Corporate Challenge: Exceeding the Expectations of … Handouts/RIMS 14/CAD008... · Corporate...

35

Page 1 Recording of this session via any media type is strictly prohibited. Page 1 Corporate Challenge: Exceeding the Expectations of Your C-Suite Presenters: Bruce Zaccanti and Valerie Franco Panelist: Jeff Tetrick 29 April 2014

Transcript of Corporate Challenge: Exceeding the Expectations of … Handouts/RIMS 14/CAD008... · Corporate...

Page 1

Recording of this session via any media type is strictly prohibited.

Page 1

Corporate Challenge: Exceeding the Expectations of Your C-Suite

Presenters: Bruce Zaccanti and Valerie Franco

Panelist: Jeff Tetrick

29 April 2014

Page 2

Recording of this session via any media type is strictly prohibited.

Housekeeping This is an interactive session. Please share your insights!

Please place your phone in silent mode.

Welcome!

Page 3

Recording of this session via any media type is strictly prohibited.

Speaker Backgrounds

Learning Objective 1: Facilitating Communication Throughout the Organization

Learning Objective 2: Embracing the Changing Landscape

Learning Objective 3: Being the Risk Management Corporate Champion

Learning Objective 4: Developing as a Risk Manager

Wrap-up and Questions

Appendix – Summary of EY CFO Survey Results

Agenda of What to Expect

Page 4

Recording of this session via any media type is strictly prohibited.

Valerie Franco, MBA

6 Years, Vice President of Risk Management, Lowe’s Corporation

1 Year, Director of Risk Management, Lowe’s Corporation

1 Years, Director of Claims Services, Strategic Risk Solutions

4 Years, Director of Client Services, Strategic Risk Solutions

MBA from Belmont University, Nashville, TN

Adjunct Professor – University of North Carolina

Speaker Backgrounds

Bruce S. Zaccanti

12 Years, Partner and National Practice Director of the Insurance Risk Management and Claims Practice EY

7 Years, National Practice Director at a Big Four Firm

4 Years, Corporate Director of Insurance and Risk Manager

3 Years, Large TPA Firm, National Claims Service Rep, Director of Quality and Compliance Audit

2 Years, Intellectual Property Consultant

Business Insurance Risk Manager of the Year Honor Roll, 1995

Page 5

Recording of this session via any media type is strictly prohibited.

Jeff Tetrick, CPA, AIF, MBA

25 Years, CFO, Pinnacol Insurance Oversees Financial Reporting, Business Planning, ERM, Audit and Actuarial Functions

4 Years, Vice President Group Operations, Capitol Life Insurance.

4 Years, Senior Vice President, Preferred Benefit Services

3 Years, Controller, Denver's Health Care United

6 Years, Public Accounting at EY, Life Insurance Focus

Board Member of Integrated Benefits Institute and Pinnacol Foundation

Panelist Backgrounds

Page 6

Recording of this session via any media type is strictly prohibited.

Risk Management Maturity Model – Tactical to Integrated

Regardless of the organizational structure, corporate risk management needs to penetrate all levels of the organization.

Thre

e D

imen

sio

ns

Front Line Operations

Tactical Risk Management

Integrated Management

Board / Executive Management

Perform Oversight ► Sets the “tone from the top” ► Establishes risk appetite and strategy ► Approves the risk management framework, methodologies, overall policies, roles and responsibilities ► Leverages risk information into decision making process. Accepts, transfers or mitigates identified risks ► Evaluates BU activities on a risk-adjusted basis

Coordinate with Other Management Areas ► Contract and indemnity lease review ► Loss control and safety oversight ► Non-insurance risk transfer ► Risk financing alternatives

Compliance

Interpret and Address ► Legal/ regulatory environment changes ► Regulatory issue advisement ► Compliance techniques and strategy planning ► Policies and procedures development ► Risk assessment based compliance testing ► Compliance monitoring

Manage Insurable Risk ► Insurance procurement ► Certificate of insurance management ► Claims management ► Brokers, carriers, and TPA oversight

Business Unit and Employee Participation ► Administration of and adherence with risk management policies ► Risk and loss identification, management, mitigation, and upward reporting ► Loss and incident data tracking

Page 7

Recording of this session via any media type is strictly prohibited.

Board of Directors

C-Suite

CEO, CFO, COO, CAO, CIO, CRO, etc.

SVPs and VPs

Human Resources, General Counsel, Treasury, Finance, Manufacturing, etc.

Director/Managers

Risk Management, Logistics, Sourcing, etc.

Employees/Staff

Common Communication

Gaps

Communication should flow

between all levels of the

organization and across levels,

although communication does not always

flow in both directions.

The Risk Management Messaging Challenge

Page 8

Recording of this session via any media type is strictly prohibited.

REAL ESTATE PURCHASING

TRANSPORTATION ENGINEERING

PRODUCTION

SAFETY

INSURANCE

COMPANIES

BROKERS

PUBLIC

RELATIONS

MARKETING

INVESTOR

RELATIONS

RESEARCH FINANCIAL

LEGAL

Risk Management

Functions

Risk Management Interdepartmental Communication

Page 9

Recording of this session via any media type is strictly prohibited.

Know the C-Suite’s top priorities and what will make them successful. According to EY surveys, C-Suite needs include:

• Trusting the numbers

o Example: Competing priorities exist and anecdote wins the day until actual data analytics are presented.

• Providing insight

o Example: Communicating value of carrier relationships, etc.

• Getting your house in order

• Funding organizational strategy

o Example: Optimization modeling to consider the best use of capital.

• Developing business strategy

• Communicating to the external marketplace

Closing the Communication Gap

Page 10

Recording of this session via any media type is strictly prohibited.

A leading practice Risk Manager and Risk Management Department:

• Masters the Core Duties and Functions to build credibility through competencies

• Knows the Products, Services, Short-Term/Long-Term Strategies, and Corporate Risk Appetite

• Develops Channels of Communication Based on Understanding of Organization’s Needs (Formal and Informal)

• Evolves into the Corporate Champion of the Organization’s Risk Management

• Obtains C-Suite Buy-in and Leads Risk Management Steering Committee

What Does This Mean for The Risk Manager and Risk Management Department?

Page 11

Recording of this session via any media type is strictly prohibited.

• Total Cost of Risk (TCOR) Analysis over 5 Years o Calculate TCOR and year over year cost of risk (COR) and identify trends

o Illustrate the COR as percent of revenue

o Benchmark the COR relative to competitors

• Cost Projections for the Fiscal Year

• Claims Data Analysis o Identify sources and causes of claims

o Identify claim counts and calculate percentage of claim dollars by claim type

o Summarize total claim dollars/or claim counts by line of coverage for the previous year compared to past four years by quarter

o Describe 10-15 largest claims in company history or currently reserved

What Can Risk Management Deliver to Management?

Page 12

Recording of this session via any media type is strictly prohibited.

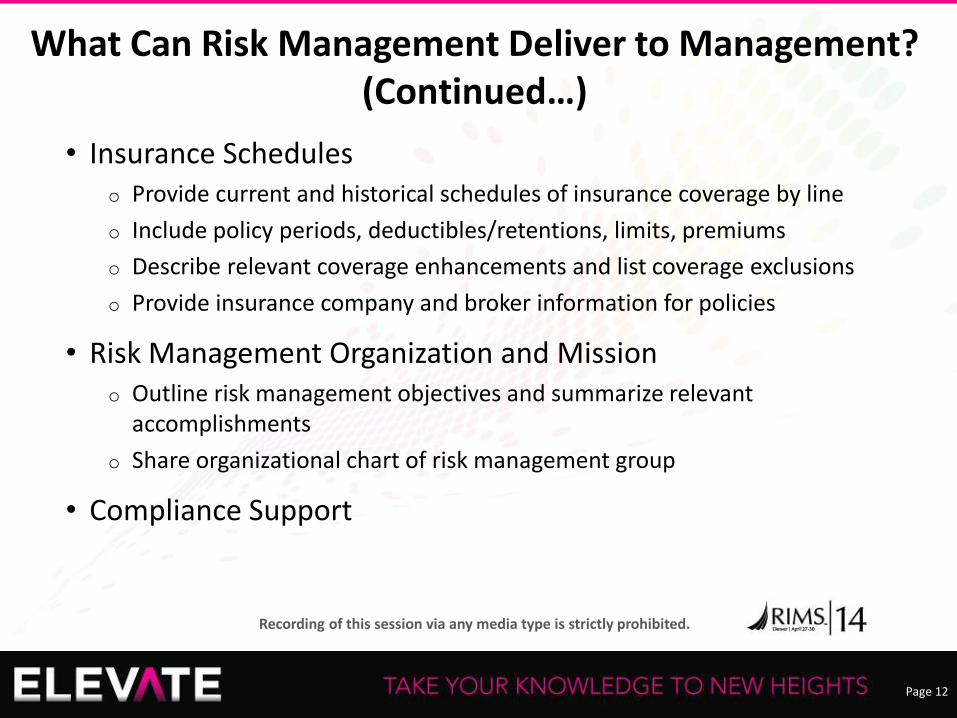

• Insurance Schedules o Provide current and historical schedules of insurance coverage by line

o Include policy periods, deductibles/retentions, limits, premiums

o Describe relevant coverage enhancements and list coverage exclusions

o Provide insurance company and broker information for policies

• Risk Management Organization and Mission o Outline risk management objectives and summarize relevant

accomplishments

o Share organizational chart of risk management group

• Compliance Support

What Can Risk Management Deliver to Management? (Continued…)

Page 13

Recording of this session via any media type is strictly prohibited.

• Shift from Traditional Risk Management to Enterprise Risk Focus o Explore a variety of techniques to avoid, mitigate, transfer, and finance risks

o Address risks associated with the evolving corporate environment

– Intellectual Risks – branding, information security, privacy

– Human Capital Risks – talent sourcing, human life and worker safety, liability issues

– Advanced Technology Risks – electronic transactions, e-mail, privacy, data storage, etc.

– Reengineering – consolidation of functions that expand personnel roles (i.e. risk management takes on environmental management; safety and wellness; etc.)

What Can Risk Management Deliver to Management? (Continued…)

Page 14

Recording of this session via any media type is strictly prohibited.

o Minimize disruptions and facilitate recovery through business continuity planning

o Identify new exposures that will require additional strategic planning and solutions

– Emerging Risks – terrorism, weather disasters, pandemics, energy, etc.

– New Products and Services

– Globalization – political risks, legal/regulatory risks, talent sourcing risks, etc.

What Can Risk Management Deliver to Management? (Continued…)

Page 15

Recording of this session via any media type is strictly prohibited.

What are top priorities and risks within your organization?

Page 16

Recording of this session via any media type is strictly prohibited.

Risk Identification for an Organization

PURE - The risk involved in situations that present the opportunity for loss but no opportunity for gain.

FINANCIAL - Uncertainty about an event under consideration that could produce either a profit or a loss.

STRATEGIC - Exposure to uncertainty arising from long-term policy decisions.

INSURABLE RISKS These are typically pure risks. Elements of insurable risk

include:

The loss is not catastrophic.

The loss must be unexpected or accidental.

The loss produced must be definite and measurable.

A significantly large number of homogeneous exposure units to make the losses reasonable predictable.

OPERATIONAL - The risk of human, process, system, or technological failure as well as risks from external events.

Organizations must understand their risk exposures (unique, market-specific, sector-specific), current issues, causes of loss, control failures, and activity impacts in order to properly identify, assess, and manage risk.

?

ENTERPRISE RISKS These encompass all risks faced by a business and may be present in any financial or economic cycle.

EMERGING RISKS These risks are a subset of enterprise risks whose impacts on a Company’s financial strength, competitive position or reputation are time-boxed to occur within the next five years. These risks may or may not be insurable.

Page 17

Recording of this session via any media type is strictly prohibited.

Changes in legislation and regulation

INSURABLE RISKS

Cyber Crime

ENTERPRISE RISKS

EMERGING RISKS

Labor Shortages, Cost Fluctuation, and Succession Planning

Market Stagnation or Decline

Terrorism

Reputation/ Brand Risk

Intensified Competition

Operational Risks (Quality, Execution, Supplier Issues)

Inflation and Deflation

Supply Chain

Fire, Explosion, Disaster Recovery

Quality Deficiencies

Pollution

Theft, Fraud, Corruption

Credit Availability

Power Blackouts

Sustainability Environmental Changes Health Issues and Pandemics

Technological Innovation and Intellectual Property

Political, Social Upheaval, and War

What Are Today’s Greatest Risks?

Business Interruption Cyber Crime Pollution

Page 18

Recording of this session via any media type is strictly prohibited.

How are domestic and global exposures impacting your organization?

Page 19

Recording of this session via any media type is strictly prohibited.

Integrating Risk Management – The Risk Steering Committee Transformation

• Why is a Risk Steering Committee fundamental to a leading practice department?

• Creates open channels of communication

• Enables the organization to identify cross-risk issues

• Creates debate and consensus for addressing risks

• What are examples of cross-risk issues? • Dealing with supply chain risk

o How should exposure be quantified?

o What are risk mitigation strategies?

o What is the organization’s risk tolerance?

• Other Examples?

Page 20

Recording of this session via any media type is strictly prohibited.

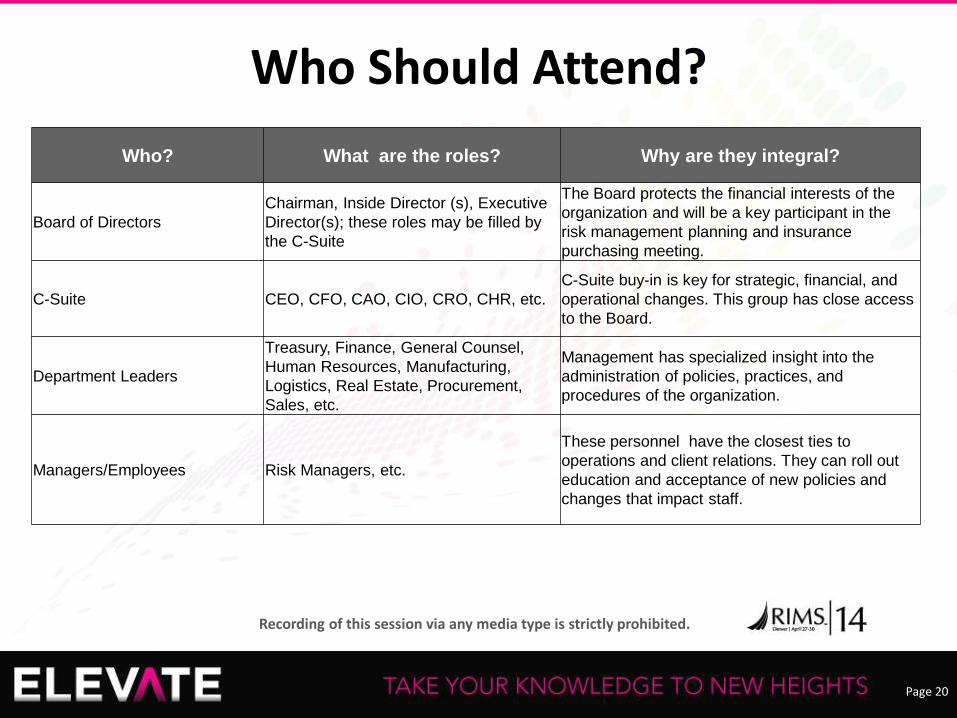

Who? What are the roles? Why are they integral?

Board of Directors

Chairman, Inside Director (s), Executive

Director(s); these roles may be filled by

the C-Suite

The Board protects the financial interests of the

organization and will be a key participant in the

risk management planning and insurance

purchasing meeting.

C-Suite CEO, CFO, CAO, CIO, CRO, CHR, etc.

C-Suite buy-in is key for strategic, financial, and

operational changes. This group has close access

to the Board.

Department Leaders

Treasury, Finance, General Counsel,

Human Resources, Manufacturing,

Logistics, Real Estate, Procurement,

Sales, etc.

Management has specialized insight into the

administration of policies, practices, and

procedures of the organization.

Managers/Employees Risk Managers, etc.

These personnel have the closest ties to

operations and client relations. They can roll out

education and acceptance of new policies and

changes that impact staff.

Who Should Attend?

Page 21

Recording of this session via any media type is strictly prohibited.

Chief Executive Officer

Chief Financial Officer

Chief Operating Officer

Chief Information Officer

Chief of Human Resources

Chief Customer Officer

Sustainability Financial Crises Supply Chain Disruption

Cyber Crime Labor Wrong Price Perception

Sustainability risk appetite aligned to organization’s corporate strategy

Risk culture, risk appetite, and metrics established; leadership restructured; defined roles/ responsibilities; and reporting/ feedback loop utilized

Strategic sourcing with manufacturers and/or wholesalers; legal, financial, and risk management leading practices followed

Physical and electronic security measures employed; electronics/ data usage policy and privacy guidelines administered

Safety and industrial hygiene policies administered; recruiting and employment rewards strategy reviewed ; time management system utilized; risk transferred where applicable

Assess costs and profit margins and balance against customer demand, competitor offerings, and other market activity

C-Suite; Management; Risk Management; Operations; Employees

Board of Directors; C-Suite; Finance

Legal, Finance, Procurement; Operations; Risk Management

C-Suite; Risk Management; Legal; Operations; Employees

Human Resources; Legal; Risk Management; Operations; Employees

COO, Finance, Operations, Employees

Publicize sustainability mission through organizational kickoff and progress updates

communicate and consistently administer risk practices; create and/or expand roles as needed; utilize liaisons at different management levels

Plan for sources, legal obligations, and financial liabilities as well as risk transfer where possible

Share policies throughout the organization; administer policies stringently; hold parties accountable

Communicate, perform checks and balances, and review the administration of organization policies; utilize third party solutions; transfer risk where possible

Utilize pricing/ performance analytics, obtain competitive information at the customer level Execution

Solution(s)

Collaboration

Risk

Collaborate and Solve Cross-Risk Issues

Page 22

Recording of this session via any media type is strictly prohibited.

Corporate Profile as of January 2000

Sales: $18.8B

Employees: 86,160

Stores: 650 stores

Corporate Profile as of January 2012

Sales: $50.5B

Employees: 245,000

Stores: 1,825 stores

Founded in 1946 in Mooresville, NC, Lowe’s has grown from a small hardware store to the second-largest home improvement retailer worldwide. Today, Lowe’s has stores in the United States, Canada, and Mexico that stock 12 product categories and more than 40,000 products. Lowe’s has 500,000 items available online and 500,000 more products available by special order.

The Lowe’s Corporation Success Story – Then and Now

Page 23

Recording of this session via any media type is strictly prohibited.

Case Study: A Risk Manager’s Career Progression • Identified loss trends and opportunities to improve client’s claims experience

• Reduced Lowe’s claim costs

• Honed technical and financial acumen through ongoing education and an MBA

• Managed adjusters at Lowe’s TPA vendor

• Continued to add value through claim management results

• Implemented quality and cost containment programs.

• Hired to oversee insurable risk and claims functions at Lowe’s

• Managed team of 17 Risk professionals

• Continued to add value through insurance program review, procurement, financing, and administration

Director of Client Services Specialty Risk Services

Claims Operations Director Specialty Risk Services

Director of Risk Management Lowe’s

• Currently oversee enterprise risk management transformation at Lowe’s

• Utilize operational knowledge of the organization and relationships to provide a strategic approach to risk management

Vice President, Risk Management Lowe’s

Page 24

Recording of this session via any media type is strictly prohibited.

• Milestones and Key Successes o Maturity of ERM Program

o Addition of Business Continuity Function

o Evolution of claims programs through in-sourcing

o Addition of Enterprise Information Governance

o Launch of Governance, Risk and Compliance function

• How was support of Senior Management Built? o Meet one-on-one with executives to discuss risk topics and concerns

o Have time with the CEO and staff on a regular cadence to engage them in risk assessment, mitigation strategies and identification of emerging risks.

o Be a trusted advisor that helps move the business forward as opposed to slowing progress

The Department’s Evolution

Page 25

Recording of this session via any media type is strictly prohibited.

• Methods for Leading Steering Committee o Provide analytics to support decisions and recommendations

o Educate on the nuances of insurance markets and reasons for movement in the market

o Illustrate the value of the ERM process and enlist them as sponsors to drive a risk-aware culture

The Department’s Evolution (Continued…)

Page 26

Recording of this session via any media type is strictly prohibited.

• Facilitate Communication Throughout the Organization

• Embrace the Changing Landscape

• Be the Risk Management Corporate Champion

• Develop as a Risk Manager and as a Department

Recap of Key Takeaways

Page 27

Recording of this session via any media type is strictly prohibited.

Questions or comments?

Page 28

Recording of this session via any media type is strictly prohibited.

According to EY surveys, C-Suite needs include:

• Trusting the numbers

• Providing insight

• Getting your house in order

• Funding organizational strategy

• Developing business strategy

• Communicating to the external marketplace

Appendix – Summary of EY CFO Survey

Page 29

Recording of this session via any media type is strictly prohibited.

Appendix – Trusting the Numbers

Page 30

Recording of this session via any media type is strictly prohibited.

Appendix – Providing Insight

Page 31

Recording of this session via any media type is strictly prohibited.

Appendix – Getting Your House in Order

Page 32

Recording of this session via any media type is strictly prohibited.

Appendix – Funding Organizational Strategy

Page 33

Recording of this session via any media type is strictly prohibited.

● Translating corporate goals into a clear strategy

● Identifying financial and risk issues in relation to corporate strategy

● Delivering a workable strategic plan within known constraints

● Thinking creatively/conceptually strong

● Analyzing portfolio of opportunities

● Visionary/story-teller ability to build trust and motivate people

● Effectively communicating financial and risk issues to C-suite colleagues

● Providing robust financial challenge at C-suite level

● Strategic and operational planning

● Knowledge of the organization's business

● Detailed knowledge of products/service lines

● Business model design

● Scenario planning

● Good overview of the industry structure and challenges

● Strategic frameworks and theory

● Awareness of the market and commercial environment

● Aware of industry and organization risk profile

● Awareness of IT as an important business enabler

● Strategy development

● Development and implementation of business plans

● Monitoring achievement of plans and targets and taking corrective actions where required

● Operational and financial risk management

● Product and market development

● Chief executive officer, chief operating officer, chief information officer

● Business unit heads, risk director, marketing director, HR director, strategy director

● Corporate development officer

View More from the EY Survey at http://www.ey.com/GL/en/Issues/Managing-finance/CFO_overview

Developing Business Strategy

Core Skills

Core

Knowledge

Key

Relationships

Key

Experiences

Appendix – Developing Business Strategy

Page 34

Recording of this session via any media type is strictly prohibited.

Appendix – Communicating to the External Marketplace

Page 35

Recording of this session via any media type is strictly prohibited.

KEEP THIS SLIDE FOR EVALUATION INFORMATION/MOBILE APP ETC.

Please complete the session survey on the RIMS14 mobile application.