Bharat Anand

48

COMPANIES ACT, 2013 Bharat Anand | New Delhi | 19 September 2013 New Rules of the Game!

description

SAD

Transcript of Bharat Anand

COMPANIES ACT, 2013

Bharat Anand | New

Delhi

| 19 September 2013

New Rules of the Game!

Copyright © Khaitan & Co 2013

| 2

Contents

1. Concepts relevant for Mergers & Acquisitions

1. Enforcement of Shareholders‟ Agreements

2. Court approved schemes & Squeeze Out

3. Restrictions on Slump Sale

4. Buy-back

2. Other Key Changes

1. Private companies | Increased compliance burden

2. One Person Companies

3. Layered Investments

4. Related Party Transactions

5. Financial Assistance

Copyright © Khaitan & Co 2013

| 3

Out of Scope!

• Corporate Social Responsibility

• Governance, Disclosures & Transparency

• Independent Director - Role & Responsibility

• Directors & KMPs - Duties, Responsibilities

& Liabilities

• Audit and financial statements

Copyright © Khaitan & Co 2013

| 4

Concepts relevant for Mergers &

Acquisitions

Copyright © Khaitan & Co 2013

| 5

Enforcement of Shareholders‟

Agreement Background

• Under CA1956, share transfer restrictions in

shareholders‟ agreement between shareholders of a public

company challenging (S 111A; no safe harbour for transfer

restrictions inter-se existing shareholders)

Key Change

• CA2013 recognises that arrangements in respect of

transfer of securities (even in case of a „public

company‟) shall be enforceable as a contract [S 58(2)

Proviso]

• A public subsidiary can continue to be in the nature of a

private company in its articles – i.e. it can have

transferability restrictions [S 2(71) Proviso]

Impact

• The change finally settles the position on

enforceability of agreements providing for pre-emptive

rights inter-se shareholders of a public company such as

lock-in period, ROFR, ROFO, tag-along, drag-along

• As CA2013 requires all transfers of securities to be in

compliance with SCRA [S 59(4)] | Enforceability of

put/call options is still an issue?

Copyright © Khaitan & Co 2013

| 6

Enforcement of Shareholders‟

AgreementS 5

• Flexibility to specify that certain provisions of the

articles may only be altered if specified conditions or

procedures more restrictive than a special resolution are

complied with

• For a private company, entrenchment provisions must be

inserted at the time of formation or by a unanimous

shareholders‟ resolution

• For a public company, entrenchment provisions must be

inserted at the time of formation or by a special

resolution

• ROC will need to be notified of entrenchment provisions

within 30 days of incorporation or amendment to articles

[R 2.7]

• Unclear how this would dovetail with S 6(b) of CA2013

(Articles cannot be repugnant to the provisions of

CA2013)

Impact

• Super-majority voting provisions preferred over veto

rights?

• Statutory sanction to entrenchment provisions will

strengthen the enforceability of those provisions

Watch outs

Entrenchment provisions should be incorporated in compliance with special

/unanimous approval requirements of CA2013, depending on type of company

Copyright © Khaitan & Co 2013

| 7

Court Approved Schemes

Copyright © Khaitan & Co 2013

| 8

Court Approved Schemes

• Broadly still requires 75% approval from the shareholders

• Wide powers of NCLT to sanction

Procedural Issues

• Application to Tribunal by company/members/creditors for a scheme of

compromise, arrangement, reconstruction or amalgamation | Scheme for

reorganisation of share capital included [S 230 read with S 232]

• Application to contain prescribed disclosures | Disclosure

obligations increased [S 230(2), S 232(2) in case of reconstruction

or amalgamation]

• Tribunal shall call meeting of members/creditors

• Notice for meeting to be accompanied with: (a) statement disclosing

details of scheme; (b) copy of valuation report; (c) effect on

creditors, key managerial personnel, promoters and non-promoters [S

230(2)] | Additional documents to be circulated in cases of

reconstructions or amalgamations [S 232(2)]

• Notice to be given to Central Government, IT authorities, RBI, SEBI,

CCI, Official Liquidator, Registrar or stock exchanges or other

sectoral regulators [S 230 (5)]

• If Central Government, IT authorities, RBI, SEBI, CCI, Official

Liquidator, Registrar or stock exchanges do not represent on a

scheme of compromise or arrangement, within 30 days of notice, then

presumption of no representation [S 230 (5)]

Copyright © Khaitan & Co 2013

| 9

Court Approved Schemes

Procedural Issues (Contd)

• Objection to scheme of compromise or arrangement can now

be made by: (a) shareholders holding at least 10% of

shareholding; or (b) 5% of total outstanding debt per

latest audited financial statements [S 230(4), Proviso]

• Dispensation from calling of creditors meeting by the

Tribunal if 90% in value agree and confirm [S 230 (9)]

• Approval of 75% member/creditors required for Tribunal to

sanction the scheme

• Creditors, members or debenture holders can also vote by

proxy within 1 month from receipt of notice | Voting to be

in person or postal ballot or by proxy [S 230(6)]

• Filing of certificate from company‟s auditor on conformity

of accounting treatment as proposed in the scheme with the

accounting standards under CA2013 is pre-requisite to

sanction [S 230 (7), Proviso, 232(3), Proviso]

• Filing of order with the Registrar within 30 days of

receipt of order [S 230(8), 232(5)]

• Tribunal has power to set-off stamp duty paid against

stamp duty payable for increase in authorised share

capital

• Scheme not whitewash for offences by officers-in-default

of the transferor company [S 232(3)(c)]

Copyright © Khaitan & Co 2013

| 10

Court Schemes | Overall (Contd)

Other Changes

• Order for compromises and arrangements to include: [S 230(7)

• Option to preference shareholders to either obtain arrears of

dividend in cash or equity shares of equal value

• Variation of shareholder rights

• Abatement of SICA proceedings before BIFR if scheme approved by

3/4th of creditors in value

• Exit offer to dissenting shareholders

• „Appointed date‟ finds its place; scheme to be effective from the

designated appointed date and not a date afterwards [S 232(6)]

• Where any scheme or contract approved by 90% shareholders,

transferee company has the option to acquire the shares of the

dissenting shareholders [S 235]

• Payments held by transferor company on trust for the

dissenting minority

• Drag along clauses : enforceable after 90% shareholders

approve?

• No treasury shares can now be issued; to be cancelled /

extinguished [S 232(3)(b)] | Tax implications on continuing

shareholders pursuant to change of rule relating to treasury

shares to be analysed

X merged with it's subsidiary Y; the merged entity ended up

with its own stock held by a trust, specially created for the

purpose. Separate ownership so full voting rights, full dividends,

right to participate in meetings | Now no longer possible

Copyright © Khaitan & Co 2013

| 11

Listed company mergers

Scheme of a listed transferor with an unlisted transferee [S

232(3)(h)]

• No “backdoor listing” permitted: If listed company merges with

unlisted company, then transferee company will remain

unlisted

• Shareholders of listed company have right to opt out of the

transferee company by payment of the value of shares and other

benefits in accordance with pre-determined formula or post

valuation (subject to floor price specified by SEBI);

arrangements for this to be made by the Tribunal

Impact

• Potential to make the process efficient and less time

consuming

Copyright © Khaitan & Co 2013

| 12

Short-Form Merger

New Concept

Short-Form Merger permitted for merger between:

• holding company and its wholly-owned subsidiary

• 2 or more small companies

• other specified companies [S 233]

In Brief

Option for eligible companies to use short-form process or the

usual process

• Need 90% shareholders approval at general meeting

• Need approval of majority of lenders representing 9/10th in

value of creditors in a meeting convened with 21 days‟ notice

• Declaration of solvency to be filed

• Registrar and Official Liquidator call for objections within

30 days; if no objections then approval, and, if objections,

then referred to Central Government for consideration by

Tribunal

Impact

• Positive development, but needs to be tested for practical

challenges

Copyright © Khaitan & Co 2013

| 13

Cross-Border Merger

Concept

• Concept of Indian company merging with foreign company

recognised [s. 234]

• Consideration can be mix of cash and depository

receipts

Impact

• If works, then can greatly benefit structuring cross-

border M&A transactions

Blind Spots

• Companies of countries that will be entitled to regime

are to be notified by the Government

• RBI regulations on such mergers will be determinant

• Several issues, like holding of real estate, and other

FDI issues may need to examined / tested

Copyright © Khaitan & Co 2013

| 14

Minority Squeeze-out

• New Concept [S 236]

• Acquirer or PAC (as understood under Takeover Regulations) with 90% ormore of issued equity capital can notify the company of intent tosqueeze-out minority

• Price to be determined on the basis of valuation by a registeredvaluer

• However, minority shareholders may also initiate this process! ExitOpportunity

• Escrow account with amount equal to the value of the minority sharesto be created and maintained for at least 1 year

• Payment to be made within 60 days of minority shareholder tenderingshares

• Anti Embarrassment provisions : s236(8); typo? Drafting unclear!

• Blind Spots

• Is this a mandatory requirement? What if the majority shareholder hasno „intention‟ to acquire? Does „intention‟ not to buy have to benotified to the company?

• If the „intention‟ is not there upon acquiring 90%, can the right beexercised later?

• When does the escrow account need to be created in the course of theprocess?

• Mechanism for minority to trigger this process? Threshold?

• Will this apply only to listed companies or all companies?

Copyright © Khaitan & Co 2013

| 15

Slump Sale

Section 180(1)(a); Chapter XII

Copyright © Khaitan & Co 2013

| 16

Slump Sale

• Background

• Under the CA1956, ordinary resolution required for

sale, lease or otherwise disposal of whole or

substantially whole of the „undertaking‟ of a company

by public companies and private companies that are

subsidiary of public companies [S 293(1)(a)]

• Key Changes

• Special resolution required by all companies for any

transfer of the whole or substantially the whole a

substantial Undertaking under CA2013 [S 180(1)]

• “Undertaking” means an undertaking:

• with investment of the company exceeding 20% of its net

worth determined as per its latest audited balance sheet OR

• which generates 20% or more of total income during previous

FY

• “Substantially whole of the undertaking” means 20% or

more of value of undertaking per preceding FY‟s audited

balance sheet

• Not all transfers of „undertakings‟ covered! |

„undertakings‟ which do not satisfy the above

materiality tests will not be subject to the

requirement for a special resolution

Copyright © Khaitan & Co 2013

| 17

• Impact

• Private companies included

• Blind spots

• How is reference to the word “investment” to

be construed? All debt and equity injected in

the Undertaking?

• Is the book value of the undertaking

irrelevant?

• Asset deals, involving cherry picking assets,

also intended to be covered – substantially

all of an Undertaking

Slump Sale

Copyright © Khaitan & Co 2013

| 18

Slump Sale

Practical Examples

• Company A, a manufacturing company with a

turnover of INR 1000 crore, wishes to

transfer a business unit „X‟ which has a

book value of less than 20% of the net

worth and generates less than 20% income?

• Company B with a net worth of INR 700

crore wishes to transfer “land bank” of

500 acres which it purchased 3 years back

for INR 200 crore?

• Company C, a WOS of Company B (a listed

company), wishes to transfer an

Undertaking to XYZ exceeding the 20% test.

Will a special resolution be require by

the shareholders of Company B?

Copyright © Khaitan & Co 2013

| 19

Buy-back

Section 68, Chapter IV

Copyright © Khaitan & Co 2013

| 20

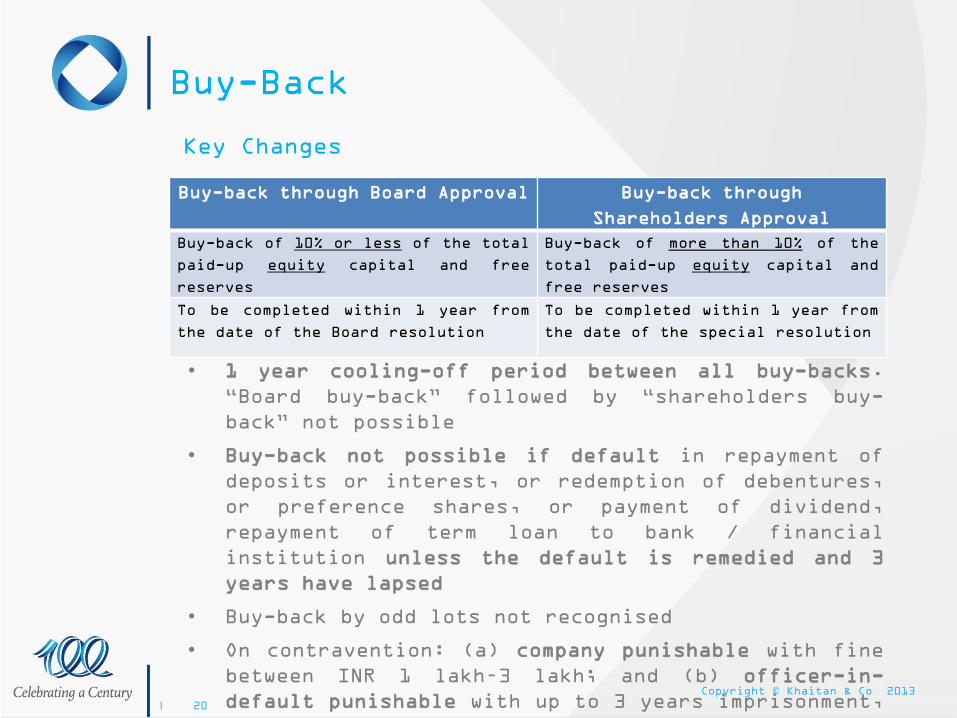

Buy-Back

• 1 year cooling-off period between all buy-backs.

“Board buy-back” followed by “shareholders buy-

back” not possible

• Buy-back not possible if default in repayment of

deposits or interest, or redemption of debentures,

or preference shares, or payment of dividend,

repayment of term loan to bank / financial

institution unless the default is remedied and 3

years have lapsed

• Buy-back by odd lots not recognised

• On contravention: (a) company punishable with fine

between INR 1 lakh–3 lakh; and (b) officer-in-

default punishable with up to 3 years imprisonment,

or fine between INR 1 lakh-3 lakh or both

Buy-back through Board Approval Buy-back through

Shareholders Approval

Buy-back of 10% or less of the total

paid-up equity capital and free

reserves

Buy-back of more than 10% of the

total paid-up equity capital and

free reserves

To be completed within 1 year from

the date of the Board resolution

To be completed within 1 year from

the date of the special resolution

Key Changes

Copyright © Khaitan & Co 2013

| 21

Buy-Back

Impact

• 1 year cooling-off period can significantly impact

transactions where multiple buy-backs are required

(subject to the overall cap); Exits through buy-back

will become more difficult

• Applicability of this restriction even where buy-

back achieved through Court Scheme (which expressly

recognizes and permits buy-back, but requires

conditions of S 68 to be satisfied) [S 230(10)]

Copyright © Khaitan & Co 2013

| 22

Other Key Changes

Copyright © Khaitan & Co 2013

| 23

Withdrawal of Dispensations

available for Private Companies

under CA1956Key Changes

• Many of the privileges and exemptions currently

available to private companies in the CA1956 stand

withdrawn in CA2013.

• Stricter compliance and disclosure regime for private

companies under the CA2013.

• This would require revamping and scaling up internal

processes by the private companies.

• The long term objective is to boost the standards of

corporate governance in private companies.

Copyright © Khaitan & Co 2013

| 24

Withdrawal of Dispensations available

for Private Companies under CA1956

Particulars Provision under

CA1956

Provisions under CA2013 Implications

Shares Sections 85 (Two kinds

of share capital), 86

(New issues of share

capital to be only of

two kinds) and 87

(Voting rights): Section

90(2) exempts a private

company (unless it is a

subsidiary of a public

company) from the

provisions under

Sections 85-87 of the

Act.

Sections 43 (Kinds of share

capital) and 47 (Voting

rights): Sections applicable to

both public companies as well

as private companies.

Exemption to private

companies has been done

away with. This means

that:

• Types of share

capital: Private

companies can now

have only two kinds

of share capital i.e.

equity and

preference; and

• Voting Rights:

- Equity Shareholder:

Right to vote on

every resolution pro

rata on poll

- Preference

Shareholder: Right to

vote only on

resolutions which

directly affect the

rights attached to

his preference shares

and any resolution

for winding up or

repayment or

reduction of share

capital | Right to

vote on all

Copyright © Khaitan & Co 2013

| 25

Withdrawal of Dispensations available

for Private Companies under CA1956

Particulars Provision under

CA1956

Provisions under CA2013 Implications

Further Issue

of Share

Capital |

Renouncement

Section 81(1)(c):

Unless the AOA of

the company

otherwise provide, a

shareholder has the

right to renounce

the shares offered

to him in favour of

any other persons.

Not applicable to

private companies.

Section 62(1)(a)(ii):

Similar provision as

Section 81(1)(c) of

CA1956. However,

applicable to private

companies also.

Restrictions on

renouncement to be

specifically

included in the AOA

of private

companies.

Preferential

Allotment

Section 81A:

Preferential

allotment requires

special resolution.

Not applicable to

private companies.

Section 62(c):

Preferential allotment -

special resolution

required for both public

companies as well as

private companies.

Price of shares to be

determined by the

registered valuer.

Copyright © Khaitan & Co 2013

| 26

Withdrawal of Dispensations available

for Private Companies under CA1956

Particulars Provision under

CA1956

Provisions under CA2013 Implications

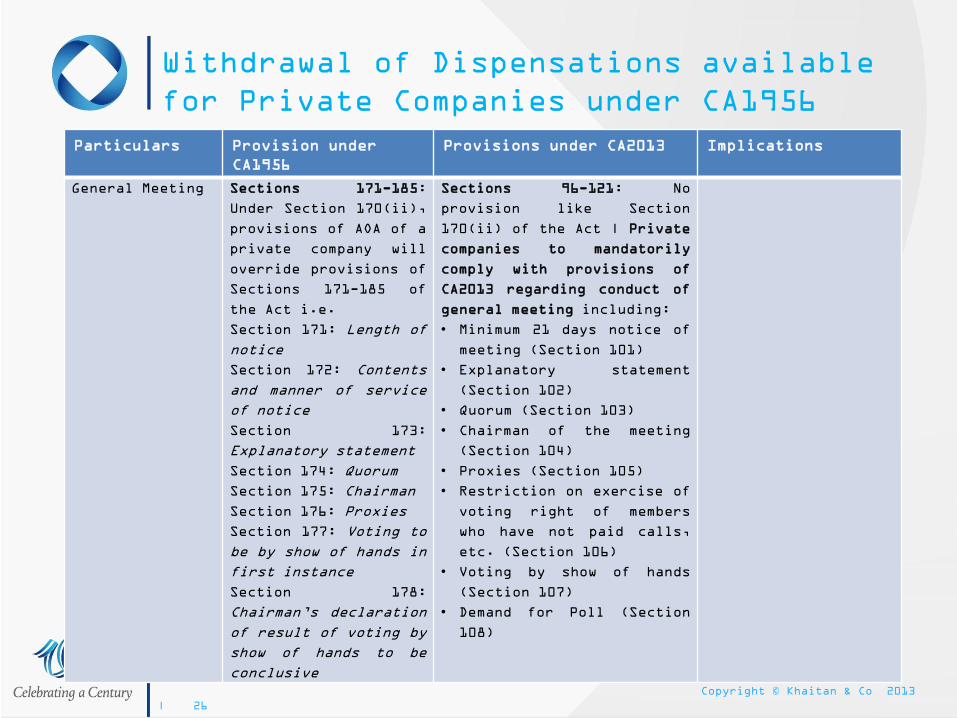

General Meeting Sections 171-185:

Under Section 170(ii),

provisions of AOA of a

private company will

override provisions of

Sections 171-185 of

the Act i.e.

Section 171: Length of

notice

Section 172: Contents

and manner of service

of notice

Section 173:

Explanatory statement

Section 174: Quorum

Section 175: Chairman

Section 176: Proxies

Section 177: Voting to

be by show of hands in

first instance

Section 178:

Chairman‟s declaration

of result of voting by

show of hands to be

conclusive

Sections 96-121: No

provision like Section

170(ii) of the Act | Private

companies to mandatorily

comply with provisions of

CA2013 regarding conduct of

general meeting including:

• Minimum 21 days notice of

meeting (Section 101)

• Explanatory statement

(Section 102)

• Quorum (Section 103)

• Chairman of the meeting

(Section 104)

• Proxies (Section 105)

• Restriction on exercise of

voting right of members

who have not paid calls,

etc. (Section 106)

• Voting by show of hands

(Section 107)

• Demand for Poll (Section

108)

Copyright © Khaitan & Co 2013

| 27

WITHDRAWAL OF DISPENSATIONS AVAILABLE FOR

PRIVATE COMPANIES UNDER THE ACT

Particulars Provision under

CA1956

Provisions under CA2013 Implications

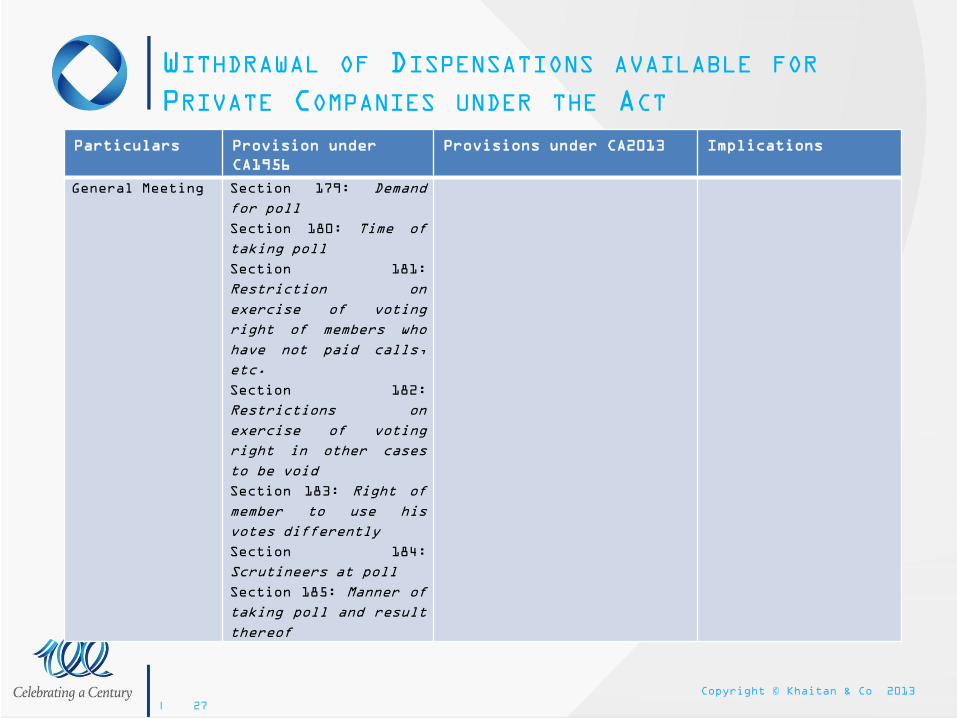

General Meeting Section 179: Demand

for poll

Section 180: Time of

taking poll

Section 181:

Restriction on

exercise of voting

right of members who

have not paid calls,

etc.

Section 182:

Restrictions on

exercise of voting

right in other cases

to be void

Section 183: Right of

member to use his

votes differently

Section 184:

Scrutineers at poll

Section 185: Manner of

taking poll and result

thereof

Copyright © Khaitan & Co 2013

| 28

Withdrawal of Dispensations available

for Private Companies under CA1956

Particulars Provision under

CA1956

Provisions under CA2013 Implications

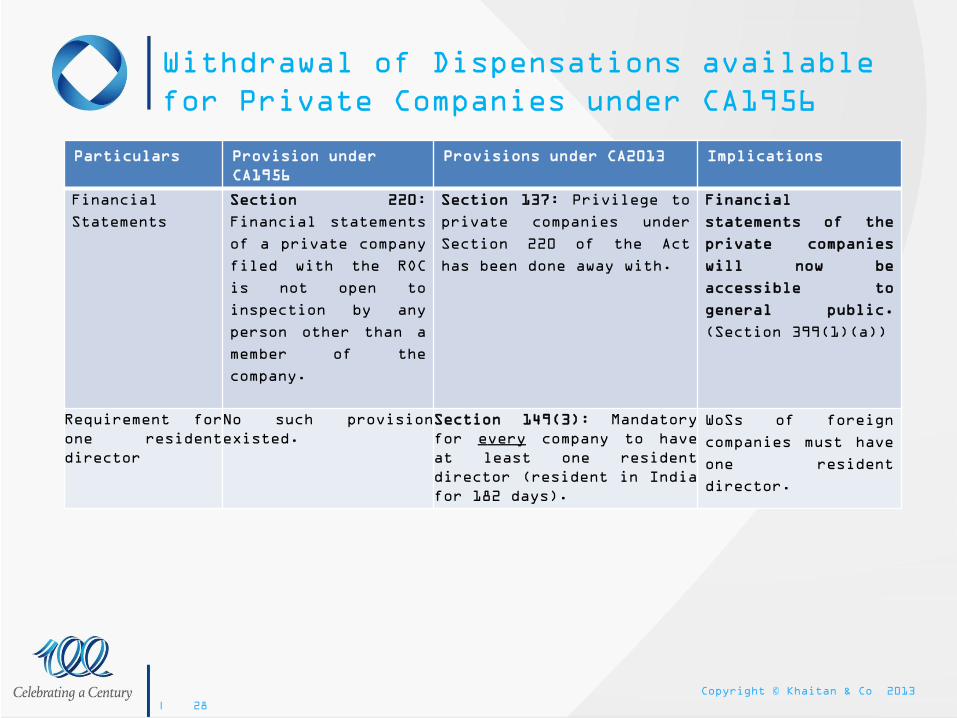

Financial

Statements

Section 220:

Financial statements

of a private company

filed with the ROC

is not open to

inspection by any

person other than a

member of the

company.

Section 137: Privilege to

private companies under

Section 220 of the Act

has been done away with.

Financial

statements of the

private companies

will now be

accessible to

general public.

(Section 399(1)(a))

Requirement for

one resident

director

No such provision

existed.

Section 149(3): Mandatory

for every company to have

at least one resident

director (resident in India

for 182 days).

WoSs of foreign

companies must have

one resident

director.

Copyright © Khaitan & Co 2013

| 29

Withdrawal of Dispensations available

for Private Companies under CA1956

Particulars Provision under

CA1956

Provisions under CA2013 Implications

Restriction on

number of

Directorships

Section 275: No person

to be a director of

more than 15 companies.

Section 278: A private

company (which is

neither subsidiary nor

a holding company of a

public company) is

excluded while

calculating the number

of companies one can be

a director for.

Section 165:

• Cap on total number of

directorships increased

from 15 to 20

• Out of 20 directorships,

not more than 10 can be of

public companies

• Directorships of private

companies will also be

counted.

Directorship in

private companies will

now be taken into

account while

calculating the number

of companies one can

be a director for.

What about section 25

Companies?

Copyright © Khaitan & Co 2013

| 30

Withdrawal of Dispensations available

for Private Companies under CA1956

Particulars Provision under

CA1956

Provisions under CA2013 Implications

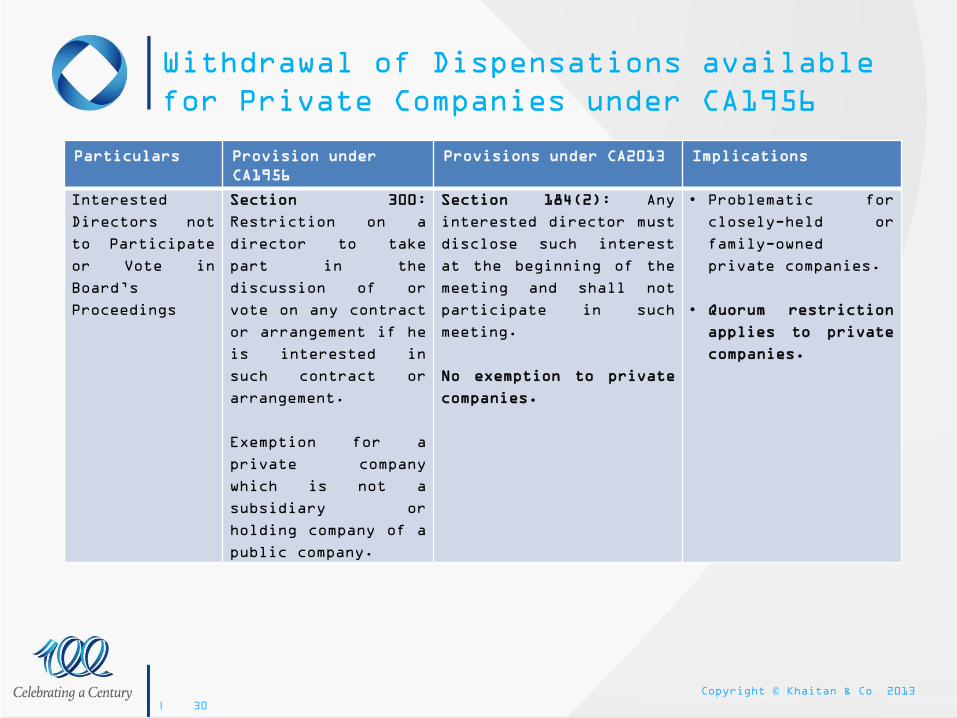

Interested

Directors not

to Participate

or Vote in

Board‟s

Proceedings

Section 300:

Restriction on a

director to take

part in the

discussion of or

vote on any contract

or arrangement if he

is interested in

such contract or

arrangement.

Exemption for a

private company

which is not a

subsidiary or

holding company of a

public company.

Section 184(2): Any

interested director must

disclose such interest

at the beginning of the

meeting and shall not

participate in such

meeting.

No exemption to private

companies.

• Problematic for

closely-held or

family-owned

private companies.

• Quorum restriction

applies to private

companies.

Copyright © Khaitan & Co 2013

| 31

One Person Companies

Copyright © Khaitan & Co 2013

| 32

OPC | Concept

New Concept

• One Person Company (“OPC”) is a new business vehicle

introduced as a private company

• Clause 2 (62) of CA2013 defines an OPC as a company

which has only one person (Indian citizen) as a member

[R 1.1(Chapt II)]

• OPC may either be a company limited by shares, a company

limited by guarantee or an unlimited company

• Words “One Person Company” are required to be mentioned

in brackets below the name of the OPC, wherever such

name is printed, affixed or engraved [S 12(3)(d),

Proviso]

Copyright © Khaitan & Co 2013

| 33

OPC | Salient Features

New Concept

• Minimum paid up share capital of INR 100,000

• Change in nominee to be intimated to the OPC and the

Registrar of Companies (“ROC”)

• Sole member to act as the first director, until the OPC

appoints director(s) [S 152(1)]

• OPC can appoint maximum 15 directors, but minimum should

be one director.

• Resolutions to require communication by the

member/director to the company and entry in minutes-book.

The minutes-book to be signed and dated by the member and

such date shall be deemed to be the date of the meeting

for all the purposes under CA2013 [S 122(3) and (4)]

• Public disclosure of financial statements: OPC to file

its financial statements with ROC within 180 days from

the closure of the financial year [S 137(1), Proviso]

Copyright © Khaitan & Co 2013

| 34

OPC | Disadvantages

• Only an Indian citizen and „resident‟ in India can

be a member [R 2.1(1)]

• Mandatory conversion to a private or public

company within 6 months if paid-up capital exceeds

INR 5 million or average annual turnover during

the relevant period* exceeds INR 20 million [R

2.3(2)]

*“relevant period” means the period of immediately

preceding 3 financial years

Copyright © Khaitan & Co 2013

| 35

Layered Investments

Section 186(1); Chapter XII

Copyright © Khaitan & Co 2013

| 36

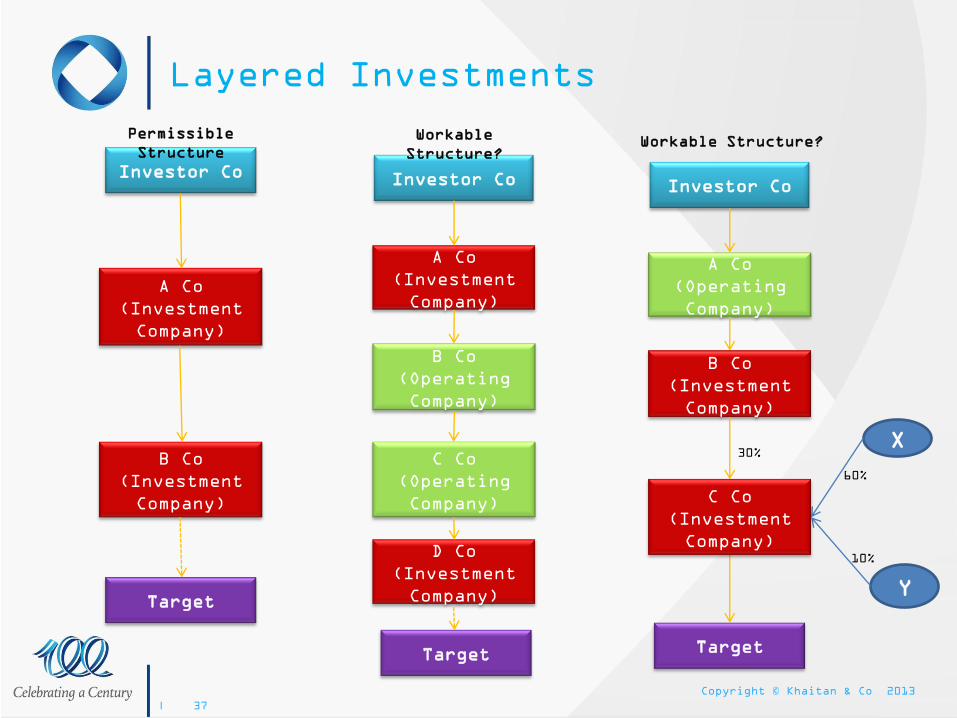

Layered Investments

Background

• Recommendation from the Parliamentary Standing

Committee on Finance post Satyam scam

• For transparency; to prevent convoluted structures

and diversion of funds

New Restriction

• A company cannot make investments through more than

2 layers of investment companies

• “Investment company” means a company whose

principal business is acquisition of shares,

debentures or other securities

• Whether the restriction is applicable only to

„investment subsidiaries‟?

Copyright © Khaitan & Co 2013

| 37

Layered Investments

Investor Co

A Co

(Investment

Company)

Permissible

Structure

Investor Co

A Co

(Investment

Company)

Workable

Structure?

C Co

(Operating

Company)

B Co

(Operating

Company)

D Co

(Investment

Company)

B Co

(Investment

Company)

Target

Target

Investor Co

A Co

(Operating

Company)

Workable Structure?

B Co

(Investment

Company)

Target

X

Y

30%

60%

10%

C Co

(Investment

Company)

Copyright © Khaitan & Co 2013

| 38

Layered Investments

Impact

• Takes away flexibility to structure

investments

• Genuine transactions will be severely

impacted, in particular, investments in

the Infrastructure sector

• Ability of India Inc to monetise at

various subsidiary levels will be

impaired

• Companies will have to demonstrate

operations in the subsidiaries |

operation and compliance costs

Outbound Acquisitions

• Statutory recognition of more than one

layers for offshore acquisitions

Copyright © Khaitan & Co 2013

| 39

Layered Investments

Exemptions:

• Offshore acquisition possible if the

offshore target has investment

subsidiaries beyond 2 levels, as per the

laws of such country

• Subsidiary can have investment subsidiary

to meet regulatory requirements

Watch outs

On contravention: (a) company punishable with fine

between INR 25,000-5 lakh; (b) officer-in-default

punishable with up to 2 years imprisonment + fine

between INR 25,000-1 lakh

Copyright © Khaitan & Co 2013

| 40

Related Party Transactions

Section 188, Chapter XII

Copyright © Khaitan & Co 2013

| 41

Related Party – Definition

Director, key managerial personnel or relative of such person

Firm in which a director, manager or relative is a partner

Private company in which a director or manager is a member or director

A public company in which a director or manager is (a) a director; or (b) along with relatives holds more than 2%

Any body corporate whose Board, MD or manager is accustomed to act in accordance with the advice, directions or instructions of a director or manager

Any person on whose advice, directions or instructions a director or manager is accustomed to act

Includes holding company, subsidiary, associate company, fellow company

Copyright © Khaitan & Co 2013

| 42

Related Party Transactions

Transactions covered [S 188]

• Sale, purchase or supply of any goods or materials

• Selling or otherwise disposing of, or buying,

property

• Leasing of property

• Availing or rendering of any services

• Appointment of any agent for purchase or sale of

goods, materials, services or property

• Such related party's appointment to any office or

place of profit in the company, its subsidiary or

associate company

• Underwriting the subscription of any securities or

derivatives thereof, of the company

Copyright © Khaitan & Co 2013

| 43

Related Party Transactions

Board Meeting Notice Requirements [R 12.13 (1)]:

• Name of the related party and nature of the

relationship;

• Nature, duration and particulars of the contract;

• Material terms of the contract, including the value,

if any;

• Advance paid or received for the contract, if any;

and

• Any other information relevant to the Board‟s

decision

Board Meeting Attendance [R 12.13 (2)]:

• Interested director to leave a Board meeting during

any discussion on the subject matter of a resolution

on a related party contract in which he is interested

Copyright © Khaitan & Co 2013

| 44

Related Party Transactions

Exemption:

• Transactions on an arm‟s length basis entered into in

the ordinary course of business

Board‟s Report:

• Related party transactions, including the reasons for

entering into the relevant transactions, to be included

in the Board‟s report to the shareholders

Impact:

• Reconciliation of board Vs. shareholder approval

• The scope of the existing provisions has been enlarged

Blind spots:

• How will prohibition on members voting be counted? Will

it apply to all items or only if members that are also

related parties are interested in the contract

Copyright © Khaitan & Co 2013

| 45

Financial Assistance

Section 67; Chapter IV

Copyright © Khaitan & Co 2013

| 46

Financial Assistance

What is the law under S 67?

• “No public company shall give, whether directly or

indirectly and whether by means of a loan, guarantee, the

provision of security or otherwise, any financial

assistance for the purpose of, or in connection with, a

purchase or subscription made or to be made, by any

person of or for any shares in the company or in its

holding company.”

Issues?

• Payment of due diligence costs or advisors fees by Target

• Indemnity by Target in the underwriting agreement

• Joint venture with royalty by Target to partner

Any exception?

• PROVISIONS NOT APPLICABLE TO PRIVATE COMPANIES

• Exemption to:

• lending by banking companies in the ordinary course;

• financial assistance for purchase/subscription of shares

under ESOP; and

• loan to employees (other than directors or KMP) for an

amount not exceeding their 6 months salary for

purchase/subscription of shares of the company or its

holding company to be held by them by way of beneficial

ownership

• Financial assistance to subsidiary company not prohibited

Copyright © Khaitan & Co 2013

| 47

Financial Assistance

• On contravention: (a) company punishable with

fine between INR 1 lakh-INR 25 lakh; and (b)

officer-in-default with up to 3 years

imprisonment, and fine between INR 1 lakh-INR

25 lakh

Impact

• One of the most severe consequences on

default

• Logic? UK has abolished Financial Assistance

offense for unlisted companies; no one has

gone to jail

www.khaitanco.com

![[XLS]mcdonline.gov.inmcdonline.gov.in/tri/ndmc_mcdportal/mcdengg/content/Docs... · Web viewBPCL Harjinder Singh, T. S. anand, Bharat Petroleum Corporation LTd. Petrol Pump Bharat](https://static.fdocuments.in/doc/165x107/5ac07aee7f8b9a4e7c8be7ea/xls-viewbpcl-harjinder-singh-t-s-anand-bharat-petroleum-corporation-ltd-petrol.jpg)