Case study: thailand’s energy Conservation (enCon)...

23

CASE STUDY: THAILAND’S ENERGY CONSERVATION (ENCON) FUND CCAP CENTER FOR CLEAN AIR POLICY How Financial Mechanisms Catalyzed Energy Efficiency and Renewable Energy Investments OCTOBER 2012 WRITTEN BY: Erica Jue Brad Johnson Anmol Vanamali Dialogue. Insight. Solutions.

Transcript of Case study: thailand’s energy Conservation (enCon)...

C a s e s t u dy:

t h a i l a n d ’ s e n e r g y C o n s e r vat i o n ( e n C o n ) f u n d

CCAPCENTER FOR CLEAN AIR POLICY

how financial Mechanisms Catalyzed energy efficiency and renewable energy investments

o C to b e r 2012

Writ ten by:

erica Jue

brad Johnson

anmol vanamali

dialogue. insight. solutions.

Case Study: Thailand’s Energy Conservation (ENCON) Fund 2

Acknowledgements This paper is a product of the Center for Clean Air Policy’s Mitigation Action Implementation Network (MAIN) and was written by Erica Jue, Brad Johnson, and Anmol Vanamali of CCAP.

This project was supported by generous funding from Denmark’s Ministry of Energy and Climate.

Special thanks are due to the individuals in Thailand who contributed their time and expertise through interviews to help inform this report. They include, Chaiwat Muncharoen of the Thailand Greenhouse Gas Management Organization, Sorawit Nunt-Jaruwong of DEDE, Ministry of Energy, Suwaporn Sirikoon of Energy for Environment Foundation, Pakaporn Teetilert of the Nollen Group Co., Ltd, Arthit Vechakij, Excellent Energy International Co., Ltd., and Wongkot Wangsapai of Chiang Mai University.

The views expressed in this report represent those of CCAP and not necessarily those of any of the other institutions or individuals mentioned above. For further information, please contact Erica Jue ([email protected]).

The exchange rate used for this report is: 1 USD = 30.60 THB

Case Study: Thailand’s Energy Conservation (ENCON) Fund 3

Contents Overview ....................................................................................................................................................... 5

The Story ....................................................................................................................................................... 6

Establishment of the ENCON Fund (1992) ................................................................................................ 6

Initial Barriers to ENCON Fund Mobilization (1992-2002) ........................................................................ 6

Establishment of the Energy Efficiency Revolving Fund ............................................................................... 7

Evaluation and Results of the EERF ........................................................................................................... 8

Establishment of the Energy Service Company (ESCO) Fund ....................................................................... 9

Financial Mechanisms under the ESCO Fund .......................................................................................... 10

Evaluation and Results of the ESCO Fund ............................................................................................... 13

Evaluation and Future Potential of the ESCO Fund ................................................................................ 14

A Closer Look: The Biogas Sector in Thailand ............................................................................................. 15

Stages of Finance .................................................................................................................................... 15

Evaluation and Future Potential of the Biogas Program ........................................................................ 16

Key Lessons from the ENCON Fund ............................................................................................................ 16

Conclusion/Next steps ................................................................................................................................ 18

References .................................................................................................................................................. 20

Case Study: Thailand’s Energy Conservation (ENCON) Fund 4

List of Abbreviations BOOT Build-own-operate-transfer M3 Cubic meter ENCON Energy Conservation ECFT Energy Conservation Foundation of Thailand EE Energy efficiency EERF Energy Efficiency Revolving Fund E for E Energy for Environment Foundation ESCO Energy service company CO 2e Equivalent carbon dioxide GEF Global Environment Facility IRR Internal rate of return Ktoe Kilo ton of oil equivalent KW Kilowatt MSW Municipal solid waste RE Renewable energy SBCG Small Business Credit Guarantee Corporation TJ Terajoule THB Thai Baht DEDE Thailand’s Department of Alternative Energy Development and Efficiency USD US Dollar VC Venture capital

Case Study: Thailand’s Energy Conservation (ENCON) Fund 5

Case Study: Thailand’s Energy Conservation (ENCON) Fund

October 2012

Overview Thailand is seeking to reach its 10-year Alternative Energy Development Plan (AEDP) target of 25% renewable energy (RE) supply by 2021. The plan will increase Thailand’s renewable energy (RE) share from total energy supply from 7,413 thousand tons of oil equivalent (ktoe) in 2012 to 25,000 ktoe by 2021, and reduce GHG emissions by around 76 million tons CO2 e relative to a 2021 business-as-usual scenario. Since Thailand is heavily (60%) dependent on imported energy the objective of the AEDP goal is to attain energy independence while developing a stable flow and diverse portfolio of clean energy generation.

In 2008, GHG emissions in Thailand reached 323 million tons CO2 e (with land-use, land-use change and forestry) and emissions are projected to increase by 54% to 498.7 million tons CO2 eq. (with land-use, land-use change and forestry) by 2020.

Minimal investments in RE and energy efficiency (EE) took place in the 1990’s, and following the 1997 Asian financial crisis, local banks’ appetite for lending to large and unfamiliar projects was substantially reduced. Other barriers that impeded the growth in RE and EE investments included:

• Lack of clear investment signals and real and perceived risk in EE and RE sectors • Lack of financial liquidity due to weak balance sheets and risk-averse banks, uncertain investor

confidence in the market and limited experience in the banking sector in RE and EE projects • High fixed investment and operation and maintenance costs • Burdensome bureaucratic procedures and paperwork

The Government of Thailand established the Energy Conservation (ENCON) Fund in 1992 to foster the expansion of EE and RE projects by mobilizing and leveraging additional investments in mitigation projects. The ENCON Fund was initially available to large-scale industrial and commercial facilities and later opened up to ESCOs and small-to-medium sized enterprises. By way of clarification, energy service companies (ESCOs) are a 3rd party service provider who engages in a performance based contract to implement measures to reduce energy consumption and costs in a technically and financially viable manner.

Case Study: Thailand’s Energy Conservation (ENCON) Fund 6

The objective of the ENCON Fund was to enable these developers to access and leverage capital, expand the ESCO market, stimulate private sector investment, and increase financial confidence in the EE and RE sector.

In this report we analyze how the ENCON Fund mobilized investments in EE and RE projects, supported local financial intermediaries and private investors to overcome barriers to investment, and by effect created public private partnerships in the energy sector to emerge in Thailand. We find that the ENCON Fund provided critical support for capital-intensive projects and/or ESCOs that were initially unable to obtain financing on available commercial terms.

The Story

Establishment of the ENCON Fund (1992) Thailand’s Energy Conservation (ENCON) Fund was established by the1992 Energy Conservation Promotion Act. The Act outlined three major program areas: a compulsory program that required large commercial and industrial ‘designated’ facilities (classified as facilities with electrical demand greater than 1,000 kW or annual energy use of more than 20 TJ/year of electrical energy equivalent) to increase energy efficiency, a voluntary program targeted at small-to -medium enterprises, and a complementary program covering research and development and publicity initiatives.

The ENCON Fund (“Fund”) was established to provide financial support for the implementation of energy efficiency and renewable energy projects. The Fund was sourced from a tax on all petroleum sold in the country (THB 0.04/USD .001 per liter) and has raised approximately USD 50 million per year since 1992. The Fund has been disbursed through a number of different economic and financial mechanisms, including: grants, subsidies, tax incentives, a feed-in premium for renewable energy, the Energy Efficiency Revolving Fund (EERF) and the ESCO Fund.

Initial Barriers to ENCON Fund Mobilization (1992-2002) Under the first phase of the ENCON Fund, various impediments deterred the deployment of funds to projects. As a result, the ENCON program progressed slowly, with inflows to the ENCON Fund far exceeded subsidies allocated to energy-efficiency projects and a total unspent accumulation of USD 350 million by 2002. The major barriers leading to the stagnant use of funds were political and administrative in nature, and the main barriers included:

1. Poor quality of many of the audits performed by energy consultants 2. Delay in government approval for energy audits 3. Lack of penalty for non-compliance 4. Lack of authority of energy managers

In order to overcome the bureaucratic and excessive reporting procedures and more effectively distribute funds, the Thai government established three pilot programs to stimulate investments in large commercial industrial energy-efficiency projects, one of which was the Energy Efficiency Revolving Fund. The other two were subsidy schemes which provided 30% subsidies for building and factories to

Case Study: Thailand’s Energy Conservation (ENCON) Fund 7

implement energy efficient projects. The schemes are modeled after the Standard Measures and Individual Projects program concepts implemented in Denmark during the mid-1990s.

The Standard Measures program provided a direct 30% subsidy for installation of any one of 11 different measures. The total amount of subsidies given was THB 1.9 billion (USD 62.1 million). The Individual Project program is a “customized” energy-efficiency subsidy program applicable to any upgrades within the specified criteria.

Another important reform involved the reduction in the number of government agencies involved in overseeing energy activities which streamlined the paperwork process and paved way for clearer process for businesses to secure funds. The Department of Alternative Energy Development and Efficiency (DEDE) within the Ministry of Energy was established and replaced the former implementing agency.

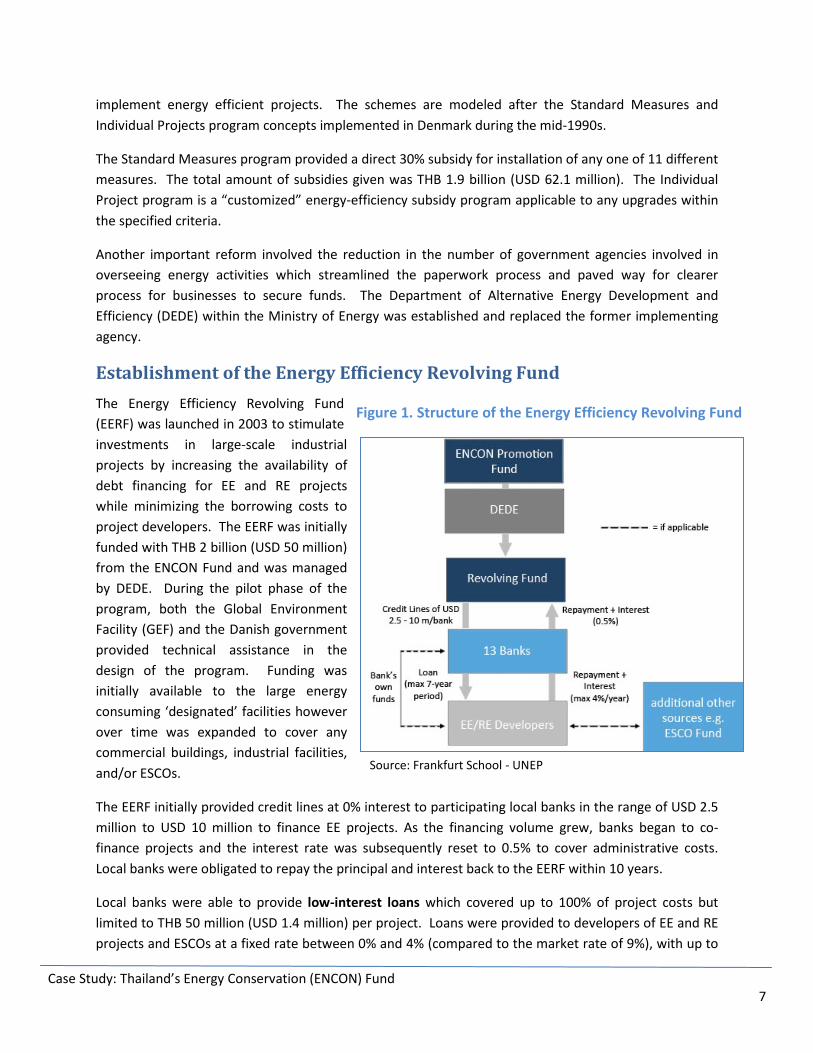

Establishment of the Energy Efficiency Revolving Fund The Energy Efficiency Revolving Fund (EERF) was launched in 2003 to stimulate investments in large-scale industrial projects by increasing the availability of debt financing for EE and RE projects while minimizing the borrowing costs to project developers. The EERF was initially funded with THB 2 billion (USD 50 million) from the ENCON Fund and was managed by DEDE. During the pilot phase of the program, both the Global Environment Facility (GEF) and the Danish government provided technical assistance in the design of the program. Funding was initially available to the large energy consuming ‘designated’ facilities however over time was expanded to cover any commercial buildings, industrial facilities, and/or ESCOs.

The EERF initially provided credit lines at 0% interest to participating local banks in the range of USD 2.5 million to USD 10 million to finance EE projects. As the financing volume grew, banks began to co-finance projects and the interest rate was subsequently reset to 0.5% to cover administrative costs. Local banks were obligated to repay the principal and interest back to the EERF within 10 years.

Local banks were able to provide low-interest loans which covered up to 100% of project costs but limited to THB 50 million (USD 1.4 million) per project. Loans were provided to developers of EE and RE projects and ESCOs at a fixed rate between 0% and 4% (compared to the market rate of 9%), with up to

Figure 1. Structure of the Energy Efficiency Revolving Fund

Source: Frankfurt School - UNEP

Case Study: Thailand’s Energy Conservation (ENCON) Fund 8

a seven-year loan period. The repaid loans were then used to finance new EE and RE projects, hence the ‘revolving’ design of the Fund. The projects that required less than THB 50 million (USD 1.63 million) borrowed 100% from the EERF, and those that required over THB 50 million (USD 1.63 million) solicited additional debt financing from local banks.

The loan eligibility for projects was determined by local banks via loan applications and assessed by evaluating balance sheet strength and the quality of securable assets versus future cash flows and savings from the projects. As collateral for a loan, banks required mortgage over land, building(s) or equipment owned by the applicant. Since project proponents were required to submit a feasibility study upon applying for a loan, very few applications were rejected during the program. Furthermore the EERF was designed to remove credit risk from the government, since banks were required to repay the credit lines to the EERF in the case of default. As such, banks were also free to terminate any loan past due or in default and restructure the loan with their own conditions to recover the losses.

EERF funding covered equipment installation and upgrades consultation, civil works, piping, transportation, and tax. Land costs, land improvement costs, and building construction projects did not qualify for funding.

The banks managed the loans and reported project results to DEDE. DEDE monitored the banks’ performance and measured the programs energy savings. This approach minimized government involvement in the financing process and helped to leverage bank finance. The cost to the government is the opportunity cost associated with providing 0% loans to the local banks.

Evaluation and Results of the EERF Based on the level of investments mobilized, the EERF was successful in stimulating local bank financing of projects in a sector previously avoided by banks and it familiarized banks with EE/RE technology financing. As a result, the EERF was phased out in 2011 since DEDE felt that banks were adequately familiar with EE/RE lending practices and could continue without government support. Even though the EERF was discontinued, DEDE still provides technical support, particularly for projects with new technologies in order to address the associated performance risks.

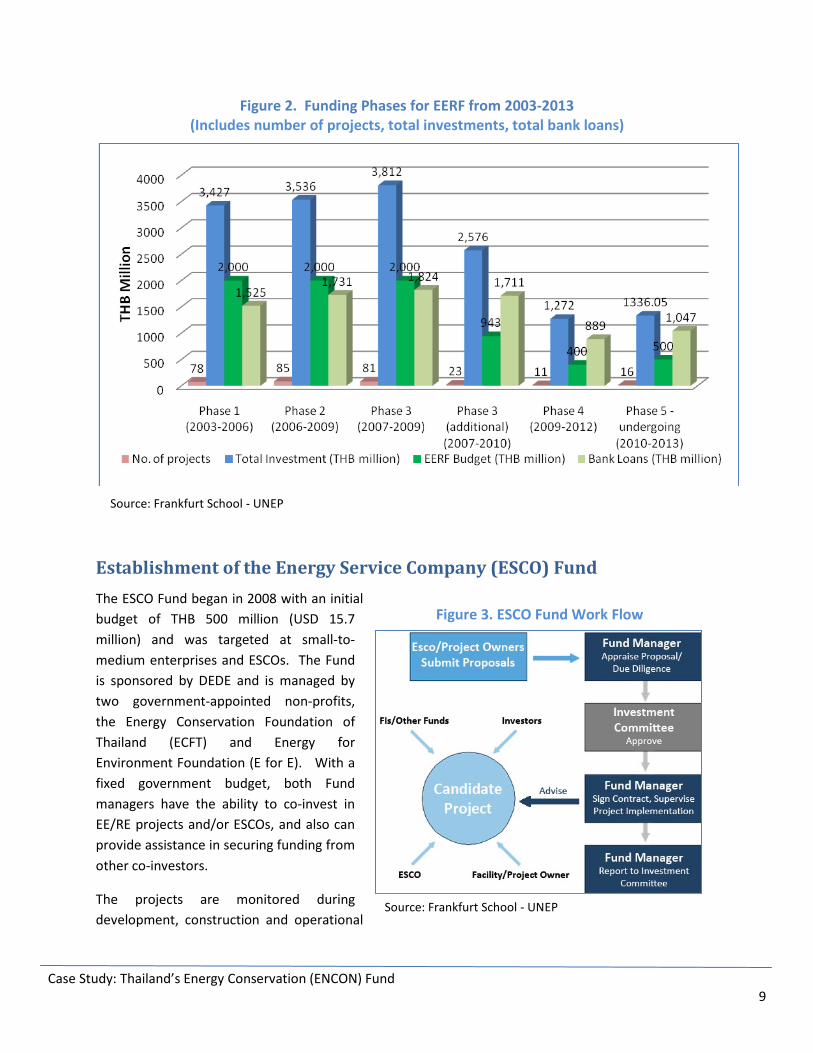

By the close of the EERF program, 13 public and local banks participated in the program which resulted in 294 projects. The total investment was THB 15,959.05 million (USD 521.5 million), which consisted of THB 7,231.94 million (USD 236.34) from the EERF and THB 8,727.10 million (285.2 USD) in debt financing from local banks. The GHG emissions reductions totaled .98 million ton CO2 eq and the total financial savings were estimated to be THB 5,394 million per year (USD 169 million). The majority of the projects funded involved the replacement of chillers and the installation of biogas facilities. While the ratio for financial contribution for lending under the program was initially 1:1 between DEDE and the banks the private sector finance ratio steadily increased over time.

Case Study: Thailand’s Energy Conservation (ENCON) Fund 9

Figure 2. Funding Phases for EERF from 2003-2013 (Includes number of projects, total investments, total bank loans)

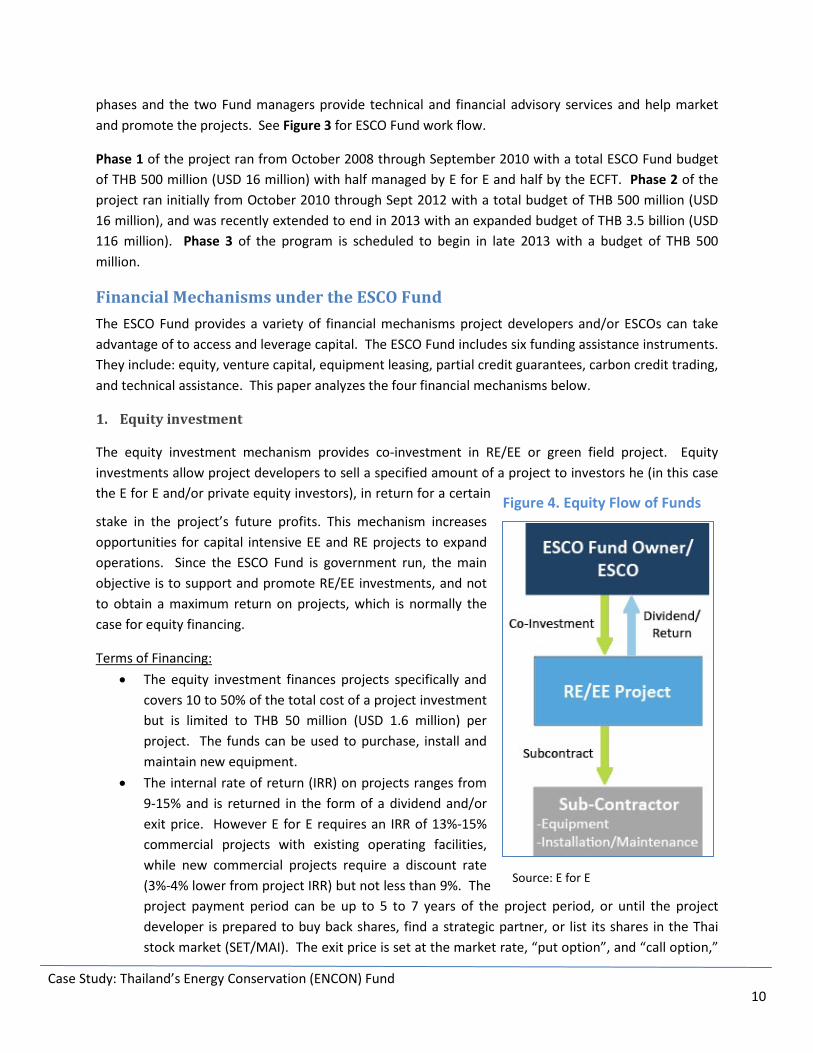

Establishment of the Energy Service Company (ESCO) Fund The ESCO Fund began in 2008 with an initial budget of THB 500 million (USD 15.7 million) and was targeted at small-to-medium enterprises and ESCOs. The Fund is sponsored by DEDE and is managed by two government-appointed non-profits, the Energy Conservation Foundation of Thailand (ECFT) and Energy for Environment Foundation (E for E). With a fixed government budget, both Fund managers have the ability to co-invest in EE/RE projects and/or ESCOs, and also can provide assistance in securing funding from other co-investors.

The projects are monitored during development, construction and operational

Source: Frankfurt School - UNEP

Figure 3. ESCO Fund Work Flow

Source: Frankfurt School - UNEP

Case Study: Thailand’s Energy Conservation (ENCON) Fund 10

phases and the two Fund managers provide technical and financial advisory services and help market and promote the projects. See Figure 3 for ESCO Fund work flow.

Phase 1 of the project ran from October 2008 through September 2010 with a total ESCO Fund budget of THB 500 million (USD 16 million) with half managed by E for E and half by the ECFT. Phase 2 of the project ran initially from October 2010 through Sept 2012 with a total budget of THB 500 million (USD 16 million), and was recently extended to end in 2013 with an expanded budget of THB 3.5 billion (USD 116 million). Phase 3 of the program is scheduled to begin in late 2013 with a budget of THB 500 million.

Financial Mechanisms under the ESCO Fund The ESCO Fund provides a variety of financial mechanisms project developers and/or ESCOs can take advantage of to access and leverage capital. The ESCO Fund includes six funding assistance instruments. They include: equity, venture capital, equipment leasing, partial credit guarantees, carbon credit trading, and technical assistance. This paper analyzes the four financial mechanisms below.

1. Equity investment

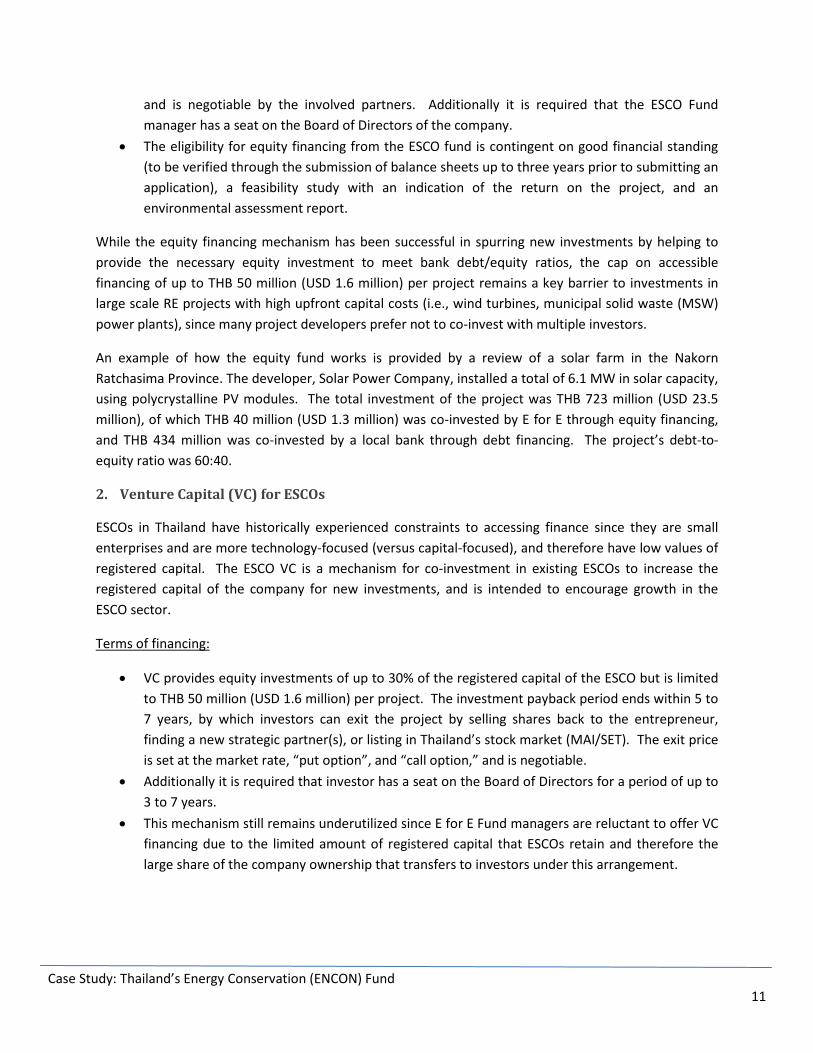

The equity investment mechanism provides co-investment in RE/EE or green field project. Equity investments allow project developers to sell a specified amount of a project to investors he (in this case the E for E and/or private equity investors), in return for a certain

stake in the project’s future profits. This mechanism increases opportunities for capital intensive EE and RE projects to expand operations. Since the ESCO Fund is government run, the main objective is to support and promote RE/EE investments, and not to obtain a maximum return on projects, which is normally the case for equity financing.

Terms of Financing: • The equity investment finances projects specifically and

covers 10 to 50% of the total cost of a project investment but is limited to THB 50 million (USD 1.6 million) per project. The funds can be used to purchase, install and maintain new equipment.

• The internal rate of return (IRR) on projects ranges from 9-15% and is returned in the form of a dividend and/or exit price. However E for E requires an IRR of 13%-15% commercial projects with existing operating facilities, while new commercial projects require a discount rate (3%-4% lower from project IRR) but not less than 9%. The project payment period can be up to 5 to 7 years of the project period, or until the project developer is prepared to buy back shares, find a strategic partner, or list its shares in the Thai stock market (SET/MAI). The exit price is set at the market rate, “put option”, and “call option,”

Figure 4. Equity Flow of Funds

Source: E for E

Case Study: Thailand’s Energy Conservation (ENCON) Fund 11

and is negotiable by the involved partners. Additionally it is required that the ESCO Fund manager has a seat on the Board of Directors of the company.

• The eligibility for equity financing from the ESCO fund is contingent on good financial standing (to be verified through the submission of balance sheets up to three years prior to submitting an application), a feasibility study with an indication of the return on the project, and an environmental assessment report.

While the equity financing mechanism has been successful in spurring new investments by helping to provide the necessary equity investment to meet bank debt/equity ratios, the cap on accessible financing of up to THB 50 million (USD 1.6 million) per project remains a key barrier to investments in large scale RE projects with high upfront capital costs (i.e., wind turbines, municipal solid waste (MSW) power plants), since many project developers prefer not to co-invest with multiple investors.

An example of how the equity fund works is provided by a review of a solar farm in the Nakorn Ratchasima Province. The developer, Solar Power Company, installed a total of 6.1 MW in solar capacity, using polycrystalline PV modules. The total investment of the project was THB 723 million (USD 23.5 million), of which THB 40 million (USD 1.3 million) was co-invested by E for E through equity financing, and THB 434 million was co-invested by a local bank through debt financing. The project’s debt-to-equity ratio was 60:40.

2. Venture Capital (VC) for ESCOs

ESCOs in Thailand have historically experienced constraints to accessing finance since they are small enterprises and are more technology-focused (versus capital-focused), and therefore have low values of registered capital. The ESCO VC is a mechanism for co-investment in existing ESCOs to increase the registered capital of the company for new investments, and is intended to encourage growth in the ESCO sector.

Terms of financing:

• VC provides equity investments of up to 30% of the registered capital of the ESCO but is limited to THB 50 million (USD 1.6 million) per project. The investment payback period ends within 5 to 7 years, by which investors can exit the project by selling shares back to the entrepreneur, finding a new strategic partner(s), or listing in Thailand’s stock market (MAI/SET). The exit price is set at the market rate, “put option”, and “call option,” and is negotiable.

• Additionally it is required that investor has a seat on the Board of Directors for a period of up to 3 to 7 years.

• This mechanism still remains underutilized since E for E Fund managers are reluctant to offer VC financing due to the limited amount of registered capital that ESCOs retain and therefore the large share of the company ownership that transfers to investors under this arrangement.

Case Study: Thailand’s Energy Conservation (ENCON) Fund 12

Figure 5. ESCO Venture Capital Flow of Funds and Contractual Agreement

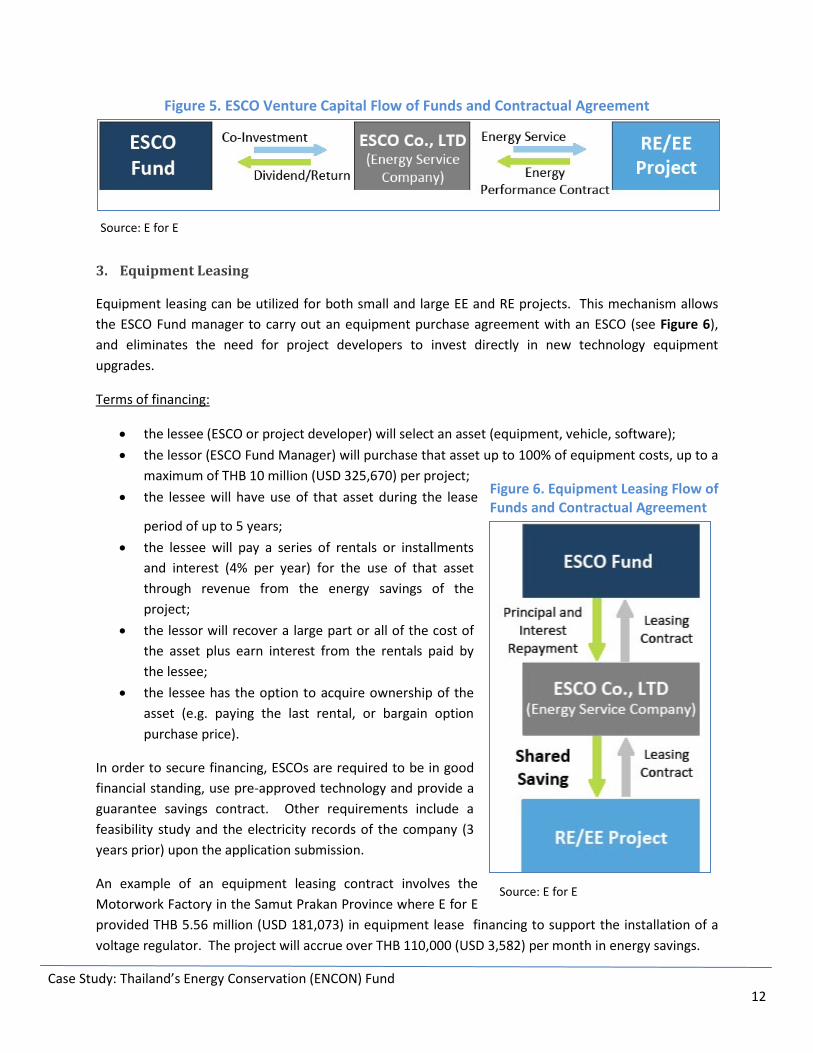

3. Equipment Leasing

Equipment leasing can be utilized for both small and large EE and RE projects. This mechanism allows the ESCO Fund manager to carry out an equipment purchase agreement with an ESCO (see Figure 6), and eliminates the need for project developers to invest directly in new technology equipment upgrades.

Terms of financing:

• the lessee (ESCO or project developer) will select an asset (equipment, vehicle, software); • the lessor (ESCO Fund Manager) will purchase that asset up to 100% of equipment costs, up to a

maximum of THB 10 million (USD 325,670) per project; • the lessee will have use of that asset during the lease

period of up to 5 years; • the lessee will pay a series of rentals or installments

and interest (4% per year) for the use of that asset through revenue from the energy savings of the project;

• the lessor will recover a large part or all of the cost of the asset plus earn interest from the rentals paid by the lessee;

• the lessee has the option to acquire ownership of the asset (e.g. paying the last rental, or bargain option purchase price).

In order to secure financing, ESCOs are required to be in good financial standing, use pre-approved technology and provide a guarantee savings contract. Other requirements include a feasibility study and the electricity records of the company (3 years prior) upon the application submission.

An example of an equipment leasing contract involves the Motorwork Factory in the Samut Prakan Province where E for E provided THB 5.56 million (USD 181,073) in equipment lease financing to support the installation of a voltage regulator. The project will accrue over THB 110,000 (USD 3,582) per month in energy savings.

Source: E for E

Source: E for E

Figure 6. Equipment Leasing Flow of Funds and Contractual Agreement

Case Study: Thailand’s Energy Conservation (ENCON) Fund 13

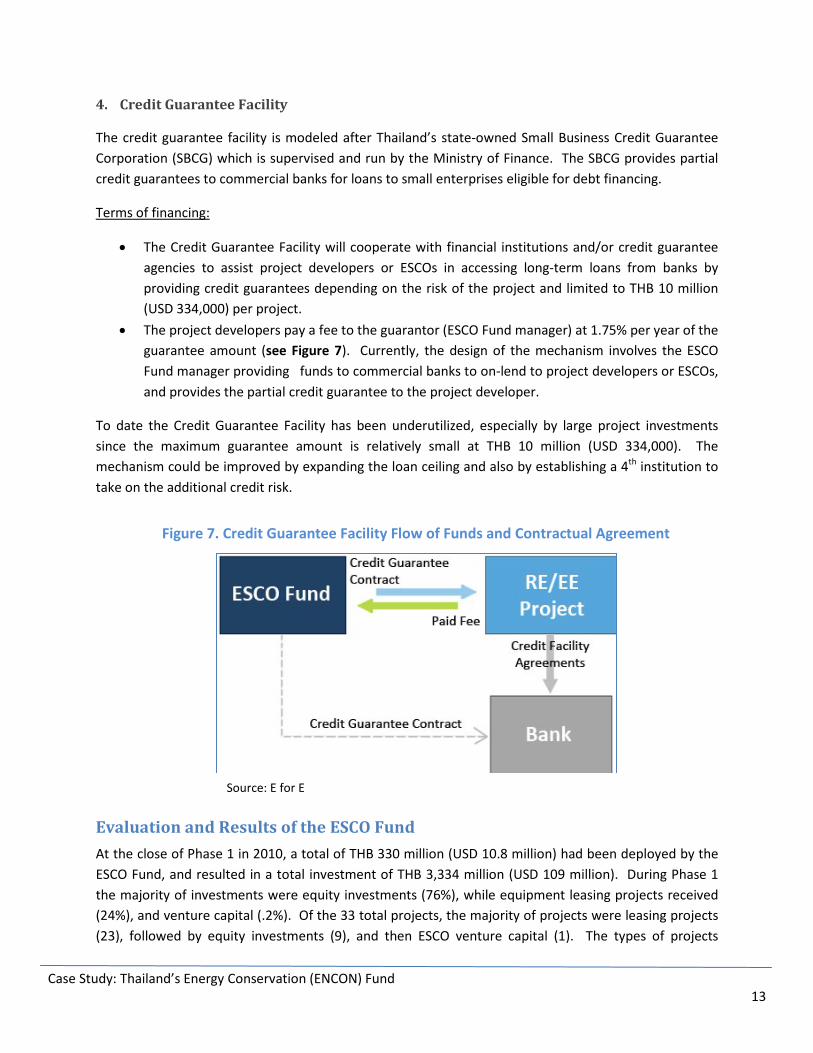

4. Credit Guarantee Facility

The credit guarantee facility is modeled after Thailand’s state-owned Small Business Credit Guarantee Corporation (SBCG) which is supervised and run by the Ministry of Finance. The SBCG provides partial credit guarantees to commercial banks for loans to small enterprises eligible for debt financing.

Terms of financing:

• The Credit Guarantee Facility will cooperate with financial institutions and/or credit guarantee agencies to assist project developers or ESCOs in accessing long-term loans from banks by providing credit guarantees depending on the risk of the project and limited to THB 10 million (USD 334,000) per project.

• The project developers pay a fee to the guarantor (ESCO Fund manager) at 1.75% per year of the guarantee amount (see Figure 7). Currently, the design of the mechanism involves the ESCO Fund manager providing funds to commercial banks to on-lend to project developers or ESCOs, and provides the partial credit guarantee to the project developer.

To date the Credit Guarantee Facility has been underutilized, especially by large project investments since the maximum guarantee amount is relatively small at THB 10 million (USD 334,000). The mechanism could be improved by expanding the loan ceiling and also by establishing a 4th institution to take on the additional credit risk.

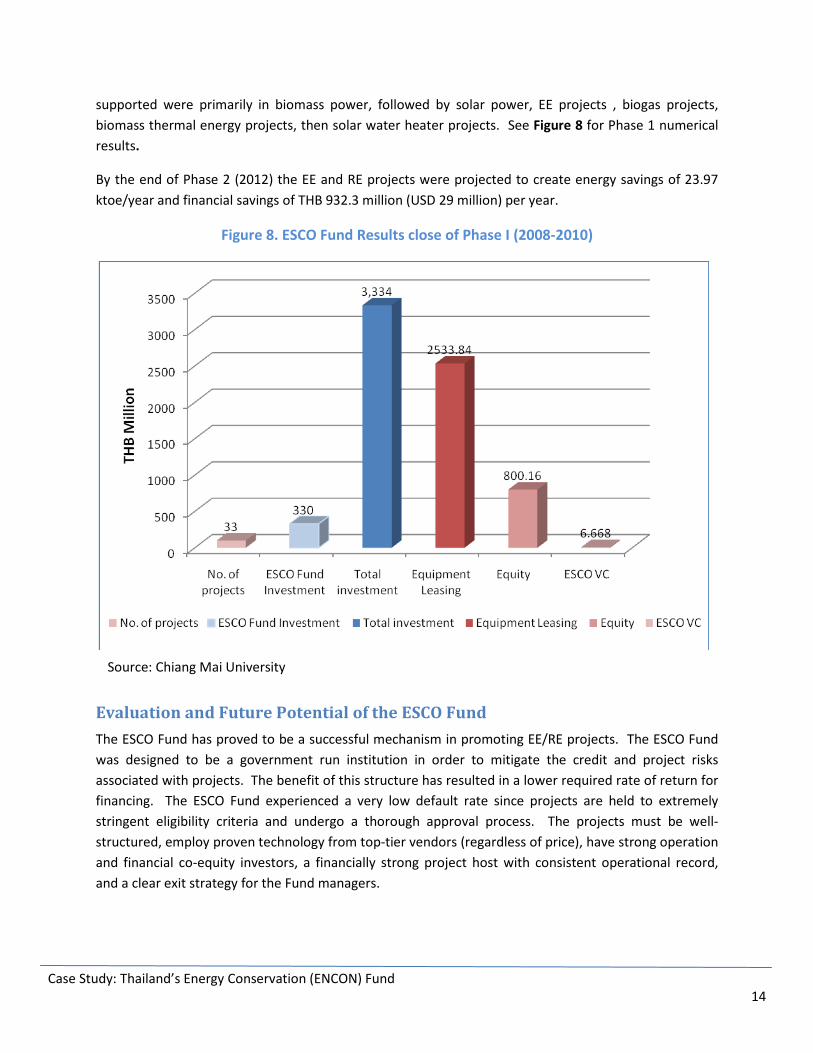

Evaluation and Results of the ESCO Fund At the close of Phase 1 in 2010, a total of THB 330 million (USD 10.8 million) had been deployed by the ESCO Fund, and resulted in a total investment of THB 3,334 million (USD 109 million). During Phase 1 the majority of investments were equity investments (76%), while equipment leasing projects received (24%), and venture capital (.2%). Of the 33 total projects, the majority of projects were leasing projects (23), followed by equity investments (9), and then ESCO venture capital (1). The types of projects

Figure 7. Credit Guarantee Facility Flow of Funds and Contractual Agreement

Source: E for E

Case Study: Thailand’s Energy Conservation (ENCON) Fund 14

supported were primarily in biomass power, followed by solar power, EE projects , biogas projects, biomass thermal energy projects, then solar water heater projects. See Figure 8 for Phase 1 numerical results.

By the end of Phase 2 (2012) the EE and RE projects were projected to create energy savings of 23.97 ktoe/year and financial savings of THB 932.3 million (USD 29 million) per year.

Figure 8. ESCO Fund Results close of Phase I (2008-2010)

Evaluation and Future Potential of the ESCO Fund The ESCO Fund has proved to be a successful mechanism in promoting EE/RE projects. The ESCO Fund was designed to be a government run institution in order to mitigate the credit and project risks associated with projects. The benefit of this structure has resulted in a lower required rate of return for financing. The ESCO Fund experienced a very low default rate since projects are held to extremely stringent eligibility criteria and undergo a thorough approval process. The projects must be well-structured, employ proven technology from top-tier vendors (regardless of price), have strong operation and financial co-equity investors, a financially strong project host with consistent operational record, and a clear exit strategy for the Fund managers.

Source: Chiang Mai University

Case Study: Thailand’s Energy Conservation (ENCON) Fund 15

As the Fund evolves over time, some barriers may be addressed to increase the deployment in larger scale projects. The Fund managers are proactively balancing funds to invest in an even mix of EE and RE projects, however they have encountered the following barriers:

• the requirement of high cost technologies from top-tier vendors has negatively affected the feasibility of projects;

• the financing cap to invest in capital-intensive projects such as wind farms and MSW biogas plants has prevented investments in such projects;

• the slow turnaround for project approval has impeded projects from getting off the ground.

A Closer Look: The Biogas Sector in Thailand RE development in Thailand has faced a number of barriers which has hindered the development of this sector. Compared to EE projects, RE projects generally face higher fixed costs for facilities and technologies, and operating and maintenance costs.

In particular the biogas sector in Thailand has presented many unrealized opportunities for biogas recovery from waste and wastewater deposited from the agriculture and industrial sectors. Historically, wastewater has involved open dumping into lagoons without consideration of biogas recovery.

The EERF and ESCO Funds were critical in helping biogas developers overcome market barriers, establish sector technologies, and assess the return on investment and GHG emissions reductions of projects. As we analyze here, both public and private financing were critical in developing a robust biogas market demonstrating the economics of biogas projects, and GHG emission reductions through pilot projects.

Stages of Finance In the early stages of development, swine farms had difficulty obtaining loans from banks to invest in biogas waste-to-energy facilities, and were therefore dependent on publicly-sponsored grants for financing. In 1995, the National Energy Policy Office (now the Energy Policy & Planning Office, EPPO) launched the National Biogas Dissemination Program for medium and large-sized livestock farms. With government technical assistance the program installed 150 plants in the medium and large sized swine farms using anaerobic digestion technology for the treatment of waste.

During Phase 1 of the program (1995-1998), farms received a direct subsidy from the government to cover all investment costs for biogas projects. This demonstration phase was critical in creating private

Biogas-to-electricity Generator

Case Study: Thailand’s Energy Conservation (ENCON) Fund 16

sector and local community confidence in the biogas sector, and assessed the technical capacity for agriculture biogas.

Once the economic and financial viability of projects were demonstrated, Phase 2 (1998-2002) and Phase 3 (2002-2010) of the program, required farm owners to invest in 2/3 of the construction and installation costs of the system. The remaining 1/3 of the costs remained financed by the ENCON Fund. This covered system design, supervision, and consultation services.

However, resistance from factories to cover such large upfront costs was still present. As a result, large industrial facilities have become developed with equity financing from private investors. The first fully commercially funded project came to fruition with the support of equity financing from three international clean energy private investors, E+Co, REEF, and Al Tayyar Energy. The Khorat waste-to-energy (biogas) project located at Sanguan Wongse Industries (SWI) operated under a Build-Own-Operate-Transfer (BOOT) model. Since the start of commercial operation in 2003, SWI is nearly energy self-sufficient and the project received an annual IRR of 15-17%. This project demonstrated significant cost savings and has been instrumental in encouraging other farms to self-invest in their own facilities. Although the BOOT model did not prove popular with future projects, KWTE served as a catalyst for accelerated industrial biogas development. The plant performance exceeded all expectations and proved the technology at scale. By 2012, biogas systems had been installed in about 50% of Thailand’s large-scale starch plants and in most of the country’s palm oil mills.

Evaluation and Future Potential of the Biogas Program Over the course of the National Biogas Dissemination Program more than 260 swine farms have developed biogas facilities, resulting in biogas production of 154.9 million m3/year and GHG emissions reduction of 1,310,778 million tons CO2e. The program helped develop technical capacity in the agriculture, academic and government sectors and set the stage for commercial bank financing in the sector. Several local banks are now providing financing for industrial biogas projects, and to date, the ESCO fund has made investments in five biogas projects totaling about THB 60 million, including two leases for biogas engines and three equity investments. This rapid deployment of biogas technology across livestock and agro-industrial sectors has been financed by a combination of public grants , bank loans, private equity and carbon finance as well as revenues generated from the sale of surplus electricity to the grid.

Currently, Phase 4 (2008-2013) is underway and has expanded to cover waste water from other sources. Over 1,700 waste water generation sites from the three main sectors (animal husbandry, food industry, and community) are targeted. Moving forward in line with AEDP’s 25% renewable energy target, biogas from effluent is expected to increase by 350% to 600 MW by 2021 relative to 2012 capacity of 138 MW.

Key Lessons from the ENCON Fund The EERF and ESCO Funds have been highly successful in encouraging participation of investors and commercial banks in EE/RE investments and the ENCON Fund has become a well-respected model and

Case Study: Thailand’s Energy Conservation (ENCON) Fund 17

case study. When project developers and ESCOs experienced difficulty accessing financing, and the ESCO Fund provided the financing in small-sized renewable energy and new technology investments, which commercial banks were otherwise reluctant to lend to. The increased number of solar farms and renewable energy capacity, and the entrance of ESCOs into the market is a testament to the success of the ENCON Fund. It has also allowed companies to focus on projects, in which they otherwise lacked time to implement, and did not fall under the core objectives of their business.

This report concludes that the combination of public financial support and access to private sector financing can successfully encourage growth in clean energy development. And, that market barriers can be overcome through a combination of policy initiatives, economic incentives, access to financing, technical and strategic oversight, and private sector involvement.

The key lessons that can be drawn from the ENCON Fund include the following:

• The EERF and ESCO Funds successfully expanded the availability of commercial financing for clean energy projects.

• EERF low interest rate loans to banks and a partial credit guarantee scheme mobilized substantial private sector financing for RE and EE projects and technologies. The EERF effectively reduced financial barriers for project developers and ESCOs and cleared the path for market entry in Thailand. Moreover these mechanisms reduced the time and management costs tied to the government by allowing local banks to on-lend public funds.

• The EERF was designed to deploy funds in a sustainable manner which increased the number of EE/RE projects overall, since loan repayments created new investments in more projects.

• The EERF required about 3 to 4 years to achieve a good application rate. This phase, however, was critical in boosting commercial lending confidence in the RE and EE sector. The EERF and ESCO Funds were effectively used to provide commercial banks with a better and deeper understanding of project risks, costs, return, and technology performance. The EERF and ESCO Funds expanded the availability of commercial financing for clean energy projects.

• Through the ESCO Fund, the management of equity financing by a government agency allowed investors to lower their required rate of return on projects, allowed for greater control and participation of shareholders in projects, and established an approval process that mitigated the risk of project overruns and uncertain energy savings.

• ESCO Fund (“Fund”) managers comprised of technical, financial, and policy experts mitigated project risks for the Fund and private sectorinvestors.

• The EERF and ESCO Funds created a space for the ESCO industry to emerge, under both a shared savings and guaranteed savings models. ESCO services have reduced credit risk and performance risk for EE/RE projects by providing turnkey energy services with performance based and/or lending based contracting to energy users. Ultimately this boosted lending confidence in the sector and local banks were eventually able to lend independent of the government’s involvement.

• Pilot projects were instrumental in determining the underlying economic feasibility, assessment of energy savings, and GHG reductions for specific projects.

Case Study: Thailand’s Energy Conservation (ENCON) Fund 18

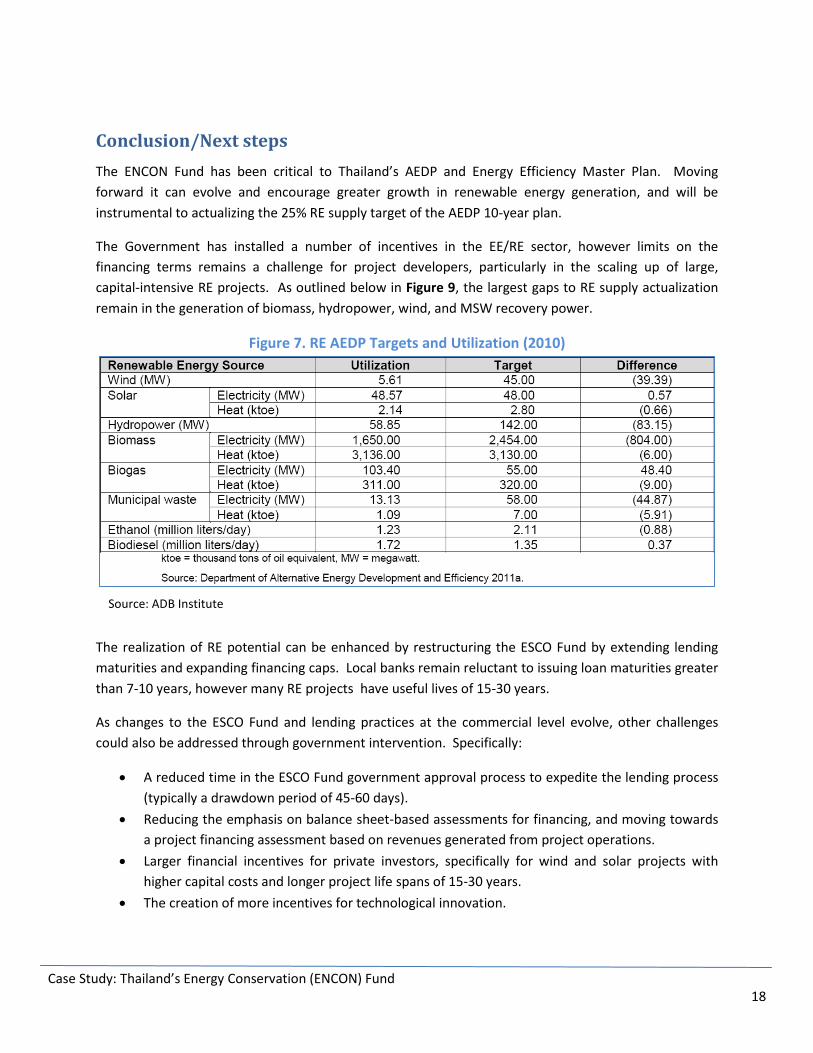

Conclusion/Next steps The ENCON Fund has been critical to Thailand’s AEDP and Energy Efficiency Master Plan. Moving forward it can evolve and encourage greater growth in renewable energy generation, and will be instrumental to actualizing the 25% RE supply target of the AEDP 10-year plan.

The Government has installed a number of incentives in the EE/RE sector, however limits on the financing terms remains a challenge for project developers, particularly in the scaling up of large, capital-intensive RE projects. As outlined below in Figure 9, the largest gaps to RE supply actualization remain in the generation of biomass, hydropower, wind, and MSW recovery power.

Figure 7. RE AEDP Targets and Utilization (2010)

The realization of RE potential can be enhanced by restructuring the ESCO Fund by extending lending maturities and expanding financing caps. Local banks remain reluctant to issuing loan maturities greater than 7-10 years, however many RE projects have useful lives of 15-30 years.

As changes to the ESCO Fund and lending practices at the commercial level evolve, other challenges could also be addressed through government intervention. Specifically:

• A reduced time in the ESCO Fund government approval process to expedite the lending process (typically a drawdown period of 45-60 days).

• Reducing the emphasis on balance sheet-based assessments for financing, and moving towards a project financing assessment based on revenues generated from project operations.

• Larger financial incentives for private investors, specifically for wind and solar projects with higher capital costs and longer project life spans of 15-30 years.

• The creation of more incentives for technological innovation.

Source: ADB Institute

Case Study: Thailand’s Energy Conservation (ENCON) Fund 19

In the past 10 years the availability of project financing to EE/RE projects has improved dramatically in Thailand. Currently, the political signals warrant even more investment in these sectors, and having an already experienced banking and public financing structure, the government has enabled a structure for public private partnerships. Future projects could be financed using a combination of domestic, public, multi-lateral, bilateral financing to execute larger scale projects, and to actualize the goals set forth in the AEDP 10-year plan.

Case Study: Thailand’s Energy Conservation (ENCON) Fund 20

References Akeprathumchai, S. 2012, personal communication, Energy for Environment Foundation, October 5, 17, 20. Chotichanathawewong, Q. and Thongplew, N., April 2012. “Development Trajectory, Emission Profile, and Policy Actions: Thailand,” ADB Institute Working Paper, http://www.adbi.org/files/2012.04.12.wp352.dev.trajectories.emission.thailand.pdf. Energy for Environment Foundation. 2012, ESCO Fund Brochure. Thailand: Energy for Environment, ESCO Fund, http://www.efe.or.th/escofund.php. Energy for Environment Foundation. October 2012, "Investment Promotion in Energy Efficiency and Renewable Energy Projects under ESCO Fund." Powerpoint presentation. Energy Futures Australia and DMG Thailand. 2005, Thailand’s Energy Efficiency Revolving Fund: A Case Study, http://efa.solsticetrial.com/admin/Library/David/Published%20Reports/2005/ThailandsEnergyEfficiencyRevolvingFund.pdf. Frankfurt School - UNEP Collaborating Centre for Climate & Sustainable Energy Finance. 2012, Case Study: The Energy Efficiency Revolving Fund, http://www.fs-unep-centre.org. Institute for Industrial Productivity. 2012, Industrial Efficiency Policy Database: Thailand TH-8: Energy Efficiency Revolving Fund (EERF), http://iepd.iipnetwork.org/policy/energy-efficiency-revolving-fund-eerf. Intarajinda, R. and Bhasaputra, P. 2012, "The Strategic Management of Energy Service Company to Enhance the Sustainable Energy Management in Thailand." International Journal of Energy Science 2.4, p. 127-32. Irawan, Silva, and Alex Heikens. 2012, Case Study Report: Thailand Energy Conservation Fund. Rep. UNDP, http://www.snap-undp.org/elibrary/Publications/EE-2012-NCF-CaseStudy-Thailand.pdf. Johnson, B. July 2012, Overview of NAMA Financial Mechanisms, Center for Clean Air Policy, http://www.ccap.org/docs/resources/1135/Overview-of-NAMA-Financial-Mechanisms_CCAP-July-2012.pdf. Mintz Levin LLC and GTM Research. December 2011, Renewable Energy Project Finance in the U.S.: An Overview and Midterm Outlook, www.tulainternational.com/wp.../mintzlevin-gtm-pf-jan-2012.pdf. Muncharoen, C. 2012, personal communication, Thailand Greenhouse Gas Management Organization, October 15.

Case Study: Thailand’s Energy Conservation (ENCON) Fund 21

Nunt-Jaruwong, S. 2012, personal communication, DEDE, Ministry of Environment, October 17. Rezessy, S, and Bertoldi, P. May 2012, Case Study Report: Thailand Energy Conservation Fund. Rep. UNDP, http://ec.europa.eu/energy/efficiency/doc/financing_energy_efficiency.pdf. Siteur, J. 2012, Rapid Deployment of Industrial Biogas in Thailand: Factors of Success. Rep. Washington DC: Institute for Industrial Productivity, http://www.iipnetwork.org/rapid-deployment-industrial-biogas-thailand-factors-success. Teetilert, P. 2012, personal communication, Nollen Group Co., Ltd, October 4,8. Toba, N., Peamsilpakulchorn, P., Zhang, Y., Manopinewes, C. September 2011, Thailand: Clean Energy for Green Low-Carbon Growth, World Bank, http://www-wds.worldbank.org/external/default/WDSContentServer/WDSP/IB/2012/01/04/000333037_20120104230930/Rendered/PDF/662200WP0p12440e0Clean0Energy0all07.pdf. Vechakij, A. 2012, personal communication, Excellent Energy International Co., Ltd., October 9. Wongsapai, Wongkot. 2012, personal communication, Chiang Mai University, July 2 and September 21.

750 first street, ne, suite 940 Washington, dC 20002

p +1.202.408.9260 f +1.202.408.8896

www.ccap.org

s u P P o r t e d by: