Bengaluru office-trends-to-watch-for-in-2015

3

1 Research & Forecast Report | January 2015 | Colliers International Bengaluru steals the show with over 13.77 million sq ft of absorption e city tops the chart with about 49% share in the pan India absorption in 2014. Robust leasing activities, especially from the IT / ITeS sector with about 73% of the city’s total absorption, backed up the overall absorption, resulting in an enormous growth from 8.65 million sq ft in 2013 to 13.77 million sq ft in 2014. Over and above this, approximately, 4.38 million sq ft of office space has been pre-committed in various IT parks that are under construction. Outer Ring Road outshined other micro-markets as the most preferred micromarket with more than 51% of the total absorption, followed by Whitefield 20% and the CBD 6%. e market has benefitted from both the increased demand from the IT/ITeS sector and the booming Indian e-commerce sector. e most significant deals in 2014 include the 3.8 million sq ft office space taken by e-commerce giant Flipkart, which alone contributed about 25% in the city’s total absorption. Moreover, existing tenants such as KPMG, IBM, L&T and Cap Gemini leased large office spaces to accommodate their growing operations. Private equity players also showed equal interest in this market. e market witnessed one of the largest JV deals between Black Stone Group and Embassy Group amounting to INR 1,951 crores for Vrindavan Tech Village spread over 106 acres. Strong absorption was complemented by robust new supply of approximately 7.17 million sq ft. About 9.1 million sq ft of supply was available for lease in the market in 4Q 2014, of which about 70% was equally distributed in EPIP Zone Whitefield and ORR. e remaining 30% of the supply City Office Barometer Research & Forecast Report Bengaluru | Office January 2015 Rental Values *Indicative Grade A rents in INR per sq ft per month **Northern part of ORR - KR Puram till Hebbal MICRO MARKETS RENTAL VALUE* % CHANGE QoQ YoY CBD 90 - 130 16% 22% Outer Ring Road (Marathalli - Sarjapur) 55 - 63 4% 7% Outer Ring Road (North)** 53 - 60 8% 28% Bannerghatta Road 50 - 60 0% 0% EPIP Zone/ Whitefield 28 - 36 0% 0% Hosur Road 25 - 40 0% 8% Electronic City 26 - 33 0% 5% INDICATORS 2014 2015 Vacancy Absorption Construction Rental Value Capital Value

-

Upload

colliers-international -

Category

Real Estate

-

view

209 -

download

0

Transcript of Bengaluru office-trends-to-watch-for-in-2015

1 Research & Forecast Report | January 2015 | Colliers International

Bengaluru steals the show with over 13.77 million sq ft of absorptionThe city tops the chart with about 49% share in the pan India absorption in 2014. Robust leasing activities, especially from the IT / ITeS sector with about 73% of the city’s total absorption, backed up the overall absorption, resulting in an enormous growth from 8.65 million sq ft in 2013 to 13.77 million sq ft in 2014. Over and above this, approximately, 4.38 million sq ft of office space has been pre-committed in various IT parks that are under construction. Outer Ring Road outshined other micro-markets as the most preferred micromarket with more than 51% of the total absorption, followed by Whitefield 20% and the CBD 6%.

The market has benefitted from both the increased demand from the IT/ITeS sector and the booming Indian e-commerce sector. The most significant deals in 2014 include the 3.8 million sq ft office space taken by e-commerce giant Flipkart, which alone contributed about 25% in the city’s total absorption. Moreover, existing tenants such as KPMG, IBM, L&T and Cap Gemini leased large office spaces to accommodate their growing operations. Private equity players also showed equal interest in this market. The market witnessed one of the largest JV deals between Black Stone Group and Embassy Group amounting to INR 1,951 crores for Vrindavan Tech Village spread over 106 acres.

Strong absorption was complemented by robust new supply of approximately 7.17 million sq ft. About 9.1 million sq ft of supply was available for lease in the market in 4Q 2014, of which about 70% was equally distributed in EPIP Zone Whitefield and ORR. The remaining 30% of the supply

City Office Barometer

Research & Forecast Report

Bengaluru | OfficeJanuary 2015

Rental Values

*Indicative Grade A rents in INR per sq ft per month**Northern part of ORR - KR Puram till Hebbal

MICRO MARKETS RENTALVALUE*

% CHANGEQoQ YoY

CBD 90 - 130 16% 22%

Outer Ring Road (Marathalli - Sarjapur)

55 - 63 4% 7%

Outer Ring Road (North)** 53 - 60 8% 28%

Bannerghatta Road 50 - 60 0% 0%

EPIP Zone/ Whitefield 28 - 36 0% 0%

Hosur Road 25 - 40 0% 8%

Electronic City 26 - 33 0% 5%

INDICATORS 2014 2015

Vacancy

Absorption

Construction

Rental Value

Capital Value

2 Research & Forecast Report | January 2015 | Colliers International

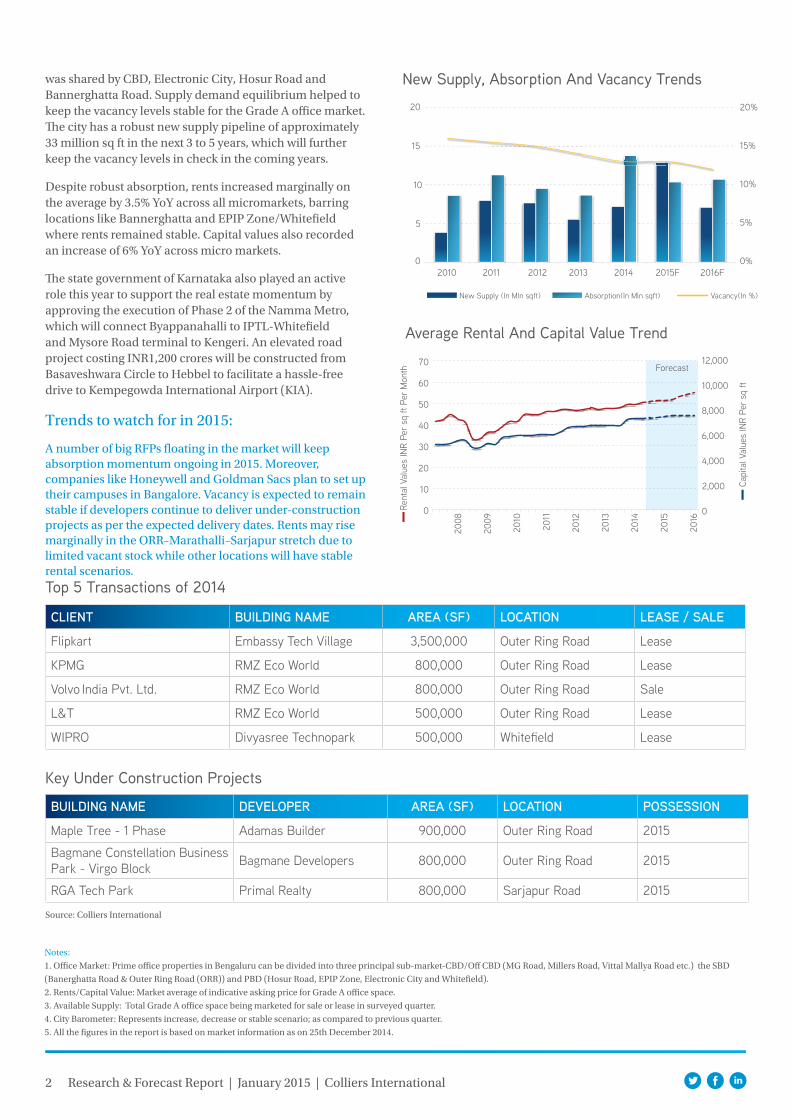

was shared by CBD, Electronic City, Hosur Road and Bannerghatta Road. Supply demand equilibrium helped to keep the vacancy levels stable for the Grade A office market. The city has a robust new supply pipeline of approximately 33 million sq ft in the next 3 to 5 years, which will further keep the vacancy levels in check in the coming years.

Despite robust absorption, rents increased marginally on the average by 3.5% YoY across all micromarkets, barring locations like Bannerghatta and EPIP Zone/Whitefield where rents remained stable. Capital values also recorded an increase of 6% YoY across micro markets.

The state government of Karnataka also played an active role this year to support the real estate momentum by approving the execution of Phase 2 of the Namma Metro, which will connect Byappanahalli to IPTL-Whitefield and Mysore Road terminal to Kengeri. An elevated road project costing INR1,200 crores will be constructed from Basaveshwara Circle to Hebbel to facilitate a hassle-free drive to Kempegowda International Airport (KIA).

Trends to watch for in 2015:

A number of big RFPs floating in the market will keep absorption momentum ongoing in 2015. Moreover, companies like Honeywell and Goldman Sacs plan to set up their campuses in Bangalore. Vacancy is expected to remain stable if developers continue to deliver under-construction projects as per the expected delivery dates. Rents may rise marginally in the ORR–Marathalli–Sarjapur stretch due to limited vacant stock while other locations will have stable rental scenarios.

Source: Colliers International

Top 5 Transactions of 2014

Key Under Construction Projects

CLIENT BUILDING NAME AREA (SF) LOCATION LEASE / SALE

Flipkart Embassy Tech Village 3,500,000 Outer Ring Road Lease

KPMG RMZ Eco World 800,000 Outer Ring Road Lease

Volvo India Pvt. Ltd. RMZ Eco World 800,000 Outer Ring Road Sale

L&T RMZ Eco World 500,000 Outer Ring Road Lease

WIPRO Divyasree Technopark 500,000 Whitefield Lease

BUILDING NAME DEVELOPER AREA (SF) LOCATION POSSESSION

Maple Tree - 1 Phase Adamas Builder 900,000 Outer Ring Road 2015

Bagmane Constellation Business Park - Virgo Block Bagmane Developers 800,000 Outer Ring Road 2015

RGA Tech Park Primal Realty 800,000 Sarjapur Road 2015

Average Rental And Capital Value Trend

8,000

10,000

12,000

6,000

4,000

2,000

0

70

60

50

40

30

10

20

0

Notes:

1. Office Market: Prime office properties in Bengaluru can be divided into three principal sub-market-CBD/Off CBD (MG Road, Millers Road, Vittal Mallya Road etc.) the SBD

(Banerghatta Road & Outer Ring Road (ORR)) and PBD (Hosur Road, EPIP Zone, Electronic City and Whitefield).

2. Rents/Capital Value: Market average of indicative asking price for Grade A office space.

3. Available Supply: Total Grade A office space being marketed for sale or lease in surveyed quarter.

4. City Barometer: Represents increase, decrease or stable scenario; as compared to previous quarter.

5. All the figures in the report is based on market information as on 25th December 2014.

Forecast

New Supply, Absorption And Vacancy Trends20 20%

15%

10%

5%

0%

15

10

5

02010 2011 2012 2013 2014 2015F 2016F

New Supply (In Mln sqft) Absorption(In Mln sqft) Vacancy(In %)

2008

2009

2010

2011

2012

2013

2014

2015

2016

Rent

al V

alue

s IN

R Pe

r sq

ft P

er M

onth

Capi

tal V

alue

s IN

R Pe

r sq

ft

About Colliers International

colliers.com

63 countries on 6 continentsUnited States: 146 Canada: 44 Latin America: 25

186 EMEA: 84

$2.1billion in annual revenue

1.46billion square feet under management

15,800professionals

Primary Authors:

Surabhi Arora Associate Director | Research +91 124 456 [email protected]

Sachin Sharma Assistant Manager | Research

Amit Oberoi I National DirectorValuation & Advisory Services & Research

For O�ce Services:

Joe Verghese Managing Director | India [email protected]

Goutam Chakraborty Director | O�ce Services [email protected]

Colliers InternationalPrestige Garnet, Level 2, Unit No. 201/202 36 Ulsoor Road, Bangalore - 560042 | India

485