEnTs

List of Investments as at 31 July 2011

PACIFIC HORIZON INVESTMENT TRUST PLC 15

Name BusinessValue

£’000% of total

assets

Singapore

Ascendas Real Estate Real estate investment trust 1,518CapitaMall Trust Real estate investment trust 1,782Elec and Eltek International Circuit board manufacturing 433M1 Wireless telecommunications provider 1,461SATS Limited Airport services provider 2,023Sembcorp Marine Shipbuilder 2,490Singapore Exchange Stock exchange 2,805Venture Corporation Electronic manufacturing services company 1,192

13,704 10.0

Malaysia

CIMB Group Commercial bank 1,411Digi.com Wireless telecommunications provider 918Kuala Lumpur Kepong Palm oil producer and refiner 2,290Parkson Holdings Department store owner and operator 2,250

6,869 5.0

Indonesia

Bank Negara Indonesia Commercial bank 1,624Bank Rakyat Indonesia Commercial bank 1,344Perusahaan Gas Negara Gas utility 887PT Bukit Asam Coal producer 1,152PT Telekomunikasi Diversified telecommunications provider 1,618

6,625 4.8

India

GAIL (India) Gas distributor 1,249Housing Development Finance Mortgage bank 1,577IFCI Non bank financial company 848Mahindra & Mahindra Indian conglomerate 1,415Reliance Capital Investment services 848

5,937 4.3

Thailand

Bangkok Bank Commercial bank 1,437Bank of Ayudhya Commercial bank 880Mermaid Maritime Oil equipment and services 763Siam Commercial Bank Commercial bank 1,332

4,412 3.2

Philippines

Philippine Townships* Property developer 22

Security Bank Commercial bank 1,625

1,647 1.2

Vietnam

Dragon Capital Management Vietnam Growth Fund Vietnam investment fund 1,053Vietnam Enterprise Investments Vietnam investment fund 406

1,459 1.1

Total Investments 135,885 98.9Net Current Assets 1,465 1.1Total Assets at Fair Value 137,350 100.0

*Denotes unlisted security.All investments are ordinary shares unless otherwise stated.

LIsT oF InVEsTmEnTs

16 ANNUAL REPORT 2011

TEn yEar rECord

Capital

At 31 July

Total assets * £’000

Bank loans

£’000

Shareholders’ funds

£’000

Net asset value

per sharep

Diluted net asset value per share † p

Shareprice

p

Premium/ (discount) # %

2001 37,713 – 37,713 47.83 47.83 38.50 (19.5)2002 38,729 – 38,729 50.63 – 45.50 (10.1)2003 40,801 – 40,801 53.34 – 48.25 (9.5)2004 47,305 – 47,305 61.84 – 56.75 (8.2)2005‡ 67,374 – 67,374 88.09 – 85.50 (2.9)2006 88,971 7,581 81,390 106.41 – 101.25 (4.8)2007 130,077 – 130,077 166.90 – 171.75 (2.9)2008 105,168 – 105,168 134.34 – 129.25 (3.8)2009 105,851 – 105,851 135.21 – 124.75 (7.7)2010 127,939 – 127,939 163.42 – 146.00 (10.7)2011 137,350 – 137,350 178.53 – 165.00 (7.6)

* Total assets comprise total assets less current liabilities and deferred tax, before deduction of bank loans.† The diluted net asset value per ordinary share figures have been calculated in accordance with FRS14 ‘Earnings per share’. 1 July 2002 was the final date for the

exercise of warrants, any remaining after that date lapsed and were delisted.# Premium/(discount) is the difference between Pacific Horizon’s quoted share price and its underlying net asset value expressed as a percentage of net asset value.‡ The figures prior to 2005 have not been restated for changes in accounting policies implemented in 2006.

Cumulative Performance (taking 2001 as 100)

At 31 July

Net assetvalue

per share

Net asset value total return ††

Share price ††

Share price total return ††

Comparative Index ̂ ^ (in sterling terms) ††

Comparative Index ̂ ^ (in sterling terms) total return ††

Revenueearnings per

ordinary share

Retail price index ††

2001 100 100 100 100 100 100 100 1002002 106 107 118 120 98 100 103 1022003 112 114 125 129 99 104 105 1052004 129 134 147 153 99 107 161 1082005 184 191 222 233 137 152 230 1112006 222 233 263 280 146 167 236 1142007 349 372 446 479 202 238 227 1192008 281 299 336 362 176 214 298 1242009 283 304 324 355 191 239 381 1232010 342 374 379 421 224 287 258 1292011 373 411 429 480 255 336 309 135

Compound annual returns5 year 10.9% 12.0% 10.3% 11.4% 11.8% 14.9% 5.6% 3.4%10 year 14.1% 15.2% 15.7% 17.0% 9.8% 12.9% 12.0% 3.1%

†† Source: Thomson Reuters Datastream.^^ MSCI All Country Far East ex Japan Index.

Past performance is not a guide to future performance.

Revenue

Year to31 July

Grossrevenue

£’000

Availablefor ordinary

shareholders£’000

Revenue earnings per ordinary share ¶ p

Dividend perordinary share

netp

Total expense ratio § p

Actual gearing ̂

Potential gearing **

2001 1,378 507 0.64 0.45 1.47 98 1002002 1,442 504 0.66 0.45 1.57 98 1002003 1,263 514 0.67 0.45 1.49 98 1002004 1,858 786 1.03 0.70 1.42 99 1002005 2,384 1,123 1.47 1.10 1.32 99 1002006 2,887 1,160 1.51 1.10 1.32 106 1092007 3,031 1,124 1.45 1.10 1.26 99 1002008 3,602 1,491 1.91 1.30 1.21 95 1002009 3,579 1,915 2.44 1.80 1.31 98 1002010 2,999 1,295 1.65 1.30 1.24 98 1002011 3,441 1,546 1.98 1.50 1.22 99 100

¶ The calculation of earnings per share is based on the net revenue from ordinary activities after taxation and the weighted average number of ordinary shares (see note 7, page 35). There was no dilution of earnings per share in any of the years 2001 to 2011.

§ Ratio of total operating costs (excluding any tax relief) against average shareholders’ funds.^ Total assets (including all debt used for investment purposes) less all cash and fixed interest securities (ex convertibles) divided by shareholders’ funds.** Total assets (including all debt used for investment purposes) divided by shareholders’ funds.

Gearing Ratios

PACIFIC HORIZON INVESTMENT TRUST PLC 17

Directors and Managers

DirectorsJean Matterson Jean Matterson was appointed a Director in 2003 and became Chairman of the Board on 25 October 2010 she is also Chairman of the Nomination Committee. She is a partner of Rossie House Investment Management which specialises in private client portfolio management with a particular emphasis on investment trusts. She was previously with Stewart Ivory & Co for 20 years, as an investment manager and a director.

Edward CreasyEdward Creasy was appointed a Director in 2010. He is Chairman of the Audit Committee and is the Senior Independent Director. He is the former chief executive officer of Kiln plc, a non-life insurer quoted on the London Stock Exchange until purchased by Tokio Marine Nichido Fire Insurance Co in March 2008. Until January 2011 he was chairman of Kiln Group and chairman of RJ Kiln & Co. Limited (an FSA registered Lloyd’s insurer). He is a director of W.R. Berkley Insurance (Europe), Ltd (an FSA registered UK insurance company), Capita Commercial Insurance Services Limited and chairman of Notcutts Limited.

Douglas McDougall OBE Douglas McDougall was appointed a Director in 1992. He is chairman of The Scottish Investment Trust plc, The Law Debenture Corporation plc, The Independent Investment Trust PLC and The European Investment Trust plc. He is a director of The Monks Investment Trust PLC, Herald Investment Trust plc and Stramongate Assets PLC and is a member of the University of Cambridge Investment Board. From 1969 to 1999 he was a partner in Baillie Gifford & Co and from 1989 to 1999 was joint senior partner and chief investment officer. He is a former chairman of the Investment Management Regulatory Organisation, the Fund Managers’ Association and the Association of Investment Companies.

Elisabeth Scott Elisabeth Scott was appointed a Director on 10 March 2011. She was managing director and country head of Schroder Investment Management (Hong Kong) Limited from 2005 to 2008 and chair of the Hong Kong Investment Funds Association from 2005 to 2007. She worked in the Hong Kong asset management industry from 1992 to 2008.

Gerald SmithGerald Smith was appointed a Director in 2009. He is a partner of Baillie Gifford & Co, Chief Investment Officer and a member of the Investment Advisory Group. He is also the head of Baillie Gifford’s Global Opportunities Team, and was the manager of Pacific Horizon from 1995 to January 2009.

All Directors, with the exception of Mr Gerald Smith, are members of the Audit Committee. All Directors are members of the Nomination Committee.

Managers and Secretaries Pacific Horizon is managed by Baillie Gifford & Co, an investment management firm formed in 1927 out of the legal firm Baillie & Gifford, WS, which had been involved in investment management since 1908.

Baillie Gifford is one of the largest investment trust managers in the UK and currently manages eight investment trusts. Baillie Gifford also manages unit trusts and Open Ended Investment Companies, together with investment portfolios on behalf of pension funds, charities and other institutional clients, both in the UK and overseas. Funds under the management or advice of Baillie Gifford totalled over £75 billion at 31 July 2011. Based in Edinburgh, it is one of the leading privately owned investment management firms in the UK, with 36 partners and a staff of around 670.

The manager of Pacific Horizon’s portfolio is Mike Gush. Mike has been a member of the Emerging Markets Team at Baillie Gifford since 2005.

Baillie Gifford have been Managers and Secretaries to the Company since August 1992.

The firm of Baillie Gifford & Co is authorised and regulated by the Financial Services Authority.

dIrECTors and managErs

18 ANNUAL REPORT 2011

dIrECTors’ rEPorT

Directors’ Report

The Directors present their Report together with the financial statements of the Company for the year to 31 July 2011.

Business ReviewBusiness and Status The Company is an investment company within the meaning of Section 833 of the Companies Act 2006.

The Company carries on business as an investment trust. In the opinion of the Directors, the Company conducts its affairs so as to enable it to obtain approval by HM Revenue & Customs as an investment trust under Section 1158 of the Corporation Tax Act 2010. The Company was approved as an investment trust for the year ended 31 July 2010, subject to matters that may arise from any subsequent enquiry by HM Revenue & Customs into the Company’s tax return. The Company will continue to seek approval under Section 1158 of the Corporation Tax Act 2010 each year.

Objective The Company’s objective is to invest in the stockmarkets of the Asia-Pacific region (excluding Japan) and in the stockmarkets of the Indian Sub-continent in order to achieve capital growth. The Company is prepared to move freely between the markets of the region as opportunities for growth vary. The portfolio will normally consist entirely of quoted securities.

Investment PolicyPacific Horizon aims to achieve capital growth principally through investment in companies listed on the stockmarkets of the Asia-Pacific region (excluding Japan) and the Indian Sub-continent. The Company may also invest in companies based in the region and in investment funds specialising in the region or particular countries or sectors within it even if they are listed elsewhere. The maximum permitted investment in such companies is 15% of gross assets.

The portfolio contains companies which the Managers have identified as offering the potential for long term capital appreciation, irrespective of whether they comprise part of any index. The portfolio is actively managed and will normally consist entirely of quoted equity securities although unlisted companies, fixed interest holdings, or other non equity investments, may be held. The Company is also permitted to invest in other pooled vehicles (general, country and sector specific) that invest in the markets of the region.

In constructing the equity portfolio a spread of risk is achieved by diversification and the portfolio will typically consist of between 40 and 120 holdings. Although sector concentration and the thematic characteristics of the portfolio are carefully monitored, no maximum limits to stock or sector weights have been set by the Board except as imposed from time to time by banking covenants on borrowings.

The Company may use derivatives which will be principally, but not exclusively, for the purpose of reducing, transferring or eliminating investment risk in its investments. These typically take the form of index futures, index options and currency forward transactions.

The Company recognises the long term advantages of gearing and has a maximum equity gearing level of 50% of shareholders’ funds but, in the absence of exceptional market conditions, equity gearing is typically less than 25% of shareholders’ funds and in the year to 31 July 2011 was nil (2010 – nil). Borrowings are invested in securities when it is considered that investment grounds merit the Company taking a geared position.

The Company is also permitted to be less than fully invested. Cash and equity gearing levels, and the extent of gearing, are discussed by the Board and Managers at every Board meeting.

Details of investment strategy and activity this year can be found in the Chairman’s Statement on pages 4 and 5 and the Managers’ Overview and Portfolio Review on pages 6, 10 and 11 respectively. A detailed analysis of the Company’s Investment Portfolio is set out on pages 14 and 15.

Performance At each Board meeting, the Directors consider a number of performance measures to assess the Company’s success in achieving its objectives.

The key performance indicators (KPIs) used to measure the progress and performance of the Company over time are established industry measures and are as follows:

• themovementinnetassetvalueperordinaryshare;

• themovementintheshareprice;

• thepremium/(discount);

• themovementinthecomparativeindex(MSCIAllCountryFarEast ex Japan Index (in sterling terms)); and

• thetotalexpenseratio.

PACIFIC HORIZON INVESTMENT TRUST PLC 19

dIrECTors’ rEPorT

The one, five and ten year records for the KPIs can be found on pages 2, 3 and 16 respectively.

Results and DividendsThe net asset value per share increased by 9.2% during the year, compared to an increase in the benchmark of 13.8%; at 31 July 2011 the discount was 7.6%.

The Board recommends a final dividend of 1.50p per ordinary share.

If approved, the recommended final dividend on the ordinary shares will be paid on 24 October 2011 to shareholders on the register at the close of business on 7 October 2011. The ex-dividend date is 5 October 2011. The Company’s Registrar offers a Dividend Reinvestment Plan (see page 45) and the final date for election for this dividend is 12 October 2011.

Review of the Year and Future TrendsA review of the main features of the year and the investment outlook is contained in the Chairman’s Statement on pages 4 and 5 and the Managers’ Overview and Portfolio Review on pages 6, 10 and 11 respectively.

Principal Risks and UncertaintiesThe Company’s assets consist mainly of listed securities and its principal financial risks are therefore market related and include market risk (comprising currency risk, interest rate risk and other price risk), liquidity risk and credit risk. An explanation of those risks and how they are managed is contained in note 17 to the financial statements on pages 38 to 41.

Other risks faced by the Company include the following:

Regulatory Risk – failure to comply with applicable legal and regulatory requirements could lead to suspension of the Company’s Stock Exchange Listing, financial penalties or a qualified audit report. Breach of Section 1159 of the Corporation Tax Act 2010 could lead to the Company being subject to tax on capital gains.

The Managers monitor investment movements and the level of forecast income and expenditure to ensure the provisions of Section 1159 are not breached. Baillie Gifford’s Heads of Business Risk & Internal Audit and Regulatory Risk provide regular reports to the Audit Committee on Baillie Gifford’s monitoring programmes.

Major regulatory change could impose unnecessary compliance burdens on the Company or threaten the viability of the investment company structure. In such circumstances representation is made to ensure that the special circumstances of investment trusts are recognised.

Operational/Financial Risk – failure of the Managers’ accounting systems or those of other third party service providers could lead to an inability to provide accurate reporting and monitoring or a misappropriation of assets. The Managers have a comprehensive business continuity plan which facilitates continued operations of the business in the event of a service disruption or major disaster. The Board reviews the Managers’ Report on Internal Controls and the reports by other key third party providers are reviewed by the Managers on behalf of the Board.

Discount Volatility – the discount at which the Company’s shares trade can widen. The Board monitors the level of discount and the Company has authority to buy back its own shares.

EmployeesThe Company has no employees.

Social and Community IssuesAs an investment trust, the Company has no direct social or community responsibilities. The Company, however, believes that it is in the shareholders’ interests to consider environmental, social and governance factors when selecting and retaining investments. Details of the Company’s policy on socially responsible investment can be found under Corporate Governance and Stewardship on page 22.

Corporate GovernanceThe Board is committed to achieving and demonstrating high standards of Corporate Governance. This statement outlines how the principles of the June 2010 UK Corporate Governance Code (the ‘Code’) and the principles of the Association of Investment Companies (AIC) Code of Corporate Governance were applied throughout the financial year. The AIC Code provides a framework of best practice for investment companies.

ComplianceThe Board confirms that the Company has complied throughout the year under review with the relevant provisions of the Code and the recommendations of the AIC Code.

The BoardThe Board has overall responsibility for the Company’s affairs. It has a number of matters formally reserved for its approval including strategy, investment policy, currency hedging, gearing, treasury matters, dividend and corporate governance policy. The Board also reviews the financial statements, investment transactions, revenue budgets and performance. Full and timely information is provided to the Board to enable the Board to function effectively and to allow Directors to discharge their responsibilities.

Following the appointment of Ms EC Scott to the Board and the retiral of Mr P Mackay and Mr MJ Morrison, the Board comprises five Directors all of whom are non-executive. Following Mr P MacKay’s retirement on 25 October 2010, Miss Matterson became Chairman of the Company and she stood down as Chairman of the Audit Committee and Mr Creasy assumed that role.

The executive responsibility for investment management has been delegated to the Company’s Managers and Secretaries, Baillie Gifford & Co, and, in the context of a Board comprising only non-executive Directors, there is no chief executive officer. Mr EG Creasy is the Senior Independent Director.

The Directors believe that the Board has a balance of skills and experience that enable it to provide effective strategic leadership and proper governance of the Company. Information about the Directors, including their relevant experience, can be found on page 17.

There is an agreed procedure for Directors to seek independent professional advice if necessary at the Company’s expense.

Terms of AppointmentThe terms and conditions of Directors’ appointments are set out in formal letters of appointment which are available for inspection on request.

Under the provisions of the Company’s Articles of Association, a Director appointed during the year is required to retire and seek election by shareholders at the next Annual General Meeting. Directors are required to submit themselves for re-election at least once every three years. Directors who have served for more than

20 ANNUAL REPORT 2011

dIrECTors’ rEPorT

nine years or who are directors of another investment trust managed by Baillie Gifford also offer themselves for re-election annually.

The names of Directors retiring and offering themselves for re-election together with the reasons why the Board supports the re-elections are set out on page 23.

Independence of DirectorsWith the exception of Mr GTE Smith, who is a partner of Baillie Gifford & Co, the Directors are considered by the Board to be independent of the Managers and free of any business or other relationship that could interfere with the exercise of their independent judgement.

Mr Smith will not be offering himself for re-election at the Annual General Meeting.

The Directors recognise the importance of succession planning for company boards and review the Board composition annually. The Board is of the view that length of service will not necessarily compromise the independence or contribution of Directors of an investment trust company, where continuity and experience can be a benefit to the Board. The Board concurs with the view expressed in the AIC Code that long serving Directors should not be prevented from bei`ng considered independent.

Mr DCP McDougall was a senior partner of Baillie Gifford & Co until he retired on 30 April 1999. As he has served on the Board for more than nine years and is a director of The Monks Investment Trust PLC, which is also managed by Baillie Gifford & Co, he offers himself for re-election annually. Following a formal performance evaluation, the Board has concluded that Mr DCP McDougall continues to be independent in character and judgement and his skills and extensive financial services experience add significantly to the strength of the Board.

MeetingsThere is an annual cycle of Board meetings which is designed to address, in a systematic way, overall strategy, review of investment policy, investment performance, marketing, revenue budgets, dividend policy and communication with shareholders. The Board considers that it meets sufficiently regularly to discharge its duties effectively. The table below shows the attendance record for the Board, the Audit Committee and the Nomination Committee Meetings held during the year. The Annual General Meeting was attended by all Directors serving at that date.

Directors’ Attendance at Meetings

BoardAudit

CommitteeNominationCommittee

Number of meetings 7 2 2

JGK Matterson 7 2 2P Mackay (retired 25 October 2010) 2 1 –

EG Creasy 7 2 2

DCP McDougall 7 2 2MJ Morrison (retired 10 March 2011) 4 2 1EC Scott (appointed 10 March 2011) 4 – 1GTE Smith 7 n/a 2

Mr GTE Smith is not a member of the Audit Committee.

Nomination CommitteeThe Nomination Committee consists of all the non-executive Directors and the Chairman of the Board is Chairman of the Committee. The Committee meets at least annually and at such other times as may be required. The Committee has written terms of reference that include reviewing the Board, identifying and nominating new candidates for appointment to the Board, Board appraisal, succession planning and training. The Committee also considers whether Directors should be recommended for re-election by shareholders. The Committee is responsible for considering Directors’ potential conflicts of interest and for making recommendations to the Board on whether or not potential conflicts should be authorised. The Committee’s terms of reference are available on request from the Company and are on the Company’s website: www.pacifichorizon.co.uk.

The Nomination Committee reviewed the Directors’ balance of age, skills, knowledge and experience during the year. The Committee concluded that, in line with the policy for regular refreshment of the Board, a new Director should be appointed. The Committee identified the skills and experience that would strengthen the Board and prepared a description of the role and capabilities required, following which a list of high quality candidates was prepared. Ms EC Scott was identified as the preferred candidate and, following an interview by the Board, she was appointed a Director on 10 March 2011. Mr Smith, not being an independent Director, did not vote on Ms Scott’s appointment. Information on Ms Scott’s background and experience can be found on page 17.

Given the quality of the candidates identified, it was not necessary to either appoint external search consultants or use open advertising on this occasion.

Performance EvaluationAn appraisal of the Chairman, each Director and a performance evaluation and review of the Board as a whole and of the Committees was carried out during the year. After inviting each Director and the Chairman to consider and respond to a set of questions; the performance of each Director was appraised by the Chairman and the Chairman’s appraisal was led by Mr EG Creasy.

The appraisals and evaluations considered, amongst other criteria, the balance of skills of the Board, the contribution of individual Directors and the overall effectiveness of the Board and the Committees. Following this process it was concluded that the performance of each Director, the Chairman, the Board and the Committees continues to be effective and each Director and the Chairman remain committed to the Company.

A review of the Chairman’s and other Directors’ commitments was carried out and the Board is satisfied that they are capable of devoting sufficient time to the Company. There were no significant changes to the Chairman’s other commitments during the year.

Induction and TrainingNew Directors are provided with an induction programme which is tailored to the particular circumstances of the appointee. Regular briefings are provided on changes in regulatory requirements that could affect the Company and Directors. Directors receive other relevant training as necessary.

RemunerationAs all the Directors are non-executive there is no requirement for a separate Remuneration Committee. Directors’ fees are considered

PACIFIC HORIZON INVESTMENT TRUST PLC 21

dIrECTors’ rEPorT

Internal AuditThe Audit Committee carries out an annual review of the need for an internal audit function. The Audit Committee continues to believe that the compliance and internal control systems and the internal audit function in place within the Investment Managers provide sufficient assurance that a sound system of internal control, which safeguards shareholders’ investment and the Company’s assets, is maintained. An internal audit function, specific to the Company, is therefore considered unnecessary.

Accountability and AuditThe respective responsibilities of the Directors and the Auditor in connection with the Financial Statements are set out on pages 27 and 28.

Going ConcernIn accordance with The Financial Reporting Council’s guidance on going concern and liquidity risk issued in 2009 the Directors have undertaken a rigorous review of the Company’s ability to continue as a going concern.

The Company’s assets, the majority of which are investments in quoted securities which are readily realisable, exceed its liabilities significantly. The Company has no loans. In accordance with the Company’s Articles of Association, shareholders have the right to vote on the continuation of the Company every five years, the next vote being on 17 October 2011. The Directors have no reason to believe that the continuation resolution will not be passed this year. After making enquiries and considering the future prospects of the Company and notwithstanding the above, the financial statements have been prepared on the going concern basis as it is the Directors’ opinion that the Company will continue in operational existence for the foreseeable future.

If the continuation resolution is not passed, the Articles provide that the Directors shall convene an Extraordinary General Meeting at which a resolution will be proposed to wind up the Company voluntarily. If the Company is wound up its investments may not be realised at their full market value.

Audit CommitteeAn Audit Committee has been established consisting of all the independent Directors. The members of the Audit Committee consider that they have the requisite financial skills and experience to fulfil the responsibilities of the Committee. Mr EG Creasy is Chairman of the Audit Committee. The Committee’s authority and duties are clearly defined within its written terms of reference which are available on request from the Company and are on the Company’s page of the Managers’ website: www.pacifichorizon.co.uk.

The Committee’s responsibilities which were discharged during the year include:

• monitoringtheintegrityofthehalf-yearlyandannualfinancialstatements and any formal announcements relating to the Company’s financial performance;

• reviewingtheadequacyandeffectivenessofinternalcontrolandrisk management systems;

• makingrecommendationstotheBoardinrelationtotheappointment of the external auditor and approving the remuneration and terms of their engagement;

by the Board as a whole within the limits approved by shareholders. The Company’s policy on remuneration is set out in the Directors’ Remuneration Report on pages 25 and 26.

Internal Controls and Risk ManagementThe Directors acknowledge their responsibility for the Company’s system of internal controls and for reviewing its effectiveness. The system of internal controls is designed to manage rather than eliminate risk and can only provide reasonable but not absolute assurance against material misstatement or loss.

The Board confirms that there is a process for identifying, evaluating and managing the significant risks faced by the Company in accordance with the guidance ‘Internal Control: Revised Guidance for Directors on the Combined Code’.

The Directors confirm that they have reviewed the effectiveness of the system and they have procedures in place to review its effectiveness on a regular basis. No significant weaknesses were identified in the year under review.

The practical measures to ensure compliance with regulation and company law, and to provide effective and efficient operations and investment management, have been delegated to the Managers and Secretaries, Baillie Gifford & Co, under the terms of the Management Agreement.

The practical measures in relation to the design, implementation and maintenance of control policies and procedures to safeguard the assets of the Company and to manage its affairs properly, including the maintenance of effective operational and compliance controls and risk management, have also been delegated to Baillie Gifford & Co. The Board acknowledges its responsibilities to supervise and control the discharge by the Managers and Secretaries of their obligations.

The Baillie Gifford & Co Heads of Business Risk & Internal Audit and Regulatory Risk provide the Board with regular reports on Baillie Gifford & Co’s monitoring programmes. The reporting procedures for these departments are defined and formalised within a service level agreement. Baillie Gifford & Co conducts an annual review of its system of internal controls which is documented within an internal controls report which has been designed to comply with Technical Release AAF 01/06 – Assurance Reports on Internal Controls of Service Organisations made available to Third Parties. This report is independently reviewed by Baillie Gifford & Co’s auditors and a copy is submitted to the Audit Committee.

The Company’s investments are segregated from those of Baillie Gifford & Co and its other clients through the appointment of The Bank of New York Mellon as independent custodian of the Company’s investments.

A detailed risk map is prepared which identifies the significant risks faced by the Company and the key controls employed to manage these risks.

These procedures ensure that consideration is given regularly to the nature and extent of the risks facing the Company and that they are being actively monitored. Where changes in risk have been identified during the year they also provide a mechanism to assess whether further action is required to manage the risks identified. The Board confirms that these procedures have been in place throughout the Company’s financial year and continue to be in place up to the date of approval of this Report.

22 ANNUAL REPORT 2011

dIrECTors’ rEPorT

• developingandimplementingpolicyontheengagementof the external auditor to supply non-audit services (there were no non-audit services during the year);

• reviewingandmonitoringtheindependence,objectivityandeffectiveness of the external auditor;

• reviewingthearrangementsinplacewithinBaillieGifford&Cowhereby their staff may, in confidence, raise concerns about possible improprieties in matters of financial reporting or other matters insofar as they may affect the Company;

• reviewingannuallythetermsoftheInvestmentManagementAgreement; and

• consideringannuallywhetherthereisaneedfortheCompany to have its own internal audit function.

Ernst & Young LLP are engaged as the Company’s Auditor. Having considered the experience and tenure of the audit partner and staff and the nature and level of services provided, the Committee remains satisfied with the Auditor’s effectiveness. The audit partners responsible for the audit are rotated every five years and the current lead partner has been in place for three years. There are no contractual obligations restricting the Company’s choice of external auditor. The Committee receives confirmation from the Auditor that they have complied with the relevant UK professional and regulatory requirements on independence. The Committee does not believe that there has been any impairment to the Auditor’s independence.

Relations with ShareholdersThe Board places great importance on communication with shareholders. The Company’s Managers meet regularly with shareholders and report shareholders’ views to the Board. The Chairman is available to meet with shareholders as appropriate. Shareholders wishing to communicate with any members of the Board may do so by writing to them at the address on the back cover.

The Company’s Annual General Meeting provides a forum for communication with all shareholders. The level of proxies lodged for each resolution is announced at the Meeting and is published on the Company’s page of the Managers’ website: www.pacifichorizon.co.uk. The notice period for the Annual General Meeting is at least twenty working days. Shareholders and potential investors may obtain up-to-date information on the Company from the Managers’ website.

Corporate Governance and StewardshipThe Company has given discretionary voting powers to the investment managers, Baillie Gifford & Co. The Managers vote against resolutions they consider may damage shareholders’ rights or economic interests.

The Company believes that it is in the shareholders’ interests to consider environmental, social and governance (‘ESG’) factors when selecting and retaining investments and have asked the Managers to take these issues into account as long as the investment objectives are not compromised. The Managers do not exclude companies from their investment universe purely on the grounds of ESG factors but adopt a positive engagement approach whereby matters are discussed with management with the aim of improving the relevant policies and management systems, and enabling the Managers to consider how ESG factors could impact long term investment returns. The Managers’ statement of compliance with the UK Stewardship code can be found on the Managers’ website at www.bailliegifford.com. The Managers’ policy has been reviewed and endorsed by the Board.

Conflicts of InterestEach Director submits a list of potential conflicts of interest to the Nomination Committee on an annual basis. The Committee considers these carefully, taking into account the circumstances surrounding them, and makes a recommendation to the Board on whether or not the potential conflicts should be authorised. Board authorisation is for a period of one year.