DWF Future of Retail Report

16

THE FUTURE OF RETAIL 05 BECOMING OMNICHANNEL 08 SAFETY IN NUMBERS 10 GLOBAL REACH WELCOME £

-

Upload

stephanie-causey -

Category

Documents

-

view

137 -

download

0

Transcript of DWF Future of Retail Report

THE FUTURE OF RETAIL

05BECOMING

OMNICHANNEL

08SAFETY IN NUMBERS

10GLOBAL REACH

WELCOME

£

02

FOR FURTHER INFORMATION PLEASE CONTACT

02

OPEN

Hilary RossHead of Retail, Food and Hospitality, DWF E: [email protected]: +44 (0)3333 20 32 10

Alan Owens Head of Technology and Communications, DWFE: [email protected] T: +44 (0)20 7645 4139

03

In a rapidly changing market, retailers are focusing on delivering value and quality in an omnichannel world, while trying to navigate the complex political landscape of the living wage and a potential exit from the European Union. The top five growth areas identified by the retailers in our survey gives an insight into the long-term strategy for investment in bridging the gap between offline and digital channels.

1. MultichannelOmnichannel is still king. Retailers need to make sure that their propositions are consistent across all channels. Click and collect may seem an old idea, but it is at the sharp end of many omnichannel experiences and continues to grow as it drives increased customer spending in-store.

E-commerce retailers are looking to set up shop on the high street. The majority of retail sales are still taking place offline and, although the retailers that participated in this survey predict this will change to a 70/30 split in favour of online in as little as five years’ time, e-commerce retailers are recognising the need to set up physical shops if they want to gain significant market share.

2. Technology systemsTraditional bricks-and-mortar retailers will need to invest to win against companies for whom data optimisation, data

security and customer fulfilment are in their DNA. Mobile will continue to grow until it matches bricks-and-mortar. Yet it will also be a key driver in bricks-and-mortar sales, as customers use their mobiles in-store, and integrated digital touchpoints will be critical investments for many.

3. International expansionOverseas expansion continues to drive opportunities for growth and increased profits. As the UK market edges ever closer to saturation, retailers are looking to mature in emerging economies, with omnichannel and supply chain technology as their passport to successful international expansion. However, expansion is not for the faint hearted, with cultural differences, mercurial regulatory regimes

and differing customer expectations all presenting significant challenges.

4. Big dataMaking data work harder is key. Bricks-and-mortar retailers know they have a lot of work to do if they are to catch up with their online competitors. Retailers are examining how they can better mine their data to get to know their customers, while optimising and personalising the shopping experiences across the omnichannel.

Finding better ways to protect customers’ privacy and data is also important. Every month brings reports of another retailer facing the reputational nightmare of a major data breach. Motivated by customers’ expectations, brand reputation, shareholders and the costs of dealing with a significant

incident, retailers are on a path of investment and improvement in this area.

5. Warehouse efficiencyInvestment will improve fulfilment. With online native retailers setting the bar for speed and convenience, traditional retailers recognise the need to invest in robust order fulfilment, stock awareness and lightning-speed deliveries.

Then, now and in the future, value and quality will remain the bywords of any successful retail proposition, but the challenge will be how to align these traditional values for a modern age of retail, where an integrated, accessible and secure customer experience is the norm rather than the exception. That will take clear strategic thinking and balanced investments that UK retailers are well placed to make.�

££

FIGURE 1 TOP 5 AREAS WHERE RETAILERS ARE FOCUSING TO DRIVE GROWTH IN THE NEXT 3 YEARS

DATA SHOWS % OF RESPONDENTS WHO CONSIDERED FACTOR TO BE IN TOP 3

51%

35%

22%

43%

51%

MULTICHANNEL TECHNOLOGY SYSTEMS

INTERNATIONAL EXPANSION

BIG DATA

WAREHOUSE EFFICIENCY

15%

9%

13%

15%

17%

17%

5%

3%

4%

PERSONALISATION OF ADVERTISING

SOCIAL MEDIA AS A RETAIL PLATFORM

SOURCING

FULFILLMENT SOLUTIONS

CORPORATE SOCIAL RESPONSIBILITY (CSR)

LOGISTICS

LOCALISATION

SUNDAY TRADING

TRANSATLANTIC TRADE AND INVESTMENT PARTNERSHIP

04

DEMOGRAPHICThis report has been compiled through telephone interviews with 150 C-suite executives from leading retail organisations in the UK

RETAILER TARGET DEMOGRAPHIC

JOB ROLE

2%CEO

39%CFO

3%CIO

7%CRO

39%HEAD OF SUPPLY CHAIN

9%HEAD OF TREASURY

SIZE

AGESOCIO-ECONOMIC GROUP

RETAIL SECTOR

9%DEPARTMENT STORESDIY, HOME & GARDEN

ELECTRICALS & TECHNOLOGYENTERTAINMENT

FASHIONFOOD & BEVERAGES

GENERAL MERCHANDISE HEALTH & BEAUTY

LUXURYPERSONAL FINANCE &

BANKING SPORTS & LEISURE

5%UTILITIES

1%

63%

36%

0%

81%

10%

70+

18-34

55-69

AB

C1

C2 8%

DE 1%

35-54

TURNOVER

EMPLOYEES

63%18%

27%

29%

26%

4% 7%

GEOGRAPHICAL COVERAGE

67%

650-1,500 1,501-5,000EMPLOYEES1,501-25,000 25,001+

$50-100m $100-250mTURNOVER$250m-1bn 1bn+

59%

10%23%

8%

REGIONAL NATIONAL GLOBALEUROPEAN

22%

04

All percentages rounded to nearest whole number

05

BECOMING OMNICHANNELDespite retailers seeing online channels as a growing sector,

few believe they have yet embraced a comprehensive strategy

retailers believe that value will remain a key demand from shoppers in the future.

Retailers are fully embracing the value and opportunities presented by online channels, with 49 per cent reporting that they are planning to give it the most investment over the next three years – retailers with limited or no e-commerce offering are now rare. Fashion retailers (77 per cent) in particular are showing signs of embracing this wholeheartedly and they already generate 65 per cent of their sales online. Consumers no longer feel they need to “try before

they buy” as they can do it in the comfort of their own home following delivery. This is due to retailers such as ASOS and Marks & Spencer making delivery quick and inexpensive, with the opportunity to return items being equally simple.

Despite the widespread recognition by retailers that online and omnichannel represent the future, 85 per cent admit that their omnichannel strategy is only at a basic or intermediate

There is no escaping omnichannel. It is at the forefront of retailers’ minds as it continues to drive the majority of sales growth. Retailers are predicting that 42 per cent of sales will be through e-commerce in five to ten years. Critically, however, they expect m-commerce sales to grow substantially to 29 per cent, equalling sales through physical stores. This shows, for the first time, a more balanced omnichannel experience.

A major reason for an omnichannel future are the digital natives who have grown up buying across channels and will, over the next five to ten years, move into the 18 to 34-year-old grouping when they will develop greater buying power.

With mobile technology now augmenting the physical shopping experience, and shopping destinations and stores increasingly offering complimentary wi-fi, it is surprising that only 17 per cent of retailers regard omnichannel as a key driver for customers. Most retailers now believe that this experience has already ceased to be a differentiator, at least as far as product purchasing decisions are concerned, as consumers increasingly expect it as standard.

By contrast, the proliferation of price promotions and claims of “everyday low prices” underlines why 61 per cent of

FIGURE 2 CHANNEL MIX: 2015 COMPARED WITH 2020-25

ONLINE E-COMMERCEM-COMMERCE BRICKS & MORTAR

44%

56%

2015

42%

29%

29%

2020/25

65% of fashion retailers’ sales are already online

>

06

8%

23%

31%

38%

FIGURE 3 WHICH STATEMENT BEST DESCRIBES YOUR COMPANY’S PROGRESS IN IMPLEMENTING/EXECUTING AN OMNICHANNEL STRATEGY?

TOTAL

64% 21% 6% 1%8%

OPPOSED: A decision has been made to pursue a multichannel strategy as opposed to omnichannel UNDEVELOPED: We are scoping out our omnichannel options but are yet to set our long-term strategy BASIC: We are defining our strategy and beginning to execute the plan INTERMEDIATE: We have identified our strategy and are executing on it ADVANCED: We have made greater progress than most of our peers and have executed most of our strategy

GENERAL MERCHANDISE

31%

54%

15%

ELECTRICALS & TECHNOLOGY

38%

31%

8%

23%

FOOD & BEVERAGES

69%

31%

SPORTS & LEISURE

69%

8%

23%

FASHION

£

31%

69%

ENTERTAINMENTLUXURY

8%

15%

77%

15%

85%

PERSONALFINANCE & BANKING

DIY, HOME & GARDEN

8%

92%85%

8%

8%

HEALTH & BEAUTY

UTILITIES

57%

43%

DEPARTMENT STORES

92%

8%

07

FIGURE 4 WHAT ARE RETAILERS’ CUSTOMERS TOP 2 DEMANDS

DATA SHOWS % OF RESPONDENTS WHO CONSIDERED DEMANDS TO BE IN TOP 2

61%

9%

PRODUCT PROVENANCE

17%

OMNICHANNEL OFFER

22%

DEMONSTRABLE CSR

GREATER VALUE/ PRICING

31%

IMPROVED IN-STORE

EXPERIENCE

11%

LOCALISED PRODUCT MIX

32%

LOYALTY PROGRAMMES

17%

MORE FLEXIBLE

FULFILMENT

61% of retailers believe thatvalue will remain a key demandfrom shoppers in the future

The “store within store” concept, linking major brands, means that the way those brands are marketed will be diverse - co-branding agreements and revenue sharing will be central.

Increased reliance on mobile marketing means that logistics agreements and tie-ups will need to be regularly reviewed.

KPIs and service-level credits will be more important, as recent case law on penalties shows.

Selective distribution channels are often in the competition regulators’ line of sight. The criteria for maintaining channels needs to be rethought where digital purchases become the norm.

KEY LEGAL ACTION POINTS

level. Just 8 per cent believe it is advanced, which suggests a competitive advantage can be achieved by those retailers that knit together a seamless cross-channel experience for their customers.

The value in pursuing omnichannel strategies is

obvious, as the belief from retailers is that growth will be derived from across a variety of channels. Retailers estimated that in five to ten years’ time, the split between e-commerce, m-commerce and bricks-and-mortar will will start to even out (see figure 2).�

08

Data is now the lifeblood of retail. Online marketplaces have created mountains of information, which have provided significant insights into customer behaviour. This data has also created opportunities for vast improvements in the management of stock with a level of precision never previously possible.

One third (32 per cent) of retailers identified loyalty programmes as a key development that customers will demand in the future. Despite the value of Tesco’s Clubcard being questioned recently, it appears there may be a renaissance in

such tools, with Lidl trialling a scheme and Morrisons having launched its Match & More loyalty card in 2014.

An electrical retailer summarises the value of these schemes, indicating it “planned to collect customer data and customise offers to meet their needs through data and analytics investments”.

Could this collation of customer data lead to a heightened fear of data breaches? Certainly a sizeable 32 per cent of retailers cite cyber/data breaches as one of the biggest threats to their businesses over the next

SAFETY IN NUMBERSThe savvy retailer will use customer data to their

advantage, but businesses are increasingly wary of the dangers of data breaches

FIGURE 5 TOP 10 FACTORS THAT WILL THREATEN GROWTH IN THE NEXT THREE YEARS

of retailers agree that data security

is imperative to brand reputation

99%

three years. Data security is undoubtedly a serious matter as a massive 99 per cent of retailers agree it is imperative for their brand reputations that they do not suffer such online security failures.

Despite the potential risks, the use of data to personalise services for customers is a major way for retailers to differentiate in a market where as many as 61 per cent of companies regard value/pricing as a key demand from customers. One area where this use of data appears is through tailored marketing and advertising, with 17 per cent of merchants believing it

DATA SHOWS % OF RESPONDENTS WHO CONSIDERED FACTOR TO BE IN TOP 3

SUPPLY CHAIN SECURITY15%

LACK OF MARGIN15%

NEW PAYMENT SYSTEMS17%

REGULATION FROM THE UK/EU40%

BUSINESS RATES17%

BREXIT21%

CURRENCY FLUCTUATIONS25%

NATIONAL LIVING WAGE27%

CYBER/DATA BREACHES32%

IT SYSTEMS38%

09

will drive future growth. One luxury goods

retailer says: “Customer engagement and continuous communication can help in identifying the need to add, change or improve product lines, offers and prices.”

Mobile devices are increasingly involved, and retailers like House of Fraser and John Lewis are investigating using in-store “beacons” to identify shoppers when they enter a store and then deliver personalised offers to their phones, as well as indicating when any click-and-collect items are ready for collection.

Despite the potential for the use of data analytics and the growing amount of trials taking place, the consensus among

retailers is that the effectiveness of their investments in this area is very poor. Few retailers score themselves above two out of five, which is a concern as the

FIGURE 6 ESTIMATED INVESTMENT LEVEL IN DATA ANALYTICS BY BUSINESS AREA

LOW MEDIUM HIGH

value of data will become evermore important to them in developing successful multichannel models.�

Tighter Europe-wide regulation of data security is coming in 2016.

Best practice and mitigation of problems caused by cyber breaches dictates clear-headed decisions about when not to collect data, move to anonymous aggregation and when to delete data.

Use of beacons and other technologies means retailers need to ensure

consent is clearly obtained, particularly from children and teens.

The collection of data also demands ongoing investments in security, regular review of retention policies and cr isis -response plans. Legal teams need to play a central role in incident responses to maintain pr ivilege in cr isis communications.

KEY LEGAL ACTION POINTS

STRATEGIC PLANNING SUPPLY CHAIN MANAGEMENT LOGISTICS INVENTORY MANAGEMENT MARKETING/SALES CUSTOMER EXPERIENCE

65%

9%

19%

51%

14%

46%

23%

45%

37%

49%

33%

56%

11%15%33%40%29%25%

10

geographical boundaries of the internet to test international strategies in a quick, cheap and often lower-risk way.

It is therefore not surprising that 49 per cent of retailers say e-commerce is the format that will receive the most focus for investment.

While international expansion offers great opportunities for growth, especially online, it is also where the biggest competition comes from, with 47 per cent of retailers saying global online represents the most significant threat to their future growth. It is clear that international, and in particular the use of online across borders, are key battlegrounds.

Expansion plans are predominantly focused on the EU and Asia, with 47 per cent of retailers looking at Europe, while 32 per cent are targeting Asia. Department stores and general merchandise retailers have a particularly strong bias to EU expansion, with 77 per cent of companies prioritising this region.

In contrast, only 2 per cent are focusing on North America, which may explain why some retailers are less interested in the potential impact of the Transatlantic Trade and Investment Partnership negotiations. It

is a similar story with Africa, where virtually no interest is being shown in expansion into the territory.

There are many models available to launch internationally, from using third parties under licence or as commercial agents or franchise, through to the business taking the plunge itself, or benefiting from the local experience of a joint

GLOBAL REACHInternational expansion is central to many retailers’

futures, with a focus on a low-cost, low-risk e-commerce strategy

see international expansion as a top three factor that will drive growth in the next three years

43%

49%

4%

17%

9%

7%

5%

7%2%

FIGURE 7 WHICH RETAIL FORMAT WILL RECEIVE THE MOST FOCUS AND INVESTMENT OVER THE NEXT THREE YEARS?

E-COMMERCEFACTORY OUTLETSFRANCHISEVENDINGBOUTIQUECLICK & COLLECTCONCESSIONSDISCOUNTER

0%POP-UPCONVENIENCE

Tesco might be retreating from its international operations – as recently demonstrated by the sale of its South Korea business - but overseas expansion remains a major area of growth for UK retailers. As many as 43 per cent regard it as one of the top three areas they intend to focus on over the next three years.

Many retailers, including the likes of N Brown, Superdry and Marks & Spencer, have used the unlimited

11

FIGURE 8 WHICH GEOGRAPHICAL AREAS WILL YOUR COMPANY LOOK TO TARGET FOR EXPANSION?

FIGURE 9 WHERE IS YOUR GREATEST COMPETITION GOING TO COME FROM OVER THE NEXT THREE YEARS?

venture. What is clear is that retailers are less keen on local market M&A, as just 5 per cent saw this as the route to market entry, clearly favouring the increased control the other routes provide.

This focus on international development perhaps explains why 31 per cent of retailers regard BREXIT (Britain leaving the EU) as a serious threat to their future

UTILITIES

SPORTS & LEISURE

FASHION

ENTERTAINMENT

DEPARTMENT STORES

M&A DIRECT INVESTMENT

JOINT VENTURES

STRATEGIC ALLIANCES

FRANCHISE/LICENCE

DIRECT EXPORT

INDIRECT EXPORT

OFFICE LOCATION

5% 21% 8% 26% 18% 16% 6%1%

40-50%30-39%20-29%10-19%0-9%

HOW WILL GROWTH BE ACHIEVED?

£

43% 57%

31% 38% 31%

92% 8%

31% 38% 31%

46% 23% 31%

DISCOUNTERS GLOBAL OFFLINE GLOBAL ONLINE UK OFFLINE UK ONLINE

TOTAL 17% 9% 47% 9% 18%

growth and the 60 per cent who viewed EU regulation as a key challenge. Inevitably, even in times of increasingly harmonised EU laws, the local interpretations and practical difficulties arising out of dealing in many languages across the EU gives rise to many practical challenges that retailers typically use technology to overcome.�

Thinking about relationships across borders is crucial. Too often, arrangements are entered into without thought as to the legal consequences in the partner’s country of origin.

Be aware of key differences, such as negotiations, that may become binding before

signature, overriding “good faith” requirements, and the inability to summarily terminate distribution or supplier contracts. Think also about commercial agents’ rights to compensation upon lawful termination – still catching out companies a decade after the EU regulations became effective.

KEY LEGAL ACTION POINTS

12

Competition from online rivals is regarded as a major threat to traditional retailers’ futures; the omnichannel revolution gives them an opportunity to compete, but a robust and flexible online order-fulfilment proposition covering both web and mobile sales is now critical to success.

Amazon and Argos are among the retailers fighting it out to offer quicker delivery times in tighter delivery-slot windows – 57 per cent of retailers are considering free delivery, 54 per cent click and collect, and 47 per cent looking to offer precise delivery times as part of their fulfilment strategy.

In contrast, while there has been considerable hype, it appears in reality there is little interest in same-day delivery or drones – not withstanding that Amazon announced it was trialling both.

Free delivery is most relevant to the food and beverage category, with 85 per cent considering such a strategy, which definitely puts margins under pressure. Further stress on the major grocers is coming from AmazonFresh and PrimeNow, with a further convergence of the big online retailers expected into more traditional markets.

DELIVERING THE GOODSMaintaining a cost-effective delivery and returns

service is a challenge facing all retailers battling to win consumer loyalty

The emergence of new delivery models from technology-led newcomers, such as Uber, are also shaking up the market. Denmark-based Dansk Supermarked has admitted finding it tough to make food delivery profitable and is therefore considering using new logistics solutions from the likes of Uber.

In our Supply Chain Report last year, we saw how it is no longer acceptable to only focus on getting goods to consumers. Another fulfilment pressure point for retailers is returns. Dealing with unwanted goods is a costly and time-consuming activity that again eats into online margins. But a failure to offer a comprehensive returns policy would be detrimental to any retailer.

Charging customers for any part of the in-store delivery-and-returns element of online ordering had been avoided by all retailers, until John Lewis recently began charging £2 for click and collect orders valued at less than £30. Early evidence is that the lost sales have been offset by some shoppers bulking up their orders to cross the minimum-spend threshold.�

12

FIGURE 10 WHICH ORDER-FULFILMENT STRATEGIES ARE YOU CONSIDERING?

DATA SHOWS % OF RESPONDENTS WHO CONSIDERED STRATEGY TO BE IN TOP 2

FIGURE 11 WHICH RETURNS SOLUTIONS WILL YOUR COMPANY FOCUS ON?

75%53% 65%

FREE RETURNS PRECISE PICK-UP TIMES IN-STORE RETURNS

DROP OFF7%

DRONES0%

DATA SHOWS % OF RESPONDENTS WHO CONSIDERED STRATEGY TO BE IN TOP 2

9% SAME-DAY DELIVERY

47%PRECISE

DELIVERY TIMES

11% ON-THE-GO RETAIL

12%NON-TRADITIONAL

DELIVERY MECHANISMS

57% FREE DELIVERY

11%CLICK AND COLLECT

(REMOTE LOCATIONS/LOCKERS)

54%CLICK AND COLLECT

(IN-STORE)

13

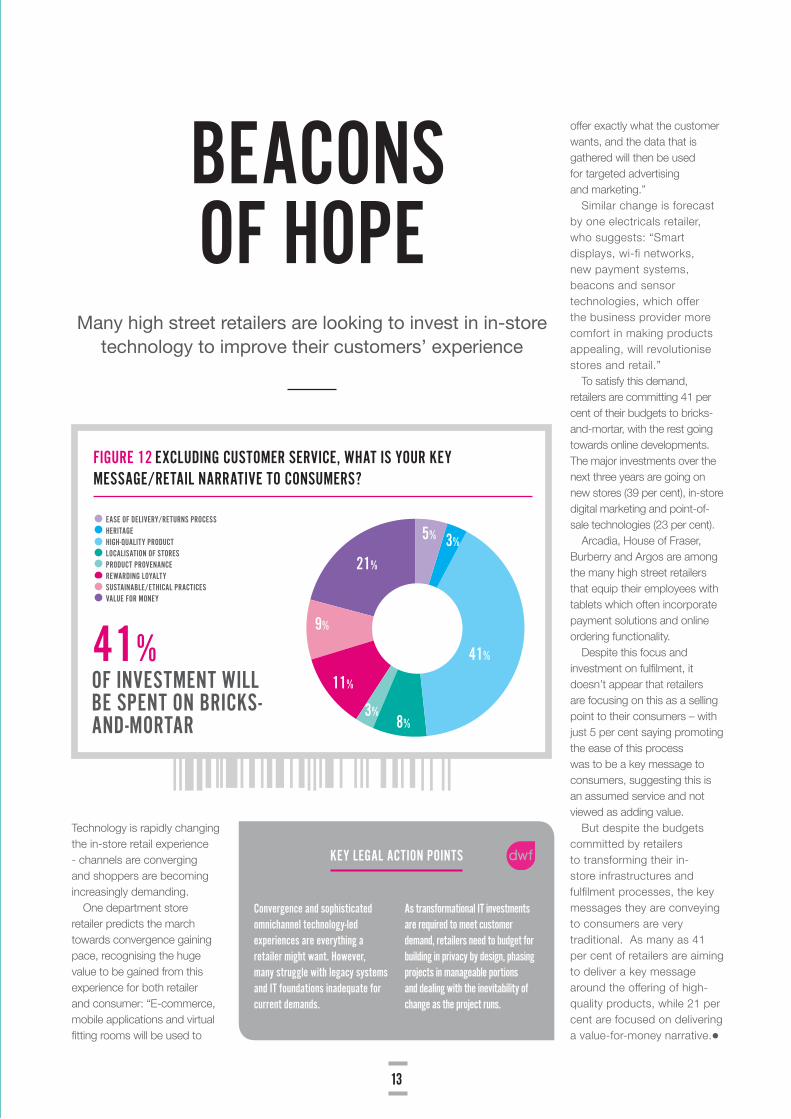

Technology is rapidly changing the in-store retail experience - channels are converging and shoppers are becoming increasingly demanding.

One department store retailer predicts the march towards convergence gaining pace, recognising the huge value to be gained from this experience for both retailer and consumer: “E-commerce, mobile applications and virtual fitting rooms will be used to

FIGURE 12 EXCLUDING CUSTOMER SERVICE, WHAT IS YOUR KEY MESSAGE/RETAIL NARRATIVE TO CONSUMERS?

BEACONS OF HOPE

Many high street retailers are looking to invest in in-store technology to improve their customers’ experience

offer exactly what the customer wants, and the data that is gathered will then be used for targeted advertising and marketing.”

Similar change is forecast by one electricals retailer, who suggests: “Smart displays, wi-fi networks, new payment systems, beacons and sensor technologies, which offer the business provider more comfort in making products appealing, will revolutionise stores and retail.”

To satisfy this demand, retailers are committing 41 per cent of their budgets to bricks-and-mortar, with the rest going towards online developments. The major investments over the next three years are going on new stores (39 per cent), in-store digital marketing and point-of-sale technologies (23 per cent).

Arcadia, House of Fraser, Burberry and Argos are among the many high street retailers that equip their employees with tablets which often incorporate payment solutions and online ordering functionality.

Despite this focus and investment on fulfilment, it doesn’t appear that retailers are focusing on this as a selling point to their consumers – with just 5 per cent saying promoting the ease of this process was to be a key message to consumers, suggesting this is an assumed service and not viewed as adding value.

But despite the budgets committed by retailers to transforming their in-store infrastructures and fulfilment processes, the key messages they are conveying to consumers are very traditional. As many as 41 per cent of retailers are aiming to deliver a key message around the offering of high-quality products, while 21 per cent are focused on delivering a value-for-money narrative. �

41%

3%

5%

21%

9%

11%

3%

8%

EASE OF DELIVERY/RETURNS PROCESS HERITAGEHIGH-QUALITY PRODUCTLOCALISATION OF STORES PRODUCT PROVENANCEREWARDING LOYALTYSUSTAINABLE/ETHICAL PRACTICESVALUE FOR MONEY

41% OF INVESTMENT WILL BE SPENT ON BRICKS-AND-MORTAR

Convergence and sophisticated omnichannel technology-led experiences are everything a retailer might want. However, many struggle with legacy systems and IT foundations inadequate for current demands.

As transformational IT investments are required to meet customer demand, retailers need to budget for building in privacy by design, phasing projects in manageable portions and dealing with the inevitability of change as the project runs.

KEY LEGAL ACTION POINTS

14

The old adage goes that retail is detail and people do detail. It has never been a more competitive market for ensuring retailers have the right people to power their business, with the living wage the latest employment-related issue to dominate the agenda.

While often portrayed in a negative light and as a cost to business, only 27 per cent of retailers saw it as a key threat to growth over the next three years, viewing areas such as regulatory change, and IT and data security as bigger issues.

The ability to retain and motivate the best staff is key. Wages are clearly crucial and therefore it is fundamental retailers buy into improved remuneration.

Only 36 per cent of those we asked thought they would

EARNING POTENTIALThe introduction of the living wage is forcing

retailers to rethink their staffing structures, training programmes and premium payments policies

not be affected by introducing the living wage. Those who thought there would be an impact on their business sought to offset this by passing on the cost to consumers (23 per cent) and suppliers (18 per cent), with very few expecting to reduce staff numbers (3 per cent) – see figure 13.

FIGURE 13 WHAT WILL BE THE BIGGEST EFFECT OF THE INTRODUCTION OF THE NATIONAL LIVING WAGE ON YOUR BUSINESS?

DECREASED STAFF NUMBERSCOSTS PASSED DOWN TO SUPPLIERSLESS INVESTMENT IN NEWS STORESINCREASED COSTS FOR CONSUMERSINCREASED RECRUITMENT FROM ABROADNO EFFECT

Larger companies feel better able to handle the living wage, with almost half believing it will be immaterial to how they run their organisation, while smaller firms think there is a greater likelihood of passing on costs to the customer.

Many employers are reviewing their pay structures

and the roles employees undertake. A fairer pay system will encourage and reward employees, and ensure greater engagement. Staff engagement is also maximised by investment in skills and employees’ understanding of the business. Training on products and ever-changing technology is of paramount importance.

Investment in training and higher wages are not, however, dampening retailers’ enthusiasm for growing their workforces with many employing an increasing number of people from outside the European Union. As many as 79 per cent of retailers expect to increase recruitment of such workers over the next three years. No company expects a decrease in numbers among their non-EU workforce. �

36%4%23%15%18%3%

Review pay structures to assess fairness, and ability to stay in line with proposed changes to national minimum wage, living wage, equal pay or pensions.

Use the opportunity to revise structures with historical unfairness or out-

of-date premium, and make an assessment of the financial risks and challenges to the organisation. It is important to consult early on with staff/unions on the changes proposed and consider the job roles and changes required as part of the pay restructure.

KEY LEGAL ACTION POINTS

15

CLOSED

CONCLUSION

Capital structure: With only 15 per cent of retailers

looking to deleverage, 85 per cent of retailers favour private equity as their main source of financing. The stock market is reluctant to invest capital in retailers, with many leading names reporting falling sales and margins. The optimal business and assets mix also remains unresolved, with concerns lingering over portfolio size, format and location. This is, in part, being driven by a challenge to traditional assumptions about freeholds underpinning value and supporting debt.

A further challenge to existing models is industry consolidation, exemplified by the Carphone Warehouse and Dixons merger, and prospect of Sainsbury’s acquisition of Argos.Private equity remains interested in seizing opportunity, but caution over leveraging debt and restricted exit routes are inhibiting investment.

Ominichannel: This creates significant opportunities, but

these can become challenges if they aren’t supported by a strong legal platform. The need to ensure that data is managed effectively and consumer information robustly protected is paramount to any retailer’s reputation. Do not wait for a crisis to unfold to test your systems – a crisis simulation event is essential to understanding what needs to be done to protect your brand.

Mobile: Increased reliance on mobile marketing means

that logistics agreements and tie-ups will need to be regularly reviewed to ensure they remain fit for purpose for the flexible world of mobile.

CSR: This is firmly on retailers’ agendas, not

least as a way to increase brand development. There are an increasing number of

legal challenges to convert the moral responsibilities associated with CSR into legal liabilities. For many retailers this is the cost of doing business; for others that seek to de-risk their business these legal developments need to be closely analysed.

Taxes: Staff reductions, pensions, directors’

remuneration, international expansion, and the increasing onus of compliance, risk and CSR all bring significant tax considerations. From April 2017, HMRC will be collecting the apprenticeship levy at 0.5 per cent of payroll cost over £3 million. For large retailers that will be a significant amount of additional tax (around £10 million for the large supermarkets).The consultation outcome suggests that some, if not all the cash may be able to be recycled to meet some training needs. Careful consideration needs to be given to the combination of tax and education.�

16