E-Retail Outlook for 2008 & Beyond

25

Teleconference The Outlook For US eCommerce In 2008 And Beyond Sucharita Mulpuru Principal Analyst Forrester Research February 20, 2008. Call in at 12:55 p.m. Eastern time

-

Upload

stanley-stevens -

Category

Documents

-

view

219 -

download

2

description

Forrester Research report on E-Retail

Transcript of E-Retail Outlook for 2008 & Beyond

TeleconferenceThe Outlook For US eCommerce In 2008 And BeyondSucharita MulpuruPrincipal AnalystForrester Research

February 20, 2008. Call in at 12:55 p.m. Eastern time

2Entire contents © 2008 Forrester Research, Inc. All rights reserved.

B2C US eCommerce will continue to grow at a double-digit clip

© 2007, Forrester Research, Inc. Reproduction Prohibited

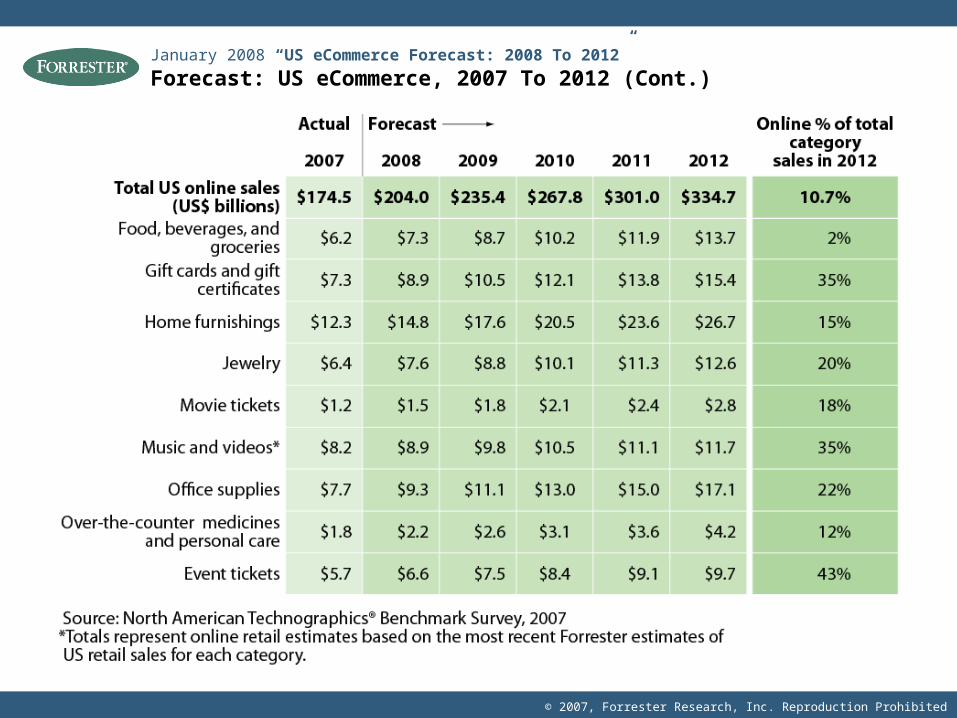

Forecast: US eCommerce, 2007 To 2012January 2008 “US eCommerce Forecast: 2008 To 2012”

© 2007, Forrester Research, Inc. Reproduction Prohibited

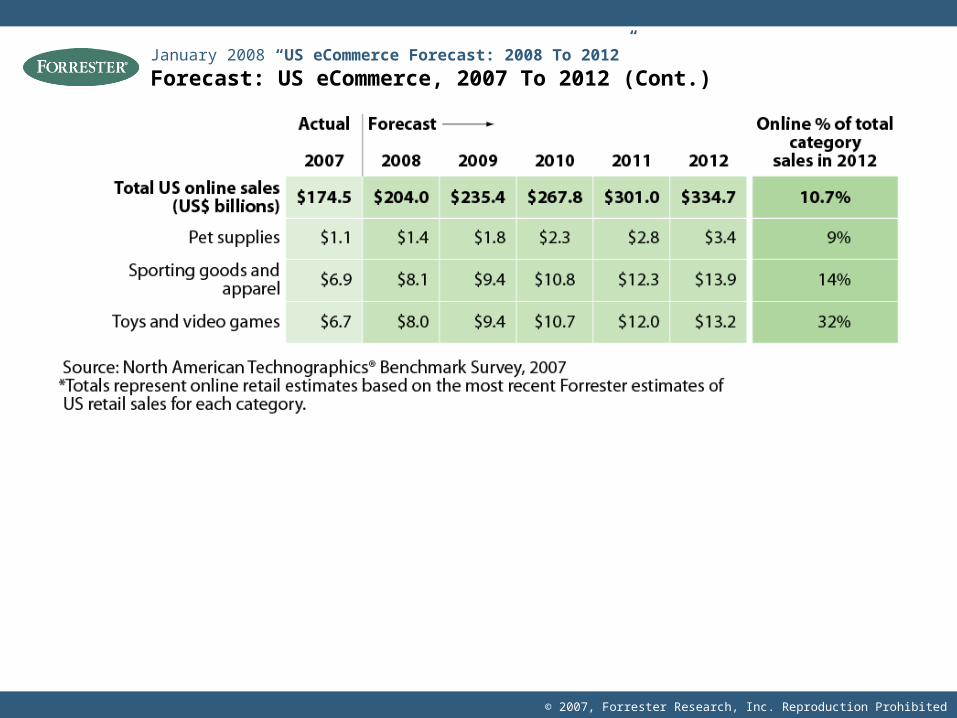

Forecast: US eCommerce, 2007 To 2012 (Cont.)January 2008 “US eCommerce Forecast: 2008 To 2012”

© 2007, Forrester Research, Inc. Reproduction Prohibited

Forecast: US eCommerce, 2007 To 2012 (Cont.)January 2008 “US eCommerce Forecast: 2008 To 2012”

6Entire contents © 2008 Forrester Research, Inc. All rights reserved.

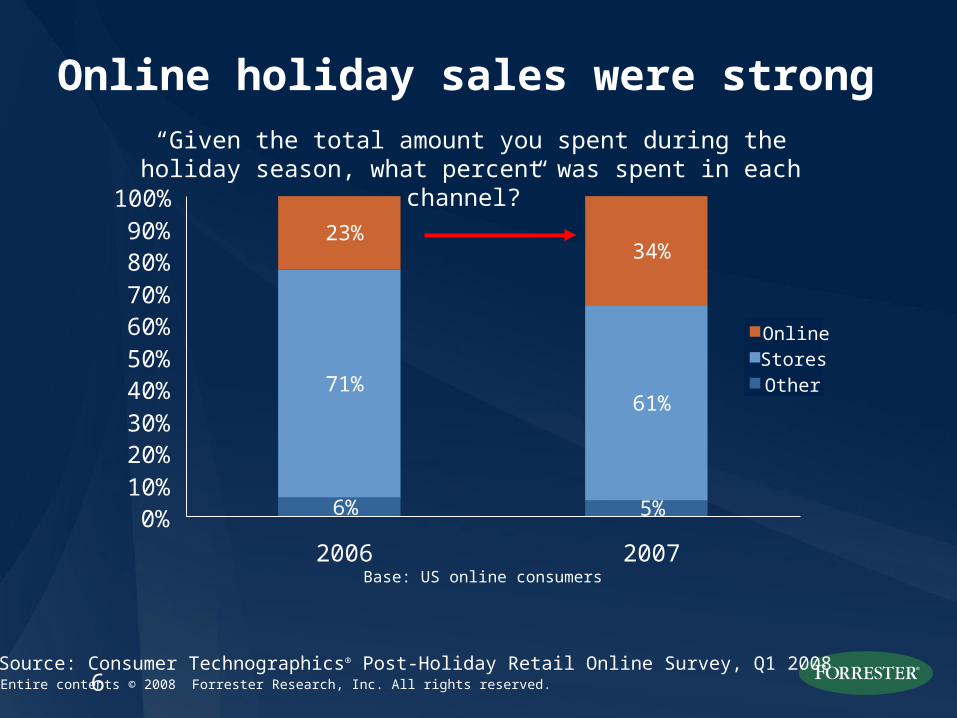

Online holiday sales were strong

Base: US online consumers

“Given the total amount you spent during the holiday season, what percent was spent in each channel?”

6% 5%

71%61%

23%34%

0%10%20%30%40%50%60%70%80%90%

100%

2006 2007

OnlineStoresOther

Source: Consumer Technographics® Post-Holiday Retail Online Survey, Q1 2008

7Entire contents © 2008 Forrester Research, Inc. All rights reserved.

This growth has happened in spite of economic conditions . . .

8Entire contents © 2008 Forrester Research, Inc. All rights reserved.

0.4

0.9

1/1/

2006

3/1/

2006

5/1/

2006

7/1/

2006

9/1/

2006

11/1

/200

6

1/1/

2007

3/1/

2007

5/1/

2007

7/1/

2007

9/1/

2007

11/1

/200

7

1/1/

2008

US$ to Euro Interbank rate

. . . including a declining dollar

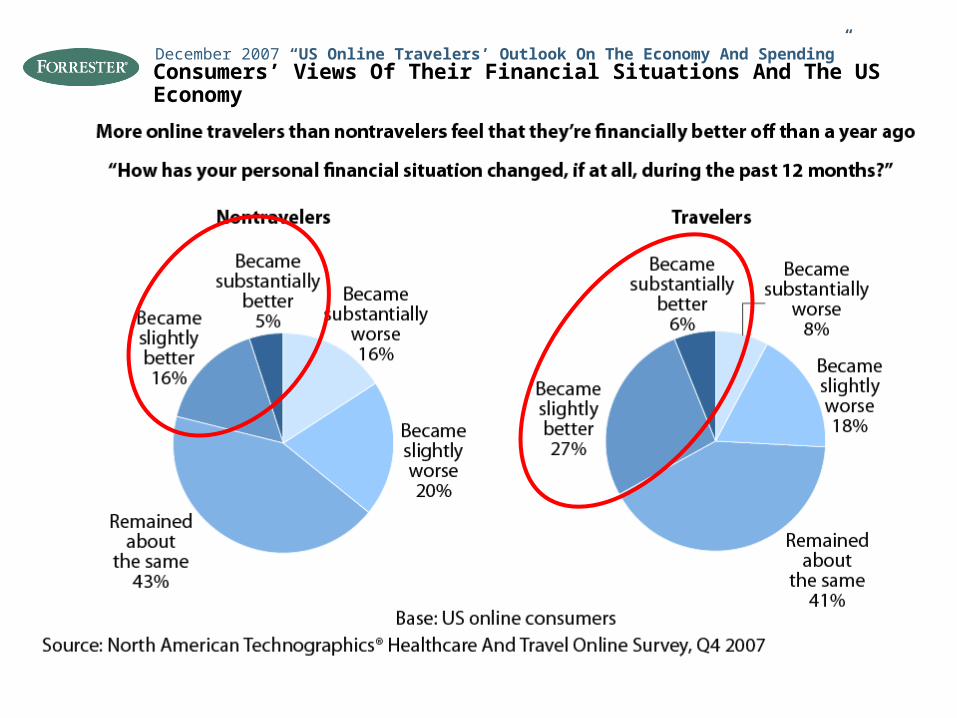

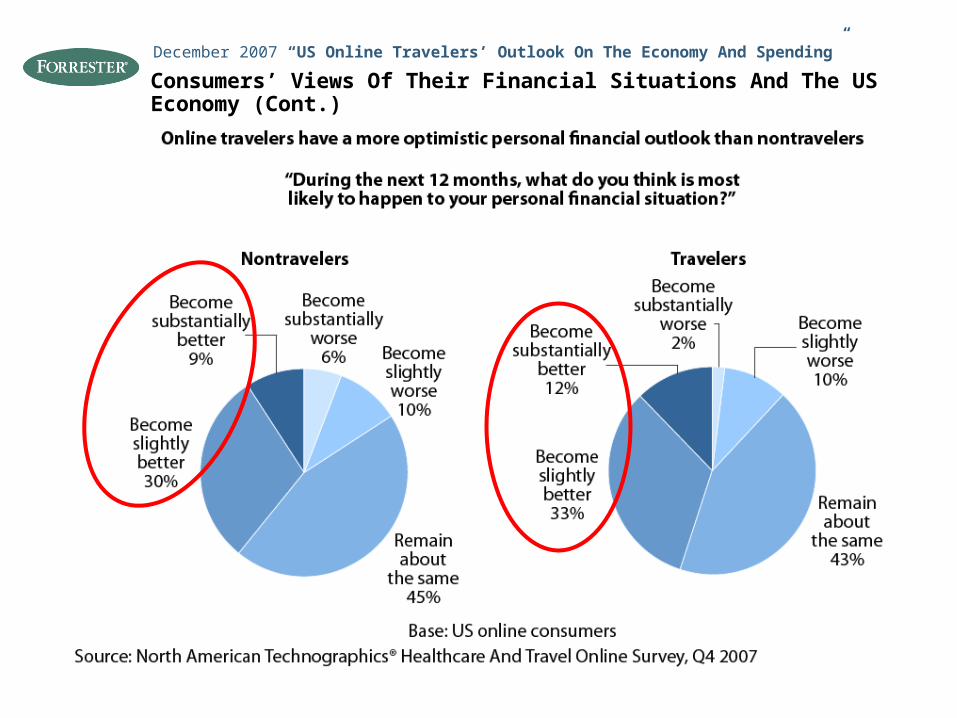

December 2007 “US Online Travelers’ Outlook On The Economy And Spending”

Consumers’ Views Of Their Financial Situations And The US Economy

Consumers’ Views Of Their Financial Situations And The US Economy (Cont.)

December 2007 “US Online Travelers’ Outlook On The Economy And Spending”

11Entire contents © 2008 Forrester Research, Inc. All rights reserved.

eCommerce may be insulated because:

• Online consumers tend to be more affluent in general.

• Online consumers use the channel because it is just more convenient.

• Only 15% of US online consumers agreed with the statement “I bought less online this holiday season due to uncertainty about the US economy.”

• While overall retail sales may be flat or declining in most stores, online retailers still experience upward trajectories from a channel shift.

12Entire contents © 2008 Forrester Research, Inc. All rights reserved.

The Web is growing faster than stores

US$B

CAGR2008-12: 2%

CAGR2008-12: 13%

$204 $235 $268 $301 $335

$2,605 $2,646 $2,689 $2,734 $2,783

$0

$1,000

$2,000

$3,000

2008 2009 2010 2011 2012

Online sales Non-online sales

13Entire contents © 2008 Forrester Research, Inc. All rights reserved.

Base: US online consumers

43%

46%

49%

40% 42% 44% 46% 48% 50%

I found the best values/deals online

I found products online that I couldn’t

find anywhere else

I prefer to shop online to avoid

crowds/linesCONVENIENCE

SELECTION

VALUE

The reasons consumers shop online remain the same

Source: Consumer Technographics® Post-Holiday Retail Online Survey, Q1 2008

14Entire contents © 2008 Forrester Research, Inc. All rights reserved.

Core shoppers drive most of eCommerce

Half of online shoppers drive two-thirds of

online shopping spend.

Source: Consumer Technographics® Post-Holiday Retail Online Survey, Q1 2008

15Entire contents © 2008 Forrester Research, Inc. All rights reserved.

“Did you experience any complications while shopping online

during holiday 2007?”

42%Yes

58%No

Base: US online Web buyers

Consumer problems haven’t improved with time

8%

13%

17%

21%

0% 5% 10% 15% 20% 25%

Poor Web site performance (e.g., sluggishness)

Shipping ended up taking longer than I had expected

The item I purchased was backordered or not in stock

Shipping prices were higher than expected

Source: Consumer Technographics® Post-Holiday Retail Online Survey, Q1 2008

© 2007, Forrester Research, Inc. Reproduction Prohibited

This makes Web shopping very utilitarianJanuary 2008 “US eCommerce Forecast: 2008 To 2012”

© 2007, Forrester Research, Inc. Reproduction Prohibited

We believe some trends will shape the coming yearsDecember 2007 “Which Personalization Tools Work For eCommerce — And Why”

18Entire contents © 2008 Forrester Research, Inc. All rights reserved.

This should mean more experiences like this:

19Entire contents © 2008 Forrester Research, Inc. All rights reserved.

“Please rank the following channels in order of your purchasing preference.”

Base: US online consumers

Rank 1 Rank 2 Rank 3 Rank 4 Rank 5

Traditional offline stores 74% 19% 4% 2% 2%

Online 22% 52% 11% 7% 8%

Print catalog 1% 18% 50% 24% 7%

By telephone (e.g., flowers) 2% 9% 26% 45% 19%

Television (e.g., shopping channel, infomercial)

1% 2% 9% 22% 64%

Consumers still prefer to shop in stores

Source: Consumer Technographics® Retail Online Survey, Q3 2007

20Entire contents © 2008 Forrester Research, Inc. All rights reserved.

This should mean stronger multichannel integration

US leaders

Circuit City

Best Buy

Wal-Mart

International leaders

FNAC

Tesco

ASDA

21Entire contents © 2008 Forrester Research, Inc. All rights reserved.

On-demand production driven by the long tail

22Entire contents © 2008 Forrester Research, Inc. All rights reserved.

Better, richer user experiences

23Entire contents © 2008 Forrester Research, Inc. All rights reserved.

Prognosis

Despite economic conditions, eCommerce

should continue on a strong, upward trajectory.

24Entire contents © 2008 Forrester Research, Inc. All rights reserved.

One last plug

• For those of you interested in more online retail metrics who also have an eCommerce business, participate in our annual “The State of Retailing Online” survey!

• Rich report with the following data points:» Marketing spend» Merchandising priorities» Percent of business through the Web channel» Multichannel priorities

• Email me ([email protected]) or [email protected] for a link to the survey.

• Must be completed very, very soon.

25Entire contents © 2008 Forrester Research, Inc. All rights reserved.

Sucharita Mulpuru

www.forrester.com

Thank you