Brand Equity in the Canadian Coffee Shop Industry -...

42

The Importance of Brand Equity in Coffee Shop Chains - A Comparative Analysis of Tim Hortons and Starbucks in Canada May 2013 Author: Tenna Heesch Jørgensen Exam Number: 401692 Supervisor: Polymeros Chrysochou Department of Business Administration Aarhus University Characters: 84,249

Transcript of Brand Equity in the Canadian Coffee Shop Industry -...

The Importance of Brand Equity in Coffee Shop Chains

- A Comparative Analysis of Tim

Hortons and Starbucks in Canada

May 2013

Author: Tenna Heesch Jørgensen

Exam Number: 401692

Supervisor: Polymeros Chrysochou

Department of Business Administration

Aarhus University

Characters: 84,249

Aarhus University Spring 2013

Page 2 of 42

Abstract The aim of the thesis is to investigate which dimensions explain brand equity as well as which of

these dimensions affect brand equity the most. The theory will be applied to two competing brands; a

domestic brand with great market share and a global brand that both operate in the same industry.

The motivation for the investigation lies in the fact that the world is a global marketplace enabling

brands to compete in many markets and industries at once. However, it is unclear whether or not it is

an advantage to be a global company when competing with local companies for the same market

share. In this connection the thesis will be researching which dimensions contribute in building

strong brand equity with a focus on a comparative analysis of the Canadian coffee-shop chain, Tim

Hortons, and the American chain, Starbucks, in Canada. It will also investigate which of these two

brands has the strongest brand equity as well as which dimensions are most important in contributing

to strong brand equity for the Canadian customer. The analysis will be put in relation to the two

brands’ respective market shares in the Canadian foodservice industry where Tim Hortons is the

leading brand and Starbucks holds a smaller share of the market.

In order to give an answer to the outlined problem different theories of brand equity will be

investigated and David A. Aaker’s work will be used as the basis for the analysis of brand equity.

Aaker suggests that five measures explains brand equity; awareness, loyalty, perceived quality,

associations and market behavior. The Canadian foodservice industry will also be researched and the

two brands’ history and relationship to the industry will be studied. A quantitative method was used

in order to investigate the brand equities of the two brands and a questionnaire based on Aaker’s

brand equity theory was send out to Canadian students. The data was analyzed using paired sample t-

tests in order to compare the variables across the two brands and factor analysis was used to group

variables in the association dimension of brand equity. Lastly, two regression analyzes were used to

determine which dimensions explained the two brands’ brand equities.

It was found that the two brands differed significantly on the dimensions of awareness, loyalty and

perceived quality where Tim Hortons had better awareness and loyalty and Starbucks was

considered having a higher perceived quality. The two brands also differed significantly on all

associations except two; they were both associated with being reliable and popular. It was however

found that no significant differences existed between the two brands’ brand equities as well as

loyalty was the only significant dimension explaining brand equity for both brands. Since brand

equity did not seem to explain the two brands’ respective market shares in the foodservice industry,

Aarhus University Spring 2013

Page 3 of 42

other alternatives to this question is discussed in the thesis. It was however discovered that though

Starbucks had a low market share in the overall foodservice industry in Canada, the brand was the

leader in the specialty coffee section of the industry. One suggestion provided in the thesis on Tim

Hortons’ high market share, is that due to the brand’s high awareness level in combination with its

consistent quality and offering good value for money, consumers choose to purchase their coffee

shop products from Tim Hortons on a regular basis. On the other hand, Starbucks’ associations

indicate a high class, modern and global-minded brand with high service levels which could fit better

with the associations of a specialty coffee shop. These associations combined with Starbucks not

offering good value for money could lead to consumers making occasional coffee shop visits to the

brand’s facilities and therefore also explain the brand’s low market share of the foodservice industry

and high share in the specialty coffee section. The thesis concludes that the two brands do differ

significantly from each other on Aaker’s dimensions constituting brand equity though no significant

difference was found in their respective brand equities. Also based on the analysis it is concluded

that only the loyalty dimension is significant in explaining both brands’ brand equity in Canada. It is

lastly concluded that Starbucks has not been able to compete with Tim Hortons in the overall

foodservice industry in Canada but has been able to distinguish its brand from Tim Hortons in the

specialty coffee section

Aarhus University Spring 2013

Page 4 of 42

Table of Contents Abstract ............................................................................................................................................................. 2

Table of Contents .............................................................................................................................................. 4

1 Introduction ............................................................................................................................................... 6

1.1 Problem Statement ............................................................................................................................. 6

1.2 Content .............................................................................................................................................. 6

1.3 Assumptions and Delimitations ......................................................................................................... 7

2 The Importance of Branding ...................................................................................................................... 7

3 Brand Equity .............................................................................................................................................. 9

3.1 The Importance of Brand Equity ....................................................................................................... 9

3.1.1 Value for the Firm ..................................................................................................................... 9

3.1.2 Value for the Consumer ........................................................................................................... 10

3.2 Differences in Measuring Brand Equity between FMCG and the Service Industry........................ 11

3.3 The Brand Equity Ten Model .......................................................................................................... 12

3.4 Alternative Measures of Brand Equity ............................................................................................ 14

4 The Consumer Foodservice Industry in Canada ...................................................................................... 15

4.1 Tim Hortons ..................................................................................................................................... 16

4.2 Starbucks ......................................................................................................................................... 17

5 Analysis ................................................................................................................................................... 18

5.1 Procedure and Method ..................................................................................................................... 18

5.2 Analysis of Data .............................................................................................................................. 19

5.2.1 Socio-Demographics ............................................................................................................... 19

5.2.2 Awareness measures ................................................................................................................ 20

5.2.3 Loyalty measures ..................................................................................................................... 21

5.2.4 Perceived Quality .................................................................................................................... 22

5.2.5 Associations ............................................................................................................................. 23

5.2.6 Brand Equity ............................................................................................................................ 26

5.3 Regression Analysis ........................................................................................................................ 26

Aarhus University Spring 2013

Page 5 of 42

5.3.1 Tim Hortons ............................................................................................................................. 26

5.3.2 Starbucks ................................................................................................................................. 28

5.3.3 Conclusion on Analysis ........................................................................................................... 29

5.4 Limitations of the Data .................................................................................................................... 29

6 Discussion ................................................................................................................................................ 30

6.1 Future Research ............................................................................................................................... 33

7 Conclusion ............................................................................................................................................... 34

8 Bibliography ............................................................................................................................................ 37

9 Appendix A - Questionnaire .................................................................................................................... 39

Aarhus University Spring 2013

Page 6 of 42

1 Introduction Every company in today’s business world wishes to establish brand equity in order to set itself apart from

competition as well as to increase firm value. As defined in previous research: “Strong brands enjoying high

brand equity can help managers to relish higher margins, greater customer loyalty, less vulnerability to

competitive attacks, […].” (Gill & Dawra 2010, p. 189). It is therefore important for a company to be aware

of the factors affecting its brand equity in order to stay on top in a competitive environment.

With today’s open markets, global companies have the chance to set themselves apart from domestic

competition, and thereby potentially become market leaders in more than one country. However, it is not

always possible for these companies to gain market share and compete with the local companies, even

though they are successful in other foreign countries. This could be caused by many things, e.g. that the

global company does not adjust to local customs, or due to a local company’s strong brand equity in the

domestic community. This could be the case in the Canadian foodservice industry where the Canadian

company, Tim Hortons, controls 18.2% of the market while the globally successful company, Starbucks,

only sits on approximately 3% of the Canadian market (Euromonitor 2012b). This paper will therefore be

searching for a reason why this is the case in Canada, and it will investigate it on the grounds of the

companies’ respective brand equities in Canada.

1.1 Problem Statement

The paper will investigate which dimensions contribute in building strong brand equity. The focus will be on

a comparative analysis of the Canadian coffee-shop chain Tim Hortons and Starbucks in Canada. It will also

investigate which of these two brands has the strongest brand equity, as well as which dimensions are most

important in contributing to strong brand equity for the Canadian customer.

1.2 Content

The first section of the paper states the purpose and the reasoning behind the chosen subject of the study. The

second section of the paper will explain the background of branding and why it is important for companies to

be aware of their brand. The third section will go in further detail with brand equity and the drivers behind it

in order to be able to research the brand equities of Tim Hortons and Starbucks, and will also put brand

equity in relation to the marketing mix of both products and services. Different researchers’ works on brand

equity will be discussed in order to give a broader sense of what research has been done in the field of brand

equity. A model explaining and measuring brand equity will be discussed in this section as well. The fourth

section in the paper will introduce the brands Tim Hortons and Starbucks, and their relation to the Canadian

foodservice industry will be investigated. The fourth section will analyze the two brands’ brand equity based

on a questionnaire answered by Canadian consumers, and will be investigating the differences in the two

brands’ equity drivers in order to answer the problem statement outlined in the first section. The fifth section

will analyze the questionnaire results using paired sample t-tests, factor analysis as well as perform two

Aarhus University Spring 2013

Page 7 of 42

regression analyses with brand equity as the dependent variable. The last sections will discuss the results

based on a comparison of the theoretical sections and the results of the questionnaire, and a conclusion on the

paper in its entirety will end the paper.

1.3 Assumptions and Delimitations

The paper does not deal with all possible explanations and models of brand equity since there are many

researchers investigating it, and many explanations can be found in the literature. The paper will therefore be

concentrating on one of the main researchers’ work on brand equity, David A. Aaker, and two other articles

will be used and their models discussed in the paper, though only Aaker’s model is used in the analysis done

in the paper.

Another important delimitation of this paper is that it does not distinguish between coffee and food purchases

when analyzing the brand equity of Tim Hortons and Starbucks, even though their respective selections vary.

This is done for simplicity’s sake which means that the questionnaire states “coffee shop visits”1 instead of

clarifying whether it was a coffee or food purchase. It is believed that this delimitation will not affect the

outcome of the analysis since consumers purchase both food and coffee at both shops, as well as the

companies belong to the foodservice industry in Canada.

Many scholars have written papers evaluating the different theories which help enlighten the weaker points

of the used theories. Though many articles exist on the subject, this paper will only be using one (Gill &

Dawra 2010) since many critique the same researchers and their theories. The article is chosen since it

presents both Aaker’s and Keller’s different viewpoints as well as the weaknesses and strengths of both

researchers. The article is also comprised of a study where the dimensions of brand equity are investigated

and discussed which can help put the results of the analysis done in this paper into perspective.

It is also acknowledged that McDonald’s is a third great player in the Canadian consumer foodservice

industry, but it has been decided not to integrate this into the study since it first recently began focusing on

coffee beverages with the opening of McCafé.

2 The Importance of Branding A brand is defined in many ways, but a commonly accepted definition is:

“A name, term, sign, symbol, or design, or combination of them which is intended to

identify the goods and services of one seller or group of sellers and to differentiate them

from those of competitors.” (Kotler in Keller 1993, p. 2)

1 See Appendix A

Aarhus University Spring 2013

Page 8 of 42

Another, different interpretation of the term brand is found from the Chartered Institute of Marketing which

sees the brand as a symbol of the consumers’ experiences with a company’s product and/or services (Kotler

et al. 2009). This definition mainly focuses on the consumers and how they distinguish a company from

other companies. It stresses that a brand is an asset that companies cannot entirely control since it is up to the

consumers to interpret the signals and symbols developed by the companies which are all intended to

strengthen the brand names. In line with this statement is the fact that “brands are often used as symbolic

resources for the construction and maintenance of identity” (Kotler et al. 2009, p. 426). This means that

branding a product is not merely about the product in itself; it is also about what the product should represent

and what associations it should reflect. An example of this could be the sports brand Nike; consumers do not

buy Nike because it is the best product or gives the best value for money. They buy Nike sports shoes

because wearing them in a public forum says something about the consumer as a person. In other words, it is

an individual statement expressed through the purchase of a brand.

A brand can also be seen as one of the most important assets a company has since it is a resource that creates

value or equity to the company (Brodie 2009). A strong and consistent brand identity can provide a company

with a strong position as well as a strong identity in the market the company operates in which makes it

easier for consumers to remember and connect with the brand (Aaker 2002). Though a brand creates value to

a company, it does take time for it to be expressed in the company’s statements. It is not developed overnight

which can potentially be problematic because marketing managers are often evaluated on their short-term

performances and therefore some managers ignore the importance of building up a strong brand due to the

lack of quick results (Aaker 1991).

Another important aspect of branding is the role it performs for consumers and for companies respectively

(Kotler et al. 2009). For consumers, a brand can signal a certain level of quality which makes it easier for a

consumer to know the level of satisfaction he/she will obtain when buying a given brand. It will also

decrease time spent during shopping since a brand represents a given set of associations in the minds of the

consumers (Aaker 1991). Shopping known brands also reduces the perceived risks with the purchase since

the consumer already knows about the product and what to expect from it. For a company, a brand provides

legal protection of unique features as well as the brand name; these can all be protected by trademarks

(Kotler et al. 2009, p. 428). A strong brand with loyal customers also creates a more predictable demand

forecast which reduces uncertainty in the production. In line with loyalty, consumers may be willing to pay a

higher price for the products or services which creates a higher profit margin for the company. These are just

a few advantages for consumers and companies that are directly related to brands and the branding of them.

It can therefore be concluded that brands are important because they set a company apart from its

competitors and thus ease the processes involved for consumers when deciding on buying a product, as well

as decrease uncertainty for the company due to more stable forecasts.

Aarhus University Spring 2013

Page 9 of 42

3 Brand Equity Brand equity has many definitions in the existing literature, but one of the most renowned definitions is

David A. Aaker’s: “a set of assets and liabilities linked to a brand, its name and symbol, that add to or

subtract from the value provided by a product or service to a firm and/or that firm’s customers.” (Aaker

1991, p. 15). A more financially based definition of brand equity is set forth by Simon & Sullivan (1993);

this definition states that brand equity is found when a firm’s book value is subtracted from the brand value,

meaning it is the extra value added to the company due to its brand.

There are many theories on the subject brand equity, and many researchers have written articles discussing

the different theories’ strengths and weaknesses. In this research paper, the Brand Equity Ten model (Aaker

2002, p. 319) will be introduced and discussed since it will form the basis of the research done in the paper.

This model has been chosen due to its ability to be used in quantitative research and because Aaker has

strived to make a standard measure of brand equity (Gill & Dawra 2010). Another researcher’s work that

will be commented on in the paper is Kevin L. Keller’s since he has a different approach of explaining brand

equity which involves both direct and indirect measures (Keller 1993).

Both authors’ focus is on consumer-based brand equity. This is relevant for the research presented in this

paper which will analyze a questionnaire answered by Canadian consumers, and the theoretical background

set out in this paper will help with understanding how to interpret the answers in connection with the drivers

behind brand equity.

3.1 The Importance of Brand Equity

Brand equity is important since financial measures tend to focus only on short term results which can lead to

brand building activities being reduced in order to obtain fast financial results in the short run. Especially

sales promotions, e.g. short term price reductions, are proved to diminish brand equity over time, even

though it creates short term financial gains (Yoo, et al 2000). Therefore having clear and easily

understandable brand strength measures will make it easier to justify why brand building activities should

not be terminated in favor of greater financial outcomes in the short run (Aaker 2002). If cutting down on

brand strengthening measures continues over a longer period of time, the profits of the firm risk being

reduced as the brand is no longer as strong as it once was. This is a reason why brand equity is important:

because it can maintain and increase profits in the longer run. Another reason why brand equity is an

important element in the product and service markets today is because it adds value to both the firm as well

as to the customers (Aaker 1991).

3.1.1 Value for the Firm

Aaker (1991) states that for a company, the added value can be found in e.g. a competitive advantage, brand

loyalty or in increased efficiency and effectiveness of marketing programs. A competitive advantage is

Aarhus University Spring 2013

Page 10 of 42

defined as: “a company’s ability to perform in one or more ways that competitors cannot or will not

match.”(Kotler et al. 2009, p. 373). According to Aaker (1991), brand equity can provide a firm with a

competitive advantage in the sense that competitors cannot match the given performance because they lack

brand equity to do so. The competitive advantage could be brand loyal customers as they will not be willing

to switch to a competitor, even though their prices are better. With strong brand equity, firms have extension

opportunities as well and can explore new markets with their brand name being the entry ticket to the new

market. This means that a brand with high brand equity does not only constitute a threat to competitors in its

own market, but also potentially in other markets. As mentioned in the beginning of the section, brand equity

also gives value to the firm by providing brand loyalty. According to Aaker (2002), brand loyalty gives a

firm time to respond to competitor threats as well as it attracts new customers. The last mentioned value-

adder which was the efficiency and effectiveness in marketing plans means that an established brand with

high brand equity does not need to prove itself through their marketing. The marketing plan is to ensure that

consumers remember and recall the brand in purchase decisions regarding the product range that the product

is part of (Aaker 1991).

3.1.2 Value for the Consumer

It is not only companies that can benefit from high brand equity; consumers greatly benefit from it in their

everyday lives as well. According to Aaker (1991), the value brand equity can provide consumers are: easier

processing of information, confidence in the purchase decision and use satisfaction.

When a consumer is bombarded with offers, price promotions and overloads of information on brands in the

supermarket after a long day on the job, it is easier for a consumer to choose a known brand they can

recognize and recall from memory. This lessens the processing of information since they already know about

the attributes of the product, and it makes them confident in the purchase decision as well. The consumer

knows what to expect from the product and also most likely knows beforehand whether or not the product is

liked in the household. This is in line with the use satisfaction that high brand equity can provide since the

consumer again knows what he/she likes about the product and whether or not the attributes of the product

are suitable for the intended use of it. All in all, high brand equity lessens the insecurities consumers can

experience in a purchase situation since they know of the brand and the value for the consumer is to know

he/she will be pleased with the purchase (Aaker 1991).

In conclusion, it can be argued that brand equity is important due to the value it provides to both firms and

consumers. This is respectively seen in competitive advantages, brand loyalty and efficiency and

effectiveness in marking plans as well as in easier information process, confidence in the purchase decision

and use satisfaction.

Aarhus University Spring 2013

Page 11 of 42

3.2 Differences in Measuring Brand Equity between FMCG and the Service Industry

The difference between a fast-moving consumer good (FMCG) and a service is the tangible product. The

consumer has a physical product to relate to the brand of a FMCG-company whereas other factors play a role

to the consumer when evaluating the brand of a service company. The marketing mix is extended when

marketing services as opposed to marketing FMCG. The marketing mix is used when assessing the tools that

can be used to influence buyer decisions (Kotler et al. 2009). When marketing FMCG, the first 4P’s of the

marketing mix is often sufficient to use, and these are: product, place, price and promotion (Kotler et al.

2009). From the studies of the marketing mix’s effect on brand equity it can be determined that:

“…managers must invest in advertising, distribute through retail stores with good images, increase

distribution intensity, and reduce frequent use of price promotions.” (Yoo, et al 2000, p. 208). The reason

advertising has an effect on brand equity is because it is first of all positively related to perceived quality,

and secondly it shows that the firm is investing in its brand (Yoo, et al 2000). The place and intensity of

distribution also has a great impact on brand equity according to Yoo et al. (2000) since consumers only

show loyalty when there is consistency between the product and the store image. The distribution intensity is

also important since consumer satisfaction will increase when a product is available in many stores due to the

convenience of less travel and search time for the consumer (Yoo, et al 2000). Price promotions will reduce

brand equity in the long run, even though it creates financial gains in the short run. It decreases brand equity

since price promotions can indicate low-quality brand image as well as create consumer confusion between

expected and observed prices which leads to an image of unstable quality (Yoo, et al 2000). The studies of

Yoo et al. (2000) also shows that price has no significant correlation to the dimensions of brand equity,

meaning that even though price indicates high quality, it does not create loyalty nor does it increase brand

awareness.

When it comes to services, another three P’s are necessary, and therefore people, process and physical

evidence have been added to the 4P’s framework. The reason for adding the last three P’s can be found in the

existing literature: “…in case of tangibles, the product represents the brand but in case of intangibles, the

whole company is treated as the brand.” (Nath & Bawa 2011, p. 137). Since the whole company represents

the brand, it is necessary to include the employees who represent the brand, the stores where the services are

bought or presented, as well as the processes of obtaining the given services. According to Tan (2012),

service quality is of great importance when it comes to consumer-based brand equity in the service industry

since it is the consumers’ perceptions of the service providers that can lead to strong brand equity.

According to Schmenner (1986) in Tan (2012), there are four types of services: service factories, service

shops, mass services and professional services. They define restaurant chains as service shops which have

two distinctive features: high level of consumers’ interaction with the service processes meaning service

shops relies heavily on their human capital as well as providing customized business services (Tan et al.

2012). This means that customers can ask for additional services or for particular attention which is not as

Aarhus University Spring 2013

Page 12 of 42

Source: Kotler et al. 2009 and Tan et al. 2012

common in a fast-moving consumer goods shop (Tan et al. 2012). It is stated that: “…service quality of a

specific brand is found to be a vital element that affects the creation of brand equity in the service shop

business.” (Tan et al. 2012, p. 71). This proves that the extra 3P’s in the marketing mix do have a significant

effect on brand equity in the service sectors. The dimensions of service quality are tangibles, responsiveness,

empathy, assurance, recovery and knowledge (Tan et al. 2012). These translate into the added 3P’s of the

marketing mix framework as seen in table 1 below.

As seen in table 1, responsiveness, empathy and knowledge can be categorized in the people dimension of

the marketing mix as they represent important elements, employees of a service shop must be given or

already possess in order to provide excellent customer services. Recovery is found in the process dimension

since it is important to implement processes that can restore errors in a correct and fast manner since service

shops rely on offering great, consistent service to customers. Tangibles and assurance is found in the

physical evidence dimension since the servicescape is of great importance in service shops because it is the

only tangible that can be associated with the brand.

It can be concluded that when dealing with service companies the 7P’s of the marketing mix has to be

assessed. Furthermore, the actual effect of the extra three P’s in the marketing mix on brand equity is found

to be the service quality since it has a significant effect on certain brand equity factors. The actual effects are

found in the dimensions of service quality portrayed in table 1 which all relates to people, process and

physical evidence in the marketing mix.

3.3 The Brand Equity Ten Model

It is necessary to have a model measuring brand equity since, as stated earlier, most measures of how well a

firm is doing are financial (Aaker 2002). The Brand Equity Ten model has therefore been a useful tool and

has been discussed and used by many researchers.

Table 1 Dimensions of service quality categorized into the added 3P's in the marketing mix

Aarhus University Spring 2013

Page 13 of 42

Source: Aaker, 2002, p. 319

In figure 1, Aaker’s Brand Equity Ten model (Aaker 2002, p. 319) is shown. It is based on five dimensions

that all reflect the strength of brand equity. The first four dimensions which are the loyalty, perceived

quality/leadership, associations/ differentiation and the awareness measures indicate the customers’

perceptions of the brand whereas the last dimension, market behavior, represents market-based behavior

(Aaker 2002). When using the model, only the dimension important to the given research should be used

since not all dimensions are of equal importance in every study.

Under loyalty measures, price premiums and satisfaction are found. Price premiums indicate the amount a

customer is willing to pay in order to obtain a certain brand in comparison with a competing brand that offers

similar or fewer benefits (Aaker 1991). Satisfaction measures how willing a customer is to stick to a brand,

and questions such as: “Does the product or service meet your expectations?” (Aaker 2002, p. 323) can be

asked. The issues with these measures are, firstly, that in consumers’ minds a price premium will always be a

comparison with competing firms, and therefore not only one price premium exists for one given brand.

When measuring satisfaction, it cannot be used on consumers who have not tried the product or service, and

can therefore only measure the brand equity within the customer base (Aaker 2002). Issues regarding

perceived quality measures are that consumers compare the quality of the given company’s product or

service with either competitors or might even compare it to a whole industry, and this comparison is

unknown to the researcher. It is also important to keep in mind that loyal customers will always be more

Figure 1 David A. Aaker’s Brand Equity Ten model

Aarhus University Spring 2013

Page 14 of 42

biased when it comes to perceived quality than the average customer will be (Aaker 2002). According to

Aaker (2002), the associations can be measured in three ways: brand-as-product, brand-as-person and brand-

as-organization. The first deals with a brand’s value and can be measured by figuring out whether or not the

brand is good value for money. When doing this, it is important to set a frame for comparison, for instance

stating: “among comparable brands”(Aaker 2002, p. 326). The second measure is good to use when the

investigated brands have minor physical differences and can be important for brands which: “have

personalities, are consumed in social settings and makes statements about those who drink [it].” (Aaker

2002). An example of this could be Coca Cola and Pepsi since the taste has minor differences, and it is more

or less the statement the two drinks have that determines which one a consumer chooses to purchase. This

measure should only be used with brands who position themselves as being personality brands. The last

measure is only relevant for organizations whose organization is visible (Aaker 2002). Awareness can be

measured on many different levels; two of the more important ones being recognition and recall of brands.

The issue with this measure is to use the most appropriate one for the given brands or product groups (Aaker

2002). The market behavior can measure the market share and can: “…provide a valid and sensitive

reflection of the brand’s standing with customers.”(Aaker 2002, p. 331).

It can be concluded that Aaker uses both customer-based dimensions as well as a market-related dimension

in order to measure the strength of brand equity in his model. The model consists of ten items, each

representing one of the five dimensions, and the dimensions should only be used in research when they are of

relevance.

3.4 Alternative Measures of Brand Equity

Another interpretation of brand equity and how to measure it is found in Kevin L. Keller’s work. He defines

brand equity as: “The differential effect of the brand knowledge on consumer response to the marketing of

the brand.” (Gill & Dawra 2010, p. 190). In this approach, brand awareness and brand image measures the

strength of brand equity (Gill & Dawra 2010) which means the focus is entirely customer-based, as opposed

to Aaker who also includes the last dimension of the market behavior to his model. In this measure of brand

equity, both indirect and direct measures are used. The indirect measure tries to assess the sources of brand

equity in terms of brand recognition and brand knowledge whereas the direct measure measures brand equity

by assessing the impact of brand knowledge on consumers’ response to the marketing program (Gill &

Dawra 2010). The first dimension of Keller’s model which was brand awareness, is an essential part of brand

equity. It is important that consumers think of the given brand when thinking of the product category it

belongs to while it can also affect the decision of buying the brand, even though the consumer knows no

other brand associations (Keller 1993). The second dimension which was brand image, is defined as:

“…perceptions about a brand as reflected by the brand associations held in consumer memory.” (Keller

1993, p. 3). The brand associations are divided into three categories: attributes, benefits and brand attitudes.

Aarhus University Spring 2013

Page 15 of 42

They respectively represent the descriptive features of the product or service, the personal value a consumer

attaches to the product or service attributes and the consumer’s overall evaluation of the brand (Keller 1993).

The first two attributes determine whether or not the overall brand attitude is positive or negative, though

brand attributes are only valued and interpreted by consumers if the attributes are important to them (Keller

1993). Therefore marketers have to be aware of what product or service attributes are important for the

consumers because focusing on these attributes can increase brand equity.

Gill and Dawra (2010) classifies Aaker and Keller into two different schools of thought; Aaker belongs to

the school that defines brand equity in terms of a set of assets whereas the school Keller is part of measures

brand equity as: “…the additional preference a consumer has for a branded product over a similar no-name

product…” (Gill & Dawra 2010, p. 189). In Gill and Dawra’s (2010) study, they attempt to combine the two

schools’ measures of brand equity since flaws are found in both models. Keller’s measure is stated to only

provide a framework for measuring brand awareness and brand image, but no actual measure of brand equity

is given (Gill & Dawra 2010). Aaker’s Brand Equity Ten model: “…only provides an indication towards a

set of items that can contribute to brand equity.” (Gill & Dawra 2010, p. 191). Through their study of the

toothpaste product category, they are able to conclude that Aaker’s dimensions only explain 34.9 percent of

the brand equity (Gill & Dawra 2010). The results of their study also show that brand awareness has an

indirect impact on brand equity through the dimension brand image. This means that brand awareness and

brand image are not two distinct dimensions of brand equity, but rather that brand awareness leads to brand

image which in turn leads to brand equity (Gill & Dawra 2010). Therefore, through Gill and Dawra’s study,

it is shown that both models lack in measuring brand equity in the toothpaste product category, but it is

unknown whether or not this translates into other product or service categories.

It can be concluded that Keller’s model is more simplistic compared to Aaker’s five dimensions of brand

equity, though it has been proven through Gill and Dawra’s study that they are both insufficient in explaining

brand equity in the toothpaste product category.

4 The Consumer Foodservice Industry in Canada Canada can be defined as a coffee drinking nation as 64% of adult Canadians drink coffee every day, and the

coffee consumption in Canada has the fastest growth among coffee consuming countries (Euromonitor

2012b). The industry that will be examined in the paper is the Canadian foodservice industry with a focus on

the overall industry as well as the sectors: coffee, chained foodservices and cafés and bars2. The Canadian

consumer foodservice industry has, as all other industries, experienced a downturn on sales due to the

economic recession. However, in 2011, it experienced a recovery in sales growth due to a decrease in

economic uncertainty and improved consumer confidence, as well as an increase in demand for specialty

2 Also referred to as the specialty coffee section

Aarhus University Spring 2013

Page 16 of 42

coffees (Euromonitor 2012b). Since Canadians have already embraced coffee, and the country has one of the

highest consumptions in the world, innovation and growth in this industry will be difficult to continuously

improve. However, the section of the consumer foodservice industry that will experience the most growth in

the coming years is café and bars due to the increase in demand of specialty coffees (Euromonitor 2012b). A

trend in the industry is caused by the increased urbanization that is taking place in Canada these years; a

more fashionable urban setting of the servicescape is now necessary, and the new designs of the

servicescapes are designed to make customers stay longer at the establishments (Euromonitor 2012b).

As can be seen in table 2, Tim Hortons has a brand share of 18.2% which makes the brand the leading

chained foodservice in Canada whereas Starbucks comes in with a much smaller share of 2.3%. However,

when it comes to the cafés/bars section of the industry which is experiencing the greatest growth due to the

specialty coffee demand increase, Starbucks sits on 44.5% of the brand shares, and Tim Hortons is not to

find in this section. This could be due to the fact that Tim Hortons first launched specialty coffees in 2011

(Euromonitor 2012b). From table 2 it can also be seen that Starbucks has 7% of the brand shares when it

comes to coffee whereas Tim Hortons has 5.2% of the brand shares. They are both not the leaders in this

category of the industry since Starbucks has the 5th

largest brand share and Tim Hortons comes in 7th (Table 8

in Euromonitor 2013).

The Canadian consumer foodservice industry can be said to be in good conditions, though currently

recovering from the economic recession. Since Canadians are great coffee consumers, the market for coffee

products and services has almost reached its growth potential, but there has, however, been a stronger growth

in the demand of specialty coffees in later years. Tim Hortons has the greatest brand share in the industry

overall but when it comes to specialty coffee, Starbucks is the brand in control and with coffee in general, the

two companies’ brand shares are close.

4.1 Tim Hortons

Tim Hortons was founded in 1964 by the Canadian hockey player Tim Horton and is today the largest quick

service restaurant chain in Canada (www.timhortons.ca 2012). The store originally only offered coffee and

donuts, but has over the years expanded its product line into also including other baked goods and lunch

Table 2 Brand Shares of Tim Hortons and Starbucks in Canada

Sources: ¹ Table 9 in Euromonitor 2012b, ² Table 8 in Euromonitor 2012a, ³ Table 8 in Euromonitor 2013

Aarhus University Spring 2013

Page 17 of 42

options, including bagels and sandwiches (www.timhortons.ca 2012). Today, the chain has 3,295 stores

across Canada and is the leading company within the consumer foodservice industry and accounts for almost

11% of value sales (Euromonitor 2012d). Due to the increased demand in specialty coffees, Tim Hortons

introduced a new specialty coffee line in 2011as well as expanding its products into including smoothies and

a more varied, healthy breakfast selection (Euromonitor 2012d). Tim Hortons has experienced great success

in Canada and many Canadians refuse to buy other brands than Tim Hortons in the consumer foodservice:

“…Canadians have become proud and patriotic towards the brand which has

become a household name. A large section of the population has developed loyalty to

Tim Hortons which is further supported by the fact that the company involves itself in

the community in form of sponsored sports programmes for children, organizing

clean-up events across the country and various other fund-raising activities.”

(Euromonitor 2012d, p. 5)

It shows that Tim Hortons is not just a company serving coffee and food products, but is also a company that

cares for its community. This can be seen in the company’s mission statement which is to deliver superior

quality products for their guests which is done through leadership, innovation and partnerships

(www.timhortons.ca 2012). The vision for Tim Hortons is to be the quality leader in everything they do

which is the reason Tim Hortons has a store policy ensuring that brewed coffee is not served if it has been

ready for more than twenty minutes (www.timhortons.ca 2012).

It is not only the Canadian consumers who acknowledge Tim Hortons’ leading position in the Canadian

foodservice industry and the Canadian communities; the Royal Canadian Mint, who produces Canada’s

circulation coins, also acknowledge the importance Tim Hortons possesses: in 2004 Tim Hortons was the

sole distributor of the world’s first colored circulation coin which is made in order to “…remind Canadians

in a singular way of our proud role in world history and to honor those who made the ultimate sacrifice to

defend our freedom.” (www.timhortons.ca 2012, Press Releases). This illustrates the great presence the

brand has in Canada and that the brand is an incorporated part of Canadian history.

It can be concluded that Tim Hortons is the leading player on the Canadian foodservice industry, and it has a

great presence in the Canadian market with many outlets throughout the country and with many loyal

consumers.

4.2 Starbucks

Starbucks is a globally renowned brand with over 15,000 stores placed in 50 countries worldwide with the

first foreign store opening in 1987 in Canada (www.starbucks.ca 2013). Today, Starbucks has 1,120

operating stores across Canada and is ranked first in the cafés/bars sector with a 15% value share in sales and

holds 13% of the outlets in the sector (Euromonitor 2012a).

Aarhus University Spring 2013

Page 18 of 42

Starbucks’ mission statement is: “To inspire and nurture the human spirit – one person, one cup and one

neighborhood at a time.”(www.starbucks.ca 2013). Starbucks will do this through serving high quality

coffee, engaging with their customers and make them feel at home at the Starbucks stores (www.starbucks.ca

2013). Starbucks also strives to position itself as a “third place experience”, meaning the stores become the

place between home and work where consumers can meet and relax with friends (Euromonitor 2012c). This

is seen as one of Starbucks’ key objectives and has always been one of its strengths in the competitive

specialty coffee shop category. However, according to Euromonitor (2012c) Starbucks no longer just

competes with its competitors in this category as many foodservice operators want to profit from the increase

in demand of specialty coffees and offers these products at lower prices which is the case with Tim Hortons

and its launch of specialty coffees in Canada in 2011. According to Starbucks’ brand positioning, it is

important for Starbucks to localize its products, and therefore different blends and products are offered in

different countries (Euromonitor 2012c). In 2011, Starbucks removed “Starbucks Coffee” from its logo due

to: “…further expansion into the grocery channel with products that are unrelated to coffee, but is also a

testament to the company’s belief in the power of its brand.” (Euromonitor 2012c, p. 38). With this removal

of the brand name from the logo indicates a confidence in the brand having a strong presence in the countries

it operates in.

It can be concluded that Starbucks is a globally strong brand with strong values that customers can appreciate

and relate to. However, Starbucks is beginning to face competition from other categories within the

consumer foodservice industry and since Tim Hortons is the industry leader in the foodservice industry, the

shift in competition is of great relevance.

5 Analysis

5.1 Procedure and Method

The analysis will be based on Aaker’s Brand Equity Ten model where the four dimensions representing the

consumers’ perceptions of the brands were used in the questionnaire. As seen below in table 3, the brand

equity dimension consists of the variable “I like the brand XX” and will be used in the analysis as the

dependent variable in order to assess and interpret the four, independent dimensions which Aaker believes

are determining factors of brand equity. It is illustrated in table 3 how the questions from the questionnaire

will be used to analyze the dimensions of brand equity and brand equity itself. Respondents were asked to

rate the items on a 5-point Likert scale with 1 being “highly disagree” and 5 being “highly agree” or on a

bipolar scale with 5 points as well which is seen with the questions under associations in table 3.

Aarhus University Spring 2013

Page 19 of 42

Table 3 Question index

In this paper, brand equity is based on the respondents’ attitude towards the brand since consumers’ opinions

on the brand are part of brand equity and part of creating value for the brand and its company.

The first part of the analysis will compare Tim Hortons and Starbucks, based on paired sample t-tests in

order to find out whether or not significant differences exist in the different dimensions and the variables

belonging to the dimensions between the two brands. The variables in the associations dimension will be

grouped based on a factor analysis on each of the brands’ associations, and lastly a multiple regression

analysis on each brand will be conducted in order to see which dimensions predict most of the value of the

brand equity. The two regression models will be compared to detect whether or not it is the same dimensions

and variables determining the brand equity.

5.2 Analysis of Data

5.2.1 Socio-Demographics

The questionnaire was sent out to students as well as exchange students who either study or have been

studying at Wilfred Laurier University in Waterloo in the province Ontario in Canada. 85 responses were

received, and 62 of these were usable for further analysis. 54.8% of the respondents were Canadian while the

rest were of different origin which is due to exchange students also answering the questionnaire. The gender

distribution of the respondents is 80.6% females and 19.4% males which causes the sample to be skewed

Aarhus University Spring 2013

Page 20 of 42

towards female participants. Since the questionnaire has been sent to a university, all respondents are

classified as students where 67.7% are unemployed and 29% have a part-time job. The average age of

respondents is 21.4 years old. This means the results are only applicable to students and their opinions and

beliefs about Tim Hortons and Starbucks.

9.7% of the respondents never visit coffee shops, 45.2% of the respondents visit coffee shops 1-2 times a

week, 21% visits coffee shops 3-4 times a week, 6.5% visits coffee shops 5-6 times a week and 17.7% visits

them daily. This means that on average the respondents visits coffee shops once to twice a week. The result

from an independent sample t-test indicates that there are no significant difference between the 9.7%

respondents, who never visit coffee shops and the rest of the sample. It is therefore recognized that these

respondents occasionally visit coffee shops which could not be expressed in the questionnaire. The 9.7%

respondents are therefore kept in the sample for further analysis.

The analysis of the dimensions is done through paired sample t-tests in order to determine whether or not

there are significant differences between Tim Hortons and Starbucks. The differences can indicate a more

positive or negative attitude towards the two brands and can help determine which dimensions the

respondents favor the most when it comes to the brand equities of the two brands.

5.2.2 Awareness measures

When asked what coffee shops the respondents could recall, 51.3% had Tim Hortons as their first recalled

brand while Starbucks was the first recalled brand in 32.3% of the cases. Aaker (1991) describes this as the

brand being top-of-mind which is the strongest position a non-dominant brand can be in since it puts the

brand ahead of the game when it comes to competition. 93.6% recalled Tim Hortons as one of their first

three recalled brands while 79.1% of the respondents recalled Starbucks as one of their first three recalled

brands. Aaker (1991) states that when consumers are able to recall a brand from memory when thinking of a

given product group, it indicates a strong brand position for the given brand. From a paired sample t-test, it

can be determined that there is a significant difference in the recall of the two brands where Tim Hortons’

recall level is significantly3 higher than the one for Starbucks. All respondents were aware of both brands

when presented with a list of coffee shops existing in Canada. Therefore recall will be the variable

considered for further analysis of the awareness dimension.

It can be determined that significantly more respondents were able to recall Tim Hortons from memory than

Starbucks, though all respondents were able to recognize both brands.

3 Sig. (2-tailed) = 0.010

Aarhus University Spring 2013

Page 21 of 42

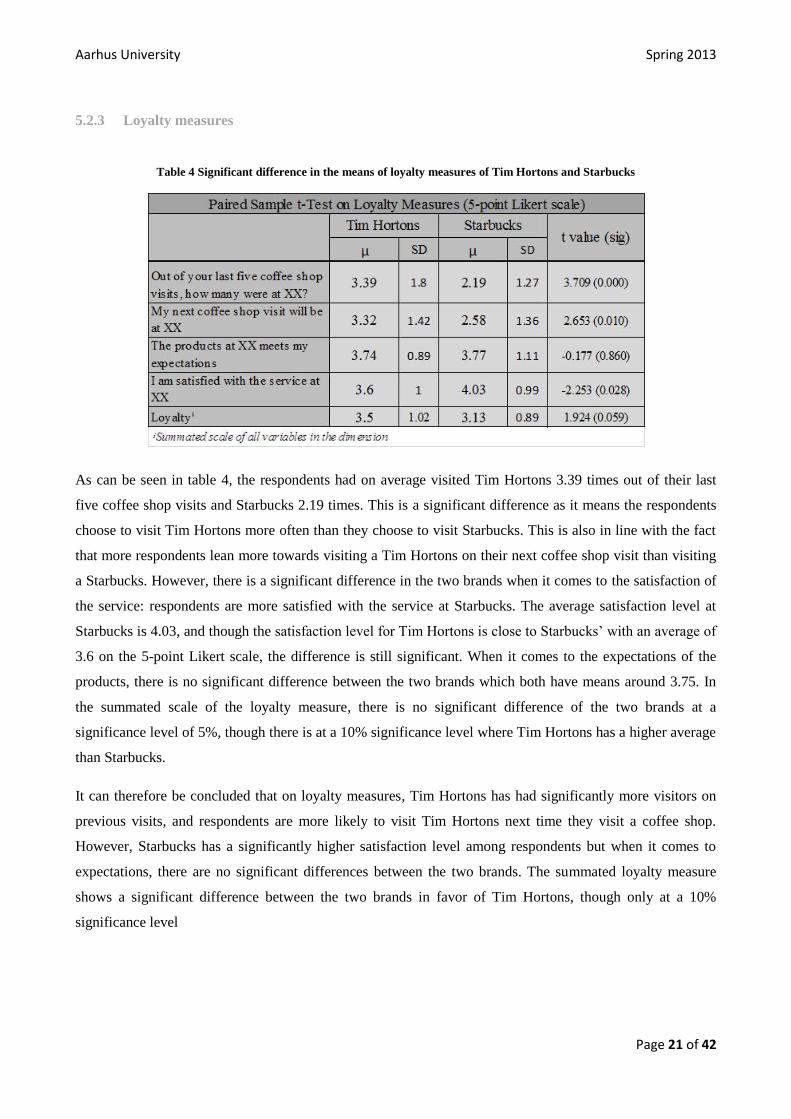

5.2.3 Loyalty measures

Table 4 Significant difference in the means of loyalty measures of Tim Hortons and Starbucks

As can be seen in table 4, the respondents had on average visited Tim Hortons 3.39 times out of their last

five coffee shop visits and Starbucks 2.19 times. This is a significant difference as it means the respondents

choose to visit Tim Hortons more often than they choose to visit Starbucks. This is also in line with the fact

that more respondents lean more towards visiting a Tim Hortons on their next coffee shop visit than visiting

a Starbucks. However, there is a significant difference in the two brands when it comes to the satisfaction of

the service: respondents are more satisfied with the service at Starbucks. The average satisfaction level at

Starbucks is 4.03, and though the satisfaction level for Tim Hortons is close to Starbucks’ with an average of

3.6 on the 5-point Likert scale, the difference is still significant. When it comes to the expectations of the

products, there is no significant difference between the two brands which both have means around 3.75. In

the summated scale of the loyalty measure, there is no significant difference of the two brands at a

significance level of 5%, though there is at a 10% significance level where Tim Hortons has a higher average

than Starbucks.

It can therefore be concluded that on loyalty measures, Tim Hortons has had significantly more visitors on

previous visits, and respondents are more likely to visit Tim Hortons next time they visit a coffee shop.

However, Starbucks has a significantly higher satisfaction level among respondents but when it comes to

expectations, there are no significant differences between the two brands. The summated loyalty measure

shows a significant difference between the two brands in favor of Tim Hortons, though only at a 10%

significance level

Aarhus University Spring 2013

Page 22 of 42

5.2.4 Perceived Quality

Table 5 Significant difference in the means of perceived quality measures of Tim Hortons and Starbucks

As it is seen in table 5, there are no significant differences in the means of the two brands when it comes to

having an overall better quality than their competitors. Tim Hortons and Starbucks respectively have an

average of 3.34 and 3.58 which indicates that respondents overall agree that the two brands have better

quality than their competitors. As mentioned previously in the paper, it is unknown whom the individual

respondents compare the brands to and if the respondents even compare the brands to the same competitors.

However since most respondents recalled the same coffee shops, it is assumed that the comparison to

competitors is somewhat similar among the respondents. When the two other questions relating to the

perceived quality dimension are investigated, it shows that there are significant differences between Tim

Hortons and Starbucks with Tim Hortons scoring lower on the scale “low quality/high quality” with an

average of 2.65 against an average of 4.3 of the quality at Starbucks. Tim Hortons’ average on “inconsistent

quality/consistent quality” is also significantly lower than the one for Starbucks. When summating the

variables, there is a significant difference between Tim Hortons and Starbucks when it comes to perceived

quality with the perceived quality of Starbucks being significantly higher than the one of Tim Hortons.

It can therefore be concluded that there is no significant difference between Tim Hortons’ and Starbucks’

overall quality being better than their competitors’, and that even though Starbucks has significantly higher

and more consistent quality than Tim Hortons. In total, Starbucks does have a significantly higher perceived

quality than Tim Hortons.

Aarhus University Spring 2013

Page 23 of 42

5.2.5 Associations

Table 6 Significant difference in the means of loyalty measures of Tim Hortons and Starbucks

There are significant differences in the means of all association measures between the two brands except on

“unreliable/reliable” and “unpopular/popular” where both brands are considered being popular with means

above 4 as seen in table 6 above. Tim Hortons offers better value for money, is more old-fashioned, more

local minded, more down to earth, has a less relaxed atmosphere than Starbucks as well as a lower service

level and it lacks more in customer service compared to Starbucks which is visualized below in figure 2.

Figure 2 Respondents’ associations of the brands Tim Hortons and Starbucks

Aarhus University Spring 2013

Page 24 of 42

The associations that distinct the two brands most from each other are, firstly, value for money where Tim

Hortons offers significantly better value for money according to the respondents. Secondly, Tim Hortons and

Starbucks differ in the minds of the consumers when it comes to being old-fashioned or modern where Tim

Hortons is seen as being significantly more old-fashioned than Starbucks. A reason for this could be the long

tradition of Tim Hortons in Canada, as well as the fact the brand only recently introduced specialty coffees in

its coffee beverage range.

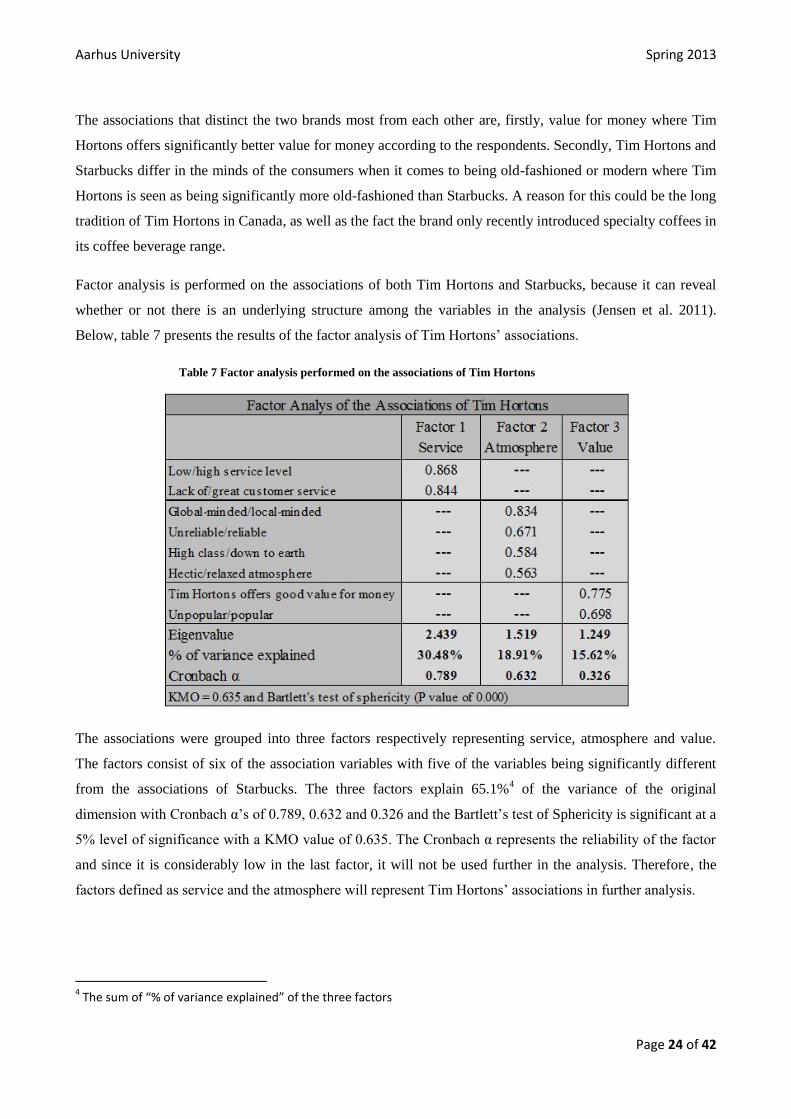

Factor analysis is performed on the associations of both Tim Hortons and Starbucks, because it can reveal

whether or not there is an underlying structure among the variables in the analysis (Jensen et al. 2011).

Below, table 7 presents the results of the factor analysis of Tim Hortons’ associations.

Table 7 Factor analysis performed on the associations of Tim Hortons

The associations were grouped into three factors respectively representing service, atmosphere and value.

The factors consist of six of the association variables with five of the variables being significantly different

from the associations of Starbucks. The three factors explain 65.1%4 of the variance of the original

dimension with Cronbach α’s of 0.789, 0.632 and 0.326 and the Bartlett’s test of Sphericity is significant at a

5% level of significance with a KMO value of 0.635. The Cronbach α represents the reliability of the factor

and since it is considerably low in the last factor, it will not be used further in the analysis. Therefore, the

factors defined as service and the atmosphere will represent Tim Hortons’ associations in further analysis.

4 The sum of “% of variance explained” of the three factors

Aarhus University Spring 2013

Page 25 of 42

The factor analysis for Starbucks is represented below in table 8.

Table 8 Factor analysis performed on the associations of Starbucks

The associations of Starbucks were grouped into two factors also representing atmosphere and service,

though with slightly different variables representing the two groups; “unpopular/popular” has replaced

“hectic/relaxed atmosphere” in the atmosphere factor and “XX offers good value for money” has been added

to the service factor. The factors consist of seven of the associations variables with five of the variables used

being significantly different from those of Tim Hortons. The two factors explain 61.9%5 of the variance of

the original dimension, and the Cronbach α’s are 0.619 and 6.92, indicating that both factors are reliable and

will therefore both be used in further analysis. The Bartlett’s test of Sphericity is significant at a 5% level of

significance with a KMO of 0.733.

A paired sample t-test will not be performed on the factors since they do not consist of the exact same

variables, and furthermore two of the bipolar variables are reversed in the atmosphere factor for Starbucks.

Due to this, the comparison would not be reliable and is therefore discarded for the association dimension.

It can be concluded that Tim Hortons’ and Starbucks’ associations differ on all the variables except on

“unpopular/popular” and “unreliable/reliable” where they are both rated as being popular and reliable brands.

The two brands’ associations have individually been grouped into two factors: service and atmosphere.

Though labeled the same, there are small differences in the factors for the two brands.

5 Again, the sum of “% of variance explained” of the two factors

Aarhus University Spring 2013

Page 26 of 42

5.2.6 Brand Equity

When it comes to liking the two brands, there are no significant differences in the means of Tim Hortons and

Starbucks which respectively have averages of 3.76 and 3.44 as displayed below in table 9.

Table 9 No significant difference in the means of brand equity of Tim Hortons and Starbucks

Though the difference is not significant, Tim Hortons’ average is slightly higher than Starbucks’, and the

standard deviation of the variable is also slightly smaller, indicating a more coherent opinion among the

respondents. It is concluded that there is no significant difference in the brand equities of the two brands.

5.3 Regression Analysis

A multiple regression analysis has been run for both brands in order to understand which dimensions predict

brand equity the best for each of the two brands. Two multiple regression models will be made in this

section; one for the brand equity of Tim Hortons and one for the brand equity of Starbucks and they will then

be compared in the discussion section. Both regression outputs have been checked for multicollinearity

which is discovered to not be an issue for either of the models as the tolerance levels are all above 20%. It

indicates that more than 20% of the variance in the independent variables are unique to the individual

variables and cannot be predicted by using other independent variables. Also, there were no Pearson

correlations above 0.7 among the independent variables which also verifies a lack of multicollinearity.

5.3.1 Tim Hortons

The regression model for Tim Hortons includes the independent variables, loyalty and perceived quality, as

well as the two association-factors, service and atmosphere. In table 10 below, the regression model on brand

equity for Tim Hortons is shown.

µ SD µ SD

I like the brand XX 3.76 1.155 3.44 1.313 1.542 (0.128)

Paired Sample t-Test on Brand Equity (5-point Likert scale)

Tim Hortons Starbuckst value (sig.)

Aarhus University Spring 2013

Page 27 of 42

Table 10 Regression analysis on brand equity for Tim Hortons

The adjusted R2 indicates that the model explains 44.3% of the variance of the dependent variable, and the

reason why the adjusted R2 has been used is because it takes the number of independent variables used to

assess the dependent variable into account. The awareness variable has a positive relationship with brand

equity indicating that when more consumers are able to recall Tim Hortons from memory, the better the

brand’s brand equity will be. However, as seen in table 10 the variable is not statistically significant. The

loyalty variable has a positive effect on brand equity since the beta-coefficient is 0.805, meaning that an

increase in loyalty of 1 point on the 5-point Likert scale increases brand equity by 0.805 point. In other

words, whenever a customer for instance returns to Tim Hortons, or the products meet a customer’s

expectations, brand equity will increase, given that the rest of the independent variables are kept constant.

The loyalty measure is statistically significant. The perceived quality measure, on the other hand, has a

small, negative relationship with brand equity but since the significance level is 0.49, it is not significant in

the regression model. This is also the case for the service-factor of the association variable which otherwise

indicates that if the service level increases, brand equity would decrease. The atmosphere-factor of the

association variable has a positive relationship with brand equity. From table 10, it can be seen that whenever

atmosphere increases with 1 point, brand equity will increase with 0.253 point if all other variables are kept

constant. This means that the more local-minded, reliable, down to earth and relaxed atmosphere Tim

Hortons portrays, the better brand equity the brand could have. Even so, the variable is not significant in the

regression model. From table 10, it is seen that the constant term is not significant6 and is therefore

disregarded, and the regression model for Tim Hortons’ brand equity is as follows:

6 Lower bound: -1.024 and upper bound: 1.604

Aarhus University Spring 2013

Page 28 of 42

From the conducted regression analysis, it can be determined that the loyalty measure is the only significant

dimension explaining Tim Hortons’ brand equity, and it has a positive correlation with the brand equity. It

can therefore be concluded that Tim Hortons’ brand equity increases when the loyalty dimension increases.

5.3.2 Starbucks

The regression model for Starbucks consists of independent variables similar to Tim Hortons’ with the

exception to small differences in the factored association variables as discussed earlier in the analysis. Table

11 below shows the regression output for the brand equity of Starbucks.

Table 11 Regression analysis on brand equity of Starbucks

The adjusted R2 for Starbucks’ regression model is 0.526 which means the independent variables explain

52.6% of the variance in brand equity. The awareness variable has a small positive relationship with brand

equity, though not statistically significant. It would mean that increasing the awareness level of Starbucks in

Canada would only lead to a small increase in the brand’s brand equity. The loyalty variable has a positive

relationship with brand equity, meaning that if coffee shop visits at Starbucks increases, Starbucks’ brand

equity will also increase, again given that the other independent variables are kept constant. The loyalty

variable is of significance in the regression model. The perceived quality variable has a beta coefficient of

0.091 which indicates that a 1 point increase in perceived quality will increase brand equity by 0.091 point as

well, though the relationship is not significant. The atmosphere factor of the association variable is also not

significant, and the variable has a negative relationship with brand equity with a beta coefficient of -0.291.

Aarhus University Spring 2013

Page 29 of 42

This means for instance that an increase towards being more global-minded or towards being perceived as

being more high class would have a negative effect on brand equity for Starbucks. The constant term is not

significant7 in the regression model and the regression model for Starbucks’ brand equity is therefore as

displayed below:

It can be concluded that the only significant measure explaining Starbucks’ brand equity is loyalty. The

loyalty measure has a positive relationship with Starbucks’ brand equity which means that whenever the

brand’s loyalty increases, so does its brand equity in Canada.

5.3.3 Conclusion on Analysis

It can first of all be concluded from the above analysis that Tim Hortons and Starbucks do have significant

differences in the dimensions defined by Aaker where the loyalty measure is significantly higher for Tim

Hortons than for Starbucks and vice versa with the perceived quality measure. Secondly, it is worth noting

that the loyalty measure has a greater impact on Starbucks’ brand equity than it has on Tim Hortons’ as seen

in the regression analysis. Both regression models show a strong, positive correlation between the loyalty

measure and brand equity, and it is the only measure that is significant. The overall conclusion based on

Aaker’s Brand Equity Ten model is that neither Tim Hortons nor Starbucks has stronger brand equity than

the other and it is the loyalty dimension that explains both brands’ brand equity.

5.4 Limitations of the Data

The sample size that the analysis was based on is small; with a completion rate of 76% and with a removal of

outliers, the sample consists of 62 respondents. Small sample sizes can cause the data being “overfitted,”

causing the result to be unnaturally good but non-generalizable (Jensen et al. 2011). The analysis is based on

a convenience sample, which means the data can: “…only be used in exploratory research for generating

ideas, insights or hypothesis” (Jensen et al. 2011, p. 246) which means it cannot be recommended to be used

for descriptive research. Therefore, the analysis done in this paper can only give insights to what dimensions

of brand equity that influences brand equity for the brands Tim Hortons and Starbucks. Since the data is

based on a convenience sample (Jensen et al. 2011) which have the limitations of selection bias and no

definable population. The bias consists of the fact that the collected data consists entirely of students in the

age of 18-45 attending a Canadian university in the area Waterloo-Kitchener in the province Ontario in

Canada. Due to this selection bias, the data does not give a representative look of the average Canadian but

only on consumers studying at Canadian universities. The percentage of male and female respondents is not

equally distributed in the data which again causes the data to not be very generalizable. Another observation

7 Lower bound: -1.003 and upper bound: 2.109

Aarhus University Spring 2013

Page 30 of 42

worth noting is that many foreign students have answered the questionnaire which is a limitation in the sense

that the analysis is to measure the brand equity and its dimensions of two brands in Canada. However, a

paired sample t-test shows that there are only few significant differences among non-Canadian respondents

and Canadian respondents, though these differences can also be caused by the small sample size. Therefore

the analysis done in the above section was based on both non-Canadians and Canadians.

A limitation connected to the association dimension is the fact that respondents’ true associations of the two

brands were not investigated; it was a predetermined set of associations the respondents was asked to rate on

a 5-point Likert scale. Though it is acknowledged it would have generated a more realistic result since, as

mentioned earlier, consumers only put value on the associations they find important themselves. However, it

was also recognized that this could have generated a lower completion rate since more work would have

been required of the respondent.

Another limitation is the fact that the brand equity dimension is not based on an analysis. By analyzing what

attributes consumers find important in coffee shops, the definition of brand equity could have been made

more precise as well as cover more aspects of the term than only the consumer’s fondness towards the brand.

Since Aaker defines this paper’s definition of brand equity as part of the loyalty measures of the Brand

Equity Ten model, the loyalty variables of the two brands will inevitably correlate positively with the brand

equity set out. This is acknowledged but due to constraint resources the pre-analysis identifying the

important attributes of coffee shops in the foodservice industry has not been possible to perform. Therefore

the definition of brand equity is found used in the analysis is found suitable though only relevant on the

consumer perspective of brand equity.

6 Discussion From the previous analysis it is evident that there is no significant difference in the brand equity between

Tim Hortons and Starbucks, though the significance level is close to 10%. It had however been expected that

a significant difference would have been the case and with Tim Hortons having a significantly greater brand

equity than Starbucks. One reason for this expectation is found in section 4.1 where it is stated that Tim

Hortons is the leading company in the foodservice industry in Canada. In this section it was also stated that

Tim Hortons has become a household name that many Canadians cares strongly about. Another reason for

this expectation is found in section 3.2 where it is emphasized that distribution intensity plays an important

role in brand equity (Yoo, et al 2000). Since Tim Hortons have more than 3,000 outlets across Canada it was

expected that due to less search and travel time to find a Tim Hortons, its brand equity would be higher than

Starbucks, who has fewer outlets across Canada. However, from the analysis conducted in this paper, it

cannot be concluded that there is a significant difference in the brand equities of the two brands.

Aarhus University Spring 2013

Page 31 of 42

A variable that was not expected to be significantly different between the two brands were the recall variable

where Tim Hortons had more presence than Starbucks had. It had been expected that both brands would be

recalled by all respondents since, as stated in section 4, both brands are leading brands; Tim Hortons in the

overall foodservice industry and Starbucks in the specialty coffee sector of that industry and with an increase

in demand of specialty coffee products, Starbucks was expected to have similar recall levels as Tim Hortons.

If taking Gill & Dawra’s (2010) work into consideration which stated that brand awareness leads to brand

image which then leads to brand equity, it can be said that Tim Hortons has a significantly better basis for

developing brand equity than Starbucks has because more consumers recall the brand.

When investigating the variables constituting the loyalty dimensions, it has been noted in section 5.2.3 that

respondents were more satisfied with the service at Starbucks. Even though this is the case, it is not reflected