Bree.gov.au Resources and energy—the outlook for Australia Australasian Rail Association Heavy...

16

bree.gov.au Resources and energy—the outlook for Australia Australasian Rail Association Heavy Haul Rail: Newcastle 27-28 August 2014 Wayne Calder Deputy Executive Director Bureau of Resources and Energy Economics (BREE)

-

Upload

gerard-claude-henderson -

Category

Documents

-

view

220 -

download

1

Transcript of Bree.gov.au Resources and energy—the outlook for Australia Australasian Rail Association Heavy...

bree.gov.au

Resources and energy—the outlook for Australia

Australasian Rail Association Heavy Haul Rail: Newcastle 27-28 August 2014

Wayne CalderDeputy Executive Director

Bureau of Resources and Energy Economics (BREE)

bree.gov.au

Key messages Still opportunities for resources and energy exports

to emerging economies Investment in capital formation and growing

energy consumption growth will support demand

for bulk commodities Transition to the production phase accelerating Iron ore and coal are key exports for Australia, and

will continue to provide significant earnings over

the medium term

bree.gov.au

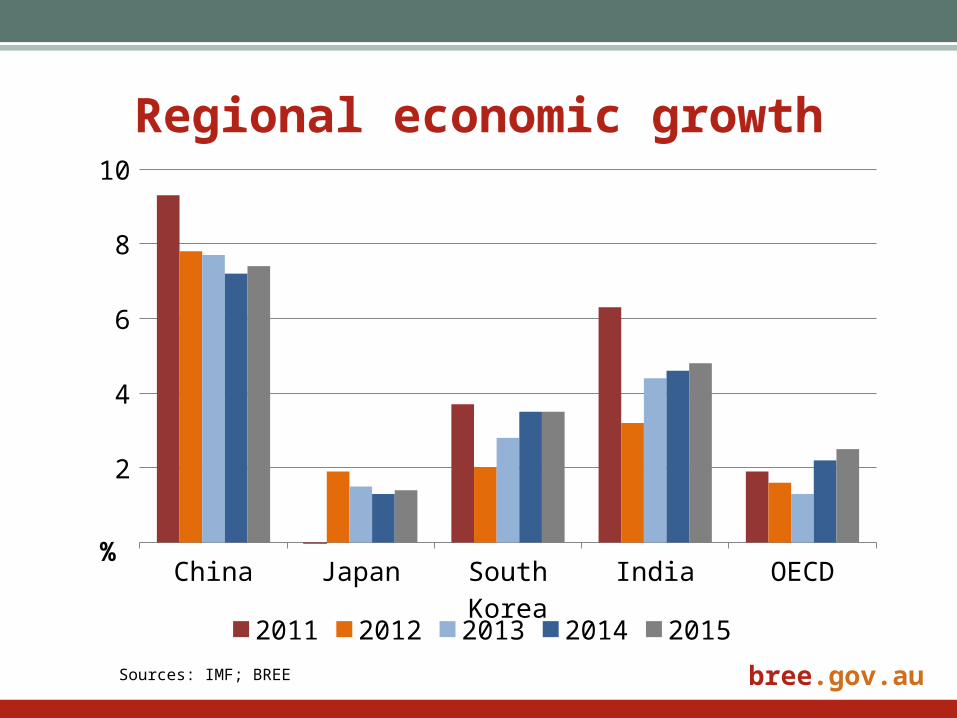

Regional economic growth

China Japan South Korea India OECD

2

4

6

8

10

2011 2012 2013 2014 2015

%

Sources: IMF; BREE

bree.gov.au

China’s GDP

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

500

1000

1500

5

10

15

Marginal GDP Growth (LHS) GDP Growth Rate % (RHS)

Billion Yuan

%yr

Source: IMF

China Boom China Bust???GFC &

Rebound

bree.gov.au

Steel production growth to be steady

2013 2014 2015 2016 2017 2018 2019

200

400

600

800

1000

1200

1400

1600

China EU 28 Japan US India

Mt

Source: BREE

bree.gov.au

China’s monthly steel production

Jan-10 Jul-10 Jan-11 Jul-11 Jan-12 Jul-12 Jan-13 Jul-13 Jan-14

20

40

60

80

Mt

bree.gov.au

Australia’s iron ore exports

Sources: ABS; BREE

199

199

200

200

200

200

200

200

200

200

200

200

201

201

201

201

201

200

400

600

800

20

40

60

80

100

volume value (right axis)

Mt2013–14A$b

bree.gov.au

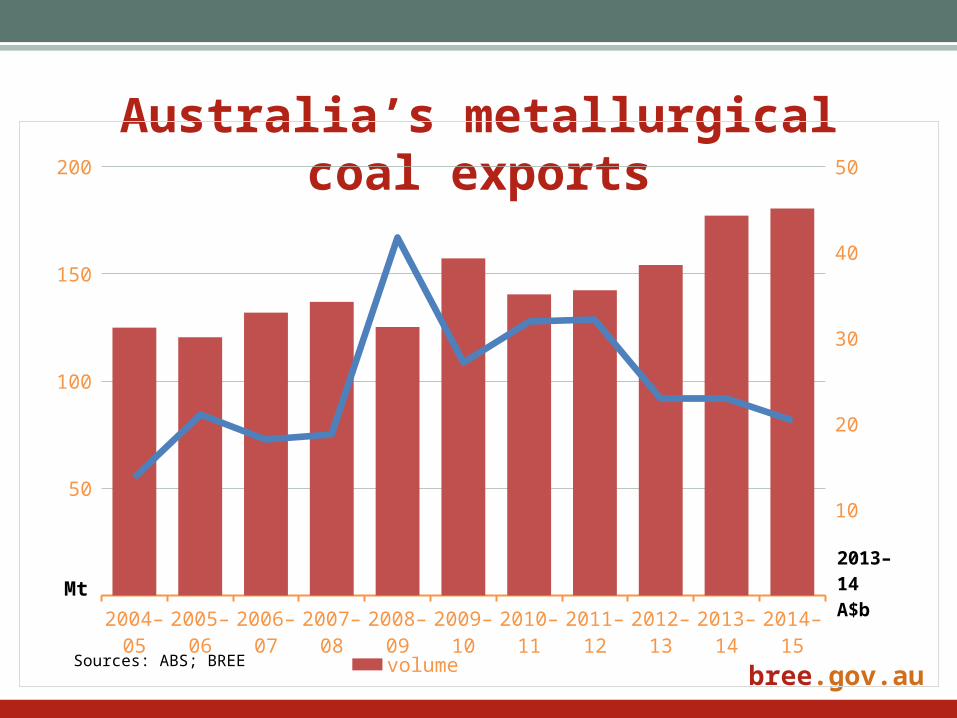

Australia’s metallurgical coal exports

Sources: ABS; BREE

2004–05

2005–06

2006–07

2007–08

2008–09

2009–10

2010–11

2011–12

2012–13

2013–14

2014–15

50

100

150

200

10

20

30

40

50

volume value (right axis)

Mt

2013–14A$b

bree.gov.au

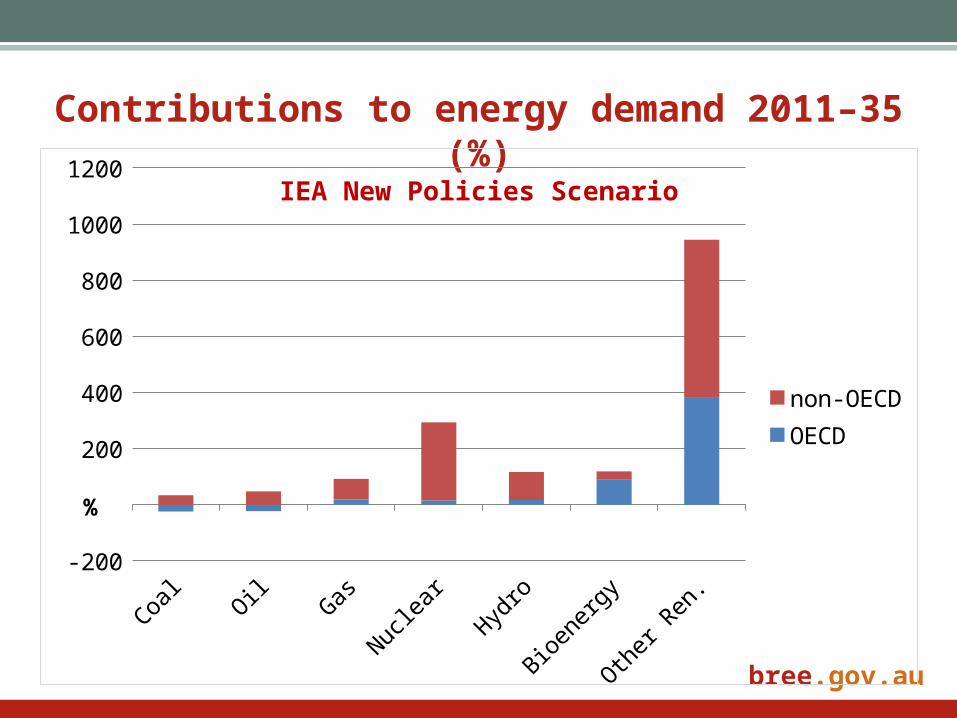

Contributions to energy demand 2011–35 (%)

IEA New Policies Scenario

Coal

OilGas

Nucle

ar

Hydro

Bioe

nerg

y

Other

Ren

.-200

200

400

600

800

1000

1200

non-OECDOECD

%

bree.gov.au

Contributions to energy demand 2011–35 (Mtoe)

IEA New Policies Scenario

Coal

OilGas

Nucle

ar

Hydro

Bioe

nerg

y

Other

Ren

.-500

500

1000

1500

non-OECDOECD

Mtoe

bree.gov.au

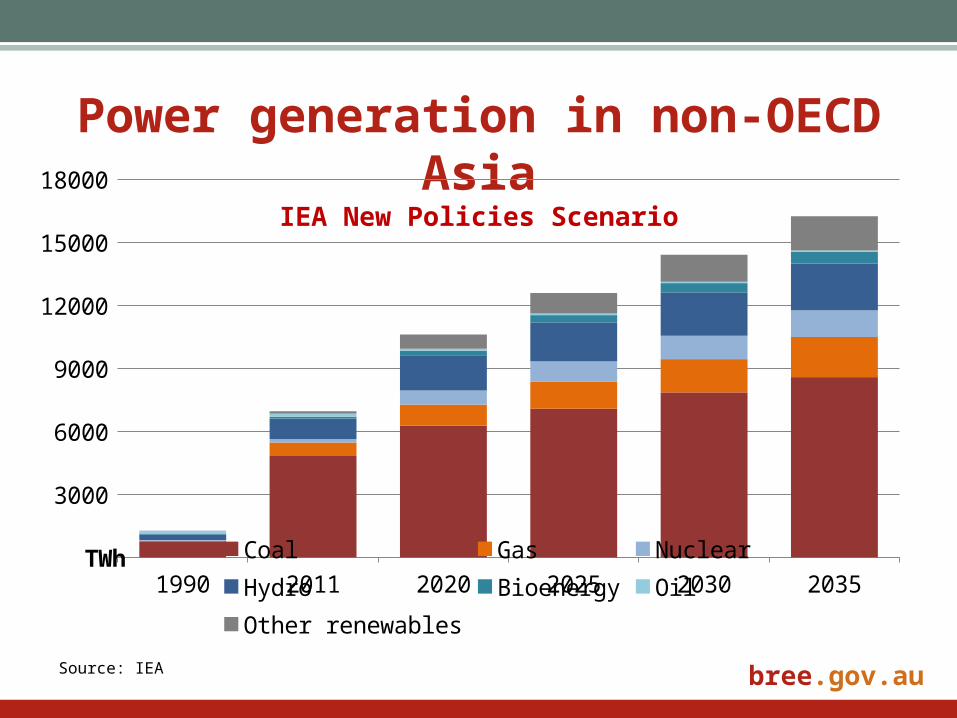

Power generation in non-OECD Asia

IEA New Policies Scenario

1990 2011 2020 2025 2030 2035

3000

6000

9000

12000

15000

18000

Coal Gas Nuclear HydroBioenergy Oil Other renewables

TWh

Source: IEA

bree.gov.au

China’s electricity generation

Jan-

96

Jan-

98

Jan-

00

Jan-

02

Jan-

04

Jan-

06

Jan-

08

Jan-

10

Jan-

12

Jan-

14

200

400

600

Thermal Hydro NuclearWind Other

Billion kWh

Electricity generation has

been increasing rapidly

and will continue to grow

Thermal (coal and gas)

sources account for the

bulk of generation

Inertia in the energy

system will prevent any

rapid change in

generation mix

bree.gov.au

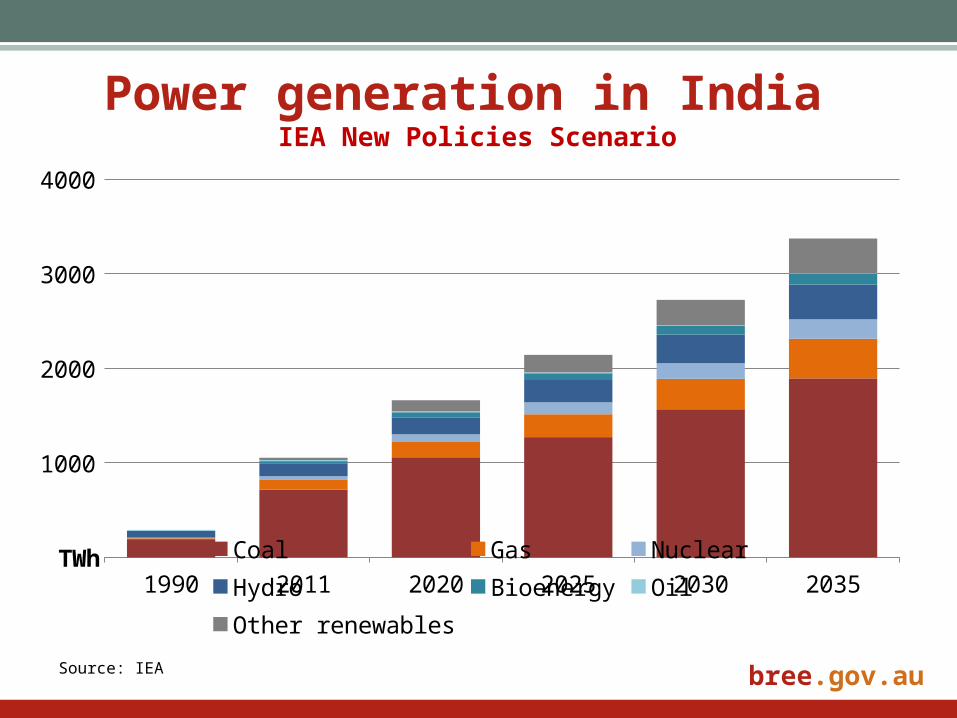

Power generation in India IEA New Policies Scenario

1990 2011 2020 2025 2030 2035

1000

2000

3000

4000

Coal Gas Nuclear HydroBioenergy Oil Other renewables

TWh

Source: IEA

bree.gov.au

Australia’s thermal coal exports

Sources: ABS; BREE

2004–05

2005–06

2006–07

2007–08

2008–09

2009–10

2010–11

2011–12

2012–13

2013–14

2014–15

-50

50

150

250

10

20

30

volume value (right axis)

Mt2013–14A$b

bree.gov.au

The production phase to increase export earnings

2008–09

2009–10

2010–11

2011–12

2012–13

2013–14

2014–15

2015–16

2016–17

2017–18

2018–19

40

80

120

160

200

240

280

energy resources

2013-14A$b

bree.gov.au

Contact

Wayne Calder

Deputy Executive Director

Bureau of Resources and Energy Economics

02 6243 7718