CLO Separate Account Proposal

40

CLO Separate Account Proposal June 2, 2021 For the Employees' Retirement System of Rhode Island Use Only Joe Lynch Managing Director, Head of Global Non-Investment Grade Credit and Senior Portfolio Manager Bank Loans Pim van Schie Managing Director, Senior Portfolio Manager CLO Strategies Chris Crevier Managing Director, Client Advisor

Transcript of CLO Separate Account Proposal

CLO Separate Account ProposalJune 2, 2021

For the Employees' Retirement System of Rhode Island Use Only

Joe Lynch

Managing Director, Head of Global Non-Investment Grade Credit and Senior Portfolio Manager Bank Loans

Pim van Schie

Managing Director, Senior Portfolio Manager CLO Strategies

Chris Crevier

Managing Director, Client Advisor

2

Table of Contents

I. EXECUTIVE SUMMARY

II. NEUBERGER BERMAN CLO PLATFORM

III. CLO EQUITY PERFORMANCE SUMMARY

IV. CLO DEBT AND OPPORTUNISTIC INVESTMENTS AND PERFORMANCE SUMMARY

V. DISCLOSURES AND RISK CONSIDERATIONS

Executive Summary

4For the Employees' Retirement System of Rhode Island Use Only

Executive Summary: CLO Equity & Mezzanine Debt Separate Account Proposal

Neuberger Berman is pleased to present our proposal to the Employees’ Retirement System of Rhode Island

Programmatic purchases of NB CLO Equity alongside Neuberger Berman, targeting 60% account exposure

Initial deployment of capital into third-party CLO Mezzanine Debt; partially sold in stages to fund CLO Equity

Portion of capital can be deployed opportunistically in third-party CLO Equity and Debt

Cost-Effective: No account-level fees on NB CLO Equity exposure; discounted fees on CLO Mezzanine Debt

Income: Account seeks to generate an attractive yield upfront through the CLO Mezzanine Debt allocation

Vintage Diversification: Programmatic purchases of CLO Equity over several years

Customized: Separate Account is structured based upon ERSRI’s constraints and objectives

Partnership: Investing with a long-standing and experienced CLO platform with leading credit analysis resources

Experience: $16bn CLO platform with experience managing CLOs and CLO markets since 2004

Quality: Neuberger Berman CLO performance in 2020 was near the top of the market across several metrics;

invest in larger, more liquid loans and seek avoidance of default

Research-Driven: Our CLO business is an integral component of our $45+bn non-Investment Grade platform, which

is supported by one of the largest fundamental research teams in the industry

Proposal Highlights

Potential Benefits to ERSRI

Why Neuberger Berman?

Objective: Efficient partnership for investments in higher-quality CLO Equity and CLO Mezzanine Debt

Past performance is not indicative of future results. As with any investment, there is the possibility of profit as well as the risk of loss. Please see the Additional Disclosures at the end of this presentation.

Preliminary terms. Subject to change.

5For the Employees' Retirement System of Rhode Island Use Only

Neuberger Berman Investment Platform

We are a 100% independent, employee-owned firm investing $429bn for clients globally to achieve their unique objectives

1. As of March 31, 2021.

Global Investment Grade

Global Non-Investment Grade

Emerging Markets

Municipals

Multi-Sector

Currency

Global

U.S.

EAFE / Japan

Emerging Markets

- China

Thematic Strategies

MLPs

PUBLIC

MARKETS

PRIVATE

MARKETS

Global

U.S.

Emerging Markets

Custom Beta

F U N D A M E N T A L Q U A N T I T A T I V E

Private Debt

Credit Opportunities

Special Situations

Residential Loans

Specialty Finance

European Private Loans

F U N D A M E N T A L Q U A N T I T A T I V E

Commodities

Options

Global Macro

Risk Parity

Risk Premia

EQUITIES FIXED INCOME HEDGE FUNDS & LIQUID ALTERNATIVES

$123bn

$77bn

$184bn

$11bn

$23bn

$3bn

Insurance-Linked Strategies

Late Stage Pre-IPO

SPACs

GLOBAL ASSET CLASS SOLUTIONS

$333bn

$96bn

Global

U.S.

Long/Short – Almanac

Private Real Estate – Almanac

Real Estate Secondaries

REAL ESTATE

$2bn

$4bn

PRIVATE EQUITY PRIVATE CREDIT SPECIALTY ALTERNATIVES PRIVATE REAL ESTATE

GLOBAL RESEARCH CAPABILITIESESG INTEGRATION DATA SCIENCE

Hedge Funds

Liquid Alternatives

Primaries

Co-Investments

Secondaries

Specialty Strategies

Alternative Asset Manager Stakes – Dyal

6For the Employees' Retirement System of Rhode Island Use Only

A Distinct Approach to ESG Investing

Continuous innovation across four key pillars, focused on material investment results and delivering solutions

1. For illustrative and discussion purposes only. PRI grades are based on information reported directly by PRI signatories, of which investment managers totaled 1,924 for 2020, 1,119 for 2019, 1,120 for 2018 and 935 for 2017.

Please see Principles for Responsible Investment (PRI) Scores and end of this material for information regarding PRI scores shown. 2. Data reported as of year-end 2020. 3. Major defined as AUM $100B or greater. 4. ESG Aware

is defined as investment teams having access to ESG resources across the firm. As of December 31, 2020, across equities and fixed income. 5. Based on AUM as of December 31, 2020 including strategies in late or final stages of

approval by firm’s ESG committee.

Member of the PRI 2020

Leaders’ Group, awarded to

only 20 of 2,100+ PRI

investment manager signatories

A+ Integral to

Our Firm 150+

scores for ESG approach by UN-supported

Principles for Responsible Investment (PRI)1

Assets managed with consistent and

demonstrable ESG integration5~80% Assets that are ESG aware4100% Sustainable and

Impact Innovations

Range of ESG-integrated investment strategies across public and private markets, including custom solutions

Proprietary, Research-

Driven Approach>1,100 Proprietary NB ESG Quotient™ Credit Ratings2

>5,000 Proprietary NB ESG Quotient™ Equity Ratings2

Assess climate

risk for all public

equity and fixed

income holdings +

seek to mitigate

investment professionals with formal

ESG responsibility2

Active Engagement

Drives Value

Engagement meetings with

corporate management teams

across equities and credit23,666 First major asset management firm to disclose in advance

a number of key proxy votes3

Leverage data science

Investment-led integration

NB

7For the Employees' Retirement System of Rhode Island Use Only

Our Commitment to Equity, Inclusion & Diversity

We believe firms perform better when there is a true equitable and inclusive environment, which in turn drives diversity

EQUITY

To be “equitable” is to level

the playing field for all

INCLUSION

An environment where

everyone can flourish and be

their best selves

DIVERSITY

We look for a breadth of

diversity across many

characteristics

+

SENIOR LEADERSHIP + EMPLOYEE ENGAGEMENT

Operating Committee Diversity Council

How closely employee survey

scores of NB’s diverse population

compare to our highest scoring

population across (1) enablement,

training, mentoring, (2) fair

meritocracy and (3) culture

inclusion.

ACCOUNTABILITY THROUGH MEASUREMENT

Business-level dashboards as well as the custom NB EID Index

NB EQUITY, INCLUSION & DIVERSITY (NB EID) INDEX

overall score = 70%

NB EQUITY & INCLUSION INDEX

score = 90%

EMPLOYEE-INITIATED RESOURCE GROUPS (ERGs)

TO

P D

OW

NB

OT

TO

M-U

P

1

2

How closely NB reflects the

college educated population

across gender and ethnicity, by

corporate title.

NB DIVERSITY INDEX

score = 50%

Senior Equity, Inclusion & Diversity Leader

Dedicated Recruiting & Human Capital Support3

Board of Directors Engagement4

8For the Employees' Retirement System of Rhode Island Use Only

Global Non-Investment Grade Credit Team

Experienced team of over 50 investment professionals managing $45+ billion in non-investment grade assets

Employee data as of March 31, 2021. AUM data as of March 31, 2021. AUM represents assets under management of Neuberger Berman Investment Advisers LLC, Neuberger Berman Loan Advisers LLC, and Neuberger Berman

Loan Advisers II LLC. Includes Alternative capabilities and Non-Investment Grade Credit assets managed within sleeves of Multi-sector & Opportunistic mandates for both separate accounts and pooled funds. U.S. High Yield AUM

includes assets managed within Short Duration High Yield and Quality Bias High Yield. Years of experience are shown in parentheses for Portfolio Management, Research, Traders and Portfolio Analysts, Special Situations, and

Client Portfolio Specialists.

Joe Lynch

Global Head of Non-Investment Grade Credit

SENIOR

PORTFOLIO MANAGERS

9 Portfolio Managers

(24 years of exp. avg.)

RESEARCH

25 Analysts

(14 years of exp. avg.)

TRADERS & PORTFOLIO

ANALYSTS

6 Team Members

(16 years exp. avg.)

Investment Professionals

SPECIAL SITUATIONS

6 Team Members

(20 years exp. avg.)

CLIENT PORTFOLIO

SPECIALISTS

5 Team Members

(15 years exp. avg.)

Global Non-Investment Grade Strategies & AUM ($bn)

U.S. High Yield$19.3

Global High Yield$4.9

Neuberger Berrman CLOs

$13.8

Loan SMAs and Funds$4.5

Third-Party CLOs$2.2

9For the Employees' Retirement System of Rhode Island Use Only

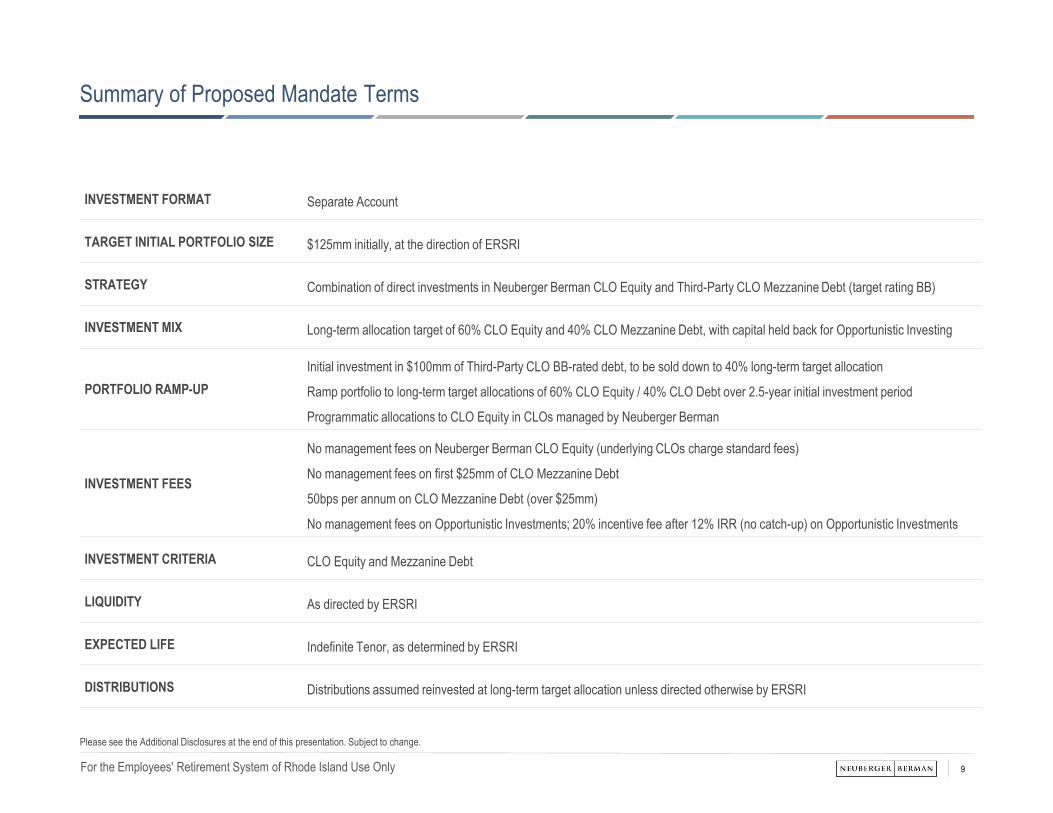

Summary of Proposed Mandate Terms

Please see the Additional Disclosures at the end of this presentation. Subject to change.

INVESTMENT FORMAT Separate Account

TARGET INITIAL PORTFOLIO SIZE $125mm initially, at the direction of ERSRI

STRATEGY Combination of direct investments in Neuberger Berman CLO Equity and Third-Party CLO Mezzanine Debt (target rating BB)

INVESTMENT MIX Long-term allocation target of 60% CLO Equity and 40% CLO Mezzanine Debt, with capital held back for Opportunistic Investing

PORTFOLIO RAMP-UP

Initial investment in $100mm of Third-Party CLO BB-rated debt, to be sold down to 40% long-term target allocation

Ramp portfolio to long-term target allocations of 60% CLO Equity / 40% CLO Debt over 2.5-year initial investment period

Programmatic allocations to CLO Equity in CLOs managed by Neuberger Berman

INVESTMENT FEES

No management fees on Neuberger Berman CLO Equity (underlying CLOs charge standard fees)

No management fees on first $25mm of CLO Mezzanine Debt

50bps per annum on CLO Mezzanine Debt (over $25mm)

No management fees on Opportunistic Investments; 20% incentive fee after 12% IRR (no catch-up) on Opportunistic Investments

INVESTMENT CRITERIA CLO Equity and Mezzanine Debt

LIQUIDITY As directed by ERSRI

EXPECTED LIFE Indefinite Tenor, as determined by ERSRI

DISTRIBUTIONS Distributions assumed reinvested at long-term target allocation unless directed otherwise by ERSRI

10For the Employees' Retirement System of Rhode Island Use Only

Allocation Deployment Model

Ramp portfolio to long-term target allocations of 60% NB CLO Equity / 40% CLO Debt over 2.5-year initial period

1 Source: Neuberger Berman. As of May 18, 2021.

Limitations of Illustrative Returns: Illustrative returns are based on statistical analysis of information including but not limited to information about default rates, recovery rates and re-investment spreads. The Illustrative returns

presented are the views of Neuberger Berman as to how they will manage the portfolio to seek to achieve the illustrative return as of the date hereof and are subject to change; they are not a suggestion, projection or guarantee that

the Illustrative returns will be realized or achieved or that an investment strategy will be successful. Investors should keep in mind that the securities markets are volatile and unpredictable. Actual results may be significantly different

than any Illustrative results and the team’s history of achieving returns has no impact on the likelihood of a team achieving Illustrative statistics in the future. There are no guarantees that the historical or Illustrative performance of an

investment, portfolio, or asset class will have a direct correlation with its future performance. Neuberger Berman does not make any representation as to the reasonableness of the assumptions or that all the assumptions used in

calculating the illustrative returns have been stated or fully considered. Additional information on these assumptions is available upon request. Changes in the assumptions may have a material impact on the illustrative returns

presented. Past performance is not indicative of future results. As with any investment, there is the possibility of profit as well as the risk of loss. Please see the Additional Disclosures at the end of this presentation, which

include important disclosures relating to these illustrative returns. Preliminary terms. Subject to change.

Model Highlights

2.5 yrs

Initial Modeled

Ramp-up Period

$125mm

Initial Target

Portfolio Size

60% / 40%

NB CLO Equity /

CLO Debt Allocation

13%

Illustrative Annual

Distribution at Target

Portfolio Mix

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

$0

$25

$50

$75

$100

$125

$150

$175

$200

Q3-2021 Q3-2022 Q3-2023 Q3-2024 Q3-2025 Q3-2026

Uncalled Opportunistic ($m) CLO Equity ($m)

CLO Mezzanine BB ($m) CLO Equity Pct. (RHS)

Target Allocation

Reached Q4-23

Neuberger Berman CLO Platform

12For the Employees' Retirement System of Rhode Island Use Only

Neuberger Berman CLO Platform Advantages

Long-standing CLO platform driven by fundamental credit philosophy has demonstrated focus on long-term returns

• Collateral Manager on 43 CLOs since 2004

• Current AUM of $13.8bn

• Focused on downside risk mitigation with

upside potential

• Over $1bn of CLO Equity Risk Retention

funds under management

CLO Collateral Manager

• Current AUM of $2.2bn

• Invests across the entire capital structure

• Focus on underlying portfolio quality with

bottom-up investment process

• Uses same credit research team and

investment philosophy

CLO Tranche Investing

Individual Loan Credit Analysis

Deal Structuring and Covenants

Knowledge of active CLO Investors

Market Technicals & Loan Supply/Demand

Relationships with CLO Arrangers

Manager and Platform Evaluation

Neuberger Berman’s CLO Team Brings Integrated CLO Equity and Debt Leadership

Long-Term Record

of Performance

Managing CLOs since 2004

across all credit cycles

One of the Largest

CLO Platforms

Success of the platform has

enabled growth; remains nimble

Higher-Quality Focus

in Leveraged Loans

Seek risk-adjusted returns

through downside protection

Leading Credit

Research Capabilities

25 credit analysts dedicated to

Non-Investment Grade credit

Employee data as of March 31, 2021. AUM data as of March 31, 2021.. This material is intended as a broad overview of the portfolio managers' style, philosophy and investment process and is subject to change without notice.

Portfolio managers' views may differ from those of other portfolio managers as well as the views of Neuberger Berman. Please see the Disclosures and Risk Considerations section of this presentation.

13For the Employees' Retirement System of Rhode Island Use Only

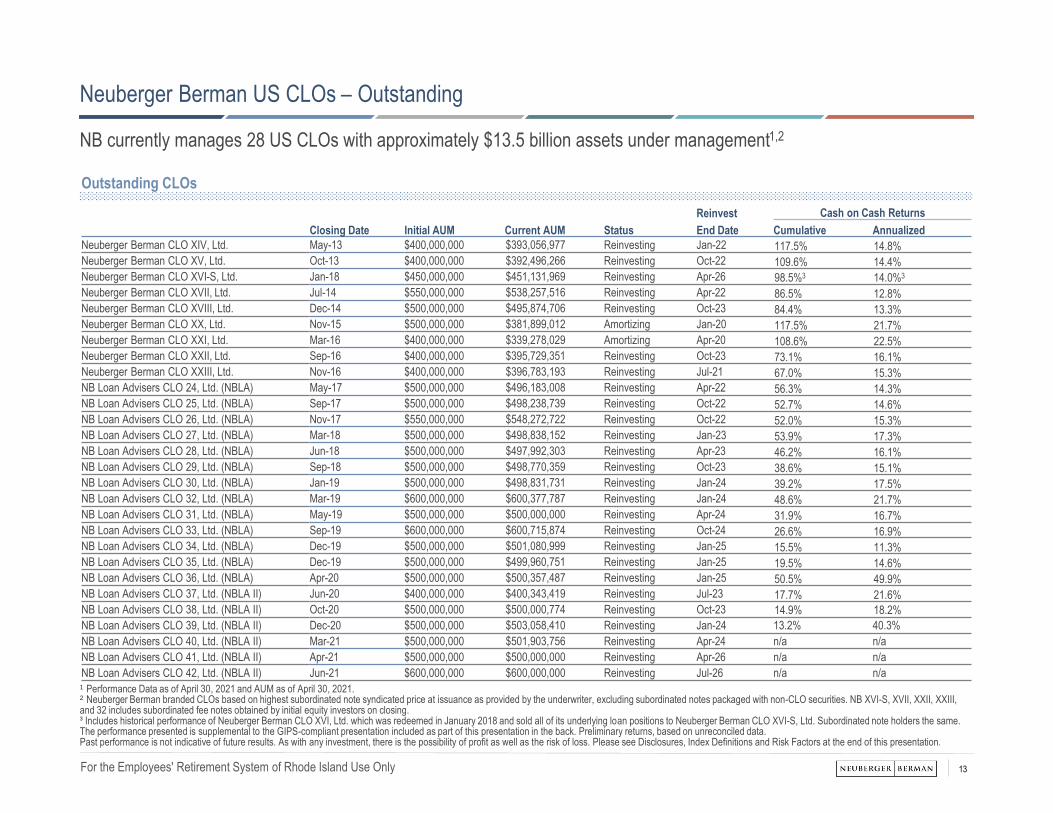

Neuberger Berman US CLOs – Outstanding

NB currently manages 28 US CLOs with approximately $13.5 billion assets under management1,2

¹ Performance Data as of April 30, 2021 and AUM as of April 30, 2021.² Neuberger Berman branded CLOs based on highest subordinated note syndicated price at issuance as provided by the underwriter, excluding subordinated notes packaged with non-CLO securities. NB XVI-S, XVII, XXII, XXIII, and 32 includes subordinated fee notes obtained by initial equity investors on closing.³ Includes historical performance of Neuberger Berman CLO XVI, Ltd. which was redeemed in January 2018 and sold all of its underlying loan positions to Neuberger Berman CLO XVI-S, Ltd. Subordinated note holders the same.The performance presented is supplemental to the GIPS-compliant presentation included as part of this presentation in the back. Preliminary returns, based on unreconciled data.Past performance is not indicative of future results. As with any investment, there is the possibility of profit as well as the risk of loss. Please see Disclosures, Index Definitions and Risk Factors at the end of this presentation.

Outstanding CLOs

Closing Date Initial AUM Current AUM Status

Reinvest Cash on Cash Returns

End Date Cumulative Annualized

Neuberger Berman CLO XIV, Ltd. May-13 $400,000,000 $393,056,977 Reinvesting Jan-22 117.5% 14.8%

Neuberger Berman CLO XV, Ltd. Oct-13 $400,000,000 $392,496,266 Reinvesting Oct-22 109.6% 14.4%

Neuberger Berman CLO XVI-S, Ltd. Jan-18 $450,000,000 $451,131,969 Reinvesting Apr-26 98.5%3 14.0%3

Neuberger Berman CLO XVII, Ltd. Jul-14 $550,000,000 $538,257,516 Reinvesting Apr-22 86.5% 12.8%

Neuberger Berman CLO XVIII, Ltd. Dec-14 $500,000,000 $495,874,706 Reinvesting Oct-23 84.4% 13.3%

Neuberger Berman CLO XX, Ltd. Nov-15 $500,000,000 $381,899,012 Amortizing Jan-20 117.5% 21.7%

Neuberger Berman CLO XXI, Ltd. Mar-16 $400,000,000 $339,278,029 Amortizing Apr-20 108.6% 22.5%

Neuberger Berman CLO XXII, Ltd. Sep-16 $400,000,000 $395,729,351 Reinvesting Oct-23 73.1% 16.1%

Neuberger Berman CLO XXIII, Ltd. Nov-16 $400,000,000 $396,783,193 Reinvesting Jul-21 67.0% 15.3%

NB Loan Advisers CLO 24, Ltd. (NBLA) May-17 $500,000,000 $496,183,008 Reinvesting Apr-22 56.3% 14.3%

NB Loan Advisers CLO 25, Ltd. (NBLA) Sep-17 $500,000,000 $498,238,739 Reinvesting Oct-22 52.7% 14.6%

NB Loan Advisers CLO 26, Ltd. (NBLA) Nov-17 $550,000,000 $548,272,722 Reinvesting Oct-22 52.0% 15.3%

NB Loan Advisers CLO 27, Ltd. (NBLA) Mar-18 $500,000,000 $498,838,152 Reinvesting Jan-23 53.9% 17.3%

NB Loan Advisers CLO 28, Ltd. (NBLA) Jun-18 $500,000,000 $497,992,303 Reinvesting Apr-23 46.2% 16.1%

NB Loan Advisers CLO 29, Ltd. (NBLA) Sep-18 $500,000,000 $498,770,359 Reinvesting Oct-23 38.6% 15.1%

NB Loan Advisers CLO 30, Ltd. (NBLA) Jan-19 $500,000,000 $498,831,731 Reinvesting Jan-24 39.2% 17.5%

NB Loan Advisers CLO 32, Ltd. (NBLA) Mar-19 $600,000,000 $600,377,787 Reinvesting Jan-24 48.6% 21.7%

NB Loan Advisers CLO 31, Ltd. (NBLA) May-19 $500,000,000 $500,000,000 Reinvesting Apr-24 31.9% 16.7%

NB Loan Advisers CLO 33, Ltd. (NBLA) Sep-19 $600,000,000 $600,715,874 Reinvesting Oct-24 26.6% 16.9%

NB Loan Advisers CLO 34, Ltd. (NBLA) Dec-19 $500,000,000 $501,080,999 Reinvesting Jan-25 15.5% 11.3%

NB Loan Advisers CLO 35, Ltd. (NBLA) Dec-19 $500,000,000 $499,960,751 Reinvesting Jan-25 19.5% 14.6%

NB Loan Advisers CLO 36, Ltd. (NBLA) Apr-20 $500,000,000 $500,357,487 Reinvesting Jan-25 50.5% 49.9%

NB Loan Advisers CLO 37, Ltd. (NBLA II) Jun-20 $400,000,000 $400,343,419 Reinvesting Jul-23 17.7% 21.6%

NB Loan Advisers CLO 38, Ltd. (NBLA II) Oct-20 $500,000,000 $500,000,774 Reinvesting Oct-23 14.9% 18.2%

NB Loan Advisers CLO 39, Ltd. (NBLA II) Dec-20 $500,000,000 $503,058,410 Reinvesting Jan-24 13.2% 40.3%

NB Loan Advisers CLO 40, Ltd. (NBLA II) Mar-21 $500,000,000 $501,903,756 Reinvesting Apr-24 n/a n/a

NB Loan Advisers CLO 41, Ltd. (NBLA II) Apr-21 $500,000,000 $500,000,000 Reinvesting Apr-26 n/a n/a

NB Loan Advisers CLO 42, Ltd. (NBLA II) Jun-21 $600,000,000 $600,000,000 Reinvesting Jul-26 n/a n/a

14For the Employees' Retirement System of Rhode Island Use Only

Neuberger Berman US CLOs – Redeemed

Investment philosophy of high quality portfolios and minimizing credit losses demonstrated through credit cycles1,2

¹ Performance Data and AUM as of April 15, 2021.².‘Lightpoint’ CLOs based on subordinated notes issuance price of par.³ LP III, LP IV, and LP VIII were non-traditional structures which resulted in cashflows to equity being more back-ended, known as Wachovia APEX and Lehman Par structures.The performance presented is supplemental to the GIPS-compliant presentation included as part of this presentation in the back. Preliminary returns, based on unreconciled data.Past performance is not indicative of future results. As with any investment, there is the possibility of profit as well as the risk of loss. Please see Disclosures, Index Definitions and Risk Factors at the end of this presentation.

Closing Date Initial AUM Redemption Date

Cumulative

Cash on

Cash Return

Annualized

Net Credit

Gains / -Losses IRR Notes

LightPoint CLO III, Ltd. July 2005 $447,500,000 Mar 2014 183% 0.12% 10.8%3 Non-Standard Structure3

LightPoint CLO IV, Ltd. April 2006 $350,000,000 Jan 2015 191% 0.11% 11.6%3 Non-Standard Structure3

LightPoint CLO V, Ltd. August 2006 $600,000,000 Nov 2015 216% -0.26% 19.6%

LightPoint CLO VII, Ltd. May 2007 $450,000,000 Feb 2017 225% -0.53% 20.2%

LightPoint CLO VIII, Ltd. August 2007 $485,400,000 Jul 2014 170% -0.11% 13.0%3 Non-Standard Structure3

Neuberger Berman CLO XII, Ltd. August 2012 $384,500,000 Jan 2017 154% -0.05% 14.9%

Neuberger Berman CLO XIII, Ltd. December 2012 $394,000,000 Jul 2017 131% -0.08% 11.4%

Neuberger Berman CLO XIX, Ltd. July 2015 $400,000,000 Mar 2021 166% Pending 17.1%

Redeemed CLOs

15For the Employees' Retirement System of Rhode Island Use Only

Neuberger Berman US CLO – Portfolio Characteristics

Source: Neuberger Berman, Intex as of March 30, 2021.

Peers is defined as CLOs issued in the same calendar quarter. 1Defined as loans which have their issuer, or affiliate thereof, not in the ICE BofA US High Yield Index or does not have a publicly listed entity.For illustrative purposes only. This material is intended as a broad overview of the portfolio managers’ style, philosophy and investment process and is subject to change without notice. Past performance is not indicative of future results. As with any investment, there is the possibility of profit as well as the risk of loss. Please see Disclosures, Index Definitions and Risk Factors at the end of this presentation.

Portfolio Liquidity Score vs Peers

Least

Liquid

Most

Liquid

Issuer Exposure with Less Than $500m of Debt vs Peers

2Q13 1Q14 4Q14 4Q15 3Q16 2Q17 4Q18 2Q18 1Q19 2Q19 4Q19 2Q20 4Q20

NB14

NB15

NB16

NB17

NB18

NB19

NB20

NB21

NB22

NB23

NB24

NB25

NB26

NB27

NB28

NB29

NB30

NB32

NB31

NB33

NB34

NB35

NB36

NB37

NB38

NB39

Distinguished by high-liquidity, larger issuers and generally lower spread

Weighted Average Spread vs Peers

310bps

320bps

330bps

340bps

350bps

360bps

370bps

2Q13 1Q14 4Q14 4Q15 3Q16 2Q17 4Q18 2Q18 1Q19 2Q19 4Q19 2Q20 4Q20

NB14

NB15

NB16

NB17

NB18

NB19

NB20

NB21

NB22

NB23

NB24

NB25

NB26

NB27

NB28

NB29

NB30

NB32

NB31

NB33

NB34

NB35

NB36

NB37

NB38

NB39

Weighted Average Exposure to Loan-Only Capital Structures1

0%

3%

6%

9%

12%

15%

2Q13 1Q14 4Q14 4Q15 3Q16 2Q17 4Q18 2Q18 1Q19 2Q19 4Q19 2Q20 4Q20

NB14

NB15

NB16

NB17

NB18

NB19

NB20

NB21

NB22

NB23

NB24

NB25

NB26

NB27

NB28

NB29

NB30

NB32

NB31

NB33

NB34

NB35

NB36

NB37

NB38

NB39

median 75pct 25pct NB

40%

45%

50%

55%

60%

65%

2Q13 1Q14 4Q14 4Q15 3Q16 2Q17 4Q18 2Q18 1Q19 2Q19 4Q19 2Q20 4Q20

NB14

NB15

NB16

NB17

NB18

NB19

NB20

NB21

NB22

NB23

NB24

NB25

NB26

NB27

NB28

NB29

NB30

NB32

NB31

NB33

NB34

NB35

NB36

NB37

NB38

NB39

median 75pct 25pct NB

16For the Employees' Retirement System of Rhode Island Use Only

Neuberger Berman US CLO – Equity Total Returns

Source: Neuberger Berman, Intex. CLO Equity Distributions as of September 30, 2020. CCC and Junor OC levels as of March 30, 2021.Peers is defined as CLOs issued in the same calendar quarter. NB XVI-S and NB XVII based on subordinated issuance price of 94, NB XIX based on subordinated notes issuance price of 90, and NB XXII and NB XXIII based on subordinated issuance price of 97.5. NB XVI-S, XVII, XXII, XXIII includes subordinated fee notes. All other CLOs based on subordinated notes issuance price of par.For illustrative purposes only. This material is intended as a broad overview of the portfolio managers’ style, philosophy and investment process and is subject to change without notice. Past performance is not indicative of future results. As with any investment, there is the possibility of profit as well as the risk of loss. Please see Disclosures, Index Definitions and Risk Factors at the end of this presentation.

Active CLO Cumulative Cash on Cash Dist. Plus Current NAV vs Peers

S&P CCC & Lower vs Peers

Stable distributions demonstrate preservation of capital and strong total returns with relatively low CCC holdings

Active CLO Cumulative Cash on Cash Dist. vs Peers

Junior Overcollateralization Level vs Peers

0%

20%

40%

60%

80%

100%

120%

140%

2Q13 1Q14 4Q14 4Q15 3Q16 2Q17 4Q18 2Q18 1Q19 2Q19 4Q19 2Q20

NB14

NB15

NB16

NB17

NB18

NB19

NB20

NB21

NB22

NB23

NB24

NB25

NB26

NB27

NB28

NB29

NB30

NB32

NB31

NB33

NB34

NB35

NB36

0%

20%

40%

60%

80%

100%

120%

2Q13 1Q14 4Q14 4Q15 3Q16 2Q17 4Q18 2Q18 1Q19 2Q19 4Q19 2Q20

NB14

NB15

NB16

NB17

NB18

NB19

NB20

NB21

NB22

NB23

NB24

NB25

NB26

NB27

NB28

NB29

NB30

NB32

NB31

NB33

NB34

NB35

NB36

0%

2%

4%

6%

8%

10%

12%

14%

2Q13 1Q14 4Q14 4Q15 3Q16 2Q17 4Q18 2Q18 1Q19 2Q19 4Q19 2Q20 4Q20

NB14

NB15

NB16

NB17

NB18

NB19

NB20

NB21

NB22

NB23

NB24

NB25

NB26

NB27

NB28

NB29

NB30

NB32

NB31

NB33

NB34

NB35

NB36

NB37

NB38

NB39

median 75pct 25pct NB

0%

1%

2%

3%

4%

5%

6%

2Q13 1Q14 4Q14 4Q15 3Q16 2Q17 4Q18 2Q18 1Q19 2Q19 4Q19 2Q20 4Q20

NB14

NB15

NB16

NB17

NB18

NB19

NB20

NB21

NB22

NB23

NB24

NB25

NB26

NB27

NB28

NB29

NB30

NB32

NB31

NB33

NB34

NB35

NB36

NB37

NB38

NB39

median 75pct 25pct NB

17For the Employees' Retirement System of Rhode Island Use Only

Neuberger Berman CLOs Exhibited Strong Market Value Performance in 2020

Multiple research desks have highlighted outperformance of Neuberger Berman CLOs through challenging markets

Source: Left side Nomura and right side BofA Securities. Data as of July 30, 2020 and October 5, 2020, respectively. Data from BofA Securities excludes CLOs that voluntarily diverted equity cashflows in 2020.

For illustrative purposes only. This material is intended as a broad overview of the portfolio managers’ style, philosophy and investment process and is subject to change without notice. Past performance is not indicative of future

results. As with any investment, there is the possibility of profit as well as the risk of loss. See Disclosures and Risk Considerations at the end of the presentation.

BofA SECURITIES – October 5, 2020NOMURA - July 30, 2020

18For the Employees' Retirement System of Rhode Island Use Only

CLO Portfolio Composite Performance

Downside risk mitigation with upside potential

Data as of December 31, 2020.1 Source: Neuberger Berman. Index performance is representative of the S&P/LSTA Leveraged Loan Index and composite performance is the Collateralized Loan Obligation Composite (gross of fees). Please see Disclosures,

Index Definitions and Risk Factors at the end of this presentation, which are required as part of this presentation. The performance presented is supplemental to the GIPS-compliant presentation included as part of this presentation

in the back. Preliminary returns, based on unreconciled data.

Past performance is not necessarily indicative of future results. As with any investment, there is the possibility of profit as well as the risk of loss.

Return by Half-Year

4.0% 4.3%

1.9%

2.8%2.0%

-0.4%

3.4%

-2.3%

4.5%5.1%

1.5%2.2%

1.8%

-1.8%

6.0%

3.6%

-3.8%

7.7%

4.5% 4.9%

2.3%

2.9%2.6%

-1.0%

2.8%

-3.4%

4.5%

5.4%

1.9% 2.2% 2.2%

-1.7%

5.7%

2.7%

-4.6%

8.1%

-6%

-4%

-2%

0%

2%

4%

6%

8%

10%

2012 1H 2012 2H 2013 1H 2013 2H 2014 1H 2014 2H 2015 1H 2015 2H 2016 1H 2016 2H 2017 1H 2017 2H 2018 1H 2018 2H 2019 1H 2019 2H 2020 1H 2020 2H

NB Composite Index

Performance vs. Index1

19For the Employees' Retirement System of Rhode Island Use Only

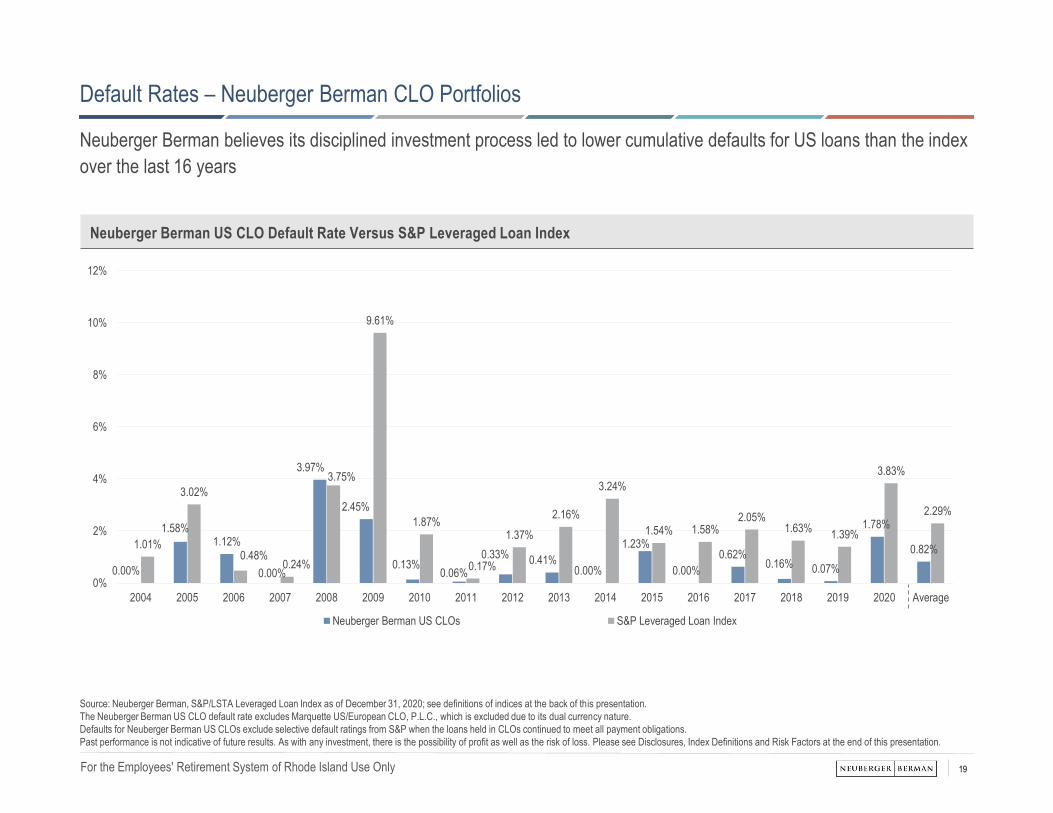

Default Rates – Neuberger Berman CLO Portfolios

Neuberger Berman believes its disciplined investment process led to lower cumulative defaults for US loans than the index

over the last 16 years

Source: Neuberger Berman, S&P/LSTA Leveraged Loan Index as of December 31, 2020; see definitions of indices at the back of this presentation.

The Neuberger Berman US CLO default rate excludes Marquette US/European CLO, P.L.C., which is excluded due to its dual currency nature.

Defaults for Neuberger Berman US CLOs exclude selective default ratings from S&P when the loans held in CLOs continued to meet all payment obligations.

Past performance is not indicative of future results. As with any investment, there is the possibility of profit as well as the risk of loss. Please see Disclosures, Index Definitions and Risk Factors at the end of this presentation.

0.00%

1.58%1.12%

0.00%

3.97%

2.45%

0.13%0.06%

0.33%0.41%

0.00%

1.23%

0.00%

0.62%0.16% 0.07%

1.78%

0.82%1.01%

3.02%

0.48%0.24%

3.75%

9.61%

1.87%

0.17%

1.37%

2.16%

3.24%

1.54% 1.58%2.05%

1.63%1.39%

3.83%

2.29%

0%

2%

4%

6%

8%

10%

12%

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 Average

Neuberger Berman US CLOs S&P Leveraged Loan Index

Neuberger Berman US CLO Default Rate Versus S&P Leveraged Loan Index

CLO Equity Performance Summary

21For the Employees' Retirement System of Rhode Island Use Only

0.50

0.60

0.70

0.80

0.90

1.00

1.10

1.20

1.30

1.40

1.50

Mar

-17

Sep

-17

Mar

-18

Sep

-18

Mar

-19

Sep

-19

Mar

-20

Sep

-20

Mar

-21

DPI

RVPI

Total Net Drawdowns,

88%

Sidecar/Reduced,

10%

Remaining Commitments,

2%

CLO Equity, 88%

Warehouse, 9%

Vertical Retention,

4%

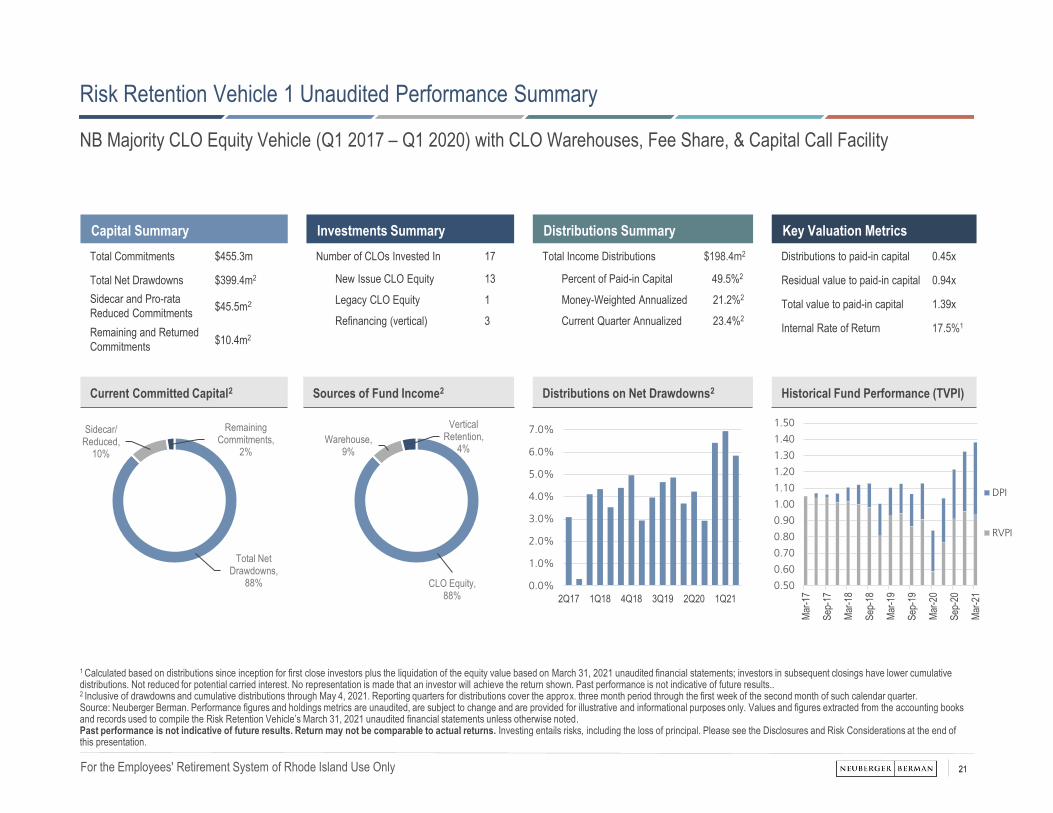

Risk Retention Vehicle 1 Unaudited Performance Summary

1 Calculated based on distributions since inception for first close investors plus the liquidation of the equity value based on March 31, 2021 unaudited financial statements; investors in subsequent closings have lower cumulative distributions. Not reduced for potential carried interest. No representation is made that an investor will achieve the return shown. Past performance is not indicative of future results..2 Inclusive of drawdowns and cumulative distributions through May 4, 2021. Reporting quarters for distributions cover the approx. three month period through the first week of the second month of such calendar quarter.Source: Neuberger Berman. Performance figures and holdings metrics are unaudited, are subject to change and are provided for illustrative and informational purposes only. Values and figures extracted from the accounting books and records used to compile the Risk Retention Vehicle’s March 31, 2021 unaudited financial statements unless otherwise noted.Past performance is not indicative of future results. Return may not be comparable to actual returns. Investing entails risks, including the loss of principal. Please see the Disclosures and Risk Considerations at the end of this presentation.

Current Committed Capital2 Sources of Fund Income2 Distributions on Net Drawdowns2 Historical Fund Performance (TVPI)

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

2Q17 1Q18 4Q18 3Q19 2Q20 1Q21

Capital Summary

Total Commitments $455.3m

Total Net Drawdowns $399.4m2

Sidecar and Pro-rata

Reduced Commitments$45.5m2

Remaining and Returned

Commitments$10.4m2

Investments Summary

Number of CLOs Invested In 17

New Issue CLO Equity 13

Legacy CLO Equity 1

Refinancing (vertical) 3

Key Valuation Metrics

Distributions to paid-in capital 0.45x

Residual value to paid-in capital 0.94x

Total value to paid-in capital 1.39x

Internal Rate of Return 17.5%1

Distributions Summary

Total Income Distributions $198.4m2

Percent of Paid-in Capital 49.5%2

Money-Weighted Annualized 21.2%2

Current Quarter Annualized 23.4%2

NB Majority CLO Equity Vehicle (Q1 2017 – Q1 2020) with CLO Warehouses, Fee Share, & Capital Call Facility

22For the Employees' Retirement System of Rhode Island Use Only

CLO Equity, 65%

Warehouse, 23%

Opportunistic, 13%

Risk Retention Vehicle 2 Unaudited Performance Summary

Current Committed Capital2 Sources of Fund Income2 Distributions on Net Drawdowns2 Historical Fund Performance (TVPI)

Total Net Drawdowns,

27%

Remaining Commitments,

73%

Capital Summary

Total Commitments $455.7m

Total Net Drawdowns $123.1m2

Remaining Commitments $322.7m2

Current Opportunistic $0.0m2

Investments Summary

Number of CLOs Invested In 6

New Issue CLO Equity 5

Legacy CLO Equity 0

Warehouse-stage CLOs 1

Key Valuation Metrics

Distributions to paid-in capital 0.17x

Residual value to paid-in capital 1.08x

Total value to paid-in capital 1.25x

Internal Rate of Return 151.0%1

Distributions Summary

Total Distributions $19.3m2

Percent of Paid-in Capital 15.7%2

Money-Weighted Annualized N/A

Current Quarter Annualized 27.4%2

0.50

0.60

0.70

0.80

0.90

1.00

1.10

1.20

1.30

DPI

RVPI

0.0%

3.0%

6.0%

9.0%

12.0%

15.0%

1Q20 2Q20* 3Q20* 4Q20 1Q20 2Q20

*Drawdown based on subsequent first call amount

NB Majority CLO Equity Vehicle (March 2020 – present) with CLO Warehouses, Fee Share, & Capital Call Facility

1 Calculated based on distributions since inception for first close investors plus the liquidation of the equity value based on March 31, 2021 unaudited financial statements; investors in subsequent closings have lower cumulative distributions. Not reduced for potential carried interest. No representation is made that an investor will achieve the return shown. Past performance is not indicative of future results..2 Inclusive of drawdowns and cumulative distributions through May 4, 2021. Reporting quarters for distributions cover the approx. three month period through the first week of the second month of such calendar quarter.Source: Neuberger Berman. Performance figures and holdings metrics are unaudited, are subject to change and are provided for illustrative and informational purposes only. Values and figures extracted from the accounting books and records used to compile the Risk Retention Vehicle’s March 31, 2021 unaudited financial statements unless otherwise noted.Past performance is not indicative of future results. Return may not be comparable to actual returns. Investing entails risks, including the loss of principal. Please see the Disclosures and Risk Considerations at the end of this presentation.

CLO Debt and Opportunistic Investments and Performance Summary

24For the Employees' Retirement System of Rhode Island Use Only

CLO Debt Investment Process Framework

Differentiated with advanced and rigorous portfolio management process

This material is intended as a broad overview of the portfolio managers' style, philosophy and investment process and is subject to change without notice. Portfolio managers' views may differ from those of other portfolio managers

as well as the views of Neuberger Berman. Please see the Disclosures and Risk Considerations section of this presentation.

Proprietary Analytics and Platform Individual CLO Deep-Dive

• Advanced integrated tools that aggregate underlying credit information

(internal ranking, analyst notes, etc), security level data (price, spread,

liquidity), and manager trading activity (style drift, performance)

• Designed to allow team to efficiently evaluate large volumes of potential

investments for selective deeper analysis

• Seek to quickly/easily exploit opportunities to take advantage of market

dislocations caused by CLO market inefficiencies

• Monitor and track investments and watchlists for trading opportunities

• Loan-level detail mapped to fundamental outlook on credits

• Fundamental assessment of collateral quality, manager style, trading

activity, and potential losses

• Credit selectivity with focus on long-term capital preservation

• Detailed evaluation of deal structure, covenants, and triggers to seek to

uncover value

• Portfolio Management team approves investments with culture of shared

risk and ownership

25For the Employees' Retirement System of Rhode Island Use Only

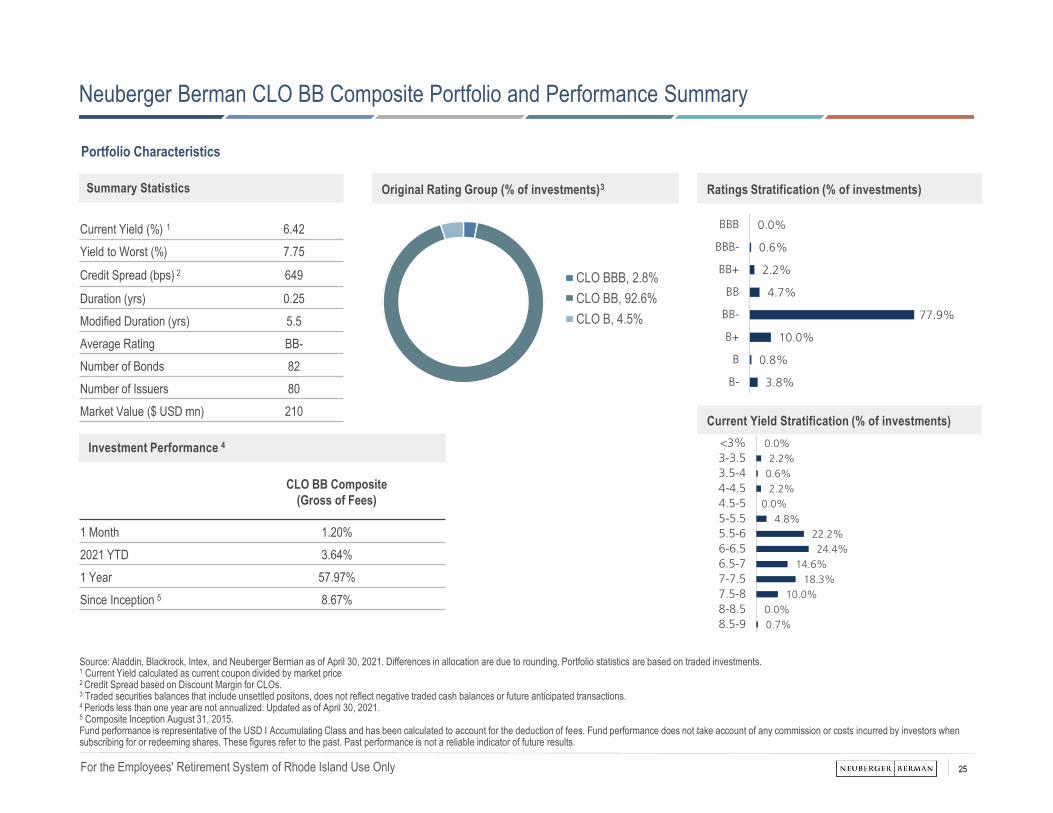

Source: Aladdin, Blackrock, Intex, and Neuberger Berman as of April 30, 2021. Differences in allocation are due to rounding. Portfolio statistics are based on traded investments.1 Current Yield calculated as current coupon divided by market price2 Credit Spread based on Discount Margin for CLOs.3 Traded securities balances that include unsettled positons, does not reflect negative traded cash balances or future anticipated transactions.4 Periods less than one year are not annualized. Updated as of April 30, 2021.5 Composite Inception August 31, 2015.Fund performance is representative of the USD I Accumulating Class and has been calculated to account for the deduction of fees. Fund performance does not take account of any commission or costs incurred by investors when subscribing for or redeeming shares. These figures refer to the past. Past performance is not a reliable indicator of future results.

Neuberger Berman CLO BB Composite Portfolio and Performance Summary

Portfolio Characteristics

CLO BBB, 2.8%

CLO BB, 92.6%

CLO B, 4.5%

Original Rating Group (% of investments)3 Ratings Stratification (% of investments)

Current Yield Stratification (% of investments)

0.0%

0.6%

2.2%

4.7%

77.9%

10.0%

0.8%

3.8%

BBB

BBB-

BB+

BB

BB-

B+

B

B-

0.0%

2.2%

0.6%

2.2%

0.0%

4.8%

22.2%

24.4%

14.6%

18.3%

10.0%

0.0%

0.7%

<3%

3-3.5

3.5-4

4-4.5

4.5-5

5-5.5

5.5-6

6-6.5

6.5-7

7-7.5

7.5-8

8-8.5

8.5-9

Investment Performance 4

CLO BB Composite

(Gross of Fees)

1 Month 1.20%

2021 YTD 3.64%

1 Year 57.97%

Since Inception 5 8.67%

Summary Statistics

Current Yield (%) 1 6.42

Yield to Worst (%) 7.75

Credit Spread (bps) 2 649

Duration (yrs) 0.25

Modified Duration (yrs) 5.5

Average Rating BB-

Number of Bonds 82

Number of Issuers 80

Market Value ($ USD mn) 210

26For the Employees' Retirement System of Rhode Island Use Only

Neuberger Berman CLO Mezzanine Debt Composite Performance Summary

Source: Neuberger Berman, JP Morgan Securities as of March 31, 2021. Please see attached additional GIPS notes and disclosures, which are required as part of this presentation. This information is supplemental to the attached GIPS notes and disclosure.The index is the JPM Collateralized Loan Obligation Index (the “Index”), which is divided into sub-indexes based on rating classes and time period of origination, or vintage (which can be measured as pre- or post-crisis or based on the year of origination). The Benchmark is the Post-Crisis BB Index. The Benchmark (Vintage Adjusted) and Benchmark (Vintage and Rating Adjusted) are custom indexes calculated by Neuberger Berman by measuring the vintages and ratings of the positions in the Composite on a monthly basis, and aggregating the performance of the corresponding sub-indexes of the Index for such month. The Benchmark (Vintage Adjusted) and Benchmark (Vintage and Rating Adjusted) are recalculated each month to generate that month’s performance. The manager believes that the Benchmark (Vintage Adjusted) and Benchmark (Vintage and Rating Adjusted) better reflect the universe in which the Composite is invested because (i) the Benchmark includes vintages and ratings not included in the Composite, and (ii) the Composite includes ratings not included in the Benchmark. The use of a custom benchmark can have many inherent limitations. For example, it does not represent the performance of any single index or sub-index. Other vintages and/or ratings may have different results, including losses. Each custom benchmark was created with the benefit of hindsight after the performance of the Composite is known, which could cause the custom benchmark to have a bias that favors the Composite performance. In addition, the monthly rebalancing of these benchmarks may make it difficult or impossible to evaluate the performance of the Composite and/or a benchmark over time. Neuberger Berman does not make any representation as to the reasonableness of the assumptions or that all the assumptions used in calculating the benchmarks have been stated or fully considered. Changes in the assumptions may have a material impact on the returns presented.This presentation is made available for illustrative purposes only. Past performance is not indicative of future results. As with any investment, there is the possibility of profit as well as the risk of loss. Please see the Disclosures and Risk Considerations section of this presentation, which are an important part of this presentation.

Outperforming custom vintage-weighted benchmark with lower downside volatility in 2016 and 2020 credit selloffs

Strategy Cumulative Total Return (base=100, gross of fees) Half-Year Returns (gross of fees)

70

80

90

100

110

120

130

140

150

160

170Benchmark (Vintage Adjusted)

Benchmark (Vintage and Rating Adjusted)

Composite

-10%

-5%

0%

5%

10%

15%

20%

25%Benchmark (Vintage Adjusted)

Benchmark (Vintage and Rating Adjusted)

Composite

Annualized

Total Return

8.07%8.29%

8.57%

27For the Employees' Retirement System of Rhode Island Use Only

Neuberger Berman CLO Opportunistic Account Summary

Dedicated Opportunistic CLO Account deployed capital in April and May 2020 at fundamentally cheap levels, harvested in

June and July as prices reached non-distressed levels

Called and Returned Capital, $40.1

Uncalled Commitments To

Date, $40.0

Capital Allocation

Committed Capital $80.1m

Called/Returned Capital $40.1m

Since Inception Invested

Capital

$34.2m

Performance Metrics (gross returns)1

0.00x Residual Value to Paid-In (RVPI)

1.26x Distribution to Paid-In (DPI)

1.26x Total Value to Paid-In (TVPI)

234% Internal Rate of Return (IRR)

Selected Portfolio Metrics

Key Dates

Investment Period Start March 24, 2020

Investment Period End March 24, 2022

1. Inclusive of cumulative distributions through July 23, 2020. .IRR is calculated based on distributions since inception for first close investors plus the NAV of current investments based on March 31, 2020 unaudited financial statements; investors in subsequent closings have lower cumulative distributions. Not reduced for potential carried interest. Source: Neuberger Berman. Performance figures and holdings metrics are unaudited, are subject to change and are provided for illustrative and informational purposes only. Values and figures extracted from the accounting books and records used to compile the CLO Opportunistic Account’s March 31, 2021 unaudited financial statements unless otherwise noted. Past performance is not indicative of future results. Return may not be comparable to actual returns. Investing entails risks, including the loss of principal. Please see the Disclosures and Risk Considerations at the end of this presentation.

Cumulative Number of

Investments 17

New Investments in 2Q 15

Investments Harvested in

2Q10

Investments Harvested

after 2Q7

Investments other than

CLO Mezzanine Debt0%

Average Purchase Price of

Investments68.60

Average Sale Price of

Investments1

89.33

Average DM at Cost 1,284

Yield to Maturity at Cost 13.50%

Yield to Maturity at Sale1 8.66%

Disclosures And Risk Considerations

29For the Employees' Retirement System of Rhode Island Use Only

Collateralized Loan Obligation Composite (Inception 7/1/2004)

Investment Performance Results – As of December 31, 2020

Past performance is no guarantee of future results.

Please see attached important disclosures which contain complete performance information and definitions.

Composite Benchmark Composite 3 Year Standard Deviation

Total Return

(%, Gross

of Fees)

Total Return

(%, Net

of Fees)

S&P/LS & TALL

Index (%)

No. of

Accounts

Market Value

($, m)

Total Firm

Assets

($, bn)

% of Firm

Assets

Internal

Dispersion

Composite

(%)

S&P/LS & TALL

Index

(%)

2020 3.60 3.04 3.12 24 11,295.2 -- -- 0.20 8.94 8.67

2019 9.73 9.13 8.64 19 9,032.1 355.8 2.54 0.11 3.12 2.77

2018 -0.05 -0.60 0.44 16 7,538.0 304.1 2.48 0.65 3.10 2.86

2017 3.70 3.14 4.12 13 6,011.7 295.2 2.04 0.20 2.81 2.69

2016 9.81 9.20 10.16 12 5,211.9 255.2 2.04 0.46 2.89 2.89

2015 1.05 0.49 -0.69 9 3,851.6 240.4 1.60 0.33 1.92 2.11

2014 1.54 0.98 1.60 7 3,033.1 250.0 1.21 -- 1.92 2.10

2013 4.77 4.19 5.29 ≤ 5 1,599.3 241.7 0.66 -- 3.52 3.77

2012 8.47 7.88 9.66 ≤ 5 1,377.8 205.0 0.67 -- 4.08 4.42

2011 2.02 1.56 1.52 7 2,362.2 193.1 1.22 0.31 8.11 8.43

30For the Employees' Retirement System of Rhode Island Use Only

CLO BB (Inception 9/1/2015)

Investment Performance Results – As of March 31, 2021

Past performance is no guarantee of future results.

Please see attached important disclosures which contain complete performance information and definitions.

Composite Benchmark Composite 3 Year Standard Deviation

Total Return

(%, Gross

of Fees)

Total Return

(%, Net

of Fees)

JPM

Collateralized

Loan Obligation

Index BB

("CLOIE") (%)

No. of

Accounts

Market Value

($, m)

Total Firm

Assets

($, bn)

% of Firm

Assets

Internal

Dispersion

Composite

(%)

JPM Collateralized

Loan Obligation

Index BB

("CLOIE")

(%)

YTD Mar-

20212.41 2.25 2.98 ≤ 5 294.9 -- -- -- 25.58 25.35

2020 8.98 8.28 8.05 ≤ 5 247.9 405.4 0.06 -- 25.58 25.32

2019 14.79 14.05 10.86 ≤ 5 258.1 355.8 0.07 -- 7.08 5.60

2018 -3.08 -3.70 0.37 6 251.4 304.1 0.08 -- 11.11 12.45

2017 14.29 13.55 17.52 ≤ 5 54.3 295.2 0.02 -- -- --

2016 18.96 18.19 21.86 ≤ 5 35.4 255.2 0.01 -- -- --

4 Months

2015-6.25 -6.45 -9.85 ≤ 5 62.7 240.4 0.03 -- -- --

31For the Employees' Retirement System of Rhode Island Use Only

Collateralized Loan Obligation Composite

Investment Performance Disclosure Statement

Compliance Statement

• Neuberger Berman Group LLC ("NB", "Neuberger Berman" or the "Firm") claims compliance with the Global Investment Performance Standards (GIPS®) and has prepared and presented this report in compliance with theGIPS® standards. Neuberger Berman has been independently verified for the period January 1, 2011 to December 31, 2019. A firm that claims compliance with the GIPS standards must establish policies and procedure forcomplying with all the applicable requirements of the GIPS standards. Verification provides assurance on whether the firm's policies and procedures related to composite and pooled fund maintenance, as well as the calculation,presentation, and distribution of performance, have been designed in compliance with the GIPS standards and have been implemented on a firm-wide basis. Verification does not ensure the accuracy of any specific compositepresentation. The verification reports are available upon request.

• The GIPS® firm definition was redefined effective January 1, 2011. For prior periods there were two separate firms for GIPS® firm definition purposes and such firms were independently verified for the periods January 1, 1997to December 31, 2010 and January 1, 1996 to December 31, 2010, respectively.

Definition of the Firm

• The firm is currently defined for GIPS® purposes as Neuberger Berman Group LLC, ("NB", "Neuberger Berman" or the "Firm"), and includes the following subsidiaries and affiliates: Neuberger Berman Investment Advisers LLC,Neuberger Berman Europe Ltd., Neuberger Berman Asia Ltd., Neuberger Berman East Asia Ltd., Neuberger Berman Singapore Pte. Ltd., Neuberger Berman Taiwan Ltd, Neuberger Berman Australia Pty. Ltd., NeubergerBerman Trust Company N.A., Neuberger Berman Trust Company of Delaware N.A., NB Alternatives Advisers LLC Neuberger Berman Breton Hill ULC, Neuberger Berman Loan Advisers LLC and Neuberger Berman LoanAdvisers II LLC.

Policies

• Policies for valuing portfolios, calculating performance, and preparing compliant presentations are available upon request.

Composite Description

• The Collateralized Loan Obligation Composite (the "Composite") includes the performance of all Collateralized Loan Obligation portfolios, with no minimum investment, managed on a fully discretionary basis by the Non Investment Grade Fixed Income team. A Collateralized Loan Obligation ("CLO") will be excluded from the strategy in any period in which such CLO is in its reinvestment period and its assets under management ("AUM") are at least 25% less than the AUM at its initial funding. The Composite creation date is September 2007, and performance inception date is July 2004. The returns presented are based on asset and cash activity within the CLOs and do not include leverage. A complete list of Neuberger Berman's composites is available upon request.

Primary Benchmark Description

• The benchmark is the Standard & Poor's / Loan Syndications & Trading Association Leveraged Loan Index (the "Index"). The Index measures the performance of the U.S. leveraged loan market based upon real-time market weightings, spreads and interest payments. Loan Syndications and Trading Association (LSTA)/Loan Pricing Corporation (LPC) mark-to-market pricing is used to price each loan in the index. The benchmark is calculated on a total return basis.

Reporting Currency

• Valuations are computed and performance is reported in U.S. Dollars. Performance includes reinvestment of dividends and other earnings.

Fees

• Composite Gross of Fee returns are the return on investments reduced by any trading expenses incurred during the period. Composite Net of Fee returns are the Gross of Fee returns reduced by investment advisory fees.

• Presented risk measures are calculated using gross-of-fee composite returns.

Fee Schedule

• The annual investment advisory fee, generally payable quarterly, is as follows: 0.55% on the first $50mn; 0.45% on the next $250mn; 0.35% thereafter.

Internal Dispersion

• Internal dispersion is calculated using the asset-weighted standard deviation of annual gross returns of those portfolios that were in the Composite for the entire year. Internal dispersion is not calculated if the Composite does not contain at least 6 portfolios for the entire year.

Annualized Standard Deviation

• The three-year annualized standard deviation measures the variability of the Composite and the benchmark returns over the preceding 36-month period. The standard deviation is not required for periods prior to 2011.

Availability and Trademark Disclosures

• The firm's list of composite descriptions, limited distribution pooled fund descriptions, and broad distribution pooled fund descriptions are available upon request.

• GIPS® is a registered trademark of CFA Institute. CFA Institute does not endorse or promote this organization, nor does it warrant the accuracy or quality of the content contained herein.

32For the Employees' Retirement System of Rhode Island Use Only

CLO BB Composite

Investment Performance Disclosure Statement

Compliance Statement

• Neuberger Berman Group LLC ("NB", "Neuberger Berman" or the "Firm") claims compliance with the Global Investment Performance Standards (GIPS®) and has prepared and presented this report in compliance with theGIPS® standards. Neuberger Berman has been independently verified for the period January 1, 2011 to December 31, 2019. A firm that claims compliance with the GIPS standards must establish policies and procedure forcomplying with all the applicable requirements of the GIPS standards. Verification provides assurance on whether the firm's policies and procedures related to composite and pooled fund maintenance, as well as the calculation,presentation, and distribution of performance, have been designed in compliance with the GIPS standards and have been implemented on a firm-wide basis. Verification does not ensure the accuracy of any specific compositepresentation. The verification reports are available upon request.

• The GIPS® firm definition was redefined effective January 1, 2011. For prior periods there were two separate firms for GIPS® firm definition purposes and such firms were independently verified for the periods January 1, 1997to December 31, 2010 and January 1, 1996 to December 31, 2010, respectively. The Firm definition was most recently changed in 2020 to include the addition of Neuberger Berman Loan Advisers LLC and Neuberger BermanLoan Advisers II LLC.

Definition of the Firm

• The firm is currently defined for GIPS® purposes as Neuberger Berman Group LLC, ("NB", "Neuberger Berman" or the "Firm"), and includes the following subsidiaries and affiliates: Neuberger Berman Investment Advisers LLC,Neuberger Berman Europe Ltd., Neuberger Berman Asia Ltd., Neuberger Berman East Asia Ltd., Neuberger Berman Singapore Pte. Ltd., Neuberger Berman Taiwan Ltd, Neuberger Berman Australia Pty. Ltd., NeubergerBerman Trust Company N.A., Neuberger Berman Trust Company of Delaware N.A., NB Alternatives Advisers LLC, Neuberger Berman Breton Hill ULC, Neuberger Berman Loan Advisers LLC and Neuberger Berman LoanAdvisers II LLC.

Policies

• Policies for valuing portfolios, calculating performance, and preparing compliant presentations are available upon request.

Composite Description

• The CLO BB Composite (the "Composite") includes the performance of all CLO BB portfolios managed on a fully discretionary basis by the Non Investment Grade Fixed Income team. The CLO BB strategy is designed for investors who seek to achieve total returns from a portfolio that invests in CLO BB rated debt but may opportunistically allocate to AAA, AA, A, and BBB ratings. The principal objectives are high current income, lower volatility and capital preservation achieved through the avoidance of credit deterioration in the underlying portfolios, manager selection, and focus on structural protections. The Composite creation date is June 2019 and performance inception date is September 2015. A complete list of Neuberger Berman's composites is available upon request.

Primary Benchmark Description

• The benchmark is the JPM Collateralized Loan Obligation Index BB ("CLOIE") (the "Index"). The Index is reflects the market for broadly-syndicated, arbitrage CLOs denominated in US dollars. CLOIE is divided by time period of origination (pre versus post crisis) and is broken out further into five original rating classes (AAA, AA, A, BBB, BB). The index is rebalanced monthly with daily reported index values.

Reporting Currency

• Valuations are computed and performance is reported in U.S. Dollars. Performance includes reinvestment of dividends and other earnings.

Fees

• Composite Gross of Fee returns are the return on investments reduced by any trading expenses incurred during the period. Composite Net of Fee returns are the Gross of Fee returns reduced by investment advisory fees.

• Presented risk measures are calculated using gross-of-fee composite returns.

Fee Schedule

• The annual investment advisory fee, generally payable quarterly, is as follows: 0.70% on the first $50mm; 0.65% on the next $250mm; 0.50% thereafter.

Internal Dispersion

• Internal dispersion is calculated using the asset-weighted standard deviation of annual gross returns of those portfolios that were in the Composite for the entire year. Internal dispersion is not calculated if the Composite does not contain at least 6 portfolios for the entire year.

Annualized Standard Deviation

• The three-year annualized standard deviation measures the variability of the Composite and the benchmark returns over the preceding 36-month period. The standard deviation is not required for periods prior to 2011.

Availability and Trademark Disclosures

• The firm's list of composite descriptions, limited distribution pooled fund descriptions, and broad distribution pooled fund descriptions are available upon request.

• GIPS® is a registered trademark of CFA Institute. CFA Institute does not endorse or promote this organization, nor does it warrant the accuracy or quality of the content contained herein.

33For the Employees' Retirement System of Rhode Island Use Only

Risk Considerations

Risks of Investing in CLOs

An investment in notes in a CLO involves risks. The following list of risk factors is a preliminary summary only and is qualified in its entirety by the more detailed description of the risk factors described in the final offering circular

relating to a particular CLO (“Offering Circular”).

The Issuer. The issuer of a CLO will generally be a newly formed entity. As a newly formed entity, the issuer will have no prior operating history. The issuer will have no significant assets other than the collateral (portfolio

investments and other assets of the issuer).

The Collateral. The collateral may primarily consist of non-investment grade senior secured loans, which have greater credit and liquidity risk than more highly-rated securities. The collateral may include debt obligations which may

be unsecured, or may have been issued in connection with highly leveraged transactions or may be subordinated to certain other obligations of the underlying obligors. The lower rating of these obligations reflects a greater

possibility that adverse changes in the financial condition of an obligor or in general economic conditions or both may impair the ability of such obligor to make payments of principal and interest.

Credit Ratings. Any credit ratings of certain of the notes, or the loans and other assets that may comprise the collateral, represent the rating agencies’ opinions regarding their credit quality and are not a guarantee of future credit

performance of such securities. Rating agencies attempt to evaluate the safety of principal and interest payments and do not evaluate the risks of fluctuations in market value. Therefore, the ratings assigned to securities by rating

agencies may not fully reflect the true risks of an investment. Also, the rating agencies may not make timely changes in credit ratings in response to subsequent events so that an issuer’s current financial condition may be better or

worse than a rating indicates. Ratings may be subject to revision or withdrawal by a rating agency at any time including to the extent the issuer doesn’t comply with its obligation under Rule 17g-5 of the Securities Exchange Act of

1934 as amended (the "Exchange Act"). Rating reductions or withdrawals may occur for any number of reasons and may affect numerous assets at a single time or within a short period of time, which in turn may have a material

adverse effect upon the notes.

Leveraged Capital Structure. A CLO will generally be substantially leveraged. Use of leverage is a speculative investment technique and involves certain risks to investors in the notes. The leverage provided to the issuer by the

issuance of the notes will result in interest expense and other costs incurred in connection with such borrowings that may not be covered by the net interest income, dividends or other proceeds of the collateral or any appreciation

thereof. The use of leverage generally magnifies the issuer’s opportunity for gain and risk of loss.

Payments in Respect of the Subordinated Notes. The issuer will generally pledge substantially all of its assets to secure the secured notes and certain other obligations pursuant to an indenture. The proceeds of such assets will

only be available to make payments in respect of the subordinated notes as and when such proceeds are released from the lien of such indenture in accordance with the priority of payments that will be set forth therein. There can

be no assurance that, after payment of principal and interest on the secured notes and other fees and expenses in accordance with such priority of payments, the issuer will have funds remaining to make distributions in respect of

the subordinated notes.

Volatility in Market. In recent years, securities issued in securitization transactions have experienced significant fluctuations in market value and accordingly high price volatility relative to historical experience. There is no

assurance that such volatility will not continue or (to the extent it has eased) return.

Regulatory Risk. Changes in the legislative and regulatory environment may affect the ability of issuers to make payments on the notes. In particular, the Dodd-Frank Wall Street Reform and Consumer Protection Act (the "Dodd-

Frank Act"), which was signed into law on July 21, 2010, includes provisions that are expected to have a broad impact on credit and other financial markets. Such changes, together with uncertainty about the nature and timing of

regulations that will be promulgated to implement such changes, may create uncertainty in the credit and other financial markets and create other unknown risks.

Default Rates on Collateral. While a number of articles and research reports have been written on historical default rates, there is no central source for relevant data or a standardized method for measuring default rates, and such

general corporate default studies cannot accurately reflect the performance of corporate debt obligations which satisfy the criteria described herein with respect to the collateral. Furthermore, the historical performance of corporate

debt markets is not necessarily indicative of its future performance. Should increases in default rates occur with respect to the type of collateral comprising the collateral for the transaction, the actual default rates of the collateral

may exceed any hypothetical default rates set forth herein.

34For the Employees' Retirement System of Rhode Island Use Only

Risk Considerations

Risks of Investing in CLOs – continued

General Market Risk with Respect to Collateral Performance. Negative economic trends nationally as well as in specific geographic areas of the United States continue to be indicators of potential loan defaults and

delinquencies. The levels of defaults and delinquencies have been increasing and/or volatile, and there is a material possibility that economic activity will continue to be volatile or to slow. Some obligors may have been significantly

and negatively impacted by such negative economic trends. A continuing decreased ability of obligors to obtain refinancing (particularly as high levels of required refinancings approach) may result in a further economic decline that

could delay an economic recovery and cause a further deterioration in loan performance generally. There is no way to determine whether such trends in the credit markets will improve or worsen in the future.

Illiquidity in the CLO, Leveraged Finance and Fixed Income Markets may Affect the Holders of Notes. A severe liquidity crisis in the global credit markets has resulted in substantial fluctuations in prices for leveraged loans

and high-yield debt securities and limited liquidity for such instruments. No assurance can be made that the conditions giving rise to such price fluctuations and limited liquidity will not continue or become more acute. During periods

of limited liquidity and higher price volatility, an issuer's ability to acquire or dispose of collateral at a price and time that the issuer deems advantageous may be severely impaired. Regardless of current or future market conditions,

certain items of collateral purchased by an issuer will have only a limited trading market (or none). Illiquid debt obligations may trade at a discount from comparable, more liquid investments.

No Information on the Obligors. Investors generally have limited rights to obtain from the collateral manager information regarding the obligors on the collateral. The collateral manager may from time to time receive material non-

public information or other notices with respect to assets comprising the collateral or the obligors thereon which they will not be required to disclose to investors. The collateral manager has no obligation to keep investors informed

as to matters arising in relation to any obligors on the collateral.

No Market for Notes. Transfer Restrictions. Generally no market will exist for CLO notes. If a secondary market does develop, there can be no assurance that it will provide holders of notes with liquidity on investment or that it will

continue for the life of notes. In addition, CLO notes not registered under the United States Securities Act of 1933, as amended, or under any United States state securities or “Blue Sky” laws or the securities laws of any other

jurisdiction, nor is the issuer registered under the United States Investment Company Act of 1940, as amended. The CLO notes are issued and sold in reliance upon exemptions from registration provided by such laws. As such,

CLO notes are subject to certain transfer restrictions. Consequently, an investor in CLO notes must be prepared to hold such notes for an indefinite period of time or until their stated maturity.

Final Maturity, Average Life and Prepayment Considerations. The average lives of notes are expected to be shorter than the number of years until the final stated maturity date, and their average lives may vary due to various

factors affecting the early retirement of the collateral, the timing and amount of sales of collateral and the ability of the collateral manager to invest in additional collateral. Retirement of the collateral prior to final maturity will depend,

among other things, on the financial condition of the obligors on the underlying collateral and the respective characteristics of such collateral, including the existence and frequency of exercise of any optional redemption, mandatory

redemption or sinking fund features, the prevailing level of interest rates, the redemption prices, the actual default rates and the actual amount collected on any defaulted collateral and the frequency of tender or exchange offers for

such collateral. In particular, loans are generally prepayable at par, and a high proportion of loans could be prepaid. The ability of the issuer to reinvest proceeds in securities with comparable interest rates that satisfy the

reinvestment criteria specified herein may affect the timing and amount of payments received by the holders of notes and the yield to maturity of notes.

Limited Recourse Obligations. CLO notes will be limited recourse obligations of the issuer and secured notes will be non-recourse obligations of the co-issuer. Distributions of interest on and principal of notes will be payable

solely from the collateral pledged to secure the secured notes. The issuer, as a special purpose entity, will have no significant assets other than the collateral. The issuer will not be obligated to make any payments on notes from a

source other than such pledged collateral. No person other than the co-issuers will be obligated to make payments on the notes. Consequently, holders of the notes must rely solely upon distributions on the collateral for the

payment of amounts payable in respect of the notes. If distributions on such collateral are insufficient to make payments on the notes, no other assets of the issuer or any other person or entity will be available for the payment of the

deficiency.

Subordination; Control by Controlling Class. Payments of principal of, or interest on and other distributions in respect of, CLO notes will be subject to the priority of payments set forth in an indenture. Pursuant to such indenture,

the senior most class of notes then outstanding in the capital structure (the “Controlling Class”) will be entitled to exercise certain rights which are superior and may be detrimental to the holders of any class of notes which is

subordinated to the Controlling Class.

35For the Employees' Retirement System of Rhode Island Use Only

Risk Considerations

Risks of Investing in CLOs – continued

Adverse Effect of Determination of U.S. Business. The United States federal income tax treatment of the issuer is not entirely free from doubt and if it were determined that the issuer was engaged in a United States trade or

business and had taxable income that is effectively connected with such United States trade or business, then the issuer would be subject under the United States Revenue Code of 1986 to the regular corporate income tax on such

effectively connected taxable income and possibly to 30% branch profits tax as well.

Other Tax Considerations. CLO issuers may be passive foreign investment companies ("PFIC"). A U.S. person holding subordinated notes will be treated as a shareholder rather than a noteholder of the PFIC and may be subject

to additional taxes unless it elects to treat the issuer as a qualified electing fund ("QEF") and to recognize currently its proportionate share of the issuer's income. Although a QEF election avoids the imposition of these additional

taxes, it can have its own adverse tax consequences. Prospective purchasers of the subordinated notes considering a QEF election should be aware that it is possible that a significant amount of the issuer's income, as determined

for U.S. federal income tax purposes, will not be distributed on a current basis to the holders of the subordinated notes. Consequently, U.S. Holders of subordinated notes making a QEF election may owe income tax on a significant

amount of such "phantom", or undistributed, income. The tax consequences of the ownership and disposition of subordinated notes can be quite complex and U.S. holders of subordinated notes should consult their own tax advisors

in this regard.

Projections. Cash-flow projections are based on assumptions that are unlikely to be consistent with, and may differ materially from, actual events. Actual events will vary from projections and the variations may be material. Some

important factors that could cause actual results to differ materially from projections include the actual composition of the portfolio, and defaults in respect of the portfolio, the timing of any defaults and recoveries, changes in interest

rates, loan prepayments, price of assets, spread on assets, liquidity of loans, the ability of the issuer to reinvest in new assets or remain fully invested, and any weakening of the specific investments included in the portfolio, among

others.

Collateral Manager: Performance. The collateral manager’s performance history in other transactions may not be indicative of future results including any results it may achieve in this transaction. The nature and risks associated

with the issuer’s future investments may differ materially from those investments and strategies historically undertaken by the collateral manager. There can be no assurance that the collateral manager or the persons associated

with it or any other entity or person will realize returns comparable to those achieved in the past or generally available in the market. Because the composition of the collateral will vary over time, the performance of the notes

depends heavily on the skills of the collateral manager in analyzing, selecting and managing the collateral. As a result, the issuer will be highly dependent on the analytical and managerial experience of the collateral manager and

certain of its officers and employees to whom the task of managing the collateral has been assigned.

Collateral Manager: Conflict of Interests. Various potential and actual conflicts of interest may arise from the overall investment activity of the collateral manager and its affiliates and the payment of management fees to the

collateral manager.

Recent Developments with Respect to LIBOR. Recent information has called into question the integrity of the process for determining LIBOR, and the full implications of such information is unknown at this time. An inaccurate

LIBOR setting could have adverse effects on a CLO issuer and/or the holders of secured notes. For example, holders of secured notes would receive lower dollar amounts as interest payments if LIBOR was artificially lower than a

properly functioning market would otherwise set LIBOR. Additionally, On July 27, 2017, the head of the UK Financial Conduct Authority made remarks indicating that LIBOR in its current form will be phased out as a benchmark rate

by the end of 2021. Actions by regulatory authorities or financial institutions to phase out, modify or eliminate LIBOR in the future may have a material adverse effect on the holders of notes, including the liquidity of such notes.

In addition, recent events have indicated that the UK’s Financial Conduct Authority intends to cease sustaining LIBOR from the end of 2021, and for the development of alternative benchmark rates. It is possible that the LIBOR

administrator and the panel banks could continue to produce LIBOR on the current basis after 2021, if they are willing and able to do so. However, the survival of LIBOR in its current form, or at all, is not guaranteed until or after

2021 and, if LIBOR in its current form does not survive, it could cause a disruption in the credit markets generally, which could negatively impact the market value and/or transferability of CLO securities and/or underlying senior

floating rate loans.

36For the Employees' Retirement System of Rhode Island Use Only

Risk Considerations

Risks of Investing in Senior Floating Rate Loans

Investing in Senior Floating Rate Loans entails certain unique risks, including but not limited to the following:

Interest Rate Risk. The value of the investments may decline when interest rates rise. In general, the longer the maturity of a security, the greater the effect a change in interest rates could have on the security’s price. In addition, a

security’s sensitivity to interest rate risk will increase with any increase in its duration. Floating rate securities can be less sensitive to interest rate changes.