Company Presentation - Indofood Agri Resources...

25

Company Presentation – 4Q and FY 2012 Results 27 Feb 2013 Company Presentation – 2Q and 1H 2013 Results 14 Aug 2013

Transcript of Company Presentation - Indofood Agri Resources...

Company Presentation – 4Q and FY 2012 Results27 Feb 2013

Company Presentation – 2Q and 1H 2013 Results14 Aug 2013

Integrated Agribusiness with Leading Brands

1 1

Click to edit Master title style

Presentation Outline

11 Plantation Highlights Plantation Highlights

22 Financial Highlights Financial Highlights

33 Strategies and ExpansionStrategies and Expansion

44 AppendixAppendix

2

Section 1Plantation Highlights

Integrated Agribusiness with Leading Brands

3

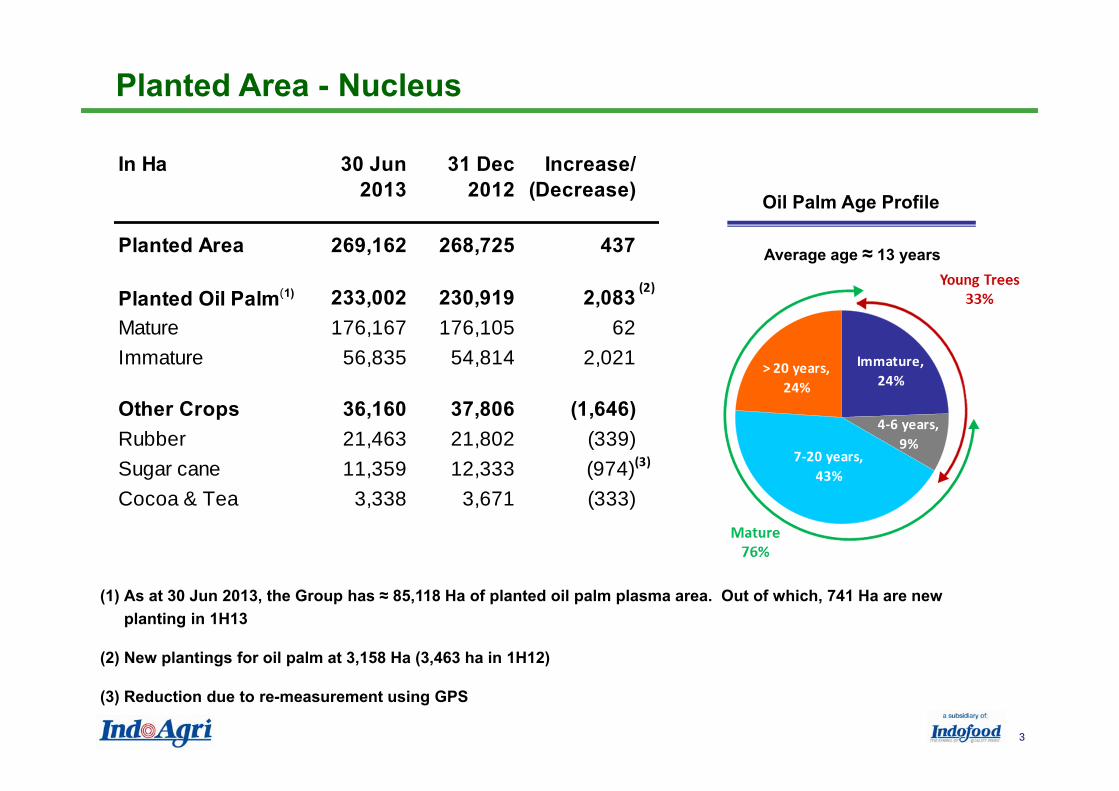

Average age ≈ 13 years

(1) As at 30 Jun 2013, the Group has ≈ 85,118 Ha of planted oil palm plasma area. Out of which, 741 Ha are new planting in 1H13

(2) New plantings for oil palm at 3,158 Ha (3,463 ha in 1H12)

(3) Reduction due to re-measurement using GPS

Planted Area - Nucleus

Oil Palm Age Profile

In Ha 30 Jun 2013

31 Dec 2012

Increase/(Decrease)

Planted Area 269,162 268,725 437

Planted Oil Palm(1) 233,002 230,919 2,083 Mature 176,167 176,105 62 Immature 56,835 54,814 2,021

Other Crops 36,160 37,806 (1,646)Rubber 21,463 21,802 (339)Sugar cane 11,359 12,333 (974)Cocoa & Tea 3,338 3,671 (333)

(2)

(3)

> 20 years, 24%

Immature, 24%

4‐6 years, 9%

7‐20 years, 43%

Integrated Agribusiness with Leading Brands

4

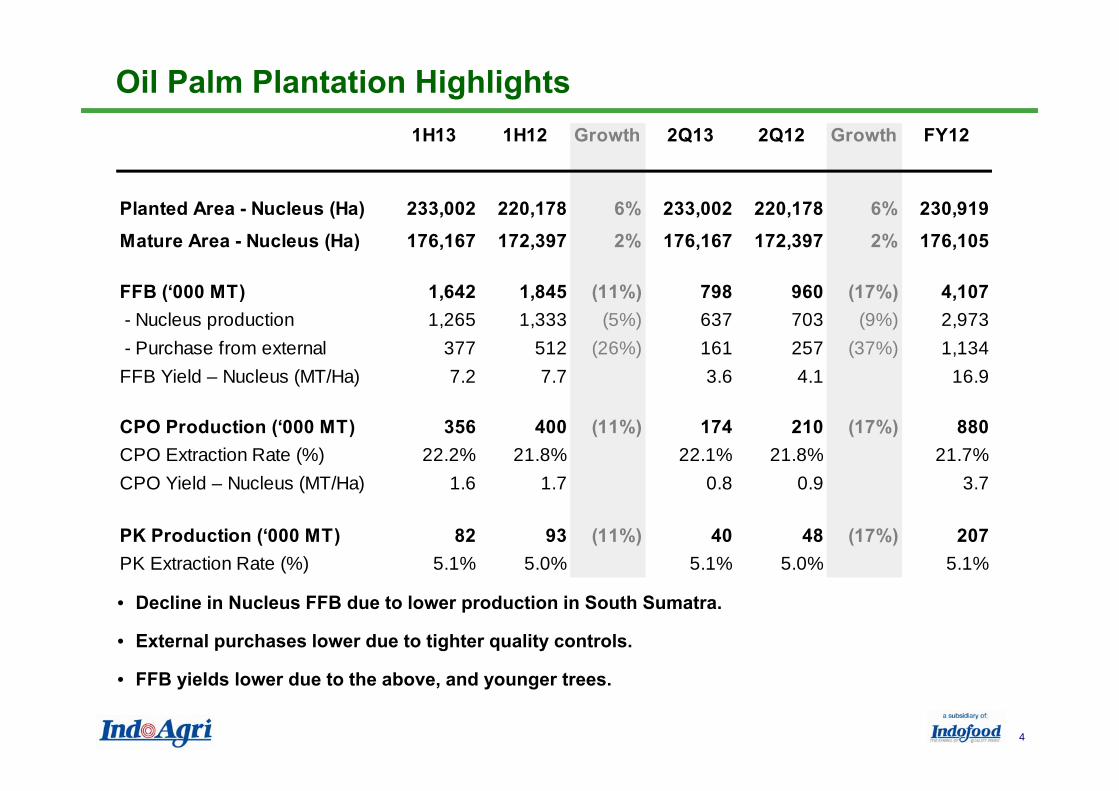

Oil Palm Plantation Highlights

• Decline in Nucleus FFB due to lower production in South Sumatra.

• External purchases lower due to tighter quality controls.

• FFB yields lower due to the above, and younger trees.

1H13 1H12 Growth 2Q13 2Q12 Growth FY12

Planted Area - Nucleus (Ha) 233,002 220,178 6% 233,002 220,178 6% 230,919Mature Area - Nucleus (Ha) 176,167 172,397 2% 176,167 172,397 2% 176,105

FFB (‘000 MT) 1,642 1,845 (11%) 798 960 (17%) 4,107 - Nucleus production 1,265 1,333 (5%) 637 703 (9%) 2,973 - Purchase from external 377 512 (26%) 161 257 (37%) 1,134FFB Yield – Nucleus (MT/Ha) 7.2 7.7 3.6 4.1 16.9

CPO Production (‘000 MT) 356 400 (11%) 174 210 (17%) 880CPO Extraction Rate (%) 22.2% 21.8% 22.1% 21.8% 21.7%CPO Yield – Nucleus (MT/Ha) 1.6 1.7 0.8 0.9 3.7

PK Production (‘000 MT) 82 93 (11%) 40 48 (17%) 207PK Extraction Rate (%) 5.1% 5.0% 5.1% 5.0% 5.1%

Integrated Agribusiness with Leading Brands

5

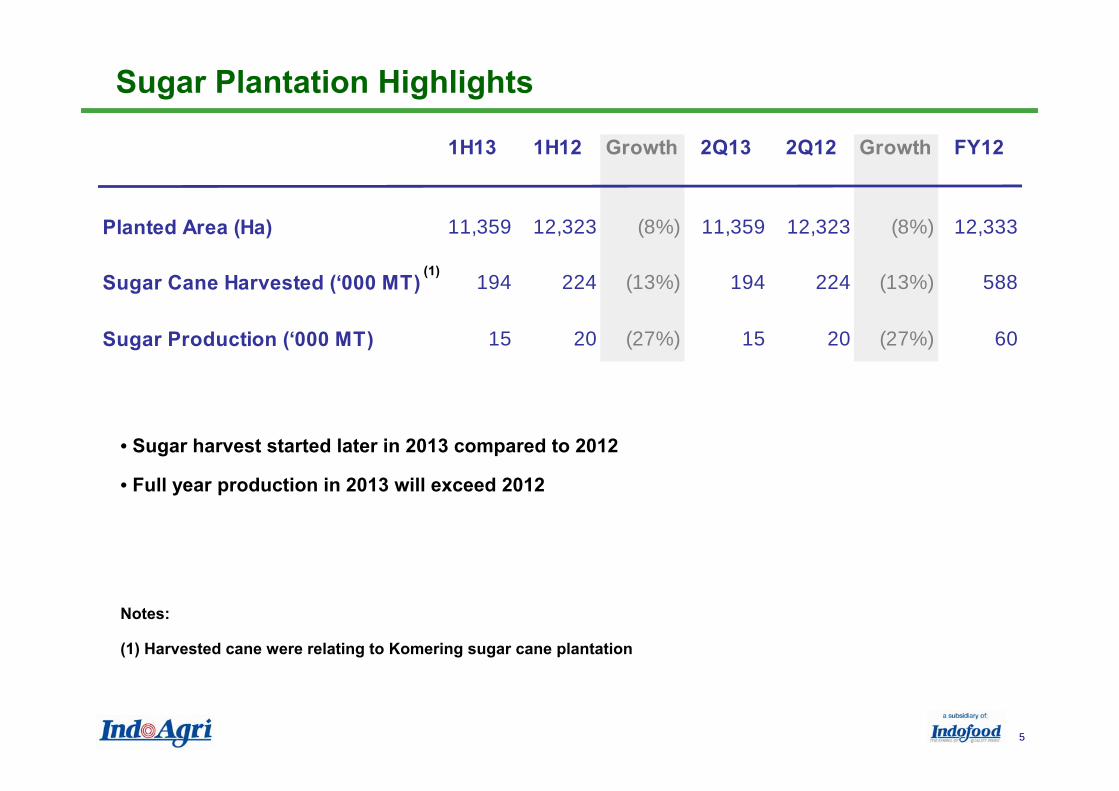

Sugar Plantation Highlights

Notes:

(1) Harvested cane were relating to Komering sugar cane plantation

• Sugar harvest started later in 2013 compared to 2012

• Full year production in 2013 will exceed 2012

1H13 1H12 Growth 2Q13 2Q12 Growth FY12

Planted Area (Ha) 11,359 12,323 (8%) 11,359 12,323 (8%) 12,333

Sugar Cane Harvested (‘000 MT) 194 224 (13%) 194 224 (13%) 588

Sugar Production (‘000 MT) 15 20 (27%) 15 20 (27%) 60

(1)

Integrated Agribusiness with Leading Brands

6

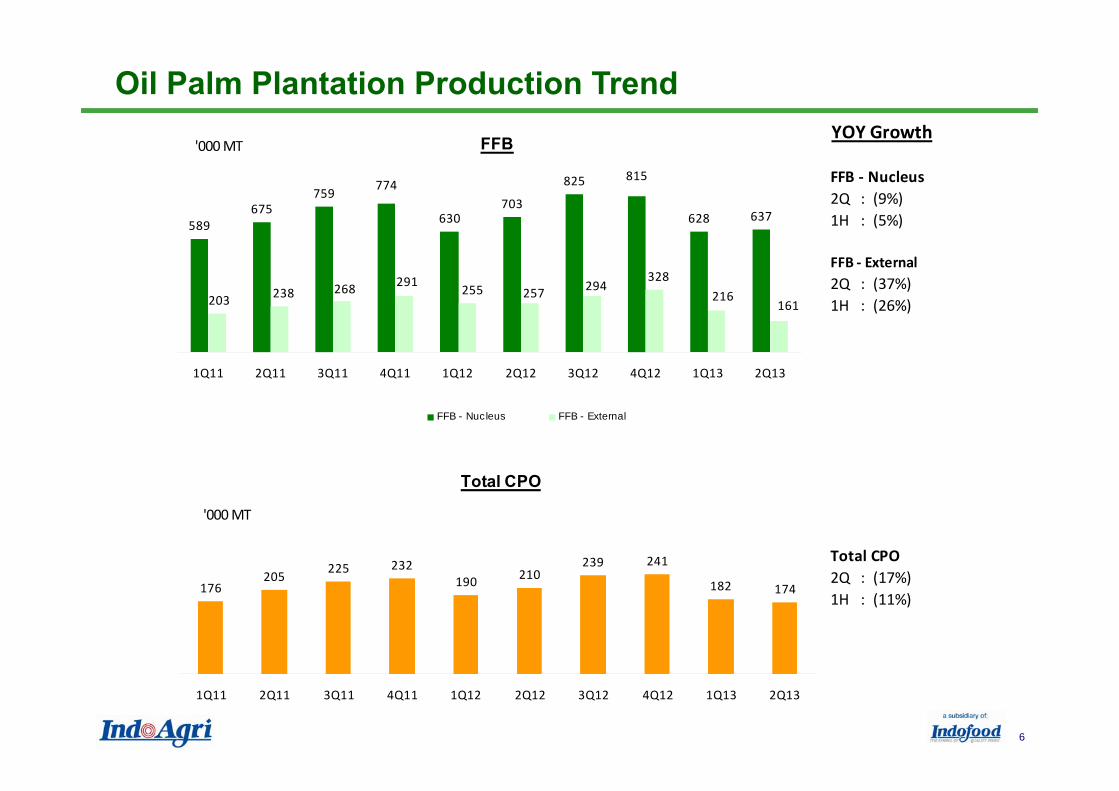

Oil Palm Plantation Production TrendYOY Growth

FFB ‐ Nucleus2Q : (9%)1H : (5%)

FFB ‐ External2Q : (37%)1H : (26%)

Total CPO2Q : (17%)1H : (11%)

Total CPO

176205 225 232

190 210239 241

182 174

1Q11 2Q11 3Q11 4Q11 1Q12 2Q12 3Q12 4Q12 1Q13 2Q13

'000 MT

FFB

589675

759

630703

825

628 637

774815

203 238 268 291 255 257 294328

216161

1Q11 2Q11 3Q11 4Q11 1Q12 2Q12 3Q12 4Q12 1Q13 2Q13

'000 MT

FFB - Nucleus FFB - External

7

Section 2Financial Highlights

Integrated Agribusiness with Leading Brands

8

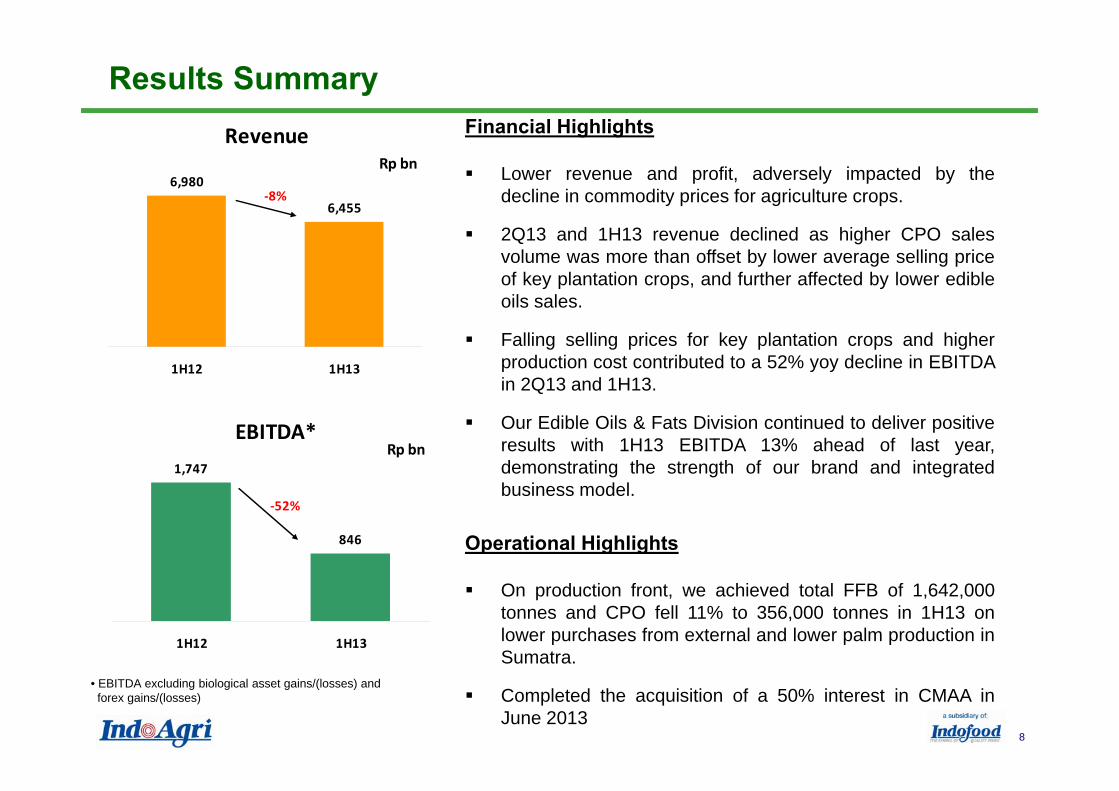

Results Summary

• EBITDA excluding biological asset gains/(losses) and forex gains/(losses)

Revenue

6,980

6,455

1H12 1H13

Rp bn

‐8%

EBITDA*1,747

846

1H12 1H13

Rp bn

‐52%

Financial Highlights

Lower revenue and profit, adversely impacted by thedecline in commodity prices for agriculture crops.

2Q13 and 1H13 revenue declined as higher CPO salesvolume was more than offset by lower average selling priceof key plantation crops, and further affected by lower edibleoils sales.

Falling selling prices for key plantation crops and higherproduction cost contributed to a 52% yoy decline in EBITDAin 2Q13 and 1H13.

Our Edible Oils & Fats Division continued to deliver positiveresults with 1H13 EBITDA 13% ahead of last year,demonstrating the strength of our brand and integratedbusiness model.

Operational Highlights

On production front, we achieved total FFB of 1,642,000tonnes and CPO fell 11% to 356,000 tonnes in 1H13 onlower purchases from external and lower palm production inSumatra.

Completed the acquisition of a 50% interest in CMAA inJune 2013

Integrated Agribusiness with Leading Brands

9

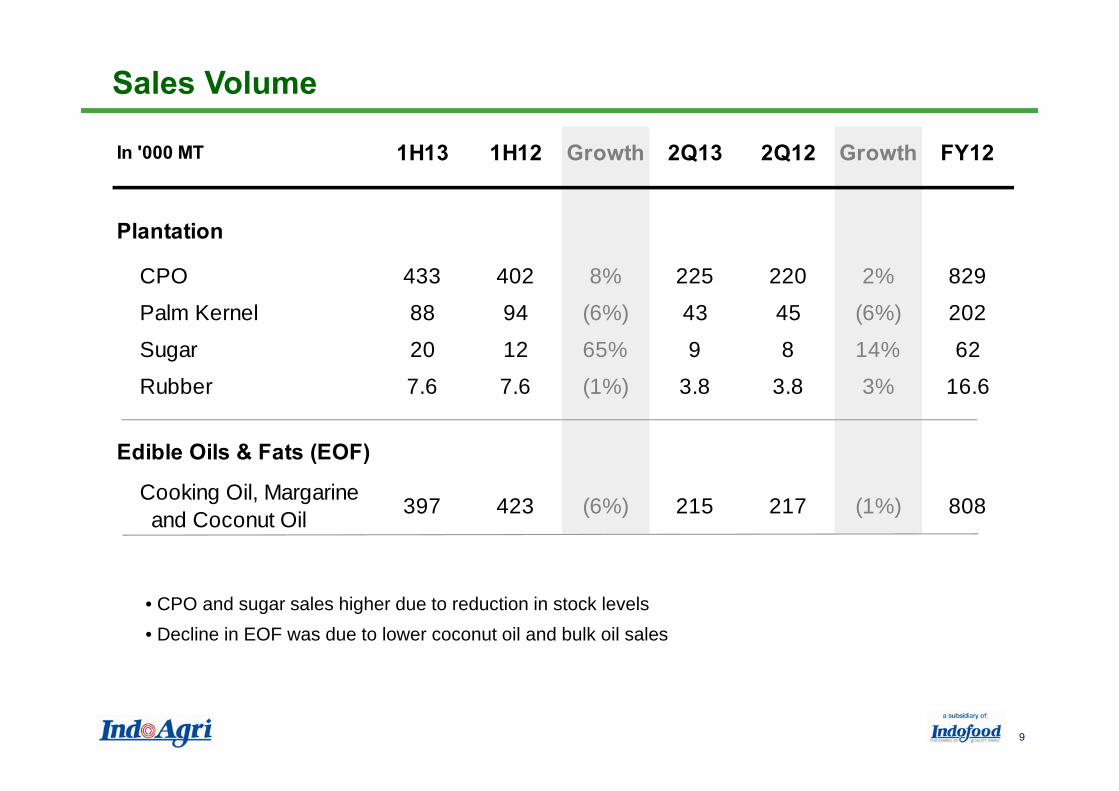

In '000 MT 1H13 1H12 Growth 2Q13 2Q12 Growth FY12

Plantation

CPO 433 402 8% 225 220 2% 829

Palm Kernel 88 94 (6%) 43 45 (6%) 202

Sugar 20 12 65% 9 8 14% 62

Rubber 7.6 7.6 (1%) 3.8 3.8 3% 16.6

Edible Oils & Fats (EOF)

Cooking Oil, Margarine and Coconut Oil 397 423 (6%) 215 217 (1%) 808

Sales Volume

• CPO and sugar sales higher due to reduction in stock levels• Decline in EOF was due to lower coconut oil and bulk oil sales

Integrated Agribusiness with Leading Brands

10

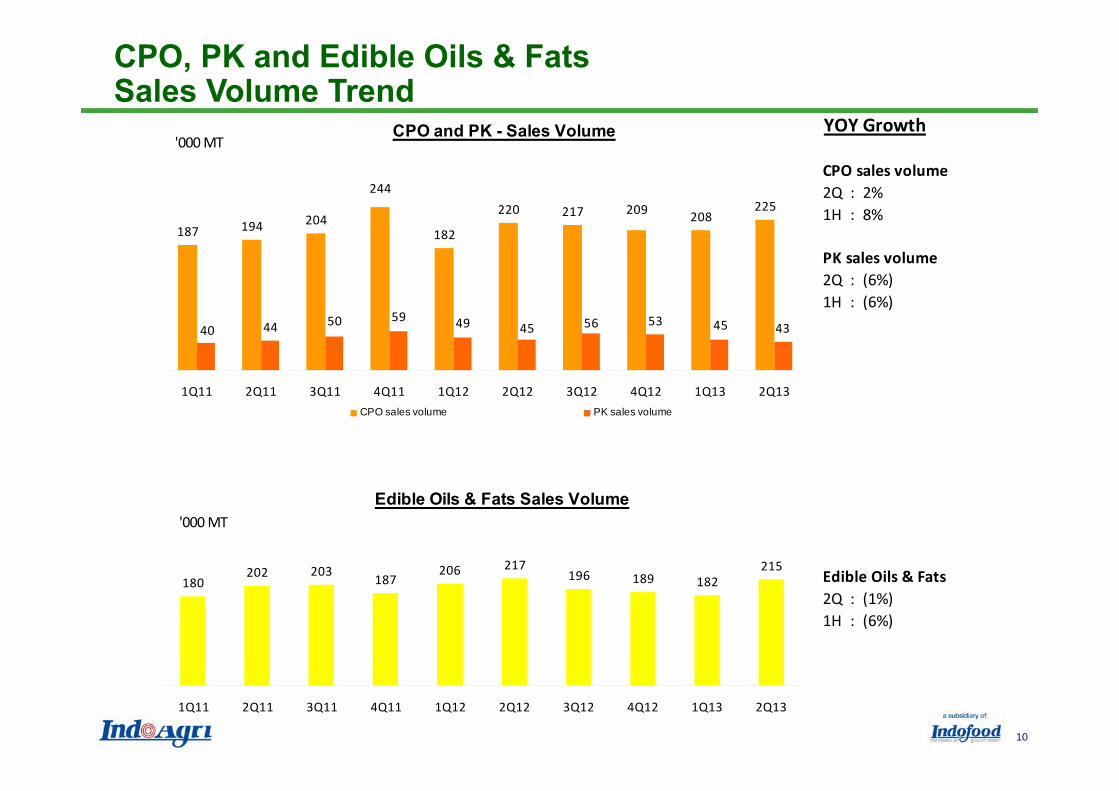

CPO, PK and Edible Oils & FatsSales Volume Trend

YOY Growth

CPO sales volume2Q : 2%1H : 8%

PK sales volume2Q : (6%)1H : (6%)

Edible Oils & Fats2Q : (1%)1H : (6%)

Edible Oils & Fats Sales Volume

180202 203 187

206 217196 189 182

215

1Q11 2Q11 3Q11 4Q11 1Q12 2Q12 3Q12 4Q12 1Q13 2Q13

'000 MT

CPO and PK - Sales Volume

187 194 204182

220 217 208225

43

244209

40 44 50 59 49 45 56 53 45

1Q11 2Q11 3Q11 4Q11 1Q12 2Q12 3Q12 4Q12 1Q13 2Q13

'000 MT

CPO sales volume PK sales volume

Integrated Agribusiness with Leading Brands

11

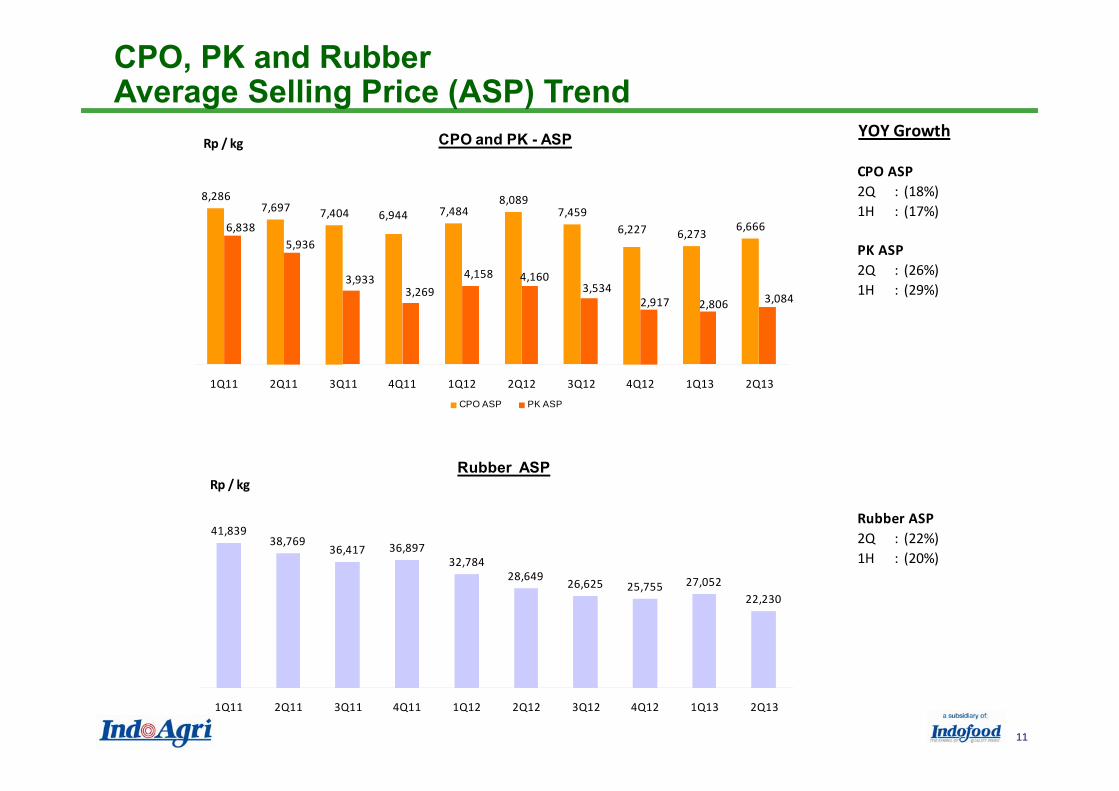

CPO, PK and RubberAverage Selling Price (ASP) Trend

YOY Growth

CPO ASP2Q : (18%)1H : (17%)

PK ASP2Q : (26%)1H : (29%)

Rubber ASP2Q : (22%)1H : (20%)

Rubber ASP

41,83938,769

36,417 36,89732,784

28,649 26,625 25,755 27,05222,230

1Q11 2Q11 3Q11 4Q11 1Q12 2Q12 3Q12 4Q12 1Q13 2Q13

Rp / kg

CPO and PK - ASP

8,2867,697 7,404 7,484

8,0897,459

6,273 6,6666,944

6,2276,8385,936

3,9333,269

4,158 4,1603,534

2,917 2,806 3,084

1Q11 2Q11 3Q11 4Q11 1Q12 2Q12 3Q12 4Q12 1Q13 2Q13

Rp / kg

CPO ASP PK ASP

Integrated Agribusiness with Leading Brands

12

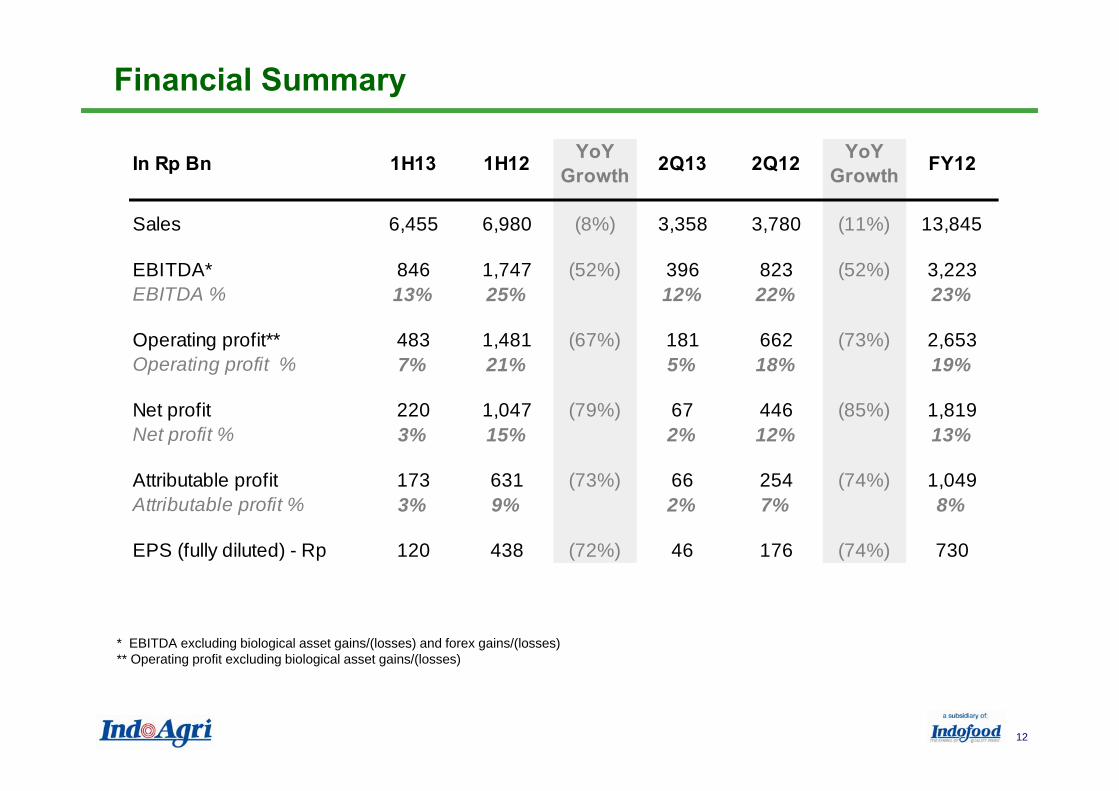

Financial Summary

* EBITDA excluding biological asset gains/(losses) and forex gains/(losses)** Operating profit excluding biological asset gains/(losses)

In Rp Bn 1H13 1H12 YoY Growth 2Q13 2Q12 YoY

Growth FY12

Sales 6,455 6,980 (8%) 3,358 3,780 (11%) 13,845

EBITDA* 846 1,747 (52%) 396 823 (52%) 3,223EBITDA % 13% 25% 12% 22% 23%

Operating profit** 483 1,481 (67%) 181 662 (73%) 2,653Operating profit % 7% 21% 5% 18% 19%

Net profit 220 1,047 (79%) 67 446 (85%) 1,819Net profit % 3% 15% 2% 12% 13%

Attributable profit 173 631 (73%) 66 254 (74%) 1,049Attributable profit % 3% 9% 2% 7% 8%

EPS (fully diluted) - Rp 120 438 (72%) 46 176 (74%) 730

Integrated Agribusiness with Leading Brands

13

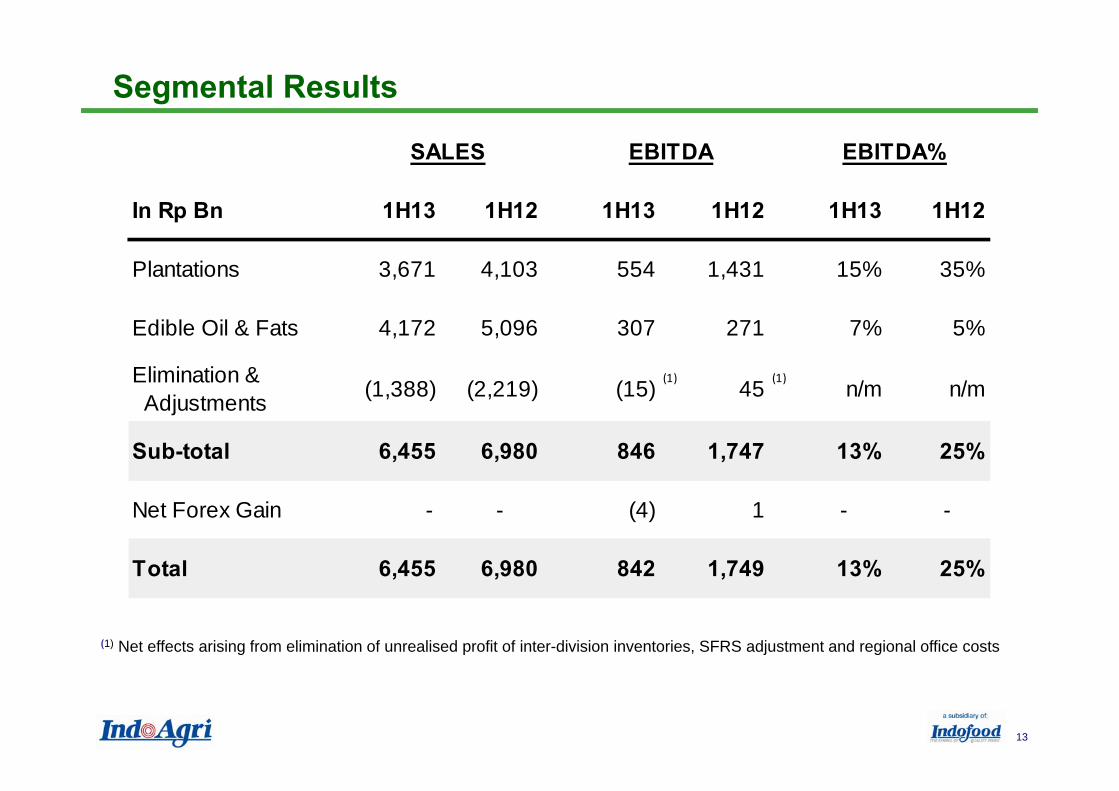

Segmental Results

(1) Net effects arising from elimination of unrealised profit of inter-division inventories, SFRS adjustment and regional office costs

SALES EBITDA EBITDA%

In Rp Bn 1H13 1H12 1H13 1H12 1H13 1H12

Plantations 3,671 4,103 554 1,431 15% 35%

Edible Oil & Fats 4,172 5,096 307 271 7% 5%

Elimination & Adjustments (1,388) (2,219) (15) 45 n/m n/m

Sub-total 6,455 6,980 846 1,747 13% 25%

Net Forex Gain - - (4) 1 - -

Total 6,455 6,980 842 1,749 13% 25%

(1) (1)

Integrated Agribusiness with Leading Brands

14

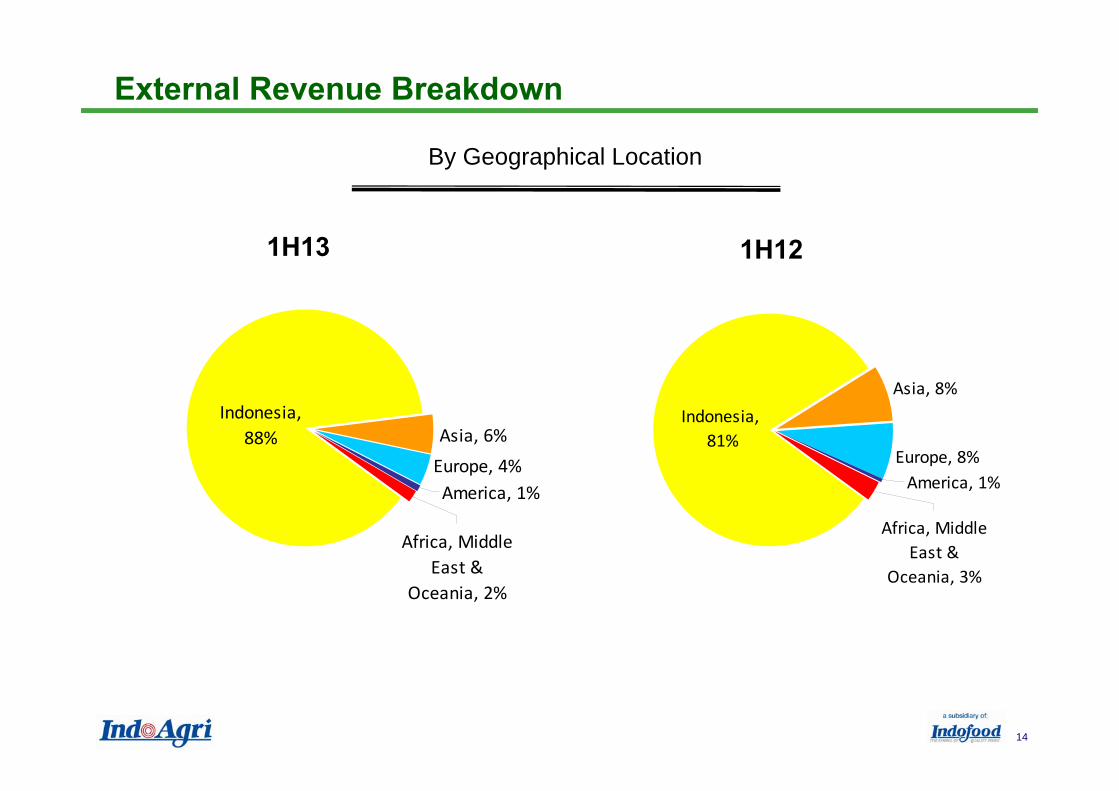

By Geographical Location

External Revenue Breakdown

1H13 1H12

Asia, 6%

America, 1%Europe, 4%

Africa, Middle East &

Oceania, 2%

Indonesia, 88%

Asia, 8%

Europe, 8%America, 1%

Africa, Middle East &

Oceania, 3%

Indonesia, 81%

Integrated Agribusiness with Leading Brands

15

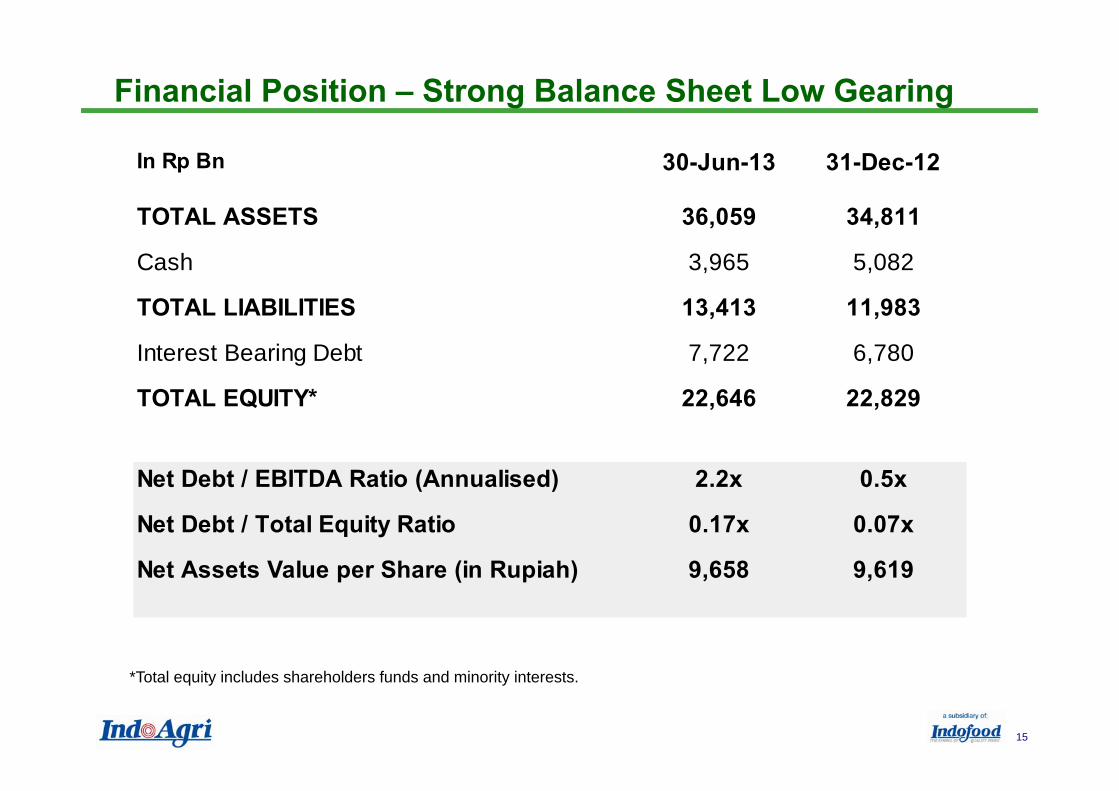

Financial Position – Strong Balance Sheet Low Gearing

*Total equity includes shareholders funds and minority interests.

In Rp Bn 30-Jun-13 31-Dec-12

TOTAL ASSETS 36,059 34,811

Cash 3,965 5,082

TOTAL LIABILITIES 13,413 11,983

Interest Bearing Debt 7,722 6,780

TOTAL EQUITY* 22,646 22,829

Net Debt / EBITDA Ratio (Annualised) 2.2x 0.5x

Net Debt / Total Equity Ratio 0.17x 0.07x

Net Assets Value per Share (in Rupiah) 9,658 9,619

16

Section 3Strategies and Expansion

Integrated Agribusiness with Leading Brands

17

2013 Strategies and Expansion – Indonesia

Focus organic expansion on new plantings of oil palm and sugar plantations

Expand CPO production capacity and enhance supply chain

• Constructing 4 oil palm mills due to higher FFB production in future from immature plantings:- 1 new mill in South Sumatra due for completion in Q4 2013- 1 new mill in Kalimantan due for completion in Q1 2014- Additionally expansion of 2 existing mills

• New bulking station in East Kalimantan with storage capacity of 5,000 tonnes, completion in2014

• Construction of 200MT/day PKO plant in Riau due for completion in 2013

Increase the utilization of internal tugboats and barges for CPO transportation to refineries

Intensifying the promotion of branded products to both modern trade and traditional market with new packaging and brand positioning

Completing roll-out of SAP ERP system in 2013 to the whole group

Integrated Agribusiness with Leading Brands

18

Expansion in Indonesia

On 8 March 2013, the Company’s subsidiaries, SIMP and Lonsum acquired an effective interest of 79.7% in PT Mentari Pertiwi Makmur (MPM) for Rp330 billion (around US$34 million)MPM in turn owns the SAL Group, which holds three industrial forest plantation concessions for a total area of 73,330 hectares in Berau and East Kutai, East KalimantanThis acquisition fits into the Group’s agriculture business model and enhances its diversification into other agriculture crops through intercropping.

Integrated Agribusiness with Leading Brands

19

Overseas Expansion

Rationale:• Expansion of geographical presence into the sugar, ethanol and co-generation industry in

Brazil• Superior technical know-how and best practices from Brazil that can be transferred back

to IndoAgri’s Indonesia sugar operations• Earnings accretive investment with a strong local partner in an expanding business

Key Highlights: • 1 sugar cane factory with a total cane crushing capacity of 3.0m MT p.a.; expanding to

3.8m MT p.a. by 2014/15; supplemented by ethanol and co-generation plants.• Has ~34,000 ha planted of sugar cane and targeted to have ~45,000 ha in the next 3

years, around 50% will be from 3rd parties• Low land competition, favourable logistics and infrastructure (near major roads, railways

and future ethanol pipeline)• Proximity to main consumer markets and suppliers• Expected to be earnings accretive in 2014/2015

CMAA acquisition completed on 25th June 2013

20

Section 4Appendix

Integrated Agribusiness with Leading Brands

21

DistributionSeed breeding

Advanced agriculture research centre

Advanced agriculture research centre

Nucleus planted oil palm of 233,002 ha*Diversified across palm oil, rubber, and sugar

Nucleus planted oil palm of 233,002 ha*Diversified across palm oil, rubber, and sugar

Leading cooking oil and margarine brands

Leading cooking oil and margarine brands

Diversified and Integrated Agribusiness Group with Leading Brands

Upstream Downstream

R&D Plantations Mills Edible oils and fats

Finished products

Capturing value across the entire supply chain

* As of 30 Jun 2013

Integrated Agribusiness with Leading Brands

22

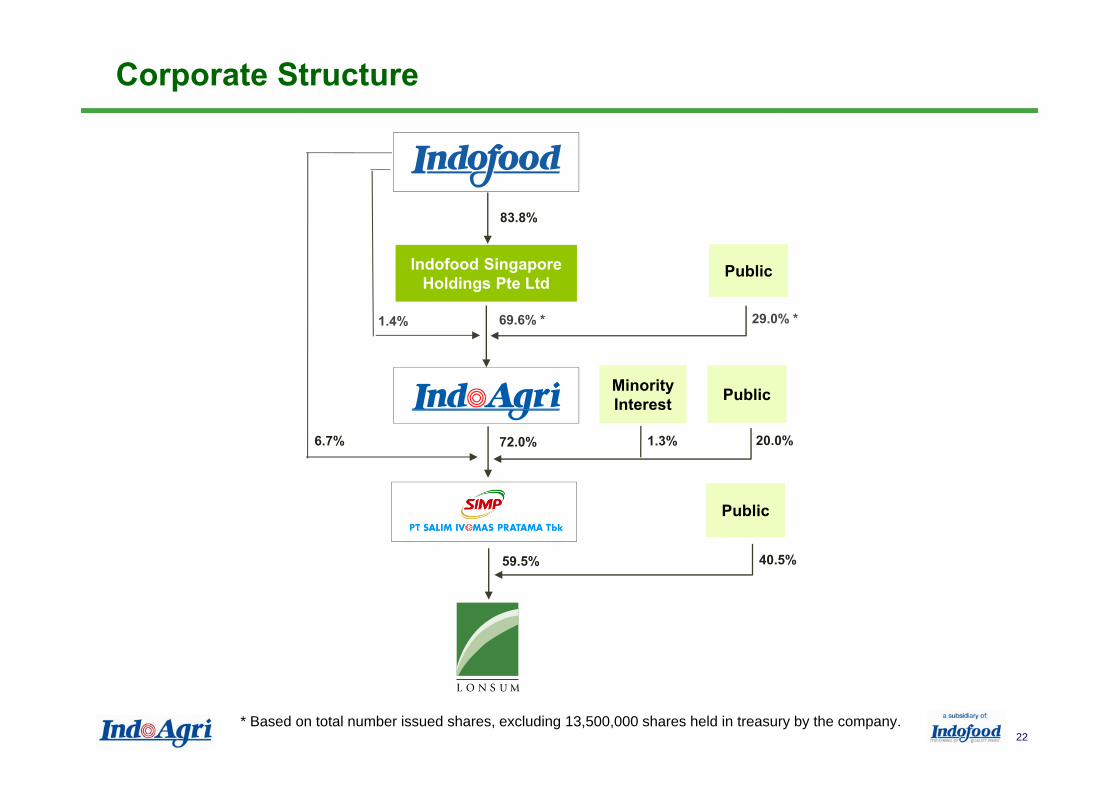

Corporate Structure

* Based on total number issued shares, excluding 13,500,000 shares held in treasury by the company.

83.8%

68.95%

72.00%

59.5%

6.7%

40.5%

Indofood Singapore Holdings Pte Ltd

Minority Interest

29.0% *

Public

1.3% 20.0%

69.6% *

72.0%

Public

Public

1.4%

Integrated Agribusiness with Leading Brands

23 23

Click to edit Master title styleTown/City

Oil Palm

Sugar Cane

Rubber

Sugar Mill

Copra Mill

Refinery

Tea

Cocoa

Supply Chain

North Sumatra

Riau

South Sumatra

Kalimantan

Strategically Located OperationsSpanning the Entire Supply Chain

Facilities Units Annual capacity (tonnes)

Palm oil mill 21 5,184,000 FFB

Crumb rubber facility 4 42,720 Dry rubber

Sheet rubber facility 3 11,100 Dry rubber

Facilities Units Annual capacity (tonnes)

Sugar mill & refinery 2 2,160,000 Sugar cane

Refinery 5 1,425,000 CPO

Integrated Agribusiness with Leading Brands

24

This presentation was prepared solely and exclusively for the parties presently being invited for the purpose ofdiscussion. Neither this presentation nor any of its content may be reproduced, disclosed or used without the priorwritten consent of Indofood Agri Resources Ltd.

This presentation may contain statements that convey future oriented expectations which represent the Company’spresent views on the probable future events and financial plans. Such views are presented on the basis of currentassumptions, are exposed to various risks, and are subject to considerable changes at any time. Presentedassumptions are presumed correct at the, and based on the data available on the, date at which this presentation isassembled. The Company warrants no assurance that such outlook will, in part or as a whole, eventually bematerialized. Actual results may diverge significantly from those projected.© Indofood Agri Resources Ltd. All rights reserved.

Indofood Agri Resources Ltd.8 Eu Tong Sen Street#16-96/97 The Central

Singapore 059818Tel: +65 6557 2389

Fax: +65 6557 2387

www.indofoodagri.com

Contact Us