DATA ANALYSIS AND INTERPRETATION - …shodhganga.inflibnet.ac.in/bitstream/10603/38431/8/chapter...

100

79 DATA ANALYSIS AND INTERPRETATION “Maintaining governance standards requires accountability at all levels of management. Hence corporate conduct and culture, based on attributes of self regulation and openness contribute to the essence of corporate governance” Naresh Chandra 4.1 INTRODUCTION: Banks are critical component of the economy. Nationalised banks are owned by the government and thus the issue of corporate governance in Indian banks is complicated due to the political intervention in their operation. Corporate governance in banks ensures transparency and prevents scandals. With high level of transparency and disclosures banks can not only achieve efficiency but also helps in better performance. The disclosure of information helps banks improve performance and increase shareholder‟s wealt h. The Sanskrit Subhashita “Satyam bruiyat, priyam bruiyat, na bruiyat satyam apriyam “which means Speak truth that is palatable, do not speak truth that is unpalatable. It is necessary that proper disclosures are made by each bank for better governance. In the present chapter the data collected is analyzed and interpreted. The chapter has the framework where initially the corporate governance index is prepared using sixty five variables. The presence of the variable is marked as 1 and the absence and not properly disclosed is marked as 0. The corporate governance disclosure of five banks for seven years is determined. The corporate governance disclosure level is divided into three main dimensions that are mandatory, non mandatory and other corporate governance disclosures. Disclosure with respect to three major dimensions is determined and later the overall corporate governance disclosure level is calculated. To evaluate the corporate governance relation with that of bank performance initially the banking performance is analyzed using the three triggers ROA, CAR, NPA. Using the bivariate correlation the corporate governance disclosure level is correlated with the bank performance. The evaluation of corporate governance in banks is also made taking into consideration the proportion of the non executive director, board committees and the board meeting. The

Transcript of DATA ANALYSIS AND INTERPRETATION - …shodhganga.inflibnet.ac.in/bitstream/10603/38431/8/chapter...

79

DATA ANALYSIS AND INTERPRETATION

“Maintaining governance standards requires accountability at all levels of management.

Hence corporate conduct and culture, based on attributes of self regulation and openness

contribute to the essence of corporate governance”

Naresh Chandra

4.1 INTRODUCTION:

Banks are critical component of the economy. Nationalised banks are owned by the

government and thus the issue of corporate governance in Indian banks is complicated due to

the political intervention in their operation. Corporate governance in banks ensures

transparency and prevents scandals. With high level of transparency and disclosures banks

can not only achieve efficiency but also helps in better performance. The disclosure of

information helps banks improve performance and increase shareholder‟s wealth. The

Sanskrit Subhashita “Satyam bruiyat, priyam bruiyat, na bruiyat satyam apriyam “which

means Speak truth that is palatable, do not speak truth that is unpalatable. It is necessary that

proper disclosures are made by each bank for better governance. In the present chapter the

data collected is analyzed and interpreted.

The chapter has the framework where initially the corporate governance index is prepared

using sixty five variables. The presence of the variable is marked as 1 and the absence and

not properly disclosed is marked as 0. The corporate governance disclosure of five banks for

seven years is determined.

The corporate governance disclosure level is divided into three main dimensions that are

mandatory, non mandatory and other corporate governance disclosures. Disclosure with

respect to three major dimensions is determined and later the overall corporate governance

disclosure level is calculated.

To evaluate the corporate governance relation with that of bank performance initially the

banking performance is analyzed using the three triggers ROA, CAR, NPA. Using the

bivariate correlation the corporate governance disclosure level is correlated with the bank

performance.

The evaluation of corporate governance in banks is also made taking into consideration the

proportion of the non executive director, board committees and the board meeting. The

80

proportion of non executive director relation with that of bank performance is analyzed. The

relation between the board committees and the number of board meeting with the disclosure

level is also evaluated.

Lastly, the corporate governance is evaluated from the shareholders perspective to evaluate

the opinion on the disclosure and whether the corporate governance has the effect on their

investment decision.

4.2 CORPORATE GOVERNANCE DISCLOSURE LEVEL:

The first step in determining the corporate governance disclosure level is to construct the

corporate governance disclosure index. Corporate governance disclosure index is constructed

using sixty five independent variables. The relation between corporate governance and bank

performance is analyzed based on 65 variables through checklist method

The important dimensions of the research analysis are

1. Bank's philosophy on code of governance

2. Board of Directors

3. Audit committee

4. Remuneration Committee

5. Shareholders Committee

6. General Body meetings

7. Disclosures

8. Means of Communication

9. General Shareholder information

10. Non-Mandatory Requirements

11. Other Corporate Governance Requirements

The eleven dimensions are further divided into sixty variables which are the base of the entire

study. Bank‟s philosophy on code of governance, Board of Directors, Audit committee,

Remuneration Committee, shareholders committee, general body meetings, disclosures,

means of communication, general shareholder information are the mandatory disclosure

requirements.

Non mandatory disclosure requirements include:

The Board which specifies the disclosures regarding non-executive Chairman who may be

entitled to maintain a Chairman's office at the bank's expense and also allowed

81

reimbursement of expenses incurred in performance of his duties. It needs to specify that

Independent Directors may have a tenure not exceeding aggregate period of nine years, on

the Board of a company. The listed bank may ensure that the person who is being appointed

as an independent director has the requisite qualifications and experience which would be of

use to the company and in the opinion of the company, would enable him to contribute

effectively to the bank in his capacity as an independent director.

Disclosure of Remuneration Committee –

i. The board may set up a remuneration committee to determine on their behalf and on

behalf of the shareholders with agreed terms of reference, the company‟s policy on

specific remuneration packages for executive directors including pension rights and

any compensation payment.

ii. To avoid conflicts of interest, the remuneration committee which would determine

the remuneration packages of the executive directors may comprise of at least three

directors, all of whom should be non-executive directors, the Chairman of

committee being an independent director.

iii. All the members of the remuneration committee could be present at the meeting.

iv. The Chairman of the remuneration committee could be present at the Annual

General Meeting, to answer the shareholder queries. However, it would be up to the

Chairman to decide who should answer the queries.

Disclosure of Shareholder Rights where a half-yearly declaration of financial performance

including summary of the significant events in last six-months, may be sent to each

household of shareholders.

Apart from above disclosures the disclosure in relation to the training of Board Members,

Audit qualifications where Bank may move towards a regime of unqualified financial

statements and whistle blower policy is part of the non mandatory requirements.

Other corporate governance requirements includes Profile of directors appointed during the

year mentioned by the bank, Code of conduct of banks, CSR ie., corporate social

responsibility taken up by the bank mentioned, disclosure about risk management, segment

wise or product wise performance part of Management Discussion & Analysis, nomination

committee, Auditor‟s certificate provided by the Bank, CEO or CFO certificate provided by

the Bank, Chairman of the Board Executive or Non Executive mentioned and information

related to Independent directors need to be well defined.

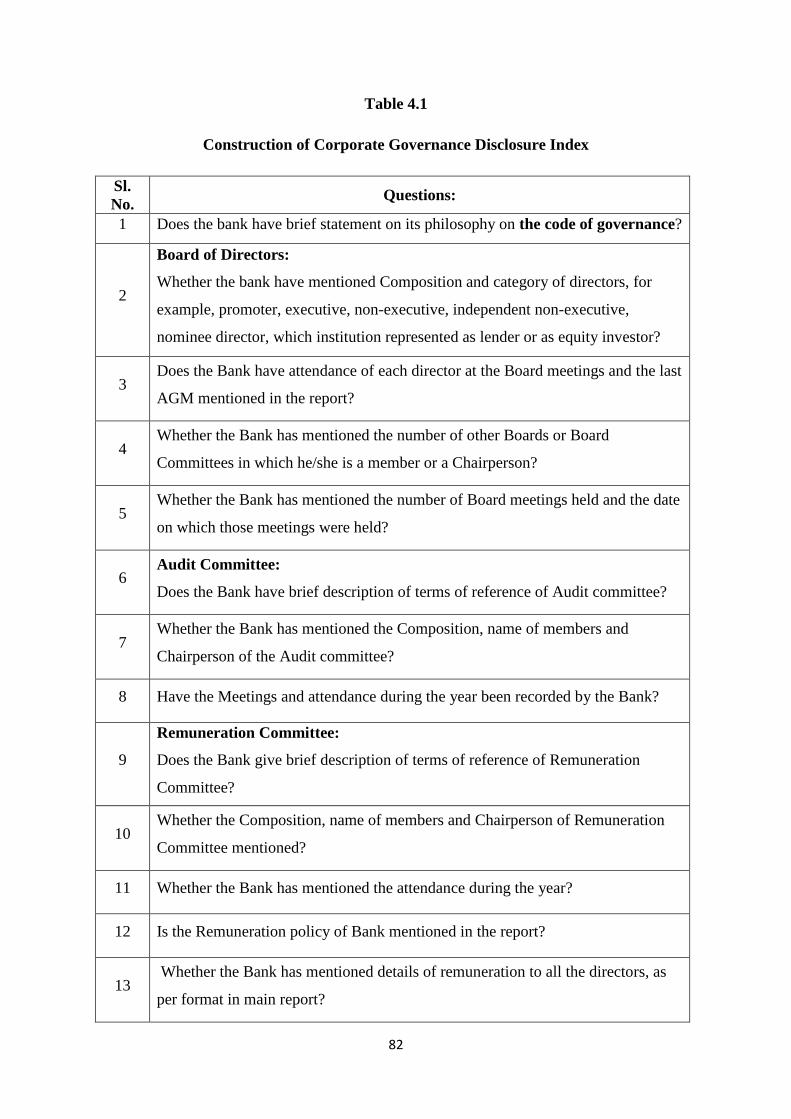

82

Table 4.1

Construction of Corporate Governance Disclosure Index

Sl.

No. Questions:

1 Does the bank have brief statement on its philosophy on the code of governance?

2

Board of Directors:

Whether the bank have mentioned Composition and category of directors, for

example, promoter, executive, non-executive, independent non-executive,

nominee director, which institution represented as lender or as equity investor?

3 Does the Bank have attendance of each director at the Board meetings and the last

AGM mentioned in the report?

4 Whether the Bank has mentioned the number of other Boards or Board

Committees in which he/she is a member or a Chairperson?

5 Whether the Bank has mentioned the number of Board meetings held and the date

on which those meetings were held?

6 Audit Committee:

Does the Bank have brief description of terms of reference of Audit committee?

7 Whether the Bank has mentioned the Composition, name of members and

Chairperson of the Audit committee?

8 Have the Meetings and attendance during the year been recorded by the Bank?

9

Remuneration Committee:

Does the Bank give brief description of terms of reference of Remuneration

Committee?

10 Whether the Composition, name of members and Chairperson of Remuneration

Committee mentioned?

11 Whether the Bank has mentioned the attendance during the year?

12 Is the Remuneration policy of Bank mentioned in the report?

13 Whether the Bank has mentioned details of remuneration to all the directors, as

per format in main report?

83

14

Shareholders Committee:

Whether the name of non-executive director heading the committee mentioned in

the report?

15 Does the Bank mention the name and designation of compliance officer of

Shareholder Committee?

16 Whether the number of shareholders‟ complaints received so far mentioned by the

Bank?

17 If the number of complaints not solved to the satisfaction of shareholders

mentioned?

18 If the Number of pending complaints mentioned by the Bank?

19 General Body meetings:

Does the Bank mention the location and time, where last three AGMs were held?

20 Whether any special resolutions passed in the previous 3 AGMs been recorded?

21 Whether any special resolution passed last year through postal ballot and details

of voting pattern mentioned?

22 Does the Bank mention the person who conducted the postal ballot exercise?

23 Whether any special resolution is proposed to be conducted through postal ballot

mentioned by the Bank?

24 Does the bank mention the procedure for postal ballot?

25

Disclosures:

Whether disclosures on materially significant related party transactions that may

have potential conflict with the interests of bank at large made?

26

Whether following is included in the disclosure: Details of non-compliance by the

company, penalties, and strictures imposed on the company by Stock Exchange or

SEBI or any other statutory authority, on any matter related to capital markets,

during the last three years?

27 Whether the Bank has the Whistle Blower policy and affirmation that no

personnel have been denied access to the audit committee?

84

28 Whether the Details of compliance with mandatory requirements and adoption of

the non-mandatory requirements of this clause given?

29 Means of communication

Whether the Quarterly results disclosed?

30 Does the bank display Newspapers wherein results normally published?

31 Does the bank disclose name of the website, where displayed?

32 Whether the official news releases has been disclosed?

33 Whether the presentations made to institutional investors or to the analysts are

made known?

34 Whether management discussion and analysis is a part of annual report or not?

35 Whether the Bank has updated General Shareholder information related to:

AGM: Date, time and venue?

36 Financial year

37 Date of Book closure

38 Dividend Payment Date

39 Listing on Stock Exchanges Stock Code

40 Market Price Data : High, Low during each month in last financial year

41 Performance in comparison to broad-based indices such as BSE Sensex, CRISIL

index etc.

42 Registrar and Transfer Agents Share Transfer System

43 Distribution of shareholding Dematerialization of shares and liquidity

44 Outstanding GDRs/ADRs/Warrants or any Convertible instruments, conversion

date and likely impact on equity

45 Branch locations and address of correspondence

46

Non-Mandatory Requirements:

The Board

Whether A non-executive Chairman may be entitled to maintain a Chairman‟s

office at the company‟s expense?

85

47 Whether they are allowed reimbursement of expenses incurred in performance of

his duties?

48 Whether there are any Independent Directors who may have a tenure not

exceeding, in the aggregate, a period of nine years, on the Board of a company?

49

Remuneration Committee

Whether the board has set up a remuneration committee to determine on their

behalf and on behalf of the shareholders with agreed terms of reference, the

company‟s policy on specific remuneration packages for executive directors

including pension rights and any compensation payment?

50

To avoid conflicts of interest, the remuneration committee, which would

determine the remuneration packages of the executive directors may comprise of

at least three directors, all of whom should be non-executive directors, the

Chairman of committee being an independent director, Does the Bank have it?

51 Do all the members of the remuneration committee be present at the meeting?

52

Shareholder Rights

Whether half-yearly declaration of financial performance including summary of

the significant events in last six-months has been sent to each individual

shareholders?

53

Audit qualifications

Whether the Bank may move towards a regime of unqualified financial

statements stated?

54 Does the Bank conduct training for its Board members?

55 Whether the Bank has Pear Group of BOD to evaluate the performance of non-

executive directors?

56 Other Corporate Governance Requirements

If the Profile of directors appointed during the year mentioned?

57 Whether the Bank has mentioned Code of conduct?

58 Whether the CSR initiatives taken up by the Bank mentioned?

86

59 Whether there is disclosure about risk management?

60 Whether segment wise or product wise performance part of Management

Discussion &Analysis?

61 Does the Bank have nomination committee?

62 Whether Auditor‟s certificate provided by the Bank?

63 Whether CEO or CFO certificate provided by the Bank?

64 Is the Chairman of the Board Executive or Non Executive mentioned?

65 Are the Independent directors well defined?

Corporate governance disclosure index is constructed based on sixty five variables. 1 to 45

are mandatory disclosure requirement related questions. 46 to 55 are non mandatory

disclosure requirements related question and 56 to 65 are other corporate governance

disclosure requirements related questions.

4.2.1 CORPORATE GOVERNANCE DISCLOSURE LEVEL OF BANKS

The analysis of the all the five banks for the seven years is made using the corporate

governance disclosure index. The presence or absence of mandatory, non mandatory and

other corporate governance is measured with the constructed index. 65 variables were

analyzed for 5 banks (65*5=) 325 variables for seven years from 2005 to 2012 (325*7=2275)

which becomes 2275 variables. The corporate governance disclosure index using

dichotomous question about presence and absence of the parameter is used to determine the

corporate governance disclosure level of each bank for seven years that is 2005-2012. The

presence of the variable is marked 1 and the absence is marked as 0. Disclosure variable

which are not properly reported in the bank‟s corporate governance report is also marked 0

since they are also considered as absence of the parameter.

In order to calculate the overall corporate governance disclosure level and its percentage the

below formula is applied.

87

Overall CGDL= Sum of total disclosures made by the bank.

Percentage of overall CGDL =

Once the corporate governance disclosure index is constructed, MS Excel work sheet which

includes the corporate governance disclosure index for seven years is prepared for the all the

five banks. The presence and the absence of the variable is marked in the constructed index

for respective banks for all the seven years that is 2005 to 2012.

Variables present in the corporate governance report and the annual report of the bank is

entered in the work sheet for the given period for all the five banks. Once the sixty five

variables are entered then the total of the variable is taken into consideration. The total score

of individual banks are calculated. Later to get the percentage of overall corporate

governance disclosure level the total score of each bank is divided by the maximum possible

score that is 65 and multiplied with 100 to get the disclosure percentage. The overall

corporate governance disclosure requirement is the sum of the mandatory, non mandatory

and other corporate governance requirement variables. The results of all the three dimensions

are analysed later the overall corporate governance disclosure level is used to correlate with

the bank performance.

88

Table: 4.2

Mandatory Corporate Governance Disclosure Level

SL.

NO. BANK

2005-

06

2006-

07 2007-08

2008-

09

2009-

10

2010-

11

2011-

12 Average %

1 Corporation

Bank 37 39 40 40 40 40 40 39.43 87.62

2 Canara

Bank 41 41 41 41 41 41 41 41.00 91.11

3 PNB 38 41 42 42 42 42 43 41.43 91.11

4 Vijaya

Bank 38 39 38 38 38 38 38 38.14 84.76

5 Syndicate

Bank 37 37 37 37 36 38 39 37.29 82.86

Average 38.2 39.4 39.6 39.6 39.4 39.8 40.2 39.46

Mandatory disclosure is an important corporate governance disclosure variable. It is

independent in nature. There are forty five mandatory requirements which are used to

construct the corporate governance disclosure index.

The above table highlights the mandatory disclosure of five banks for seven years. Canara

Bank and PNB shows the highest disclosure level with 91.11 percent, followed by

Corporation Bank with 87.62%, Vijaya Bank with 84.76% and the least disclosure is by

Syndicate Bank with 82.86%.

In the year 2005-06 the average disclosure of five banks were 38.2 which has gradually

increased year after year where in 2011-12 it is 40.2.

After 2006 where SEBI made the compulsion for disclosures there is an increase in the

disclosure level of the banks.

There is gradual increase in the mandatory disclosure level but in the year 2011-12 it is

showing declining trend which needs to be considered.

89

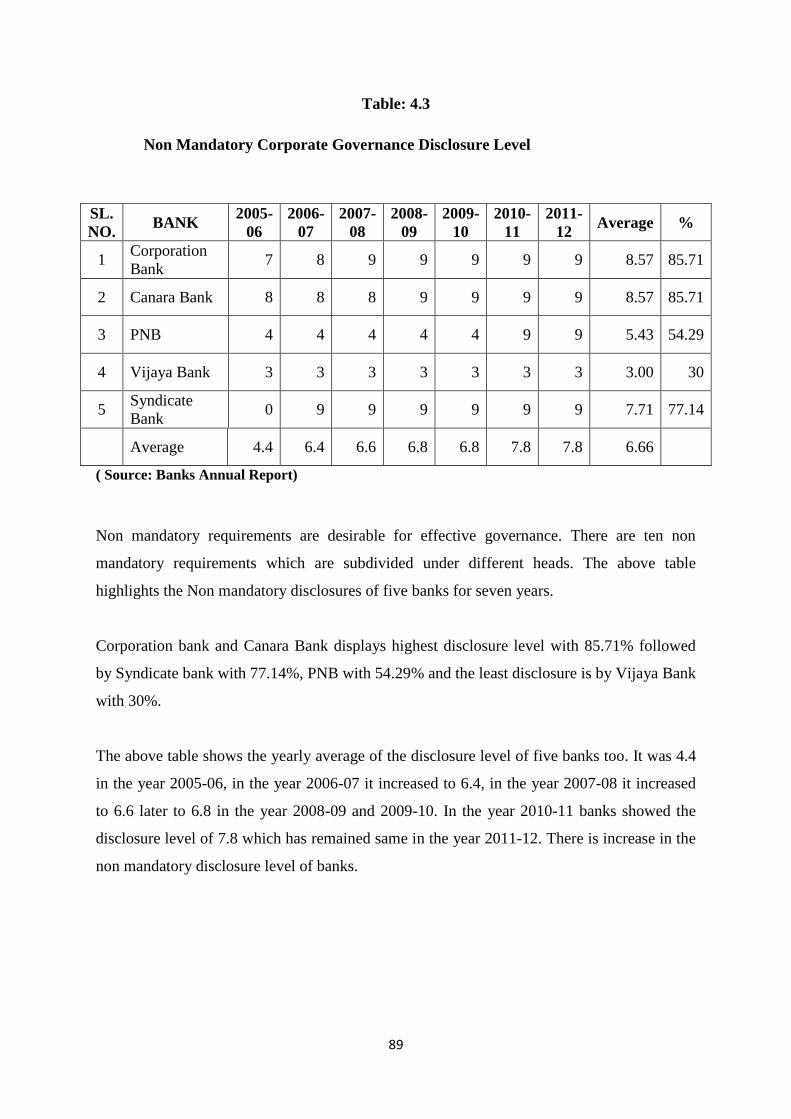

Table: 4.3

Non Mandatory Corporate Governance Disclosure Level

SL.

NO. BANK

2005-

06

2006-

07

2007-

08

2008-

09

2009-

10

2010-

11

2011-

12 Average %

1 Corporation

Bank 7 8 9 9 9 9 9 8.57 85.71

2 Canara Bank 8 8 8 9 9 9 9 8.57 85.71

3 PNB 4 4 4 4 4 9 9 5.43 54.29

4 Vijaya Bank 3 3 3 3 3 3 3 3.00 30

5 Syndicate

Bank 0 9 9 9 9 9 9 7.71 77.14

Average 4.4 6.4 6.6 6.8 6.8 7.8 7.8 6.66

( Source: Banks Annual Report)

Non mandatory requirements are desirable for effective governance. There are ten non

mandatory requirements which are subdivided under different heads. The above table

highlights the Non mandatory disclosures of five banks for seven years.

Corporation bank and Canara Bank displays highest disclosure level with 85.71% followed

by Syndicate bank with 77.14%, PNB with 54.29% and the least disclosure is by Vijaya Bank

with 30%.

The above table shows the yearly average of the disclosure level of five banks too. It was 4.4

in the year 2005-06, in the year 2006-07 it increased to 6.4, in the year 2007-08 it increased

to 6.6 later to 6.8 in the year 2008-09 and 2009-10. In the year 2010-11 banks showed the

disclosure level of 7.8 which has remained same in the year 2011-12. There is increase in the

non mandatory disclosure level of banks.

90

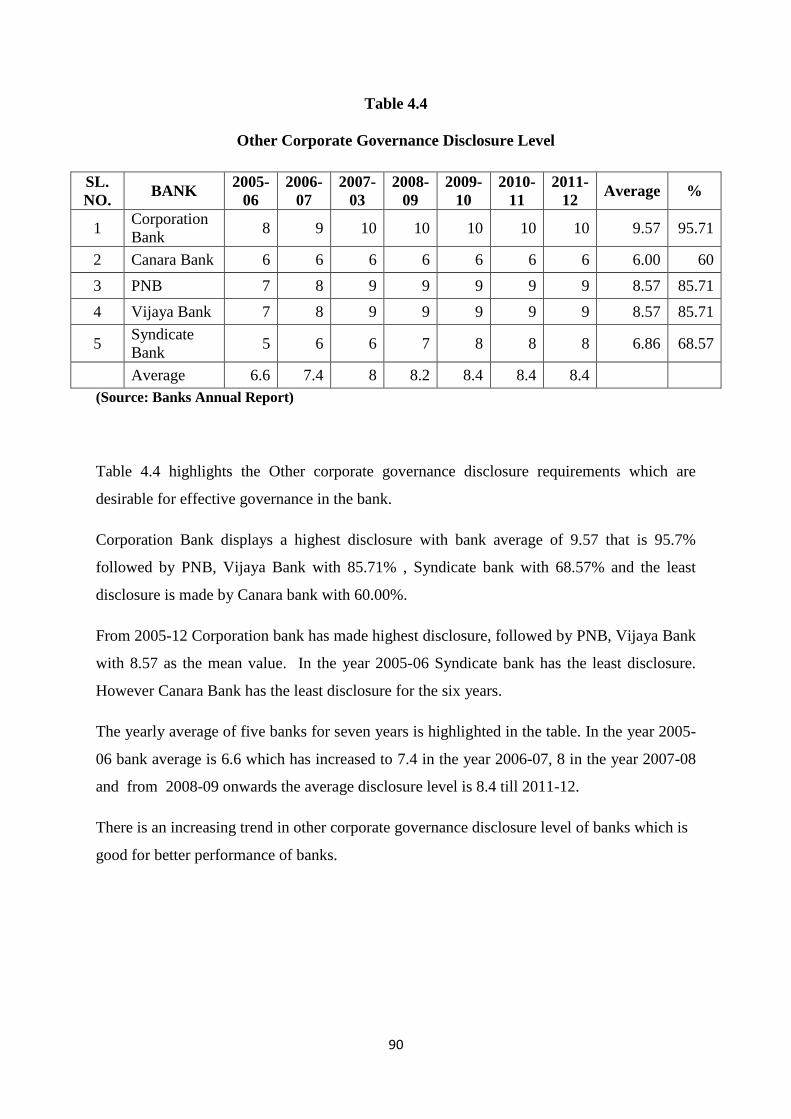

Table 4.4

Other Corporate Governance Disclosure Level

SL.

NO. BANK

2005-

06

2006-

07

2007-

03

2008-

09

2009-

10

2010-

11

2011-

12 Average %

1 Corporation

Bank 8 9 10 10 10 10 10 9.57 95.71

2 Canara Bank 6 6 6 6 6 6 6 6.00 60

3 PNB 7 8 9 9 9 9 9 8.57 85.71

4 Vijaya Bank 7 8 9 9 9 9 9 8.57 85.71

5 Syndicate

Bank 5 6 6 7 8 8 8 6.86 68.57

Average 6.6 7.4 8 8.2 8.4 8.4 8.4

(Source: Banks Annual Report)

Table 4.4 highlights the Other corporate governance disclosure requirements which are

desirable for effective governance in the bank.

Corporation Bank displays a highest disclosure with bank average of 9.57 that is 95.7%

followed by PNB, Vijaya Bank with 85.71% , Syndicate bank with 68.57% and the least

disclosure is made by Canara bank with 60.00%.

From 2005-12 Corporation bank has made highest disclosure, followed by PNB, Vijaya Bank

with 8.57 as the mean value. In the year 2005-06 Syndicate bank has the least disclosure.

However Canara Bank has the least disclosure for the six years.

The yearly average of five banks for seven years is highlighted in the table. In the year 2005-

06 bank average is 6.6 which has increased to 7.4 in the year 2006-07, 8 in the year 2007-08

and from 2008-09 onwards the average disclosure level is 8.4 till 2011-12.

There is an increasing trend in other corporate governance disclosure level of banks which is

good for better performance of banks.

91

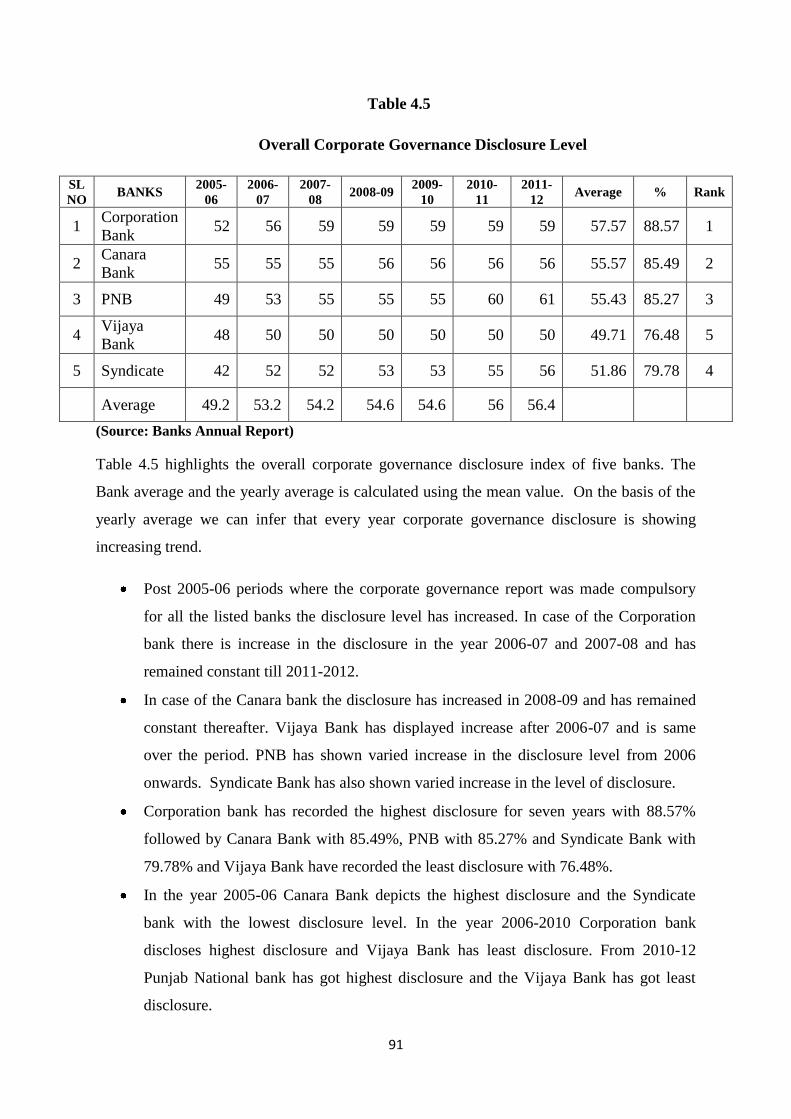

Table 4.5

Overall Corporate Governance Disclosure Level

SL

NO BANKS

2005-

06

2006-

07

2007-

08 2008-09

2009-

10

2010-

11

2011-

12 Average % Rank

1 Corporation

Bank 52 56 59 59 59 59 59 57.57 88.57 1

2 Canara

Bank 55 55 55 56 56 56 56 55.57 85.49 2

3 PNB 49 53 55 55 55 60 61 55.43 85.27 3

4 Vijaya

Bank 48 50 50 50 50 50 50 49.71 76.48 5

5 Syndicate 42 52 52 53 53 55 56 51.86 79.78 4

Average 49.2 53.2 54.2 54.6 54.6 56 56.4

(Source: Banks Annual Report)

Table 4.5 highlights the overall corporate governance disclosure index of five banks. The

Bank average and the yearly average is calculated using the mean value. On the basis of the

yearly average we can infer that every year corporate governance disclosure is showing

increasing trend.

Post 2005-06 periods where the corporate governance report was made compulsory

for all the listed banks the disclosure level has increased. In case of the Corporation

bank there is increase in the disclosure in the year 2006-07 and 2007-08 and has

remained constant till 2011-2012.

In case of the Canara bank the disclosure has increased in 2008-09 and has remained

constant thereafter. Vijaya Bank has displayed increase after 2006-07 and is same

over the period. PNB has shown varied increase in the disclosure level from 2006

onwards. Syndicate Bank has also shown varied increase in the level of disclosure.

Corporation bank has recorded the highest disclosure for seven years with 88.57%

followed by Canara Bank with 85.49%, PNB with 85.27% and Syndicate Bank with

79.78% and Vijaya Bank have recorded the least disclosure with 76.48%.

In the year 2005-06 Canara Bank depicts the highest disclosure and the Syndicate

bank with the lowest disclosure level. In the year 2006-2010 Corporation bank

discloses highest disclosure and Vijaya Bank has least disclosure. From 2010-12

Punjab National bank has got highest disclosure and the Vijaya Bank has got least

disclosure.

92

Based on the average disclosure for the period of 2005-2012 Corporation Bank has got

highest rank followed by Canara Bank, PNB, Syndicate Bank and the Vijaya Bank has got

lowest rank. It is inferred that there is no uniformity in the disclosure level of banks.

Table: 4.6

Mandatory Requirements:

Code of governance and Board of Directors

Sl.

No. CG variable

Corporation

Bank

Canara

bank PNB

Vijaya

Bank

Syndicate

bank

1. Does the bank have brief

statement on its philosophy

on the code of governance? 100.00 100.00 100.00 100.00 100.00

2. Board of Directors:

Whether the bank have

mentioned Composition and

category of directors, for

example, promoter,

executive, non-executive,

independent non-executive,

nominee director, which

institution represented as

lender or as equity investor? 100.00 100.00 100.00 100.00 100.00

3. Does the Bank have

attendance of each director at

the Board meetings and the

last AGM mentioned in the

report? 100.00 100.00 100.00 100.00 100.00

4. Whether the Bank has

mentioned the number of

other Boards or Board

Committees in which he/she

is a member or a

Chairperson? 100.00 100.00 100.00 0.00 100.00

5. Whether the Bank has

mentioned the number of

Board meetings held and the

date on which those meetings

were held? 100.00 100.00 100.00 100.00 100.00

6. Audit Committee:

Does the Bank have brief

description of terms of 100.00 100.00 100.00 100.00 100.00

93

reference of Audit

committee?

7. Whether the Bank has

mentioned the Composition,

name of members and

Chairperson of the Audit

committee? 100.00 100.00 100.00 100.00 100.00

8. Have the Meetings and

attendance during the year

been recorded by the Bank? 100.00 100.00 100.00 100.00 100.00

The above table displays the mandatory disclosure level of each bank for seven years. It can

be observed that all the banks have disclosed the code of conduct, board of directors.

Regarding the information related to board of directors and other variables all the banks has

given good disclosures.

The information regarding whether bank has mentioned the number of other Boards or Board

Committees in which he/she is a member or a Chairperson is done by Vijaya Bank has made

least disclosure.

94

Table: 4.7

Mandatory Requirements: Remuneration Committee

Sl.

No. CG variable

Corporation

Bank

Canara

bank PNB

Vijaya

Bank

Syndicate

bank

1

Remuneration

Committee:

Does the Bank give

brief description of

terms of reference of

Remuneration

Committee? 100.00 100.00 100.00 100.00 100.00

2

Whether the

Composition, name

of members and

Chairperson of

Remuneration

Committee

mentioned? 85.71 100.00 85.71 100.00 85.71

3

Whether the Bank

has mentioned the

attendance during the

year? 85.71 100.00 85.71 100.00 100.00

4

Is the Remuneration

policy of Bank

mentioned in the

report? 100.00 100.00 85.71 100.00 100.00

5

Whether the Bank

has mentioned details

of remuneration to all

the directors, as per

format in main

report? 100.00 100.00 100.00 100.00 14.29

From the above table we can infer that Canara bank is displaying good disclosure in terms of

remuneration committee. Syndicate Bank has the least disclosure about details of

remuneration to all the directors, as per format in main report.

95

Table: 4.8

Mandatory Requirements: Shareholders Committee

Sl.

No. CG variable

Corporation

Bank

Canara

bank PNB

Vijaya

Bank

Syndicate

bank

1

Shareholders

Committee:

Whether the name of

non-executive director

heading the committee

mentioned in the

report? 100.00 100.00 100.00 100.00 100.00

2

Does the Bank

mention the name and

designation of

compliance officer of

Shareholder

Committee? 100.00 100.00 100.00 100.00 100.00

3

Whether the number

of shareholders‟

complaints received so

far mentioned by the

Bank 100.00 100.00 100.00 100.00 100.00

4

If the number of

complaints not solved

to the satisfaction of

shareholders

mentioned? 100.00 100.00 100.00 100.00 100.00

5

If the Number of

pending complaints

mentioned by the

Bank? 100.00 100.00 100.00 100.00 100.00

All the five banks are displaying good disclosure in terms of information related to

shareholder committee.

96

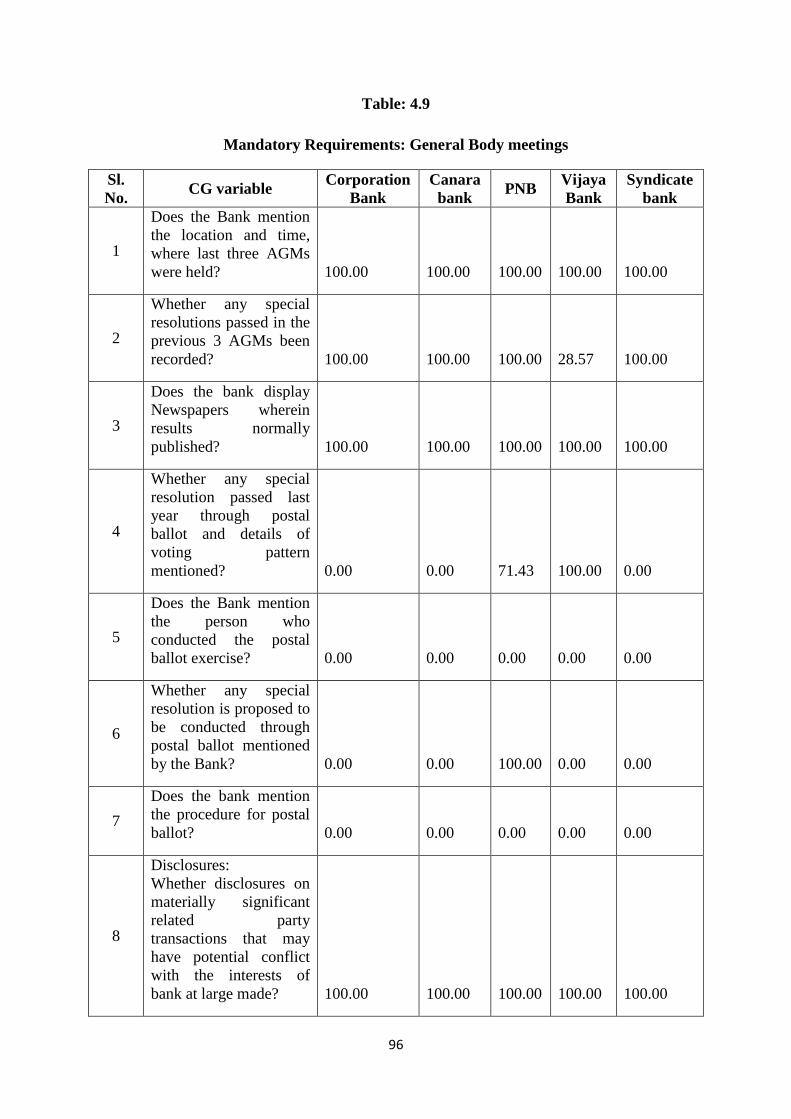

Table: 4.9

Mandatory Requirements: General Body meetings

Sl.

No. CG variable

Corporation

Bank

Canara

bank PNB

Vijaya

Bank

Syndicate

bank

1

Does the Bank mention

the location and time,

where last three AGMs

were held? 100.00 100.00 100.00 100.00 100.00

2

Whether any special

resolutions passed in the

previous 3 AGMs been

recorded? 100.00 100.00 100.00 28.57 100.00

3

Does the bank display

Newspapers wherein

results normally

published? 100.00 100.00 100.00 100.00 100.00

4

Whether any special

resolution passed last

year through postal

ballot and details of

voting pattern

mentioned? 0.00 0.00 71.43 100.00 0.00

5

Does the Bank mention

the person who

conducted the postal

ballot exercise? 0.00 0.00 0.00 0.00 0.00

6

Whether any special

resolution is proposed to

be conducted through

postal ballot mentioned

by the Bank? 0.00 0.00 100.00 0.00 0.00

7

Does the bank mention

the procedure for postal

ballot? 0.00 0.00 0.00 0.00 0.00

8

Disclosures:

Whether disclosures on

materially significant

related party

transactions that may

have potential conflict

with the interests of

bank at large made? 100.00 100.00 100.00 100.00 100.00

97

9

Whether following is

included in the

disclosure: Details of

non-compliance by the

company, penalties,

strictures imposed on

the company by Stock

Exchange or SEBI or

any other statutory

authority, on any matter

related to capital

markets, during the last

three years? 100.00 100.00 100.00 100.00 100.00

10

Whether the Bank have

the Whistle Blower

policy and affirmation

that no personnel have

been denied access to

the audit committee? 71.43 100.00 14.29 85.71 28.57

11

Whether the Details of

compliance with

mandatory requirements

and adoption of the non-

mandatory requirements

of this clause given? 100.00 100.00 100.00 100.00 100.00

Vijaya Bank is displaying least disclosure for special resolutions passed in the previous

3AGMs been recorded. All the banks are displaying least disclosure for the postal ballot

related information. Canara bank is showing good disclosure for the information related to

whistle Blower policy and affirmation that no personnel have been denied access to the audit

committee.

98

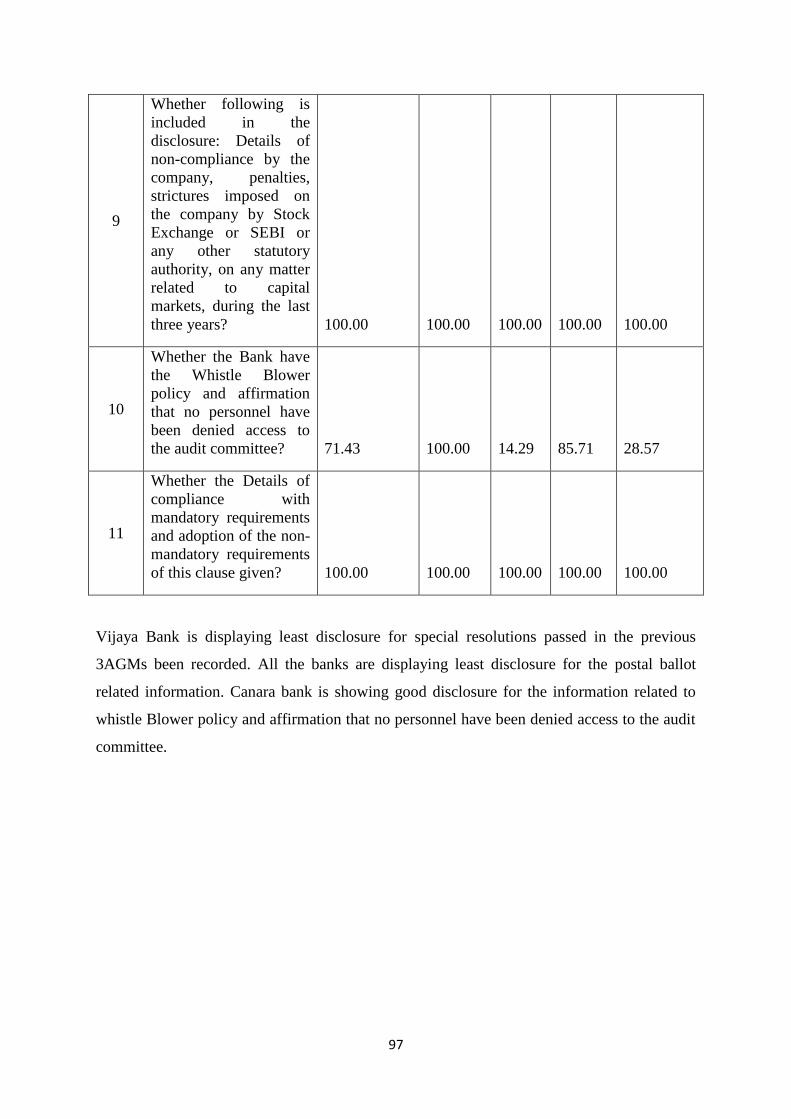

Table: 4.10

Mandatory Requirements: Means of communication

Sl.

No. CG variable

Corporation

Bank

Canara

bank PNB

Vijaya

Bank

Syndicate

bank

1 Whether the Quaterly

results disclosed? 100.00 100.00 100.00 100.00 100.00

2

Does the bank disclose

name of the website,

where displayed? 100.00 100.00 100.00 100.00 100.00

3

Whether the official

news releases has been

disclosed? 100.00 100.00 100.00 100.00 100.00

4

Whether the

presentations made to

institutional investors

or to the analysts are

made known? 0.00 100.00 100.00 0.00 0.00

5

Whether management

discussion and analysis

is a part of annual

report or not? 100.00 100.00 100.00 100.00 100.00

6

Whether the Bank has

updated General

Shareholder

information related to:

AGM : Date, time and

venue? 100.00 100.00 100.00 100.00 100.00

7 Financial year 100.00 100.00 100.00 100.00 100.00

8 Date of Book closure 100.00 100.00 100.00 100.00 100.00

9 Dividend Payment

Date 100.00 100.00 100.00 100.00 100.00

10 Listing on Stock

Exchanges Stock Code 100.00 100.00 100.00 100.00 100.00

11

Market Price Data :

High., Low during

each month in last

financial year 100.00 100.00 100.00 100.00 100.00

99

12

Performance in

comparison to broad-

based indices such as

BSE Sensex, CRISIL

index etc. 100.00 100.00 100.00 100.00 100.00

13

Registrar and Transfer

Agents Share Transfer

System 100.00 100.00 100.00 100.00 100.00

14

Distribution of

shareholding

Dematerialization of

shares and liquidity 100.00 100.00 100.00 100.00 100.00

15

Outstanding

GDRs/ADRs/Warrants

or any Convertible

instruments,

conversion date and

likely impact on equity 100.00 100.00 100.00 0.00 0.00

16

Branch locations and

address of

correspondence 100.00 100.00 100.00 100.00 100.00

Corporation bank, Syndicate bank and Vijaya Bank is showing least disclosure for the

information related to presentations made to institutional investors or to the analysts are made

known.

Vijaya Bank has made least disclosure for information related to any special resolutions

passed in the previous 3 AGMs been recorded. In case of information related to outstanding

GDRs/ADRs/Warrants or any Convertible instruments, conversion date and likely impact on

equity Vijaya Bank and Syndicate bank has least disclosure.

Corporation bank, PNB and Syndicate has made least disclosure about the presentations

made to institutional investors or to the analysts are made known.

100

Table: 4.11

Non-Mandatory Requirements: The Board

Sl.

No

Non-Mandatory

Requirements

Corporatio

n

Bank

Canara

Bank PNB

Vijaya

Bank

Syndicat

e Bank

1

Whether A non-executive

Chairman may be entitled

to maintain a Chairman‟s

office at the company‟s

expense? 100.00 100.00 100.00 100.00 85.71

2

Whether they are allowed

reimbursement of

expenses incurred in

performance of his

duties? 100.00 100.00 100.00 0.00 85.71

3

Whether there are any

Independent Directors

who may have a tenure

not exceeding, in the

aggregate, a period of

nine years, on the Board

of a company? 0.00 0.00 0.00 0.00 0.00

The above table shows the disclosure related to the information related to the board

requirement. The information related to the independent directors is showing no disclosure.

Out of five banks Syndicate bank is showing least disclosure related to the board information.

101

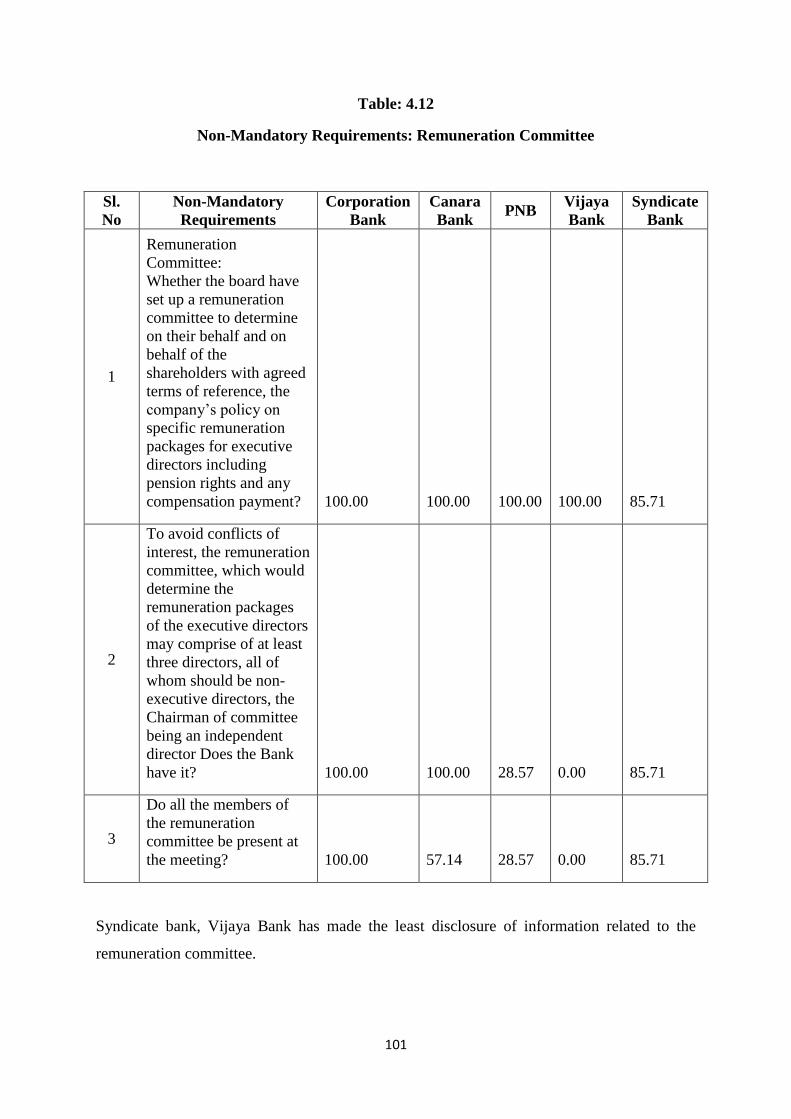

Table: 4.12

Non-Mandatory Requirements: Remuneration Committee

Sl.

No

Non-Mandatory

Requirements

Corporation

Bank

Canara

Bank PNB

Vijaya

Bank

Syndicate

Bank

1

Remuneration

Committee:

Whether the board have

set up a remuneration

committee to determine

on their behalf and on

behalf of the

shareholders with agreed

terms of reference, the

company‟s policy on

specific remuneration

packages for executive

directors including

pension rights and any

compensation payment? 100.00 100.00 100.00 100.00 85.71

2

To avoid conflicts of

interest, the remuneration

committee, which would

determine the

remuneration packages

of the executive directors

may comprise of at least

three directors, all of

whom should be non-

executive directors, the

Chairman of committee

being an independent

director Does the Bank

have it? 100.00 100.00 28.57 0.00 85.71

3

Do all the members of

the remuneration

committee be present at

the meeting? 100.00 57.14 28.57 0.00 85.71

Syndicate bank, Vijaya Bank has made the least disclosure of information related to the

remuneration committee.

102

Table: 4.13

Non-Mandatory Requirements: Shareholders Rights

Sl.

No.

Non-mandatory

requirements

Corporation

Bank

Canara

bank PNB

Vijaya

bank

Syndicate

bank

1.

Shareholder Rights

Whether half-yearly

declaration of financial

performance including

summary of the

significant events in

last six-months been

sent to each individual

shareholders? 100.00 100.00 100.00 100.00 85.71

Syndicate bank has made least disclosure for the information related to the shareholder‟s

rights.

Table: 4.14

Non-Mandatory Requirements: Audit Qualification, Training for board members, and

Pear Group of BOD

Sl.

No.

Non-mandatory

requirements

Corporation

Bank

Canara

bank PNB

Vijaya

bank

Syndicate

bank

1

Audit qualifications

Whether the Bank

may move towards a

regime of unqualified

financial statements

stated? 100.00 100.00 28.57 0.00 85.71

2

Does the Bank

conduct training for

its Board members? 85.71 100.00 28.57 0.00 85.71

3

Whether the Bank has

Pear Group of BOD

to evaluate the

performance of non-

executive directors? 71.43 100.00 28.57 0.00 85.71

According to the table 4.14 Vijaya Bank is displaying least disclosure for the all the variable

related to the audit qualifications, training for board members and the pear group of BOD.

103

Table: 4.15

Other Corporate Governance Requirements (A)

Sl.

No.

Other Corporate

Governance Requirements

Corporation

Bank

Canara

Bank PNB

Vijaya

Bank

Syndicate

Bank

1

If the Profile of directors

appointed during the year

mentioned? 100.00 0.00 100.00 100.00 100.00

2

Whether the Bank has

mentioned Code of

conduct? 100.00 0.00 100.00 100.00 42.86

3

Whether the CSR initiatives

taken up by the Bank

mentioned? 85.71 100.00 85.71 71.43 57.14

4 Whether there is disclosure

about risk management? 100.00 100.00 100.00 100.00 100.00

The above reveals that Canara Bank has the least disclosure for the information related to the

profile of directors, code of conduct of bank. Syndicate bank has least disclosure for the CSR

initiatives.

Table: 4.16

Other Corporate Governance Requirements (B)

Sl.

No.

Non-mandatory

requirements

Corporation

Bank

Canara

bank PNB

Vijaya

bank

Syndicate

bank

1

Whether segment wise or

product wise performance

part of MD&A? 100.00 100.00 100.00 100.00 100.00

2 Does the Bank have

nomination committee? 71.43 0.00 71.43 85.71 0.00

3

Whether Auditor‟s

certificate provided by the

Bank? 100.00 100.00 100.00 100.00 100.00

4

Whether CEO or CFO

certificate provided by the

Bank? 100.00 100.00 100.00 100.00 100.00

5

Is the Chairman of the

Board Executive or Non

Executive mentioned? 100.00 100.00 100.00 100.00 85.71

6 Are the Independent

directors well defined? 100.00 0.00 0.00 0.00 0.00

Canara bank and Syndicate bank doesn‟t have disclosure related to nomination committee

since they aren‟t having it in the given time frame. Regarding independent directors been

well defined except Corporation bank no banks have proper disclosure.

104

Table 4.17

Dimension wise analysis of the disclosures of five banks for seven years

Sl. No. Dimension Percent

1 Code of governance 100.00

2 Board of Directors 95.00

3 Audit committee 100.00

4 Remuneration Committee 94.29

5 Shareholders Committee 100.00

6 General Body meetings 48.57

7 Disclosures 90.00

8 Means of Communication 88.00

9 General Shareholder information 96.36

10 Non-Mandatory Requirements 66.57

11 Other Corporate Governance Requirements 79.14

Table 4.17 displays disclosure level for five banks for seven years. According to the Clause

49 the board lays down a code of conduct for all the board members and senior management

of the bank. The code of conduct is posted on the website of the bank. In the present study the

code of governance is showing hundred percent disclosures for all the banks.

Disclosures related to the board of directors includes composition and category of directors,

attendance of each director at the board meetings, number or boards or board committee in

which he or she is a member or chairperson, and number of meetings held, dates on which

held. Board of directors has disclosures of 95%.

Qualified and independent audit committee with financially literate and at least one member

having accounting or related financial management expertise is set up by all the banks

according to the norm. The audit committee is displaying hundred percent disclosures by

banks.

Disclosure in relation to the remuneration committee is showing 94.29%. It reveals

information about the brief description of terms of reference, composition, name of members,

chairperson, attendance during the year, remuneration policy and details of remuneration to

all the directors.

105

Shareholder‟s committee is showing hundred percent disclosures. Shareholders committee

includes the name of non executive director heading the committee, name and designation of

compliance officer, number of shareholders compliant received so far, number not solved to

the satisfaction of shareholders and number of pending complaints.

General Body meetings location and time, where last three AGMs held, whether any special

resolutions passed in the previous 3 AGMs, whether any special resolution passed last year

through postal ballot – details of voting pattern, person who conducted the postal ballot

exercise, whether any special resolution is proposed to be conducted through postal ballot,

procedure for postal ballot shows 48.57% disclosures, though it is mandatory variable the

disclosure level is very low.

Disclosures on materially significant related party transactions that may have potential

conflict with the interests of company at large, Details of non-compliance by the company,

penalties, strictures imposed on the company by Stock Exchange or SEBI or any statutory

authority on any matter related to capital markets, during the last three years, Whistle

Blower policy and affirmation that no personnel has been denied access to the audit

committee and details of compliance with mandatory requirements and adoption of the non

mandatory requirements of clause shows 90% disclosures.

Means of communication with 88% disclosures includes disclosure related to newspapers

wherein results normally published, any website, where displayed whether it also displays

official news releases; and the presentations made to institutional investors or to the analysts.

General shareholder information includes details about the annual general meeting, date,

time venue, financial year, book closure date, dividend payment date, listing on stock

exchanges, stock code, market price data, performance in comparison to broad based indices,

registrar and transfer agents, share transfer system, distribution of shareholding,

dematerialization of shares and liquidity, outstanding Global Depository

Receipts(GDRs)/American Depository Receipts(ADRs), plant location, address for

correspondence. It shows 96.36% disclosures.

106

Non mandatory requirements has 66.57% disclosures includes disclosure related to the board,

about the person who is being appointed as an independent director has the requisite

qualifications and experience which would be of use to the company and which, in the

opinion of the company, would enable him to contribute effectively to the company in his

capacity as an independent director.

Remuneration Committee information under non mandatory requirement includes bank‟s

policy on specific remuneration packages for executive directors including pension rights and

any compensation payment, to avoid conflicts of interest, the remuneration committee, which

would determine the remuneration packages of the executive directors may comprise of at

least three directors.

It also contains information that the members of committee all of whom should be non-

executive directors, the chairman of committee being an independent director, all the

members of the remuneration committee could be present at the meeting, the Chairman of the

remuneration committee could be present at the Annual General Meeting, to answer the

shareholder queries.

The variables of non mandatory requirement includes information about the Shareholder

Rights, Audit qualifications, Training of Board Members, Mechanism for evaluating non-

executive Board Members and Whistle Blower Policy. Other corporate governance

disclosures display 79.14% disclosures.

107

Table: 4.18

CG Variables with hundred percent disclosures

Sl.

No. CG variable

1 Does the bank have brief statement on its philosophy on the code of governance?

2

Board of Directors: Whether the bank have mentioned Composition and category of

directors, for example, promoter, executive, non-executive, independent non-

executive, nominee director, which institution represented as lender or as equity

investor?

3 Does the Bank have attendance of each director at the Board meetings and the last

AGM mentioned in the report?

4 Whether the Bank has mentioned the number of Board meetings held and the date on

which those meetings were held?

5 Audit Committee: Does the Bank have brief description of terms of reference of

Audit committee?

6 Whether the Bank has mentioned the Composition, name of members and Chairperson

of the Audit committee?

7 Have the Meetings and attendance during the year been recorded by the Bank?

8 Remuneration Committee: Does the Bank give brief description of terms of

reference of Remuneration Committee?

9 Shareholders Committee: Whether the name of non-executive director heading the

committee mentioned in the report?

10 Does the Bank mention the name and designation of compliance officer of

Shareholder Committee?

11 Whether the number of shareholders‟ complaints received so far mentioned by the

Bank

12 If the number of complaints not solved to the satisfaction of shareholders mentioned?

13 If the Number of pending complaints mentioned by the Bank?

14 General Body meetings: Does the Bank mention the location and time, where last

three AGMs were held?

15 Does the bank display Newspapers wherein results normally published?

16 Disclosures: Whether disclosures on materially significant related party transactions

that may have potential conflict with the interests of bank at large made?

17

Whether following is included in the disclosure: Details of non-compliance by the

company, penalties, and strictures imposed on the company by Stock Exchange or

SEBI or any other statutory authority, on any matter related to capital markets, during

the last three years?

18 Whether the Details of compliance with mandatory requirements and adoption of the

non-mandatory requirements of this clause given?

19 Means of communication: Whether the Quarterly results disclosed?

20 Does the bank disclose name of the website, where displayed?

21 Whether the official news releases has been disclosed?

22 Whether management discussion and analysis is a part of annual report or not?

23 Whether the Bank has updated General Shareholder information related to: AGM :

Date, time and venue?

24 Financial year

108

25 Date of Book closure

26 Dividend Payment Date

27 Listing on Stock Exchanges Stock Code

28 Market Price Data : High, Low during each month in last financial year

29 Performance in comparison to broad-based indices such as BSE Sensex, CRISIL

index etc.

30 Registrar and Transfer Agents Share Transfer System

31 Distribution of shareholding Dematerialization of shares and liquidity

32 Branch locations and address of correspondence

33 Whether there is disclosure about risk management?

34 Whether segment wise or product wise performance part of MD&A?

35 Whether Auditor‟s certificate provided by the Bank?

36 Whether CEO or CFO certificate provided by the Bank?

The above table displays the hundred percent disclosures of the CG variable of five banks for

seven years. There are thirty six variables which has hundred percent disclosures for all the

seven years.

The checklist method helped to determine the varied percentage of mandatory, non

mandatory and other corporate governance requirements. Out of forty five variables of

mandatory disclosure requirements fifteen variables is showing varied disclosure level.

Bank‟ philosophy of the code displays hundred percent disclosures which envisages and

expects:-adherence to the highest standards of honest and ethical conduct, including proper

and ethical procedures in dealing with actual or apparent conflicts of interest between

personal and professional relationships.

Full, fair, accurate, sensible, timely and meaningful disclosures in the periodic reports

required to be filed by the bank with government and regulatory agencies.

Compliance with applicable laws, rules and regulations.

To address misuse or misappropriations of the bank‟s assets and resources.

The highest level of confidentiality and fair dealing within and outside the banks.

On the basis of the percentage wise analysis of the disclosure of requirements it was found

that following attributes of the corporate governance didn‟t have hundred percent disclosures

for the period 2005 to 2012.

The procedure for postal ballot has the least disclosure made by the bank. The person

who conducts the postal ballot exercise and the special resolution proposed to be

109

conducted through postal ballot shows 20% disclosures however the details of voting

pattern shows 34.29%. The presentation made to the institutional investors or to the

analysts is displaying 40% for seven years. GDRs/ADRs/Warrants or any Convertible

instruments, conversion date and likely impact on equity shows 60% disclosures.

Whistle Blower policy and affirmation that no personnel have been denied access to the

audit committee has 62.86% disclosures, number of other Boards or Board Committees

in which he/she is a member or a Chairperson shows 80% disclosures, disclosures on

materially significant related party transactions that may have potential conflict with the

interests of bank at large made shows 80% disclosures, details of remuneration to all the

directors, as per format in main report has 82.86%, special resolutions passed in the

previous 3 AGMs been recorded has 85.71% disclosures, composition, name of

members and chairperson of remuneration committee mentioned has 91.43%

disclosures, Bank has mentioned the attendance during the year shows 94.29%

disclosure, Remuneration policy of Bank mentioned in the report shows 97.14%

disclosure the details of compliance with mandatory requirements and adoption of the

non-mandatory requirements of this clause given shows 97.14% disclosures.

In the year 2011-12 the mandatory disclosure level of Punjab national bank is highest.

On the basis of the corporate governance report of five banks following non mandatory

variable is been analyzed. In case of non-executive chairman may be entitled to maintain a

chairman's office at the company's expense its is showing 97.14% disclosures, Whether they

are allowed reimbursement of expenses incurred in performance of his duties shows 77.14%

disclosures.

Though non mandatory but it is desirable to have hundred percent disclosures for effective

governance there is no clear disclosure about the independent director which is showing 0%.

The requirements related to board and the shareholder‟s right is showing 97.14% disclosure.

Whether the boards have set up a remuneration committee to determine on their behalf and

on behalf of the shareholders with agreed terms of reference, the company's policy on

specific remuneration packages for executive directors including pension rights and any

compensation payment shows 97.14% disclosures, in case of variable does the Bank have it

provisions to avoid conflicts of interest, the remuneration committee, which would determine

the remuneration packages of the executive directors may comprise of at least three directors,

all of whom should be non-executive directors, the Chairman of committee being an

110

independent director has 62.86% disclosure, members of the remuneration committee be

present at the meeting has 54.29 % disclosure, half-yearly declaration of financial

performance including summary of the significant events in last six-months has been sent to

each individual shareholders has 97.14% disclosure, Bank may move towards a regime of

unqualified financial statements stated in relation to the audit qualification shows 62.86%

disclosure, training for its Board members shows 60.00% disclosure, Pear Group of BOD to

evaluate the performance of non-executive directors shows 57.14% disclosure.

In case of other corporate governance requirements there are four items which have shown

hundred percent disclosures but other six variables is showing less than hundred percent

disclosures. Though the requirement is non mandatory but it is desirable to have disclosure of

above requirements for the effective governance. Is the Chairman of the Board Executive or

Non Executive mentioned shows 97.14% disclosure and if the Profile of directors appointed

during the year mentioned shows 80 % disclosure. Nomination committee plays a vital role

for better governance has 45.71% disclosure level. There is least disclosure about the

independent directors with 20%. It is important have the code of conduct which has only

68.67% of disclosure.

Out of the five bank analyzed each Bank has taken various innovative Corporate Social

Responsibilities initiatives which contributes to the society. It is found that all the five bank

has given ample importance for rural development, education, self employment, healthcare as

important Corporate Social Responsibilities (CSR) initiatives. CSR initiatives show 80%

disclosure level.

4.2.2 CSR INITIATIVES OF NATIONALISED BANKS

Banks consider CSR as an investment in society. An important facet of the corporate

governance is active participation in the community development programmes with corporate

social responsibility. Banks are engaging themselves in various CSR activities which is

indirectly contributing to their increased market performance Rural development is taken as a

major initiatives by the Nationalised banks, apart from education, employment and women

empowerment. Banks need to have proper disclosure and clear CSR strategy for its better

performance.

Canara Bank has hundred percent disclosure level, Corporation bank and Punjab national

bank displays 85.71%, Vijaya Bank has 71.43% since it took the disclosure of CSR initiative

111

from 2006 onwards, and the disclosure level is low in Syndicate Bank due to taking up the

disclosure of CSR initiatives from 2008 onwards. Banks have been doing various activities

which are socially responsible but having proper disclosure in the relevant field helps in

better performance of the Bank in terms of improving its goodwill and reputation.

Important CSR initiatives of bank are analyzed below.

Canara Bank: So far, the Bank has assisted 487 doctors to set up rural clinics in remote

rural areas. The Bank pioneered an innovative scheme called Rural Service Volunteers in

the year 1982. The Jalayoga Scheme was introduced in the year 1996 to commemorate

Bank's 90th year of establishment to provide safe drinking water to Scheduled

caste/Scheduled Tribes/Backward communities of rural areas coming under lead districts

of the Bank. It has set up Rural Resource Development Centre. It has sponsored a Retail

Mobile Marketing Van for Display cum Sale of House hold products, articles made by

Self - Help Groups, Small women entrepreneurs, Artisans, Self Employed women etc.

Canara Bank has been conferred award for its initiatives.

Punjab National Bank: Bank has taken various CSR initiatives such as development of

village Sacha Khera as a Model Village, vocational trainings 3 months‟ duration trainings

on sewing, cutting and embroidery for ladies. Besides, trainings on preparation of home

made goods like pickle, papad etc. are also being organized with the help of NGOs. PNB

regards Corporate Social Responsibility (CSR) as an investment in society. It has

undertaken corporate volunteering where a growing number of our employees are

committed to civic leadership and responsibility.

The Bank has set up numerous training institutes and counselling centres to eradicate

unemployment. It has taken initiatives in health care and education too. It is bagging CSR

awards consistently for its rural development, Self employment, community services,

Sports, Women empowerment and environment concerns. It has disclosed a separate

report on CSR from 2010 onwards.

Corporation Bank: The Bank has also involved itself with several initiatives in the field

of Education, development of infrastructure, rural development, Health and Hygiene and

Promotion of Art and Culture. During the year the Bank initiated several welfare

measures focusing on the basic needs and for the larger benefit of the society, to fulfill its

commitment to social priorities as a responsible.

112

The Bank has extended donations to Jaycees Society for Rehabilitation of the

Handicapped, a school for special children and Malabar Rehabilitation Centre for

Handicapped, Payyanur, a rehabilitation centre for physically handicapped. As part of its

Centenary celebrations, the Bank had launched the project of setting up 100 rural libraries

at identified rural centres across the country, to be developed as Rural Knowledge

Centres, in association with local Village Panchayats/Educational institutions. It has

announced scholarships to pursue higher studies too. The Bank has taken up the project

of developing infrastructure in the campus of Mangalore University-Mangala Gangothri

and extended financial support to Ramakrishna Mission, Mumbai for organizing youth

oriented projects. The Bank also funded the Armed Forces Flag Day in Mumbai and

Mangalore.

Syndicate bank :Syndicate bank has also taken various CSR initiatives such as cleaning

village tanks and ponds, helping flood victims, supporting the cause of gift of vision that

is corneal transplantation in rural areas, providing educational facilities for poor students

in rural areas, serving policemen and their families, free medical facilities for poor by

donating artificial limbs, wheel chair and providing gainful employment for tribal‟s.

Uplift of downtrodden, education for poor students, distribution of free meal to school

children, integrated tribal development, rehabilitation of Endosulfan victims are some of

the other CSR activities of the bank.

Vijaya Bank: Vijaya Bank has earmarked its CSR fund towards rural development,

women empowerment, Self employment, healthcare and literature. It has established rural

Health Centre and provided free services of a doctor and medicines at a Capital cost of

Rs. 10000.00 and a recurring cost of Rs. 15000 per month for each village, adoption of

one girl child with Educational expenses borne by the Bank up to graduation level,

construction of Bus Shelter in the village incurring a cost of Rs. 2 lakh per village,

providing of water tank and construction of flag mast to village schools at a cost of Rs.

20,000 per village. Bank has constructed a bus shelter a cost of Rs. 1.50 Lakhs in

Wazirpur village in Rajasthan state. Besides, Bank also was instrumental in setting up a

Computer training centre at Mangalore for imparting free computer training to the under

privileged children. Bank also provided Cots and essential furniture items to Daari Deepa

Old Age Home at Ramnagara district of Karnataka State. Vijaya Bank has also been

awarded for its CSR initiatives.

113

Out of the five bank analyzed each Bank has taken various innovative CSR initiatives

which contributes to the society. It is found that all the five bank has given ample

importance for rural development, education, self employment, healthcare as important

CSR initiatives.

4.3 ANALYSIS OF BANKS PERFORMANCE

The main focus of this study is to examine the relationship between corporate governance in

the Banks and the Bank performance. An attempt has been made to identify the relationship

between corporate governance proxies and the firm value. In the present study the three

variables are studied. Return on Assets, Capital adequacy ratio and Non-performing Assets

are proxies for asset quality, profitability, and as a measure of supervision of the corporate

governance mechanism. It is helpful in effective supervision of banks, it helps in taking

prompt corrective action and for better compliance.

Capital Adequacy Ratio: It is the ratio of capital fund to risk weighted assets expressed in

percentage terms and is used to check the availability of the bank‟s capital to cover for its

risk-weighted assets. Banks need to maintain CAR at 9% and a higher level of capital funds.

The important objective of CAR is to strengthen the soundness and stability of the banking

system. It is also termed as CRAR that is capital to risk weighted assets ratio. It can be

calculated as follows

TIER 1 Capital = (paid up capital + statutory reserves + disclosed free reserves) - (equity

investments in subsidiary + intangible assets + current & b/f losses)

TIER 2 Capital =Undisclosed Reserves + General Loss reserves + hybrid debt capital

instruments and subordinated debts

Risk can either be weighted assets or the respective national regulator's minimum total capital

requirement. If using risk weighted assets – fund based assets such as cash, loans,

investments and other assets then degrees of credit risk expressed as percentage weights have

been assigned by RBI to each such asset.

114

Return on assets (ROA): The return on assets percentage shows how profitable a company's

assets are in generating revenue. ROA is computed as,

ROA=

Return on assets is an indicator of how profitable a company is before leverage and is

compared with companies in the same industry. Since the figure for total assets of the

company depends on the carrying value of the assets, some caution is required for companies

whose carrying value may not be correspondence to the actual market value. Return on assets

is a common figure used for comparing performance of financial institutions (such as banks),

because the majority of their assets will have a carrying value that is close to their actual

market value. Total assets include fixed assets and assets having interest overdue for more

than 90 days. Banks need to maintain ROA at 0.25%. Higher the proportion of average

earnings assets, better would be the resulting return on assets.

Non Performing Assets (NPA): A non performing asset is used to measure the overall

quality of the bank‟s loan book. Banks need to maintain NPA at 10%. It is calculated as

follows,

NPA=

*Assets having interest overdue for more than 90 days.

With a view to moving towards international best practices and to ensure greater

transparency, 90 days overdue norms for identification of NPAs have been made applicable

from the year ended March 31, 2004. There are certain relaxations mentioned for Tier I

Banks and Tier II Banks as defined below, with effect from March 31, 2004.

As on 2011-12 Nationalised banks had the ROA of 0.88, Capital adequacy ratio of 13.03 and

the NPA of 1.43. According to RBI report 2012 Indian banks need to maintain ratios with the

following benchmarking standard with ROA 0.25 percent, CAR with 9 percent and NPA with

10%.

In order to analyze the effect of corporate governance disclosure level to that of bank

performance in the present study these three dependent variables i.e., Return on Assets,

Capital Adequacy Ratio and Non-performing Assets for the period from 2005 to 2012 is

used.

115

Table: 4.19

NPA as percentage to net advances

Bank/Year 2005

-06

2006-

07

2007

-08

2008-

09

2009

-10

2010-

11

2011

-12 Mean SD CV

Corporation

Bank 0.64 0.47 0.32 0.29 0.31 0.46 0.87 0.48 0.2 0.41

Canara Bank 1.12 0.94 0.84 1.09 1.06 1.1 1.46 1.09 0.18 0.16

Punjab

National

Bank

0.29 0.76 0.64 0.17 0.53 0.85 1.52 0.68 0.41 0.6

Syndicate

Bank 0.86 0.76 0.97 0.77 1.07 0.97 0.96 0.91 0.11 0.12

Vijaya Bank 0.85 0.59 0.57 0.82 1.4 1.52 1.72 1.07 0.44 0.41

Mean 0.75 0.7 0.67 0.63 0.87 0.98 1.31

SD 0.28 0.16 0.22 0.34 0.4 0.34 0.33

CV 0.37 0.23 0.34 0.55 0.45 0.35 0.25

The non performing assets have a major impact on profitability and liquidity of the banks

which in long run affect the goodwill and brand image leading to investor withdrawing their

funds. Based on the mean value Canara bank is showing highest value of 1.09 and

Corporation bank with least mean value 0.48.

From the above table we can conclude that Canara Bank shows a high level of NPA

compared to other banks and Corporation Bank has shown good sign of reduction in the NPA

level for the period of 2005 to 2012. The average level of NPA in the year was 0.75 which

has increased to 1.31 in the year 2012.

116

Table 4.20

Capital Adequacy Ratio

Bank/Year 2005-

06

2006-

07

2007-

08

2008-

09

2009-

10

2010-

11

2011-

12 Mean SD CV

Corporation

Bank 13.92 12.76 12.09 13.61 15.37 14.11 13 13.55 0.99 0.07

Canara Bank 11.22 13.5 13.25 14.1 13.43 15.38 13.76 13.52 1.15 0.08

Punjab National

Bank 11.95 12.29 13.46 14.03 14.16 14.11 13 13.29 0.84 0.06

Syndicate Bank 11.73 11.74 11.82 12.68 12.7 13.04 12.24 12.28 0.5 0.04

Vijaya Bank 11.94 11.21 11.22 13.15 12.5 13.88 13.06 12 0.75 0.06

Mean 12.15 12.3 12.37 13.51 13.63 14.16 13

SD 0.92 0.79 0.86 0.54 1.05 0.83 0.54

CV 0.08 0.06 0.07 0.04 0.08 0.06 0.04

Capital is essential and critical to the perpetual continuity of a bank as a going concern.

Banks with reasonable CRAR can absorb the unexpected losses easily and their cost of

funding is also reduced which ultimately improve the profitability of banks. Table highlights

the capital adequacy ratio of five banks for seven years. Corporation bank‟s average capital

adequacy ratio for seven year is 13.55 and Vijaya Bank average capital adequacy ratio is 12.

On the basis of the Capital adequacy ratio we can conclude that except Vijaya Bank and

Syndicate Bank other three banks has capital adequacy which is more than 13% where the

Corporation Bank shows high level of capital adequacy ratio. There is increase in the capital

adequacy ratio from 12.15% to 14.16% from 2005 to 2011 however in 2012 capital adequacy

ratio has declined to 13%.

117

Table 4.21

Return on Assets ( ROA In Percentage)

Bank/Year 2005-

06

2006-

07

2007-

08

2008-

09

2009-

10

2010-

11

2011-

12 Mean SD CV

Corporation

Bank 1.24 1.17 1.29 1.24 1.24 1.21 1.06 1.21 0.07 0.06

Canara

Bank 1.13 0.98 0.92 1.06 1.3 1.42 0.95 1.11 0.17 0.16

Punjab

National

Bank

1.09 1.03 1.15 1.39 1.44 1.34 1.19 1.23 0.15 0.12

Vijaya

Bank 0.45 0.92 0.75 0.59 0.76 0.72 0.66 0.69 0.14 0.2

Syndicate

Bank 0.91 0.91 0.88 0.81 0.62 0.76 0.81 0.81 0.1 0.12

Mean 0.96 1 1 1.02 1.07 1.09 0.93

SD 0.28 0.09 0.19 0.29 0.32 0.29 0.19

CV 0.29 0.09 0.2 0.28 0.3 0.27 0.2

The above table shows the ratio of return on total assets for the period of 2005-12 for five

banks. The average return of the bank is high in case of Punjab National Bank i.e., 1.23% and

least in case of Vijaya Bank. The ratio in terms of dispersion that is Coefficient of Variation

(CV) shows more variable in case of Vijaya Bank and less variable in case of Corporation

Bank.

Therefore in terms of dispersion Vijaya Bank is less consistent and Corporation Bank is more

consistent. The average return of banks was 0.96% in 2005-06 which has decreased to 0.93%

in 2012.

118

Table 4.22

Descriptive Statistics of dependent variables

Based on the descriptive statistics the mean value of the all the five banks is observed in the

below table.

VARIABLE Minimum Maximum Mean Std. Deviation

ROA Corporation Bank 1.06 1.29 1.2071 .07432

ROA Canara Bank .92 1.42 1.1086 .18872

ROA Vijaya Bank .45 .92 .6929 .14762

ROA PNB 1.03 1.44 1.2329 .15777

ROA Syndicate Bank .62 .91 .8143 .10277

CRA Corporation Bank 12.09 15.37 13.5514 1.06651

CRAR Canara Bank 11.22 15.38 13.5200 1.23996

CRAR Vijaya Bank 11.21 13.88 12 1.01775

CRAR PNB 11.95 14.16 13.2857 .90235

CRAR Syndicate Bank 11.73 13.04 12.2786 .53561

NPA Corporation Bank .29 .87 .4800 .21166

NPA Canara Bank .84 1.46 1.0871 .19311

NPA Vijaya Bank .57 1.72 1.0671 .46995

NPA PNB .17 1.52 .6800 .44294

NPA Syndicate Bank .76 1.07 .9086 .11539

The above table depicts the three important triggers ROA, CAR and NPA level of five banks

for seven years. It shows the mean value and the standard deviations. Return on assets of

PNB is highest with mean value of 1.2329 and is lowest for Vijaya Bank with mean value of

.6929. Capital adequacy ratio of Corporation bank is highest with the mean value of 13.5514

and the Vijaya bank has lowest mean value of 12. NPA of Corporation banks shows the mean

value of .4800 which is better compared to other banks and the Canara bank has the highest

NPA level with mean value of 1.0871.

119

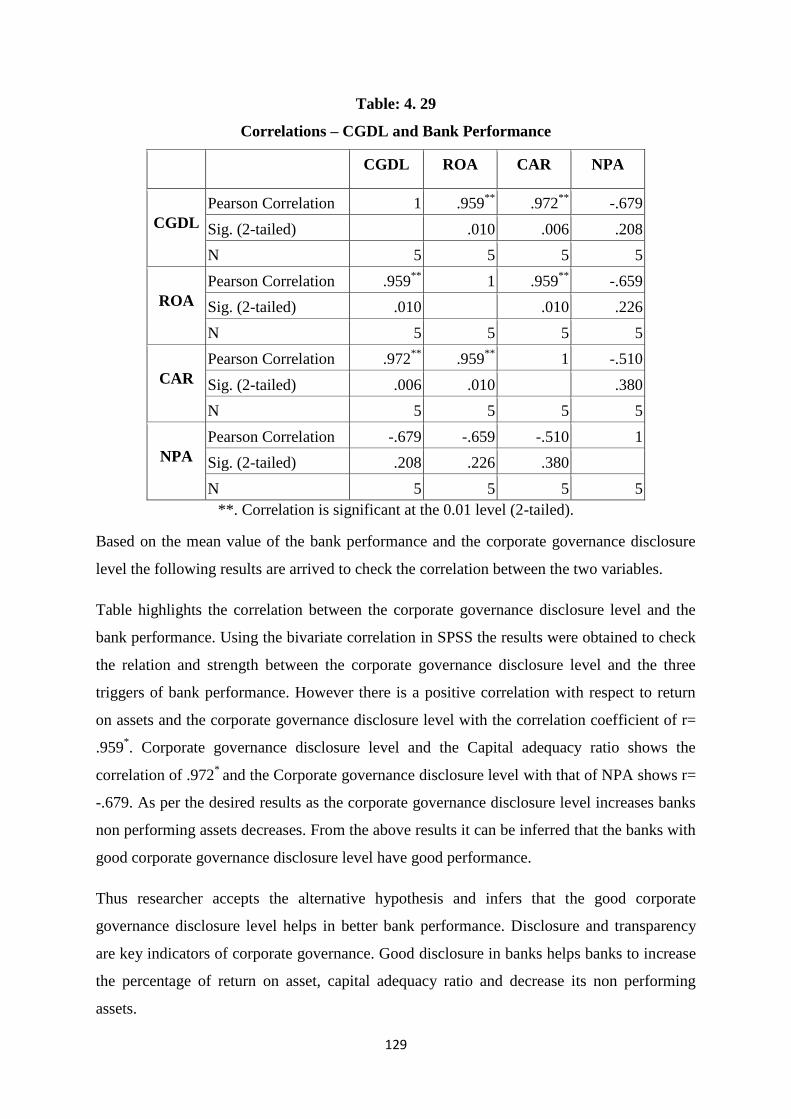

4.4 CORPORATE GOVERNANCE DISCLOSURE LEVEL AND BANK

PERFORMANCE

In order to examine the relationship between corporate governance disclosure level and the

performance of the bank‟s annual report the bank performance indicators that is ROA, CAR,

NPA were used and Corporate governance disclosure level of five banks was determined

based on the Corporate governance index prepared using 65 requirements that is mandatory,

non mandatory and other corporate governance requirements.

H0: The extent of corporate governance disclosure level and bank performance is not

related

Table: 4.23

Corporation Bank- Correlation Matrix

CGDI (Corporate governance disclosure index) is expected to have a negative relationship

with bank‟s NPA. To test this relationship Pearson Correlation Matrix analysis was

performed with CGDI and bank‟s NPA for the period 2005–2012. The analysis indicated a

partial strong positive correlation with the selected variables, i.e. r = -0.31798 & p-value =

0.487052 Therefore from the above table it is inferred that in case of Corporation Bank ,

YEAR NPA CAR ROA CGDL CGDL-NPA CGDL-CAR CGDL-ROA

2005-

06 0.64 13.92 1.24 52 r p r p r p

2006-

07 0.47 12.76 1.17 56

-

0.31798 0.487052 -0.01191 0.979782

-

0.09851 0.833577

2007-

08 0.32 12.09 1.29 59

2008-

09 0.29 13.61 1.24 59

2009-

10 0.31 15.37 1.24 59

2010-

11 0.46 14.11 1.21 59

2011-

12 0.87 13 1.06 59

r - Correlation Coefficient, p - Significance Value at 5%

120

CGDI & NPA are showing the same trend & they both move in the same direction exhibiting

a negative relationship. This result is matching with the general expectation which suggests

that, as the CGDI increases the resultant NPA should come down & indicates an

improvement in performance.

CGDI is expected to have a positive relationship with bank‟s CRAR. To test this relationship

Pearson Correlation Matrix analysis was performed with CGDI and bank‟s CRAR for the

period 2005–2012. The analysis indicated a negative correlation with the selected variables,

i.e. r = -0.01191& p-value = 0.979782. This result is not matching with the general

expectation which suggests that, as the CGDI increases the resultant CRAR should increase

& reflect an improvement in performance.

CGDI is expected to have a positive relationship with bank‟s ROA. To test this relationship

Pearson Correlation Matrix analysis was performed with CGDI and bank‟s ROA for the

period 2005–2012. The analysis indicated a partial strong positive correlation with the

selected variables, i.e. r = -0.09851 & p-value = 0.833577. Therefore from the above table it

is inferred that in case of Corporation Bank CGDI & ROA are not showing the same trend &

they both are not moving in the same direction. They are exhibiting a negative relationship.

This result is not matching with the general expectation which suggests that, as the CGDI

increases the resultant ROA should increase which helps in the improvement in performance.

121

Table 4.24

Canara Bank- Correlation Matrix

YEAR NP

A CAR

RO

A

CGD

L CGDL-NPA CGDL-CAR CGDL-ROA

2005-

06 1.12

11.2

2 1.13 55 r p r p r p

2006-

07 0.94 13.5 0.98 55

0.583588 0.16897 0.65129 0.113047 0.48858 0.265896

2007-

08 0.84

13.2

5 0.92 55

2008-

09 1.09 14.1 1.06 56

2009-

10 1.06

13.4

3 1.3 56

2010-

11 1.1

15.3

8 1.42 56

2011-

12 1.46