EII CPD Webinar - BVP

57

EII CPD WEBINAR Proudly presented by 1 The Impact of the 2019 Finance Act on the EII Scheme

Transcript of EII CPD Webinar - BVP

EII CPD WEBINAR

Proudly presented by

1

The Impact of the 2019 Finance

Act on the EII Scheme

AGENDA

2

Qualifying companies

Introduction to BVP

History of Employment and Investment Incentive Scheme (EIIS)

Investing in EIIS in 2020

Investor considerations

Qualifying Companies

2018 Finance Act & 2019 Finance Act impact on EIIS

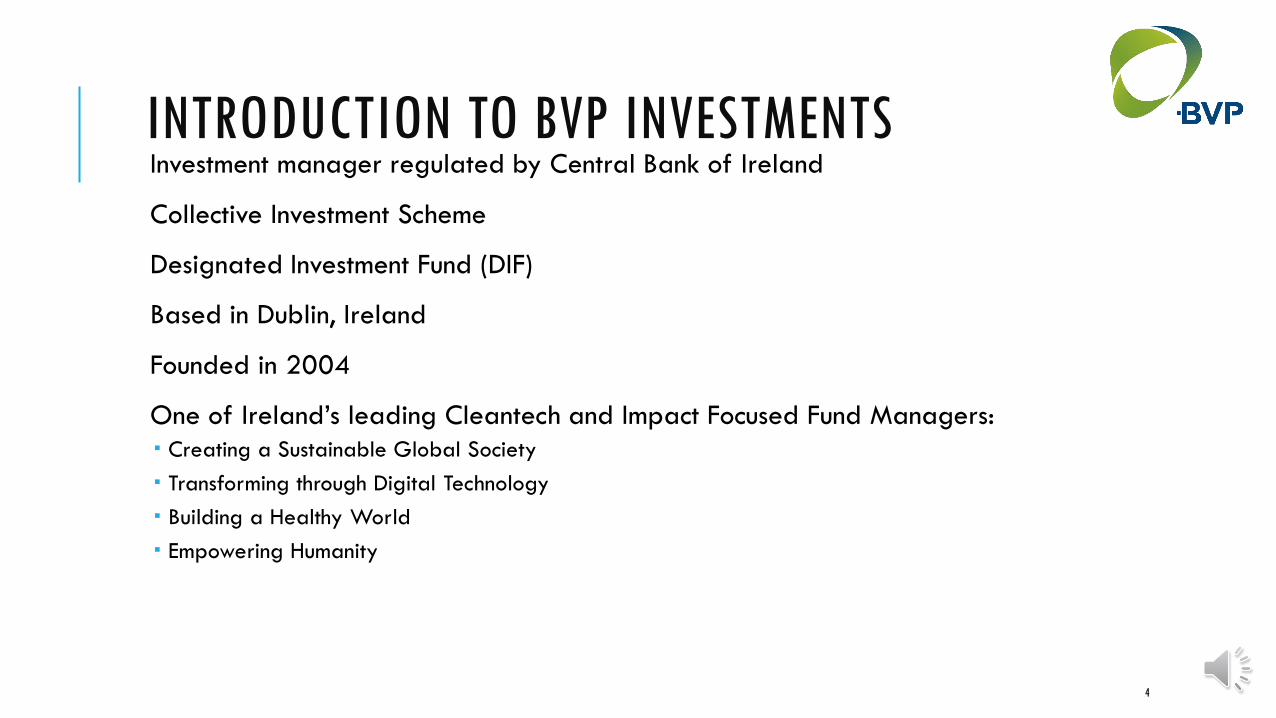

INTRODUCTION TO BVP INVESTMENTSInvestment manager regulated by Central Bank of Ireland

Collective Investment Scheme

Designated Investment Fund (DIF)

Based in Dublin, Ireland

Founded in 2004

One of Ireland’s leading Cleantech and Impact Focused Fund Managers:

Creating a Sustainable Global Society

Transforming through Digital Technology

Building a Healthy World

Empowering Humanity

4

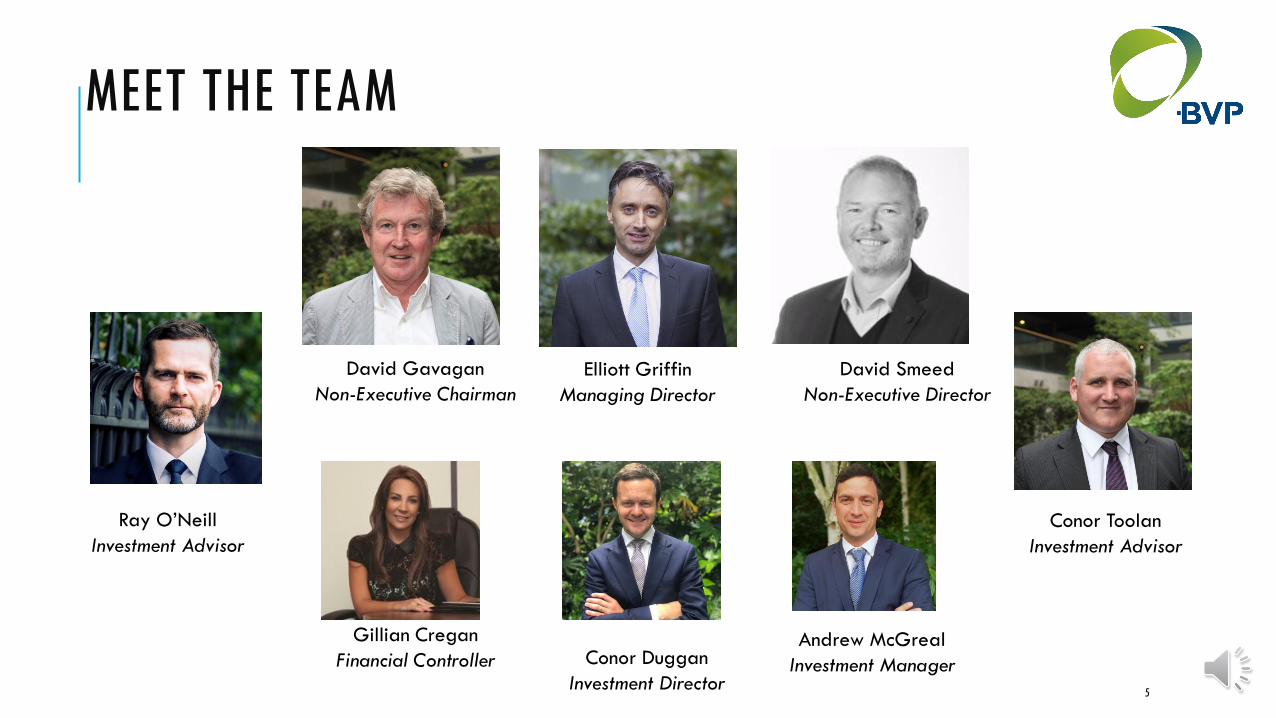

MEET THE TEAM

5

David Smeed

Non-Executive Director

Elliott Griffin

Managing Director

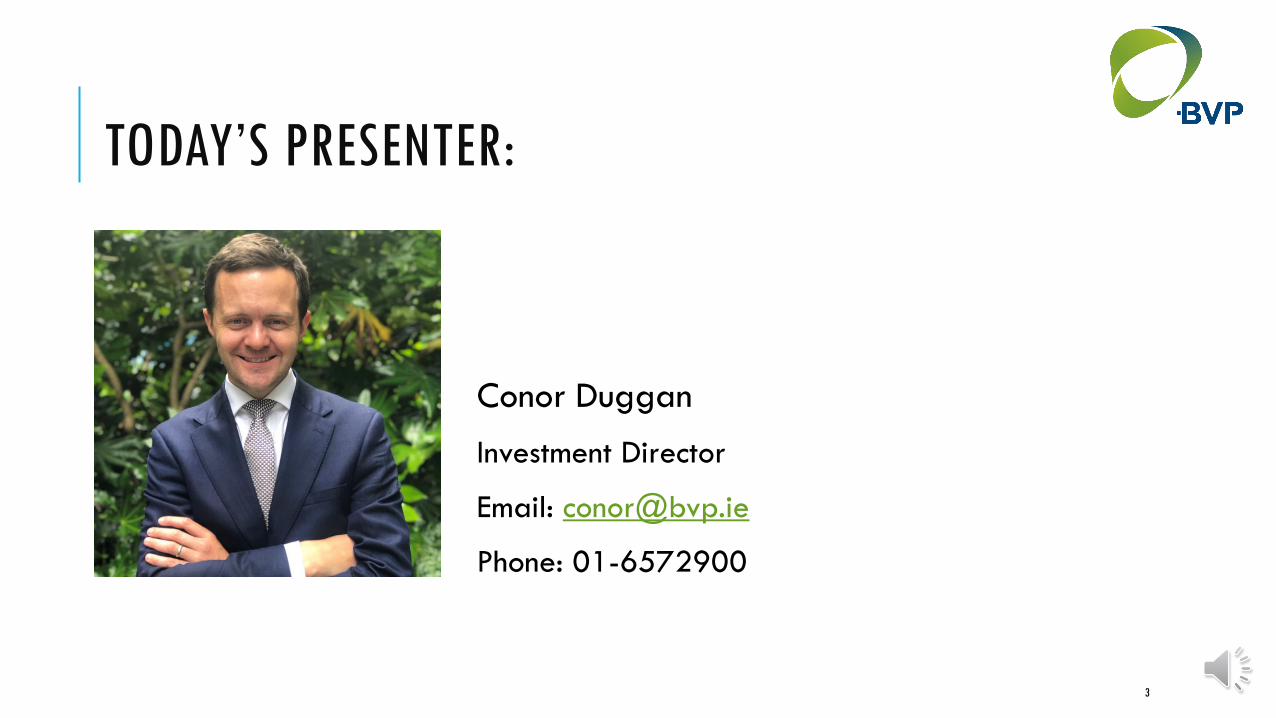

Conor Duggan

Investment Director

Gillian Cregan

Financial Controller

Conor Toolan

Investment Advisor

Ray O’Neill

Investment Advisor

Andrew McGreal

Investment Manager

David Gavagan

Non-Executive Chairman

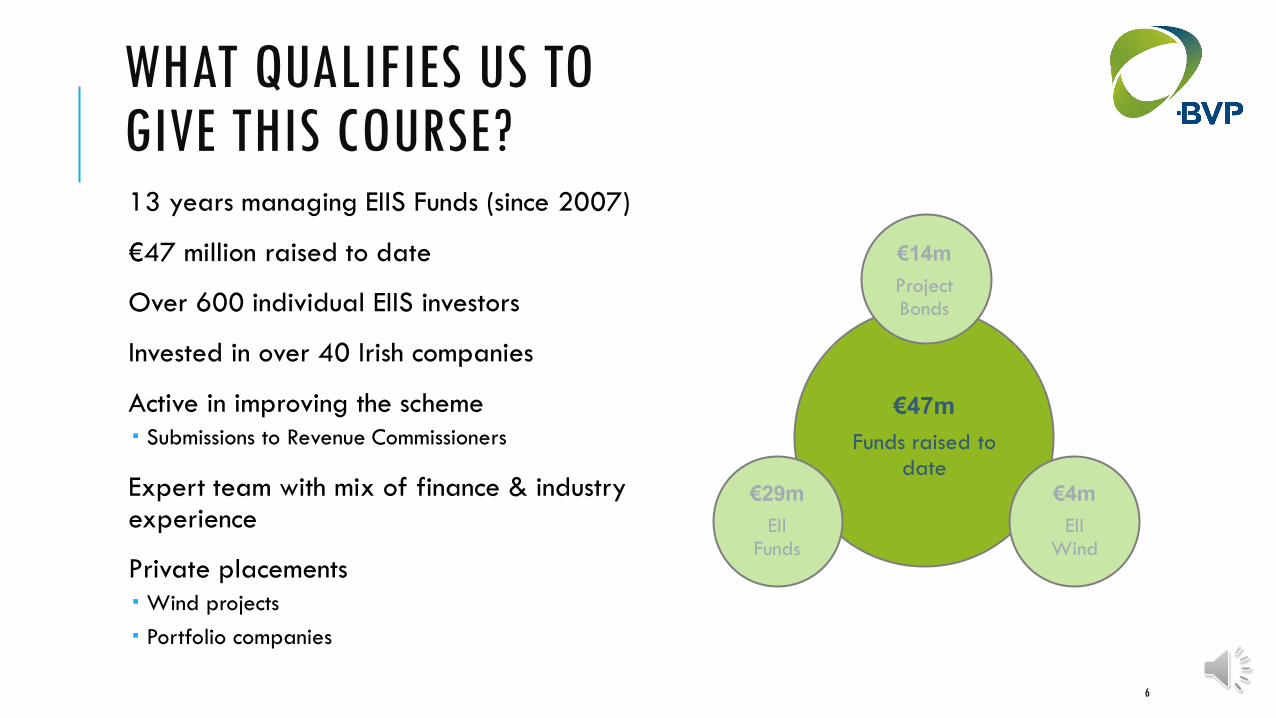

WHAT QUALIFIES US TO GIVE THIS COURSE?13 years managing EIIS Funds (since 2007)

€47 million raised to date

Over 600 individual EIIS investors

Invested in over 40 Irish companies

Active in improving the scheme

Submissions to Revenue Commissioners

Expert team with mix of finance & industry experience

Private placements

Wind projects

Portfolio companies

6

€47m

Funds raised to date

€4m

EII Wind

€14m

Project Bonds

€29m

EII Funds

RECENT BVP INVESTMENTS

BVP’s 2019 EIIS Fund has invested in the following companies in 2020:

Provides on-demand grocery delivery through a smartphone app. Now operating in Dublin, Cork and Bristol

Builds human-powered technology for people who supply and protect the worlds supply of quality information

Legal process outsourcing company who are bringing a unique service offering to the legal world

7

Companies in closing process

Waste Management Company Windfarm Medical Device company

2019 EIIS ACTIVITY

Supervisory Role

• Hold management to account

• Provide challenge

• Monitor financial reporting and overall compliance

• Seek assurance that strategy and performance are on track

8

Stewardship Role

• Guide and shape the business

• Help set strategy

• Establish the company culture, values and ethics

• Determine performance targets

INVESTMENT MANAGER FIDUCIARY OVERSIGHT

HISTORY OF EMPLOYMENT AND INVESTMENT

INCENTIVE SCHEME (EIIS)

9

Qualifying companies

Introduction to BVP

History of Employment and Investment Incentive Scheme (EIIS)

Investing in EIIS in 2020

Investor considerations

Qualifying Companies

2018 Finance Act & 2019 Finance Act impact on EIIS

WHAT IS EIIS?

The Employment and Investment Incentive Scheme (EIIS)

Source of equity funding for Irish small and medium-sized enterprises (SMEs)

Revenue scheme

Tax relief aimed to encourage individuals to provide equity based unsecured finance to trading companies with the potential for capital appreciation

Investor claims tax relief as a deduction from total income. Reduction of individual income tax liability but not PRSI or USC

Entire amount of relief claimed upfront

Investment must be held for a minimum of four years

In 2018 €48m+ invested in 37 companies through EIIS

10

EIIS LEGISLATION

The EII scheme is subject to Irish and EU legislation

The three regulations that dictate the operating rules of the EII scheme are:

1. Part 16 Taxes Consolidation Act, 1997 (as amended)

• Income Tax Relief for Investment in Corporate Trades is the main body of legislation applying to the EII scheme.

2. General Block Exemption Regulation (GBER)

Incorporated in the Finance Act 2015, it integrated EU regulations on allowable state aid.

Have heavily influenced the 2018 and 2019 Finance Act amendments to the EII scheme.

3. Designated Investment Funds Act, 1985(as amended)

This applies to rules surrounding approved EIIS Designated Investment Funds

11

HISTORY OF BESOriginally called Business Expansion Scheme (BES)

First introduced in 1984

Incentive to private investors to invest equity in companies

Focus on small to medium-sized enterprises (SMEs)

Tax relief of 41% upfront

5 year minimum holding period

More restrictive in terms of qualifying sectors

Self-assessment qualification process

Revision of the scheme over the years

12

HISTORY OF EIISCurrent name is Employment and Investment Incentive Scheme (EIIS)

Launched at end-of-year 2011

€150,000 cap in tax relief per investor per annum

€250,000 cap from Jan 1st 2020 onwards

Broader set of sectors qualify

Initially a 3 year minimum holding period

4 year minimum holding period from 2015 onwards

2-step qualification process

40% tax relief upfront, formerly two tranches of tax relief

Businesses can raise up to €5 million in any 12 month period and €15 million in its lifetime

13

Source: Revenue Statistics & Economics Research Branch

14

Growth in EII investors choosing the EII fund managers

HISTORICAL DATA INVESTORS

15

Source: Revenue Statistics & Economics Research Branch

HISTORICAL DATA INVESTEE COMPANIES

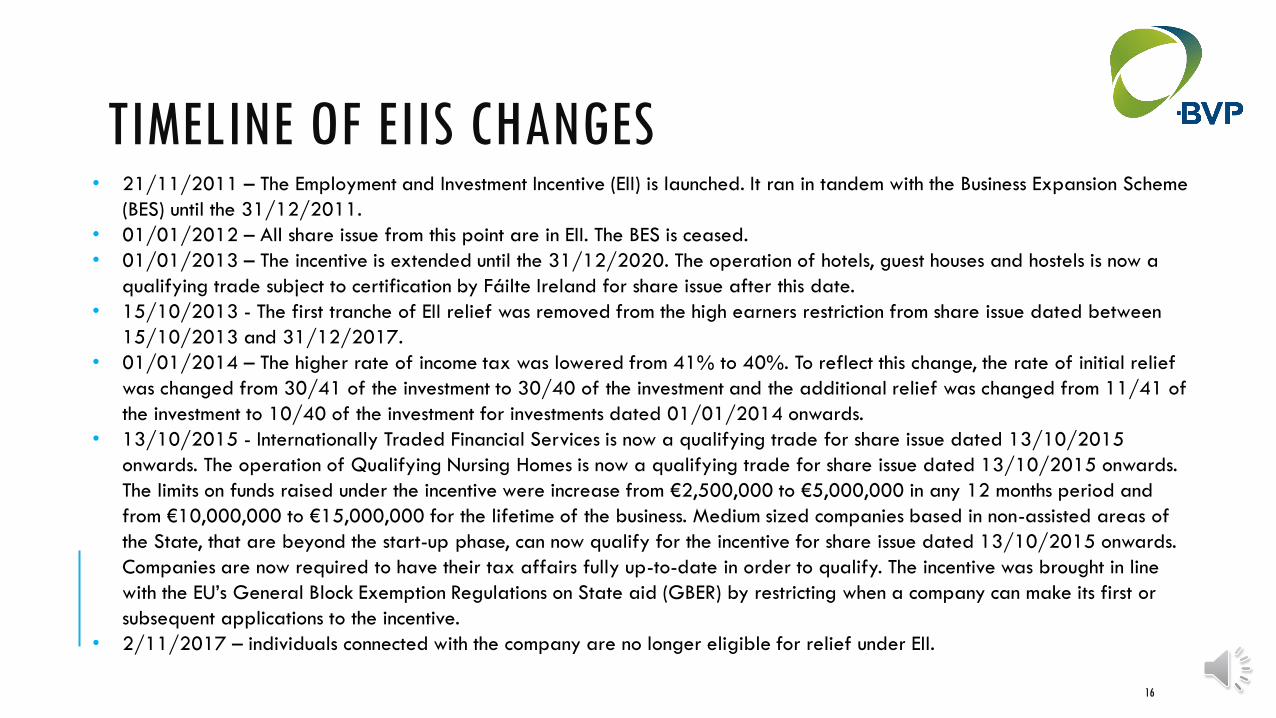

TIMELINE OF EIIS CHANGES

16

• 21/11/2011 – The Employment and Investment Incentive (EII) is launched. It ran in tandem with the Business Expansion Scheme

(BES) until the 31/12/2011.

• 01/01/2012 – All share issue from this point are in EII. The BES is ceased.

• 01/01/2013 – The incentive is extended until the 31/12/2020. The operation of hotels, guest houses and hostels is now a

qualifying trade subject to certification by Fáilte Ireland for share issue after this date.

• 15/10/2013 - The first tranche of EII relief was removed from the high earners restriction from share issue dated between

15/10/2013 and 31/12/2017.

• 01/01/2014 – The higher rate of income tax was lowered from 41% to 40%. To reflect this change, the rate of initial relief

was changed from 30/41 of the investment to 30/40 of the investment and the additional relief was changed from 11/41 of

the investment to 10/40 of the investment for investments dated 01/01/2014 onwards.

• 13/10/2015 - Internationally Traded Financial Services is now a qualifying trade for share issue dated 13/10/2015

onwards. The operation of Qualifying Nursing Homes is now a qualifying trade for share issue dated 13/10/2015 onwards.

The limits on funds raised under the incentive were increase from €2,500,000 to €5,000,000 in any 12 months period and

from €10,000,000 to €15,000,000 for the lifetime of the business. Medium sized companies based in non-assisted areas of

the State, that are beyond the start-up phase, can now qualify for the incentive for share issue dated 13/10/2015 onwards.

Companies are now required to have their tax affairs fully up-to-date in order to qualify. The incentive was brought in line

with the EU’s General Block Exemption Regulations on State aid (GBER) by restricting when a company can make its first or

subsequent applications to the incentive.

• 2/11/2017 – individuals connected with the company are no longer eligible for relief under EII.

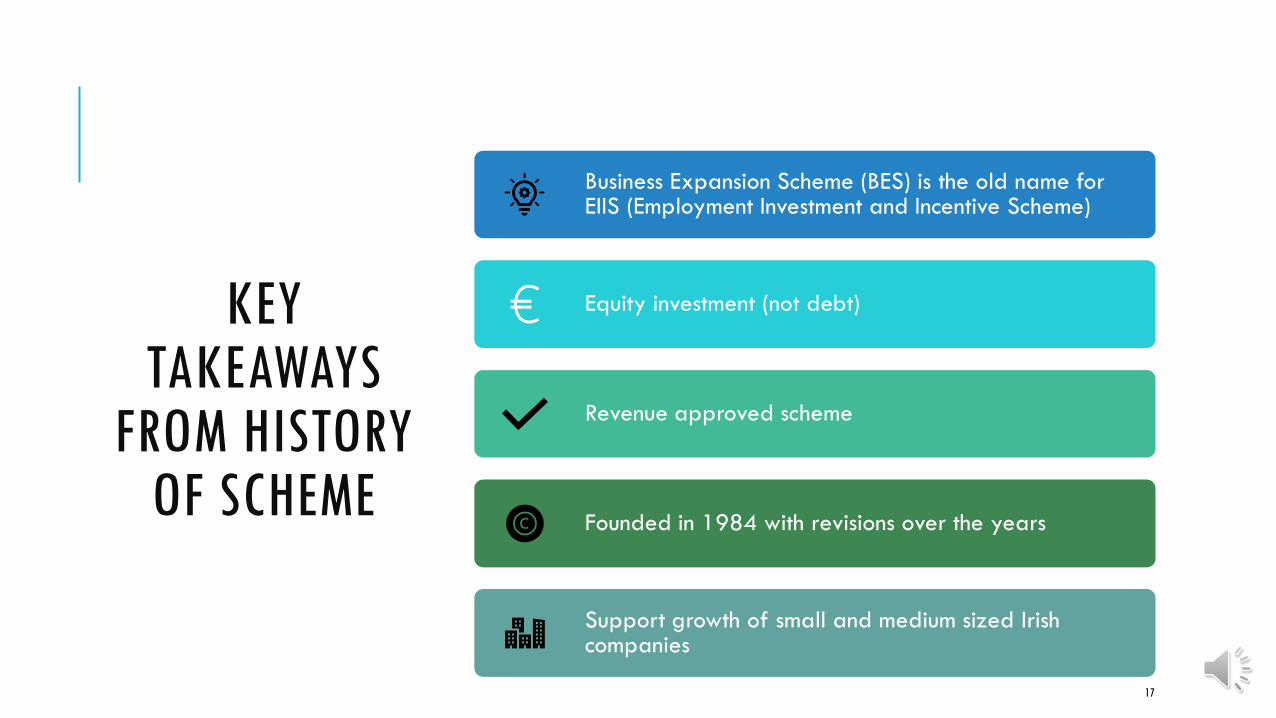

KEY TAKEAWAYS

FROM HISTORY OF SCHEME

Business Expansion Scheme (BES) is the old name for EIIS (Employment Investment and Incentive Scheme)

Equity investment (not debt)

Revenue approved scheme

Founded in 1984 with revisions over the years

Support growth of small and medium sized Irish companies

17

INVESTING IN EIIS IN 2020

18

Qualifying companies

Introduction to BVP

History of Employment and Investment Incentive Scheme (EIIS)

Investing in EIIS in 2020

Investor considerations

Qualifying Companies

2018 Finance Act & 2019 Finance Act impact on EIIS

WHO IS EIIS SUITABLE FOR?

An individual with a taxable income liability in the year the EIIS investment is made

Taxable income includes

PAYE earnings

Rental income from property held in a personal capacity

Other investment income e.g dividends

Pension income

19

EII SCHEME HIGH LEVEL PROCESS – DIRECT

20

Investment in BusinessPrivate Investors

Broker/advisor

Revenue

1a

1b

2

3

Investment Through Broker

Direct Investment

EII Certificate

EII Statement of Qualification

EII SCHEME HIGH LEVEL PROCESS – VIA DIF

21

Equity Investments in

CompaniesInvestment

Manager

Private Investors

Broker/advisor

Designated

Investment Fund

(Trustee)

Revenue

1a

1b

2 3

5

4

Distributions

Direct EIIS Investment

EIIS Investment Through Broker

Shares

EII

Certificate

EII Statement of

Qualification

Investment

in Companies*

*Investments through a designated investment fund are executed through a Trustee.

The due diligence is completed by an approved designated investment fund manager.

WHAT IS A STATEMENT OF QUALIFICATION?A statement by the company to the effect that

The company is a qualifying company

The investment is a qualifying investment within the meaning of Section 496 of the TCA

Contains the company and investment details and any such other information as the Revenue Commissioners may reasonably require

Tax relief after they have spent 30% of the investment amount

22

PRACTICAL ILLUSTRATION

23

2020 Income & Tax Payable

With EII Without EII

Gross Pay €78,000 €78,000

EII Investment €40,000 -

Taxable Pay €38,000 €78,000

€35,300 @ 20% €7,060 €7,060

Remainder @ 40% €1,080 €17,080

Gross Tax Payable €8,140 €24,140

Less:

Tax Credits €3,300 €3,300

Net Tax Payable €4,840 €20,840

Tax Savings through

EII

€16,000

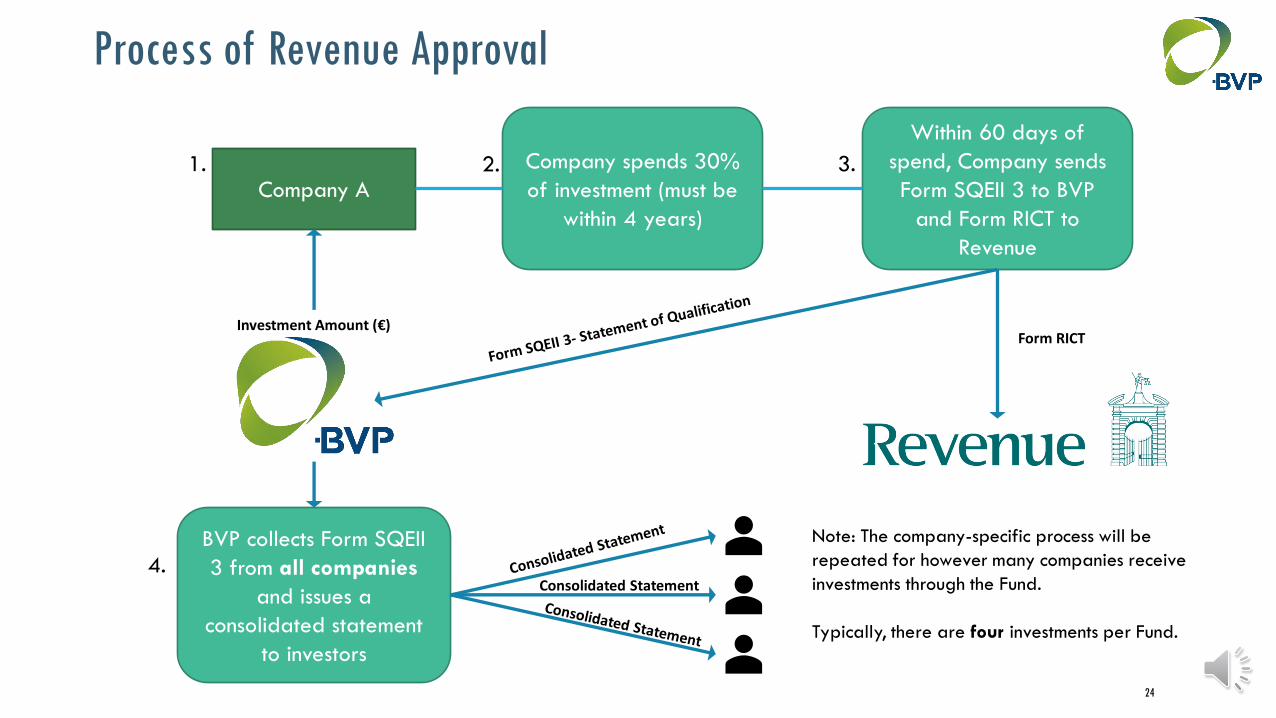

Company A

Company spends 30%

of investment (must be

within 4 years)

Within 60 days of

spend, Company sends

Form SQEII 3 to BVP

and Form RICT to

Revenue

Investment Amount (€)Form RICT

BVP collects Form SQEII

3 from all companies

and issues a

consolidated statement

to investors

Consolidated Statement

Note: The company-specific process will be

repeated for however many companies receive

investments through the Fund.

Typically, there are four investments per Fund.

Process of Revenue Approval

1. 2. 3.

4.

24

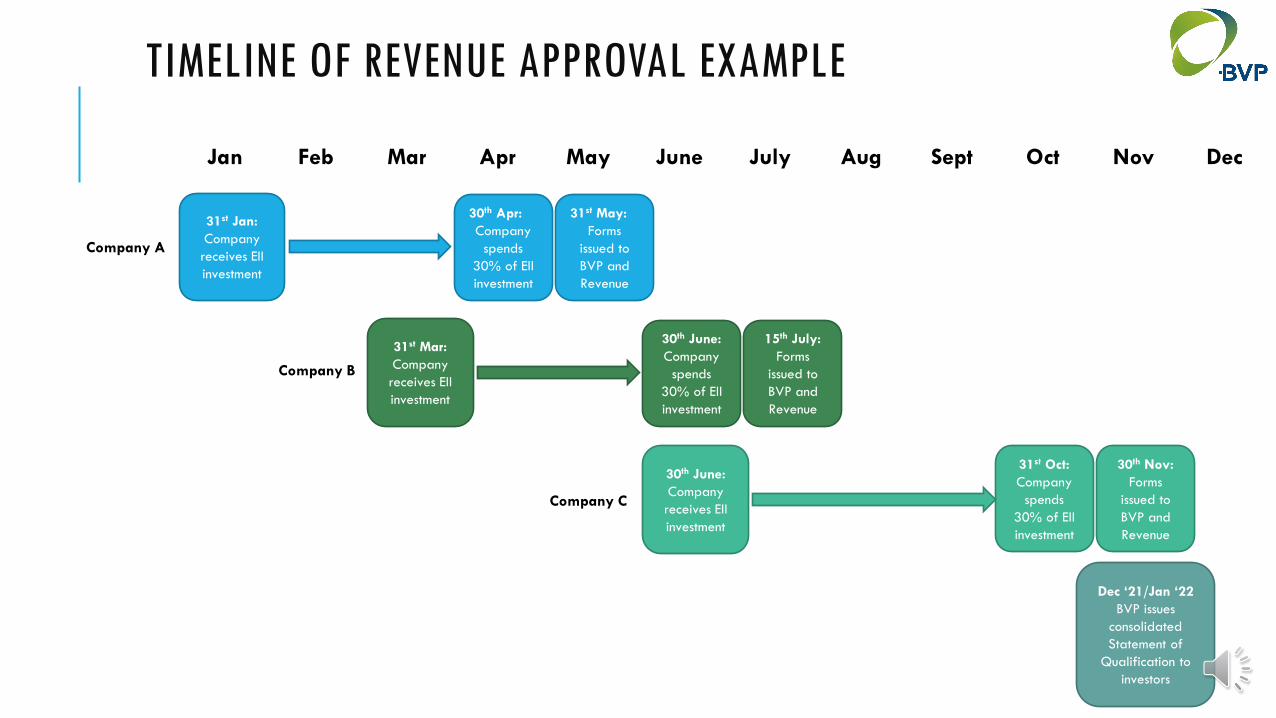

TIMELINE OF REVENUE APPROVAL EXAMPLE

25

Jan Feb Mar Apr May June July Aug Sept Oct Nov Dec

31st Jan:

Company

receives EII

investment

30th Apr:

Company

spends

30% of EII

investment

31st May:

Forms

issued to

BVP and

Revenue

31st Mar:

Company

receives EII

investment

30th June:

Company

spends

30% of EII

investment

15th July:

Forms

issued to

BVP and

Revenue

30th June:

Company

receives EII

investment

31st Oct:

Company

spends

30% of EII

investment

30th Nov:

Forms

issued to

BVP and

Revenue

Dec ‘21/Jan ‘22

BVP issues

consolidated

Statement of

Qualification to

investors

Company A

Company B

Company C

EIIS DESIGNATED INVESTMENT FUNDS

Investment Managers authorised by Central Bank under Section 10 to manage EIIS designated investment funds (“DIF”)

Also recently required to register as Alternative Investment Fund Managers (“AIFM”)

A designated investment fund is an investment fund that has been designated by the Revenue Commissioners in accordance with the rules laid down in Section 508 of the Taxes Consolidation Act 1997, as amended

The Investment Manager will invest the funds raised in the year after the DIF is raised, at which point shares will be issued

Revenue will issue the Fund with the Designated Fund Reference Number (“DFRN”)

26

DESIGNATED INVESTMENT FUNDS

The Revenue Commissioners shall designate a fund if they are satisfied that:

(a) There is a Trustee in place for the DIF

(b) under the terms of the trusts it is provided that:i. the entire fund is to be invested without undue delay in eligible shares,

ii. pending investment in eligible shares, any moneys subscribed for the purchase of shares are to be placed on deposit in a separate account with a bank licensed to transact business in the State,

iii. any amounts received by means of dividends or interest are, subject to a commission in respect of management expenses at a rate not exceeding a rate which shall be specified in the deed of trust under which the fund has been established, to be paid without undue delay to the participants,

iv. any charges to be made by means of management or other expenses in connection with the establishment, the running, the winding down or the termination of the fund shall be at a rate not exceeding a rate which shall be specified in the deed of trust under which the fund is established,

v. audited accounts of the fund are submitted annually to the Revenue Commissioners as soon as may be after the end of each period for which accounts of the fund are made up,

vi. the managers, the trustees of the fund and any of their associates are not for the time being connected either directly or indirectly with any company whose shares comprise part of the fund,

vii. any discounts on eligible shares received by the trustees or managers of the fund are accepted solely for the benefit of theparticipants,

viii. if a limit is placed on the size of the fund or a minimum amount for investment is stipulated, any subscriptions not accepted are to be returned without undue delay, and

ix. no participant is allowed to have any shares in any company in which the fund has invested transferred into his or her name until 4 years have elapsed from the date of the issue of the shares to the fund.

27

BENEFITS OF DESIGNATED INVESTMENT FUNDS

Investing in a range of companies diversifying risk

Professional due diligence on investments

Oversight of investment by investment manager

Stronger legal representation

Portfolio reporting

28

PRACTICAL IMPLICATIONS FOR BROKERS AND ADVISORS

For direct investments – look for company own due diligence on their reasons for qualification

For investments via a designated investment fund – look for diversification in choice of target investments

For both – look for commitments to provide investors with preference shares (which have priority over founders’ shares)*

*Possible conflict for direct investments

29

INVESTOR CONSIDERATIONS

30

Qualifying companies

Introduction to BVP

History of Employment and Investment Incentive Scheme (EIIS)

Investing in EIIS in 2020

Investor considerations

Qualifying Companies

2018 Finance Act & 2019 Finance Act impact on EIIS

PRACTICAL IMPLICATIONS FOR INVESTORS

Can expect quicker turnaround in claiming tax relief

Increase in company responsibility should reduce risk on non-qualification

More choice of funds is good for investors

More diversification within funds should reduce risk for investors

Additional investor protections should increase the ability of the investor/DIF to exit investment and get a return on capital after the minimum holding period of 4 years

31

KEY TAKEAWAYS FROM INVESTOR CONSIDERATIONS

40% provided upfront

Minimum holding period of 4 years

Must be equity and cannot take secured

position

Designated Investment Fund v Direct Investments

QUALIFYING COMPANIES

33

Qualifying companies

Introduction to BVP

History of Employment and Investment Incentive Scheme (EIIS)

Investing in EIIS in 2020

Investor considerations

Qualifying Companies

2018 Finance Act & 2019 Finance Act impact on EIIS

QUALIFYING COMPANIES

For a company to raise funding that will provide EII relief to investors, must be a “qualifying company”

Qualifying company designation is based on the activities of the company itself and the activities of other businesses within the RICT group

A RICT group is made up of a qualifying company and all of its partner businesses or linked businesses

The qualifying company can be either

A trading company itself, or

The holding company of a trading company

Company and RICT group must meet conditions throughout the 4-year relevant period:

Company must be either tax resident in Ireland, EU or EEA Member State

Must carry on relevant trading activities in the State or if carrying our R&D+I it must intend to carry out relevant trading activities in the State

34

INVESTMENT IN TRADING

COMPANY

The investment can be made in:

A company that exists wholly for the purposes of carrying on relevant trading activities

Must not carry out any other activities, other than incidental activities

Cannot carry on a business that consists partially of a trade and partially of professional services

A holding company that exists either wholly for the purpose of being a holding company or wholly for the purposes of both carrying on relevant trading activities and being a holding company

The company cannot be in control of any company that is not a qualifying subsidiary

The company cannot be under the control of any other company

35

QUALIFYING SUBSIDIARIES

Two types of qualifying subsidiaries a qualifying company can have:

Subsidiaries which trade in their own right

Subsidiaries which carry out support functions for the qualifying company’s trade

Subsidiaries that carry out a trade in their own right must be a resident in Ireland or an EU or EEA state and must carry out, or intend to carry out, relevant trading activities from a fixed place of business in the State

Subsidiaries carrying out support functions can be established anywhere in the world, assuming the business carries on relevant trading activities and can only involve

Purchasing or selling goods or materials for use by the qualifying company or its subsidiaries

Providing services on behalf of the qualifying company or its qualifying subsidiaries

36

QUALIFYING PURPOSE

The company must intend to use the amounts raised for a “qualifying purpose” within 4 years of share issue

A qualifying purpose is spending the amounts either

For the purposes of carrying out relevant trading activities, or

Where the company has not yet commenced to carry out relevant trading activities, on research, development and innovation (R&D+I)

The amounts spent must contribute to the maintenance or creation of employment

The amounts cannot be spent on buying a trade or shares in a company, with the exception of shares in a qualifying subsidiary

37

ELIGIBLE SHARES

Eligible shares carry a right to a preference dividend, granting investors liquidation preference rights

Eligible shares are redeemable

Investments with agreements that substantially reduce the risk to the investors are prohibited (e.g. personal guarantees and security over assets)

38

RICT GROUP

Wording refined for a connected parties

“Linked businesses” >50% control

“Partner businesses” >25% shareholdings

Challenges where promoters of the company raising EIIS involved in a Linked or Partner business particularly where operating in “Adjacent market”

39

UNDERTAKING IN DIFFICULTY

A RICT group, which is less than 3 years old, cannot be an “undertaking in difficulty”

An “undertaking in difficulty” is a RICT group that will almost certainly go out of business in the short or medium term

Where more than half of its share capital and share premium has disappeared as a result of accumulated losses

Irish GAAP allows companies to make choices in preparing their accounts and the company can consider conservative accounting choices they have made

Ex: Expensing R&D when that R&D also met the conditions for capitalisation

Need signed statement by a registered auditor that it would be possible to restate the accounts and what the amended figure would be is sufficient. Actual restatement is not necessary

40

TAX RELIEF: COMPANY SELF-CERTIFICATIONThe approval process for qualifying company applications has changed from Revenue review to self-certification by the investee companies and investors

Revenue support is available to Companies seeking confirmation that they meet the qualifying Irish and GBER criteria

Revenue support is available to investors seeking confirmation that they are eligible for tax relief

Statement of qualification can be issued by companies for tax relief after they have spent 30% of the investment

For EII direct investments companies issue a ‘statement of qualification’ to investors to claim tax relief

Companies seeking investment from an EII designated investment fund issue a ‘statement of qualification’ to the designated investment fund manager. The designated investment fund manager consolidates the information for all the companies in the fund and issues a certificate to investors to claim tax relief

41

REPORTING TO REVENUE/LOSS OF TAX RELIEF

Where the investment was made through a Designated Investment Fund, the managers of the designated investment fund who have knowledge of a matter which disqualifies a company/connected person individual for tax relief, shall within 60 days of the event, give a notice in writing to a Revenue officer of the event

The Company/Designated Investment Fund is responsible for including details of the qualifying investment in a return to Revenue for the accounting period in which the eligible shares were issued

If the company issues a statement of qualification when they were not qualified, the clawback of tax relief will be chargeable to the Company

42

REPORTING TO REVENUE/LOSS OF TAX RELIEF

The company should within 30 days of the share issue date for a qualifying investment provide Revenue through electronic means:

Name of company; Address of company; CRO Number; Amount raised; Investor Name, address PPS; Amount etc.

Revenue may publish this information in accordance with GBER for companies receiving state aid

If the company fails to comply with the above requirements and deadlines, they will be liable for a penalty of €2,000 and €50 per day after the 30-day deadline

43

REDEMPTION/EXIT PROCESS

The Manager co-ordinates the Exit of the Fund after expiration of the Minimum Investment Period (4 years) by seeking to make arrangements with the Board of Directors of each of the Investee Companies/projects for redemption of the investment

These may include:

A sale of the shares on the Irish Stock Exchange or any other recognized securities market, if such share are listed;

An acquisition or take-over;

A private placing, e.g. a trade sale

A repurchase or redemption by the Investee Company of its own shares;

A sale of the EII shareholdings to the promoters of the Investee companies;

Pre-2018 Finance Act , the exercise of a call or put option at market value with the promoters of the Investee Companies; and/or

Any other method of realization which may, in the opinion of the Manager, be appropriate at that time

44

DISTRIBUTIONS FROM INVESTEE COMPANIES WITH FOLLOW ON EII INVESTMENTS

Capital Redemption Window: Company can redeem shares or purchase shares from any member other than investors within the EIIS minimum holding period subject to following conditions:

Most recent EIIS raised by the RICT group was 18 month prior

The RICT group will not seek to raise EIIS for 12 months after return of capital

45

KEY TAKEAWAYS FROM QUALIFYING COMPANIES

Designation of a qualifying company based on the activities of the company or its RICT group

The company cannot control or be under the control of any other companies, except for qualifying subsidiaries

Investment amounts must be spent on relevant trading activities or R&D+I and must ultimately contribute to the maintenance or creation of employment

Relevant trading activities must take place in Ireland or in EU or EEA Member State

A qualifying company cannot be an undertaking in difficulty

2018 FINANCE ACT & 2019 FINANCE ACT IMPACT ON

EIIS

47

Qualifying companies

Introduction to BVP

History of Employment and Investment Incentive Scheme (EIIS)

Investing in EIIS in 2020

Investor considerations

Qualifying Companies

2018 Finance Act & 2019 Finance Act impact on EIIS

FINANCE ACT 2019

48

Several changes made to the EII Scheme

01Brought into law in December 2019

02EII Scheme will be extended for a further year to 31 December 2021

03

HIGH LEVEL CHANGES

Level of Relief: Full income tax relief (40%) be provided in the year in which the investment is made. This compares with prior arrangements where 30% relief is provided upon the initial investment and a further 10% is given after Year 3 subject to certain conditions. This change is effective from 8 October 2019.

Higher investment limit: The annual investment limit was increased from €150k to €250K from 1st January 2020 and up to €500k in the case of those who invest for a minimum period of 7 years.

Relief from Funds**From 1 January 2020, investors in certain designated investment funds (funds that have been approved by Revenue as such) will no longer have a choice as to the year of assessment that the deduction can be claimed. For investments made through all designated investment funds, the deduction will only be available in the year the amount was subscribed to the fund.

49

TAX RELIEFProviding all of the conditions of the EII scheme are met, relief on the invested amount is due in the tax year in which the investment is made in the company

Where an investor invests in eligible shares through a designated fund manager (DFM) but the shares are not issued to the fund until the following year, he/she can claim tax relief in the year in which he/she made the investment in the fund.

Qualifying companies need to have spent 30% of the investment on qualifying activities before issuing a statement of qualification. The typical time from investment to issuance of statement is 3-4 months.

EXAMPLE:

Peter invests in a designated investment fund in December 2020. The shares are not issued by the company the designated investment fund invested in until March 2021. Peter can claim tax relief on the EII scheme investment in 2020 [the year he made the investment]

50

CLAIMING TAX RELIEF Investors can only claim relief when they have received the statement of qualification from the company or consolidated certificate from the designated investment fund manager

The statement of qualification must be issued by the company within 2 years of the end of the year of assessment

The maximum tax relief claim an individual can make in a year is €250,000

If the investor’s subscription to the EII investment is in excess of €250,000 or they have insufficient total income to offset the relief, the amount that was not offset will be carried forward

If relief is carried forward and further relief is available from an investment in the subsequent year, the oldest relief is used first. The final year of assessment for which relief can be carried forward is 2021

51

2019 FINANCE ACT: SUMMARY OF RECENT EII CHANGES

Before

Two tranches of tax relief: 30% in year of investment, 10% after 4-year min holding period

After

40% tax relief in the year of investment

Maximum annual investment of €150,000

Maximum annual investment of €250,000

Maximum investment of €500,000 for those who invest a minimum period of 7 years

KEY TAKEAWAYS FROM 2019 FINANCE ACT

Process uses self-certification leading to faster EII approval

Changes are good for investors- shares rank ‘pari passu’ with strategic investors

Companies raising EIIS need to act responsibly

Look out for mixed venture capital funds with % EIIS offering

Tax relief can now be claimed entirely upfront

Investments of up to €250,000 can offset income for tax purposes

OUTLOOK FOR 2021 AND THE EXPECTED IMPACT ON EIIS

Economic Forecasts suggest that global GDP will grow by circa 5% in 2021

Irish growth in GDP is forecasted to be between 1.4% and 5.6% in 2021

ESRI have stated that they forecast that savings as a % of income in likely to rise to 20% this year from 10.5% in 2019 which could lead to a surge in demand

BVP’s Portfolio Companies have responded very strongly to challenge of Covid-19.

BVP’s investment strategy for 2021 will likely be more conservative than 2020

Community projects and other project type investments allow for further diversification

54

THE 2020 BVP EII FUND – OPENING SOON

56

THANK YOU FOR ATTENDING!

57

Contact Us:

Phone

01-6572900

Website

bvp.ie

*BVP is not a tax advisor. You should always seek independent tax advice before making an investment