Do political connections affect a firm performance? · i Abstract Previous studies have indicated...

136

Do political connections affect a firm’s performance? Amiruddin This thesis is presented for the degree of Doctor of Business Administration of The University of Western Australia UWA Business School Accounting and Finance 2016

Transcript of Do political connections affect a firm performance? · i Abstract Previous studies have indicated...

Do political connections affect a firm’s performance?

Amiruddin

This thesis is presented for the degree of

Doctor of Business Administration of

The University of Western Australia

UWA Business School

Accounting and Finance

2016

i

Abstract

Previous studies have indicated that political connection can be a source of value to a

firm, and may affect firm performance.

This study has examined the links between political connection and firm performance in

Indonesia after the Soeharto era, when politically connected firms enjoyed favourable

benefits such as exclusive import licences, bail-outs and favourable financings.

The study used a mixed method approach: interviews with 34 bankers, analysts, fund

managers, academics, lawyers and business owners on their perception regarding the

need for political connection for business to be competitive in Indonesia, and a

regression analysis on panel data of listed non-financial companies in the Indonesia

Stock Exchange (IDX).

To define politically connected firms, this study used a measure whether a firm has any

member of the board of directors or the board of commissioners a politically exposed

person (PEP) or not. As measures of firm performance, return on assets (ROA) was

used for accounting-based firm performance and Tobin’s Q and market-adjusted returns

were used for market-based firm performance.

The findings from the interviews indicated that political connections were still needed

in the post-Soeharto era for ‘political protection’, as well as for access to information

and to regulators. The findings from examining the financial performance of the listed

companies in the IDX have corroborated the findings from the interviews. More than

one-third (36%) of Indonesian listed companies had political connectedness: 91%. The

concentration of politically connected firms was in the agricultural, mining,

property/real estate and miscellaneous industries (e.g., auto and auto parts). Not only

were they prevalent, the politically connected firms were some of the largest in the

country, where the mean and median value were higher in terms of market

capitalisation, total assets, total revenue and net profits.

The degree of political connection depended on the industry, the scale of the business

and the stage of the business. The dispersion of power structures necessitated businesses

to obtain wider political connections, especially in more regulated industries such as

ii

mining, oil and gas, plantations and property/real estate. However, the perception of the

interviewees was that political connection was just one of the factors required for

success; the key factor for a company’s success is its management. The results of the

regression showed that political connection had significant effects on market-based firm

performance, but not accounting-based firm performance. The effects on Tobin’s Q

were significant and positive, while the effects on returns were significant and negative.

Various robustness tests were conducted, such as including the top 40 business groups

in the definition of PEP, the addition of industry dummies, and matched pair tests on the

means of ROA and the change in ROA. Robustness tests confirmed Tobin’s Q

maintained significant and positive effects, with no difference in the means of ROA or

the change in ROA using a matched pair tests. The consumer industry had a positive

significant effect on Tobin’s Q. The number of the PEP board members did not have

any effect on ROA or market-adjusted returns, except on Tobin’s Q; however, the

number of PEP board members had significant and positive effects on the ROA within

the sample of PEP companies that experienced changes in their boards.

The findings of a relationship between political connection and market-based firm

performance have corroborated previous findings. This study has contributed to the

research on political connection, firm performance, institutions and how business is

conducted in emerging markets.

iii

Contents

Abstract ........................................................................................................................ i

Contents .................................................................................................................... iii

List of Figures ............................................................................................................ vi

List of Tables ............................................................................................................ vii

List of Abbreviations ............................................................................................. viii

Declaration of Originality.......................................................................................... x

Acknowledgements .................................................................................................... xi

Chapter 1: Research Rationale ................................................................................. 1 1.1 Introduction ........................................................................................................ 1 1.2 Research Background ......................................................................................... 1 1.3 Research Purpose and Key Questions ................................................................ 3 1.4 Research Significance ........................................................................................ 3 1.5 Research Scope .................................................................................................. 4 1.6 Thesis Structure .................................................................................................. 4

Chapter 2: Background & Literature Review ........................................................ 5 2.1 Introduction ........................................................................................................ 5 2.2 Overview of the Indonesian Economy ............................................................... 6

2.2.1 Recent Developments ................................................................................. 6 2.2.2 Capital Market Development ...................................................................... 7 2.2.3 Business Landscape .................................................................................... 8

2.3 Overview of Indonesia’s Political System ....................................................... 12 2.3.1 Recent Developments ............................................................................... 12 2.3.2 Brief History of the Political System ........................................................ 14

2.3.2.1 The Soekarno Era ............................................................................... 14 2.3.2.2 The Soeharto Era ............................................................................... 15 2.3.2.3 The Reformation Era .......................................................................... 18

2.4 Politics and Business in Indonesia ................................................................... 20 2.4.1 Introduction ............................................................................................... 20 2.4.2 The State and Rent-Seeking ...................................................................... 21 2.4.3 Oligarchy ................................................................................................... 22 2.4.4 Culture ....................................................................................................... 23 2.4.5 Government Intervention .......................................................................... 26 2.4.6 Case Study: The Salim Group ................................................................... 30

2.5 The Theoretical Foundations of Earlier Research ............................................ 32 2.5.1 Determinants of Firm Performance ........................................................... 32 2.5.2 Institutional Voids ..................................................................................... 33 2.5.3 The Effects of Having Political Connections on Firm Performance......... 35

Chapter 3: Perceptions of Business and Politics in Indonesia ............................. 40 3.1 Introduction ...................................................................................................... 40 3.2 Research Design ............................................................................................... 41

3.2.1 Rationale for Interview Method ................................................................ 41 3.2.2 Selection of Interview Participants ........................................................... 41 3.2.3 Data Analysis ............................................................................................ 42

iv

3.3 Findings ............................................................................................................ 42 3.3.1 Interviewee Characteristics ....................................................................... 42 3.3.2 Data Analysis—Manual Coding ............................................................... 45

3.3.2.1 What Factors are Important to Compete Effectively in Indonesia? .. 45 3.3.2.2 Why the Need for Political Connection? ............................................ 51 3.3.2.3 Need for Political Connection During and After the Suharto Era .... 53 3.3.2.4 Variation in Political Connection by Sectors of Industry .................. 55 3.3.2.5 Mechanism of Political Connection ................................................... 58

3.3.3 Data Analysis Using Leximancer ............................................................. 62 3.4 Summary .......................................................................................................... 65

3.4.1 Interviewees’ Characteristics .................................................................... 65 3.4.2 Does Political Connection Matter? ........................................................... 66 3.4.3 Why the Need for Political Connection? .................................................. 67 3.4.4 Conditions During and After the Soeharto Era ......................................... 67 3.4.5 Variation of Political Connection by Sectors of Industry ......................... 67 3.4.6 Mechanisms of Political Connection ........................................................ 68 3.4.7 Summary Data Analysis Using Leximancer ............................................. 68

3.5 Discussion and Implications ............................................................................ 69

Chapter 4: Political Connection and Firm Performance in Indonesia ............... 72 4.1 Introduction ...................................................................................................... 72 4.2 Background and Hypotheses ............................................................................ 72

4.2.1 Research Background ............................................................................... 72 4.2.2 Research Hypotheses ................................................................................ 73

4.3 Research Design ............................................................................................... 75 4.3.1 Sample and Time Period ........................................................................... 75 4.3.2 Research Data ........................................................................................... 75

4.3.2.1 Data Collection Method ..................................................................... 75 4.3.2.2 Independent Variables ....................................................................... 76

4.3.3 Research Models ....................................................................................... 77 4.3.3.1 Dependent Variables .......................................................................... 77 4.3.3.2 Control Variables ............................................................................... 78 4.3.3.3 Ordinary Least Squares ..................................................................... 78 4.3.3.4 Research Model.................................................................................. 79

4.4 Results .............................................................................................................. 80 4.4.1 Overview of Sample.................................................................................. 80 4.4.2 Descriptive Statistics and Correlation ....................................................... 81 4.4.3 Comparison of PEP and Non-PEP Companies ......................................... 82 4.4.4 Regression Model Results ......................................................................... 88

4.5 Robustness Tests .............................................................................................. 92 4.5.1 Robustness Test 1 ..................................................................................... 92 4.5.2 Robustness Test 2 ..................................................................................... 95 4.5.3 Robustness Test 3 ..................................................................................... 97

4.6 Discussion ........................................................................................................ 97

Chapter 5: Conclusions ......................................................................................... 100 5.1 Introduction .................................................................................................... 100 5.2 Theoretical and Empirical Findings and Contributions ................................. 100 Research Limitations ........................................................................................... 104 5.3 104 5.4 Implication of Findings .................................................................................. 106

v

References ............................................................................................................... 107

Appendix A ............................................................................................................. 120

Appendix B ............................................................................................................. 123

Appendix C ............................................................................................................. 125

vi

List of Figures

Figure 3.1: Key Success Factors Viewed as Necessary for Competitiveness ........... 49

Figure 3.2: Perceptions of Variation in Political Connectedness by Industry Sector 58

Figure 3.3: Concept Map of Political Connectedness ................................................ 64

vii

List of Tables

Table 2.1: Top 80 Business Groups in Indonesia ........................................................ 9

Table 3.1: Characteristics of Interviewees Based on Their Professions .................... 43

Table 3.2: Characteristics of Interviewees Based on Their Positions ........................ 43

Table 3.3: The Cross-Tabulation of Interviewees’ Jobs and Education .................... 44

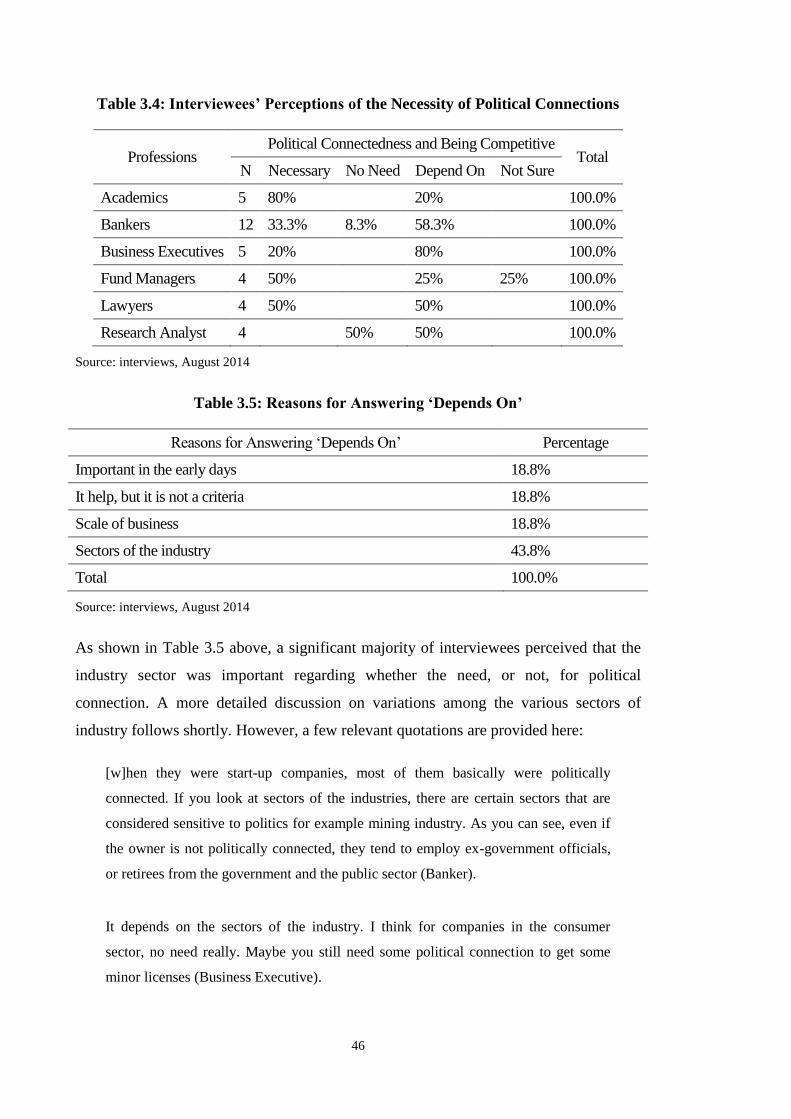

Table 3.4: Interviewees’ Perceptions of the Necessity of Political Connections ....... 46

Table 3.5: Reasons for Answering ‘Depends On’ ..................................................... 46

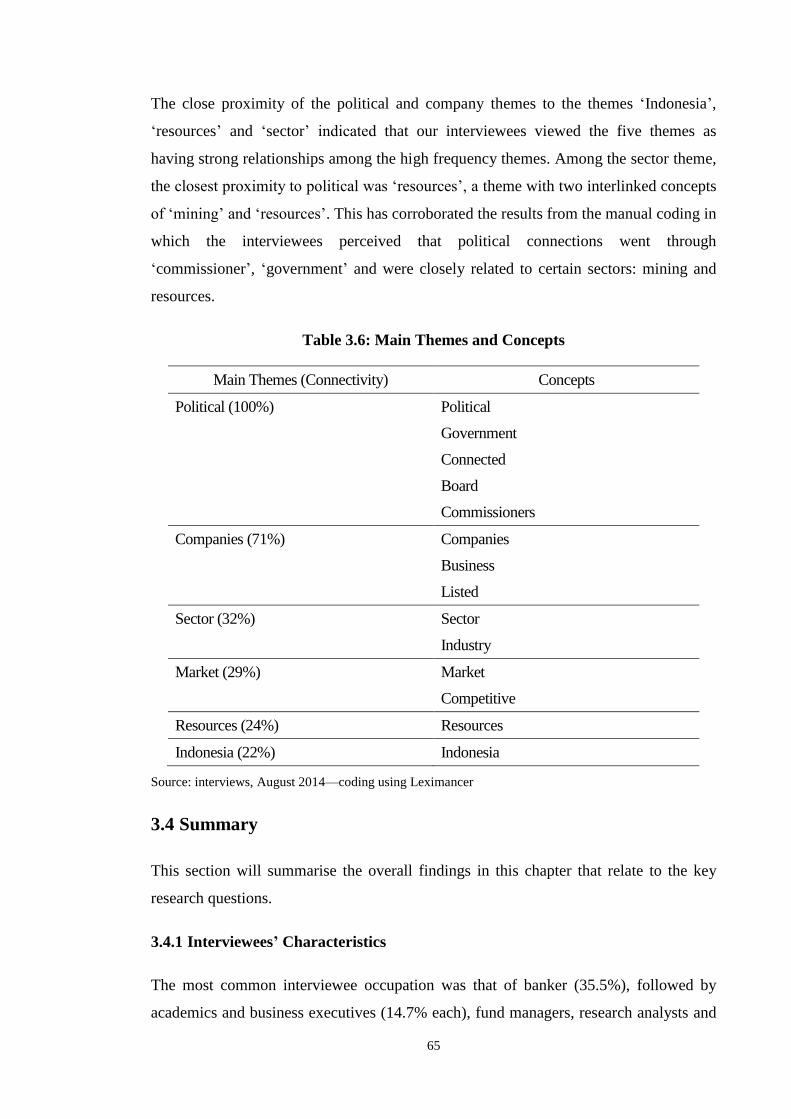

Table 3.6: Main Themes and Concepts ...................................................................... 65

Table 4.1: Number of Companies with PEP and the Number of PEPs ..................... 81

Table 4.2: Descriptive Statistics of Variables ............................................................ 81

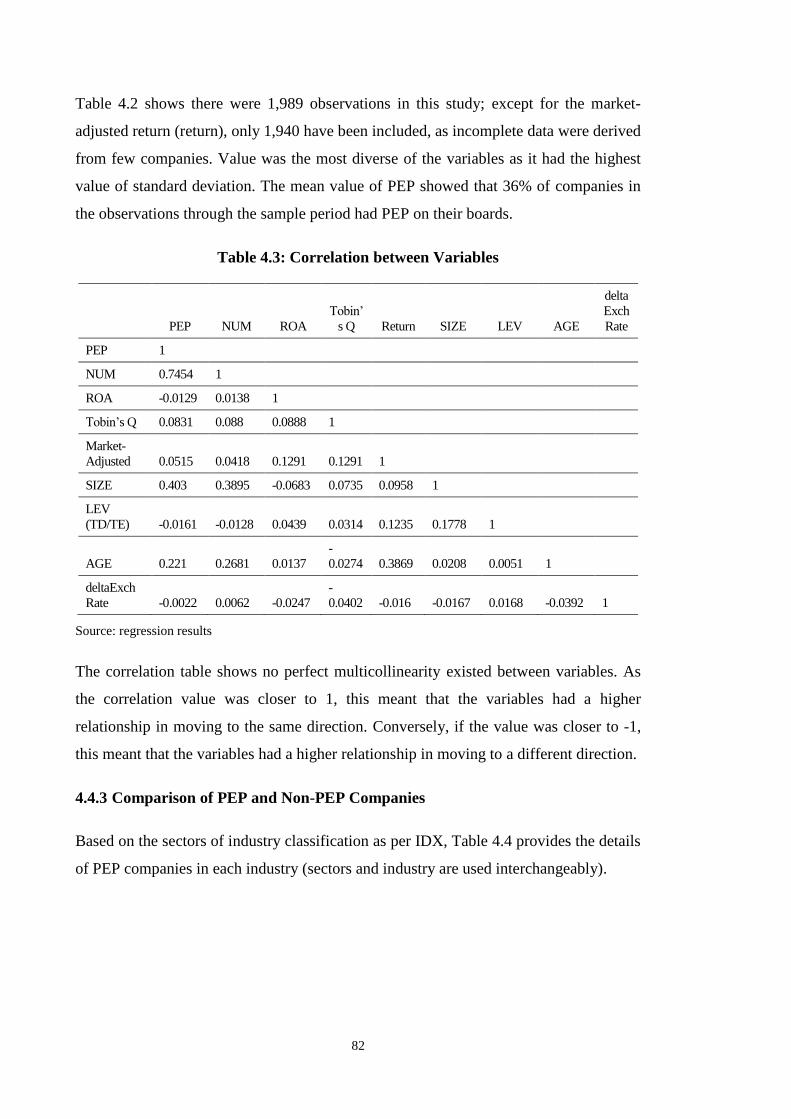

Table 4.3: Correlation between Variables .................................................................. 82

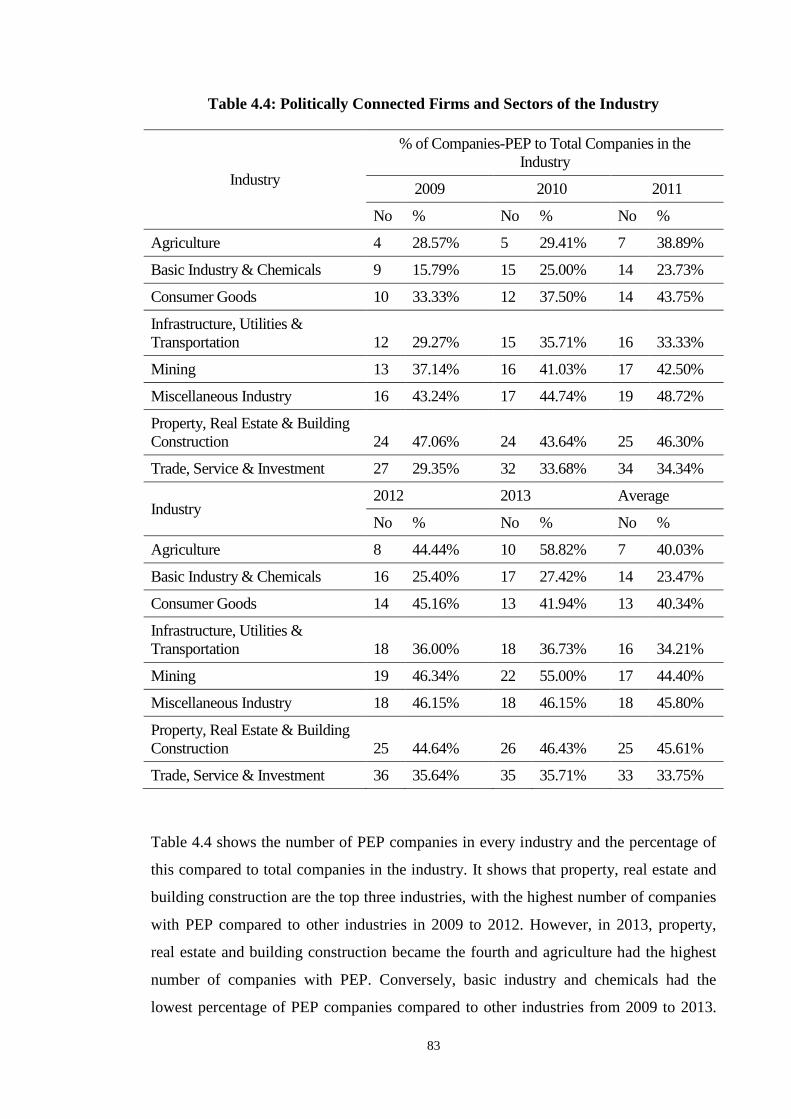

Table 4.4: Politically Connected Firms and Sectors of the Industry.......................... 83

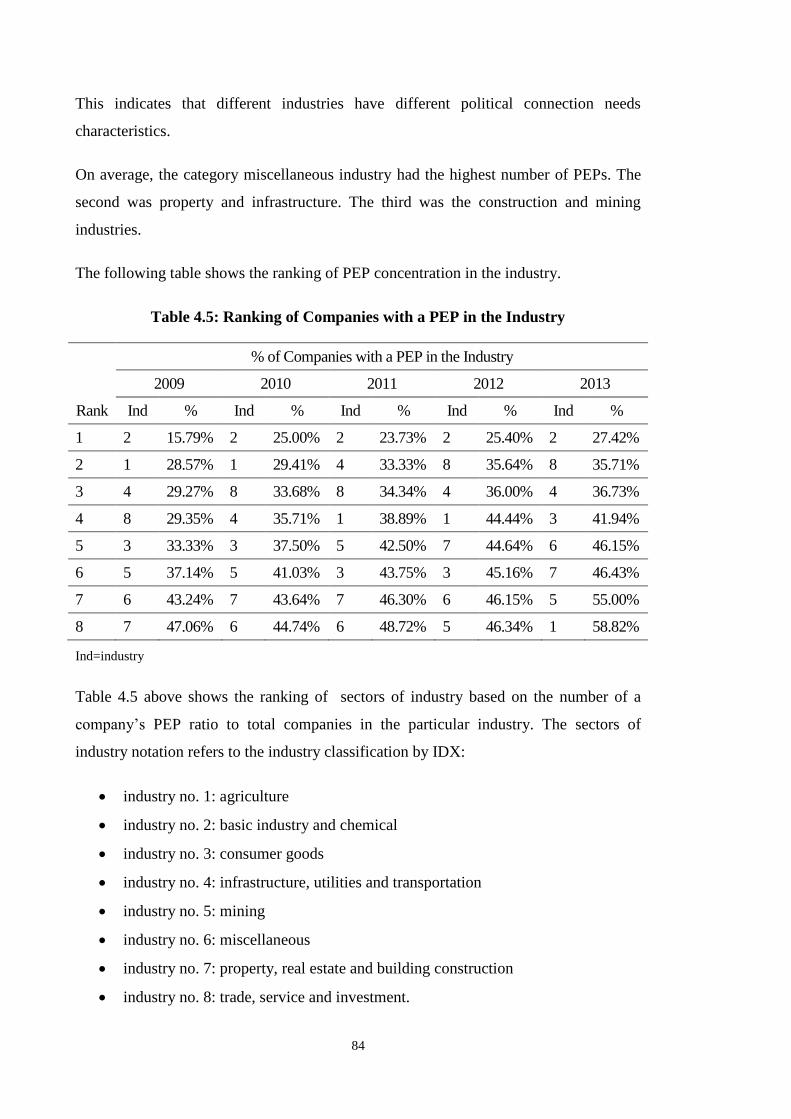

Table 4.5: Ranking of Companies with a PEP in the Industry................................... 84

Table 4.6: Mean Value of Variables for PEP Companies and Non-PEP Companies 85

Table 4.7: Regression Results .................................................................................... 88

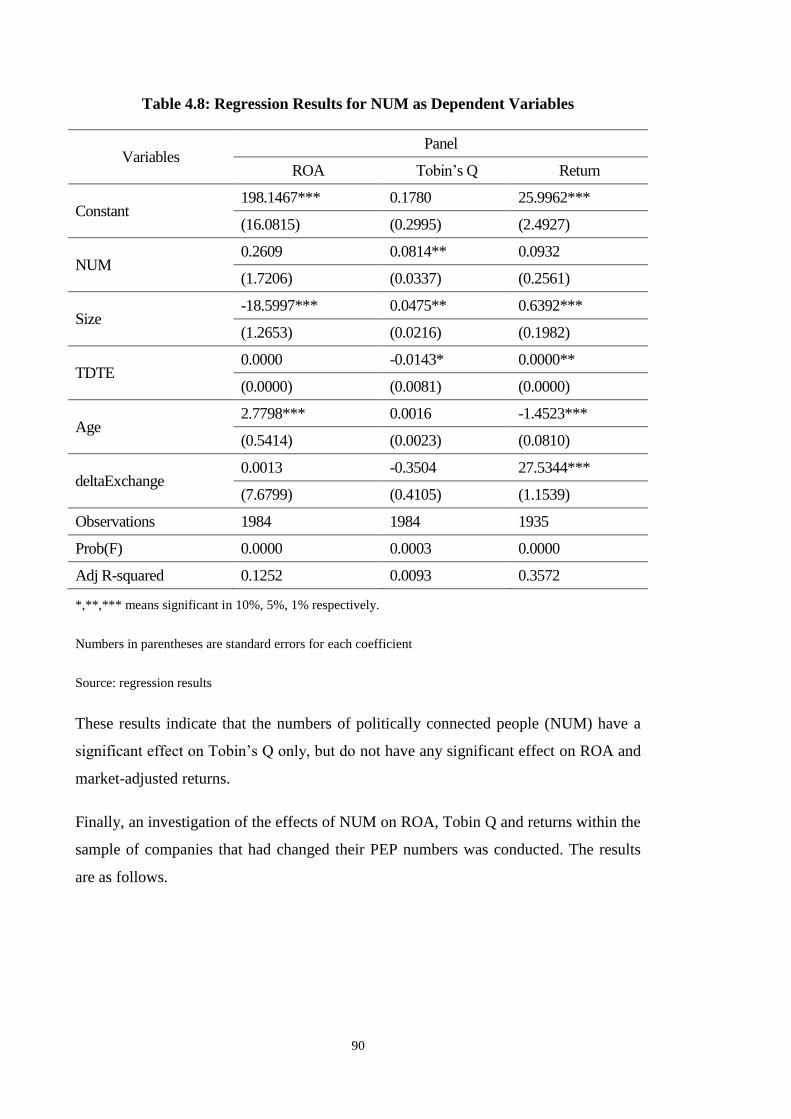

Table 4.8: Regression Results for NUM as Dependent Variables ............................. 90

Table 4.9: Regression Results for Changing NUM ................................................... 91

Table 4.10: Regression Results with Top 40 Business Groups ................................. 93

Table 4.11: T-test of ROA between All Companies and Top 40 Business Group .... 94

Table 4.12: Regression Results with Industry Dummies ........................................... 95

Table 4.13: T-test Result for ROA of Matched Pair Companies ............................... 97

viii

List of Abbreviations

AFC Asian Financial Crisis

AMDAL Analisa Mengenai Dampak Lingkungan

APINDO Asosiasi Pengusaha Indonesia

ASEAN Association of South East Asian Nations

BAPPENAS Badan Perencanaan Nasional

BCA Bank of Central Asia

BI Bank Indonesia

BODCOM Board Composition

BPOM Badan Pengawas Obat & Makanan

BUMN Badan Usaha Milik Negara

CONTR Concentrated Ownership

EPS Earnings Per Share

FDI Foreign Direct Investment

Golkar Golongan Karya

GFC Global Financial Crisis

IBRA Indonesian Banking Restructuring Agency

ICBP Indofood Consumer Brand Products

IDR Indonesian Rupiah

IMF International Monetary Fund

JCRA Japan Credit Rating Agency

KADIN Kamar Dagang & Industri Indonesia

KIP Kartu Indonesia Pintar

KIS Kartu Indonesia Sehat

KKP Kartu Keluarga Sejahtera

KPK Komisi Pemberantasan Korupsi

KPU Komisi Pemilihan Umum

KSO Kerja Sama Operasi

MAC Middle Class and Affluent Consumers

MNC Media Nusantara Citra

MOF Ministry of Finance

MP Member of Parliament

MPR Majelis Permusyawaratan Rakyat

NPL Non-Performing Loans

NUM Number of PEPs

OJK Otoritas Jasa Keuangan

OLS Ordinary Least Squares

ix

PAN Partai Amanat Nasional

PDIP Partai Demokrasi Indonesia Perjuangan

PEP Politically Exposed Person/s

PERDA Peraturan Daerah

PKI Partai Komunis Indonesia

PSC Production sharing contract

R&D Research & Development

ROA Return on Assets

ROE Returns of Equity

ROS Return on Sales

RUP Rencana Urgensi Perekonomian

SBY Susilo Bambang Yudhoyono

SOE State-Owned Enterprise

TI Transparency International

UBO Ultimate Beneficiary Owners

US United States of America

USD US Dollar

x

Declaration of Originality

I certify that this thesis does not incorporate without acknowledgement any material

previously submitted for a degree or diploma in any university; and that to the best of

my knowledge and belief it does not contain any material previously published or

written by another person except where due reference is made in the text.

Signed: On: 4 July 2016

xi

Acknowledgements

When I started out on the journey of the DBA programme, I was warned that the

journey of a Doctorate programme would be a long and lonely journey. It was indeed

so. However, the journey was very rewarding. Without the help and support of

countless individuals whom I cannot mention each and everyone of them, I would not

be able to complete this journey.

First and foremost, I would like to thank my mother - Khatijah and my late father -

Husin Ibrahim. Though my mother cannot even read and write and my father never

finished primary school, they instilled in me the importance of education in life and a

passion for a lifelong learning.

I would like to thank my wife - Rosalin Devi and my sons - Alif, Bing and Faridz. They

have been my constant supporters, inspirations, critics and encouragement even when I

had to take some time off my career to complete this journey.

I would like to thank Winthrop Professor Raymond da Silva Rosa and Associate

Professor Marvin Wee, my co-supervisors. Without their advice, guidance, and

patience, I would have been lost in the journey. Also my sincere thanks to Winthrop

Professor Geoffrey Soutar, DBA Programme Director and all staff at the UWA

Business School Research Office.

My thanks and sincere gratitude to the 34 interviewees who took time and efforts to

share their views despite their busy schedules. And to all friends, family, colleagues that

have supported me in this process, I am forever indebted for the exchanges of ideas,

words of encouragement, and any help extended to me.

Last, I would also like to thank and acknowledge the editing works by Elite Editing

(Australia). All editorial works were restricted to Standards D and E of the Australian

Standards for Editing Practice.

1

Chapter 1: Research Rationale

1.1 Introduction

The background to this research provides the rationale for and description of why I am

interested in examining the relationship between business, politics and firm (or

company)1 performance. Further, I will describe the research purpose and key questions.

I will then explain the thesis structure and contents.

1.2 Research Background

I worked in Indonesia for over 20 years. During the first four years, I worked in the

corporate world; for the last 16 of those years I worked as a senior banker. I observed

the phenomenon of a close relationship between business and politics both during and

after the post-Soeharto era. This prompted my idea to study the correlation between

business, politics and company performance in Indonesia.

In an emerging market such as that of Indonesia, the lack of institutional settings—a

situation called ‘institutional voids’—has been nominated as a reason for the emergence

of business groups concentrated in the hands of a few families (Khanna & Yafeh 2007;

Sato 2004). The majority of big family firms in Indonesia are owned by the descendants

of Chinese business people. They did not have the option of a political career, or joining

the bureaucracy or military during Soeharto’s time; hence, some perceive this is why the

Indonesian business world has been dominated by the Chinese (Muhaimin 1991;

Yoshihara 1988). However, as discussed in the literature review, the Chinese have

participated in business since the Dutch colonial period. Chinese cultural traits have

been perceived as the reason for this phenomenon (Yoshihara 1988). The Chinese have

been ‘subjugated’ and ‘co-opted’ by the political powers in a neo-patrimonialist regime

during Soeharto’s time (Chua 2008).

In the post-Soeharto era, Chinese dominance in business has not abated, although some

business groups have suffered major losses or have even disappeared completely in the

aftermath of the 1988 Asian financial crisis (AFC) (Chua 2008). Chua (2008) has

1 The terms company and firm are used interchangeably throughout this thesis.

2

argued that they are now more assertive and have better leverage due to their

indispensable capital. Since regional autonomy was established in 2001, power has been

dispersed regionally. In a democratic Indonesia, elections at the regional and central

levels require a huge amount of funding. Business people have become the source of

capital (Chua 2008).

Has the existence of politically connected firms translated into better firm performance

for these companies in Indonesia recently? This thesis will attempt to provide answers

through empirical evidence regarding the potential correlation between politics and

businesses in recent times (2009–2013); specifically, whether ‘politically connected’

firms perform better or not than other firms.

For this study, politically connected firms are defined as firms that have a Politically

Exposed Person (PEP) in the board of directors or commissioners. A more detailed

description of politically connected firms and PEP is available on page 78 (section

4.3.2.2 Chapter 4).

First, interviews with senior professionals, business owners, lawyers and academics

were conducted to obtain perceptions of business and politics in Indonesia’s post-

Soeharto era. These interviews will provide the background and further insight into the

quantitative analysis. Quantitative analysis will apply ordinary least square (OLS)

regression to the panel data of listed companies’ performance and their political

connectedness in subsequent chapters.

Business focuses on profit maximisation and firms tend to use all means to seize

opportunities and mitigate risk, including using political connections. This phenomenon

has been observed in Indonesia in previous studies such as those described in Chapter 2

(‘Literature Review’). Politics and business have been intimately intertwined to the

point that some of the largest business groups in Indonesia were born and flourished

under ‘political protection’ during Soeharto’s regime.

Since 1998, democracy has replaced Soeharto’s authoritarian regime. Have conditions

changed post-Soeharto? This thesis will explore the need for political connections to

compete in business in the post-Soeharto era, and whether political connections have

added value to Indonesian listed companies in recent times.

3

1.3 Research Purpose and Key Questions

This research examines the existence of political connections when conducting business

in Indonesia. An attempt was made to investigate the necessity of political connections

in doing business: how a different political era could result in different political

connection mechanisms and whether different company characteristics would affect

performance. To develop this research, the following questions were analysed and

discussed:

1. Are political connections necessary to be competitive in Indonesia? If so, why?

2. Has the situation become better or worse post-Soeharto?

3. Do political connections vary across industry sectors? How?

4. What mechanisms for political connections are used by firms?

5. Do political connections affect a firm’s performance in Indonesia?

6. Does the number of politically exposed persons (PEPs) on a board affect a

firm’s performance in Indonesia?

This research has used a mixed methods approach to answer the key research questions.

A qualitative method was used for interviews with 34 senior executives, business

owners, lawyers and academics in Indonesia regarding their perceptions of key research

questions 1 to 4; a quantitative method using OLS regression analysis on the

performance of listed companies that are politically connected or not in Indonesia was

conducted for research questions 5 and 6.

1.4 Research Significance

Previous studies have examined the correlation between politics and business in

Indonesia from the perspective of sociology, history or political economics and have

largely focused on the Soeharto era. This study has also examined the correlation

between politics and business in Indonesia, but has focused on business and

management perspectives in the post-Soeharto era. In addition, this study has examined

the correlation between political connection and a firm’s performance using the OLS

regression method on panel data. Moreover, using both qualitative and quantitative

approaches will provide enriched findings.

4

1.5 Research Scope

This research has used financial data from the audited financial statements of listed

companies in the Indonesian Stock Exchange (IDX) from 2009 to 2013. The

measurement of political connections has been based on previous studies (Faccio 2006)

that have examined whether board members, directors or commissioners are or have

been senior officials in the government, military and judiciary. Moreover, in-depth

interviews were conducted with 34 senior executives, business owners, lawyers and

academics. This will provide some important data to support the whole range of

arguments presented in this research.

1.6 Thesis Structure

The thesis will begin by discussing the institutional settings and providing a literature

review in Chapter 2. This chapter will review Indonesia’s recent economy and its

political system.

Chapter 3 describes the perceptions of respondents regarding politics and business in

Indonesia. It begins with a brief outline of the previous studies, followed by a main

section analysing the interview data using manual coding. To enrich this manual coding,

the analysis has used Leximancer software to code the interview results. Leximancer

coding produces a concept map. This map will indicate the closeness of the various

themes emerging from the Leximancer coding. These sections are constructed based on

the key research questions. A short summary is followed by discussion and

implications.

Chapter 4 describes the analysis of the key research questions using a quantitative

approach. Panel data regression was employed to answer whether politically connected

firms have better accounting performance using the measure return of assets (ROA),

and market-based performance using Tobin’s Q and market-adjusted returns. The

results and their implications are described at the close of Chapter 4.

Chapter 5 consists of a conclusion and some directions for future research. This chapter

will finish with a discussion on the implications of the findings for managers and policy

makers.

5

Chapter 2: Background & Literature Review

2.1 Introduction

Since its independence in 1945, Indonesia has experienced different political regimes.

Different regimes have resulted in different governmental dynamics, including policies,

priorities and expenditure, depending on the respective needs and allocations of the

regime’s period (Permana & Wika 2014).

During the Soeharto era, business and politics were intertwined intensely (Borsuk &

Chng 2014). Power was concentrated in one person—President Soeharto. In post-

Soeharto authoritarian regimes, reformation resulted in a democracy with more

transparency, better supervisory systems and an open trade regime (Basri 2013).

However, the intertwining of business and politics has not subsided in the post-Soeharto

era (Chua 2008).

Indonesia has the fourth largest population in the world, with a growing middle class

and increasing numbers of middle class and affluent consumers (MAC). Rastogi et al.

(2013) from Boston Consulting Group have predicted that Indonesia’s MAC population

could double in size, reaching 141 million people by 2020. Oberman et al. (2012) from

McKinsey have estimated that Indonesia could become the seventh largest economy in

the world in 2030; in terms of gross domestic product (GDP), Indonesia was ranked

sixteenth in the world in 2012.

I will start the literature review by reviewing institutional settings. In Section 2.2, I will

review the Indonesian economy, focusing on the business landscape concentrated in the

hands of a few families. In Section 2.3, I will review Indonesia’s political systems

during the different regimes: the Soekarno, Soeharto and post-Soeharto eras. The links

between politics and business in Indonesia are outlined in Section 2.4. I will focus on

oligarchy, the state and rent-seeking, and culture and government intervention as

possible explanations for this intertwining of politics and business. I will discuss a brief

case study of the Salim Group. Finally, I will review the earlier research on

‘institutional voids’, political connectedness and firm performance, and the potential

mechanisms to explain why political connectedness can add value or be detrimental to a

firm’s performance, in Section 2.5.

6

2.2 Overview of the Indonesian Economy

2.2.1 Recent Developments

Indonesia is a member of the G20 countries and the Association of South East Asian

Nations (ASEAN). Indonesia was ranked third among the G20 countries—after China

and India—for its GDP growth of 5.36% (year-on-year) as of April 2014 (International

Monetary Fund [IMF] 2014). In the past four years (2010-2013), Indonesia has

sustained a GDP growth of 4 to 6%.

Indonesia has the largest population of the ASEAN countries, numbering 253.6 million.

However, Indonesia’s GDP per capita of USD 3,420 ranks fifth after Singapore, Brunei

Darussalam, Malaysia and Thailand (IMF 2014). Indonesia’s biggest sector with respect

to its GDP is the manufacturing industry (21.02%) followed by trade, hotel, and

restaurants (16.52%), agriculture, farming (13.38%), and construction (12.67%) (Biro

Pusat Statistik [BPS] 2014).

Indonesia was affected less severely by the 2008 GFC compared to other countries; this

is because Indonesia had a strong base of domestic consumption, which accounted for

56.51% of GDP in 2010. This remained stable until 2014 (55.71% of GDP), and

Indonesia’s share of exports as part of its GDP was relatively small at around 17% of

GDP (Tambunan 2010; Wie 2012).

Exports and imports amounted to USD 13.5 billion and USD 13.1 billion respectively

for November 2014 (BPS 2014). The most significant contributor to exports is the

manufacturing industry, with 68.15% of the total export value (Bank Indonesia [BI]

2015). The manufacturing industry also received the largest portion of foreign direct

investment (FDI) in the third quarter of 2014 (Q3-2014), 32.67% of the total FDI in Q3-

2014 (BI 2015). The next largest recipients were agriculture and forestry (15.38%),

mining and quarrying (12.63%), transportation, storage and communication (12.43%).

FDI accounted for 68% of total investment in Q1-2014, while domestic direct

investment was only 32% of the total investment (Badan Koordinasi Penanaman Modal

[BKPM] 2014).

Actual full year inflation was 4%, 8.38% and 8.36% for 2012, 2013 and 2014,

respectively. BI’s rate was maintained at 7.5% as of February 2015. The BI rate, which

7

is a policy rate, has been maintained in the range of 7.50 to 7.75% since December

2013. This reflects BI’s stance to maintain a loose monetary policy.

Regarding the exchange rate policy, Indonesia has adopted a flexible exchange rate. The

exchange rate’s assumption for the 2014 government budget was around IDR

(Indonesian rupiah) 12,000/USD; however, as of 24 August 2015, the rupiah had

surpassed IDR 13,800/USD.

Indonesia has an increasing absolute value of debt from year to year amounting to IDR

2,576 trillion for 2014, of which the higher portion comes from the private sector

(Ministry of Finance [MOF] 2015). For the government debt, there is an upper limit of

3% of budget deficit as per Act No. 17/2003 on Public Finance. The reserve as of

September 2014 was relatively high (historically) at USD 111.16 billion. However, it

was the lowest compared to Japan, China, India, Malaysia, Thailand and Singapore; that

is only 2.86% from China’s reserves (BI (2015). As for the Indonesian rating, in 2011,

Standard & Poors (S&P) – a rating agency - increased Indonesia’s rating from BB to

BB+2. Other rating agencies, such as Japan Credit Rating Agency (JCRA), Fitch and

Moody’s have classified Indonesia into an investment grade rating category (i.e., BBB

[MOF 2015]).

Eradicating corruption has been one of the main agendas of President Susilo Bambang

Yudhoyono (SBY) and President Joko Widodo (Jokowi) (Dodd 2014). However,

perceptions of a high level of corruption still exist; for example in the Transparency

International (TI) index, Indonesia ranked 107 out of 175 countries in 2014 on the TI

Corruption Perception Index (TI 2014). Nevertheless, this is an improvement from the

ranking of 133 out of 145 countries in 2004, and being classified as the world’s third

most corrupt country in 2001.

2.2.2 Capital Market Development

Indonesia’s stock exchange was established in Jakarta in 1912 by the Dutch East Indies

government (Jakarta was then known as Batavia). It was closed several times during

both World War One (WWI) and Two (WWII). In 1977, President Soeharto re-activated

2 S&P use a rating scale from the highest to the lowest as follows: AAA, AA, A, BBB, BB, B,

CCC, CC, C and D for default. The ratings maybe noted with ‘+’ or “-‘ to show relative

standing within the categories.

8

the stock exchange. It was supervised by the Capital Market Supervisory Agency

(Badan Pengawas Pasar Modal). In 1989, the Surabaya Stock Exchange began to

operate, merging with the Jakarta Stock Exchange in 2007 to become the IDX. As of

February 2015, there were 506 companies listed in the market; the value of Jakarta

Composite Index was 5,223.29 on 7 April 2015 which was a historic high (Otoritas

Jasa Keuangan [OJK] 2015).

In the first week of 2015, Indonesian market capitalisation accounted for USD 414.26

billion, with a transaction volume of 42.70 billion shares (OJK 2015). The highest

market capitalisation was from the financial sector (19.54%), followed by the consumer

goods sector (19.54%), the infrastructure sector (14.10%) and the trade sector (11.91%).

The lowest value of market capitalisation occurred in the agricultural sector, with

3.10%.

The value of bonds outstanding was IDR 1,436.48 trillion, of which 84.23% of the total

value consisted of government bonds. For mutual funds, the net asset under

management was IDR 242.25 trillion in January 2015 (or approximately 5% of the total

assets of the banking sector). The highest valued mutual fund was the shares type, with

a value of IDR 103.31 trillion. This was followed by protected mutual funds (IDR 43.01

trillion), fixed income mutual funds (IDR 36.05 trillion), with lowest being syariah-

index mutual funds (IDR 0.14 trillion).

2.2.3 Business Landscape

In Indonesia, concentrated ownership of the largest companies in the hands of a few

families has been observed by Claessens, Djankov, & Klingebiel (1999). Claessens,

Djankov & Klingebiel (1999) note that the top 15 families in Indonesia owned 67.3% of

corporations prior to the 1997 AFC—a much higher figure compared to Thailand and

Malaysia (between 30–40%) and Korea (between 15–25%). This figure would be 82.5%

if state ownership were included. Djiwandono (2005) attributes this concentration to the

high use of non-performing loans (NPL) and the violation of legal lending limits during

the AFC. He further states that the situation is linked to corruption resulting from

institutional weaknesses such as ineffective corporate governance, legal and judiciary

systems.

9

This finding has been corroborated by Khanna and Yafeh (2007) and Sato (2004).

Khanna and Yafeh (2007) state that Indonesia has the largest fraction of firms classified

as a business group (two-thirds) among the various emerging countries for which data

were available for the period 1993 to 1995.3 Sato (2004) corroborates Khanna and

Yafeh (2007) and states that in 1996, of the top 100 listed companies, 58 were group-

affiliated, accounting for 70% of aggregate sales and 73% of aggregate assets. By 2000,

the number of group-affiliated companies in the top 100 listed companies had decreased

to 44, their shares had fallen to 56% and their shares in assets had fallen to 36% (Sato

2004). However, they have remained relatively significant up to the present date, as

indicated in the following table.

Table 2.1: Top 80 Business Groups in Indonesia

Rank Groups

Rev

($b) Rank Groups

Rev

($b)

1. Salim Group 13.2 41. Berca Group 0.85

2. Sinarmas Group 8.9 42.

Kompas Gramedia

Group 0.85

3. Djarum Group 8.5 43. Harita Group 0.83

4. Lippo Group 6 44. Sungai Budi Group 0.82

5. Gudang Garam Group 5 45. Sugar Group 0.78

6. Royal Golden Eagle 4.2 46. ABM Investama Group 0.75

7. Bakrie Group 3.5 47. Medco Energi 0.75

8. Adaro Energy 3.2 48. Musim Mas 0.7

9. Alfamart Group 3.1 49. Tempo Scan 0.67

10. CT Corpora 3.1 50. Harum Energi 0.65

11. Tiphone Mobile 3 51. Ramayana Lestari 0.65

12. Wings Group 2.4 52. Rekso Group 0.6

13 Triputra Group 2.3 53. Mayapada Group 0.6

14. Barito Pacific 2.3 54. Mulia Group 0.6

15. Charoen Phokpand 2.2 55. Sritex Group 0.59

16. AKR Corporindo 2.1 56. First Resources Group 0.57

17. Gadjah Tunggal Group 1.9 57. Modern Group 0.57

3 Business groups are defined as a set of legally-separate firms with stable relationship in multiple

strategically-unrelated activities and under common ownership and control by Cuervo-Cazurra (2006).

10

Rank Groups

Rev

($b) Rank Groups

Rev

($b)

18. Japfa Comfeed 1.9 58. Hadji Kalla Group 0.56

19. Kalbe Farma 1.84 59. Bank Bukopin 0.55

20. Gobel Group 1.8 60. Garuda Food 0.52

21. Panin Group 1.53 61. Rodamas group 0.52

22. Indorama Synthetics 1.52 62. Emtek Group 0.5

23. Argo Manunggal 1.5 63. Santini Group 0.5

24. Mayora Indah 1.2 64. Supreme Cable 0.49

25. ABC Group 1.2 65. Toba Bara Group 0.48

26. Wilmar Group 1.1 66. Samudera Indonesia 0.48

27. Indika Energy Group 1.1 67. Fajar Paper 0.45

28. Bosowa Group 1 68. Lautan Luas 0.42

29. TNT Group 1 69. Agung Podomoro 0.41

30. MNC Group 1 70. Summarecon 0.41

31. Tunas Ridean 0.99 71. Sriwijaya Air 0.42

32. Lion Air Group 0.99 72. Maspion Group 0.36

33. Arsari Group 0.99 73. Kawan Lama (ACE) 0.35

34. Persada Capital Group 0.98 74. Pan Brothers 0.34

35. Trikomsel Group 0.93 75. Fast Food Indonesia 0.32

36. FKS Multi Agro 0.9 76. OSO Group 0.3

37. Gunung Sewu Group 0.89 77. Rajawali Group 0.28

38. Sintesa Group 0.88 78. Artha Graha Group 0.28

39 Darmex Agro Group 0.86 79. Sumi Indo Kabel 0.27

40. Ciputra Group 0.86 80. Total Bangun Persada 0.16

The table above is modified from the 100 top groups published by the Globe Asia

magazine August 2015 edition, using revenue in USD billion for 2015. I have excluded

foreign-owned business groups such as Astra/Jardine, Sampoerna/Philip Morris,

Danamon/Temasek, CIMB Niaga/Khazanah and Indosat/Qatar Telecom, as the focus of

this study is on locally owned business groups.

The largest business group in Indonesia prior to the AFC was the Salim Group. The

Salim Group remains one of the largest groups today. According to Globe Asia, it

ranked second after Astra in the top 100 groups, with a combined revenue of USD13.2

billion as of August 2015. It is still ranked number one. The Astra Group has been

11

excluded, as it is owned by the Jardine C&C Group of Hong Kong (as seen in the above

table). This ranking may change over time as some of the business groups’ fortunes are

linked to the commodities cycle; nevertheless, these business groups represent some of

the largest and most prominent business groups in Indonesia.

The AFC formed a watershed period that brought the IMF to Indonesia, where it

implemented various measures of austerity that affected business groups. Through

IBRA (Indonesian Banking Restructuring Agency), many business groups de-

concentrated and focused on their core competencies (Basri & van der Eng 2005). Salim

Group chose to maintain their core businesses (i.e., food and beverage businesses

[Indofood and Bogasari]). They devolved their ownership of virtually every other

business to IBRA, including stakes in leading automotive, cement and coal companies

and the Bank of Central Asia (BCA). Sinarmas Group remained relatively intact during

the AFC, as did Lippo group. However, Sinarmas Group had to declare the largest

private sector debt default in 2001. Bakrie Group had owned businesses ranging from

steel pipe, plantation, real estate and financial services such as banks, securities and

insurance. They lost almost all their financial services companies. The other companies

remain part of the Bakrie Group, but are now much smaller relative to their thermal-coal

businesses acquired from BHP Billiton after the AFC. Some business groups did not

survive the AFC at all, such as the Dharmala and Nusamba/Bob Hasan groups.

Yuri Sato has studied various business groups in Indonesia, along with their origins and

strategies. Sato (1993) has examined Salim Group’s expansion and transformation

processes. This group is one of the largest business groups in Indonesia. Sato (1996) has

also examined the Astra Group, emphasising how they have developed their

management system, and are now considered the pioneer of management modernisation

in Indonesia. Sato (2004) has found that business group affiliation and borrowing

behaviour resulted in performance differences among companies. Group-affiliated

companies had higher leverage before the AFC and suffered heavily during this crisis.

Firms affiliated with established groups had higher indebtedness, but also higher returns

of equities (ROE) before the crisis and were likely to survive the crisis. In contrast,

firms affiliated with rapid-growth groups had the lowest profitability and suffered most

from the AFC.

12

Lukviawarman (2004) has studied the relationship between ownership structures,

monitoring and firm performance in Indonesia using the agency theory of contractual

relationship among various parties. He found that the existence of controlling

shareholders in the hands of a family was a source of corporate governance problems.

Using the same agency theory, Prabowo (2010) studied the composition of boards of

directors on firm performance in Indonesia. Independent leadership was found to have a

positive relationship with firm performance. Prabowo (2010) also found that

shareholding by controlling owners had negative associations with firm performance.

Corporate diversification has many causes. Claessens et al. (1999) have argued that

firms diversify to create internal factor markets that are most cost-effective in allocating

resources when compared to external markets. One stream of research views business

groups as responses to market failures and associated transaction costs (Leff 1978). This

has been supported by Khanna (1999, 2000). These researchers have argued that

business groups can serve as functional substitutes to fill the ‘institutional voids’ in

emerging economies. Khanna and Yafeh (2007) have argued that as groups arise for

different reasons and in different environments, their effect on social welfare is

unambiguous; groups may sometimes play a positive role by making up for

underdeveloped economic institutions (Khanna 1999, 2000). However, they can also be

detrimental for social welfare due to rent-seeking or monopoly power (Fisman 2001;

Mobarak & Purbasari 2005).

2.3 Overview of Indonesia’s Political System

2.3.1 Recent Developments

After President Soeharto stepped down in 1998, there was a significant improvement in

Indonesia’s democratic system including free elections and freedom of expressions in

the media.

In 2004, SBY and Jusuf Kalla were elected as president and vice president through

direct election. This was Indonesia’s first direct election of a president. In addition, the

military’s power was diminished: they no longer had seats in parliament and separation

between the police and military forces was established.

13

President SBY was again elected in the next presidential general election in 2009, with

Budiono as vice president. According to Marcus Mitzer (of the Lowy Institute in

Sydney, Australia), President SBY’s popularity resulted from several factors. These

include the distribution of massive cash programs for the poor and a strong perception

by Indonesian society that the national economic condition had improved compared to

the preceding year.

Notwithstanding SBY’s popularity, public support for him decreased during his second

term in office. This lack of support was indicated by his reduced approval rating: from

85% after his election to 66% by October 2010. This posed little problem for SBY, as

the constitution barred the president from entering a third round of elections. This

decline in popularity was due to the controversial Bank Century bail out, which ended

with the departure of the Minister of Finance, Sri Mulyani Indrawati. Some have argued

that Indrawati’s departure was beneficial for Aburizal Bakrie from Golkar (a key

coalition party of SBY’s Democratic Party), since this might have strengthened Bakrie’s

position for the 2014 presidential election (Vaughn 2011). However, as we will see

below, Bakrie did not make the final round of the 2014 presidential elections.

In 2014, Indonesia held a general election to elect legislative members, the president

and vice president. The legislative election was first held on April 2014; for this, the

party with largest number of supporters would propose the presidential and vice

presidential candidates for the election in July 2014. The result from the legislative

election was as follows: Partai Demokrasi Indonesia Perjuangan (PDIP) party was the

first winner with 23, 681, 471 supporters, Golkar party held second place with 18, 432,

312 supporters and Gerindra party had 14, 760, 371 supporters (Komisi Pemilihan

Umum [KPU] 2014).

The last presidential election in 2014 saw the popular former governor of Jakarta—Joko

Widodo (Jokowi)—and Jusuf Kalla (both proposed by PDIP Party’s coalition) winning

the election by 53.15% against Gerindra’s chairperson Prabowo Subianto and his

running mate from Partai Amanat Nasional (PAN) Hatta Rajasa, who obtained 46.85%

of the votes (KPU 2014).

There are 34 ministers under President Jokowi’s cabinet, the so-called ‘working cabinet’

(Parlina & Widiarto 2014). During his 100 days in government, Jokowi was criticised

14

for some of his policies, such as those that increased fuel prices. This was accompanied

by the distribution of the Kartu Indonesia Sehat (KIS or Indonesia Health Cards), Kartu

Keluarga Sejahtera (KKS or Prosperous Family Cards) and Kartu Indonesia Pintar (KIP

(KIP or Indonesia Smart Cards) as compensation to low-income people. More recently,

there have also been critiques about the president’s ability and commitment to

combating corruption in Indonesia in relation to the conflict between the police and the

Corruption Eradication Commission (Sidjabat 2015).

2.3.2 Brief History of the Political System

2.3.2.1 The Soekarno Era

The influences of Hinduism, Buddhism, Islam, Dutch colonial rule and powerful

nationalistic independence movements—along with other cultural and external

influences—have shaped Indonesia’s political system. Indonesia was occupied by the

Dutch for three-and-a-half centuries. Dutch colonial rule shaped the current

geographical make-up of contemporary Indonesia. The Dutch colonial period ended

when the Japanese arrived in 1942. During WWII, making the most of the momentum

of Japanese surrender in 1945, Indonesia proclaimed her independence on 17 August

1945. Two central figures in this proclamation were Soekarno and Mohammad Hatta,

who became Indonesia’s first president and vice president (respectively). In its early

period of independence, as stipulated in Indonesia’s 1945 Constitution, the country

practiced a presidential system of government. This system was characterised by a clear

separation between the executive and legislative functions. In addition, this system

provided checks and balances to safeguard the government. At the same time, the

legislative body possessed the right to dismiss the president. According to Noor (2008),

Indonesia practiced a pure presidential system of government characterised by: (1) the

president as head of government; (2) the president having a fixed tenure of five years;

(3) the president not being accountable to the legislative body; and (4) the president

having no mandate to dismiss the legislative body. Further, Noor (2008) has asserted

that Indonesia implemented a hybrid system of government in that period, which

incorporated both a presidential and a parliamentary system. The evidence supporting

this argument is that the president was accountable to Majelis Permusyawaratan Rakyat

(MPR or People’s Consultative Assembly) as legislative body in which MPR had the

authority to enact laws.

15

Indonesia experienced a parliamentary system by enacting legislations on 14 November

1945 and a federal system by enacting legislations on 27 December 1949. A substantial

instability existed in the government and political system during this period, which was

characterised by the rise and fall of cabinets in the parliament within short periods;

hence, the parliamentary system was not successful in contributing to Indonesia’s

political stability. President Soekarno then embarked upon Guided Democracy from

1959; this lasted until 1965, with a coalition of mutually hostile nationalists,

communists and religious groups. This period was marked by high levels of government

intervention in the economy, excessive debt, high inflation and low growth. Political

groups competed fiercely and the threat of disintegration was always present (Cassing

2000).

2.3.2.2 The Soeharto Era

President Soekarno was forced to step down when Indonesia was threatened by the

military rebellions of Partai Komunis Indonesia (PKI or the Communist Party of

Indonesia. These rebellions forced President Soekarno to be eased out of power and

gave Soeharto the opportunity to consolidate his own position as Indonesia’s ruler over

the next 32 years. As the ruler, Soeharto had exceptional power and authority over

almost every aspect of life, including politics, the economy and the military. The Golkar

party was the consistent winner of general elections. Cassing (2000) has maintained that

Soeharto gained full support from the military and the broad backing of society. Further,

Cassing (2000) explains that Soeharto’s strategy was to compete with the executive

office for a power that created limitations on political discourse and isolation for the

political opposition. Soeharto did not believe in political competition and openness. The

function of cabinet ministers was to execute the policies of the president with no

political power of their own. As Cassing (2000, p.160) argues:

[S]oeharto eliminated political competition and that this in particular allowed for the

creation of a mercantilistic economic environment akin to 16th century England and

France.

Seda (2005) has asserted that pervasive patrimonalism was an embedded characteristic

of Soeharto’s regime, in which Soeharto gained his exceptionally strong political power

through his efforts to ensure the loyalty of key sections of the political elite. This was

16

done by satisfying the political elite’s interests, mainly material interests. The finances

for servicing this aspiration and interest were derived from the country’s oil boom

revenue in 1973, which gave the country abundant prosperity. This abundant prosperity

had allowed Soeharto to patronise his supporters and simultaneously threaten his

opponents. This gave him the opportunity to maintain his power and transform the

bureaucracy into an instrument of presidential power. As a consequence, there was a

high concentration of power in Soeharto’s hands.

As part of a strategy to patronise his supporters, Soeharto also allowed key government

officers to grant licences for certain economic activities. These officers were thus

enabled to extract financial resources from private parties. It was not only the

government officers who gained substantial benefits from Soeharto’s strategy.

Soeharto’s associates, including Chinese businessman Liem Sioe Liong, along with Bob

Hasan and his children, also obtained facility in the form of monopolies over the import

and distribution of major commodities. These associates and their families were given

the facility to become involved in projects: they won several large government projects

financed by state-owned banks with low interest rates. Unfortunately, some of these

loans defaulted, forcing the banks to collect payments (Schwarz 2004). Soeharto’s

pervasive patrimonialist strategy resulted in the elimination of political competition and

increased the concentration of power to a small group of people; in addition, it resulted

in a set of rent-seeking incentives,4

which ultimately shaped regulation in the

Indonesian economy (Cassing 2000).

In terms of economic policy, as per Seda (2005), Soeharto’s strategy was influenced

considerably by two groups: technocrats (market-oriented), most of whom were in the

Badan Perencanaan Nasional (BAPPENAS or Central Planning Bureau) and MOF, and

the nationalists (government planning-oriented), most of whom were in the Ministry of

Trade and Industry and the State Ministry of Research and Technology. The

technocrats, led by Prof. Widjojo Nitisastro emphasised market mechanisms when

overseeing the national economy. Policies included market deregulation and

privatisation of state assets to foster economic growth. In contrast, the nationalists

emphasised the role of government in conducting the national economy. Their policies

4 Rent-seeking is defined as ‘the activities whereby individuals seek return from state-sanctioned

monopoly rights’ (Ekelund & Tollison 1981).

17

encouraged the maximisation of state resources to build and strengthen domestic

markets. The nationalist group argued that the government should implement import

substitution policies and allocate more resources to high-tech state enterprises.

Generally, the direction of development strategies in Soeharto’s era was dependent on

the state of the economy. In periods of economic boom, the nationalists’ strategies were

implemented, while in times of economic stagnation, the technocrats’ strategies were

preferred.

In terms of natural resources management, Soeharto attracted foreign companies to

participate in extracting Indonesia’s natural resources, ascribing this approach to

Indonesia’s insufficient technology and capital (Seda 2005). To facilitate foreign

companies’ participation in the extraction of Indonesia’s natural resources, Soeharto

initiated important laws pertaining to foreign investment. These laws include: (1) Law

1/1967 on foreign investment, which stipulates clear procedures for foreign operations

in Indonesia; (2) Law 5/1967 on forestry, which stipulates that all forests fall under the

control of the state, and (3) Law 11/1967 on mining, stating that all lands within the

Republic of Indonesia could be used for mining. As a result of enacting the laws, a large

number of multinational companies have participated in natural resources extraction in

Indonesia (Seda 2005).

During the 1970s, oil became Indonesia’s main export and the primary source of

government revenue. However, this changed with the collapse of oil prices in the 1980s,

leading to budget deficits for Indonesia. The international oil price decreased from USD

38 per barrel to USD 12. This decline reduced the portion of oil and gas exports from

USD 18.4 billion (82% of total exports in 1982) to USD 8.3 billion (56% of total

exports in 1986). On the fiscal side, the decrease in oil prices resulted in decreased

government revenue from the oil and gas sectors: from IDR 8.6 trillion to IDR 6.3

trillion, or from 70% to 39% of total revenue (Robison & Rosser 1998).

This budget deficit required corrective action. One proposed action was trade

liberalisation to allow for a more diversified, manufacturing-based economy. However,

this proposal raised new problems for Soeharto, as trade liberalisation would have

required the relaxation of some trade barriers; in turn, this would have reduced the

monopoly power of Soeharto’s associates through import substitution. This dilemma

resulted in some misguided and crucial policies such as policies of granting monopolies

18

of car imports and toll roads to the family member of Soeharto (Cassing 2000).

However, economic structural adjustment appeared to be the only choice. To reduce the

Indonesian budgetary reliance on oil and gas and to encourage labour intensiveness, the

government deregulated trade, finance and investment. This corrective action was

effective, shown in the increase of non-oil and gas exports exceeding oil and gas

exports. Indonesia’s national economy had started to recover by the beginning of the

1990s.

Another economic shock came in the late 1990s, as a result of insufficient regulation

and prudence and the control mechanisms necessary to conduct liberalisation policies.

Although most macroeconomic variables signalled a healthy economy, corruption and

favouritism in the industrial and financial sectors meant that the economy was not as

strong and stable as it seemed. For instance, banking deregulation made it much easier

to establish new banks by lowering capital requirements substantially and opened up

new licenses and branches. This relaxation stimulated banks to expand their credit,

increasing the money supply by up to two-and-a-half times in three years. This

condition worsened when banks began lending large sums of public money to the

banks’ owners or to their associates for unfeasible projects (Cassing 2000). This

banking sector deregulation has been considered a fundamental policy mistake. In

addition, the decision to implement the nationalists’ idea to give government support for

large state enterprises was inefficient as only few of these state enterprises performed

well. In the absence of strong economic performance, the Indonesian economy

collapsed when the AFC struck in 1997, when Soeharto was forced to step down.

2.3.2.3 The Reformation Era

Soeharto’s fall was followed by a major transformation in all aspects of Indonesia’s

politics and economy. This period of reform (known as reformasi) involved the

economy, political sphere, bureaucracy and government regulations. Confidence

improved regarding the opportunities to foster democracy in Indonesia. Soeharto was

succeeded by President BJ Habibie (1998–1999), Abdurrahman Wahid (1999–2001),

Megawati Soekarno Putri (2001–2004), SBY (2004–2014), and Joko Widodo (2014-

2019).

19

A number of key reforms have been designed to enhance good government practices

and to increase the quality of Indonesia’s democracy. For example, in the political

system, the power divided between the president (as the executive body) and the

parliament (as the legislative body) has been balanced through the acknowledgement of

new political parties and their right to participate in general elections, prescribed by

Law 2/1999 and 31/2002. With regard to fiscal policy, the enactment of Law 22/1999

on local government and Law 25/1999 has allowed a more balanced budget allocation

between the central and regional governments (Resosudarmo 2005). Based on these

laws, the central government is mandated to transfer increased authority to provincial

and district level governments (Vaughn 2011). Along with the expectation that this

transformation will enable Indonesia to achieve long term development, this radical

change also raises negative effects such as political uncertainty, inconsistent laws and

regulations, weak law enforcement and a weak governmental system (Vaughn 2011).

The Abdulrahman Wahid presidency, which was followed by that of Megawati, did not

produce many reforms; the main party that supported Wahid held a minority in the

parliament. In fact, all governments post-Soeharto, including SBY’s (2004–2014)

government, have been based on the so-called ‘rainbow coalition’: SBY’s Democrat

Party also did not win a majority of seats. SBY’s government post-2009 consisted of six

out of the nine parties in parliament. This created a dominant among perception within

Indonesia’s mainstream literature regarding ‘cartelisation’ tendencies, borrowing from

the work of Katz and Mair (1995), and as elaborated here by Mietzner (2013, p.3):

[c]ontemporary political parties no longer compete with each other but form collusive

alliances to jointly exploit state resources.

Despite this, Mietzner (2013) argues there is little evidence that cartelisation was indeed

the main feature of post-Soeharto era politics.

Resosudarmo (2005) has noted the immediate effects of reformasi and the

implementation of the decentralisation policy. First, there was an increase in conflict

between central and local governments due to a lack of harmony among various levels

of government. There was a sense of competition regarding the dominance of both

central and regional governments. Second, a number of local conflicts involved both

disputes between local communities and the state, along with disputes among local

20

communities themselves. These types of conflicts had increased in particular due to

competition over obtaining the rights to exploit natural resources. Third, a change in the

nature of corruption existed, in which a centralised corruption was replaced by a more

fragmented and widespread bribe-collection system. Fourth, there was tendency of the

regional governments to raise revenue through nuisance taxes such as regional taxes

levied on the consumers payable to the local government on top of central government

taxes and resource licences.

2.4 Politics and Business in Indonesia

2.4.1 Introduction

The Indonesian business landscape has been characterised as ‘ersatz capitalism’

(Yoshihara 1988), ‘crony capitalism’ or ‘patron-client’ (Muhaimin 1991). Yoshihara

(1988) has defined Indonesia’s economy as ‘ersatz’ since the Indonesian economy has

been dominated by foreign capital, Chinese capitalists, rent-seekers, crony capitalists

and bureaucratic capitalists. The patron-client concept resulted from ‘neo-

patrimonialism’, a concept that originated in Max Weber’s patrimonialism (Muhaimin

1991). Muhaimin (1991) used this patron-client framework in his thesis on politics and

business in Indonesia.

Soeharto, Indonesia’s second and longest serving president (1968–1998) did not begin

the patron-client system. During Sukarno’s regime (1945–1968), business people also

enjoyed special favours. However, during Soeharto’s regime, politics and business

became much more closely intertwined (Borsuk & Chng 2014). Such links between

politics and business—especially during Soeharto’s regime—were well documented by

the ground-breaking works of Muhaimin (1991), Shin (1989), Yoshihara (1988),

Robison (1986) and a biography on Liem Sioe Liong’s Salim Group by Borsuk and

Chng (2014).

After the Soeharto era, exclusive import licences and monopolies for certain companies

or business groups were dismantled by the IMF. An era of democracy had begun. The

regime adopted civilian rule under Habibie (1998–1999), Abdurrahman Wahid (1999–

2002), Megawati (2002–2004) and SBY (2004–2014). Having political connections no

longer had the same effect. The excess and easy profits from exclusive import licences

21

and monopolies that had resulted from political connections in the past were no longer

the modus operandi. The manifestations of these relationships were less blatant.

Nonetheless, the links between business and politics in Indonesia post-Soeharto

continue and even flourish, despite democratisation, decentralisation and deregulation

(Chua 2008).

Previous studies examining the links between politics and business in Indonesia can be

categorised in general as examinations from the perspective of political economists,

such as works by Shin (1989) and Robison (1986) or socio-historical-cultural works,

such as those by Borsuk and Chng (2014), Backman (2001), Muhaimin (1991) and

Yoshihara (1988). In the following sections, I will first examine the mechanisms of how

the state apparatus can take advantage of its position for rent-seeking. I will then discuss

the possible causes of this intertwining of politics and business in Indonesia: oligarchy,

culture and government intervention.

2.4.2 The State and Rent-Seeking

Despite a decline in its power, the presidency remains the most contested position in

Indonesia, due its central role in the budgeting, law-making and economic planning

(Mietzner 2013). Accordingly:

[t]ycoons have continued to seek the president’s favour by offering financial

inducement (Mietzner 2013, p.75).

The second most coveted position is that of a minister. Besides a ministerial budget and

the managerial autonomy that comes with it, a ministry has the power to implement

policies such as determining quotas for imports of certain commodity. This has

provided ample opportunity for patronage from the Soekarno era to the present day

(Mietzner 2013).

Being a member of parliament (MP), especially in the post-Soeharto era, is a lucrative

position that is contested heavily. The ability to draft laws and influence any proposed

legislation can encourage MPs to use their institutional powers to advantage (Mietzner

2013). For example, the parliament has to approve government-proposed budgets.

‘Budget scalping’—the insertion and or approval of certain projects in exchange for

kickbacks from businesspeople—has been observed and identified as a very serious

22

phenomenon (Mietzner 2013). MPs have also been accused of accepting kickbacks to

block or approve certain points in proposed legislation (Mietzner 2013). For example,

Mietzner (2013) mentions a certain paragraph that was disadvantageous to the tobacco

industry that suddenly disappeared from proposed legislation on the tobacco industry.

Yoshihara (1988, p.87), as far back as the late 1980s, has argued that:

[d]emocracy has not necessarily done better than dictatorship; it too has created many

rent-seekers, although the use of government connections for business is not as

blatant as under dictatorship.

One major problem with democracy is that politicians need funds to run for office and

they turn to business people as their main source of capital.

2.4.3 Oligarchy

Winters (2014) mentions that Indonesia has followed a typical capitalist development,

whereby ‘a small number of ultra-wealthy citizens at the top are rapidly pulling away

from the rest’ (Winters 2014, p.11). He further notes that extreme inequality in wealth

brings with it extreme inequality in politics. Oligarchy theory captures this relationship

best, as wealth is the most potent of power resources. Oligarchs are ‘actors empowered

by wealth’ (Winters 2014, p.14). Winters’ theory was derived from power resources

theory, and wealth as one of the powers.

Winters (2011) further typifies four ideal oligarchies according to whether oligarchs are

armed or disarmed: warring, ruling, sultanistic or civil. Indonesia has been classified ‘as

a classic example of ‘sultanistic oligarchy’ under Soeharto’ (Winters 2014, p.15). The

emergence of a wealthy stratum in Indonesia began mostly during Soeharto’s time in

office. To maintain one’s wealth, one had to be in the proximity of and aligned with

Soeharto. Since 1998, Indonesia had been ruled by an electorally chosen oligarch. In

concluding his analysis, Winters (2014) was not optimistic regarding the potential of the

law to constrain oligarchs in Indonesia as they will not impose punitive legal constraints

on themselves. The core of oligarchy is the politics of defending wealth. Post-Soeharto,

Indonesian oligarchs have used their ‘material power for wealth and property defence in

a political economy overflowing with threats and uncertainties’ (Winters 2011, p.192).

Another seminal work on oligarchy in Indonesia is a study by Robison and Hadiz

23

(2004). Robison and Hadiz approached the oligarchs as a class and examined the

collective nature of their behaviour in pursuit of authority; hence, this is more of a neo-

Marxist approach. However, both works note that democratisation has changed

Indonesian politics but has not eliminating oligarchic rule (Ford & Pepinsky 2014).

Hadiz and Robison (2014) argue that up to the current era, over a decade after Soeharto

resigned, a close proximity to public officials is still how the private sector accumulates

its wealth. Social and economic power has been reorganised but largely remains the

same. The same names continue to dominate politics and business in contemporary

Indonesia.

2.4.4 Culture

Some scholars try to identify culture as a reason for the intertwining of politics and

business in Indonesia. Indonesian culture, dominated by Javanese culture, inhibits risk

taking; hence the indigenous population aspires to become civil servants, bureaucrats or

to join the military. In contrast, Chinese Indonesians have little choice but to go into

business. During Soeharto’s era, no Chinese Indonesians became ministers (except for

Bob Hasan; Soeharto’s ‘crony’ was appointed to a ministerial role for a brief period at

the end of his reign), top bureaucrats or top military officers. This fact aligns well with

the culture and nature of the Chinese who are perceived as hardworking, and who have

business networks within and beyond Indonesia for sources of capital (Yoshihara 1988).

A mutual relationship has evolved to a point where patron-client relations (as per

Weber’s concept) have developed and where Chinese businesspeople ‘were co-opted

and subjugated during Soeharto era’ (Chua 2008).

Indonesia’s economic performance has been attributed to Chinese minorities (Yoshihara

1988). Yoshihara (1995) attributes the success of the rent-seeking Chinese ‘ersatz

capitalists’ to culture of a lack of strong work ethics. By a lack of strong work ethics

Yoshihara means that the value orientation of the indigenous population emphasised

leisure and adaptation to nature. Moreover, he claims that indigenous Indonesians have

a built-in bias against plain money-making and towards the non-materialistic aspects of

life (Yoshihara 1995).

‘Chineseness’ has been compared with Protestantism and European capitalism, in that

they hold similar values regarding materialism, an emphasis on education, obedience,

24

handwork and thrift (Mackie 1998). Mackie (1999) claims that the Chinese have the

capabilities as well as incentives for commercial success due to their values and culture

cause the Chinese. Mackie (1989, p.99) cites their ‘strong motivation to succeed’, or

even ‘the widespread Chinese propensity towards gambling’ as the traits that enabled

them to flourish in business.

Culturally based premises, such as trust (xin yong) and connection (guanxi) have been

cited to explain the widespread influence of Chinese businesspeople in South East Asia

(see Backman 2001; Menkhoff & Gerke 2002; Tan 2000; Wu 2000); however, typically

they take guanxi (connections) as just another characteristic trait of ethnic Chinese

(Backman 2001; Wu 2000).

Soon after Soeharto came into power, Chinese capital was welcomed and was treated

more and more as domestic capital. As a result, the Chinese expanded into various

fields the new economic policy had opened up (Yoshihara 1988). During Soeharto’s

New Order regime, the interests of the rulers and Chinese capitalists were aligned; links

to state officials as patrons were critical for the emergence of business groups and

crucial for further capital accumulation (Chua 2008).