Balanced Growth Accumulator - Balanced... · The impact of the multiplier may be reduced because of...

16

FOR FINANCIAL PROFESSIONAL USE ONLY. NOT FOR USE WITH THE PUBLIC. Products Issued by: Minnesota Life Insurance Company FINANCIAL PROFESSIONAL GUIDE Balanced Growth Accumulator Indexed Universal Life Insurance

Transcript of Balanced Growth Accumulator - Balanced... · The impact of the multiplier may be reduced because of...

FOR FINANCIAL PROFESSIONAL USE ONLY. NOT FOR USE WITH THE PUBLIC.

Products Issued by: Minnesota LifeInsurance Company

FINANCIAL PROFESSIONAL GUIDE

Balanced Growth Accumulator Indexed Universal Life Insurance

2 2

Accumulation, income and

flexibility to help clients face

whatever comes their way.

3

Benefits of Indexed Universal LifeBalanced Growth Accumulator Indexed Universal Life (BGA) is a life insurance policy that provides

protection and innovative interest crediting options to help give clients a series of benefits, including:

• Uncapped accumulation The unique Balanced Indexed Accounts provide uncapped interest crediting potential.

Uncapped strategies o"er higher interest crediting potential with downside protection.

• Downside protection When index performance is positive, the accounts are credited at the end of the segment term.

If the index is down, clients are protected from negative performance.

• Financial flexibility

Policy loans and partial surrenders provide a source of supplemental retirement income and cash

for planned and unexpected expenses. Loans allow clients to borrow money on a tax-advantaged

basis by utilizing their cash accumulation at any time after the first policy year – even before age

59½.1 Properly structured, all withdrawals and loans from BGA can be distributed income tax-free.

• Income tax-free death benefit The purpose of life insurance is to provide a tax-free death benefit to your client’s beneficiaries.

It can be used to help beneficiaries pay for end-of-life expenses, cover estate taxes, o"set a loss

of future income or to help establish a lasting family legacy.

• No traditional contribution limits

BGA does not have traditional contribution limits, as long as it is not over funded and becomes a

Modified Endowment Contract (MEC).

This brochure will introduce you to the key BGA product features.

Policy loans and withdrawals will reduce the surrender value and death benefit and may create a taxable event in the event of lapse or policy surrender. Withdrawals may be subject to taxation within the first fifteen years of the contract. Clients should consult with their tax advisor when considering taking a policy loan or partial or full surrender.

1 The policy design selected may impact the tax status of the policy. If cients pay too much premium, their policy could become a modified endowment contract (MEC).

4

Select from multiple index opportunitiesBGA o"ers several account options that provide global, domestic and international growth

opportunities, giving clients the flexibility to adapt to changing market conditions. The crediting within

these accounts is based on the performance of underlying indices. The cash value has the opportunity

to increase based on the positive performance of the underlying index, and will not experience

negative crediting due to negative index performance.

The Blended Indexed Account credits interest based on a blend of the following diverse

indices: S&P 500® Index, Russell 2000®, Barclay’s Capital U.S. Aggregate Bond Index and

Euro Stoxx 50®.

A broadly diversified index drawing from a mix of asset classes including Equities, Bonds,

Commodities and Cash. This dynamic index reallocates daily – taking into account market

indicators, risk and momentum.

S&P 500® INDEX

S&P PRISMSM INDEX

GLOBAL BLEND

A stock market index based on market capitalizations of 500 of the largest U.S. companies.

The index is designed to measure performance of the broad domestic economy through

changes in the aggregate market value of 500 stocks representing all major industries.2

2 Source: Bloomberg L.P., About S&P 500® Index, retrieved from bloomberg.com, May 6, 2018.

5

BGA o"ers account options with capped and uncapped crediting potential or a crediting multiplier.5

Each of the accounts will provide di"erent crediting based on the underlying index and other factors

used to calculate indexed credit for that account.

Fixed Account

BGA also o"ers a fixed-interest account, which earns interest daily at a fixed rate and will always credit a

guaranteed minimum of 2% interest.

Provide growth potential through

multiple account options BGA o"ers the potential to earn interest based on the performance of one or more underlying stock

market indices through capped and uncapped accounts. When index performance is positive, the

accounts are credited at the end of the segment term.3 If the index is down, clients are protected from

negative performance.

3 Crediting is based on the balanced indexed or indexed account participation rate and is subject to any cap.

4 If the index allocation is less than 100%, the remaining portion receives a declared rate.

5 The index multiplier provides additional crediting when the indexed account has a positive index credit on the segment date. The impact of the multiplier may be reduced because of withdrawals and charges taken from the segment during the segment term.

6 BIA partial withdrawals are only paid on these account options.7 This indexed account uses a weighted average of the Barclay’s Capital U.S. Aggregate Bond Index, Standard & Poor’s 500® Composite Stock Price Index, excluding dividends,

EURO STOXX 50® Index, excluding dividends, and the Russell 2000® Index.

*Uncapped indexed account participation rates are subject to change. This could have the impact of the indexed account credit being less than the change in the reference index.

† Index caps and/or participation rates may change over time but not once an index segment is established, and may be less than 90%. See the latest BGA Rate Sheet for the most current information. Rates as of Jan. 18, 2019.

UNCAPPED BALANCED INDEXED ACCOUNTS*

CAPPED INDEXED ACCOUNTS†

SEGMENT TERM

INDEX ALLOCATION4

PARTICIPATION RATE*

INDEX MULTIPLIER5

S&P PRISM℠

(Balanced Indexed Account 7)6

3-year 200% 115% 0%

S&P PRISM℠

(Balanced Indexed Account 6)6

1-year 135% 105% 0%

S&P PRISM℠

(Balanced Indexed Account 4)6

1-year 120% 105% 10%

S&P PRISM℠ with Index Multiplier

(Balanced Indexed Account 8)6

available for 1.50% Index Segment Charge

1-year 135% 105% 30%

S&P 500® Index

(Balanced Indexed Account 2)6

available with 1.95% Index Segment Spread

2-year 90% 105% 0%

SEGMENT TERM

INDEX CAP PARTICIPATION RATE*

INDEX MULTIPLIER5

Blended (includes global components)7

(Indexed Account E)

1-year 14.00% 100% 0%

S&P 500® Index

(Indexed Account A)

1-year 10.50% 100% 0%

S&P 500® Index with Index Multiplier

(Indexed Account L)

available for 1.50% Index Segment Charge

1-year 10.50% 100% 30%

6

Enhanced accumulation and

income opportunitiesThese Balanced Indexed Account features help further enhance interest crediting potential during

the segment term and on full index credits.

Partial interest credits on withdrawalsOne of the many innovative BGA features is the ability to provide BIA

partial index credits on loans, partial surrenders and monthly charges

including cost of insurance. Clients can potentially experience more

long-term growth when they receive partial index credits before the end

of the segment term.

Participation RateThe accumulation potential of the uncapped Balanced Indexed

Accounts is maximized when segments reach their full term and receive

the participation rate.

7

8 If accumulation value is deducted from a Balanced Indexed Account for a policy loan with a fixed policy loan interest rate, a BIA partial index credit will be credited on the amount withdrawn from the balanced indexed account. The BIA partial index credit will be calculated based on the BIA partial index credit term. Additionally, a fixed interest rate loan will begin a 12-month lockout period during which no transfers from the fixed account to an indexed and/or balanced indexed accounts can be made.

9 As long as the policy is not a modified endowment contract. The policy design you choose may impact the tax status of your policy. If you pay too much premium, your policy could become a modified endowment contract (MEC). Distributions from a MEC may be taxable.

10 The short-term loan provision provides for interest waiver if the loan is paid in full within 90 days of the date the loan was taken. In the event the policyholder does not repay the loan in full within 90 days, interest and other policy loan provisions will apply as of the date the loan was taken. Additional restrictions may apply.

Financial flexibility when clients need it

Whether your clients need supplemental tax-advantaged retirement income or money for an

unexpected emergency, BGA’s cash value can help support them when they need it most. Clients can

access the policy’s cash value through loans and partial surrenders.8

Tax-advantaged policy loan optionsLoans allow your clients to borrow money against their policy’s cash value tax-advantaged at any time.9

BGA IUL features short-term, fixed interest, indexed and variable interest rate loan options.

Partial SurrendersPartial surrenders allow clients to withdraw money from their policy and will reduce the policy’s surrender

value and death benefit.

BGA’s cash value gains are credited on an income tax-deferred basis. Clients may take partial surrenders

up to the cost basis without paying income taxes, as long as their policy remains in force and is not a

modified endowment contract.

LOAN TYPE RATE CHARGED RATE CREDITED

Short-term

(interest-free for 90 days) 10

No charge if repaid within 90 days;

otherwise a 5% fixed rate applies

Directly tied to performance of your

chosen accounts

Fixed interest rate 4%; loan rate charged remains constant Loan credited at one of two rates

based on how long the policy has

been in force:

• Years 1-10: 3.0%

• Years 11+: 4.0%

Indexed 4.75%; loan rate charged remains constant Directly tied to performance of the

Indexed Loan Account

Variable interest rate Maximum of 1% above the current Fixed

Account crediting rate

Directly tied to performance of the

chosen accounts

8

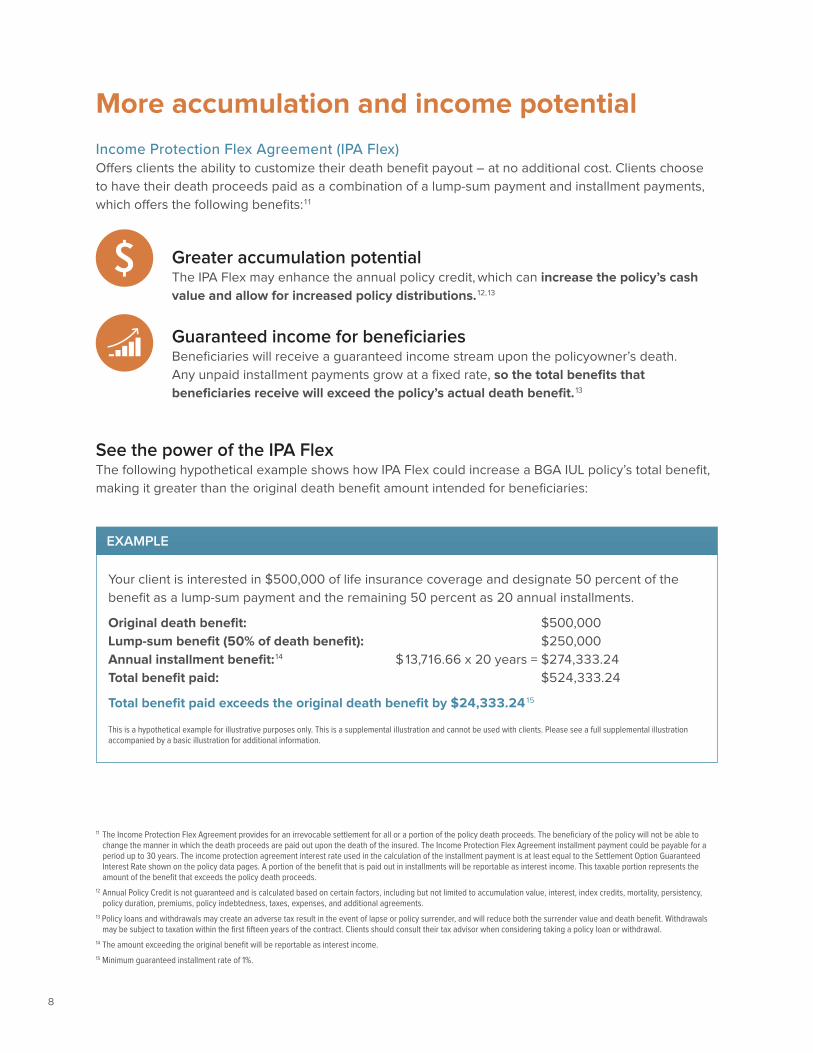

EXAMPLE

Your client is interested in $500,000 of life insurance coverage and designate 50 percent of the

benefit as a lump-sum payment and the remaining 50 percent as 20 annual installments.

Original death benefit: $500,000

Lump-sum benefit (50% of death benefit): $250,000

Annual installment benefit:14 $13,716.66 x 20 years = $274,333.24

Total benefit paid: $524,333.24

Total benefit paid exceeds the original death benefit by $24,333.2415

This is a hypothetical example for illustrative purposes only. This is a supplemental illustration and cannot be used with clients. Please see a full supplemental illustration accompanied by a basic illustration for additional information.

More accumulation and income potential

Income Protection Flex Agreement (IPA Flex)

O"ers clients the ability to customize their death benefit payout – at no additional cost. Clients choose

to have their death proceeds paid as a combination of a lump-sum payment and installment payments,

which o"ers the following benefits:11

Greater accumulation potential The IPA Flex may enhance the annual policy credit, which can increase the policy’s cash

value and allow for increased policy distributions.12,13

Guaranteed income for beneficiariesBeneficiaries will receive a guaranteed income stream upon the policyowner’s death.

Any unpaid installment payments grow at a fixed rate, so the total benefits that

beneficiaries receive will exceed the policy’s actual death benefit.13

See the power of the IPA FlexThe following hypothetical example shows how IPA Flex could increase a BGA IUL policy’s total benefit,

making it greater than the original death benefit amount intended for beneficiaries:

11 The Income Protection Flex Agreement provides for an irrevocable settlement for all or a portion of the policy death proceeds. The beneficiary of the policy will not be able to change the manner in which the death proceeds are paid out upon the death of the insured. The Income Protection Flex Agreement installment payment could be payable for a period up to 30 years. The income protection agreement interest rate used in the calculation of the installment payment is at least equal to the Settlement Option Guaranteed Interest Rate shown on the policy data pages. A portion of the benefit that is paid out in installments will be reportable as interest income. This taxable portion represents the amount of the benefit that exceeds the policy death proceeds.

12 Annual Policy Credit is not guaranteed and is calculated based on certain factors, including but not limited to accumulation value, interest, index credits, mortality, persistency, policy duration, premiums, policy indebtedness, taxes, expenses, and additional agreements.

13 Policy loans and withdrawals may create an adverse tax result in the event of lapse or policy surrender, and will reduce both the surrender value and death benefit. Withdrawals may be subject to taxation within the first fifteen years of the contract. Clients should consult their tax advisor when considering taking a policy loan or withdrawal.

14 The amount exceeding the original benefit will be reportable as interest income.

15 Minimum guaranteed installment rate of 1%.

9

The Chronic Illness Access Agreement and the Accelerated Death Benefit for Chronic Illness Agreement may not cover all of the costs associated with chronic illness. The Agreements are generally not subject to health insurance requirements and do not provide long-term care insurance subject to state long-term care insurance law. These Agreements are not state-approved Partnership for Long Term Care Program Agreements and are not a Medicare supplement policy. Receipt of chronic illness benefit payments under these agreements may adversely a#ect eligibility for Medicaid or other government benefits or entitlements.

Due to uncertainty in the tax law, chronic illness benefits paid from a life insurance contract may be taxable. Please ensure your clients consult a tax advisor regarding chronic illness benefit payments from a life insurance contract.

All requirements and qualifications must be met before chronic illness benefits can begin under these agreements.

The accumulation value, surrender value, loan value and death benefit will be reduced by a chronic illness benefit payment under these agreements.

Chronic illness protection

Chronic Illness Access Agreement (CIAA)

Provides access to a portion of the death benefit while alive and upon the insured’s being certified

as a chronically ill individual. Although there is no additional cost for the agreement, this agreement

utilizes a discount method, which means the benefit payment will be less than the death benefit that

is accelerated.

Accelerated Death Benefit for Chronic Illness Agreement (CIA)

The CIA gives clients access to a portion of the death benefit while living if they are certified as

chronically ill and meet certain requirements. They have the freedom to save or spend the benefit

payments any way they choose. They can stop receiving benefits, if no longer needed, and start again

with recertification. They can select from:

• 10% to 100% of the life insurance face amount for chronic illness benefits ($100,000 minimum, not to

exceed $5 million)

• A monthly benefit maximum of 2 or 4 percent of the dedicated face amount

Clients determine the chronic illness death benefit amount and monthly benefit percentage at the time

of application and have access to 100% of the benefit value they purchase while on a claim. CIA charges

are deducted from the accumulation value along with the other charges on the contract. Any remaining

death benefit will be paid to beneficiaries. CIA can be added to your client’s policy at issue, or later with

underwriting approval, for an additional cost.

Source: LIMRA/Life Happens 2016 Insurance Barometer Study.

The ability to a"ord a comfortable retirement is the most common

financial concern among Americans.

10

16 Due to uncertainty in the tax law, terminal illness benefits paid from a life insurance contract may be taxable. Please ensure that your clients consult a tax advisor regarding chronic illness or terminal illness benefit payments from a life insurance contract.

Additional policy agreements

Terminal illness protection

Accelerated Death Benefit for Terminal Illness (TIA)16

Allows access to a portion of the death benefit while living and upon diagnosis of a terminal illness. There is

no charge for this agreement.

Disability protection

Waiver of Charges Agreement

Waives monthly charges if the insured is totally and permanently disabled before age 65.

Waiver of Premium Agreement

Waives premiums on a monthly basis if the insured becomes totally and permanently disabled before age 65.

Business benefits

Exchange of Insureds Agreement

Provides for the exchange of one insured for another insured. The policy must be corporate-owned by

the same corporation before and after the exchange.

Surrender Value Enhancement Agreement (SVEA)

Guarantees that surrender values will be no less than 100% of cumulative premiums paid during the first

three years.

• Must be a business-owned policy

• Requires use of the Early Values Agreement

Additional death benefit agreements

Guaranteed Insurability Option Agreement

Provides future options to increase coverage without underwriting on specified dates between the ages

of 22 and 40. These dates can be substituted for date of marriage, or birth or adoption of a child, which

will then forfeit the next regular option date. The maximum additional increase amount is $100,000 and

must be selected at issue.

Inflation Agreement

Increases the face amount of the policy every three years based on increases in the Consumer Price

Index (CPI).

Term Insurance Agreement

Provides additional temporary life insurance – up to four times the base coverage. This agreement will

increase rates annually for the insured up to age 100 and can only be added at policy issue, but may be

removed after the first policy year.

11

Income protection

Guaranteed Income Agreement (GIA)17

Allows your clients to turn cash value into guaranteed income to age 100. When exercised, a one-time

charge is assessed and all other agreements will be terminated, except any agreement that provides an

irrevocable settlement option.

Death benefit options

Clients can use BGA to create an income tax-free death benefit for their loved ones. BGA provides

two options for death benefit. Certain Agreements may require clients to choose a specific death

benefit option. These death benefit options may be changed after policy issue to best fit your clients’

changing needs.

Level Death Benefit (Option 1)

Death benefit is equal to the face amount. Option 1 may have lower costs of insurance later in life.

Increasing Death Benefit (Option 2)

Death benefit is equal to the face amount plus the policy accumulation value. Policies can potentially

receive index credits. This means clients with uncapped indexed account value can potentially pass a

larger death benefit than they would if policy value were only in a capped account.

Other agreementsEarly Values Agreement

Eliminates policy surrender charges in exchange for a separate monthly charge, and spreads out

compensation over a longer period.

Overloan Protection Agreement18

Prevents an outstanding policy loan from terminating the policy, even if the accumulation value is

InsuHcient to cover policy charges.

Premium Deposit Account Agreement19

Provides the opportunity to fund a life insurance policy through a single deposit that will result in a series

of fixed payments into the policy. Interest is earned on the funds in the premium deposit account.

17 Policyholders who add the Guaranteed Income Agreement (GIA) should take into consideration that the policy accumulation value on the exercise-e#ective date may not be su$cient to continue providing the minimum benefit payment until the insured’s age 100. If this occurs, it will not be possible to exercise the GIA. Minnesota Life and Securian Life believe the Policy will continue to qualify as life insurance under the Internal Revenue Service Code (“the Code”) after the GIA exercise-e#ective date, and that distributions and loans made under the terms of the GIA will generally not be taxed to the policyholder. However, the IRS or the courts could reach a di#erent result. Policyholders who have added the GIA should consult a tax advisor regarding the tax treatment of distributions and loans under the GIA. Since the Policy’s death benefit will be reduced to the minimum amount allowable under the Code after the exercise-e#ective date, policyholders should consider the impact on their individual circumstances and their need for death benefit before exercising the GIA. There is no charge for the GIA when the Policy is purchased; however, we will assess a one-time charge against the Policy accumulation value on the exercise-e#ective date. When the GIA is exercised, all other policy agreements will be terminated. However, if the GIA is issued with BGA Indexed Universal Life, any agreement that provides an irrevocable settlement option will not be terminated. The impact of exercising the GIA on a policy that contains an agreement providing an irrevocable settlement option may result in lump-sum death benefits not being available.

18 The tax treatment of the Overloan Protection Agreement is uncertain and it is not clear whether the Overloan Protection Agreement will be e#ective to prevent taxation of any out standing loan balance as a distribution in those situations where Overloan Protection takes e#ect. Clients contemplating exercising the Policy's Overloan Protection Agreement should consult a tax advisor.

19 Interest credited when used to pay policy premiums will be reported as taxable income to the policy owner.

12

Premiums and charges

PremiumsA minimum initial premium is required to issue the policy. The required minimum premium is shown on

each illustration. Premiums that exceed the tests for life insurance are not allowed. If the client wants the

policy to avoid becoming a Modified Endowment Contract (MEC), we will not accept any premium – or

make any other policy change – that would cause the policy to become an MEC. Depending upon the

actual policy experience, clients may need to increase premium payments to keep the policy in force.

The client chooses to allocate premiums and accumulation value to the Balanced Indexed Accounts,

Indexed Accounts and/or the fixed account. These allocation percentages can be changed on premiums

submitted after issue. The client also chooses an amount to pay in premium at issue, and that amount

can be changed at any time based on the restrictions above.

ChargesA 5.5% premium charge may be deducted from premium payments.20 The remaining amount is added to

the policy’s accumulation value.

Minnesota Life deducts administrative and insurance charges from the accumulation value each month.

These charges will first be deducted from the fixed account. If there is insuHcient accumulation value in

the fixed account, the balance of the charges will be deducted from the Balanced Indexed Accounts and

Indexed Account segments on a last-in/first-out basis.

Charges deducted from balanced indexed accounts may receive a BIA partial index credit. Transaction

charges may apply to changes made to the policy.

Surrender charges recover the expenses not yet covered by other policy charges. For BGA,

surrender charges apply to the first 10 years of the contract or 10 years from a face amount increase.

Tests for life insuranceSection 7702 of the Internal Revenue Code generally treats a contract as life insurance for federal

income tax purposes if it meets one of two tests. The client must select the test at contract issue, and

the test cannot be changed.

Guideline Premium Test (GPT)The GPT uses one set of corridor factors to maintain an IRS-mandated minimum amount of death benefit

above the contract’s accumulated value.

It places limits on the amount of premium that can be paid into the contract. These limits are set using

the Guideline Level Premium and the Guideline Single Premium for life insurance. Illustration pages list

both GPT test amounts when you choose this test for an illustration.

The Guideline Single Premium amount will be the same for a policy regardless of the death benefit

option chosen. The Guideline Level Premium amount will vary with the death benefit option that is chosen.

Cash Value Accumulation Test (CVAT)The CVAT does not place limits on the amount of premium that can be paid as long as there is a

minimum death benefit maintained above the contract’s accumulation value.

20 The premium charge is subject to change and will not exceed a maximum rate of 7%.

13

Balanced Indexed Accounts (BIA)

Uncapped account options that

credit interest to the cash value

at the end of the index term by

applying the index allocation and

participation rate to any index

growth, and adjusting for the

segment spread, index multiplier

or declared rate (if applicable).

BIA Partial Index Credits

BIA Partial index credits are

applied when a withdrawal is

taken from any uncapped option

during a crediting term, and are

subject to the participation rate,

segment spread and declared

rate (if applicable).

Cash value

A portion of the premium

payment, also called the

accumulation value, that can grow

based on interest credits from the

account options and may be

accessed at any time for income.

Cap

The maximum growth that will be

credited each segment term.

Cost basis

The total premiums paid into

the policy, less any tax-free

distributions.

Declared Rate Allocation

Percentage of the Balanced

Indexed Account that grows at

a fixed rate of interest – the

declared rate.

Floor

A guaranteed minimum growth

rate, or floor, that protects the

policy from negative crediting.

Index allocation

A percentage used to measure

index growth and used in the

calculation of interest credits or

BIA partial index credits.

Indexed accounts

Account options that credit 100%

of any interest to the cash value at

the end of the index term up to the

annual Cap.

Index segment

The portion of an indexed account,

Balanced Indexed Account or

indexed loan account created

from transfers from other accounts

and any amount retained in those

accounts at the end of previous

segment term.

Index term

The time period over which an

index credit is calculated based

on the performance of an

underlying index.

Modified Endowment Contract (MEC)

A life insurance policy that exceeds

maximum premium funding allowed

by the federal government.

Participation rate

A percentage applied at the end

of the segment term used in the

calculation of interest credits based

on index growth.

Premium charge

A percentage amount deducted

from each premium payment

before the remaining amount

is applied to the cash value in

the policy.

Premiums

The payments clients make on

the policy.

Segment spread

A percentage deducted from

index credits and any partial

index credits, but will never cause

interest credits to be less than zero.

KEY TERMS AND DEFINITIONS

14

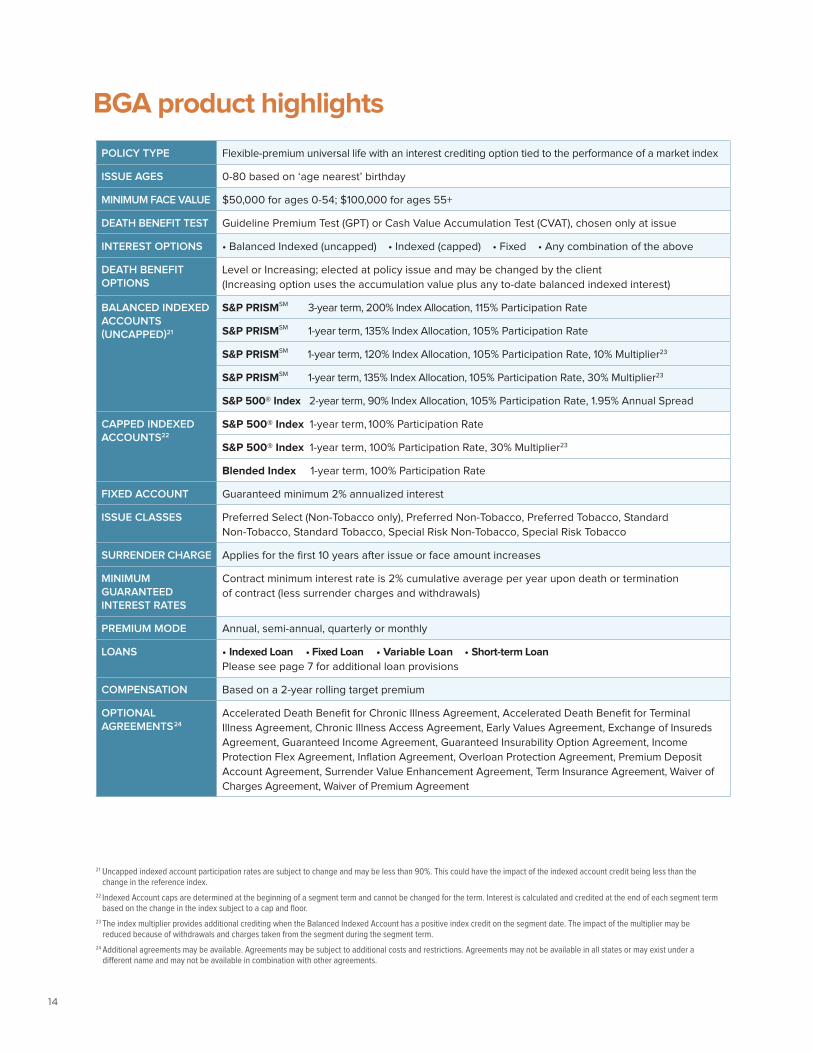

BGA product highlights

21 Uncapped indexed account participation rates are subject to change and may be less than 90%. This could have the impact of the indexed account credit being less than the change in the reference index.

22 Indexed Account caps are determined at the beginning of a segment term and cannot be changed for the term. Interest is calculated and credited at the end of each segment term based on the change in the index subject to a cap and floor.

23 The index multiplier provides additional crediting when the Balanced Indexed Account has a positive index credit on the segment date. The impact of the multiplier may be reduced because of withdrawals and charges taken from the segment during the segment term.

24 Additional agreements may be available. Agreements may be subject to additional costs and restrictions. Agreements may not be available in all states or may exist under a di#erent name and may not be available in combination with other agreements.

POLICY TYPE Flexible-premium universal life with an interest crediting option tied to the performance of a market index

ISSUE AGES 0-80 based on ‘age nearest’ birthday

MINIMUM FACE VALUE $50,000 for ages 0-54; $100,000 for ages 55+

DEATH BENEFIT TEST Guideline Premium Test (GPT) or Cash Value Accumulation Test (CVAT), chosen only at issue

INTEREST OPTIONS • Balanced Indexed (uncapped) • Indexed (capped) • Fixed • Any combination of the above

DEATH BENEFIT OPTIONS

Level or Increasing; elected at policy issue and may be changed by the client

(Increasing option uses the accumulation value plus any to-date balanced indexed interest)

BALANCED INDEXED ACCOUNTS (UNCAPPED)21

S&P PRISMSM 3-year term, 200% Index Allocation, 115% Participation Rate

S&P PRISMSM 1-year term, 135% Index Allocation, 105% Participation Rate

S&P PRISMSM 1-year term, 120% Index Allocation, 105% Participation Rate, 10% Multiplier23

S&P PRISMSM 1-year term, 135% Index Allocation, 105% Participation Rate, 30% Multiplier23

S&P 500® Index 2-year term, 90% Index Allocation, 105% Participation Rate, 1.95% Annual Spread

CAPPED INDEXED ACCOUNTS22

S&P 500® Index 1-year term, 100% Participation Rate

S&P 500® Index 1-year term, 100% Participation Rate, 30% Multiplier23

Blended Index 1-year term, 100% Participation Rate

FIXED ACCOUNT Guaranteed minimum 2% annualized interest

ISSUE CLASSES Preferred Select (Non-Tobacco only), Preferred Non-Tobacco, Preferred Tobacco, Standard

Non-Tobacco, Standard Tobacco, Special Risk Non-Tobacco, Special Risk Tobacco

SURRENDER CHARGE Applies for the first 10 years after issue or face amount increases

MINIMUM GUARANTEED INTEREST RATES

Contract minimum interest rate is 2% cumulative average per year upon death or termination

of contract (less surrender charges and withdrawals)

PREMIUM MODE Annual, semi-annual, quarterly or monthly

LOANS • Indexed Loan • Fixed Loan • Variable Loan • Short-term Loan

Please see page 7 for additional loan provisions

COMPENSATION Based on a 2-year rolling target premium

OPTIONAL AGREEMENTS24

Accelerated Death Benefit for Chronic Illness Agreement, Accelerated Death Benefit for Terminal

Illness Agreement, Chronic Illness Access Agreement, Early Values Agreement, Exchange of Insureds

Agreement, Guaranteed Income Agreement, Guaranteed Insurability Option Agreement, Income

Protection Flex Agreement, Inflation Agreement, Overloan Protection Agreement, Premium Deposit

Account Agreement, Surrender Value Enhancement Agreement, Term Insurance Agreement, Waiver of

Charges Agreement, Waiver of Premium Agreement

15

Contact your Annexus Independent Distribution Company for more information.

INSURANCE | INVESTMENTS | RETIREMENTSecurian Financial Group, Inc.

www.securian.com

Insurance products are issued by Minnesota Life Insurance Company in all states except New York. In New York, products are issued by Securian Life Insurance Company, a New York authorized insurer. Minnesota Life is not an authorized New York insurer and does not do insurance business in New York. Both companies are headquartered in Saint Paul, MN. Product availability and features may vary by state. Each insurer is solely responsible for the financial obligations under the policies or contracts it issues. 400 Robert Street North, St. Paul, MN 55101-2098 ©2019 Securian Financial Group, Inc. All rights reserved.

Policy form numbers: ICC16-20073 16-20073 and any state variations; ICC17-20118 17-20118 and any state variationsF91441-6 DOFU 1-2019 Rev 1-2019585044

Insurance products described here are underwritten and issued by Minnesota Life Insurance Company. Annexus Enterprises, LLC serves as a distributor of these products and is independently owned and not a$liated with Minnesota Life Insurance Company.

Annexus designs insurance solutions combining principal protection with index growth opportunities. Annexus uses patented technologies developed in partnership with Genesis Financial to help individuals face their financial future with confidence.

This information should not be considered as tax or legal advice. Clients should consult their tax or legal advisor regarding their own tax or legal situation.

BGA Indexed Universal Life Insurance is designed first and foremost to provide life insurance protection. While the interest crediting options are attractive for cash value accumulation, this product should always be promoted to first meet the death benefit needs of families and businesses with cash accumulation as a secondary benefit. One can lose money in this product.

Life insurance products contain fees, such as mortality and expense charges (which may increase over time), and may contain restrictions, such as surrender charges. Guarantees are based on the claims-paying ability of the issuing insurance company.

The underlying indices only recognize the changes in stock prices and do not include any dividend returns. While the policy and the Indexed Accounts do not actually participate in the stock market or the indicies, and one cannot invest directly in an Index, the performance of the underlying index may exceed the o#ered indexed growth caps. Interest crediting within these accounts will vary based on the movement of the equities within the underlying index. If the index experiences growth less than or equal to 0%, no index credit will be applied to the account. Administrative and insurance charges are deducted every month, regardless of whether premium outlays are made.

The "S&P 500 Index" and "S&P PRISM Index" are products of S&P Dow Jones Indices LLC or its a$liates ("SPDJI"), and have been licensed for use by Minnesota Life Insurance Company. Standard & Poor's® and S&P® are registered trademarks of Standard & Poor's Financial Services LLC, a division of S&P Global ("S&P"); Dow Jones® is a registered trademark of Dow Jones Trademark Holdings LLC ("Dow Jones"); and these trademarks have been licensed for use by SPDJI and sublicensed for certain purposes by Minnesota Life Insurance Company ("Minnesota Life'). The Indexed Universal Life Insurance Policy Series ("the Policies") are not sponsored, endorsed, sold or promoted by SPDJI, Dow Jones, S&P, any of their respective a$liates (collectively, "S&P Dow Jones Indices"). S&P Dow Jones Indices does not make any representation or warranty, express or implied, to the owners of the Policies or any member of the public regarding the advisability of investing in securities generally or in the Policies particularly or the ability of the S&P 500 Index or S&P PRISM Index to track general market performance. Past performance of an index is not an indication or guarantee of future results. S&P Dow Jones Indices only relationship to Minnesota Life with respect to the S&P 500 Index and S&P PRISM Index is the licensing of the Indices and certain trademarks, service marks and/or trade names of S&P Dow Jones Indices and/or its licensors. The S&P 500 Index or S&P PRISM Index are determined, composed and calculated by S&P Dow Jones Indices without regard to Minnesota Life or the Policies. S&P Dow Jones Indices has no obligation to take the needs of Minnesota Life or the owners of the Policies into consideration in determining, composing or calculating the S&P 500 Index or S&P PRISM Index. S&P Dow Jones Indices is not responsible for and has not participated in the determination of the prices, and amount of the Policies or the timing of the issuance or sale of the Policies or in the determination or calculation of the equation by which the Policies are to be converted into cash, surrendered or redeemed, as the case may be. S&P Dow Jones Indices has no obligation or liability in connection with the administration, marketing or trading of the Policies. There is no assurance that investment products based on the S&P 500 Index or S&P PRISM Index will accurately track index performance or provide positive investment returns. S&P Dow Jones Indices LLC is not an investment advisor or tax advisor. A tax advisor should be consulted to evaluate the impact of any tax-exempt securities on portfolios and the tax consequences of making any particular investment decision. Inclusion of a security within an index is not a recommendation by S&P Dow Jones Indices to buy, sell, or hold such security, nor is it considered to be investment advice.

NEITHER S&P DOW JONES INDICES NOR THIRD PARTY LICENSOR GUARANTEES THE ADEQUACY, ACCURACY, TIMELINESS AND/OR THE COMPLETENESS OF THE S&P 500 INDEX OR S&P PRISM INDEX OR ANY DATA RELATED THERETO OR ANY COMMUNICATION, INCLUDING BUT NOT LIMITED TO, ORAL OR WRITTEN COMMUNICATION (INCLUDING ELECTRONIC COMMUNJCATIONS) WITH RESPECT THERETO. S&P DOW JONES INDICES SHALL NOT BE SUBJECT TO ANY DAMAGES OR LIABILITY FOR ANY ERRORS, OMISSIONS, OR DELAYS THEREIN. S&P DOW JONES INDICES MAKES NO EXPRESS OR IMPLIED WARRANTIES, AND EXPRESSLY DISCLAIMS ALL WARRANTIES, OF MERCHANTABILITY OR FITNESS FOR A PARTICULAR PURPOSE OR USE OR AS TO RESULTS TO BE OBTAINED BY MINNESOTA LIFE, OWNERS OF THE POLICIES, OR ANY OTHER PERSON OR ENTITY FROM THE USE OF THE S&P 500 INDEX OR S&P PRISM INDEX OR WITH RESPECT TO ANY DATA RELATED THERETO. WITHOUT LIMITING ANY OF THE FOREGOING, IN NO EVENT WHATSOEVER SHALL S&P DOW JONES INDICES BE LIABLE FOR ANY INDIRECT, SPECIAL, INCIDENTAL, PUNITIVE, OR CONSEQUENTIAL DAMAGES INCLUDING BUT NOT LIMITED TO, LOSS OF PROFITS, TRADING LOSSES, LOST TIME OR GOODWILL, EVEN IF THEY HAVE BEEN ADVISED OF THE POSSIBILITY OF SUCH DAMAGES, WHETHER IN CONTRACT, TORT, STRICT LIABILITY, OR OTHERWISE. THERE ARE NO THIRD PARTY BENEFICIARIES OF ANY AGREEMENTS OR ARRANGEMENTS BETWEEN S&P DOW JONES INDICES AND MINNESOTA LIFE, OTHER THAN THE LICENSORS OF S&P DOW JONES INDICES.

ii Russell Investment group. Russell 2000® is an equity index that measures the performance of the 2,000 smallest companies in the Russell 3000® Index, which is made up of 3,000 of the biggest U.S. stocks. The Russell 2000® is constructed to provide a comprehensive and unbiased small-cap barometer and is completely reconstituted annually to ensure larger stocks do not a#ect the performance and characteristics of the true small-cap index. Russell 2000® is a registered service mark of Frank Russell Company. The Indexed Universal Life Series ("the Policies") are not sponsored, endorsed, sold or promoted by Russell Investment Group and the Russell Investment Group makes no representation regarding the advisability of the Policies or use of the Russell 2000® Index or any data included therein. Russell Investment Group is the source and owner of the trademarks, service marks and copyrights related to the Russell Indexes. Russell® is a trademark of Russell Investment Group.

iii Barclays Capital Inc. and its a$liates ("Barclays") is not the issuer or producer of the Indexed Universal Life Series Policies ("the Policies"), and Barclays has no responsibilities, obligations or duties to investors in the Policies. The Barclays Capital U.S. Aggregate Index is a trademark owned by Barclays Bank PLC and licensed for use by Minnesota Life Insurance Company ("Minnesota Life") and Securian Life Insurance Company ("Securian Life") as the Issuer of the Policies. While Minnesota Life and Securian Life may for itself execute transaction(s) with Barclays in or relating to the Barclays Capital U.S. Aggregate Bond Index, the Policies investors shall not acquire any interest in Barclays Capital U.S. Aggregate Bond Index nor do they enter into any relationship of any kind whatsoever with Barclays upon making an investment in the Policies. The Policies are not sponsored, endorsed, sold or promoted by Barclays and Barclay's makes no representation regarding the advisability for the Policies or use of the Barclays Capital U.S. Aggregate Bond Index or any data included therein. Barclays shall not be liable in any way to the Issuer, investors or to other third parties in respect of the use of accuracy of the Barclays Capital U.S. Aggregate Bond Index or any data included therein.

iv The EURO STOXX 50® is the intellectual property (including registered trademarks) of STOXX Limited, Zurich, Switzerland and/or its licensors ("Licensors"), which is used under license. The interest crediting for the Indexed Universal Life Series Policies based on the Index are in no way sponsored, endorsed, sold or promoted by STOXX and its Licensors and neither of the Licensors shall have any liability with respect thereto.

These are general marketing materials and, accordingly, should not be considered investment advice or a recommendation that any particular product or feature is appropriate or suitable for any particular individual. These materials are based on hypothetical scenarios and are not designed for any particular individual or group of individuals (for example, any demographic group by age or occupation). The materials were prepared for financial professionals who are experienced in investment and/or insurance matters. As a result, they should not be reviewed or relied on by any other persons. Securian Financial Group and its a$liates have a financial interest in the sale of their products.

FOR FINANCIAL PROFESSIONAL USE ONLY. NOT FOR USE WITH THE PUBLIC. This material may not be reproduced in any form where it would be accessible to the general public.