CHAPTER 21 Independent Power Projects in Sub...

30

A t the beginning of the 1990s, virtually all major power generation providers in Sub-Saharan Africa were financed by public coffers, including concessionary loans from development finance institutions (DFIs). These publicly financed power generation assets were considered one of the core elements of state-owned, vertically integrated power systems. A confluence of fac- tors, however, brought about a significant change in the ensuing years. With insufficient public funds for new power generation and decades of poor performance by state-run utilities, African countries began to adopt a new model for their power systems, influenced by pioneering reformers in Chile, Norway, the United Kingdom, and the United States. 1 Urged on by multilateral and bilateral develop- ment institutions, which were withdrawing funding from state-owned projects, a number of countries adopted plans to unbundle their power systems and introduce pri- vate participation and competition. Independent power projects (IPPs)—privately financed, greenfield generation supported by nonrecourse or limited-recourse loans and with long-term power purchase agreements (PPAs) with the state utility or another off-taker—thus became a pri- ority in overall power sector reform (World Bank 1993; World Bank and USAID 1994). IPPs were considered a solution to persistent supply constraints, and they also 371 Independent Power Projects in Sub-Saharan Africa: Determinants of Success Anton Eberhard and Katharine Nawal Gratwick CHAPTER 21 had the potential to benchmark state-owned supply to gradually introduce competition (APEC Energy Working Group 1997). In 1994 Côte d’Ivoire became one of the first African countries to attract a foreign-led IPP to sell power to the national grid under long-term contracts with the state util- ity. Ghana, Kenya, Nigeria, Senegal, Tanzania, and Uganda, among others, opened their doors to foreign and local investors in their power sectors shortly thereafter. Although IPPs were considered part of larger power sec- tor reform programs in Sub-Saharan Africa, the reforms were not far-reaching. In most cases, state utilities remained vertically integrated and maintained a dominant share of the power generation market, while private investors were allowed to operate only on the margin of the sector. 2 Policy frameworks and regulatory regimes, necessary to maintain a competitive environment, were limited. International com- petitive bids (ICBs) for IPPs were often not conducted because of tight time frames, resulting in limited competi- tion for the market and, because of the long-term PPAs, no competition in the market. These long-term PPAs, along with government guarantees and security arrangements such as escrows and liquidity facilities, exposed countries to significant exchange rate risks. Finally, while Africa has seen continued private participation in greenfield electricity proj- ects, that progress has been erratic, with 2007 representing Anton Eberhard is a professor and Katharine Nawal Gratwick is a PhD graduate at the University of Cape Town Graduate School of Business.

Transcript of CHAPTER 21 Independent Power Projects in Sub...

At the beginning of the 1990s, virtually all majorpower generation providers in Sub-SaharanAfrica were financed by public coffers, including

concessionary loans from development finance institutions(DFIs). These publicly financed power generation assetswere considered one of the core elements of state-owned,vertically integrated power systems. A confluence of fac-tors, however, brought about a significant change in theensuing years.

With insufficient public funds for new power generationand decades of poor performance by state-run utilities,African countries began to adopt a new model for theirpower systems, influenced by pioneering reformers inChile, Norway, the United Kingdom, and the UnitedStates.1 Urged on by multilateral and bilateral develop-ment institutions, which were withdrawing funding fromstate-owned projects, a number of countries adoptedplans to unbundle their power systems and introduce pri-vate participation and competition. Independent powerprojects (IPPs)—privately financed, greenfield generationsupported by nonrecourse or limited-recourse loans andwith long-term power purchase agreements (PPAs) withthe state utility or another off-taker—thus became a pri-ority in overall power sector reform (World Bank 1993;World Bank and USAID 1994). IPPs were considered asolution to persistent supply constraints, and they also

371

Independent Power Projects in Sub-Saharan Africa: Determinants of SuccessAnton Eberhard and Katharine Nawal Gratwick

C H A P T E R 2 1

had the potential to benchmark state-owned supply togradually introduce competition (APEC Energy WorkingGroup 1997).

In 1994 Côte d’Ivoire became one of the first Africancountries to attract a foreign-led IPP to sell power to thenational grid under long-term contracts with the state util-ity. Ghana, Kenya, Nigeria, Senegal, Tanzania, and Uganda,among others, opened their doors to foreign and localinvestors in their power sectors shortly thereafter.

Although IPPs were considered part of larger power sec-tor reform programs in Sub-Saharan Africa, the reformswere not far-reaching. In most cases, state utilities remainedvertically integrated and maintained a dominant share ofthe power generation market, while private investors wereallowed to operate only on the margin of the sector.2 Policyframeworks and regulatory regimes, necessary to maintain acompetitive environment, were limited. International com-petitive bids (ICBs) for IPPs were often not conductedbecause of tight time frames, resulting in limited competi-tion for the market and, because of the long-term PPAs, nocompetition in the market. These long-term PPAs, alongwith government guarantees and security arrangementssuch as escrows and liquidity facilities, exposed countries tosignificant exchange rate risks. Finally, while Africa has seencontinued private participation in greenfield electricity proj-ects, that progress has been erratic, with 2007 representing

Anton Eberhard is a professor and Katharine Nawal Gratwick is a PhD graduate at the University of Cape Town Graduate School of Business.

the zenith, largely because of the financial close of one largeproject, Bujagali.

Several factors explain the recent trends in investmentin Africa’s power sector. First, private sector firms weredeeply affected by the Asian and subsequent Latin Ameri-can financial crises in the late 1990s and early 2000s. TheEnron collapse and its aftershocks also influenced U.S.-and European-based firms to reduce risk exposure indeveloping-country markets and to refocus on core activi-ties at home. The financial crisis of 2008 and 2009 has alsohad a toll. Furthermore, DFIs began to reconsider theirposition of restricted infrastructure investment, a modelthat was predominant throughout the 1990s.3 As conces-sionary funding became available again, many countriesopted for a hybrid solution—part public, part private.Kenya represents one of the clearest examples of such ahybrid, with KenGen, the state-owned generator, buildingalongside IPPs, with support from DFIs.

Despite this revival of concessionary lending, powersector investments have been insufficient in addressingSub-Saharan Africa’s power needs. Only 25 percent of thepopulation currently has access to electricity, and poorsupply is the rule, not the exception. The cost of meetingAfrica’s power sector needs is estimated at $40.8 billion peryear, equivalent to 6.35 percent of Africa’s 2005 grossdomestic product (GDP). Approximately two-thirds of thespending needed is for capital investment ($26.7 billionper year), and the remainder for operations and mainte-nance (O&M). Current spending on power infrastructuretotals approximately $11.6 billion per year. Approximately80 percent of existing spending is domestically sourcedfrom taxes or user charges. The remainder is split amongofficial development assistance (ODA) financing (6 percentof the total); other sources, mainly China (9 percent); andprivate sector investment (4 percent). Tackling existing util-ity inefficiencies, including system losses, underpricing,undercollection of revenue, and overstaffing, would makean additional $8.24 billion available, but a funding gap ofabout $21 billion would still remain (Eberhard andShkaratan 2010).

Closing Africa’s power infrastructure funding gapinevitably requires undertaking reforms to reduce or elimi-nate system inefficiencies. This will help existing resourcesgo farther and create a more attractive investment climatefor external and private finance, which still has growthpotential. With the original drivers for market reform stillpresent, future private sector involvement appears inevitable.

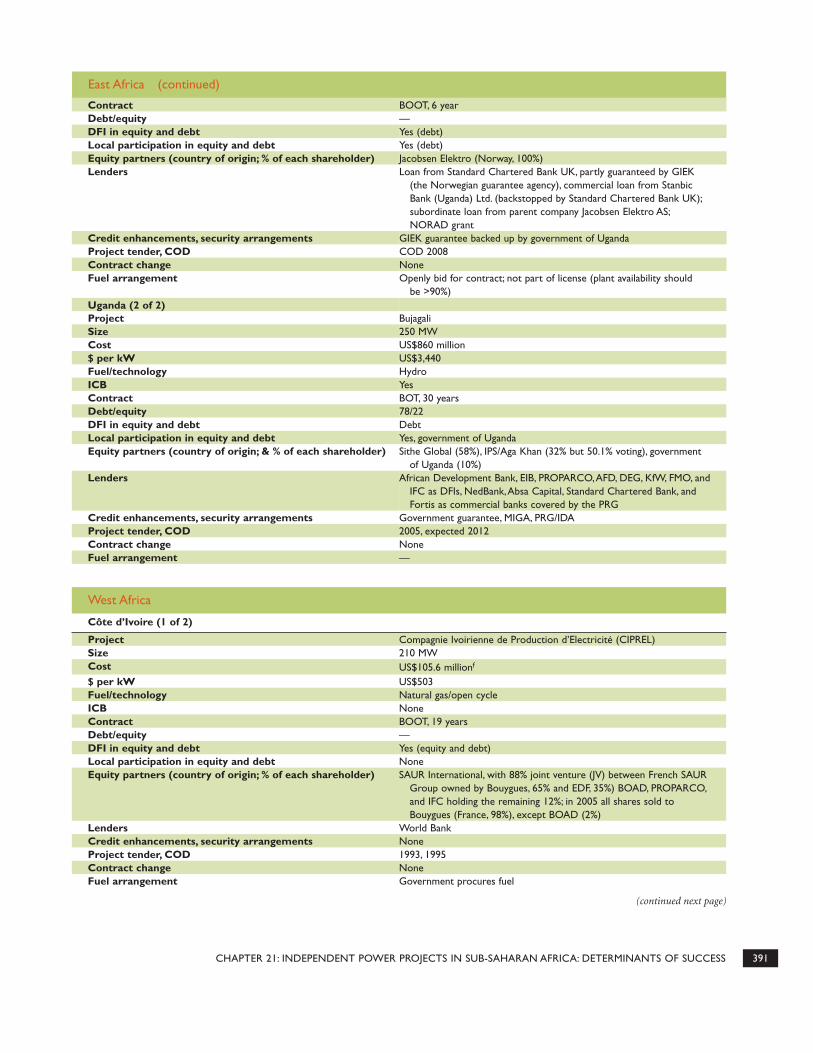

Approximately 20 grid-connected IPPs, each in excess of40 megawatts (MW) and with long-term PPAs with the

largely state-run utilities, have been developed in Sub-Saharan Africa as of early 2010 (table 21.1). In total, aboutfour gigawatts (GW) of IPP capacity has been added. Withfew exceptions,4 these IPPs represent a small fraction oftotal power generation capacity and have mostly comple-mented incumbent state-owned utilities.

Nevertheless, IPPs are an important source of newinvestment in the power sector in a number of Africancountries. In Togo, for example, Centrale Thermique deLomé, the country’s first IPP, will triple the country’sinstalled capacity.

The majority of IPP contracts in Sub-Saharan Africahave been upheld (namely, CIPREL and Azito in Côted’Ivoire, Takoradi II in Ghana, Iberafrica, Tsavo, OrPower 4,and Rabai in Kenya, Afam VI and Aba Integrated in Nigeria,and Namanve in Uganda). Although the contracts of thetwo Senegalese projects, GTi Dakar and Kounoune I, remainlargely intact, there are reports of changes in fuel supplyarrangements. A number of other IPPs, such as Bui Hydroin Ghana, Bujagali in Uganda, and Centrale Thermique deLomé in Togo, have reached financial closure and are underconstruction.5 Kenya is in the process of negotiating threemore IPPs after an international competitive tender.

For all of this progress, however, there have been sev-eral high-profile IPP mishaps in Sub-Saharan Africa. Twoprojects—AES Barge in Nigeria and Independent PowerTanzania Limited (IPTL) in Tanzania—are in arbitration.The costs of Songas, in Tanzania, meanwhile, haveescalated as a result of the unplanned, and later disputed,contracting of IPTL; Songas’s capacity charges were laterreduced after the government agreed to buy down theaccumulated allowance for funds used during constructioncosts. A dispute about escalating investment costs alsomarked the Okpai project in Nigeria. In Kenya changesmay be made in the contracts of OrPower 4, whichreduced its tariff for the second phase of the plant.Another Kenyan project, Westmont, had an initial seven-year contract that was not renewed. The other early IPP inKenya, IberAfrica, had its contract renewed but withmuch lower capacity charges.

Following contract changes, IPPs have generally gone onto make a significant contribution to the countries’ powergeneration—the main exceptions being Westmont, whichceased operation, and IPTL, which has operated intermit-tently during its arbitration proceedings. Another high-profile failure was the nontransparent procurement processsurrrounding the Richmond/Dowans plant in Tanzania,which has not been allowed to operate since corruptioncharges were filed. Furthermore, there is evidence of stalling

372 CHAPTER 21: INDEPENDENT POWER PROJECTS IN SUB-SAHARAN AFRICA: DETERMINANTS OF SUCCESS

373

Tabl

e 21

.1G

ener

al P

roje

ct S

peci

ficat

ions

of S

ub-S

ahar

an A

fric

an IP

P Pr

ojec

ts

Co

untr

y/pr

oje

ctS

ize

(MW

)F

uel/c

ycle

Co

ntra

ct t

ype

Len

gth

of

cont

ract

(ye

ars)

Pro

ject

ten

der

Co

mm

erci

alo

pera

ting

dat

a

Eas

t A

fric

aK

enya

Wes

tmon

t46

Ker

osen

e/ga

s co

nden

sate

/gas

Tur

bine

(ba

rge-

mou

nted

)BO

O7

1996

1997

Iber

afri

ca10

9aH

FO/m

ediu

m-s

peed

die

sel e

ngin

eBO

O7/

15/2

519

96,1

999,

2008

1997

,200

0,20

09O

rPow

er 4

48G

eoth

erm

alBO

O20

1996

2000

,200

9T

savo

75H

FO/m

ediu

m-s

peed

die

sel e

ngin

eBO

O20

1995

2001

Rab

ai90

HFO

BOO

T20

2006

2009

Tanz

ania

IPT

L10

0H

FO/m

ediu

m-s

peed

die

sel e

ngin

eBO

O20

1997

1998

Song

as18

0N

atga

s/op

en c

ycle

BOO

2019

9420

04U

gand

aN

aman

ve

50H

FOBO

OT

6—

2008

Buja

gali

250

Hyd

roBO

T30

2005

b—

Wes

t A

fric

aC

ôte

d’Iv

oire

CIP

REL

210

Nat

gas/

open

cyc

leBO

OT

1919

9319

95A

zito

288c

Nat

gas/

open

cyc

leBO

OT

2419

9620

00G

hana

Tako

radi

II22

0dLi

ght

crud

e/si

ngle

cyc

leBO

OT

2519

9820

00Su

non

Aso

gli

200

Com

bust

ion

engi

neBO

O20

2007

—

Bui H

ydro

e40

0H

ydro

BOO

—20

05—

Nig

eria

AES

Bar

ge27

0N

atga

s/op

en c

ycle

(ba

rge-

mou

nted

)BO

O20

(2

part

s)19

9920

01O

kpai

450

Nat

gas/

com

bine

d cy

cle

BOO

2020

0120

05A

fam

VI

630

Nat

gas/

com

bine

d cy

cle

BOO

2020

0020

07

Aba

Inte

grat

edf

140

Nat

gas/

open

-cyc

le

BOO

20/1

520

05—

Sene

gal

GT

i Dak

ar

52D

iese

l/Naf

taBO

OT

1519

9619

99K

ouno

une

I 68

HFO

BOO

1520

0320

08To

go Cen

tral

e T

herm

ique

de

Lom

é10

0Tr

iple

fuel

(na

tgas

/HFO

/die

sel)

BOO

T25

—20

10

Sour

ce:A

uth

ors.

Not

e:P

roje

cts

incl

ud

ed h

ere

are

grea

ter

than

40

MW

;hav

e re

ach

ed fi

nan

cial

clo

se;a

nd

are

un

der

con

stru

ctio

n,o

per

atio

nal

,or

con

clu

ded

.BO

O =

bu

ild

-ow

n-o

per

ate

con

trac

t;B

OO

T =

bu

ild

-ow

n-

oper

ate-

tran

sfer

con

trac

t;H

FO =

Hea

vy f

uel

oil

.— =

Not

ava

ilab

le.

a.Ib

eraf

rica

has

bee

n d

evel

oped

in t

hre

e st

ages

,wit

h 4

4,12

an

d 52

.3 M

W,t

otal

ing

109

MW

at

tim

e of

wri

tin

g.b.

Th

e fi

rst

phas

e of

Bu

jaga

li’s

con

cept

ual

izat

ion

,spa

nn

ing

the

mid

-199

0s u

nti

l 200

3 an

d in

volv

ing

AE

S,is

not

cov

ered

in

th

is a

rtic

le.I

t sh

ould

be

not

ed t

hat

th

e pr

ojec

t di

d n

ot r

each

fin

anci

al c

lose

duri

ng

this

tim

e.A

uth

ors

repo

rt o

nly

on

th

e pr

ojec

t fr

om it

s se

con

d ph

ase,

star

tin

g in

200

5.c.

Th

e in

itia

l pro

ject

con

cept

incl

ude

d sp

ecif

icat

ion

s to

rai

se c

apac

ity

to 4

20 M

W.

d.A

lth

ough

th

e in

itia

l pro

ject

con

cept

incl

ude

d sp

ecif

icat

ion

s to

add

a s

econ

d ph

ase

of11

0 M

W a

nd

conv

ert

to c

ombi

ned

cyc

le,l

ack

offu

ndi

ng

has

lim

ited

th

e co

mpl

etio

n o

fth

is p

has

e.e.

Th

e B

ui

proj

ect

was

in

itia

ted

in t

he

1960

s bu

t ab

orte

d af

ter

the

cou

p in

Gh

ana

in 1

966.

Th

e pr

ojec

t w

as r

econ

side

red

seve

ral t

imes

in

th

e de

cade

s th

at f

ollo

wed

.In

200

5 th

e go

vern

men

t of

Gh

ana

sign

ed a

mem

oran

dum

of

un

ders

tan

din

g w

ith

th

e C

hin

ese

firm

Sin

o H

ydro

,an

d th

e pl

ant

is e

xpec

ted

to b

e on

line

in 2

012.

f.A

ba I

nte

grat

ed is

pri

vate

ly f

inan

ced

but

is n

ot a

cla

ssic

IP

P in

th

at o

wn

ersh

ip w

ill e

xten

d to

th

e of

f-ta

ker.

in Takoradi II’s second phase and in Sunon Asogli, which asof early 2010 had no gas supply—although efforts to rectifythis situation are under way.

COUNTRY-LEVEL FACTORS AFFECTING THE IPP MARKET

Several elements have contributed to the success of IPPprojects in Sub-Saharan Africa: a favorable investment cli-mate; new policy frameworks and regulation; the linking ofplanning, procurement, and contracting; and low-cost fueland secure fuel contracts.

Favorable investment climate

Even though a investment climate is not the only factor ininfluencing IPP outcomes, it sets the stage for negotia-tions and contract terms and helps explain the initialimbalance in some of the Sub-Saharan African cases. Hostcountries with a strong investment profile attracted moreinvestors and ultimately were able to negotiate deals withmore favorable terms than countries with weak invest-ment conditions. Because all countries and entities com-pete for capital, a risk-reward balance needs to be offeredthat will attract investors and lenders. That “balance”starts with a stable and predictable investment environ-ment (Rudo 2010a).

Of the Sub-Saharan countries whose IPPs are examinedin this chapter, none has an investment-grade sovereigncredit rating. Of the five countries that have received a spec-ulative rating (Ghana, Kenya, Nigeria, Senegal, and Uganda),all except Ghana received their rating after the first IPPdeals were signed. Kenya’s investment climate was defined, atthe time, by its aid embargo in the mid-1990s. Tanzania is alsoworth mentioning in this context. Throughout the 1990s, allexport credit agencies were off-cover in Tanzania. Foreigncommercial banks were not willing to lend, because therewas no track record of successful repayment of commercialloans. Consequently, traditional, project-financed IPP dealsin this climate were limited. In contrast in North Africa, theArab Republic of Egypt, Morocco, and Tunisia have allattained either a credit rating of investment grade or onenotch below and have experienced successful IPPs(Gratwick and Eberhard 2008a). While credit enhance-ments and security arrangements have differed broadlybetween North and Sub-Saharan Africa, interestingly,incentives offered to investors in IPPs were relatively similarin both regions, though there was some variety with regardto tax breaks. For instance, nearly all projects appear to have

benefited from both customs and value added tax (VAT)exemptions during construction, as well as the right to fullrepatriation of profits. Currency conversion was also pro-vided for virtually all projects. In East Africa, Tanzania pro-vided a tax holiday of five years, but Kenya extended thisbenefit only until plants were commissioned. Althoughone would expect investment incentives to increase withperceived risk, such a pattern is not apparent.

New policy frameworks and regulation

While all eight Sub-Saharan African countries examined inthis chapter have introduced legislation allowing for pri-vate sector power generation, few have actually formulatedand implemented a clear and coherent policy frameworkfor procuring IPPs. Thus, there is abundant evidence oftentative experimentation with private power that doesnot always lead to a sustained opening of the market forprivate investment. Furthermore, long-term power pur-chase agreements have the potential to constrain futurewholesale competition, although means to transition towholesale competition with IPPs have been identified(Woolf and Halpern 2001). In addition, state-owned utili-ties are rarely exposed to market costs of capital, and directcomparisons of state-owned utilities’ costs and IPPs’ costsare often difficult to discern.

The standard reform model for power sector reform—namely, unbundling of generation, transmission, and dis-tribution; as well as the introduction of competition andprivate-sector participation at both the generation anddistribution level—is not being fully adopted anywhere inSub-Saharan Africa (UNEP and UNECA 2006; Malgras,Gratwick, and Eberhard 2007a; Gratwick and Eberhard2008b). Most incumbent national utilities are state-owned6

and in a dominant position. However, elements of thereform model have been adopted: for example, Kenya hasunbundled power generation from its national transmissionand distribution utility; Uganda and Ghana have unbun-dled generation, transmission, and distribution; andUganda and Côte d’Ivoire have introduced private conces-sions. The private sector has also invested in IPPs in manycountries. In general, there has been competition for themarket, but not ongoing competition in the market interms of customer choice. In effect, hybrid power marketshave emerged across Africa, and in other developingregions. As such, the incumbent state-owned utility typi-cally continues to play a key role in the sector, but becauseof inefficiencies and inadequate investment resources, IPPsare gradually being introduced. These hybrid power

374 CHAPTER 21: INDEPENDENT POWER PROJECTS IN SUB-SAHARAN AFRICA: DETERMINANTS OF SUCCESS

markets are giving rise to new challenges that need explicitattention if private investment is to be accelerated.

In addition to introducing legislation allowing for pri-vate power generation, the eight countries examined in thischapter also have established independent regulators. InKenya the presence of the regulator, together with the adop-tion of International Competition in Bidding (ICB) prac-tices, helped reduce PPA charges radically between the firstset of IPPs and the second. A similar trend may be observedin Senegal, where the first IPP (GTi Dakar) was not overseenby the independent regulatory body and the second (Kou-noune I) was (Regulatory Commission of Senegal 2010; IFC2010b). Kenya’s Energy Regulatory Commission (ERC) hasalso been instrumental in helping set tariffs and manage theoverall interface between private and public sectors. InUganda sponsors note the benefits of having the regulatorinvolved from project inception, particularly in helping toincrease overall transparency, especially in the case ofBujagali. An ERC staff member affirms that the commis-sion’s “presence has helped to focus minds on the require-ments for setting up power supply projects so that investorscoming in are clear of what is expected of them from thebeginning and hence align their bids to these require-ments. As a result, we have increasing numbers of investorsapplying to set up IPP projects” (ERC 2010a).

In Côte d’Ivoire, Ghana, Nigeria, and Tanzania, however,regulatory agencies have come into force only after IPPshave been negotiated, and as yet the agencies have had littleimpact on new investment. In general, the mere presence ofa regulator does not appear to be a defining factor in attract-ing IPPs. An independent regulator may have positive, neg-ative, or no impact on IPP outcomes. If, however, regulatorygovernance is transparent, fair, and accountable, and if reg-ulatory decisions are credible and predictable, there isgreater potential for positive outcomes for both the hostcountry and investor alike. Evidence also suggests that effec-tive regulatory oversight may lead to a reduction in thestated capital costs of projects and improved efficiency forselectively bid projects (Phadke 2007; Eberhard andShkaratan 2010).7

In Nigeria and Tanzania efforts have been made toexploit stranded gas as part of the IPP program.8 In Nigeriaa reduction in gas flaring is central to the push for gas-firedpower, while in Tanzania the IPP program commercializedpreviously stranded (although not flared) gas throughSongas and Mtwara (a small private concession in the southof the country). Although these two countries have a dis-tinct set of challenges,9 in general the larger policy of involv-ing stranded gas has insulated projects from intense public

scrutiny, with project sponsors and policy makers alike ableto point to the benefits of the commercialized gas and thereduction in fuel imports.

Finally, DFIs are behind many countries’ power sectorpolicy frameworks; notably the World Bank has had a handin nearly all power sector reform programs in Africa. DFIshave been particularly instrumental in advancing privatesector participation in generation. And as many of thosesame institutions began reconsidering publicly fundedinfrastructure investments at the end of the 1990s, coun-tries’ policies have followed—from state to market and backagain, albeit with some changes to accommodate the morehybrid market that has emerged.

Linking planning, procurement, and contracting

Intricately connected to sound policy frameworks arecoherent power sector plans. Ideally, planning, procure-ment, and contracting follow from sound policy frame-works and include a number of core components: setting areliability standard for energy security, completion ofdetailed supply and demand forecasts, development of aleast-cost plan with alternative scenarios, clarification ofhow new generation production will be split between theprivate and public sectors, and identification of requisitebidding and procurement processes for new projects. Oneimportant aspect of coherent power sector planning is vest-ing planning and procurement in one empowered agency toensure that implementation takes place with minimalmishaps (Eberhard and Malgas forthcoming).

While that planning and procurement arrangement maybe ideal, the reality is often quite different. As one stakeholderat Ghana’s Public Utilities Regulatory Commission (PURC)notes about the recent past, “A crisis arises, and everybodypanics; anybody who comes in [to propose generation] islistened to” (PURC 2010). Indeed, in the eight countriesexamined here, there have been several noteworthy plan-ning mishaps that subsequently affected procurement andcontracting. In some cases, demand and supply were notbeing accurately forecast partly because of weather condi-tions such as extended droughts, which in turn necessitatedfast-tracking IPPs—that is, plans for IPPs were spedthrough to meet immediate power shortages. The firsttwo plants in Kenya (Westmont and Iberafrica), the firstplant in Nigeria (AES Barge), and Ghana’s Takoradi II IPPwere all negotiated during drought conditions. Althoughboth the Westmont and Iberafrica plants came onlinewithin 11 months, they were later investigated for suspiciousbidding practices and what were perceived as unnecessarily

CHAPTER 21: INDEPENDENT POWER PROJECTS IN SUB-SAHARAN AFRICA: DETERMINANTS OF SUCCESS 375

expensive charges. Furthermore, public stakeholders’unwillingness to make concessions over a tariff resulted inWestmont not securing a second PPA. The AES Barge proj-ect in Nigeria took nearly two years to come online becauseof a renegotiation of the PPA, despite the project beingfast-tracked. In Ghana, no agreement was reached over thesecond phase of the Takoradi II project.

Inability to estimate demand and supply accurately or toset a clear reliability standard has also led to several cases inwhich emergency power units needed to be leased for one totwo years with the purpose of plugging a short-term crisis.In 2009 approximately 750 MW of emergency power was inoperation in Sub-Saharan Africa (Foster and Briceno-Garmendia 2010). The governments of Ghana, Kenya,Tanzania, and Uganda all have been forced to addressdrought and black-outs in recent years, often turning toemergency power suppliers (see box 21.1 for an example).Kenya harnessed 100 MW of emergency power twice: in1999, 2000, and 2001, and again in 2006 (supplied by Aggreko,Cummins, and Deutz in the first instance and Aggreko alonein the second). In 2007 Aggreko’s contract was extended foran additional two years, and in 2009 Aggreko was selected toprovide a further 140 MW for a total of 250 MW of emer-gency power.10 In Ghana emergency power was instrumentalin reducing the impact of the 1998 drought, but as droughtconditions reversed, the state failed to honor its contractswith SIIF Accra; as of 2007 those contracts were still in dis-pute. The cost of emergency power, at approximately 30 to40 cents a kilowatt hour (kWh), is high (IFC 2005). Tanzania,for example, has estimated that it saves around $1 for everykWh of outage averted (or about 5 to 10 times the ordinarycost of generating electricity).11

Competitive International Bidding Practices.Although it is easy, in hindsight, to accuse IPP stakehold-ers of acting imprudently in the face of emergencies, theactual conditions of load-shedding and shortages in thepower sector appear to have provided few alternatives. Twostudies highlight the importance of the international com-petition in bidding practices in reducing up to 60 percentof the capital cost of plants (Deloitte Touche TohmatsuEmerging Markets Ltd. and Advanced Engineering Associ-ates International 2003; Phadke 2007). There is also evi-dence for selective bidding proving effective in certaininstances, provided there is regulatory scrutiny. Of the 21IPPs examined here, ICBs are known to have been con-ducted for nine. Six of the projects in East Africa (OrPower4, Tsavo, Rabai, Songas, Namanve, and Bujagali) con-formed to these bidding practices, as did three projects in

West Africa (Azito, GTi Dakar, and Kounoune I). Of theprojects examined here that have faced renegotiation, fourwere not bid through an ICB (IPTL, Iberafrica, AES Barge,and Okpai); the two exceptions were Songas and OrPower4. Absence of regulatory scrutiny is also noteworthy ineach of these four projects. Furthermore, Westmont,which was selectively bid, quit the country after its firstseven-year PPA expired. Other non-ICB projects have alsoencountered difficulties. For example, Ghana’s Takoradi IIhas not been able to raise financing for the second phase ofthe plant. Although reasons for these stumbling blocksmay be traced well beyond the presence or absence of anICB, the correlation is nonetheless revealing.

Furthermore, the success of the ICB process is intricatelylinked to the number of bids received, with more bidding

376 CHAPTER 21: INDEPENDENT POWER PROJECTS IN SUB-SAHARAN AFRICA: DETERMINANTS OF SUCCESS

The quick and obscure process through which IPTL(Tanzania) was negotiated resulted in the highest-profile IPP mishap on the continent to date. Theproject’s total investment costs were estimated at$150 million ($163 million including fuel conver-sion), an amount the government and the WorldBank later argued was inflated by 40 percent. Thisdispute led to a three-year arbitration process duringwhich another project in Tanzania, the Songo Songogas-to-electricity project, was also put on hold,mainly through pressure from the World Bank, itslargest donor, because of alleged corruption.Although the IPTL arbitration reduced its estimatedcosts it was still well above the price the governmentsought to pay. In addition, since both IPPs wereunavailable until 2002 and 2004 respectively, the statehad to negotiate with another company, Rich-mond/Dowans, for emergency power, a contract thatcame with its own inflated costs and controversies.Furthermore, because of the delays, Songo Songoaccumulated $100 million in interest charges onowner’s equity.

In this project, critical planning elements are miss-ing, namely, a clear reliability standard, an accuratedemand and supply forecast, a detailed plan for pri-vately powered and publicly powered generation, and,most important, timely initiation of procurement andeffective conclusion of contracts.

Source: Authors.

Box 21.1 Poor Planning Led to Significant Delaysfor Tanzania’s Projects

driving down prices,12 as evidenced by IPPs in North Africa,where the number of bids submitted to ICBs has been gen-erally double to triple those submitted to ICBs in East andWest Africa. That said, the time and cost required to com-plete an international competitive bid should not be under-estimated. In Sub-Saharan Africa, drought-related energycrises are often cited as the reason why ICBs have not beenpursued. In Togo, for example, the drought conditions of2006 prompted a move to discontinue a rehabilitate-own-transfer contract with Electro Togo to manage the Centralethermique de Lomé. Rather than launching an ICB, the gov-ernment chose to negotiate directly with an existing player,Contour Global, which was already in discussions with theutility. In this case, time and project familiarity proved moreimportant than complying with international bidding prac-tices, which risked extending the project development time-line (Ministry of Energy of Togo 2010).13

The reason for these planning and contracting mishapsseems to lie in the changing nature of power marketsacross Africa and other developing regions. In addition, aspower markets continue to include private sector partici-pation, it is not always clear who has responsibility formaintaining security of supply. Often, the planning func-tion is shifted from the state-owned utility company tothe energy ministry, which does not have the capacity,resources, or experience to undertake detailed power sectorplanning. Alternatively, planning is contracted to consult-ants who produce master plans that quickly becomeoutdated as global equipment, fuel costs, and other keyparameters change (Eberhard and Malgas forthcoming).Absence of regulatory control and institutional capacity isevident in more areas than just planning. In manyinstances, there are no clear criteria for allocating powerplant building opportunities to either the incumbentstate-owned utility or the private sector.

Often, it is not clear whether plans are merely indicative,whether unsolicited proposals may be considered, orwhether plans have legal force in determining which plantsthe regulator may license. Too often, plans do not translateinto timely initiation of competitive bid processes for newplants. Similarly, there is often insufficient capacity to nego-tiate with winning bidders or to conclude sustainable con-tracts. Transaction advisers may be appointed, but oftenthere is little continuity and the overall policy framework islacking information about security packages or creditenhancement measures being offered by government.Despite past planning deficiencies and forced reliance onemergency power generation, Kenya provides an interestingrecent example in which progress is being made in dealing

with these planning, procurement, and contracting chal-lenges (box 21.2).

Abundant, low-cost fuel and secure fuel contracts

The availability of competitively priced fuel supplies hasalso emerged as a key factor in how IPPs are perceived andultimately whether there is public appetite for such projects,in large part because fuel is generally a pass-through cost tothe utility and, in many cases, also to the final consumer.Thus, if the IPP uses a different fuel than other plants, andif that fuel is more expensive, there is greater potential fordisputes surrounding the new project.

In several Sub-Saharan African countries—Ghana, Kenya,Senegal, Tanzania, and Togo—low-priced hydropower wasthe dominant fuel source for power production, but IPPswere thermal powered, using a combination of imported fuel

CHAPTER 21: INDEPENDENT POWER PROJECTS IN SUB-SAHARAN AFRICA: DETERMINANTS OF SUCCESS 377

Box 21.2 Planning, Procurement, and ContractingChallenges in Kenya

Recognizing that it does not have the internal capacity,resources, or planning tools to develop detailed andup-to-date electricity plans, Kenya’s Energy RegulatoryCommission (ERC) has delegated this function to theKenya Power and Light Company (KPLC), guided by agovernment committee chaired by the ERC. KPLCceased being an electricity-generating company in1997, and thus has a neutral stance between the stateutility, Kenya Electricity Generating Company(KenGen), on one hand and private IPPs on theother. KPLC has also been assigned responsibilityfor managing the procurement and contractingprocess for IPPs. As described by one project sponsorin Kenya, commenting in May 2010,“Kenya has an IPPstructure that is working. It has a track record. It canstructure new projects based on experience gainedfrom previous projects. And it has a very capable set ofteams working in KPLC, the Ministry of Energy/Finance and KenGen. It understands project financeand is not surprised when a developer requests a com-fort letter, as one example.” The fruits of this approachare evident. Kenya is about to add three new IPPs to itsexisting five, maintaining its lead position in Sub-Saharan Africa in terms of IPP investments.a

a. Kenya also has been cited by public stakeholders in Ghanaand Tanzania as having processes that should be emulated(PURC 2010; EWURA 2010).

oil and domestically procured natural gas. These same coun-tries witnessed a series of debilitating droughts during the1990s and 2000s, during which existing hydropower infra-structure proved insufficient, and thermal power, providedalmost entirely by IPPs, was increasingly integrated into thefuel supply mix (from 10 percent to 60 percent in Tanzania,for example), forcing up the price of power. Although morethermal power may be required, the public perception hasbeen that IPPs drive up the price of power. OrPower 4,Kenya’s geothermal IPP, deserves special mention in the con-text of hydro-dominant systems that have been diversifiedwith (largely imported) fuel oil (box 21.3).

The number of IPPs in Sub-Saharan Africa with secure,low-cost fuel sources is still relatively few. In Tanzania,although natural gas from the Songo Songo field is cheaperthan the imported fuel oil currently powering IPTL,14 dis-putes continue to surround its use, and IPTL’s diesel unitshave yet to be converted to gas. In Ghana the Sunon AsogliPower Plant is completed but awaits fuel. Ghana’s VoltaRiver Authority (VRA), the state-owned generator, is afoundation customer for the West African Gas Pipeline(WAGP), from which it has been receiving gas since Febru-ary 2010, but the recently completed Shenzhen IPP willreceive gas only when the pipeline is pressurized and highervolumes of gas flow. In short, an IPP’s access to abundant,low-cost fuel is not only a matter of whether such fuel isavailable in a country, but whether the supply of such fuel is

guaranteed through contracts well into the future. Fuelsourcing and other country-level elements that contributeto successful IPPs are summarized in table 21.2.

PROJECT-LEVEL FACTORS CONTRIBUTING TO SUCCESSFUL IPPS

Investors in IPPs in Sub-Saharan Africa must navigatechanging investment climates, national policies, and plan-ning frameworks. Starting with an evaluation of equityarrangements, this section examines trends in investorbehavior and how investors secured revenue to service debtand reward equity, particularly in the face of exogenousstresses.

Favorable equity arrangements

In assessing the project-level factors contributing to the suc-cess of IPPs, it is useful to ask several questions. Does thepresence of local equity shareholders make a difference inproject outcomes? Are projects with such participation lesslikely to face pressure from host-country governments tochange their contract terms? How does a firm’s previousexperience with a country play out in making or breakingdeals? Does the presence of DFI or firms with internationaldevelopment experience, such as Industrial Promotion Ser-vices (IPS), Globeleq, and Aldwych International, affect thelikelihood of an IPP’s success? Table 21.3 shows the countryorigin of Sub-Saharan African IPP sponsors, along withtheir respective equity share, whether the project faced achange in contract terms, and whether there was turnover ofthe majority equity partner.

Unlike in China and Malaysia, where local investors inIPPs abound, foreign firms have long been dominant play-ers in Sub-Saharan African IPPs (Woodhouse 2005). Giventhe limited availability of capital in Sub-Saharan Africancountries in the sample, this is not surprising. Foreigninvolvement, however, raises the issue of foreign exchangeexposure.15 Only 3 of the 21 projects examined here havelocal majority stakeholders: Nigeria’s Okpai, Afam VI, andAba Integrated. In two of these cases, however, the stake-holder was either the national utility or the NigerianNational Petroleum Company (NNPC).

Several observers (for example, Hoskote 1995; Wood-house 2005) have cited local participation in IPPs as apossible means of reducing risk. Ten of the 21 projectshave local equity participation—namely, Sunon Asogli,Iberafrica,16 IPTL, Songas, Takoradi II, AES Barge, Okpai,Afam VI, Aba Integrated, and Bujagali. As noted, six of these

378 CHAPTER 21: INDEPENDENT POWER PROJECTS IN SUB-SAHARAN AFRICA: DETERMINANTS OF SUCCESS

As indicated in a press release from Ormat (2009), “Ata price of US$29 per barrel of petroleum crude oil, [a]48 MW geothermal plant is cheaper to operate than aheavy fuel oil fired plant. This means that at the cur-rent oil prices still above US$40 per barrel, OrPower 4is providing cheaper electricity to the national gridthan any existing oil fired plants in Kenya.” In con-trast, Nigeria has relied entirely on domestically pro-cured natural gas to fuel its IPPs, and gas is the incum-bent fuel. Until recently, although a series of issuesaffected project outcomes, most notably the invest-ment climate and bidding procedures, fuel had notbeen an issue; however, civil unrest in the Niger Deltaled to a disruption in the fuel supply in 2007–09,albeit with improved conditions as of 2010.

Source: Authors.

Box 21.3 Petroleum-Fired Versus Natural Gas-Fired IPPs

projects have encountered some form of change to theircontract, and in four of the six, either the state utility oranother government entity held an equity share, indicatingthat the existence of a local partner might not be critical inpreserving the original financing balance.

As for renegotiating contract terms, it is unclearwhether having a local partner makes a difference. Kenya’sWestmont and Iberafrica, for example, were negotiated atthe same time under similar policy frameworks, althoughIberafrica had local participation and Westmont did not.Iberafrica first voluntarily reduced its tariff and then went

on to negotiate a second 15-year PPA, in contrast to West-mont, which stopped production after failing to come toan agreement on a second PPA. Although the presence of alocal partner may have helped Iberafrica create a long-term solution, with just one example, the evidence is notconclusive. Togo’s Centrale thermique de Lomé, due to beonline in July 2010, may provide a more sustainablemethod for balancing investment and development out-comes. In this project, 25 percent of the project equitymust be sold to local investors within the first five years(Ministry of Energy of Togo 2010).

CHAPTER 21: INDEPENDENT POWER PROJECTS IN SUB-SAHARAN AFRICA: DETERMINANTS OF SUCCESS 379

Table 21.2 Elements within Purview of Host Governments Contributing to Successful IPPs

Element Details

Favorable investment climate ■ Stable macroeconomic policies■ Legal system that allows contracts to be enforced, laws to be upheld,

and arbitration ■ Good repayment record and investment-grade credit rating■ Requires less (costly) risk mitigation techniques to be employed,

translating into lower cost of capital, lower project costs, and morecompetitive prices

■ Potentially more than one investment opportunityClear policy framework ■ Policy framework enshrined in legislation

■ Framework clearly specifies market structure and roles and terms forprivate and public sector investments (generally for single-buyer model,as wholesale competition does not yet exist in African context)

■ Framework is led and implemented by reform-minded “champions,”concerned with long-term power sector conditions

Clear, consistent, and fair regulatory oversight ■ Oversight improves general performance of private and public sector assets

■ Transparent and predictable licensing and tariff framework improvesinvestor confidence

■ Cost-reflective tariffs ensure revenue sufficiency■ Consumers protected

Coherent power sector planning linked to procurement and contracting

■ Energy security standard in place; planning roles and functions are clear

■ Power planning vested with lead, appropriate (skilled, resourced, andempowered) agency

■ Power sector planning takes into consideration the hybrid market(public and private stakeholders and their respective real costs ofcapital) and fairly allocates new building opportunities amongstakeholders

■ Planning has built-in contingencies to avoid emergency power plants or blackouts

■ Responsibility for procurement is clearly allocated; plans are linked to procurement and bids are initiated in time

■ Procurement process is transparent and competition ultimately drives down prices

■ Capacity is built to contract effectivelyAbundant, low- cost fuel and secure contracts ■ Cost-competitive with other fuels

■ Contract safeguards affordable and reliable; fuel supply sufficient forduration of contract

Source: Authors.

380

Tabl

e 21

.3Eq

uity

Par

ticip

atio

n in

IPPs

in S

ub-S

ahar

an A

fric

a

Pro

ject

E

quit

y pa

rtne

rs (

coun

try

and

perc

ent

of

equi

ty h

eld)

C

hang

e in

co

ntra

ct t

erm

s

Maj

ori

ty e

quit

y pa

rtne

r tu

rnov

er

(num

ber

of

tim

es)

Wes

tmon

t (K

enya

)W

estm

ont

(Mal

aysi

a,10

0%);

has

soug

ht t

o se

ll pl

ant

sinc

e 20

04—

—Ib

eraf

rica

(K

enya

)U

nion

Fen

osa

(Spa

in,8

0%),

KPL

C P

ensi

on F

und

(Ken

ya,2

0%)

sinc

e 19

97ye

s0

OrP

ower

4 (

Ken

ya)

Orm

at (

Uni

ted

Stat

es/Is

rael

,100

%)

sinc

e 19

98ye

s0

Tsa

vo (

Ken

ya)

Cin

ergy

(U

nite

d St

ates

) an

d IP

S (in

tern

atio

nal)

join

tly o

wne

d 49

.9%

,Cin

ergy

sol

d to

Duk

e En

ergy

(U

nite

d St

ates

) in

200

5;C

DC

/Glo

bele

q (U

nite

d K

ingd

om,3

0%),

War

tsila

(Fi

nlan

d,15

%),

IFC

(in

tern

atio

nal,

5%)

have

ret

aine

d re

mai

ning

sha

res

sinc

e 20

00

no1

Rab

ai (

Ken

ya)

Ald

ywch

-Inte

rnat

iona

l (N

ethe

rlan

ds,3

4%),

BWSC

(D

enm

ark,

but

owne

d by

Mits

ui o

f Jap

an,2

5.5%

),FM

O (

Net

herl

ands

,20%

),IF

U (

Den

mar

k,20

%)

no0

IPT

L (T

anza

nia)

Mec

hmar

(M

alay

sia,

70%

),V

IP (

Tanz

ania

,30%

in k

ind)

;bot

h ha

ve s

ough

t to

sel

l sha

res,

and

actu

al e

quity

co

ntri

butio

n is

cur

rent

ly d

ispu

ted

yes

—

Song

as (

Tanz

ania

)Tr

ansC

anad

a so

ld m

ajor

ity s

hare

s to

AES

(U

nite

d St

ates

) in

199

9,an

d A

ES s

old

maj

ority

sha

res

to

Glo

bele

q (U

nite

d K

ingd

om)

in 2

003.

aA

ll pr

efer

red

equi

ty s

hare

s w

ere

conv

erte

d in

to “

loan

not

es”

in Ju

ne 2

009,

only

com

mon

sha

res

rem

ain

yes

2

Buja

gali

(Uga

nda)

Sith

e G

loba

l (U

nite

d St

ates

,58%

),IP

S-A

KFE

D (

32%

),go

vern

men

t of

Uga

nda

(10%

)no

0N

aman

ve (

Uga

nda)

Jaco

bsen

(N

orw

ay,1

00%

)no

0C

IPR

EL (

Côt

e d’

Ivoi

re)

SAU

R In

tern

atio

nal (

88%

).T

his

is a

join

t ve

ntur

e be

twee

n Fr

ench

SA

UR

Gro

up o

wne

d by

Bou

ygue

s (6

5%),

and

Elec

tric

ité d

e Fr

ance

(35

%).

The

rem

aini

ng 1

2% w

as o

wne

d by

a c

ombi

natio

n of

BO

AD

(W

est A

fric

an B

ank

for

Dev

elop

men

t);t

he In

vest

men

t an

d Pr

omot

ions

Com

pany

for

Econ

omic

C

oope

ratio

n,a

subs

idia

ry o

f AFD

;and

IFC

.In

2005

98%

of t

he s

hare

s w

ere

sold

to

Bouy

gues

(F

ranc

e);B

OA

D r

etai

ned

2%.

no1

Azi

to (

Côt

e d’

Ivoi

re)

Cin

ergy

(65

.7%

;joi

nt v

entu

re b

etw

een

Swis

s A

BB a

nd G

lobe

leq)

,CD

C/G

lobe

leq

(11%

),an

d IP

S-A

KFE

D (

23%

)no

1Ta

kora

di II

(G

hana

)C

MS

(Uni

ted

Stat

es,9

0%),

VR

A (

Gha

na,1

0%);

CM

S so

ld s

hare

s to

TA

QA

(U

AE,

90%

) in

200

7ye

s1

Suno

n A

sogl

i (G

hana

)Sh

enzh

en (

Chi

na),

Togb

e A

fede

XIV

(G

hana

/loca

l str

ateg

ic in

vest

or)

no0

Bui h

ydro

(G

hana

)Si

nohy

dro

(Chi

na)

no0

AES

Bar

ge (

Nig

eria

)En

ron

(Uni

ted

Stat

es,1

00%

);so

ld t

o A

ES (

Uni

ted

Stat

es,9

5%)

and

YFP

(N

iger

ia,5

%)

in 2

000

yes

1O

kpai

(N

iger

ia)

Nig

eria

n N

atio

nal P

etro

leum

Cor

pora

tion

(Nig

eria

,60%

),N

iger

ian

Agi

p O

il C

ompa

ny (

Ital

y,20

%),

and

Phill

ips

Oil

Com

pany

(U

nite

d St

ates

,20%

) ha

ve m

aint

aine

d eq

uity

sin

ce 2

001

yes

0

Afa

m V

I (N

iger

ia)

Nig

eria

n N

atio

nal P

etro

leum

Cor

pora

tion

(Nig

eria

,55%

),Sh

ell (

Uni

ted

Kin

gdom

/Net

herl

ands

,30%

),El

f (To

tal)

(Fra

nce,

10%

),A

gip

(Ital

y,5%

)no

0

Aba

Inte

grat

ed (

Nig

eria

) G

eom

etri

c Po

wer

Lim

ited

(Nig

eria

)no

0G

Ti D

akar

(Se

nega

l)G

E C

apita

l Str

uctu

red

Fina

nce

Gro

up (

SFG

) (U

SA),

Edis

on (

Ital

y),I

FCno

0K

ouno

une

(Sen

egal

)M

itsub

ishi

(Ja

pan)

,Mat

elec

S.A

.L (

Leba

non)

no0

Cen

tral

e th

erm

ique

de

Lom

é (T

ogo)

Con

tour

Glo

bal (

Uni

ted

Stat

es,8

0%)

IFC

(20

%)

no0

Sour

ce: A

uth

ors.

Not

e:—

= P

endi

ng

deve

lopm

ents

.a.

Turn

over

wit

hin

th

e So

nga

s pr

ojec

t h

as b

een

com

plex

:Oce

lot

(Can

ada)

,Tra

nsC

anad

a (C

anad

a),T

anza

nia

Pet

role

um

Dev

elop

men

t C

orpo

rati

on,T

PD

C (

Tan

zan

ia),

TAN

ESC

O (

Tan

zan

ia),

Tan

zan

ia D

evel

opm

ent

Fin

ance

Com

pany

,TD

FL (

Tan

zan

ia,s

pon

sore

d by

Eu

rope

an I

nves

tmen

t B

ank)

,IFC

(m

ult

ilate

ral)

,DE

G (

Ger

man

y),a

nd

CD

C (

Un

ited

Kin

gdom

) w

ere

shar

ehol

ders

by 1

996,

wit

h T

ran

sCan

ada

the

maj

orit

y sh

areh

olde

r.IF

C a

nd

DE

G s

old

thei

r sh

ares

to

CD

C in

199

7/98

;Tra

nsC

anad

a so

ld it

s sh

ares

to

AE

S (U

nit

ed S

tate

s) in

199

9;O

celo

t/Pa

nO

cean

sol

dsh

ares

to

AE

S in

200

1;an

d A

ES

sold

maj

orit

y sh

ares

to

Glo

bele

q (U

nit

ed K

ingd

om)

and

FMO

(th

e N

eth

erla

nds

) in

200

3.A

fter

th

e A

ES

sale

,equ

ity

shar

es a

nd

asso

ciat

ed f

inan

cial

com

mit

-m

ents

in S

onga

s w

ere

as f

ollo

ws:

Glo

bele

q,$3

3.8

mill

ion

(56

per

cen

t);F

MO

,$14

.6 m

illio

n (

24 p

erce

nt)

;TD

FL,$

4 m

illio

n (

7 pe

rcen

t);C

DC

,$3.

6 m

illio

n (

6 pe

rcen

t);T

PD

C,$

3 m

illio

n

(5 p

erce

nt)

;an

d TA

NE

SCO

,$1

mill

ion

(2

per

cen

t).T

he

amou

nt

give

n f

or G

lobe

leq

does

not

ref

lect

th

e ad

diti

onal

$50

mill

ion

th

at t

he

com

pany

com

mit

ted

for

the

expa

nsi

on o

fth

e pr

ojec

t.

Origins, Experience, and Mandates of Partners. Froma global perspective, IPP investments during the 1990s wereled by a host of American and European investors who sawreturns in their home markets diminishing. A wave ofinvestors originating from developing countries, however,particularly from Malaysia, was also present. Although itwould be inaccurate to say that investors based in develop-ing countries overlooked the risk involved in African coun-tries (or did not ultimately charge higher returns), they mayhave had a greater willingness to consider IPP investmentsin Sub-Saharan Africa in the first place.

While the number of developing-country-based investorsin IPPs appears to be growing, three such firms are trying tosell their shares (Mechmar, VIP, and Westmont). Thus, thehome country of the firm does not mean that project equityis permanent, or that firms based in developing countries arebest positioned to service debt and reward equity.

An aspect more important than the nationality of theinvesting firm appears to be a firm’s experience and mandate.Across the pool of IPPs examined in table 21.3, several firmswere actively involved in the country before making an IPPinvestment. Union Fenosa, for example, the parent companyof Iberafrica, had previous experience in Kenya through aninformation-technology contract. IPS, a major shareholder inTsavo (Kenya), Azito (Côte d’Ivoire), and Bujagali (Uganda),has operated in Kenya since 1963 and in Côte d’Ivoire since1965. For certain projects, it may be argued that long-termrelationships, particularly those with strong local manage-ment, appear to have contributed to the staying power offirms and often the rebalancing of contract terms.

In addition to the terms of the deal, the mandate of theinvesting firm appears to play a central role in firms’ deci-sions about whether to invest in IPP projects. AlthoughGlobeleq, IPS, and Aldwych, for example, are commercialentities, they emerged from agencies with a strong commit-ment to social and economic development. Until recently,the two firms that were increasing their stakes were Glo-beleq and IPS. Globeleq holds a 43 percent share in Côted’Ivoire’s Azito, 30 percent equity in Kenya’s Tsavo, and 56 percent in Tanzania’s Songas. IPS holds a 23 percentshare in Azito, and together with Duke Energy, a 49.9 percentshare in Tsavo. IPS is also leading development ofUganda’s Bujagali project and is a 35 percent shareholderin equity. Although a smaller player than either Globeleqor IPS, Aldwych International has also made significantinroads via Rabai in Kenya and is evaluating furtherexpansion.

With the exception of Tanzania’s Songas, none of theSub-Saharan African IPP projects with involvement of firms

with development origins examined here has had anychanges in contract terms, which may signal that they werebetter balanced from inception in terms of investors andhad a better ability to withstand public pressure. Further-more, in terms of the Songas change, although the $103 million buy-down of the allowance for funds usedduring construction resulted in a reduction in the capac-ity charge, the firm received full payment upon the buy-down—a different case from many of the contract changescited earlier. Alongside companies with development ori-gins, foreign investors remain directly involved in IPPinvestments. Indeed, DFI equity shares have increased inrecent years for at least five IPPs. With the exception ofSongas, no project with DFI involvement has seen any con-tract changes. Box 21.4 provides further insights on IPPprojects concerned with their developmental impacts.

Equity Turnover. Of the 46 original equity partners inthe 21 projects considered here, 7 have exited (from5 projects). This ratio, however, tells only part of the story.First, as previously indicated, shareholders in Westmont(Kenya) and IPTL (Tanzania) have been trying for several

CHAPTER 21: INDEPENDENT POWER PROJECTS IN SUB-SAHARAN AFRICA: DETERMINANTS OF SUCCESS 381

Development is perhaps more important for Indus-trial Promotion Services (IPS) than for any other firminvesting in IPPs in Sub-Saharan Africa. As a rule, IPSinvests only in projects with a substantial develop-mental impact and a reasonable internal rate ofreturn. For the Tsavo project, that rate is 17–18 per-cent, and for Bujagali, 19 percent—considerably lowerthan typical internal rates of return for IPP projects inSub-Saharan Africa (IPS 2010).

Aldwych International, on the other hand, requiresthat its project investments both make commercialsense and serve a clear developmental function for thecountry and local community. The company’s experi-ence in the Rabai in Kenya helps to illustrate thispoint. The firm has faced three major hurdles as partof its involvement in the project—legal trouble duringthe tendering process, national postelection civilunrest in late 2007, and the global financial crisis.Despite the challenges, the project reached financialclose successfully in 2008; it even won the ProjectFinance International’s deal of the year award.

Source: Authors.

Box 21.4 Two IPPs with Development andInvestment Mandates

years to sell their assets. In the case of IPTL, Mechmar, thelead shareholder, has indicated that the sale has beendriven by an arbitration settlement that hurt its equitypartners. VIP, the minority shareholder, cites oppressionby the majority shareholder, fraud by Mechmar in inflat-ing the IPTL capital cost, and failure by Mechmar to payits equity contribution (that is, the project was 100 per-cent debt financed) as reasons behind its desire to sell itsstake. For this and other projects, investors repeatedly saythat their motivation to sell stakes in IPPs is driven pri-marily by changing circumstances in home markets orcorporate strategy—that is, the desire to sell has little todo with host-country actions and reactions or with poorinvestment outcomes, namely, the ability to service debtadequately and reward equity.

While investment outcomes may be partially motivatingsales, turnover does not in and of itself appear to be chal-lenging the long-term sustainability of contracts, since innearly all cases sellers have found willing buyers to take overthe original or recently renegotiated PPAs. The two excep-tions, again, are Westmont, in which the first PPA expiredand was shrouded in controversy, and IPTL, which has beenembroiled in lawsuits. Under such circumstances, it maytherefore be understandable that the plants have notattracted buyers. One stakeholder went so far as to assertthat “[equity turnover is a] healthy factor in a maturingmarket. It is a good sign when investors come and go—nota bad or threatening thing.” The return of the governmentas a shareholder, as planned in the case of Tanzania’s IPTL,would, however, signal that some markets are less maturethan initially expected.

Debt arrangements: Global and local

With debt financing often representing more than 70 percentof total project costs, competitively priced financing hasemerged as a key factor in successful projects. How and whereto get this low-cost financing is a challenge, but possibleapproaches in the case of Sub-Saharan Africa are DFIs,credit enhancements, and flexibility in repayment terms andconditions, including possible refinancing.17 The goal forsustainable financing should be that the risk premiumdemanded by financiers or capped by the off-taker matchesthe actual country risk and that project risks and risk pre-miums are not inflated.

While there is no uniform pattern in the debt financ-ing for the projects considered here, observation of sev-eral trends in terms of how investors handled costs maycontribute to the success of other projects. Although

nonrecourse project financing is the norm for privatelyfinanced electric power plants in developing regions, the21 projects examined here represent several notable excep-tions: Nigeria’s Okpai and Afam VI, which were 100 percentfinanced by the balance sheet of equity partners, and thesecond phase of Songas, which was largely refinanced by aWorld Bank loan in 2009 (Globeleq 2010a). Until recently,Westmont, Iberafrica, and OrPower 4 were all financedentirely with the balance sheets of their sponsors. For West-mont and Iberafrica, the reason cited for this arrangementwas insufficient time to arrange project finance, becauseplants had to be brought online within 11 months. ForOrPower4, the reason was linked to lack of a security pack-age, which was not finalized until 2006.

The Impact of DFIs on Projects. With limited appetitefor IPPs among commercial banks, DFIs provide a sub-stantial amoung of credit to projects. Indeed, DFIs such asthe World Bank, International Finance Corporation (IFC),European Investment Bank, DEG, FMO, African Develop-ment Bank, PROPARCO, the Emerging Africa Infrastruc-ture Fund, and European Financing Partners, KfW, andAgence Française de Développement have participated innearly every IPP. Beyond these institutions’ long history ofactivity in Sub-Saharan Africa, their involvement is attrib-utable to real and perceived risks by private investors,which keep them from filling the financing gap, and to theDFIs’ interest in participating in the broader mandate ofpower sector reform.

Although projects with DFI funding tended to takelonger to reach financial closure than those financedthrough private sources, project sponsors in Kenya say thatmultilateral and bilateral development institutions helpedthem maintain contracts and resist renegotiation in the faceof external challenges such as droughts, when developerswere pressured to reduce tariffs. A particularly revealingcontrast is between the two Kenyan plants, OrPower 4 andTsavo. Although the two projects were negotiated under thesame policy framework, the former initially had no multi-lateral involvement in either its equity or debt,18 whereas theIFC arranged all the debt for Tsavo and took a 5 percentequity stake. Tsavo has since resisted KPLC pressure toreduce its tariffs. OrPower 4, on the other hand, ultimatelyreduced its tariff for the second phase of the plant. Tanza-nia’s Songas project, for which the World Bank and Euro-pean Investment Bank financed all project debt, alsodeserves special mention here. The project took almost adecade to reach financial closure; the World Bank played aninstrumental role in, among other things, pressuring the

382 CHAPTER 21: INDEPENDENT POWER PROJECTS IN SUB-SAHARAN AFRICA: DETERMINANTS OF SUCCESS

IPTL arbitration, which ultimately led to more balancedcontract terms.

Locally Sourced Finance. While observers argue thatlocal financing is key to increasing sustainable foreigninvestment, capital markets in many Sub-Saharan Africancountries are underdeveloped and illiquid, hence unableto provide financing for all projects. Three exceptions inthe project sample are Kounoune I of Senegal, Geometricof Nigeria, and Namanve of Uganda. The Kounoune Iproject received financing from both the West AfricanBank for Development (BOAD), based in Togo, and theBanking Company of West Africa (CBAO), a private bankbased in Senegal. Funding for Geometric has been pro-vided by Diamond Bank and Stanbic IBTC Bank Plc, bothof Nigeria. Similarly, for Uganda’s Namanve project, financ-ing was provided by Standard Chartered Bank of the UnitedKingdom through Stanbic Bank of Uganda. By contrast, inNorth Africa, all of the €213 million debt of Tahaddart, a384 megawatt combined-cycle gas turbine plant inMorocco, was financed by local banks. Local financing wasaided by a number of factors, including the state utility’sprominent role in the plant (it holds nearly 50 percent oftotal equity) and the fact that Morocco’s commercial bankshave a significant degree of state involvement. With or with-out state involvement, however, no other country in Sub-Saharan Africa has yet been able to manage to arrange thislevel and depth of local financing for IPPs.

One main drawback for IPPs without local finance is theimpact of macroeconomic shocks and local currency deval-uation. Since the late 1990s, Ghana, Kenya, and Tanzaniahave experienced substantial depreciation, with their cur-rencies losing more than 100 percent, 200 percent, and 400 percent of their value against the U.S. dollar, respec-tively. Inevitably, these currency shifts have led to pressureto reduce capacity charges and to countries reconsideringIPP development.

Securing revenue:The PPA

All 21 of the projects examined here had a long-term powerpurchase agreement with the incumbent state-owned utilityto ensure a market for the power produced and to securerevenue flows for debt and equity providers. In addition tostating who would buy the power, the PPAs detailed howmuch power capacity would be available and how muchbuyers would be charged. Provisions concerning fuel meter-ing, interconnection, insurance, force majeure, transfer, ter-mination, change of legal provisions, and refinancing were

generally also addressed. Nearly all the contracts specifiedsome form of international dispute resolution and mini-mum power availability.

For each project, sponsors negotiated or were grantedPPAs in U.S. dollars, thereby reducing their exposure tocurrency devaluation. Over time, the bulk of projectcontracts have been upheld, but not without changes.Box 21.5 reviews PPA renegotiations in Kenya, Nigeria,and Tanzania.

Credit enhancements and security arrangements

The underlying credit risk of IPP projects in Sub-SaharanAfrica has been dealt with largely through a suite of creditenhancements, namely, guarantees, insurance, and cash (thelatter of which took the form of escrow accounts, liquidityfacilities, and letters of credit of varying amounts andtenures). The Tsavo project in Kenya, for example, has anescrow account equivalent to one month’s capacity chargeand a standby letter of credit from KPLC covering threemonths’ billing (approximately $12 million). At least 12 ofthe 21 projects examined in this chapter had some form ofcash security arrangement, with typical terms of betweenone and four months’ capacity charge in reserve.

Not surprisingly, the number of credit enhancementsappears to diminish as a country’s risk profile improves.There are, however, noticeable exceptions such as the firstwave of IPPs in Kenya (Westmont and Iberafrica), for whichrisk appears to be entirely reflected in the higher capacitypayments negotiated. That said, corruption was also allegedin both these plants.19 Thus, the “security arrangement”may lie not in a letter of credit but in an informal agreementamong sponsors.

Of the many different credit enhancements used inconnection with IPPs, sovereign guarantees are mostcommon. Such guarantees are known to have beenextended for at least nine of the pool of 21 projects:Tanzania’s IPTL, Nigeria’s AES Barge, Côte d’Ivoire’sAzito, Ghana’s Takoradi II (phase I), both GTi Dakar andKounoune I in Senegal, Togo’s Centrale thermique de Lomé,and Bujagali and Namanve in Uganda. Several of the proj-ects without guarantees—Tsavo and Rabai, for example—were, however, given assurances by the government in theform of comfort or support letters, through which politicalrisk is assumed. In the case of the Okpai plant in Nigeria,security was extended in the form of the state-owned oilcompany’s revenues. Thus, if the off-taker defaults, NNPC,among the most liquid firms in the country, is liable. Partialrisk guarantees (PRGs) issued by the World Bank were used

CHAPTER 21: INDEPENDENT POWER PROJECTS IN SUB-SAHARAN AFRICA: DETERMINANTS OF SUCCESS 383

for two of the projects, Azito and Bujagali.20 In theseinstances, the PRG covered all debt of the commercialbanks. In the case of default by the project company, thePRG (backed by World Bank) would pay the commerciallenders, and the World Bank would then claim repaymentfrom the government (World Bank 1997, 1999). For otherIPPs, political risk insurance was provided by the OverseasPrivate Investment Corporation (OPIC), whereas guaran-tees relating to currency inconvertibility, expropriation,and political violence were issued by the World Bank’sMultilateral Investment Guarantee Agency (MIGA).

In several cases, these credit enhancements haveimproved the sustainability of projects and attracted orassuaged lenders. The Bujagali project’s PRG, for example,was instrumental in motivating and solidifying the involve-ment of four commercial banks, which contributed a com-bined $115 million at very competitive pricing. Some havelikened the PRG to a hammer effect, with the World Bankguaranteeing what the government has already guaranteedand thus making the government’s commitment twofold.That said, PRGs are not appropriate for all Sub-SaharanAfrican IPPs because they are typically used for large proj-ects in countries that are in an early stage of reform andwhen commercial lenders are also present. Furthermore,

the government of the country must request a PRG; thus,the project must be significant in the eyes of both the gov-ernment and the World Bank. For projects without PRGssecurity arrangements and credit enhancements aresimilar, with the DFIs generally accepting the political risks,such as in the Azito and Songas projects.

In Kenya, the only country among those in Sub-SaharanAfrica examined here to extend sovereign guarantees toIPPs, stakeholders in Tsavo indicated that, without such aguarantee, the presence of the IFC became critical, both tohelp arrange debt and share in equity. In Ghana, lack of sov-ereign guarantees has been cited as the main obstacle todeveloping the second phase of the Takoradi II project.

Other credit enhancements have been used in abundancein Kenya, including a suite of escrow facilities, which havecontributed to KPLC’s cash-strapped position. Althoughgovernment guarantees were recently debated by officials,it looks as if the government will retain its no-guaranteepolicy going forward, providing only letters of support toIPPs. KPLC cites the absence of sovereign guarantees ashampering its ability to raise private finance, while ERCcounters that IPPs have been introduced to help commer-cialize the sector. Government guarantees work againstthis goal, however.

384 CHAPTER 21: INDEPENDENT POWER PROJECTS IN SUB-SAHARAN AFRICA: DETERMINANTS OF SUCCESS

In Kenya’s first wave of IPPs, costs were inflated in part due to the short duration of contracts—only seven years. WithIberafrica facing ongoing pressure to reduce its tariff, coupled with an interest in negotiating another contract, thesponsor voluntarily reduced the capacity charge enshrined in the PPA. (Iberafrica’s second and third PPAs are for aconsiderably longer time frame than its first, and tariffs have been reduced significantly.) Westmont, on the otherhand, did not negotiate a second contract after it failed to obtain the same terms—in particular, those related to capac-ity charges—spelled out in its first PPA. Likewise, changes in Kenya’s OrPower 4 and Tanzania’s Songas PPA agree-ments are related in part to the final amount of the capacity charge (as originally spelled out in the PPA).a