Estimating Semi Parametric

67

Estimating Semiparametric ARCH (∞) Models by Kernel Smoothing Methods Author(s): O. Linton and E. Mammen Source: Econometrica, Vol. 73, No. 3 (May, 2005), pp. 771-836 Published by: The Econometric Society Stable URL: http://www.jstor.org/stable/3598867 Accessed: 01/03/2010 21:33 Your use of the JSTOR archive indicates your acceptance of JSTOR's Terms and Conditions of Use, available at http://www.jstor.org/page/info/about/policies/terms.jsp. JSTOR's Terms and Conditions of Use provides, in part, that unless you have obtained prior permission, you may not download an entire issue of a journal or multiple copies of articles, and you may use content in the JSTOR archive only for your personal, non-commercial use. Please contact the publisher regarding any further use of this work. Publisher contact information may be obtained at http://www.jstor.org/action/showPublisher?publisherCode=econosoc . Each copy of any part of a JSTOR transmission must contain the same copyright notice that appears on the screen or printed page of such transmission. JSTOR is a not-for-profit service that helps scholars, researchers, and students discover, use, and build upon a wide range of content in a trusted digital archive. We use information technology and tools to increase productivity and facilitate new forms of scholarship. For more information about JSTOR, please contact [email protected]. The Econometric Society is collaborating with JSTOR to digitize, preserve and extend access to Econometrica. http://www.jstor.org

-

Upload

alkindi-ramadhan -

Category

Documents

-

view

225 -

download

0

Transcript of Estimating Semi Parametric

8/7/2019 Estimating Semi Parametric

http://slidepdf.com/reader/full/estimating-semi-parametric 1/67

Estimating Semiparametric ARCH (∞) Models by Kernel Smoothing MethodsAuthor(s): O. Linton and E. MammenSource: Econometrica, Vol. 73, No. 3 (May, 2005), pp. 771-836Published by: The Econometric SocietyStable URL: http://www.jstor.org/stable/3598867

Accessed: 01/03/2010 21:33

Your use of the JSTOR archive indicates your acceptance of JSTOR's Terms and Conditions of Use, available at

http://www.jstor.org/page/info/about/policies/terms.jsp. JSTOR's Terms and Conditions of Use provides, in part, that unless

you have obtained prior permission, you may not download an entire issue of a journal or multiple copies of articles, and you

may use content in the JSTOR archive only for your personal, non-commercial use.

Please contact the publisher regarding any further use of this work. Publisher contact information may be obtained at

http://www.jstor.org/action/showPublisher?publisherCode=econosoc.

Each copy of any part of a JSTOR transmission must contain the same copyright notice that appears on the screen or printed

page of such transmission.

JSTOR is a not-for-profit service that helps scholars, researchers, and students discover, use, and build upon a wide range of

content in a trusted digital archive. We use information technology and tools to increase productivity and facilitate new forms

of scholarship. For more information about JSTOR, please contact [email protected].

The Econometric Society is collaborating with JSTOR to digitize, preserve and extend access to Econometrica.

http://www.jstor.org

8/7/2019 Estimating Semi Parametric

http://slidepdf.com/reader/full/estimating-semi-parametric 2/67

Econometrica,Vol.73, No. 3 (May, 2005),771-836

ESTIMATING SEMIPARAMETRIC ARCH(oo) MODELS BY

KERNEL SMOOTHING METHODS1

BY O. LINTON2 AND E. MAMMEN3

We investigatea classof semiparametricARCH(oo) models that includes as a spe-cial case the partiallynonparametric(PNP) model introducedby Engle andNg (1993)and whichallows for both flexibledynamicsand flexible functionform with regardtothe "newsimpact"function. We show that the functionalpartof the model satisfies a

typeII linearintegralequationandgivesimpleconditionsunderwhichthere is a uniquesolution.Weproposeanestimationmethod that is based on kernelsmoothingandpro-filed likelihood.We establishthe distributiontheoryof the parametriccomponentsandthe pointwisedistributionof the nonparametriccomponentof the model. Wealso dis-cussefficiencyof both the parametricpartand the nonparametricpart.Weinvestigatethe

performanceof our

procedureson simulateddata andon a

sampleof S&P500 in-

dex returns.We findevidence of asymmetricnewsimpactfunctions,consistentwith the

parametricanalysis.

KEYWORDS: ARCH, inverseproblem,kernel estimation,news impactcurve,non-

parametricregression,profilelikelihood;semiparametricestimation,volatility.

1. INTRODUCTION

STOCHASTICVOLATILITYMODELS are of considerable current interest in em-

piricalfinance following the seminal work of Engle (1982). Perhapsthe most

popularversion of this is Bollerslev's(1986) GARCH(1, 1) model in whichtheconditionalvariance o2 of a martingaledifferencesequence Ytis

(1) t= -f1a,_ + a +a yy_.

This model has been extensivelystudied and generalizedin variousways.Seethe reviewof Bollerslev,Engle, and Nelson (1994). This paperis abouta par-ticularclass of nonparametric/semiparametricgeneralizationsof (1). The mo-tivation for this line of workis to increase the flexibilityof the class of models

we use and to learn from this the shape of the volatilityfunction without re-strictingit a priorito have or not have certainshapes.

The nonparametricARCH literature apparently begins with Pagan andSchwert (1990) and Pagan and Hong (1991). They consider the case wherer2 = o2(Yt,_), where a(.) is a smooth but unknownfunction,and the multilag

1Wewould like to thank Costas Meghir, two referees, Xiaohong Chen, Paul Doukhan,

WolfgangHardle,ChristianHuse,Dennis Kristensen,JensNielsen,and Eric Renault forhelpfulcomments.

2Researchwassupportedbythe EconomicandSocial Science ResearchCouncil of the United

Kingdom.3Supportedby the Deutsche Forschungsgemeinschaft,Sonderforschungsbereich373 "Quan-

tifikationund SimulationOkonomischerProzesse,"Humboldt-Universitatzu Berlin andProjectMA1026/6-2.

771

8/7/2019 Estimating Semi Parametric

http://slidepdf.com/reader/full/estimating-semi-parametric 3/67

O. LINTON AND E. MAMMEN

versiona- = or2(yt-l, Yt-2, ..., Yt-d). Hardle andTsybakov(1997) appliedlocallinearfit to estimatethevolatilityfunctiontogetherwith the mean function and

derivedtheir

joint asymptoticproperties.The multivariateextension is

givenin

Hardle,Tsybakov,andYang(1996). MasryandTj0stheim(1995) also estimate

nonparametricARCH models using the Nadaraya-Watsonkernel estimator.In practice,it is necessaryto includemanylaggedvariables.The problemwiththis is thatnonparametricestimationof a multidimensionalregressionsurfacesuffersfromthewell-known"curseof dimensionality":the optimalrate of con-

vergence decreaseswith dimensionalityd; see Stone (1980). In addition, it ishard to describe, interpret,and understandthe estimated regressionsurfacewhen the dimensionis morethantwo.Furthermore,evenforlarged this model

greatlyrestrictsthe dynamicsfor the varianceprocess since it effectivelycor-

responds to an ARCH(d) model, which is knownin the parametriccase notto capturethe dynamicswell. In particular,if the conditionalvarianceis highlypersistent, the nonparametricestimator of the conditionalvariance will pro-vide a poor approximation,as reportedin Perron(1998). So not only does thismodel not capture adequately the time series properties of many data sets,but the statisticalproperties of the estimators can be poor and the resultingestimatorshard to interpret.

Additive models offer a flexible but parsimoniousalternative to nonpara-metricmodels,and have been used in manycontexts,see Hastie and Tibshirani

(1990). Supposethat or2= C, + yEd o-(y,_j). The best achievablerate of con-vergence for estimates of r2( ) is that of one-dimensionalnonparametricre-

gression; see Stone (1985). Yang, Hardle, and Nielsen (1999) proposed analternativenonlinear ARCH model in which the conditional mean is addi-

tive, but the volatility is multiplicative:2 = c I= o-2(Y-j). Their estima-

tion strategy is based on the method of partial means/marginalintegrationusing local linear fits as a pilot smoother. Kim and Linton (2004) generalizethis model to allow for arbitrary(but known) transformations,i.e., G(ur2)=

Cv+ EjLd ?'(yt_j), where G(.) is a knownfunction like log or level. Horowitz

(2001) hasanalyzedthe model where G(-) is alsounknown,but hisresultswereonly in a cross-sectionalsetting.These separablemodels deal with the curse of

dimensionality,but still do not capturethe persistenceof volatilityandspecifi-cally they do not nest the favoriteGARCH(1, 1) process.

This paperanalyzesa class of semiparametricARCH models that has both

general functional form aspects and flexible dynamics.A special case of ourmodel is the Engle and Ng (1993) PNP model where a2 = a132_1+ m(yt_j),where m(.) is a smooth but unknown function. Our semiparametricmodelnests the simple GARCH(1, 1) model but permits more general functionalform: it allows for an

asymmetricleverageeffect and as much

dynamicsas

GARCH(1, 1). A majorissue we solve is how to estimate the function m(.)by kernel methods. Our estimationapproachis to derivepopulationmomentconditions for the nonparametricpart and then solve them with empiricalcounterparts.The moment conditionswe obtain are linear type II Fredholm

772

8/7/2019 Estimating Semi Parametric

http://slidepdf.com/reader/full/estimating-semi-parametric 4/67

SEMIPARAMETRICARCH(oc) MODELS

integralequations,and so they fall in the class of inverseproblemsreviewed in

Carrasco,Florens, and Renault (2003). These equationshave been extensively

studiedin the appliedmathematicsliterature;see, forexample,Tricomi(1957).They also arise a lot in economic theory; see Stokey and Lucas (1989). Thesolution of these equations in our case only requiresthe computationof two-dimensionalsmoothing operationsandone-dimensionalintegration,and so isattractivecomputationally.From a statisticalperspective,there hasbeen somerecent work on this class of estimationproblems. Startingwith Friedman andStuetzle (1981), in Breiman and Friedman(1985) and Hastie and Tibshirani

(1990) these methods have been investigatedin the context of additive non-

parametric regression and related models, where the estimating equationsare

usuallyof

typeII.

Recently, Opsomerand

Ruppert (1997)and

Mammen,Linton, and Nielsen (1999) have provideda pointwise distributiontheory forthis specificclass of problems. Newey and Powell (2003) studiednonparamet-ric simultaneous equations and obtained an estimation equation that was alinearintegralequation also, except that it is the more difficulttypeI. Theyes-tablishthe uniformconsistencyof their estimator;see also Darolles, Florens,and Renault (2002). Hall and Horowitz (2003) establishthe optimalrate forestimation in this problem and propose two estimatorsthat achieve this rate.Neither paper provides pointwise distributiontheory. Our estimation meth-ods andproof techniquearepurelyapplicableto the type II situation,which is

nevertheless quite common elsewhere in economics. For example, BerryandPakes (2002) derive estimators for a class of semiparametricdynamicmodelsused in industrialorganizationapplications,andwhich solve type II equationssimilar to ours.

Our paper goes significantlybeyond the existingliteraturein two respects.First, the integral operatordoes not necessarilyhave normless than 1 so thatthe iterative solution methodof successiveapproximationsis not feasible.Thisalso affects the way we derive the asymptoticproperties, and we cannot di-

rectlyapplythe results of Mammen,Linton,andNielsen (1999) here. Second,

we have also finite-dimensionalparametersand their estimationis of interestin itself. We establish the consistency and pointwise asymptoticnormalityofour estimatesof the parameterandof the function. We establishthe semipara-metric efficiencybound for a Gaussianspecial case and show that our para-meter estimator achieves this bound. We also discuss the efficiency questionregardingthe nonparametriccomponentandconclude thata likelihood-basedversion of our estimator cannot be improvedon without additionalstructure.Weinvestigatethe practicalperformanceof ourmethod on simulateddataand

present the resultof an applicationto S&P500 data. The empiricalresults in-

dicatesome

asymmetryand

nonlinearityin the news

impactcurve.Our model is introduced in the next section. In Section 3 we present ourestimators.In Section 4 we give the asymptoticproperties.In Section 5 we dis-cuss an extension of our basicsettingthataccommodatesa richervarietyof tailbehavior.Section 6 reportssome numericalresultsand Section 7 concludes.

773

8/7/2019 Estimating Semi Parametric

http://slidepdf.com/reader/full/estimating-semi-parametric 5/67

O. LINTON AND E. MAMMEN

2. THE MODELAND ITS PROPERTIES

We shall suppose throughoutthat the process {yt},o is stationarywith fi-

nite fourth moment. We concentrate most of our attention on the case wherethere is no mean process, althoughwe later discussthe extension to allow forsome mean dynamics.Define the volatilityprocessmodel

00

(2) t2(0, m) = ,t + Ej(0)m(yt_j),

j=1

where /t E R, 0 E O c RP, and m E M, where M = {m: measurable}. Thecoefficients Qj(0)

satisfyat least /j(0) > 0 and qj

?j(0)< oo for all 0 E 0.

The true parameters 00 and the true function mo(.) are unknown and to beestimated from a finite sample {yl, ..., YTI. The process /, can be allowed to

depend on covariatesand unknownparameters,but at this stage it assumed tobe known.In much of the sequel it can be put equal to zero withoutanyloss of

generality.It will become importantbelow when we consider more restrictivechoicesof M. Robinson(1991) isperhapsthe firststudyof ARCH(oo) models,

althoughhe restrictedattention to the quadraticm case.

FollowingDrost andNijman(1993),we cangive threeinterpretationsto (2).ThestrongformARCH(oo) process ariseswhen

(3)Y ?t?-t

is i.i.dwithmean 0 and variance 1,where o-( = o-2(0o, mo). Thesemistrongformariseswhen

(4) E(yL, t_i) ==0 and E(y2l_i) 2,

where Ft-_ is the sigma field generated by the entire past history of the

y process. Finally,there is a weakform in which ot2is defined as the projec-tion on a certainsubspace.Specifically,let 00,mobe defined as the minimizersof the populationleast squarescriterion function

-r 2-

(5) S(, m) =EYt2

- j(0)m(yt-j)j=l

and let t2= qi1j(0o)mo(yt_-). The criterion(5) is well defined only when

E(y4)< oo.

In the special case that Qj(0) = 0j-1, with 0 < 0 < 1, we can rewrite (2) as a

differenceequationin the unobservedvariance

(6) ot2= 02 + m(y_) (t = 1,2...),

774

8/7/2019 Estimating Semi Parametric

http://slidepdf.com/reader/full/estimating-semi-parametric 6/67

SEMIPARAMETRICARCH(oo) MODELS

and this is consistentwith a stationaryGARCH(1, 1) structurefor the unob-served variance when m(y) = a + yy2 for some parametersa, y. It also in-cludes other

parametricmodels as

specialcases: the

Glosten,Jegannathan,and

Runkle (1993) model, takingm(y) = a + yy2+ Sy21(y< 0), the Engle (1990)asymmetricmodel, takingm(y) = a + y(y + 8)2, andthe Engle and Bollerslev

(1986) model, takingm(y) = a + yIylI.The functionm(.) is the "newsimpactfunction,"and it determines the way

in which the volatilityis affectedby shocks to y. Our model allows forgeneralnews impact functions including both symmetricand asymmetricfunctions,and so accommodatesthe leverage effect (Nelson (1991)). The parameter 0,

throughthe coefficients Qj(0), determines the persistenceof the process, andwe in principle allow for quite general coefficient values. A general class of

coefficients can be obtained from the expansionof autoregressivemovingav-erage (ARMA) lag polynomials,as in Nelson (1991).

Our model generalizes the model considered in Carroll, Mammen, andHardle (2002) in which -2= j

-100 mo(yt_j)for some finite r. Their esti-

mation strategywas quite different from ours: they relied on an initial esti-mator of a r-dimensional surface and then marginal integration(Linton andNielsen (1995)) to improvethe rate of convergence.This method is likely towork poorlywhen r is very large. Also, their theory requiresthe smoothnessof m to increasewith r. Indeed,a contributionof ourpaperis to providean es-

timation method for 00andm(.) thatjustrelies on one-dimensionalsmoothingoperations,but is also amenable to theoreticalanalysis.Some otherpaperscanbe considered precursorsto this one. First, Gourieroux and Monfort (1992)introduced the qualitativethreshold ARCH (QTARCH)which allowed quiteflexiblepatternsof conditional mean and variancethrough step functions,al-

though their analysiswas purely parametric. Engle and Ng (1993) analyzedpreciselythe semistrongmodel (2) with j(0) = Oj-1and called it partiallynon-

parametricor PNP for short.They proposed an estimation strategybased on

piecewise linearsplines.Finally,we should mention some workbyAudrinoand

Biihlmann(2001): their model is that o2 = A(yt_l, ot2_) for some smooth butunknown function A(.), and includes the PNP model as a special case. How-

ever, although they proposed an estimation algorithm,they did not establishthe distributiontheoryof their estimator.

In the next subsection we discuss a characterizationof the model that gen-erates our estimation strategy.If m were known, it would be straightforwardto estimate 0 from some likelihood or least squarescriterion. The main issueis how to estimate m(.) even when 0 is known. The kernel method likes to ex-

pressthe function of interest as a conditionalexpectationor densityof a smallnumberof observable

variables,but this is not

directly possiblehere because

m is only implicitlydefined. However,we are able to show that m can be ex-

pressed in terms of all the bivariatejoint densities of (Yt, t_-j),j = ?1, ..., i.e.,this collection of bivariate densities forms a set of sufficient statisticsfor ourmodel. We use this relationshipto generate our estimator.

775

8/7/2019 Estimating Semi Parametric

http://slidepdf.com/reader/full/estimating-semi-parametric 7/67

O. LINTON AND E. MAMMEN

2.1. Linear Characterization

Supposefor pedagogic purposesthat the semistrongprocess defined in (4)

holds, and for simplicity define 2 = y2 - . Takemarginalexpectationsforanyj> 1,

00

(7) E(yt,jyt-= y= ) +j(0o)Em() + ()E[m(yt-)ly- = y].

k#j

For each such j the above equation implicitlydefines m(-). This is really amoment conditioninthe functionalparameterm(.) foreachj, and can be usedas anestimatingequation.As inthe parametricmethod of momentscase,it can

payto combine the estimatingequationsin terms of efficiency.Specifically,wetake the linear combinationof these momentconditions,

0C

(8) q,j(o)E(Yt2lyt_, = y)j=1

= Lir(0o)m(y) + j(Oo)Et k(0O)E[m(yt-k)lyt-j =],j=l j=1 kj

whichyields anotherimplicit equationin m(.).This equation arises as the first order condition from the least squaresdef-inition of o-2,given in (5), as we now discuss. We can assume that the quanti-ties 00, mo(.) are the uniqueminimizersof (5) over 0 x M bythe definition ofconditionalexpectation,see Drost andNijman (1993). Furthermore,the mini-mizer of (5) satisfies a first-ordercondition andin the Appendixwe show thatthis first-ordercondition isprecisely(8). Infact,ifwe minimize(5) withrespectto m E MAfor any0 e 0 and let modenote thisminimizer,then mosatisfies(8)with 00replaced by 0. Note that we are treating/t as a knownquantity.

We next rewrite(8) (forgeneral 0) in a more convenient form. Let Podenote

the marginaldensityof y and let pjT,denote thejoint densityof yj,yi. Define

(9) Ho(y, x) -- ~ (0) poj(y, x))po(y)po(x)'

0)

(10) m*(y) = E j(0)g;(y),jij=l

whereqt(0)

=if(0)/ = I(0)

andj (0)

=kO ij+k(0) i(0)/El= I (0while gj(y) = E(yt2yiy_j= y) for j > 1. Then the function m0(.) satisfies

(11) mO(y)= m*(y) + 7(y, x)m()o(x)(x) dx

776

8/7/2019 Estimating Semi Parametric

http://slidepdf.com/reader/full/estimating-semi-parametric 8/67

SEMIPARAMETRICARCH(oo) MODELS

for each 0 E 0 (this equation is equivalent to (8) for all 0 E 0). The opera-tor Hj(y, x) = po,j(y,x)/po(y)po(x) is well studied in the statistics literature

(see Bickel, Klaassen, Ritov, and Wellner (1993, p. 440)); our operator 'Heis just a weighted sum of such operators,where the weights are declining tozero rapidly.In additivenonparametricregression,the correspondingintegraloperatoris an unweightedsumof operatorslike 7-j(y, x) over the finite num-ber of dimensions (see Hastie and Tibshirani(1990) and Mammen, Linton,and Nielsen (1999)). Although the operators-j are not self-adjointwithoutan additionalassumptionof time reversibility,it can easilybe seen that lHe is

self-adjointin L2(po) due to the two-sided summation.4

Our estimation procedurewill be based on pluggingestimates m* and 'HOof

m0or

Ho, respectively,into

(11)and then

solvingfor

mi.The estimates

m* and He will be constructedby pluggingestimates of poj, po, and gj into

(10) and (9). Nonparametricestimates of these functionsonlyworkaccuratelyfor argumentsnot too large. We do not want to enter into a discussion oftail behavior of nonparametricestimates at this point. For this reason we

change our minimizationproblem (5), or rather restrict the parameter setsfurther. We consider minimization of (5) over all 0 E 0 and m E Mc, wherenow Mc is the class of all bounded measurable functions that vanish out-side [-c, c], where c is some fixed constant (this makes o,2 = ft, whenever

Yt-j? [-c, c] for all j). Let us denote these minimizersby Ocand mc. Fur-

thermore,denote the minimizerof (5) for fixed 0 over m c MCby me,c.ThenOcandmcminimizeE[{y2-

J?,1 r(0)m(y, j)}2]over 0 x MCandmo,cmini-

mizes E[{yj2- L j1 i j(0)mo(yt_j)}2]over MA.For now we adopta fixed trun-cationwhere c and iLtare constant andknown,but return to this in Section 5.Then mo,c satisfies mo,c(y) = m;(y) + fcCcHo(y, x)mo,c(x)po(x) dx for lyI < c

and vanishes for lyI> c. For simplicitybut in abuse of notation we omit thesubindex c of mo,cand we write

(12) me= m?+'-emo.

For each 0 E 0, He0is a self-adjointlinear operatoron the Hilbert space offunctions m that are defined on [-c, c] with norm lmll2 = fCcm(x)2po(x) dxand (12) is a linearintegralequation of the second kind.There are some gen-eral resultsprovidingsufficientconditionsunderwhich suchintegralequationshave a uniquesolution. See Darolles, Florens,andRenault(2002) for a discus-sion on existence anduniquenessfor the moregeneralclass of typeI equations.

We assume the following highlevel condition:

4Specifically, with (f,g) = f f(x)g(x)po(x)dx denoting the usual inner prod-uct in L2(po), we have (g,1om) =

--Ejyk kj(O)OIk(O)E[g(yt-j)E[m(ytk)lYt-j]] =

- Y jLk tfj(0)qJk(0)E[g(yt-j)m(yt-k)] = (Htg, m) because the double sum is symmetricin j, k. The definition of adjointoperatorcan be found in Bickel, Klaassen,Ritov, and Wellner

(1993,p. 416).

777

8/7/2019 Estimating Semi Parametric

http://slidepdf.com/reader/full/estimating-semi-parametric 9/67

O. LINTON AND E. MAMMEN

ASSUMPTIONAl: Theoperator1-o(x, y) is Hilbert-Schmidtuniformlyover0,i.e., supo fcS fScH(x, y)2po(x)po(y) dx dy < oo.

A sufficientcondition forAssumptionAl is thatthejointdensitiespo,j(y,x)are uniformlybounded for j 7 0 and Ixl, IYI< c, and that the densitypo(x) isboundedawayfrom0 for Ixl< c.

Under AssumptionAl, for each 0 E 0, Ho is a self-adjointbounded com-

pact linear operator on the Hilbert space of functions L2(po), and there-fore has a countable number of eigenvalues: oo > IA0,l > IAO,21> , with

supo, ,= A2j < oo.

ASSUMPTIONA2: Thereexist no 0 E0 and m EMc

withlml112

= 1 such that

ji1 fj(0)m(y,_j) = 0 withprobability1.

Thiscondition rules out a certain"concurvity"in the stochasticprocess.That

is, the data cannot be functionallyrelated in this particularway. It is a natural

generalizationto our situation of the condition that the regressorsbe not lin-

earlyrelatedin a linearregression.A specialcase of this conditionwasused inWeiss(1986) andKristensenand Rahbek(2003) for identificationin paramet-ricARCHmodels, see alsothe argumentsused inLumsdaine(1996,Lemma5)and RobinsonandZaffaroni

(2002,Lemma

9).ASSUMPTIONA3: Theoperator7-H,fulfills thefollowing continuitycondition

for 0, H'E O':supi,lml2<l 1im - 0'm12 -- Ofor110- 0'11-? 0.

This condition is straightforwardto verify. We now argue that because of

AssumptionsA2 andA3, for a constant 0 < y < 1,

(13) supA,1 < y.0Oe

Toprovethis note that for 0 E 0 and m e Mc with Ilmll2= 1,

-oc 2-

0 < E E j(0)m(yt_j)- j=l -

rc= Xo m2(x)po(x)dx

/c

+xoJ m(x)m(y) q(0)po,k(x,y) dxdy

c c

Ikl>l

= m2(x)po(x) dx- X, m(x)Hem(x)po(x) dx,-c c

778

8/7/2019 Estimating Semi Parametric

http://slidepdf.com/reader/full/estimating-semi-parametric 10/67

SEMIPARAMETRIC ARCH(oo) MODELS

where Xo= qij2 (0) is a positive constant dependingon 0. For eigenfunc-tions m E MA of 'e with eigenvalue A this shows that f m2(x)po(x)dx -

Af m2(x)po(x)dx > 0. Therefore

AO,j< 1 for 0 E 0 and

j> 1.

Now,because

of AssumptionA3 andcompactnessof 0, this implies (13).From (13) we get that I- 'Ho has eigenvalues bounded from below by

1 - y > 0. Therefore I - 7H is strictlypositive definite and hence invertible,and (I - H0)-1has only positiveeigenvaluesthat are boundedby (1 - y)-1:

(14) sup 1(I-7-)-lm112 <(1 - y)-1.O0E,mEMc,1lmll21=

Therefore,we can directlysolve the integralequation (12) and write

(15) m= (I - o)- lm*

for each 0 E O. The representation(15) is fundamentalto our estimation strat-

egy, as ityields identificationof mo.Wenext discussa furtherpropertythat leads to an iterative solution method

rather than a direct inversion.If it holds that AO,I < 1, then mo= Ej= mJm

In this case the sequence of successiveapproximationsm[n = m*+ om[n-1]

n = 1, 2,..., converges in norm geometricallyfast to me from any starting

point. This sort of propertyhas been established in other related problems-see Hastie and Tibshirani(1990) for discussion-and is the basis of most es-timation algorithmsin this area.Unfortunately,the conditions that guaranteeconvergenceof the successiveapproximationsmethod are not likelyto be sat-isfied here even in the special case that fj(0) = Oj-1. The reason is that theunit functionis alwaysan eigenfunctionof 0Hwith eigenvalue determinedby- "j=il 0ll = o. 1,whichimplies that A = -20/(1 - ). This is less than 1in absolute value only when 0 < 1/3. This implies that we will not be able touse directlythe particularlyconvenient method of successive approximations

(i.e., backfitting)for estimation:however,with some modifications it can be

applied;see Linton and Mammen(2003).

2.2. LikelihoodCharacterization

In thissectionwe providean alternativecharacterizationof mo,0 in termsofthe Gaussian likelihood. We use this characterizationlater to define the semi-

parametricefficiencybound for estimating 0 in the presence of unknownm.This characterizationis also importantfor robustnessreasons, since it doesnot requirefourthmoments on y,.

Supposethatmo(), 00aredefined asthe minimizersof the criterionfunction

(16) (0, m) =E log -,2(0,m)+ yto'2(0, m)

779

8/7/2019 Estimating Semi Parametric

http://slidepdf.com/reader/full/estimating-semi-parametric 11/67

0. LINTONAND E. MAMMEN

with respect to both 0, m(.), where o-2(0, m) = tt + Ej=I jj(0)m(y,_j). No-tice that this criterionis well defined in many cases where the quadraticloss

function is not.Minimizing(16) with respect to m for each given 0 yields the first-order

condition,which is a nonlinearintegral equationin m:

00

(17) L j(0)E[t4,-4(, m){y2 - o('0, m)}\yt= ] = 0.

j=l

Thisequationis difficultto workwith from the pointof view of statisticalanaly-sis because of the nonlinearity;see Horowitz and Mammen (2002). We con-

sider insteada linearizedversion of this equation.Suppose that we have someinitialapproximationto o-2.Then linearizing(17) about o-2,we obtain the lin-ear integral equation

(18) mo= mo+ HHmo;

* 1qjj ( O)ga(y)m?=y j;r_ 02(0)g1 (y)

= oo oo

o (x,Y cIjxy)-)W O-= ~ 71=1+J'qj(r0) i (0)gej(X,Y)Po(Y)po(x)

N0(x, y) = ocL~xqf2(0)gb(y)

Here, gJ(y) = E[ t-4 lyt_j = y] = E[- -2yt_j = Y], gb(Y) = E[ t4lyt_j = Y],

and g j(x, y) = E[oa-4lyt_l= x, yt_j= y]. This is a second kind linear integral

equation in me(.) but with a different intercept and operatorfrom (12). SeeHastie and Tibshirani(1990, Section 6.5) for a similar calculation.Under our

assumptions,see B4, the weighted operatorsatisfiesAssumptionsAl and A3also.For a proofof AssumptionA3 note that 0 < E[ot-4YE/ qJ(O)m(yt-j)]2.

Note thatin generalm0differs frommo,since theyare defined as minimizersof different criteria.However, for the strong and semistrongversions of ourmodel we get m,0 = miO.

3. ESTIMATION

We shall construct estimates of 0 and m from a sample {Yi, ..., Tr}.We pro-ceed in four steps. First,for each given 0 we computeestimatesof m0and7-o,and then estimate mo by solving an empiricalversion of the integral equa-tion

(12).We then estimate 0

by minimizinga

profileleast

squarescriterion.

We then use the estimated parameter to give an estimator of m(.). Finally,we use our consistentestimatorsto define likelihood-basedestimatorsthat im-

prove efficiencyunder some conditions. In particular,we solve an empiricalversion of the linearized likelihood implied integral equation (18) and then

780

8/7/2019 Estimating Semi Parametric

http://slidepdf.com/reader/full/estimating-semi-parametric 12/67

SEMIPARAMETRICARCH(oo) MODELS

minimize a negative quasi-likelihoodcriterionto update the parameteresti-mate. In Section 3.1we discusshowto computem; andHe,whilein Section 3.2

we state our estimationalgorithm;in Section 3.3 we give furtherdetails aboutsolvingintegralequationsof this type.

3.1. OurEstimatorsof m, andHe

We now definelocalpolynomial-basedestimatesm'iof m*andkerneldensityestimates -Heof -H, respectively.Local linearestimation is a popularapproachfor estimatingvarious conditional expectationswith nice properties (see Fan

(1992)). Define the estimator j(y) = a, where (,..., , p) are the minimizers

of the weighted sums of squarescriterion

E ({y-_ t - ao - al (Yt- - y) - ** -ap(yt_

-y)p}2

t: 1<t-j<T

x Kh(yt-j -Y)

with respect to (ao,..., ap), where K is a symmetric probability densityfunction, h is a positive bandwidth,and Kh(') = K(./h)/h. We can allowh = hT(y), but for notational and theoretical simplicitywe shall drop the de-

pendence on y. Our theoretical properties are stated for the case p = 1, butthe theoryeasilyextends;in practiceother choices mayhavesome advantages.

Select a truncation sequence TT with 1 < TT< T and compute mi*(y)=

ETj1 t5 (0)g(y) for any Iyl< c. Toestimate 'H we take the scheme

?TT

NR0(y,)- r(P) io,A(y,x)oPoy xPo-(x)?1

Poj(Y,x) =T- jl -Kh(y-yt)Kh(x- t+) andt: <t-j<T

1

po(X)= EKh(x-

Yt).t=1

The action of the empiricaloperatoris defined as -om = fc 7o((y, x)m(x) x

p0(x) dx. For each 0 e 0, 0H is a self-adjointlinear operator on the Hilbert

space of functions m that are defined on [-c, c] with norm IImI2 = fCc m(x)2 x

po(x) dx.Suppose that the sequence {t2, t = 1,..., T} and 0 are given. Then de-

fineg() to be the local linear smooth of t 472 on Yt-j,let g(.) be the locallinear smooth of t-4 on Yt-j,andlet g,j(-) be the bivariatelocal linear smooth

781

8/7/2019 Estimating Semi Parametric

http://slidepdf.com/reader/full/estimating-semi-parametric 13/67

O. LINTON AND E. MAMMEN

of ,-4 on (Yt-l,Yt-j). Then define

.,)m? ( - j 2(O))g((y)

ST7Tt1() j(Y) lC(0)gi O(X,Y)-(x)

n9mo~(Xy)TT=( y(y)

3.2. OurEstimatorsof 0 and m

Here we give a formal definitionof our estimators.

STEP1:Define mi(') asany sequenceof randomfunctions defined on [-c, c]that approximatelysolves miO= mi + Hoee. Specifically,we shall assume that

mi is anysequence of functions that satisfies

(19) sup I(I- o)mio(y) - m(y)l = op(T-1/2).OeO,yE[-c,c

This step is the most difficultandrequiresa numberof choices. In practice,wesolve the integralequationon a finitegridof points,whichreducesit to a largelinearsystem.

STEP2: Choose 0 e O to be any sequence suchthat

ST(0) <argminST(0) + op(T-12), where0EO

1T

ST(0) = T {y - at (0)1\2

t=l

'2(0 _T1)T ^2(A\-- m2 -&2 in{tTT t-1,where o2(0) T-1 y2 ando -2(0) = max{tt+ .1= qj(0)o(y-), E},t = 2,..., T. Here, E is a smallnonnegativenumber introducedto ensure that

at2(0) > 0.5 When 0 is scalar this optimization can be done by grid search.Otherwiseit maybe desirable to use some derivative-basedoptimizationalgo-rithm like Newton-Raphson or its variants,which would requireanalyticalornumericalderivativesof ST(0).

STEP3: Define for any y E [-c, c] and t > 2,

m(y) = im(y),

5Note that in smallsampleswe canfindm&(y)< 0 for some y, even if mi*(y)> 0 for all y and

)foq(x,y) > 0 for all x, y. One canreplacemoi(y)bya trimmedversion to ensureitspositivity.

782

8/7/2019 Estimating Semi Parametric

http://slidepdf.com/reader/full/estimating-semi-parametric 14/67

SEMIPARAMETRICARCH(co) MODELS

=mxI( min{t-1,aT-} -

of2= maxAt /+ E j(0)mo(yt-j), e ,j=1

and o2(0) T-1 t=l1y. The estimates (m(.), 0) are our proposal for theweak versionof our model. For the semistrongandstrongversionof the modelthe following updatesof the estimatemay yield improvements.

STEP 4: Given (0, (.)). Compute m; and 'Housing the sequence {ft,t = 1,..., T} definedin Step 3. Then solve the linearintegralequation

(20) mO= m?+ -tiiem

for the estimator mi and let a2(0) = max{utt+ ET1 qj(0)mo(yt-j),E},t = 2,..., T, for each 0. Define 0 e 0 to be anysequence such that

?T(0) < argminer(0) + o(T-1/2), where0Oe

fT(O) = y log 2(0)t + )

To avoida globalsearchwe supposethat 0 is the locationof the local minimumof ?T(0) with smallest distance to 0. Let m(y) = -m(y) and ,2= max{ltt +

yjTi1 tj(0)m(yt,_j), , t = 2,..., T.

These calculationsmaybe iteratedfor numericalimprovements.Step 4 canbe interpretedas a version of Fisherscoring,discussedinHastie andTibshirani

(1990, Section 6.2).

3.3. Solutionof IntegralEquations

There aremanyapproachesto computingthe solutions of integralequations.Rust (2000) gives a nice discussion about solution methods for a more generalclass of problems,withemphasison the high-dimensionalstate. The two issues

are how to approximatethe integral in 7-Iemand how to solve the resultinglinearsystem.

For any integrable function f on [-c,c] define J(f) = fScf(t)dt. Let

{tj,, j = 1, ..., n} be some grid of points in [-c, c] and let wj,, be some weightswith n a chosen integer.A valid integrationrule wouldsatisfyJn(f) -- J(f) asn - oc, where J,(f) = Y' Wj,n,f(tj,n). Simpson's rule and Gaussian quadra-

ture both satisfythis for smooth f. Now approximate(19) byn

(21) om(x) = m(x) + wj,nHO(x, tj,n)me(tj,n)po(tj,n).j=l

783

8/7/2019 Estimating Semi Parametric

http://slidepdf.com/reader/full/estimating-semi-parametric 15/67

O. LINTON AND E. MAMMEN

In solvability,this is equivalentto the linearsystem(Atkinson(1976))

n

(22) m^(tin) = im(ti,n) + E Wj,n(ti,n, tj,n)Rm(tj, n)po(tj,n)

j=l

(i= 1,..., n).

Toeach solution of (22) there is a unique correspondingsolution of (21) with

which it agrees at the node points. The solution of the system (22) convergesin L2(p) to the solution of (19) as n -- oc, at a rate determinedpartlyby the

smoothnessof He. The linearsystem (22) canbe writtenin matrixnotation

(23) (I, - Ho)m = m*,

where In is the n x n identity, mi = (mo(t1,),..., mi(t,n,)), and mi =

(m*i,,..., m*(t,,))T, while

H w E ,*? ) P0, (ti

n,tj,n)

m.?-(t ,,) pPo(t,,)

is an n x n matrix. We then find the solution values mi = (i(tl,,),...,i(tn,n))T to this system (23). Note that once we have found m0(tj,,), j=

1,..., n, we can substitutebackinto (21) to obtain mi(x) for any x E [-c, c],which is called Nystrom interpolation. More sophisticatedmethods also in-

volve adaptiveselection of the gridsize n andthe weightingscheme {wj,,, tj,n}.Therearetwomainclassesof methodsforsolvinglargelinearsystems:direct

methods,includingCholeskydecompositionor straightinversion,anditerative

methods. Direct methodswork fine so long as n is only moderate, say up to

n =1000; we have used directcomputationof mo= (I, - H0)-lm in our nu-

mericalworkbelow. Forlargergridsizes, iterativemethodsare indispensable.In LintonandMammen(2003) we describevariousiterativeapproaches.

4. ASYMPTOTICPROPERTIES

4.1. RegularityConditions

We will discussproperties of the estimates mihand 0 firstunder the weak

form model wherewe do not assumethat (4) holds but where Oo,moare de-

fined as the minimizersof the least squarescriterionfunction(5). Asymptotics

form = iaMandfor the likelihoodcorrectedestimatesm and 0will be discussedunder the more restrictivesetting that (4) holds. Note that as usual our regu-

larityconditionsarenot necessary,only sufficient,andourmethod is expectedto work well undermore generalcircumstances.

784

8/7/2019 Estimating Semi Parametric

http://slidepdf.com/reader/full/estimating-semi-parametric 16/67

SEMIPARAMETRICARCH(oo) MODELS

Define r,, = y2+j E(yt2+jyt)and ,t(0) = mo(yt+j) - E[mo(yt+j)lyt], and let

(24) =EL(0)ui j,t and = - J(0 ()j=1j=1l

where Jt(0), +,(0) were defined below (10). Let a(k) be the strong mixingcoefficient of {Yt}defined as a(k) =

supAFoB,,o c IP(A n B) - P(A)P(B)I,

where bais the sigmaalgebraof eventsgenerated by {ytb.

B1: Theprocess {y,}t_o is stationary with absolutely continuous density po,and a-mixing with a mixing coefficient a(k) such thatfor some C > 0 and some

large So,a(k) < Ck-so.B2: The expectation E(lytl2P) < oo for some p > 2.

B3: The kernel function is a symmetric probability density function with

bounded support such thatfor some constant C, IK(u) - K(v)l < Clu - vl. De-

fine fpj(K)= f ujK(u) du and vj(K) = f ujK2(u)du.B4: The function m together with the densities (marginal and joint) m(.),

po(.), and po,j(-) are continuous and twice continuously differentiable over

[-c, c], and are uniformlybounded. The density po(') is bounded awayfrom zero

on [-c, c], i.e., inf_cw<,cpo(w) > O.Furthermore,for a constant c, > 0 we have

that a.s.

(25) o2 > c,.

B5: Thedensityfunction Aof (ri o, 0o)is Lipschitzcontinuouson its do-main.

B6: Thejoint densities Ao,j j = 1, 2, ..., of((rq,o, ro,o),(ro)i, 7 ,j)) are uni-

formly bounded.

B7: The parameter space 0 is a compact subset of RP and the value 0ois an interior point of 0. Also, Assumption A2 holds and for any e > 0,

infIlo_Oo,I>ES(0, m) > S(0o, moo).B8: The truncation sequence TT satisfies TT = Clog T for some constant C.

B9: The bandwidth sequence h(T) satisfies h(T) = y(T)T-1/5 with y(T)bounded away from zero and infinity.

B10: The coefficients satisfy supoEok=0,1,2 IIkld (0)/(d0kll CiJ for some

f < 1 and somefiniteconstantC, whileinf0oe ij l 12(0) > 0.

The following assumption will be used when we make asymptotics under the

assumption of (4).

Bll: The semistrong model assumption (4) holds, so that the variables

77t= y2- a2 form a stationary ergodic martingaledifferencesequence with respect

to Ft-,. Let Et = yt/ot and Ut= (y2 - ct2)/ot2, whichare also bothstationary er-

godic martingale difference sequences.

785

8/7/2019 Estimating Semi Parametric

http://slidepdf.com/reader/full/estimating-semi-parametric 17/67

O. LINTON AND E. MAMMEN

Note that B1-B11 implyAssumption A1-A3. Condition B1 is quite weak,

althoughthe value of socan be quite large dependingon the value of p given

in B2. Carrascoand Chen (2002) provide some general conditions for a classof strongGARCH(1, 1)-type processesto be stronglystationary,to havefinite

p moments,and to be exponentially/3-mixing(whichimplies a-mixing);these

conditions involve restrictionson the function mo and on the distributionof

the innovations,in additionto restrictionson the parametersof the process.

MasryandTj0stheim(1995, Lemma3.1) also providesconditionson finite or-

der but "nonparametric"processes that imply geometric strong mixing.6We

will make use of the mixing propertyto applythe exponential inequalityof

Bosq (1998) and to establisha centrallimit theorem for me in the weak form

case. In this weak form case we cannotapplymartingalelimit

theory.We need

to applyacentrallimit theoremto (local) averagesof theprocessesr1 and772

definedin (24). These processesneed not be mixingbut arenearepoch depen-dent processeson the a-mixingbases y2 or mo(yt) (see Hansen (1991) for dis-

cussion) with exponentiallydecliningweights under our conditionson fj(0);we applya centrallimit theorem (CLT)due to Lu (2001) for suchprocesses.

The momentconditionB2 on Ytmay appearquite strong:it is commonprac-tice now in the parametricliteratureto not assume any moments for Ytbut

to make assumptionson the rescaled error E = yt/ot; see Lee and Hansen

(1994).This is because in

manyfinancial data sets there is evidence that the

tails preclude fourth moments from existing.Note howeverthat althoughwe

assume more than four moments in B2 and in defining (5), the moment con-

ditions (7) and (8) arewell definedunderonly second moments, and so some

results like consistencywill hold under less moments. Indeed, the results for

likelihood-basedestimatorsonly requirethis condition because it provides a

consistent initial estimator;if one is willing to assumethe existence of a con-

sistent estimator(withsome rate) like in Horowitz and Mammen(2002), the

distributiontheory should follow throughwithout moments on y. Bollerslev

(1986) showed that in the strongGARCH(1, 1) model with st - N(0, 1), it is

necessaryand sufficientfor E(y4) < oo that 2y2+ (y + /3)2< 1. Thusonly lim-ited dynamics(/3, y) are consistentwith fourthmomentsin thismodel. Because

we havefreed up the shapeof m, this problemdoes not arisein our model. In

principle,anyvalue of the dynamicparameter0 is consistentwith p moments

existingprovidedthe tails of m increaseonly slowly.ConditionsB3 andB4 arequite standardassumptionsin the nonparametric

regressionliterature.Under the assumptionof (4), the bound (25) follows ifwe assume that inf_c<w<m(w) > -

supt,.0 // J Ij(O).Conditions B5 and B6 are used to apply the central limit theorem of Lu

(2001) for NED processesover an a-mixingbase.

6These include restrictions on the tail of the conditional moments, for example, that

liml1(yI ... ,)l12o var(ytlyIYt = yl,... , Yt-d = Yd)/l(YI, ***, Yd)112< C < 0.

786

8/7/2019 Estimating Semi Parametric

http://slidepdf.com/reader/full/estimating-semi-parametric 18/67

SEMIPARAMETRICARCH(oo) MODELS

InB7we explicitlyassumethe identificationof the parametricpart.We makethis high level assumptionfor three reasons. First, we need identificationin

theweakARCH(oo) case, and this seems like a naturalassumptionto makeinview of our definition of the processthrough(5). Second,we allow the coeffi-cients ?qj(0)to dependon 0 in a complicatedway.Third,the mapping0 - mo

maybe quite complicatedto analyze.Hannan(1973)used highlevel conditions

(cf. his condition (4)) similar to ours. In special parametricARCH models ithas been possibleto workfrommoreprimitiveconditions:see Lee and Hansen

(1994) and Lumsdaine(1996) for the GARCH(1, 1) model, and Robinson andZaffaroni(2002) for a parametricARCH(oo) model.

The distributiontheory for parametricGARCH(1, 1) models has only re-

cently been established.Lumsdaine

(1996)established the

consistencyand

asymptoticnormalityof the quasi-maximumlikelihood estimator in a strongform model, while Lee and Hansen (1994) established the same results butfor semistrongform case, i.e., they allowed for martingaledifference errors.Both authors make use of ergodicityin theirconsistencyproof andmartingalecentrallimittheoremsin the asymptoticnormality.The distributiontheoryforweakform GARCHprocesseshas not yet been workedout, to ourknowledge.

The truncation rate assumed in B8 can be weakened at the expense ofmore detailed argumentation.In B9 we are anticipatinga rate of convergenceof T-215 for

mi,which is consistentwith second-ordersmoothnesson the data

distribution.AssumptionB10is used for avarietyof arguments;it can be weak-ened in some cases, but again at some cost. It is consistent with the GARCHcase where ij(0) = Oj-1and dkq j(0)/90k = (j 1) ... (j - k)j-k-1.

The assumptionwe made in Section 2.1 about the fixed truncation c canalso be weakened to allow c = c(T) -> oo as T -- oc, and we discuss this issue

below.

4.2. Propertiesof moand 0

We establish the properties of mi for all 0 E 0 under the weak form as-

sumption.Specifically,we do not requirethat (3) holds, but define mo as theminimizerof (5) over Mc.

Define the functions gi (y), j = 1, 2, as solutions to the integral equations

Pi~= i'"(y) + 'ePJ, in which (with V2= (92/dx2) + 2(d2/xSdy) + d2/oy2)

r*'1) = (y)= and

?00 , If( \

gPo(y)=

y =Y)fi0'2(y)-= 0Lf(0)' E(mo(yt+j)lyt- y)

- [V2pO,j(y,x)] o( dxpo(Y)-f^p^y^ ^ ~~dr

.

787

8/7/2019 Estimating Semi Parametric

http://slidepdf.com/reader/full/estimating-semi-parametric 19/67

0. LINTONAND E. MAMMEN

Then define /-L(y) = - L q1 (O)E[m0(yt+j)Iyt= y] and,j=? i<>E"(t+)y =y n

vo(K) 1&MY= o(){var[r1,t+ijo t]+ I4(y)} andI p () p )]

Po(Y) ,~ ~~I

bo(y) = 2-A2(K)[/3R(y) --

where r-q, ] = 1, 2, were defined in (24). We prove the following theorem inthe Appendix.

THEOREM1: Suppose that Bi-BIO hold. Thenfor each 6 c 0 and y E [-c, c],

(26) N/ThUiio(y) - m0(y) - h2bo(y)] ==i N(O, wo(y)),

and 6i6(y) and Mi'i(y')are asymptotically independent when y 4 y'. Furthermore,

(27) sup iio(y) - mo(y)l = o(T1/4,OEO,Iyl<c

(28) sup [at7( )_- t7(O) = op(T 1/4)

0eO,7TT<t<T

da2 d

0214)(29) sup t(o) t(O) = op(T14)-

OGO,TT<t<T d6 d8

Both the bias and the variance in this result are quite complicated even

though a local linear smoother has been used in estimating gj.From Theorem 1 we obtain the properties of 0 by an application of the as-

ymptotic theory for semiparametric profiled estimators; see Severini and Wong(1992) and Newey (1994). This requires a uniform expansion for 1h6(y) and forthe derivatives (with respect to 6) of Fi0(y).

THEOREM2: Suppose that Bi-BlO hold except that in B2 we require p > 4.

Then N/T(O- 00) = O (1).

In Theorem 2 we require stronger moment conditions for the root-T consis-

tency of 0 than for the s/Th consistency of mii(y). By using the quasi-likelihoodcriterion these moment conditions can be reduced to p > 2. These results canbe applied to get the asymptotic distribution of Mi= mi'. Define

(vo(K)L711frq(O)E[y2 - t2)21yt_j=

y](30) oi(y)j=

po(y>[[ 1:1

j1 02r/I /

) ]2

Iy +( p'o d

b(y) = ,tt(K) !mf(y) + (I - 7H)o1 E!(F-(om) (y)2 -pody

788

8/7/2019 Estimating Semi Parametric

http://slidepdf.com/reader/full/estimating-semi-parametric 20/67

SEMIPARAMETRICARCH(oc) MODELS

THEOREM3: Supposethat B1-B10 hold and that 0 is an arbitraryestimate

(possiblydifferentfromthe abovedefinition)with ,/T(0- 0o)= Op(1). Thenfor

y E [-c, c],

(31) -/T-h[m (y) - m0(y)] = op(l)

and m'i(y) and mi(y') are asymptoticallyindependentwhen y =y'. Undertheadditionalassumptionof B11 wegetthat

(32) dTh[mi(y) - mo0(y) - h2b(y)] =- N(0, w(y)).

Theasymptotic

variance has contributionsfrom the estimation of m* andfrom the estimationof Howhich combine to give a nice simple formula. Thebias of m is rather complicated and it contains a term that depends on the

density po of y,. We now introducea modificationof m that has a simplerbias

expansion.For 0 E 0 the modified estimate .mod is defined as any (approxi-

mate) solution of mmod = Im + mod ,od where the operator -m?dis defined

byuse of modifiedkerneldensityestimates

?TT -y'modf7'modoj (y, x)od(Y, x)= - y f,?0)

?

f11?d (Y) )po (X)'

p^od(y, x)= p^o,j(x, y)

+ 0o(x) 1p"(x) T- Xl-l yK(y(t

-y )Kh(Yt-y) + )

pd(x) (X) + p"~(x) iTvAT Ppoy(X)=p+o() T E(yt - y)Kh(Yt - y).po(x t=l

In the definition of the modified kernel density estimates Apcould be re-

placed by another estimate of the derivativeof po that is uniformlyconsistent

on [-c, c], e.g., T-1 T=l(Yt - y)Kh(Yt - y)/[h2tA2(K)]. The asymptotic distri-

bution of the modified estimate is stated in the next theorem.

THEOREM4: Suppose that B1-B11 hold and that 0 is an estimateas in

Theorem 3. Then for y E [-c, c], x/Th[mo?d(y)- moo(y)

- h2bm?d(y)]=

N(0, w(y)), where w(y) is defined as in Theorem3 and where bm?d(y)=

bL2(K)m"(y)/2.

This bias has a particularlyappealingform since it is the bias that would re-sult were m(.) a one-dimensionalregressionfunctionand the estimatora locallinear kernelsmoother.Hence, this estimatoris design adaptive (Fan(1992)).

789

8/7/2019 Estimating Semi Parametric

http://slidepdf.com/reader/full/estimating-semi-parametric 21/67

O. LINTON AND E. MAMMEN

4.3. Propertiesof m and 0

We now assume that 0 is consistent and so we can confine ourselves to

workingin a small neighborhoodof 00,and our results will be stated only forsuch 0. We shall now assumethat (4) holds, so that the variables7rt= y2 - aform a martingale difference sequence with respect to t-i. Let ?t = Yt/ltandut= (y2- 2)/It2 = 82 - 1,whichare also both martingaledifferencese-

quencesby assumption.Define

ff 1 vo(K) E- I2(0Oo)E(t-4t lYt-j = Y)weff (y) =

I

po(Y) [EjI ](00)E(T-4]t-j = y)]2

Note that ceff(y) can exist even when the fourthmomentsof ytdo not exist.

THEOREM5: SupposethatB1-B11 hold.Then,forsome boundedcontinuous

function beff(y) we have -Th[mi(y) - mn(y) - h2beff(y)] == N(0, oeff(y)).

The next theorem gives the asymptoticdistributionof 0. Define the "leastfavorable" process 2o(0) = t + EJ= 1 fj(0)m0(yt_j), where me(') was defined

below (18). Define also

d I O2 d2 2a,..E(.4d-5to~ u~-

2

-

J=E(to- Oa 0t(0?)) and I= var o-2ut

t(00) .

THEOREM6: SupposethatB1-B11 hold. ThenV/T(0- 0o) >N(O, J-1 xJ,-1).

The result permits inference robust to higher-ordermoment variation anddistributionalshape. Consistent standard errors can be obtained by the for-

mula

= E O't-4

8 T() and I=o't4t U

t= t t=

wherehatsdenote estimatedquantities.We show in the next sectionthat whenthe rescaled errors are Gaussian, the semiparametricefficiencybound for 0is 27-1, andthat our estimatorachievesthis bound.

4.4. SemiparametricEfficiencyWe next investigate the semiparametricefficiency question, confining our

attention to the strongform model where St is i.i.d. and in fact standardnormal. Our approach to this is heuristic, but is founded on the work of

790

8/7/2019 Estimating Semi Parametric

http://slidepdf.com/reader/full/estimating-semi-parametric 22/67

SEMIPARAMETRICARCH(oo) MODELS

Bickel, Klaassen,Ritov, and Wellner(1993) and Newey (1990) for i.i.d. data.There has been some previouswork on semiparametricefficiency in related

semiparametricARCH models. Engle and Gonzalez-Rivera (1991) consid-ered a semiparametricmodel with a standardGARCH(1, 1) specificationforthe conditionalvariance,but allowedthe errordistributionto be of unknownfunctional form. They suggested a semiparametricestimator of the variance

parametersbasedon splines.Linton(1993) examinedthe Engle andGonzalez-Rivera (1991) model and proved that a kernelversion of their procedurewas

semiparametricallyefficient and even adaptivein the ARCH(p) model whenthe error distributionwas symmetricabout zero. Drost and Klaassen (1997)extended this work to consider GARCH structuresand asymmetricdistribu-tions: they compute the semiparametricefficiencybound for a general class

of models.We will represent our semiparametric model by Po,m= {Po,m},where Po,m is

the probabilitydistributionof the processwith parameters0, m(.). Now sup-pose that m is a known functionbut 0 is unknown,inwhichcase we havea spe-cificparametricmodel, denoted P0= {Pe},whereP0C Po,m.The log-likelihoodfunction is proportional to eT(0) = tEt=1 logs2(O) + yt2/l(0), wherest(0) =

il ji(0)m(y,t_j) The score function withrespect to 0 is

deT(0) 1 Tdlog s(0)

6 -Lu(?6) 86t=l

1T=2Eu,(0) 2() L (0)m(yt-j)

t=l t j=1

where ut(0) = (y2/s2(6) - 1) and fj(0) = doij(0)/60. The Cramer-Rao lower

bound in the model Po is then -01 = 2(E[[d og2d ]-1, since E(u2) = 2.d ([ T1])-1,

since E(ut) = 2.

Suppose that we parameterize m by a scalar rj and write m,, so that we

have a parametric model Po,, = {Pe,,}, where Po,7 c PO,m. For simplicity wejust assumetemporarilythat 0 is also a scalar.The score withrespectto r1is

fTA(0, T}) 1 aT 0log(t2(0,7r)

1 =-ut m ) d(

t=2 (0, = d77

The efficient score function do*(0, r7)/d8 is the projection of XTr(0, r))/90onto the orthocomplement of span[dfT(0,7))/d7/] in Po,7,where span[l] de-notes the linear subspace generated by the given element. It follows thatd(e(0, 7)130d is a linear combination of deT(0, rn)/0 and drT(0, rl)/ld

791

8/7/2019 Estimating Semi Parametric

http://slidepdf.com/reader/full/estimating-semi-parametric 23/67

O. LINTON AND E. MAMMEN

and has variance (called the efficient information) less than the varianceof dTr(0, r)/o0; this reflects the cost of estimatingthe nuisanceparameter.

Now consider the semiparametricmodel Po,m. We compute the efficientscore functions for all such parameterizationsof m, and find the worst suchcase. Because of the definition of the process o-2,the set of all possible scorefunctionswith respectto parametersof m at the trueparameters00is

Sm=ut~L2 j(0o)g(tij): g measurable .

t=l 0'-j=l

To find the efficient score function in the semiparametricmodel, we find the

projectionof drT(0o, m)/0Oonto the orthocomplementof Sm.We seek a func-tion gothatminimizes

j(33) E| d QEj(0o)g(Yt-j)ue st =1 J -

over all measurable g. This minimizationproblem is similar to that which

monsolves. We show that go satisfies the linear integral equation (see the Ap-

pendixfor details)

(34) go = g* + '0g0o,

where the operator Howas definedbelow (18), while

g*() dS2- 00

g*(y)== (0o)E =ydo S=y I_(o)E[ yt-j =Y].j1 t I =

Note that the integral equation (34) is similarto (18) except that the interceptfunction g* is different from m* ; it has solution go = (I - Ho0)-1g*. The im-

pliedpredictorof d log s2/O in (33) is st-2 J 1?j(Oo)go(yt-j),whichwe denote

byEm(dlog s2/10). The efficient score functionin the semiparametricmodel isthus

Tf(0o,m) 1 T- ~logst (dlog52f8 ~_ct'- 80

t8

=2 U 14 [tj(0o0)(I - I0O) m-t=l j=

- oj(0o)(I - Ho)-lg*](y,-7)

792

8/7/2019 Estimating Semi Parametric

http://slidepdf.com/reader/full/estimating-semi-parametric 24/67

SEMIPARAMETRIC ARCH(oo) MODELS

TT 100

=Eut2 E[(I- o)-Lt=l t j=l

x {*j(00)m0 - Ij(0o)g*}](yt-j).

By constructionde (0o, m)/8d is orthogonalto anyelement of S,. The semi-

parametricefficiency information bound is Z0 = var[dE(0oo,m)/0]. It fol-lows that any regular estimator of 0 in this semiparametricmodel has as-

ymptotic variance not less than ZO1. This bound is clearly larger than in

the parametricsubmodel where m is known. It can be easily checked that

dlog":/20 = dlogs2/dO - Em(dlogst2/d0) from which it follows that our es-

timatorachieves the bound.An alternativejustificationfor our claims comes fromworkingwith the least

favorable parametric submodel of P,m, which is {Po,,: m, = mo + 77g0,q E IR,0 E I P},where gois defined in (34). For this parametricmodel the asymptotic

(efficient) informationfor 0 is preciselyZ0. Since our estimator,which does

not use this parametricstructure,has the asymptoticvarianceZ 1,it mustbe

semiparametricallyefficient.We have taken a constructiveapproachto finding the information bound

and we acknowledgethatmore workis needed to make this rigorous.Perhapsthis couldbe done alongthe lines of Drost andKlaassen(1997).

4.5. NonparametricEfficiency

Here, we discussthe issue aboutefficiencyof the nonparametricestimators.

Ourdiscussionis confined to a special case of the strongmodel. In this case,

eff( - 1 (K4+ 2)vo(K)

oy Po(Y)E==2(0o)E(o- 4lyo= y)

where K4 is the excess kurtosisof et.Our discussionis heuristicand is confined to the comparisonof asymptotic

variances.This type of analysishas been carried out before in many separa-ble nonparametricmodels; see Linton (2000). The general idea is to set out a

standardof efficiency againstwhich to measure a given procedurealongwith

a strategyfor achievingefficiency.HorowitzandMammen(2002) applythis in

generalizedadditivemodels. In our model, there are some novel features due

to the presence of the infinitenumberof lags.Horowitz,Klemela, and Mammen(2002) establishthe minimaxsuperiority

of a local linearbackfittingestimatorin an additivenonparametricregressionmodel.

793

8/7/2019 Estimating Semi Parametric

http://slidepdf.com/reader/full/estimating-semi-parametric 25/67

O. LINTONAND E. MAMMEN

We firstcomparethe asymptoticvarianceof mi and mimodwith the varianceof an infeasibleestimator that is based on certainleast squarescriteria.Definefor each

j=

1, 2,...,

(35) Sj(A) = h K(y h - (A)]

where ot2(A) = L=,k Jk()k(m)m(yt-k) + fj(0)A, and let hj(y)= A, =

argmaxASj(A).This least squares estimator is infeasible since it requiresknowledge of m at {yt-k, k : j) points. We suppose without loss of general-itythat fj(0) > 0 for each j. It can then be shown that

VTh[Mfj(y) - m(y) - h2bj(y)]

tN(, (K4+ 2)vo(K)E((y2 - o-t)2Iyt_-= y)

=\ N(O'+ Ioj(0)po(y) J

for allj = 1, 2,... with some bounded continuousbias functionsbj(.). Further-

more, mj(y), Mk(y) with j]/ k are asymptoticallyindependent. Now definea class of estimators{ j wjnj: j Wj= 1}, each of whichwill satisfya similar

centrallimittheorem.The optimal (accordingto variance)linear combinationof these least squaresestimators satisfies

(36) /Thi[mip(y) - m(y) - h2b(y)]

>N(0vo0,

( pyPo(Y) Tj=l (0)[E((y2 -o2)21yt_j= y-l )

with some bias functionb(y). See Xiao, Linton, Carroll,and Mammen(2003).This is the best that one could do by this strategy;the question is, does ourestimatorachieve the same efficiency?

Define sj(y) = E(oa4u2ly,_j = y). By the Cauchy-Schwarz inequality,oo oc 1/2 1/2 1/2 -1/2 oo oc1 j= j j= l Yj Sj2 /2y)a 1( y ) < aj=1 sj(y) j= CajsJ (y), where

j = 2(0)/Lj1 j2 (0), which implies that Ej=1 ()sj(y)/(J=1 ())2 >

1/y- 1fj2(0)s-1 (y) with equality only when sj(y) does not depend on j.So our estimatorwith variance (30) would achieve the asymptotic efficiencybound (36) in the case of constant conditional variancessj(y). It is generallyinefficient when sj(y) are not constant.Because our estimator is motivatedbyan unweightedleast squarescriterion,it could not be expected that it correctsfor heteroscedasticity.We next turn to the likelihood criterion,which takesaccount of the heteroscedasticityin a naturalway.

Define analogouslyto (35) the (infeasible) local likelihoods

ej(A)= ETK( h logo'21(A)+j( Thh K pT;j U2-(A)+o', t)-

794

8/7/2019 Estimating Semi Parametric

http://slidepdf.com/reader/full/estimating-semi-parametric 26/67

SEMIPARAMETRICARCH(oo) MODELS

and let mi=k(y) = Aj= argmaxA 3j(A).It can be shown that

/Th[m-ik(y M(y)] (K4 + 2)vo(K)r/N[m2(y) --m(y)]t_N 0, 2

,

j\ V(0)p0(y)E(o.4\yt y )

for each j, and again jm'k(y), mk(y) with j 7Ak are asymptoticallyindepen-

dent. As before this suggests that any single ik(y) is inefficient and canbe improvedon by taking linear combinations.It can be shown that the op-timal linear combination of mik(y) has asymptoticvariance (K4 + 2)vo(K)/

(po(y Ej 22(O)E(t-4lyt_j= y)). This is preciselythe varianceachievedbyour

estimator in(y). In other words, our likelihood-basedestimator m((y) ap-

pearsto be as efficientas it canbe, at least underGaussianity.

5. MODELINGTHE TAILS

In this section we discusshow to select c and tu. A simple method is just toset c at some quantileof the empiricaldistributionof the data and let ,t= 0.This workswellwhen c is takenprettylargeand when the tails are not so influ-ential.This is the sortof trimmingthat one findsinmuchworkin econometrics.It may,however,be preferablein some cases to allow for a more sophisticated

tail model. Weproposebelow some more refined methodsand then give theo-reticalresultsaboutone of them.

5.1. EstimationMethod

We consider fits of the news impact curve that are of the following form.For Iyl< c the fit is a nonparametricsmoother miand for the tails Iyl> cit is chosen as a parametricfit /x(y;s). Here Lu(y;4) is a parametricmodel

dependingon a vector of unknownparameters6. We also write 1uC(y;4) for

the functionthat is equal to ,(y; s) for Iyl> c and vanishes for Iyl< c. Thenwe have the estimateof the volatility,

a2-= j(0 m),

where ot2(0, , m) =qij= j(0)[m(yt_j) + AC(yt_j; )] with parametric esti-

mates 0 and 5 and a smoothing estimate mithat vanishes for Iyl> c. This

generalizesour approachwherewe have chosen /x(y;5) = 0. Parametricspec-ificationsinclude Wu(y;s) = 61+ 62y2,whicheffectivelyimposes that the news

impactcurveis quadraticin the tails (as y-*

+oo).The

Engleand

Ng (1993)procedureassumeda lineartail (indeed, they assumedpiecewise linearevery-where).

The estimation strategy for this case is pretty much the same as in Sec-tion 3. For given 0 and s one can estimate mo., on [-c, c] by putting now

795

8/7/2019 Estimating Semi Parametric

http://slidepdf.com/reader/full/estimating-semi-parametric 27/67

0. LINTON AND E. MAMMEN

2 = y2 - t (0,(). To estimate 0 and (one maximizes the profiled least squarescriterionor the profiledlikelihood withrespectto this largerparametervector.

In practiceone has to choose c. One could treat c as an unknownparameterandtryto estimate it or one can select it on a pragmaticbasisby settingit to a

highempiricalquantile.The resultingestimate im(y)+ t,C(y; o)of the news impactcurve is discon-

tinuous at the point c. This can be repairedby calculatingthe estimates fora continuum(i.e., for a large number)of values of c andby takingan averageof these estimates.Another possibilitywould be to calculate the estimate fortwo values of c and to smoothly change from the first estimate to the secondone when going to ?oo. Some heuristics that support the second modification

of our estimatewill be givenbelow.

We also considera slightlydifferentapproachto explicit trimmingbased onvariable bandwidths.In this method one computes the standardestimators ofSection 3.2, but uses a variablebandwidthhT(y) in the local polynomialesti-mators of gj(-). If hT(y) -> o as lJy-> c, then the local polynomial estimates

of gj and hence m*become global polynomialsfor all y with IyI> c. Likewisethe estimatedoperator'Hbecomesproportionalto the identityoperatorin thetails. Therefore,we can expect the estimated m to be polynomialin the tails.This method therefore achievesa similarobjectiveto the explicit trimmingap-proach we described above, but it has a nice advantage:provided hT (y) is

continuous in y, the resultingestimatorof m will also be continuous.We usethis method in the simulationsbelow.

5.2. AsymptoticProperties

In this section we discuss the propertiesof the trimming-basedestimators.We focus on the case that c -- oo. The strategy is to analyze the corresponding

populationproblemfor givenc and then to let c -> oo. Wewill discuss this forthe weak formspecificationof ourARCH(oo) model.

We still suppose that Ytis a stationaryprocess. Define for fixed 0 the func-

tion mo,o as minimizer of E[{y2 - j=1 /j(0)m(yt_j)}2]. The best fit in thetrimmed model, with fixed c, is given by mo,c(y)+ ,tC(y; o,c), where m =

mo,c(y) and == ,c minimize E[{y2 - E j iyj(0)[m(y,_j) +?C(yt_j; )]}2] overall functionsm withsupport[-c, c] andover allparameters4. As above it canbe checked that for fixed 0 the best fit mo, is uniquelydeterminedbythe inte-

gral equations

me,c(y) = mo(y) +Ix 7o(y, x)LC(y; :o,c)po(x)

dx

c>_c

+ /Ho(y, x)mo,c(x)po(x) dx-c

for IyI< c, if c < oo, and mo,O(y) = m;(y) + f_ (oe(y,x)mo,o(x)po(x) dx forall y. The model bias, caused by trimming, is equal to mo,o(y) - mo,c(y). The

796

8/7/2019 Estimating Semi Parametric

http://slidepdf.com/reader/full/estimating-semi-parametric 28/67

SEMIPARAMETRICARCH(oo) MODELS

bias will depend on the choice of c and on how well mo,o is approximatedby,C(y; 5(,c) in the tails. The following theorem gives an estimate for the bias.

For the theoremwe need the following assumptionsthat are slightlystrongerthanAssumptionsA1-A3.

Cl: It holds that

sup po,(y,x)2 dxdy < oo,jAo - oo po(x)po(y)

supo x)

dxdy--0 for c -- o.j4o -o xI>cpo(x)po(y)

C2: Thereexistno 6 c 0 and nofunctionm withf? m2(x)po(x) dx =1 such

thatLj 1 j(i0)(m(yt-j)= 0 withprobability1.

C3: It holds that sup,,, j,_j(0) < oo, infELoj,>lj(0)2 > 0, and

sup0,,*:11-* l0o Ej> I j ( ) - ji(*)l-

0.

In particular, conditions C1 and C3 imply that sup0E f f_ -(y, )2 x

po(x)po(y) dx dy < oo. Note that this is strongerthanAssumptionAl, wherethe

integral onlyrunsover

[-c, c].THEOREM7: Supposethat C1-C3 hold. Thenfor some constantsC1,C2 > 0

(notdependingon c) itholds that

(37) J[mo,c - m0,](x)2po(x) dx < C1A(c)2,-c

(38) Imo,(y) - mo,o(y)l < C2po(y)zAo(c)for Iyl< c

with Ao(c)2 = flM,c[meo,(x) - t-c(x; o,c)]2po(x) dx and po(y)2 = f_o (y,

x)2po(x) dx.

ConditionCl canbe checked for transformedGaussianprocessesYt=G(xt),where x, is a stationaryGaussian process with variance 1 and autocorrela-tion function r(j). Then it holds with a constant C that po(y)2 < [(1 - 5)(1 +

8)]-1/2 exp[6(1 + S)-1G-l(y)2] with 8 = supj>1r(j)2. Then

_

f (y, x)2 x

po(x)po(y) dx dy = E[pe(yt)2]< o0. This discussion shows that Cl is fulfilledalso for heavytailed processes. ConditionCl only puts a condition on the de-

pendencestructureof the transformed

processxt = G-1(yt). It

requiresthat

the conditionalcorrelationof xt and Xs(given Ix Iis largerthan c) is bounded

awayfrom 1 or does not convergeto 1 too fast (for c -> oo).In this exampleit holds that po(c) -->oo for c -- o. Thus Theorem 7 does

not imply that mo,c(c)approximatesmo,X(c) if Ao(c) converges to zero too

797

8/7/2019 Estimating Semi Parametric

http://slidepdf.com/reader/full/estimating-semi-parametric 29/67

O. LINTONAND E. MAMMEN

slowly.This suggests to use mo,c(y)as an approximationof mo,o(y) only for

ljy <<c. For fixed y, mo,o(y) can be always approximatedby mo,c(y)with

c -> oo. This heuristicsalso supportsthe use of the second proposalof smoothtrimmingthatwe had discussed above.

Weconjecturethat conditionC1 also holds for (strong form) GARCH(1, 1)processes.Thisconjectureis supportedbyTheorem 2.3 of Mikoschand Starica

(2000). This theorem gives expansions for tail probabilities of (yt, yt+j) andof yt,and it suggeststhe approximationspoj(y, x) ((x2+ y2)-~-2f[(x, y)(x2 +y2)-1/2] and po(x) . Cx-K-1 for lxl and jyj large. Here, C is a constantand f is a function on the sphere. The constant K is determined by the

equation E(f3 + ye2)K/2 = 1. Plugging these approximations into the inte-

gral

f

f p2j(x, y)po(x)-1po(y)-~dx dy results in a finite

integral.This

suggeststhat Cl holds. For p2(c) we get an approximationthat is of order c-2. It followsthat in this case p2(c) ->f 0 for c -> ox.

We next provide results for a linear parametrization iu(y, s) = STv(y), wherev is a vector of known functions.For doing so we need slightly strongercon-ditions. In particular,smoothness conditions for the densities and regressionfunctions have to been stated for the whole real line.

C4: The trimmingthreshold c = cTconvergesto oofor T -- oo with CT< CTY

for constantsC, y > 0.

C5: It holds thatElytl2P< o fora constantp > 5/2.

ConditionC5is slightlystrongerthan B2. Note thatin the followingtheoremwe show a fasteruniform rate of convergence.

C6: Thefunction m togetherwiththedensitiespoand po,jare twicedifferen-tiable on (-oo, oo). Thefunctions po and po,j and theirderivatives are uniformlybounded on (-o0, oo). For Po it holds that po(x) > C'T-Y for Ixl < CTfor some

positiveconstantsC',y'. Thefunction m(x) and its derivativesare boundedfor

Ixl < CT byC"T'"forsomepositiveconstantsC",y".Furthermore,for a constantcw> 0 we have that ot2> c, (a.s.).

This conditionreplacesthe old condition B4.

C7: It holds thatEvj(x)IP < oofor a constantp > 5/2. Furthermoreit holdsthat the minimaleigenvalueof thematrixfx>c v(x)v(x)T po(x) dx is largerthan

C",,T-Y'for C",, y,, > 0.

Conditions C4-C7 hold for thestrong GARCH(1, 1) process

under someconditions on the dynamicparametersand the moments of the innovation.We now state our result that gives similarresults as Theorem 1. We do notconsider asymptoticnormalityat a fixedpointbecause nowwe are estimatinga functionin a growinginterval.

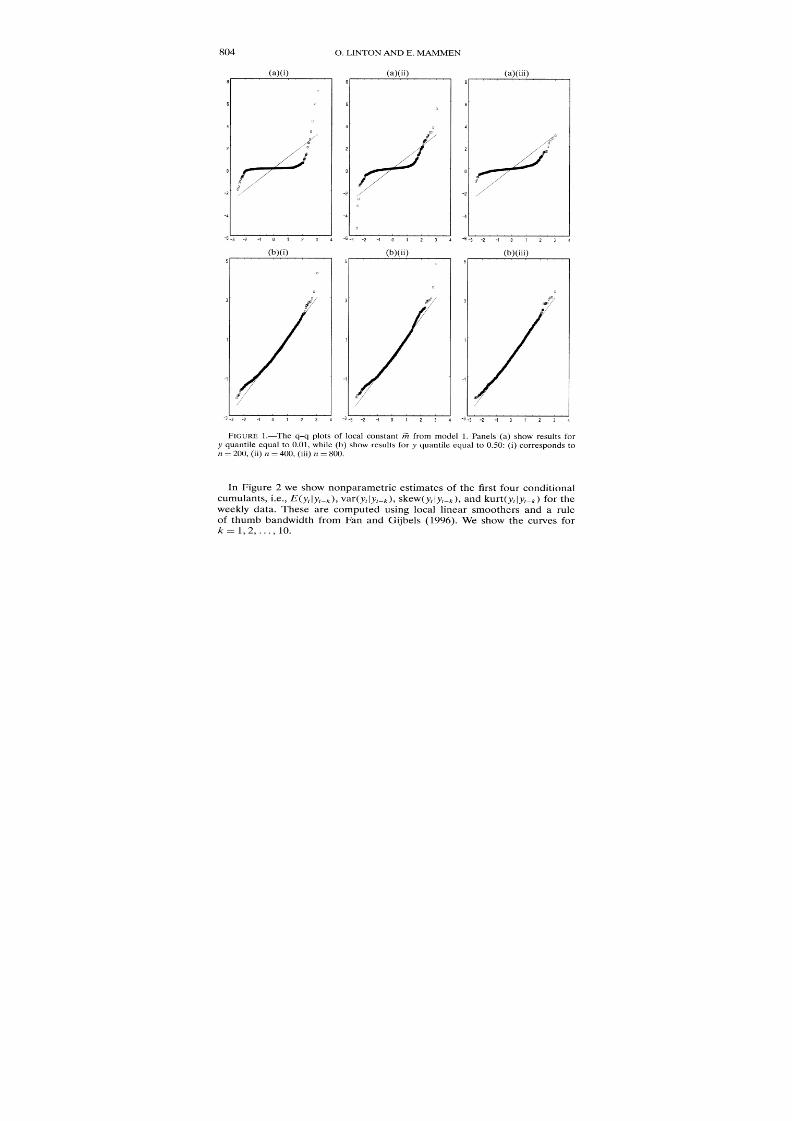

798

8/7/2019 Estimating Semi Parametric

http://slidepdf.com/reader/full/estimating-semi-parametric 30/67

8/7/2019 Estimating Semi Parametric

http://slidepdf.com/reader/full/estimating-semi-parametric 31/67

O. LINTONAND E. MAMMEN

a function that decreasesto zero rapidlyafter some thresholdCo.Specifically,7r(y) = 1 for all y with jly < Co< c, while rr(y) - 0 as Yl-C c. Note that as

lyI -C c, the bandwidthincreases to infinityand so the local polynomialesti-mate of E(y2ly,_j= y) becomes a globalpolynomial;thereforethis estimation

strategyforces mi(y)to have the samepolynomialshape in the tails.For the truncation parameter rT, we have chosen T to make

sup0o EOj=+1, j(0) < e for some smallprespecifiedtolerance level E.One canalso use some formal model selection techniquebut at computationalcost.

6.2. SimulatedData

Wereport

the results of a small simulationexperiment.

There are several

papers that provide simulation evidence on the finite sample performanceofGARCHquasimaximumlikelihood (and related) estimators(QMLE). A ma-

jor issue in these studies is the reliabilityof the results and their robustnessto alternativeimplementations.This is acknowledgedin most of the studieswe examined:e.g., Lumsdaine(1995) andFiorentini, Calzolari,and Pannatoni

(1996). Nonlinear estimators in nonconvex optimization problems can havea variety of problems. To some extent this is a problem with the nature of

large scale simulationsrather than with the estimator itself-when one runs

10,000replicationsof a procedure one is restricted to a relativelycrude im-

plementation,whereas for a single data set one can modify the procedureasrequiredfor thatparticularsample.However,there are also studies thatreportfindingsignificantlydifferentresultsfor a given single data set using differentcommercialsoftware;see Brooks, Burke,and Persand(2001) andMcCulloughandRenfro (1999).

The focus of our studyis on the news impactcurvem(.). In an earlier ver-sion of this paper,Linton and Mammen(2003), we reportresultsfor a designwhere 0was estimatedalongwith m(y) by choosing 0 from a gridof 100pointson (0, 1). The estimates of 0 were quitewell behaved even for relativelysmall

sample sizes. In parametricapplicationsone often finds estimates of 0 to bestrongly significant.The resultswe report here address the issue of how wellthe nonparametricestimate of the newsimpactcurvem performsin compari-son witha parametricmethod in a situation that is favorableto the parametricmethod.Specifically,we shall assume that 0 is knownin both procedures.

We considertwo sets of experiments.In the firstcase (model 1) we gener-ated data from (6), where Yt= stot and Etis standardnormal,with 0 = 0.45,y = 0.35, a = 0.20. These are the parametervalues chosen in Fiorentiniet al. (1996). In the second case (model 2) we consider Yt,et as above and

ot

=

0o-t2 +a+a

yyt2+

8y2In(yt-_<

0)with 0 =

0.9, y=

0.06,8 =

0.03and

a as before.For model 1,E(lyti8) < oc and so bothleast squaresand likelihoodestimates of the parametersare consistent and asymptoticallynormal,whilefor model 2 we have E(lytl4+E)< oc for some small e > 0 but E(lyIl8)= oc.

Althoughmodel 1 is far from the sortof model one encounterswithdailystock

800

8/7/2019 Estimating Semi Parametric

http://slidepdf.com/reader/full/estimating-semi-parametric 32/67

SEMIPARAMETRICARCH(oo) MODELS

return data, it is not a bad match for standardizedmonthlydata. Model 2 ismore realistic for dailydata and poses a challenge for the least squaresmeth-

ods because of the approximateviolation of ourregularityconditions. We con-sider T E {200,400, 800}.We investigate both least squares estimators mi(y) and likelihood estima-

tors m(y). In each case the intercept functions were estimated with local

constant, local linear, and local quadraticsmoothers with a Gaussian kernel.We chose throughoutn = 200 grid points equally spaced in quantile space.7We estimateon the entiresamplerangeof the data,8but use the variableband-width method (39) with the downweightingdescribeddirectlyafterwardwith

ir(y) = exp(-(lyl - 2)2) for lyI > 2. Although the estimates of m sometimes

takenegativevalues,

we do not trim them.To compare the performanceof the nonparametricestimators we need a

benchmark.Our benchmarkis the asymptoticvariancethat would applyto aGARCH maximumlikelihood estimator(MLE) (assuming 0 is known).Thisavoids the tricky implementation issues associated with these estimators asdiscussed above. It has to be noted that this sets a very high standard,sinceit is an infeasible estimator. The GARCH MLE of the news impact curve is

mLik(Y) = a + --y2, where (a, y) are the MLEs of (a, y). The asymptoticvari-anceof mLik(y) is VLik(Y)= (O'aa + Jyyy4 + 2a,yy2)/ T, whereoaa, -y,,andaare the correspondingasymptoticvariancesand covariancesof the parameterestimates.WecomputevLik(Y) by simulationto three decimalplace accuracy.

We present in TableI the bias and standarddeviationof the local constant,local linear,and local quadraticimplementationsof m(y) andmi(y)alongwiththe (asymptotic)MLE at the 1%, 10%, 25%, 50%,75%, 90%,and99%quan-tiles of the distributionof yt. We summarizethe main findingsfor model 1 asfollows: 1. The results for all implementationsseem to improvewith samplesize,with some exceptions regardingthe biases in the extreme tails.2. The per-formance is much better in the center of the news distribution,but this is alsotrue with the parametric estimator. 3. The MLE, mLik(y), performs better ac-

cordingto mean squarederror.However, this advantagedecreases relativelywithsamplesize, due to the largesmallsample componentin the performanceof the nonparametricestimators.94. The local likelihood estimator migen-erally performsmuch better than the least squaresestimator m accordingtomean squarederror,regardlessof whether a local constant,local linear,or lo-cal quadraticsmoother is used, except in the tailswhere it can performworse.5. The local constantimplementationgenerallyworks better in terms of mean

squarederror than the local linear or local quadraticimplementationsof m.

7Thatis, the gridpoints tj,, are chosen to be the j/n sample quantile,wherej = 0,..., n.8Thismeans thatwe take c to be the maximumvalue of yt and -c to be the minimumvalue

of Yt.9NotethatthecomparableresultsinFiorentiniet al. (1996)for animplementationof the MLE

showslightlyworseperformancedue to smallsampleissues.

801

8/7/2019 Estimating Semi Parametric

http://slidepdf.com/reader/full/estimating-semi-parametric 33/67

TABLE I

FINDINGSFORPARAMETERVALUESIN FIORENTINIETAL. (1996), o-2= 0.2 + 0.450f2

oQue 1% 10% 25% 50% 75% Quantile

n Bias Std Bias Std Bias Std Bias Std Bias Stdm

Quadratic 200400800

Linear 200400800

Constant 200400800

Quadratic 200400800

Linear 200400800

Constant 200400800

mLik

MLE 200400800

0.5980.6190.608

-2.349-1.396-0.398

-3.332-2.804-2.218

-0.746-0.445-0.441

-0.562-0.404-0.047

-1.022-0.951-0.921

3.7122.5241.750

3.4532.2131.435

2.9552.0041.325

20.0003.1593.143

12.5043.5271.765

10.6123.0401.508

0.5340.3780.267

0.0890.0620.029

0.1520.1270.088

-0.035-0.016-0.014

-0.109-0.102-0.092

-0.092-0.072-0.057

-0.154-0.146-0.144

0.3630.2430.170

0.4220.2670.168

0.2220.1590.113

0.2780.1450.060

0.2230.1730.065

0.1370.0920.042

0.0950.0670.047

-0.086-0.092-0.091

-0.013-0.024-0.028