Desk Note Wednesday, Russian Oil Gas - Gazprom...

27

Research Department + 7 (495) 785‐53‐36 www.bcs.ru Timur Salikhov, CFA +7 (495) 785 5336 (4631) [email protected] Desk Note Wednesday, October 9, 2013 Russian Oil & Gas Trade ideas for all types of investors Share price upside summary * Since the trough in June Source: FactSet, BCS The discount reflects sliding returns and high regulatory risks Source: FactSet, BCS Returns are sliding and regulatory risks remain high, but trade ideas still exist. In this report, we highlight our preferred dividend and positive catalyst plays, warn of the riskiest and misperceived stocks and offer short‐ and long‐term pair trade advice. Long‐term (upstream with greenfields) – Gazprom Neft, Lukoil and Rosneft Catalysts – Novatek (Yamal LNG), Lukoil (W. Qurna‐2) and Gazprom (dividends) Dividends – Bashneft (8‐12%), Gazprom (rising to 9%) and Lukoil (>15% pa growth) Stocks to avoid – Transneft (pref), Alliance Oil and Tatneft Gazprom Neft, Lukoil and Rosneft – safest LT exposure. Industry regulatory risks remain high as the government seeks additional sources of tax revenues to prevent budget deficit growth. The recent oil tax reshuffle alone will result in over $2.5bn pa of additional payments. Tax hikes in the future are highly likely, especially in the profitable refining and gas sectors. Upstream companies with significant greenfield exposure are the safest play on the sector: Gazprom Neft, Lukoil and Rosneft. Novatek, Lukoil and Gazprom – momentum plays. Global energy investors have kept Novatek on their radar, anticipating it to de‐risk on the back of liberalization of LNG exports, new partners for Yamal and FID. Lukoil offers the best exposure to oil price stabilization, while the launch of West Qurna‐2 in November should crystalize over 10% of the company’s value. Gazprom is yet to price in the 35% dividend payout requirement, most of the bad news is behind it, and a continued rise in gas sales to Europe and a gas pricing agreement with China could further improve sentiment towards the stock. Bashneft, Gazprom and Lukoil – dividend yielders. Russian O&G companies have nearly trebled dividend payments since 2008. Bashneft’s and SurgutNG pref’s double‐digit dividend yields are among the highest globally. Lukoil’s past and future dividend growth (20% pa) is far ahead of its peers. Gazprom minorities are the primary beneficiaries of the dividend payout increase, unlike holders of Transneft prefs, who have no guarantee that the benefits of a larger dividend pool will all go to common shareholders. Bashneft upgraded to Buy. Due to underperformance following the recent rally (3% vs sector’s 29%) and a generous year‐end dividend (8% common, 12% preferred) we have upgraded Bashneft to Buy. The investment story is clean – Bashneft is growing production (4% CAGR 2013‐16e) unlike most of its peers, its CapEx cycle is fairly light, and therefore the 10% FCF yield is above the sector average of 6%. A potential London IPO next year would improve liquidity, attract new investors and finance resource base growth and asset acquisitions. Lukoil, Gazprom Neft and Novatek – still top picks; Bashneft – upgraded to Buy Company Rating Current Target price Upside Dividend P/E EV/EBITDA price New Old yield ‘13 ‘14e ‘15e ‘14e ‘15e Lukoil BUY $64.00 $75.00 $75.00 17% 5.1% 4.5x 4.9x 2.5x 2.6x Gazprom Neft BUY $22.32 $25.00 $25.00 12% 5.7% 4.3x 5.0x 3.0x 3.3x Bashneft BUY Rb1,887.60 Rb2,100.00 Rb2,100.00 11% 8.0% 6.5x 6.8x 4.9x 5.1x Novatek BUY $135.00 $145.00 $145.00 7% 2.1% 13.8x 12.5x 10.5x 9.3x Rosneft HOLD $8.08 $8.30 $8.30 3% 3.2% 6.6x 7.2x 4.9x 4.8x Surgutneftegas (pref) HOLD Rb23.50 Rb24.00 Rb23.50 2% 9.2% 5.7x 6.0x 0.7x 0.7x Gazprom HOLD $9.08 $9.00 $8.50 ‐1% 4.7% 3.4x 3.7x 3.0x 3.0x Surgutneftegas SELL $8.61 $8.50 $8.30 ‐1% 2.1% 5.7x 6.0x 0.7x 0.7x Tatneft SELL $38.99 $40.00 $39.00 3% 4.0% 6.4x 6.6x 4.6x 4.7x Transneft (pref) SELL Rb83,786.00 Rb75,000.00 Rb75,000.00 ‐10% 0.8% 3.0x 2.8x 3.0x 2.9x Alliance Oil SELL SEK 52.95 SEK 41.00 SEK 41.00 ‐23% ‐ 4.0x 3.1x 4.4x 3.9x As of 7 October 2013 Source: FactSet, BCS ‐23% ‐10% ‐1% ‐1% 2% 3% 3% 7% 11% 12% 17% ‐30% ‐ 10% 10% 30% 50% ‐30% ‐ 10% 10% 30% 50% AOIL TRNFP SGGD OGZD SNGSP ATAD ROSN NVTK BANE GAZ LKOD Past performance* Upside 0 2 4 6 8 10 12 Oct‐ 08 Jan‐10 Apr‐11 Jul ‐ 12 Oct‐13 P/E Russian oils Global majors 40% discount

Transcript of Desk Note Wednesday, Russian Oil Gas - Gazprom...

Research Department + 7 (495) 785‐53‐36 www.bcs.ru

Timur Salikhov, CFA+7 (495) 785 5336 (4631)

Desk Note

Wednesday, October 9, 2013

Russian Oil & Gas

Trade ideas for all types of investors

Share price upside summary

* Since the trough in June Source: FactSet, BCS

The discount reflects sliding returns and high regulatory risks

Source: FactSet, BCS

Returns are sliding and regulatory risks remain high, but trade ideas still exist. In this report, we highlight our preferred dividend and positive catalyst plays, warn of the riskiest and misperceived stocks and offer short‐ and long‐term pair trade advice.

Long‐term (upstream with greenfields) – Gazprom Neft, Lukoil and Rosneft

Catalysts – Novatek (Yamal LNG), Lukoil (W. Qurna‐2) and Gazprom (dividends)

Dividends – Bashneft (8‐12%), Gazprom (rising to 9%) and Lukoil (>15% pa growth)

Stocks to avoid – Transneft (pref), Alliance Oil and Tatneft

Gazprom Neft, Lukoil and Rosneft – safest LT exposure. Industry regulatory risks remain high as the government seeks additional sources of tax revenues to prevent budget deficit growth. The recent oil tax reshuffle alone will result in over $2.5bn pa of additional payments. Tax hikes in the future are highly likely, especially in the profitable refining and gas sectors. Upstream companies with significant greenfield exposure are the safest play on the sector: Gazprom Neft, Lukoil and Rosneft.

Novatek, Lukoil and Gazprom – momentum plays. Global energy investors have kept Novatek on their radar, anticipating it to de‐risk on the back of liberalization of LNG exports, new partners for Yamal and FID. Lukoil offers the best exposure to oil price stabilization, while the launch of West Qurna‐2 in November should crystalize over 10% of the company’s value. Gazprom is yet to price in the 35% dividend payout requirement, most of the bad news is behind it, and a continued rise in gas sales to Europe and a gas pricing agreement with China could further improve sentiment towards the stock.

Bashneft, Gazprom and Lukoil – dividend yielders. Russian O&G companies have nearly trebled dividend payments since 2008. Bashneft’s and SurgutNG pref’s double‐digit dividend yields are among the highest globally. Lukoil’s past and future dividend growth (20% pa) is far ahead of its peers. Gazprom minorities are the primary beneficiaries of the dividend payout increase, unlike holders of Transneft prefs, who have no guarantee that the benefits of a larger dividend pool will all go to common shareholders.

Bashneft upgraded to Buy. Due to underperformance following the recent rally (3% vs sector’s 29%) and a generous year‐end dividend (8% common, 12% preferred) we have upgraded Bashneft to Buy. The investment story is clean – Bashneft is growing production (4% CAGR 2013‐16e) unlike most of its peers, its CapEx cycle is fairly light,and therefore the 10% FCF yield is above the sector average of 6%. A potential London IPO next year would improve liquidity, attract new investors and finance resource base growth and asset acquisitions.

Lukoil, Gazprom Neft and Novatek – still top picks; Bashneft – upgraded to Buy Company Rating Current Target price Upside Dividend P/E EV/EBITDA price New Old yield ‘13 ‘14e ‘15e ‘14e ‘15e

Lukoil BUY $64.00 $75.00 $75.00 17% 5.1% 4.5x 4.9x 2.5x 2.6x

Gazprom Neft BUY $22.32 $25.00 $25.00 12% 5.7% 4.3x 5.0x 3.0x 3.3x

Bashneft BUY Rb1,887.60 Rb2,100.00 Rb2,100.00 11% 8.0% 6.5x 6.8x 4.9x 5.1x

Novatek BUY $135.00 $145.00 $145.00 7% 2.1% 13.8x 12.5x 10.5x 9.3x

Rosneft HOLD $8.08 $8.30 $8.30 3% 3.2% 6.6x 7.2x 4.9x 4.8x

Surgutneftegas (pref) HOLD Rb23.50 Rb24.00 Rb23.50 2% 9.2% 5.7x 6.0x 0.7x 0.7x

Gazprom HOLD $9.08 $9.00 $8.50 ‐1% 4.7% 3.4x 3.7x 3.0x 3.0x

Surgutneftegas SELL $8.61 $8.50 $8.30 ‐1% 2.1% 5.7x 6.0x 0.7x 0.7x

Tatneft SELL $38.99 $40.00 $39.00 3% 4.0% 6.4x 6.6x 4.6x 4.7x

Transneft (pref) SELL Rb83,786.00 Rb75,000.00 Rb75,000.00 ‐10% 0.8% 3.0x 2.8x 3.0x 2.9x

Alliance Oil SELL SEK 52.95 SEK 41.00 SEK 41.00 ‐23% ‐ 4.0x 3.1x 4.4x 3.9x

As of 7 October 2013 Source: FactSet, BCS

‐23%

‐10%

‐1%

‐1%

2%

3%

3%

7%

11%

12%

17%

‐30% ‐10% 10% 30% 50%

‐30% ‐10% 10% 30% 50%

AOIL

TRNFP

SGGD

OGZD

SNGSP

ATAD

ROSN

NVTK

BANE

GAZ

LKOD

Past performance* Upside

0

2

4

6

8

10

12

Oct‐08 Jan‐10 Apr‐11 Jul‐12 Oct‐13

P/E

Russian oils Global majors

40% discount

Russian Oil & Gas

2

Investment case

Looking for trade ideas after the strong rally: We remain cautious on the sector’s returns, highlight strong regulatory risks and therefore see limited upside in share prices (4%, on average) despite attractive valuations on a global scale (40% discount). For this reason, we focus on trade ideas for different investor types with different investment horizons. We highlight our preferred dividend and catalyst plays, warn of the riskiest and misperceived stocks and offer short‐ and long‐term pair trade advice.

Top ‘3s’ Dividend plays

Stock Yield ‘13 Reason Comments Bashneft 8‐12% Robust yield just days away Sustainably high dividend yield backed by FCF, despite heavy CapEx

cycle (10%, on average, during 2013‐16)

Gazprom 5% Switch to 35% IFRS payout The stock is primarily driven by consensus dividend expectations, which are currently reflecting a 25% IFRS payout

Lukoil 5% Beating consensus expectations Management beat its 15% pa dividend growth guidance in 2010‐12, but the Street remains conservative with respect to future growth

Catalyst plays

Stock Catalyst Comments Novatek Liberalization of LNG exports Allows export of LNG directly to customers

New partner(s) for Yamal LNG Partners’ commitment will further de‐risk the project

FID on Yamal LNG Adds credibility to the project in the eyes of investors

Domestic gas sales increase High chance to beat FY13 target as Gazprom is directing more volumes toEurope

Lukoil Test launch of West Qurna‐2 De‐risking consensus 2014 FCF forecasts

Oil price stabilization Least sensitive to the oil price decline

3Q13 US GAAP results Upside risk to consensus 2013 FCF forecasts

Gazprom Strong momentum in Europe Rising volumes and spot prices are driving earnings

Deal with China Guaranteed profitable gas supplies (save for a costly pipeline)

Dividend talks Consensus’ DPS expectations are major share price drivers

Long‐term trades1

Trade Reason Risks Long Lukoil / Short Rosneft

Shareholder returns mismatch and commitment to shareholder value

‐ Lukoil abandons the 15% pa dividend growth target ‐ Rosneft: value‐accretive resource base growth and asset acquisition

Long Novatek / Short Gazprom

Novatek management’s track‐record vs Gazprom’s lack of CapEx discipline

‐ Novatek: execution issues with Yamal LNG and decelerating growth

‐ Gazprom fights to preserve its domestic market share, optimizes costs and executes strict control over CapEx

Long Gazprom / Short Transneft (pref)

Playing the state companies’ dividend policy change (switch to 35% IFRS)

‐ Gazprom pushes back the dividend policy change and hikes CapEx

‐ Transneft guides for similar dividends for both classes of shares

Short‐term trades2

Trade Reason Risks Long Lukoil / Short Rosneft

A play on oil price stabilization and Lukoil’s West Qurna‐2 launch

‐ Lukoil: West Qurna‐2 launch delay, issues with cost recovery

‐ Rosneft: value‐accretive asset acquisition / resource base expansion

Long Gazprom Neft / Short SurgutNG

Valuation mismatch (4.3x P/E vs 5.7x) and a play on changes in greenfield regulation

‐ Gazprom Neft delays the development of greenfields, receives oil assets from Gazprom and reimburses the latter for historical costs

‐ SurgutNG: focus switch towards growth and resource base expansion

Long Alliance Oil (pref) / Short Alliance Oil

Guaranteed income vs execution risk and elevated valuation

‐ Uplift in refining margins sooner than expected; output growth above expectations at a reasonable cost

Stocks to avoid

Stock Reason Comments Transneft (pref) No guarantee to benefit from the switch to

a 35% dividend payout Increase in total dividend pool could all go to common shares, as charter does not stipulate that the dividend paid on preferred shares (10% RAS net income) must equal that paid on commons

Alliance Oil Expensive valuation does not justify fundamentals

Refinery upgrade delay, risk of consensus forecast downgrade, high M&A and execution risk

Tatneft Falling EPS; low shareholder returns; expensive

The second stage of Taneco will prevent value‐accretive use of FCF and will cap shareholder returns and growth

1. 1‐2 years, 2. 3‐6monthsSource: BCS

Russian Oil & Gas

3

Valuation

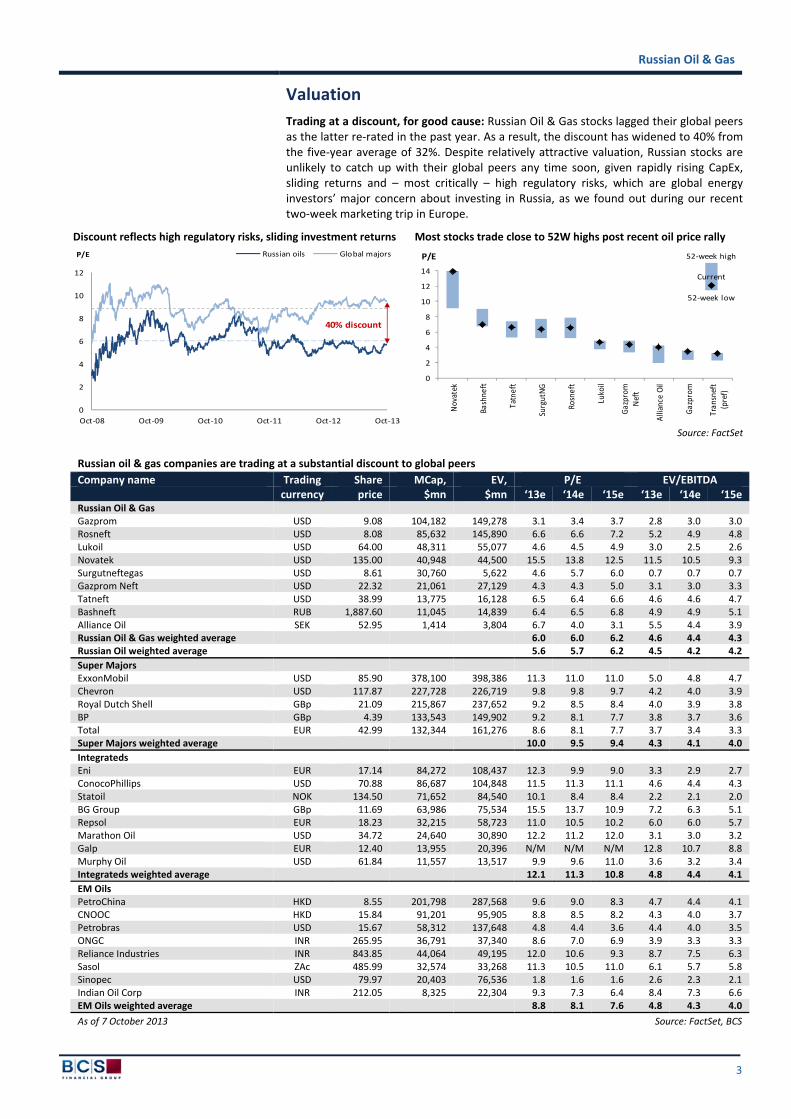

Trading at a discount, for good cause: Russian Oil & Gas stocks lagged their global peers as the latter re‐rated in the past year. As a result, the discount has widened to 40% from the five‐year average of 32%. Despite relatively attractive valuation, Russian stocks are unlikely to catch up with their global peers any time soon, given rapidly rising CapEx, sliding returns and – most critically – high regulatory risks, which are global energy investors’ major concern about investing in Russia, as we found out during our recent two‐week marketing trip in Europe.

Discount reflects high regulatory risks, sliding investment returns Most stocks trade close to 52W highs post recent oil price rally

Source: FactSet

Russian oil & gas companies are trading at a substantial discount to global peers

Company name Trading Share MCap, EV, P/E EV/EBITDA currency price $mn $mn ‘13e ‘14e ‘15e ‘13e ‘14e ‘15e

Russian Oil & Gas Gazprom USD 9.08 104,182 149,278 3.1 3.4 3.7 2.8 3.0 3.0Rosneft USD 8.08 85,632 145,890 6.6 6.6 7.2 5.2 4.9 4.8Lukoil USD 64.00 48,311 55,077 4.6 4.5 4.9 3.0 2.5 2.6Novatek USD 135.00 40,948 44,500 15.5 13.8 12.5 11.5 10.5 9.3Surgutneftegas USD 8.61 30,760 5,622 4.6 5.7 6.0 0.7 0.7 0.7Gazprom Neft USD 22.32 21,061 27,129 4.3 4.3 5.0 3.1 3.0 3.3Tatneft USD 38.99 13,775 16,128 6.5 6.4 6.6 4.6 4.6 4.7Bashneft RUB 1,887.60 11,045 14,839 6.4 6.5 6.8 4.9 4.9 5.1Alliance Oil SEK 52.95 1,414 3,804 6.7 4.0 3.1 5.5 4.4 3.9Russian Oil & Gas weighted average 6.0 6.0 6.2 4.6 4.4 4.3Russian Oil weighted average 5.6 5.7 6.2 4.5 4.2 4.2

Super Majors ExxonMobil USD 85.90 378,100 398,386 11.3 11.0 11.0 5.0 4.8 4.7Chevron USD 117.87 227,728 226,719 9.8 9.8 9.7 4.2 4.0 3.9Royal Dutch Shell GBp 21.09 215,867 237,652 9.2 8.5 8.4 4.0 3.9 3.8BP GBp 4.39 133,543 149,902 9.2 8.1 7.7 3.8 3.7 3.6Total EUR 42.99 132,344 161,276 8.6 8.1 7.7 3.7 3.4 3.3Super Majors weighted average 10.0 9.5 9.4 4.3 4.1 4.0

Integrateds Eni EUR 17.14 84,272 108,437 12.3 9.9 9.0 3.3 2.9 2.7ConocoPhillips USD 70.88 86,687 104,848 11.5 11.3 11.1 4.6 4.4 4.3Statoil NOK 134.50 71,652 84,540 10.1 8.4 8.4 2.2 2.1 2.0BG Group GBp 11.69 63,986 75,534 15.5 13.7 10.9 7.2 6.3 5.1Repsol EUR 18.23 32,215 58,723 11.0 10.5 10.2 6.0 6.0 5.7Marathon Oil USD 34.72 24,640 30,890 12.2 11.2 12.0 3.1 3.0 3.2Galp EUR 12.40 13,955 20,396 N/M N/M N/M 12.8 10.7 8.8Murphy Oil USD 61.84 11,557 13,517 9.9 9.6 11.0 3.6 3.2 3.4Integrateds weighted average 12.1 11.3 10.8 4.8 4.4 4.1

EM Oils PetroChina HKD 8.55 201,798 287,568 9.6 9.0 8.3 4.7 4.4 4.1CNOOC HKD 15.84 91,201 95,905 8.8 8.5 8.2 4.3 4.0 3.7Petrobras USD 15.67 58,312 137,648 4.8 4.4 3.6 4.4 4.0 3.5ONGC INR 265.95 36,791 37,340 8.6 7.0 6.9 3.9 3.3 3.3Reliance Industries INR 843.85 44,064 49,195 12.0 10.6 9.3 8.7 7.5 6.3Sasol ZAc 485.99 32,574 33,268 11.3 10.5 11.0 6.1 5.7 5.8Sinopec USD 79.97 20,403 76,536 1.8 1.6 1.6 2.6 2.3 2.1Indian Oil Corp INR 212.05 8,325 22,304 9.3 7.3 6.4 8.4 7.3 6.6EM Oils weighted average 8.8 8.1 7.6 4.8 4.3 4.0

As of 7 October 2013 Source: FactSet, BCS

0

2

4

6

8

10

12

Oct‐08 Oct‐09 Oct‐10 Oct‐11 Oct‐12 Oct‐13

P/E Russian oils Global majors

40% discount

0

2

4

6

8

10

12

14

Novatek

Bashne

ft

Tatneft

SurgutNG

Rosneft

Lukoil

Gazprom

Neft

Alliance

Oil

Gazprom

Tran

sneft

(pref)

P/E 52‐week high

52‐week low

Current

Russian Oil & Gas

4

Key changes

Upgrading Bashneft to Buy due to the following reasons:

o The stock’s underperformance following the oil price rally (3% vs sector’s 29%);

o generous dividends in the coming months (8% yield for common, 12% for preferred);

o the company’s clean investment story (group structure optimization, rising production and solid FCF).

Raising TPs by 2‐6% reflecting the upward shift in the Brent forward curve. The positive effect was partially offset by the freeze on 2014 gas tariffs and the crude oil tax reshuffle.

Revising estimates

We revised our financial forecasts to reflect 2Q13 financial results, the oil price increase and the government’s decision to freeze gas tariffs next year and reshuffle crude oil taxes (increase MET and reduce export duty).

Oil price increase: We mark to market the Brent forward curve to reflect the shift in

consensus oil price expectations (2013: $109 from $104; 2014: $105 from $99). We

adjust 2014 refining crack spreads accordingly.

o Key beneficiaries: i) Surgutneftegas and Tatneft, due to the largest upstream exposure; ii) Rosneft, due to high leverage.

Gas tariff freeze: Downside to our numbers is insignificant (4% for Novatek, 3% for

Gazprom), because we originally expected a maximum 5% pa increase in the tariff

vs the government’s target of 15% pa growth.

o The action is in line with our view that the gas sector’s high investment returns are associated with significant regulatory risks, be it the top line (tariff) or the bottom line (taxes).

o Novatek is more sensitive to changes in domestic gas tariffs than Gazprom, due to a higher share of domestic sales and Gazprom’s low margins on domestic gas sales.

Crude oil tax reshuffle:

o Government: c$2.5bn pa of additional tax revenues by 2015‐16.

o Key beneficiaries: i) Novatek – unaffected by the oil MET hike; benefits from lower export duties on crude/condensate and products, ii) Tatneft and Surgutneftegas – significant share of depleted fields absorbs a quarter of the MET increase; benefits of lower crude export duty offset higher cost of third‐party crude purchases.

o Key losers: Bashneft and Alliance Oil – higher cost of third‐party crude offsets lower product export duties.

Recently proposed oil & gas tax changes 2013 2014 2015 2016

Oil MET base rate (Rb/mcm)

Old 470 470 470 470

New 470 493 530 559

Change ‐ 5% 13% 19%

Oil export duty

Old 60% 60% 60% 60%

New 60% 59% 57% 55%

Change ‐ ‐1pp ‐3pp ‐5pp

Gas tariff growth

Old 15% 15% 15% N/A

New 15% 0% 5%* 5%*

Change ‐ ‐15pp ‐10pp N/A

* BCS real inflation rate expectationSource: Ministry of Finance, Federal Tariff Service, BCS

Russian Oil & Gas

5

Summary of macro and regulatory changes on financial forecasts

EBITDA

2014 Oil price increase

Gas tariff freeze

Oil tax maneuver Total

EBITDA 2015

Oil price increase

Gas tariff freeze

Oil tax maneuver Total

EBITDA 2016

Gas tariff freeze

Oil tax maneuver Total

Surgutneftegas 8,040 4.3% ‐0.2% ‐0.2% 3.9% 8,273 1.5% ‐0.4% 1.0% 2.1% 8,782 ‐0.4% 3.7% 3.3%

Tatneft 3,506 4.2% 0.0% ‐1.6% 2.6% 3,010 1.6% ‐0.1% ‐2.9% ‐1.4% 3,541 ‐0.1% ‐1.9% ‐2.0%

Rosneft 27,680 4.1% ‐0.2% ‐1.6% 2.3% 24,528 1.7% ‐0.4% ‐2.8% ‐1.5% 28,398 ‐0.5% ‐1.5% ‐2.0%

Lukoil 23,387 2.0% 0.0% ‐1.0% 1.0% 22,231 0.9% ‐0.1% ‐1.5% ‐0.7% 22,359 ‐0.1% ‐0.9% ‐1.0%

Gazprom Neft 8,831 2.4% ‐0.2% ‐1.4% 0.8% 8,039 1.3% ‐0.4% ‐2.8% ‐1.9% 8,776 ‐0.4% ‐1.1% ‐1.5%

Novatek 4,531 2.1% ‐1.7% 0.4% 0.8% 4,286 0.8% ‐3.8% 1.4% ‐1.5% 4,465 ‐3.8% 2.8% ‐1.0%

Alliance Oil 840 1.3% ‐0.1% ‐0.6% 0.6% 945 0.9% ‐0.2% ‐0.5% 0.2% 845 ‐0.2% ‐1.3% ‐1.5%

Bashneft 3,061 1.2% 0.0% ‐1.0% 0.2% 2,818 1.1% 0.0% ‐1.5% ‐0.4% 2,781 0.0% ‐0.5% ‐0.5%

Gazprom 52,156 0.8% ‐1.3% ‐0.1% ‐0.6% 49,521 0.3% ‐2.9% 0.0% ‐2.5% 50,157 ‐2.9% 0.5% ‐2.3%

Source: BCS

Our new financial forecasts reflect the upward shift in the oil price expectations and the proposed changes in taxation

Revenue EBITDA Net income

$mn 2013e 2014e 2015e 2013e 2014e 2015e 2013e 2014e 2015eGazprom Old 149,970 149,655 149,932 52,028 49,564 48,637 30,603 29,229 27,426 New 154,655 152,410 150,232 56,001 52,156 49,521 32,952 31,187 27,828 Difference 3% 2% 0% 8% 5% 2% 8% 7% 1%

Rosneft Old 139,233 150,737 144,668 26,503 30,994 26,214 10,328 13,235 8,772 New 140,815 148,616 144,668 26,964 27,680 24,528 10,988 10,290 6,949 Difference 1% ‐1% 0% 2% ‐11% ‐6% 6% ‐22% ‐21%

Lukoil Old 143,007 146,221 138,178 19,353 24,623 21,966 10,259 9,726 8,627 New 140,947 143,055 139,885 18,698 23,387 22,231 9,870 8,873 8,663 Difference ‐1% ‐2% 1% ‐3% ‐5% 1% ‐4% ‐9% 0%

Novatek Old 9,896 10,891 11,727 4,132 4,223 4,224 2,864 3,095 3,087 New 9,612 11,091 11,782 4,042 4,531 4,286 2,834 3,380 3,222 Difference ‐3% 2% 0% ‐2% 7% 1% ‐1% 9% 4%

Surgutneftegas Old 39,294 38,591 36,412 7,972 8,774 7,476 7,878 6,852 5,572 New 40,597 38,900 36,589 8,034 8,040 7,002 8,169 6,262 5,143 Difference 3% 1% 0% 1% ‐8% ‐6% 4% ‐9% ‐8%

Gazprom neft Old 44,005 43,683 42,430 8,786 9,810 8,133 4,877 5,581 4,324 New 44,565 43,628 42,686 8,583 8,831 8,039 4,736 4,818 4,219 Difference 1% 0% 1% ‐2% ‐10% ‐1% ‐3% ‐14% ‐2%

Tatneft Old 13,724 13,642 12,813 3,666 3,715 3,182 2,200 2,340 1,925 New 13,914 13,965 13,382 3,555 3,506 3,010 2,148 2,146 1,721 Difference 1% 2% 4% ‐3% ‐6% ‐5% ‐2% ‐8% ‐11%

Bashneft Old 16,297 16,159 15,659 3,103 3,271 2,942 1,794 1,955 1,759 New 17,120 16,574 16,160 3,030 3,061 2,818 1,753 1,716 1,639 Difference 5% 3% 3% ‐2% ‐6% ‐4% ‐2% ‐12% ‐7%

Alliance Oil Old 3,424 3,797 3,615 588 998 922 146 475 428 New 3,627 3,716 3,749 671 840 945 182 321 410 Difference 6% ‐2% 4% 14% ‐16% 2% 25% ‐32% ‐4%

Transneft Old 23,644 24,046 24,675 10,965 11,256 11,754 5,152 5,651 6,071 New 23,886 23,741 24,280 11,177 10,896 11,387 5,526 5,477 5,880 Difference 1% ‐1% ‐2% 2% ‐3% ‐3% 7% ‐3% ‐3%

Source: BCS

Russian Oil & Gas

6

BCS vs consensus estimates

Our financial forecasts are generally below consensus due to more conservative oil price assumptions* Revenue EBITDA Net income

$mn 2013e 2014e 2015e 2013e 2014e 2015e 2013e 2014e 2015eGazprom Consensus 155,362 154,804 157,085 53,333 50,299 49,098 33,272 30,478 28,091 BCS 154,655 152,410 150,232 56,001 52,156 49,521 32,952 31,187 27,828 Difference 0% ‐2% ‐4% 5% 4% 1% ‐1% 2% ‐1%

Rosneft Consensus 143,681 151,389 150,696 28,070 29,988 30,320 12,908 12,957 11,907 BCS 140,815 148,616 144,668 26,964 27,680 24,528 10,988 10,290 6,949 Difference ‐2% ‐2% ‐4% ‐4% ‐8% ‐19% ‐15% ‐21% ‐42%

Lukoil Consensus 134,836 134,972 133,683 18,660 21,737 21,004 10,526 10,809 9,817 BCS 140,947 143,055 139,885 18,698 23,387 22,231 9,870 8,873 8,663 Difference 5% 6% 5% 0% 8% 6% ‐6% ‐18% ‐12%

Novatek Consensus 9,240 10,851 11,839 3,868 4,258 4,787 2,646 2,969 3,276 BCS 9,612 11,091 11,782 4,042 4,531 4,286 2,834 3,380 3,222 Difference 4% 2% 0% 4% 6% ‐10% 7% 14% ‐2%

Surgutneftegas Consensus 31,836 30,703 31,020 8,589 8,098 7,587 6,634 5,359 5,117 BCS 40,597 38,900 36,589 8,034 8,040 7,002 8,169 6,262 5,143 Difference 28% 27% 18% ‐6% ‐1% ‐8% 23% 17% 1%

Gazprom neft Consensus 45,802 45,450 45,179 8,749 8,906 8,284 4,940 4,911 4,234 BCS 44,565 43,628 42,686 8,583 8,831 8,039 4,736 4,818 4,219 Difference ‐3% ‐4% ‐6% ‐2% ‐1% ‐3% ‐4% ‐2% 0%

Tatneft Consensus 18,207 17,481 17,741 3,519 3,530 3,431 2,133 2,155 2,091 BCS 13,914 13,965 13,382 3,555 3,506 3,010 2,148 2,146 1,721 Difference ‐24% ‐20% ‐25% 1% ‐1% ‐12% 1% 0% ‐18%

Bashneft Consensus 17,022 16,764 16,479 3,042 3,035 2,925 1,728 1,700 1,631 BCS 17,120 16,574 16,160 3,030 3,061 2,818 1,753 1,716 1,639 Difference 1% ‐1% ‐2% 0% 1% ‐4% 1% 1% 0%

Alliance Oil Consensus 3,630 3,859 3,905 693 872 988 212 356 452 BCS 3,627 3,716 3,749 671 840 945 182 321 410 Difference 0% ‐4% ‐4% ‐3% ‐4% ‐4% ‐14% ‐10% ‐9%

Transneft Consensus 22,740 23,058 23,423 11,333 11,577 11,510 5,642 5,848 5,737 BCS 23,886 23,741 24,280 11,177 10,896 11,387 5,526 5,477 5,880 Difference 5% 3% 4% ‐1% ‐6% ‐1% ‐2% ‐6% 2%

* $108/bbl in 2013, $103/bbl in 2014, and $97/bbl in 2015Source: FactSet, BCS

Russian Oil & Gas

7

Recommendation summary1

Buy

Lukoil (TP $75/GDR) – Highest shareholder returns in the sector

Robust dividend growth (15% pa) translates into highest returns among peers

Diversified asset growth portfolio (Uzbek gas, Iraqi PSA, tax‐exempt Caspian fields) implying gradual production and earnings increase

Consensus has yet to re‐assess the FCF outlook taking into account CapEx optimization and West Qurna‐2 immediate cost recovery

West Siberian production starting to show positive signs; contribution of Imilor is underestimated

Attractive valuation – 4.5x P/E '14 – does not reflect robust shareholder returns

Novatek (TP $145/GDR) – Robust growth and catalysts

Strong execution track‐record, value‐accretive expansion projects and vast resource base have justified Novatek's valuation premium…

… which we expect to persist going forward, given Novatek's robust growth prospects and investment returns

Anticipated growth is significantly above the sector average, accelerating in the second half of the decade once Gydan fields and Yamal LNG come on‐stream

The stock is especially attractive in the short term, given numerous up‐coming catalysts de‐risking Novatek's flagship Yamal LNG project (19% of our fair value)

Industry regulatory risks – including slower domestic tariff growth and gas and condensate MET hike – are already in the price

Gazprom Neft (TP $25/GDR) – Robust growth, highest shareholder returns

Highest shareholder returns over the next two years (3% pa EPS growth and 6% dividend yield)

Robust FCF generation in the long‐term (c$16bn during 2017‐21, three quarters of the current market cap)

Valuation implies a 27% discount to peers vs 13% during 2010‐12

Large portfolio of greenfield projects (1.1mmboe/d hydrocarbon production) is not in the price, while additional tax breaks imply further potential upside

Catalysts include additional greenfield tax breaks, transfer of oil licenses from Gazprom and potential liquidity improvement, however, outcomes are twofold and timing is uncertain

Bashneft (TP Rb2,100/share) – Attractive dividend play

Robust FCF generation despite refinery upgrade CapEx: we estimate FCF yield to average 11% during 2013‐16e (vs sector average of 5%)

The highest dividend yield during 2009‐11 thanks to the company's flexible dividend policy (distribute generated FCF)

High interim dividend (Rb150/share; 8% yield on common, 12% yield on preferred) to be paid by year‐end

A potential London IPO next year would improve liquidity, expand the investor base and finance resource base growth and asset acquisitions

Valuation premium but justified – reflects strong execution track record and solid shareholder returns (6.5x P/E '14 vs sector's 5.7x)

1 For risks to BCS theses and valuation methodology, please refer to pages 24‐26

Russian Oil & Gas

8

Hold

Rosneft (TP $8.30/GDR) – Shareholder returns captive to high CapEx

Solid financial position and immense FCF generation capabilities

TNK‐BP merger synergies have yet to be monetized, reflected in stock valuation

Primary beneficiary of the greenfield tax reform proposals…

… due to largest portfolio of greenfield projects, potentially translating into robust returns in the long term

However, large CapEx requirements in coming decade…

… restrain near‐term shareholder returns to the 3% dividend yield, one of the lowest among peers

Gazprom (TP $9/GDR) – World’s cheapest energy name, for good cause

World's cheapest energy name (2014e P/E of 3.4x) reflects poor ROI

Stock value is worth Gazprom's future dividend stream

Dividend yield, currently 5%, will be among highest of peers, once management approves the 35% IFRS dividend payout (9% vs 5%)

However, vast number of expansion projects will absorb most FCF…

… and earnings growth will contribute little to valuation

Surgutneftegas pref (TP Rb24/share) – Falling FCF to underscore prefs’ relative attractiveness

The highest, most stable and defensive dividend among sector peers;

Preferreds' dividend favored over commons' on higher (9% vs 2%), more stable payout…

… potentially leading to a narrower preferred‐common spread (15% today, down from 49% three years ago)

Russian Oil & Gas

9

Sell

Surgutneftegas (TP $8.50/GDR) – Falling FCF to underscore prefs’ relative attractiveness

Common share dividend payout pressured by negative FCF during 2014‐16…

… due to limited upside from crude production and rising CapEx

Preferreds' dividend favored over commons' on higher (9% vs 2%), more stable payout…

… potentially leading to a narrower preferred‐common spread (15% today, down from 49% three years ago)

Conservative use of $32bn 'war chest' not value‐accretive to shareholders; M&A/greenfield development could generate 3‐fold the return

Tatneft (TP $40/GDR) – Premium unjustified

Robust upstream FCF ($16/bbl vs Rosneft's $14/bbl, Lukoil's $15/bbl)…

… is not translating into attractive shareholder returns:

o 30% RAS payout implies one of lowest dividend yields (4%), zero EPS growth;

o Uninspiring investment returns on Taneco refinery – Taneco upgrade/ expansion is estimated to cost c30% more than average, and bitumen reserves development, whose scale/profitability is uncertain;

Valuation premium to peers is unsustainable, in our view, taking into account some other companies' superior shareholder returns

Alliance Oil (TP SEK 41/share) – Risk‐reward skewed to the downside

Risk of consensus earnings downgrade – consensus too bullish…

… BCS 2013‐15e EPS forecast is 15% below consensus; BCS 2012‐15e EPS CAGR estimate of 1% compares to consensus' 4%

Delay in the refinery’s commercial start and connection to ESPO until 2H14 is equivalent to c$150mn of foregone EBITDA

Robust FCF once upgraded refinery is operational and connection to ESPO could fully deleverage the balance sheet by 2018…

… but search for further production growth will require significant investment, thus putting pressure on near‐term shareholder returns

Current valuation (4.4x EV/EBITDA '14e) is inflated by speculation over a potential takeover by Rosneft (25 July, Vedomosti) and is not fundamentally justified

Transneft pref (TP Rb75,000/share) – Risk‐reward not worth the gamble

Robust FCF – $10bn during 2013‐15 – is encouraging hope in higher dividends

Preferred share price aggressive, assumes 2013e IFRS payout of 20% (vs 3% in 2012)

Risk‐reward unattractive:

o potential downside (82%) (no change in dividend policy)

o exceeds upside (53%) (35% IFRS payout)

No guarantee holders of preferred shares will benefit from IFRS‐based payout, since the charter does not stipulate that the dividend paid on preferred shares (10% RAS net income) be at the level paid on commons

Russian Oil & Gas

10

Stock picking in a challenging sector

Pressure on the budget leads to sector instability. In our sector initiation report, Russian Oil & Gas: Greenfields – key to profitability and stability (1 August), we concluded that Russian federal budget revenues, half of which come from the oil & gas sector, face significant downside risks in coming years and that the government will likely look for ways to compensate for any shortfall. The government’s actions in the past month proved our point:

Next year’s freeze in gas tariffs should save consumers over $2bn pa;

The crude oil tax reshuffle has hit refining‐heavy companies and should generate

over $2.5bn pa of extra revenues for the government.

According to our analysis, the government will still be at least c$10bn short of current tax inflows by the end of the decade. A tax increase is the most efficient tool to address this problem. Given numerous projects which, assuming a stable macro environment, will generate substantial returns (in excess of 30% IRR), especially in the refining and gas sectors, additional tax hikes in the coming years are highly likely.

Upstream companies with multiple greenfields are investors’ best long‐term play. Such regulatory risks, i.e., risks of unexpected tax hikes, tariff growth deceleration and so on, are the primary factors that prevent global energy investors from investing long term in the Russian oil & gas sector, as we found out during our two‐week roadshow in September among global equity fund managers (refer to the feedback from the meetings Russian Oil & Gas: What YOU think of the sector, 25 September). Indeed, last year’s gas MET saga is still fresh in the minds of the many investors who lost millions of dollars on the stocks’ volatility.

We do not expect regulatory risks to be any lower going forward. On the contrary, the more acute the issue with budget revenues becomes, the higher the taxation risks are going to be. Having analyzed the returns of each oil & gas subsector and every major project, we have concluded that investors’ safest long‐term bet are companies with large exposure to upstream (already heavily taxed) and with the largest amount of greenfields (minimum investment returns guaranteed). These companies are Gazprom Neft, Lukoil and Rosneft.

Dividends – a bird in hand is worth two in the bush. Monetization of the value of upstream greenfields, for which the new tax regulation guarantees a minimum return rate, is, in most cases, too far off. On a shorter horizon, investors are better off with opportunistic dividend plays, we think. These are Bashneft, Gazprom and Lukoil.

Bashneft: the new dividend king. Unlike peers undergoing a major CapEx cycle and investing in future growth, Bashneft is already enjoying rising output, lower OpEx and CapEx and, therefore, will continue churning healthy FCF. The company has moderate leverage and hence could distribute most of its FCF as dividends as per its dividend policy. We estimate that investors could receive a third of its market cap in the next three years by investing in preferred shares. This makes Bashneft the highest dividend paying oil & gas stock in Russia.

Gazprom: the 35% IFRS payout creates an attractive bull case. State‐owned companies are to pay 35% of IFRS net income as dividends starting from 2016, based on the government’s recent resolution. If confirmed by Gazprom, this would have major valuation implications, since consensus dividend expectations are the major driver for the company’s shares. Based on a dividend discount model, adoption of a higher dividend payout would translate into an additional $3/GDR of value, or a third of the current share price.

Lukoil: highly committed to dividend growth. In pursuing market cap growth, management has chosen the most efficient tool to achieve its goals. Lukoil has posted the highest dividend growth in the last three years (20% CAGR) and plans to maintain such pace going forward. Unlike its peers, Lukoil has passed the bottom of the CapEx cycle and starting from next year should see the fruit of past investments. Its FCF profile adds significant credibility to management’s ambitious dividend growth target (15% pa).

Investors’ safest long‐term play is oil companies with high exposure to upstream and greenfields

Source: BCS

Gazprom minorities are primary beneficiaries of the 35% dividend payout requirement

Source: FactSet, BCS

Greenfield exposure

Upstream exposure

Gazprom Neft

Rosneft

BashneftLukoil

Tatneft

Alliance Oil

SurgutNG

6.7%

3.5%

0.8%

Gazprom Rosneft Transneft (pref)

35% IFRS

25% IFRS

9.3%

4.9%

Russian Oil & Gas

11

Bashneft – the major with unparalleled dividends O&G companies nearly trebled dividend payments since 2008

Source: Company data, FactSet, BCS

Three momentum plays, or stocks to avoid on short side of a pair trade in near term:

Novatek: news flow de‐risking Yamal LNG. The project is awaiting new partner(s), pre‐sale of LNG volumes and FID. Yamal LNG is long‐term, complicated and capital‐intensive; however, in the short term, the Novatek stock offers an attractive play on catalysts, which in the past have proved to drive the share price. Moreover, Novatek is very likely to beat its FY13 output guidance as Gazprom’s continuously rising gas exports have created a window of opportunity for independent gas producers on the domestic market.

Lukoil: oil price stabilization and West Qurna‐2 launch. The stock was the worst performer during the late oil price rally despite in‐line performance in previous years. This underperformance and the company’s low sensitivity to oil price changes make the stock one of the most defensive instruments for withstanding oil price stabilization. Moreover, successful delivery of West Qurna‐2 in November should lift most investors’ concerns, de‐risk c$3bn of next year’s FCF and add credibility to the continued increase in dividends.

Gazprom: dividend discussions, robust gas sales and the pending agreement with China. In the short term, Gazprom is the best exposure to the dividend payout increase imposed by the government. Moreover, the company will continue enjoying rising gas exports to Europe. This has limited valuation implications, but it should improve sentiment towards the stock. Finally, the long‐awaited agreement to supply profitable gas volumes to China is just around the corner.

Maximizing returns and hedging risks with pair trades. Although there is not much upside across the sector, the range between the highest upside and downside is still significant to generate returns on the long‐short trades, we believe.

Short‐term pair trades: Playing the momentum themes and catalysts

Lukoil vs Rosneft

o Anticipating the oil price stabilization. The oil price seems to have traded ahead of fundamentals: the excess supply of oil from the non‐OPEC members is significant and the fears of the Syrian crisis escalating to the nearby countries are easing. Falling crude price traditionally accompanied by a similar move in oil companies’ shares will draw investor interest to more defensive names. Rosneft’s high leverage has made the company one of the most sensitive to oil price changes and, therefore, ill‐suited to hide in from the declining oil price.

o Lukoil: The launch of the long‐awaited West Qurna‐2 in November should de‐risk up to 10% of the company’s value. As we have discussed in Lukoil: Approaching the turning point (10 September), the Iraqi operations will contribute up to $3bn of FCF next year in the form of the historical cost recovery, which the market does not have in its forecasts yet.

o Rosneft: Value implications from the corporate activity are overblown. The company has pulled many rabbits out of its hat in the last year, but the contribution to the shareholder value has been neutral, we estimate. Given

30%

22%20%

18%17% 16%

11%

8%7%

5%

2%

0%

5%

10%

15%

20%

25%

30%Bashneft

(pref)

SurgutNG

(pref)

Bashneft

Gazprom

Lukoil

Gazprom

Neft

Tatneft

Rosneft

Novatek

SurgutNG

Transneft

(pref)

2015e 2014e 2013e

5.4

7.0 7.66.3 6.7

9.6

16.4

13.9

15.8

19.1

16.6

0

5

10

15

20

2005 2006 2007 2008 2009 2010 2011 2012 2013e 2014e 2015e

$bn TNK‐BP Russian O&G (ex‐TNK‐BP)

Pick defensive stocks as the oil price stabilizes*

* Sensitivity to the $10/bbl oil price decline

Source: FactSet, BCS

‐8%

‐4%

‐5%

‐5%

‐2%

‐3%

‐2%

2%

3%

‐12%

‐9%

‐7%

‐5%

‐4%

‐4%

‐2%

2%

5%

‐15% ‐10% ‐5% 0% 5%

Gazprom

Rosneft

Tatneft

SurgutNG

Lukoil

Novatek

GazpromNeft

Bashneft

Alliance Oil

Net income EBITDA

Russian Oil & Gas

12

Rosneft’s scale, any future acquisitions or resource base expansion, new contracts with customers or strategic alliances will have little value implications and should not trigger re‐rating of shares.

Gazprom Neft vs Surgutneftegas

o Valuation does not match shareholder returns. Gazprom Neft is trading at a 25% discount to Surgutneftegas despite the superior dividend yield (6% vs 2%) and growth (‐6% EPS CAGR 2013‐15 vs ‐21%).

o Exposure to ruble is not a differentiating factor. Both companies are equally better off from weaker ruble. Although Surgutneftegas’ bottom line enjoys the FX gain contribution, it does not translate into additional FCF and the dividend uplift is insignificant given the common shares’ modest yield.

o Exposure to the greenfield tax regulation (to come into effect in January) is the key profitability driver, in our view. Among Russian oil producers, Gazprom Neft has one of the largest portfolios of greenfield projects that is still not appreciated by the investor community. The value of tax savings under the proposed greenfield legislation is worth $3/GDR for Gazprom Neft, or 14% of its current value, we estimate. Surgutneftegas, in turn, has the smallest amount of greenfields.

Alliance Oil (pref) vs Alliance Oil

o Guaranteed income vs corporate risk. Even though preferred shares may have limited share price appreciation potential, the instrument generates a stable 10% annualized return paid quarterly. Common shares, which have traded up in the last two months on the unconfirmed speculation over the takeover by Rosneft (Vedomosti, 25 July), are susceptible to all company‐specific risks of which, in Alliance Oil’s case, there are many (refinery launch delay, M&A).

Long‐term pair trades: It is all about returns

Lukoil vs Rosneft

o Higher shareholder returns. Lukoil shareholders will benefit in the short term from the company’s exposure to profitable greenfields (Caspian fields, Uzbekistan ramp‐up, West Qurna‐2 launch, the start of Imilor, etc). Lukoil’s production growth until 2015 is 4% pa, on average, vs Rosneft’s 1%, and the cumulative dividend is almost twice higher.

o Lukoil: Aligned interests. Lukoil’s management is committed to market value growth and has wisely chosen the most effective instrument to achieve its goal – the dividend. Purchase of shares by management also contributes to the positive sentiment. Whatever management’s motivation, the key point is that minorities’ interests are closely aligned with those of management.

o Rosneft: Scale comes at a price. Rosneft carries the primary responsibility for the Russian oil industry. The company has the largest portfolio of greenfields, but will require billions of dollars to finance the development. To ensure continuous oil production, Rosneft may accelerate the development of its projects and look for ways to expand the resource base. Thus, the company may find itself in a permanent CapEx cycle with shareholder interest taking the backseat.

Novatek vs Gazprom

o Investment return differential. Gazprom’s ROE averaged 17% during 2010‐12 vs Novatek’s 30%. Going forward, the difference may widen further as Gazprom proceeds with the capital‐intensive Eastern Gas Program, South Stream and Nord Stream expansion, all of which are NPV‐negative or value‐neutral at best, we estimate. Novatek’s approach to investing is more disciplined with the projects’ IRR above 30%.

o Gazprom: Subject to higher tax risk. Searching for alternative tax revenue sources, the government may, as it has already proved so several times, hike taxes on the most profitable sectors and companies. Gazprom is generating robust profitability on export sales of gas and liquids and is enjoying solid

Russian Oil & Gas

13

balance sheet (0.5x net debt / EBITDA). While the government is attempting to make the tax mechanism more transparent, additional ad hoc taxation is possible if necessary, and Gazprom will remain its primary target, we believe.

o Novatek: Attractive risk‐reward. Most of the risks that dominated sentiment around Novatek in the last year seem to have materialized and been priced in (slowed gas tariff growth, higher taxes and Rosneft’s emergence as a gas giant). The company’s bull case includes steeper ramp‐up of profitable liquids sales (condensate and refined products), domestic customer base expansion via acquisition of regional gas marketers, infrastructure and existing producing assets and taking advantage of Gazprom’s expiring agreements.

Gazprom vs Transneft (pref)

o Exposure to the dividend payout increase. Both companies are subject to the government’s request to increase the dividend payout to 35% IFRS from 2016. Gazprom’s potential yield could nearly double to 9%. Implications for Transneft (pref) holders are not straightforward: unless management guarantees (though is not required to) a similar dividend for both classes of shares, the risk of the dividend uplift being absorbed solely by the common shares is high.

o Gazprom: a dividend play. As we have already discussed, Gazprom is one of the best exposures to the dividend increase. Not just its dividend would be the highest among Russian O&G companies, but also its share price highly correlated with consensus dividend expectations could see significant re‐rating (by 30%, we estimate).

o Transneft (pref): Dividend increase is not carved in stone. The company stated on numerous occasions that it has no intention of benefiting its minority shareholders, i.e., holders of preferred shares, via higher dividends. The company has no legal obligation to guarantee a similar dividend for both classes of shares and therefore could award the entire dividend increase to the government, i.e., the holder of all common shares. Such scenario is even more likely in light of the growing budget deficit, a problem which will become more acute after 2015 as O&G tax revenues start declining, on our estimates.

Misperceived high‐risk stocks. Finally, there are three investment stories that we advise to avoid due to absence of clarity on future development and, therefore, high associated risks.

Transneft (pref): Dividends, the shares’ sole driver, are at risk. The charter outlines the 10% RAS dividend payout on preferred shares and does not require dividends for two classes of shares to be equal. Once the company adopts the IFRS payout, management will have full discretion to allocate the dividend increase among the commons and preferreds. In the absence of any incentive to benefit holders of preferred shares, management may award the dividend increase to the government, the sole owner of the common shares.

Alliance Oil: Valuation ignores execution risks. Alliance Oil is yet to disappoint with the delayed launch of the refinery and the subsequent consensus’ forecast downgrade. The current asset portfolio does not ensure sustainable production, nor does it benefit the company in the ongoing sector transformation (tax burden shift from upstream to downstream). This raises M&A and execution risks, which the company has not scored well on in the past.

Tatneft: Lowest shareholder returns. The company could have been the FCF generation benchmark among Russian O&G companies, were it not for its costly Taneco refinery. The robust FCF witnessed over the past year is at its dawn as management proceeds with the Taneco expansion and upgrade. On our estimates, the refinery’s break‐even costs (including investments made in the past) are $22/bbl vs the average Russian refining margin of $9/bbl ($14/bbl after the upgrade).

Russian Oil & Gas

14

Lukoil – Financial and Operational Summary

Source: Company data, FactSet, BCS

Key price assumptions 2010 2011 2012 2013e 2014e 2015e Market statistics

Crude oil ($/bbl) Share Price ($) 64.00

Brent 80 111 112 108 103 97 Market Cap ($mn) 48,311

Urals 77 109 110 107 102 97 EV ($mn) 55,077

Domestic (Samara) 36 49 50 49 48 47

Crack spreads ($/bbl) Income Statement ($mn) 2010 2011 2012 2013e 2014e 2015e

Gasoline 16 17 23 21 20 21 Revenue 104,956 133,650 139,171 140,947 143,055 139,885

Diesel 12 17 19 18 16 16 Opex -7,969 -9,055 -9,359 -10,030 -9,820 -9,944

Jet fuel 15 22 23 22 21 21 Purchased oil -43,579 -59,694 -64,148 -65,751 -64,628 -61,785

Fuel oil -21 -30 -26 -32 -30 -26 Taxes other than income tax -8,978 -12,918 -13,666 -14,017 -14,050 -14,296

Gas, domestic Excise and export duties -18,878 -22,217 -22,836 -22,074 -20,573 -20,418

$/mcm 82 98 99 110 116 118 Other operating costs -9,865 -12,138 -10,260 -10,377 -10,597 -11,209

$/mcf 2.3 2.8 2.8 3.1 3.3 3.3 EBITDA 15,687 17,628 18,902 18,698 23,387 22,231

Depreciation 4,154 4,473 4,832 5,966 12,043 11,265

Macro assumptions 2010 2011 2012 2013e 2014e 2015e Operating income 11,533 13,155 14,070 12,732 11,344 10,967

USD/RUB 30.36 29.39 31.04 31.81 32.60 32.90 Finance expenses -538 -483 -281 -223 -371 -302

CPI 8.2% 6.0% 6.0% 6.1% 5.0% 5.0% Other expense/income 475 447 -66 418 519 556

Pre-tax income 11,470 13,119 13,723 12,928 11,493 11,221

Production 2010 2011 2012 2013e 2014e 2015e Income taxes -2,351 -3,293 -2,798 -3,080 -2,643 -2,581

Crude oil Minority interest/other -113 531 79 23 23 23

annual output (mmt) 96 91 90 91 93 97 Net income 9,006 10,357 11,004 9,870 8,873 8,663

daily output (kbd) 1,920 1,821 1,790 1,813 1,858 1,934 Fully diluted EPS ($) 10.94 12.96 14.09 12.64 11.36 11.09

Refined products

annual output (mmt) 64 63 64 62 62 62 Balance sheet ($mn) 2010 2011 2012 2013e 2014e 2015e

daily output (kbd) 1,272 1,253 1,272 1,243 1,244 1,244 Cash 2,368 2,753 2,914 3,167 3,167 3,167

light product yield 69% 69% 73% 73% 73% 76% Inventories 6,231 7,533 8,098 8,082 8,064 8,133

Gas (bcm) 18.6 18.6 19.9 20.5 20.8 24.2 Accounts receivable 8,219 8,921 8,667 9,243 9,013 9,126

Other current assets 3,799 4,322 4,594 3,799 3,799 3,799

Reserves (SEC) Total current assets 20,617 23,529 24,273 24,291 24,042 24,225

1P 2P 1P+2P 3P 1P+2P+3P Fixed assets 54,629 56,803 66,883 79,164 83,335 88,927

Oil (bn bbl) 13.4 5.9 19.3 3.7 23.0 Other non-current assets 8,771 10,860 7,805 7,895 7,895 7,895

Gas (bcm) 665 304 969 101 1,070 Total non-current assets 63,400 67,663 74,688 87,059 91,230 96,822

Total (bn boe) 17.3 7.7 25.0 4.3 29.3 Total assets 84,017 91,192 98,961 111,350 115,273 121,048

EV/Reserves ($/boe) 3.2 2.2 1.9 Short-term debt 2,125 1,792 658 1,751 0 1,012

Reserve life (years) 22 32 37 Accounts payable 5,607 5,995 7,263 8,168 7,691 7,757

Other current liabilities 3,043 3,321 4,532 5,326 5,326 5,326

Financial ratios 2010 2011 2012 2013e 2014e 2015e Total current liabilities 10,775 11,108 12,453 15,245 13,017 14,095

Valuation Long-term debt 9,069 7,300 5,963 8,774 8,532 7,344

P/E (x) 5.4 4.7 4.4 4.9 5.4 5.6 Other non-current liabilities 4,976 5,146 7,338 7,851 7,828 7,805

PEG (x) 18.9 31.1 70.3 NM NM NM Total non-current liabilities 14,045 12,446 13,301 16,625 16,360 15,149

P/B (x) 0.8 0.8 0.7 0.6 0.6 0.5 Total shareholders' equity 59,197 67,638 73,207 79,480 85,896 91,803

EV/EBITDA (x) 3.5 3.1 2.9 2.9 2.4 2.5 Total liabilities and equity 84,017 91,192 98,961 111,350 115,273 121,048

EV/DACF (x) 3.6 3.1 3.2 3.4 2.5 2.7

Dividend yield (%) 3.0% 4.0% 4.5% 5.1% 5.7% 6.5% Cash flow statement ($mn) 2010 2011 2012 2013e 2014e 2015e

FCF Yield (%) 14.6% 15.4% 16.1% 4.7% 9.3% 6.1% Net income 9,006 10,357 11,004 9,870 8,873 8,663

Profitability Depreciation 4,154 4,473 4,832 5,966 12,043 11,265

EBITDA Margin (%) 15% 13% 14% 13% 16% 16% Changes in working capital -826 -1,529 2,474 440 -229 -117

EBIT Margin (%) 11% 10% 10% 9% 8% 8% Other 1,207 2,213 687 62 0 0

Net Margin (%) 9% 8% 8% 7% 6% 6% Operating cash flow 13,541 15,514 18,997 16,338 20,687 19,811

Leverage Capex -6,468 -8,093 -11,235 -14,091 -16,215 -16,857

Gross Debt/Equity (x) 0.2 0.1 0.1 0.1 0.1 0.1 Acquisitions -813 -2,655 -1,060 -2,435 0 0

Net Debt/Equity (x) 0.1 0.1 0.0 0.1 0.1 0.1 Other -15 -25 -921 -849 0 0

Gross Debt/EBITDA (x) 0.7 0.5 0.4 0.6 0.4 0.4 Investing cash flow -7,296 -10,773 -13,216 -17,375 -16,215 -16,857

Net Debt/EBITDA (x) 0.6 0.4 0.2 0.4 0.2 0.2 Change in debt 35 -2,004 -1,266 3,902 -1,993 -175

Net Interest Cover (x) 21.4 27.2 50.1 57.2 30.6 36.3 Dividends -1,556 -1,830 -2,913 -2,532 -2,456 -2,756

Returns Other -4,625 -2,189 -1,501 -21 -23 -23

ROE (%) 16% 16% 16% 13% 11% 10% Financing cash flow -6,146 -6,023 -5,680 1,349 -4,473 -2,954

ROACE (%) 14% 14% 15% 12% 10% 9% Effect of Forex -5 -93 60 -59 0 0

ROA (%) 11% 12% 12% 9% 8% 7% Increase (decrease) in cash flow 94 -1,375 161 253 0 0

Russian Oil & Gas

15

Gazprom Neft – Financial and Operational Summary

Source: Company data, FactSet, BCS

Key price assumptions 2010 2011 2012 2013e 2014e 2015e Market statistics

Crude oil ($/bbl) Share Price ($) 22.32

Brent 80 111 112 108 103 97 Market Cap ($mn) 21,061

Urals 77 109 110 107 102 97 EV ($mn) 25,815

Domestic (Samara) 36 49 50 49 48 47

Crack spreads ($/bbl) Income Statement ($mn) 2010 2011 2012 2013e 2014e 2015e

Gasoline 16 17 23 21 20 21 Revenue 32,772 44,172 48,818 44,565 43,628 42,686

Diesel 12 17 19 18 16 16 Opex -2,111 -2,464 -3,974 -4,623 -4,823 -4,844

Jet fuel 15 22 23 22 21 21 Purchased oil -7,459 -10,817 -13,869 -9,552 -8,604 -8,519

Fuel oil -21 -30 -26 -32 -30 -26 Taxes other than income tax -5,240 -8,038 -8,090 -9,580 -9,365 -8,931

Gas, domestic Excise and export duties -6,631 -8,092 -9,240 -7,009 -6,761 -6,968

$/mcm 82 98 99 110 116 118 Other operating costs -5,054 -5,819 -5,415 -5,217 -5,244 -5,385

$/mcf 2.3 2.8 2.8 3.1 3.3 3.3 EBITDA 6,277 8,942 8,230 8,583 8,831 8,039

Depreciation 1,619 1,963 1,883 2,364 2,355 2,350

Macro assumptions 2010 2011 2012 2013e 2014e 2015e Operating income 4,658 6,979 6,347 6,219 6,476 5,688

USD/RUB 30.36 29.39 31.04 31.81 32.60 32.90 Finance expenses -288 -263 -257 -200 -199 -194

CPI 8.2% 6.0% 6.0% 6.1% 5.0% 5.0% Other expense/income -93 115 942 45 27 27

Pre-tax income 4,277 6,831 7,031 6,064 6,305 5,521

Production 2010 2011 2012 2013e 2014e 2015e Income taxes -844 -1,244 -1,155 -1,118 -1,268 -1,111

Crude oil Minority interest/other -285 -235 -253 -210 -219 -191

annual output (mmt) 50 50 51 50 53 53 Net income 3,148 5,352 5,623 4,736 4,818 4,219

daily output (kbd) 1,003 1,009 1,017 1,001 1,051 1,062 Fully diluted EPS ($) 3.34 5.67 5.96 5.02 5.11 4.47

Refined products

annual output (mmt) 38 41 44 44 43 43 Balance sheet ($mn) 2010 2011 2012 2013e 2014e 2015e

daily output (kbd) 754 824 884 871 865 863 Cash 1,146 914 2,488 3,002 3,567 3,533

light product yield 64% 61% 62% 63% 63% 63% Inventories 1,862 2,343 2,890 2,537 2,307 2,355

Gas (bcm) 4.0 8.7 11.3 14.3 15.1 16.8 Accounts receivable 2,566 3,562 2,180 2,175 2,180 2,160

Other current assets 1,519 2,252 4,344 4,269 4,269 4,269

Reserves (PRMS) Total current assets 7,093 9,071 11,902 11,983 12,323 12,317

1P 2P 1P+2P 3P 1P+2P+3P Fixed assets 15,914 19,313 21,914 27,201 30,716 33,460

Total (bn boe) 8.3 5.9 14.2 5.3 19.5 Other non-current assets 9,057 8,299 8,744 6,336 6,381 6,424

EV/Reserves ($/bbl) 3.1 1.8 1.3 Total non-current assets 24,971 27,612 30,657 33,537 37,097 39,883

Reserve life (years) 19 32 44 Total assets 32,064 36,683 42,560 45,520 49,421 52,200

Short-term debt 1,694 1,277 2,167 2,356 2,632 2,168

Financial ratios 2010 2011 2012 2013e 2014e 2015e Accounts payable 2,730 3,075 2,942 4,308 4,058 4,110

Valuation Other current liabilities 427 65 1,249 1,002 1,002 1,002

P/E (x) 6.7 3.9 3.7 4.4 4.4 5.0 Total current liabilities 4,851 4,417 6,358 7,666 7,692 7,280

PEG (x) 149.3 5.6 73.8 NM 251.2 NM Long-term debt 4,942 5,420 5,448 6,379 6,379 6,379

P/B (x) 1.2 1.0 0.8 0.8 0.7 0.6 Other non-current liabilities 3,584 3,334 3,423 4,168 4,387 4,580

EV/EBITDA (x) 4.1 2.9 3.1 3.0 2.9 3.2 Total non-current liabilities 8,526 8,754 8,871 10,547 10,766 10,959

EV/DACF (x) 4.7 3.0 3.2 3.4 3.2 3.0 Total shareholders' equity 18,687 23,512 27,330 27,307 30,963 33,996

Dividend yield (%) 3.3% 5.6% 6.7% 5.7% 5.8% 5.1% Total liabilities and equity 32,064 36,683 42,560 45,520 49,421 52,235

FCF Yield (%) 11.3% 6.2% 8.4% 8.2% 5.1% 8.7%

Profitability Cash flow statement ($mn) 2010 2011 2012 2013e 2014e 2015e

EBITDA Margin (%) 19% 20% 17% 19% 20% 19% Net income 3,433 5,587 5,877 4,946 5,037 4,410

EBIT Margin (%) 14% 16% 13% 14% 15% 13% Depreciation 1,619 1,963 1,883 2,364 2,355 2,350

Net Margin (%) 10% 12% 12% 11% 11% 10% Changes in working capital 247 -2,359 -296 203 -25 25

Leverage Other 93 810 -76 180 614 1,577

Gross Debt/Equity (x) 0.4 0.3 0.3 0.3 0.3 0.3 Operating cash flow 5,392 6,001 7,388 7,693 7,981 8,362

Net Debt/Equity (x) 0.3 0.2 0.2 0.2 0.1 0.1 Capex -3,292 -4,029 -5,019 -5,702 -7,094 -6,714

Gross Debt/EBITDA (x) 1.1 0.7 0.9 1.0 1.0 1.1 Acquisitions -1,536 -1,156 -146 -10 0 0

Net Debt/EBITDA (x) 0.9 0.6 0.6 0.5 0.5 0.5 Other -24 -289 -203 -411 0 0

Net Interest Cover (x) 16.2 26.5 24.7 31.1 32.6 29.3 Investing cash flow -4,852 -5,474 -5,368 -6,122 -7,094 -6,714

Returns Change in debt 419 273 819 940 276 -464

ROE (%) 18% 25% 22% 17% 17% 13% Dividends -728 -1,025 0 -1,442 -1,196 -1,217

ROACE (%) 16% 21% 17% 16% 15% 12% Other 0 0 -1,206 -94 0 0

ROA (%) 10% 16% 14% 11% 10% 8% Financing cash flow -309 -752 -387 -596 -921 -1,681

Effect of Forex 47 -7 -60 104 0 0

Increase (decrease) in cash flow 278 -232 1,574 1,079 -34 -33

Russian Oil & Gas

16

Bashneft – Financial and Operational Summary

Source: Company data, FactSet, BCS

Key price assumptions 2010 2011 2012 2013e 2014e 2015e Market statistics

Crude oil ($/bbl) Share Price (ords) ($/share) 58.53

Brent 80 111 112 108 103 97 Share Price (prefs) ($/share) 40.43

Urals 77 109 110 107 102 97 Market Cap ($mn) 11,045

Domestic (Samara) 36 49 50 49 48 47 EV ($mn) 14,802

Crack spreads ($/bbl)

Gasoline 16 17 23 21 20 21 Income Statement ($mn) 2010 2011 2012 2013e 2014e 2015e

Diesel 12 17 19 18 16 16 Revenue 13,341 16,549 17,155 17,120 16,574 16,160

Jet fuel 15 22 23 22 21 21 Opex -2,665 -1,684 -1,728 -1,750 -1,702 -1,697

Fuel oil -21 -30 -26 -32 -30 -26 Purchased oil -2,882 -3,994 -4,022 -3,781 -3,588 -3,525

Taxes other than income tax -1,421 -2,052 -2,149 -2,204 -2,131 -2,073

Macro assumptions 2010 2011 2012 2013e 2014e 2015e Excise and export duties -2,753 -4,231 -4,649 -4,917 -4,663 -4,593

USD/RUB 30.36 29.39 31.04 31.81 32.60 32.90 Other operating costs -1,116 -1,396 -1,427 -1,437 -1,428 -1,453

CPI 8.2% 6.0% 6.0% 6.1% 5.0% 5.0% EBITDA 2,504 3,192 3,179 3,030 3,061 2,818

Depreciation 711 616 592 593 633 670

Production 2010 2011 2012 2013e 2014e 2015e Operating income 1,793 2,576 2,587 2,437 2,429 2,148

Crude oil Finance expenses -290 -434 -228 -175 -298 -220

annual output (mmt) 14.1 15.1 15.4 15.6 15.7 15.7 Other expense/income 34 62 -8 -24 32 137

daily output (kbd) 283 302 309 311 314 314 Pre-tax income 1,537 2,204 2,351 2,239 2,162 2,065

Refined products Income taxes -468 -513 -529 -474 -432 -413

annual output (mmt) 19.4 19.2 18.9 19.2 19.0 19.0 Minority interest/dividends -116 5 -144 -12 -14 -13

daily output (kbd) 389 384 378 384 380 380 Net income 953 1,696 1,678 1,753 1,716 1,639

light product yield 64% 64% 64% 64% 65% 67% Fully diluted EPS ($) 4.65 8.28 7.77 7.71 7.55 7.21

Reserves (PRMS) Balance sheet ($mn) 2010 2011 2012 2013e 2014e 2015e

1P 2P 1P+2P 3P 1P+2P+3P Cash 1,067 881 658 40 248 216

Oil (bn bbl) 2.0 0.5 2.5 0.7 3.2 Inventories 625 748 780 825 739 749

EV/Reserves ($/bbl) 7.4 5.8 4.6 Accounts receivable 1,208 1,395 1,666 1,599 1,571 1,571

Reserve life (years) 18 22 28 Other current assets 852 1,245 876 800 800 800

Total current assets 3,752 4,269 3,981 3,265 3,359 3,336

Financial ratios 2010 2011 2012 2013e 2014e 2015e Fixed assets 9,552 7,882 9,073 9,253 9,817 10,362

Valuation Other non-current assets 1,687 1,422 2,120 2,478 2,936 3,277

P/E (x) 11.6 6.5 6.6 6.3 6.4 6.7 Total non-current assets 11,239 9,304 11,192 11,731 12,753 13,639

PEG (x) 9.1 8.4 NM 140.9 NM NM Total assets 14,991 13,573 15,173 14,996 16,111 16,975

P/B (x) 2.1 2.0 1.6 1.4 1.3 1.1 Short-term debt 795 420 1,048 455 455 455

EV/EBITDA (x) 5.9 4.6 4.7 4.9 4.8 5.3 Accounts payable 1,071 1,242 1,308 1,538 1,239 1,255

EV/DACF (x) 7.0 5.5 6.8 7.1 6.5 6.5 Other current liabilities 650 632 487 227 227 227

Dividend yield (ords) (%) 13.3% 5.8% 1.4% 8.0% 6.0% 6.2% Total current liabilities 2,516 2,294 2,842 2,220 1,921 1,937

Dividend yield (prefs) (%) 19.2% 8.3% 2.0% 11.6% 8.8% 9.0% Long-term debt 3,118 2,965 2,560 3,281 2,981 2,981

FCF Yield (%) 13.0% 14.9% 12.8% 11.3% 10.2% 8.8% Other non-current liabilities 4,082 2,704 1,817 1,705 1,719 1,732

Profitability Total non-current liabilities 7,200 5,669 4,377 4,986 4,700 4,713

EBITDA Margin (%) 19% 19% 19% 18% 18% 17% Total shareholders' equity 5,275 5,610 7,954 7,790 9,490 10,324

EBIT Margin (%) 13% 16% 15% 14% 15% 13% Total liabilities and equity 14,991 13,573 15,173 14,996 16,111 16,975

Net Margin (%) 7% 10% 10% 10% 10% 10%

Leverage Cash flow statement ($mn) 2010 2011 2012 2013e 2014e 2015e

Gross Debt/Equity (x) 0.7 0.6 0.5 0.5 0.4 0.3 Net income 953 1,696 1,678 1,753 1,716 1,639

Net Debt/Equity (x) 0.4 0.3 0.3 0.4 0.3 0.3 Depreciation 711 655 592 593 633 670

Gross Debt/EBITDA (x) 1.6 1.1 1.1 1.2 1.1 1.2 Changes in working capital -531 -264 -101 -427 -184 6

Net Debt/EBITDA (x) 0.9 0.4 0.7 1.0 0.9 0.9 Other 267 141 135 96 -21 -126

Returns Operating cash flow 1,400 2,228 2,304 2,015 2,144 2,189

ROE (%) 18% 31% 25% 22% 20% 17% Capex -492 -851 -992 -1,192 -1,197 -1,215

ROACE (%) 19% 27% 23% 18% 17% 13% Acquisitions -939 - -282 -29 - -

ROA (%) 7% 12% 12% 12% 11% 10% Other -564 -157 12 -99 - -

Investing cash flow -1,995 -1,008 -1,262 -1,319 -1,197 -1,215

Change in debt 2,145 -401 52 365 -300 -

Dividends -1,314 -950 -591 -1,229 -15 -805

Other -343 -32 -731 -464 -423 -202

Financing cash flow 488 -1,383 -1,270 -1,329 -738 -1,007

Effect of Forex 8 -23 5 15 - -

Increase (decrease) in cash flow -99 -186 -223 -618 209 -33

Russian Oil & Gas

17

Novatek – Financial and Operational Summary

Source: Company data, FactSet, BCS

Key price assumptions 2010 2011 2012 2013e 2014e 2015e Market statistics

Crude oil ($/bbl) Share Price ($) 135.00

Brent 80 111 112 108 103 97 Market Cap ($mn) 40,948

Urals 77 109 110 107 102 97 EV ($mn) 44,888

Domestic (Samara) 36 49 50 49 48 47

Gas, domestic Income Statement ($mn) 2010 2011 2012 2013e 2014e 2015e

$/mcm 82 98 99 110 116 118 Revenue 3,911 5,999 6,801 9,612 11,091 11,782

$/mcf 2.3 2.8 2.8 3.1 3.3 3.3 Transportation -1,225 -1,639 -1,960 -3,317 -3,357 -3,624

Taxes other than income tax -332 -597 -543 -686 -1,088 -1,281

Macro assumptions 2010 2011 2012 2013e 2014e 2015e Other operating costs -482 -771 -1,189 -1,567 -2,115 -2,590

USD/RUB 30.36 29.39 31.04 31.81 32.60 32.90 EBITDA 1,872 2,992 3,109 4,042 4,531 4,286

CPI 8.2% 6.0% 6.0% 6.1% 5.0% 5.0% Depreciation 218 316 360 405 475 579

Operating income 1,655 2,676 2,749 3,637 4,056 3,707

Production 2010 2011 2012 2013e 2014e 2015e Finance expenses 5 42 -48 -98 -53 -19

Gas (bcm) Other expense/income 23 -266 77 -21 174 270

Yurkharovskoye 24.4 32.0 34.1 36.4 36.8 36.8 Pre-tax income 1,683 2,452 2,778 3,518 4,178 3,958

Other fields 12.8 15.5 16.5 15.5 15.5 15.5 Income taxes -356 -535 -540 -685 -797 -735

Subtotal 37.3 47.5 50.5 52.0 52.3 52.3 Minority interest/other 8 12 1 1 - -

Sibneftegas 5.4 5.3 5.4 5.5 5.5 Net income 1,335 1,929 2,238 2,834 3,380 3,222

Nortgas 2.3 3.0 4.0 Fully diluted EPS ($) 4.40 6.35 7.37 9.33 11.13 10.61

Severenergia 0.6 1.2 1.9 3.5

Total 37.3 52.9 56.5 60.9 62.7 65.2 Balance sheet ($mn) 2010 2011 2012 2013e 2014e 2015e

Cash 333 740 603 212 212 212

Liquids (mmboe) 29.6 33.6 34.6 44.3 47.5 51.7 Inventories 61 52 101 166 190 215

Accounts receivable 282 519 537 904 916 1,009

Reserves (PRMS) Other current assets 286 500 665 516 516 516

1P 2P 1P+2P 3P 1P+2P+3P Total current assets 962 1,811 1,907 1,798 1,834 1,951

Gas (bcm) 2,195 911 3,106 698 3,804 Fixed assets 5,519 4,632 5,306 5,830 7,049 8,709

Liquids (mmbbl) 1,242 801 2,043 1,193 3,236 Other non-current assets 2,801 5,466 7,948 8,052 8,052 8,052

Oil and Gas (bn boe) 15.6 6.8 22.4 5.8 28.1 Total non-current assets 8,320 10,098 13,254 13,883 15,102 16,761

EV/Reserves ($/boe) 2.9 2.0 1.6 Total assets 9,282 11,909 15,161 15,680 16,936 18,712

Reserve life (years) 35 51 64 Short-term debt 819 630 1,135 0 33 73

Accounts payable 927 774 521 588 673 760

Financial ratios 2010 2011 2012 2013e 2014e 2015e Other current liabilities 124 152 148 144 164 186

Valuation Total current liabilities 1,870 1,557 1,805 732 870 1,019

P/E (x) 30.7 21.2 18.3 14.4 12.1 12.7 Long-term debt 1,532 2,335 3,202 3,346 2,141 1,504

PEG (x) 49.0 47.7 114.4 54.2 62.8 NM Other non-current liabilities 1,092 532 660 681 681 681

P/B (x) 9.6 6.7 4.8 4.0 3.4 2.8 Total non-current liabilities 2,624 2,867 3,861 4,028 2,823 2,185

EV/EBITDA (x) 24.0 15.0 14.4 11.1 9.9 10.5 Total shareholders' equity 4,789 7,486 9,495 10,921 13,243 15,508

EV/DACF (x) 27.0 17.1 16.6 12.5 11.4 11.6 Total liabilities and equity 9,282 11,909 15,161 15,680 16,936 18,712

Dividend yield (%) 1.0% 1.5% 1.6% 2.1% 2.5% 2.4%

FCF Yield (%) 1.7% 3.6% 2.8% 3.4% 5.1% 3.2% Cash flow statement ($mn) 2010 2011 2012 2013e 2014e 2015e

Profitability Net income 1,335 1,929 2,238 2,834 3,380 3,222

EBITDA Margin (%) 48% 50% 46% 42% 41% 36% Depreciation 218 316 360 405 475 579

EBIT Margin (%) 42% 45% 40% 38% 37% 31% Changes in working capital -139 -155 -165 -390 69 -9

Net Margin (%) 34% 32% 33% 29% 30% 27% Other 63 356 10 236 - -

Leverage Operating cash flow 1,478 2,446 2,443 3,085 3,924 3,793

Gross Debt/Equity (x) 0.5 0.4 0.5 0.3 0.2 0.1 Capex -772 -981 -1,291 -1,548 -1,694 -2,239

Net Debt/Equity (x) 0.4 0.3 0.4 0.3 0.1 0.1 Other -1,511 -722 -1,475 284 - -

Gross Debt/EBITDA (x) 1.3 1.0 1.4 0.8 0.5 0.4 Investing cash flow -2,283 -1,702 -2,766 -1,832 -1,694 -2,239

Net Debt/EBITDA (x) 1.1 0.7 1.2 0.8 0.4 0.3 Change in debt 1,100 637 1,312 -900 -1,172 -597

Net Interest Cover (x) NM NM 56.7 37.3 76.7 191.1 Dividends -325 -516 -635 -704 -1,058 -957

Returns Other -8 -460 500 113 - -

ROE (%) 31% 31% 26% 28% 28% 22% Financing cash flow 766 -339 177 -1,716 -2,230 -1,554

ROACE (%) 21% 25% 19% 21% 22% 18% Effect of Forex -3 2 -63 71 - -

ROA (%) 17% 18% 17% 18% 21% 18% Increase (decrease) in cash flow -42 407 -210 -391 0 0

Russian Oil & Gas

18

Rosneft – Financial and Operational Summary

Source: Company data, FactSet, BCS

Key price assumptions 2010 2011 2012 2013e 2014e 2015e Market statistics

Crude oil ($/bbl) Share Price ($) 8.08

Brent 80 111 112 108 103 97 Market Cap ($mn) 85,632

Urals 77 109 110 107 102 97 EV ($mn) 145,890

Domestic (Samara) 36 49 50 49 48 47

Crack spreads ($/bbl) Income Statement ($mn) 2010 2011 2012 2013e 2014e 2015e

Gasoline 16 17 23 21 20 21 Revenue 63,208 92,465 99,161 140,815 148,616 144,668

Diesel 12 17 19 18 16 16 Opex -4,743 -6,430 -7,088 -12,240 -14,125 -14,512

Jet fuel 15 22 23 22 21 21 Purchased oil -2,372 -10,138 -11,952 -11,068 -9,986 -9,547

Fuel oil -21 -30 -26 -32 -30 -26 Taxes other than income tax -10,903 -16,942 -20,779 -32,230 -35,062 -35,415

Gas, domestic Excise and export duties -16,765 -26,875 -29,027 -42,270 -44,159 -42,567

$/mcm 82 98 99 110 116 118 Other operating costs -9,124 -9,560 -10,696 -16,043 -17,605 -18,100

$/mcf 2.3 2.8 2.8 3.1 3.3 3.3 EBITDA 19,302 22,521 19,620 26,964 27,680 24,528

Depreciation 6,653 7,246 7,313 10,654 11,712 12,528

Macro assumptions 2010 2011 2012 2013e 2014e 2015e Operating income 12,648 15,275 12,307 16,311 15,969 11,999

USD/RUB 30.36 29.39 31.04 31.81 32.60 32.90 Finance expenses -33 34 290 -1,901 -2,546 -2,711

CPI 8.2% 6.0% 6.0% 6.1% 5.0% 5.0% Other expense/income -791 -1,531 1,482 -948 -561 -602

Pre-tax income 11,825 13,778 14,078 13,462 12,862 8,686

Production 2010 2011 2012 2013e 2014e 2015e Income taxes -1,910 -2,926 -3,061 -2,474 -2,572 -1,737

Crude oil Minority interest/other -264 -102 -32 0 0 0

annual output (mmt) 114 119 122 191 213 214 Net income 9,651 10,750 10,986 10,988 10,290 6,949

daily output (kbd) 2,276 2,375 2,439 3,812 4,254 4,276 Fully diluted EPS ($) 1.01 1.12 1.17 1.11 0.97 0.66

Refined products

annual output (mmt) 48 48 48 72 81 81 Balance sheet ($mn) 2010 2011 2012 2013e 2014e 2015e

daily output (kbd) 958 962 967 1,432 1,610 1,610 Cash 4,134 5,156 9,788 10,578 10,578 10,578

light product yield 57% 58% 58% 55% 55% 65% Inventories 2,116 3,914 4,387 5,866 5,642 5,754

Gas (bcm) 12.3 12.8 16.4 34.8 40.3 47.6 Accounts receivable 5,045 6,740 7,758 10,962 10,436 10,426

Other current assets 11,360 9,504 8,839 13,116 13,116 13,116

Reserves (PRMS) Total current assets 22,654 25,314 30,771 40,522 39,772 39,874

1P 2P 1P+2P 3P 1P+2P+3P Fixed assets 66,758 69,294 86,356 150,043 161,842 170,491

Oil (bn bbl) 18.3 9.8 28.2 8.9 37.1 Other non-current assets 8,723 10,281 13,291 25,100 25,100 25,100

Gas (bcm) 992 372 1,363 262 1,625 Total non-current assets 75,481 79,575 99,646 175,143 186,942 195,591

Total (bn boe) 24.2 12.0 36.2 10.4 46.6 Total assets 98,135 104,888 130,418 215,665 226,714 235,464

EV/Reserves ($/boe) 6.0 4.0 3.1 Short-term debt 5,436 4,721 4,681 18,357 22,350 26,482

Reserve life (years) 13 20 26 Accounts payable 3,678 5,622 6,973 12,742 12,255 12,497

Other current liabilities 2,344 2,516 3,241 5,503 5,503 5,503

Financial ratios 2010 2011 2012 2013e 2014e 2015e Total current liabilities 11,457 12,859 14,895 36,602 40,109 44,482

Valuation Long-term debt 17,869 18,512 27,400 57,415 57,415 57,415

P/E (x) 8.9 8.0 7.8 7.8 8.3 12.3 Other non-current liabilities 11,555 10,312 13,389 36,595 36,595 36,595

PEG (x) 18.4 NM NM NM NM NM Total non-current liabilities 29,424 28,823 40,788 94,011 94,011 94,011

P/B (x) 1.7 1.4 1.2 1.1 1.0 0.9 Total shareholders' equity 57,254 63,206 74,735 85,052 92,594 96,971

EV/EBITDA (x) 7.6 6.5 7.4 5.4 5.3 5.9 Total liabilities and equity 98,135 104,888 130,418 215,665 226,714 235,464

EV/DACF (x) 9.0 6.8 7.4 5.7 6.1 6.7

Dividend yield (%) 1.1% 3.0% 3.2% 3.2% 3.0% 2.0% Cash flow statement ($mn) 2010 2011 2012 2013e 2014e 2015e

FCF Yield (%) 8.8% 9.5% 5.8% 11.2% 1.4% 1.3% Net income 9,914 10,852 11,018 10,988 10,290 6,949

Profitability Depreciation 6,653 7,246 7,313 10,654 11,712 12,528

EBITDA Margin (%) 31% 24% 20% 19% 19% 17% Changes in working capital -494 -2,654 966 6,833 264 140

EBIT Margin (%) 20% 17% 12% 12% 11% 8% Other -329 3,300 1,675 2,322 - -

Net Margin (%) 15% 12% 11% 8% 7% 5% Operating cash flow 15,744 18,745 20,973 30,797 22,265 19,618

Leverage Capex -8,696 -13,302 -15,013 -20,977 -23,511 -21,177

Gross Debt/Equity (x) 0.4 0.4 0.4 0.9 0.9 0.9 Acquisitions -3,162 987 -193 -4,041 - -

Net Debt/Equity (x) 0.2 0.2 0.3 0.7 0.7 0.7 Other -626 -1,157 838 3 - -

Gross Debt/EBITDA (x) 1.2 1.0 1.6 2.8 2.9 3.4 Investing cash flow -12,484 -13,472 -14,368 -25,016 -23,511 -21,177

Net Debt/EBITDA (x) 0.6 0.6 1.0 2.2 2.3 2.8 Change in debt 296 306 7,893 37,936 3,993 4,132

Net Interest Cover (x) 384.0 NM NM 8.6 6.3 4.4 Dividends -725 -919 -2,287 -2,403 -2,747 -2,572

Returns Other -696 -3,707 -7,288 -40,943 - -

ROE (%) 19% 18% 16% 14% 12% 7% Financing cash flow -1,124 -4,319 -1,682 -5,410 1,246 1,559

ROACE (%) 15% 16% 10% 9% 8% 6% Effect of Forex 0 68 -290 418 - -

ROA (%) 11% 11% 9% 6% 5% 3% Increase (decrease) in cash flow 2,137 1,022 4,632 790 0 0

Russian Oil & Gas

19

Gazprom – Financial and Operational Summary

Source: Company data, FactSet, BCS

Key price assumptions 2010 2011 2012 2013e 2014e 2015e Market statistics

Gas ($/mcm) Share Price ($) 9.08

Domestic 76 90 93 100 106 108 Market Cap ($mn) 104,182

Europe 302 383 385 377 362 343 EV ($mn) 144,472

FSU 232 290 305 304 291 280

Crude oil ($/bbl) Income Statement ($mn) 2010 2011 2012 2013e 2014e 2015e

Brent 80 111 112 108 103 97 Revenue 118,912 157,494 153,761 154,655 152,410 150,232

Urals 77 109 110 107 102 97 Transportation -9,021 -9,539 -10,318 -11,465 -12,309 -12,746

Domestic (Samara) 36 49 50 49 48 47 Taxes other than income tax -9,617 -14,244 -18,672 -20,436 -22,835 -23,848

Other operating costs -55,226 -68,137 -72,413 -66,753 -65,112 -64,117

Macro assumptions 2010 2011 2012 2013e 2014e 2015e EBITDA 45,047 65,574 52,358 56,001 52,156 49,521

USD/RUB 30.36 29.39 31.04 31.81 32.60 32.90 Depreciation 8,243 9,365 10,767 13,827 15,352 16,881

CPI 8.2% 6.0% 6.0% 6.1% 5.0% 5.0% Operating income 36,804 56,209 41,591 42,175 36,804 32,640

Finance expenses -595 -441 -348 -47 -58 -156

Production 2010 2011 2012 2013e 2014e 2015e Other expense/income 5,960 1,203 7,572 23 2,997 2,979

Natural gas (bcm) 509 510 481 481 488 499 Pre-tax income 42,168 56,971 48,815 42,150 39,743 35,463

Liquids (mmboe) 43 46 48 47 50 50 Income taxes -8,222 -9,473 -8,933 -5,429 -7,949 -7,093

Minority interest/other -1,878 -3,142 -1,702 -3,770 -607 -542

Gas deliveries 2010 2011 2012 2013e 2014e 2015e Net income 32,068 44,356 38,180 32,952 31,187 27,828

Domestic (bcm) 277 281 265 255 249 252 Fully diluted EPS ($) 2.79 3.87 3.33 2.87 2.72 2.43

FSU (bcm) 70 82 66 58 61 62

Non-FSU (bcm) 148 157 151 160 162 165 Balance sheet ($mn) 2010 2011 2012 2013e 2014e 2015e

Cash 14,347 15,572 13,734 18,431 18,431 18,431

Domestic market share 67% 70% 67% 65% 63% 63% Inventories 10,602 12,658 15,043 12,663 12,844 12,837

European market share 23% 27% 25% 28% 28% 29% Accounts receivable 24,669 24,352 30,775 27,453 28,058 27,913

Other current assets 11,115 17,001 19,300 18,719 18,719 18,719

Reserves (PRMS) Total current assets 60,733 69,583 78,851 77,266 78,051 77,899

1P 2P 1P+2P Fixed assets 178,578 208,677 255,938 279,378 308,917 336,927

Gas (bcm) 19,100 4,300 23,400 Other non-current assets 61,312 60,313 60,266 51,653 51,653 51,653

Liquids (mmbbl) 10,599 5,310 15,909 Total non-current assets 239,889 268,989 316,204 331,031 360,570 388,580

Oil and Gas (bn boe) 135.5 33.4 168.9 Total assets 300,623 338,572 395,055 408,296 438,621 466,479

EV/Reserves ($/boe) 1.1 0.9 Short-term debt 6,212 11,395 10,698 11,026 14,120 21,420

Reserve life (years) 44 55 Accounts payable 26,697 29,270 38,072 26,493 26,871 26,856

Other current liabilities 7 - - - - -

Financial ratios 2010 2011 2012 2013e 2014e 2015e Total current liabilities 32,916 40,665 48,770 37,519 40,992 48,276

Valuation Long-term debt 36,598 36,442 38,560 40,188 40,188 40,188

P/E (x) 3.2 2.3 2.7 3.2 3.3 3.7 Other non-current liabilities 18,357 20,411 22,892 29,233 29,233 29,233

PEG (x) 11.1 6.1 NM NM NM NM Total non-current liabilities 54,955 56,853 61,452 69,421 69,421 69,421

P/B (x) 0.5 0.5 0.4 0.4 0.3 0.3 Minority interest 9,329 9,238 10,127 9,970 10,577 11,119

EV/EBITDA (x) 3.2 2.2 2.8 2.6 2.8 2.9 Total shareholders' equity 203,423 231,816 274,706 291,387 317,632 337,663

EV/DACF (x) 3.6 2.5 3.2 2.9 3.1 3.2 Total liabilities and equity 300,623 338,572 395,055 408,296 438,621 466,479

Dividend yield (%) 2.8% 6.9% 4.5% 4.7% 7.5% 6.7%

FCF Yield (%) 11.4% 0.8% 1.1% 4.0% -0.5% -1.7% Cash flow statement ($mn) 2010 2011 2012 2013e 2014e 2015e

Profitability Net income 32,068 44,356 38,180 32,952 31,187 27,828

EBITDA Margin (%) 38% 42% 34% 36% 34% 33% Depreciation 8,243 9,365 10,767 13,827 15,352 16,881

EBIT Margin (%) 31% 36% 27% 27% 24% 22% Changes in working capital 8,356 -1,099 1,054 1,537 -407 137

Net Margin (%) 27% 28% 25% 21% 20% 19% Other -375 2,634 -3,411 3,562 607 542

Leverage Operating cash flow 48,293 55,256 46,590 51,877 46,739 45,389

Gross Debt/Equity (x) 0.2 0.2 0.2 0.2 0.2 0.2 Capex -36,393 -54,404 -45,418 -45,499 -44,891 -44,891

Net Debt/Equity (x) 0.1 0.1 0.1 0.1 0.1 0.1 Other 1,784 208 4,473 761.51 - -

Gross Debt/EBITDA (x) 1.0 0.7 0.9 0.9 1.0 1.2 Investing cash flow -34,609 -54,196 -40,945 -44,738 -44,891 -44,891

Net Debt/EBITDA (x) 0.6 0.5 0.7 0.6 0.7 0.9 Change in debt -7,013 10,435 -1,935 4,037 3,095 7,299

Net Interest Cover (x) 61.8 127.5 119.7 895.5 639.5 209.1 Dividends -1,808 -3,211 -6,158 -4,722 -4,943 -7,797

Returns Other 1,844 -6,382 49 -1,476 - -

ROE (%) 17% 20% 15% 12% 10% 8% Financing cash flow -6,977 841 -8,044 -2,162 -1,848 -497

ROACE (%) 13% 19% 12% 11% 9% 7% Effect of Forex -619 -677 561 -280 - -