Chappuis Halder - SREP one pager april 2015

2

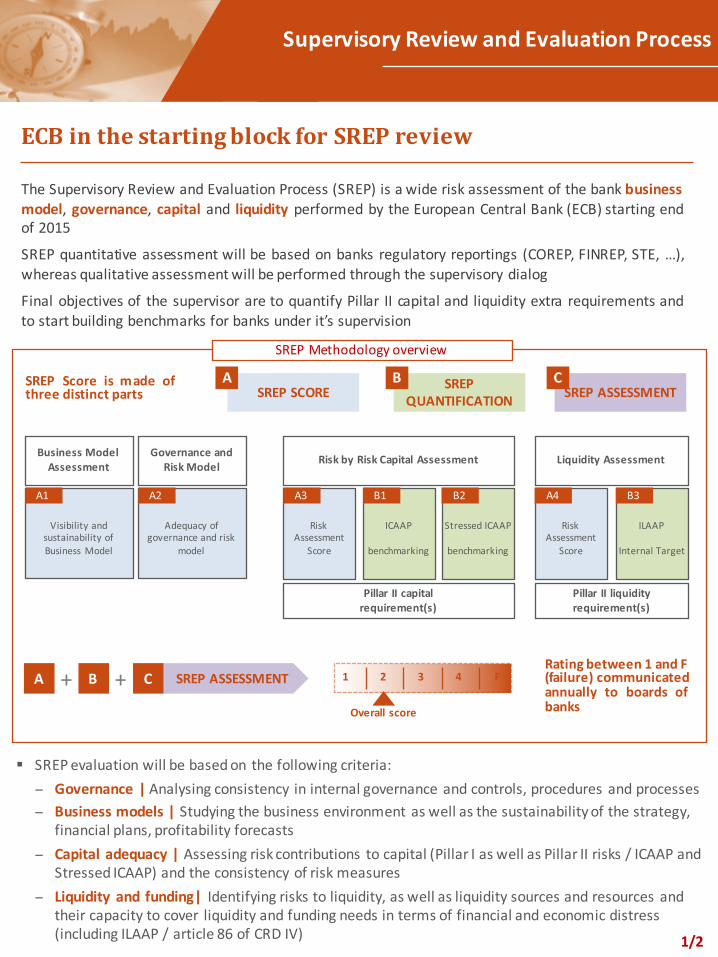

Risk Assessment Score ILAAP Internal Target ECB in the starting block for SREP review The Supervisory Review and Evaluation Process (SREP) is a wide risk assessment of the bank business model, governance, capital and liquidity performed by the European Central Bank (ECB) starting end of 2015 SREP quantitative assessment will be based on banks regulatory reportings (COREP, FINREP, STE, …), whereas qualitative assessment will be performed through the supervisory dialog Final objectives of the supervisor are to quantify Pillar II capital and liquidity extra requirements and to start building benchmarks for banks under it’s supervision Supervisory Review and Evaluation Process SREP Score is made of three distinct parts 1 2 3 4 F SREP SCORE SREP QUANTIFICATION SREP ASSESSMENT A B C Business Model Assessment Governance and Risk Model Risk by Risk Capital Assessment Liquidity Assessment Visibility and sustainability of Business Model Adequacy of governance and risk model ICAAP benchmarking Stressed ICAAP benchmarking Risk Assessment Score Pillar II capital requirement(s) Pillar II liquidity requirement(s) A1 A2 A3 B1 B2 A4 B3 B SREP ASSESSMENT Rating between 1 and F (failure) communicated annually to boards of banks A C + + Overall score SREP evaluation will be based on the following criteria: − Governance | Analysing consistency in internal governance and controls, procedures and processes − Business models | Studying the business environment as well as the sustainability of the strategy, financial plans, profitability forecasts − Capital adequacy | Assessing risk contributions to capital (Pillar I as well as Pillar II risks / ICAAP and Stressed ICAAP) and the consistency of risk measures − Liquidity and funding| Identifying risks to liquidity, as well as liquidity sources and resources and their capacity to cover liquidity and funding needs in terms of financial and economic distress (including ILAAP / article 86 of CRD IV) 1/2 SREP Methodology overview

-

Upload

vincent-w -

Category

Economy & Finance

-

view

265 -

download

0

Transcript of Chappuis Halder - SREP one pager april 2015

Risk Assessment

Score

ILAAP

Internal Target

ECB in the starting block for SREP review

The Supervisory Review and Evaluation Process (SREP) is a wide risk assessment of the bank businessmodel, governance, capital and liquidity performed by the European Central Bank (ECB) starting endof 2015

SREP quantitative assessment will be based on banks regulatory reportings (COREP, FINREP, STE, …),whereas qualitative assessmentwill be performed through the supervisory dialog

Final objectives of the supervisor are to quantify Pillar II capital and liquidity extra requirements andto start building benchmarks for banks under it’s supervision

Supervisory Review and Evaluation Process

SREP Score is made ofthree distinct parts

1 2 3 4 F

SREP SCORE SREP QUANTIFICATION SREP ASSESSMENT

A B C

Business Model Assessment

Governance and Risk Model Risk by Risk Capital Assessment Liquidity Assessment

Visibility and sustainability of Business Model

Adequacy of governance and risk

model

ICAAP

benchmarking

Stressed ICAAP

benchmarking

Risk Assessment

Score

Pillar II capital requirement(s)

Pillar II liquidity requirement(s)

A1 A2 A3 B1 B2 A4 B3

B SREP ASSESSMENTRating between 1 and F(failure) communicatedannually to boards ofbanks

A C+ +Overall score

§ SREP evaluation will be based on the following criteria:− Governance | Analysing consistency in internal governance and controls, procedures and processes− Business models | Studying the business environment as well as the sustainability of the strategy,

financial plans, profitability forecasts− Capital adequacy | Assessing risk contributions to capital (Pillar I as well as Pillar II risks / ICAAP and

Stressed ICAAP) and the consistency of risk measures− Liquidity and funding| Identifying risks to liquidity, as well as liquidity sources and resources and

their capacity to cover liquidity and funding needs in terms of financial and economic distress (including ILAAP / article 86 of CRD IV) 1/2

SREP Methodology overview

Governance / capital & liquidity allocation

Methodologies, models, data

EBA underlying objectives Implications for the financial institutions

Control & processes

§ Strengthen risk appetite definition and documentation

§ Harmonisation of ICAAP, stressed ICAAP and ILAAP frameworks

§ Homogenise capital & liquidity measures§ Understand detailed banks business

models (profitability, forecasting, operational efficiency)

§ Ensure Pillar II coverage of all risks (rate risk -‐ IRRBB, concentration, diversification effect, reputation) not measured with Pillar 1

§ Ensure comprehensiveness of data framework (linkages with BCBS 239 and post-‐AQR action plan)

§ Simplification, strengthening and harmonisation of control & monitoring framework

§ Review of ICAAP & ILAAP framework§ Adjustment of risks to capital profile

& liquidity and funding risk profile§ Less flexibility in terms of capital &

liquidity allocation

§ Challenge of all deviations, exceptions, exemptions validated by the local regulator so far

§ Potential P&L and Balance Sheet impacts

§ Less flexibility in terms of methodology andmodel design

§ Establish new control processes between regulatory reporting

§ Enhance monitoring and reporting tools

§ Improve IT architecture

1

2

3

2/2

Supervisory Review and Evaluation Process

Vincent [email protected]

Charles [email protected]

SREP induces 3 major challenges for the Financial Institutions

Our approach

§ We have built a methodology in order to anticipate SREP process based on market practice and our Pillar II expertise

§ We have prepared a benchmark and sensitivity analysis to anticipate the key drivers your SREP process

§ As a result we are able to prepare a detailed work plan in order to help bank to be ready for the supervisory dialog