Booster Clubs and School Support Organizations Guidelines Training May 29, 2009.

36

Booster Clubs Booster Clubs and and School Support School Support Organizations Organizations Guidelines Training Guidelines Training May 29, 2009

-

Upload

kory-robertson -

Category

Documents

-

view

213 -

download

0

Transcript of Booster Clubs and School Support Organizations Guidelines Training May 29, 2009.

Booster ClubsBooster Clubsandand

School Support School Support OrganizationsOrganizations

Guidelines TrainingGuidelines Training

May 29, 2009

WelcomeWelcome DeAnne Hatfield, RTSBADeAnne Hatfield, RTSBA

Executive Director of Business Executive Director of Business [email protected] 817-215-0041 [email protected] 817-215-0041

Jerhea NailJerhea NailSpecial Assistant to the Special Assistant to the [email protected] [email protected] 817-215-0144 817-215-0144

Kitty PoehlerKitty PoehlerDirector of Personnel ServicesDirector of Personnel [email protected] [email protected] 817-215-0071

AgendaAgenda

GuidelinesGuidelines OrganizationOrganization State and Federal ReportingState and Federal Reporting Sales TaxSales Tax Accounting for TransactionsAccounting for Transactions Fund RaisingFund Raising DonationsDonations Scholarship ProgramsScholarship Programs District ServicesDistrict Services

GuidelinesGuidelines

UIL Booster ClubsUIL Booster Clubs

School Support Organizations School Support Organizations

Role of the OrganizationRole of the Organization

UIL Booster ClubUIL Booster Club The UIL states that booster The UIL states that booster

clubs are formed to help clubs are formed to help enrich the school’s enrich the school’s participation in participation in extracurricular activities.extracurricular activities.

All meetings should be open All meetings should be open to the public with prior to the public with prior notice given and meeting notice given and meeting minutes kept.minutes kept.

Fund Raising is a major part Fund Raising is a major part of the booster club of the booster club activities.activities.

Funds collected must be Funds collected must be used to support school used to support school activities.activities.

Fund Raising projects are Fund Raising projects are subject to state laws and subject to state laws and local school district local school district guidelines and/or policies.guidelines and/or policies.

Non-Profit status should be Non-Profit status should be obtained from the IRS.obtained from the IRS.

Since UIL rules regulate Since UIL rules regulate what UIL participants, what UIL participants, sponsors and coaches may sponsors and coaches may and may not accept, it is and may not accept, it is important the booster clubs important the booster clubs are aware of these rules.are aware of these rules.

Please reference the Please reference the UIL ParentUIL Parent Information Manual for more Information Manual for more iinformation on UIL guidelines for Booster Clubs at nformation on UIL guidelines for Booster Clubs at http://www.uil.utexas.edu/athletics/manuals/pdf/parent_informationhttp://www.uil.utexas.edu/athletics/manuals/pdf/parent_information.pdf.pdf

School Support OrganizationsSchool Support Organizations

PTA is a nonprofit, democratic, voluntary organization PTA is a nonprofit, democratic, voluntary organization whose membership is concerned with the welfare of whose membership is concerned with the welfare of children and youth and who are willing to uphold its children and youth and who are willing to uphold its basic policies and subscribe to its bylaws.basic policies and subscribe to its bylaws.

The mission of the PTA is:The mission of the PTA is: to support and speak on behalf of children and youth in the schools, to support and speak on behalf of children and youth in the schools,

in the community and before governmental agencies and other in the community and before governmental agencies and other organizations that make decisions affecting children;organizations that make decisions affecting children;

to assist parents in developing the skills they need to raise and to assist parents in developing the skills they need to raise and protect their children; andprotect their children; and

to encourage parent and public involvement in the public schools of to encourage parent and public involvement in the public schools of this nation.this nation.

Role of the OrganizationRole of the Organization

Booster Clubs and School Support Booster Clubs and School Support Organizations shall organize and functionOrganizations shall organize and function

in a way that is consistent with the District’s in a way that is consistent with the District’s philosophy and objectivesphilosophy and objectives

with adopted Board policieswith adopted Board policies

in accordance with UIL regulations as in accordance with UIL regulations as applicableapplicable

OrganizationOrganization

BylawsBylaws

OfficersOfficers

Organization BylawsOrganization Bylaws

Each booster/school support organization Each booster/school support organization must maintain bylaws.must maintain bylaws.

Bylaws must be reviewed jointly by the Bylaws must be reviewed jointly by the school principal/designee and the school principal/designee and the organizations’ executive officers.organizations’ executive officers.

The bylaws must address rules for The bylaws must address rules for membership in the organization, the fiscal membership in the organization, the fiscal year, and the structure and method to be year, and the structure and method to be used to elect officers.used to elect officers.

Organization OfficersOrganization Officers• Below is a diagram indicating the minimum number of officers for a booster/school Below is a diagram indicating the minimum number of officers for a booster/school

support organization.support organization.

• Typically officer election should be completed by May of each year so that training Typically officer election should be completed by May of each year so that training can be completed and officers in place for the start of the school year.can be completed and officers in place for the start of the school year.

• Larger organizations may elect several vice presidents with responsibility over Larger organizations may elect several vice presidents with responsibility over different areas.different areas.

• Due to the increasing requirement placed on charitable organizations by the IRS, it Due to the increasing requirement placed on charitable organizations by the IRS, it is strongly recommended that the Treasurer have an accounting background.is strongly recommended that the Treasurer have an accounting background.

• The transfer of records and audit of accounts should be completed by July 1 of each The transfer of records and audit of accounts should be completed by July 1 of each year.year.

President

Secretary Treasurer Parliamentarian

Vice President

Liability InsuranceLiability Insurance Booster Clubs and School Support Organizations are Booster Clubs and School Support Organizations are

independent; therefore not covered by District insurance independent; therefore not covered by District insurance policies.policies.

General LiabilityGeneral Liability – protects your organization if someone is – protects your organization if someone is injured at eventinjured at event

Accident MedicalAccident Medical – provides medical coverage for risks – provides medical coverage for risks specifically excluded from the liability policy such as specifically excluded from the liability policy such as mechanical rides, school buses, automobiles and water craftmechanical rides, school buses, automobiles and water craft

BondBond – covers anyone entrusted with organization’s money – covers anyone entrusted with organization’s money

PropertyProperty – protects raffle merchandise, auction items and – protects raffle merchandise, auction items and fundraising supplies while in your possessionfundraising supplies while in your possession

Officers’ LiabilityOfficers’ Liability – protects officers for any decision making – protects officers for any decision making

State and Federal ReportingState and Federal Reporting

State and Federal ReportingState and Federal ReportingApplication for Federal Tax Exempt Application for Federal Tax Exempt

StatusStatus All booster/school support organizations should apply All booster/school support organizations should apply

for for FederalFederal Tax Exempt Status Tax Exempt Status on Form 1023, on Form 1023, Application for Application for Recognition of Exemption Under Recognition of Exemption Under Section 501(c)(3). Section 501(c)(3).

(General instructions and information can be found in(General instructions and information can be found in IRS Publication 557, Tax- IRS Publication 557, Tax-Exempt Status for your Organization.Exempt Status for your Organization.)) Further information may be obtained at Further information may be obtained at www.irs.ustreas.govwww.irs.ustreas.gov under under Application for State Tax Exempt StatusApplication for State Tax Exempt Status

Each organization must file for an employer Each organization must file for an employer identification number.identification number.

State and Federal ReportingState and Federal Reporting

Each organization must submit a copy of the determination Each organization must submit a copy of the determination letter issued by the IRS with regard to it’s exempt status. letter issued by the IRS with regard to it’s exempt status. This letter is required annually as proof of the This letter is required annually as proof of the organization’s exempt status.organization’s exempt status.

The organization must apply for their own sales permit from The organization must apply for their own sales permit from the Comptroller’s office. the Comptroller’s office.

You must obtain sales and use tax permit if you are You must obtain sales and use tax permit if you are engaged in business in Texas and you:engaged in business in Texas and you: Sell tangible personal property in TexasSell tangible personal property in Texas Lease tangible personal property in Texas; orLease tangible personal property in Texas; or Sell taxable services in TexasSell taxable services in Texas

Further information from the Comptroller’s office may be found atFurther information from the Comptroller’s office may be found at www.window.state.tx.uswww.window.state.tx.us

State and Federal ReportingState and Federal Reporting

Annual Filing RequirementsAnnual Filing Requirements• All booster/school support All booster/school support

organization exempt from organization exempt from federal taxes under 501(C)(3) federal taxes under 501(C)(3) must determine the necessity must determine the necessity for filing Form 990,for filing Form 990, Return of Return of Organization Exempt from Organization Exempt from Income Tax.Income Tax.

• An organization recognized as An organization recognized as tax exempt may be liable for tax exempt may be liable for tax on income deemed tax on income deemed unrelated business.unrelated business.

More information can be obtained from Publication More information can be obtained from Publication 598, Tax on Unrelated Business Income of Exempt 598, Tax on Unrelated Business Income of Exempt Organizations.Organizations.

Public DisclosurePublic Disclosure• All non-profit organizations All non-profit organizations

must comply with the must comply with the timelines and established by timelines and established by the Texas Public Information the Texas Public Information Act. Texas Government Code Act. Texas Government Code Chapter 552. Chapter 552.

Sales TaxSales Tax

Sales TaxesSales Taxes Organization must provide a vendor with a valid signed exemption Organization must provide a vendor with a valid signed exemption

certificate when claiming exempt status.certificate when claiming exempt status.

The NISD exempt status can not be utilized by a booster/school The NISD exempt status can not be utilized by a booster/school support organization. Each organization must apply and receive support organization. Each organization must apply and receive their own exempt status.their own exempt status.

Items that become personal property of the student are not Items that become personal property of the student are not exempt. Awards given to students by the organization are exempt. Awards given to students by the organization are exempt.exempt.

Individual members of the teams, band, etc may not claim Individual members of the teams, band, etc may not claim exemption from the sales tax on meals they purchase while on a exemption from the sales tax on meals they purchase while on a school trip. Only meals contracted by the organization are exempt school trip. Only meals contracted by the organization are exempt from sales tax.from sales tax.

Organization shall collect and remit sales tax on all taxable items. Organization shall collect and remit sales tax on all taxable items. When imposing sales tax, the organization may add the tax to the When imposing sales tax, the organization may add the tax to the sale item or absorb it into the selling price.sale item or absorb it into the selling price.

Accounting for TransactionsAccounting for Transactions

Accounting for TransactionsAccounting for Transactions The membership of the organization should be provided The membership of the organization should be provided

with a financial statement and bank reconciliation at a with a financial statement and bank reconciliation at a regular meeting at least once per month.regular meeting at least once per month.

The financial statement should detail the budget to actual The financial statement should detail the budget to actual expenditures and receipts.expenditures and receipts.

Choose a computerized accounting package to assist your Choose a computerized accounting package to assist your organization in accurate record keeping. Adopt a package organization in accurate record keeping. Adopt a package that can be used for several fiscal years. Avoid manual that can be used for several fiscal years. Avoid manual record keeping for this type of reporting.record keeping for this type of reporting.

Cash receipts and disbursement reports should be available Cash receipts and disbursement reports should be available when needed for the annual audit.when needed for the annual audit.

District employees and individuals who actively coach or District employees and individuals who actively coach or direct a UIL Activity should NOT have control or signature direct a UIL Activity should NOT have control or signature authority over an organization’s funds.authority over an organization’s funds.

Cash Receipt and Petty CashCash Receipt and Petty Cash All cash collections for fees, dues, and fundraising must be All cash collections for fees, dues, and fundraising must be

deposited upon receipt.deposited upon receipt.

All funds must be supported by some type of record All funds must be supported by some type of record documenting the source, amount, and be available for audit documenting the source, amount, and be available for audit purposes.purposes.

Booster/support organization funds will not be stored in the Booster/support organization funds will not be stored in the school vault or collected by a District employee.school vault or collected by a District employee.

A petty cash account may be kept by the organization. A petty cash account may be kept by the organization. Only the Treasurer and one other officer of the organization Only the Treasurer and one other officer of the organization should have access to it. A district employee cannot be in should have access to it. A district employee cannot be in control of this account. It should be used for emergency control of this account. It should be used for emergency purchases only. purchases only.

Bank AccountBank Account

To open bank account, the organization must To open bank account, the organization must obtain Employer Identification Number (EIN) from obtain Employer Identification Number (EIN) from the IRSthe IRS

Suggested that at least two (2) officers be signersSuggested that at least two (2) officers be signers

Reconcile bank statement monthlyReconcile bank statement monthly District employee may not be the signer on District employee may not be the signer on

organization’s bank accountorganization’s bank account

District employee cannot serve as TreasurerDistrict employee cannot serve as Treasurer

Bank Reconciliation and Bank Reconciliation and Disbursement of FundsDisbursement of Funds

Each month the balance indicated on the statement shall Each month the balance indicated on the statement shall be reconciled to the account balance as of the last day of be reconciled to the account balance as of the last day of the month.the month.

All disbursement requests must be made from established All disbursement requests must be made from established budget line items. If a request exceeds or is not a line item budget line items. If a request exceeds or is not a line item in the budget, then a vote of the membership must be in the budget, then a vote of the membership must be taken before the expenditure of the funds.taken before the expenditure of the funds.

A disbursement voucher should be completed for all A disbursement voucher should be completed for all expenditures regardless of amount.expenditures regardless of amount.

Booster/school support organizations may not contribute Booster/school support organizations may not contribute funds in an effort to increase the personnel allocations funds in an effort to increase the personnel allocations and/or stipends of a particular program without the express and/or stipends of a particular program without the express written approval of the appropriate Assistant written approval of the appropriate Assistant Superintendent. Superintendent.

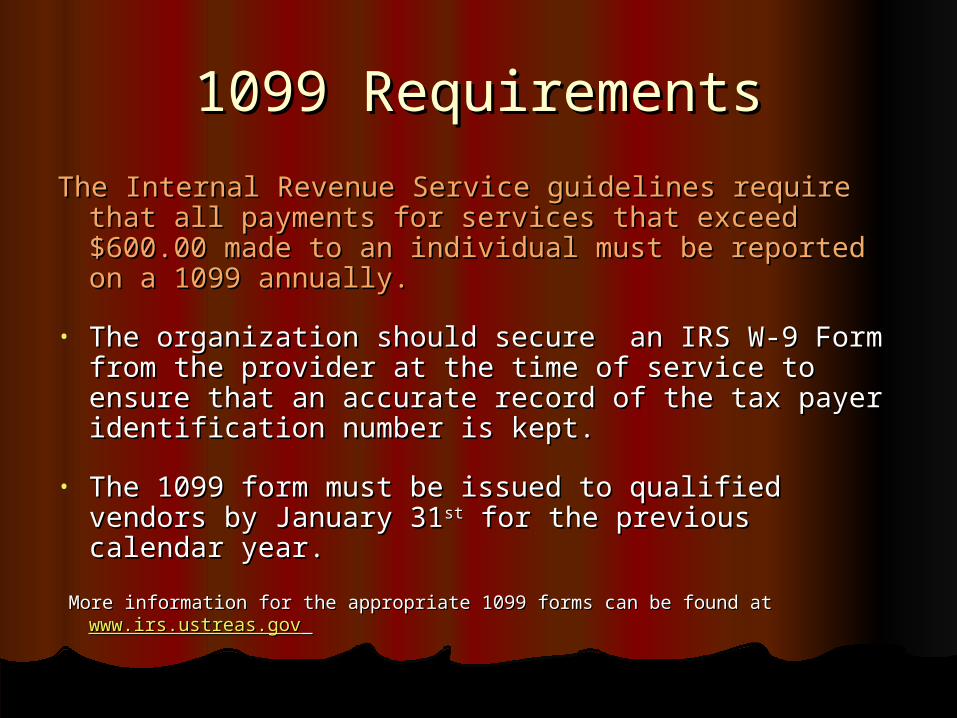

1099 Requirements1099 Requirements

The Internal Revenue Service guidelines require that The Internal Revenue Service guidelines require that all payments for services that exceed $600.00 made all payments for services that exceed $600.00 made to an individual must be reported on a 1099 to an individual must be reported on a 1099 annually.annually.

• The organization should secure an IRS W-9 Form The organization should secure an IRS W-9 Form from the provider at the time of service to ensure from the provider at the time of service to ensure that an accurate record of the tax payer that an accurate record of the tax payer identification number is kept.identification number is kept.

• The 1099 form must be issued to qualified vendors The 1099 form must be issued to qualified vendors by January 31by January 31stst for the previous calendar year. for the previous calendar year.

More information for the appropriate 1099 forms can be found at More information for the appropriate 1099 forms can be found at www.irs.ustreas.govwww.irs.ustreas.gov

GASB 39 RequirementsGASB 39 Requirements

The Governmental Accounting Standards The Governmental Accounting Standards Board Statement #39 requires school Board Statement #39 requires school districts to consider financial activities of all districts to consider financial activities of all parent teacher organizations, booster clubs, parent teacher organizations, booster clubs, foundations and other fund raising entities foundations and other fund raising entities for inclusion in the district’s financial for inclusion in the district’s financial statements.statements.

GASB 39 Information FormGASB 39 Information Form

Submit to the District’s Financial Services Department no Submit to the District’s Financial Services Department no later than August 1, annuallylater than August 1, annually

Include financial records year ending June 30thInclude financial records year ending June 30th

Fund RaisingFund Raising

Fund RaisingFund Raising

What is a Fund Raiser?What is a Fund Raiser? Planned – Scheduled – AnticipatedPlanned – Scheduled – Anticipated

EventEventActivityActivityProduct SaleProduct SaleServiceService

All booster/school support organizations All booster/school support organizations shall complete and submit a fund raising shall complete and submit a fund raising application and receive the approval of the application and receive the approval of the campus principal or designee.campus principal or designee.

DonationsDonations

DonationsDonations School district staff and students are discouraged from School district staff and students are discouraged from

accepting gifts of value.accepting gifts of value.

Students in UIL activities shall not accept gifts except as Students in UIL activities shall not accept gifts except as provided by the provided by the UIL Constitution and Contest Rules.UIL Constitution and Contest Rules.

Donations to the District shall become the sole property of Donations to the District shall become the sole property of the District not the accepting organization. Please see the District not the accepting organization. Please see Policy CDC (LOCAL) for NISD criteria for gifts.Policy CDC (LOCAL) for NISD criteria for gifts.

A gift that may impact a campus (i.e. facility, grounds, A gift that may impact a campus (i.e. facility, grounds, infrastructure, technology, or curriculum) must have prior infrastructure, technology, or curriculum) must have prior approval. approval.

Scholarship ProgramsScholarship Programs

Scholarship ProgramsScholarship Programs

The District encourages scholarship The District encourages scholarship programs that benefit studentsprograms that benefit students

Scholarships for a Graduating SeniorScholarships for a Graduating Senior

Student Scholarships for Campus Related Student Scholarships for Campus Related ActivitiesActivities

District ServicesDistrict Services

District ServicesDistrict Services

District services available to booster District services available to booster clubs/school support organizationsclubs/school support organizations

• Printing services are available at the cost of the servicePrinting services are available at the cost of the service

• First Class mailing is also available. The organization will First Class mailing is also available. The organization will be billed on a monthly basis for usage. Bulk mailing cannot be billed on a monthly basis for usage. Bulk mailing cannot be processed by the District.be processed by the District.

• Catering services are available through ARAMARK, the Catering services are available through ARAMARK, the District Food Service Provider.District Food Service Provider.

• Armored Car Service is not available through the District. Armored Car Service is not available through the District. • Employer Identification Number is not available through the Employer Identification Number is not available through the

District. District.

SummarySummary

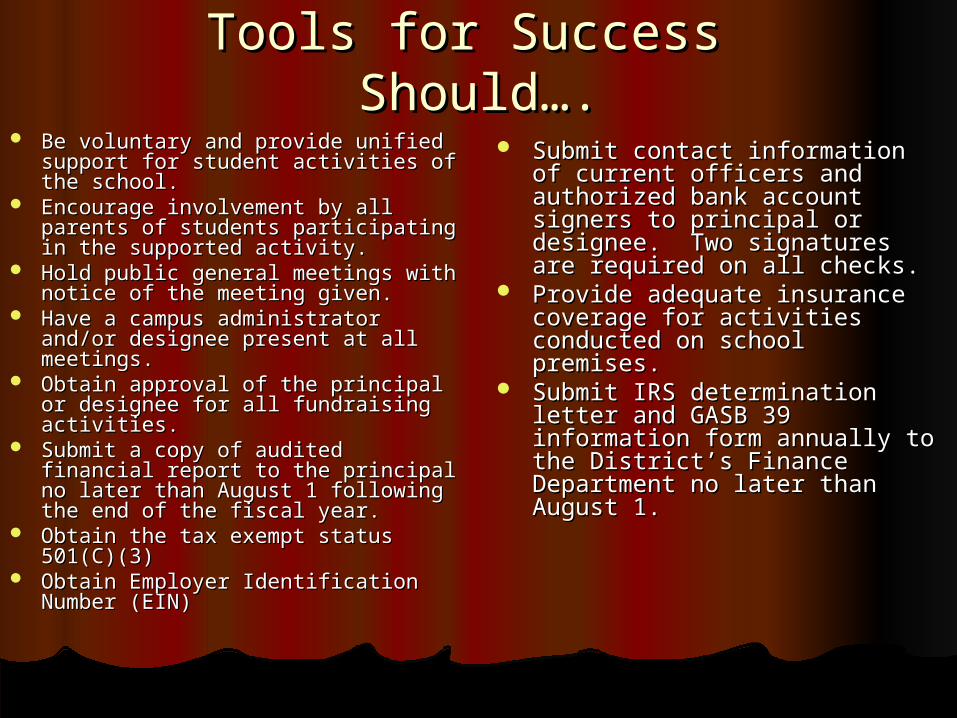

Tools for Success Tools for Success Should….Should….

Be voluntary and provide unified Be voluntary and provide unified support for student activities of the support for student activities of the school.school.

Encourage involvement by all Encourage involvement by all parents of students participating in parents of students participating in the supported activity.the supported activity.

Hold public general meetings with Hold public general meetings with notice of the meeting given.notice of the meeting given.

Have a campus administrator Have a campus administrator and/or designee present at all and/or designee present at all meetings.meetings.

Obtain approval of the principal or Obtain approval of the principal or designee for all fundraising designee for all fundraising activities.activities.

Submit a copy of audited financial Submit a copy of audited financial report to the principal no later than report to the principal no later than August 1 following the end of the August 1 following the end of the fiscal year.fiscal year.

Obtain the tax exempt status Obtain the tax exempt status 501(C)(3)501(C)(3)

Obtain Employer Identification Obtain Employer Identification Number (EIN)Number (EIN)

Submit contact information of Submit contact information of current officers and authorized current officers and authorized bank account signers to principal bank account signers to principal or designee. Two signatures are or designee. Two signatures are required on all checks.required on all checks.

Provide adequate insurance Provide adequate insurance coverage for activities conducted coverage for activities conducted on school premises.on school premises.

Submit IRS determination letter Submit IRS determination letter and GASB 39 information form and GASB 39 information form annually to the District’s Finance annually to the District’s Finance Department no later than August Department no later than August 1.1.

Tools for SuccessTools for SuccessShould Not…Should Not…

Have authority in directing or Have authority in directing or influencing District employees in influencing District employees in the administration of duties.the administration of duties.

Be involved in decision or policy Be involved in decision or policy making activities for a student making activities for a student group.group.

Give employee gift or cash in Give employee gift or cash in excess of UIL guidelines in excess of UIL guidelines in recognition of, or appreciation recognition of, or appreciation for coaching, directing or for coaching, directing or sponsoring student activities.sponsoring student activities.

Give anything to students Give anything to students without prior approval from the without prior approval from the school administration.school administration.

Give a member any gift without Give a member any gift without the approval of club the approval of club membership.membership.

Employ or pay any member Employ or pay any member for services rendered with the for services rendered with the organizations funds.organizations funds.

Sign contracts or pay Sign contracts or pay expenses directly from the expenses directly from the organization accounts for any organization accounts for any arrangements for student arrangements for student travel associated with the travel associated with the organization without prior organization without prior approval of the principal.approval of the principal.

Use the District’s Tax Use the District’s Tax Identification Number as the Identification Number as the organization’s identification organization’s identification number. number.

Use the District’s sales permit Use the District’s sales permit number as the organization’s number as the organization’s sales permit number.sales permit number.

Questions ?Questions ?