Bank of Kigali Investor Presentation Full Year 2014 of... · Bank of Kigali Investor Presentation...

47

Bank of Kigali Investor Presentation Page 1 Bank of Kigali Investor Presentation Full Year 2014

Transcript of Bank of Kigali Investor Presentation Full Year 2014 of... · Bank of Kigali Investor Presentation...

Bank of Kigali Investor Presentation Page 1

Bank of Kigali Investor Presentation

Full Year 2014

Bank of Kigali Investor Presentation Page 2

Disclaimer This presentation contains statements that constitute “forward-looking statements”, including, but not limited to, statements relating to the implementation of strategic initiatives and other statements relating to our business development and financial performance. While these forward-looking statements represent our judgments and future expectations concerning the development of our business, a number of risks, uncertainties and other factors could cause actual developments and results to differ materially from our expectations. These factors include, but are not limited to, (1) general market, macroeconomic, government policies, legislative and regulatory trends, (2) movements in local and international currency exchange rates, interest rates and securities markets, (3) competitive pressures, (4) technological developments, (5) changes in the financial position or credit worthiness of our customers, obligors and counterparties and developments in the markets in which they operate, (6) management changes and changes to the Bank’s structure and (7) other key factors that we have indicated could adversely affect our business and financial performance, which are contained elsewhere in this presentation and in our past and future filings and reports, including those filed with the National Bank of Rwanda and the Rwanda Stock Exchange. We are under no obligation (and expressly disclaim any such obligations to) update or alter our forward-looking statements whether as a result of new information, future events, or otherwise.

Bank of Kigali Investor Presentation Page 3

Key Executives

J a m e s G a t e r a C h i e f E x e c u t i v e O f f i c e r E m a i l : j g a t e r a @ b k . r w T e l : + 2 5 0 2 5 2 5 9 3 1 2 1

L a w s o n N a i b o C h i e f O p e r a t i n g O f f i c e r E m a i l : l n a i b o @ b k . r w M o b i l e : + 2 5 0 7 8 8 3 0 2 0 7 6

L a d o G u r g e n i d z e C h a i r m a n o f t h e B o a r d E m a i l : l g u r g e n i d z e @ b k . r w M o b i l e : + 9 9 5 5 9 9 4 7 7 2 7 2 S k y p e : l a d o . g u r g e n i d z e . 2 0 0 8

N a t h a l i e M p a k a A g . C h i e f F i n a n c e O f f i c e r E m a i l : n m p a k a @ b k . r w M o b i l e : + 2 5 0 7 8 8 3 8 0 8 0 4

Bank of Kigali Investor Presentation Page 4

Agenda

1. Key Investment Highlights

2. Country Overview Information

3. Banking Sector Overview

4. Bank Overview

5. Corporate Governance

6. Business Overview

7. Review of Financial Performance in YE 2014 & 2013

8. Strategic Outlook

9. Contact Information

Bank of Kigali Investor Presentation Page 5

Sound Macro Fundamentals

Politically stable country with sound governance

Very attractive demographic profile: population of 10.5 million with 83% below the age of 40

Robust economic growth of an average of 8% pa with aim of reaching 11.5% by 2018

Moderate inflation: Inflation rate of 2.1% as at December 2014

The 2014 World Bank Doing Business Report ranked Rwanda as the 32nd out of 189 countries in terms of ease of doing business and 3rd in Africa. It was also named the most improved economy worldwide since 2005.

Significant headroom for growth given low banking penetration

Total assets/GDP of 31%

Large unbanked population of approximately 77%

Well regulated banking sector: fairly conservative regulator relative to other regulators in the EAC

Market leadership by

Total assets (RwF 482.6 billion - YE 2014) – 33.7% market share

Net Loans (RwF 233.4 billion – YE 2014) – 30.7% market share

Customer Deposits (RwF 324.6 billion – YE 2014) –31.0% market share

Shareholders’ Equity (RwF 89.5 billion –YE2014) –41.6% market share

Relatively high capital adequacy ratios ranging from 18.7% - 25.8% between 2010 and 2014

Manageable level of non-performing loans – 6.6% of gross loans in 2014, down from 19.4% in 2007

Net loans to customer deposits ratio of 71.9% in 2014.

High liquid asset holding of 64.9% (minimum requirement 20%)

Significant Banking Sector

Potential

Market Leadership

Conservative Business Model

Experienced

Management

Team

Management team with significant banking sector experience

Complemented by an experienced and diversified Board of Directors

Track record of producing stellar results

Profitable

Growth

Robust asset growth at a CAGR of 24.9% (2010-2014) – 482.6 billion as at 31 December 2014

ROAA ranging from 3.5% - 4.0% between 2010 and 2014

Key Investment Highlights

3. Bank of the Year 2009-2012,2014

4. Best Bank in Rwanda 2009-2014

7. AA-/A1 Credit Rating

The rating reflects the Bank’s established domestic franchise value, strong capital position, its systemic importance, strong asset quality and financial performance.

2. Best East African Bank 2012 & 2014

5. Best African Listing 2011

6. Best Financial Reporting Company Rwanda 2012 & 2014

1. Best Bank in Rwanda 2013 &2014

Bank of Kigali Investor Presentation Page 6

COUNTRY OVERVIEW INFORMATION

Bank of Kigali Investor Presentation Page 7

7

Rwanda – Country Profile

Real GDP Growth Rate 2013 4.6%

Real GDP Growth Rate 2014E 6%

Inflation Rate (Dec 2014) 2.1%

Private Sector Credit Growth(2014) 19.6%

Current-account deficit as a % of GDP-2014E 9.5%

External Debt to GDP 29%

Currency Depreciation against USD (Dec 2014) 3.6%

FDI as % of GDP 2.2%

Official Reserves 4.6 months’ imports

Ranked second only to Mauritius as the best destination to do business in

Africa in the World Bank 2014 Doing Business Report.

Since 2005, Rwanda has implemented over 22 business regulation

reforms in the areas measured by the World Bank Doing Business Index.

Today, entrepreneurs can register a new business online in 6 hours

Ranked first in Africa in the 2014 World Bank Country Policy and

Institutional Assessment (CPIA) report. The report shows that Rwanda’s

economic management and structural policies as the most improved in

sub-Saharan Africa. Rwanda was also named the most competitive

economy in East Africa and third in Africa by Global Competitiveness

Index Report 2014

Source: IMF, CIA World Factbook, World Bank, Ministry of Finance and Economic Planning, National Institute of

Statistics of Rwanda and National Bank of Rwanda,

Business Environment

Macro Economic Indicators

National Facts

Area 26,338 sq km

Population 10.5 million

Official Languages Kinyarwanda, French, English

Capital Kigali

Currency Rwandan Franc (RwF)

Credit Rating ‘B +‘ (Fitch Ratings) B/Stable (Standard & Poors)

Nominal GDP (2014E ) US$ 7.6 billion

Nominal GDP Per Capita (2013 ) US$ 693

Bank of Kigali Investor Presentation Page 8

GDP per Capita continues to grow

Healthy GDP growth with moderating inflation

Population Pyramid for Rwanda

Sound Macro Fundamentals

Source: National Institute of Statistics of Rwanda Source: Ministry of Finance and Economic Planning, World Bank

54% of the population is under 19 years.

83% of the population is under 40 years.

3% of the population over 65 years.

Bank of Kigali Investor Presentation Page 9

GDP Breakdown By Economic Activity 9M 2014

Current Account Deficit as a % of GDP Trade Deficit as a % of GDP

Macroeconomic Indicators

Source: NBR Monetary Policy Statement

Source: Ministry of Finance and Economic Planning Projections

Rwanda’s exports are dominated by coffee, tea and minerals

(tin, coltan and wolfram).

The country remains a net importer. Major imports include

fuel and oils, intermediary goods especially construction

materials, consumer goods, and capital goods.

Informal cross-border trade is a significant component of

Rwandan external trade (approx. 17.8% of formal exports).

75% of these exports are destined to DRC

Official reserves were estimated at 4.6 months of goods

imports as of Dec 2014

Source: National Institute of Statistics of Rwanda

Source: National Institute of Statistics of Rwanda

Trade Structure

Bank of Kigali Investor Presentation Page 10

Macro Economic Review

Review of the Macro Economic Environment

GDP in Q3 2014 was 7.8 percent higher in real terms higher than

6.1% and 7.5% achieved in Q2 and Q1 of 2014 respectively.

The Services sector contributed 47 percent of GDP while the

Agriculture sector contributed 34 percent. The Industry sector

contributed 14 percent and 5 percent was attributed to

adjustment for taxes less subsidies on products.

Traditional exports composed of tea, coffee, pyrethrum, hides

and skins as well as minerals accounted for 55.2% of the total

export earnings compared to 72.6% recorded for 2010 ,

followed by re-exports (27.6%)and non- traditional exports

(17.2%). The structural change in export was mainly due to

increase in re-exported petroleum products, rice, sugar and fats.

On average, headline inflation decelerated from 4.0% in Jan

2014 to 2.1% in Dec 2014. In 2014, inflationary pressures from

many components reduced and the main driver of the

developments in inflation was food, housing, transport,

education, restaurants and hotels.

Trade deficit widened by 7.5% from USD 1674.38 million in

2013 to USD 1,799.54 million in Dec 2014.

Inflationary Environment 2014

Exchange Rate Developments 2014

Source: National Institute of Statistics of Rwanda, NBR Monetary Policy & Research Department

Bank of Kigali Investor Presentation Page 11

BANKING SECTOR OVERVIEW

Bank of Kigali Investor Presentation Page 12

2013 Banking Assets/GDP Large Unbanked Population

Economy is moving away from being cash based through the

various financial inclusion initiatives being undertaken by financial

institutions including the launch of agency banking and mobile

money transfer services

Approximately 72% of the population have or use financial

products or mechanisms including those offered by non- bank

formal financial institutions such as SACCOs

(1) Source: EY Eastern Africa 2013 Banking Sector Review & World Bank data (2) Source: EY Eastern Africa 2013 Banking Sector Review & World Bank data (3) Source: African Alliance YE 2013 Uganda Banking Sector Analysis & World Bank data (4) Source: National Bank of Rwanda YE 2013 Monetary Policy Statement (5) Source: Population stats by World Bank

2013 Banking Assets Per Capita5

Significant Banking Sector Potential

(US$)

Source: Finscope Rwanda 2012

Prudential Regulations

31%

31%

36%

71%

Rwanda

Uganda

Tanzania

Kenya

214

178

244

705

Rwanda

Uganda

Tanzania

Kenya

Bank of Kigali Investor Presentation Page 13

Banking Sector Overview

Rwanda Banking System Total Assets

Banking Sector Review Recent Regulatory Reforms To Improve Access To Credit

Enactment of Law on Mortgages, requiring the registration of mortgages

and enabling lenders to foreclose on defaulters

Establishment of Commercial Courts dealing solely with commercial

disputes

Reorganization of the Land Centre which has computerised records and

operations in addition to timely issuance of property titles

Reorganization of the Office of the Registrar General to enhance and fast

track registration of mortgages and foreclosures

Establishment of Credit Reference Bureau to enhance information sharing

among banks and other financial institutions in order to assist with credit

risk assessment

Interest Rate Analysis

As at end of YE 2014 , total CAR stood at 24.2% (YE 2013: 23.1%) well

above the regulatory minimum of 15%. The sector’s liquidity position

stood at 51.7% (YE 2013: 49.5%).

The industry balance sheet measured by total assets grew by 19.3% from

RwF 1,510.7 billion in December 2013 to RwF 1,800 billion at the end of

2014.

The quality of assets improved significantly as the Non-performing loans

(NPLs) to total gross loans reduced to 6.0% as at YE 2014 (YE 2013: 7.0%).

Source: NBR Monetary Policy Statement for the year ended 31 December 2014

Source: NBR Monetary Policy Statement for year ended 31 December 2014

Bank of Kigali Investor Presentation Page 14

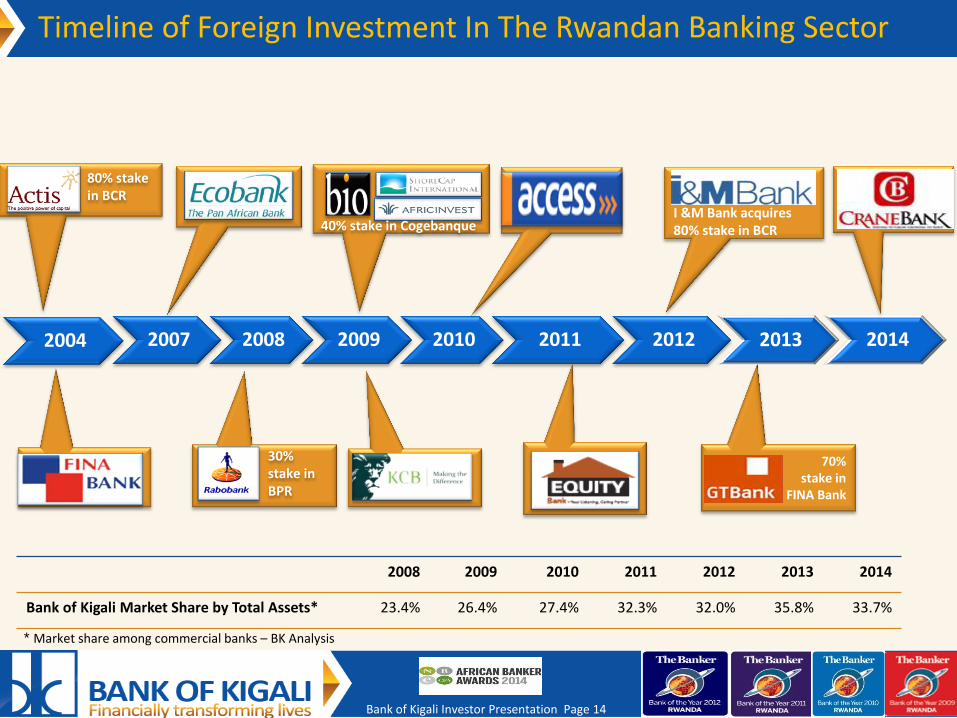

Timeline of Foreign Investment In The Rwandan Banking Sector

2004 2007 2008 2009 2010 2011 2012 2014

30% stake in BPR

80% stake in BCR

40% stake in Cogebanque I &M Bank acquires 80% stake in BCR

70% stake in

FINA Bank

* Market share among commercial banks – BK Analysis

2008 2009 2010 2011 2012 2013 2014

Bank of Kigali Market Share by Total Assets* 23.4% 26.4% 27.4% 32.3% 32.0% 35.8% 33.7%

Bank of Kigali Investor Presentation Page 15

Banking Sector Overview Cont’d

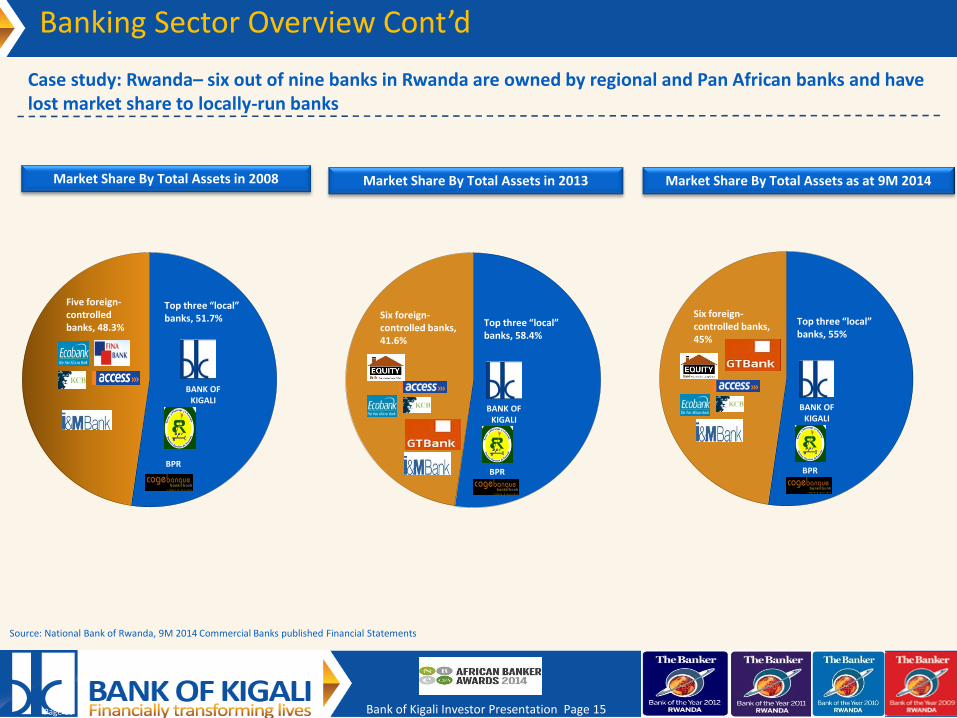

Case study: Rwanda– six out of nine banks in Rwanda are owned by regional and Pan African banks and have lost market share to locally-run banks

Market Share By Total Assets in 2008

Page 15

Source: National Bank of Rwanda, 9M 2014 Commercial Banks published Financial Statements

Market Share By Total Assets in 2013

BANK OF KIGALI

Top three “local” banks, 51.7%

Five foreign-controlled banks, 48.3%

Market Share By Total Assets as at 9M 2014

BANK OF KIGALI

BPR

Top three “local” banks, 55%

Six foreign-controlled banks, 45%

BPR

BANK OF KIGALI

BPR

Top three “local” banks, 58.4%

Six foreign-controlled banks, 41.6%

Bank of Kigali Investor Presentation Page 16

Competitive Landscape

Market Share Dynamics

Concentration of Banking Sector Assets Selected Indicators 2014

Source: NBR Supervision Department, BK Company Filings and published financials statements of Banks

Bank of Kigali Growth vs. Commercial Banks’ Growth, CAGR YE 2010 – YE 2014

Source: 9M 2014 Published Financial Statements Source: NBR Monetary Policy Statement , BK YE 2014 Published Financial Statements

YE 2013

Top 5 Banks, 78.5%

Others, 21.5%

Top 5 Banks, 75.7%

Others, 24.3%

9M 2014

Bank of Kigali Investor Presentation Page 17

Strong Market Leadership

Source: 9M 2014 published financial statements for commercial banks

Rank Total Assets Net Loans Customer Deposits Equity

33.9%

BANK OF KIGALI

BPR

11.4%

ECOBANK

10.4%

I & M Bank

10.2%

COGEBANQUE

9.8%

GT BANK

6.3%

KCB

7.9%

ACCESS BANK

6.3%

1

2

3

4

5

6

7

8

30.8%

BANK OF KIGALI

30.8%

BANK OF KIGALI

45.1%

BANK OF KIGALI

BPR

13.8%

BPR

11.7%

BPR

10.9%

8.2%

ECOBANK

11.6%

I & M Bank

11.0%

COGEBANQUE

10.2%

ACCESS BANK

5.5%

GT BANK

8.5%

ACCESS BANK

6.5%

COGEBANQUE

9.2%

9.0%

KCB

6.8%

COGEBANQUE

6.6%

GT BANK

5.6%

KCB

7.0%

ACCESS BANK

4.8%

KCB

6.0%

9

EQUITY BANK EQUITY BANK

EQUITY BANK

EQUITY BANK

4.8% 3.8% 2.6% 4.1%

ECOBANK

11.4%

I & M Bank

10.5%

ECOBANK

7.0%

I & M Bank

GT BANK

Bank of Kigali Investor Presentation Page 18

BANK OVERVIEW

Bank of Kigali Investor Presentation Page 19

Background and History

A+ credit rating by GCR (Global Credit

Rating)

Government of Rwanda acquired 50% stake from

Belgolaise becoming 100% shareholder

2006

Established in 1966 as a JV with

Belgolaise S.A

1966

Current management

team assembled

New strategy focusing on the

universal banking business model and

profitable growth adopted

2009

Supervisory Board enhanced &

internationalized

AFD loan signed: ‒ US$ 20 mln ‒ 10 years

AfDB loan signed:

-US$12 mln -10 years

US$62.5 mln Initial Public

Offering of 45% of its shares and listing on the RSE

2010 2011 2013

Signed lines of credit with: • PTA Bank- US$ 10 mln • OFID- US$ 10 mln • EADB- US $10 mln

Bank of Kigali Investor Presentation Page 20

Key Facts

A Snapshot of Bank of Kigali

The leading bank in Rwanda (33.7% market share by total assets as at 31st

December 2014), offering a wide spectrum of commercial banking services

to corporate, SME and retail customers

As at 31st December 2014 the Bank had:

Over 24,000 corporate clients

Over 266,000 retail clients

70 branches

76 ATMs

1,019 employees

Western Union, Money Gram and Express Money services for International

Transfers

20

Branch Network Evolution

Source: Bank of Kigali Audited Financials 2008-2014 ,NBR Supervision Department data

Growth in ATMs, POS Terminals and # of Retail Current accounts

Bank of Kigali Investor Presentation Page 21

CORPORATE GOVERNANCE

Bank of Kigali Investor Presentation Page 22

Sharehold ing Structure & Corporate Governance

The Board has eight independent non-executive directors

(including two non-resident directors with extensive expertise in

international banking practices)

The Board of Directors is appointed by the shareholders and

approved by the Central Bank and meets on a quarterly basis or

more frequently as the business demands

The Board sets the strategy and retains full responsibility for the

direction and control of the Bank as spelled out in the

Memorandum and Articles of Association, the Board Charter and

the BNR Corporate Governance guidelines

The Board sub-committees have clear TORs which underscore the

scope and context of their mandate and performance as approved

by the Board & the BNR Corporate Governance regulation

The Board receives detailed financial information and regular

presentations from the management on the Bank’s business

performance; this enables the Directors to make informed

decisions on governance, strategic, financials and operational

issues.

Shareholding Structure as at 31st December 2014 Corporate Governance

Free float- 45%

Employees and Directors

2% International Institutional

Investors 16.4%

Local Institutional

Investors 8.4%

Other State Owned Entities

0.1%

Regional Institutional

Investors 6.2%

Retail Investors

12.2%

Rwanda Social Security Board

25.1%

Government of Rwanda

29.6%

Bank of Kigali Investor Presentation Page 23

Share Trading Performance

Share Price Performance since start of trading

31 December 2014 Current price, RwF 300 Market Cap, US$ mln 290 Free float 45% Free float in US$ mln 131.7 Average daily traded volume in US$ mln 0.13 Common shares outstanding, mln shares 671.9 12-month high 365 12-month low 170 P/E 2014 (based on current price) 11.66x P/BV 2014 (based on current price) 2.45x

Dividend yield, 2013 4.6% Dividend yield, 2014 (based on price of RwF 300) 5.4% Ticker Code BOK Bloomberg BOK. RW

Rwf/USD Exchange Rate of 694.374 as at 31st December 2014(BNR)

*Capital gains on RSE transactions are exempted from Capital Gains Tax

Recommendation: BUY Target Price: Rwf 390 Last coverage report: March 2014

Analyst Coverage

Recommendation: HOLD Target Price: Rwf 285 Last coverage report: 1 September 2014

100130160190220250280310340370400

3-J

an-1

31

3-J

an-1

32

3-J

an-1

32

-Fe

b-1

31

2-F

eb

-13

22

-Fe

b-1

34

-Mar

-13

14

-Mar

-13

24

-Mar

-13

3-A

pr-

13

13

-Ap

r-1

32

3-A

pr-

13

3-M

ay-1

31

3-M

ay-1

32

3-M

ay-1

32

-Ju

n-1

31

2-J

un

-13

22

-Ju

n-1

32

-Ju

l-1

31

2-J

ul-

13

22

-Ju

l-1

31

-Au

g-1

31

1-A

ug-

13

21

-Au

g-1

33

1-A

ug-

13

10

-Se

p-1

32

0-S

ep

-13

30

-Se

p-1

31

0-O

ct-1

32

0-O

ct-1

33

0-O

ct-1

39

-No

v-1

31

9-N

ov-

13

29

-No

v-1

39

-Dec

-13

19

-Dec

-13

29

-Dec

-13

8-J

an-1

41

8-J

an-1

42

8-J

an-1

47

-Fe

b-1

41

7-F

eb

-14

27

-Fe

b-1

49

-Mar

-14

19

-Mar

-14

29

-Mar

-14

8-A

pr-

14

18

-Ap

r-1

42

8-A

pr-

14

8-M

ay-1

41

8-M

ay-1

42

8-M

ay-1

47

-Ju

n-1

41

7-J

un

-14

27

-Ju

n-1

47

-Ju

l-1

41

7-J

ul-

14

27

-Ju

l-1

46

-Au

g-1

41

6-A

ug-

14

26

-Au

g-1

45

-Se

p-1

41

5-S

ep

-14

25

-Se

p-1

45

-Oct

-14

15

-Oct

-14

25

-Oct

-14

4-N

ov-

14

14

-No

v-1

42

4-N

ov-

14

4-D

ec-1

41

4-D

ec-1

42

4-D

ec-1

4

Price Closing Price Rwf Volume Weighted Average Price Rwf Initial Price Rwf

Bank of Kigali Investor Presentation Page 24

C u sto d i a l S e r v i c e C h a i n

Standard Chartered Mauritius

State Street Bank

Pictet CIE (Africa)

Chase Manhattan Bank Mutual

Northern Trust Company

HSBC Bank PLC Client Safe Custody

RBC Investor Services Trust

Standard Chartered Ghana, Uganda &

Zambia

Cacies Bank Luxembourg & France

Citigroup Global Markets LTD

CITI Custody Bank

Fidelity Central Invest Port LLC

FirstRand Bank Limited

RMB Multimanager

BNP Paribus

Brown Brothers Harriman

Citibank

Credit Suisse

Deutsche Bank

JP Morgan Chase

Morgan Stanley

UBS

Northern Trust

CFC Stanbic

Altree Financial Services

Kenya Commercial

Bank Rwanda

Bank of Kigali Investor Presentation Page 25

BUSINESS OVERVIEW

Bank of Kigali Investor Presentation Page 26

Gross Loan Portfolio Loan Book Segmentation

Overview of the Loan Book

Corporate Loan Book YE 2014

YE 2013

68.5%

31.5%

Corporate Loans Retail Loans

Over 1 Billion, 37.8%

500M-1 Billion, 12.6%

100M-500 Million, 26.7%

50M-100Million, 7.1%

0-50 million, 15.8%

*TWC- Transport, Warehousing and Communication

Top 10 Corporate

Loan, 27.6%

Other Corporate

Loan, 72.4%

75.9%

24.1%

YE 2014

Bank of Kigali Investor Presentation Page 27

Total Deposits Growth

Structure of Deposits, YE 2014 Customer Deposits Concentration

Customer Deposit Base

* depositors with total balances above 5% of shareholders’ equity

Customer Deposit Segmentation

YE 2013

YE 2013 YE 2014

73.4%

26.6%

Corporate Deposits Retail Deposits

29.2%

70.8%

Corporate: RwF 185.9Bn Retail: RwF 73.4Bn

71.1%

28.9%

YE 2014

35.4%

64.6%

Large Depositors Other

86.1%

1.3%

12.6%

CB Demand DepositsCB Collateral DepositsCB Term Deposits

11.0% 5.2%

83.8%

Term Deposits

Savings Deposits

Demand Deposits

Bank of Kigali Investor Presentation Page 28

Description Key Segments as at YE 2014

Number of Corporate Accounts

Clients include corporate, SMEs and NBAs*

Interest rates are in the 16-18.5% range. Key

products:

CAPEX loans: long-term loans for investment or

expansion of the business

Commercial mortgage loans: typical customer

participation at 30% of property value, typical

tenor of up to 10 years

Working capital loans: financing business needs

to an agreed limit for a short period (usually

<1yr)

Overdrafts

Strategy

Introduce new services, integrate client

coverage

Grow and consolidate market share

Leverage superior lending capacity

Focus on payroll services

*NBAs (Non Business Associations) includes Non-Profit

Organizations, Charities, Religious institutions, Educational

Institutions, Cooperatives, etc.

Corporate Banking

Merez Petroleum

Tolirwa

Corporate Loans: RwF 187.7Bn Corporate Deposits: RwF 185.9Bn

71.6%

25.0%

3.4%

Corporate SMEs NBAs

86.1%

1.3%

12.6%

CB Demand Deposits CB Collateral DepositsCB Term Deposits

Bank of Kigali Investor Presentation Page 29

Executing The Retail Strategy

Bank of Kigali Investor Presentation Page 30

Description Retail Lending

Number of Retail Accounts

Retail Banking

Source: Bank of Kigali

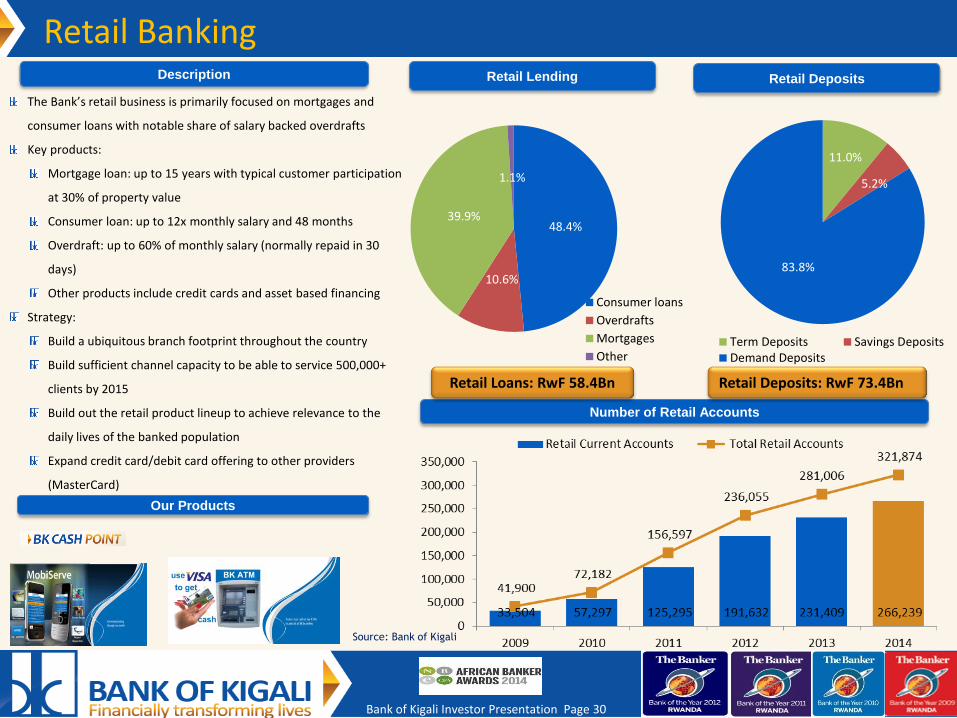

The Bank’s retail business is primarily focused on mortgages and

consumer loans with notable share of salary backed overdrafts

Key products:

Mortgage loan: up to 15 years with typical customer participation

at 30% of property value

Consumer loan: up to 12x monthly salary and 48 months

Overdraft: up to 60% of monthly salary (normally repaid in 30

days)

Other products include credit cards and asset based financing

Strategy:

Build a ubiquitous branch footprint throughout the country

Build sufficient channel capacity to be able to service 500,000+

clients by 2015

Build out the retail product lineup to achieve relevance to the

daily lives of the banked population

Expand credit card/debit card offering to other providers

(MasterCard)

x etc) Our Products

Retail Deposits

Retail Loans: RwF 58.4Bn Retail Deposits: RwF 73.4Bn

11.0%

5.2%

83.8%

Term Deposits Savings DepositsDemand Deposits

48.4%

10.6%

39.9%

1.1%

Consumer loans

Overdrafts

Mortgages

Other

Bank of Kigali Investor Presentation Page 31

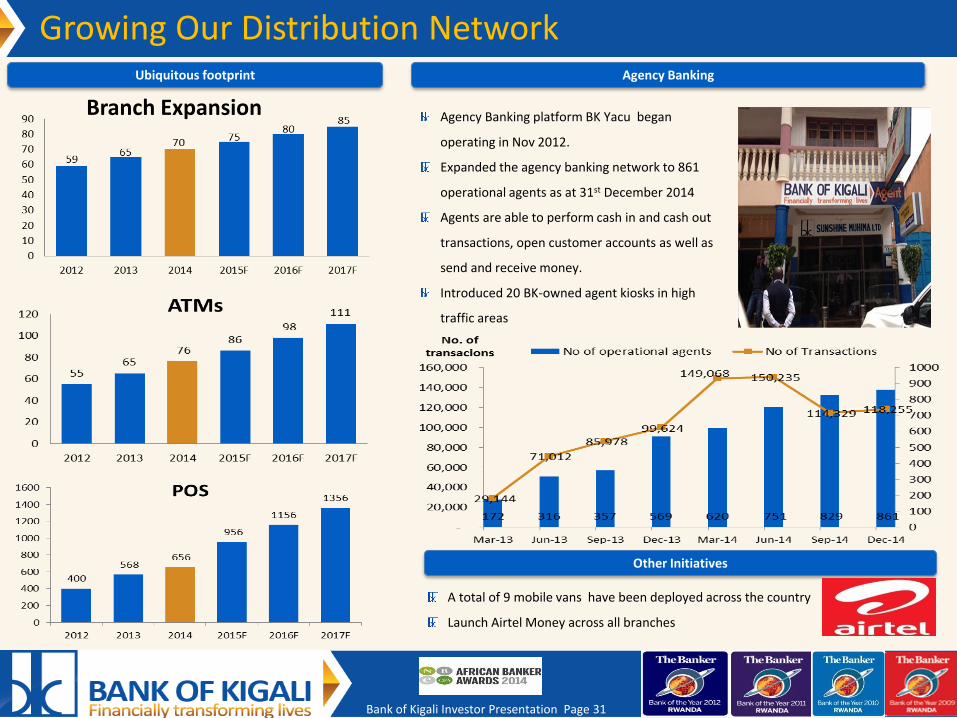

Ubiquitous footprint Agency Banking

Growing Our Distribution Network

Agency Banking platform BK Yacu began

operating in Nov 2012.

Expanded the agency banking network to 861

operational agents as at 31st December 2014

Agents are able to perform cash in and cash out

transactions, open customer accounts as well as

send and receive money.

Introduced 20 BK-owned agent kiosks in high

traffic areas

Other Initiatives

A total of 9 mobile vans have been deployed across the country

Launch Airtel Money across all branches

Branch Expansion

Bank of Kigali Investor Presentation Page 32

Growing our Card Business Increasing our Mobile Product Offering

Expanding Our Self Service Products

Key Achievements

Launch of Visa Classic and Visa Gold Credit

Cards

Over 166,000 Visa Electron debit cards

currently in circulation

Union Pay and Diners Club Card Acquiring

Deposit-taking ATMs

Signing of E-commerce contract with Iveri

2015 Targets

Issuing of MasterCard for the mass market

and HNW clients

Mass roll out of credit cards to the retail

segment -10,000 new credit cards by YE 2015

Master card Issuing and Acquiring

Launch of E-commerce platform

Enhancing our mobile banking service

Our mobile banking service Mobiserve allows customers

to perform the following transactions:

Send money to any mobile phone user

regardless of whether they operate a bank

account or not

Purchasing prepaid TV, airtime and electricity

Check Balances and Bank information

Order cheque books

230,636 Mobiserve users as of 31st December 2014.

Bank of Kigali Investor Presentation Page 33

REVIEW OF F INANCIAL PERFORMANCE IN YE 2014

Bank of Kigali Investor Presentation Page 34

Balance Sheet Highlights Total Assets Customer Deposits

Shareholder’s Equity Net Loans

Bank of Kigali Investor Presentation Page 35

Maturity Profile Loans

Customer Deposits

Bank of Kigali Investor Presentation Page 36

Cost of Risk**, %

Asset Quality

Notes: ** LLP charge / Average gross loans for period

Manageable NPL Ratio

Improving Coverage Ratio

NPLs by segment

YE 2013

Corporate NPLs, 57.8%

Retail NPLs, 42.2%

Corporate NPLs, 62.8%

Retail NPLs, 37.2%

Corporate NPLs

Retail NPLs

YE 2014

Bank of Kigali Investor Presentation Page 37

Asset Quality Gross loan Yield by Segment

Cost of Risk by Segment

2.1%

8.5%

4.4%

2.3% 2.5% 2.8%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

2012 2013 YE - 2014

Retail Corporate

17.4%

19.9% 20.8%

16.5%

20.8% 20.4%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

2012 2013 YE 2014

Retail Corporate

Bank of Kigali Investor Presentation Page 38

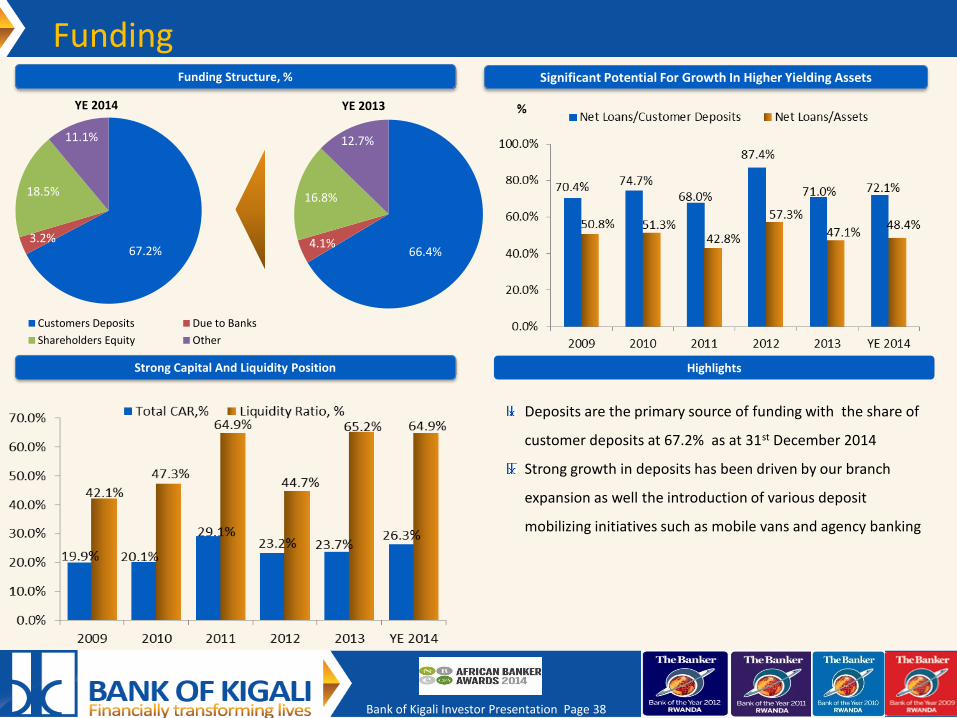

Funding Structure, % Significant Potential For Growth In Higher Yielding Assets

Strong Capital And Liquidity Position Highlights

Deposits are the primary source of funding with the share of

customer deposits at 67.2% as at 31st December 2014

Strong growth in deposits has been driven by our branch

expansion as well the introduction of various deposit

mobilizing initiatives such as mobile vans and agency banking

Funding

YE 2013 YE 2014

66.4% 4.1%

16.8%

12.7%

67.2% 3.2%

18.5%

11.1%

Customers Deposits Due to Banks

Shareholders Equity Other

Bank of Kigali Investor Presentation Page 39

YE 2014 Performance Highlights Net Interest Income Net Non-Interest Income Total Operating Income

Total Recurring Operating Costs Profit Before Provisions Net Income

ROAA 4.0%

ROAE 22.9%

Bank of Kigali Investor Presentation Page 40

2013 Performance Highlights

Net Interest Income Net Non-Interest Income Total Operating Income

Total Recurring Operating Costs Profit Before Provisions Net Income

ROAA 4.0%

ROAE 22.1%

Bank of Kigali Investor Presentation Page 41

Total Operating Income Composition of Total Operating Income

Total Recurring Operating Costs Composition of Total Operating Expenses

Income Statement Highlights

YE 2013

YE 2013

YE 2014

65.5% 18.0%

13.9% 2.6%

YE 2014

45.1%

17.8%

37.1%

Personnel expenses Depreciation and amortization Other operating expenses

37.0%

13.2%

49.8%

67.2% 18.1%

13.3% 1.4%

Net interest income

Fees & Commissions

FX related income

Other non- interest income

Bank of Kigali Investor Presentation Page 42

YE 2014

Fees & Commission Income

YE 2013

Commissions on operations of accounts

25%

Commissions on payment facility

30%

Commission on loans services

20%

Commissions received from financing commitments

6%

Commissions from transactions with other

banks 13%

Other fees from services 6%

Commissions on operations of

accounts 22%

Commissions on payment facility

25% Commission on loans services

26%

Commissions received from financing commitments

4%

Commissions from transactions with

other banks 12%

Other fees from services

11%

Bank of Kigali Investor Presentation Page 43

Sustainable Net Interest Margin % Attractive Cost/Income ratio

Stable Returns To Shareholders % Strong Return on Average Assets %

Consistent Profitable Growth

Source: Bank of Kigali Audited 2009-2013 IFRS Statements and YE 2014 published financial statements

Bank of Kigali Investor Presentation Page 44

STRATEGIC OUTLOOK

Bank of Kigali Investor Presentation Page 45

Strategic Outlook Objectives Strategies Action Outcomes

Earnings growth ~22% Return on Average Equity

> 20%

Continuous improvement of risk management policies & procedures

Disciplined capital management, medium term target CAR of 15%-18% and ROAE of 20%+, implying ROAA in the 3.5% range

No profitability sacrifices for the sake of market share gains

Sensible dividend policy as the growth curve flattens out over time

Maintain profitable growth

Customer growth in terms of current

accounts – increase current accounts by

100,000 in 2015

Benefit from first-mover advantage outside the capital city, making it more difficult for the competitors to follow suit Reach out to the unbanked (but bankable) population

Become the bank of choice and convenience for the middle class and youth entering the employment sector Create capacity to service 500,000+ clients

Increase the number of ATMs, POS terminals and cards outstanding Build a modern and scalable mobile banking and Internet banking platforms Alternative client acquisition & service channels (retail chains, co-branded cards, utilities, etc)

Expand the branch network to 75+ branches by YE 2015

“Grow with clients” Valuable source of retail clients through payroll programs Growth of loan book and F&C income

Maximize the product-to-client ratio

Expand retail product offering

Build sufficient channel capacity

Build a ubiquitous branch footprint throughout the country

Flexible, offset, variable-rate, etc. mortgages Full range of consumer loan products Revolving credit cards Payroll & pension-backed loans & overdrafts Modern, multi-currency current accounts with debit cards Ubiquity of ATMs and POS terminals in urban centers and reasonable proximity elsewhere Payment & e-wallet solutions Full range of deposit products

Healthy structure & growth of balance sheet

>20% growth in 2015

Integrated client coverage Leverage the superior lending capacity Cross-selling opportunities Documentary operations & trade finance, FX, other solutions Rep offices in EAC

Private Banking, Securities, Insurance

Leverage the superior access to wholesale funding to complement the deposit funding base Reduce maturity gap

Enable further expansion of long-term lending

Increase the maturity profile of liabilities

Create a universal banking platform

Consolidate the leading position in corporate banking

Further diversification of revenue streams

Increase retail loans penetration

Increase the loan to asset ratio to 60% Diversification of funding base

Expand the share of higher-margin lending Maximise the cross-sell opportunities Grow the share of retail in the loan book up to 30%-40% in the medium term

Bank of Kigali Investor Presentation Page 46

Management Targets

Branch expansion Return on Average Equity Other Selected Management 2015 targets

52.4% 9M 2013

Growth in net income >20% Y-o-Y

Growth in total assets +20% Y-o-Y

Non funded income ratio : 40% of the total

operating income

Reduce NPL ratio to < 5%

Increase number of retail current accounts by

100,000

Bank of Kigali Investor Presentation Page 47

For further information please contact:

Lado Gurgenidze Chairman of the Board Email: [email protected] Mobile: +995 599 477 272

James Gatera Chief Executive Officer Email: [email protected] Mobile: +250 788 143 000

Josephine Murangira Investor Relations Officer Email: [email protected] Mobile: +250 788 308 064

Lawson Naibo Chief Operating Officer Email: [email protected] Mobile: +250 788 302 076

Visit our website, www.bk.rw to access our Investor Presentations, Press Releases and Annual

Reports.

Telephone number: +250 252 593 100 Address: Plot 6112, Avenue de la Paix, Kigali, Rwanda.

Contact Information

Nathalie Mpaka Ag. Chief Finance Officer Email: [email protected] Mobile: +250 788 380 804

Shivon Byamukama Company Secretary Email: [email protected] Mobile: +250 788 384 547

![PM 2014 investor day 2014-06-26-Operations Investor Day Slides [FINAL]](https://static.fdocuments.in/doc/165x107/577cbc651a28aba7118da314/pm-2014-investor-day-2014-06-26-operations-investor-day-slides-final.jpg)