Fairchild PowerPoint Presentation Template functions for key customers . 5 • Energy efficiency,...

48

INVESTOR PRESENTATION January 2015

Transcript of Fairchild PowerPoint Presentation Template functions for key customers . 5 • Energy efficiency,...

INVESTOR

PRESENTATION

January 2015

2

Notes on Forward Looking Statements

and Non-GAAP Measures • Comments in this presentation other than statements of historical fact may constitute forward looking statements and are

based on Fairchild’s management’s estimates and projections and are subject to various risks and uncertainties

• These risks and uncertainties are described in the Company’s periodic reports and other filings with the Securities and Exchange Commission (see the Risk Factors section) and are available at http://sec.gov and investor.fairchildsemi.com

• Actual results may differ materially from those projected in the forward looking statements

• Some data in this presentation may include non-GAAP measures that we believe provide useful information about the operating performance of our businesses that should be considered by investors in conjunction with GAAP measures that we also provide. You can find a reconciliation of non-GAAP to comparable GAAP measures at the Investor Relations section of our web site at http://investor.fairchildsemi.com

Recent additions to our website at http://investor.fairchildsemi.com

Updated Financials (through current quarter with segment revenue/gross margin breakouts)

• Quarterly Fact Sheet with current quarter highlights

• This investor presentation

3

Fairchild Overview

4

Fairchild Today…

Fairchild Semiconductor

2014 Revenue $1.43B Mobile, Computing, Consumer &

Communications Group

(MCCC)

(38% of 2014 Revenue)

Mobile Power

Switches & Interface

Signal Conditioning

LV MOSFETs

Logic

Comprehensive offering of low voltage solutions (<200V)

Power Conversion, Industrial & Automotive Group

(PCIA)

(52% of 2014 Revenue)

Power Conversion

HV MOSFET & IGBT

SPM

Automotive

Opto

Comprehensive offering of high voltage solutions (>200V)

Standard Products Group

(SPG)

(10% of 2014 Revenue)

Standard discrete & analog

Essential functions for key customers

5

• Energy efficiency, mobility and cloud

mega-trends

• Power silicon content grows faster than

end market sales – premium paid for

efficiency

• Fairchild has deep power system

knowledge to support greater integration

and higher efficiency

• Company focused on delighting all

customers from large OEMs to the ―long

tail‖

Markets That Drive Our Business

6

Building a Great Leadership Team

• Promoting from within in areas of progress

Automotive, Supply Chain, Assembly & Test

• Recruiting & upgrading in areas of weakness

Sales & Marketing, Fab Operations, Engineering

• Opportunistically adding talent

Strategy, Finance

7

Building a Great Company

SALES &

MARKETING

TECHNOLOGY

OPERATIONS

BUSINESS

UNITS

• Solid operations org is key foundation

• Sales & marketing as well as

technology also well in place

• Business units key focus now

8

Our Culture

EXCEL

ENGAGED EMPLOYEE

DELIGHTED CUSTOMER

RESPECT

SPEED

EXPLORE SIMPLIFY

PLAY

DIRECT

WORLD-

CLASS

COMPANY

CHALLENGE

9

Fairchild Strategy

10

Strategy as a Daily Activity

Differentiated Products

Application-Centric

Customer Focus

Product-Centric

BEFORE

Commoditized Technology Approach

NOW

Driving Innovation & Disruption

11

$0

$6

$12

$18

$24

$30

$36 $

B U

SD

MOBILITY

ENERGY

CLOUD

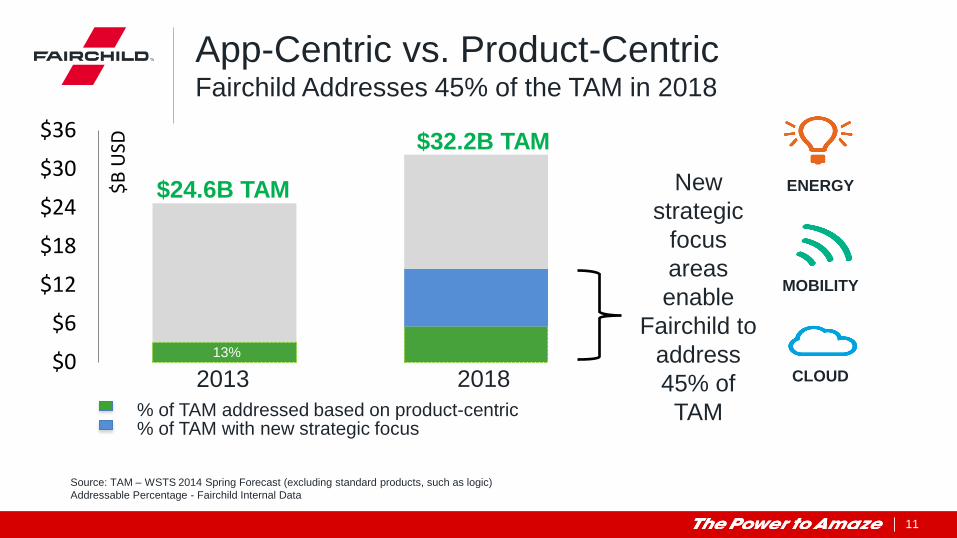

App-Centric vs. Product-Centric Fairchild Addresses 45% of the TAM in 2018

New

strategic

focus

areas

enable

Fairchild to

address

45% of

TAM

$24.6B TAM

2013 2018

Source: TAM – WSTS 2014 Spring Forecast (excluding standard products, such as logic)

Addressable Percentage - Fairchild Internal Data

$32.2B TAM

% of TAM addressed based on product-centric % of TAM with new strategic focus

13%

12

All companies have PRODUCTS

Good companies have STRATEGY

LINKING the two

LEADS TO a

GREAT company

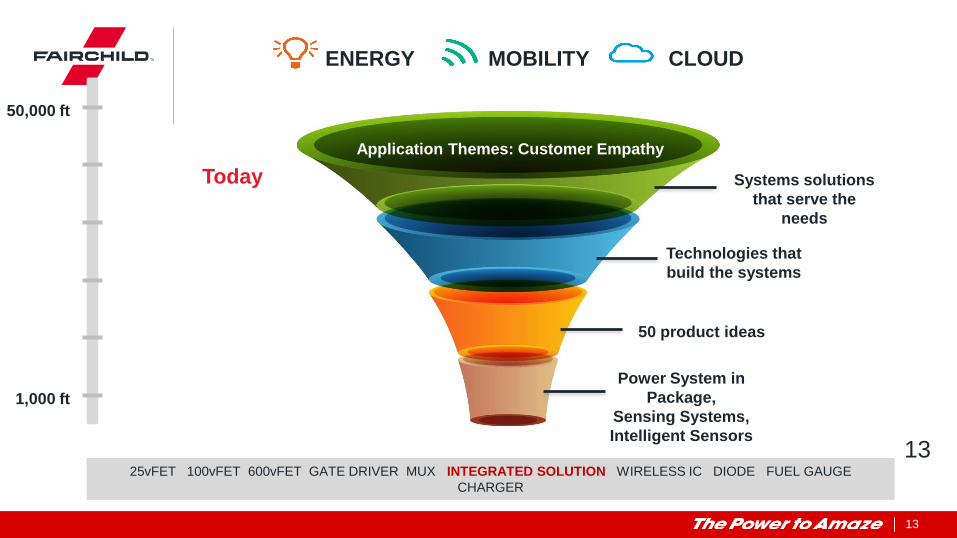

50,000 ft

1,000 ft

13

13

50,000 ft

1,000 ft

CLOUD ENERGY MOBILITY

25vFET 100vFET 600vFET GATE DRIVER MUX INTEGRATED SOLUTION WIRELESS IC DIODE FUEL GAUGE

CHARGER

Systems solutions

that serve the

needs

Technologies that

build the systems

50 product ideas

Power System in

Package,

Sensing Systems,

Intelligent Sensors

Today

Application Themes: Customer Empathy

14

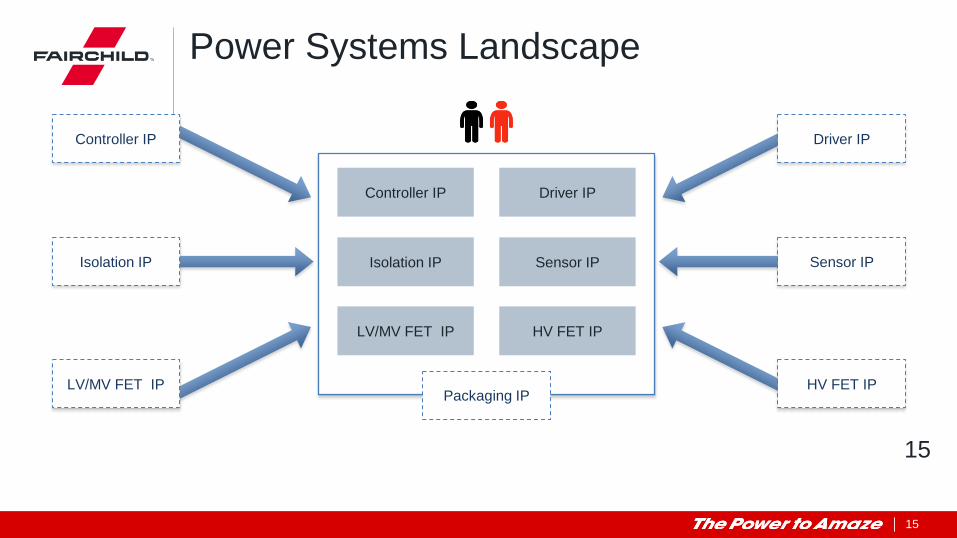

Controller IP

Isolation IP

LV/MV FET IP Packaging IP

Driver IP

Sensor IP

HV FET IP

COMPETITOR

14

Power Systems Landscape

15

Controller IP

Isolation IP

LV/MV FET IP HV FET IP

Sensor IP

Driver IP

Packaging IP

Controller IP

Isolation IP Sensor IP

Driver IP

HV FET IP LV/MV FET IP

15

Power Systems Landscape

16

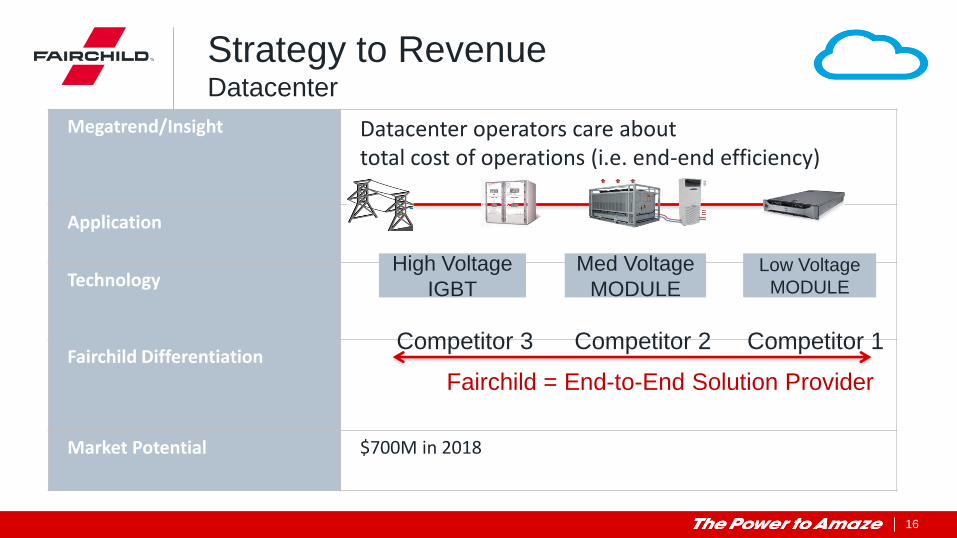

Megatrend/Insight Datacenter operators care about total cost of operations (i.e. end-end efficiency)

Application

Technology

Fairchild Differentiation

Market Potential $700M in 2018

Strategy to Revenue Datacenter

High Voltage

IGBT

Med Voltage

MODULE

Low Voltage

MODULE

Competitor 1 Competitor 2

Fairchild = End-to-End Solution Provider

Competitor 3

17

Megatrend/Insight Consumers don’t want to think about charging

Application Mobile, Phone, & Tablet

Technology Adaptive, Smart-Charging ICs

Design In 2015 Large Chinese Mobile Customer — Fairchild Total System Solution Fairchild communications protocol enables customers to provide a total system solution, from wall AC adaptor to battery.

Market Potential $3.8B in 2018

Strategy to Revenue Wall to Battery (W2B)

18

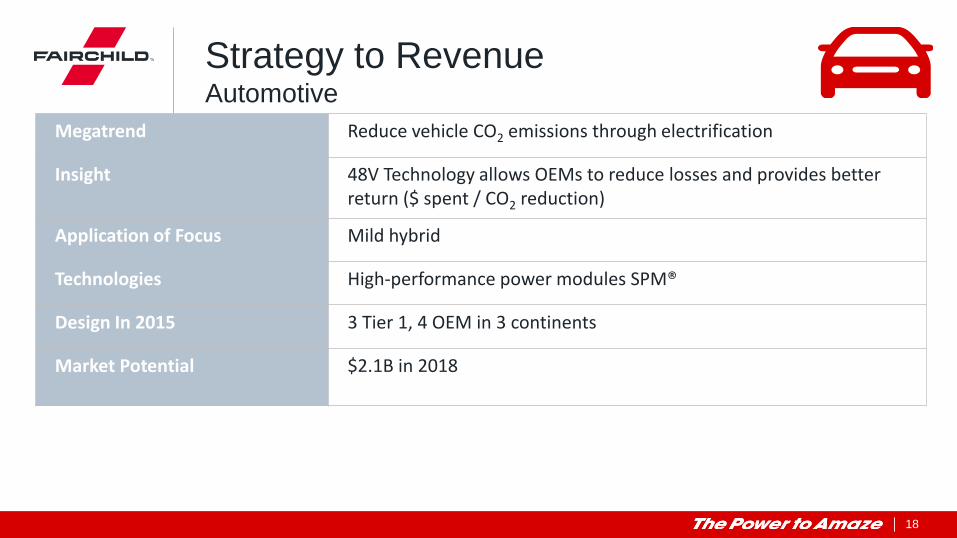

Megatrend Reduce vehicle CO2 emissions through electrification

Insight 48V Technology allows OEMs to reduce losses and provides better return ($ spent / CO2 reduction)

Application of Focus Mild hybrid

Technologies High-performance power modules SPM®

Design In 2015 3 Tier 1, 4 OEM in 3 continents

Market Potential $2.1B in 2018

Strategy to Revenue Automotive

19

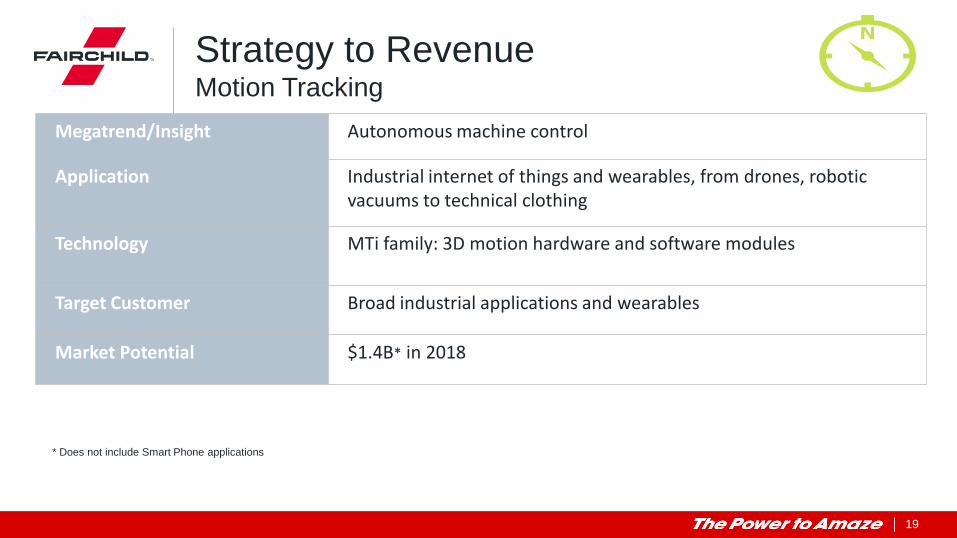

Megatrend/Insight Autonomous machine control

Application Industrial internet of things and wearables, from drones, robotic vacuums to technical clothing

Technology MTi family: 3D motion hardware and software modules

Target Customer Broad industrial applications and wearables

Market Potential $1.4B* in 2018

Strategy to Revenue Motion Tracking

* Does not include Smart Phone applications

20

Marketing & Sales Overview

21

Sales Overview

• Foundation — New sales strategy

• People — New leaders, skills, mindset

• Deployment — New growth opportunities

• Execution — New customer engagement model

22

Foundation New Sales Strategy

• DEMAND CREATION - Design In/Win — shift coverage to R&D

- System approach — understand the application

- Customer empathy — fill a latent need, solve a problem

• CLOSER TO CUSTOMERS - Proximity — quick response

- Adaptive — fragmented customer base

- Agile — early engagement with emerging customers

• ACCOUNTABILITY - Revenue accountability moved to design origin

- Pay on results — new sales bonus on design-in, revenue growth

23

• NEW SKILLS – VALUE ADDED TO CUSTOMERS

- More technical sales – EE

- More Field Applications Engineers (FAE) – FAE as application experts

• NEW MINDSET – PROACTIVE, DRIVE DEMAND

- More field-based people, less operations

- Relationship-builders

People New Leaders, Skills, Mindset

JOSEPH KARIM Americas VP

22 years Atmel, Intersil, ADI

ANDY LAI China VP 22 years

ADI, NSC, TI

ANDREAS HAMMER EMEA VP 16 years SiLabs, TI

JOSEPH NOTARO Motion Tracking VP

22 years STM

WEI LI Taiwan GM

20 years Lucent, Maxim

• RAISING THE BAR – NEW LEADERSHIP TEAM

24

Resources Best Deployed

• Increase investment on most significant markets

- China

- Germany

- Silicon Valley

• Shift resources to most promising opportunities

- Generated revenue vs. transacted revenue locations

- Invest where the growth will be vs. where revenue is today

- Aligned company focus segments

• Expand customer base

- More in fragmented markets: (i.e. Industrial, Auto)

- Emerging segments and customers: (i.e. Wearables)

- Mass market

25

Resources Go-to-Market

ASSIGNED

ACCOUNTS

MASS MARKET

LONG TAIL

Growth

Potential

• Biggest growth opportunity

• Focus, depth — 80% of resources

• Demand creation

• More customers

• Leveraging distribution

• More engineers

• Leverage the web & catalog distributors

• Build brand awareness

26

New Customer Engagement

• CUSTOMERS DRIVE PRODUCT DEFINITION - System expertise provides unique insight - FAE conduit of customer pain points

• INCREASE COMPLETE RECEIVED VALUE

- Product to solution, design expertise - Supply chain excellence - No EOL policy

• RELATIONSHIPS MAKE A DIFFERENCE

- Attention to every customer - Focus on customer empathy

27

• CLOUD & TELECOM - Move to IC & System approach - More strategic engagement - Growth acceleration

• MOBILE POWER & W2B - Full end-end solution - Huge value to customer - Major ASP increase YR13 Y14 $M Y15 $M Y16 $M

Others

Mobile Power & W2B

Cloud & Telecom

Source: Fairchild Internal Data

Execution Customer Showcase Relationship, Focus, System Approach Drives Growth

28

Marketing Overview

• New Brand

• New Go-to-Market

• Success

• Customer Count

29

Why Reposition The Brand?

• Brand history: older company & commodity sales Stagnation in customer growth & revenue

• A new Fairchild brand Energize employees

Attract top-notch engineering & sales talent

Grow relationships with design engineers

• Long-Tail customers create innovative products

30

Old brand identity

2013

31

New Brand Identity

2014

32

New Branding ―Xiantong‖ in China

• Historical significance

• Strong awareness

• Positive connotation

33

New Go-to-Market Website: Optimized for Long-Tail Lead Generation

• SHIFT commodity sales content to

value-added content

• MOVE design engineers through

the entire buying journey

34

New Go-to-Market Success Via Power Seminars in 2014

• 3x new customer leads

• Scalability

Live streaming to remote locations

Post-seminar engagement

• Wider awareness

New prospects

Social media & community

Boston, MA – May 1

Taichung, Taiwan – May 15

Beijing, China – May 20

Shenzhen, China – May 22

San Jose, CA – June 3

35

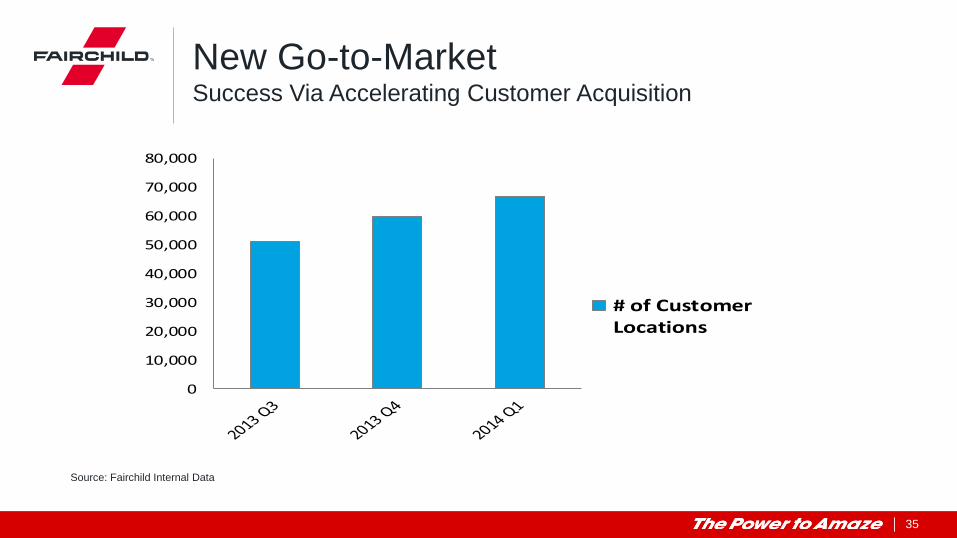

New Go-to-Market Success Via Accelerating Customer Acquisition

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

# of CustomerLocations

Source: Fairchild Internal Data

36

Finance Overview

37

Highlights of the Quarter – Q4 2014 Sales were $337m, down 12% QoQ due to under-shipping distribution channel sell through

Full year 2014 sales were up 2% despite weakness at one large customer (3 point impact)

Double digit sales growth into auto, battery charging, comm infrastructure & data center…expect same type growth in 2015

Mobile sales down in 2014 due to one large customer…deign wins expected to drive overall sales growth in 2015

Demand was seasonally lower in most end markets…bookings light in Oct & Nov…Dec stronger…Significant strength in Jan

Channel inventory decreased $8m to 9 weeks of inventory. Fairchild maintains one of the leanest inventory positions in the

industry

Adjusted gross margin was down 3 points to 32.4% due to lower loadings in prior quarter and higher inventory write offs

OPEX was lower than forecast at $92m, down 4% QoQ due to ongoing cost controls and lower variable compensation

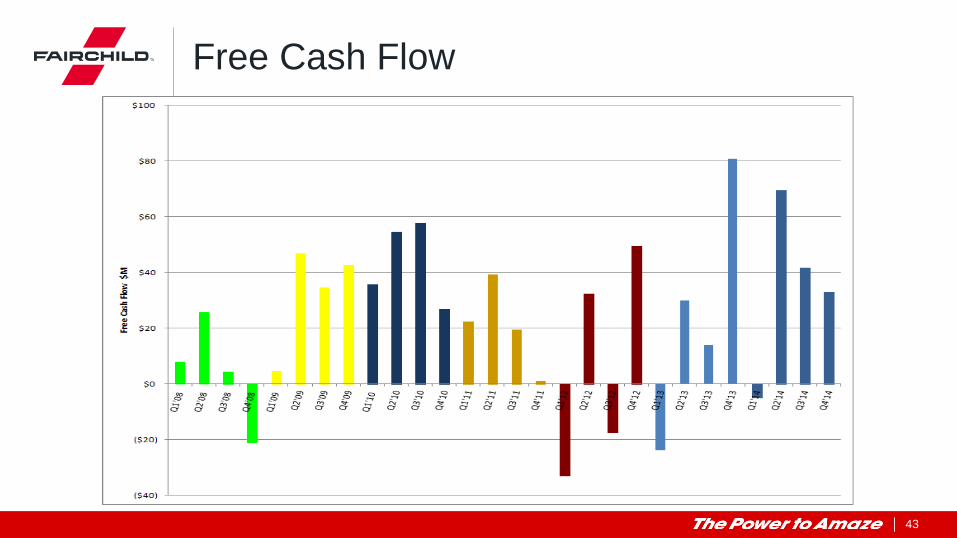

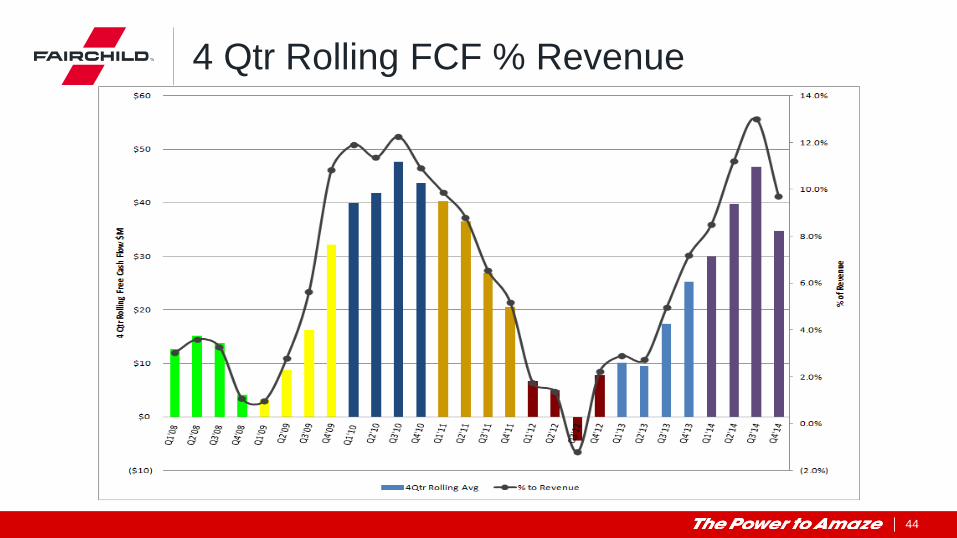

Free cash flow was $33m in Q4 and up 38% for 2014 to $139m. Net cash was higher QoQ at $155m

Repurchased 10m shares in 2014 for $142m…plan to continue returning 100% of excess free cash flow in 2015

Lead times remain short and supply chain is well positioned to support turns business

Manufacturing consolidation remains on track to significantly improve flexibility and margins in the 2H 2015

38

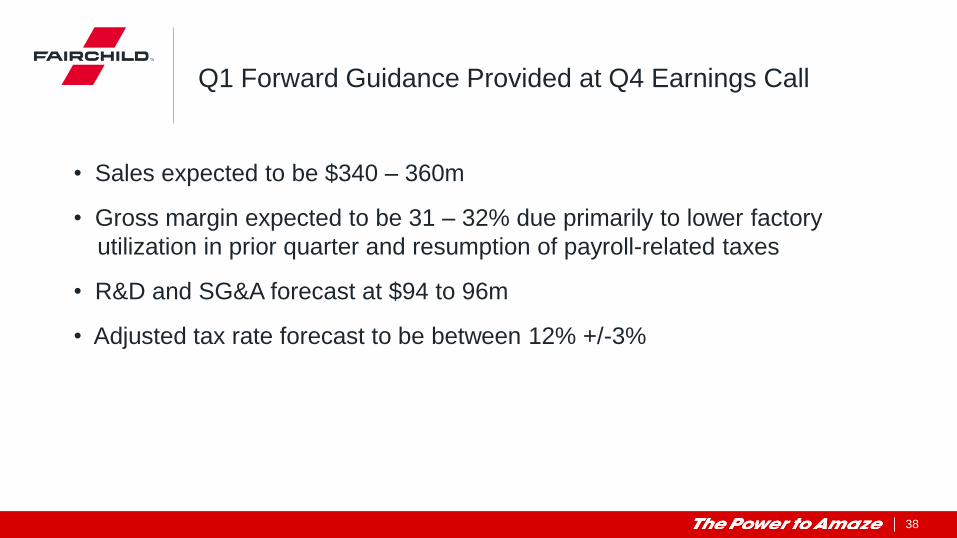

Q1 Forward Guidance Provided at Q4 Earnings Call

• Sales expected to be $340 – 360m

• Gross margin expected to be 31 – 32% due primarily to lower factory

utilization in prior quarter and resumption of payroll-related taxes

• R&D and SG&A forecast at $94 to 96m

• Adjusted tax rate forecast to be between 12% +/-3%

39

Adjusted Revenue & GM%

40

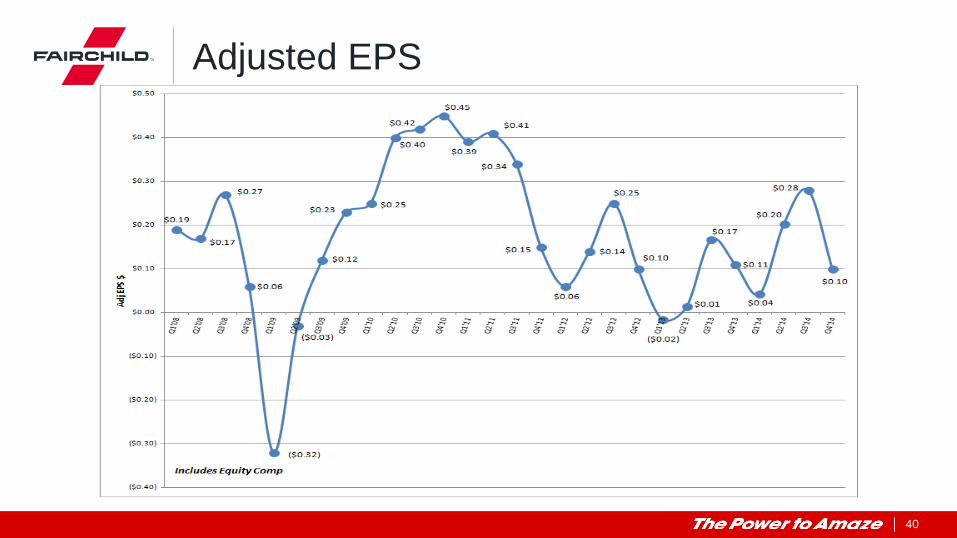

Adjusted EPS

41

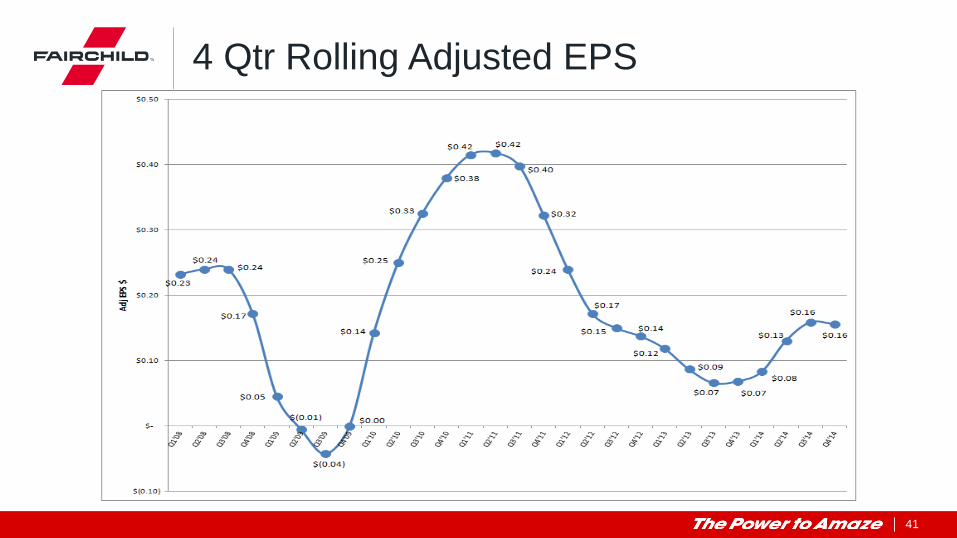

4 Qtr Rolling Adjusted EPS

42

Balance Sheet Improvement Disciplined Asset Management

• Q4 balance sheet summary:

• Cash and investments exceed debt by $155m

• Internal inventory increased to 106 DOI due to bridge inventory required to complete factory closures

• DSO flat QoQ at 34 days

• Days of payables increased QoQ to 42 days

• FCF was $33m for Q4 and +38% for the full year 2014 to $139m

• Primary focus remains investing in our business and enhanced buyback

• Repurchased 10m shares of stock for $142m in 2014

• Plan to return 100% of excess FCF to investors in 2015

43

Free Cash Flow

44

4 Qtr Rolling FCF % Revenue

45

Debt Composition

0

200,000

400,000

600,000

800,000

1,000,000

1,200,000

1997 1999 2001 2007 2008 2009 2010 2011 2012 2013

Drawn Revolver Term Loan Convert High Yield

46

Net Debt & Interest Trend

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

9.0%

-$700.0

-$600.0

-$500.0

-$400.0

-$300.0

-$200.0

-$100.0

$0.0

$100.0

$200.0

$300.0

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 Q1 '14 Q2 '14 Q3 '14

Net Cash Interest % of Revenue

47

Follow us on Twitter @ twitter.com/fairchildSemi

View product and company videos, listen to podcasts and comment on our

blog @ www.fairchildsemi.com/engineeringconnections

Visit us on Facebook @ www.facebook.com/FairchildSemiconductor

THANK YOU