Corporate Presentation Private Lender...

39

Private Lender Presentation NYSE American: HLTH January 8, 2018 Corporate Presentation 1

-

Upload

vuongxuyen -

Category

Documents

-

view

218 -

download

1

Transcript of Corporate Presentation Private Lender...

PrivateLender PresentationNYSEAmerican:HLTHJanuary8,2018

CorporatePresentation

1

Thispresentationcontainsforward-lookinginformation(withinthemeaningofapplicablesecuritieslaws)relatingtothebusinessofNobilisHealthCorp.(the"Company")andtheenvironmentinwhichitoperates.Forward-lookinginformationmayincludestatementsregardingtheobjectives,businessstrategiestoachievethoseobjectives,expectedfinancialresults,economicormarketconditions,industryspecificinformation,andtheoutlookoforinvolvingtheCompanyanditsbusiness.Suchforwardlookinginformationorstatementsaretypicallyidentifiedbywordssuchas"believe","anticipate","expect","intend","plan","will", "may"andothersimilarexpressions.

Forward-lookinginformation,includinganyfinancialoutlooks,isprovidedforthepurposeofprovidinginformationaboutmanagement'sexpectationsandplansaboutthefutureandmaynotbeappropriateforotherpurposes.Forward-lookinginformationhereinisbasedonvariousassumptionsandexpectationsthattheCompanybelievesarereasonableinthecircumstances.Noassurancecanbegiventhattheseassumptionsandexpectationswillprovetobecorrectandtheforward-lookinginformation,includingthefinancialoutlooksincludedinthisPresentation,shouldnotbeundulyreliedupon.ThoseassumptionsandexpectationsarebasedoninformationcurrentlyavailabletotheCompany,includingthehistoricperformanceoftheCompany'sbusiness.Suchassumptionsincludeanticipatedfinancialperformance,currentbusiness,industryandeconomictrends,andbusinessprospectsandaresubjecttotherisksanduncertaintieswhicharediscussedintheCompany'sregulatoryfilingsavailableontheCompany'swebsiteatwww.NobilisHealth.com,www.sec.gov,oratwww.sedar.com.Anyforward-lookingstatementsthatwe make are based on assumptions as oftoday, and weundertake no obligation to update them.

TheCompany’smanagementhasapproved thefinancialoutlookscontainedinthispresentation.

FORWARD-LOOKINGINFORMATION

2

LOCATIONS

• 10marketsacross5states

• 5surgicalhospitals• 13ASCs

• 13multi-specialtyclinics

• 36partnerfacilities

STRATEGY

• Optimizedcasemixandpayor mixacrosstheportfolio

• Higheracuityproceduresleadingtohigherlevelsofreimbursements

• Focusonminimallyinvasiveprocedures

• Compellingvaluepropositionforphysicians,

patients,andpayors

• LowCap-Exrequirements

• Scalableplatformenablesnationwidegrowth

COMPANYOVERVIEW

DIRECT-TO-PATIENTMARKETINGMODEL

• Brandedproceduresdriveadditionalsurgicalvolumetonation-wide

networkoffacilities• Capitalizesongrowingtrendof‘consumerism’inhealthcare

• Drivesorganicgrowth

$315millioninrevenue&$40millioninAdjustedEBITDA,LTMSeptember2017

MarketswithNobilisownedfacilities

MarketswithNobilispartnerfacilities

3

UNIQUEMARKETINGMODEL• Multiplemarketingchannelsdriveorganicvolumegrowth• Proprietarytechnologyplatformtargetsprospectivepatients• Strongvalueproposition:Superiorpatientexperiencethatexpandsphysicians’practices

ATTRACTIVEFINANCIALPROFILE

PATIENT-CENTRICVALUEPROPOSITION

FAVORABLEPAYORANDPROCEDUREMIX

ATTRACTIVEINDUSTRYFUNDAMENTALS

EXPERIENCEDMANAGEMENTTEAM

• Lowleverage• Lowcapitalexpenditurerequirements• Stablecashbalance

• Uniquemarketingmodelincreasescasevolumeandprovidessuperiorpatientexperience• Offersoptimalsurgicalenvironmentsthatresultinbetteroverallqualityofcare• Offersancillaryservicesthatleadtobetterefficiencyandoutcomes

• Marketingsegmenttargetshigheracuitycasesresultinginahighlyattractivecasemix• Procedurediversificationincreasesthestabilityoftherevenuebase• Minimalgovernmentpayor claimsreducesriskofMedicare/Medicaidratechanges

• 66%ofallsurgeriesareoutpatientwith>50%performedinASCsvs.32%in2005• Lowercost,highqualityoutpatientsetting;trendtowardincreasedconsumerisminhealthcare• Abundanceofdesirableacquisitionopportunitiesduetofragmentedmarket

• StrongmanagementteamwithM&Aandhealthcareexperience• SeasonedOpsteamleadstofinancialandoperationalefficiencies• Strongin-houseandoutsidelegalteamtosafelynavigatecomplexhealthcarespace

INVESTMENTHIGHLIGHTS

4

UNIQUEPATIENTACQUISITIONMODEL

• Acquirespatientsfromphysicianpartnerswhoarenotobligatedtobringcasestotheirfacility

• Physiciansoftenformpartnershipswithinequitablepercentages:

• Productivedoctorsresentlessproductivedoctors

• ManagementCo.onlymanagesanddoesnotdrivepatientstocenters

• Nogrowthdrivers– mustrelyonphysicianpartnerstogrowtheirpracticestothenbringmorepatients

• Noverticalintegration

Traditional Model The Nobilis Model

• Acquirepatientsthrough:• Marketingprograms• Networkofprimarycare

physicianpartners• Physicianemployees

• OwnershipisjustoneofseveralalignmentopportunitiesbetweenphysiciansandNobilis

• Nobilisowns andmanages itsfacilities

Nobilis Health Network / ClinicallyIntegrated Network

Physician Partners

Direct to Consumer Marketing

Joint Marketing with Physicians

Nobilis Health Employed Primary Care Physicians

• Drivepatientflowtoourfacilities

• Controlthepatientexperiencethroughanexpanding continuum ofcare:

• Patientacquisition• Primarycare• Ancillaries• Surgeries• Post-Op

Physician Partners

(Minority Ownership)

5

FAVORABLECASEMIX FAVORABLEPAYORMIX

Note: Unless otherwise dated, figures are based on the LTM period ended 9/30/2017, pro forma for the full year impact of the AZ Vein acquisition.Note 2: Case mix based on number of cases; payor mix based on revenue.

ENT4%

General Surgery4%

Ortho7%

Pain26%

Spine18%

Bariatrics19%

Vein/Vascular4%

Podiatrist2%

GI1%

Plastic Surgery

10%

GYN3%

Migraine2%

AETNA22%

BCBS16%

CIGNA9%

UHC33%

Other Commercial

10%

Self Pay6%

WC3%

Medicare1%

NOBILISBUSINESSOVERVIEW

6

“TargetingHigherAcuityCases” “MinimalGovernmentPayorClaims”

PrivateLender PresentationINDUSTRYOVERVIEW

7

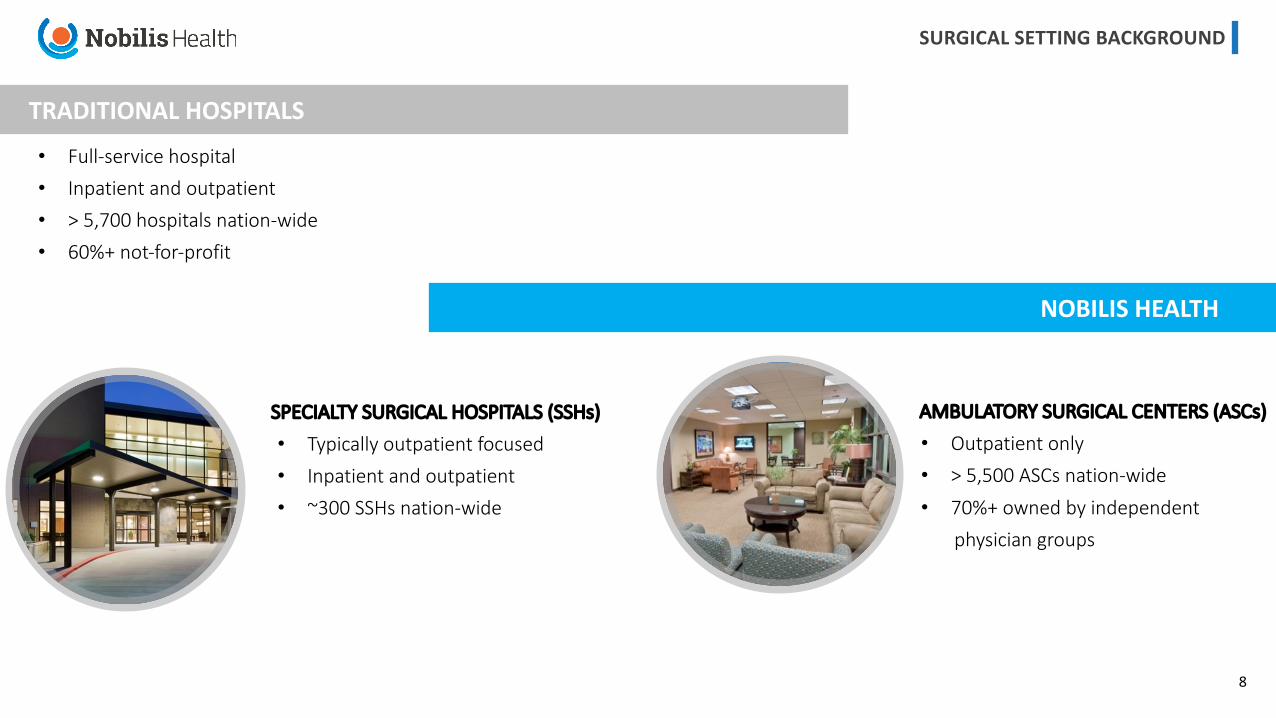

AMBULATORYSURGICALCENTERS(ASCs)

• Outpatientonly• >5,500ASCsnation-wide• 70%+ownedbyindependent

physiciangroups

• Full-servicehospital• Inpatientandoutpatient• >5,700hospitalsnation-wide• 60%+not-for-profit

SPECIALTYSURGICALHOSPITALS(SSHs)

• Typicallyoutpatientfocused• Inpatientandoutpatient• ~300SSHsnation-wide

SURGICALSETTINGBACKGROUND

TRADITIONALHOSPITALS

NOBILISHEALTH

8

INDUSTRYGROWTH

• Efficientcoststructures• Increasedgovernmentfocusonhealthcare• Agingpopulation• Newlyinsuredaccesscare• Economiesofscaledrivepartnershipdecision

forphysician-ownedfacilities• >50%ofoutpatientsurgeriesperformedin

ASCsettingvs.32%in2005

GROWTHOFTHEASCINDUSTRY

PROJECTEDASCINDUSTRYREVENUE

Independentoperators,hospitals,&smallchainscomprised78%ofASCsintheU.S.

($ in billions)

$16 $17$19 $20 $21

$22 $23$25 $27

$30 $32$34 $36

$38$40

$0$5$10$15$20$25$30$35$40$45

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015E

2016E

2017E

2018E

2019E

2020E

Source: CSM, Equity Research, IBIS healthcare expenditures estimates, Becker’s.

9

THESPINESHIFT• Lesscomplexspineproceduresshiftingfrominpatienttooutpatient• Keyspineprocedureshavestrongertailwindsduetodemographicsandimprovementsintechnology• ~31millionAmericanssufferfromchronicbackpain• ~600,000Americansundergospinesurgeryeveryyear

INPATIENTSPINEDISCHARGES2014- 2019

SHIFTTOOUTPATIENT

OUTPATIENTSPINEDISCHARGES2014- 2019

Note: Growth rate data reflects U.S. market. Source: Wall Street Research.

Advanced Imaging 13%

Arthrocentesis / Injections 5%

Rehab & Chiropractic14%

Standard Imaging 13%

E&MVisits 17%

Fusion Surgery

Spinal Decom. / Laminec.

Vertebral Augmentation

23%

27%

25%17%

-9%

-5%

-2%

2%

-11%

Nobilis Key Procedures

Lumbar / Thoracic Fusion

Cervical Fusion

No Procedure andDiagnostics

Spinal Decompression/Laminectomy

Vertebral Augmentation Procedures

Revision Spinal Procedure

10

PrivateLender PresentationGROWTHSTRATEGY

11

MARKETINGEXPERTISEDRIVESORGANICGROWTH

• Multiplemarketingchannelsdrivevolumegrowthathospitals,ASCs,andancillaryservicelines

• Bundledpaymentcapabilities• Strategicallyaddingnewmarketingbrandstoportfolio• Brandedreferralprogram,360Concierge

SERVICELINESANDSPECIALTIES

• Continueoptimizingcasemixtomaximizerevenuepotential

• Increasethevolumeofhighacuityproceduresthatbenefitfromhigherlevelsofreimbursement

• Identifyanddevelopadditionalservicelinesappropriateforoutpatientenvironment

GROWTHSTRATEGY

ACQUISITIONOPPORTUNITIES

• Highlyfragmentedmarketwithmanyidealacquisitiontargets• FocusontargetsthatallowNobilisHealthtocross-sell

servicelinesandleveragemarketingcapabilities• Pursuingin-networktargetsthatareamenabletoNobilisHealth

marketingplatformandallowtheCompanytoleverageexistinginfrastructure

• Acquisitionstrategyincludesfacilitiesandclinicalpractices

1

3

2

4 OPERATIONALLEVERAGE• Focusondrivingcostreductionsthroughoutsystem• IdentifyandachievegreatereconomiesofscaleasNobilis

continuesacquiringnewbusinessesandexpandingitsplatform

• Experiencedleadershipteamwithdecadesofhealthcareexperience

• Clinicallyintegratednetworkforcontractingandcarecoordination

12

DIRECT-TO-CONSUMERMARKETING

• Marketingandtechnologyplatformtargetsprospectivepatients

• Uniquevaluepropositiontophysicians;superiorpatientexperience

• Scalablerevenuedriver• Portfolioeffect– directcasestospecificfacilitiesona

procedure-by-procedurebasisforbestclinicaloutcomeandreturnoninvestment

UNIQUEPATIENTACQUISITIONSTRATEGY

PHYSICIANSALES

• In-housemarketingteam• Buildsandexecutesmarketingplansonbehalfofphysicians• Expandsphysicians’practices,optimizedpayor andprocedure

mix,anddrivesadditionalvolumetoNobilisfacilities• Highaveragereturn-on-investment(ROI)

13

HIGHTOUCHMARKETINGMODEL

LeadGenerationDirect-to-PatientEngagementPoints• Digital• Traditional(TV,Radio)• Email&Content• Real-TimeFulfillment

ConciergeServiceInsideSalesTeam+ITPlatform• DedicatedPatientCoordinators• Multi-touch,FullServiceProcess• ProprietarySoftwareSolutions• CRM

ConversiontoSurgicalPatientPatientProcessManagement• PatientEducation• ImagingReviewbyMedicalTeam• InsuranceVerification&Explanation• SurgeryClearanceManagement• SurgeryScheduling/Coordination

PatientTrackingPatientExperienceFollowUp/FacilitateResearch• PostOperativeFollow-upContact• PatientExperienceSurveys&Testimonial• ReferralRequest• 360ConciergeTrackingThrough-outContinuum

ofCare• PromotesSuccinctTreatmentAlgorithmwhich

ResultsinImprovedPatientOutcomesandLowerHealthcareCosts

14

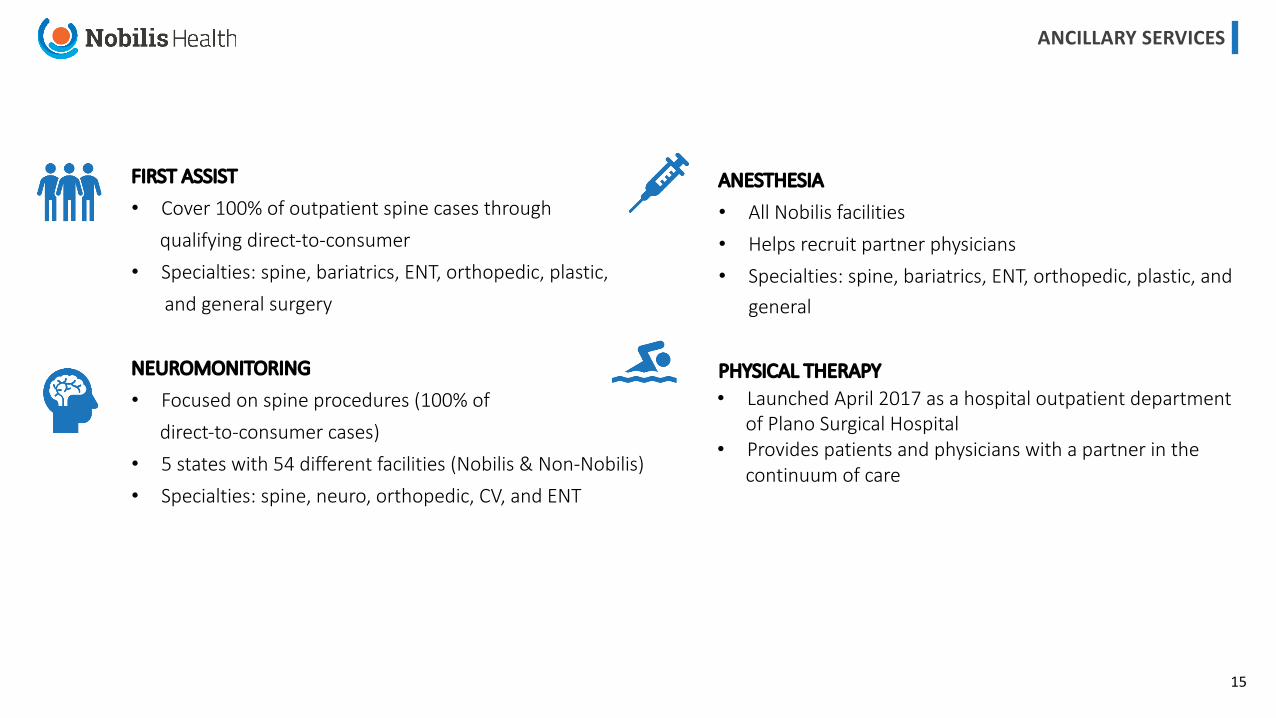

FIRSTASSIST

• Cover100%ofoutpatientspinecasesthroughqualifyingdirect-to-consumer

• Specialties:spine,bariatrics,ENT,orthopedic,plastic,andgeneralsurgery

NEUROMONITORING

• Focusedonspineprocedures(100%ofdirect-to-consumercases)

• 5 stateswith54differentfacilities(Nobilis &Non-Nobilis)• Specialties:spine,neuro,orthopedic,CV,andENT

ANCILLARYSERVICES

ANESTHESIA

• AllNobilis facilities• Helpsrecruitpartnerphysicians• Specialties:spine,bariatrics,ENT,orthopedic,plastic,and

general

PHYSICALTHERAPY• LaunchedApril2017asahospitaloutpatientdepartment

ofPlanoSurgicalHospital• Providespatientsandphysicianswithapartnerinthe

continuumofcare

15

BENEFITS

• Continuityofcareforpatients• Helpsrecruittopphysicians• Increasespatientandphysiciansatisfaction• Improvespatientoutcomes• Accretivetoearnings

ANCILLARYSERVICES

DEVELOPMENT

• Nobilis activelyseekspotentialM&Atargetsintheancillaryservicesspace

• Focusonacquisitionswithrevenuepotentialsystemwide

• IncreasedcapabilitiespositionNobilis toexecutealternativepaymentmethodologiesforpayors

PATIENTCENTRICSTRATEGY

• Achieveeconomiesofscale• Makeefficientuseofcapitalandoperatingresources• Treatsamelevelofdemandwithlesscapacitythen

standalonefacilities• Resultsinincreasedproductivity,lowerstaffing

requirementsandreducedoperatingandunitcosts

FINANCIALCONTRIBUTION

• 2016revenueof$20.4millioncomparedto$2.3millionin2015

• Maximizesrevenuebycapturingadditionalrevenuestreamsperpatient

16

• Concertis isNobilisHealth’sClinicallyIntegratedNetwork(CIN)ofhealthcareproviders,ancillaryproviders,andfacilitiesthatimprovesthepatientexperienceacrossthecontinuumofcare

• TheCINcapturesreferralsfromprimarycarephysicianstocoordinatepatientcarewithNobilisHealthancillaryproviders,surgeonsandfacilities

• 360Conciergeandthephysicianportal,divisionsofConcertis,allowproviderstheabilitytomonitorpatientcareastheymovethroughtheNobilisHealthcontinuumofcare

• AsofSeptember,wehaveover100providersinthe360Conciergesystemacrossourthreemajormarkets,whichhasresultedinover1,000referralstotheNobilisHealthsystem

• Alignwithphysiciansthroughemployment,bundledpaymentproducts,360Concierge,andotherfinancialandclinicalproducts

CONCERTISSTRATEGY

PRIMARYCAREPRACTICES

• Lessexpensivetoacquirethanspecialists• AllowsNobilisHealthtocontrolpatientexperienceacrossthe

continuumofcare• Feedsvolumeintobundledpaymentand360Concierge• Achievesclinicalintegration• Bringphysiciansintoournarrownetwork• Ourcarenavigatorsaretrainedhealthcareprofessionalswho

serveaspatientconcierges,guidingpatientsthroughtheentireepisodeofcarefromdiagnosistopost-surgicalcare

17

PrivateLender PresentationELITETRANSACTIONOVERVIEW

18

• 4ASCs&SurgicalHospitalsinHoustonMetroArea• $49.0MLTM9/30/17Revenue• $30.3MLTM9/30/17AdjustedEBITDA• 76PhysicianPartners• 86ReferringPhysicians

COMBINEDREGIONALLEADER

This image cannot currently be displayed.

• 14ASCs&SurgicalHospitals• 5 ASCs&SurgicalHospitalsinHoustonMetroArea• $314.8MLTM9/30/17Revenue(1)• $39.6MLTM9/30/17AdjustedEBITDA(1)• 41PhysicianPartners• 490ReferringPhysicians

(1) Pro forma for the full year impact of the AZ Vein acquisition.(2) Includes $2 million of estimated cost synergies resulting from the consolidation of one Elite and one Nobilis ASC currently colocated at the same address.

ASCs&SurgicalHospitals

ASCs,SurgicalHospitals&Clinicsin

HoustonMetro

LTM9/30/17Revenue

LTM9/30/17AdjustedEBITDA

(NetNCI)

PhysicianPartners

ReferringPhysicians

19

CASEMIX

PAYORMIX

19,325

29,12630,978 30,701

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

2014 2015 2016 LTM6/30/17

Cases

CASEVOLUME&REVENUEPERCASE

IN-NETWORKCASEMIX

Pain27%

Spine15%

Ortho14%

Bariatrics14%

ENT9%

Plastic7%

Podiatrist4%

Other11%

UHC 29%

Aetna 23%BCBS TX

12%

BCBS 6%

Other Commercial

12%

Cigna 11%

Self4%

Worker's Comp 2%Medicare 0.6%

Out-of-Network

54%

In-Network 46%

$7,380

$9,634

$11,432$12,344

$0

$2,000

$4,000

$6,000

$8,000

$10,000

$12,000

$14,000

2014 2015 2016 LTM6/30/17

Rev. Per Case

PROFORMAPOSTACQUISTION

Note: All figures unless otherwise stated are based on LTM 6/30/2017 pro forma for the full year impact of the AZ Vein acquisition. 20

PrivateLender PresentationFINANCIALOVERVIEW

21

REVENUEANDADJUSTEDEBITDA

FINANCIALPERFORMANCE

(Millions)

$31

$84

$229

$286

$310- $325

$3

$11

$40$34

$40- $45

$-

$20

$40

$60

$80

$100

$120

$140

$-

$50

$100

$150

$200

$250

$300

$350

2013 2014 2015 2016 2017E

TotalRevenue Adj.EBITDA

TrackRecordofStrongRevenueandAdj.EBITDAGrowth

22

*LowerendofguidanceduetoimpactofHurricaneHarvey.2017GuidanceprovidedonMarch13,2017:Revenue:$310M-$325MAdj.EBITDA:$40M-$45M

Revenu

e

Adj.EB

ITDA

TOTALREVENUE

$51$68 $62

$80$71 $65

$286

$310- $325

$0

$50

$100

$150

$200

$250

$300

$350

Q116 Q117 Q216 Q217 Q316 Q317 2016 2017E

Revenu

e

2017OPERATINGPERFORMANCE

23

*LowerendofguidanceduetoimpactofHurricaneHarvey.2017GuidanceprovidedonMarch13,2017:Revenue:$310M-$325MAdj.EBITDA:$40M-$45M

(Millions)

ADJUSTEDEBITDA

$0.4$2

$9$10

$4$7

$34

$40- $45

$0

$10

$20

$30

$40

$50

Q116 Q117 Q216 Q217 Q316 Q317 2016 2017E

Adj.EB

ITDA

2017OPERATINGPERFORMANCE

24

*LowerendofguidanceduetoimpactofHurricaneHarvey.2017GuidanceprovidedonMarch13,2017:Revenue:$310M-$325MAdj.EBITDA:$40M-$45M

(Millions)

ORGANICvs.ACQUISITIONGROWTH

25(Millions)

YEAR-OVER-YEARORGANICGROWTH

$0

$50

$100

$150

$200

$250

$300

$350

2013 2014 2015 2016

Revenu

e

TotalOrganicRevenue TotalAcquiredRevenue

TotalRev:$84mmYoYGrowth:$53mm

TotalRev:$229mmYoYGrowth:$146mm

TotalRev:$286mmYoYGrowth:$57mm

TotalRev:$31mmYoYGrowth:$10mm

26

KEYMETRICS

Totalcashof$34.1millionatSeptember30,2017,comparedwith$24.6millionatDecember31,2016

STOCKSNAPSHOT(01/05/18) FINANCIALSNAPSHOT(9/30/2017)

*Allamountsinmillions,unlessdenotedotherwise

*Source:YahooFinance

Symbol(NYSEAmerican) HLTH

SharePrice $1.35

MarketCap $105

SharesOutstanding 77.8

Float 56

InsiderOwnership(%) 28

LTMAdjustedEBITDA $39.6

EV/EBITDA 4.3x

Price/Sales(LTM) 0.33x

Cash $34.1

Accounts Receivable $112.4

NetIncome $1.0

FullyDilutedEPS $0.01

ProjectedCAPEX $7- $8

TotalDebt $75.7

NetDebt $41.6

LeverageRatio 1.9x

27

FINANCIALSTATEMENTHIGHLIGHTS

INCOMESTATEMENT

STATEMENTOFCASHFLOWS

BALANCESHEET

Asof9/30/2017

(Millions)

Cash $34.1

TotalAssets $317.1

TotalDebt $75.7

TotalLiabilities $159.1

NetCashProvidedbyOperatingActivities $27.9

NetCashUsed ForInvestingActivities $(13.3)

Net CashUsedForFinancingActivities $(5.0)

Total Revenue $64.7

OperatingExpensesSalariesandBenefitsDrugsandSuppliesGeneralandAdministrativeDepreciationandAmortization

TotalOperatingExpenses

Corporate ExpensesSalariesandBenefitsGeneralandAdministrativeLegalDepreciation

TotalCorporateExpenses

$15.7$10.4$27.6$2.7

$56.4

$2.9$3.3$0.7$0.1

$7.0

NetIncome $1.0

AdjustedEBITDA $6.7

PrivateLender PresentationAPPENDIX

28

HARRYFLEMING

ChiefExecutiveOfficer&ChairmanoftheBoard

• JoinedNobilisin2010• PreviouslyservedasCFO,PresidentandExecutiveChairmanofNobilis• EarnedanMBAfromBostonCollege,aJ.D.fromtheUniversityofHouston,andaB.A.fromthe

UniversityofSt.Thomas

• JoinedNobilisin2010• PreviouslyservedasChiefOperatingOfficer&ChiefBusinessDevelopmentOfficeratNobilis• Founder&CEOofDiagnosticandInterventionalSpineCenters• DoctoratefromTexasChiropracticCollege

• JoinedNobilisin2017• PreviouslyservedasDivisionalCFOforSt.JudeMedical’sAmericadivision• LicensedCPA• EarnedanMBAfromtheUniversityofTexasatAustin

• JoinedNobilisin2014• 15yearsofhealthcaresalesandbusinessdevelopment• PreviouslyheldsuccessfulsalesleadershippositionsatIntuitiveSurgical,Medtronic,andPfizer• EarnedaB.A.fromRhodesCollege

• JoinedNobilisin2016• PartneratBakerDonelson,specializinginhealthlawandservedasaDirectorofLegalServices

atHoustonMethodistHospitalSystem• EarnedaJ.D.fromtheUniversityofHoustonandB.A.cumlaudefromRiceUniversity

MANAGEMENTTEAM

KENNETHEFIRD

President

DAVIDYOUNG

ChiefFinancialOfficer

PATRICKYODER

ChiefRevenueOfficer

MARISSAARREOLA

ChiefStrategyOfficer/President,Concertis

29

MARCOSRODRIGUEZ

ChiefAccountingOfficer

• JoinedNobilisin2016• BeganhiscareeratDeloitte&Touche LLPandservedfiveyearsasDirectoratOpportuneLLP• 19yearsoffinancial&accountingreporting,externalandinternalaudits,andSECregulations• EarnedaB.S.fromLouisianaStateUniversityandisalicensedCPA

• JoinedNobilisin2017• 20yearsofoperationalandmanagerialexperienceinthehealthcareindustry• VPofContinuousImprovementforUnitedSurgicalPartnersInternational/TenetHealthcare

(“USPI”)andCEOofMemorialHermannSurgicalHospitalKingwood,inHouston,Texas• M.S.inHealthcareManagement-EmergencyServicesfromUniversityofMaryland

• JoinedNobilisin2015• PreviouslyservedasCFOatNorthstar HealthcareLLCandNobilisHealth• 20yearsoffinancialandaccountingreportinginthehealthcareindustry• EarnedanM.B.A.fromTexasWoman’sUniversityandaB.S.fromSacredHeartUniversity

• JoinedNobilisin2017• PreviouslyservedasDirectorofMarketingforTravelocityandDirectorofOnlineMarketingat

Hotels.com• EarnedaJ.D.fromUniversityofTennesseeCollegeofLawandaB.S.fromVanderbiltUniversity

• JoinedNobilisin2014• 10yearsoffinance&accountingexperienceinthehealthcareindustry,includingHCA&Tenet• EarnedanM.B.A.fromUniversityofTexas– SanAntonioanda B.S.fromNewYorkUniversity

MANAGEMENTTEAM

MARCCELIA

EVPofOperations

KENNETHKLEIN

CFOofOperations

PHILAYRES

VPofMarketing

BRANDONMORENO

VPofFinance

30

TEXAS(DALLASANDHOUSTON) EQUITY

FirstNobilisHospital-------------------------------------------------------------------------- 51%HermannDriveSurgicalHospital---------------------------------------------------------- 54.75%PlanoSurgicalHospital----------------------------------------------------------------------- 100%HospitalforSurgicalExcellenceofOakBend-------------------------------------------- 50.1%

ARIZONA(SCOTTSDALE)

ScottsdaleLibertyHospital------------------------------------------------------------------ 75%

NOBILISFACILITIES

Hospita

ls

31

TEXAS(DALLAS,HOUSTON,ANDELPASO) EQUITY

First Nobilis Surgical Center (HOPD) ------------------------------------------------------ 51%Kirby Surgical Center -------------------------------------------------------------------------- 25%Medical Park Drive Specialty Center (HOPD) -------------------------------------------- 51%Elite Center for Minimally Invasive Surgery (HOPD) ------------------------------------ 50.1%Houston Metro Ortho & Spine Surgery Center (HOPD) ------------------------------- 50.1%Elite Sinus Spine & Ortho (HOPD) ---------------------------------------------------------- 50.1%Mountain West Surgery Center (HOPD) ------------------------------------------------ 100%Uptown Surgery Center (HOPD) ---------------------------------------------------------- 100%

ARIZONA (PHOENIX, SCOTTSDALE, AND TUCSON)

Northstar Healthcare Surgery Center – Scottsdale -------------------------------------- 100%Chandler Surgery Center ---------------------------------------------------------------------- 100%Oracle Surgery Center -------------------------------------------------------------------------- 100%Phoenix Surgery Center ------------------------------------------------------------------------ 100%Surprise Surgery Center ------------------------------------------------------------------------ 100%

NOBILISFACILITIES

ASCs

32

TEXAS (DALLAS, HOUSTON, ROUND ROCK, SAN ANTONIO) EQUITY

HamiltonVeinSugarLandClinic------------------------------------------------------------- 100%HamiltonVeinWoodlandsClinic------------------------------------------------------------ 100%HamiltonVeinClearLakeClinic-------------------------------------------------------------- 100%HamiltonVeinKatyClinic---------------------------------------------------------------------- 100%HamiltonVeinStoneOakClinic--------------------------------------------------------------- 100%HamiltonVeinRoundRockClinic------------------------------------------------------------- 100%

ARIZONA (CHANDLER, GLENDALE, PHOENIX, SCOTTSDALE, AND TUCSON)

ArizonaVein&VascularChandlerClinic---------------------------------------------------- 100%ArizonaVein&VascularOracleClinic------------------------------------------------------- 100%ArizonaVein&VascularPhoenixClinic----------------------------------------------------- 100%ArizonaVein&Vascular SurpriseClinic---------------------------------------------------- 100%DeRosaMedicalClinic– Glendale----------------------------------------------------------- 100%DeRosaMedicalClinic– Chandler----------------------------------------------------------- 100%DeRosaMedicalClinic– Scottsdale---------------------------------------------------------- 100%

NOBILISFACILITIES

Clinics

33

NOBILISFACILITIES

34

FACILITYNAME FACILITYDETAILS SPECIALTIESPLANOSURGICALHOSPITAL •26InpatientBeds •Bariatrics

•6ORs •Spine•2ProcedureRooms •Plastic Surgery

•Orthopedics•GeneralSurgery•PainManagement

KIRBYSURGICALCENTER •4ORs •Orthopedics•1ProcedureRoom •GeneralSurgery

•Pain•ENT

HERMANNDRIVESURGICALHOSPITAL •22Beds •Bariatrics•18PrivateRooms •Spine•6ORs •Plastic Surgery•2ProcedureRooms •Orthopedics

•GeneralSurgeryFIRSTSTREETSURGICALHOSPITAL •4ORs •Bariatrics

•1ProcedureRoom •SpineHOPDsofFirstSurgicalHospital: •Plastic Surgery

FirstStreetSurgeryCenter •4ORs •OrthopedicsMedicalParkSpecialtyCenter•1OR •GeneralSurgery

•PainManagementATRIUMMEDICALCENTER •Bariatrics

•SpineHOPDsofAtrium MedicalCentre: •Plastic Surgery

UptownSurgeryCenter •2 ORs •Orthopedics•GeneralSurgery•PainManagement

NOBILISFACILITIES

35

FACILITYNAME FACILITYDETAILS SPECIALTIESNORTHSTARHEALTHCARESURGERYCENTER- SCOTTSDALE •4ORs •Plastic Surgery

•1ProcedureRoom •Orthopedics•GeneralSurgery•Painmanagement•Bariatrics•Podiatry

SCOTTSDALELIBERTYHOSPITAL •12InpatientBeds •Spine•2ORs •OrthopedicSurgery•1ProcedureRoom •GeneralSurgery

•Podiatry•Bariatrics•Migraine•Vascular

ARIZONAVEIN&VASCULARCENTER •4Clinics •Vascular•4ASCs•15ORs

HAMILTONVEINCENTER •6Clinics •Vascular•20Radiofrequency Ablations(RFAs)

DEROSAMEDICAL •3Clinics •Health&Wellness•9 Providers •WeightLoss

•ChronicHealthConditionManagementMESAHILLSSPECIALTYHOSPITAL

HOPDsofMesa HillsSpecialtyHospital:

MountainWest SurgeryCenter •2ORs•2ProcedureRooms

•Spine•Orthopedic Surgery•GeneralSurgery•Podiatry•Bariatrics•Migraine•PlasticSurgery

NOBILISFACILITIES

36

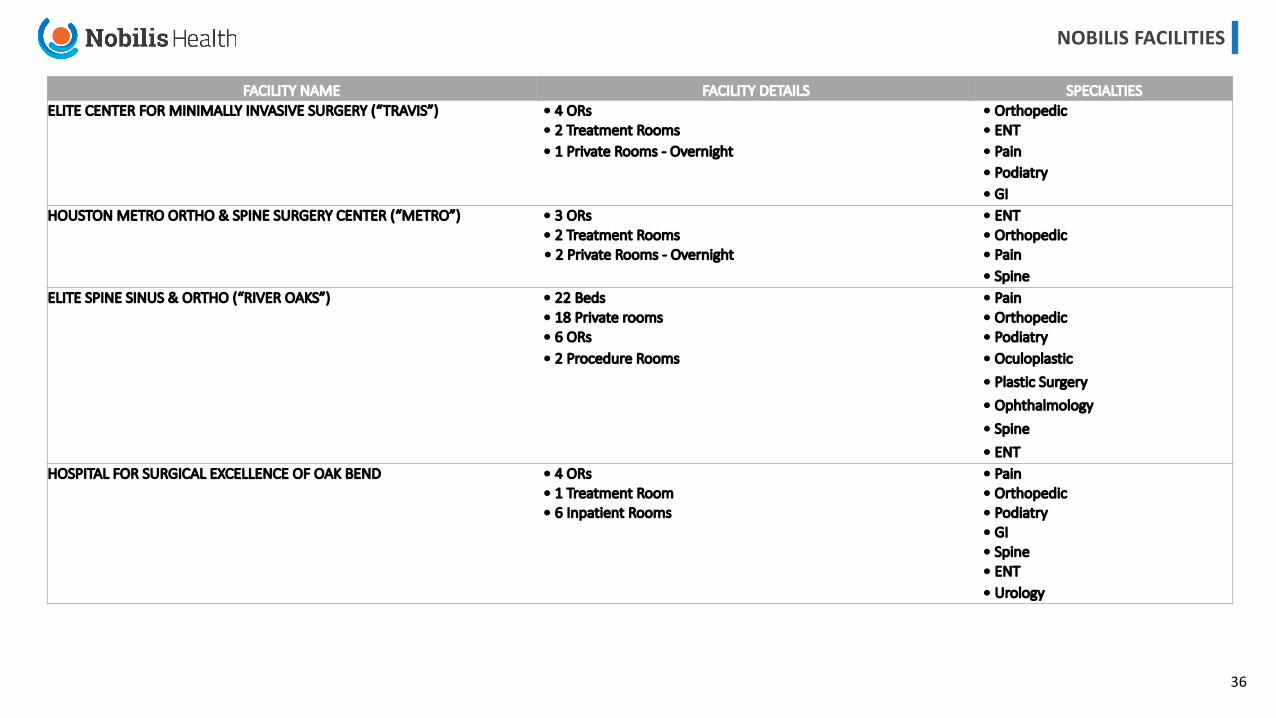

FACILITYNAME FACILITYDETAILS SPECIALTIESELITECENTERFORMINIMALLYINVASIVESURGERY(“TRAVIS”) •4ORs •Orthopedic

•2 Treatment Rooms •ENT•1PrivateRooms- Overnight •Pain

•Podiatry•GI

HOUSTON METROORTHO&SPINESURGERYCENTER(“METRO”) •3 ORs •ENT•2TreatmentRooms •Orthopedic• 2 Private Rooms - Overnight •Pain

•SpineELITESPINESINUS&ORTHO (“RIVEROAKS”) •22Beds •Pain

•18Privaterooms •Orthopedic•6ORs •Podiatry•2ProcedureRooms •Oculoplastic

•PlasticSurgery• Ophthalmology•Spine• ENT

HOSPITAL FORSURGICALEXCELLENCEOFOAKBEND •4ORs •Pain•1 Treatment Room •Orthopedic•6Inpatient Rooms •Podiatry

•GI•Spine•ENT•Urology

NOBILISBRANDS

NorthAmericanSpineTheflagshipbrand,NorthAmericanSpineoffersinnovative,minimallyinvasivebackandnecksurgeriesandenjoysasolidtrackrecordofsuperioroutcomes.Theminimallyinvasive,laserspineproceduresenjoyhighrecognitionintheirmarketsandtheagingpopulationencouragesstrongnaturalgrowth.

ClarityVein&VascularClarityVeinandVascularprovidesminimallyinvasivesurgicaltreatmentofpainfuland/orunsightlyvascularconditionsrangingfromtherelativelybenign,likevaricoseorspiderveins,tothedangerous,likedeepveinthrombosisorperipheralarterydisease.

HamiltonVeinCenterHamiltonVeinandVascularisafull-serviceclinicalpracticewithmultipleTexaslocationsandanimpressiverecordofsuccessfultreatments.Adeptatcosmeticproceduresforconditionslikespiderandvaricoseveins,thepracticealsoexcelsatdiagnosingandtreatingpotentiallyharmfulunderlyingconditions.

MigraineTreatmentCentersofAmericaMigraineTreatmentCentersofAmericaistheexclusiveprovideroftheOmega™Procedure,anon-pharmaceuticalsurgicalimplantforthereliefofchronicmigrainepain.Increasingawarenessofneurostimulation techniques,vocalsupportfrompastpatients,andfavorableinsurancepoliciespositionthebrandasveryhighgrowth.

ArizonaVein&VascularCenterArizonaVeinandVascularisamaturepracticeinthePhoenix/Scottsdaleareathat,likeClarityVeinandVascular,providesminimallyinvasivetreatmentofvenousconditionsanddisordersfromtheunsightlytothedangerous.

MIRIWomen’sHealthMIRIWomen’sHealthfocusesonminimallyinvasivesurgeriesforgynecologicalconditionsandofferssecondopinionsforthoseseekinganalternativetotraditionalhysterectomies.

EvolveEvolve,abariatricsurgerybrand,benefitsfromincreasingmedicalconsensusonthehealthbenefitsofbariatricsurgeryoverconventionaldietandexerciseforthesignificantlyormorbidlyobese.Nationallyrisingratesofobesityandmorefarsighted,preventiveinsurancepoliciespoisethebrandforstronggrowth.

OnwardOrthopedicsOnwardOrthopedicstreatsnon-spinejointissuesforpatientsofallagesandtypes.Thebrandbenefitsfrompartnerphysicianswithsolidhistoriesofhigh-profilesportsclients,andcanprovidereferralstotheNorthAmericanSpineandNueStep brands.

NueStepNueStep focusesontheminimallyinvasivereliefoffootandanklepainduetonerveentrapmentandavarietyofotherpodiatricissues.Thebrand’ssuccessisaresultofeducationalmarketingcampaignsdesignedtocorrectahistoricalunder-appreciationoffootpainandtherapeuticmodesusedtoaddressit.

37

Personalizedtreatment&accesstomulti-disciplinarymedicalstaff&physicians

Goal: Self-source business and maximize ROISales & Marketing

1

Direct to Consumer (DTC)

Lead Generation

Concierge Service

Conversion to Surgical Patient

Patient Experience Follow Up

Successful Patient Outcomes

Sales Outreach to Referral Community

Physician Referral to Nobilis Brand

Leverage concierge service for enhanced patient experience

3

360 Concierge

Sales Outreachto Physicians

Physician & Patient Conversion

Nobilis Facility CaseAcquisition

2

PhysicianRecruitment

Patient and PhysicianSatisfaction

SALESANDMARKETINGSTRATEGY

Our UniqueApproach

38

PrivateLender PresentationNYSEAmerican:HLTH

39