CREATING VALUE IN FINANCIAL SERVICES - · PDF fileCREATING VALUE IN FINANCIAL SERVICES by...

35

CREATING VALUE IN FINANCIAL SERVICES by Michael Pinedo Sridhar Seshadri Presentation at the “Vision Into Reality Conference”

Transcript of CREATING VALUE IN FINANCIAL SERVICES - · PDF fileCREATING VALUE IN FINANCIAL SERVICES by...

CREATING VALUE INFINANCIAL SERVICES

byMichael Pinedo

Sridhar Seshadri

Presentation at the “Vision Into Reality Conference”

The topics covered in thispresentation are from thisbook. You can view it atthe following web page.

Http://www.stern.nyu.edu/om/cvfs.html

Overview of Talk

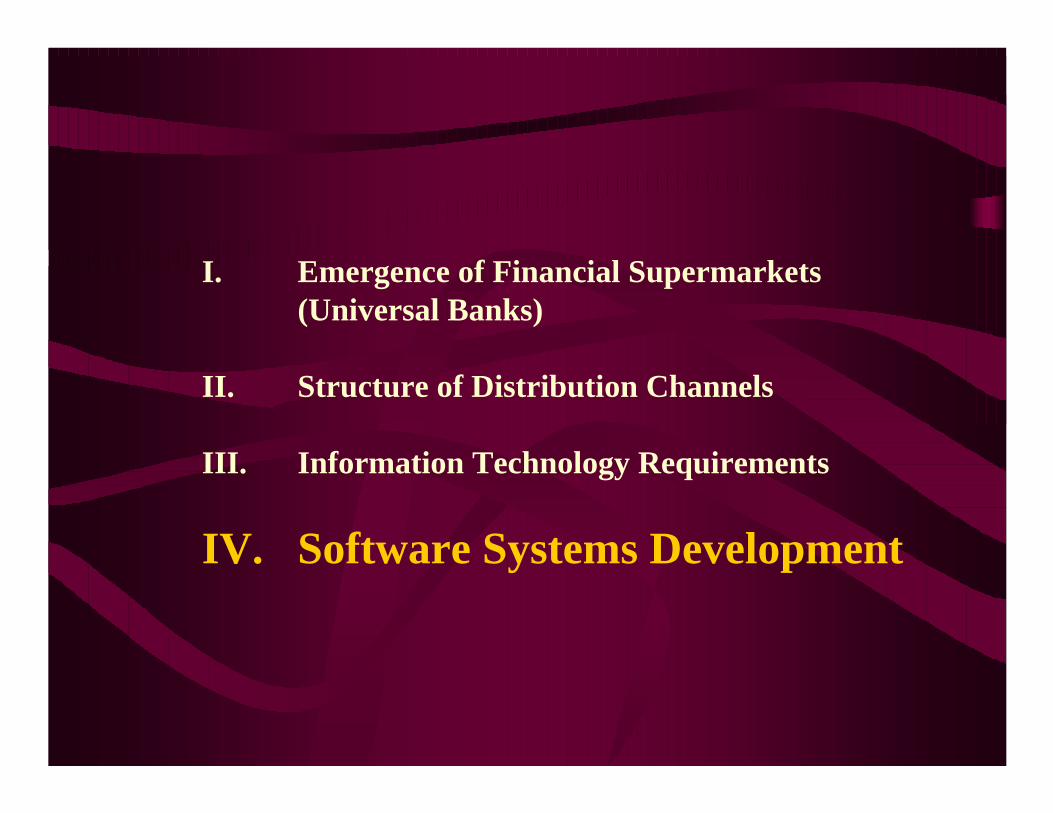

I. Emergence of Financial Supermarkets(Universal Banks)

II. Structure of Distribution Channels

III. Information Technology Requirements

IV. Software Systems Development

I. Emergence of Financial Supermarkets(Universal Banks)

II. Structure of Distribution Channels

III. Information Technology Requirements

IV. Software Systems Development

Emergence of Global FinancialSupermarkets (Universal Banks)

Examples:

• Citigroup• HSBC• Deutsche• ABN-AMRO• ING

Product Divisions•Retail Banking (Checking Accounts, Personal Loans, Mortgages)

•Credit Card Operations

•Commercial Banking (Loans, Letters of Credits)

•Investment Banking (Investment Advice, Trading)

•Brokerage (Stock Portfolio Accounts, Cash Management Accounts)

•Mutual Funds (Managed Equity funds, Index funds, Bond funds)

•Insurance (Life, Property and Casualty)

•How many clients prefer a one-stop supermarket?

•What is potential for Cross-Sales?

Þ Customer Relationship Management (CRM)

New Kid on the Block

I. Emergence of Financial Supermarkets(Universal Banks)

II. Structure of Distribution Channels

III. Information Technology Requirements

IV. Software Systems Development

Distribution Channels

•Branches

•Mini-Branches, Kiosks

•ATM Networks

•Phone, Call Centers

•PC-Banking, Internet

•Sales Force, Agents

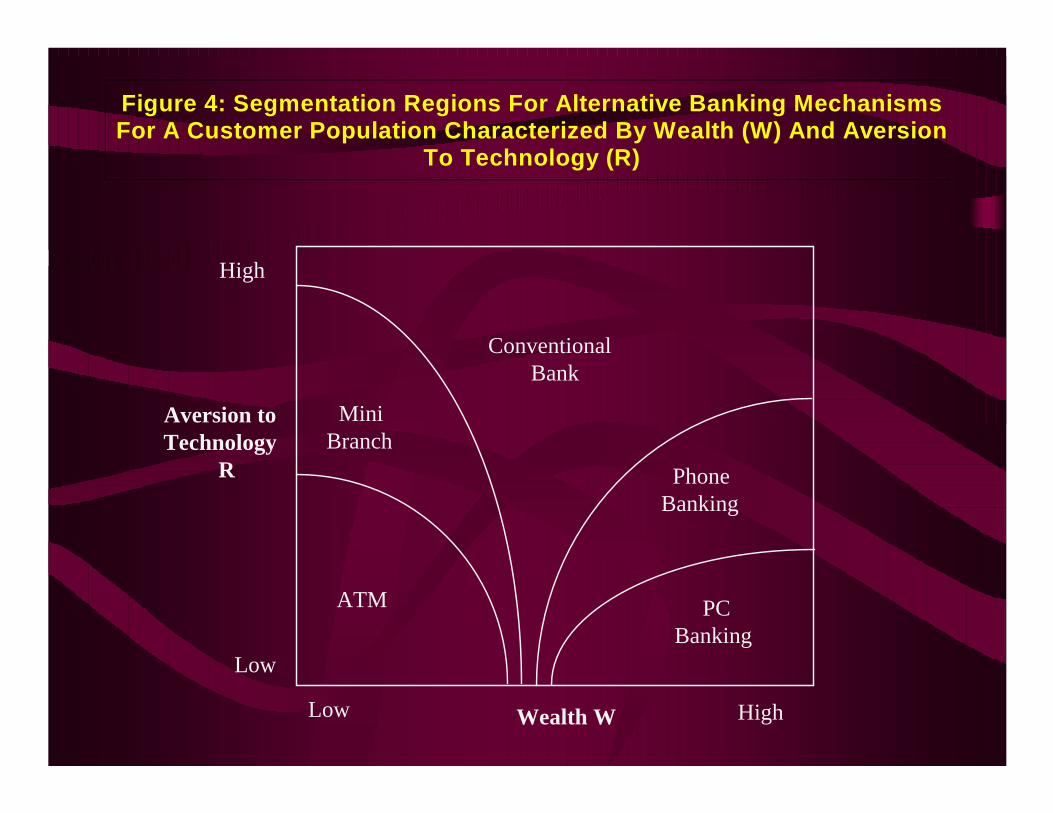

Figure 4: Segmentation Regions For Alternative Banking MechanismsFor A Customer Population Characterized By Wealth (W) And Aversion

To Technology (R)

Wealth W

Aversion toTechnology

R

ATM

ConventionalBank

PhoneBanking

PCBanking

MiniBranch

Low

Low High

High

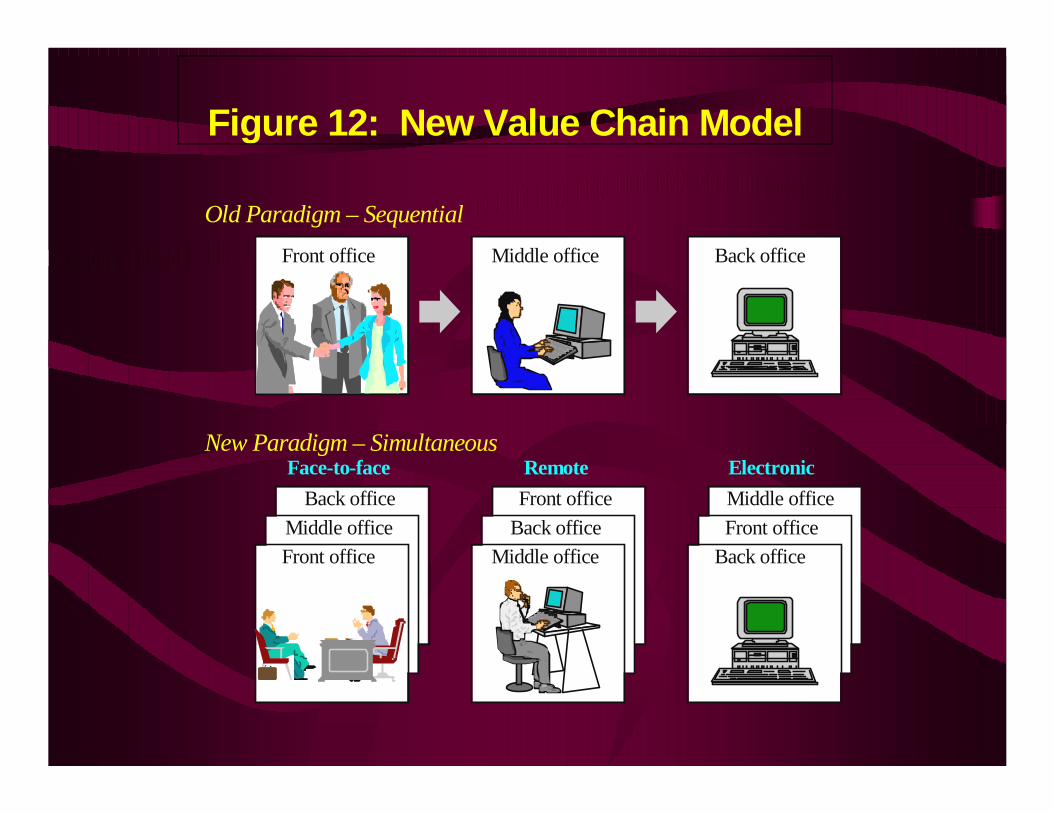

Figure 12: New Value Chain Model

Front officeBack office

Middle office

Front office Middle office Back office

Front officeBack office

Middle office

Middle office

Front office

Old Paradigm – Sequential

New Paradigm – SimultaneousFace-to-face Remote Electronic

Back office

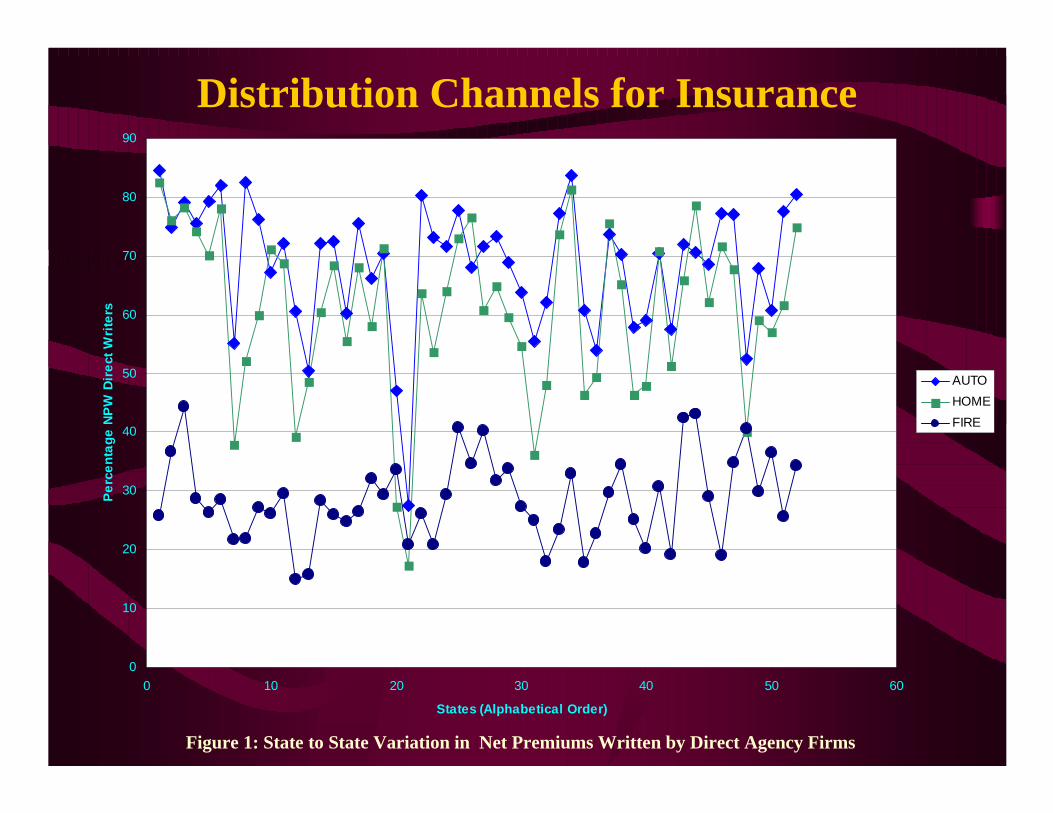

Distribution Channels for Insurance

0

10

20

30

40

50

60

70

80

90

0 10 20 30 40 50 60

States (Alphabetical Order)

Pe

rce

nta

ge N

PW

Dire

ct W

rite

rs

AUTO

HOME

FIRE

Figure 1: State to State Variation in Net Premiums Written by Direct Agency Firms

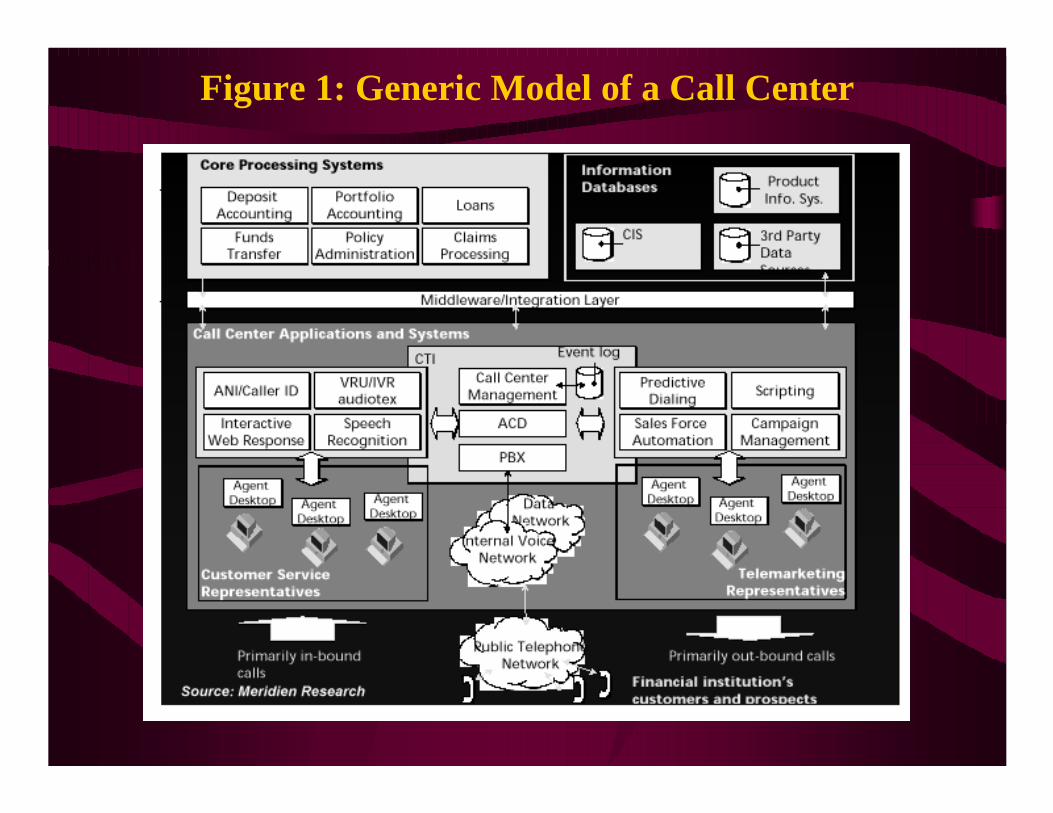

Figure 1: Generic Model of a Call Center

I. Emergence of Financial Supermarkets(Universal Banks)

II. Structure of Distribution Channels

III. Information Technology Requirements

IV. Software Systems Development

Exhibit 3: Information Technology Spending Levels

First Chicago

Banc One

Credit Suisse

Wells Fargo

Societe Generale

SBC

ABN Amro

Bankers Trust

Nations Bank

Credit Agricole

UBS

JP Morgan

NatWest

Bank of America

Barclays

Credit Lyonnais

Deutsche Bank

Chase

Citicorp

0 0.5 1 1.5 2$ billions

Source: The Tower Group, 1996.

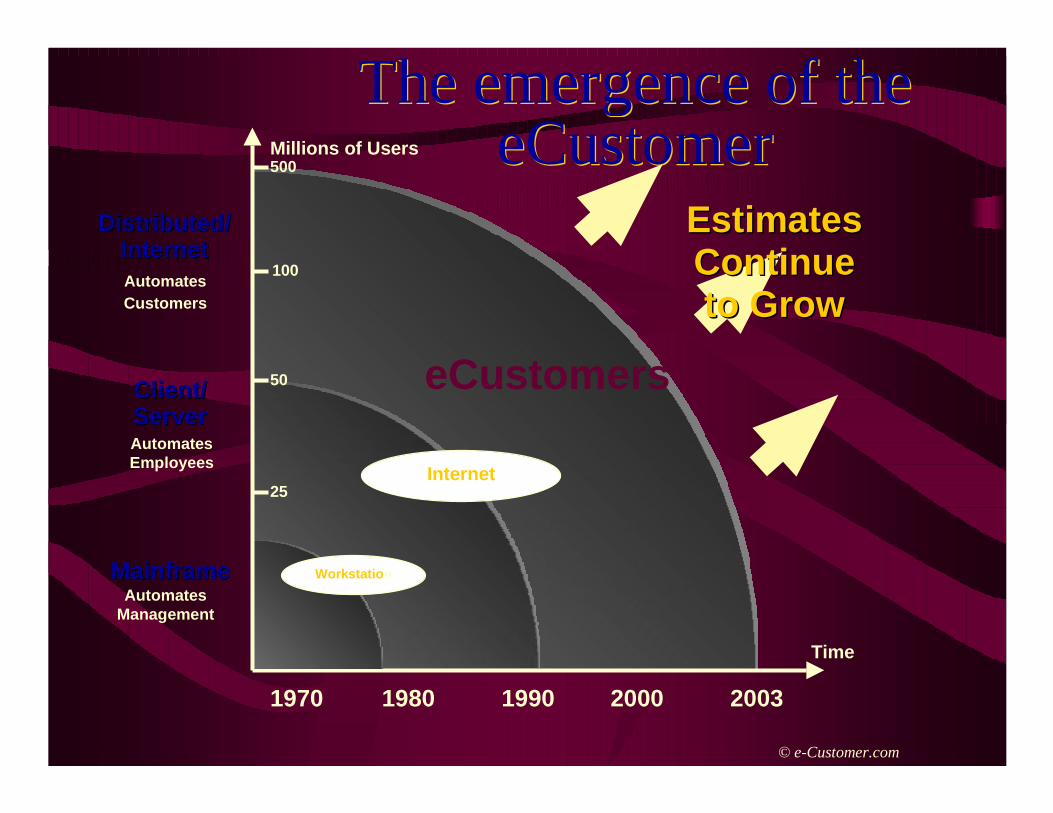

The emergence of theeCustomer

The emergence of theeCustomer

1970 1980 1990 2000 2003

Time

E s timatesE s timatesContinueContinueto Growto Grow

eCustomers

Millions of Users

Distributed/Dis tributed/InternetInternetAutomatesCustomers

Client/Client/S erverS erverAutomatesE mployees

MainframeMainframeAutomates

Management

100

500

Workstatio n

Internet25

50

© e-Customer.com

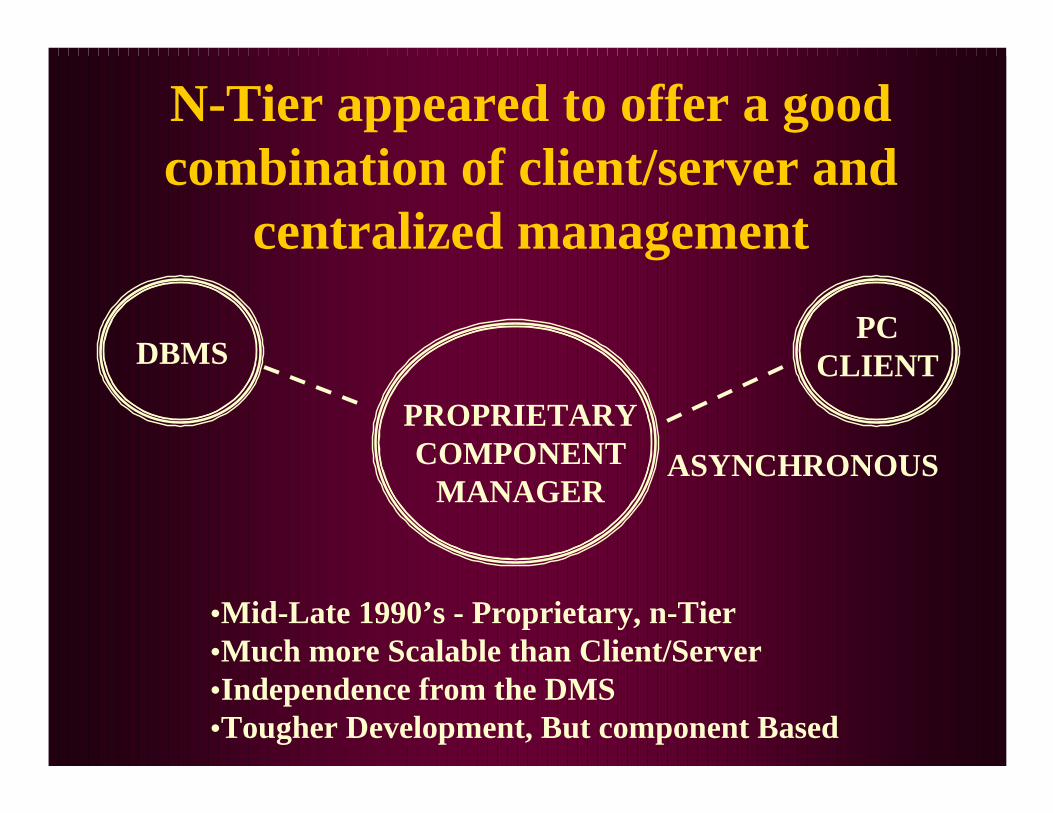

N-Tier appeared to offer a goodcombination of client/server and

centralized management

•Mid-Late 1990’s - Proprietary, n-Tier•Much more Scalable than Client/Server•Independence from the DMS•Tougher Development, But component Based

DBMSPC

CLIENT

PROPRIETARYCOMPONENT

MANAGERASYNCHRONOUS

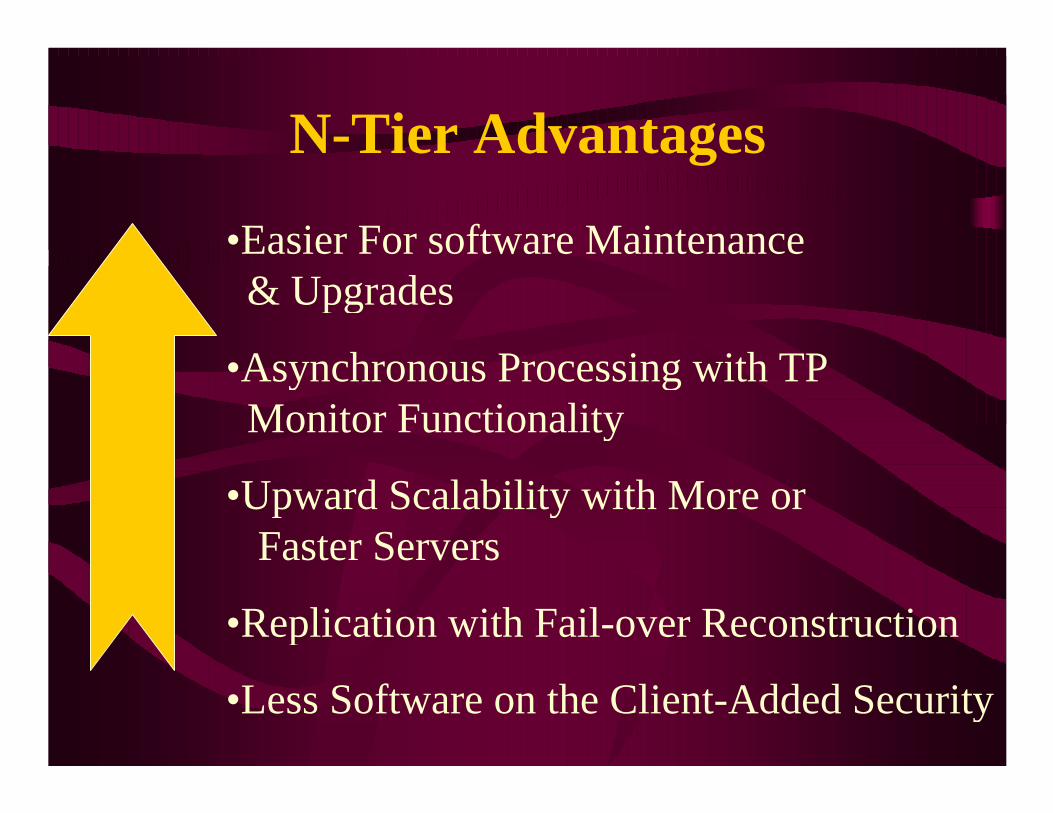

N-Tier Advantages

•Easier For software Maintenance & Upgrades

•Asynchronous Processing with TP Monitor Functionality

•Upward Scalability with More or Faster Servers

•Replication with Fail-over Reconstruction

•Less Software on the Client-Added Security

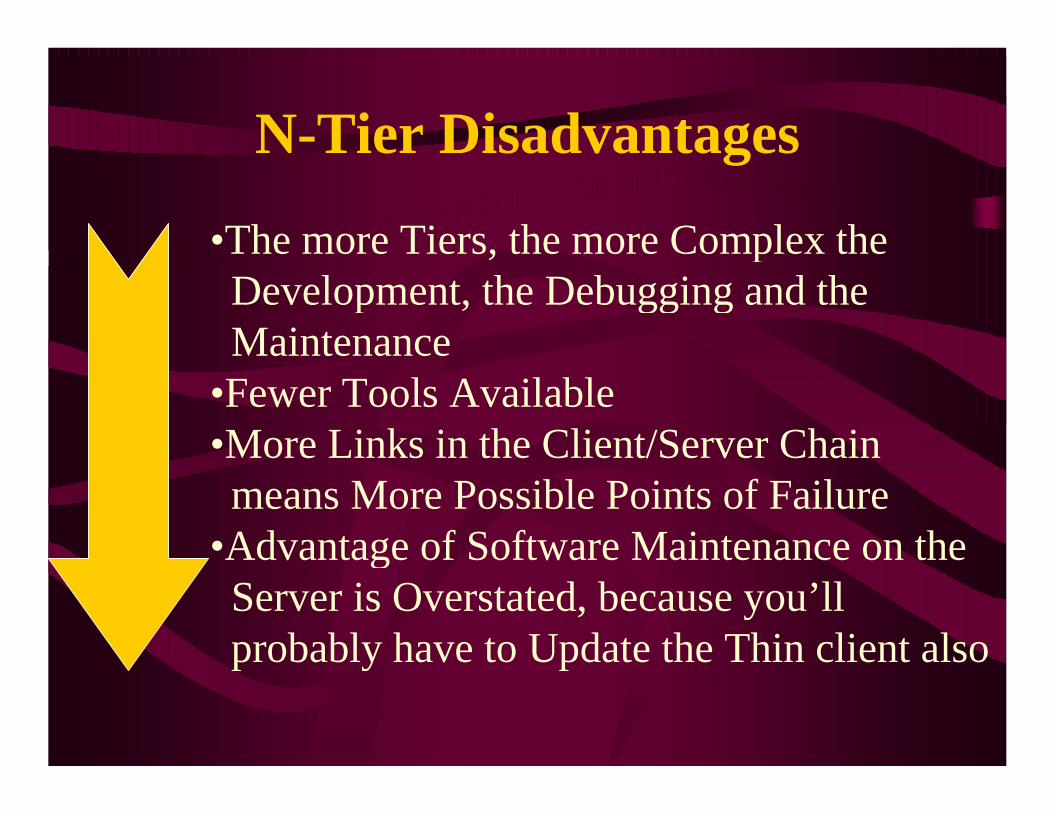

N-Tier Disadvantages

•The more Tiers, the more Complex the Development, the Debugging and the Maintenance•Fewer Tools Available•More Links in the Client/Server Chain means More Possible Points of Failure•Advantage of Software Maintenance on the Server is Overstated, because you’ll probably have to Update the Thin client also

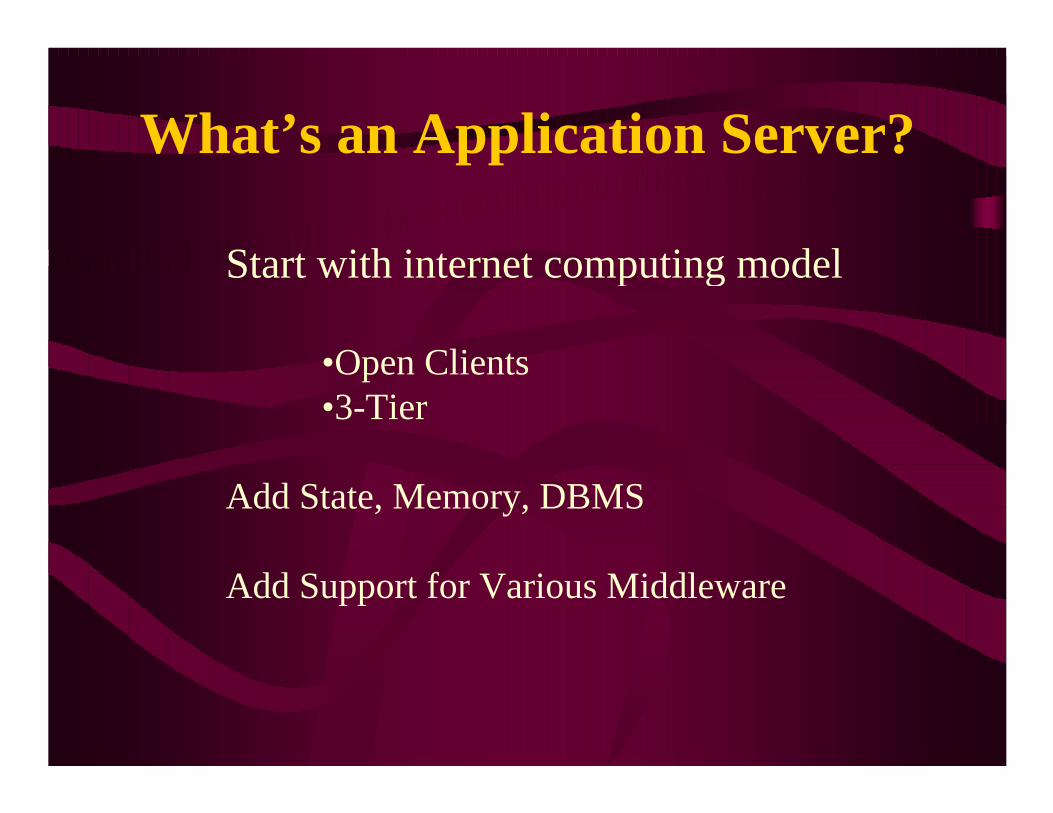

What’s an Application Server?

Start with internet computing model

•Open Clients•3-Tier

Add State, Memory, DBMS

Add Support for Various Middleware

What’s an Application Server?

Add Transaction Management

•Caching & Thread Management•DB Connectivity•Asynchronous Connections•Scalability•Load Balancing•Multiple Instances•Fail-over•Security

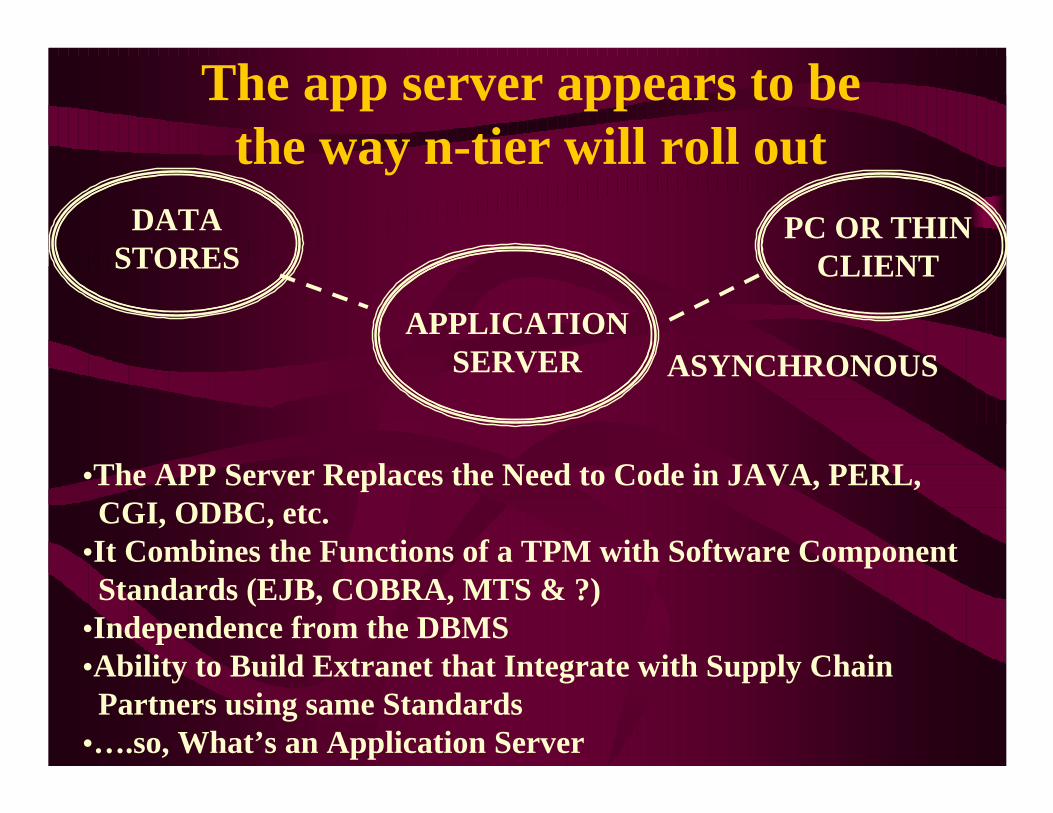

The app server appears to bethe way n-tier will roll out

•The APP Server Replaces the Need to Code in JAVA, PERL, CGI, ODBC, etc.•It Combines the Functions of a TPM with Software Component Standards (EJB, COBRA, MTS & ?)•Independence from the DBMS•Ability to Build Extranet that Integrate with Supply Chain Partners using same Standards•….so, What’s an Application Server

DATASTORES

PC OR THINCLIENT

APPLICATIONSERVER ASYNCHRONOUS

http://www.sun.com/software/solutions/third-party/ecommerce/pdf/etrade.pdf

Will existing ERP solutions fit the bill?

I. Emergence of Financial Supermarkets(Universal Banks)

II. Structure of Distribution Channels

III. Information Technology Requirements

IV. Software Systems Development

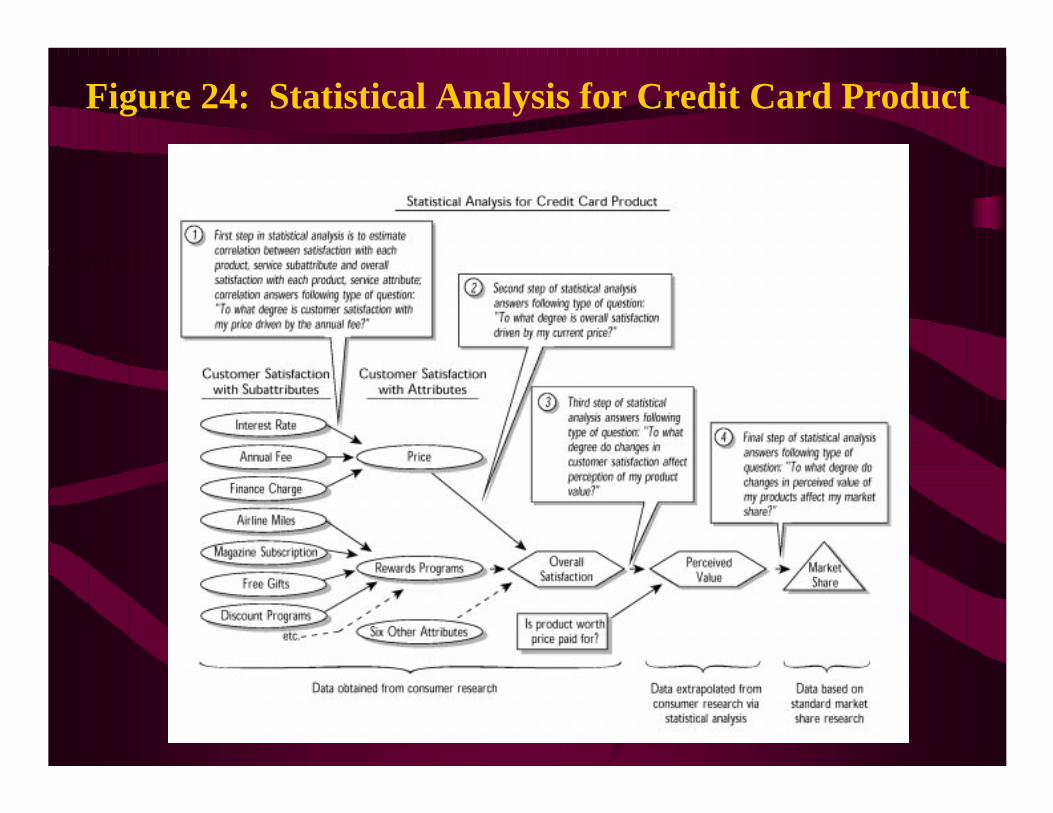

Figure 24: Statistical Analysis for Credit Card Product

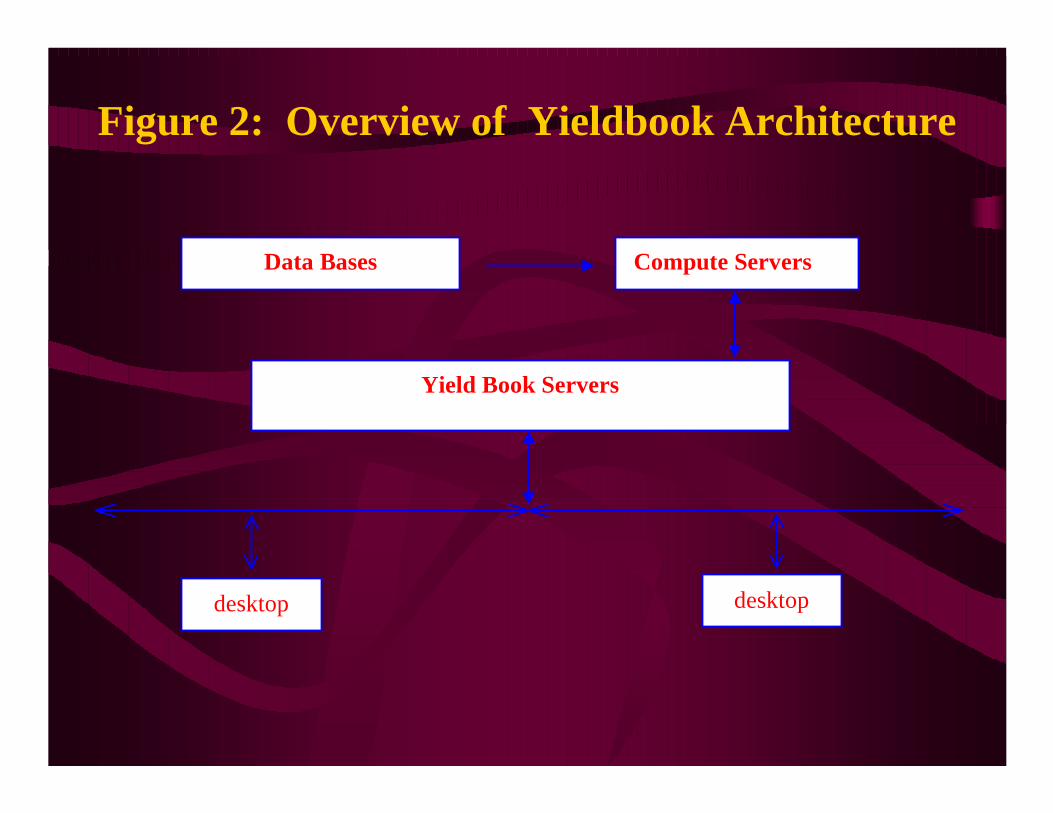

Figure 2: Overview of Yieldbook Architecture

Data Bases Compute Servers

Yield Book Servers

desktop desktop

Figure 1: Screenshot of CMO Cash Flows

Examples of Software Systemsin Financial Services

•Churn Management Systems

•Mortgage Application Expert Systems

•Call Routing Software in Call Centers

•Data Mining for Trading Systems

•Yield Book

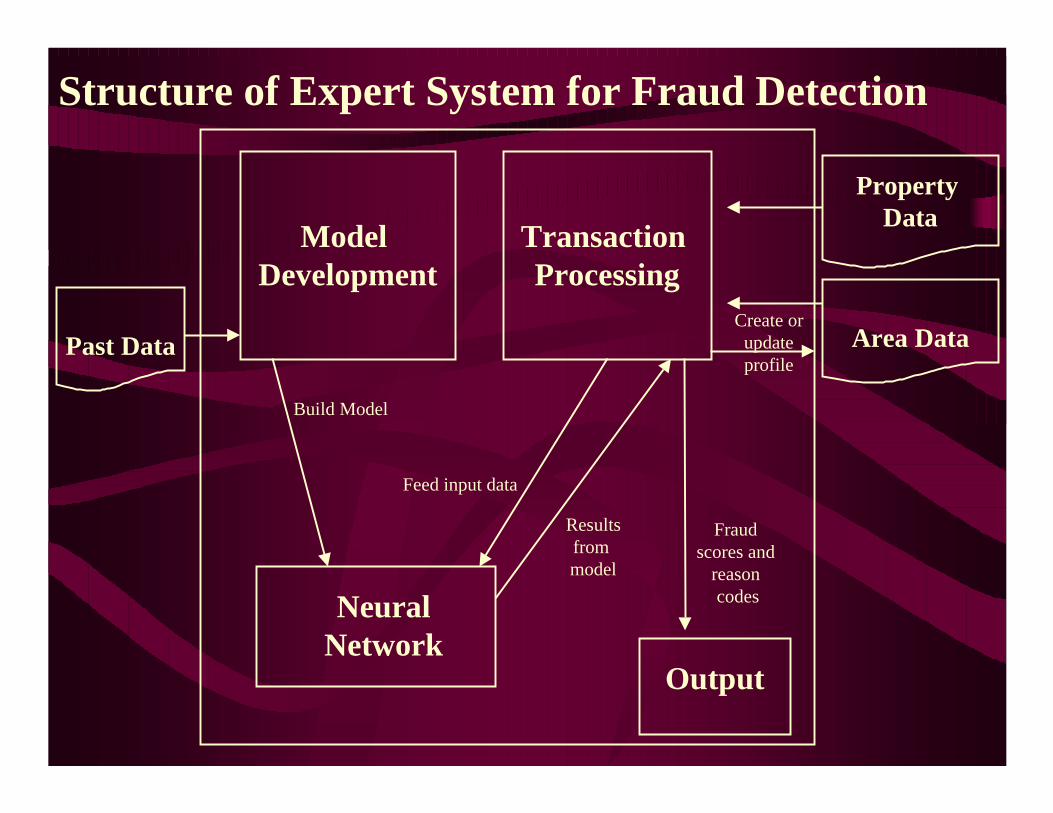

Model Development

Transaction Processing

NeuralNetwork

Output

Fraud scores and

reason codes

Property Data

Area DataCreate orupdateprofile

Past Data

Resultsfrom model

Feed input data

Build Model

Structure of Expert System for Fraud Detection

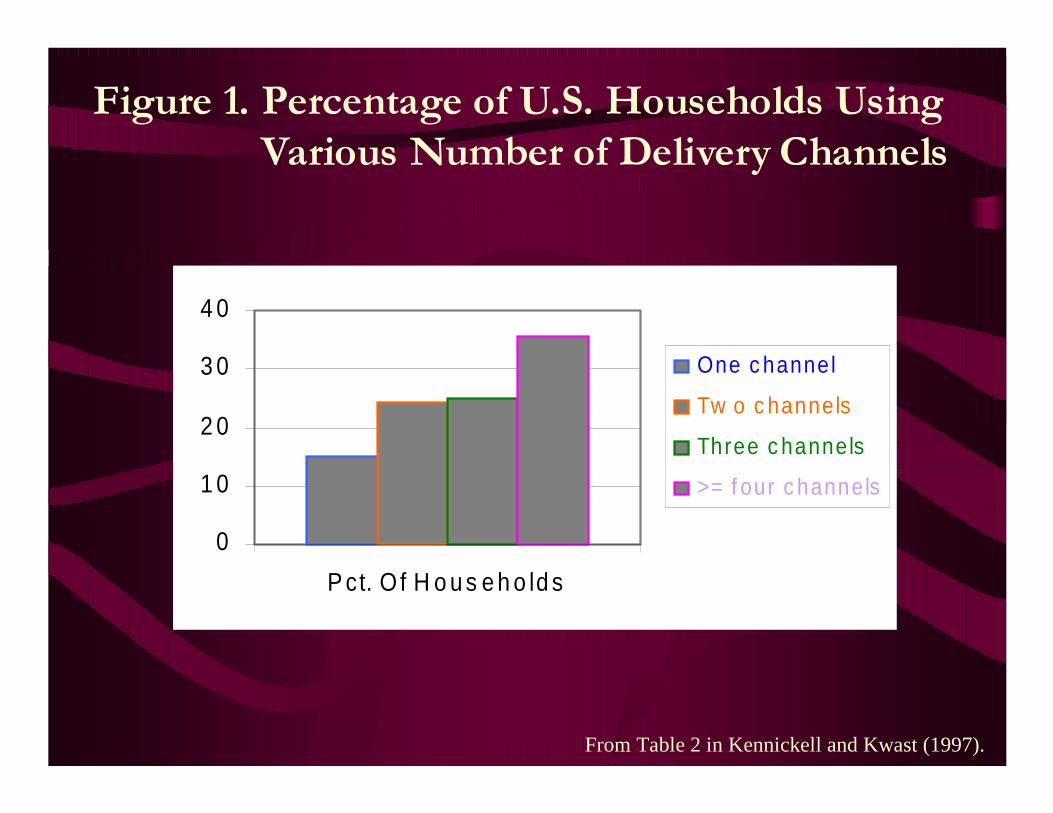

Figure 1. Percentage of U.S. Households Using

Various Number of Delivery Channels

0

1 0

2 0

3 0

4 0

P ct. O f H o u s e h o ld s

One c hannel

Tw o c hannels

Three c hannels

>= f our c hannels

From Table 2 in Kennickell and Kwast (1997).