China Taiping Insurance Holdings Company Limited Investor ... · 2015年末 2016年末...

108

China Taiping Insurance Holdings Company Limited Investor/Analyst Open Day 22 June, 2017

Transcript of China Taiping Insurance Holdings Company Limited Investor ... · 2015年末 2016年末...

China Taiping Insurance

Holdings Company Limited

Investor/Analyst Open Day

22 June, 2017

2

The presentation herein contains unaudited data. While the Company has endeavored to accurate and complete data, it makes no express or implied statement or warranty regarding fairness, accuracy, completeness and correctness of such information or opinions. All data contained in this presentation are only subject to the circumstances when they were provided and the Company makes no commitment to perform any update of the presentation for any consequent change

The “forward-looking statements” contained in the presentation herein refer to the statements of the Company on possible future business activities, events or evolutions. Such statements are assumptions formed on the basis of the Company’s future operations and various factors out of the control of the Company, hence actual operation outcomes may differ greatly from such statements

Data, statements or opinions contained in the presentation herein do not constitute any open offer or investment advice. The Company and its staff, whatever reason it might be, assume no responsibility for any loss or damage incurred from the use or interpretation of the presentation herein or any information in connection with it

Forward-looking Statements

3

China Taiping Insurance Holdings Company Limited was listed on the Hong Kong Stock Exchange Main Board in 2000, making it the first Chinese-funded insurer that was listed overseas

The parent company China Taiping Insurance Group Ltd. was founded in Shanghai in 1929 as a national insurance brand with the longest history in China, and is the only Chinese state-owned financial and insurance group whose management headquarters is located in Hong Kong. Its business covers many countries and regions in the world, particularly in Mainland China, Hong Kong, Macau, North America, Europe, East and Southeast Asia. In 2013, successfully completed its reorganization and restructuring as well as overall listing synchronously through China Taiping Insurance Holdings Company Limited (China Taiping hereinafter)

The principal activity of China Taiping is investment holding. The principal activities of China Taiping’s subsidiaries are the underwriting of direct life insurance business in the PRC and Hong Kong, direct property and casualty insurance business in the PRC, Hong Kong and overseas, pension and group life business, and all classes of global reinsurance business. Its subsidiaries also carry on operations in asset management, insurance intermediary, E-commerce, property investment, financial leasing, securities dealing and broking business

Company Introduction

China Taiping

— Overall Business Review

4

Business Overview

Overall Realization of Sustained, Healthy and Rapid Development from Jan to May, 2017

Balanced and rapid growth of scale and value

Continuous increase of overall strength

Continuous optimization of business structure

Significant improvement in operating efficiency

Continuous improvement in international influence

5

Business Overview (Cont’d)

Scale and Value of Mainland Insurance Business Have Gained Balanced and Rapid Development, and Business Structure Has Continued to be Optimized

By the end of May, direct premium written of life insurance totaled RMB 69.18 billion*, increased by 31.6% YoY

Agency force increased by 43.0% compared with 2016 year-end, resulting in an 56.3% increase in individual FYP YoY, which ranked No.4 in the industry; high productivity agents (FYP ≥ RMB 300,000) increased by 60.2% YoY; bancassurance regular premium increased by 88.9% YoY, with its business structure continued to be optimized

The four persistency ratio indicators of individual and bancassurance channel continued to maintain the industry-leading position; the loss ratio of short-term group insurance kept in a satisfactory range

TPI’s direct premium written increased by 11.5% YoY, continued to maintain double-digit growth. Growth rate of motor insurance is 15.5% YoY, which outperformed the market. Combined ratio decreased, continuing to make underwriting profits

Balance of pension assets under management was over RMB 140 billion

6 * All data related in this material is stated in RMB, if not specified

Business Overview (Cont’d)

Overseas Insurance Businesses Recorded Accelerated Growth, and international influence kept rising

Premium of CTPI(HK) increased steadily, keeping its forefront ranking in the HK P&C market

Overseas life insurance business was developing rapidly; TPL(HK) was founded in 2015 year-end

and achieved a premium income of HK$400 million from Jan to Mar 2017, with its ranking in

the market improved

The scale of TP Macau continued to rank No.1 in the market, with premiums and underwriting

profits both increased

Overseas companies actively provided insurance services for the Belt and Road strategic

projects, and the Chinese capitalized business of TP Indonesia developed rapidly

TPRe continued to promote international business by expanding the base of new customers in

Singapore, Thailand and Europe, and business with Lloyd's achieved a rapid growth; TPRe

(China) continued to improve its service level, and gradually enhanced its market influence

7

Business Overview (Cont’d)

Effective Implementation of Strategic Cooperation and Cross-selling

Initiatives with Large Clients

By the end of May 2017, China Taiping signed Group Strategic Cooperation

Agreements with 76 large clients; 4 new large clients was signed and 6 are being

worked on in 2017

Our cross-selling initiatives achieved RMB 2.09 billion premium sales, including RMB

1.69 billion of property insurance sales through TPL, RMB 0.36 billion of pension

sales through TPL, and RMB 30 million of property insurance sales through TPP

The Sinopec gas station project achieved rapid development, achieving RMB 0.505

billion of premium sales from Jan to May, in which RMB 0.34 billion is motor

insurance

8

• TPL

Mainland Life Insurance Business Review

9

Note: The Group holds 75.1% of the equity interest in TPL

Life insurance: The leading Indicator of Value Growth Continued

to be Excellent

Agency force grew rapidly on a year-on-year basis, and had reached 375,000

as at the end of May. The number of high productivity agents reached

10,000, realizing a substantial increase of 60.2% in the period of Jan to May

New business premium for individual and bancasurance core business

achieved rapid growth; structure for new business premium optimized, with

health insurance proportion being increased

Persistency ratio indicators continued to lead the industry

10

Life insurance: Premium remained a fast growth and solvency was

stable

11

Direct Premiums Written

( RMB million)

Comprehensive Solvency Ratio

69,181

Jan-May 2016

+31.6% 240% 251%

At 31 Mar 2017 At 31 Dec 2016

52,551

Jan-May 2017

C-Ross C-Ross

Further Increase in Proportion of Individual Business

Life Insurance: Structure of Gross Premiums – By Distribution

Channels

12

Jan-May 2016

Jan-May 2017

819 1,005

26,607 26,512

25,124 41,665

(RMB million,%)

Individual

Group and telemarketing

Bancassurance

Jan-May 2016 Jan-May 2017

47.8%

50.6%

1.6%

60.2%

38.3%

1.5%

Life Insurance: Individual New Business Premium for Health

Insurance Grew Substantially and its Proportion Increased

significantly

13

Individual New Business Health Insurance Premium

(RMB Million)

Others

Health Insurance

Individual New Business Structure

(%)

Jan-May 2016 Jan-May 2017

89.3%

10.7%

82.8%

17.2% +6.5pp

Jan-May 2016 Jan-May 2017

1,291

3,142

+143.4%

Year Distribution of Critical Illness Insurance In-force Business

Insurer Age Distribution of Critical Illness In-force Business

38.5% 47.9%

30.1%

24.1%

20.5%

20.0%

11.3% 9.8%

9.6%

8.6% 5.4%

8.8%

17.6% 16.5%

31.6%

Coverage Premium Policy

1 Year 2 Year 3 Year 4 Year 5 Year and above

33.6%

16.8% 29.3%

9.7%

6.4%

8.5%

16.9%

15.2%

17.0%

24.7%

30.2%

25.3%

12.8%

24.1%

16.3%

2.4% 7.4% 3.7%

Coverage Premium Policy

Age 0-9 Age 10-19 Age 20-29

Age 30-39 Age 40-49 Age 50-59

Critical Illness Insurance:New Business Grew Rapidly in Recent Two Years;

Actual Experience and Pricing Assumption for Insurer Age Closely Matched

14

Life Insurance: Agency Force Realized Rapid Growth; High

Productivity Agents Grew Substantially

15

Number of Agents

374,630

261,922

+43.0%

251,856

10,147

6,335

+60.2%

Number of High Productivity Agents*

(person) (person)

* High productivity agent refers to agent with RMB300,000 FYP and above

At 31 May 2017 At 31 Dec 2016 At 31 May 2017 At 31 May 2016

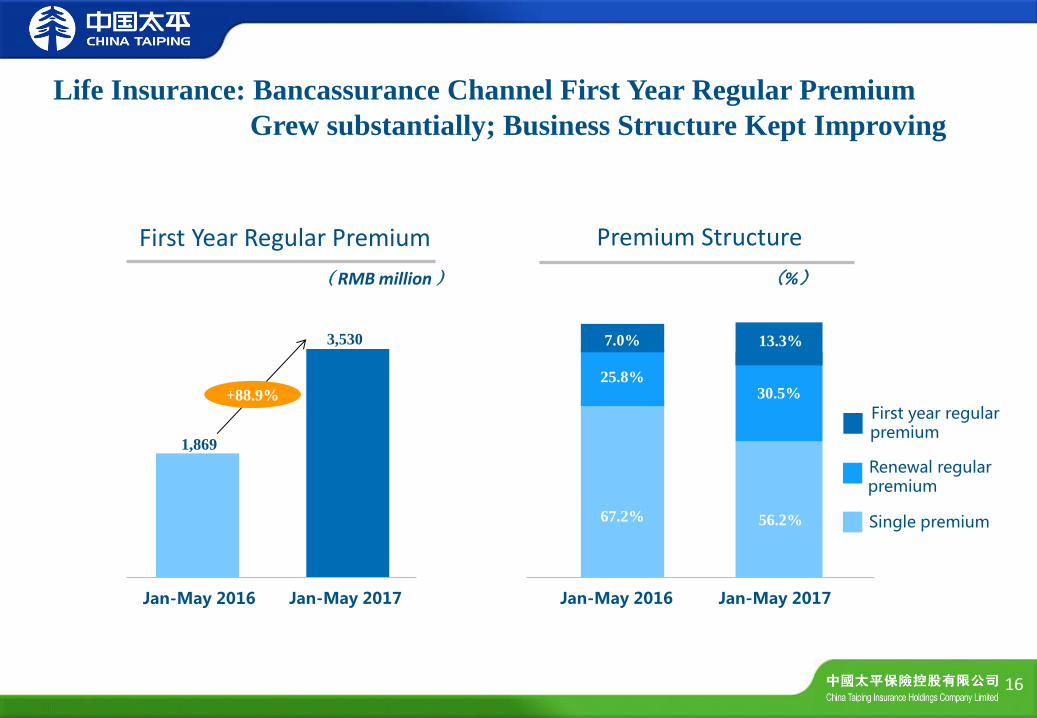

Life Insurance: Bancassurance Channel First Year Regular Premium

Grew substantially; Business Structure Kept Improving

16

(%)

3,530

1,869

Jan-May 2016

+88.9%

67.2%

25.8%

7.0%

56.2%

30.5%

13.3%

First Year Regular Premium

(RMB million)

Premium Structure

Jan-May 2017 Jan-May 2016 Jan-May 2017

First year regular premium

Renewal regular premium

Single premium

17

Life Insurance: Persistency Ratios Stood at the Forefront of the

Industry

93%

95% 97%

88% 89%

92%

2015年末 2016年末 2017年5月末

第13个月之保费继续率

第25个月之保费继续率

At 31 Dec 2015 At 31 Dec 2016 At 31 May 2017

92% 94%

96%

87%

89% 91%

2015年末 2016年末 2017年5月末

第13个月之保费继续率

第25个月之保费继续率

At 31 Dec 2015 At 31 Dec 2016 At 31 May 2017

Individual Bancassurance

Persistency ratio – 13th month

Persistency ratio – 25th month

Persistency ratio – 13th month

Persistency ratio – 25th month

Note: According to communications with peers, TPL was No.1 in both Individual and Bancassurance Channels in terms of 13th month persistency ratio

18 * result from the same valuation assumptions of 2015 unless otherwise specified, similarly hereinafter

+17.6%

+60.1%

-14.1%

2016 2015

+37.6%

New Business Value

Life Insurance: New Business Value Continued the Growth Trend

(RMB million)

Standard Change & Assumption Change Movement Analysis

(RMB million)

Standard Change

Business Growth

Assumption Change

2015 Solvency l

2015 C-Ross

2016* C-Ross

2016 C-Ross

C-Ross

C-Ross

5,927

8,154

5,927

5,041

8,154

9,488

19

+6.8%

+19.2% -5.7%

Adjusted Net

Worth

In-force Business

Value

+3.5%

+36.2% -10.4%

At 31 Dec 2016

+12.4%

At 31 Dec 2015

Embedded Value

Life Insurance: Embedded Value Continued Steady Growth Trend

(RMB million)

2015 Solvency l

2015 C-Ross

2016* C-Ross

2016 C-Ross

Standard Change

Business Growth

Assumption Change

(RMB million)

Standard Change & Assumption Change Movement Analysis

C-Ross C-Ross

82,338

73,240

68,582

34,643

33,939

73,240

38,128

35,112

87,313

47,839

39,474

82,338

42,864

39,474

• TPI

Mainland P&C Insurance Business Review

20

Note:The Group holds the 100% equity interest of TPI

Direct Premiums Written

(RMB million)

Comprehensive Solvency Ratio

Mainland P&C Insurance: Premiums Kept Growing Steadily

202% 206%

At 31 Mar 2017 At 31 Dec 2016

21

8,439

7,566

Jan-May 2017 Jan-May 2016

+11.5%

C-Ross C-Ross

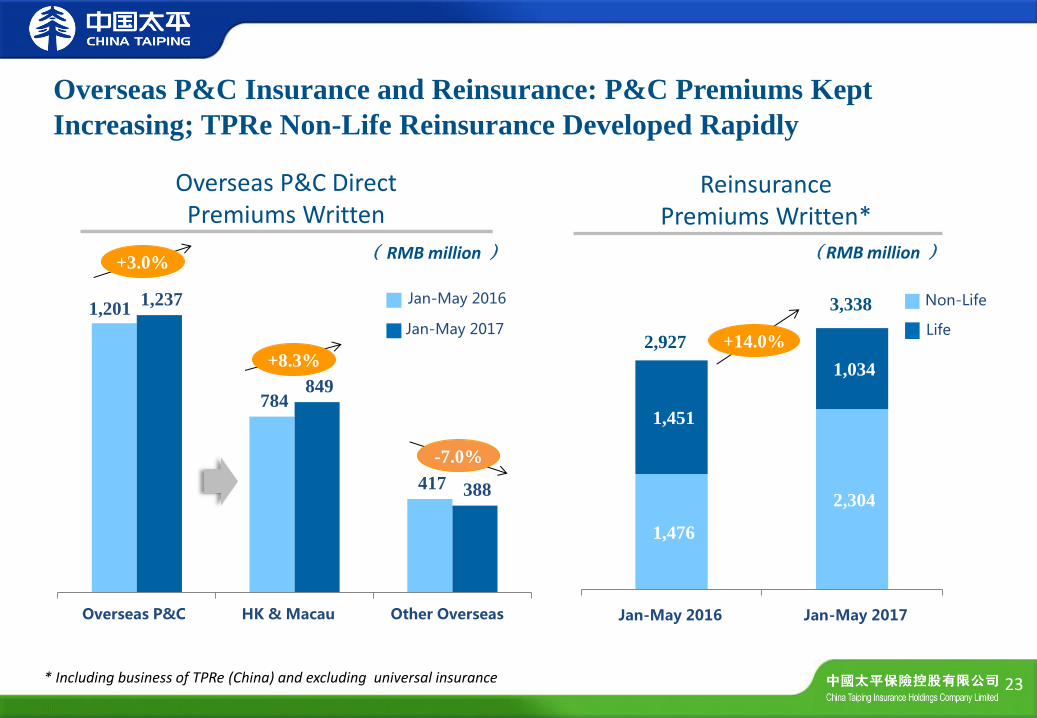

Overseas P&C Insurance and Reinsurance Businesses Review

HK & Macau

• CTPI (HK)

• TP Macau

Overseas

• TP Singapore

• TP UK

• TP Indonesia

Reinsurance

• TPRe

• TPRe (China)

22

Note:The Group holds 55% of the equity interest in TP Indonesia, and 100% in the other companies listed above

1,476

2,304

1,451

1,034

2016年1-5月 2017年1-5月 Jan-May 2016 Jan-May 2017

1,201

784

417

1,237

849

388

境外产险 港澳 海外 Overseas P&C HK & Macau Other Overseas

Jan-May 2016

Jan-May 2017

Overseas P&C Insurance and Reinsurance: P&C Premiums Kept

Increasing; TPRe Non-Life Reinsurance Developed Rapidly

23

-7.0%

+8.3%

+3.0%

3,338

+14.0% 2,927

Overseas P&C Direct Premiums Written

( RMB million )

Reinsurance Premiums Written*

(RMB million )

* Including business of TPRe (China) and excluding universal insurance

Non-Life

Life

• TPP

Pension and Group Life Insurance Businesses Review

Note: The Group holds 100% of the equity interest in TPP

24

25

Pension and Group Life Insurance Businesses: Premium Income Kept

Growing; Annuity Business Achieved Steady Growth

55,890

54,145

At 31 May 2017 At 31 Dec 2016

+3.2%

68,761

62,957

+9.2%

Jan-May 2017 Jan-May 2016

2,464

2,223

+10.8%

(RMB million)

Annuity Entrusted Assets Annuity Invested Assets

(RMB million) (RMB million)

Premiums Written

At 31 May 2017 At 31 Dec 2016

Outlook

26

Outlook Life Insurance Business

Under the guidance of the concept of "protection is the fundamental function of the insurance industry", life insurance market transformed, and the high-growth of individual new business drove the life insurance premium of the industry to maintain a high growth. A high growth of new business value is expected for the whole industry in 2017. Meanwhile the surrender rate continued to improve, indicating a rebound of the life insurance industry

In the context of a comprehensive trend of strict insurance regulation, the listed insurance companies with a sound internal control system and operating compliance are expected to be in a stronger position in the market competition

With the gradual promotion and implementation of the Outline of the Plan for Health China 2030 issued by the CPC Central Committee and the State Council, the health insurance market is expected to usher in a new growth point

Occupational annuity is expected to break through in the second half of 2017, and the annuity market is expected to usher in development opportunities

Investment assets are expected to grow faster in 2017 while rising interest rates are expected to ease the investment pressure; investment return is expected to remain stable throughout the year

27

Outlook (Cont’d)

P&C Business

The growth of new car sales slows down, and the traditional non-motor insurance business such as corporate property insurance and cargo insurance with strong relevance to economic environment grows slowly, seriously restricting the overall development of the P&C insurance industry

With the deepening of the motor insurance marketization reform and the launch of the second round of the reform, the market competition is increasingly intensive, the premium adequacy ratio is further reduced, the motor insurance growth continues to slow down, and underwriting profitability continues to be under pressure

With the national the Belt and Road strategy and the acceleration of the modernization of national governance, the new economy is booming, and non-motor insurance business such as liability insurance, accidental health insurance and agricultural insurance will usher in the development opportunities while raising high demand on the professional services and risk management capabilities of insurance companies

28

Outlook (Cont’d)

29

Reinsurance Business

Reinsurance market funds are still abundant, and a lot of capital in entering the reinsurance industry and the Chinese market. Fierce competition will lead to the continuous decline of the premium rate, and underwriting profit margins will continue to narrow

With the increase in claim of insurance with large coverage, the driving of the regulatory policies including C-ROSS and the new risks brought about by the development of science and technology, new insurance needs are generated. Reinsurance, as an effective means to diversify risks, manage capital and control business fluctuations, is re-evaluated and recognized by the market

With the system of C-ROSS, the impose of differentiation requirement on risk capital of domestic and overseas reinsurance companies is conducive to business development and market performance of TPRe in China

Thank you!

30

TPL

— Life Insurance Business Review

31

• Business Development

Individual Life Insurance Business Review

32

Business Development

Agency Force and Premium Increased Steadily

As of the end of Mar 2017, the number of agents was 321,000, and regular premium was RMB 16.14 billion in the first quarter of 2017; as of the end of May, agency force reached 366,000, and regular premium was RMB 17.78 billion

As of the end of Mar 2017, the market ranking of individual new business premium continued to remain No.4

33

Jan-Mar 2016 Jan-Mar 2017 YoY Growth Jan-May 2017

Agency Force 234,000 321,000 37% 366,000

Regular Premium 9.6 billion 16.14 billion 68% 17.78 billion

Regular Premium per Month

3.2 billion 5.38 billion 68% 3.56 billion

Note:1. Data in this page does not include the Sinopec gas station project, and similarly hereinafter 2. Regular premium in this page is company’s assessment indicator, which is calculated as “FYP+Single Premium*0.1”,

and similarly hereinafter

Business Development (Cont’d)

34

Agency Force Trend since 2016

Assessment was made in strict accordance with the Basic Law in 2016, and agency force reached 250,000 in the fourth quarter, and reached 254,000 at the end of the year, an increase of 17% over the beginning of the year; after a year of integration of agents in the first quarter of 2017, agency force realized growth with break through, reaching 321,000 at the end of the quarter, and 366,000 as of the end of May

20.7 20 23.4 22.7 21.5

23 22.8 24.2 24.5 25.2 25.4 25.4 26.1

30.632.1 33

36.6

15

20

25

30

35

40

Jan-16 Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Jan-17 Feb Mar Apr May

10 Thousand Agents

• Key Agent and Performance Indicators

Individual Life Insurance Business Review

35

2015 2016 Jan-Mar 2017

Group 24,962 32,489 34,493

Agency Force per Group 9.1 8.0 9.3

Department 4,677 5,892 6,061

Agency Force per Department 48.7 44.2 52.9

Key Agent and Performance Indicators

Agency Force per Group, Agency Force per Department

Retention Rate

36

2015 2016 Jan-Mar 2017

6th Month Retention Rate 83.0% 75.1% 82.7%

13th Month Retention Rate 52.5% 41.6% 48.1%

24th Month Retention Rate 24.4% 24.3% 23.3%

Key Agent and Performance Indicators (Cont’d)

37

2017 Agent Development

In the first quarter of 2017, strict basic management was made for individual channel, the new agent retention system was continued to be strengthened, and the Basic Law was followed for promotion. The number of new agents reached 101,000 in the first quarter, and the agency force reached 321,000 at the end of the first quarter, and reached 366,000 as of the end of May

Assessment was made in strict accordance with the Basic Law of the 2016 version. We have moderately raised some of the basic standards of the Basic Law. For example, the standard of new contract commission for active agent was raised from RMB 300 to RMB 500; the group structure standard for promotion to senior executives was adjusted, and the requirement for direct groups was increased

Key Agent and Performance Indicators (Cont’d)

Key Performance Indicators

38

2015 2016 Jan-Mar 2017 Jan-May 2017

Policy Per Month Per Capita 0.95 1.09 1.9 1.3

Productivity Per Month Per Capita (Regular)*

14,181 15,145 36,227 27,416

Monthly Overall Activation Ratio 49.8% 52.5% 60.8% 59.5%

Three Month Formalization Ratio 37.9% 45% 41% 44.8%

Cumulative Activation Ration In Three Months

76.3% 81.3% 91.4% 88.4%

Monthly Agents With RMB 10K Sales (regular Premium)*

30,635 39,273 100,477 77,224

Annual Agents With RMB 1MM Sales (regular Premium)

1,451 1,924 2,167 2,275

* In the first quarter of 2017, the high regular premium for the Jump Start period significantly increased the agent productivity; products with high NBV will be sold in the second half of the year, and it is expected that the average annual indicators will fall back

Key Agent and Performance Indicators (Cont’d)

39

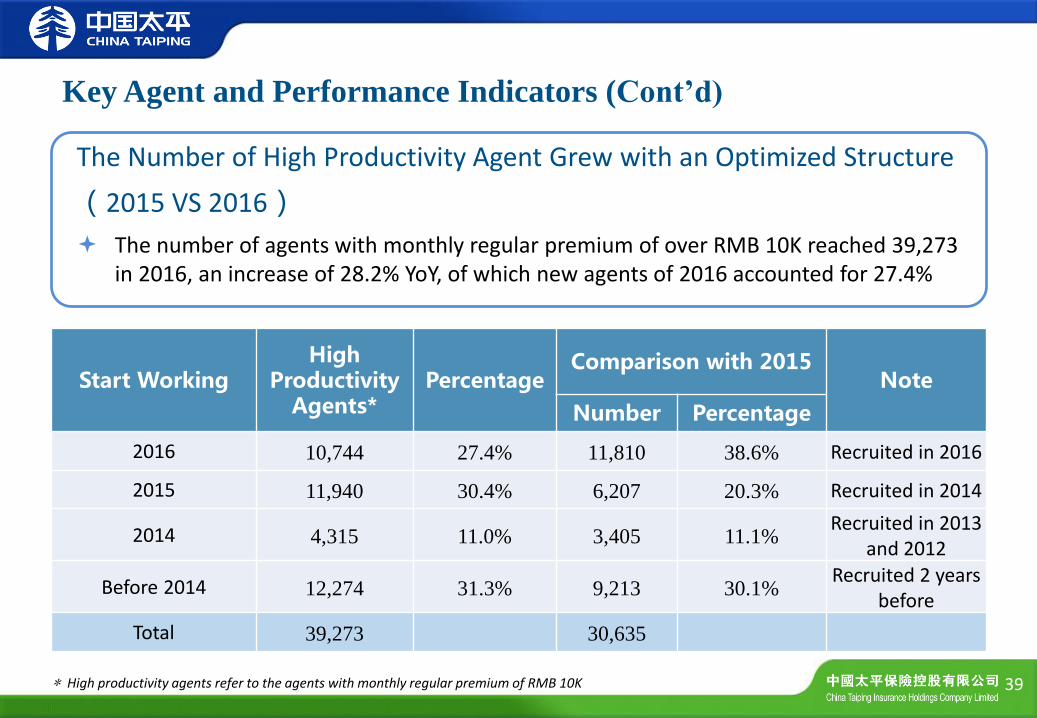

Start Working High

Productivity Agents*

Percentage Comparison with 2015

Note

Number Percentage

2016 10,744 27.4% 11,810 38.6% Recruited in 2016

2015 11,940 30.4% 6,207 20.3% Recruited in 2014

2014 4,315 11.0% 3,405 11.1% Recruited in 2013

and 2012

Before 2014 12,274 31.3% 9,213 30.1% Recruited 2 years

before

Total 39,273 30,635

* High productivity agents refer to the agents with monthly regular premium of RMB 10K

The Number of High Productivity Agent Grew with an Optimized Structure

(2015 VS 2016)

The number of agents with monthly regular premium of over RMB 10K reached 39,273 in 2016, an increase of 28.2% YoY, of which new agents of 2016 accounted for 27.4%

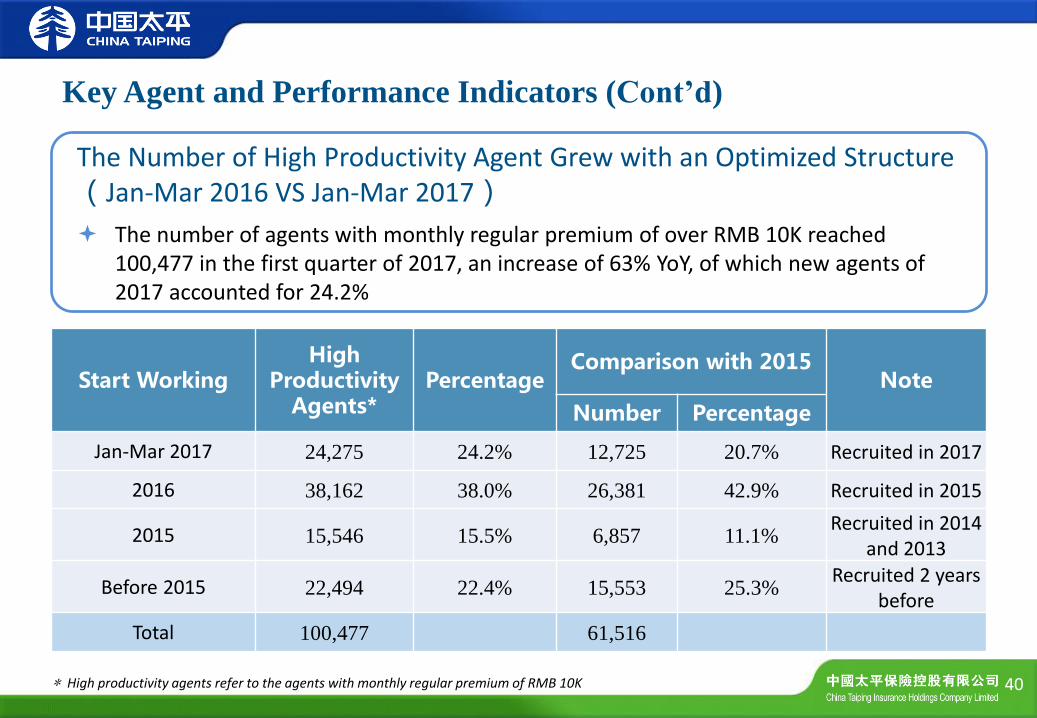

The Number of High Productivity Agent Grew with an Optimized Structure(Jan-Mar 2016 VS Jan-Mar 2017)

The number of agents with monthly regular premium of over RMB 10K reached 100,477 in the first quarter of 2017, an increase of 63% YoY, of which new agents of 2017 accounted for 24.2%

Key Agent and Performance Indicators (Cont’d)

40

Start Working High

Productivity Agents*

Percentage Comparison with 2015

Note

Number Percentage

Jan-Mar 2017 24,275 24.2% 12,725 20.7% Recruited in 2017

2016 38,162 38.0% 26,381 42.9% Recruited in 2015

2015 15,546 15.5% 6,857 11.1% Recruited in 2014

and 2013

Before 2015 22,494 22.4% 15,553 25.3% Recruited 2 years

before

Total 100,477 61,516

* High productivity agents refer to the agents with monthly regular premium of RMB 10K

• Development Strategy for 2017

Individual Life Insurance Business Review

41

As of the end of the first quarter of 2017, agents employed for 6 months in the existing teams accounted for 42%, and agents employed for 12 months accounted for 64%. The high proportion of new agents imposed pressure on basic management, and their increased productivity and effective retention require time and ongoing training

The growth of TPL’s individual insurance business is much higher than the growth of agent force; the agent force increased by 17% in 2016, and the premium increased by 39%; how to maintain the continuous improvement of productivity is the pressure we face

The new policies of the regulation from CIRC affects the design of new products. It is expected that the growth of premium in 2017 will depend on the increase of agency force and the total number of policies. In the first quarter of 2017, the number of new agents reached 101,000, accounting for 50% of the number of agents recruited in 2016

1. Opportunities and Challenges

42

2. Development Strategy for Individual Channel in 2017

43

Product Promotion: Implementing the value-scale dual-driven strategy of rhythm switching

Agent Development: Making strict basic management, improving the retention rate of new agents, and stressing the operations of business groups and tier-four institutions

Training: Focusing on promoting the standard training, business manager promotion and self-management of high-level executives, and increasing the training of counselors and improving the effectiveness of training

Institutional Management: Combing and optimizing management logic and management structure, enhancing the capacity of institutions at all levels, and integrating resources to enhance the market position of the institutions

Product Promotion: Improving Product Switching

44

Continuously Improve the Mode of Switching and Alternating Operation of Health Products and Annuity Products

Drive two rounds of annuity products and two rounds of health products, and clarify the pace of business throughout the year in advance. At the same time focus on selling key products by relying on operation advantages of various types of projects

Attract Customers with Online and Offline Activities, and Help the Agents to Get Access to the Market As Soon As Possible

Manage the Alternation Between Old and New Products Combined with Regulatory Policy Requirements

Ensure the smooth delisting of old products and timely converge competitive new products in line with market demand combined with regulatory policy requirements, while holding the team's product training, and guiding the team to quickly adapt to sales of new products

45

Agent Development: Effective Growth of Agency Force Ensures Healthy,

Stable and Sustainable Development of Individual Business

Continue to Promote Effective Growth of Agency Force

Business managers are key force to promote the growth of individual business; continue to speed up promotion in 2017, and improve the number and quality of business groups. In the first quarter of 2017, the number of new business managers promoted was 9,184, accounting for 55% of the total promotion of 2016

Continue to Improve the “New Agent Retention System”

Without affecting the existing pre-service and orientation 135 training projects, the System focused on operating units of tier-four institutions by optimizing and transforming the link of new agents’ retaining; the focus is on the habit curing of new agents within 30 days; 310 marketing service units will be added in the System in 2017, and 149 service units were already added in the first quarter of 2017

Build a Multi-channel Sales Force Focusing on Individual Business and Supplemented by Sinopec Project and Service Marketing, so as to Enhance the Number and Quality of Agents

46

Training: Focusing on Retaining New Agents and Training Executives

Continuously Promote the Standard Training and Stabilize System Training Platform to Build the Basic Ecological Foundation for the Retention of New Comers

Strictly implement the induction training requirements for new agents (various channels); Insurance Agents Qualifying Examination APP was put into effect

Continuously Enhance the Business Managers’ Ability to Guide the Operation, and Continue to Promote Self-management through High-level Executive Management Seminars

Continuously improve the ability of the executives in guiding operations through promotion oral examination, MCA training and business manager training

Sales department training (building a new agent development platform in the business department)

Continue to Promote the Training of Internal Work Training Cadre

New agent auxiliary training is held for 640 people in 4 sessions in the year; in-service auxiliary training is held continuously

Strengthen Online Support, and Gradually Realize The “Rich, Visual, Audible, Interactive, and Integrated” Training Management Platform in Which Learning Management Can be Conducted

Optimize the existing training management and micro-classroom system, and enrich online courses; develop the live interactive feature and integrate online resources

47

Institutional management: Improve the institutional management

system and drive institutions to become bigger and stronger

According to The Company's Development Strategy and Institutional Development, Revise the Star Standard and Drive the Operating Units under Institutions to Comprehensively Develop with All Indicators Combing and optimizing management logic and management structure; in February the Approach to Meet Star Standard for Institutions was revised, and the Basic Law where the Approach is used for institutional assessment is vigorously promoted

Further Improve the Institutional Management System by Driving Systematic and Standardized Operation of the Institutions Facilitate the use of the Operating Manual of Tier-Four Institutions of TPL Individual Channel in the institutions; and examine responsible persons of Tier-Four Institutions on their understanding of the Manual

Improve the Training System of Management Cadres Hold senior management personnel training by classification and categories to improve their management capacity and overall quality

Develop more online and offline marketing support tools such as H5 page of the company's profile, claims report and customer service newspaper.

Mobile agent on-line self-service system

The Sales Support system APP builds agent insurance supermarket platform (business card, product introduction, insurance book, news center)

Make the revised version of Individual Insurance Morning Training by deepening and optimizing the contents and add new channels for optimization and dissemination (dual number, Corporate blog can be more targeted, safe and effective dissemination of internal training content)

48

3. Utilized Internet with Marketing Support Tools

• Business Development and Strategy

Bancasurrance Business Review

49

Bancassurance Business Development

Bancasurrance (RMB 100 million)

Jan-Mar 2017 YoY Growth Percentage Jan-May 2017

Single Premium 145.17 -16.3% 82.9% 145.41

Regular Premium 29.97 122.1% 17.1% 35.34

In the first quarter of 2017, Bancassurance took the initiative to adjust the business

structure by reducing single premium and increasing regular premium business

Single premiums decreased by 16.3% YoY while regular premiums increased by 122.1%,

accounting for 17.1% of total premium, with an increase of nearly 10 percentage

points YoY

50

Bancassurance Channel Structure

5.6

4.8 4.6

3.4

2.4

1.5 1.2

1.2

5.3

187%

93%

211%

222%

71%

12%

93%

47%

124%

0%

50%

100%

150%

200%

250%

0

1

2

3

4

5

6

ICBC CCB BOCOM BOC ABC CMB Industrial

Bank

SPDB Others

Jan-Mar 2016 Jan-Mar 2017 YoY Growth(RMB 100 million)

We had a substantial growth in regular business among the five major banks YoY, and the channel structure was significantly improved

51

Bancassurance Development Strategy for the Second Half of the Year

In accordance with the overall requirement that protection is the fundamental function of the insurance industry, speed up the transition to the protection business, adhere to value growth, and further expand the regular business

Deepen channel cooperation by strengthening the channel linkage, and focusing on key banks including ICBC, ABC, BOC, CCB and BOCOM; continue to promote precision marketing, and improve business proportion to achieve stability and increase of channel share and ranking

Innovate the mode of operation by improving and optimizing the existing mode of operation and improving the level of project operation and output efficiency to achieve accurate customer marketing and intensively farmed projects

Strengthen team building by making strict basic law assessment, strengthening cost control, and encouraging outstanding institutions to develop agency force; continue to promote the growth of high productivity agents with "Fortune 500" as the starting point

Expand business coverage by enhancing the classification and category management of institutions, and strive to build 100 tier-three institutions and improve the business coverage of tier-four institutions

Continue compliance management by strictly carrying out inspection and supervision in accordance with the requirements of regulatory authorities and resolutely investigating and dealing with the problem found and seriously implementing accountability

52

• 2017 First Quarter Sales Introduction

Jump Start Review

53

Individual Channel Focused on Value Growth; Long-term Protection

Business Growth Rate was Higher Than Overall Growth by Focusing on

Customers’ Health Protection Needs

17.0

45.1

Jan-Mar 2016 Jan-Mar 2017

+165%

(RMB 100 million)

Note: Long-term protection products refer to the products of illness insurance, accident insurance, term life insurance and whole life insurance with an insurance period of more than one year

In the first quarter of 2017,new business grew 69% YoY, of which long-term protection products grew 165%, which is higher than the overall growth. Compared with the first quarter of 2016, proportion of long-term protection products increased by 10 percentage points

Among long-term protection products, illness insurance sales accounted for nearly 90%. Will continue to focus on customers’ health protection needs and promote its normal operation

Long-term Protection Products FYP (2016vs2017)

54

Bancassurance Insists on Transformation Towards Value with Rapid

Growth of Regular Business. Proportion of 10-year and above Regular

Premiums is Stable, and Participating Products Still Dominate

Bancassurance FYP (2016 vs 2017)

13.5

30.0

Jan-Mar 2016 Jan-Mar 2017

+122%

(RMB 100 million)

Bancassurance Regular Products Structure

(Jan-Mar 2017)

64%

33%

3%

10 years and above

5-9 years

Others

In the first quarter of 2017, single premium business was steady but declined, and regular premium business was doubled compared to the same period in 2016; regular premium products were mainly long-term

For regular premium business, sales volume of ordinary products accounted for 35%, and participating products still dominate

55

• Product Strategy for 2017

Product Introduction

56

Focus on Customers’ Protection Needs and Support Collaborative Growth

of Business Scale and Value to Achieve Breakthrough Growth for Core

Value Business

Bancassurance Product

Individual Product

Support transformation towards value, match the operation of precision marketing projects and normal business model, classify customer base, and actively develop high-value regular products

Strengthen high value annuity regular products, shrink the size of single business, and supplement long-term protection products throughout the year

Focus on customers’ pension and health needs, constantly optimize the product structure, and support the coordinated development of regular premium and business value

Focus on annuity products in Jump Start and mid-year, continue to promote long-term protection products throughout the year, build worry-free series products, and help achieve agency force target

57

Thank you!

58

TPI

— P&C Business Review

59

P&C Business Development

60

Core Business Realized Sound Growth

In the first quarter of 2017, direct premiums written were RMB 4.66 billion; from Jan to May, direct premiums written were RMB 8.44 billion, and RMB 6.80 billion was motor insurance

Operating Efficiency Continued to Improve

In the complex and fluctuate market environment , realized underwriting profit in six consecutive years with continuous accelerated development

In-depth Practice of the Boutique Strategy

By the end or May 2017, the Group signed the contract to achieve premium income of RMB 630 million and customer cooperation coverage rate of 81.3%; comprehensive financial results were significant, property insurance sales through TPL increased by 43.7% YoY and the premium increase accounted for 47.6%. Promote customer-centric and technology-led product innovation "+ Internet" and conduct continuous research and application of insurance innovation brought about by new technologies of the Internet

Jan-May 2016Jan-May 2017Jan-Mar 2016Jan-Mar 2017

2.6

2.9

Jan-May 2016Jan-May 2017

1.5

1.9

Jan-Mar 2016Jan-Mar 2017

61

Adhere to the Principle of Core Business Outperforming the Market,

and Actively Fulfill the Responsibility as A Central Enterprise

Actively deal with the motor insurance marketization reform; as of the first quarter of 2017,

motor insurance premium was RMB 3.60 billion; by the end of May 2017, motor insurance premium was RMB 6.80 billion with an increase of 15.5% YoY, outperforming the market by 7.8pp

Make in-depth study of national strategies to accelerate the development of agricultural insurance, liability insurance and other policy insurance business; as of the first quarter of 2017, agricultural insurance and liability insurance business maintained rapid growth

Agriculture Insurance Premium Motor Insurance Premium

+ 26.7%

+ 11.5% +254.8% + 265.3%

(RMB 100 million)

4,285

Jan-May 2016Jan-May 2017

36.0

Jan-Mar 2016Jan-Mar 2017

+ 15.5% + 8.1%

68.0

58.9 33.3

1,173 757

2,686

Liability Insurance Premium (RMB 100 million) (RMB 10 thousand)

Accelerate Development with the Bottom Line of Maintaining

Underwriting Profit

62

Combined Ratio Direct Premiums Written

108.0

132.7

156.1

181.8

84.4

2013 2014 2015 2016 Jan-May

2017

99.9% 99.9% 99.8% 99.8%

2013 2014 2015 2016 Jan-May

2017

(RMB 100 million)

Jan-May 2016 Jan-May 2017

6.8

9.5

Jan-Mar 2016 Jan-Mar 2017

4.6

6.3

Jan-May 2016 Jan-May 2017

2.6

4.0

Jan-Mar 2016 Jan-Mar 2017

Develop the Boutique Strategy and Highlight Characteristics Business

The Group strategic costumer business effectively had break through signing the insurance project of the Hong Kong-Zhuhai-Macao Bridge of Zhuhai municipal government and the Kunming Metro Line 4 project of China Railway Group with a total premium income of RMB 3.8 million . Promote the CGN Singapore project to achieve breakthrough in the overseas strategic customer business

Property insurance sales through TPL continued to improve with a 43.2% growth YoY from Jan to May 2017

New progress has been made in the North American market. Successfully contacted with the major domestic reinsurer, and established an appointment sub-agreement in speeding up the cooperate with STARR

Linkage with Japan orderly advanced. A meeting was held to promote the insurance business of travel in Japan; a project team was set up, job objectives and responsibilities were clarified, and regular work meetings were held. Actively cooperate with the "cross-border" project development while studying the launch of we-chat service platform and products

63

Strategic Customer Business

Property Insurance Sales through TPL

+ 53.8% + 37.0%

+ 39.7% + 43.2% 16.9

11.8

(RMB 100 million)

(RMB 100 million)

Initiate Customer Management and Fully Embrace the Internet

Dock Internet giants, independently develop innovative products, and enhance pricing power through big data

Dock the Five Major Internet Giants

Carry out Big Data Experiments

Work with Ant Financial to carry out motor insurance data building and enhance motor insurance pricing ability; optimize the existing pricing model from human factor + big data accurate pricing, which is beneficial for TPI to establish stronger pricing advantage

Set up five team of Ant, Qunar, Baidu, Jingdong and Tencent to dock Internet giants, and become the backbone in the business expansion of network marketing for the company

Developed non-motor insurance network marketing products such as Alipay account security insurance, passenger accident insurance, RMB 3.99 aviation accident insurance, and parents anti-telecommunications fraud insurance

64

Adhere to The Strategy of "Product Innovation Driven"

P&C Development Strategy for 2017

65

Seize New Opportunities and Get off to a Good Start to Become Leader In the Second Tier of the Industry Take the preemptive opportunities in the market, and build up business development advantages. Promote

professional building of motor insurance channels, deepen strategic interaction and interconnection of P&C business, and strengthen innovation driven for accident & health insurance

Strive to develop overseas business, and actively coordinate with overseas subsidiaries. Strengthen the efforts to expand strategic customers, support domestic enterprises to expand overseas, and enhance coordination and interaction with overseas subsidiaries

Accelerate strategic business development, and implement characteristic business. Promote contract signing with group customers, build the organizational structure for development of worksite marketing, and develop agriculture insurance business steadily

Focus on the problem of claim ratio reduction and renewal, and comprehensively enhance cost-saving and profit-increasing. Strictly prohibit fraud cases, fully strengthen claim management, accelerate building of Internet and phone renewal platform, and establish a total-cost analysis system

Drive channel specialization, and implement the differentiated development strategy. Cross-selling Channel shall promote high quality growth , Group Channel shall promote team building, Sinopec Channel shall build new business foundation, Car Dealer Channel shall boost increase of renewal rate, Agent Channel shall advance transitional development, and Bancassurance Channel shall promote specialized operation

Intensify cost-saving and profit-increasing, and comprehensively upgrade service level. Improve the effectiveness of management team, enhance building of sales team, intensify management and control of expenses and costs, manage service evaluation ranking, and increase the information technology level

Optimize internal control of risks, and strengthen risk prevention management. Reinforce risk management, improve quality of auditing, inspection and rectification, and enhance compliance control ability building

Thank you !

66

China Taiping

— Investment

67

• Group Investment Introduction

Investment

68

69

Asset Size Rose Rapidly, and Asset Under Management of The Group

Reached the Level of RMB 700 billion

As of the end of May, insurance asset under management within the Group was RMB 403.6 billion, increased by 6.4% compared to the beginning of the year; third-party entrusted asset was RMB 309.4 billion, increased by 16.8% compared to the beginning of the year

0

1000

2000

3000

4000

5000

2012年 2013年 2014年 2015年 2016年 2017年5月

Asset Under Management with the Group

0

500

1000

1500

2000

2500

3000

3500

2012年 2013年 2014年 2015年 2016年 2017年5月

Third-party entrusted Asset

2012 2013 2014 2015 2016 May 2017 2012 2013 2014 2015 2016 May 2017

70

Bond asset and debt scheme jointly account for 60.2%, and constitute the main segments in asset allocation of the Group

Equity securities account for 8.1%. The latest industry data shows that the proportion of stocks and funds at the end of March was 12.7%

Asset Allocation is Positive and Steady, with the Debt Portfolio Covering

60.2% and Equity Portfolio Covering 8.1%

10%

45%

8%

15%

6%

4%

12%

Proportion of Main Asset Categories

现金存款及货币市场工

具

债券资产

权益类证券

债权计划

股权投资

投资性物业

其他金融产品

Cash deposit and instruments of money market

Bond assets

Equity securities

Debt Scheme

Equity investment

Investment property

Other financial products

71

Market Value Yield and Book Yield

As of the end of May, market value yield of investment assets of the Group surpassed that of the same period last year

Part of unrealized equity loss was realized and book yield was behind the same period last year, but the equity position structure has been optimized

2016年5月末 2017年5月末

Market Value Yield

-0.19%

2.17%

2016年5月末 2017年5月末

Book Yield

At 31 May 2016 At 31 May 2017 At 31 May 2016 At 31 May 2017

72

Traditional Assets Performed Differently. Bond Performance Surpassed

Market, while Stock Performance Lagged Behind

As of the end of May, the overall yield of trading and available-for-sale bond assets of Taiping Asset was above ChinaBond Total Wealth Index

As of the end of May, the overall yield of stock portfolio of Taiping Asset was below the Shanghai and Shenzhen 300 Total Return Index and the stock type publicly offered funds

Bond Investment Performance

Taiping Assets ChinaBond total

wealth Index

Stock Investment Performance

-1.7%

Taiping Assets Index of Stock

Funds

Shanghai and Shenzhen 300 Total

Return Index

-0.4%

5.8%

73

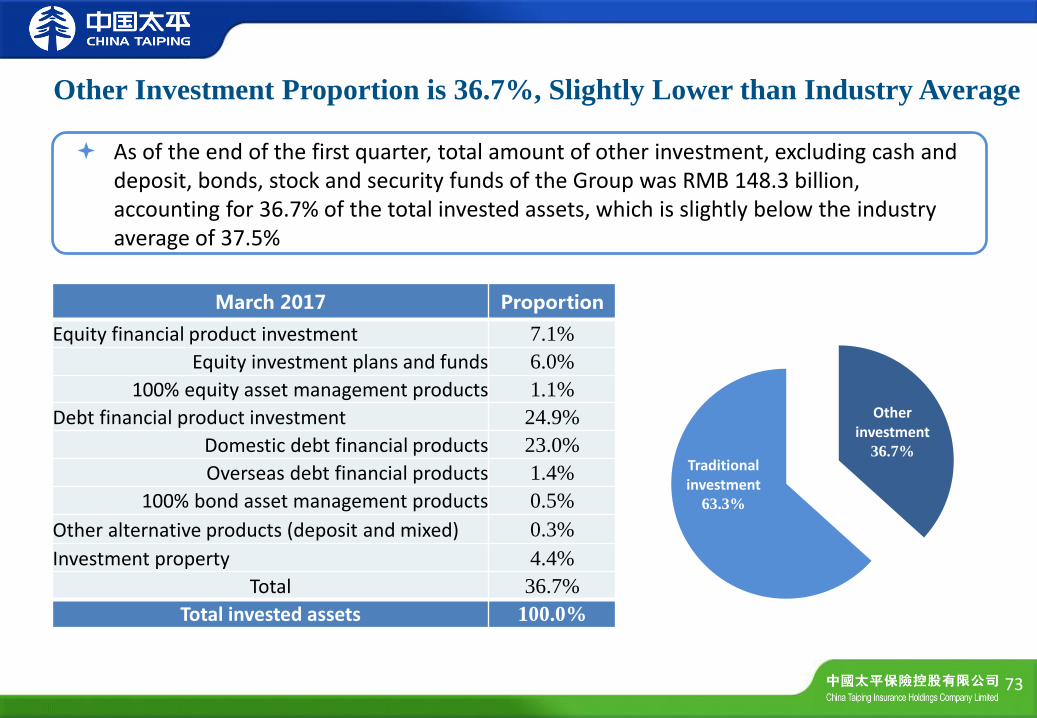

March 2017 Proportion

Equity financial product investment 7.1%

Equity investment plans and funds 6.0%

100% equity asset management products 1.1%

Debt financial product investment 24.9%

Domestic debt financial products 23.0%

Overseas debt financial products 1.4%

100% bond asset management products 0.5%

Other alternative products (deposit and mixed) 0.3%

Investment property 4.4%

Total 36.7%

Total invested assets 100.0%

Other Investment Proportion is 36.7%, Slightly Lower than Industry Average

As of the end of the first quarter, total amount of other investment, excluding cash and deposit, bonds, stock and security funds of the Group was RMB 148.3 billion, accounting for 36.7% of the total invested assets, which is slightly below the industry average of 37.5%

Other investment

36.7% Traditional investment

63.3%

35%

20%

17%

13%

7%

4% 3%

1%

地方国企及其他担保

准中央政府债/银行担保

免增信

大型企业担保

抵押/质押

优先劣后

其他

无增信

74

82.1%

6.2%

0.8% 10.8%

Debt Financial Products Ratings

AAA

AA+

AA

不适用 NA

Debt Financial Products Feature High Credit Rating and Credit

Enhancement Measures were Sound

As of the end of the first quarter, debt financial products within the Group have maintained high credit rating, of which AAA level products account for 82.1%, and AA+ and AA account for 7.0%. The remaining 10.8% of overseas fixed income funds and convertible debts does not apply

In terms of credit enhancement, quasi central government debts/bank guarantee and credit enhancement exempted products cover 37.2%, large-scale enterprise guarantee covers 13.0%, local SOE and other guarantee covers 34.6%, mortgage/pledge products 7.5%, and others 7.7%

Debt Financial Products Credit Enhancement

Local SOE and other guarantee Quasi-central Government Debts/Bank Guarantee Credit Enhancement Exempted

Large-scale Enterprise Guarantee

Mortgage/Pledge

Superior/Inferior

Others

No Credit Enhancement

75

Types of Other Investment Become Diversified Along with Development of

the Industry

As of the end of the first quarter, in the debt financial product investment, infrastructures and real estate investment jointly cover 41.0%, trust products cover 38.2%, asset management products 6.3%, special asset-backed plan 3.7%, and the overseas bond funds and convertible debts 10.8%

As of the end of the first quarter, in the debt financial product investment, real estate industry accounts for 26%, public utilities industry accounts for 21%, transportation industry for 19%, non-bank financial industry 14%, and the other industry 20%

38%

31%

10%

6%

4% 11%

Classification of Debt Financial Product Investment

信托

基础设施建设债权计划

房地产债权计划

资管产品

资产支持计划

境外债权基金与可转债

26%

21%

19%

14%

3% 3%

3%

Primary Industry Classification of Shenyin & Wanguo Securities Co., Ltd.

房地产 公用事业 交通运输 非银金融 建筑材料 商业贸易 综合 采掘 建筑装饰 航运 医疗生物 医药生物

Trust

Infrastructure Construction Debt Scheme

Real Estate Debt Scheme

Asset Management Products

Asset-backed Plan

Overseas Bond Funds and Convertible Debts

Real Estate

Public Utilities Industry

Transportation Industry

Non-bank Financial Industry

Construction Material

Commercial Trade

Comprehensive

Extractive Industry

Architectural Ornament

Shipping

Bio-medicine

Bio-pharmacy

76

Center on National Strategies, Correspond to the Core Insurance Business,

and Innovate Investment Form

Center on the national strategies to make alternative investment innovation, actively explores in terms of public-private partnership (PPP), the Belt and Road, senior health service and supply-side reform and has obtained favorable returns and brand effect.

PPP

Taiping-Shanghai

Construction Group PPP

Industry Fund Project

The Belt and

Road

Silk Road Prosperity

Taiping Fund

Senior Health Service

Taiping Shanghai “Wutong Renjia” senior

housing community

Taiping Yifang Health

Pension Industry Equity

Investment Fund

Taiping –Watermark

Joint Venture

Support Supply-side Reform

CICO-Taiping Infrastructure

Equity Investment

Fund

Taiping-Qinghai

Supply-side Reform

Industry Fund Equity

Investment Plan

The Group invests in properties mainly in the first-tier cities of Beijing, Shanghai and Shenzhen, the second-tier cities of Suzhou, Nanning and other economically developed ones with growth potential, as well as Hong Kong and Macau

Area and quality for most of the projects are superior, and rent operation situation is well

Yield of the Group’s property investment for the past five years were high and steady, and the compound yield reached 11.13%

Projects Locations Business types

Main projects

completed

Shanghai Taiping Financial Tower

Lujiazui, Shanghai Office building

Hong Kong Taiping Tower

Causeway Bay, Hongkong

Office building

The Exchange Building Beijing

China World Tower Office building

Shenzhen Taiping Financial Tower

Futian Central District, Shenzhen

Office building

Longbi Industrial Zone Bantian, Shenzhen Industry

Main projects under

construction

Beijing Guangan Center Beijing Financial

Street Office building

Suzhou Taiping Financial Tower

Jinji Lake, Suzhou Office building

Nanning Taiping Financial Tower

Wuxiang New District, Nanning

Office building

Shanghai Zhoupu Old-Senior Service Communities

Zhoupu, Pudong District, Shanghai

Senior service community

77

Real Estate Investment Focuses on Core Cities and Core Areas

• Investment Strategy for 2017

Investment

78

Global Economy Recovers Slowly, and China’s Economy has Maintained

Steady Performance and Made Positive Advances

79

The global economy recovers slowly. International Monetary Fund (IMF) forecasts that global GDP growth rate is expected to rise from 3.1% in 2016 to 3.4% in 2017. However, emergence of trade protectionism and accumulation of geopolitical conflict risk factors makes the global economy face with more risks. US economy grew well. In May 2017, the US Markit manufacturing PMI registered 52.7, and the US service industry PMI registered 53.6. Unemployment rate of the United States fell to a 16-year low of 4.3%; core CPI registered 1.7%

The Chinese economy shows an overall stable performance with good momentum for growth. In the first five months, Chinese economy showed four characteristics: stable production and demand, continuously improving employment, moderate inflation, and improved international balance of payments. Total retail sales of consumer goods increased by 10.7%, remaining as the main engine of economic growth. Growth rate of fixed asset investment registered 8.6%, higher than last year’s annual growth rate of 8.1%. As for external demand, exports in May increased by 15.5%, 1.2 percentage points higher MoM. In the first five month, the number of newly increased urban jobs was 5.99 million, completing 54.4% of the annual target in this regard; and the unemployment rate was less than 5%. CPI rose moderately by 1.5% YoY, up 0.3% MoM. In May, trade surplus totaled RMB 281.6 billion. Foreign currency reserves rebounded for four consecutive months, reaching US$ 3,053.6 billion at the end of May. The exchange rate is basically stable

Monetary Policy of China is “Steady and Neutral”, and Financial Regulation

Pays More Attention on Risk Prevention

80

Monetary Policy for the US presents a combination of “interest rate increase + balance sheet reduction”. On June 15, the Federal Reserve increased interest rate by 25bp to 1.25%, and increased discount rate by 25bp to 1.75%. The Fed restated that it expected that the economy would guarantee FOMC’s steady rate hike. Meanwhile, it is expected that reduction of balance sheet will start in 2017

Monetary Policy of China is “Steady and Neutral”, but tightening in essence. Firstly, interest rate increase of USA poses a pressure on China’s exchange rate and foreign exchange reserves. Secondly, China’s economy growth has provided space for tightening of monetary policy. Thirdly, risk prevention and deleveraging becomes the emphasis of the central government

A series of financial regulation policies have been adopted for deleveraging. The Central Bank has raised the policy rates: On January 24, 2017, the Central Bank raised MLF rates by 10bp, and on February 3, 2017, it increased reverse repo rates by 10bp, which was the first time to raise policy rates since 2012. The CBRC deleveraged in the banking system, and issued documents to remove chaotic phenomenon of "three violations", "three arbitrages" and "four misconducts", so as to restrain asset bubbles. The CIRC issued the important "1 + 4" series of documents to strengthen risk prevention, intensify regulation, crack down illegal activities, regulate market chaos, and to maintain steady and healthy industrial development

Strategy for Bond Investment in 2017: Increase Allocation and Optimize

Structure

81

Increase debt investment allocation. The yield to maturity of domestic and overseas bonds rise, and the allocation value has been obviously improved compared with that in the last year. Enlarge the allocation proportion of bond asset

Optimize debt allocation structure. Optimize maturity structure, grasp the trend of yield curve, make proper allocation of long, medium and short duration, and effectively cope with fluctuation of interest rate; improve credit structure, make proper allocation of national debts and corporate debts with different credit level, and take efforts to increase investment yield; optimize accounting structure, make proper allocation of held-to-maturity and available-for-sale bond, and balance requirements for book yield and the market value yield requirements

Take strict precautions against credit default risk. Regularly check existing bond investment, and take strict precautions against credit default risk. Perform credit review and risk investigation selectively in terms of credit rating, industrial distribution and regional distribution, develop an emergency response plan, implement accountability, and enhance post-investment management and auditing

82

Under the new accounting standard, if the equity instrument is included in “Fair value through other comprehensive income (FVOCI)”, the book yield will be systematically undervalued relative to the market value yield for a long term since “the income and loss is maintained in other comprehensive income (i.e. re-classification not available)”. Hence, most of the equity instruments will be included in “Financial liabilities measured at fair value and whose movements are included in the profit and loss of the current period (FVPL)

Adhere to value investment philosophy. The stock allocation style will change obviously when the fair value change is included in the profit and loss of the current period. More importance will be attached to value investment, long term investment, prudent investment, and blue chip stocks with good fundamentals, strong profitability and high dividend level

Seize opportunities for long term equity investment. Give full play to advantages of large volume, stable supply and long term of insurance funds, and seize opportunities for long term equity investment in the listed and non-listed companies with good profitability and dividends payment capacity. Under the premise of friendly cooperation, make efforts to realize accrediting at board of directors and equity method accounting, and obtain stable and sound investment yield

Strategy for Stock Investment in 2017: Adhere to Value Investment, and

Seize Opportunities For Long Term Equity Investment

Strategies for Alternative and Real Estate Investment in 2017: Follow National

Strategies and Grasp Key Points of Investment

83

Alternative Investment should actively respond to national strategies, and support industry transformation and upgrading. Firstly, give full play to advantages of integrated financial layout and cross-border business of the Group, and keep in line with “the Belt and Road” strategy, coordinated development of Beijing, Tianjin and Hebei Province, and the Yangtze River Economic Belt development strategy in multiple manners. Secondly, actively invest in major national infrastructures, significant livelihood projects and new type urbanization, energetically serve China capital enterprises to “going globally” and overseas customers, and strive to become important ties for cross-border investment and financing cooperation. Thirdly, Seek quality targets in senior service, health service, medical treatment service, automobile industry chain and other segments by virtue of the core insurance business of the Group

Real estate investment should keep in step with the national policies, and pay close attention to regional opportunities. Domestically, focus on regions with significant development potential in future, e.g. Xiongan New District, Guangdong-Hongkong-Macau Greater Bay Area, Qianhai Shenzhen-Hong Kong Modern Service Industry Cooperation Zone, and China (Hangzhou) Cross-border E-commerce Comprehensive Pilot Area. Mature properties in developed countries and regions with active transaction are the main focus of overseas real estate investment

Strengthen building of credit rating ability. Accelerate establishment of the unified credit rating center of the Group, and further intensify the overall credit rating ability of the Group

Enhance investigation of existing asset risk. Set up a post-investment risk early-warning mechanism combining on-site inspection and off-site supervision, regularly track and inspect the investment projects, and organize special investigation for various risks on an unscheduled basis. Lay emphasis on penetration type management, and discover, cope with and solve the risks as early as possible. Results for investigation of Alternative projects, credit debt and finance rent showed that capital was invested prudently and steadily, comply with regulations, asset quality is sound, and total risk is under control

Optimize investment risk disposal mechanism. For projects with potential risk, stick to the principle of “one company one policy”. Implement credit enhancement by guarantee and pledge, increasing backed asset, improving obligations of guarantor or re-purchase person, seeking government support. Perform investment risk disposal by taking actions of investment halting, asset preservation, requesting the guarantor or re-purchase person to execute responsibilities, legal action and others

84

Investment Protection Measures in 2017: Establish a risk prevention and

management system covering pre-investment, in-process and post-

investment stages

China Taiping

—Featured Highlights

85

• Impacts of Interest Rate Upside Environment and Countermeasures

Featured Highlights

86

Flat Upside Trend of Yield Curve

87

数据来源:wind资讯

2017-5-31 2016-6-30

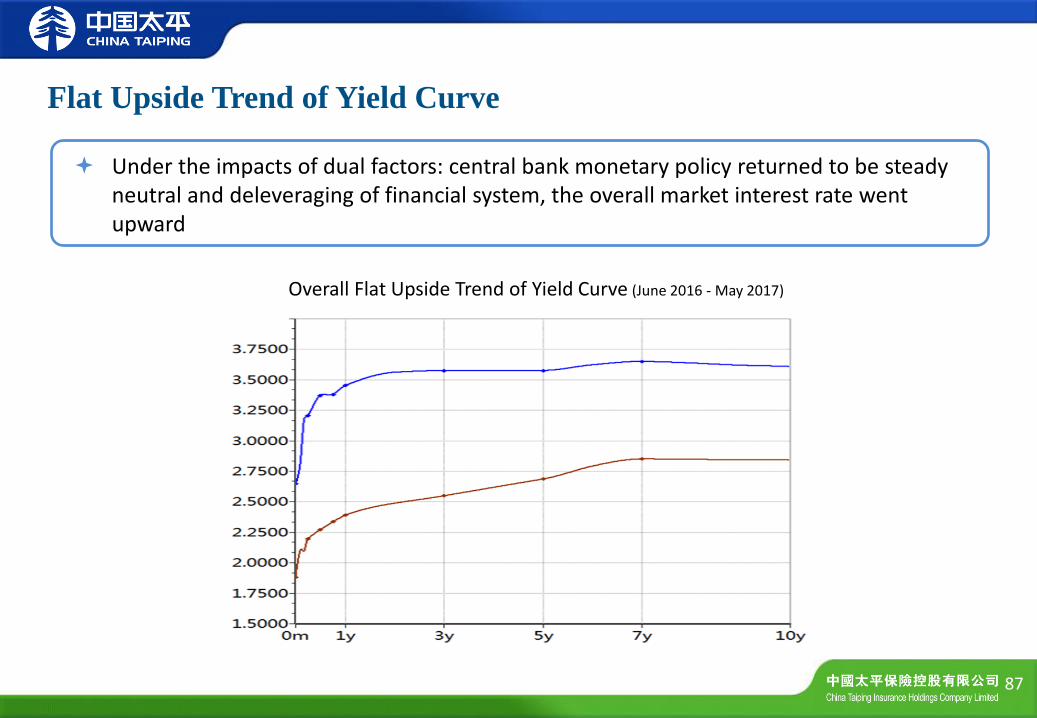

Under the impacts of dual factors: central bank monetary policy returned to be steady neutral and deleveraging of financial system, the overall market interest rate went upward

Overall Flat Upside Trend of Yield Curve (June 2016 - May 2017)

1.5

2.0

2.5

3.0

3.5

4.0

中债国债到期收益率:1年 中债国债到期收益率:10年 Yield to Maturity of China Bond

Treasury Bond: 1-year Yield to Maturity of China Bond Treasury Bond: 10-year

Flat Upside Trend of Yield Curve

88

2.0

2.5

3.0

3.5

4.0

4.5

5.0

5.5

2016-0

1

2016-0

2

2016-0

3

2016-0

4

2016-0

5

2016-0

6

2016-0

7

2016-0

8

2016-0

9

2016-1

0

2016-1

1

2016-1

2

2017-0

1

2017-0

2

2017-0

3

2017-0

4

2017-0

5

银行间质押式回购加权利率:7天 中债国开债到期收益率:5年 Weighted Interest Rate of Interbank Pledge-style Repo: 7-day

Yield to Maturity of China Bond Treasury Bond: 5-year

However, as real economy was still weak, yield to maturity of long-term bond rose to a limited extent, the yield curve became more flat, and term spread narrowed significantly

Term Spread Narrowed Significantly (10-year Treasury Bond – 1-year Treasury Bond Yield)

Interest Rate Volatility Increased, and Repo Rate was Sometimes Higher than Interest Rate of 5-year CBD Bond

Credit Spread Widened Significantly

89

0.4

0.6

0.8

1.0

1.2

1.4

1.6

Overall upside of interest rate and lower risk appetite of institutional investors made credit spread of AAA corporate bond yield and treasury bond yield widen significantly, which was beneficial for improving the return of insurance fund

The Overall Upward Trend in Interest Rates, Coupled with Lower Risk Appetite, Resulted in a Significant Increase in Credit Spreads

(Yield of 10-year AAA Corporate Debt - Treasury Bond)

The Impacts of Current Interest Rate Environment and Countermeasures

90

The overall impact of interest rate upside on insurance company was positive. It was mainly because that the liability duration is longer than asset duration in insurance companies. In the interest rate upside cycle, return on reinvestment at maturity was high, and interest spread improves

In early stage of interest rate upside, it had some impacts on the balance sheet for insurance company. These impacts mainly included that 750-day moving average for the yield of treasury bond, which is applicable for calculating reserve, was still lowering, reserve provisioning was still increasing, while fair value of available-for-sale existing bond was decreasing. But such impacts will change from negative to positive in the late stage of interest rate upside

The impacts on income statement for insurance company will be both positive and negative, which will be dominated by positive impact on the whole. The reserve provision on liability side is likely to increase, but yield of held-to-maturity fix income assets for new money will rise. Decrease in the fair value of available-for-sale assets is only recognized in “Other Consolidated Gains And Losses” in balance sheet rather than be recognized in income statement

The Impacts of Current Interest Rate Environment and Countermeasures

(Con’d)

91

Grasp opportunities from high volatility of market interest rates, and allocate at peak points. Improve the forecasting ability for interest rate trends, grasp the inflection point in short-term trend and long-term trend, increase the allocation proportion of held-to-maturity assets with new and reinvesting funds, and icrease investment income.

Build a balanced term structure, and make comprehensive balancing of current income and long-term value. On the basis of accurate judgment on the mid/long-term interest rate trends, make preparation for proper term structure of fix income assets, and avoid the allocation of excessive long-term bonds under the pursuit of short-term book profits in early stage of the interest rate upside

Flexibly adjust credit structure of fix income assets, and increase investment income. Take advantage of the characteristics of rising credit spreads, and make reasonable adjustment for credit distribution of the bonds above investment rating. Appropriately allocate in credit debt and increase investment income on the basis of further strengthening of the Group's credit risk prevention capacity

Thank you !

92

• Implication of IFRS 9 & IFRS 17

Featured Highlights

93

1. IFRS9 and IFRS17

94

IFRS9-Financial Instruments: 2014 issued, effective on 1 Jan 2018

Insurance companies which meet the requirements could delay the execution of

IFRS 9 to 2021

On 31 Mar 2017, MOF of PRC issued three CAS for financial instruments. As with

IFRS, insurance companies which meet the requirements could delay the execution

to 2021

IFRS17-Insurance Contracts: 2017 issued, effective on 1 Jan 2021

When will CAS of insurance contracts be issued?

2.1 IFRS9 Category: How to Classify

95

Could financial assets be classified as below if our purpose and intention of holding the assets are unchanged:

HFT FVPL All assets

AFS

FVOCI

LAR

HTM AMC All assets

2.2 IFRS9 Category: Considerations for Classification

96

Increase volatility in P/L if to classify the financial assets as FVPL

AMC classification requirements

Implications on the A/L match in F/S

Implications on capital solvency

Certain AFS have to be classified as FVPL

2.3 IFRS9 Classification: Equity Instruments

97

Equity instruments are measured at fair value

“FVOCI-equity instruments”: Given low dividend yield ratio, how to

meet equity investment’s high return expectation in P/L?

When equity instrument investments could not be exempted from the

cost measurement, how to evaluate FV of the non-listed equity

investments reasonably?

2.4 IFRS9 Classification: Debt Instruments

98

Debt instrument investments: the business model and the contractual

cash flow characteristics for FVOCI and AMC should be assessed

Some structured and non-standard investments may need to be

classified as FVPL

When requirements met, FVOCI would be preferred classification for

P/L and A/L measurement

2.5 IFRS9 Impairment: Single Model

99

Impairment for non-FVPL debt instrument only, with Single Expected Credit Loss Model

Investment return and performance evaluation:impairment recognition timing, 12-month expected loss and life cycle expected credit loss

“FVOCI-debt instruments”recognize the impairment provision, and the profit/loss on the impairment is recognized in current period’s income statement

2.6 IFRS9 Impairment: Expected credit loss model

100

Difficulties in building up expected credit loss model

Information & data on the macro-economic forecast

Low asset amounts, transaction volume and data fineness

Insurance companies lack complete credit risk structure, control

process and historical data, unlike banks

2.7 IFRS17 Implications: Information Providers and Users

101

Information providers

Different F/S users

Comprehensive Income Statement

Insurance contract revenue X

Losses and expenses (X)

Underwriting profit X

Investment income X

Insurance financial income (X)

Investment profit X

Other profit X

Income tax (X)

Profit after tax X

Other comprehensive income (X)

Comprehensive income X

2.8 IFRS17 Implications: Professional Judgment and Earning

Management

102

No shadow accounting, changes in actuarial estimate (non-market) adjust to CSM instead of P/L

Should effect of changes in discount rate and other financial risks go to P/L or OCI?

Financial assets and insurance contractual liabilities are not matched: discount rate changes, market price fluctuation, timing difference on the recognition of assets and liabilities changes

Implications of actuarial assumptions & IFRS17 transitions

2.9 IFRS9 and IFRS17: ALM and Solvency

103

Financial asset classification and liability measurement affect NAV、P/L and ALM

Under C-ROSS, financial asset classification affect actual capital & minimal capital, C-ROSS rules should be revised

If IFRS9 and IFRS17 are not implemented simultaneously, asset/liability’s measurement and ALM would be more difficult

2.10 IFRS9 and IFRS17 Implications: Others

104

Asset reclassification’s impact on the strategic assets allocation and capital market

Social intermediaries and media

Small companies how to implement

Knowledge and technical skills for the insurance companies' financial staff

3.1 How to Implement

105

Seek for understanding and support: company’s senior management and outside consultancy firms

Form the implementation team: classification and measurement, insurance contract, impairment model, and IT system

Knowledge sharing: knowledge and technical training

Expertise selection and training: actuary, investment, IT and financial compound talents

Financial statement parallel disclosure: financial statement and tax report, regulatory report and internal management report

3.2 Implementation Time: the Year of 2021

106

Analysis, assessment and planning

Project teams formation: include the below sub-teams in 2018:

(1) Asset classification and measurement (2) Asset impairment model (3) Insurance liabilities measurement (4) Information system reform

Implementation and improvement: process and information systems update in 2019 and 2020, and implementation in 2021

Thank you !

107

Q&A

108