CIT Retail Industry Outlook - 2015

12

1 2015 Retail Outlook KEY HEADLINES FROM RESEARCH Cautiously Optimistic Outlook for Current and Future Finances Holiday Season Looking Up According to Most Retailers Staff Increasing for Holidays, Promotions Earlier and Earlier Top Priorities: Innovation, Marketing and Online/Mobile Key Threats: One-Stop Shops and New Technologies Online Channel Growing, Supporting and Challenging Mobile (Perhaps Under-exploited) Edge Social Media Less of a Hurdle Throughout this report there are references to subsets of the total sample (Brick-and-mortar-only, online-only and combined retailers). Due to small base sizes, findings among these subsets are more qualitative in nature. In 2014, the financial condition of retailers appears strong—and growing—with retailers having a more positive outlook on the upcoming holiday season as well as overall sales than even a year ago. Despite challenges related to technology adoption and the ability to buy anything anywhere, retailers are embracing change. They are making new investments in products, expanding their digital strategy and becoming more comfortable with social media as a tool for multiple facets of their business. In order to understand current trends, challenges and outlook for the retail industry, Harris Poll, on behalf of CIT, a leader in financing and advisory services to the retail sector, conducted research online from September 16 to October 3 among 251 financial decision makers in U.S.-based middle market retailers.

Transcript of CIT Retail Industry Outlook - 2015

1

2015 Retail Outlook

KEY HEADLINES FROM RESEARCH

Cautiously Optimistic Outlook for Current and Future Finances

Holiday Season Looking Up According to Most Retailers

Staff Increasing for Holidays, Promotions Earlier and Earlier

Top Priorities: Innovation, Marketing and Online/Mobile

Key Threats: One-Stop Shops and New Technologies

Online Channel Growing, Supporting and Challenging

Mobile (Perhaps Under-exploited) Edge

Social Media Less of a Hurdle

Throughout this report there are references to subsets of the total sample (Brick-and-mortar-only, online-only and combined retailers). Due to small base sizes, findings among these subsets are more qualitative in nature.

In 2014, the financial condition of retailers appears

strong—and growing—with retailers having a

more positive outlook on the upcoming holiday

season as well as overall sales than even a year ago.

Despite challenges related to technology adoption

and the ability to buy anything anywhere, retailers

are embracing change. They are making new

investments in products, expanding their digital

strategy and becoming more comfortable with

social media as a tool for multiple facets of

their business.

In order to understand current trends, challenges

and outlook for the retail industry, Harris Poll,

on behalf of CIT, a leader in financing and advisory

services to the retail sector, conducted research

online from September 16 to October 3 among

251 financial decision makers in U.S.-based middle

market retailers.

2

2015 Retail Outlook

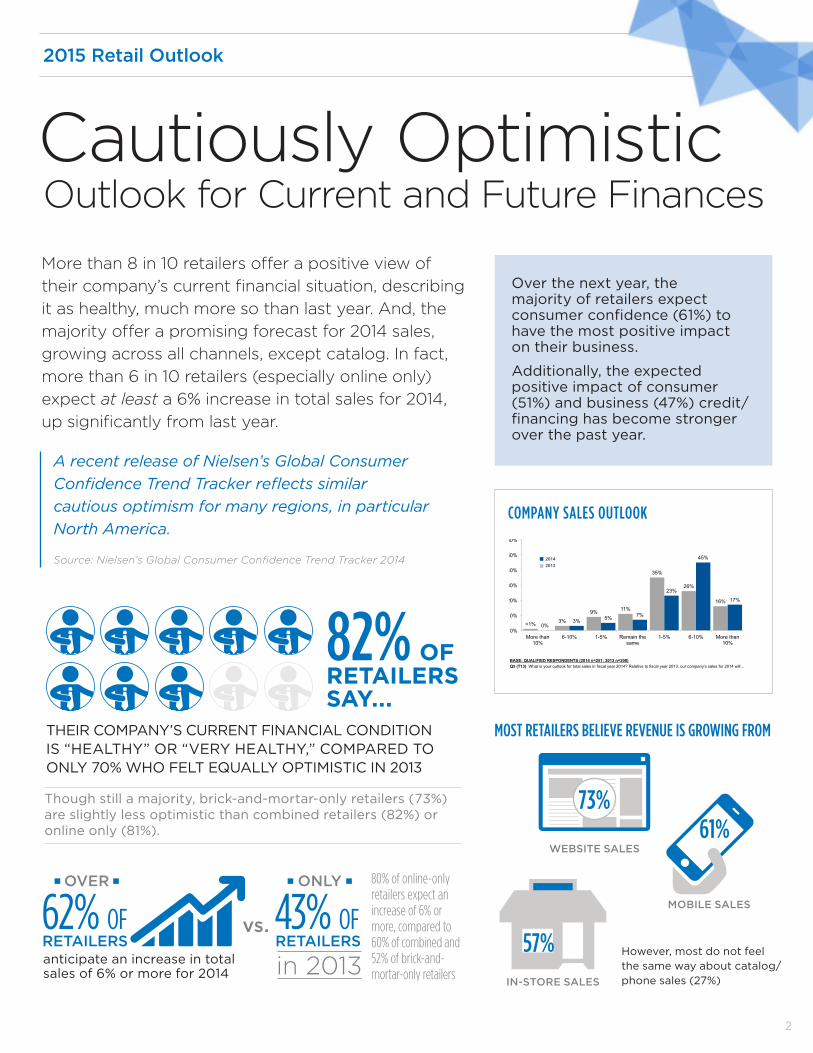

Cautiously OptimisticOutlook for Current and Future Finances

More than 8 in 10 retailers offer a positive view of

their company’s current financial situation, describing

it as healthy, much more so than last year. And, the

majority offer a promising forecast for 2014 sales,

growing across all channels, except catalog. In fact,

more than 6 in 10 retailers (especially online only)

expect at least a 6% increase in total sales for 2014,

up significantly from last year.

However, most do not feel the same way about catalog/phone sales (27%)

Over the next year, the majority of retailers expect consumer confidence (61%) to have the most positive impact on their business.

Additionally, the expected positive impact of consumer (51%) and business (47%) credit/financing has become stronger over the past year.

THEIR COMPANY’S CURRENT FINANCIAL CONDITION IS “HEALTHY” OR “VERY HEALTHY,” COMPARED TO ONLY 70% WHO FELT EQUALLY OPTIMISTIC IN 2013

80% of online-only retailers expect an increase of 6% or more, compared to 60% of combined and 52% of brick-and-mortar-only retailers

anticipate an increase in total sales of 6% or more for 2014 in 2013

vs.62% OFRETAILERS

OVER

43% OFRETAILERS

ONLY

MOST RETAILERS BELIEVE REVENUE IS GROWING FROM

MOBILE SALES

61%

IN-STORE SALES

57%

WEBSITE SALES

73%

COMPANY SALES OUTLOOK

A recent release of Nielsen’s Global Consumer

Confidence Trend Tracker reflects similar

cautious optimism for many regions, in particular

North America.

Source: Nielsen’s Global Consumer Confidence Trend Tracker 2014

<1% 3%

9% 11%

35%

26%

16%

0% 3% 5% 7%

23%

45%

17%

0%

10%

20%

30%

40%

50%

60%

70%

More than 10%

6-10% 1-5% Remain the same

1-5% 6-10% More than 10%

BASE: QUALIFIED RESPONDENTS (2014 n=251; 2013 n=208) Q5 (T13) What is your outlook for total sales in fiscal year 2014? Relative to fiscal year 2013, our company’s sales for 2014 will…

COMPANY SALES OUTLOOK

Decrease Net 8%

Increase Net 85%

Significantly higher than 2013 at the 95% confidence level Significantly lower than 2013 at the 95% confidence level

FOR SLIDE 2

2014 2013

Though still a majority, brick-and-mortar-only retailers (73%) are slightly less optimistic than combined retailers (82%) or online only (81%).

82%RETAILERS SAY...

OF

3

2015 Retail Outlook

2014 HOLIDAY SALES OUTLOOK

Holiday Season Looking UpAccording to Most Retailers

Not only are retailers optimistic about sales overall,

most also express confidence specifically about the

upcoming holiday season. More than half of retailers

(a significant jump from 2013) anticipate that total

sales for the 2014 holiday season will increase by at

least 6%, driven primarily by online shopping and

proposed discounts.

According to the Holiday

Sales Forecast released from

Nielsen, due to rising consumer

confidence, holiday spending

is predicted to increase 1.9%

compared to last year.

Source: Nielsen Holiday Survey 2014

Online-only and combined retailers are much more

likely to feel holiday sales will increase than those

who are brick-and-mortar-only (96% and 87%,

respectively vs. 67%).

EXPECT ONLINE SHOPPING TO HAVE THE BIGGEST INCREMENTAL IMPACT ON HOLIDAY SALES

More than two in five expect in-store and online discounts (43%) to have a notable impact.

¡ Brick-and-mortar-only retailers expect the weather (54%)

and fuel prices (44%) to have the most incremental impact

on holiday sales whereas online only and combined retailers

anticipate increases in online shopping (76% and 60%,

respectively) and in-store or online discounts (66% and 56%,

respectively) to be the biggest holiday sales drivers.

MORE THAN HALF OF RETAILERS anticipate total sales for the 2014 holiday season to increase by 6% (or more), compared to only 1 in 3 retailers (33%) in 2013.55%

53%

<1% 1%

9%

24%

33%

23%

10%

0% 1% 3%

14%

26%

36%

19%

0%

10%

20%

30%

40%

50%

60%

70%

More than 10%

6-10% 1-5% Remain the same

1-5% 6-10% More than 10%

Decrease (Net) 4%

Increase Net 81%

2014 HOLIDAY SALES OUTLOOK

Significantly higher than 2013 at the 95% confidence level Significantly lower than 2013 at the 95% confidence level

FOR SLIDE 3

2014 2013

BASE: QUALIFIED RESPONDENTS (2014 n=251; 2013 n=208) Q8 (T13) What is your outlook for the 2014 Holiday Season? Relative to the 2013, Holiday Season our company’s sales for 2014 will…

4

2015 Retail Outlook

Copyright ©

2014 The Nielse

n Co

mpany. Con

fidenJal and proprietary.

3

Upcoming Holiday Season

5%

8%

9%

5%

4%

74%

58%

37%

41%

35%

21%

34%

54%

54%

60%

Number of headquarters executives

Number of in-store exempt (e.g., store managers)

workers

Total number of hours worked by hourly

employees

Number of staff devoted to Internet/mobile sales

channels

Total number of hourly employees

Upcoming New Year, 2015

■ Decrease ■ About the same ■ Increase

6%

10%

11%

8%

8%

63%

54%

53%

51%

44%

31%

37%

36%

41%

49%

Number of headquarters executives

Number of in-store exempt (e.g., store managers)

workers

Total number of hours worked by hourly

employees

Number of staff devoted to Internet/mobile sales

channels

Total number of hourly employees

FOR SLIDE 4

BASE: ALL QUALIFIED RESPONDENTS (n=251) Q3 Thinking about the upcoming holiday season (Thanksgiving and Christmas), in terms of both hourly and exempt workers, do you expect your staff size to increase, decrease or will it remain about the same? BASE: ALL QUALIFIED RESPONDENTS (n=251) Q4 Starting in 2015, in terms of both hourly and exempt workers, do you expect your staff size to increase, decrease or will it remain about the same?

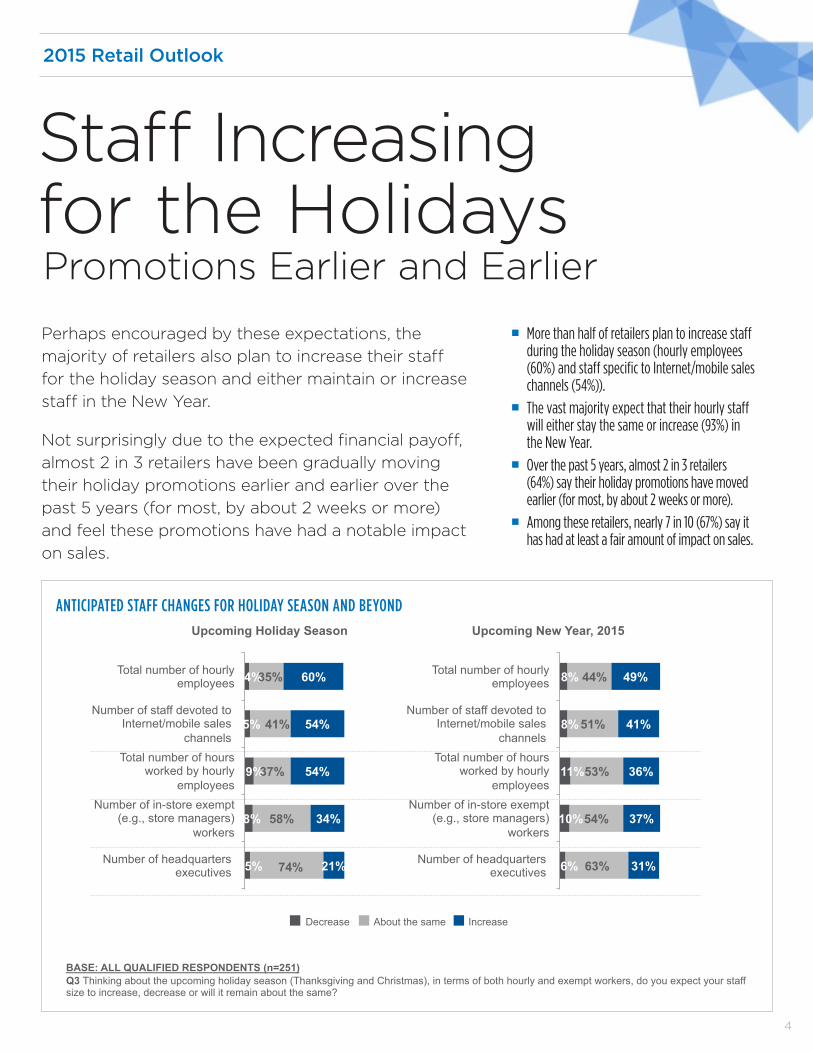

Staff Increasing for the HolidaysPromotions Earlier and Earlier

Perhaps encouraged by these expectations, the

majority of retailers also plan to increase their staff

for the holiday season and either maintain or increase

staff in the New Year.

Not surprisingly due to the expected financial payoff,

almost 2 in 3 retailers have been gradually moving

their holiday promotions earlier and earlier over the

past 5 years (for most, by about 2 weeks or more)

and feel these promotions have had a notable impact

on sales.

¡ More than half of retailers plan to increase staff during the holiday season (hourly employees (60%) and staff specific to Internet/mobile sales channels (54%)).

¡ The vast majority expect that their hourly staff will either stay the same or increase (93%) in the New Year.

¡ Over the past 5 years, almost 2 in 3 retailers (64%) say their holiday promotions have moved earlier (for most, by about 2 weeks or more).

¡ Among these retailers, nearly 7 in 10 (67%) say it has had at least a fair amount of impact on sales.

ANTICIPATED STAFF CHANGES FOR HOLIDAY SEASON AND BEYOND

5

2015 Retail Outlook

However, not everything is auspicious in the retail

industry; most retailers say they will face several

challenges in the near and long term. The majority

predict that some prominent retailers will close in

the next 1-3 years, or at least decline in value.

Specifically, brick-and-mortar-only stores are seen

as unsustainable in the future and do not represent

a viable long-term strategy, even according to many

brick-and-mortar retailers themselves. However,

many retailers (especially those with a brick-and-

mortar presence) acknowledge that the online world

is a major hurdle that will need to be overcome.

Key ThreatsOne-Stop Shops and New Technologies

¡ Approximately 7 in 10 retailers

feel that the consumer appeal

and overall brand value of

prominent retailers is on the

decline, much more so than one

year ago (65% vs. 48% in 2013).

¡ Four in ten retailers with both a brick-and-

mortar and online presence (40%) view the

online world as a significant challenge to their

brand and recognize their need to adjust

accordingly.

believe one or more prominent retailers will likely disappear in the next 1-3 years

NEARLY 3 IN 4 RETAILERS

OF RETAILERS AGREE THAT

BRICK-AND-MORTAR-ONLY STORES

WILL NOT SURVIVE IN THE FUTURE

Nearly half (45%) of brick-and-mortar-only retailers agree

58%

72%

BRICK AND MORTAR SURVIVAL

*= base size <100

FOR SLIDES 5-‐6

37%

21%

Retailers with only a brick-‐and-‐mortar presence will not survive in the future

58 % TOP 2 BOX

BASE: ALL QUALIFIED RESPONDENTS (n=251) Q23 How strongly do you agree or disagree with the following statements?

Strongly agree Somewhat agree

6

2015 Retail Outlook

Key ThreatsOne-Stop Shops and New Technologies

Nearly half of retailers (especially those with an

online presence) believe that the death of the

American mall is also inevitable. And rather, most

believe one-stop shops like Walmart and Target

will become the stores of the future. Along with

adjusting to new technologies, most see these

“one-stop shops” as one of the biggest threats

to their retail success.

On another challenging note, despite most retailers

feeling that they have leverage over their supply

chain, more than 4 in 10, express some concern

about the health of their supply chain going forward.

Continued

¡ According to retailers, the two most disruptive factors (asked in an unaided, open-ended fashion) to the business model include: adjusting to new technologies (5%) and the ability to get anything anywhere (6%).

¡ Approximately 2 in 3 (63%) retailers, agree that “one-stop shop” retailers, such as Walmart or Target, will become the stores of the future.

¡ Most retailers (61%) agree that they have leverage over their supply chain.

¡ However, 4 in 10 retailers (41%), especially online only (53%), are at least somewhat concerned about the viability of their supply chain.

47% OF RETAILERS FEEL THE DEATH OF THE AMERICAN MALL IS INEVITABLEespecially those with an online presence 65% online and 58% combined

This perception is further supported by outside

data from the Nielsen Shopper Trend Survey 2014,

in which shoppers rated finding “everything in one

shop” as one of the five most important reasons

in deciding where to shop in 37 out of 54 markets

around the world.

Source: Nielsen’s Category Fundamentals Study 2014

FUTURE OF ONE-STOP SHOPS AND THE AMERICAN MALL

Copyright ©

2014 The Nielse

n Co

mpany. Con

fidenJal and proprietary.

5

29%

44%

18%

19%

The death of the American mall is inevitable

"One-‐stop shop" retailers such as Walmart and Target will

become the stores of the future

Somewhat agree Strongly agree

MORE COMPETITION – BUT PERHAPS LESS VARIETY

* = base size <100

FOR SLIDES 5-‐6

63%

TOP 2 BOX

47%

BASE: ALL QUALIFIED RESPONDENTS (n=251) Q23 How strongly do you agree or disagree with the following statements?

7

2015 Retail Outlook

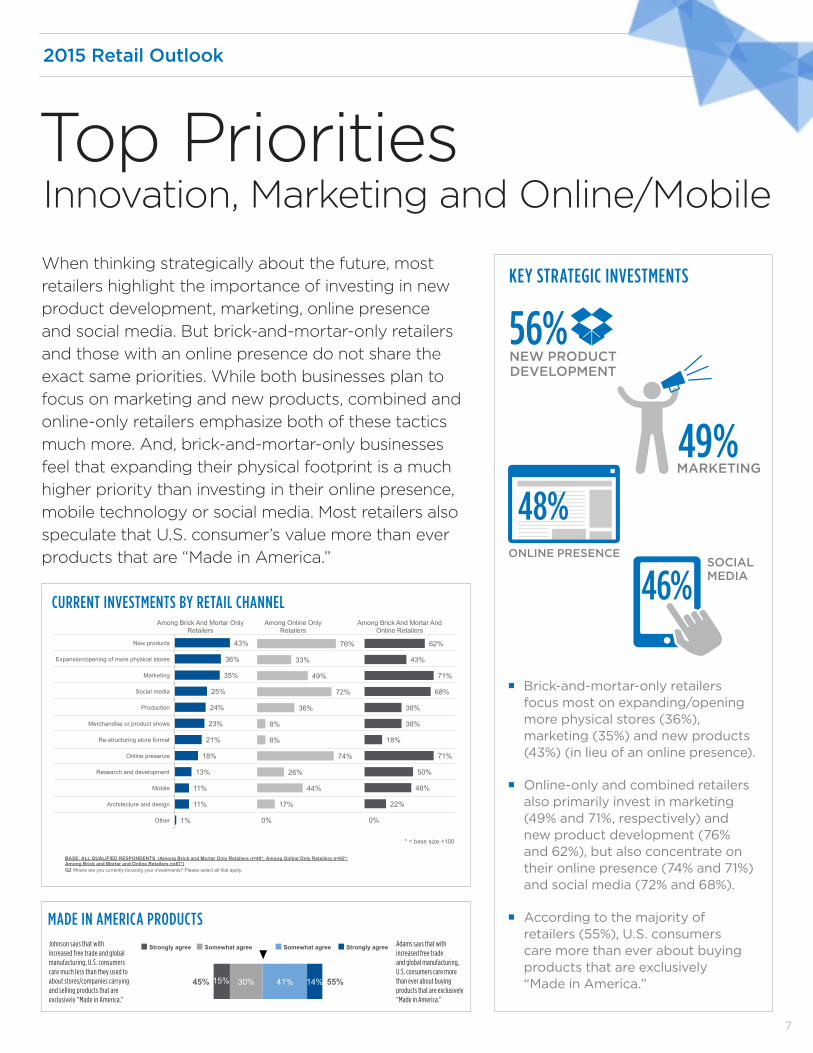

Top PrioritiesInnovation, Marketing and Online/Mobile

When thinking strategically about the future, most

retailers highlight the importance of investing in new

product development, marketing, online presence

and social media. But brick-and-mortar-only retailers

and those with an online presence do not share the

exact same priorities. While both businesses plan to

focus on marketing and new products, combined and

online-only retailers emphasize both of these tactics

much more. And, brick-and-mortar-only businesses

feel that expanding their physical footprint is a much

higher priority than investing in their online presence,

mobile technology or social media. Most retailers also

speculate that U.S. consumer’s value more than ever

products that are “Made in America.”

KEY STRATEGIC INVESTMENTS

¡ Brick-and-mortar-only retailers focus most on expanding/opening more physical stores (36%), marketing (35%) and new products (43%) (in lieu of an online presence).

¡ Online-only and combined retailers also primarily invest in marketing (49% and 71%, respectively) and new product development (76% and 62%), but also concentrate on their online presence (74% and 71%) and social media (72% and 68%).

¡ According to the majority of retailers (55%), U.S. consumers care more than ever about buying products that are exclusively “Made in America.”

48%

NEW PRODUCT DEVELOPMENT

56%

MARKETING49%

ONLINE PRESENCESOCIAL MEDIA46%CURRENT INVESTMENTS BY RETAIL CHANNEL

Copyright ©

2014 The Nielse

n Co

mpany. Con

fidenJal and proprietary.

6

Among Brick And Mortar Only Retailers

1%

11%

11%

13%

18%

21%

23%

24%

25%

35%

36%

43%

Other

Architecture and design

Mobile

Research and development

Online presence

Re-structuring store format

Merchandise or product shows

Production

Social media

Marketing

Expansion/opening of more physical stores

New products

Among Online Only Retailers

0%

17%

44%

26%

74%

8%

8%

36%

72%

49%

33%

76%

0%

22%

48%

50%

71%

18%

38%

38%

68%

71%

43%

62%

Among Brick And Mortar And Online Retailers

* = base size <100

CURRENT INVESTMENTS

FOR SLIDES 7

BASE: ALL QUALIFIED RESPONDENTS (Among Brick and Mortar Only Retailers n=40*; Among Online Only Retailers n=65*; Among Brick and Mortar and Online Retailers n=87*) Q2 Where are you currently focusing your investments? Please select all that apply.

MADE IN AMERICA PRODUCTS

7

Copyright ©

2013 The Nielse

n Co

mpany. Con

fidenJal and proprietary. 30% 15% 45% 41% 14% 55%

Adams says that with increased free

trade and global manufacturing, U.S.

consumers care more than ever about buying

products that are exclusively “Made

in America.”

■ Somewhat agree ■ Strongly agree ■ Strongly agree ■ Somewhat agree

Johnson says that with increased free trade and global manufacturing, U.S. consumers care much less than they used to about stores/companies carrying and selling products that are exclusively “Made in America.”

“MADE IN AMERICA” RESONATES (SOMEWHAT)

FOR SLIDES 7

7

Copyright ©

2013 The Nielse

n Co

mpany. Con

fidenJal and proprietary. 30% 15% 45% 41% 14% 55%

Adams says that with increased free

trade and global manufacturing, U.S.

consumers care more than ever about buying

products that are exclusively “Made

in America.”

■ Somewhat agree ■ Strongly agree ■ Strongly agree ■ Somewhat agree

Johnson says that with increased free trade and global manufacturing, U.S. consumers care much less than they used to about stores/companies carrying and selling products that are exclusively “Made in America.”

“MADE IN AMERICA” RESONATES (SOMEWHAT)

FOR SLIDES 7

Johnson says that with increased free trade and global manufacturing, U.S. consumers care much less than they used to about stores/companies carrying and selling products that are exclusively “Made in America.”

Adams says that with increased free trade and global manufacturing, U.S. consumers care more than ever about buying products that are exclusively “Made in America.”

8

2015 Retail Outlook

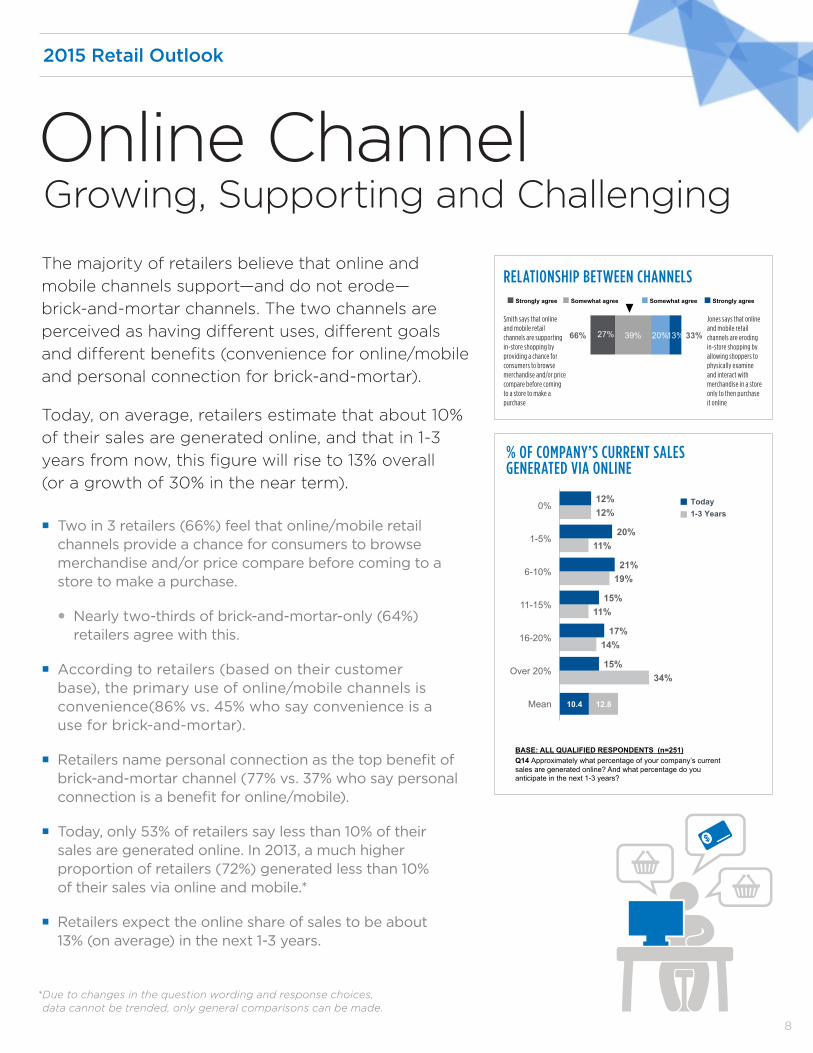

Online ChannelGrowing, Supporting and Challenging

The majority of retailers believe that online and

mobile channels support—and do not erode—

brick-and-mortar channels. The two channels are

perceived as having different uses, different goals

and different benefits (convenience for online/mobile

and personal connection for brick-and-mortar).

Today, on average, retailers estimate that about 10%

of their sales are generated online, and that in 1-3

years from now, this figure will rise to 13% overall

(or a growth of 30% in the near term).

¡ Two in 3 retailers (66%) feel that online/mobile retail channels provide a chance for consumers to browse merchandise and/or price compare before coming to a store to make a purchase.

� Nearly two-thirds of brick-and-mortar-only (64%) retailers agree with this.

¡ According to retailers (based on their customer base), the primary use of online/mobile channels is convenience(86% vs. 45% who say convenience is a use for brick-and-mortar).

¡ Retailers name personal connection as the top benefit of brick-and-mortar channel (77% vs. 37% who say personal connection is a benefit for online/mobile).

¡ Today, only 53% of retailers say less than 10% of their sales are generated online. In 2013, a much higher proportion of retailers (72%) generated less than 10% of their sales via online and mobile.*

¡ Retailers expect the online share of sales to be about 13% (on average) in the next 1-3 years.

* Due to changes in the question wording and response choices, data cannot be trended, only general comparisons can be made.

RELATIONSHIP BETWEEN CHANNELS

8

Copyright ©

2013 The Nielse

n Co

mpany. Con

fidenJal and proprietary. 39% 27% 66% 20% 13% 33%

Jones says that online and mobile retail channels are eroding in-‐store

shopping by allowing shoppers to

physically examine and interact with merchandise in a store only to then purchase it online.

■ Somewhat agree ■ Strongly agree ■ Strongly agree ■ Somewhat agree

Smith says that online and mobile retail channels are supporJng in-‐store shopping by providing a chance for consumers to browse merchandise and/or price compare before coming to a store to make a purchase.

ONLINE AND MOBILE SUPPORT; DON’T DETRACT

FOR SLIDES 8-‐9

8

Copyright ©

2013 The Nielse

n Co

mpany. Con

fidenJal and proprietary. 39% 27% 66% 20% 13% 33%

Jones says that online and mobile retail channels are eroding in-‐store

shopping by allowing shoppers to

physically examine and interact with merchandise in a store only to then purchase it online.

■ Somewhat agree ■ Strongly agree ■ Strongly agree ■ Somewhat agree

Smith says that online and mobile retail channels are supporJng in-‐store shopping by providing a chance for consumers to browse merchandise and/or price compare before coming to a store to make a purchase.

ONLINE AND MOBILE SUPPORT; DON’T DETRACT

FOR SLIDES 8-‐9

0%

34%

14%

11%

19%

11%

12%

15%

17%

15%

21%

20%

12%

Mean

Over 20%

16-20%

11-15%

6-10%

1-5%

0%

Significantly higher than Today at the 95% confidence level Significantly lower than Today at the 95% confidence level

10.4 12.8

FOR SLIDES 8-‐9

BASE: ALL QUALIFIED RESPONDENTS (n=251) Q14 Approximately what percentage of your company’s current sales are generated online? And what percentage do you anticipate in the next 1-3 years?

Today 1-3 Years

Jones says that online and mobile retail channels are eroding in-store shopping by allowing shoppers to physically examine and interact with merchandise in a store only to then purchase it online

Smith says that online and mobile retail channels are supporting in-store shopping by providing a chance for consumers to browse merchandise and/or price compare before coming to a store to make a purchase

% OF COMPANY’S CURRENT SALES GENERATED VIA ONLINE

9

2015 Retail Outlook

Online ChannelGrowing, Supporting and Challenging

However, despite the majority feeling that brick-and-

mortar-only stores represent an untenable future

business model, these retailers are concentrating

much less on their online strategy than combined

and online-only retailers.

Additionally, combined retailers see the online world

as a significant challenge that they need to adjust

to. Online-only retailers are less confounded by the

online world with more than 8 in 10 feeling they

are faring fairly well (either holding their own or

outperforming the competition).

Retailers (including online-only) favor by about a

3:2 margin to pass The Marketplace Fairness Act

in order to level the playing field between remote

sellers and local businesses.

Continued

with both a brick-and-mortar and on-line presence view the online world as a significant challenge to their brand and recognize their need to adjust accordingly

34% OF COMBINED RETAILERS say their brand works well in the online world and they are holding their own

¡ Only 18% of brick-and-

mortar-only retailers are

currently focusing their

investments on their online

presence, compared to 74%

of online-only and 71% of

combined retailers.

¡ Twenty six percent of

combined retailers feel their

brand works well in online

world and are outperforming

the competition.

¡ Nearly 6 in 10 (56%) favor the

Marketplace Fairness Act in

order to level the playing field

between remote sellers and

local retailers.

¡ Support for the Marketplace

Fairness Act is even evident

among online-only retailers

(65%).

40% OF RETAILERS

10

2015 Retail Outlook

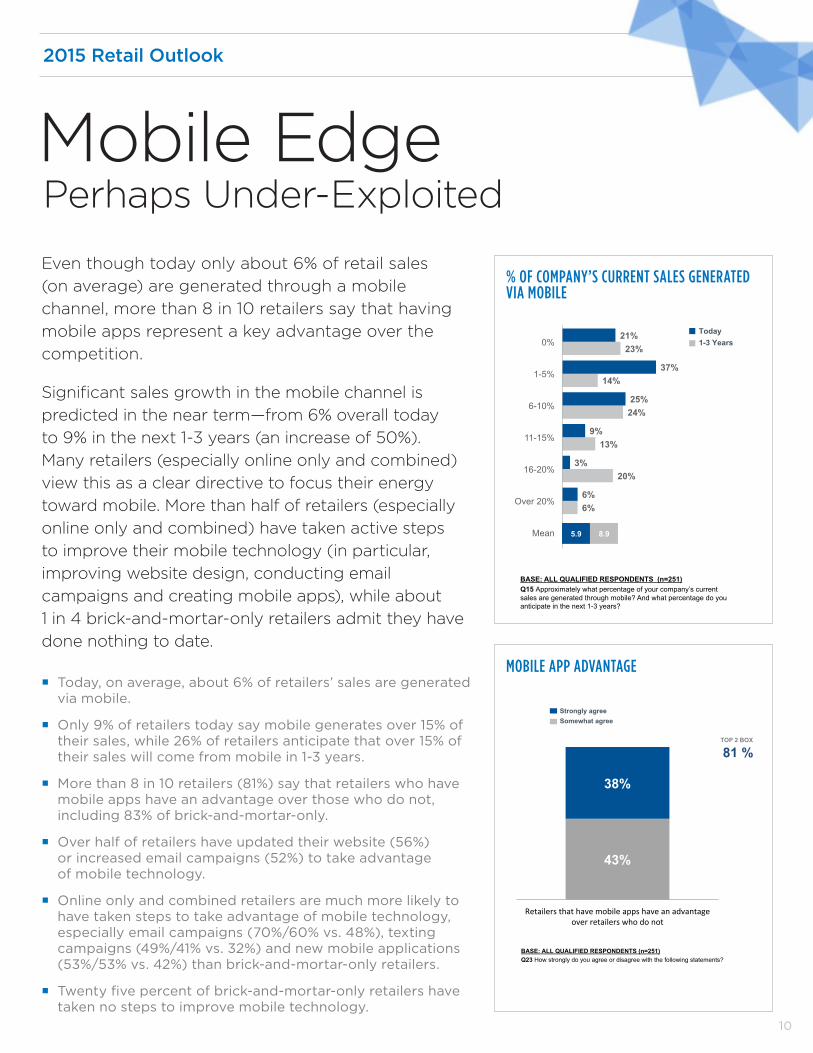

Mobile EdgePerhaps Under-Exploited

Even though today only about 6% of retail sales

(on average) are generated through a mobile

channel, more than 8 in 10 retailers say that having

mobile apps represent a key advantage over the

competition.

Significant sales growth in the mobile channel is

predicted in the near term—from 6% overall today

to 9% in the next 1-3 years (an increase of 50%).

Many retailers (especially online only and combined)

view this as a clear directive to focus their energy

toward mobile. More than half of retailers (especially

online only and combined) have taken active steps

to improve their mobile technology (in particular,

improving website design, conducting email

campaigns and creating mobile apps), while about

1 in 4 brick-and-mortar-only retailers admit they have

done nothing to date.

¡ Today, on average, about 6% of retailers’ sales are generated via mobile.

¡ Only 9% of retailers today say mobile generates over 15% of their sales, while 26% of retailers anticipate that over 15% of their sales will come from mobile in 1-3 years.

¡ More than 8 in 10 retailers (81%) say that retailers who have mobile apps have an advantage over those who do not, including 83% of brick-and-mortar-only.

¡ Over half of retailers have updated their website (56%) or increased email campaigns (52%) to take advantage of mobile technology.

¡ Online only and combined retailers are much more likely to have taken steps to take advantage of mobile technology, especially email campaigns (70%/60% vs. 48%), texting campaigns (49%/41% vs. 32%) and new mobile applications (53%/53% vs. 42%) than brick-and-mortar-only retailers.

¡ Twenty five percent of brick-and-mortar-only retailers have taken no steps to improve mobile technology.

% OF COMPANY’S CURRENT SALES GENERATED VIA MOBILE

MOBILE APP ADVANTAGE

0%

6%

20%

13%

24%

14%

23%

6%

3%

9%

25%

37%

21%

Mean

Over 20%

16-20%

11-15%

6-10%

1-5%

0%

Significantly higher than Today at the 95% confidence level Significantly lower than Today at the 95% confidence level

5.9 8.9

FOR SLIDE 10

Today 1-3 Years

BASE: ALL QUALIFIED RESPONDENTS (n=251) Q15 Approximately what percentage of your company’s current sales are generated through mobile? And what percentage do you anticipate in the next 1-3 years?

43%

38%

Retailers that have mobile apps have an advantage over retailers who do not

Page 10

BASE: ALL QUALIFIED RESPONDENTS (n=251) Q23 How strongly do you agree or disagree with the following statements?

*= base size <100

81 % TOP 2 BOX

Strongly agree Somewhat agree

11

2015 Retail Outlook

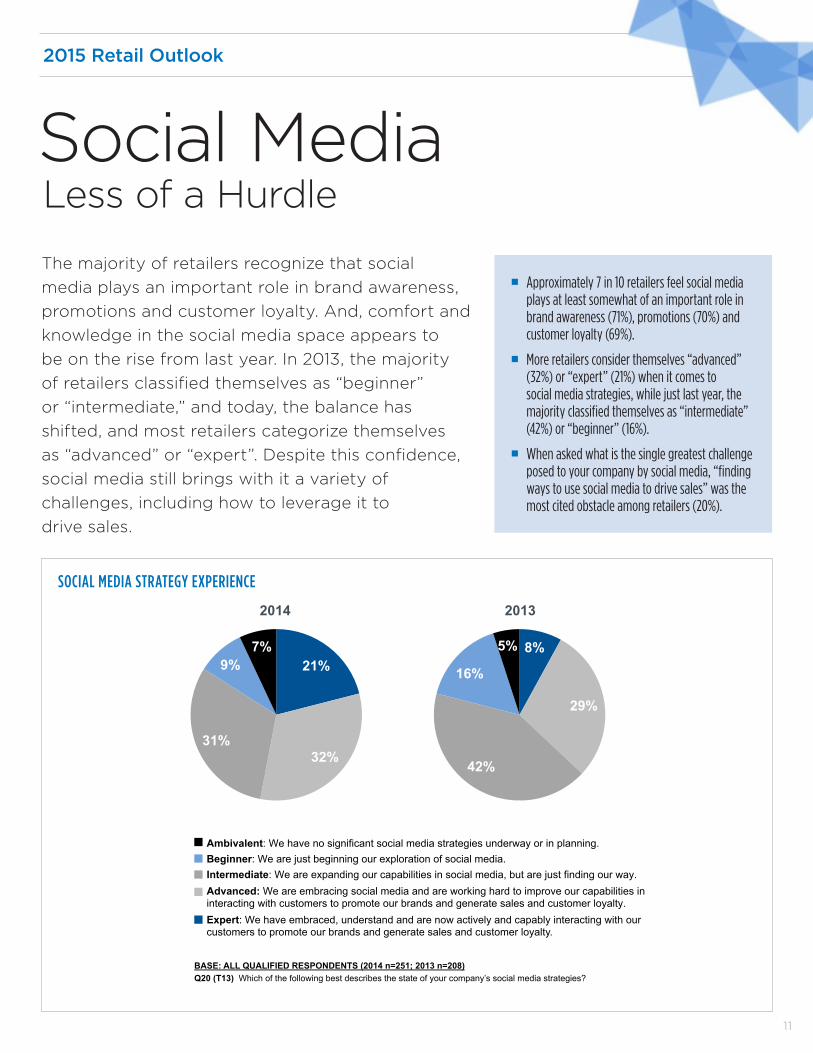

Social MediaLess of a Hurdle

The majority of retailers recognize that social

media plays an important role in brand awareness,

promotions and customer loyalty. And, comfort and

knowledge in the social media space appears to

be on the rise from last year. In 2013, the majority

of retailers classified themselves as “beginner”

or “intermediate,” and today, the balance has

shifted, and most retailers categorize themselves

as “advanced” or “expert”. Despite this confidence,

social media still brings with it a variety of

challenges, including how to leverage it to

drive sales.

¡ Approximately 7 in 10 retailers feel social media plays at least somewhat of an important role in brand awareness (71%), promotions (70%) and customer loyalty (69%).

¡ More retailers consider themselves “advanced” (32%) or “expert” (21%) when it comes to social media strategies, while just last year, the majority classified themselves as “intermediate” (42%) or “beginner” (16%).

¡ When asked what is the single greatest challenge posed to your company by social media, “finding ways to use social media to drive sales” was the most cited obstacle among retailers (20%).

FOR SLIDE 11

Ambivalent: We have no significant social media strategies underway or in planning. Beginner: We are just beginning our exploration of social media. Intermediate: We are expanding our capabilities in social media, but are just finding our way. Advanced: We are embracing social media and are working hard to improve our capabilities in interacting with customers to promote our brands and generate sales and customer loyalty. Expert: We have embraced, understand and are now actively and capably interacting with our customers to promote our brands and generate sales and customer loyalty.

BASE: ALL QUALIFIED RESPONDENTS (2014 n=251; 2013 n=208) Q20 (T13) Which of the following best describes the state of your company’s social media strategies?

8%

29%

42%

16%

5% 21%

32% 31%

9% 7%

2014 2013

SOCIAL MEDIA STRATEGY EXPERIENCE

12

2015 Retail Outlook

Methodology

About the Harris Poll

This study was commissioned by CIT and conducted online by Harris Poll within the United States between September 16 and October 3, 2014, among 251 financial decision makers within the retail industry working at companies with revenue between $5 million and $3 billion.

The data for this research study was weighted to ensure that the data is balanced and accurately represents the firmographics of interest to CIT. Figures for: industry, title, functional role, decision-maker role, company ownership structure and company location/region were weighted to bring them into line with the respondent profile from prior research.

All sample surveys and polls, whether or not they use probability sampling, are subject to multiple sources of error which are most often not possible to quantify or estimate, including sampling error, coverage error, error associated with nonresponse, error associated with question wording and response options, and post-survey weighting and adjustments. Therefore, The Harris Poll avoids the words “margin of error” as they are misleading. All that can be calculated are different possible sampling errors with different probabilities for pure, unweighted, random samples with 100% response rates. These are only theoretical because no published polls come close to this ideal.

Over the last 5 decades, Harris Polls have become media staples. With comprehensive experience and precise technique in public opinion polling, along with a proven track record of uncovering consumers’ motivations and behaviors, The Harris Poll has gained strong brand recognition around the world. The Harris Poll offers a diverse portfolio of proprietary client solutions to transform relevant insights into actionable foresight for a wide range of industries including health care, technology, public affairs, energy, telecommunications, financial services, insurance, media, retail, restaurant and consumer packaged goods. Contact us for more information: [email protected].

ABOUT CITFounded in 1908, CIT (NYSE: CIT)

is a financial holding company with

more than $35 billion in financing

and leasing assets. It provides

financing, leasing and advisory

services to its clients and their

customers across more than 30

industries. CIT maintains leadership

positions in middle market lending,

factoring, retail and equipment

finance, as well as aerospace,

equipment and rail leasing. CIT’s

U.S. bank subsidiary CIT Bank

(Member FDIC), BankOnCIT.com,

offers a variety of savings options

designed to help customers achieve

their financial goals. www.cit.com

www.cit.com/viewfromthemiddleTo subscribe to the CIT View from the Middle, please send an email to: [email protected].

FOR PRESS INQUIRIES PLEASE CONTACTCurt RitterSenior Vice President, Corporate [email protected]

Matt KleinVice President, Media [email protected]

FOR BUSINESS INQUIRIES PLEASE CONTACTDan InfantiSenior Vice President, Marketing and [email protected]

Debbie HaeringerDirector, Content [email protected]