Eduardo Rossi University of...

92

GARCH Models Eduardo Rossi University of Pavia

Transcript of Eduardo Rossi University of...

GARCH Models

Eduardo Rossi

University of Pavia

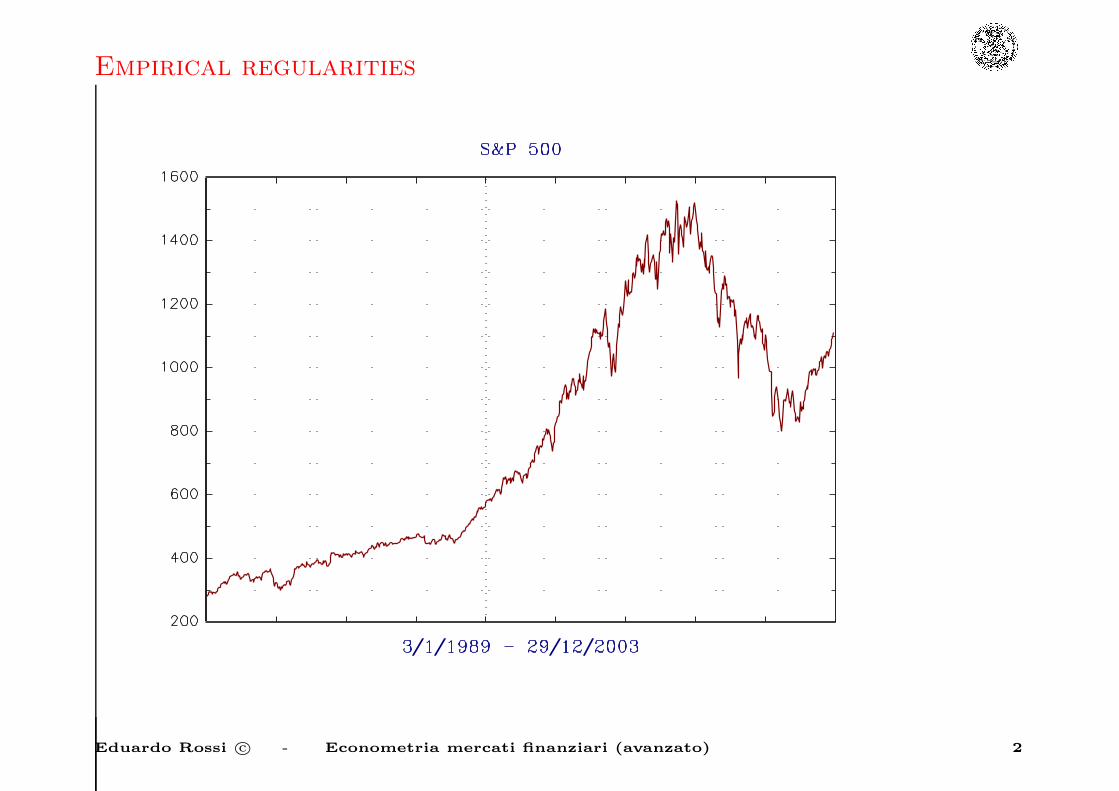

Empirical regularities

Eduardo Rossi c© - Econometria mercati finanziari (avanzato) 2

Empirical regularities

Eduardo Rossi c© - Econometria mercati finanziari (avanzato) 3

Empirical regularities

GARCH models have been developed to account for empirical

regularities in financial data. Many financial time series have a

number of characteristics in common.

• Asset prices are generally non stationary. Returns are usually

stationary. Some financial time series are fractionally integrated.

• Return series usually show no or little autocorrelation.

• Serial independence between the squared values of the series is

often rejected pointing towards the existence of non-linear

relationships between subsequent observations.

Eduardo Rossi c© - Econometria mercati finanziari (avanzato) 4

Empirical regularities

• Volatility of the return series appears to be clustered.

• Normality has to be rejected in favor of some thick-tailed

distribution.

• Some series exhibit so-called leverage effect, that is changes in

stock prices tend to be negatively correlated with changes in

volatility. A firm with debt and equity outstanding typically

becomes more highly leveraged when the value of the firm

falls.This raises equity returns volatility if returns are constant.

Black, however, argued that the response of stock volatility to the

direction of returns is too large to be explained by leverage alone.

• Volatilities of different securities very often move together.

Eduardo Rossi c© - Econometria mercati finanziari (avanzato) 5

Why do we need ARCH models?

Wold’s decomposition theorem establishes that any covariance

stationary {yt} may be written as the sum of a linearly deterministic

component and a linearly stochastic with a square-summable,

one-sided moving average representation. We can write,

yt = dt + ut

dt is linearly deterministic and ut is a linearly regular covariance

stationary stochastic process, given by

ut = B (L) εt

B (L) =∞∑

i=0

biLi

∞∑

i=0

b2i <∞ b0 = 1

Eduardo Rossi c© - Econometria mercati finanziari (avanzato) 6

Why do we need ARCH models?

E [εt] = 0

E [εtετ ] =

σ2ε <∞, if t = τ

0, otherwise

The uncorrelated innovation sequence need not to be Gaussian and

therefore need not be independent. Non-independent innovations are

characteristic of non-linear time series in general and conditionally

heteroskedastic time series in particular.

Eduardo Rossi c© - Econometria mercati finanziari (avanzato) 7

Why do we need ARCH models?

Now suppose that yt is a linear covariance stationary process with

i.i.d. innovations as opposed to merely white noise. The

unconditional mean and variance are

E [yt] = 0

E[

y2t

]

= σ2ε

∞∑

i=0

b2i

which are both invariant in time. The conditional mean is time

varying and is given by

E [yt |Φt−1 ] =∞∑

i=1

biεt−i

where the information set is Φt−1 = {εt−1, εt−2, . . .}.

Eduardo Rossi c© - Econometria mercati finanziari (avanzato) 8

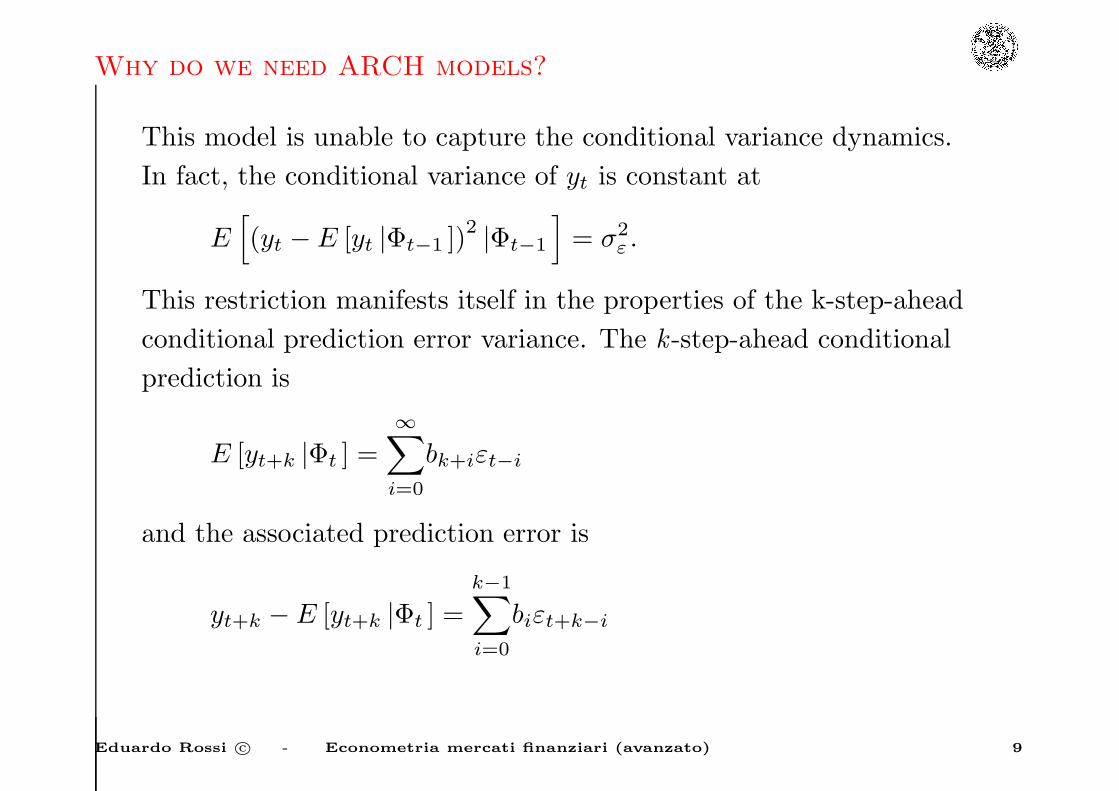

Why do we need ARCH models?

This model is unable to capture the conditional variance dynamics.

In fact, the conditional variance of yt is constant at

E[

(yt −E [yt |Φt−1 ])2|Φt−1

]

= σ2ε .

This restriction manifests itself in the properties of the k-step-ahead

conditional prediction error variance. The k -step-ahead conditional

prediction is

E [yt+k |Φt ] =∞∑

i=0

bk+iεt−i

and the associated prediction error is

yt+k − E [yt+k |Φt ] =k−1∑

i=0

biεt+k−i

Eduardo Rossi c© - Econometria mercati finanziari (avanzato) 9

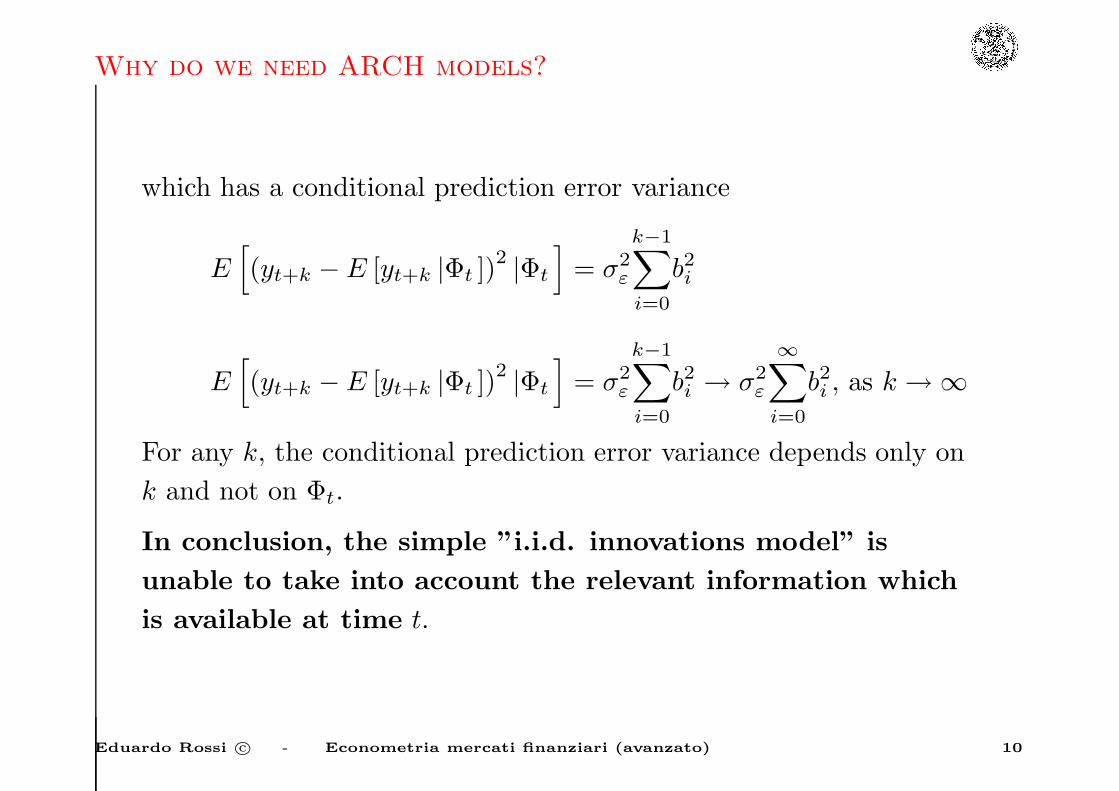

Why do we need ARCH models?

which has a conditional prediction error variance

E[

(yt+k − E [yt+k |Φt ])2|Φt

]

= σ2ε

k−1∑

i=0

b2i

E[

(yt+k − E [yt+k |Φt ])2|Φt

]

= σ2ε

k−1∑

i=0

b2i → σ2ε

∞∑

i=0

b2i , as k → ∞

For any k, the conditional prediction error variance depends only on

k and not on Φt.

In conclusion, the simple ”i.i.d. innovations model” is

unable to take into account the relevant information which

is available at time t.

Eduardo Rossi c© - Econometria mercati finanziari (avanzato) 10

The ARCH(q) Model

(Bollerslev, Engle and Nelson, 1994) The process {εt (θ0)} follows an

ARCH (AutoRegressive Conditional Heteroskedasticity) model if

Et−1 [εt (θ0)] = 0 t = 1, 2, . . . (1)

and the conditional variance

σ2t (θ0) ≡ V art−1 [εt (θ0)] = Et−1

[

ε2t (θ0)]

t = 1, 2, . . . (2)

depends non trivially on the σ-field generated by the past

observations: {εt−1 (θ0) , εt−2 (θ0) , . . .} .

Eduardo Rossi c© - Econometria mercati finanziari (avanzato) 11

The ARCH(q) Model

Let {yt (θ0)} denote the stochastic process of interest with

conditional mean

µt (θ0) ≡ Et−1 (yt) t = 1, 2, . . . (3)

µt (θ0) and σ2t (θ0) are measurable with respect to the time t− 1

information set. Define the {εt (θ0)} process by

εt (θ0) ≡ yt − µt (θ0) . (4)

Eduardo Rossi c© - Econometria mercati finanziari (avanzato) 12

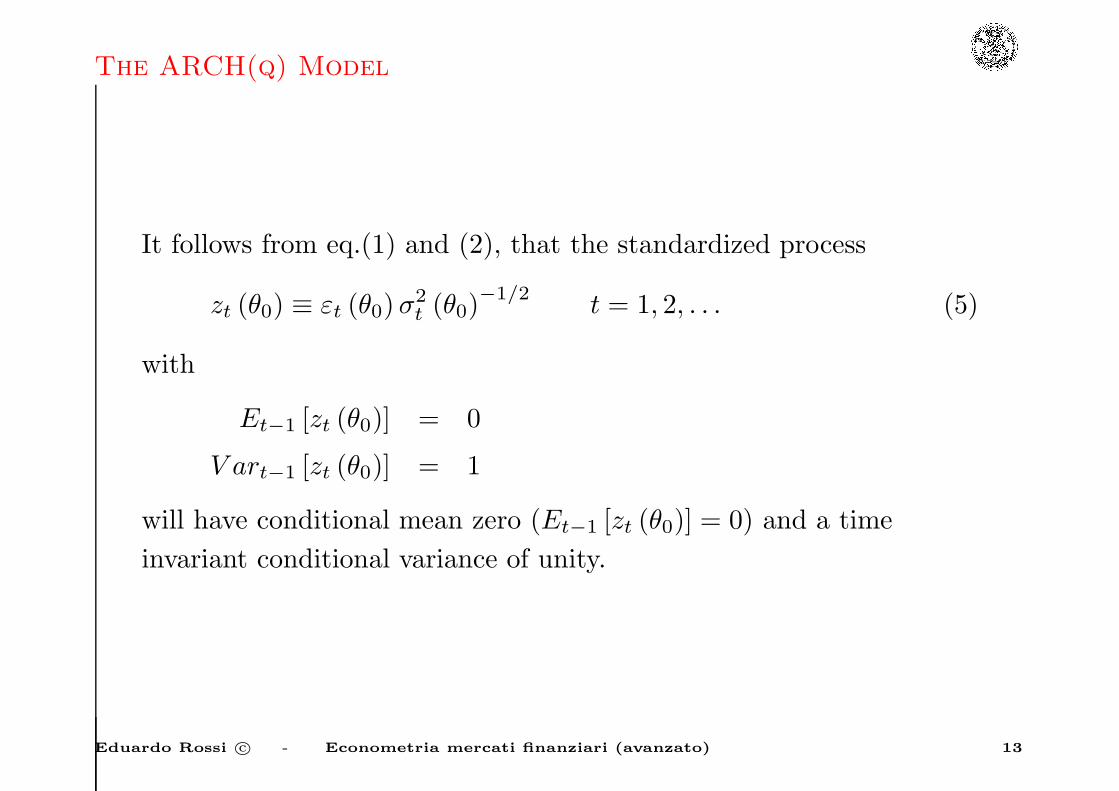

The ARCH(q) Model

It follows from eq.(1) and (2), that the standardized process

zt (θ0) ≡ εt (θ0)σ2t (θ0)

−1/2 t = 1, 2, . . . (5)

with

Et−1 [zt (θ0)] = 0

V art−1 [zt (θ0)] = 1

will have conditional mean zero (Et−1 [zt (θ0)] = 0) and a time

invariant conditional variance of unity.

Eduardo Rossi c© - Econometria mercati finanziari (avanzato) 13

The ARCH(q) Model

We can think of εt (θ0) as generated by

εt (θ0) = zt (θ0)σ2t (θ0)

1/2

where ε2t (θ0) is unbiased estimator of σ2t (θ0).

Let’s suppose zt (θ0) ∼ NID (0, 1) and independent of σ2t (θ0)

Et−1

[

ε2t]

= Et−1

[

σ2t

]

Et−1

[

z2t

]

= Et−1

[

σ2t

]

= σ2t

because z2t |Φt−1 ∼ χ2

(1).

Eduardo Rossi c© - Econometria mercati finanziari (avanzato) 14

The ARCH(q) Model

If the conditional distribution of zt is time invariant with a finite

fourth moment, the fourth moment of εt is

E[

ε4t]

= E[

z4t

]

E[

σ4t

]

≥ E[

z4t

]

E[

σ2t

]2= E

[

z4t

]

E[

ε2t]2

where the last equality follows from

E[σ2t ] = E[Et−1(ε

2t )] = E[ε2t ]

E[

ε4t]

≥ E[

z4t

]

E[

ε2t]2

by Jensen’s inequality. The equality holds true for a constant

conditional variance only.

Eduardo Rossi c© - Econometria mercati finanziari (avanzato) 15

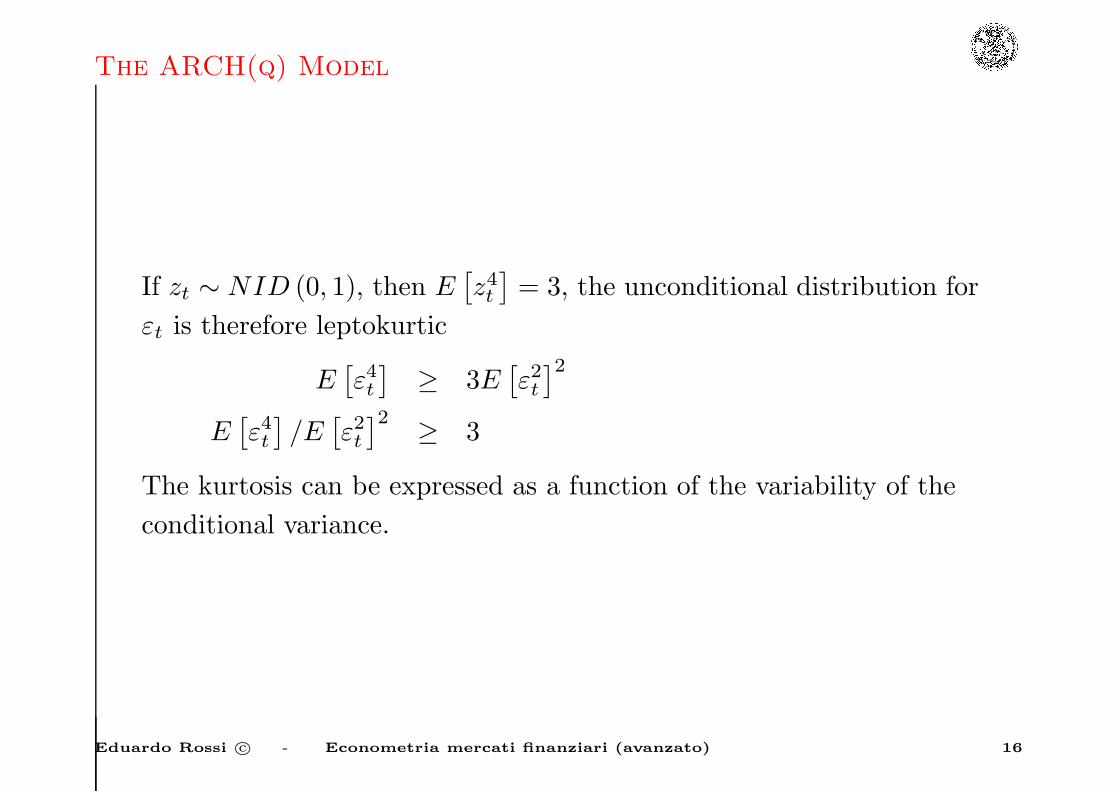

The ARCH(q) Model

If zt ∼ NID (0, 1), then E[

z4t

]

= 3, the unconditional distribution for

εt is therefore leptokurtic

E[

ε4t]

≥ 3E[

ε2t]2

E[

ε4t]

/E[

ε2t]2

≥ 3

The kurtosis can be expressed as a function of the variability of the

conditional variance.

Eduardo Rossi c© - Econometria mercati finanziari (avanzato) 16

The ARCH(q) Model

In fact, if εt |Φt−1 ∼ N(

0, σ2t

)

Et−1

[

ε4t]

= 3Et−1

[

ε2t]2

E[

ε4t]

= 3E[

Et−1

(

ε2t)2]

≥ 3{

E[

Et−1

(

ε2t)]}2

= 3[

E(

ε2t)]2

E[

ε4t]

− 3[

E(

ε2t)]2

= 3E{

Et−1

[

ε2t]2}

− 3{

E[

Et−1

(

ε2t)]}2

E[

ε4t]

= 3[

E(

ε2t)]2

+ 3E{

Et−1

[

ε2t]2}

− 3{

E[

Et−1

(

ε2t)]}2

k =E[

ε4t]

[E (ε2t )]2 = 3 + 3

E{

Et−1

[

ε2t]2}

−{

E[

Et−1

(

ε2t)]}2

[E (ε2t )]2

= 3 + 3V ar

{

Et−1

[

ε2t]}

[E (ε2t )]2 = 3 + 3

V ar{

σ2t

}

[E (ε2t )]2 .

Eduardo Rossi c© - Econometria mercati finanziari (avanzato) 17

The ARCH(q) Model

Another important property of the ARCH process is that the process

is conditionally serially uncorrelated. Given that

Et−1 [εt] = 0

we have that with the Law of Iterated Expectations:

Et−h [εt] = Et−h [Et−1 (εt)] = Et−h [0] = 0.

This orthogonality property implies that the {εt} process is

conditionally uncorrelated:

Covt−h [εt, εt+k] = Et−h [εtεt+k] −Et−h [εt]Et−h [εt+k] =

= Et−h [εtεt+k] = Et−h [Et+k−1 (εtεt+k)] =

= Et−h [εtEt+k−1 [εt+k]] = 0

The ARCH model has showed to be particularly useful in modeling

the temporal dependencies in asset returns.

Eduardo Rossi c© - Econometria mercati finanziari (avanzato) 18

The ARCH(q) Model

The ARCH (q) model introduced by Engle (Engle (1982)) is a linear

function of past squared disturbances:

σ2t = ω +

q∑

i=1

αiε2t−i (6)

In this model to assure a positive conditional variance the parameters

have to satisfy the following constraints: ω > 0 e

α1 ≥ 0, α2 ≥ 0, . . . , αq ≥ 0. Defining

σ2t ≡ ε2t − vt

where Et−1 (vt) = 0 we can write (6) as an AR(q) in ε2t :

ε2t = ω + α (L) ε2t + vt

where α (L) = α1L+ α2L2 + . . .+ αqL

q.

Eduardo Rossi c© - Econometria mercati finanziari (avanzato) 19

The ARCH(q) Model

(1 − α(L))ε2t = ω + vt

The process is weakly stationary if and only ifq∑

i=1

αi < 1; in this case

the unconditional variance is given by

E(

ε2t)

= ω/ (1 − α1 − . . .− αq) . (7)

Eduardo Rossi c© - Econometria mercati finanziari (avanzato) 20

The ARCH(q) Model

The process is characterised by leptokurtosis in excess with respect

to the normal distribution. In the case, for example, of ARCH(1)

with εt |Φt−1 ∼ N(

0, σ2t

)

, the kurtosis is equal to:

E(

ε4t)

/E(

ε2t)2

= 3(

1 − α21

)

/(

1 − 3α21

)

(8)

with 3α21 < 1, when 3α2

1 = 1 we have

E(

ε4t)

/E(

ε2t)2

= ∞.

In both cases we obtain a kurtosis coefficient greater than 3,

characteristic of the normal distribution.

Eduardo Rossi c© - Econometria mercati finanziari (avanzato) 21

The ARCH(q) Model

The result is readily obtained:

E(

ε4t)

= 3E(

σ4t

)

E(

ε4t)

= 3[

ω2 + α21E(

ε4t−1

)

+ 2ωα1E(

ε2t−1

)]

E(

ε4t)

=3[

ω2 + 2ωα1E(

ε2t−1

)]

(1 − 3α21)

=3[

ω2 + 2ωα1σ2]

(1 − 3α21)

Eduardo Rossi c© - Econometria mercati finanziari (avanzato) 22

The ARCH(q) Model

substituting σ2 = ω/ (1 − α1):

E(

ε4t)

=3[

ω2 (1 − α1) + 2ω2α1

]

(1 − 3α21) (1 − α1)

=3ω2 (1 + α1)

(1 − 3α21) (1 − α1)

finally

E(

ε4t)

/E(

ε2t)2

=3ω2 (1 + α1) (1 − α1)

2

(1 − 3α21) (1 − α1)ω2

=3(

1 − α21

)

1 − 3α21

. (9)

Eduardo Rossi c© - Econometria mercati finanziari (avanzato) 23

The ARCH Regression Model

We have an ARCH regression model when the disturbances in a

linear regression model follow an ARCH process:

yt = x′tb+ εt

Et−1 (εt) = 0

εt |Φt−1 ∼ N(

0, σ2t

)

Et−1

(

ε2t)

≡ σ2t = ω + α (L) ε2t

Eduardo Rossi c© - Econometria mercati finanziari (avanzato) 24

The GARCH(p,q) Model

In order to model in a parsimonious way the conditional

heteroskedasticity, Bollerslev (1986) proposed the Generalised ARCH

model, i.e GARCH(p,q):

σ2t = ω + α (L) ε2t + β (L)σ2

t . (10)

where α (L) = α1L+ . . .+ αqLq, β (L) = β1L+ . . .+ βpL

p.

The GARCH(1,1) is the most popular model in the empirical

literature:

σ2t = ω + α1ε

2t−1 + β1σ

2t−1. (11)

Eduardo Rossi c© - Econometria mercati finanziari (avanzato) 25

The GARCH(p,q) Model

To ensure that the conditional variance is well defined in a

GARCH (p,q) model all the coefficients in the corresponding linear

ARCH (∞) should be positive:

σ2t =

(

1 −

p∑

i=1

βiLi

)

−1

ω +

q∑

j=1

αjε2t−j

= ω∗ +∞∑

k=0

φkε2t−k−1 (12)

σ2t ≥ 0 if ω∗ ≥ 0 and all φk ≥ 0.

The non-negativity of ω∗ and φk is also a necessary condition for the

non negativity of σ2t .

Eduardo Rossi c© - Econometria mercati finanziari (avanzato) 26

The GARCH(p,q) Model

In order to make ω∗ e {φk}∞

k=0 well defined, assume that :

i. the roots of the polynomial β (x) = 1 lie outside the unit circle,

and that ω ≥ 0, this is a condition for ω∗ to be finite and positive.

ii. α (x) e 1 − β (x) have no common roots.

Eduardo Rossi c© - Econometria mercati finanziari (avanzato) 27

The GARCH(p,q) Model

These conditions are establishing nor that σ2t ≤ ∞ neither that

{

σ2t

}

∞

t=−∞is strictly stationary. For the simple GARCH(1,1) almost

sure positivity of σ2t requires, with the conditions (i) and (ii), that

(Nelson and Cao, 1992),

ω ≥ 0

β1 ≥ 0

α1 ≥ 0 (13)

Eduardo Rossi c© - Econometria mercati finanziari (avanzato) 28

The GARCH(p,q) Model

For the GARCH(1,q) and GARCH(2,q) models these constraints can

be relaxed, e.g. in the GARCH(1,2) model the necessary and

sufficient conditions become:

ω ≥ 0

0 ≤ β1 < 1

β1α1 + α2 ≥ 0

α1 ≥ 0 (14)

Eduardo Rossi c© - Econometria mercati finanziari (avanzato) 29

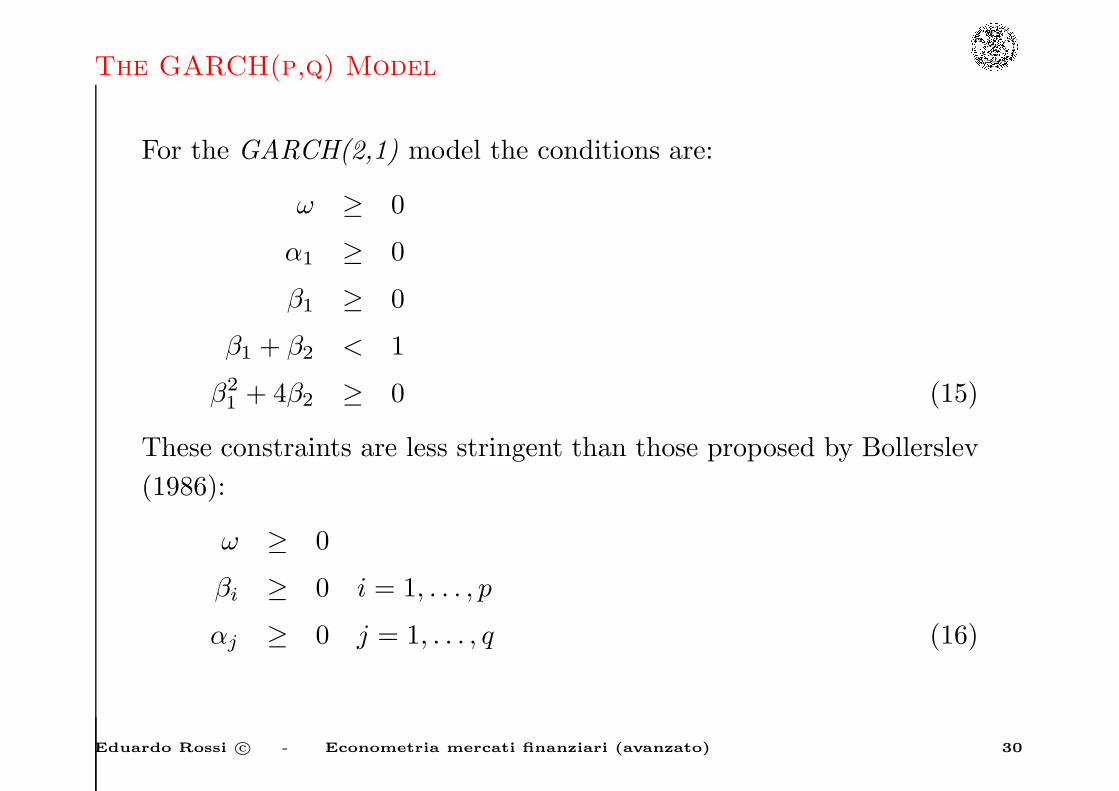

The GARCH(p,q) Model

For the GARCH(2,1) model the conditions are:

ω ≥ 0

α1 ≥ 0

β1 ≥ 0

β1 + β2 < 1

β21 + 4β2 ≥ 0 (15)

These constraints are less stringent than those proposed by Bollerslev

(1986):

ω ≥ 0

βi ≥ 0 i = 1, . . . , p

αj ≥ 0 j = 1, . . . , q (16)

Eduardo Rossi c© - Econometria mercati finanziari (avanzato) 30

The GARCH(p,q) Model

These results cannot be adopted in the multivariate case, where the

requirement of positivity for{

σ2t

}

means the positive definiteness for

the conditional variance-covariance matrix.

Eduardo Rossi c© - Econometria mercati finanziari (avanzato) 31

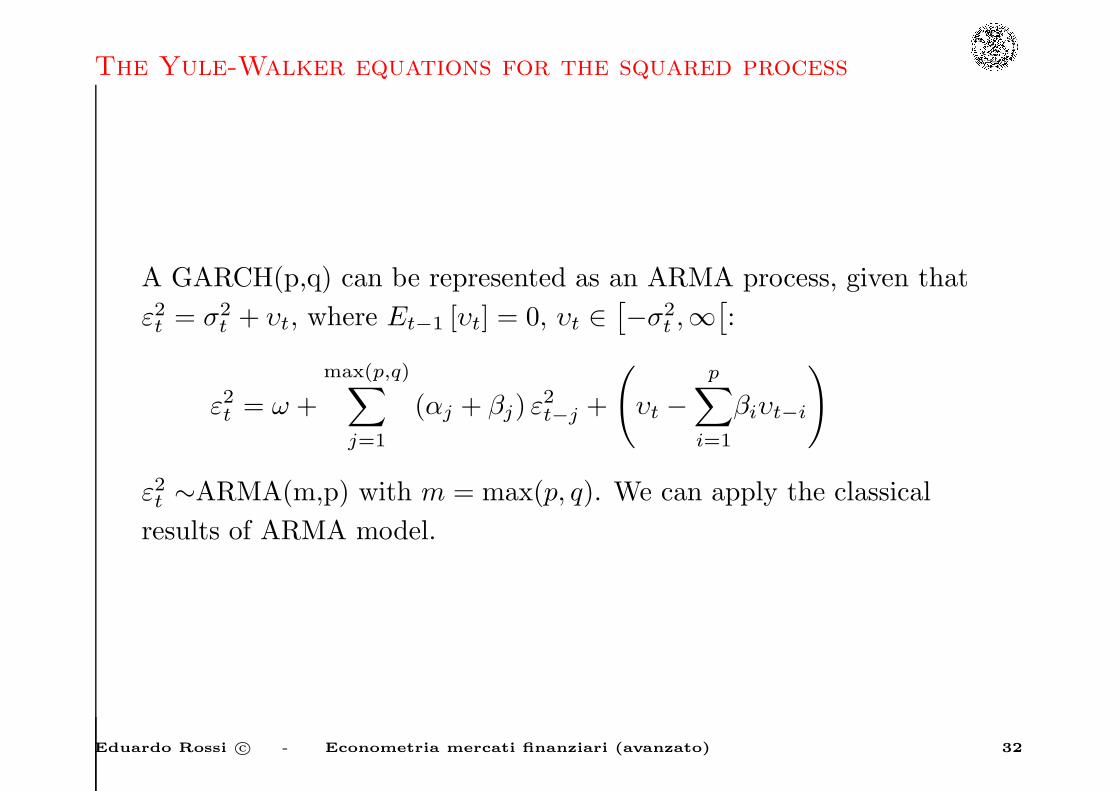

The Yule-Walker equations for the squared process

A GARCH(p,q) can be represented as an ARMA process, given that

ε2t = σ2t + υt, where Et−1 [υt] = 0, υt ∈

[

−σ2t ,∞

[

:

ε2t = ω +

max(p,q)∑

j=1

(αj + βj) ε2t−j +

(

υt −

p∑

i=1

βiυt−i

)

ε2t ∼ARMA(m,p) with m = max(p, q). We can apply the classical

results of ARMA model.

Eduardo Rossi c© - Econometria mercati finanziari (avanzato) 32

The Yule-Walker equations for the squared process

Example: GARCH(1,1)

σ2t = ω + α1ε

2t−1 + β1σ

2t−1

replacing σ2t with ε2t − υt, we obtain

ε2t − υt = ω + α1ε2t−1 + β1(ε

2t−1 − υt−1)

hence

ε2t = ω + (α1 + β1)ε2t−1 + υt − β1υt−1

Eduardo Rossi c© - Econometria mercati finanziari (avanzato) 33

The Yule-Walker equations for the squared process

We can study the autocovariance function, that is:

γ2 (k) = cov(

ε2t , ε2t−k

)

γ2 (k) = cov

ω +

m∑

j=1

(αj + βj) ε2t−j +

(

υt −

p∑

i=1

βiυt−i

)

, ǫ2t−k

γ2 (k) =

m∑

j=1

(αj + βj) cov(

ε2t−j , ε2t−k

)

+cov

[

υt −

p∑

i=1

βiυt−i, ε2t−k

]

(17)

When k is big enough, the last term on the right of expression (17) is

null.

Eduardo Rossi c© - Econometria mercati finanziari (avanzato) 34

The Yule-Walker equations for the squared process

The sequence of autocovariances satisfy a linear difference equation

of order max (p, q), for k ≥ p+ 1

γ2 (k) =

m∑

j=1

(αj + βj) γ2 (k − j)

This system can be used to identify the lag order m and p, that is the

p and q order if q ≥ p, the order p if q < p.

Eduardo Rossi c© - Econometria mercati finanziari (avanzato) 35

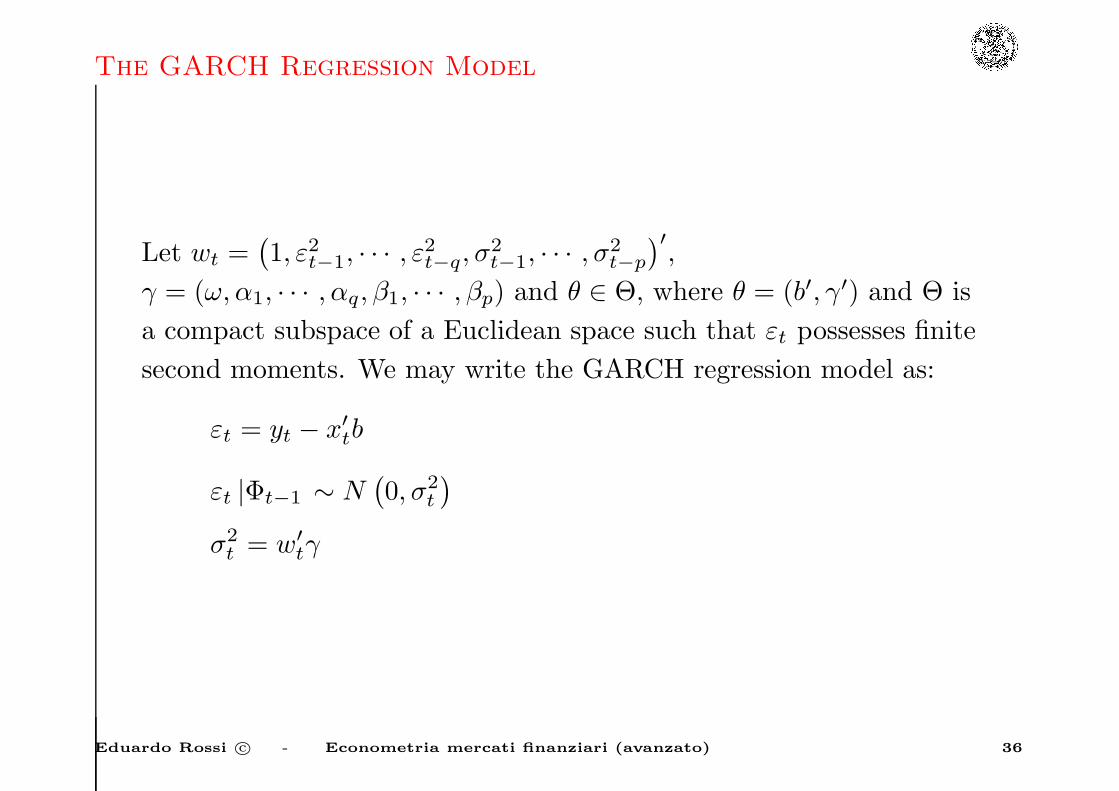

The GARCH Regression Model

Let wt =(

1, ε2t−1, · · · , ε2t−q, σ

2t−1, · · · , σ

2t−p

)

′

,

γ = (ω, α1, · · · , αq, β1, · · · , βp) and θ ∈ Θ, where θ = (b′, γ′) and Θ is

a compact subspace of a Euclidean space such that εt possesses finite

second moments. We may write the GARCH regression model as:

εt = yt − x′tb

εt |Φt−1 ∼ N(

0, σ2t

)

σ2t = w′

tγ

Eduardo Rossi c© - Econometria mercati finanziari (avanzato) 36

Stationarity

The process {εt} which follows a GARCH(p,q) model is a martingale

difference sequence. In order to study second-order stationarity it’s

sufficient to consider that:

V ar [εt] = V ar [Et−1 (εt)] +E [V art−1 (εt)] = E[

σ2t

]

and show that is asymptotically constant in time (it does not depend

upon time).

A process {εt} which satisfies a GARCH(p,q) model with positive

coefficient ω ≥ 0, αi ≥ 0 i = 1, . . . , q, βi ≥ 0 i = 1, . . . , p is covariance

stationary if and only if:

α (1) + β(1) < 1

Eduardo Rossi c© - Econometria mercati finanziari (avanzato) 37

Stationarity

This is a sufficient but non necessary conditions for strict

stationarity. Because ARCH processes are thick tailed, the conditions

for covariance stationarity are often more stringent than the

conditions for strict stationarity.

A GARCH(1,1) model can be written as

σ2t = ω

[

1 +∞∑

k=1

k∏

i=1

(

β1 + α1z2t−i

)

]

Eduardo Rossi c© - Econometria mercati finanziari (avanzato) 38

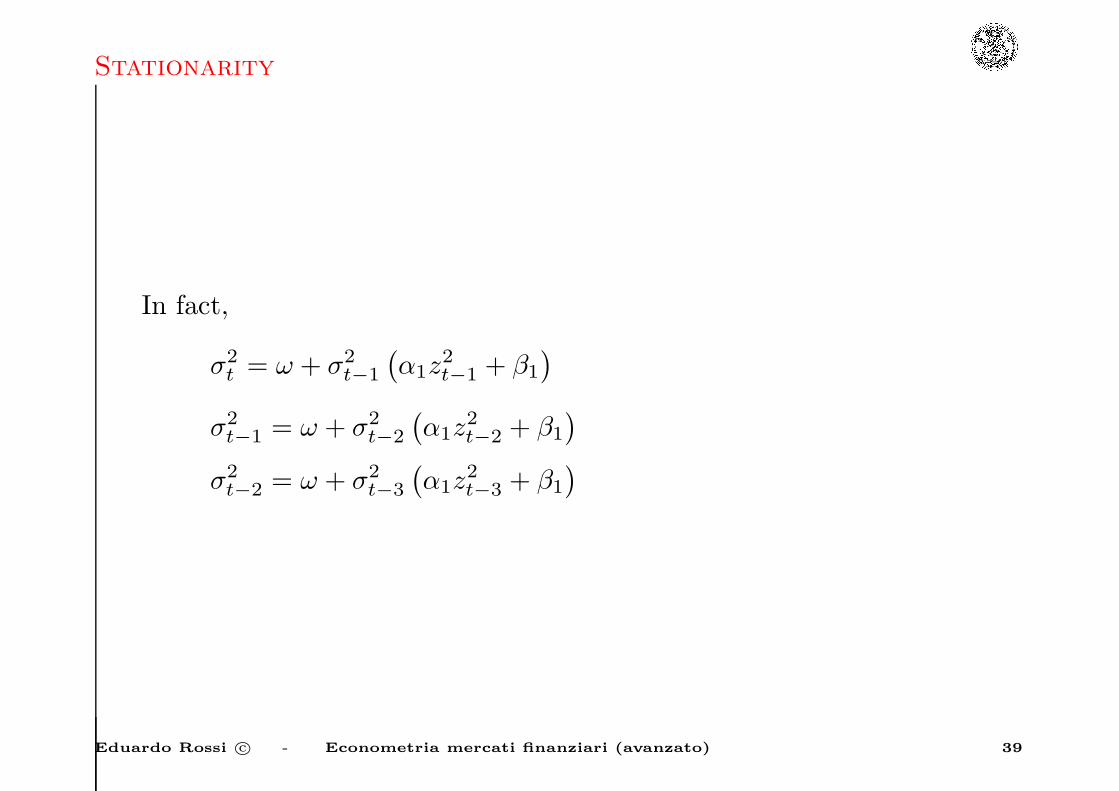

Stationarity

In fact,

σ2t = ω + σ2

t−1

(

α1z2t−1 + β1

)

σ2t−1 = ω + σ2

t−2

(

α1z2t−2 + β1

)

σ2t−2 = ω + σ2

t−3

(

α1z2t−3 + β1

)

Eduardo Rossi c© - Econometria mercati finanziari (avanzato) 39

Stationarity

σ2t = ω +

[

ω + σ2t−2

(

α1z2t−2 + β1

)] (

α1z2t−1 + β1

)

= ω + ω(

α1z2t−1 + β1

)

+ σ2t−2

(

α1z2t−2 + β1

) (

α1z2t−1 + β1

)

= ω + ω(

α1z2t−1 + β1

)

+ ω(

α1z2t−1 + β1

) (

α1z2t−2 + β1

)

+σ2t−3

(

α1z2t−3 + β1

) (

α1z2t−2 + β1

) (

α1z2t−1 + β1

)

finally,

σ2t = ω

[

1 +∞∑

k=1

k∏

i=1

(

α1z2t−i + β1

)

]

Eduardo Rossi c© - Econometria mercati finanziari (avanzato) 40

Stationarity

Nelson shows that when ω > 0, σ2t <∞ a.s. and

{

εt, σ2t

}

is strictly

stationary if and only if E[

ln(

β1 + α1z2t

)]

< 0

E[

ln(

β1 + α1z2t

)]

≤ ln[

E(

β1 + α1z2t

)]

= ln (α1 + β1)

when α1 + β1 = 1 the model is strictly stationary.

E[

ln(

β1 + α1z2t

)]

< 0 is a weaker requirement than α1 + β1 < 1.

Eduardo Rossi c© - Econometria mercati finanziari (avanzato) 41

Stationarity

Example

ARCH(1), with α1 = 1, β1 = 0, zt ∼ N (0, 1)

E[

ln(

z2t

)]

≤ ln[

E(

z2t

)]

= ln (1)

It’s strictly but not covariance stationary. The ARCH(q) is

covariance stationary if and only if the sum of the positive

parameters is less than one.

Eduardo Rossi c© - Econometria mercati finanziari (avanzato) 42

Forecasting volatility

Forecasting with a GARCH(p,q) (Engle and Bollerslev 1986):

σ2t+k = ω +

q∑

i=1

αiε2t+k−i +

p∑

i=1

βiσ2t+k−i

we can write the process in two parts, before and after time t:

σ2t+k = ω+

n∑

i=1

[

αiε2t+k−i + βiσ

2t+k−i

]

+m∑

i=k

[

αiε2t+k−i + βiσ

2t+k−i

]

where n = min {m, k − 1} and by definition summation from 1 to 0

and from k > m to m both are equal to zero.

Eduardo Rossi c© - Econometria mercati finanziari (avanzato) 43

Forecasting volatility

Thus

Et

[

σ2t+k

]

= ω+n∑

i=1

[

(αi + βi)Et

(

σ2t+k−i

)]

+m∑

i=k

[

αiε2t+k−i + βiσ

2t+k−i

]

.

Eduardo Rossi c© - Econometria mercati finanziari (avanzato) 44

Forecasting volatility

In particular for a GARCH(1,1) and k > 2:

Et

[

σ2t+k

]

=k−2∑

i=0

(α1 + β1)i ω + (α1 + β1)

k−1 σ2t+1

= ω

[

1 − (α1 + β1)k−1]

[1 − (α1 + β1)]+ (α1 + β1)

k−1 σ2t+1

= σ2[

1 − (α1 + β1)k−1]

+ (α1 + β1)k−1

σ2t+1

= σ2 + (α1 + β1)k−1 [

σ2t+1 − σ2

]

When the process is covariance stationary, it follows that Et

[

σ2t+k

]

converges to σ2 as k → ∞.

Eduardo Rossi c© - Econometria mercati finanziari (avanzato) 45

The IGARCH(p,q) model

The GARCH(p,q) process characterized by the first two conditional

moments:

Et−1 [εt] = 0

σ2t ≡ Et−1

[

ε2t]

= ω +

q∑

i=1

αiε2t−i +

p∑

i=1

βiσ2t−i

where ω ≥ 0, αi ≥ 0 and βi ≥ 0 for all i and the polynomial

1 − α (x) − β(x) = 0

has d > 0 unit root(s) and max {p, q} − d root(s) outside the unit

circle is said to be:

Eduardo Rossi c© - Econometria mercati finanziari (avanzato) 46

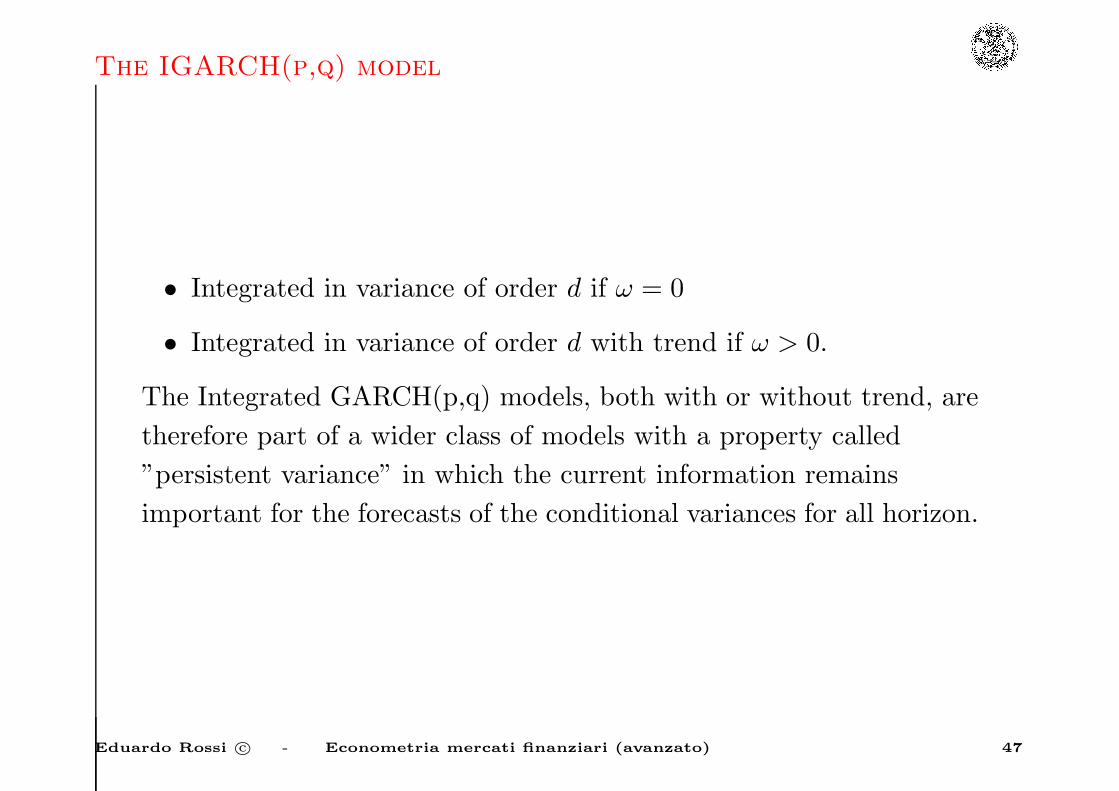

The IGARCH(p,q) model

• Integrated in variance of order d if ω = 0

• Integrated in variance of order d with trend if ω > 0.

The Integrated GARCH(p,q) models, both with or without trend, are

therefore part of a wider class of models with a property called

”persistent variance” in which the current information remains

important for the forecasts of the conditional variances for all horizon.

Eduardo Rossi c© - Econometria mercati finanziari (avanzato) 47

The IGARCH(p,q) model

So we have the Integrated GARCH(p,q) model when (necessary

condition)

α (1) + β(1) = 1

To illustrate consider the IGARCH(1,1) which is characterised by

α1 + β1 = 1

σ2t = ω + α1ε

2t−1 + (1 − α1)σ

2t−1

σ2t = ω + σ2

t−1 + α1

(

ε2t−1 − σ2t−1

)

0 < α1 ≤ 1

For this particular model the conditional variance k steps in the

future is:

Et

[

σ2t+k

]

= (k − 1)ω + σ2t+1

Eduardo Rossi c© - Econometria mercati finanziari (avanzato) 48

Persistence

• In many studies of the time series behavior of asset volatility the

question has been how long shocks to conditional variance persist.

• If volatility shocks persist indefinitely, they may move the whole

term structure of risk premia.

• There are many notions of convergence in the probability theory

(almost sure, in probability, in Lp), so whether a shock is

transitory or persistent may depend on the definition of

convergence.

Eduardo Rossi c© - Econometria mercati finanziari (avanzato) 49

Persistence

• In linear models it typically makes no difference which of the

standard definitions we use, since the definitions usually agree.

• In GARCH models the situation is more complicated.

In the IGARCH(1,1):

σ2t = ω + α1ε

2t−1 + β1σ

2t−1

where α1 + β1 = 1. Given that ε2t = z2t σ

2t , we can rewrite the

IGARCH(1,1) process as

σ2t = ω + σ2

t−1

[

(1 − α1) + α1z2t−1

]

0 < α1 ≤ 1.

When ω = 0, σ2t is a martingale.

Eduardo Rossi c© - Econometria mercati finanziari (avanzato) 50

Persistence

Based on the nature of persistence in linear models, it seems that

IGARCH(1,1) with ω > 0 and ω = 0 are analogous to random walks

with and without drift, respectively, and are therefore natural models

of ”persistent” shocks.

This turns out to be misleading, however:

• in IGARCH(1,1) with ω = 0, σ2t collapses to zero almost

surely

• in IGARCH(1,1) with ω > 0, σ2t is strictly stationary and ergodic

and therefore does not behave like a random walk, since random

walks diverge almost surely.

Eduardo Rossi c© - Econometria mercati finanziari (avanzato) 51

Persistence

Two notions of persistence.

1. Suppose σ2t is strictly stationary and ergodic. Let F

(

σ2t

)

be the

unconditional cdf for σ2t , and Fs

(

σ2t

)

the conditional cdf for σ2t ,

given information at time s < t. For any s F(

σ2t

)

− Fs

(

σ2t

)

→ 0

at all continuity points as t→ ∞. There is no persistence when{

σ2t

}

is stationary and ergodic.

2. Persistence is defined in terms of forecast moments. For some

η > 0, the shocks to σ2t fail to persist if and only if for every s,

Es

(

σ2ηt

)

converges, as t→ ∞, to a finite limit independent of

time s information set.

Eduardo Rossi c© - Econometria mercati finanziari (avanzato) 52

Persistence

Whether or not shocks to{

σ2t

}

”persist” depends very much on

which definition is adopted. The conditional moment may diverge to

infinity for some η, but converge to a well-behaved limit independent

of initial conditions for other η, even when the{

σ2t

}

is stationary and

ergodic.

Eduardo Rossi c© - Econometria mercati finanziari (avanzato) 53

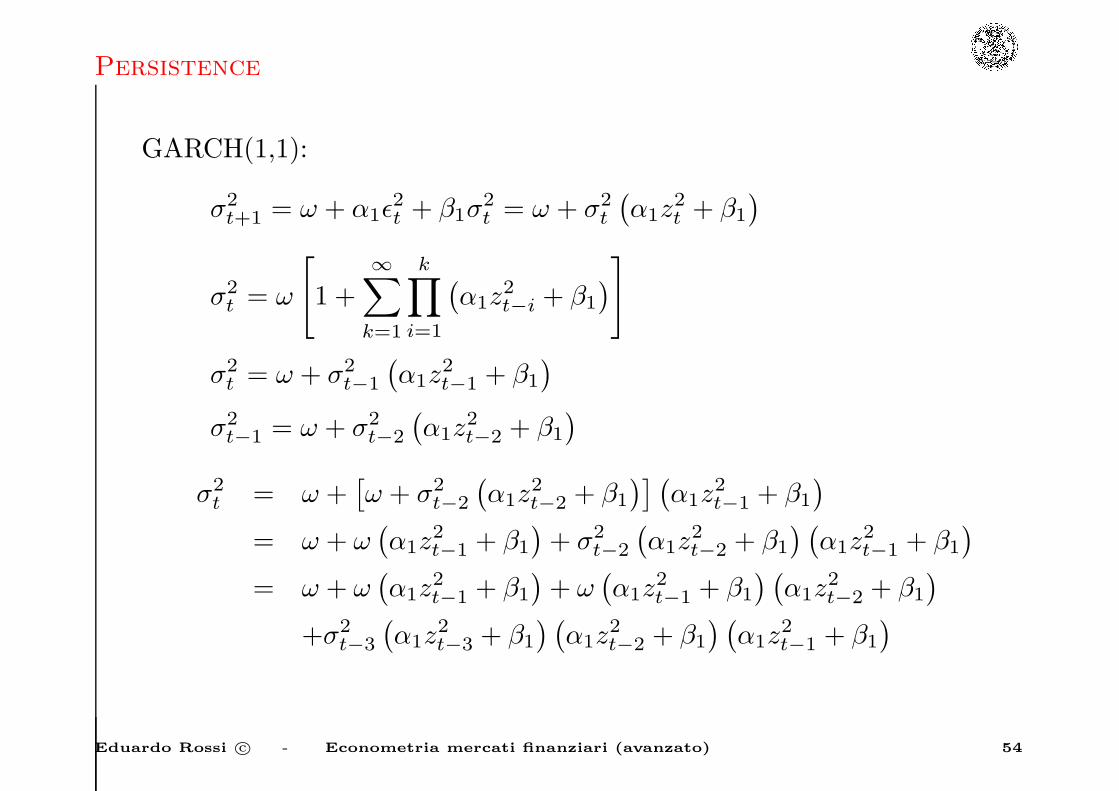

Persistence

GARCH(1,1):

σ2t+1 = ω + α1ǫ

2t + β1σ

2t = ω + σ2

t

(

α1z2t + β1

)

σ2t = ω

[

1 +∞∑

k=1

k∏

i=1

(

α1z2t−i + β1

)

]

σ2t = ω + σ2

t−1

(

α1z2t−1 + β1

)

σ2t−1 = ω + σ2

t−2

(

α1z2t−2 + β1

)

σ2t = ω +

[

ω + σ2t−2

(

α1z2t−2 + β1

)] (

α1z2t−1 + β1

)

= ω + ω(

α1z2t−1 + β1

)

+ σ2t−2

(

α1z2t−2 + β1

) (

α1z2t−1 + β1

)

= ω + ω(

α1z2t−1 + β1

)

+ ω(

α1z2t−1 + β1

) (

α1z2t−2 + β1

)

+σ2t−3

(

α1z2t−3 + β1

) (

α1z2t−2 + β1

) (

α1z2t−1 + β1

)

Eduardo Rossi c© - Econometria mercati finanziari (avanzato) 54

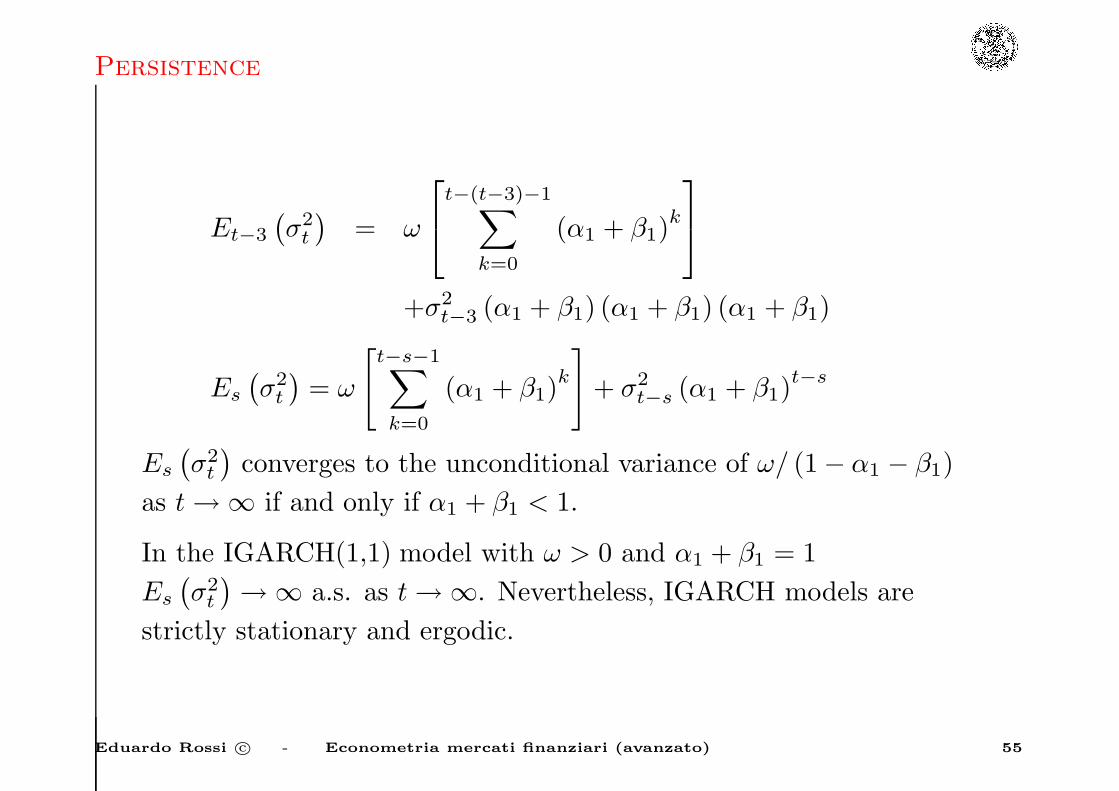

Persistence

Et−3

(

σ2t

)

= ω

t−(t−3)−1∑

k=0

(α1 + β1)k

+σ2t−3 (α1 + β1) (α1 + β1) (α1 + β1)

Es

(

σ2t

)

= ω

[

t−s−1∑

k=0

(α1 + β1)k

]

+ σ2t−s (α1 + β1)

t−s

Es

(

σ2t

)

converges to the unconditional variance of ω/ (1 − α1 − β1)

as t→ ∞ if and only if α1 + β1 < 1.

In the IGARCH(1,1) model with ω > 0 and α1 + β1 = 1

Es

(

σ2t

)

→ ∞ a.s. as t→ ∞. Nevertheless, IGARCH models are

strictly stationary and ergodic.

Eduardo Rossi c© - Econometria mercati finanziari (avanzato) 55

The EGARCH(p,q) Model

• GARCH models assume that only the magnitude and not the

positivity or negativity of unanticipated excess returns

determines feature σ2t .

• There exists a negative correlation between stock returns and

changes in returns volatility, i.e. volatility tends to rise in

response to ”bad news”, (excess returns lower than expected)

and to fall in response to ”good news” (excess returns higher

than expected).

Eduardo Rossi c© - Econometria mercati finanziari (avanzato) 56

The EGARCH(p,q) Model

If we write σ2t as a function of lagged σ2

t and lagged z2t , where

ε2t = z2t σ

2t

σ2t = ω +

q∑

j=1

αjz2t−jσ

2t−j +

p∑

i=1

βiσ2t−i

it is evident that the conditional variance is invariant to changes in

sign of the z′ts. Moreover, the innovations z2t−jσ

2t−j are not i.i.d.

• The nonnegativity constraints on ω∗ and φk, which are imposed

to ensure that σ2t remains nonnegative for all t with probability

one. These constraints imply that increasing z2t in any period

increases σ2t+m for all m ≥ 1, ruling out random oscillatory

behavior in the σ2t process.

Eduardo Rossi c© - Econometria mercati finanziari (avanzato) 57

The EGARCH(p,q) Model

• The GARCH models are not able to explain the observed

covariance between ε2t and εt−j . This is possible only if the

conditional variance is expressed as an asymmetric function of

εt−j .

• In GARCH(1,1) models, shocks may persist in one norm and die

out in another, so the conditional moments of GARCH(1,1) may

explode even when the process is strictly stationary and ergodic.

• GARCH models essentially specify the behavior of the square of

the data. In this case a few large observations can dominate the

sample.

Eduardo Rossi c© - Econometria mercati finanziari (avanzato) 58

The EGARCH(p,q) Model

In the EGARCH(p,q) model (Exponential GARCH(p,q)) put forward

by Nelson the σ2t depends on both size and the sign of lagged

residuals. This is the first example of asymmetric model:

ln(

σ2t

)

= ω +

p∑

i=1

βi ln(

σ2t−i

)

+

q∑

i=1

αi [φzt−i + ψ (|zt−i| −E |zt−i|)]

α1 ≡ 1, E |zt| = (2/π)1/2given that zt ∼ NID(0, 1), where the

parameters ω, βi, αi are not restricted to be nonnegative. Let define

g (zt) ≡ φzt + ψ [|zt| −E |zt|]

by construction {g (zt)}∞

t=−∞is a zero-mean, i.i.d. random sequence.

Eduardo Rossi c© - Econometria mercati finanziari (avanzato) 59

The EGARCH(p,q) Model

• The components of g (zt) are φzt and ψ [|zt| −E |zt|], each with

mean zero.

• If the distribution of zt is symmetric, the components are

orthogonal, but not independent.

• Over the range 0 < zt <∞, g (zt) is linear in zt with slope φ+ ψ,

and over the range −∞ < zt ≤ 0, g (zt) is linear with slope φ−ψ.

• The term ψ [|zt| −E |zt|] represents a magnitude effect.

Eduardo Rossi c© - Econometria mercati finanziari (avanzato) 60

The EGARCH(p,q) Model

• If ψ > 0 and φ = 0, the innovation in ln(

σ2t+1

)

is positive

(negative) when the magnitude of zt is larger (smaller) than its

expected value.

• If ψ = 0 and φ < 0, the innovation in conditional variance is now

positive (negative) when returns innovations are negative

(positive).

• A negative shock to the returns which would increase the debt to

equity ratio and therefore increase uncertainty of future returns

could be accounted for when αi > 0 and φ < 0.

Eduardo Rossi c© - Econometria mercati finanziari (avanzato) 61

The EGARCH(p,q) Model

In the EGARCH model ln(

σ2t+1

)

is homoskedastic conditional on σ2t ,

and the partial correlation between zt and ln(

σ2t+1

)

is constant

conditional on σ2t .

An alternative possible specification of the news impact curve is the

following (Bollerslev, Engle, Nelson (1994))

g(zt, σ2t ) = σ−2θ0

t

θ1zt

1 + θ2 |zt|+σ−2γ0

t

[

γ1 |zt|ρ

1 + γ2 |zt|ρ − Et

(

γ1 |zt|ρ

1 + γ2 |zt|ρ

)]

The parameters γ0 and θ0 parameters allow both the conditional

variance of ln(

σ2t+1

)

and its conditional correlation with zt to vary

with the level of σ2t .

Eduardo Rossi c© - Econometria mercati finanziari (avanzato) 62

The EGARCH(p,q) Model

If θ1 < 0 then Corrt(ln(

σ2t+1

)

, zt) < 0: leverage effect.

The EGARCH model constraints θ0 = γ0 = 0, so that the conditional

correlation is constant, as is the conditional variance of ln(

σ2t

)

.

The ρ, γ2, and θ2 parameters give the model flexibility in how much

weight to assign to the tail observations: e.g., γ2 > 0, θ2 > 0, the

model downweights large |zt|’s.

Nelson assumes that zt has a GED distribution (exponential power

family). The density of a GED random variable normalized is:

f (z; υ) =υ exp

[

−(

12

)

|z/λ|υ]

λ2(1+1/υ)Γ (1/υ)−∞ < z <∞, 0 < υ ≤ ∞

Eduardo Rossi c© - Econometria mercati finanziari (avanzato) 63

The EGARCH(p,q) Model

where Γ (·) is the gamma function, and

λ ≡[

2(−2/υ)Γ (1/υ) /Γ (3/υ)]1/2

υ is a tail thickness parameter.

z’s distribution

υ = 2 standard normal distribution

υ < 2 thicker tails than the normal

υ = 1 double exponential distribution

υ > 2 thinner tails than the normal

υ = ∞ uniformly distributed on[

−31/2, 31/2]

With this density, E |zt| =λ21/υΓ (2/υ)

Γ (1/υ).

Eduardo Rossi c© - Econometria mercati finanziari (avanzato) 64

The EGARCH(p,q) Model

The Generalized t Distribution takes the form:

f(

εtσ−1t ; η, ζ

)

=η

2σtbζ1/ηB (1/η, ζ) [1 + |εt|η / (ζbηση

t )]ζ+1/η

where B (1/η, ζ) ≡ Γ (1/η) Γ (ζ) Γ (1/η + ζ) denotes the beta function,

b ≡ [Γ (ζ) Γ (1/η) /Γ (3/η) Γ (ζ − 2/η)]1/2

and ζη > 2, η > 0 and ζ > 0. The factor b makes V ar(

εtσ−1t

)

= 1.

The Generalized t nests both the Student’s t distribution and the

GED.

Eduardo Rossi c© - Econometria mercati finanziari (avanzato) 65

The EGARCH(p,q) Model

The Student’s t-distribution sets η = 2 and ζ = 12 times the degree of

freedom

The GED is obtained for ζ = ∞. The GED has only one shape

parameter η, which is apparently insufficient to fit both the central

part and the tails of the conditional distribution.

Eduardo Rossi c© - Econometria mercati finanziari (avanzato) 66

Stationarity of EGARCH(p,q)

In order to simply state the stationarity conditions, we write the

EGARCH(p,q) model as:

[

1 −

p∑

i=1

βiLi

]

ln(

σ2t

)

= ω +

q∑

i=1

αiLi [φzt + ψ (|zt| −E |zt|)]

ln(

σ2t

)

=

[

1 −

p∑

i=1

βi

]

−1

ω +

[

1 −

p∑

i=1

βiLi

]

−1 [ q∑

i=1

αiLi

]

g (zt)

ln(

σ2t

)

= ω∗ +

∞∑

i=1

ϕig (zt−i)

Eduardo Rossi c© - Econometria mercati finanziari (avanzato) 67

Stationarity of EGARCH(p,q)

Given φ 6= 0 or ψ 6= 0, then

∣

∣ln(

σ2t

)

− ω∗∣

∣ <∞ a.s. when∞∑

i=1

ϕ2i <∞

follows from the independence and finite variance of the g (zt) and

from Billingsley (1986, Theorem 22.6). From this we have that∣

∣

∣

∣

ln

(

σ2t

exp(ω∗)

)∣

∣

∣

∣

< ∞ a.s.

∣

∣

∣

∣

σ2t

exp(ω∗)

∣

∣

∣

∣

< ∞ a.s.

{

exp (−ω∗)σ2t

}

<∞, {exp (−ω∗/2) εt} <∞, a.s., where εt = ztσt, zt

is i.i.d.. We can also show that they are ergodic and strictly

stationarity.

Eduardo Rossi c© - Econometria mercati finanziari (avanzato) 68

Stationarity of EGARCH(p,q)

The first two moments of ln(

σ2t

)

− ω∗ are finite and time invariant :

E[

ln(

σ2t

)

− ω∗]

= 0 for all t

V ar[

ln(

σ2t

)

− ω∗]

= V ar (g (zt))∞∑

i=1

ϕ2i

since V ar (g (zt)) is finite and the distribution of(

ln(

σ2t

)

− ω∗)

is

independent of t, the first two moments of(

ln(

σ2t

)

− ω∗)

are finite

and time invariant, so(

ln(

σ2t

)

− ω∗)

is covariance stationary if∞∑

i=1

ϕ2i <∞. If

∞∑

i=1

ϕ2i = ∞, then

∣

∣ln(

σ2t

)

− ω∗∣

∣ = ∞ almost surely.

Eduardo Rossi c© - Econometria mercati finanziari (avanzato) 69

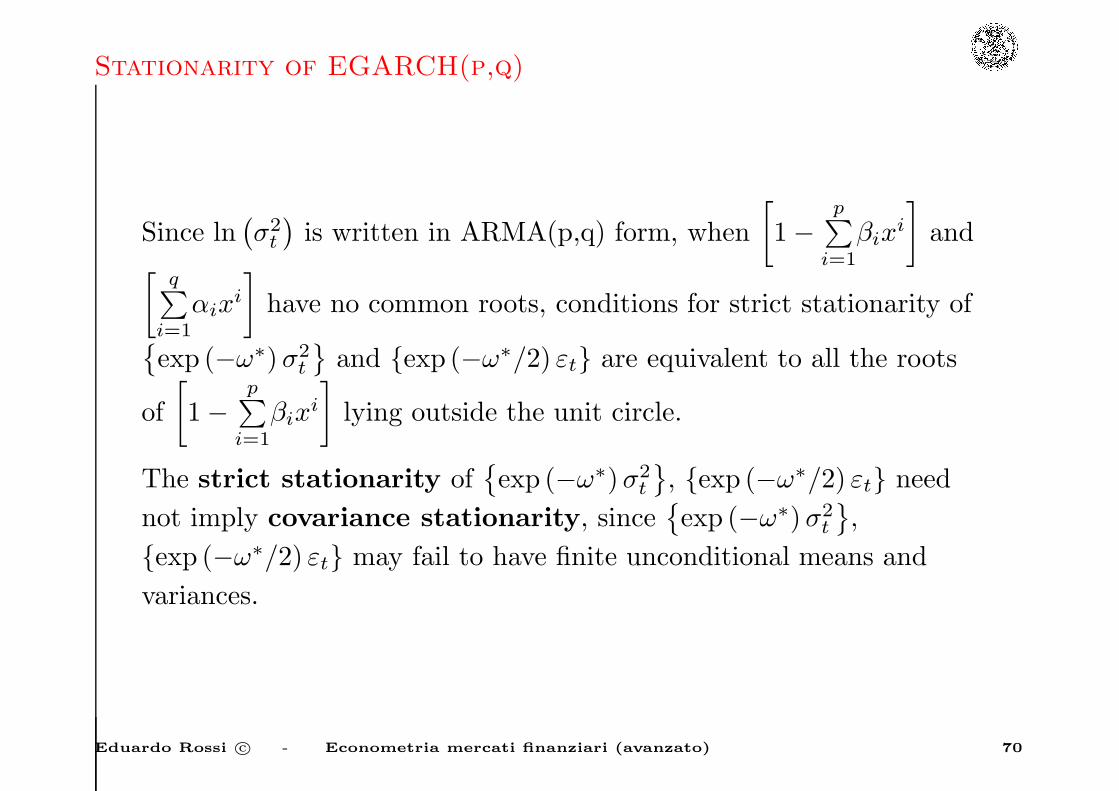

Stationarity of EGARCH(p,q)

Since ln(

σ2t

)

is written in ARMA(p,q) form, when

[

1 −p∑

i=1

βixi

]

and[

q∑

i=1

αixi

]

have no common roots, conditions for strict stationarity of{

exp (−ω∗)σ2t

}

and {exp (−ω∗/2) εt} are equivalent to all the roots

of

[

1 −p∑

i=1

βixi

]

lying outside the unit circle.

The strict stationarity of{

exp (−ω∗)σ2t

}

, {exp (−ω∗/2) εt} need

not imply covariance stationarity, since{

exp (−ω∗)σ2t

}

,

{exp (−ω∗/2) εt} may fail to have finite unconditional means and

variances.

Eduardo Rossi c© - Econometria mercati finanziari (avanzato) 70

Stationarity of EGARCH(p,q)

For some distribution of {zt} (e.g., the Student t with finite degrees

of freedom),{

exp (−ω∗)σ2t

}

and {exp (−ω∗/2) εt} typically have no

finite unconditional moments.

If the distribution of zt is GED and is thinner-tailed than the double

exponential (ν > 1), and if∞∑

i=1

ϕ2i <∞, then

{

exp (−ω∗)σ2t

}

and

{exp (−ω∗/2) εt} are not only strictly stationary and ergodic,

but have arbitrary finite moments, which in turn implies

that they are covariance stationary.

Eduardo Rossi c© - Econometria mercati finanziari (avanzato) 71

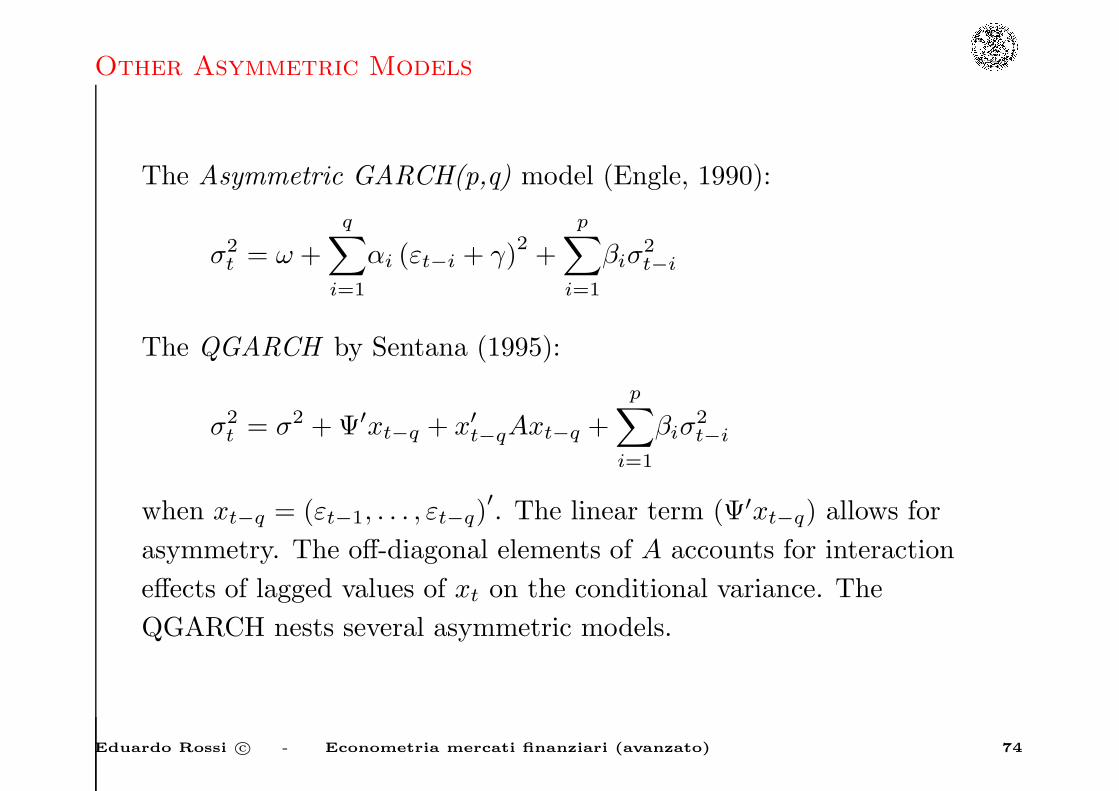

Other Asymmetric Models

The Non linear ARCH(p,q) model (Engle - Bollerslev 1986):

σγt = ω +

q∑

i=1

αi |εt−i|γ

+

p∑

i=1

βiσγt−i

σγt = ω +

q∑

i=1

αi |εt−i − k|γ

+

p∑

i=1

βiσγt−i

for k 6= 0, the innovations in σγt will depend on the size as well as the

sign of lagged residuals, thereby allowing for the leverage effect in

stock return volatility.

Eduardo Rossi c© - Econometria mercati finanziari (avanzato) 72

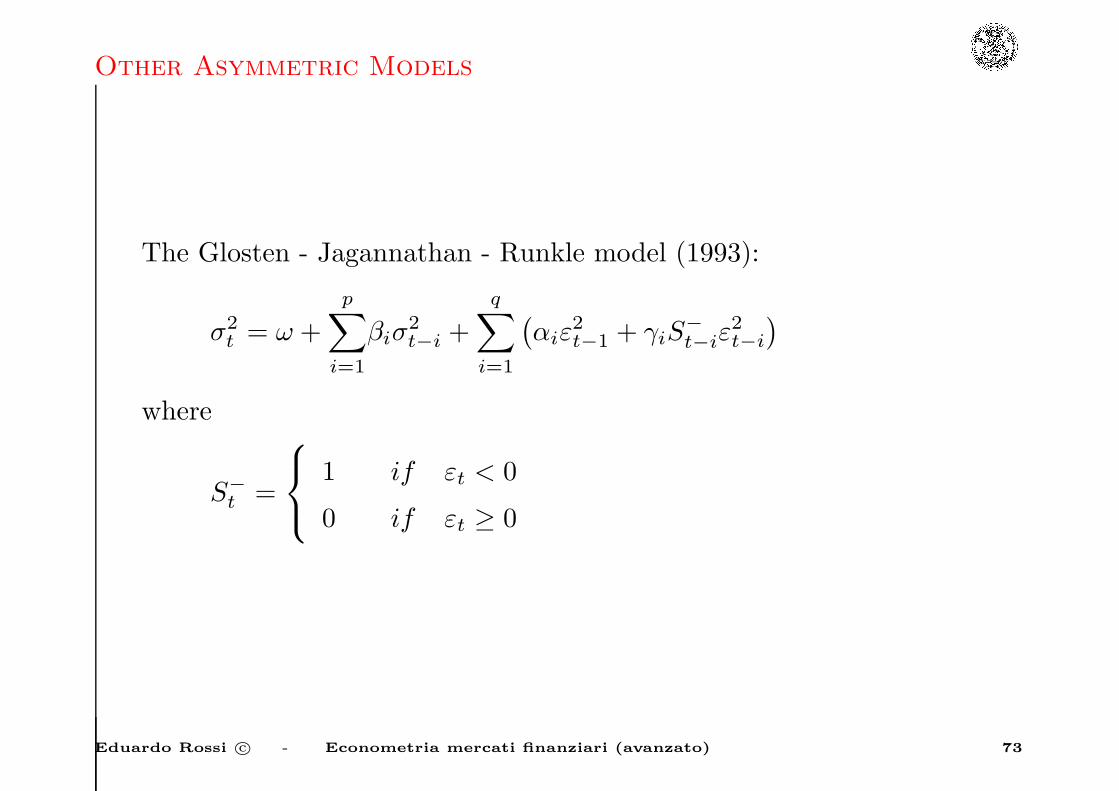

Other Asymmetric Models

The Glosten - Jagannathan - Runkle model (1993):

σ2t = ω +

p∑

i=1

βiσ2t−i +

q∑

i=1

(

αiε2t−1 + γiS

−

t−iε2t−i

)

where

S−

t =

1 if εt < 0

0 if εt ≥ 0

Eduardo Rossi c© - Econometria mercati finanziari (avanzato) 73

Other Asymmetric Models

The Asymmetric GARCH(p,q) model (Engle, 1990):

σ2t = ω +

q∑

i=1

αi (εt−i + γ)2

+

p∑

i=1

βiσ2t−i

The QGARCH by Sentana (1995):

σ2t = σ2 + Ψ′xt−q + x′t−qAxt−q +

p∑

i=1

βiσ2t−i

when xt−q = (εt−1, . . . , εt−q)′

. The linear term (Ψ′xt−q) allows for

asymmetry. The off-diagonal elements of A accounts for interaction

effects of lagged values of xt on the conditional variance. The

QGARCH nests several asymmetric models.

Eduardo Rossi c© - Econometria mercati finanziari (avanzato) 74

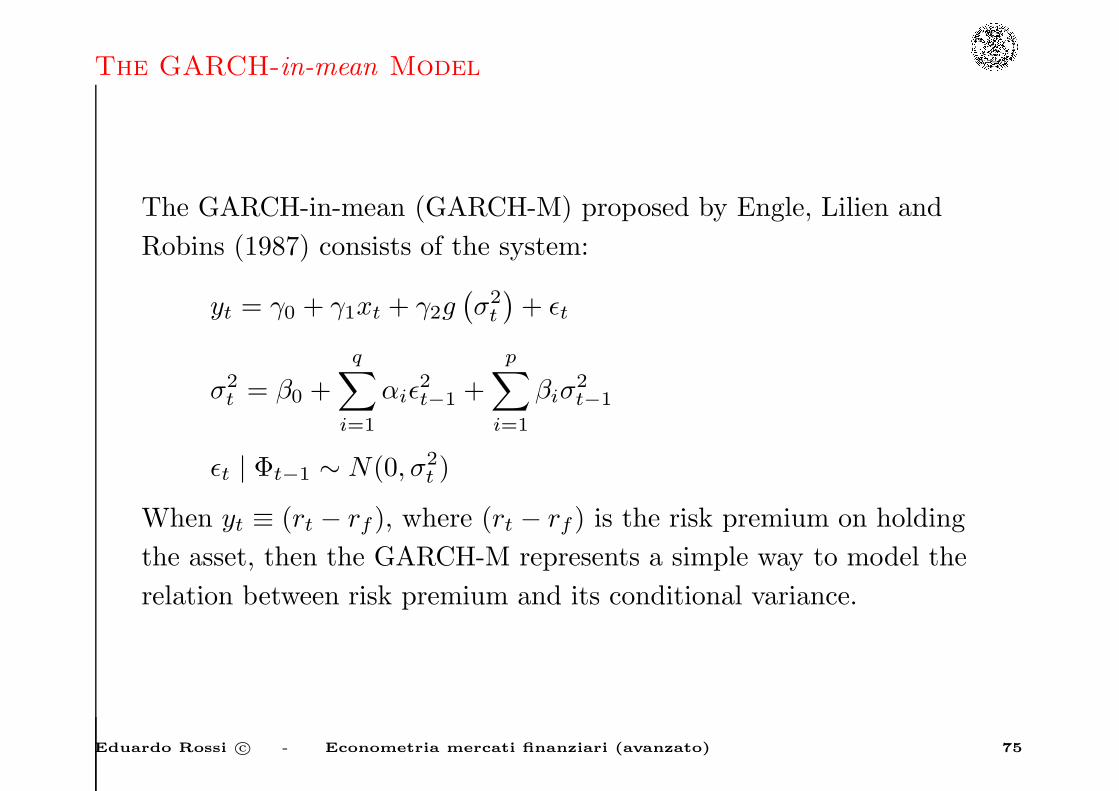

The GARCH-in-mean Model

The GARCH-in-mean (GARCH-M) proposed by Engle, Lilien and

Robins (1987) consists of the system:

yt = γ0 + γ1xt + γ2g(

σ2t

)

+ ǫt

σ2t = β0 +

q∑

i=1

αiǫ2t−1 +

p∑

i=1

βiσ2t−1

ǫt | Φt−1 ∼ N(0, σ2t )

When yt ≡ (rt − rf ), where (rt − rf ) is the risk premium on holding

the asset, then the GARCH-M represents a simple way to model the

relation between risk premium and its conditional variance.

Eduardo Rossi c© - Econometria mercati finanziari (avanzato) 75

The GARCH-in-mean Model

This model characterizes the evolution of the mean and the variance

of a time series simultaneously.

The GARCH-M model therefore allows to analize the possibility of

time-varying risk premium.

It turns out that:

yt | Φt−1 ∼ N(γ0 + γ1xt + γ2g(

σ2t

)

, σ2t )

In applications, g(

σ2t

)

=√

σ2t , g

(

σ2t

)

= ln(

σ2t

)

and g(

σ2t

)

= σ2t have

been used.

Eduardo Rossi c© - Econometria mercati finanziari (avanzato) 76

The News Impact Curve

• The news have asymmetric effects on volatility.

• In the asymmetric volatility models good news and bad news

have different predictability for future volatility.

• The news impact curve characterizes the impact of past return

shocks on the return volatility which is implicit in a volatility

model.

Eduardo Rossi c© - Econometria mercati finanziari (avanzato) 77

The News Impact Curve

Holding constant the information dated t− 2 and earlier, we can

examine the implied relation between εt−1 and σ2t , with σ2

t−i = σ2

i = 1, . . . , p.

This impact curve relates past return shocks (news) to current

volatility.

This curve measures how new information is incorporated into

volatility estimates.

Eduardo Rossi c© - Econometria mercati finanziari (avanzato) 78

The News Impact Curve

For the GARCH model the News Impact Curve (NIC) is centered on

ǫt−1 = 0.

GARCH(1,1):

σ2t = ω + αǫ2t−1 + βσ2

t−1

The news impact curve has the following expression:

σ2t = A+ αǫ2t−1

A ≡ ω + βσ2

Eduardo Rossi c© - Econometria mercati finanziari (avanzato) 79

The News Impact Curve

In the case of EGARCH model the curve has its minimum at

ǫt−1 = 0 and is exponentially increasing in both directions but with

different paramters.

EGARCH(1,1):

σ2t = ω + β ln

(

σ2t−1

)

+ φzt−1 + ψ (|zt−1| −E |zt−1|)

where zt = ǫt/σt. The news impact curve is

σ2t =

A exp

[

φ+ ψ

σǫt−1

]

for ǫt−1 > 0

A exp

[

φ− ψ

σǫt−1

]

for ǫt−1 < 0

A ≡ σ2β exp[

ω − α√

2/π]

φ < 0 ψ + φ > 0

Eduardo Rossi c© - Econometria mercati finanziari (avanzato) 80

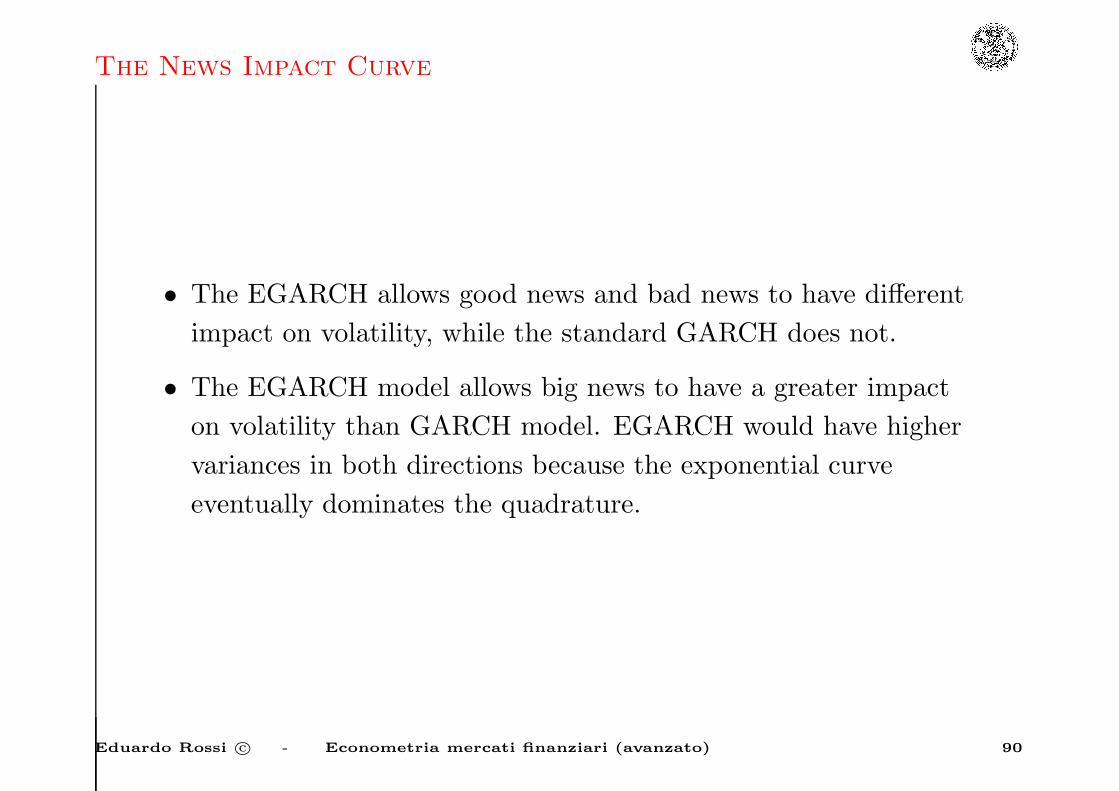

The News Impact Curve

• The EGARCH allows good news and bad news to have different

impact on volatility, while the standard GARCH does not.

• The EGARCH model allows big news to have a greater impact

on volatility than GARCH model. EGARCH would have higher

variances in both directions because the exponential curve

eventually dominates the quadrature.

Eduardo Rossi c© - Econometria mercati finanziari (avanzato) 81

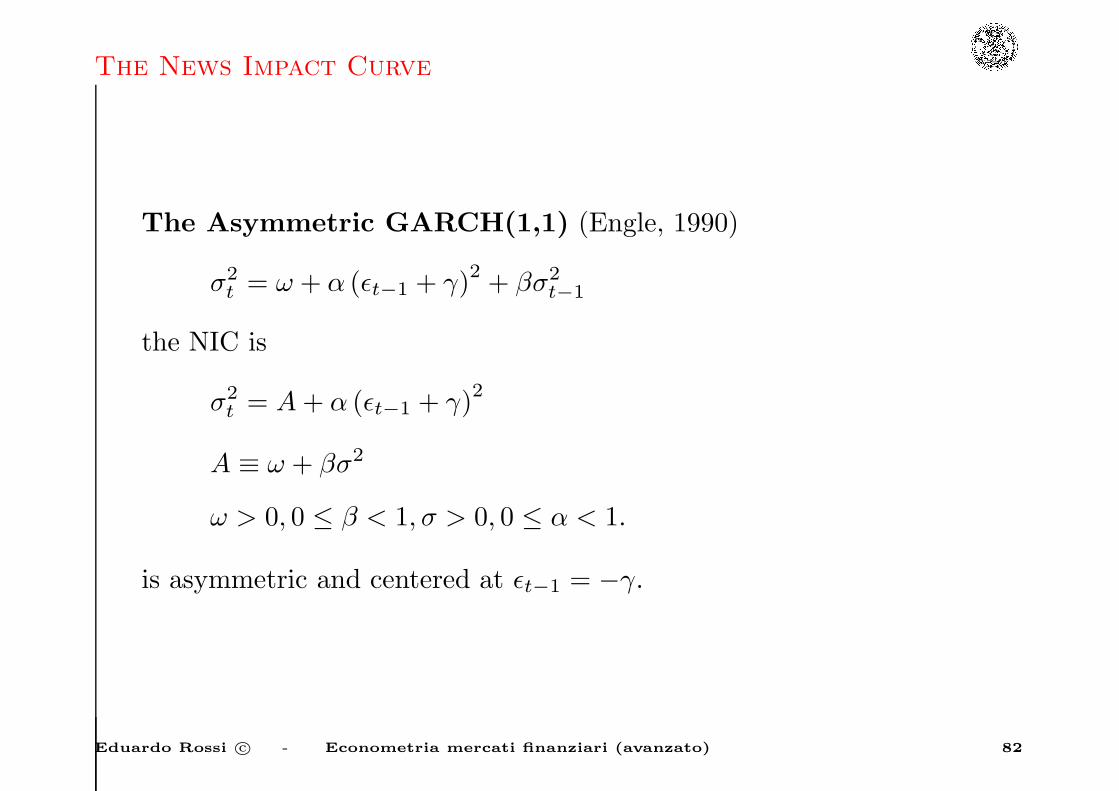

The News Impact Curve

The Asymmetric GARCH(1,1) (Engle, 1990)

σ2t = ω + α (ǫt−1 + γ)2 + βσ2

t−1

the NIC is

σ2t = A+ α (ǫt−1 + γ)

2

A ≡ ω + βσ2

ω > 0, 0 ≤ β < 1, σ > 0, 0 ≤ α < 1.

is asymmetric and centered at ǫt−1 = −γ.

Eduardo Rossi c© - Econometria mercati finanziari (avanzato) 82

The News Impact Curve

The Glosten-Jagannathan-Runkle model

σ2t = ω + αǫ2t + βσ2

t−1 + γS−

t−1ǫ2t−1

S−

t−1 =

1 if ǫt−1 < 0

0 otherwise

The NIC is

σ2t =

A+ αǫ2t−1 if ǫt−1 > 0

A+ (α+ γ) ǫ2t−1 if ǫt−1 < 0

A ≡ ω + βσ2

ω > 0, 0 ≤ β < 1, σ > 0, 0 ≤ α < 1, α+ β < 1

is centered at ǫt−1 = −γ.

Eduardo Rossi c© - Econometria mercati finanziari (avanzato) 83

The GARCH-in-mean Model

The GARCH-in-mean (GARCH-M) proposed by Engle, Lilien and

Robins (1987) consists of the system:

yt = γ0 + γ1xt + γ2g(

σ2t

)

+ ǫt

σ2t = β0 +

q∑

i=1

αiǫ2t−1 +

p∑

i=1

βiσ2t−1

ǫt | Φt−1 ∼ N(0, σ2t )

When yt ≡ (rt − rf ), where (rt − rf ) is the risk premium on holding

the asset, then the GARCH-M represents a simple way to model the

relation between risk premium and its conditional variance.

Eduardo Rossi c© - Econometria mercati finanziari (avanzato) 84

The GARCH-in-mean Model

This model characterizes the evolution of the mean and the variance

of a time series simultaneously.

The GARCH-M model therefore allows to analyze the possibility of

time-varying risk premium.

It turns out that:

yt | Φt−1 ∼ N(γ0 + γ1xt + γ2g(

σ2t

)

, σ2t )

In applications, g(

σ2t

)

=√

σ2t , g

(

σ2t

)

= ln(

σ2t

)

and g(

σ2t

)

= σ2t have

been used.

Eduardo Rossi c© - Econometria mercati finanziari (avanzato) 85

The News Impact Curve

• The news have asymmetric effects on volatility.

• In the asymmetric volatility models good news and bad news

have different predictability for future volatility.

• The news impact curve characterizes the impact of past return

shocks on the return volatility which is implicit in a volatility

model.

Eduardo Rossi c© - Econometria mercati finanziari (avanzato) 86

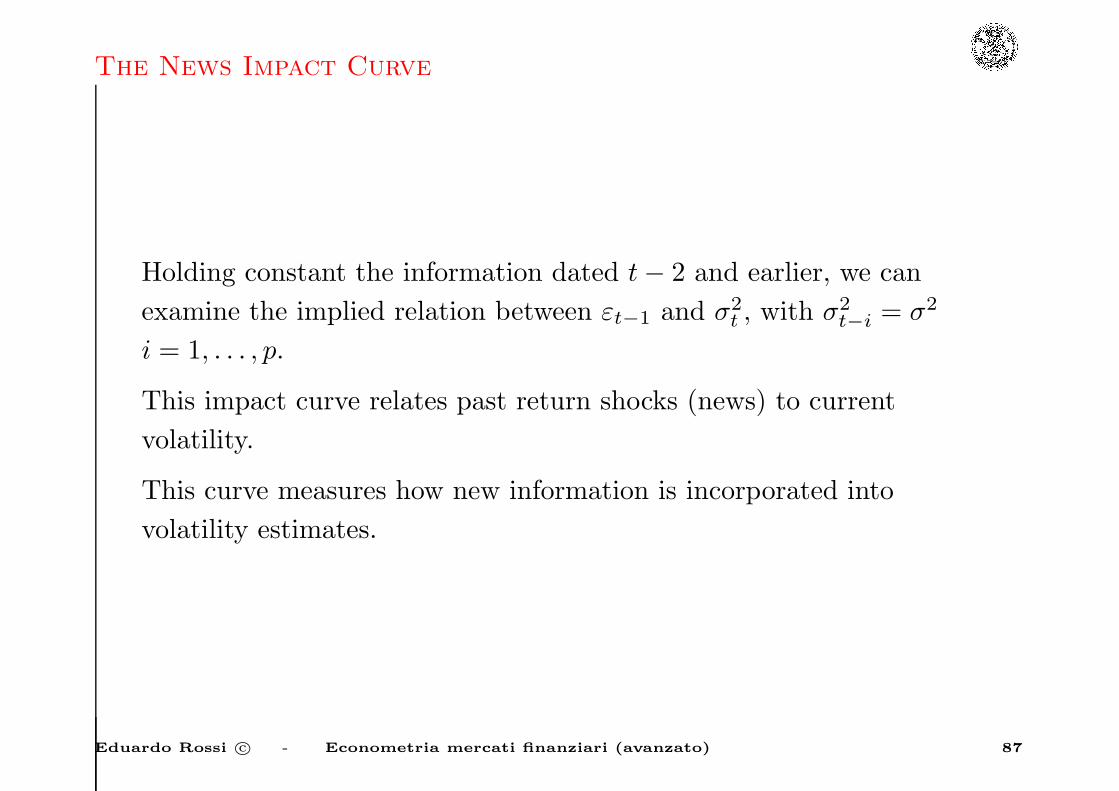

The News Impact Curve

Holding constant the information dated t− 2 and earlier, we can

examine the implied relation between εt−1 and σ2t , with σ2

t−i = σ2

i = 1, . . . , p.

This impact curve relates past return shocks (news) to current

volatility.

This curve measures how new information is incorporated into

volatility estimates.

Eduardo Rossi c© - Econometria mercati finanziari (avanzato) 87

The News Impact Curve

For the GARCH model the News Impact Curve (NIC) is centered on

ǫt−1 = 0.

GARCH(1,1):

σ2t = ω + αǫ2t−1 + βσ2

t−1

The news impact curve has the following expression:

σ2t = A+ αǫ2t−1

A ≡ ω + βσ2

Eduardo Rossi c© - Econometria mercati finanziari (avanzato) 88

The News Impact Curve

In the case of EGARCH model the curve has its minimum at

ǫt−1 = 0 and is exponentially increasing in both directions but with

different paramters.

EGARCH(1,1):

σ2t = ω + β ln

(

σ2t−1

)

+ φzt−1 + ψ (|zt−1| −E |zt−1|)

where zt = ǫt/σt. The news impact curve is

σ2t =

A exp

[

φ+ ψ

σǫt−1

]

for ǫt−1 > 0

A exp

[

φ− ψ

σǫt−1

]

for ǫt−1 < 0

A ≡ σ2β exp[

ω − α√

2/π]

φ < 0 ψ + φ > 0

Eduardo Rossi c© - Econometria mercati finanziari (avanzato) 89

The News Impact Curve

• The EGARCH allows good news and bad news to have different

impact on volatility, while the standard GARCH does not.

• The EGARCH model allows big news to have a greater impact

on volatility than GARCH model. EGARCH would have higher

variances in both directions because the exponential curve

eventually dominates the quadrature.

Eduardo Rossi c© - Econometria mercati finanziari (avanzato) 90

The News Impact Curve

The Asymmetric GARCH(1,1) (Engle, 1990)

σ2t = ω + α (ǫt−1 + γ)2 + βσ2

t−1

the NIC is

σ2t = A+ α (ǫt−1 + γ)

2

A ≡ ω + βσ2

ω > 0, 0 ≤ β < 1, σ > 0, 0 ≤ α < 1.

is asymmetric and centered at ǫt−1 = −γ.

Eduardo Rossi c© - Econometria mercati finanziari (avanzato) 91

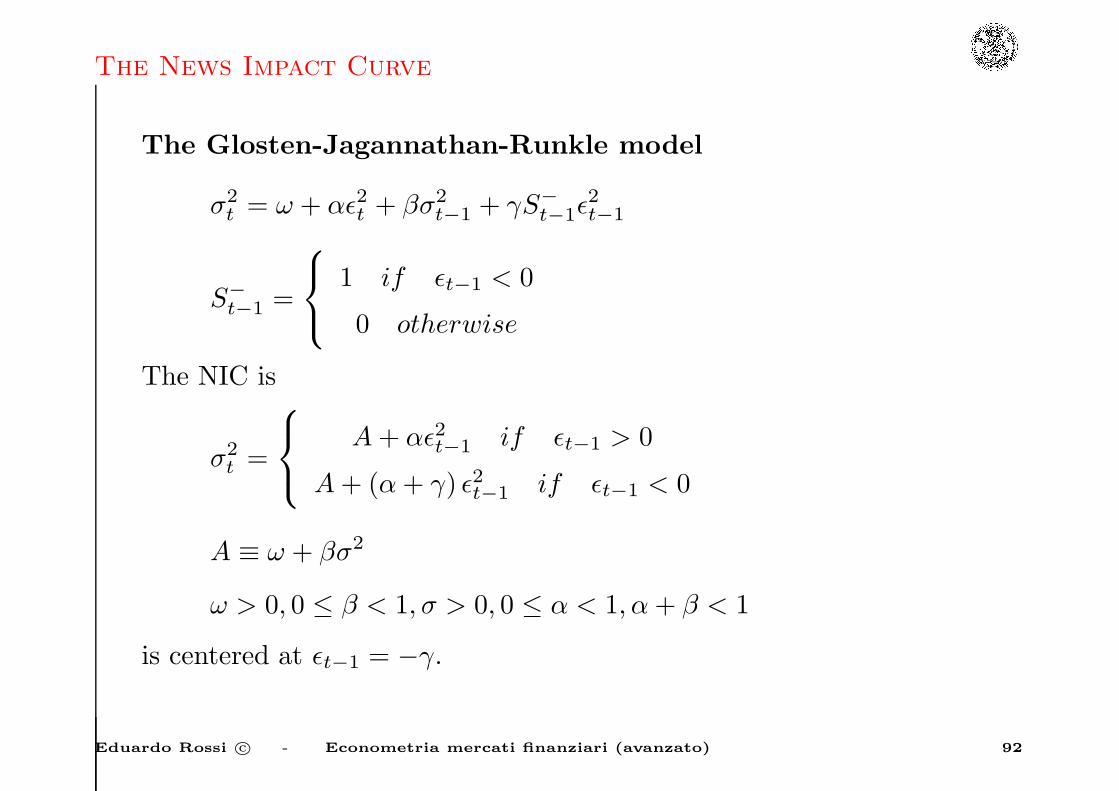

The News Impact Curve

The Glosten-Jagannathan-Runkle model

σ2t = ω + αǫ2t + βσ2

t−1 + γS−

t−1ǫ2t−1

S−

t−1 =

1 if ǫt−1 < 0

0 otherwise

The NIC is

σ2t =

A+ αǫ2t−1 if ǫt−1 > 0

A+ (α+ γ) ǫ2t−1 if ǫt−1 < 0

A ≡ ω + βσ2

ω > 0, 0 ≤ β < 1, σ > 0, 0 ≤ α < 1, α+ β < 1

is centered at ǫt−1 = −γ.

Eduardo Rossi c© - Econometria mercati finanziari (avanzato) 92