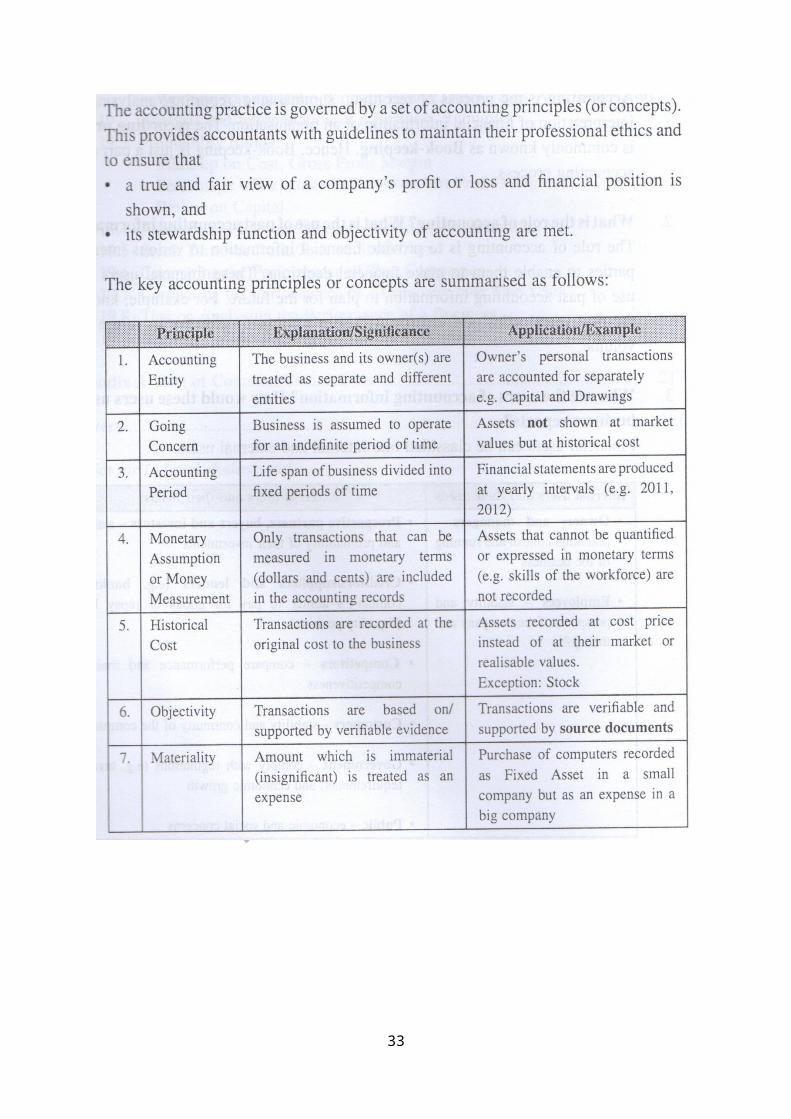

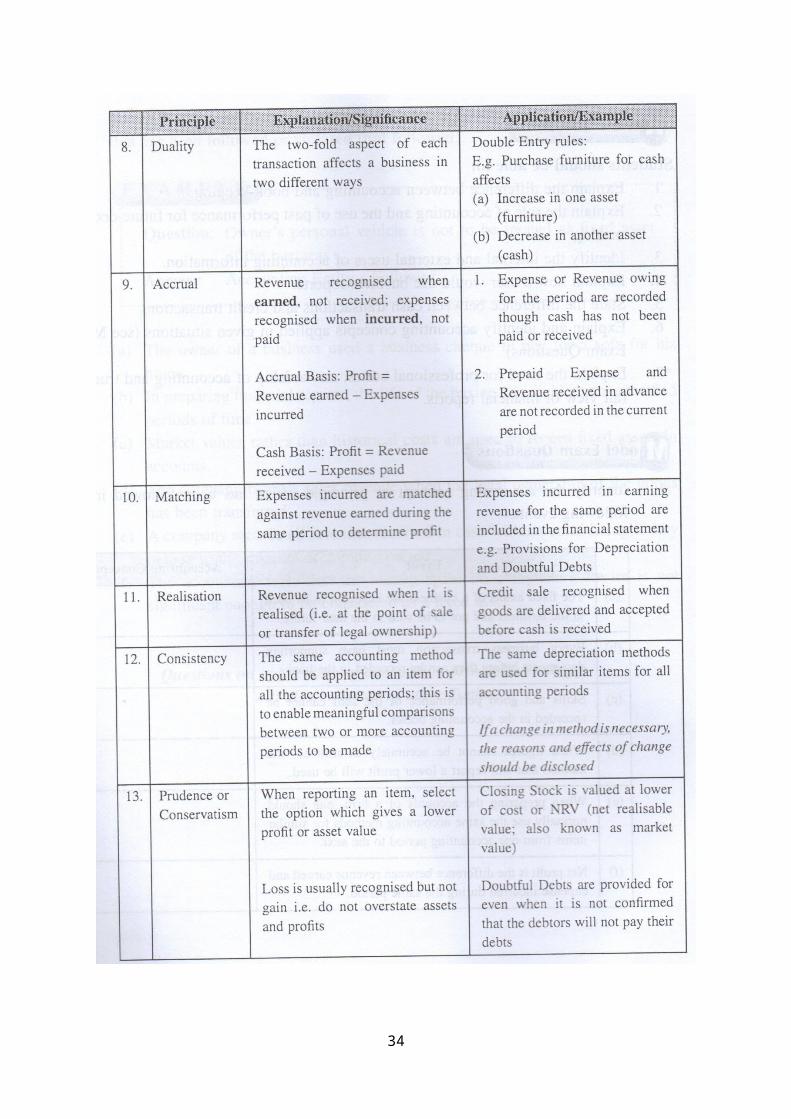

Complete POA Summary

43

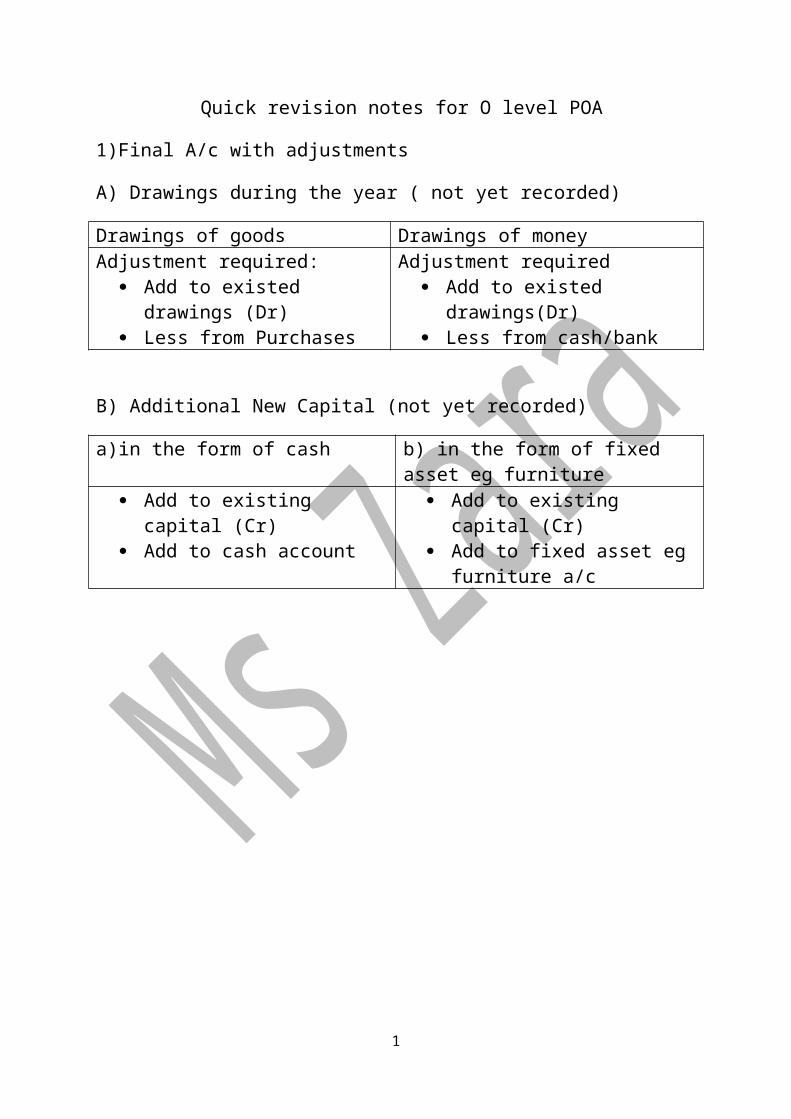

Quick revision notes for O level POA 1)Final A/c with adjustments A) Drawings during the year ( not yet recorded) Drawings of goods Drawings of money Adjustment required: Add to existed drawings (Dr) Less from Purchases Adjustment required Add to existed drawings(Dr) Less from cash/bank B) Additional New Capital (not yet recorded) a)in the form of cash b) in the form of fixed asset eg furniture Add to existing capital (Cr) Add to cash account Add to existing capital (Cr) Add to fixed asset eg furniture a/c 1

-

Upload

zara-hazirah -

Category

Documents

-

view

119 -

download

9

description

POA O level

Transcript of Complete POA Summary

Quick revision notes for O level POA

1)Final A/c with adjustments

A) Drawings during the year ( not yet recorded)

Drawings of goods Drawings of moneyAdjustment required:

Add to existed drawings (Dr)

Less from Purchases

Adjustment required Add to existed

drawings(Dr) Less from cash/bank

B) Additional New Capital (not yet recorded)

a)in the form of cash b) in the form of fixed asset eg furniture

Add to existing capital (Cr) Add to cash account

Add to existing capital (Cr) Add to fixed asset eg furniture

a/c

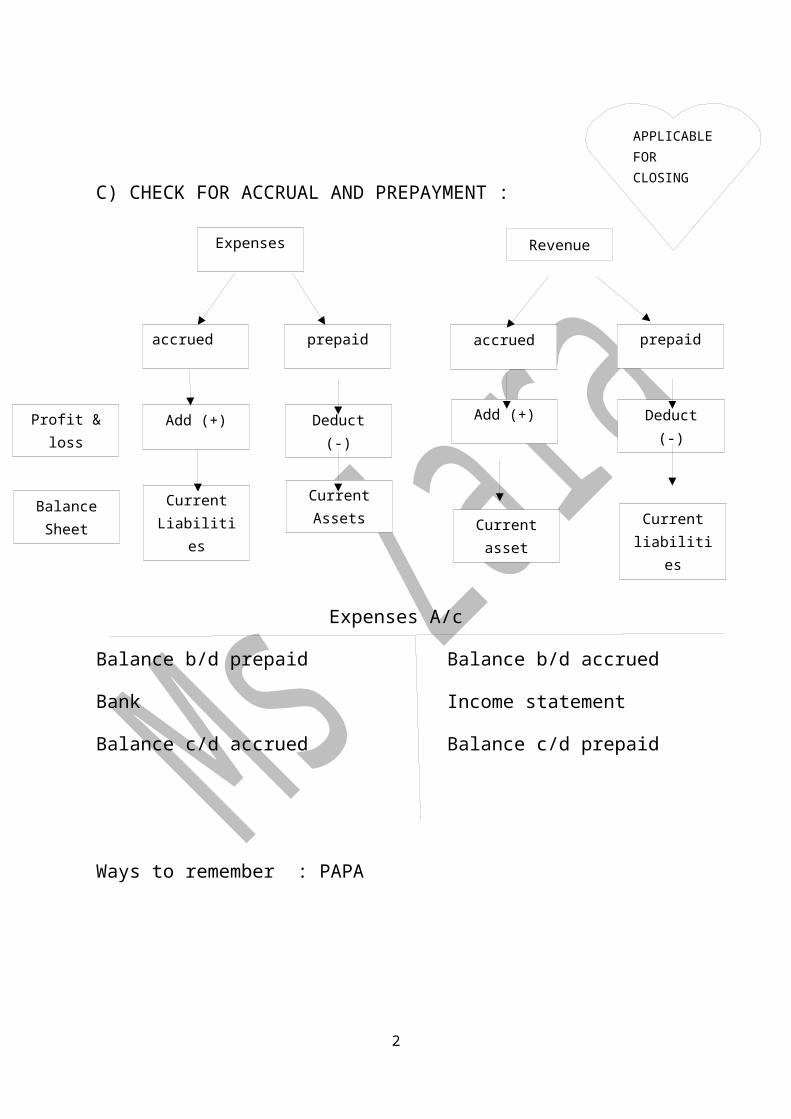

C) CHECK FOR ACCRUAL AND PREPAYMENT :

1

APPLICABLE FOR CLOSING BALANCE ( BAL C/D ) ONLY.

Expenses A/c

Balance b/d prepaid Balance b/d accrued

Bank Income statement

Balance c/d accrued Balance c/d prepaid

Ways to remember : PAPA

2

Expenses Revenue

accrued prepaid accrued prepaid

Profit & loss

Balance Sheet

Add (+)

Current Liabilities

Deduct (-)

Current Assets

Add (+)

Current asset

Deduct (-)

Current liabilities

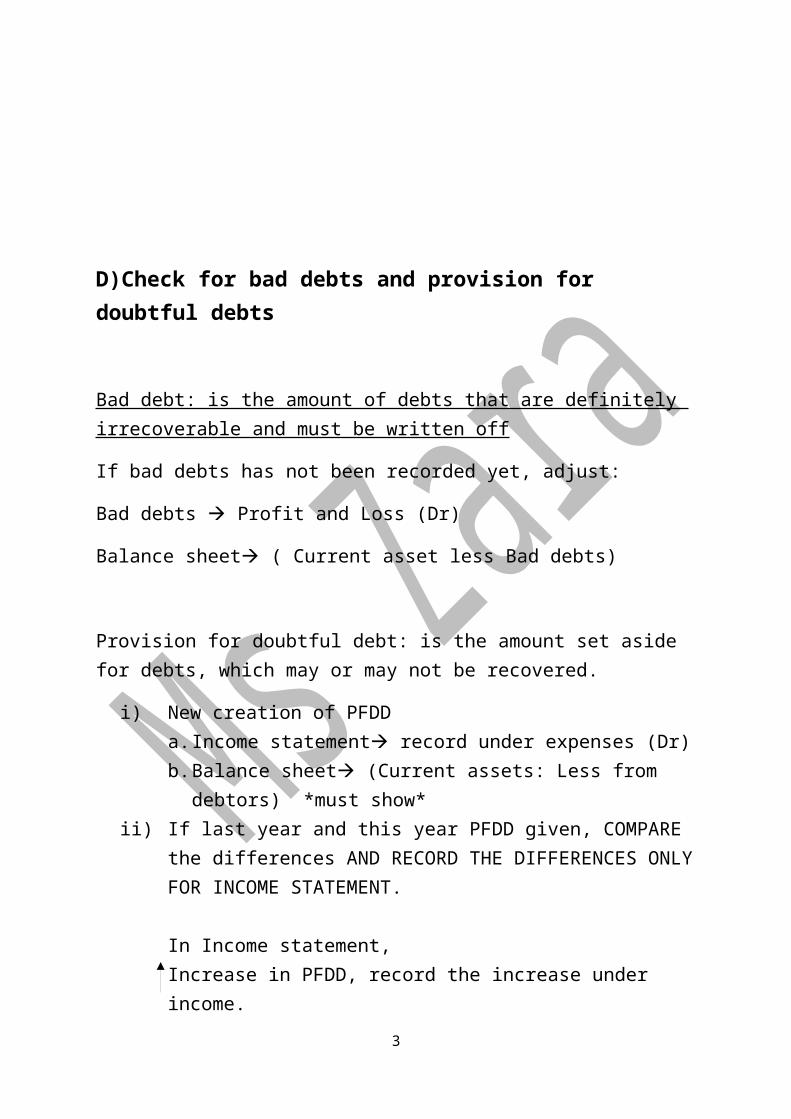

D)Check for bad debts and provision for doubtful debts

Bad debt: is the amount of debts that are definitely irrecoverable and must be written off

If bad debts has not been recorded yet, adjust:

Bad debts Profit and Loss (Dr)

Balance sheet ( Current asset less Bad debts)

Provision for doubtful debt: is the amount set aside for debts, which may or may not be recovered.

i) New creation of PFDDa. Income statement record under expenses (Dr)b. Balance sheet (Current assets: Less from debtors) *must show*

ii) If last year and this year PFDD given, COMPARE the differences AND RECORD THE DIFFERENCES ONLY FOR INCOME STATEMENT.

In Income statement,Increase in PFDD, record the increase under income. Decrease in PFDD, record the decrease under expenses In Balance sheet, whether increase or decreases, record the new provision of the year only. (Debtor-PFDD) under current assets.

3

E) Check for Depreciation

Depreciation = amount of cost written off in one year.

Accumulated depreciation ( Provision for depreciation)=The total cost that has been written off at a particular point in time

Net book value = Cost of asset- accumulated provision for depreciation

Three methods of depreciation :Straight line method It is an equal amount of cost is written off each yearDepreciation formula :Depreciation = Cost of fixed asset-scrap value

Life span (No. of years)

Depreciation : % x cost of fixed assets

Reducing balance method/ Diminishing method

A reducing amount of cost is written off in each year

Depreciation = % x (cost- provision for last year)

Revaluation method

If the fixed assets is revalued downward at year end, the difference between value the beginning of the year and value at the end of the year amounts to depreciation

Depreciation : Cost (at beginning ) + additions – cost (at the end)

How do you record depreciation?

Depreciation of fixed assets Profit and Loss A/c (Dr)

Accumulated depreciation (LAST year provision + This year provision) Balance sheet (Less from Non Current asset) to get Net book value of an assets.

4

F) Sales of Fixed assets

i) By cash/ bank :

In Balance sheet, less from non current assets

Add cash/bank balance.

ii)On credit :

In Balance sheet, less from non current assets

Add from trade receiveable

G) Purchases of Non Current assets

i) By cash/ bank:

In balance sheet, add from non current assets

Less cash/bank balance

ii) On creditIn balance sheet, add from non current assets Add to creditors.

Income statement for the year….

5

$ $ $ $

Opening inventory xxx Sales xxx

(+)Purchases xx (-) Sales Return (xx)

(-) Purchases returns (xx) Net sales xxx

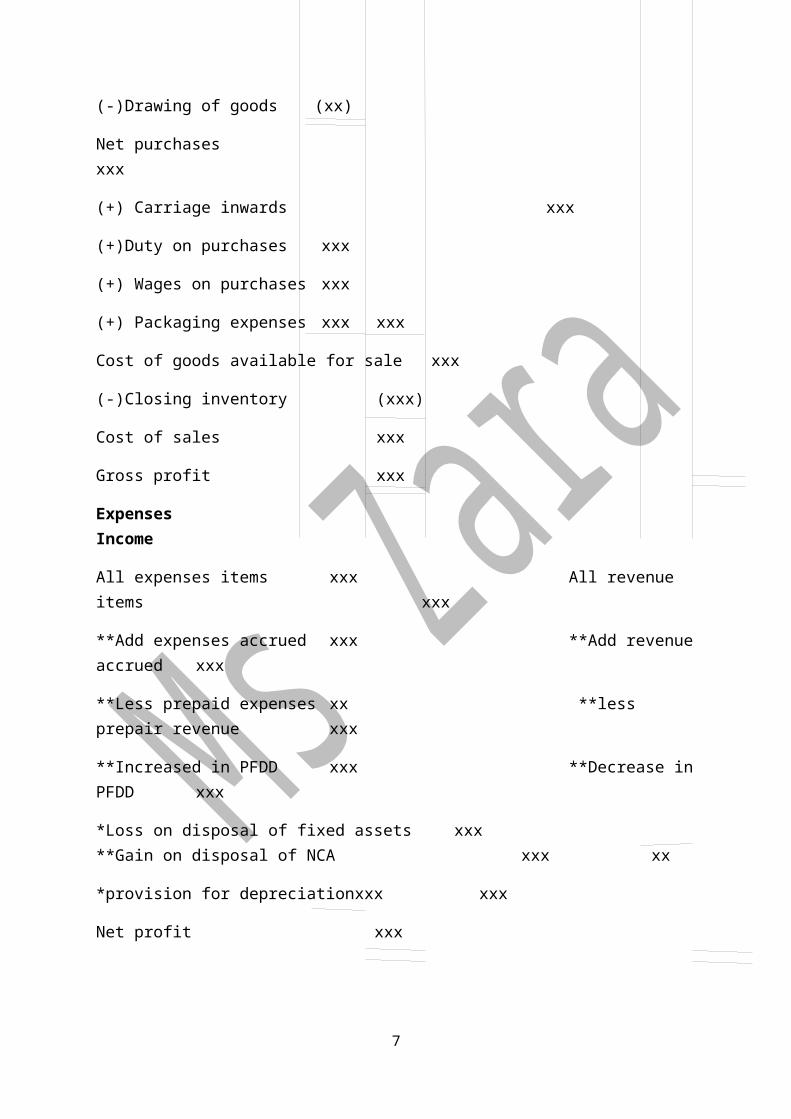

(-)Drawing of goods (xx)

Net purchases xxx

(+) Carriage inwards xxx

(+)Duty on purchases xxx

(+) Wages on purchases xxx

(+) Packaging expenses xxx xxx

Cost of goods available for sale xxx

(-)Closing inventory (xxx)

Cost of sales xxx

Gross profit xxx

Expenses Income

All expenses items xxx All revenue items xxx

**Add expenses accrued xxx **Add revenue accrued xxx

**Less prepaid expenses xx **less prepair revenue xxx

**Increased in PFDD xxx **Decrease in PFDD xxx

*Loss on disposal of fixed assets xxx **Gain on disposal of NCA xxx xx

*provision for depreciation xxx xxx

Net profit xxx

6

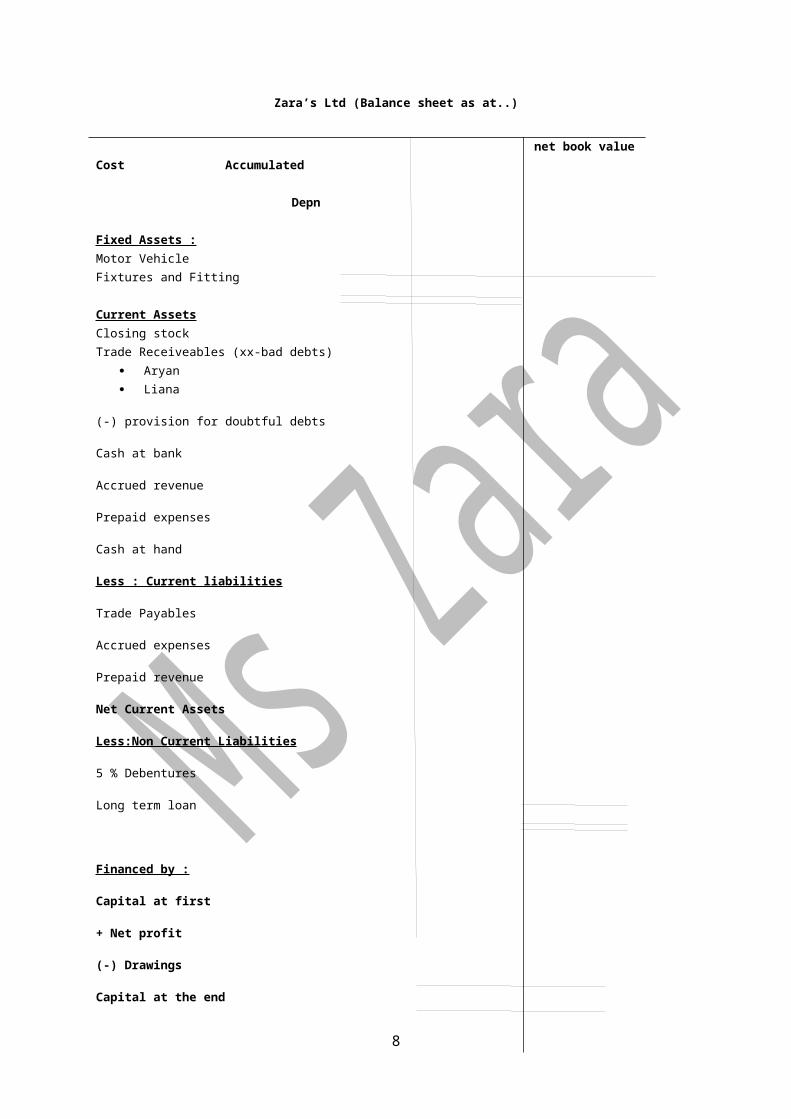

Zara’s Ltd (Balance sheet as at..)

7

Cost Accumulated Depn

Fixed Assets :Motor VehicleFixtures and Fitting

Current AssetsClosing stockTrade Receiveables (xx-bad debts)

Aryan Liana

(-) provision for doubtful debts

Cash at bank

Accrued revenue

Prepaid expenses

Cash at hand

Less : Current liabilities

Trade Payables

Accrued expenses

Prepaid revenue

Net Current Assets

Less:Non Current Liabilities

5 % Debentures

Long term loan

Financed by :

Capital at first

+ Net profit

(-) Drawings

Capital at the end

net book value

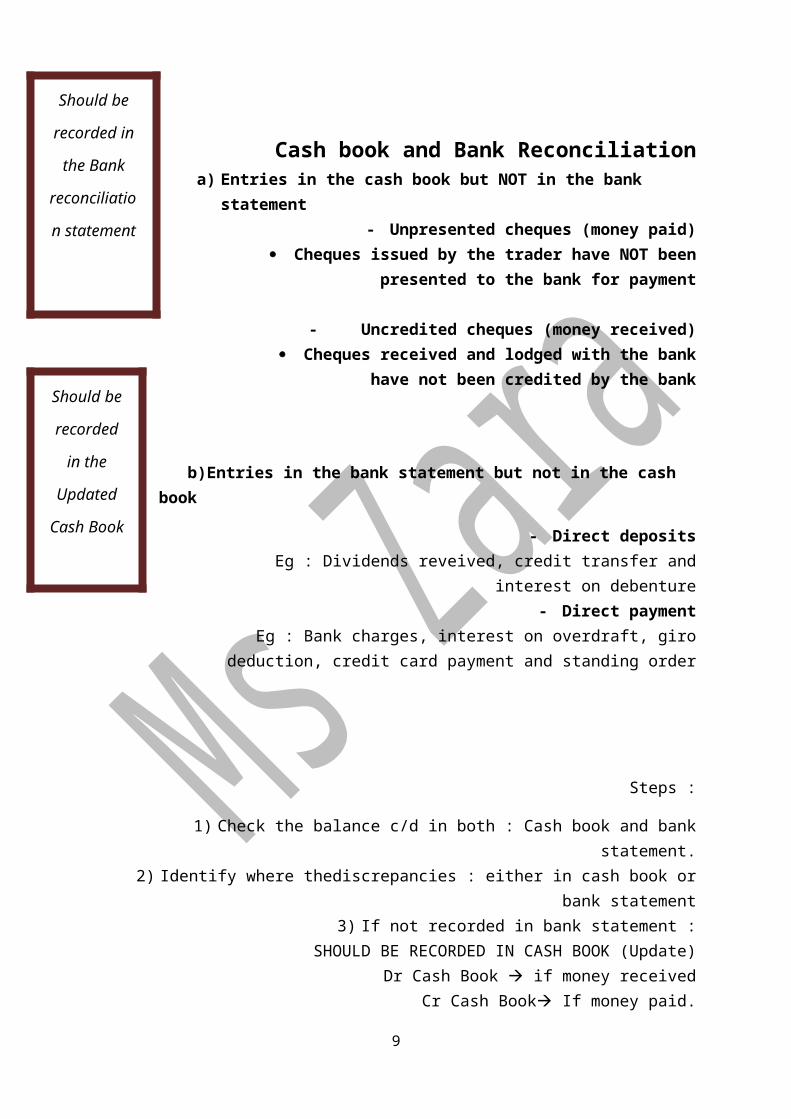

Cash book and Bank Reconciliationa) Entries in the cash book but NOT in the bank statement

- Unpresented cheques (money paid) Cheques issued by the trader have NOT been presented to

the bank for payment

- Uncredited cheques (money received) Cheques received and lodged with the bank have not been

credited by the bank

b)Entries in the bank statement but not in the cash book

- Direct deposits Eg : Dividends reveived, credit transfer and interest on debenture

- Direct paymentEg : Bank charges, interest on overdraft, giro deduction, credit card

payment and standing order

Steps :

1) Check the balance c/d in both : Cash book and bank statement.2) Identify where thediscrepancies : either in cash book or bank statement

3) If not recorded in bank statement :SHOULD BE RECORDED IN CASH BOOK (Update)

Dr Cash Book if money receivedCr Cash Book If money paid.

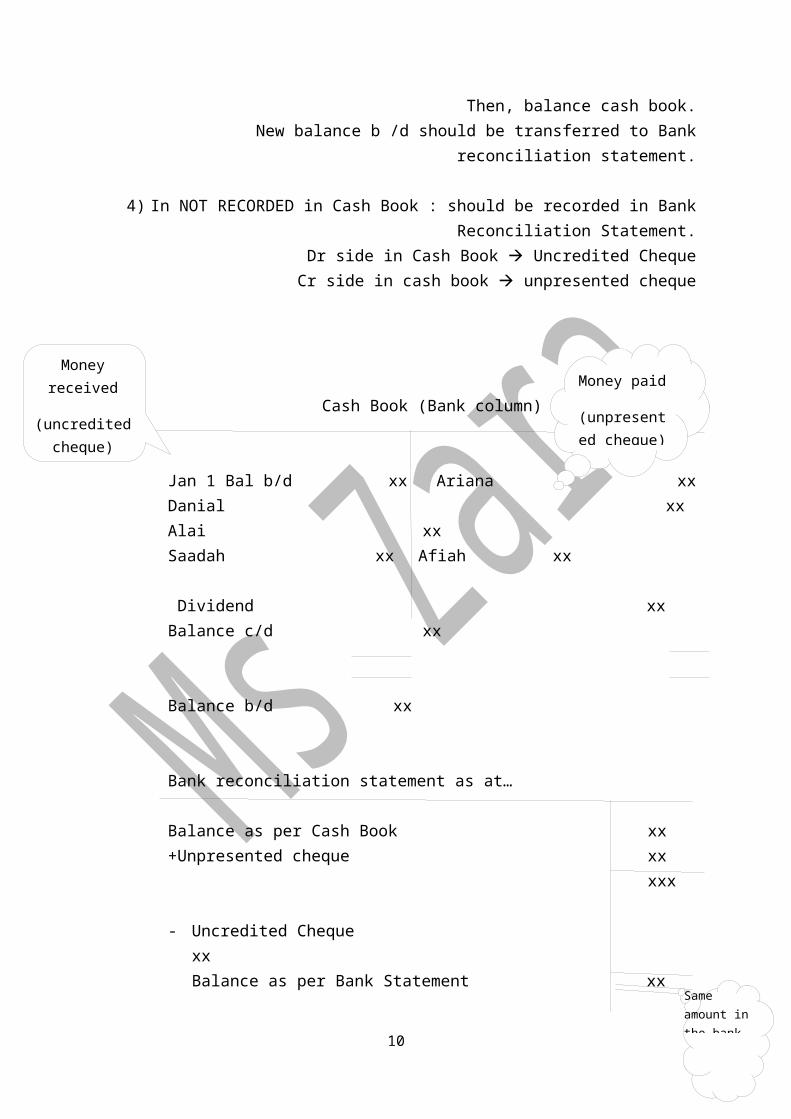

Then, balance cash book.New balance b /d should be transferred to Bank reconciliation statement.

4) In NOT RECORDED in Cash Book : should be recorded in Bank Reconciliation Statement.

Dr side in Cash Book Uncredited ChequeCr side in cash book unpresented cheque

8

Should be

recorded in

the Bank

reconciliatio

n statement

Should be

recorded

in the

Updated

Cash Book

Cash Book (Bank column)

Jan 1 Bal b/d xx Ariana xxDanial xx Alai xxSaadah xx Afiah xx

Dividend xx Balance c/d xx

Balance b/d xx

Bank reconciliation statement as at…

Balance as per Cash Book xx+Unpresented cheque xx

xxx

- Uncredited Cheque xxBalance as per Bank Statement xx

9

Money received

(uncredited cheque)

Money paid

(unpresented cheque)

Same amount in the bank

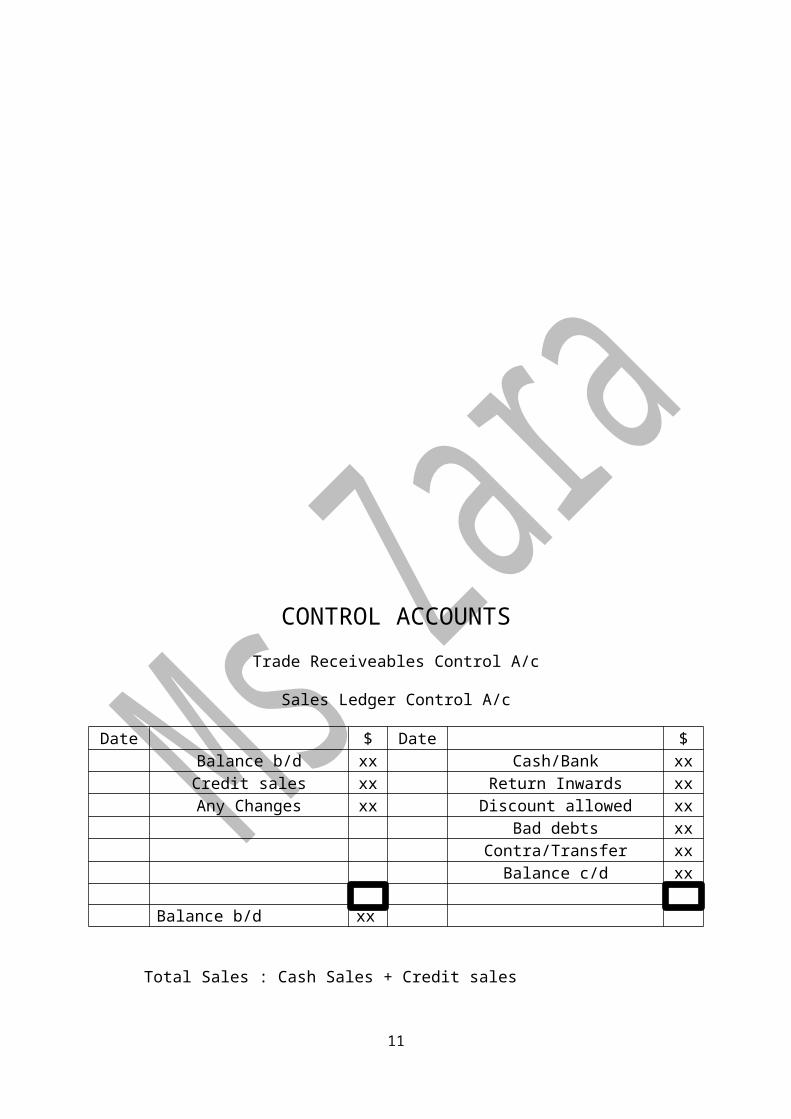

CONTROL ACCOUNTS

Trade Receiveables Control A/c

Sales Ledger Control A/c

Date $ Date $Balance b/d xx Cash/Bank xxCredit sales xx Return Inwards xx

Any Changes xx Discount allowed xxBad debts xx

Contra/Transfer xxBalance c/d xx

Balance b/d xx

Total Sales : Cash Sales + Credit sales

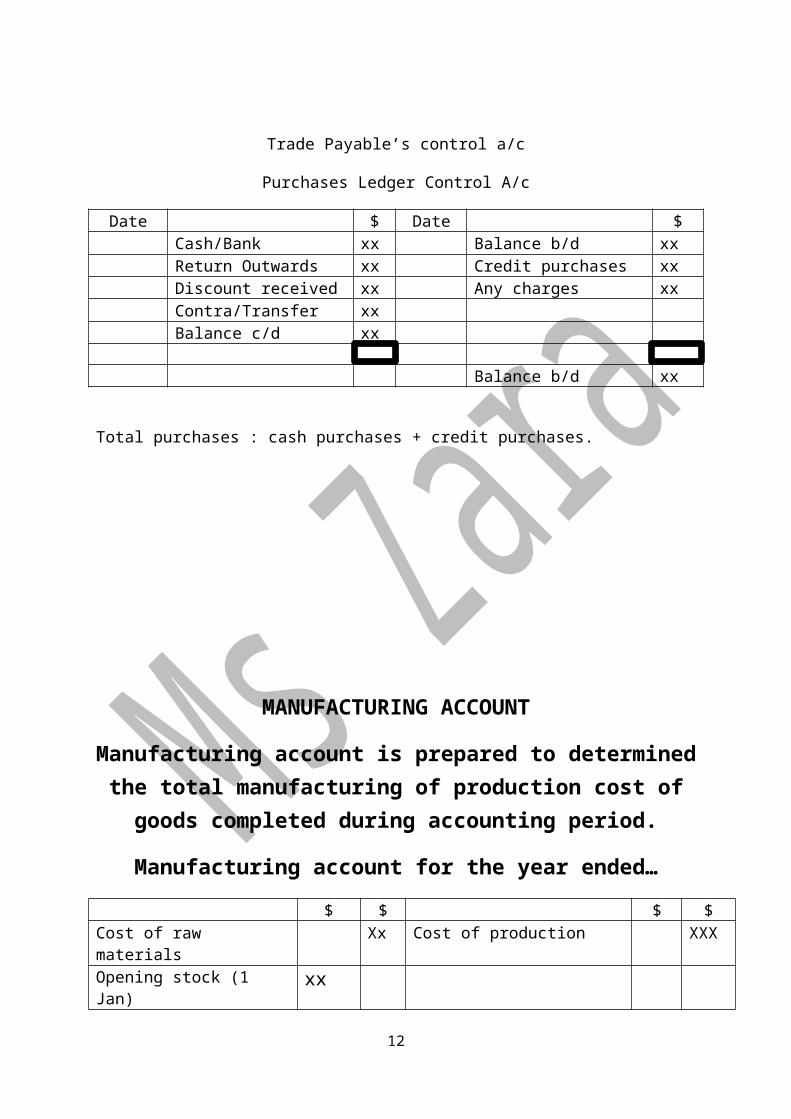

Trade Payable’s control a/c

Purchases Ledger Control A/c

Date $ Date $Cash/Bank xx Balance b/d xxReturn Outwards xx Credit purchases xxDiscount received xx Any charges xxContra/Transfer xxBalance c/d xx

Balance b/d xx

Total purchases : cash purchases + credit purchases.

10

MANUFACTURING ACCOUNT

Manufacturing account is prepared to determined the total manufacturing of production cost of goods completed during

accounting period.

Manufacturing account for the year ended…

$ $ $ $Cost of raw materials Xx Cost of production XXX

Opening stock (1 Jan) xx

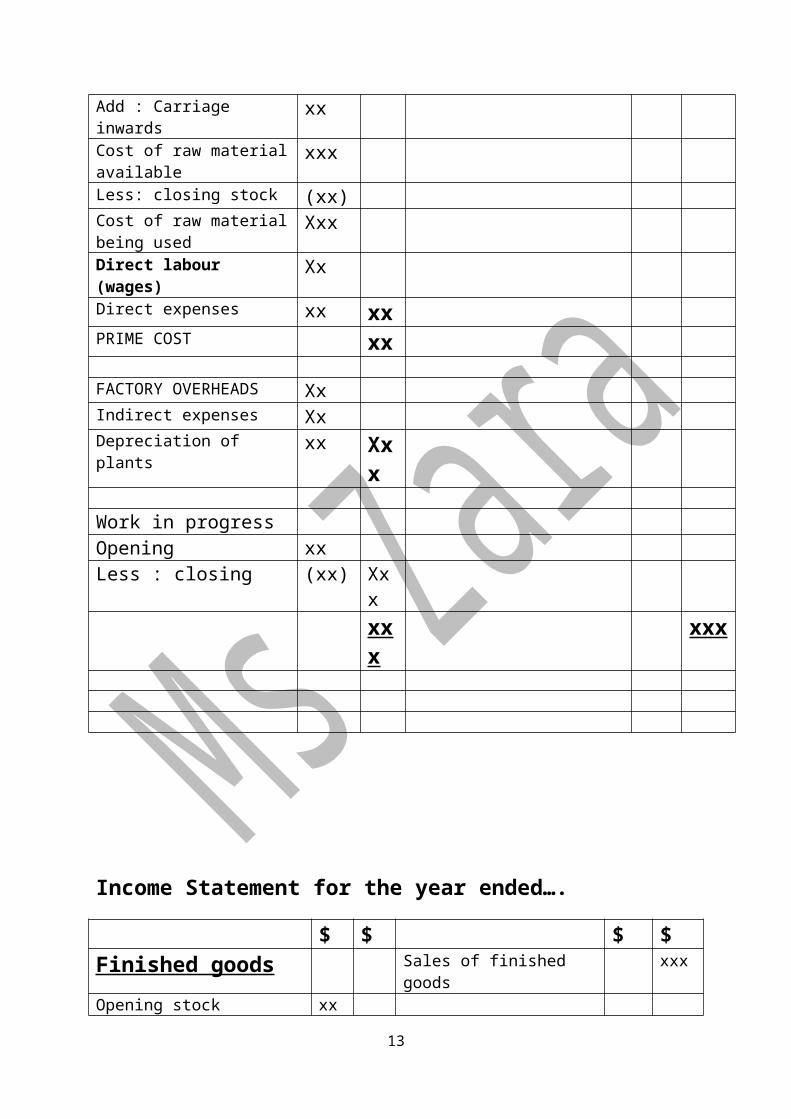

Add : Carriage inwards xxCost of raw material available xxxLess: closing stock (xx)Cost of raw material being used

Xxx

Direct labour (wages) XxDirect expenses xx xxPRIME COST xx

FACTORY OVERHEADS XxIndirect expenses XxDepreciation of plants xx Xx

x

Work in progressOpening xxLess : closing (xx) Xxx

xxx xxx

11

Income Statement for the year ended….

$ $ $ $Finished goods Sales of finished goods xxx

Opening stock xx

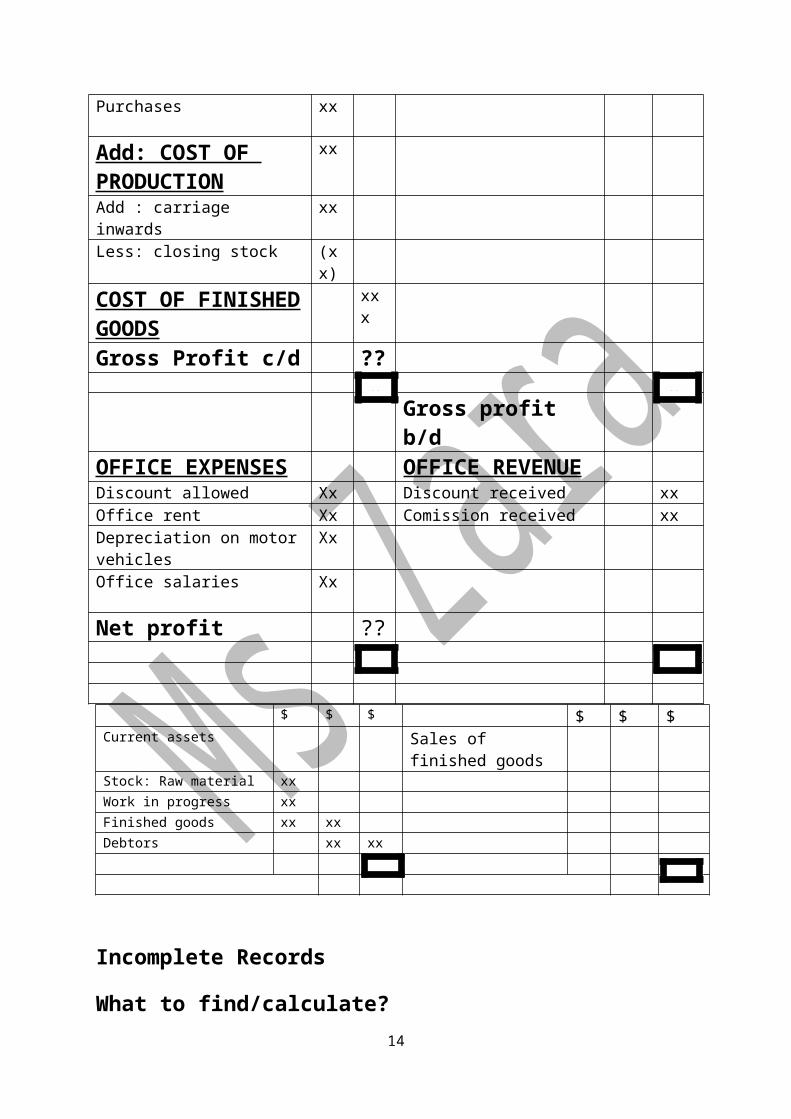

Purchases xx

Add: COST OF PRODUCTION

xx

Add : carriage inwards xx

Less: closing stock (xx)

COST OF FINISHED GOODS

xxx

Gross Profit c/d ??

Gross profit b/dOFFICE EXPENSES OFFICE REVENUEDiscount allowed Xx Discount received xx

Office rent Xx Comission received xx

Depreciation on motor vehicles Xx

Office salaries Xx

Net profit ??

$ $ $ $ $ $Current assets Sales of finished goodsStock: Raw material xxWork in progress xxFinished goods xx xxDebtors xx xx

12

xx

x xx

x xx

Incomplete Records

What to find/calculate?

I. Total purchasesII. Total sales

III. Depreciation of fixed assetIV. Capital : initial or finalV. Cash or bank balance at the end

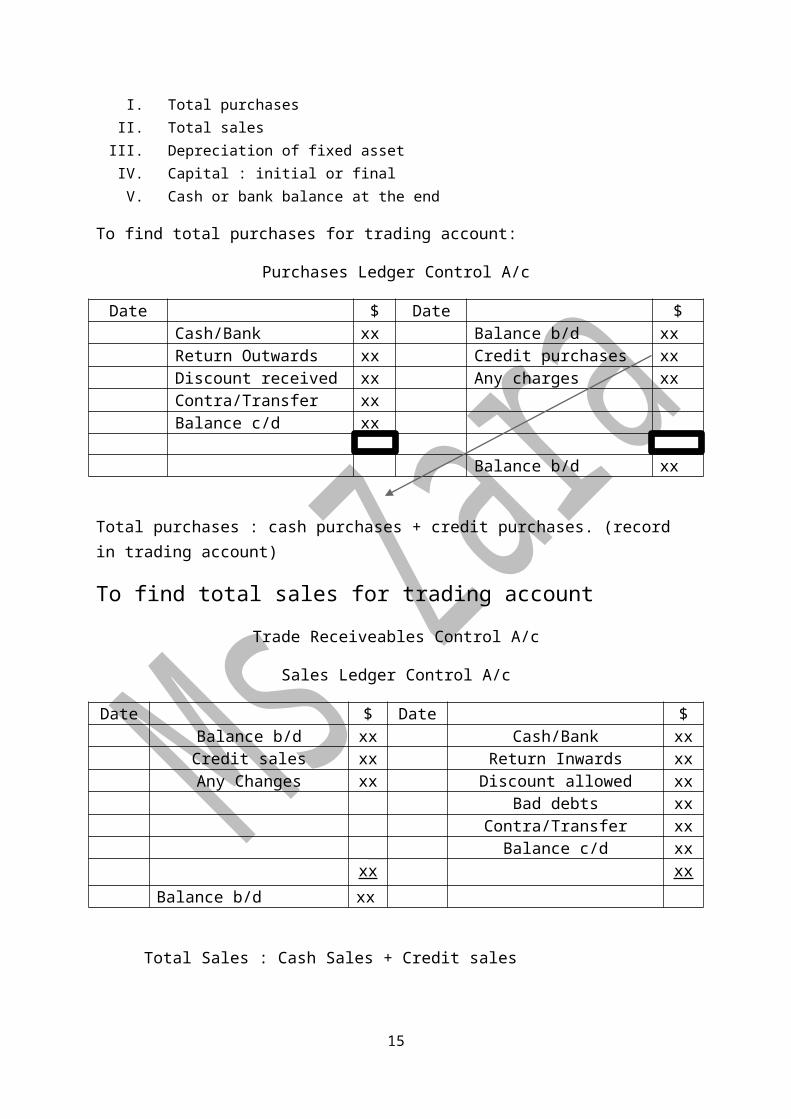

To find total purchases for trading account:

Purchases Ledger Control A/c

Date $ Date $Cash/Bank xx Balance b/d xxReturn Outwards xx Credit purchases xxDiscount received xx Any charges xxContra/Transfer xxBalance c/d xx

Balance b/d xx

Total purchases : cash purchases + credit purchases. (record in trading account)

To find total sales for trading account

Trade Receiveables Control A/c

Sales Ledger Control A/c

Date $ Date $Balance b/d xx Cash/Bank xxCredit sales xx Return Inwards xx

Any Changes xx Discount allowed xxBad debts xx

Contra/Transfer xxBalance c/d xx

xx xx

Balance b/d xx

Total Sales : Cash Sales + Credit sales

13

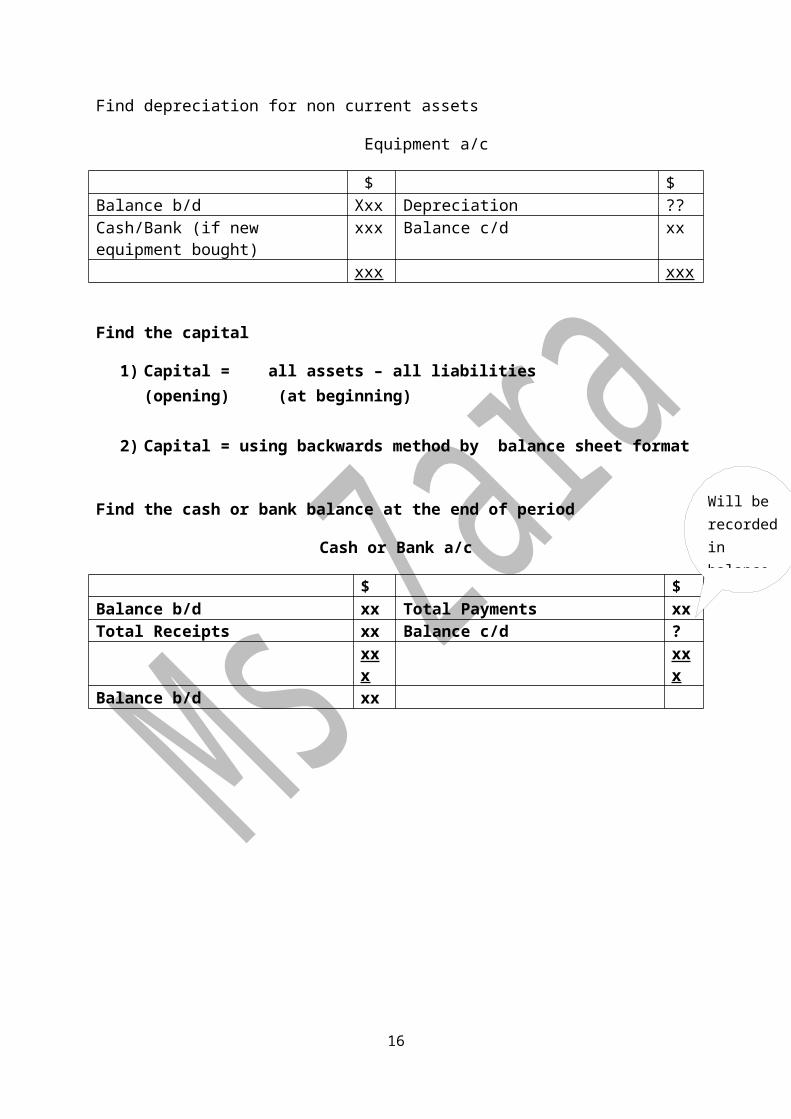

Find depreciation for non current assets

Equipment a/c

$ $Balance b/d Xxx Depreciation ??Cash/Bank (if new equipment bought)

xxx Balance c/d xx

xxx xxx

Find the capital

1) Capital = all assets – all liabilities(opening) (at beginning)

2) Capital = using backwards method by balance sheet format

Find the cash or bank balance at the end of period

Cash or Bank a/c

$ $Balance b/d xx Total Payments xxTotal Receipts xx Balance c/d ?

xxx xxx

Balance b/d xx

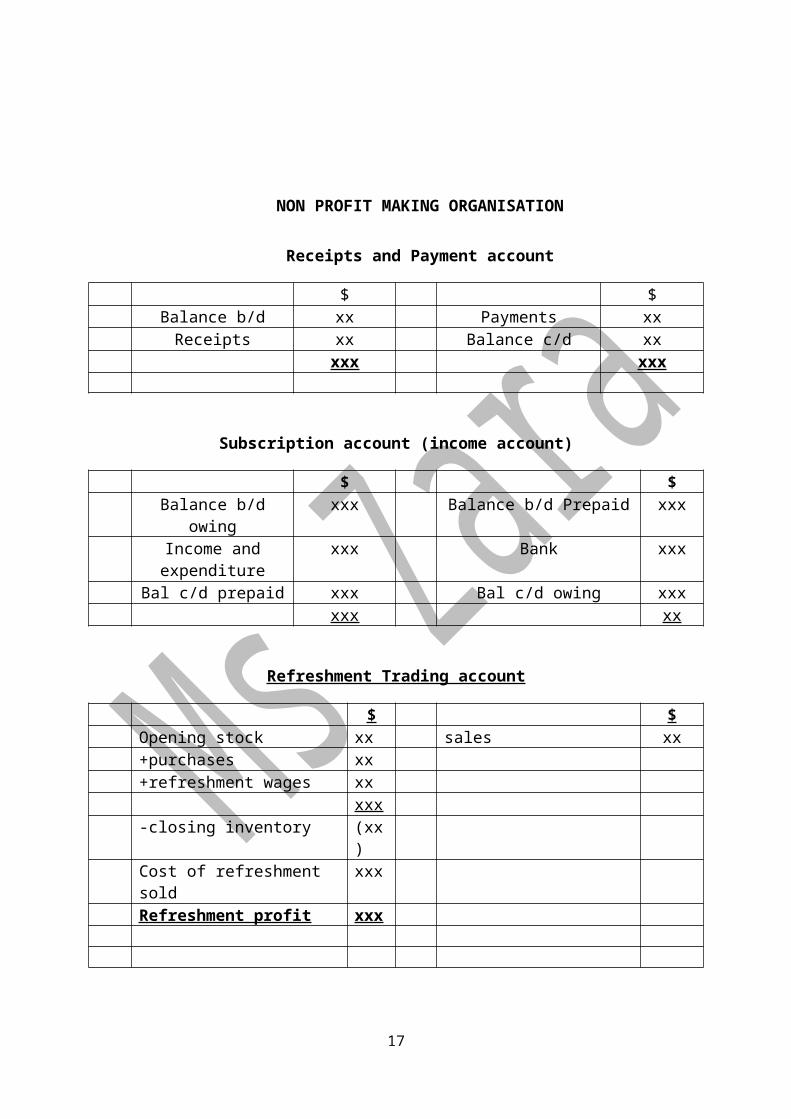

NON PROFIT MAKING ORGANISATION

14

Will be recorded in balance sheet

Receipts and Payment account

$ $Balance b/d xx Payments xx

Receipts xx Balance c/d xxxxx xxx

Subscription account (income account)

$ $Balance b/d owing xxx Balance b/d Prepaid xxx

Income and expenditure

xxx Bank xxx

Bal c/d prepaid xxx Bal c/d owing xxxxxx xx

Refreshment Trading account

$ $Opening stock xx sales xx+purchases xx+refreshment wages xx

xxx-closing inventory (xx)Cost of refreshment sold xxxRefreshment profit xxx

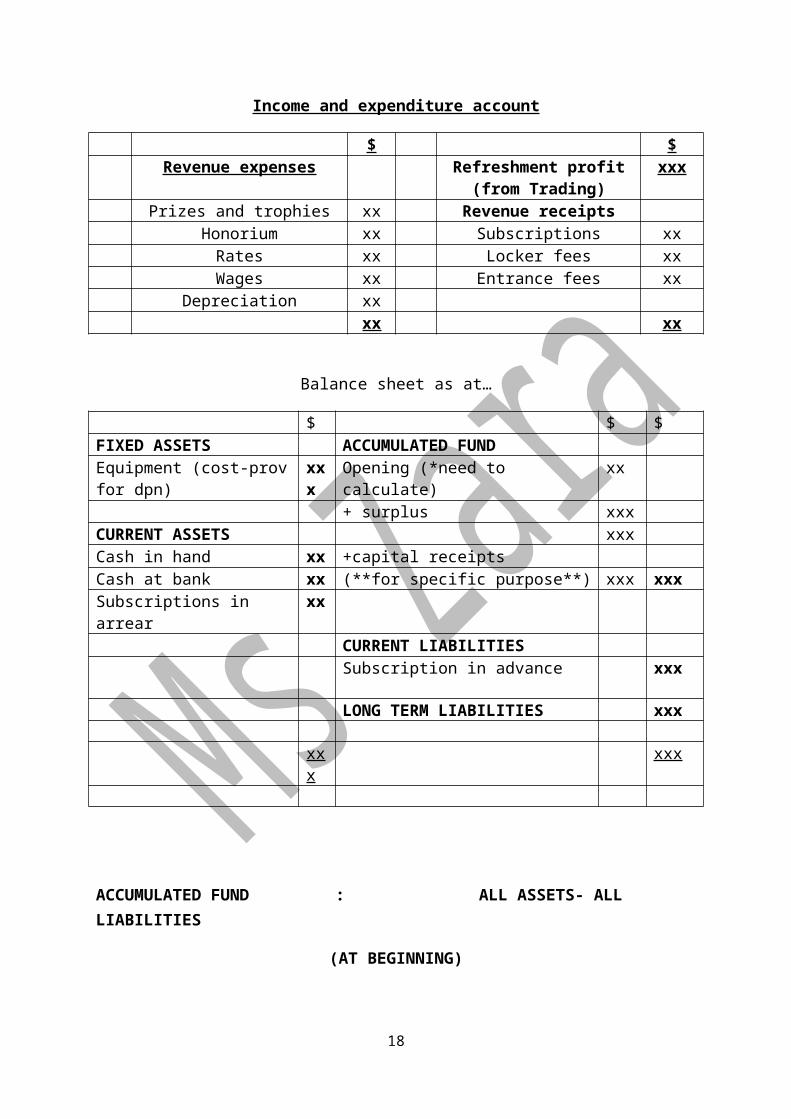

Income and expenditure account

$ $Revenue expenses Refreshment profit (from

Trading)xxx

Prizes and trophies xx Revenue receiptsHonorium xx Subscriptions xx

Rates xx Locker fees xxWages xx Entrance fees xx

Depreciation xxxx xx

15

Balance sheet as at…

$ $ $FIXED ASSETS ACCUMULATED FUNDEquipment (cost-prov for dpn)

xxx Opening (*need to calculate) xx

+ surplus xxxCURRENT ASSETS xxxCash in hand xx +capital receiptsCash at bank xx (**for specific purpose**) xxx xxxSubscriptions in arrear xx

CURRENT LIABILITIESSubscription in advance xxx

LONG TERM LIABILITIES xxx

xxx xxx

ACCUMULATED FUND : ALL ASSETS- ALL LIABILITIES

(AT BEGINNING)

16

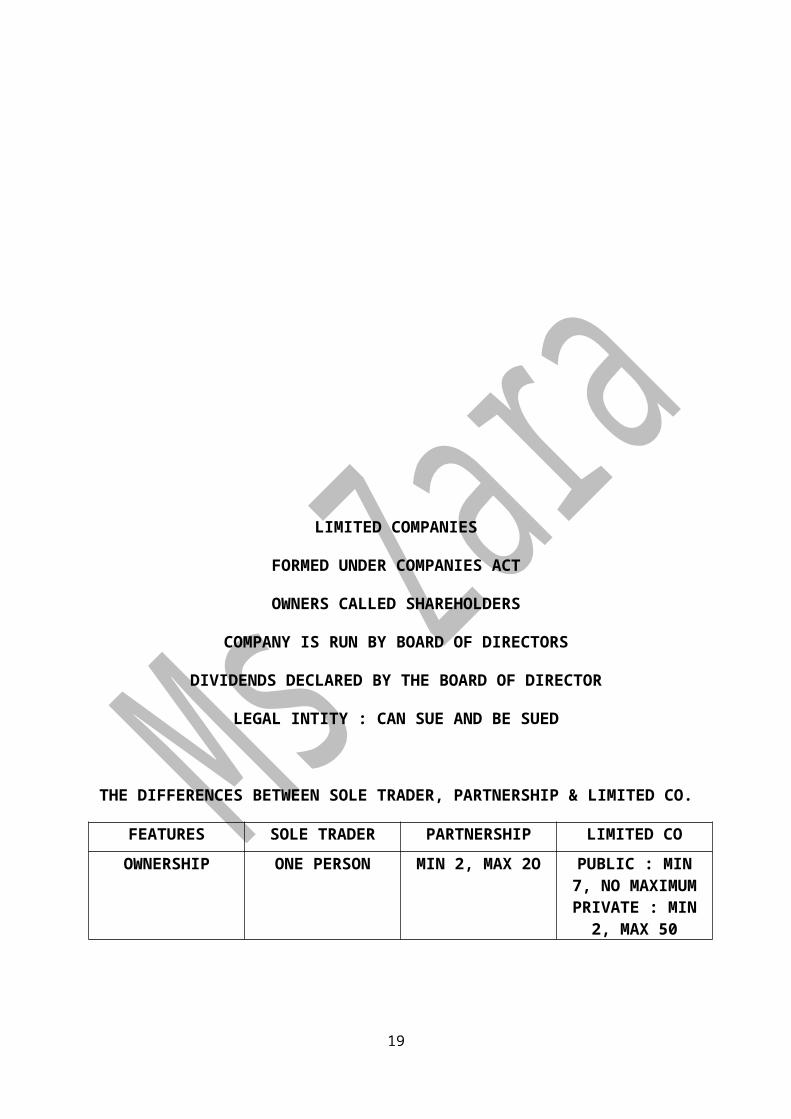

LIMITED COMPANIES

FORMED UNDER COMPANIES ACT

OWNERS CALLED SHAREHOLDERS

COMPANY IS RUN BY BOARD OF DIRECTORS

DIVIDENDS DECLARED BY THE BOARD OF DIRECTOR

LEGAL INTITY : CAN SUE AND BE SUED

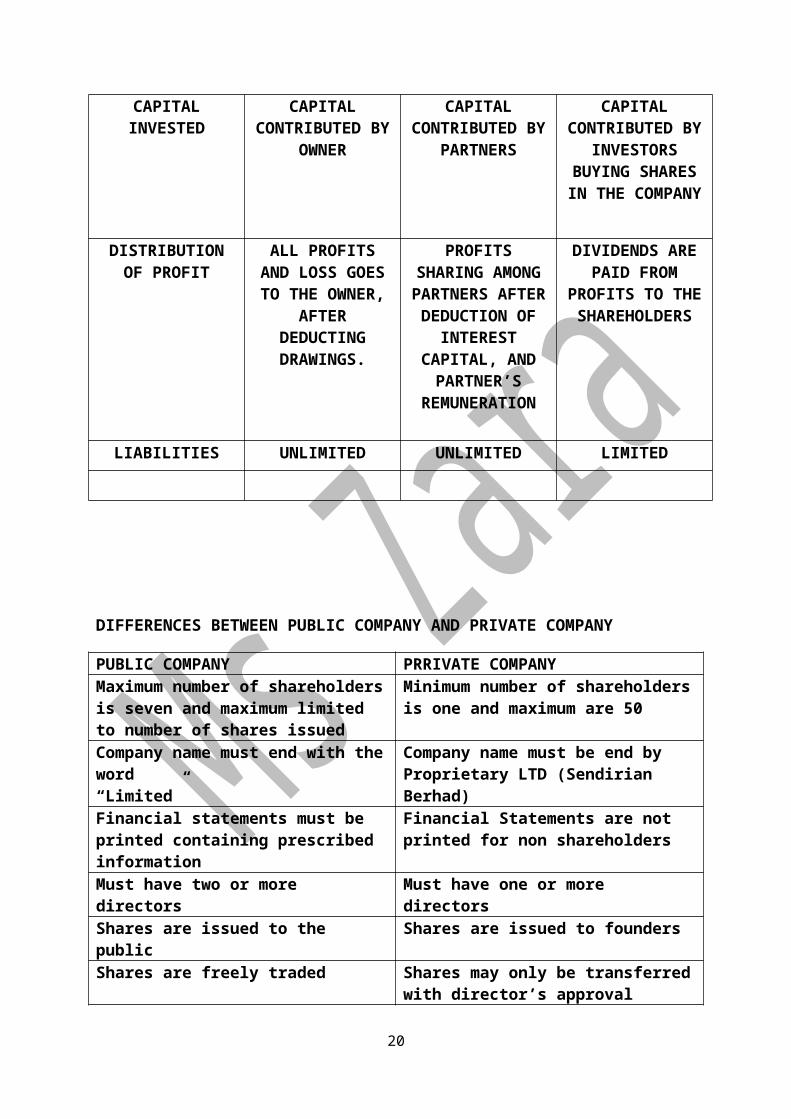

THE DIFFERENCES BETWEEN SOLE TRADER, PARTNERSHIP & LIMITED CO.

FEATURES SOLE TRADER PARTNERSHIP LIMITED CO

OWNERSHIP ONE PERSON MIN 2, MAX 2O PUBLIC : MIN 7, NO MAXIMUM

PRIVATE : MIN 2, MAX 50

CAPITAL INVESTED CAPITAL CONTRIBUTED BY

OWNER

CAPITAL CONTRIBUTED BY

PARTNERS

CAPITAL CONTRIBUTED BY

INVESTORS BUYING SHARES IN THE

COMPANY

DISTRIBUTION OF PROFIT

ALL PROFITS AND LOSS GOES TO THE

OWNER, AFTER DEDUCTING DRAWINGS.

PROFITS SHARING AMONG PARTNERS AFTER DEDUCTION

OF INTEREST CAPITAL, AND

PARTNER’S REMUNERATION

DIVIDENDS ARE PAID FROM PROFITS TO

THE SHAREHOLDERS

LIABILITIES UNLIMITED UNLIMITED LIMITED

DIFFERENCES BETWEEN PUBLIC COMPANY AND PRIVATE COMPANY

17

PUBLIC COMPANY PRRIVATE COMPANYMaximum number of shareholders is seven and maximum limited to number of shares issued

Minimum number of shareholders is one and maximum are 50

Company name must end with the word “Limited”

Company name must be end by Proprietary LTD (Sendirian Berhad)

Financial statements must be printed containing prescribed information

Financial Statements are not printed for non shareholders

Must have two or more directors Must have one or more directorsShares are issued to the public Shares are issued to foundersShares are freely traded Shares may only be transferred with

director’s approval

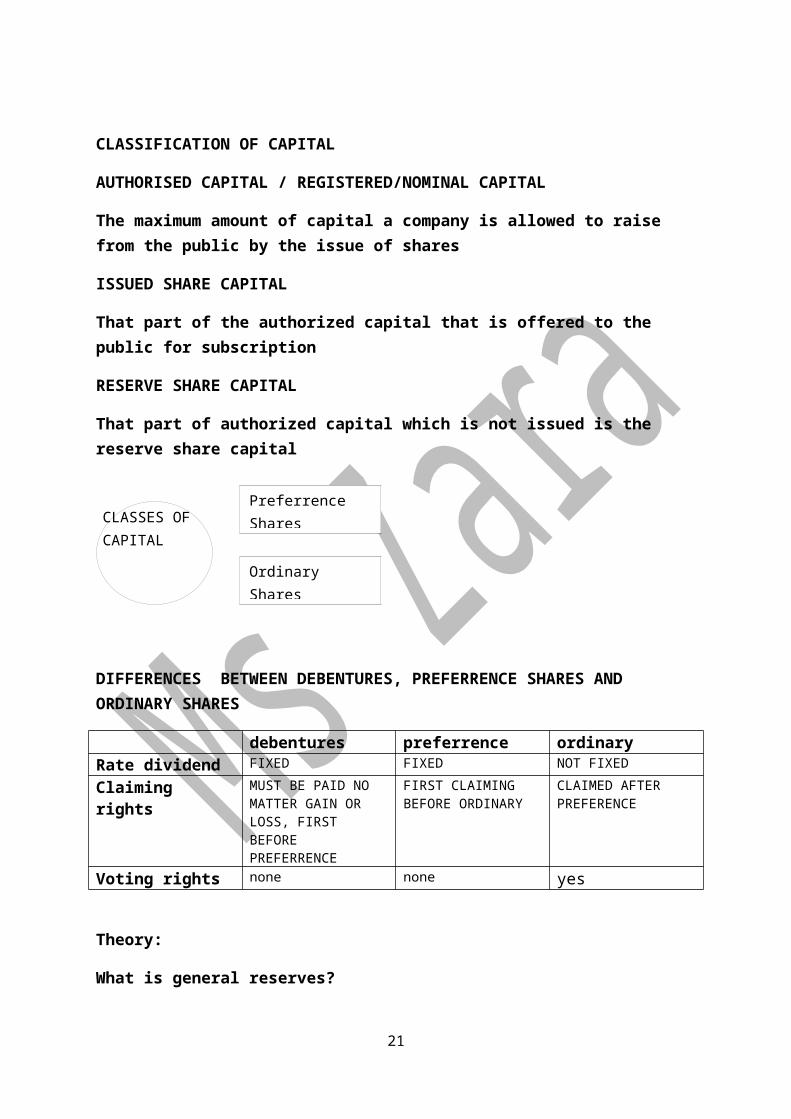

CLASSIFICATION OF CAPITAL

AUTHORISED CAPITAL / REGISTERED/NOMINAL CAPITAL

The maximum amount of capital a company is allowed to raise from the public by the issue of shares

ISSUED SHARE CAPITAL

That part of the authorized capital that is offered to the public for subscription

RESERVE SHARE CAPITAL

That part of authorized capital which is not issued is the reserve share capital

DIFFERENCES BETWEEN DEBENTURES, PREFERRENCE SHARES AND ORDINARY SHARES

debentures preferrence ordinaryRate dividend FIXED FIXED NOT FIXED

Claiming rights MUST BE PAID NO MATTER GAIN OR LOSS, FIRST BEFORE PREFERRENCE

FIRST CLAIMING BEFORE ORDINARY

CLAIMED AFTER PREFERENCE

Voting rights none none yes

18

CLASSES OF CAPITAL

Preferrence Shares

Ordinary Shares

Theory:

What is general reserves?

The funds that are set aside by a financial institutions for the sole purpose of covering possible losses that have not yet been specifically identified

Functions?

A general reserves separate retained profits which shareholders might expect to be distributed from those which are likely to be kept long term in the company

By transferring funds to a general reserve the company indicates retained profits are being reinvested long term

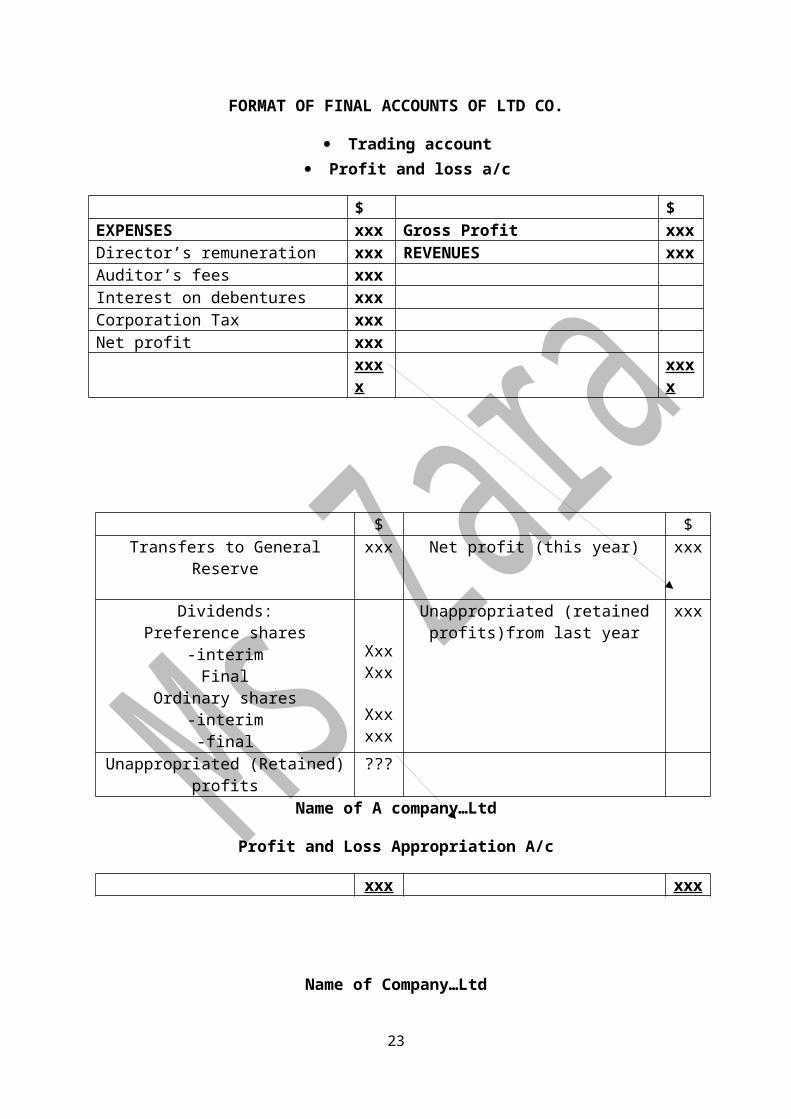

FORMAT OF FINAL ACCOUNTS OF LTD CO.

19

Trading account Profit and loss a/c

$ $EXPENSES xxx Gross Profit xxxDirector’s remuneration xxx REVENUES xxxAuditor’s fees xxxInterest on debentures xxxCorporation Tax xxxNet profit xxx

xxxx xxxx

$ $Transfers to General Reserve xxx Net profit (this year) xxx

Dividends:Preference shares

-interimFinal

Ordinary shares-interim

-final

XxxXxx

Xxxxxx

Unappropriated (retained profits)from last year

xxx

Unappropriated (Retained) profits ???Name of A company…Ltd

Profit and Loss Appropriation A/c

Name of Company…Ltd

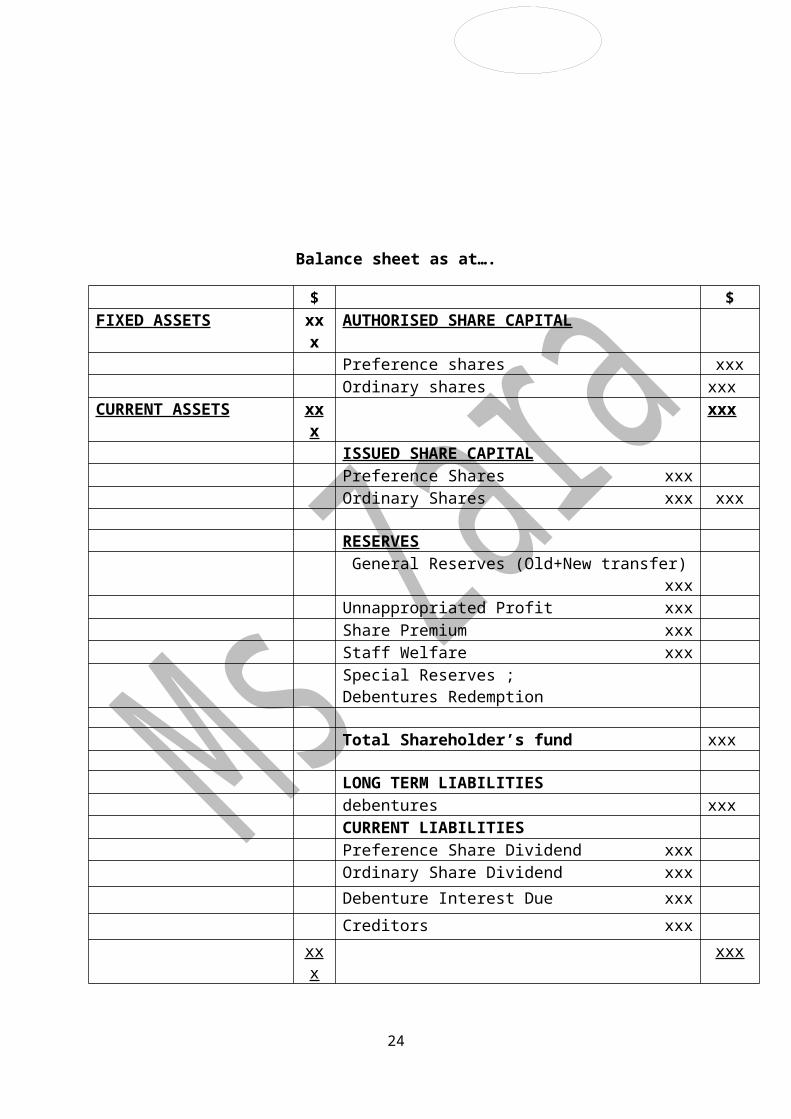

Balance sheet as at….

20

Transfer to balance sheet

xxx xxx

$ $FIXED ASSETS xxx AUTHORISED SHARE CAPITAL

Preference shares xxxOrdinary shares xxx

CURRENT ASSETS xxx xxxISSUED SHARE CAPITALPreference Shares xxxOrdinary Shares xxx xxx

RESERVES General Reserves (Old+New transfer) xxxUnnappropriated Profit xxxShare Premium xxxStaff Welfare xxxSpecial Reserves ;Debentures Redemption

Total Shareholder’s fund xxx

LONG TERM LIABILITIESdebentures xxxCURRENT LIABILITIESPreference Share Dividend xxxOrdinary Share Dividend xxx

Debenture Interest Due xxx

Creditors xxx

xxx xxx

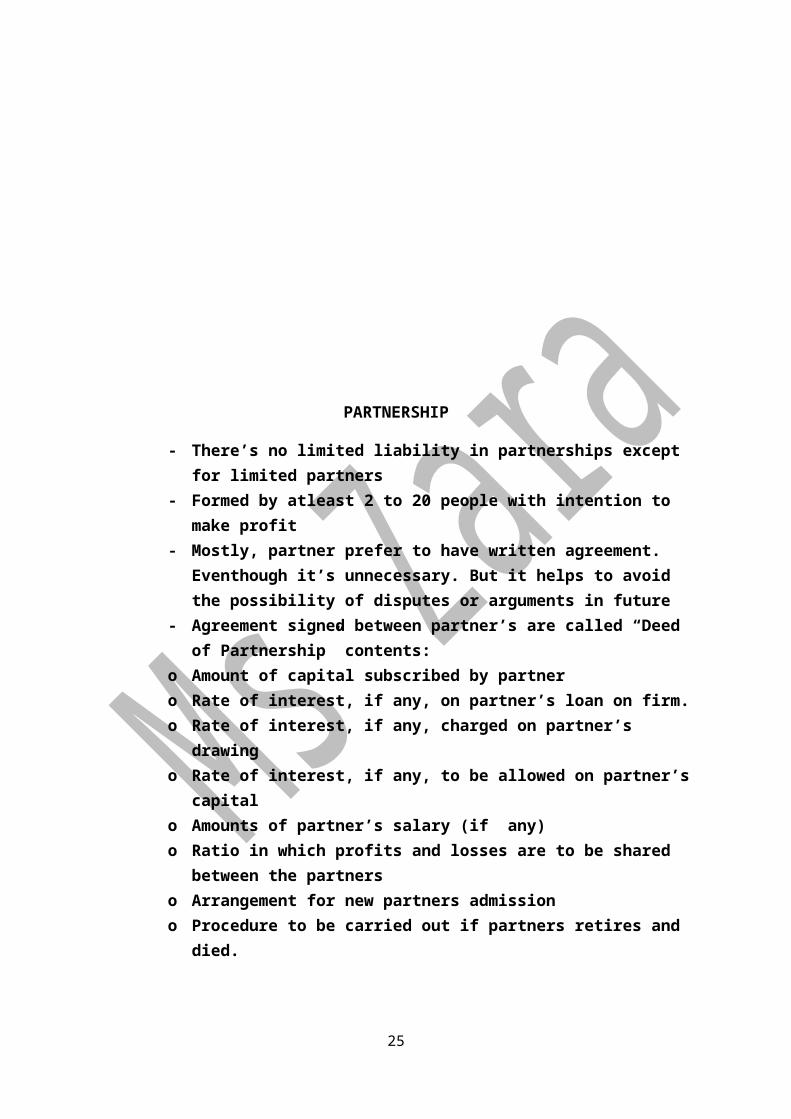

PARTNERSHIP

21

- There’s no limited liability in partnerships except for limited partners- Formed by atleast 2 to 20 people with intention to make profit- Mostly, partner prefer to have written agreement. Eventhough it’s

unnecessary. But it helps to avoid the possibility of disputes or arguments in future

- Agreement signed between partner’s are called “Deed of Partnership” contents:

o Amount of capital subscribed by partnero Rate of interest, if any, on partner’s loan on firm.o Rate of interest, if any, charged on partner’s drawingo Rate of interest, if any, to be allowed on partner’s capitalo Amounts of partner’s salary (if any)o Ratio in which profits and losses are to be shared between the partnerso Arrangement for new partners admission o Procedure to be carried out if partners retires and died.

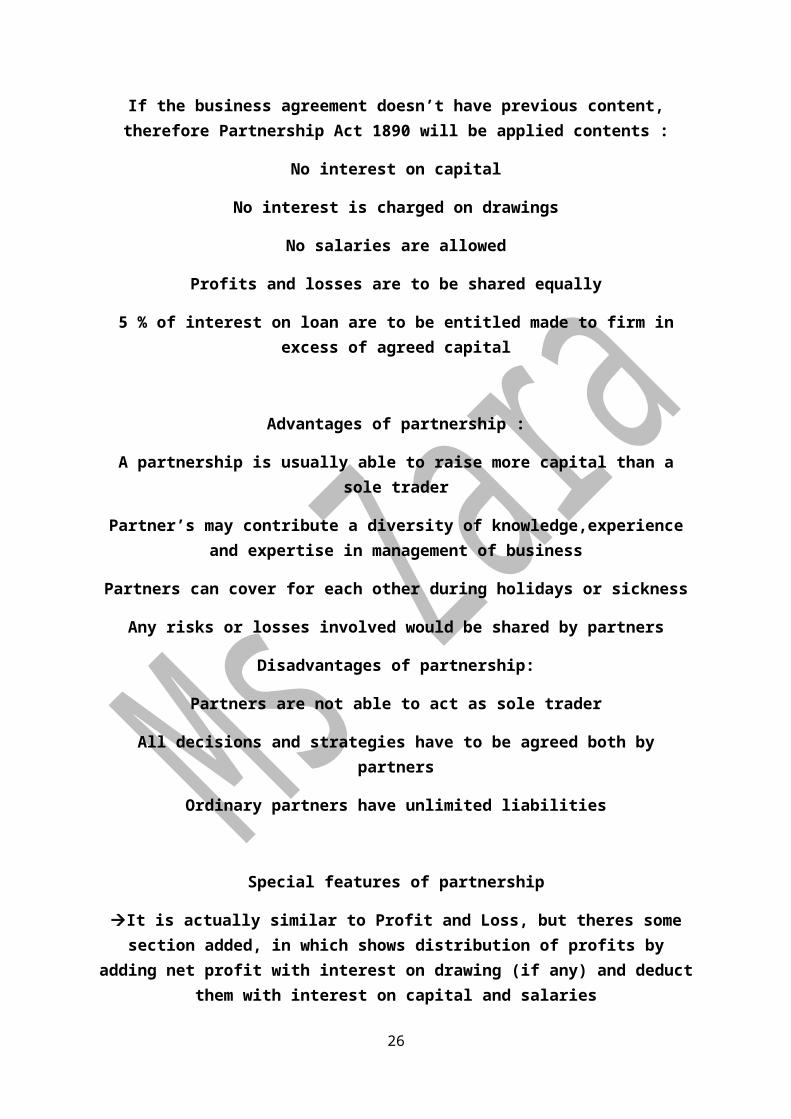

If the business agreement doesn’t have previous content, therefore Partnership Act 1890 will be applied contents :

No interest on capital

No interest is charged on drawings

No salaries are allowed

Profits and losses are to be shared equally

5 % of interest on loan are to be entitled made to firm in excess of agreed capital

Advantages of partnership :

A partnership is usually able to raise more capital than a sole trader

Partner’s may contribute a diversity of knowledge,experience and expertise in management of business

Partners can cover for each other during holidays or sickness

Any risks or losses involved would be shared by partners

Disadvantages of partnership:

Partners are not able to act as sole trader

All decisions and strategies have to be agreed both by partners

22

Ordinary partners have unlimited liabilities

Special features of partnership

It is actually similar to Profit and Loss, but theres some section added, in which shows distribution of profits by adding net profit with interest on drawing (if any) and deduct

them with interest on capital and salaries

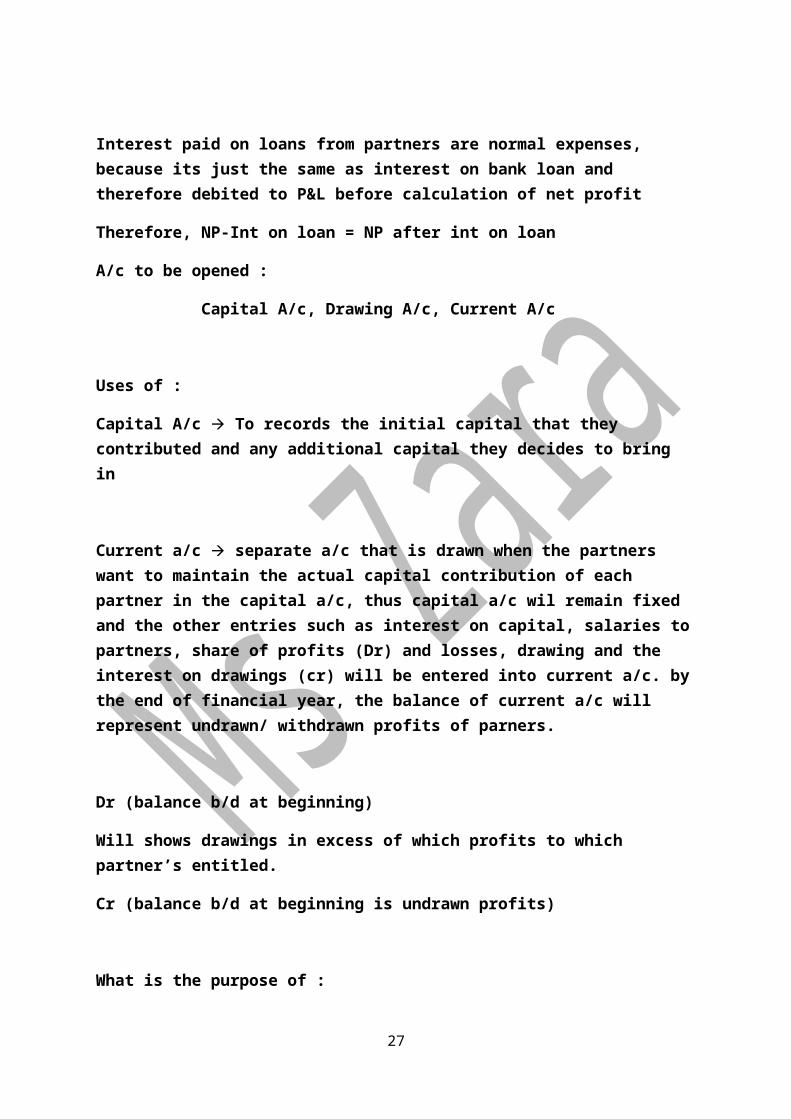

Interest paid on loans from partners are normal expenses, because its just the same as interest on bank loan and therefore debited to P&L before calculation of net profit

Therefore, NP-Int on loan = NP after int on loan

A/c to be opened :

Capital A/c, Drawing A/c, Current A/c

Uses of :

Capital A/c To records the initial capital that they contributed and any additional capital they decides to bring in

Current a/c separate a/c that is drawn when the partners want to maintain the actual capital contribution of each partner in the capital a/c, thus capital a/c wil remain fixed and the other entries such as interest on capital, salaries to partners, share of profits (Dr) and losses, drawing and the interest on drawings (cr) will be entered into current a/c. by the end of financial year, the balance of current a/c will represent undrawn/ withdrawn profits of parners.

Dr (balance b/d at beginning)

Will shows drawings in excess of which profits to which partner’s entitled.

Cr (balance b/d at beginning is undrawn profits)

What is the purpose of :

23

i) Preparing profit and loss? To find net profitii) Preparing Profit loss appropriation a/c? To show net profit of business and share

profits of partners. It is a bit similar to normal P&L but with additional section. NP will be added to interest on drawing and will be deducted with salaries and interest on capital

iii) Why interest is allowed on capital? To overcome the difficulty of compensating for the investment of capital

iv) Why interest charged on drawings?To deters the partners from taking out the cash unnecessarily. (The more cash in the business the more expansion can be financed)

v) Why interest charged on drawings?To deters the partners from taking out the cash unnecessarily. (The more cash in the business the more expansion can be financed)

HOW TO RAISE CAPITAL IN THE BUSINESS?ADD IN NEW PARTNER : Adv: raise business capital and eases workloadDis: Share of profits shall decreaseFORMING PRIVATE LTD CO:Adv: No workloadDis: Profits getting lesserSAVE UP OWN MONEY :Adv : No need to loan or borrow moneyDis: It takes time.SALE THEIR FIXED ASSETS, LEASED BACK.Adv : able to limit expensesDis : the machine might broke down.

AMALGAMATION 0F PARTNERSHIP – MERGE OF TWO BUSINESS INTO A PARTNERSHIP

STEPS :o Consider the goodwillo Revalue the assetso Disclose all liabilities or bring them into partnership

i) Goodwill and an increase in the value of assets will increase the capital of the owner. A decrease in the value of the assets will decrease his capital

ii) If a liability is discharged by additional cash brought in by the owner, his capital will increase

24

iii) Goodwill, the adjusted capitals, existing liabilities and the new values of the assets of the partners are combined in the balance sheet of new partnership.

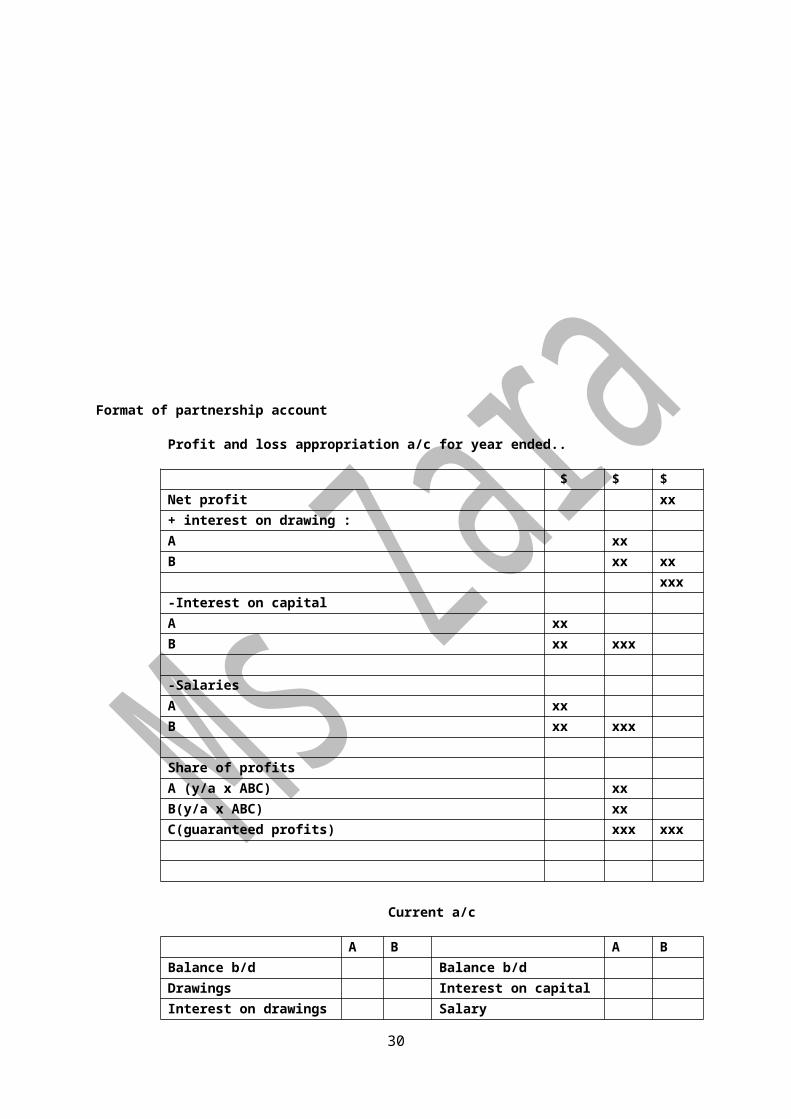

Format of partnership account

25

Profit and loss appropriation a/c for year ended..

$ $ $Net profit xx+ interest on drawing :A xxB xx xx

xxx-Interest on capitalA xxB xx xxx

-SalariesA xxB xx xxx

Share of profitsA (y/a x ABC) xxB(y/a x ABC) xxC(guaranteed profits) xxx xxx

Current a/c

A B A BBalance b/d Balance b/dDrawings Interest on capitalInterest on drawings SalaryShare of loss Interest on loanBalance c/d Share of profits

xxx xxx xxx xxxBalance b/d

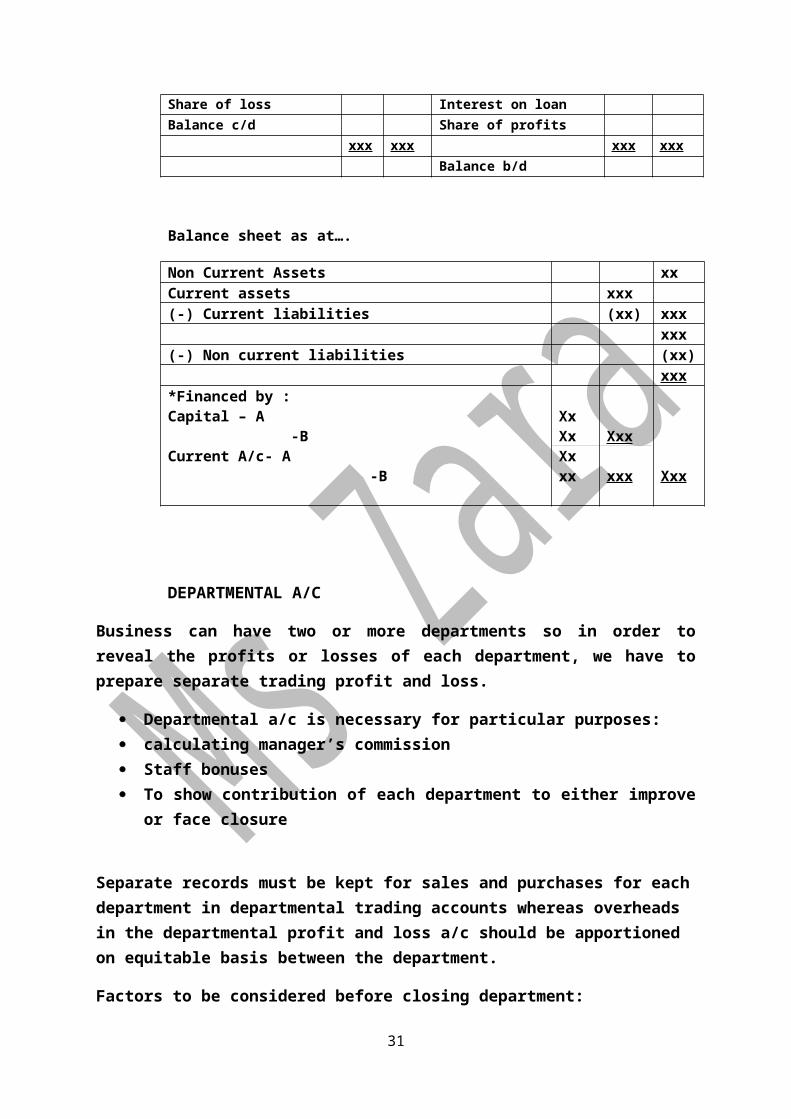

Balance sheet as at….

Non Current Assets xxCurrent assets xxx(-) Current liabilities (xx) xxx

xxx(-) Non current liabilities (xx)

xxx*Financed by :Capital – A -BCurrent A/c- A -B

XxXxXxxx

Xxx

xxx Xxx

26

DEPARTMENTAL A/C

Business can have two or more departments so in order to reveal the profits or losses of each department, we have to prepare separate trading profit and loss.

Departmental a/c is necessary for particular purposes: calculating manager’s commission Staff bonuses To show contribution of each department to either improve or face closure

Separate records must be kept for sales and purchases for each department in departmental trading accounts whereas overheads in the departmental profit and loss a/c should be apportioned on equitable basis between the department.

Factors to be considered before closing department:

Loss : making department may in fact be attracting customers for other departments

The possibility of using the space freed by closure for the benefit of the other departments for a new department

Cost of closing department Closure may have social consequences the department may be providing only

source of supply or service to the local community Other department may suffer id the loss making department, the lesser the

department, the higher overheads must the department pay. A profitable department may appear to be making a loss because the

apportionment of overheads between the department is unfair on not equitable.

27

CONCEPTS :

28

29

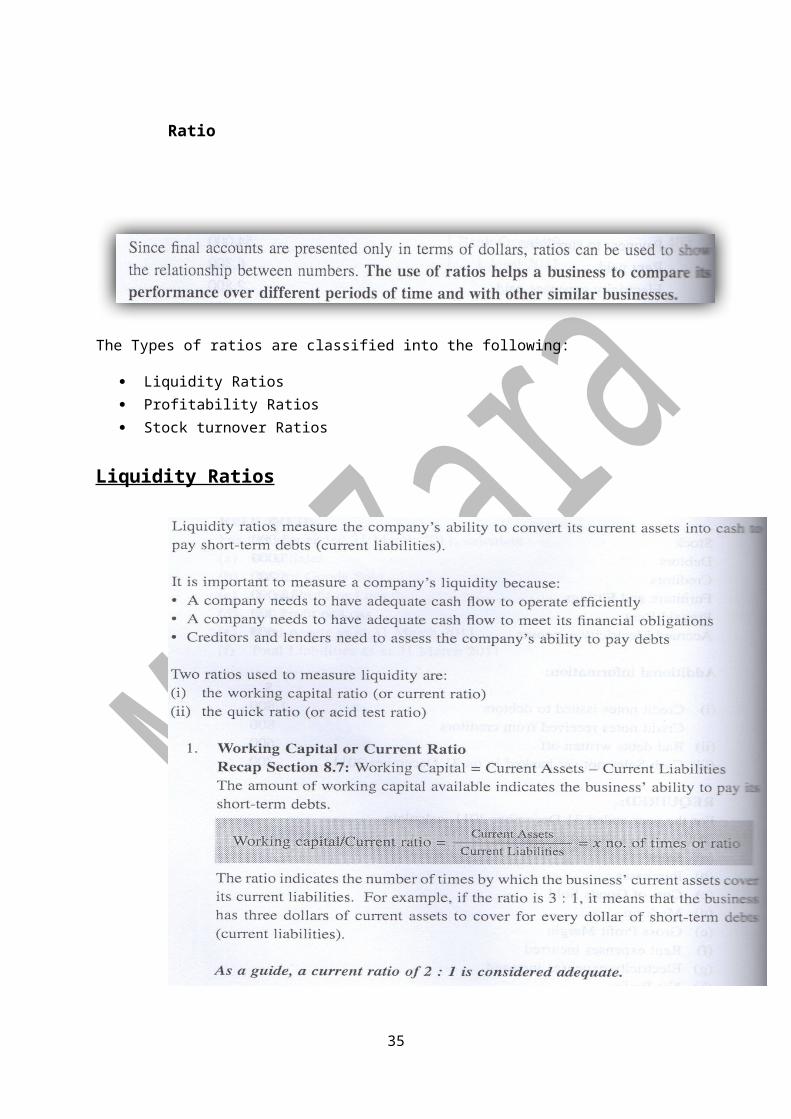

Ratio

The Types of ratios are classified into the following:

Liquidity Ratios Profitability Ratios Stock turnover Ratios

Liquidity Ratios

30

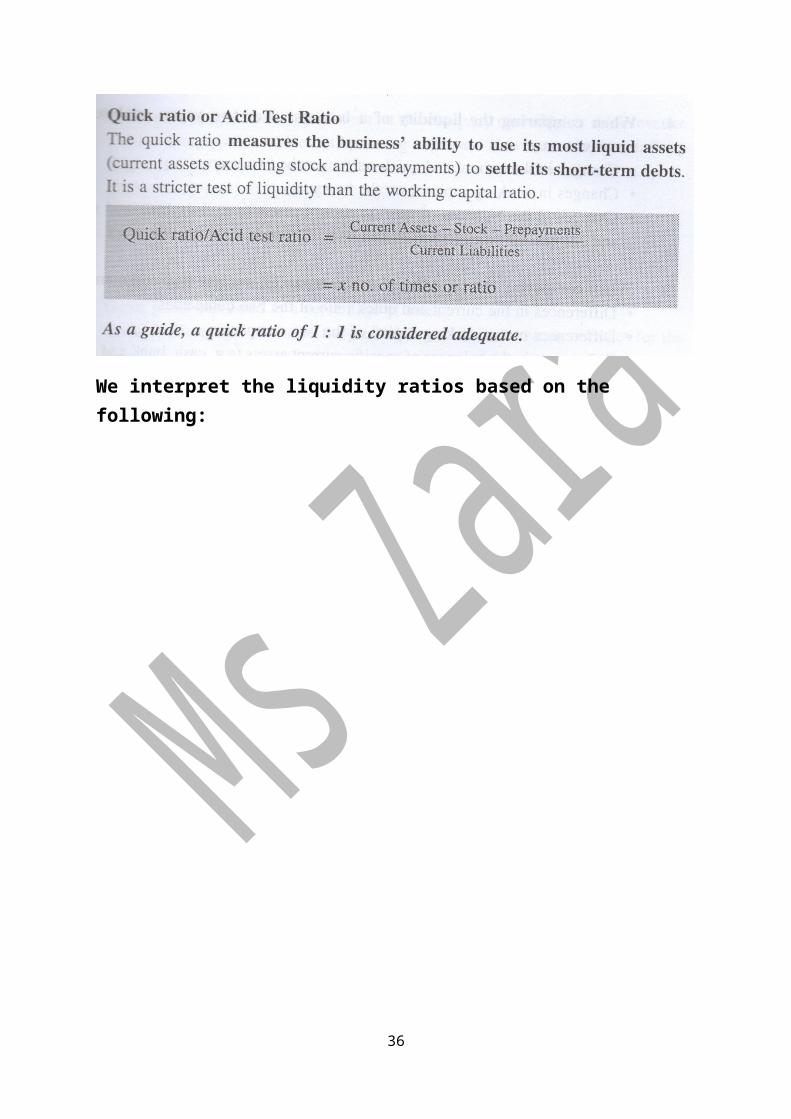

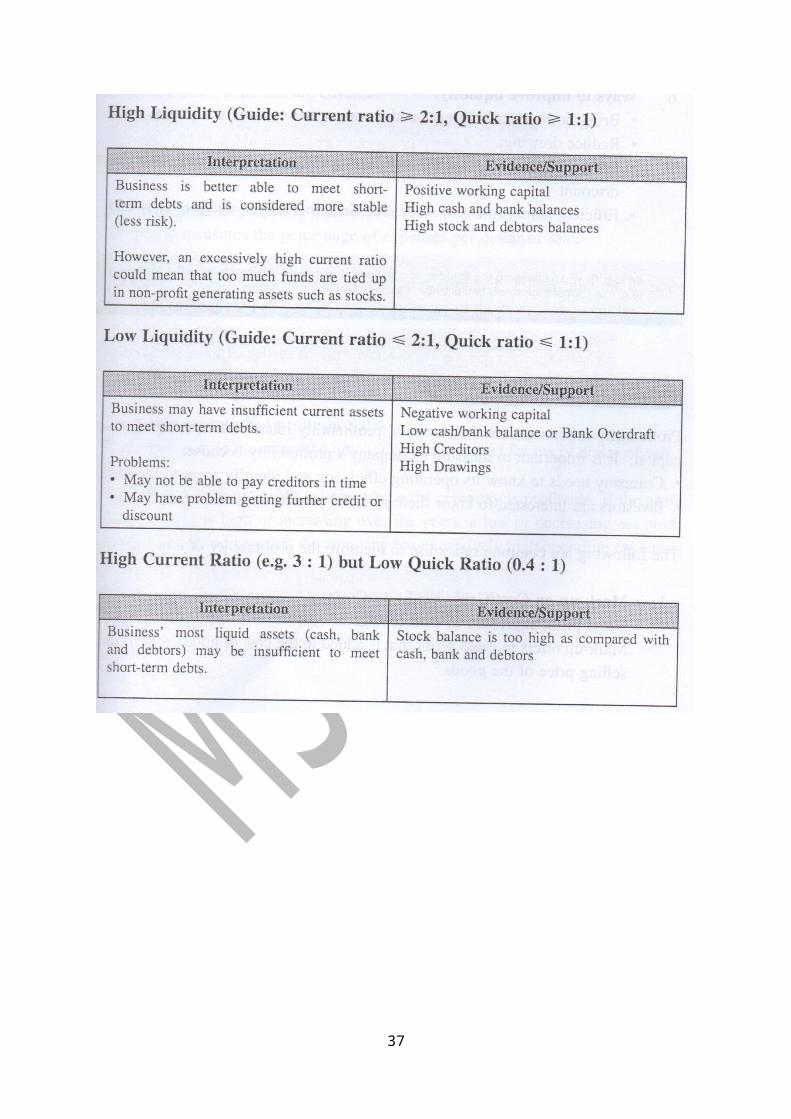

We interpret the liquidity ratios based on the following:

31

32

33

PROFITABLITY RATIOS

34

35

36

STOCK TURNOVER RATIO

Stock should be valued on the basis of the lower of either cost or ‘net realisable value (market price).

37