Investor Day 2014

55

MIC Fixed Income Presentation – March 24, 2014 1 1 Genworth MI Canada Inc.

-

Upload

genworthfinancial -

Category

Business

-

view

488 -

download

5

Transcript of Investor Day 2014

MIC Fixed Income Presentation – March 24, 20141 1Genworth MI Canada Inc.

MIC Fixed Income Presentation – March 24, 20142 2Genworth MI Canada Inc.

> FORWARD-LOOKING AND

NON-IFRS STATEMENTS

This presentation relating to Genworth MI Canada Inc. (the “Company”, “Genworth Canada” or “MIC”) includes certain forward-

looking statements. These forward-looking statements include, but are not limited to, statements with respect to the Company’s

future operating and financial results, expectations regarding premiums written, losses on claims and investment income,

unearned premiums, adjacent opportunities, capital optimization, the Canadian housing market and potential housing prices, and

other statements that are not historical facts. These forward-looking statements may be identified by their use of words such as

“may”, “would”, “could”, “will,” “intend”, “plan”, “anticipate”, “believe”, “seek”, “propose”, “estimate”, “expect”, and similar

expressions. These statements are based on the Company’s current assumptions, including assumptions regarding economic,

global, political, business, competitive, market and regulatory matters. These forward-looking statements are inherently subject to

significant risks, uncertainties and changes in circumstances, many of which are beyond the control of the Company. The

Company’s actual results may differ materially from those expressed or implied by such forward-looking statements, including as a

result of changes in the facts underlying the Company’s assumptions, and the other risks described in the Company’s Annual

Information Form dated March 17, 2014, its Short Form Base Shelf Prospectus dated June 18, 2014, the Prospectus Supplements

thereto and all documents incorporated by reference in such documents. Other than as required by applicable laws, the Company

undertakes no obligation to publicly update or revise any forward-looking statement, whether as a result of new information,

future developments or otherwise.

To supplement its financial statements, the Company uses select non-IFRS financial measures. Non-IFRS financial measures include

net operating income, interest and dividend income (net of investment expenses), operating earnings per common share (basic),

operating earnings per common share (diluted), shareholders’ equity excluding accumulated other comprehensive income

(“AOCI”), operating return on equity and underwriting ratios such as loss ratio, expense ratio and combined ratio. The Company

believes that these non-IFRS financial measures provide meaningful supplemental information regarding its performance and may

be useful to investors because they allow for greater transparency with respect to key metrics used by management in its financial

and operational decision making. Non-IFRS measures do not have standardized meanings and are unlikely to be comparable to any

similar measures presented by other companies. These measures are defined in the Company’s glossary, which is posted on the

Company’s website at http://investor.genworthmicanada.ca. A reconciliation from non-IFRS financial measures to the most readily

comparable measures calculated in accordance with IFRS, where applicable can be found in the Company’s most recent

management’s discussion and analysis, which is posted on the Company’s website and is also available at www.sedar.com.

> BRIAN HURLEY, CHAIRMAN AND CEO

SOLID AND SUSTAINABLE BUSINESS

MIC Fixed Income Presentation – March 24, 2014Genworth MI Canada Inc. 4 4Genworth MI Canada Inc.

LARGEST PRIVATE RESIDENTIAL

MORTGAGE INSURER IN CANADA

Since 1995 helped 1.5 million families COAST

TO COAST achieve homeownership.

We support more than 250 Canadian lenders.

MARKET FACTS (as at Sept 30, 2014)

$5.9 billion Total Assets

$3.3 billion Shareholders’ Equity

$3.8 billion Market Capitalization

95 million Shares Outstanding

COMPETITIVE STRENGTHS

Strong

Market

Presence

Long-Standing

Customer

Relationships

Best-in Class

Technology

and Processes

Prudent Risk

Management

Impressive

Long-Term

Track Record

Experienced

and Engaged

Workforce

> WHO WE ARE

MIC Fixed Income Presentation – March 24, 20145 5Genworth MI Canada Inc.

> THE MARKET HAS EVOLVED

SINCE WE ENTERED…

IPO of

Company

Implemented

Influencer

Strategy

Launched Loss

Mitigation

Strategy

Implemented

Lender Service

Agreements

MI Product

Development

Leader

In-House

Valuation

Model

Entered

Market

Master

Policies with

Big 5 BanksOmni Score

Developed

Auto-

Decisioning

Implemented

INSURED 1.5 MILLION HOMEOWNERS

ACROSS CANADA TO DATE

6Genworth MI Canada Inc.Genworth MI Canada Inc.

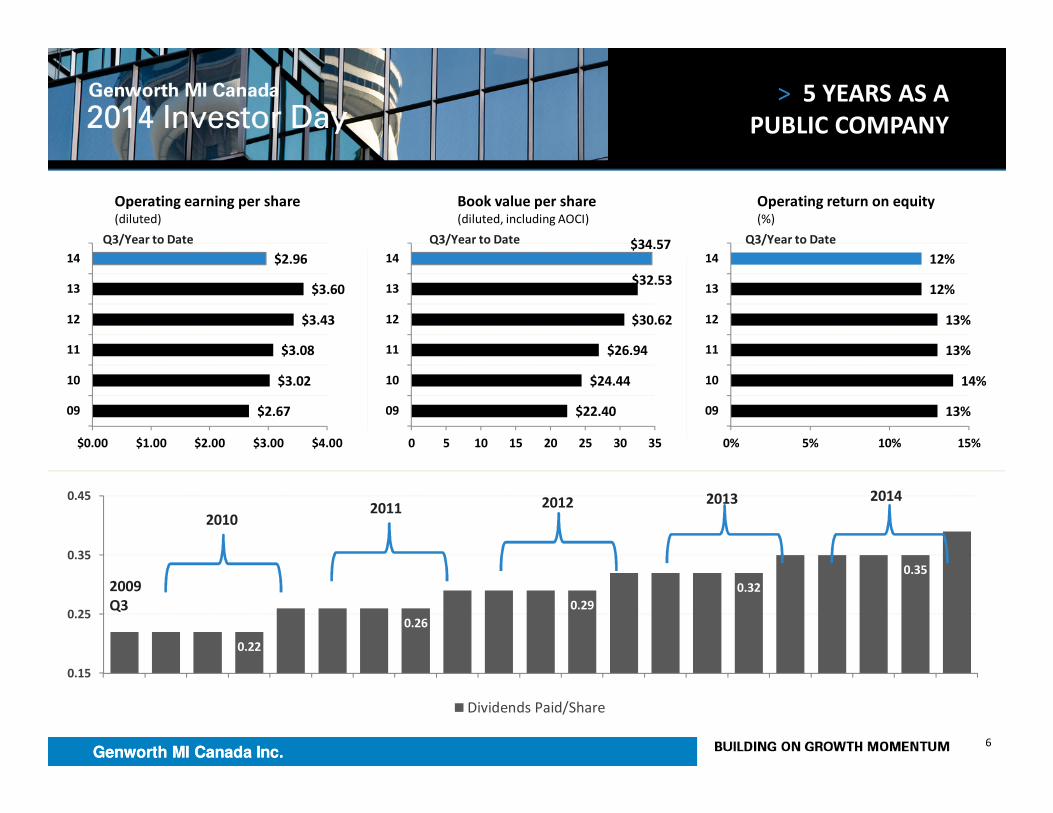

> 5 YEARS AS A

PUBLIC COMPANY

0.22

0.26

0.29

0.32

0.35

0.15

0.25

0.35

0.45

Dividends Paid/Share

20102011 2012 2013 2014

$2.67

$3.02

$3.08

$3.43

$3.60

$2.96

$0.00 $1.00 $2.00 $3.00 $4.00

09

10

11

12

13

14

Operating earning per share(diluted)

$22.40

$24.44

$26.94

$30.62

$32.53

$34.57

0 5 10 15 20 25 30 35

09

10

11

12

13

14

Book value per share(diluted, including AOCI)

13%

14%

13%

13%

12%

12%

0% 5% 10% 15%

09

10

11

12

13

14

Operating return on equity(%)

Q3/Year to Date Q3/Year to Date Q3/Year to Date

2009

Q3

MIC Fixed Income Presentation – March 24, 20147 7Genworth MI Canada Inc.

> AGENDA

Vision for prudent growth

Managing mortgage default risk

Capitalizing on strong capital position

Q&A

Conclusion

TODAY’S AGENDA

> STUART LEVINGS, CHIEF OPERATING OFFICER

VISION FOR PRUDENT GROWTH

9Genworth MI Canada Inc.

> MISSION AND VISION

CANADA’S MORTGAGE INSURER OF CHOICE

Working with our lender partners, regulators and influencers we

› help people responsibly achieve and maintain the dream of

homeownership

› promote strong and sustainable communities across Canada

While enhancing stakeholder value

OUR MISSION

OUR VISION

10Genworth MI Canada Inc.

> GROWTH CATALYSTS

Strong

Market

Presence

Long-Standing

Customer

Relationships

Best-in Class

Technology

and Processes

Prudent Risk

Management

Impressive

Long-Term

Track Record

Experienced

and Engaged

Workforce

COMPETITIVE STRENGTHS

GROWTH CATALYSTS

FOCUS ON PEOPLE, RISK AND TECHNOLOGY

Market Share Market SizePremium

Rates

Adjacent

Opportunities

MIC Fixed Income Presentation – March 24, 201411 11Genworth MI Canada Inc.

> KEY STRATEGIC PRIORITIES

Expand Market Share

Proactive Risk Management

Strong Government Relations

Efficient Capital Structure

Adjacent Opportunities

Employ and Engage Top Talent

Expand Market Share

Proactive Risk Management

Strong Government Relations

Efficient Capital Structure

Adjacent Opportunities

Employ and Engage Top Talent

High Quality, Diversified Portfolio

Operating Income Growth

HOW WE MEASURE SUCCESSHOW WE MEASURE SUCCESS

Market Share Gains

Strong Employee Engagement

STRATEGIC PRIORITIES

MIC Fixed Income Presentation – March 24, 201412 12Genworth MI Canada Inc.

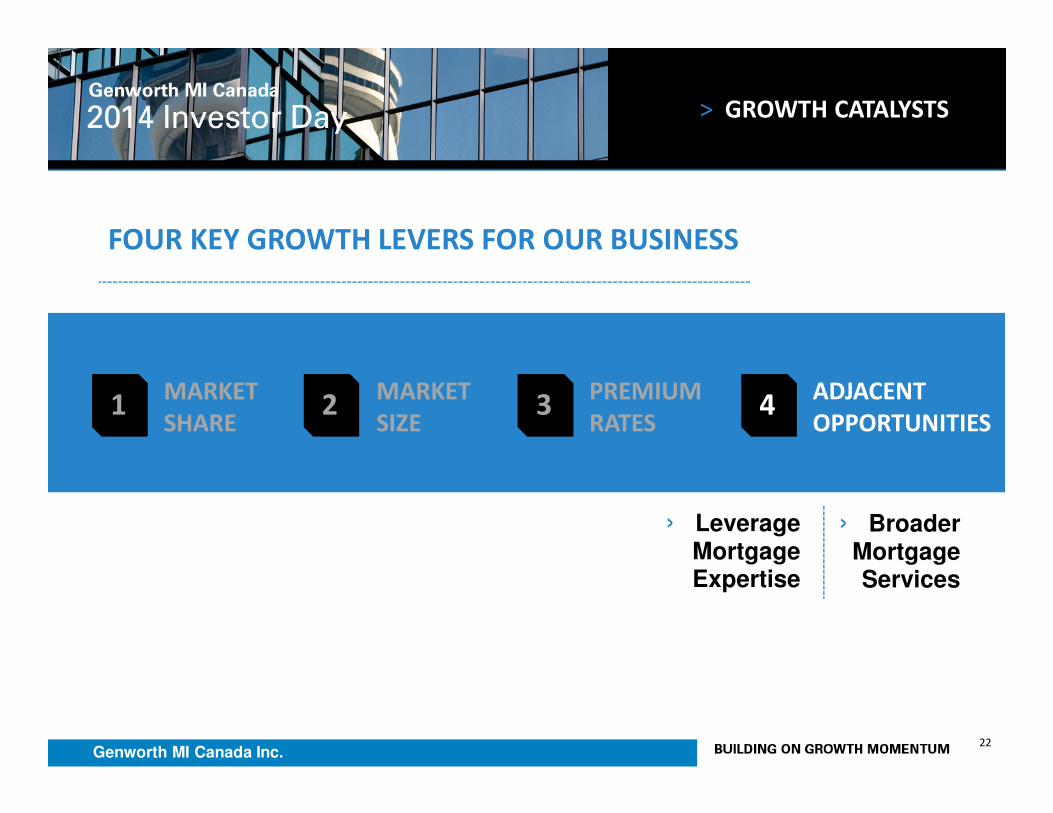

FOUR KEY GROWTH LEVERS FOR OUR BUSINESS

1MARKET

SHARE2 3

MARKET

SIZE

PREMIUM

RATES4

ADJACENT

OPPORTUNITIES

> GROWTH CATALYSTS

MIC Fixed Income Presentation – March 24, 201413 13Genworth MI Canada Inc.

FOUR KEY GROWTH LEVERS FOR OUR BUSINESS

1MARKET

SHARE2 3

MARKET

SIZE

PREMIUM

RATES4

ADJACENT

OPPORTUNITIES

› Enhance Customer Experience

› Build on Value Proposition

› Deepen Collaboration

> GROWTH CATALYSTS

14Genworth MI Canada Inc.

96% 97% 96% 96% 97%

09 10 11 12 13

HIGH DEGREE OF LENDER SATISFACTION> Service Innovation

> Deep Relationships

> Customer-Centric Culture

> Customized Experience

> MARKET SHARE

DRIVING VALUE THROUGH CUSTOMIZED SERVICE EXPERIENCE

ENHANCE CUSTOMER EXPERIENCE

15Genworth MI Canada Inc.

> MARKET SHARE

DELIVERING VALUE BEYOND THE MI TRANSACTION

Customer Training and EducationCustomer Training and Education

Mortgage Default ManagementMortgage Default Management

Portfolio InsurancePortfolio Insurance

Sales TechnologySales Technology

Industry InfluencersIndustry Influencers

BUILD VALUE PROPOSITION

MIC Fixed Income Presentation – March 24, 201416 16Genworth MI Canada Inc.

COLLABORATE ON

> Portfolio Reviews

> Regulatory Change

> Product Development

> MARKET SHARE

ADVISING ON

> Market Trends

> Performance Statistics

> Competitive Intelligence

ADDING VALUE THROUGH THOUGHT LEADERSHIP & APPLICATION

DEEPEN OUR COLLABORATION

MIC Fixed Income Presentation – March 24, 201417 17Genworth MI Canada Inc.

THREE STRATEGIC INITIATIVES

> Enhancing the customer experience

> Building on our value proposition

> Deepening our collaboration

6

2

6

5

8

13

Dec'11 Sep'14

TOP 20 LENDER SHARE

<20% 20-30% >30%MIC Market

Share(Company estimates)

> MARKET SHARE

CAPITALIZE ON MARKET MOMENTUM IN 2015

DEMONSTRATED SHARE GAINS

MIC Fixed Income Presentation – March 24, 201418 18Genworth MI Canada Inc.

FOUR KEY GROWTH LEVERS FOR OUR BUSINESS

1MARKET

SHARE2 3

MARKET

SIZE

PREMIUM

RATES4

ADJACENT

OPPORTUNITIES

› High Ratio Penetration

› First-Time Homebuyer

› Private MI Segment

> GROWTH CATALYSTS

MIC Fixed Income Presentation – March 24, 201419 19Genworth MI Canada Inc.

> Growth in prime home-buying age (30-39) outpacing general population growth (1.8% vs. 1.1%)

> Household formation in Canada supported by immigration

> drives ~60% of population growth > new immigrant quota increased to ~285,000

> Homeownership still seen as a vehicle for building wealth in Canada

> MARKET SIZE

DEMOGRAPHICS AND IMMIGRATION FUEL FIRST-TIME BUYER MARKET

FIRST-TIME BUYERS CONTINUE TO SUPPORT THE HIGH RATIO MARKET

MIC Fixed Income Presentation – March 24, 201420 20Genworth MI Canada Inc.

> MARKET SIZE

Broad Value PropositionCustomer Experience

Tools and Technology Deep Collaboration

EXTENSIVE CUSTOMER ENGAGEMENT

STRONG CUSTOMER ENTRENCHMENT

MIC Fixed Income Presentation – March 24, 201421 21Genworth MI Canada Inc.

FOUR KEY GROWTH LEVERS FOR OUR BUSINESS

1MARKET

SHARE2 3

MARKET

SIZE

PREMIUM

RATES4

ADJACENT

OPPORTUNITIES

> GROWTH CATALYSTS

› Increased Capital Levels

› Annual Review

MIC Fixed Income Presentation – March 24, 201422 22Genworth MI Canada Inc.

1MARKET

SHARE2 3

MARKET

SIZE

PREMIUM

RATES4

ADJACENT

OPPORTUNITIES

› Leverage Mortgage Expertise

› Broader Mortgage Services

> GROWTH CATALYSTS

FOUR KEY GROWTH LEVERS FOR OUR BUSINESS

23Genworth MI Canada Inc.

> CONCLUSION

CLEAR STRATEGY FOR PRUDENT GROWTH

Sound Business Model

Customer-Centric Culture

Supportive Regulatory and Economic Environment

Strong Risk Management Culture

> CRAIG SWEENEY, CHIEF RISK OFFICER

MANAGING MORTGAGE DEFAULT RISK

MIC Fixed Income Presentation – March 24, 2014Genworth MI Canada Inc. 25 25

› Regulatory and Economic Environment

› Assessment of Canadian Markets

› Genworth MIC Portfolio Quality

› Emerging Trends

Genworth MI Canada Inc.

> MANAGING

MORTGAGE DEFAULT RISK

MIC Fixed Income Presentation – March 24, 2014Genworth MI Canada Inc. 26 26

QUALITY OF NEW BUSINESS

CONTINUES TO IMPROVE

POLICY ACTIONS REDUCE RISK

Macroprudential Actions

�Purchase LTV Reduced From 100% to 95%

�Refinance LTV Reduced From 95% to 80%

�Investment Properties Reduced From 95% to 80%

�Max Amortization Reduced From 40 to 25 Years

�All Borrowers Must Qualify at 5-year Fixed Rate

�Max Debt Service Ratio’s Lowered

�Minimum FICO 600 Required For MI

Microprudential Actions

�Increased Regulatory Oversight of Private MIs through PRMHIA

�OSFI Assumes Oversight Of CMHC

�New Limits Planned on Gov’t Backed MI For low-LTV

Mortgages

�B20 & B21 Policy Guidelines On Mortgage Lending

Monetary Policy

�Very Accommodative

�Interest Rates Remain Low To Support Economic Recovery

50%

42%

40% 40%

30% 30%

27% 27%

716

720

726 727 727

730732

737

2007 2008 2009 2010 2011 2012 2013 2014 YTD

HLTV as % of Overall Mortgage Originations

Average Credit Score

Source: Genworth data, as at September 30, 2014

> ECONOMIC AND

REGULATORY ENVIRONMENT

Genworth MI Canada Inc.

MIC Fixed Income Presentation – March 24, 2014Genworth MI Canada Inc. 27 27

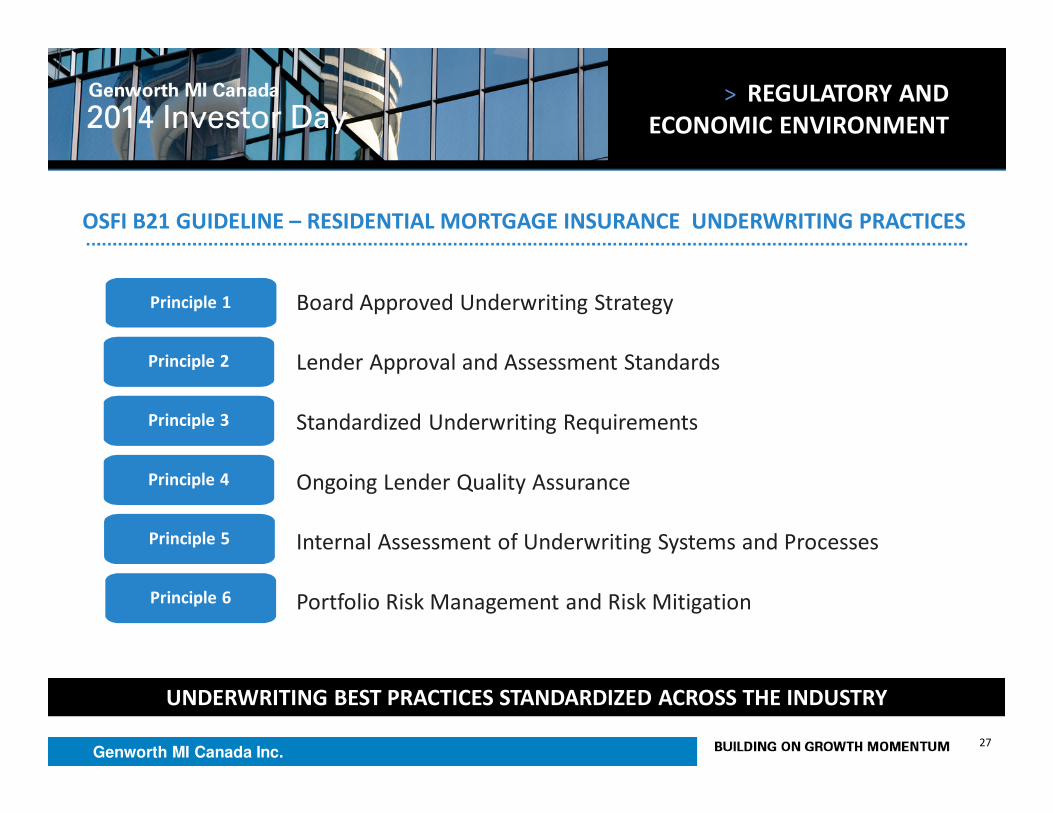

OSFI B21 GUIDELINE – RESIDENTIAL MORTGAGE INSURANCE UNDERWRITING PRACTICES

Principle 2

Principle 3

Principle 4

Principle 1

Principle 5

Principle 6

Board Approved Underwriting Strategy

Lender Approval and Assessment Standards

Standardized Underwriting Requirements

Ongoing Lender Quality Assurance

Internal Assessment of Underwriting Systems and Processes

Portfolio Risk Management and Risk Mitigation

UNDERWRITING BEST PRACTICES STANDARDIZED ACROSS THE INDUSTRY

Genworth MI Canada Inc.

> REGULATORY AND

ECONOMIC ENVIRONMENT

MIC Fixed Income Presentation – March 24, 2014Genworth MI Canada Inc. 28 28

› Solid employment gains supporting

housing market since 2010

› Job growth expected to be positive

over forecast period

› Rising rates in 2015 should keep

price gains modest5.5%

6.0%

6.5%

7.0%

7.5%

8.0%

8.5%

9.0%

0%

10%

20%

30%

40%

50%

60%

National HPI (Teranet) and UE Rate

Cumulative HPI (L) UE Rate (R)

Sources: UE Rate – Statistics Canada, RBC Economics (November 2014 forecast); HPI – Teranet,

Genworth calculations (forecast); data as at September 30, 2014

Forecast

Genworth MI Canada Inc.

STABLE ECONOMIC ENVIRONMENT

> REGULATORY AND

ECONOMIC ENVIRONMENT

MIC Fixed Income Presentation – March 24, 2014Genworth MI Canada Inc. 29 29

Sources: Teranet (HPI), Statistics Canada (UE), CREA (SLR), RBC Economics (Affordability); data as of Q3’14

42

44

46

48

50

52

54

Housing Affordability (Standard 2-Storey)

Good

30%

40%

50%

60%

70%

80%

Supply vs Demand (Sales-to-New-Listings Ratio)

Balanced Market › Housing market remains balanced

› Stable employment supporting

housing demand

› Low interest rates continue to

support affordability

Genworth MI Canada Inc.

STABLE HOUSING MARKET

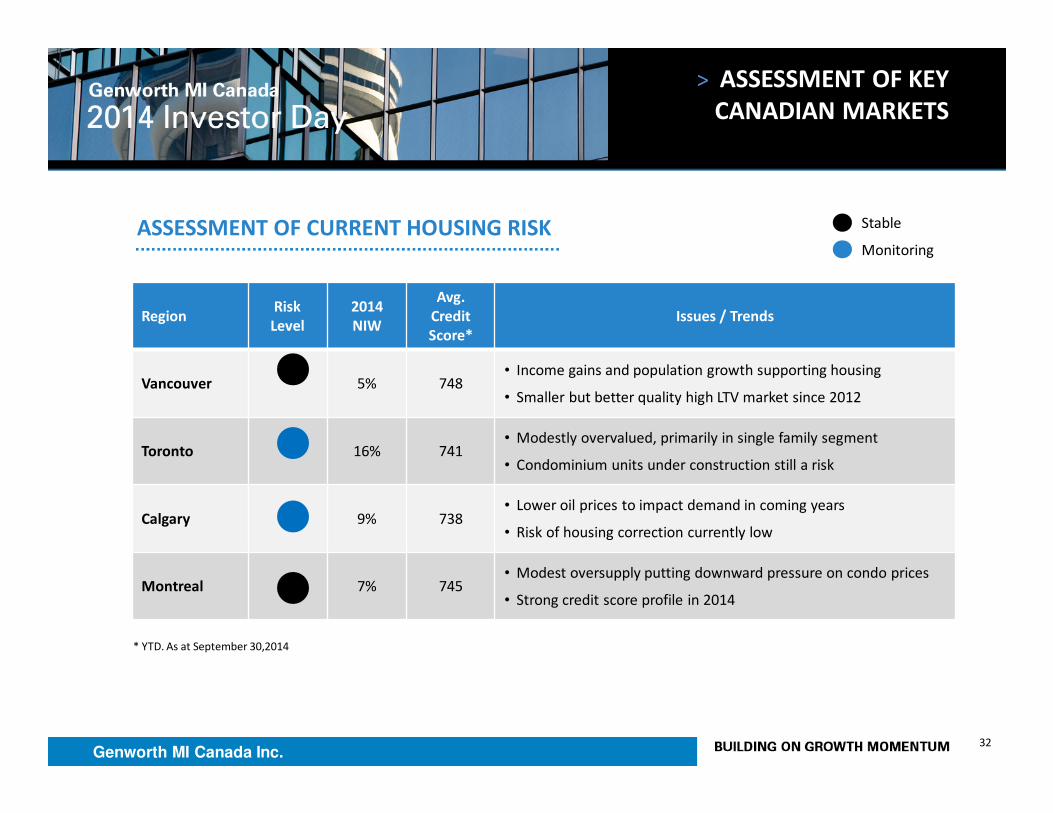

> ASSESSMENT OF KEY

CANADIAN MARKETS

MIC Fixed Income Presentation – March 24, 2014Genworth MI Canada Inc. 30 30

> ASSESSMENT OF KEY

CANADIAN MARKETS

› Stronger growth trend in Ontario

primarily driven by limited supply in

Greater Toronto Area

› Strong employment driving house

price growth in Western provinces

› Softer housing markets in Quebec

and Atlantic regions

HOME PRICES AND SUPPLY

Note: 3-month moving average of the seasonally adjusted year-over-year price change is shown. Months of inventory uses adjusted values.

Sources: Canadian Real Estate Association and Bank of Canada calculations

Genworth MI Canada Inc.

MIC Fixed Income Presentation – March 24, 2014Genworth MI Canada Inc. 31 31

2.0

3.0

4.0

5.0

6.0

7.0

2000 2002 2004 2006 2008 2010 2012 2014

MIC HOUSING RISK MONITOR

Stable

Monitoring

Elevated

ROBUST HOUSING FRAMEWORK TO ASSESS MARKET RISK

> ASSESSMENT OF KEY

CANADIAN MARKETS

Genworth MI Canada Inc.

KEY HOUSING MEASURES

› Supply vs. Demand

› Price-to-income

› Price-to-rent

› House price appreciation

› Affordability

MIC Fixed Income Presentation – March 24, 2014Genworth MI Canada Inc. 32 32

> ASSESSMENT OF KEY

CANADIAN MARKETS

ASSESSMENT OF CURRENT HOUSING RISK

RegionRisk

Level

2014

NIW

Avg.

Credit

Score*

Issues / Trends

Vancouver 5% 748• Income gains and population growth supporting housing

• Smaller but better quality high LTV market since 2012

Toronto 16% 741• Modestly overvalued, primarily in single family segment

• Condominium units under construction still a risk

Calgary 9% 738• Lower oil prices to impact demand in coming years

• Risk of housing correction currently low

Montreal 7% 745• Modest oversupply putting downward pressure on condo prices

• Strong credit score profile in 2014

* YTD. As at September 30,2014

Stable

Monitoring

Genworth MI Canada Inc.

MIC Fixed Income Presentation – March 24, 2014Genworth MI Canada Inc. 33 33

> PORTFOLIO QUALITY

Region Average Home Price Average Income

Average

Gross Debt

Servicing

Genworth Market % Variance Genworth Genworth

Vancouver $449K $814K -45% $107K 28%

Toronto $436K $581K -25% $104K 29%

Calgary $413K $469K -12% $110K 27%

Montreal $280K $342K -18% $87K 25%

Canada $316K $419K -25% $97K 24%

GENWORTH’S AVERAGE HOME PRICE ~25% LOWER THAN MARKET AVERAGE

Note: Q3’14 data; Genworth averages for purchase deals only, market averages from CREA

GENWORTH SERVED MARKET

Genworth MI Canada Inc.

MIC Fixed Income Presentation – March 24, 2014Genworth MI Canada Inc. 34 34

Vancouver Toronto

Detached HomeCondo

High-riseDetached Home

Condo

High-rise

# of borrowers 1.9 1.5 1.8 1.4

Age 39 37 39 37

Credit score 747 751 738 745

Property price $630,000 $347,000 $499,500 $313,000

Income level $129,000 $92,800 $116,000 $90,000

Gross debt service

ratio30% 27% 29% 27%

> PORTFOLIO QUALITY

Note: Based on Genworth data as at September 30, 2014

STRONG BORROWER PROFILE IN MAJOR MARKETS

Genworth MI Canada Inc.

GENWORTH SERVED MARKET

MIC Fixed Income Presentation – March 24, 2014Genworth MI Canada Inc. 35 35

> PORTFOLIO QUALITY

Note: Company data: ~

27%

13%

11%

37%

13%

Alberta Other BC Ontario Quebec

% based on high loan-to-value new insurance written as at 2014 Q3 YTD

9% 8% 6%

18% 17% 15%

74% 75% 79%

0%

20%

40%

60%

80%

100%

2012 2013 2014 YTD

<660 660 - 669 >=700

Genworth MI Canada Inc.

CREDIT SCORE DISPERSION REGIONAL DISPERSION

MIC Fixed Income Presentation – March 24, 2014Genworth MI Canada Inc. 36 36

Key RisksRisk

LevelAssessment / Actions

Rising Interest Rates Affordability› 73% of borrowers YTD choosing 5-yr fixed rate mortgage

› Portfolio well positioned for modest rate increases

Debt levelsDebt-to-income

ratio

› Debt service ratios at historic lows

› Prudent home buying with manageable debt levels

Alberta - Oil pricesLower GDP in

2015-17

› Monitoring provincial economic health

› Enhanced due diligence in economically sensitive areas

> EMERGING TRENDS

Acceptable

MonitoringKEY RISKS

Genworth MI Canada Inc.

MIC Fixed Income Presentation – March 24, 201437 37Genworth MI Canada Inc.

> Positive economic and regulatory environment

> Portfolio quality continues to be strong

> Housing risk limited to isolated pockets

> Proactive response to emerging risks

> CONCLUSIONS

MIC Fixed Income Presentation – March 24, 201438 38Genworth MI Canada Inc.

> PHILIP MAYERS, CHIEF FINANCIAL OFFICER

CAPITALIZING ON STRONG CAPITAL POSITION

MIC Fixed Income Presentation – March 24, 201439 39Genworth MI Canada Inc.

PRIORITIES IMPACT ON FINANCIAL METRICS

› Prudent top line growth› Increasing premiums written

› Improving premiums earned

› Proactive risk management

› High quality insurance portfolio› Loss ratio In 15-25% range for 2014

› High quality investment portfolio › Investment income pressured by low rate environment

› Proactive approach to capital

management

› Operating modestly above MCT holding target of 220%

› Ongoing capital generation

› Strong ratings

> POSITIONED TO DELIVER ON

STRATEGIC PRIORITIES

TARGETING ROE EXPANSION OVER TIME

MIC Fixed Income Presentation – March 24, 201440 40Genworth MI Canada Inc.

GROWTH CATALYSTS

› Price Increase

Example: Impact of 2014 price increase on

$20 B of High LTV NIW

› Market Share Momentum Continuing

› Market Size - First-Time Homebuyers

45

70 70

2014 2015 2016

Incremental Premiums Written($MM)483 447

328 392

77 65

54

70

2012 2013 2013 Q3 YTD 2014 Q3 YTD

Portfolio Insurance High LTV

($MM)

> PREMIUMS WRITTEN

560 512 382 462

21% VPY

PREMIUMS WRITTEN

TOP LINE GROWTH IN 2014 DRIVEN BY HIGHER VOLUME & PREMIUM RATE INCREASE

MIC Fixed Income Presentation – March 24, 201441 41Genworth MI Canada Inc.

589 573 431 423

2012 2013 2013 Q3 YTD 2014 Q3 YTD

($MM)

45

70 70

2014 2015 2016

Incremental Premiums Written($MM)

2 10 20

40

2014 2015 2016 2017

Incremental Premiums Earned($MM)

EXAMPLE: IMPACT OF 2014 PRICE INCREASE

ON $20 B OF HIGH LTV NIW

› Declining trend coming to an end

› Higher insured volumes & 2014 price increase

should contribute to higher Premiums Earned

in 2015 and beyond

LTV = High Loan to Value

NIW = New Insurance Written

> PREMIUMS EARNED

PREMIUMS EARNED

PREMIUMS EARNED EXPECTED TO RISE IN COMING QUARTERS

MIC Fixed Income Presentation – March 24, 201442 42Genworth MI Canada Inc.

2,248 1,819 1,293 1,170

3,129 2,954 2,259 2,233

2012 2013 2013 Q3 YTD 2014 Q3 YTD

Net New Delinquencies Cures

> LOSSES ON CLAIMS

Loss Drivers:

› Continued home price appreciation

› Declining unemployment

› Proactive loss mitigation programs

NEW DELINQUENCIES NET OF CURES

33%

25% 26%

18%

2012 2013 2013 Q3 YTD 2014 Q3 YTD

LOSS RATIO

Results:

› High rate of cures

› Declining average paid claim severity

› Loss ratio of 18% Q3’14 YTD

8- Points VPY

5,377 4,773

3,552 3,403

Net

Cures

Total

MIC Fixed Income Presentation – March 24, 201443 43Genworth MI Canada Inc.

26%18%

18%

18%

2013 Q3 YTD 2014 Q3 YTD

Loss ratio Expense Ratio

$ MM (except EPS)2014 Q3

YTD

2013 Q3

YTD

Underwriting Income $270 240

Operating Investment

Income130 134

Interest Expense (18) (17)

Net Operating Income $283 $264

Investments $5,609 $5,435

Investment Yield 3.5% 3.7%

Operating ROE 12% 12%

Operating EPS (Diluted) $2.96 $2.70

› Strong underwriting performance driving improving profitability

› Investment yield continues to be pressured by low rate environment

› ROE stable at 12% as higher profitability was offset by higher capital levels

8-Points VPY44%

36%

> EARNINGS PROFILE

& KEY DRIVERS

COMBINED RATIO KEY FINANCIAL RESULTS

STRONG EARNINGS MOMENTUM GOING INTO 2015

MIC Fixed Income Presentation – March 24, 201444 44Genworth MI Canada Inc.

$ MM except NIWPre- Price

Increase

Post- Price

Increase

HLTV NIW - $ B $20 B $20 B

Average Premium Rate 2.30% 2.65%

Premiums Written / Earned $460 $530

Losses on Claims (161) (161)

Expenses (92) (95)

Underwriting Income 207 274

Loss Ratio 35% 30%

Expense Ratio 20% 18%

Combined Ratio 55% 48%

> IMPACT OF PRICE INCREASE

KEY HIGHLIGHTS

› 2014 price increase should translate

into higher underwriting profitability

› Annual pricing review - potential for

future price increases

LIFETIME UNDERWRITING INCOME EXAMPLE

2014 PRICE INCREASE A CATALYST FOR EARNINGS GROWTH IN COMING YEARS

MIC Fixed Income Presentation – March 24, 201445 45Genworth MI Canada Inc.

Diversify Globally

› IG Emerging Markets Debt› US CLOs (<3% of AUM / “A’ or Above)

› Hedge FX Risk

Diversify By Sector

› Market Weight Financials › Underweight Energy

Preserve Principal› Gov’t Bonds (~50% of AUM)

› Investment Grade Bonds

Protect From Rising Rates› Short Duration (3.6 Years)› Floating Rate Notes

Cash Flow Match Liabilities› Portfolio Duration < 5 Years

Enhance Income› Dividend Paying Equities› IG Emerging Markets Debt› US CLOs (<3% of AUM / “A” or Above)

ACTIVE PORTFOLIO

MANAGEMENT

› 4 External Managers

› In House Investment

Allocation & Oversight

› Focus on Investment

Grade Fixed Income

› Limited Appetite for

“Risk” Assets

1. Pre-tax equivalent book yield after dividend gross-up of general portfolio

$5.5 B INVESTMENT PORTFOLIO PRE-TAX YIELD1 OF 3.5% (SEPT. 30/14)

> DISCIPLINED APPROACH TO

INVESTMENT MANAGEMENT

IG = Investment Grade CLOs = Collateral Loan Obligations

YIELD CURRENTLY PRESSURED BY LOW RATES ... POSITIVE OUTLOOK FOR MEDIUM TERM

MIC Fixed Income Presentation – March 24, 201446 46Genworth MI Canada Inc.

$ MMSeptember 30,

2014

Assets

Cash and investments $5,609

Other Assets 258

Total Assets $5,867

Liabilities

Loss reserves 108

Unearned Premiums 1,763

Long Term Debt 432

Other Liabilities 242

Total Liabilities 2,545

Shareholders’ Equity 3,322

Total Liabilities and

Shareholders’ Equity$5,867

Book Value Per Share

(diluted)$34.57

> STRONG BALANCE SHEET

KEY HIGHLIGHTS

› $1.8 B of unearned premiums represent future

revenues & profits

› Illustration:

Unearned Premiums $1.8 B

Future Losses on Claims & Expenses1

(1.0)

Future Pre-tax Underwriting Income 0.8

Future Net Income $0.6 B

1. Future Loss on Claims & Expenses Calculated using 55% Combined Ratio

MIC Fixed Income Presentation – March 24, 201447 47Genworth MI Canada Inc.

Efficiency

Strength Flexibility

CAPITAL MANAGEMENT OBJECTIVES

> STRONG CAPITAL

CAPITAL STRENGTH

› Operate modestly above MCT Holding Target of 220%

› Conservative leverage of 12%

› Maintain Holding Company Cash & Marketable

Securities of >$100 MM

223% 224%

Dec. 31, 2013 Sept. 30, 2014

Minimum Capital Test

MIC Fixed Income Presentation – March 24, 201448 48Genworth MI Canada Inc.

Efficiency

Strength Flexibility

> STRONG CAPITAL

CAPITAL FLEXIBILITY & EFFICIENCY

› Target dividend payout ratio of 35 to 45%

› Pursue efficient capital structure using available levers

› Target leverage of 15% over the long run

› Share Buybacks & Special Dividends

› Optimize regulatory capital requirements

127 137

41 105

75

2013 2014

Ordinary Dividends Special Dividend

Share Buybacks

($MM)

$232 $253

CAPITAL RETURNED TO SHAREHOLDERS

CAPITAL MANAGEMENT OBJECTIVES

MIC Fixed Income Presentation – March 24, 201449 49Genworth MI Canada Inc.

POTENTIAL IMPACT OF PERFORMANCE LEVERS OVER TIME

Levers EPS ROE Comments

Price Increase ↑ ↑2014 price increase

Potential for future increases

Market Share Gains ↑ ↑ Capitalizing on momentum

Investment Yield

Improvement↑ ↑

10 Bps improvement in yield adds

$4MM in net operating income

Capital Optimization ↑Potential for a lower MCT Holding

Target reflecting the 2014 price

increase

> ROE EXPANSION

SEVERAL LEVERS TO DRIVE ROE EXPANSION OVER TIME

Q&A

> STUART LEVINGS, CHIEF OPERATING OFFICER

CLOSING REMARKS

MIC Fixed Income Presentation – March 24, 201452 52Genworth MI Canada Inc.

> Proven and sustainable business model

> Clear strategy for prudent growth

> Supportive market and regulatory environment

> Experts at managing mortgage default risk

> Solid financial position

> Experienced and engaged employees

> KEY TAKE-AWAYS

CANADA’S MORTGAGE INSURER OF CHOICE

53Genworth MI Canada Inc.

> SPEAKER BIOGRAPHIES

Brian led the establishment of

Genworth into the Canadian

marketplace in 1994 and later led it

through its initial public offering in

2009. He has more than 20 years of

senior management experience in the

mortgage insurance industry

worldwide. From 2004 to 2009 he led

Genworth’s activities and expansion in

key international markets. Prior roles

includes Senior Vice President,

International of General Electric’s U.S.

mortgage insurance business and

Senior Vice President of Sales and

Operations. As of January 1, 2015,

Brian will step down from the CEO

position and occupy the role of

Chairman of the Company.

Stuart has held a variety of senior

management positions within Genworth

Canada since joining the company in

2000. These roles include five years as

Chief Financial Officer prior to becoming

the Chief Risk Officer in January 2008.

More recently he has held the positions

of Chief Operations and Chief Operating

Officer, and effective January 1, 2015 he

will hold the position of President and

CEO. Stuart brings more than 20 years of

finance and general management

experience in financial services

businesses. Prior to joining the

Company, Stuart spent seven years with

Deloitte & Touche. He holds a Bachelor

of Accounting Science degree from the

University of South Africa and is a

member of both the South African and

Canadian Institutes of Chartered

Accountants.

Brian

Hurley

Chairman

and CEO

Stuart

Levings

Chief

Operating

Officer

54Genworth MI Canada Inc.

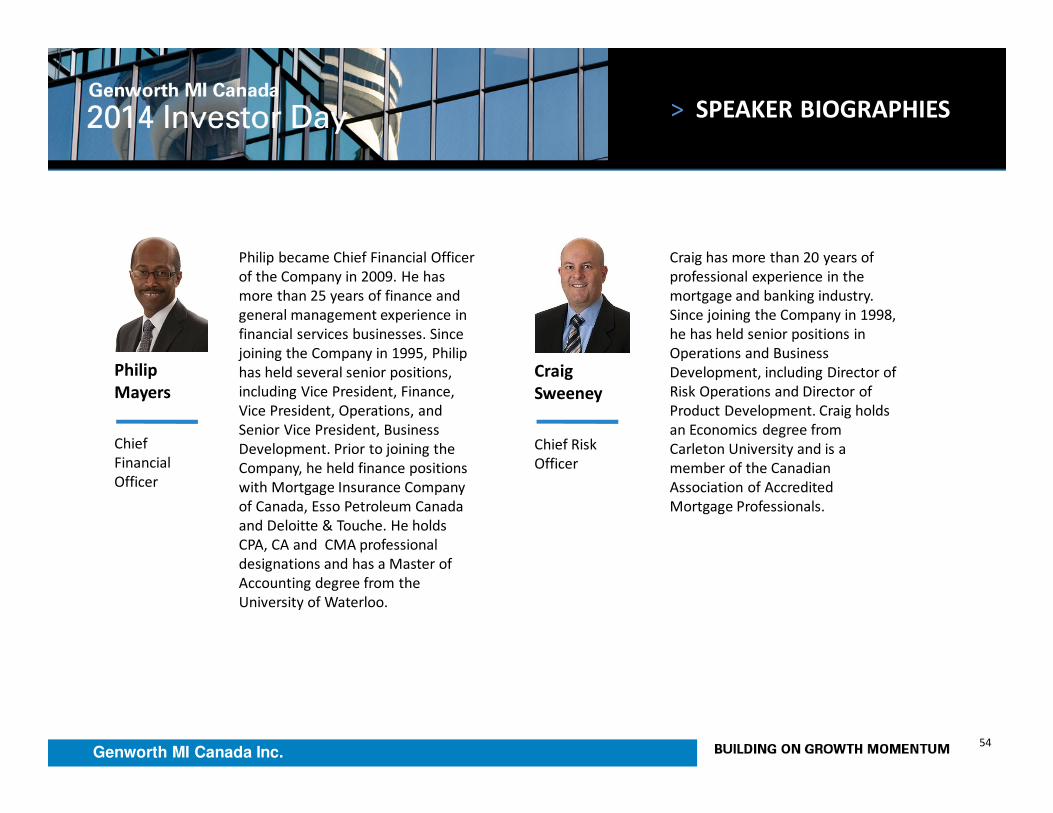

> SPEAKER BIOGRAPHIES

Philip became Chief Financial Officer

of the Company in 2009. He has

more than 25 years of finance and

general management experience in

financial services businesses. Since

joining the Company in 1995, Philip

has held several senior positions,

including Vice President, Finance,

Vice President, Operations, and

Senior Vice President, Business

Development. Prior to joining the

Company, he held finance positions

with Mortgage Insurance Company

of Canada, Esso Petroleum Canada

and Deloitte & Touche. He holds

CPA, CA and CMA professional

designations and has a Master of

Accounting degree from the

University of Waterloo.

Craig has more than 20 years of

professional experience in the

mortgage and banking industry.

Since joining the Company in 1998,

he has held senior positions in

Operations and Business

Development, including Director of

Risk Operations and Director of

Product Development. Craig holds

an Economics degree from

Carleton University and is a

member of the Canadian

Association of Accredited

Mortgage Professionals.

Philip

Mayers

Chief

Financial

Officer

Craig

Sweeney

Chief Risk

Officer

MIC Fixed Income Presentation – March 24, 201455 55Genworth MI Canada Inc.

> CONTACT INFORMATION

INVESTOR RELATIONS

www.genworth.ca

HEAD OFFICE

2060 Winston Park Drive

Suite 300

Oakville, Ontario

905-287-5300 (reception)

NATIONAL CALL CENTRE

1.800.511.8888

DIRECT CONTACT

Samantha Cheung, MBA

Vice-President, Investor Relations

905.287.5482