Audit and Risk Management Meeting Standard - Minutes... · 1. Receive the Compliance Audit Return...

43

MINUTES AUDIT AND RISK MANAGEMENT COMMITTEE Tuesday, 13 February 2018, 5.30 pm

Transcript of Audit and Risk Management Meeting Standard - Minutes... · 1. Receive the Compliance Audit Return...

MINUTES

AUDIT AND RISK MANAGEMENT COMMITTEE

Tuesday, 13 February 2018, 5.30 pm

TABLE OF CONTENTS

ITEM NO SUBJECT PAGE

RESPONSE TO PREVIOUS PUBLIC QUESTIONS TAKEN ON NOTICE 2

PUBLIC QUESTION TIME 2

REPORTS BY OFFICERS 3

ARMC1802-1 ADOPTION OF THE 2017 COMPLIANCE AUDIT RETURN 3

ARMC1802-4 INTERNAL AUDIT REPORTS - PURCHASING, DELEGATION OF AUTHORITY AND INFORMATION/RECORDS MANAGEMENT 6

ARMC1802-2 INVESTIGATION OF BEST PRACTICE PROCUREMENT OF ARTISTS IN THE LOCAL GOVERNMENT SECTOR 16

ARMC1802-3 OVERDUE DEBTORS REPORT AS AT 31 DECEMBER 2017 19

ARMC1802-5 AUDIT AND RISK UPDATE FOR ASSETS 23

ARMC1802-6 INFORMATION REPORT - OFFICE OF THE AUDITOR GENERAL PROCUREMENT PERFORMANCE AUDIT 27

ARMC1802-7 INFORMATION REPORT - PURCHASING POLICY EXEMPTIONS DECEMBER 2017 AND JANUARY 2018 29

ARMC1802-8 INFORMATION REPORT - FINANCIAL MANAGEMENT REVIEW 2017 PROGRESS ON ACTIONS 31

ARMC1802-9 INFORMATION REPORT - LOCAL GOVERNMENT AUDITING REFORMS 38

CONFIDENTIAL MATTERS 40

ARMC1802-10 CONFIDENTIAL REPORT - PROPERTY DISPUTE HIGH STREET ROAD RESERVE 40

CLOSURE OF MEETING 41

Minutes Attachments – Audit and Risk Management Committee 13 February 2018

Page 1

AUDIT AND RISK MANAGEMENT COMMITTEE

Minutes of the Audit and Risk Management Committee meeting held in the City of Fremantle Administration Building at Fremantle Oval

on 13 February 2018 at 5.30 pm. DECLARATION OF OPENING / ANNOUNCEMENT OF VISITORS The Presiding Member declared the meeting open at 5.55 pm and welcomed members to the meeting. NYOONGAR ACKNOWLEDGEMENT STATEMENT "We acknowledge this land that we meet on today is part of the traditional lands of the Nyoongar people and that we respect their spiritual relationship with their country. We also acknowledge the Nyoongar people as the custodians of the greater Fremantle/Walyalup area and that their cultural and heritage beliefs are still important to the living Nyoongar people today." IN ATTENDANCE Cr Jeff McDonald Presiding Member / Hilton Ward Cr Doug Thompson North Ward (entered at 5.59pm) Cr Rachel Pemberton City Ward Mr Phillip Draber External Committee Member Mr Glen Dougall Acting Chief Executive Officer/Director City Business Ms Narelle French Manager Finance Ms Charlie Clarke Manager Governance Mr Kevin Porter Senior Contracts and Procurement Officer Ms Helen Bliss Governance Officer Ms Holly Glossop Minute Secretary Cameron Palassis Executive Director of Paxton Group (Auditor) Brendan Peyton Managing Director Peyton Consulting (Auditor) There were approximately no members of the public and no member/s of the press in attendance. APOLOGIES Cr Jenny Archibald Deputy Presiding Member / East Ward Mr Philip St John Chief Executive Officer LEAVE OF ABSENCE

Minutes Attachments – Audit and Risk Management Committee 13 February 2018

Page 2

Nil DISCLOSURES OF INTEREST BY MEMBERS Nil RESPONSE TO PREVIOUS PUBLIC QUESTIONS TAKEN ON NOTICE Nil PUBLIC QUESTION TIME Nil DEPUTATIONS / PRESENTATIONS Nil CONFIRMATION OF MINUTES MOVED: Cr Jeff McDonald That the minutes of the Audit and Risk Management Committee meeting dated 5 December 2017 be confirmed as a true and accurate record. CARRIED: 3/0 For Against Cr Jeff McDonald Cr Rachel Pemberton Mr Phillip Draber

TABLED DOCUMENTS Nil. LATE ITEMS NOTED Nil

Minutes Attachments – Audit and Risk Management Committee 13 February 2018

Page 3

REPORTS BY OFFICERS At 5.59pm Cr Doug Thompson entered the meeting. ARMC1802-1 ADOPTION OF THE 2017 COMPLIANCE AUDIT RETURN Meeting Date: 13 February 2018 Previous Item: Nil Responsible Officer: Manager Governance Decision Making Authority: Council Agenda Attachments: Summary report by Peyton Consultancy

2017 Compliance Audit Return Confidential auditor’s report (under separate cover)

SUMMARY

The 2017 Compliance Audit Return (CAR) has now been completed by an independent auditor and is presented to Council for adoption in accordance with the requirements set by the Department of Local Government, Sport and Cultural Industries. It is recommended that Council:

1. Receive the Compliance Audit Return 2017 Summary Report by Peyton Consultancy, as shown in Attachment 1 of this agenda item.

2. Adopt the 2017 Compliance Audit Return as shown in Attachment 2 of this

agenda item, to be signed by the Mayor and CEO and submitted to the Department of Local Government, Sport and Cultural Industries before 31 March 2018.

BACKGROUND

In accordance with the Act, each local government authority is required to carry out a compliance audit for the period 1 January to 31 December of each year as instructed by the department. The return consists of 87 questions relating to the local government’s compliance with the requirements of the Act and its Regulations, concentrating on areas of compliance considered “high risk”. Questions are generally asked in a positive phrase where a ‘yes’ response indicates compliance and a ‘no’ response indicates non-compliance. In some cases an ‘NA’ response may be recorded which indicates that the question did not apply to the City during the return period. The audit and risk committee is required under section 14 (3A) of the Local Government (Audit) Regulations 1996 to review the compliance audit return and make recommendations to Council on any action required in response to the audit findings. The Council are required to adopt the CAR prior to the return being submitting to the department before the due date, 31 March 2017.

Minutes Attachments – Audit and Risk Management Committee 13 February 2018

Page 4

Peyton Consulting were again appointed as the independent consultant to undertake the 2017 CAR. FINANCIAL IMPLICATIONS

Nil LEGAL IMPLICATIONS

In accordance with section 7.13 (i) of the Local Government Act 1995 and regulations 13, 14 and 15 of the Local Government (Audit) Regulations 1996, local governments are required to carry out an audit of compliance for the period 1 January to 31 December in each year. After carrying out the compliance audit the local government is to prepare a compliance audit return in a form approved by the Minister. A compliance audit return is to be:

(a) Presented to the council at a meeting of the council; (b) Adopted by the council; and (c) Recorded in the minutes of the meeting of which it is adopted.

The return is to be signed by the Mayor and Chief Executive Officer and is to be submitted to the Department of Local Government, Sport and Cultural Industries by 31 March following the period to which the return relates. CONSULTATION

In order to provide an appropriate response to each question, the auditor consulted with a variety of officers within the City seeking information and evidence in relation to the questions asked in the Return. OFFICER COMMENT

In response to the 87 questions contained in the CAR, the auditor has examined the City’s documents and records relevant to these questions and recorded responses based on these findings. Two questions of non-compliance were recorded in the CAR, as detailed below: Question – Primary Returns Auditors findings Disclosure of Interest (Q5) – Was a primary return lodged by all newly designated employees within three months of their start day?

Five Primary Returns not submitted within 3 months of start date.

Officer response After further investigation of five late primary returns, it was ascertained that:

• one instance was due to an officer’s extended sick leave;

Minutes Attachments – Audit and Risk Management Committee 13 February 2018

Page 5

• one instance was an administrative error in the Attain system with the incorrect start date of the officer being entered into the system;

• the other instances involved officers with very heavy workloads and the failure to complete their primary returns was a simple oversight

Question – Primary Returns Auditors findings Disclosure of Interest (Q7) – Was an annual return lodged by all designated employees by 31 August 2017?

Three Annual Returns lodged after 31 August 2017.

The City’s 2017 CAR has recorded 2 non-compliance answers from a total of 87 questions. This represents a 2% non-compliance result, or 98% compliance achieved which is well above the City’s intended target of achieving at least 95% compliance with its legislative requirements. This is in comparison with: 96% compliance in 2013, 97.5%, in 2014, 95.4% in 2015, and 96.5% in 2016. The two areas of non-compliance were from the same section as the previous year. The high number of late submissions for Returns may be related to the large number of new employees who started in positions with delegated authority during 2017. This could be an indication that some employees require further training in their position responsibilities. The City acknowledges that process and procedural improvement is required to reduce the risk and address the matters that have been raised during the audit process and have taken steps to improve our processes and procedures as issues arise. VOTING AND OTHER SPECIAL REQUIREMENTS

Absolute Majority Required COMMITTEE AND OFFICER'S RECOMMENDATION

MOVED: Cr J McDonald That Council: 1. Receive the Compliance Audit Return (2017) Summary Report by Peyton

Consultancy, as shown in Attachment 1 of this agenda item. 2. Adopt the 2017 Compliance Audit Return as shown in Attachment 2 of this

agenda item, to be signed by the Mayor and CEO and submitted to the Department of Local Government and Communities before 31 March 2018.

CARRIED: 4/0

Minutes Attachments – Audit and Risk Management Committee 13 February 2018

Page 6

For Against Cr Doug Thompson Cr Jeff McDonald Cr Rachel Pemberton Mr Phillip Draber

ARMC1802-4 INTERNAL AUDIT REPORTS - PURCHASING, DELEGATION OF AUTHORITY AND INFORMATION/RECORDS MANAGEMENT

Meeting Date: 13 February 2018 Responsible Officer: Manager Governance Decision Making Authority: Council Agenda Attachments: Audit Report - Purchasing Authorisation

Audit Report - Delegation of Authority Audit Report - Information/Records Management

SUMMARY

To update the Audit and Risk Management Committee on the issues highlighted in the independent audit reports received from Paxon Group on 12 January 2018 regarding the City’s • Purchasing Authorisation; • Delegation of Authority; and • Information/Records Management processes A number of issues were noted in the audit reports as requiring attention and / or improvement as indicated in the attached Tables of Issues, Recommendations and Actions Taken. It is recommended that council: 1. Receive the internal audit report in relation to:

a. Purchasing Authorisation b. Delegation of Authority c. Information and Records Management.

2. Note recommendations and actions taken.

3. Require an update, on the completion of recommended actions, at the Audit and Risk Management Committee meeting held in August 2018, or at the next proceeding meeting if a meeting is not to be held in August.

Minutes Attachments – Audit and Risk Management Committee 13 February 2018

Page 7

BACKGROUND

In June 2016, the City appointed the Paxon Group Pty Ltd to undertake the City's internal audit services for a period of 3 years covering the 2016/2017, 2017/2018 and 2018/2019 Financial Years. At the Ordinary Meeting of Council held on 23 November 2016, Council approved the internal audit of the following business processes to be undertaken between 1 December 2016 and 30 March 2017: 1. Asset Management 2. Purchasing Authorisation 3. Delegation of Authority 4. Information/records management The Asset Management portion of the above-mentioned internal audits was completed in March 2017. An audit of the City’s Purchasing Authorisation, Delegation of Authority and Information/Records Management processes was undertaken by the appointed auditor (Paxon Group) in August 2017. The subsequent reports received on 12 January 2018 highlighted a number of fundamental areas requiring substantial improvement. The next stage of the City’s internal audit will cover the areas of: 1. Fraud and misconduct 2. Project management 3. Contract management 4. Procurement process Paxon Group will be meeting with relevant officers over the next few weeks to gather information required to complete the above-mentioned reports. FINANCIAL IMPLICATIONS

There are no financial implications identified as a result of this report. LEGAL IMPLICATIONS

Part 7 of the Local Government Act 1995 addresses the situation of audit in relation to the duties of the local government generally. Regulation 17 of the Local Government Act (Audit) Regulations 1996 requires the Chief Executive Officer to review the appropriateness and effectiveness of the local government’s systems and procedures in relation to: • risk management; and • internal control; and • legislative compliance.

Minutes Attachments – Audit and Risk Management Committee 13 February 2018

Page 8

CONSULTATION

No external consultation was undertaken.

Minutes Attachments – Audit and Risk Management Committee 13 February 2018

Page 9

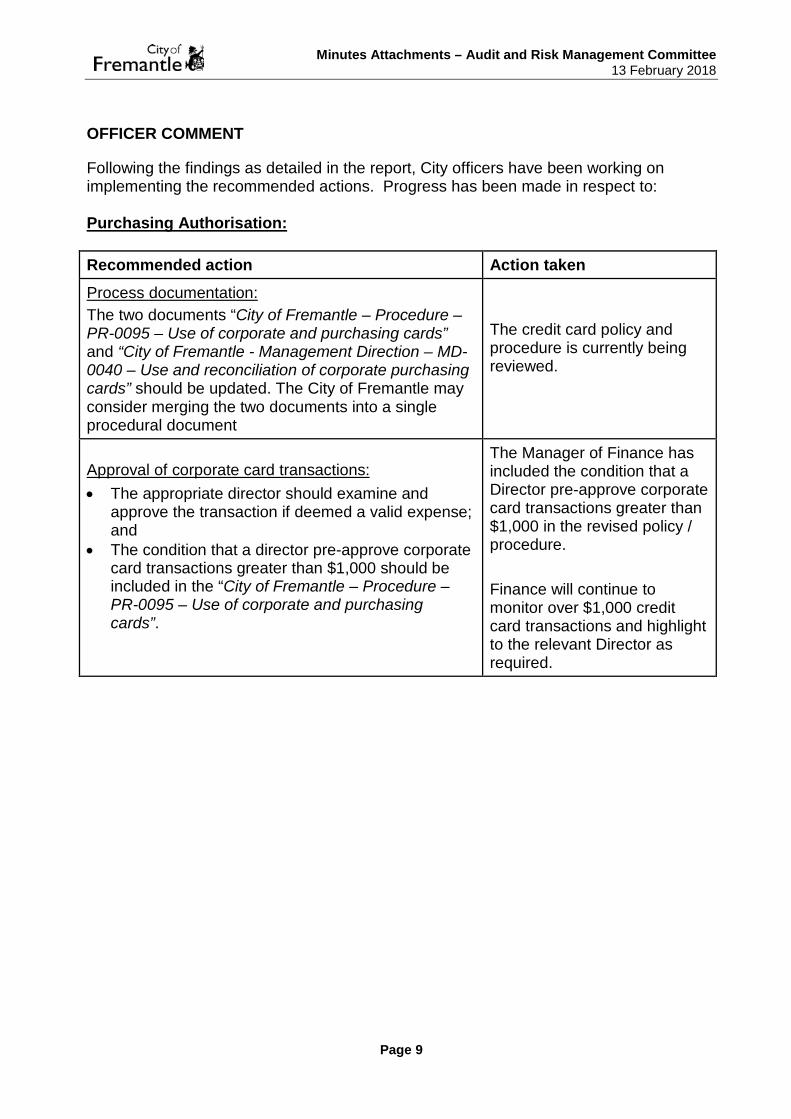

OFFICER COMMENT

Following the findings as detailed in the report, City officers have been working on implementing the recommended actions. Progress has been made in respect to: Purchasing Authorisation: Recommended action Action taken

Process documentation: The two documents “City of Fremantle – Procedure – PR-0095 – Use of corporate and purchasing cards” and “City of Fremantle - Management Direction – MD-0040 – Use and reconciliation of corporate purchasing cards” should be updated. The City of Fremantle may consider merging the two documents into a single procedural document

The credit card policy and procedure is currently being reviewed.

Approval of corporate card transactions: • The appropriate director should examine and

approve the transaction if deemed a valid expense; and

• The condition that a director pre-approve corporate card transactions greater than $1,000 should be included in the “City of Fremantle – Procedure – PR-0095 – Use of corporate and purchasing cards”.

The Manager of Finance has included the condition that a Director pre-approve corporate card transactions greater than $1,000 in the revised policy / procedure. Finance will continue to monitor over $1,000 credit card transactions and highlight to the relevant Director as required.

Minutes Attachments – Audit and Risk Management Committee 13 February 2018

Page 10

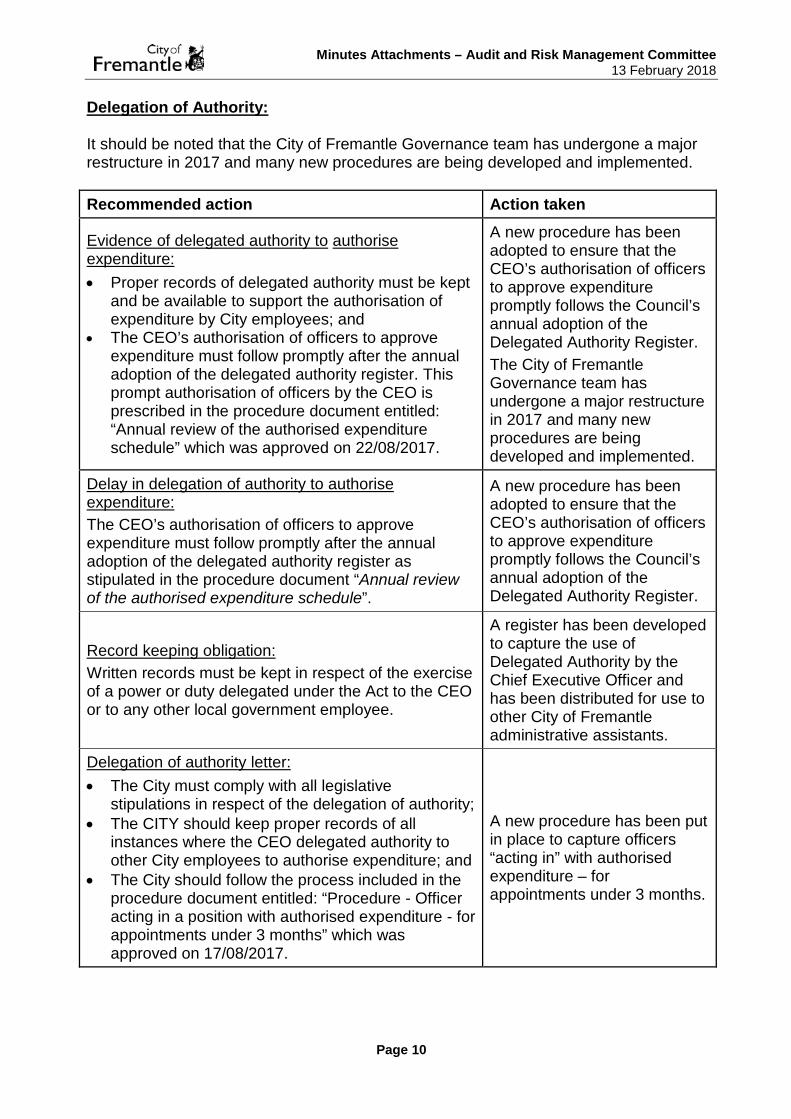

Delegation of Authority: It should be noted that the City of Fremantle Governance team has undergone a major restructure in 2017 and many new procedures are being developed and implemented. Recommended action Action taken

Evidence of delegated authority to authorise expenditure: • Proper records of delegated authority must be kept

and be available to support the authorisation of expenditure by City employees; and

• The CEO’s authorisation of officers to approve expenditure must follow promptly after the annual adoption of the delegated authority register. This prompt authorisation of officers by the CEO is prescribed in the procedure document entitled: “Annual review of the authorised expenditure schedule” which was approved on 22/08/2017.

A new procedure has been adopted to ensure that the CEO’s authorisation of officers to approve expenditure promptly follows the Council’s annual adoption of the Delegated Authority Register. The City of Fremantle Governance team has undergone a major restructure in 2017 and many new procedures are being developed and implemented.

Delay in delegation of authority to authorise expenditure: The CEO’s authorisation of officers to approve expenditure must follow promptly after the annual adoption of the delegated authority register as stipulated in the procedure document “Annual review of the authorised expenditure schedule”.

A new procedure has been adopted to ensure that the CEO’s authorisation of officers to approve expenditure promptly follows the Council’s annual adoption of the Delegated Authority Register.

Record keeping obligation: Written records must be kept in respect of the exercise of a power or duty delegated under the Act to the CEO or to any other local government employee.

A register has been developed to capture the use of Delegated Authority by the Chief Executive Officer and has been distributed for use to other City of Fremantle administrative assistants.

Delegation of authority letter: • The City must comply with all legislative

stipulations in respect of the delegation of authority; • The CITY should keep proper records of all

instances where the CEO delegated authority to other City employees to authorise expenditure; and

• The City should follow the process included in the procedure document entitled: “Procedure - Officer acting in a position with authorised expenditure - for appointments under 3 months” which was approved on 17/08/2017.

A new procedure has been put in place to capture officers “acting in” with authorised expenditure – for appointments under 3 months.

Minutes Attachments – Audit and Risk Management Committee 13 February 2018

Page 11

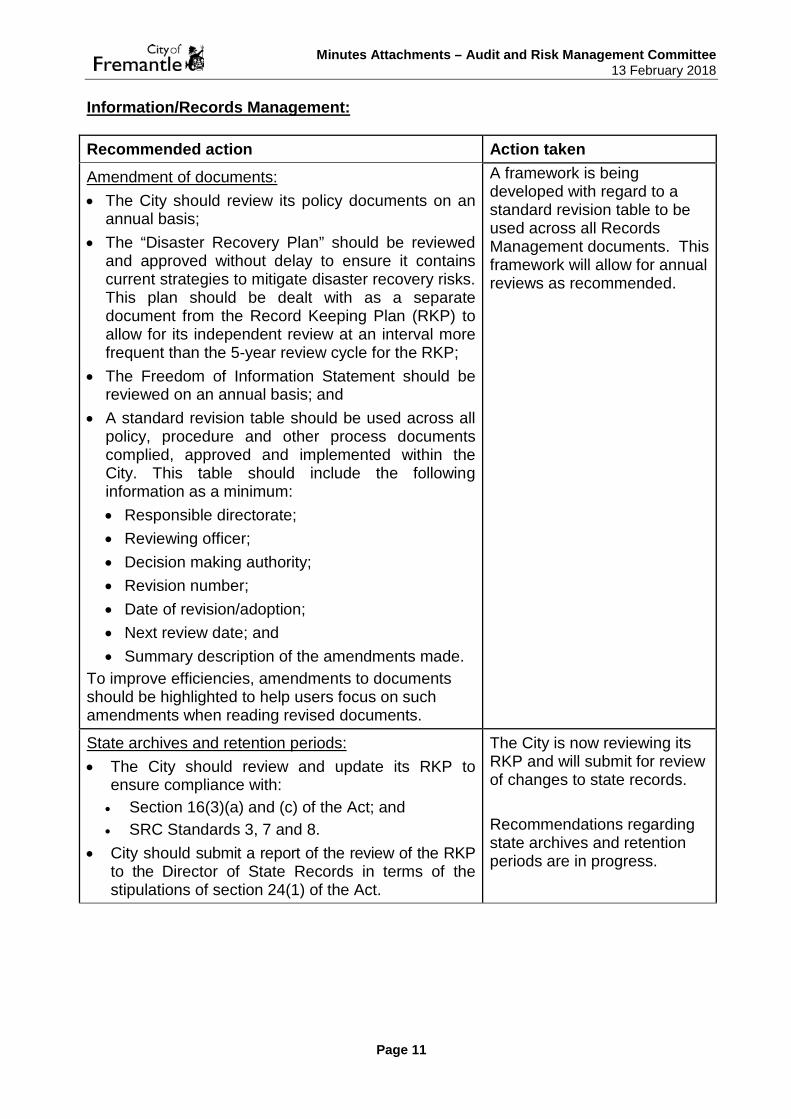

Information/Records Management: Recommended action Action taken

Amendment of documents: • The City should review its policy documents on an

annual basis; • The “Disaster Recovery Plan” should be reviewed

and approved without delay to ensure it contains current strategies to mitigate disaster recovery risks. This plan should be dealt with as a separate document from the Record Keeping Plan (RKP) to allow for its independent review at an interval more frequent than the 5-year review cycle for the RKP;

• The Freedom of Information Statement should be reviewed on an annual basis; and

• A standard revision table should be used across all policy, procedure and other process documents complied, approved and implemented within the City. This table should include the following information as a minimum: • Responsible directorate; • Reviewing officer; • Decision making authority; • Revision number; • Date of revision/adoption; • Next review date; and • Summary description of the amendments made.

To improve efficiencies, amendments to documents should be highlighted to help users focus on such amendments when reading revised documents.

A framework is being developed with regard to a standard revision table to be used across all Records Management documents. This framework will allow for annual reviews as recommended.

State archives and retention periods: • The City should review and update its RKP to

ensure compliance with: • Section 16(3)(a) and (c) of the Act; and • SRC Standards 3, 7 and 8.

• City should submit a report of the review of the RKP to the Director of State Records in terms of the stipulations of section 24(1) of the Act.

The City is now reviewing its RKP and will submit for review of changes to state records. Recommendations regarding state archives and retention periods are in progress.

Minutes Attachments – Audit and Risk Management Committee 13 February 2018

Page 12

Security and authentication controls: • The City should review and update its RKP to

ensure compliance with principle 3 in SRC 8; and • The City should submit a report of the review of the

RKP to the Director of State Records in terms of the stipulations of section 24(1) of the Act.

The City is now reviewing its RKP and will submit for review of changes to state records.

Employees’ responsibility to keep records: • The City should continue to enhance the record

keeping culture within the organisation to help ensure each individual employee takes ownership for record keeping; and

• The City should take steps to identify and manage instances where City employees did not register documents in ECM. These steps may include: o Comparison of the number of records registered

in ECM over a period of time by an employee against his/her job specification and expected output of documents;

o Compilation of a specific procedure to address instances found where records were not registered in ECM; and

o Compilation and implementation of a specific form which employees can use to report missing records.

Version control is used to look at updated documents in ECM as the updater may not be the same as the original person who registered the document. Staff are provided with compulsory training in the City’s Electronic Content Management system when they commence employment at the City or have been identified as not having received the training previously for any reason. The ECM system applies retention policies and securities on registered content in accordance with how the staff member classifies the content. Staff sign off on receiving training and confirming they understand their responsibilities in regards to records management. “Acknowledgement of records management policy and guidelines” declaration was developed on 2 August 2017 (Doc set ID 3349663).

General disposal authority for state records: • The City should implement a general disposal

authority for source records without delay.

The City are currently working with the state records department and internal stakeholders to create a general disposal authority for source records. This should be completed by June 2018.

Destruction of records: • The City should implement a general disposal

authority for source records without delay; and • The City should resolve the technical issue which

prevents it from destroying records.

The City is currently working with the state records department and internal stakeholders to create a general disposal authority for source records. This should be

Minutes Attachments – Audit and Risk Management Committee 13 February 2018

Page 13

completed by June 2018. The Information Technology manager has been made aware of the technical issue and is currently working to implement a solution. The existing document management system limitation has also been escalated to the software provider who are also investigating the matter.

Freedom of information applications: • The City should manage all applications for access

to information to ensure compliance with section 13(3) of the Freedom of Information Act 1992; and

• The City should keep proper records of all documentation received and all responses sent to applicants for access to information.

The City is aware of the permitted period of 45 days after the access application is received or such other period as is agreed between the agency and the applicant. The City has an officer in place to ensure compliance. The City’s FOI Coordinator is entrusted to keep proper records of all documentation and communications resulting from a request for information. The Information Management Team Leader will review the existing process and make improvements as required.

VOTING AND OTHER SPECIAL REQUIREMENTS

Simple Majority Required COMMITTEE AND OFFICER'S RECOMMENDATION

MOVED: Cr J McDonald Council: 1. Receive the internal audit report in relation to:

a. Purchasing Authorisation b. Delegation of Authority c. Information and Records Management.

2. Note recommendations and actions taken. 3. Require an update, on the completion of recommended actions, at the Audit

and Risk Management Committee meeting held in August 2018, or at the next proceeding meeting if a meeting is not to be held in August.

Minutes Attachments – Audit and Risk Management Committee 13 February 2018

Page 14

Minutes Attachments – Audit and Risk Management Committee 13 February 2018

Page 15

CARRIED: 4/0 For Against Cr Doug Thompson Cr Jeff McDonald Cr Rachel Pemberton Mr Phillip Draber

Minutes Attachments – Audit and Risk Management Committee 13 February 2018

Page 16

ARMC1802-2 INVESTIGATION OF BEST PRACTICE PROCUREMENT OF ARTISTS

IN THE LOCAL GOVERNMENT SECTOR Meeting Date: 13 February 2018 Responsible Officer: Manager Finance Decision Making Authority: Council Agenda Attachments: Nil SUMMARY

At the Audit and Risk Management Committee meeting of 5 December 2017, the city reported the total value of exemptions used in October and November 2017, for artists, was $293,348. At the meeting the committee recommended that: Council 1. receive the purchasing policy exemptions information report for October and November 2017. 2. request the investigation of best practise initiatives within the Local government industry in relation to the procurement of artistic services. This report summarises the approach of other local governments to the procurement of artistic services and recommends that Council agrees to the city’s recommendation to implement a procedure that clearly defines the term ‘artist’ for the purposes of the city’s purchasing policy. BACKGROUND

At the Ordinary Council Meeting of 27 September 2017, Council adopted a new purchasing policy. The policy contains a list of tender exemptions (exempt under Regulation 11(2) of the Local Government (Functions and General) Regulations 1996) and policy exemptions. The policy states: ‘The following purchasing decisions are exempt from the purchasing thresholds of the policy:

……Acts / Entertainers / Artists for festivals and events where it can be demonstrated that the act has appropriate artistic merit and the decision is consistent with the purpose and intent of the event and have no conflicts of interest, up to a value of $9,999. The decision is to be approved by the relevant Director……”

Minutes Attachments – Audit and Risk Management Committee 13 February 2018

Page 17

FINANCIAL IMPLICATIONS

Nil. LEGAL IMPLICATIONS

The city, when procuring goods and services, is required to follow it’s Purchasing policy and the Local Government (Functions and General) Regulations 1996, Divisions 1, 2 and 3, Regulations 11A to 24AJ. CONSULTATION

The Senior Contracts and Procurement Officer discussed the procurement of artists with officers at the:

• City of Perth, • City of South Perth, • City of Albany and • City of Cockburn.

The Senior Contracts and Procurement Officer also reviewed the purchasing policies of the Cities of:

• Canning, • Joondalup, • Stirling, • Kwinana and • Rockingham.

OFFICER COMMENT

As part of the review into the use of Artist Exemptions under the policy, the City approached a number of local governments, to understand how members of the sector procure the services of Artists. Most purchasing policies reviewed, within the sector; do not have explicit exemptions for purchases, except for those purchases handled as tender exemptions under Regulation 11. All purchasing policies reviewed have a requirement for one, two or three quotes depending upon the value of the purchase. Most of the City’s reviewed or contacted, required the procurement of artists to abide by the city’s purchasing policy. A number of the local government purchasing policies reviewed had higher purchasing thresholds, before more than one quotes was required. However, most policies also recognised that some markets are difficult to achieve two or more quotes, for example events and artists. In this case all the policies had some flexibility for the purchase to be granted an exemption to the requirement of the relevant purchasing policy by requiring Officers to request Manager or Director Approval, which

Minutes Attachments – Audit and Risk Management Committee 13 February 2018

Page 18

included a written recommendation from an Officer to accept a quote and written managerial or Director Approval for an exemption to policy. No other local government policy reviewed, required the use of exemptions to be reported to the local government’s Audit Committee. In conclusion none of the local governments reviewed had specific artist exemptions from their purchasing policy. However, the majority procured artists whereby a purchase could be exempted from the purchasing policy thresholds by written Director or Manager Approval. To move the discussion forwards, the city intends to define the term artist more closely. By defining the term artist, generic artistic services, such as face painting, MC, DJ’s are removed from the exemption to policy, thereby reducing the value of exemptions. However, it should be recognised that some artistic performers offer specific artistic merit, theme, outcome or drawcard to city festivals and events. The timing of artist procurement will relate to current popularity therefore increasing the draw to a city organised event and potentially the cost of exemption. VOTING AND OTHER SPECIAL REQUIREMENTS

Simple Majority Required COMMITTEE AND OFFICER'S RECOMMENDATION

MOVED: Cr J McDonald Council request the Chief Executive Officer develop a procedure, defining the term ‘acts / entertainers / artist’ to be used alongside the city’s purchasing policy. CARRIED: 4/0 For Against Cr Doug Thompson Cr Jeff McDonald Cr Rachel Pemberton Mr Phillip Draber

Minutes Attachments – Audit and Risk Management Committee 13 February 2018

Page 19

ARMC1802-3 OVERDUE DEBTORS REPORT AS AT 31 DECEMBER 2017 Meeting Date: 13 February 2018 Responsible Officer: Finance Manager Decision Making Authority: Council Agenda Attachments: Summary of Overdue Debts above Threshold

(Confidential) SUMMARY

This report with a confidential attachment is provided to the Audit and Risk Management Committee with details of overdue debts that exceed a threshold value of $10,000. This report recommends that Council note $222,751.42 of overdue debts that were overdue in excess of ninety (90) days and the combined value those debt(s) exceed $10,000 as at 31 December 2017. BACKGROUND

The report is part of a framework for the write off of bad debts that was endorsed by the Audit and Risk Management Committee on 16 December 2014 and referred to Council who endorsed the framework on 28 January 2015 on how it handles the write off of bad and doubtful debts:- a. That bi-annually (September and March) a report with a confidential attachment in an

agreed format is submitted to the Strategic and General Service's committee (current Finance, Policy, Operations and Legislation Committee) to receive under delegated details of overdue debts that exceed a threshold value.

b. That the threshold value for items to be reported for each debtor are debts overdue in excess of ninety (90) days and the combined value those debt(s) exceed $10,000. Rates debtors that remain a charge against the property are excluded from the requirement to report.

c. Two months after (i.e., November and May) the report in (a) has been submitted an item be submitted to Council via Strategic and General Services for approval to write off those debts that are considered bad or doubtful.

d. That once a recommendation is received from Department of Attorney General to write off monies referred to the Fines Enforcement Registry (FER) then an item is submitted to council within two months of the receipt of the recommendation.

FINANCIAL IMPLICATIONS

Cost of Credit Management: If an organisation does not have good credit management then it will have negative budgetary impacts as cash will not be collected for the sales of goods and services made.

Minutes Attachments – Audit and Risk Management Committee 13 February 2018

Page 20

It should be noted that even with good credit management, bad debts can still be incurred, but they normally arise within an environment where the risk and reward factors have been balanced to try and achieve the best outcome for the organisation. It is a requirement for completing annual financial statements that any potential bad debts are provisioned for and that is a cost to the budget in the year in which the provision is made. LEGAL IMPLICATIONS

Section 6.12 (1) (c) of the Local Government Act 1995 provides authority for the Council to write off outstanding monies. In accordance with section 5.42 and 5.44 of the Local Government Act 1995 the following delegated authority applies:

• The Chief Executive Officer has delegated authority to write off debts (not including rates or infringement) considered unrecoverable up to $20,000 per account where in the opinion of the Chief Executive Officer all other reasonable avenues of recovery have been exhausted.

• Directors and Managers have various sub-delegated authority to write off debts (not including rates or infringement) considered unrecoverable up to $10,000 per account where in the opinion of the Director or Manager all other reasonable avenues of recovery have been exhausted.

All records of the uses of this delegated authority must be reported to the audit and risk management committee. Any amount in excess of $20,000 is to be written off by Council resolution. A council resolution authorising the write off of any bad debt does not prevent Council from reinstating the debt if the future circumstances change and the debt becomes collectable. CONSULTATION

Nil OFFICER COMMENT

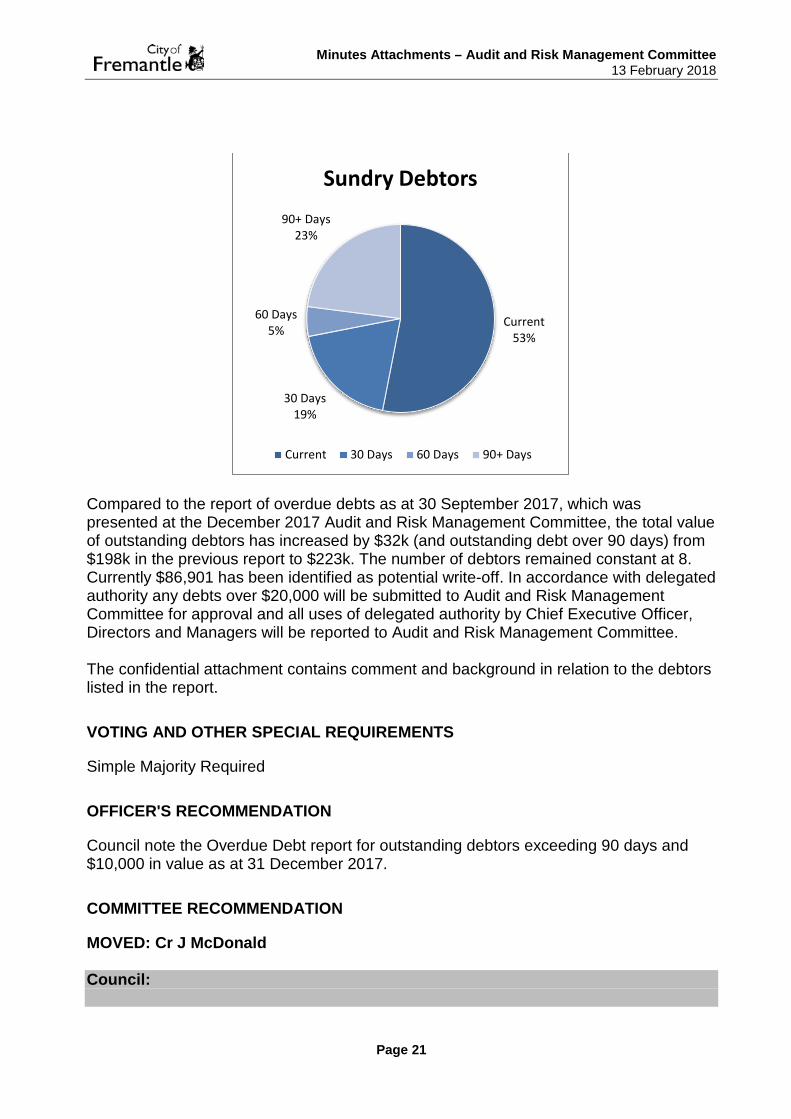

The amount of total debtors outstanding as at 31 December 2017 was $981,089. A breakdown of aged debt for the current period compared to prior year for the same period is tabled below. Period Ending Current 30 Days 60 Days 90+ Days Total December 2017 - Current 524,216 184,028 43,763 229,082 981,089 December 2016 - Prior 528,447 153,162 38,881 156,648 877,138

Of the total debt balance the amount outstanding for 90+ days is $229,082 or 23%.

Minutes Attachments – Audit and Risk Management Committee 13 February 2018

Page 21

Compared to the report of overdue debts as at 30 September 2017, which was presented at the December 2017 Audit and Risk Management Committee, the total value of outstanding debtors has increased by $32k (and outstanding debt over 90 days) from $198k in the previous report to $223k. The number of debtors remained constant at 8. Currently $86,901 has been identified as potential write-off. In accordance with delegated authority any debts over $20,000 will be submitted to Audit and Risk Management Committee for approval and all uses of delegated authority by Chief Executive Officer, Directors and Managers will be reported to Audit and Risk Management Committee. The confidential attachment contains comment and background in relation to the debtors listed in the report. VOTING AND OTHER SPECIAL REQUIREMENTS

Simple Majority Required OFFICER'S RECOMMENDATION

Council note the Overdue Debt report for outstanding debtors exceeding 90 days and $10,000 in value as at 31 December 2017. COMMITTEE RECOMMENDATION

MOVED: Cr J McDonald Council:

Current 53%

30 Days 19%

60 Days 5%

90+ Days 23%

Sundry Debtors

Current 30 Days 60 Days 90+ Days

Minutes Attachments – Audit and Risk Management Committee 13 February 2018

Page 22

1. Note the Overdue Debt report for outstanding debtors exceeding 90 days and $10,000 in value as at 31 December 2017.

2. Seek a report providing options for a process to reduce overdue debts to be

bought back to the audit and risk management committee for consideration. CARRIED: 4/0 For Against Cr Doug Thompson Cr Jeff McDonald Cr Rachel Pemberton Mr Phillip Draber

Minutes Attachments – Audit and Risk Management Committee 13 February 2018

Page 23

ARMC1802-5 AUDIT AND RISK UPDATE FOR ASSETS Meeting Date: 13 February 2018 Responsible Officer: Manager Asset Management Decision Making Authority: Council Agenda Attachments: Nil SUMMARY

The purpose of this report is to update the Audit and Risk Committee on the City’s progress in addressing the issues highlighted in the independent audit report received in March 2017, regarding the City’s Corporate Asset Management Planning. This report recommends that Council The purpose of this report is to update the Audit and Risk Committee on the City’s progress in addressing the issues highlighted in the independent audit report received in March 2017, regarding the City’s Corporate Asset Management Planning. This report recommends that Council receive the update in relation to the City’s current position and progress. BACKGROUND

The City is committed to improving the quality and extent of its asset management information. Officers are progressing a number of initiatives that were identified as requiring improvement through an extended audit report (received March 2017). Officers have committed to an update program that will run through the course of the 2017/18 financial year. Officers have committed to provide regular updates by way of report to the Audit and Risk committee. FINANCIAL IMPLICATIONS

Budget provision is included the 2017/18 budget to carry out the asset assessments / audit program. LEGAL IMPLICATIONS

Regulation 17 of the Local Government Act (Audit) Regulations 1996 requires the Chief Executive Officer to review the appropriateness and effectiveness of the local government’s systems and procedures in relation to —

• Risk management. • Internal control.

Minutes Attachments – Audit and Risk Management Committee 13 February 2018

Page 24

• Legislative compliance. CONSULTATION

Nil OFFICER COMMENT

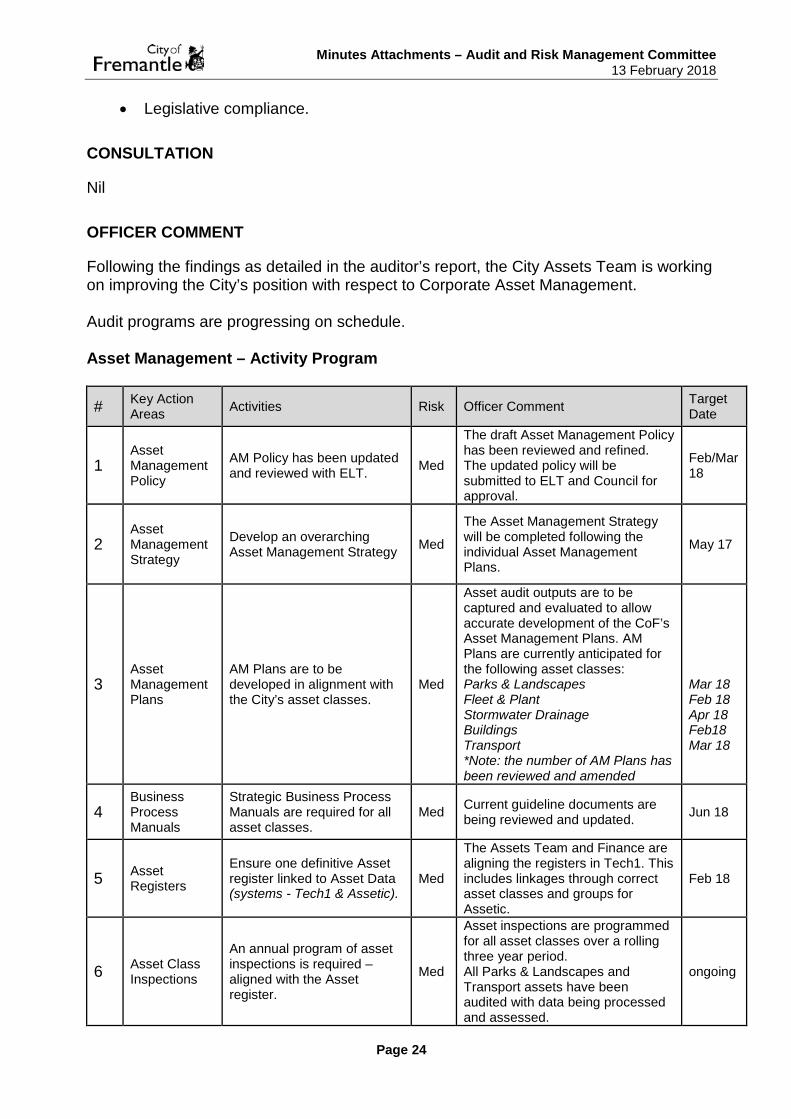

Following the findings as detailed in the auditor’s report, the City Assets Team is working on improving the City’s position with respect to Corporate Asset Management. Audit programs are progressing on schedule. Asset Management – Activity Program

# Key Action Areas Activities Risk Officer Comment Target

Date

1 Asset Management Policy

AM Policy has been updated and reviewed with ELT. Med

The draft Asset Management Policy has been reviewed and refined. The updated policy will be submitted to ELT and Council for approval.

Feb/Mar 18

2 Asset Management Strategy

Develop an overarching Asset Management Strategy Med

The Asset Management Strategy will be completed following the individual Asset Management Plans.

May 17

3 Asset Management Plans

AM Plans are to be developed in alignment with the City’s asset classes.

Med

Asset audit outputs are to be captured and evaluated to allow accurate development of the CoF’s Asset Management Plans. AM Plans are currently anticipated for the following asset classes: Parks & Landscapes Fleet & Plant Stormwater Drainage Buildings Transport *Note: the number of AM Plans has been reviewed and amended

Mar 18 Feb 18 Apr 18 Feb18 Mar 18

4 Business Process Manuals

Strategic Business Process Manuals are required for all asset classes.

Med Current guideline documents are being reviewed and updated. Jun 18

5 Asset Registers

Ensure one definitive Asset register linked to Asset Data (systems - Tech1 & Assetic).

Med

The Assets Team and Finance are aligning the registers in Tech1. This includes linkages through correct asset classes and groups for Assetic.

Feb 18

6 Asset Class Inspections

An annual program of asset inspections is required – aligned with the Asset register.

Med

Asset inspections are programmed for all asset classes over a rolling three year period. All Parks & Landscapes and Transport assets have been audited with data being processed and assessed.

ongoing

Minutes Attachments – Audit and Risk Management Committee 13 February 2018

Page 25

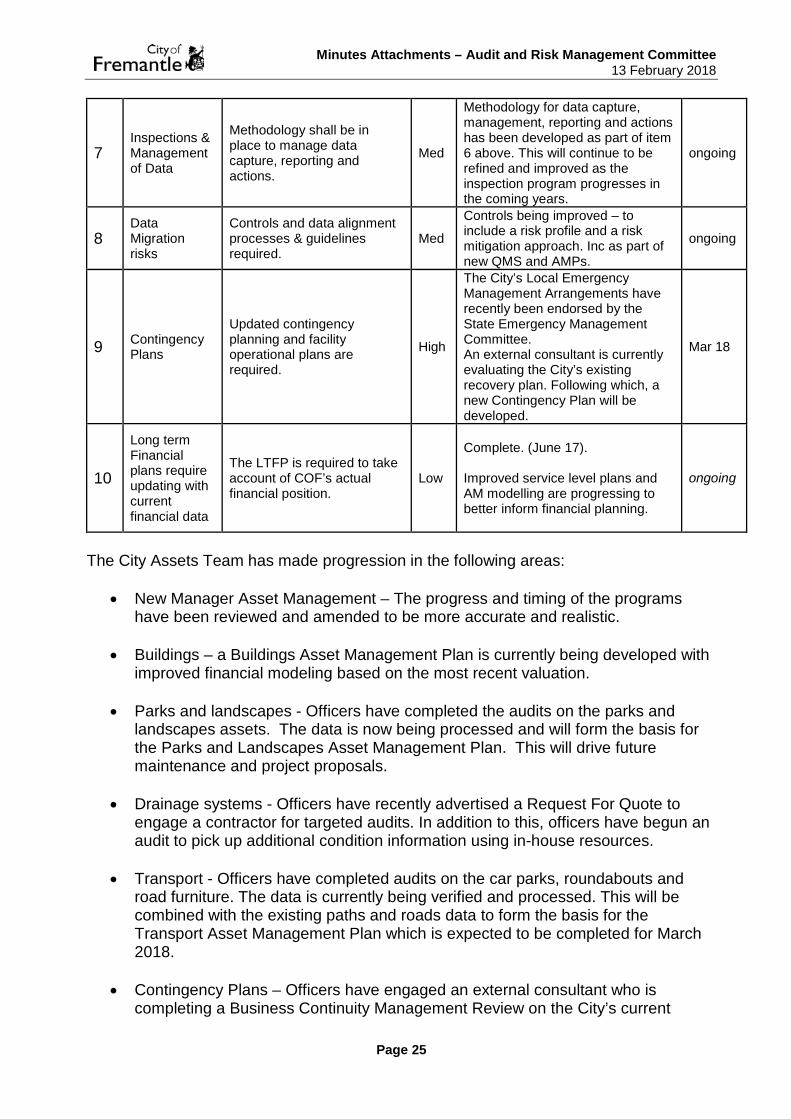

7 Inspections & Management of Data

Methodology shall be in place to manage data capture, reporting and actions.

Med

Methodology for data capture, management, reporting and actions has been developed as part of item 6 above. This will continue to be refined and improved as the inspection program progresses in the coming years.

ongoing

8 Data Migration risks

Controls and data alignment processes & guidelines required.

Med

Controls being improved – to include a risk profile and a risk mitigation approach. Inc as part of new QMS and AMPs.

ongoing

9 Contingency Plans

Updated contingency planning and facility operational plans are required.

High

The City’s Local Emergency Management Arrangements have recently been endorsed by the State Emergency Management Committee. An external consultant is currently evaluating the City’s existing recovery plan. Following which, a new Contingency Plan will be developed.

Mar 18

10

Long term Financial plans require updating with current financial data

The LTFP is required to take account of COF’s actual financial position.

Low

Complete. (June 17). Improved service level plans and AM modelling are progressing to better inform financial planning.

ongoing

The City Assets Team has made progression in the following areas:

• New Manager Asset Management – The progress and timing of the programs have been reviewed and amended to be more accurate and realistic.

• Buildings – a Buildings Asset Management Plan is currently being developed with improved financial modeling based on the most recent valuation.

• Parks and landscapes - Officers have completed the audits on the parks and landscapes assets. The data is now being processed and will form the basis for the Parks and Landscapes Asset Management Plan. This will drive future maintenance and project proposals.

• Drainage systems - Officers have recently advertised a Request For Quote to

engage a contractor for targeted audits. In addition to this, officers have begun an audit to pick up additional condition information using in-house resources.

• Transport - Officers have completed audits on the car parks, roundabouts and

road furniture. The data is currently being verified and processed. This will be combined with the existing paths and roads data to form the basis for the Transport Asset Management Plan which is expected to be completed for March 2018.

• Contingency Plans – Officers have engaged an external consultant who is

completing a Business Continuity Management Review on the City’s current

Minutes Attachments – Audit and Risk Management Committee 13 February 2018

Page 26

recovery plans and processes. The consultant will provide feedback with recommendations and improvements aligned with ISO 22301:2012 Societal Security. Following the review, a new Contingency Plan will be produced in consultation with stakeholders.

VOTING AND OTHER SPECIAL REQUIREMENTS

Simple Majority Required COMMITTEE AND OFFICER'S RECOMMENDATION

MOVED: Cr J McDonald Council receive the Officer’s update summary with respect to the City’s Asset Management program of activity, as contained within this report. CARRIED: 4/0 For Against Cr Doug Thompson Cr Jeff McDonald Cr Rachel Pemberton Mr Phillip Draber

Minutes Attachments – Audit and Risk Management Committee 13 February 2018

Page 27

ARMC1802-6 INFORMATION REPORT - OFFICE OF THE AUDITOR GENERAL

PROCUREMENT PERFORMANCE AUDIT Meeting Date: 13 February 2018 Responsible Officer: Senior Contracts and Procurement Officer Decision Making Authority: Council Agenda Attachments: NIL BACKGROUND

The Local Government Amendment (Auditing) Act 2017 makes legislative changes to the Local Government Act 1995 to provide for the auditing of local governments by the Auditor General of WA (AG). The Act allows the AG to contract out some or all of the financial audits, but all audits will be the responsibility of the AG and Office of the Auditor General (OAG). The Act also allows for performance audits, which will examine the economy, efficiency and effectiveness of any aspect of local government operations. The first performance audit in local government, undertaken by the OAG focuses on procurement. The objective of this audit is to determine whether local governments have effective procurement arrangements in place. Questions asked by the OAG of local governments include, but are not limited to:

1. Do LGs have established policies and procedures for procurement of goods and services?

2. Is there effective oversight and control of procurement activities? The AG is currently auditing 3 areas of local government operations:

1. Local Government Procurement 2. Timely payment of suppliers 3. Controls over corporate credit cards

Commencement of Audit In December 2017, the OAG informed the city of its involvement in the first round of procurement performance audits. The city is one of 6 local governments being audited in this round. To date the city has provided the following information to the OAG for the audit:

• The City’s Procurement (Purchasing) Policy, including any procedures that sit underneath it

• Templates for procurement activities • Codes of Conduct

Minutes Attachments – Audit and Risk Management Committee 13 February 2018

Page 28

• Organisational structure, including where the procurement function sits, size of team, roles etc

• Outline of any procurement training • Transactional data for all purchases made in the 2016 / 2017 financial year • Trial Balance as at 30 June 2017

The full audit is expected to take place in February 2018. Information on the results of the procurement performance audit is (according to the OAG website) anticipated in the second quarter of 2018. COMMITTEE AND OFFICER'S RECOMMENDATION

MOVED: Cr J McDonald Council receive the Office of the Auditor General procurement performance audit, information report. CARRIED: 4/0 For Against Cr Doug Thompson Cr Jeff McDonald Cr Rachel Pemberton Mr Phillip Draber

Minutes Attachments – Audit and Risk Management Committee 13 February 2018

Page 29

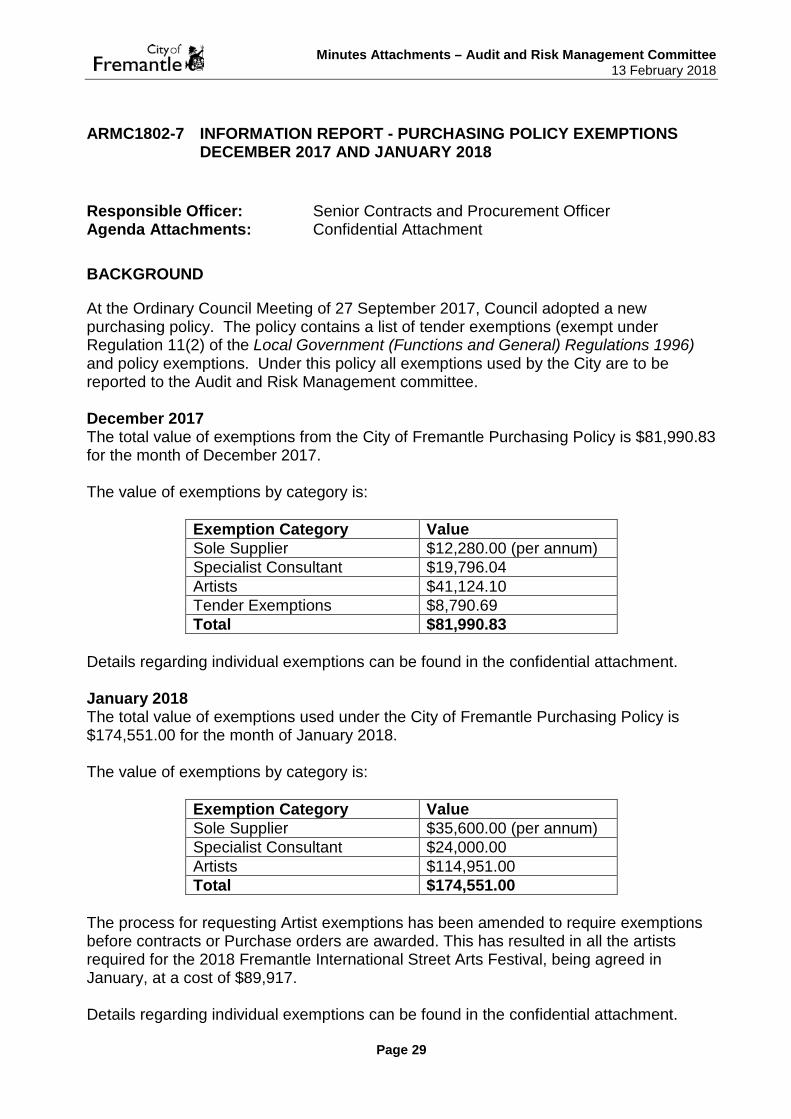

ARMC1802-7 INFORMATION REPORT - PURCHASING POLICY EXEMPTIONS

DECEMBER 2017 AND JANUARY 2018 Responsible Officer: Senior Contracts and Procurement Officer Agenda Attachments: Confidential Attachment BACKGROUND

At the Ordinary Council Meeting of 27 September 2017, Council adopted a new purchasing policy. The policy contains a list of tender exemptions (exempt under Regulation 11(2) of the Local Government (Functions and General) Regulations 1996) and policy exemptions. Under this policy all exemptions used by the City are to be reported to the Audit and Risk Management committee. December 2017 The total value of exemptions from the City of Fremantle Purchasing Policy is $81,990.83 for the month of December 2017. The value of exemptions by category is:

Exemption Category Value Sole Supplier $12,280.00 (per annum) Specialist Consultant $19,796.04 Artists $41,124.10 Tender Exemptions $8,790.69 Total $81,990.83

Details regarding individual exemptions can be found in the confidential attachment. January 2018 The total value of exemptions used under the City of Fremantle Purchasing Policy is $174,551.00 for the month of January 2018. The value of exemptions by category is:

Exemption Category Value Sole Supplier $35,600.00 (per annum) Specialist Consultant $24,000.00 Artists $114,951.00 Total $174,551.00

The process for requesting Artist exemptions has been amended to require exemptions before contracts or Purchase orders are awarded. This has resulted in all the artists required for the 2018 Fremantle International Street Arts Festival, being agreed in January, at a cost of $89,917. Details regarding individual exemptions can be found in the confidential attachment.

Minutes Attachments – Audit and Risk Management Committee 13 February 2018

Page 30

COMMITTEE AND OFFICER'S RECOMMENDATION

MOVED: Cr J McDonald Council receive the purchasing policy exemptions information report for December 2017 and January 2018. CARRIED: 4/0 For Against Cr Doug Thompson Cr Jeff McDonald Cr Rachel Pemberton Mr Phillip Draber

Minutes Attachments – Audit and Risk Management Committee 13 February 2018

Page 31

ARMC1802-8 INFORMATION REPORT - FINANCIAL MANAGEMENT REVIEW 2017

PROGRESS ON ACTIONS Meeting Date: 13 February 2018 Responsible Officer: Manager Finance Decision Making Authority: Council Agenda Attachments: Nil SUMMARY

City of Fremantle engaged Moore Stephens to undertake a review of the appropriateness and effectiveness of the financial management systems and procedures in accordance with Regulations 5(2)(c) of the Local Government (Financial Management) Regulations 1996. The City received the Financial Management Review dated March 2017 on 11 September 2017 and this was reviewed at the Audit and Risk Management Committee meeting of 5 December 2017. The purpose of this report is to update the Audit and Risk Committee on the City’s progress in addressing the issues highlighted in the Financial Management Review. This report recommends that Council receive the update in relation to the City’s current position and progress. BACKGROUND

Regulations 5(2)(c) of the Local Government (Financial Management) Regulations 1996 requires the Chief Executive Officer to undertake reviews of the appropriateness and effectiveness of the financial management systems and procedures of the local government regularly and report to the local government the results of those reviews. The City is committed to improving its financial processes by implementing the recommendations in the report. Officers have committed to provide regular updates by way of report to the Audit and Risk Management Committee. FINANCIAL IMPLICATIONS

There is no direct financial implication with the requirement for this report.

Minutes Attachments – Audit and Risk Management Committee 13 February 2018

Page 32

LEGAL IMPLICATIONS

Local Government (Financial Management) Regulations 1996 The financial management responsibilities of the Chief Executive Officer are established under Regulation 5 of the Local Government (Financial Management) Regulations 1996: “(1) Efficient systems and procedures are to be established by the CEO of a local government:

(a) for the proper collection of all money owing to the local government; (b) for the safe custody and security of all money collected or held by the local government; (c) for the proper maintenance and security of the financial records of the local government (whether maintained in written form or by electronic or other means or process); (d) to ensure proper accounting for municipal or trust:

(i) revenue received or receivable; (ii) expenses paid or payable; and (iii) assets and liabilities;

(e) to ensure proper authorisation for the incurring of liabilities and the making of payments; (f) for the maintenance of payroll, stock control and costing records; and

(g) to assist in the preparation of budgets, budget reviews, accounts and reports Required by the Act or these Regulations.”

In addition, the Chief Executive Officer is to: “(2) (a) ensure that the resources of the local government are effectively and efficiently

managed; (b) assist the council to undertake reviews of fees and charges regularly (and not less not less than once in every financial year); and (c) undertake reviews of the appropriateness and effectiveness of the financial management systems and procedures of the local government regularly (and no less than once in every 4 financial years) and report to the local government the results of those reviews.”

CONSULTATION

Moore Stephens (appointed as City of Fremantle auditors). OFFICER COMMENT

The following is a summary of the key matters noted for improvement by the independent reviewer. Management have included comments in response and provide details of actions taken to date.

Minutes Attachments – Audit and Risk Management Committee 13 February 2018

Page 33

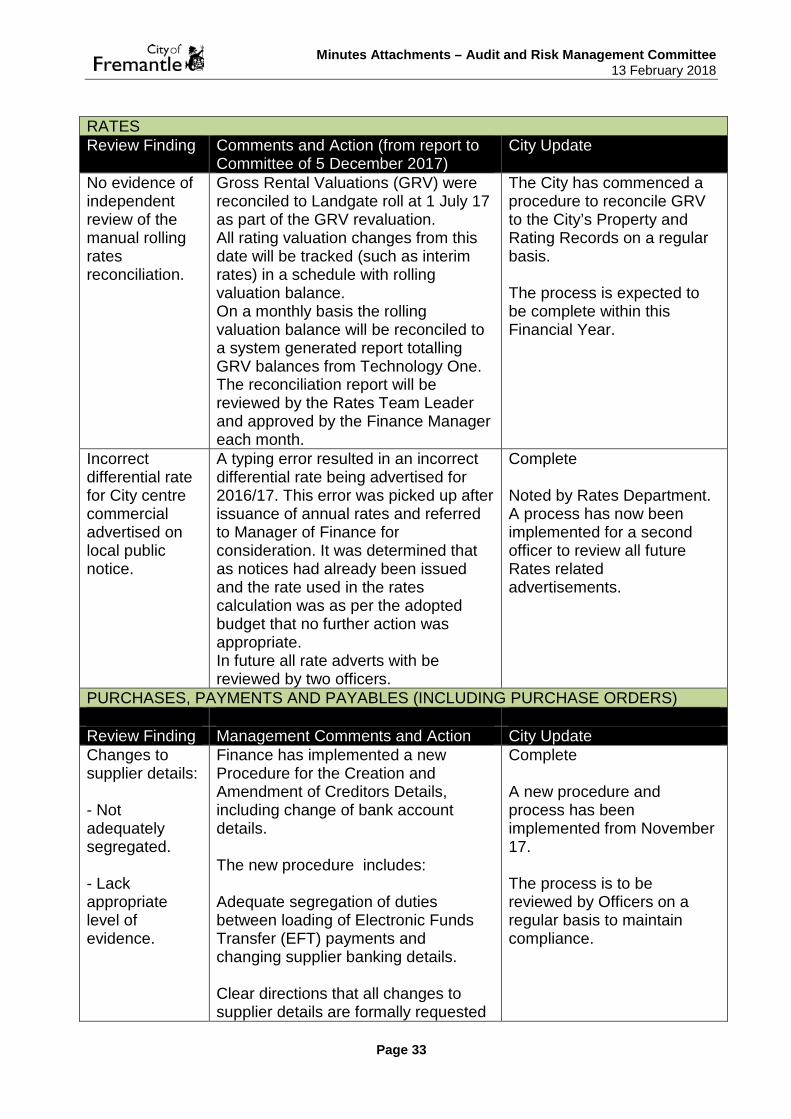

RATES Review Finding Comments and Action (from report to

Committee of 5 December 2017) City Update

No evidence of independent review of the manual rolling rates reconciliation.

Gross Rental Valuations (GRV) were reconciled to Landgate roll at 1 July 17 as part of the GRV revaluation. All rating valuation changes from this date will be tracked (such as interim rates) in a schedule with rolling valuation balance. On a monthly basis the rolling valuation balance will be reconciled to a system generated report totalling GRV balances from Technology One. The reconciliation report will be reviewed by the Rates Team Leader and approved by the Finance Manager each month.

The City has commenced a procedure to reconcile GRV to the City’s Property and Rating Records on a regular basis. The process is expected to be complete within this Financial Year.

Incorrect differential rate for City centre commercial advertised on local public notice.

A typing error resulted in an incorrect differential rate being advertised for 2016/17. This error was picked up after issuance of annual rates and referred to Manager of Finance for consideration. It was determined that as notices had already been issued and the rate used in the rates calculation was as per the adopted budget that no further action was appropriate. In future all rate adverts with be reviewed by two officers.

Complete Noted by Rates Department. A process has now been implemented for a second officer to review all future Rates related advertisements.

PURCHASES, PAYMENTS AND PAYABLES (INCLUDING PURCHASE ORDERS) Review Finding Management Comments and Action City Update Changes to supplier details: - Not adequately segregated. - Lack appropriate level of evidence.

Finance has implemented a new Procedure for the Creation and Amendment of Creditors Details, including change of bank account details. The new procedure includes: Adequate segregation of duties between loading of Electronic Funds Transfer (EFT) payments and changing supplier banking details. Clear directions that all changes to supplier details are formally requested

Complete A new procedure and process has been implemented from November 17. The process is to be reviewed by Officers on a regular basis to maintain compliance.

Minutes Attachments – Audit and Risk Management Committee 13 February 2018

Page 34

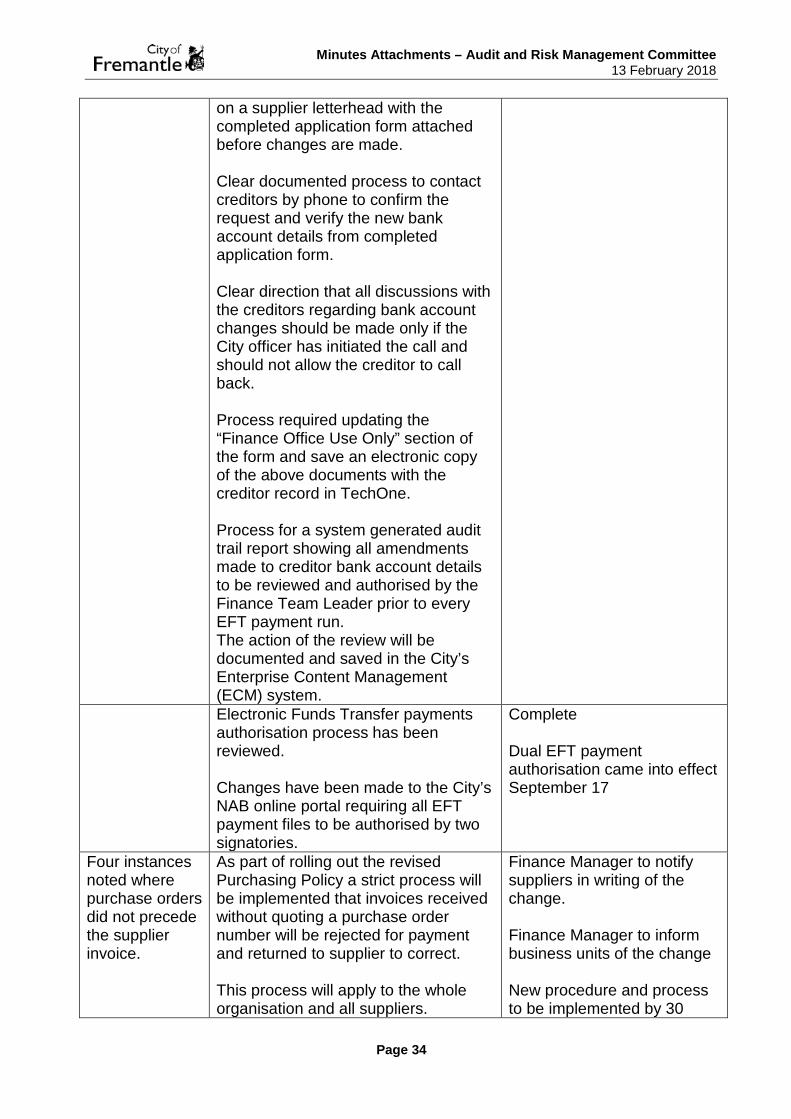

on a supplier letterhead with the completed application form attached before changes are made. Clear documented process to contact creditors by phone to confirm the request and verify the new bank account details from completed application form. Clear direction that all discussions with the creditors regarding bank account changes should be made only if the City officer has initiated the call and should not allow the creditor to call back. Process required updating the “Finance Office Use Only” section of the form and save an electronic copy of the above documents with the creditor record in TechOne. Process for a system generated audit trail report showing all amendments made to creditor bank account details to be reviewed and authorised by the Finance Team Leader prior to every EFT payment run. The action of the review will be documented and saved in the City’s Enterprise Content Management (ECM) system.

Electronic Funds Transfer payments authorisation process has been reviewed. Changes have been made to the City’s NAB online portal requiring all EFT payment files to be authorised by two signatories.

Complete Dual EFT payment authorisation came into effect September 17

Four instances noted where purchase orders did not precede the supplier invoice.

As part of rolling out the revised Purchasing Policy a strict process will be implemented that invoices received without quoting a purchase order number will be rejected for payment and returned to supplier to correct. This process will apply to the whole organisation and all suppliers.

Finance Manager to notify suppliers in writing of the change. Finance Manager to inform business units of the change New procedure and process to be implemented by 30

Minutes Attachments – Audit and Risk Management Committee 13 February 2018

Page 35

Business units and suppliers will be notified of this change in process. Request for an invoice to quote a purchase order number will ensure orders are raised prior to the time of authorising works/services or ordering goods.

June 18

SALARIES AND WAGES Review Finding Management Comments and Action City Update No monthly payroll reconciliation was performed.

A new payroll reconciliation process will be established to prepare a system generated monthly reconciliation payroll report to the general ledger. The reconciliation report will be reviewed by the Senior Payroll Officer and approved by the Finance Manager each month. The action of review will be documented and saved in the City’s Enterprise Content Management (ECM) system

Payroll and Finance Team has implemented a new report to Managers to review year to date payroll expense and payroll payments. The reconciliation of payroll report to general ledger report has commenced and is expected to be completed for 30 June 2018.

CREDIT CARD Review Finding Management Comments and Action City Update The credit card policy is outdated and inconsistent with current procedures in place.

The credit card policy is out of date due to change of system used for processing credit card transactions (from Flexi Purchase to Purchasing Card Module in TechOne.) The current “Use and reconciliation of corporate purchasing cards” administration policy will be reviewed and updated to reflect the change of system and practice.

Finance Manager to submit a draft revised policy to the Executive Leadership Team meeting for comment and approval. Revised policy to be submitted and approved by 30 June 18

COST AND ADMINISTRATION OVERHEAD ALLOCATIONS Review Finding Management Comments and Action City Update No evidence of review of internal plant charge out rates in Technology One. No formal documentation in relation to the

As part of establishing budget 2018/19, the assumptions and basis of determination of each plant items internal plant charge out rate will be reviewed and revised to reflect the current market conditions and consumption patterns. The review will be undertaken annually as part of budget process and will be documented as part of budget working

Finance Manager to establish plant operating budget and resulting calculated plant charge during budget 2018/19 preparations. The City remains on target to achieve this requirement by May 2018 Calculated plant hourly rates

Minutes Attachments – Audit and Risk Management Committee 13 February 2018

Page 36

basis of determination of internal plant charge out rates in Technology One.

papers. to be updated in Technology One. This remains ongoing but is likely to be achieved by the end of this financial year – 30 June 2018.

FINANCIAL REPORTS Review Finding Management Comments and Action Management Timeframe Annual report was not submitted to the department within 30 days of receiving the auditor’s report.

Due to misinterpretation of legislation requirement, the annual financial statements were submitted to the Department of Local Government on 25 November 2016 after the Council adopted the reports at the council meeting on 23 November 2016.

Complete & noted. As this matter represented a non-compliance with the Financial Management Regulations it was included in the audit report for year ending 30 June 17

COMPLIANCE WITH INTEGRATED PLANNING AND REPORTING Review Finding Management Comments and Action City Update Asset management plans do not exist for most asset classes.

Refer to report submitted to Audit and Risk Management Committee 18 July 2017 on City Assets – Implementation Plan. The Manager City Assets is the custodian of the plan and will co-ordinate the development as reported.

A new Manager City Assets commenced in January 2018. Part of their responsibility is to implement an action plan, which is anticipated to be completed by the end of December 2018.

The City’s LTFP has not been updated to reflect the actual financial performance and changes in the financial position since it was first completed.

The working draft of LTFP 2017-2027 was provided to the Audit and Risk Management Committee (ARMC) on 9 May 2017 for feedback and consideration of the principles to guide and complete its development. The feedback from the committee is being used to develop a draft Plan for formal consideration by council and possible public comment.

Director of City Business and Finance Manager to present a draft 10 year budget (LTFP) with details of discretionary funds in February 18 for council consultation. Adoption before 30 June 2018.

GENERAL COMPLIANCE AND OTHER MATTERS Review Finding Management Comments and Action City Update No clear restriction on the terms of investments as required by Financial Management

Financial Management Regulation 19c(2)(b) was amended with effect from 13 May 2017, allowing local governments to invest in fixed term deposit up to three years. No change of policy is required.

Complete Policy is compliant. No further action required.

Minutes Attachments – Audit and Risk Management Committee 13 February 2018

Page 37

Regulation 19C. The following monthly reconciliations were not regularly performed and/or independently reviewed: - Sundry debtors - Sundry creditors - Rate debtors.

The debtor reconciliation had been delayed due to the changeover of chart of account. This is now up to date. Rates debtor reconciliations to be reviewed by Rates Team Leader and independently reviewed by Finance Manager. A clear reconciliation process with documented preparer and reviewers will be developed which will be formally recorded and saved in ECM.

Complete Monthly reconciliations for balance sheet accounts are up to date. Finance Manager to implement documented review process in ECM. The new procedure is on track for completion from month ending 31 January 2018.

It is recommended that the Audit and Risk Management Committee note and review the City’s progress in completing the recommendations of the Financial Management Review 2017. VOTING AND OTHER SPECIAL REQUIREMENTS

Simple Majority Required COMMITTEE AND OFFICER'S RECOMMENDATION

MOVED: Cr J McDonald Receive the Officers update summary with respect to the City’s actions regarding the Financial Management Review 2017, as outlined within this report. CARRIED: 4/0 For Against Cr Doug Thompson Cr Jeff McDonald Cr Rachel Pemberton Mr Phillip Draber

Minutes Attachments – Audit and Risk Management Committee 13 February 2018

Page 38

ARMC1802-9 INFORMATION REPORT - LOCAL GOVERNMENT AUDITING

REFORMS Meeting Date: 13 February 2018 Responsible Officer: Manager Governance Decision Making Authority: Council Agenda Attachments: Guide to Local Government Auditing Reforms BACKGROUND

The Department of Local Government, Sport and Cultural Industries has prepared a guide to inform local governments about the recent reforms to the conduct of local government audits. On 24 August 2017, amendments to the Local Government Act 1995 were passed by State Parliament enabling the Auditor General to audit local government finances and performance. The Act received Royal Assent on 1 September 2017. Following the passage of this legislation, a transitional period for local government auditing commences whereby the Auditor General will assume responsibility for financial audits as existing contracts expire. All local governments will be audited by the Auditor General by 2020-21. Under the legislation, local governments will be required to publish their annual report, including the annual financial report and auditor’s report on their websites. Performance audits, examining the economy, efficiency and effectiveness of programs and organisations, including compliance with legislative provisions and internal policies, were also introduced and will be paid for by the State Government. The Auditor General has informed the department that he intends to commence liaising with local governments in October on the transition. Local governments are encouraged to familiarise themselves with the changes. FINANCIAL IMPLICATIONS

There are no financial implications identified as a result of this report. LEGAL IMPLICATIONS

There are various legislative implications as a result of this reform as outlined in the attached “Guide to Local Government Auditing Reforms”. CONSULTATION

No consultation has been undertaken in regard to this report.

Minutes Attachments – Audit and Risk Management Committee 13 February 2018

Page 39

OFFICER COMMENT

The recent reforms to the conduct of local government audits will also result in changes to the role of Audit Committees:

“With the transfer of auditing to the Auditor General, local government Audit Committees will have a new and important role. The role of the Audit Committee will be amended so that the Audit Committee will have greater involvement in assisting the CEO to carry out the review under Regulation 17 of the Audit Regulations of systems and procedures concerning risk management, internal control, and legislative compliance. This will include helping the CEO to formulate recommendations to council to address issues identified in the reviews. The Audit Committee will also support the auditor as required and have functions to oversee:

• the implementation of audit recommendations made by the auditor, which have been accepted by council; and

• accepted recommendations arising from reviews of local government

systems and procedures. These roles reflect the importance of the Audit Committee as a section of council charged with specific responsibilities to scrutinise performance and financial management. The regulations continue to allow for external membership of Audit Committees. Councils are encouraged to consider inviting appropriate people with expertise in financial management and audit to be members of their Audit Committee.”

VOTING AND OTHER SPECIAL REQUIREMENTS

Simple Majority Required COMMITTEE AND OFFICER'S RECOMMENDATION

MOVED: Cr J McDonald Council receive the purchasing policy exemptions information report for December 2017 and January 2018. CARRIED: 4/0 For Against Cr Doug Thompson Cr Jeff McDonald Cr Rachel Pemberton Mr Phillip Draber

Minutes Attachments – Audit and Risk Management Committee 13 February 2018

Page 40

CONFIDENTIAL MATTERS ARMC1802-10 CONFIDENTIAL REPORT - PROPERTY DISPUTE HIGH STREET

ROAD RESERVE Meeting Date: 13 February 2018 Responsible Officer: Director City Business Decision Making Authority: Council Agenda Attachments: Confidential Legal Advice REASON FOR CONFIDENTIALITY

This report is CONFIDENTIAL in accordance with Section 5.23(2) of the Local Government Act 1995 which permits the meeting to be closed to the public for business relating to the following: (d) legal advice obtained, or which may be obtained, by the local government and

which relates to a matter to be discussed at the meeting COMMITTEE AND OFFICER’S RECOMMENDATION

MOVED: Cr J McDonald That the officer’s confidential recommendation be recommended to Council. CARRIED: 4/0 For Against Cr Doug Thompson Cr Jeff McDonald Cr Rachel Pemberton Mr Phillip Draber

Minutes Attachments – Audit and Risk Management Committee 13 February 2018

Page 41

CLOSURE OF MEETING THE PRESIDING MEMBER DECLARED THE MEETING CLOSED AT 6.49 PM.