Blakes: Doing Business in China

25

Doing Business in China MONTRÉAL OTTAWA TORONTO CALGARY VANCOUVER NEW YORK CHICAGO LONDON BAHRAIN AL-KHOBAR* BEIJING SHANGHAI* *Associated Office Blake, Cassels & Graydon LLP | blakes.com

-

date post

17-Oct-2014 -

Category

Documents

-

view

722 -

download

0

description

Transcript of Blakes: Doing Business in China

Doing Businessin China

MONTRÉAL OTTAWA TORONTO CALGARY VANCOUVER NEW YORK CHICAGO LONDON BAHRAIN AL-KHOBAR* BEIJING SHANGHAI*

*Associated Office Blake, Cassels & Graydon LLP | blakes.com

A disciplined, team-driven approach focused squarely on the success of your

business. Over 550 lawyers in 12 offices across Canada, the United States,

Europe, the Middle East and China — Montréal, Ottawa, Toronto, Calgary,

Vancouver, New York, Chicago, London, Bahrain, Beijing and associated

offices in Al-Khobar and Shanghai. Among the world's most respected

corporate law firms, with expertise in virtually every area of business law.

Blakes Means Business.

BLAKE, CASSELS & GRAYDON LLP Contents Page 1

BLAKES GUIDE TO DOING BUSINESS IN CHINA Blakes Guide to Doing Business in China is intended as an introductory summary. Specific advice should be sought in connection with particular transactions.

Blake, Cassels & Graydon LLP produces regular reports and special publications on Canadian legal developments. For further information about these reports and publications, please contact Alison Jeffrey in our Toronto office by telephone at 416-863-4152 or by email at [email protected].

CONTENTS

I. Introduction ..................................................................................................................................... 1 1. Overview of Government and Law in China .............................................................................. 1 2. Structure of Government ............................................................................................................... 1

2.1 National People’s Congress ................................................................................................... 2 2.2 State Council ............................................................................................................................ 2 2.3 Ministerial Departments ........................................................................................................ 2 2.4 Regional and Local Governments ........................................................................................ 2 2.5 Judiciary ................................................................................................................................... 2 2.6 Special Development Zones .................................................................................................. 2 2.7 Hong Kong and Macao .......................................................................................................... 3

3. Legal System .................................................................................................................................... 3 II. Establishing a Business Vehicle in China .................................................................................. 4

1. Representative Office...................................................................................................................... 4 2. Limited Liability Company ........................................................................................................... 5

2.1 Incorporation: China v. Canada ........................................................................................... 5 2.2 Business Scope Requirements ............................................................................................... 5 2.3 Capitalization Requirements ................................................................................................. 6 2.4 Selecting an Ownership Structure ........................................................................................ 8

3. Investment Process ......................................................................................................................... 9 3.1 Establishing a New Company ............................................................................................... 9 3.2 Acquisition of Existing Company .......................................................................................10

III. China’s Business Law Environment .......................................................................................... 11 1. Tax Law ...........................................................................................................................................11 2. Employment Law ...........................................................................................................................12 3. Intellectual Property Law .............................................................................................................13

3.1 Patent Rights ..........................................................................................................................13 3.2 Trade-Mark Law ....................................................................................................................14 3.3 Foreign Registration ..............................................................................................................14

4. Competition Law ...........................................................................................................................14 4.1 Regulation of Monopolies ....................................................................................................14 4.2 Regulation of Unfair Competition .......................................................................................15

5. Foreign Exchange Law ..................................................................................................................15 6. Import and Export Law .................................................................................................................16

IV. The Next Steps ............................................................................................................................... 17 V. China Practice Group Contacts ................................................................................................... 18

Page 1 BLAKE, CASSELS & GRAYDON LLP

I. INTRODUCTION ver the past several decades, the People’s Republic of China (China) has shifted from a closed, state-planned economy to an increasingly open and internationally integrated marketplace. This trend is only expected to increase in the future, as China continues to establish its position as one

of the world’s foremost economic powers. Given China’s prominence on the global stage, businesses, investors and states around the world are constantly developing and honing their “China strategy”. Canadian businesses and investors are no different in this regard.

This guide is intended to provide a basic understanding of the legal issues involved in setting up and operating a business in China. In the following sections, we will review the main business vehicles that may be employed to enter the Chinese market. We will also provide a brief overview of the following key areas of China’s business law environment: tax law, employment law, intellectual property law, competition law, foreign exchange law and import/export law.

It is important to note that there is no template for establishing and operating a business in China. The approach in any given case will depend upon numerous factors such as the industry, business activities, size and specific location of the business. As such, this guide should be viewed simply as a general starting point for the road ahead.

This information is current as of March 1, 2013.

1. Overview of Government and Law in China Before discussing China’s business vehicles and legal environment, it is helpful to review the structure of government and the legal system in China. This will provide useful context for many of the issues discussed in this guide.

2. Structure of Government The Chinese government regulates the private sector much more than the Canadian government. Canadian businesses and investors can expect to have significant interaction with government authorities in many aspects of their China operations. As such, it is important to have a basic understanding of the structure of government in China.

China employs a centralized government model. Each level of government is generally structured with the same bodies and departments, and is responsible to the next higher level of government, although in practice it is not uncommon for government departments to be more closely aligned horizontally than vertically. In this regard, the central (or national) government is China’s highest level of authority, followed in turn by the provincial, municipal and county levels of government – and lower levels in some cases. We will briefly describe the main bodies of the central government: the National People’s Congress, the State Council, and the Ministerial Departments.

O

Page 2 BLAKE, CASSELS & GRAYDON LLP

2.1 National People’s Congress

The National People’s Congress (the NPC) is China’s highest legislative authority. The NPC consists of representatives elected by the provincial People’s Congresses throughout the country. Although the NPC only convenes once a year, it appoints a standing committee to exercise certain of its powers while not in session. The NPC also appoints China’s president, the head of state.

2.2 State Council

The State Council, which is loosely equivalent to a “cabinet”, is China’s highest body of state administration. The State Council’s primary role is to implement the state policy formulated by the NPC. The State Council fulfills its role by enacting legislation and by overseeing China’s national ministerial departments and provincial level People’s Governments. The head of the State Council is referred to as the Premier of China.

2.3 Ministerial Departments

China’s ministerial departments are empowered to supervise and administer the law and policy within their respective administrative portfolios. The main ministerial departments that foreign businesses will encounter are the National Development & Reform Commission (the NDRC), the Ministry of Commerce (the MOC), the State Administration for Industry and Commerce (the SAIC), the State Administration of Foreign Exchange (the SAFE) and the General Administration of Customs (Customs). The ministerial departments enact legislation, regulations and policy statements to direct activities within their jurisdiction.

2.4 Regional and Local Governments

Each level of government below the central government has its own People’s Congress, People’s Government and ministerial departments. The levels of government below the central government may also enact legislation, regulations and policy statements within the scope of their jurisdiction. Although such legislative efforts must generally comply with the efforts of the higher levels of government, in practice it is common to see local governments enacting policies that are not necessarily in line with central government edicts. This is a primary cause of confusion for foreign investors, who are often not able to reconcile competing, and sometimes contrary, statutory requirements.

2.5 Judiciary

The judiciary in China is appointed or otherwise approved by the People’s Congress corresponding to the level of the court. For example, the NPC appoints or otherwise approves the judges sitting on China’s Supreme Court, and any given provincial People’s Congress appoints or otherwise approves the judges sitting on its provincial courts.

2.6 Special Development Zones

In the initial stages of opening its economy, China made extensive use of a variety of special development zones (under various names). These zones operated under special rules designed to facilitate foreign investment , while allowing for a sheltered, more gradual economic transition in the areas of China

Page 3 BLAKE, CASSELS & GRAYDON LLP

outside the zones. In recent years, some of the formal incentives that were initially used to attract foreign investment in the zones have been phased out. For instance, special development zones no longer have the power to grant tax incentives that are not otherwise contemplated by the national tax laws. Despite these changes, it still makes sense to base certain investments in special development zones.

2.7 Hong Kong and Macao

It should be noted that Hong Kong and Macao, while part of China, operate under different systems of government and different legal systems than mainland China. This guide is focused on the principal mainland China business vehicles available to foreign investors and the laws of mainland China of primary interest to foreign investors, and will not address the unique circumstances in Hong Kong and Macao. It should be further noted that investors based in Hong Kong and Macao are generally subject to the same mainland China foreign investment rules as any other foreign investor.

3. Legal System As Canadian investors and businesses consider entering the Chinese market, it is important to understand some of the key differences between the legal systems in China and in Canada.

China’s legislative bodies have enacted a tremendous volume of statutes, regulations, policies, directives and other forms of legislation in the past several decades. Despite this abundance of legislation, the state of the law on any given point is sometimes difficult to determine with certainty. It is not uncommon, for example, to encounter vague, ambiguous or contradicting legal provisions, or to discover areas with respect to which the law is silent.

Where legal uncertainty is encountered in Canada, legal and business professionals look to the courts and quasi-judicial bodies (tribunals and commissions, for example) to provide an authoritative and binding interpretation upon which they can structure their affairs. In China, however, the body of published case law is sparse, and is generally not binding on other courts and quasi-judicial bodies. This serves to empower China’s administrative authorities, which often have significant discretion in the manner in which they choose to interpret and apply the law. Administrative policy can vary, frequently from case to case and over time, and can be rigid, formalistic and bureaucratic. This often requires foreign businesses and investors to be flexible in their approach to achieving their objectives.

Foreign businesses and investors are often concerned about the enforceability of their legal rights in China. Given that most judicial rulings in China are unreported, it is difficult to reliably assess the success rate of foreign investors and businesses before the Chinese courts. It is possible to mitigate the risk posed by Chinese judicial proceedings in some cases by negotiating the use of foreign courts or alternate dispute resolution mechanisms. Under Chinese law, foreign arbitration decisions are generally enforceable, subject to similar public policy exceptions that are common in most jurisdictions. Judgments issued by foreign courts are generally not enforceable in China. It should be noted that Chinese courts do not have the same inherent authority as common law courts to grant so-called “equitable remedies” such as injunctions and specific performance. Similar remedies are sometimes provided by statute, but are generally more limited in their scope and application. That being said, as a general rule Chinese courts do consider the equities in any given matter.

Page 4 BLAKE, CASSELS & GRAYDON LLP

II. ESTABLISHING A BUSINESS VEHICLE

IN CHINA Before establishing a business vehicle in China, Canadian investors and businesses should first determine whether such a business vehicle is in fact required. In some instances, the intended business activities can be performed without spending the time and incurring the costs involved in setting up a Chinese business vehicle. This is often the case where a foreign business intends to enter into contractual relationships with counterparties in China, but does not intend to establish a presence in China, such as certain exporting and importing activities and offshore manufacturing arrangements.

There are some industry-specific exceptions allowing foreign businesses to establish a registered presence and conduct narrow or limited business activities in China through a branch office, such as certain oil exploration and development, construction, engineering, and banking activities. Of course, the use of a branch office negates the limited liability that is available to foreign investors who establish subsidiaries in China. Generally, if a foreign business intends to establish a presence in China, a Chinese business vehicle will be required.

There are numerous types of business vehicles that can be established in China. For the purposes of this introductory guide, we will focus on the two business vehicles that are most commonly used by foreign businesses and investors: representative offices, and limited liability companies, either by way of a wholly foreign-owned enterprise or an incorporated joint venture.

1. Representative Office A representative office (RO) is essentially a registered office of a foreign company in China. ROs are relatively easy and inexpensive to establish, though they are limited in their permitted scope of activities. Many foreign businesses choose to open an RO in China as a way to explore the market before making a more substantial investment.

One of the main differentiating factors between ROs and limited liability companies is the relative ease of the RO approval process. As will be discussed in the next section, the Chinese government conducts an active review and approval process with respect to the establishment of foreign-invested limited liability companies. In the case of ROs, approvals are generally granted relatively quickly and as a matter of routine, as long as the establishing company is a legitimate enterprise which has been in existence for at least two years prior to application. Establishing an RO can take as little as four to six weeks in a non-specialized sector. It should be noted, however, that in areas of China that have benefited from an influx of foreign investment, ROs are no longer as welcome as they once were.

As a result of the relatively streamlined approval process, ROs are much less expensive to establish than companies. In addition, ROs are not subject to the minimum investment requirements imposed on companies and their investors.

Although an RO is an easier and less expensive vehicle to establish than a limited liability company, it is also significantly limited in its permitted scope of activities. Under Chinese law, an RO is considered to be an extension of its establishing company, and does not have the status of a “legal person”. In this regard,

Page 5 BLAKE, CASSELS & GRAYDON LLP

an RO is generally only permitted to act as a liaison between the Chinese market and the establishing foreign company. Such liaison activities are restricted to research, marketing, technical exchanges with Chinese companies and other activities that facilitate business between the Chinese market and the foreign company. In other words, an RO is generally not permitted to conduct business activities such as buying and selling goods and services either on its own behalf or on behalf of the foreign investor. As a result, an RO will not be appropriate if a foreign investor wishes to establish an operating entity in China. In addition, ROs do not offer limited liability protection to their “parent” companies.

2. Limited Liability Company In many cases, doing business in China will require foreign investors to establish or acquire a Chinese limited liability company. In this section, we will describe Chinese aspects of company formation and management that may not be familiar to foreign investors, the various ownership structures that may be employed by foreign investors, and the options of incorporating or acquiring a Chinese company.

2.1 Incorporation: China v. Canada

In Canada, corporations can be established with relative speed and ease. Investors are required to provide basic information about the structure of the company but do not need to specify a business plan or a scope of intended business activities. Incorporations may be completed in one or two days if required, and may take on forms ranging from an empty shell to a fully capitalized and organized company. In effect, the incorporation process allows investors to form a company without committing to a corporate structure, a set of business activities, or a level of capitalization commensurate with its intended business activities.

In China, the incorporation process is much more regulated and bureaucratic, often requiring review and approval by several branches of the Chinese government. The review process includes an examination of the structure, business scope and capitalization of the proposed company (discussed in more detail later in this guide). Based on this review process, the authorities determine whether or not the proposed company should be approved, and what requirements or restrictions should be imposed upon the structure and operations of the proposed company.

From the foregoing, it should be evident that incorporation in China is a much more complicated, time-consuming and expensive process in China than in Canada. In the next two sections, we will examine in particular the business scope and capitalization requirements involved in China’s incorporation process. These requirements, which are not found in the Canadian incorporation process, are important to understand when setting up a company in China.

2.2 Business Scope Requirements

In China, it is not possible to incorporate a company to perform a general range of business activities. The incorporation process requires investors to specify a business scope which describes the company’s proposed business activities – such as buying, selling, distributing, providing services, importing, exporting, etc. – and the industry sectors in which it will conduct such activities. Once formulated, the proposed business scope is subject to review and approval by the Chinese authorities.

Page 6 BLAKE, CASSELS & GRAYDON LLP

The PRC Foreign Investment Industrial Guidance Catalogue (Revised) (the Industry Catalogue) is the most important tool for determining whether activities in a proposed industry sector will be acceptable. The Industry Catalogue, which is jointly issued by the NDRC and the MOC, classifies industries into three categories: encouraged industries, restricted industries and prohibited industries. Any industries that are not listed in the Industry Catalogue are deemed to be permitted industries.

Generally speaking, proposed companies that intend to conduct business in:

• encouraged or permitted industries will be approved more readily;

• restricted industries will often be subject to more time-consuming and higher-level examination; or

• prohibited industries will not be approved.

Beyond categorizing investment, the Industry Catalogue also specifies any restrictions that apply to foreign-invested enterprises operating in certain industries. In some industries such as oil and gas exploration, automobile manufacturing, and cargo shipping, a company cannot be established by a foreign company without a Chinese partner. In such cases, the Industry Catalogue may also specify that the Chinese partner must hold a minimum amount of investment or control in the joint venture.

The business scope is one of the central points that is reviewed and approved by the Chinese authorities as part of the incorporation process. It must be precise and correspond to the type of business the company will undertake once established. Chinese companies are not entitled to enter into business activities beyond their approved business scope. Should a company wish to expand or change its operations post-incorporation, it will need to apply to the appropriate government authorities to amend its business scope. It should be understood that regional regulators will often apply boilerplate business scopes when conducting their review of applications, regardless of whether such formulations are entirely appropriate. As such, business scope is often a point that is subject to negotiation with the approval authorities.

2.3 Capitalization Requirements

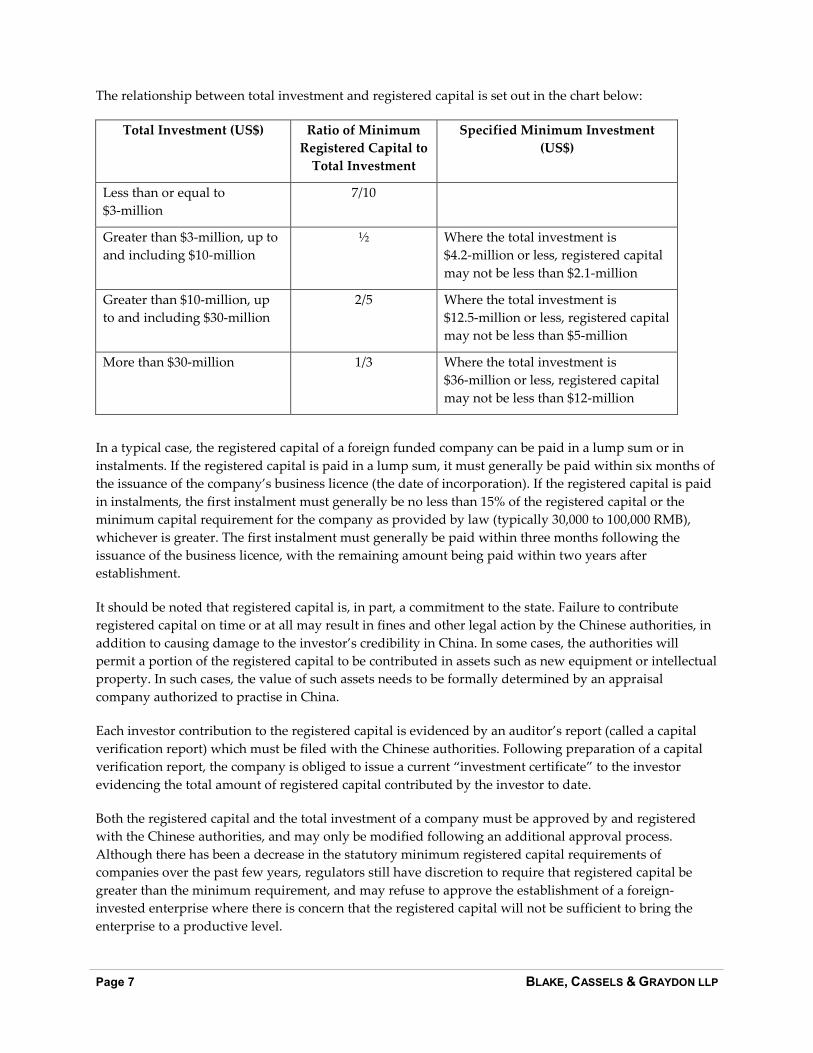

In Canada, it is quite common for corporations to be formed with only a nominal amount of capitalization – one share issued for one dollar, for example. This is not an available option in China, although minimum capitalization requirements have been relaxed in the past few years. In this section, we will discuss the capitalization concepts of “total investment” and “registered capital” as they apply to the establishment of limited liability companies in China.

When seeking to establish a company in China, a foreign investor is required to determine the appropriate level of total investment for the proposed company. The total investment can be generally explained as the total amount of funding (whether debt or equity) required to bring the proposed company to the point that it is able to conduct its proposed business operations without financial support from its parent(s) or other source of financing. At least a specified portion of the total investment of a company must be contributed in the form of an equity investment by its parent(s). This minimum equity investment is referred to as the registered capital.

Page 7 BLAKE, CASSELS & GRAYDON LLP

The relationship between total investment and registered capital is set out in the chart below:

Total Investment (US$) Ratio of Minimum Registered Capital to

Total Investment

Specified Minimum Investment (US$)

Less than or equal to $3-million

7/10

Greater than $3-million, up to and including $10-million

½ Where the total investment is $4.2-million or less, registered capital may not be less than $2.1-million

Greater than $10-million, up to and including $30-million

2/5 Where the total investment is $12.5-million or less, registered capital may not be less than $5-million

More than $30-million 1/3 Where the total investment is $36-million or less, registered capital may not be less than $12-million

In a typical case, the registered capital of a foreign funded company can be paid in a lump sum or in instalments. If the registered capital is paid in a lump sum, it must generally be paid within six months of the issuance of the company’s business licence (the date of incorporation). If the registered capital is paid in instalments, the first instalment must generally be no less than 15% of the registered capital or the minimum capital requirement for the company as provided by law (typically 30,000 to 100,000 RMB), whichever is greater. The first instalment must generally be paid within three months following the issuance of the business licence, with the remaining amount being paid within two years after establishment.

It should be noted that registered capital is, in part, a commitment to the state. Failure to contribute registered capital on time or at all may result in fines and other legal action by the Chinese authorities, in addition to causing damage to the investor’s credibility in China. In some cases, the authorities will permit a portion of the registered capital to be contributed in assets such as new equipment or intellectual property. In such cases, the value of such assets needs to be formally determined by an appraisal company authorized to practise in China.

Each investor contribution to the registered capital is evidenced by an auditor’s report (called a capital verification report) which must be filed with the Chinese authorities. Following preparation of a capital verification report, the company is obliged to issue a current “investment certificate” to the investor evidencing the total amount of registered capital contributed by the investor to date.

Both the registered capital and the total investment of a company must be approved by and registered with the Chinese authorities, and may only be modified following an additional approval process. Although there has been a decrease in the statutory minimum registered capital requirements of companies over the past few years, regulators still have discretion to require that registered capital be greater than the minimum requirement, and may refuse to approve the establishment of a foreign-invested enterprise where there is concern that the registered capital will not be sufficient to bring the enterprise to a productive level.

Page 8 BLAKE, CASSELS & GRAYDON LLP

The portion of the total investment above the amount of the registered capital is not a financial commitment on the part of the investor. Instead, this amount represents the total amount of additional funds the company may raise by way of debt. In the event that a limited liability company runs out of working capital and all its total investment has been contributed, it will only be able to obtain additional funds through an increase to its registered capital and total investment, which increase must be approved by the government. As government approvals may take several weeks to obtain, a lack of proper cash flow planning may leave the company in financial difficulties. Therefore, the amount of total investment and registered capital of a company should be determined strategically. Investors need to balance the desire to limit their investment risk in China against the risk of cash flow problems.

2.4 Selecting an Ownership Structure

There are two types of companies that are generally used by foreign investors:

1. a wholly foreign-owned enterprise (“WFOE”, commonly pronounced as “woofee”) formed by one or more foreign investors; or

2. a Sino-foreign joint venture formed by one or more foreign investors and one or more domestic Chinese companies.

We will discuss each of these structures below.

2.4.1 Wholly Foreign-Owned Enterprise

A WFOE is a Chinese company that is wholly owned by one or more foreign investors. The main advantage of a WFOE is that the foreign investor (assuming a sole shareholder) has complete control over the management and financial affairs of the company. Several foreign investors may partner to establish a WFOE either by investing directly in the WFOE or by jointly establishing an offshore entity to establish the WFOE.

Establishing a WFOE is relatively simple in comparison to establishing a Sino-foreign joint venture. Although the required documentation is similar (with the significant exception of the joint venture contract), such documentation does not need to be negotiated and settled between a foreign investor and a Chinese party. This reduces both the cost and time required to complete the incorporation process.

2.4.2 Sino-Foreign Joint Ventures

As discussed earlier, the Industry Catalogue requires foreign investors to partner with a Chinese party in order to do business in certain industry sectors. Even where the Industry Catalogue does not make this explicit requirement, the government authorities may choose to impose this requirement at their discretion. The law also requires that, in certain industry sectors, the Chinese party must obtain and maintain a majority position in the joint venture. In such cases, a foreign investor will not be able to invest in a Chinese limited liability company unless the investment is structured as a Sino-foreign joint venture in the manner specified by the law and administrative authorities.

Where a joint venture with a Chinese party is not required, foreign investors should consider carefully whether there is a genuine advantage to working with a local partner. There are several points to consider in this regard. Chinese partners will often resist managing the joint venture in accordance with

Page 9 BLAKE, CASSELS & GRAYDON LLP

the foreign party’s practices, which can be a source of friction between the parties and may even lead to breaches of the law of the foreign investor’s home jurisdiction. In dispute situations, the Chinese partner to the joint venture will often have the upper hand, no matter how carefully agreements are drafted, simply because they are familiar with the system. In most Chinese jurisdictions, foreign investors can work directly with government and regulators without the assistance of a local business partner. In this regard, promises of access to or special treatment from local government should not form the basis for establishing a business relationship.

There are two types of Sino-foreign joint ventures under Chinese law: the equity joint venture (EJV) and the co-operative (or contractual) joint venture (CJV), both of which can be established as limited liability companies.

In an EJV, each party may contribute registered capital in the form of cash, land, buildings, intellectual property, equipment and/or technology. The parties then share in the management, profits, risks and losses of the joint venture in proportion to their relative equity interests.

CJVs are similar in many ways to EJVs but have the potential to be more flexible in certain aspects. Unlike EJVs, the profits, risks and losses of CJVs may be allocated between the parties in a proportion that differs from the equity contributions of the parties. It may also be possible for the foreign party to recover its investment before the end of the term of the CJV although the quid pro quo in this situation is that the Chinese investor will be entitled to receive the fixed assets of the CJV upon its dissolution, and for the parties to contract out management of the joint venture to a third party. CJVs may also be formed as unincorporated joint ventures, although this is a less frequently employed structure (no limited liability for the investors being the main disadvantage).

3. Investment Process Foreign investors can invest in Sino-foreign joint ventures and WFOEs by establishing a new company or by acquiring an equity interest in an existing company. We will discuss both of these options below.

3.1 Establishing a New Company

Establishing a new company allows the investor to design the company according to its needs, including the internal structure as well as the external relationships and activities of the company.

In order to incorporate a company, the foreign investor (in conjunction with its Chinese partner, if any) must prepare and submit an application package for review and approval by the Chinese authorities (typically the NDRC and the MOC). The package notably includes a feasibility study describing the proposed company, including the proposed company’s business scope, corporate structure, proposed premises, capitalization, basic profit and expense projections, environmental impact, energy requirements, land requirements, and other aspects on a case-by-case basis. The package also includes the proposed articles of association of the company, which describe the internal parameters and governance of the proposed company in a manner similar to the bylaws of federally incorporated companies in Canada. If the nature of the proposed business requires prior review or approval by other branches of the Chinese government, such approvals must be included in the package. It will also be necessary to provide documentation establishing the credit and reputation of the investor(s). In the case of Sino-foreign joint ventures, the foreign investor must additionally negotiate and execute a joint venture contract with its Chinese partner. This joint venture contract must then be submitted as part of the application package.

Page 10 BLAKE, CASSELS & GRAYDON LLP

The nature and size of the investment in a foreign-invested company and the proposed business scope of the company will dictate whether local, provincial or central government approval is required. Central government approvals, since they invariably involve larger investments or investments in key sectors, tend to take longer than local and provincial approvals.

It is realistic to budget for a time period of between three to six months from the date the application for a foreign-invested company is submitted to the date of incorporation. It is, however, customary for government authorities to request documents and additional clarifications that may slow down the process.

3.2 Acquisition of Existing Company

Foreign investors generally prefer to establish new companies rather than acquire some or all of the equity of an existing Chinese company. It can be difficult to identify an appropriate acquisition target, particularly since Chinese companies may be reluctant to provide information (in a timely fashion or at all) that foreign investors might normally expect to receive in a due diligence process. Still, in certain cases, investors may wish to take advantage of an existing structure or market position of an established company as opposed to building a business from the ground up.

As with incorporating a new company, the authorities will be involved in reviewing and approving the documentation necessary to allow a foreign business to acquire some or all of the equity of a Chinese company. In particular, the authorities will review the substance of the purchase agreement to assess its compliance with Chinese corporate law and to determine whether or not the proposed compensation and structure of the transaction is acceptable. The authorities will also review the suitability of the investor in the same way as they would if the investor was incorporating a new company.

It will likely take several months or longer to acquire an existing Chinese company depending on the size and complexity of the transaction. If the Chinese company is not currently a foreign-invested enterprise, additional approvals will be required to transform the company from a wholly Chinese-owned company to a foreign-invested enterprise. Similar approvals will be required in the event that the investor’s proposed acquisition would change a Sino-foreign joint venture into a WFOE.

Page 11 BLAKE, CASSELS & GRAYDON LLP

III. CHINA’S BUSINESS LAW ENVIRONMENT In the previous sections, we examined the business vehicles that a foreign investor may use to enter the Chinese market. In this section, we will provide an overview of certain key aspects of China’s business law environment. Canadian businesses and investors may find that certain business laws and administrative regimes do not operate the way they might expect. It is not uncommon for foreign investors to encounter legal and administrative stumbling blocks where they are least expected. As with all areas of doing business in China, the best approach is to gather as much information as possible, plan and prepare accordingly, and remain flexible and patient if plans need to be modified as events unfold.

We will provide a background overview of the following areas of China’s business law environment:

1. Tax Law

2. Employment Law

3. Intellectual Property Law

4. Competition Law

5. Foreign Exchange Law

6. Import/Export Law

1. Tax Law There are numerous forms of taxation that Canadian businesses and investors may encounter in China. It is important to note that China’s tax laws operate in the context of the tax treaty formed between China and Canada. This treaty provides rules for the levy of tax on both individuals and enterprises, and sets out provisions designed to eliminate or mitigate instances of double taxation. We will provide an overview of China’s income tax regime and certain other taxes that are commonly encountered.

The taxation of enterprise income in China is governed by the Enterprise Income Tax Law and its associated laws and regulations. An enterprise’s taxable income is primarily based on whether a company is considered to be a “resident” or a “non-resident” of China. Resident companies are those companies established under Chinese law or foreign companies with management or control based in China. Resident companies are subject to income tax on their worldwide income within the taxation period. Non-resident companies are subject to tax on their income relating to their China operations. In general, the enterprise income tax is 25% on the taxable income of a resident business. Non-resident businesses may be subject to a reduced tax rate, as may qualifying small businesses or businesses operating in certain encouraged geographic zones or industry sectors.

China also has several forms of tax that may be levied depending on the nature of a transaction. The Value Added Tax (VAT) is a tax generally payable on the production, sale and importation of goods (generally tangible goods), and certain types of services. In general, the VAT is designed to pass the ultimate payment of the tax to the end consumer of the goods or services. The Consumption Tax is a tax

Page 12 BLAKE, CASSELS & GRAYDON LLP

payable on certain non-essential or luxury consumer goods. The Business Tax is a tax payable on the provision of services (that are not covered by the VAT), and the transfer of intangible and real property. The tax rate for these taxes varies depending on factors such as the industry at issue and the particular circumstances of the payor.

There are numerous other taxes that may apply depending on the specific business activities at issue. Foreign investors should always seek advice on the taxes that may apply in any given case as part of their decision to do business in China.

2. Employment Law The relationship between employers and employees is heavily governed by statute in China. The law provides basic minimums with respect to most aspects of the employment relationship, and in some areas stipulates the terms that must form the basis of the employment contract. In recent years, China has established certain state-administered social insurance programs for employees. These programs typically involve contributions from both employers and employees (through payroll deductions), and provide benefits such as medical insurance, injury and disability insurance, unemployment insurance, old age pension, housing fund and other benefits. Employers and employees are free to negotiate such aspects as salary, job description, vacation entitlement, and other benefits above the minimums provided by law.

Employment contracts in China may be formed on an open-term, fixed-term or task-specific basis. Employers are often reluctant to form open-term contracts, as they are not permitted to terminate employment relationships except in the event of serious dereliction of duty, protracted illness and similarly high thresholds. For this reason, employers generally prefer to structure their employment relationships on a fixed-term or, less commonly, on a task-specific basis. However, it is to be noted that fixed-term agreements also have limited benefits since the law provides that, following two consecutive renewals of a fixed-term employment contract, it will automatically be treated under the law as an open-term contract.

Employers are often concerned about their ability to protect their business interests in relation to past and present employees. Chinese law recognizes the concepts of confidential information and trade secrets, and provides protection against theft or misuse thereof. China’s patent legislation also contains provisions that generally deem intellectual property developed by an employee in the context of his or her employment to be the property of the employer, although additional compensation for the inventor may be required. In any event, the employment agreement should carefully set out the employee’s confidentiality and use of intellectual property obligations, as well as the employer’s entitlement to intellectual property created by the employee.

Chinese law also permits the use of post-employment non-competition arrangements, although they differ from their Canadian counterparts in numerous respects. Unlike in Canada, a non-competition clause in China must provide the employee with compensation throughout the non-competition period. The exact parameters of the compensation are not specifically addressed in the law, although in practice the amount is generally between one-half to two-thirds of the employee’s typical compensation, paid on a monthly basis. An employer and an employee are also permitted to negotiate a penalty that will apply if the employee breaches his or her non-competition obligations. As in Canada, non-competition clauses should be drafted as narrowly and fairly as possible to increase the likelihood of enforcement. The term

Page 13 BLAKE, CASSELS & GRAYDON LLP

of the non-competition obligation must not exceed two years after the expiry or termination of the employment relationship.

3. Intellectual Property Law Intellectual property protection is a key consideration for companies entering the Chinese market. In this section, we will provide an overview of patent and trade-mark rights in China. Investors may also wish to register domain names and copyrights in China. In the subsequent Competition section, we will also discuss certain unregistered forms of intellectual property protections such as confidential information and trade secrets.

3.1 Patent Rights

There are three different types of patents in China: invention patents, utility model patents and design patents. As a simplified explanation, invention patents relate to innovative new products, processes and improvements thereof, utility model patents relate to innovative aspects of the shape and structure of a product, and design patents relate to certain aesthetic aspects (colour, shape and pattern) of the presentation of a product. Invention patents are the most robust of the three patents, involving a meticulous review process that takes several years to complete, and providing protection for a period of 20 years from the date of filing. Design patents and utility model patents have a less meticulous and lengthy review process, and provide protection for a period of 10 years after the date of filing. Each of these patents provides protection throughout China (excluding Hong Kong and Macao).

China’s patent system works on a first-to-file basis. For invention and utility model patent applications, patent examiners will review the purported invention or utility model and the relevant “prior art” to determine whether or not the purported invention or utility model is novel, creative (ingenious) and practical. Design patent applications are examined on the basis of whether the design infringes upon a well-known existing design or another registered design. Both foreign and domestic prior art and designs are reviewed in determining patentability.

China is a party to the Patent Co-operation Treaty (PCT). In this regard, a Canadian company that wishes to protect its innovations in China may apply directly to the Chinese patent authorities or may apply indirectly through the PCT or “international” process. Timing is critical in either of these processes, and early consultation with a legal adviser is encouraged to ensure that the window of time for patentability does not expire.

The enforcement of foreign-owned patent rights in China remains an area of concern for foreign investors and businesses. It is difficult to determine with certainty the degree to which foreign patent rights may be successfully enforced against local infringers. As noted, the judicial system is not based on precedent and is generally neither transparent to the public nor independent. Where patents are successfully enforced, the remedies available to the successful party are often not as robust as those in Canada. For these reasons, the enforceability of patents in China remains a business risk that must be factored in when entering the Chinese market.

Page 14 BLAKE, CASSELS & GRAYDON LLP

3.2 Trade-Mark Law

Trade-mark protection in China is based on a first-to-file system. Unlike in Canada, the use of a trade-mark itself will not establish a property right to such trade-mark. There is an exception in the case of famous trade-marks – Nike, Coca-Cola, and similar globally recognized trade-marks – which receive protection under the law whether or not they have been registered as trade-marks in China. In general, however, trade-mark rights can only be acquired by filing a trade-mark in one or more classes of goods and services.

Registered trade-marks remain in effect for 10 years, with subsequent 10-year extensions being available. Trade-marks protect against infringing uses on the same or similar goods as those specified in the trade-mark registration. As with patent protection, enforceability of trade-mark rights remains unpredictable. Trade-mark infringement, particularly in relation to consumer goods, remains a significant problem in China.

China is a party to the Paris Convention for the Protection of Industrial Property, and in that regard it is possible for a person to obtain priority rights to marks previously filed by the person in other party states. As with the PCT process for patent registration, timing is critical and it is important to consult with legal counsel as early as possible.

3.3 Foreign Registration

Many forms of intellectual property protection in China may be registered by foreign businesses without a Chinese business vehicle. In this regard, foreign businesses may wish to consider protecting certain intellectual property rights in China in preparation for future entry to the Chinese market or to pre-empt the registration of competing intellectual property claims.

4. Competition Law China has consolidated and expanded regulatory schemes in recent years to regulate monopolistic business structures and commercial practices, and to regulate certain forms of unfair competition.

4.1 Regulation of Monopolies

Under China’s Anti-Monopoly Law (AML) and its associated regulations, there are three general categories of prohibited activity:

• business mergers and combinations that unduly restrict or eliminate competition (the M&A Category);

• collusive business agreements (the Collusion Category); and

• abuse of dominant market position (the Dominant Position Category).

The M&A Category, which is a relatively new feature of Chinese law, is administered by the MOC, and regulates concentrations of business operators that may influence, eliminate or restrict competition. In the vast majority of cases, the reviewed transactions have been approved, albeit with certain restrictions in some cases. The Collusion Category is administered by the SAIC, and regulates agreements between

Page 15 BLAKE, CASSELS & GRAYDON LLP

competing business operators that, among other things, artificially control the price or supply of commodities, restrict the purchase or development of new technologies, or involve the joint boycott of certain transactions. The Dominant Position Category is administered by the NDRC, and regulates certain tactics when employed by businesses with a dominant market position, such as selling below cost, tied selling, selling commodities at unfairly high prices or buying commodities at unfairly low prices, and refusing to trade with certain parties without justification.

4.2 Regulation of Unfair Competition

The PRC’s Anti-unfair Competition Law provides some of the same marketplace protections that are embodied in the statutory and common law of Canada. The law prohibits such acts as passing off the registered trade-marks and enterprise name of another party, selling products below cost, obtaining and using the trade secrets of other parties, tied selling, collusion among parties to a tendering process, and libel and slander of a competitor’s products. In particular, it is not permissible to obtain trade secrets from a party where doing so would breach such party’s confidentiality obligations (for example, employees and other parties bound by confidentiality agreements). The remedies for acts of unfair competition include an accounting of damages suffered by the injured party, state-administered fines, and cease-and-desist orders.

5. Foreign Exchange Law China’s currency is called the Renminbi or, most commonly, the RMB. Unlike the Canadian dollar, the RMB is a controlled currency that is generally not freely tradeable outside China, although exceptions are developing. The RMB is ultimately monitored and controlled by China’s State Administration of Foreign Exchange (SAFE). In the past, all foreign currency exchanges involving the purchase or sale of RMB were subject to SAFE review and approval. Since becoming a member of the WTO in 2001, however, China’s foreign currency policy has become increasingly less restrictive.

Foreign currency transactions in China are categorized as pertaining to the “capital account” or the “currency account”. From a company’s perspective, capital account transactions refer to the transfer of ownership of a non-financial asset (other than inventories) or the forgiveness of a debt. Capital account transactions are typically large and infrequent. Current account transactions may generally be defined as transfers other than capital account transfers. Most transfers in the ordinary course of business, including the issue of dividends and the repayment of foreign debt, are current account transfers.

Foreign currency exchanges involving RMB are less regulated for current account transactions. If proper documentation is in place, many such transactions can be processed with little or no review of the underlying transaction. In contrast, the exchange of RMB in the context of capital account transactions is still quite regulated in China. Such transactions are subject to SAFE review and approval, among other procedures.

When contemplating transactions involving the purchase or sale of RMB, it is always advisable to consider whether or not the conditions for the exchange will satisfy SAFE and its delegated banks. In some cases, it is a prudent step to seek review and approval from SAFE prior to executing a transaction to ensure that problems will not be encountered at a later stage. However, as with most pre-approvals issued in China, there is still a risk that a different conclusion will be reached on formal review.

Page 16 BLAKE, CASSELS & GRAYDON LLP

6. Import and Export Law As a member of the WTO, China’s system of tariffs and duties is structured in accordance with the WTO agreements and other bilateral and multilateral trade agreements. As in Canada, the applicable tariff or duty, if any, depends on several factors, most notably the nature of the particular good at issue. China has put in place certain mechanisms – such as bonded zones and processing trade arrangements – that can be employed to import and re-export goods with reduced or eliminated tariffs and duties.

In China, companies are not permitted to engage in import or export activities unless they first undergo a registration process provided by law. It is also possible to conduct import and export activities using a qualified agent as an intermediary. Unless otherwise provided by law, qualified importers and exporters are permitted to conduct import and export activities without restrictions and subject to certain procedural requirements. In some cases, the law of China imposes special licence and quota requirements on the import and export of certain goods and imposes special licence requirements on the import and export of certain technologies. The law also prohibits the import and export of certain goods and technologies. The goods and technologies that are subject to certain restrictions or prohibitions are updated in catalogues released by the authorities from time to time.

Page 17 BLAKE, CASSELS & GRAYDON LLP

IV. THE NEXT STEPS In this guide, we have emphasized the value of conducting due diligence and understanding legal and business standards prior to establishing a business vehicle in China or otherwise doing business in China. The first step should be to gather as much information as possible to determine whether and to what degree it makes sense to enter the China market. In some cases, it may make sense to establish a representative office to get a better understanding of whether a larger commitment in the future makes good business sense.

If a business case can be made for entering the China market, the next step is to formulate a strategy going forward. At this stage of the process, investors should consider enlisting the help of experienced legal advisors. With offices in Canada, the United States, China, London and the Middle East/Gulf regions, Blake, Cassels & Graydon LLP has extensive experience working with Canadian businesses and investors to achieve their objectives in China. We would be happy to discuss how we can help you and your business formulate and implement your China strategy.

Page 18 BLAKE, CASSELS & GRAYDON LLP

V. CHINA PRACTICE GROUP CONTACTS For further information, please feel free to contact one of our China Group members:

BEIJING Robert Kwauk Telephone: 011-8610-6530-9001 Facsimile: 011-8610-6530-9008 Email: [email protected] Peter Morley Telephone: 011-8610-6530-9001 Facsimile: 011-8610-6530-9008 Email: [email protected] TORONTO Robert Granatstein Telephone: 416-863-2748 Facsimile: 416-863-2653 Email: [email protected] Andrew Pollock Telephone: 416-863-2431 Facsimile: 416-863-2653 Email: [email protected]

VANCOUVER Bill Maclagan Telephone: 604-631-3336 Facsimile: 604-631-3309 Email: [email protected] MONTRÉAL Denis Boudreault Telephone: 514-982-4004 Facsimile: 514-982-4099 Email: [email protected] CALGARY Michael Laffin Telephone: 403-260-9692 Facsimile: 403-260-9700 Email: [email protected] UNITED STATES Geoff Belsher Telephone: 212-893-8223 Facsimile: 212-829-9500 Email: [email protected]

BLAKE, CASSELS & GRAYDON LLP

OFFICE LOCATIONS

MONTRÉAL 600 de Maisonneuve Boulevard West

Suite 2200 Montréal, Quebec H3A 3J2 Telephone: 514-982-4000 Facsimile: 514-982-4099

Email: [email protected]

CHICAGO Blake, Cassels & Graydon (U.S.) LLP

181 West Madison Street, Suite 3925 Chicago, Illinois U.S.A. 60602–4645

Telephone: 312-739-3610 Facsimile: 312-739-3611

Email: [email protected]

OTTAWA 45 O'Connor Street

Suite 2000, World Exchange Plaza Ottawa, Ontario K1P 1A4 Telephone: 613-788-2200 Facsimile: 613-788-2247

Email: [email protected]

LONDON 23 College Hill, 5th Floor

London, England EC4R 2RP Telephone: +44-20-7429-3550 Facsimile: +44-20-7429-3560

Email: [email protected]

TORONTO 199 Bay Street

Suite 4000, Commerce Court West Toronto, Ontario M5L 1A9 Telephone: 416-863-2400 Facsimile: 416-863-2653

Email: [email protected]

BAHRAIN Blake, Cassels & Graydon LLP in association

with Dr. Saud Al-Ammari Law Firm 5th Floor, GB Corp Tower

Bahrain Financial Harbour, P.O. Box 11005 Manama, Kingdom of Bahrain

Telephone: +973-17-15-15-00 Facsimile: +973-17-10-49-48

Email: [email protected]

CALGARY 855 - 2nd Street S.W.

Suite 3500, Bankers Hall East Tower Calgary, Alberta T2P 4J8 Telephone: 403-260-9600 Facsimile: 403-260-9700

Email: [email protected]

AL-KHOBAR* Dr. Saud Al-Ammari Law Firm in association

with Blake, Cassels & Graydon LLP Apicorp Building, P.O. Box 1404

Al-Khobar 31952, Kingdom of Saudi Arabia Telephone: +966-3-847-5050 Facsimile: +966-3-847-5353

Email: [email protected] VANCOUVER

595 Burrard Street, P.O. Box 49314 Suite 2600, Three Bentall Centre

Vancouver, British Columbia V7X 1L3 Telephone: 604-631-3300 Facsimile: 604-631-3309

Email: [email protected]

BEIJING 7 Dong Sanhuan Zhonglu, Suite 901 Office Tower A, Beijing Fortune Plaza

Chaoyang District, Beijing 100020 People's Republic of China

Telephone: +86-10-6530-9010 Facsimile: +86-10-6530-9008

Email: [email protected]

NEW YORK Blake, Cassels & Graydon (U.S.) LLP

126 East 56th Street, Suite 801, Tower 56 New York, New York U.S.A. 10022–3613

Telephone: 212-893-8200 Facsimile: 212-829-9500

Email: [email protected]

SHANGHAI* 1376 Nan Jing Xi Lu

Suite 718, Shanghai Centre Shanghai 200040, People’s Republic of China

Telephone: +86-10-6530-9010 Facsimile: +86-10-6530-9008 Email: [email protected]

www.blakes.com * Affiliated office 12408926.2

© 2012 Blake, Cassels & Graydon LLP