Improve the access to mental health care in the Kigoma Region.

SOCIAL ACTION TRUST FUND

ANNUAL REPORT 2006

SOCIAL ACTION TRUST FUND

SOCIAL ACTION TRUST FUND

1

TRUSTEES’ REPORTAND FINANCIAL STATEMENTS

FOR THE YEAR ENDED 31 DECEMBER 2006

SOCIAL ACTION TRUST FUND

2

TRUSTEES’ REPORT AND FINANCIAL STATEMENTS

FOR THE YEAR ENDED 31 DECEMBER 2006

CONTENTS PAGE

Organisation information 1

Trustees’ report 2 to 4 Independent auditors’ report 5 and 6

Income statement 7

Balance sheet 8

Statement of changes in equity 9

Cash flow statement 10

Notes to the financial statements 11 to 26

SOCIAL ACTION TRUST FUND

3

ORGANISATION INFORMATION

PRINCIPAL PLACE OF BUSINESS: Plot No. 35, Mikocheni B P. O. Box 10123 Dar es salaam Tanzania

REGISTERED OFFICE: Muccadam Building Ali Hassan Mwinyi Road P. O. Box 10123 Dar es salaam Tanzania

BANKERS: Exim Bank Main Branch P. O. Box 9510 Dar es Salaam

Citibank Dar es salaam Branch

P. O. Box 71625 Dar es Salaam

Barclays Bank Ohio Branch

P. O. Box 5137 Dar es Salaam AUDITORS: Ernst & Young Certified Public Accountants P. O. Box 2475 DAR ES SALAAM

SOCIAL ACTION TRUST FUND

4

SOCIAL ACTION TRUST FUND

CHAIRMAN’S STATEMENT 2006

I am pleased to present the 9th Annual Report for the Social Action Trust Fund (SATF) for the

calendar year ended 31st December 2006.

The Fund was launched on 3rd April 1998 by the Governments of Tanzania and USA and capitalized

by the United States Agency for International Development (USAID) to promote through investment

the development of the private sector in Tanzania, working directly with the private sector or through

existing institutions; and to use the earnings from interest and dividends to make grants to Non-

Governmental Organizations (NGOs) working in Tanzania in order to assist Orphans and Vulnerable

Children (OVC) to become productive members of society. If at any one point the resources of

the Trust become greater than the needs of OVC then the aim and objective of the Trust shall be

expanded to benefit child education in Tanzania.

REVIEW OF THE YEAR 2006

During the year under review we have witnessed a shift in SATF vision in response to changing

realities in Tanzania economy. Following the retreat held in June 2006 the Board of Trustees resolved

to shift private sector support from direct lending to equity participation and lending through other

institutions. It has been resolved that SATF will focus more on support to the NGO, as the pacemaker

for helping the OVC in Tanzania. During 2006 the Fund participated in the Initial Purchase Offer

(IPO) of Tanzania Portland Cement Company Limited by acquiring shares worth TZS 106.14m. out

of the TZS 1 bill initially allocated for this investment. SATF realized TZS 512m from dividends

in various companies. The Fund has netted TZS 536m profit as compared to a loss of TZS 185m in

2005.

During the year TZS 79.6m was issued as grants to 18 NGOs which supported 3,124 OVC in

primary and secondary schools. A total of TZS.981.31m was received from Global Fund, thus

facilitating support to 16,124 OVC. A further grant of TZS 152m was received from the Rapid

Funding Envelope (RFE) which supported vocational training of 500 OVC. The Board of Trustees

undertakes to exploit emerging opportunities to strengthen the grants making activity of the Fund.

I wish to take this opportunity to thank Trustees on the Board for their dedication and seriousness

in spearheading the mission and vision of the Fund and providing the strategic direction, the

Management and Staff for their commitment to uphold high standards of performance, and lastly to

our business partners and the collaborating NGOs for their roles in fulfilling our mission.

Professor Samuel Wangwe

Chairman

Prof. Samuel WangweChairman

SOCIAL ACTION TRUST FUND

5

Its a pleasure to present the performance of the Fund for the year 2006.The year under review has been a remarkable one to the Fund as the Fund recorded a surplus of Tzs 536mil. compared to the previous year income which had a deficit of Tzs 185mil.Our major sources of income are dividend income, interest from loans, bank deposits and Management fees from projects. The major expenses being personnel costs, Office Rent and Grant administration. During the period under review, the operational costs have reduced from Tzs 223mil to Tzs 167mil; this is equivalent to 25% reduction which is attributed by cost control measures instituted by the Management and apportionment of costs between projects.

ACHIEVEMENTS:Income from operationsSATF holds interest in Tanzania Oxygen Limited; Tanzania Breweries Ltd; Tanzania Tea Packers; Tanga Cement; Swissport, Tanzania Portland Cement Company Ltd; Unit Trust of Tanzania and La Fleur D’Afrique. The dividend income has contributed Tzs.511.66mil. as compared to the previous year which we realized Tzs 366.84mil.This an increase of 39% as compared to the previous year. The Interest on bank deposits has recorded at Tzs.121.22mil as compared to the previous year which earned Tzs 40.3mil.

On the other hand the interest on loan has been Tzs 332.01mil. this is below the interest of the previous year which was Tzs.427.05mil being by 22% lower. This is due to exit of three projects i.e. Zajara Fishing, SHE investment and Mpomabiva. The Global Fund program has contributed Tzs 72.78mil as management fees.

Investment activities:During the year, Tzs 106.14m was invested in 168,713 Twiga shares. Whereas we realized Tzs 530.5mil from disposal of 5,000,000 Unit Trust Units. The receipts from loan debtors amounted

to Tzs 446.53mil. while the preceding year collections were Tzs.1,556.26mil. This signifies the reluctance of loan debtors to reduce their outstanding debts.

Grant making activities:During the year Tzs.79.6m was disbursed to 18 Non Governmental Organizations (NGOs) and Faith Based organization (FBOs) for the SATF OVC Education programme to support orphans in primary and secondary schools. We have received grants from the Global Fund for Aids,Malaria and Tuberculosis (GFATM) and Rapid Funding Envelop(RFE) of Tzs Tzs.981.31m and 152mil respectively. (performance of grant making activities is explained in detail on page…….)

CHALLENGESWe need to institute strict measures in collection of long outstanding loans debts and search for alternative investment avenues so as to ensure sustainability of the fund and to generate adequate funds to support more orphans. On the other hand with increasing numbers of Orphans in Tanzania, we see a need of sourcing more funds from other donors in collaboration with other players in support of the OVC.

CONCLUDING REMARKS:I would like to recognize the contributors whose efforts has made this results possible. I therefore take this opportunity to express my appreciation to the SATF Board of Trustees for their guidance and also thank members of staff for their efforts. The outstanding achievements in the grant making wing has been attained by having a strong network base of collaborating partners through out the country.

We look forward to a performance exceeding excellence in the coming year.

Sincerely yours,

Beatrice MgayaAg.Chief Executive Officer

Beatrice MgayaAg.Chief Executive Officer

PERFORMANCE OF THE FUND FOR YEAR 2006

OVERALL PERFORMANCE:

SOCIAL ACTION TRUST FUND

6

PERFORMANCE OF GRANTS MAKING ACTIVITIES FOR YEAR 2006

During the period under review, Social Action Trust Fund (SATF) undertake four major grant programs, namely SATF Orphans Education, Global Fund OVC program, Rapid Funding Envelope (RFE) and USAID Bomb Victims program. The performance of each program is analyzed as hereunder;

1. SATF OVC Education program The Board of Trustees had initially approved for year 2006 grant amounted to Tzs 250

mil for education support to Orphans and Vulnerable Children in primary and secondary schools of Tanzania mainland. In June 2006, SATF conducted retreat which resulted into a major change in the direction of the grant making activities. New Grant making guidelines were introduced and tested during the year taking effect of the deliberations made at the retreat with a view of improving the process of selecting, awarding and monitoring of the grants to Partner NGOs. SATF has advanced Tzs 79.6m, which has supported 3,124 OVC 18 NGOs/FBOs from 14 regions of Tanzania mainland. The organizations supported with the respective regions in the table below;

No. NGO/FBO Region

1. St. Theresia

Kagera

2. KARADEA3. BUDEA

4. HUYAWA

5. KINSHAI Kilimanjaro6. KIWAKKUKI7. MWAOMI Mwanza8. UHAI Centre Arusha9. UHAI Centre Manyara10. Faraja Trust Fund Morogoro11. Village of Hope Dodoma12. Catholic Diocese of Kigoma Kigoma13. Archdiocese of Songea Ruvuma14. AFRIWAG Tanga15. Tabora NGO Cluster Tabora16. MEDI Mtwara17. TAHEA Iringa18. CARITAS Mbeya

Table1. List of NGO/FBO received grant in year 2006

2. GLOBAL FUND OVC PROGRAM The Global Fund (GF) OVC is a five years program aims at reducing the adverse effect

of HIV/AIDS, poverty, exploitation and abuse of orphans and children identified as most vulnerable. It targets 24 districts with the highest rates of children vulnerability. The program contains key elements of improving access to education, health, food and nutrition, shelter and legal protection. The program is implemented in collaboration with the Department of Social Welfare in the Ministry of Health and Social Welfare and Pact Tanzania.

SATF had received grant amounting to USD 866,878 to support 9,852 Orphans and Vulnerable Children (OVC) in three districts of Tanzania mainland, namely Makete, Songea

SOCIAL ACTION TRUST FUND

7

Urban and Kigoma Rural. The program provides a range of support services including provision to technical expertise in such as situational analysis, financial management, psycho-social support and general capacity building.

During the year under review the Global Fund program marks successfully the closure of year one in June 2006. The program supported; Health(12,109 OVC);in Education(1,099 OVC);in Food & Nutrition(646 OVC) ;Shelter-house repairs(121 houses),702 OVC-shelter-bed and beddings(702 OVC) and shelter-rent(114 OVC). A total of 100 caregivers had received psychosocial support and 25 families (in groups of 5) supported with Income Generating project in Songea municipality.

3. RFE OVC VOCATIONAL EDUCATION PROJECT The OVC Vocational Education project is a one year project funded by the Rapid Funding

Envelop (RFE) under the Management of Deloitte and Touché. The project focuses on Impact mitigation of the effects of HIV/AIDS by assisting Orphans and Vulnerable Children (OVC) to access Vocational Education so as to acquire technical and life skills. In addition the project is designed to provide psychosocial support and startup toolkits to OVC.The project will support 500 OVC from Mbeya city, Tanga municipality, and Morogoro Urban, Tukuyu, Rungwe and Kyela districts. The project cost is TZS 283mil.During the year under review, SATF had received first installment of TZS152,019,210 in November 2006 to implement quarter one activities.SATF has signed contracts with registered vocational training colleges in Mbeya city, Morogoro urban, Mikumi, Tanga, Rungwe and Tukuyu districts. A total of 500 OVC were placed in vocational colleges of which 225 were girls and 275 boys. Under the guidance of the course tutors, OVC had an opportunity of selecting the suitable course that would fit into the environment they live.

4. USAID Bomb Victims SATF is managing the US Embassy Bomb victim’s education program supported by USAID

Mission in Tanzania. The program was initially supporting sixteen Orphans in education at different levels in Tanzania. During the year 2006, 14 children were supported while two children were not in school by 2006, one had completed form four but failed to go for further studies and another child had dropped out in form two. We expect the two children will find alternative courses to advance their education. Out of the 14 supported 7 are in primary schools and 7 in secondary schools. During the year SATF spent a total of TZS 8,553,500/= to pay for school fees and other education related expenses.

Mr. Yogesh ManekBoard Member

Hon. Janet M mariBoard Member

Mr. Ali MufurukiBoard Member

Mrs. Blandina NyoniBoard Member

SOCIAL ACTION TRUST FUND

8

TRUSTEES’ REPORT FOR THE YEAR ENDED 31 DECEMBER 2006

1. INTRODUCTION2.

The Trustees present herewith their report and audited financial statements for the year ended 31 December 2006.

3. PERFORMANCE4.

A gross income of TZS 2,166 million was realised during the year, being 96% above actual income recorded in year 2005. Interest accounted for 21% of total income, dividends – 24%, Global Fund grant – 39%, other grant income 1%, gain on sale of Unit Trust of Tanzania units – 8%, management fees from Global Fund – 3%; and other income – 4%.

Operating expenses before provisions amounted to TZS 1,358 million, being 63% of income and 89% above actual expenses recorded in year 2005. Surplus for the year is recorded at TZS 536 million (2005: Deficit – TZS 185 million), being 25% of the total income.

TZS 271.8 million has been charged to the income statement during the year as a result of increase in the provisions for impairment of loans and advances.

Disbursements to NGOs during the year for orphans education amounted to TZS 79.6 million and the number of orphans supported was 3,124. Trustees approved TZS 350 million out of the retained surplus as donation for Orphans and Vulnerable Children (OVC) education in year 2007.

5. PRINCIPAL ACTIVITIES OF THE TRUST6. 7. The principal activity of the Trust is to promote through investments the development of private

sector in Tanzania and use earnings from the interest and investments to make grants to non-governmental organizations (NGOs) registered in Tanzania in order to assist OVC to become productive members of society.

8.

SOCIAL ACTION TRUST FUND

9

TRUSTEES’ REPORT FOR THE YEAR ENDED 31 DECEMBER 2006 (continued)

9. ATTAINMENT IN PHYSICAL TERMS

1.1 Investments1.2

At the beginning of the year, the Fund’s portfolio comprised 5 equity investments and 16 loan projects. Three projects, Zajara Fishing Company, Mpomabiva Investment Limited and SHE investment Limited exited during the year. An additional equity investment of 168,713 shares was made (TZS 106.1 million), while TZS 530.5 million was realised from sale of 5 million units of Unit Trust of Tanzania (UTT).

1.3 Orphans Education Grants Program1.4

Disbursements amounting to TZS 79.6 million were made to 18 NGOs in 14 regions of Tanzania mainland for OVC education. This amount supported 3,124 children in education (i.e. 2,211 in primary and 913 in secondary schools) during the year. The cumulative number of orphans supported since 1999 is 139,040. Trustees approve TZS 350 million as donation to OVC education in year 2007.

1.5 Global Fund- Orphans and Vulnerable Children Interventions (OVC)

During the year SATF has implemented the second phase of the year one of the Global Fund Orphans and Vulnerable Children (OVC) component. SATF is implementing the program in partnership with Pact Tanzania and the Department of Social Welfare under the ministry of Health and Social Welfare. The second year of implementation commenced in July 2006. The program is scaling up to three additional districts namely Kahama, Bariadi and Lushoto whilst the three districts covered in year one will also be supported in year two.

1.6 Rapid Funding Envelope- Orphans and Vulnerable Children Interventions (OVC)

This is RFE Impact Mitigation of the effects of HIV/AIDS- OVC Vocational Education Support Programme (TZS 263,447,310), this is a one year project and the implementation started in November 2006. The program will support orphans from Mbeya Municipality, Rungwe, Kyela, Tanga City and Morogoro Urban.

10. ADMINISTRATIVE EFFICIENCY11.

Set-out below are details of matters which are deemed to demonstrate the administrative efficiency of the Trust:

a) Overtime: The Trust does not pay any overtime.

b) Labour Turnover: Two employees (Chief Executive Officer and Finance and Administration Manager) left the services of the Fund during the year and their positions have been filled. Five new employees (Chief Executive Officer, Finance and Administration Manager, Assistant Programme Officer, Programme Officer and Finance officer) were engaged.

TRUSTEES’ REPORT FOR THE YEAR ENDED 31 DECEMBER 2006 (continued)

12. EMPLOYEES WELFARE13.

a) Management and Employee Relationshipb)

The relationship between the Management and Employees of the Trust during the year was good.

SOCIAL ACTION TRUST FUND

10

c) Medical Facilitiesd)

The Trust meets the medical expenses for each employee and his/her immediate family members.

14. SOLVENCY

There were no short or long term claims on the assets of the Trust and the solvency of the Fund as at 31 December 2006 is set out on Page 8 of these financial statements.

15. OPERATING RESULTS

These are set out on Page 7 of the financial statements.

16. AUDITORS17. 18. Ernst & Young were the Trust auditors for the year 2006. They have expressed their willingness

to continue and are eligible for reappointment.

19. TRUSTEES

The Trustees of the Fund in office at the date of this report are:

i. Prof. Samuel Wangwe - Chairmanii. Mrs. Blandina Nyoni - Trusteeiii. Mr. Ali Mufuruki - Trusteeiv. Mr. Yogesh Manek - Trustee v. Hon. Janet Mmari - Trustee

BY ORDER OF THE BOARD OF TRUSTEES

_______________________ SECRETARY

SOCIAL ACTION TRUST FUND

11

INDEPENDENT AUDITORS’ REPORT

to the Board of Trustees ofSOCIAL ACTION TRUST FUND (SATF)

We have audited the accompanying financial statements of Social Action Trust Fund (SATF), which comprise the balance sheet as at 31 December 2006 and the income statement, statement of changes in stakeholders’ interest and cash flow statement for the year then ended, and a summary of significant accounting policies and other explanatory notes set out on pages 8 to 26.

Management’s responsibility for the financial statements

Management is responsible for the preparation and fair presentation of these financial statements in accordance with International Financial Reporting Standards, and in compliance with the Societies Ordinance of 1954. This responsibility includes: designing, implementing and maintaining internal control relevant to the preparation and fair presentation of financial statements that are free from material misstatement, whether due to fraud or error; selecting and applying appropriate accounting policies; and making accounting estimates that are reasonable in the circumstances.

Auditors’ responsibility

Our responsibility is to express an opinion on these financial statements based on our audit. We conducted our audit in accordance with International Standards on Auditing. Those standards require that we comply with ethical requirements and plan and perform the audit to obtain reasonable assurance whether the financial statements are free from material misstatement.

An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the financial statements. The procedures selected depend on the auditors’ judgment, including the assessment of the risks of material misstatement of the financial statements, whether due to fraud or error. In making those risk assessments, the auditor considers internal control relevant to the entity’s preparation and fair presentation of the financial statements in order to design audit procedures that are appropriate for the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the entity’s internal control. An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of accounting estimates made by management, as well as evaluating the overall presentation of the financial statements.

We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinion.

SOCIAL ACTION TRUST FUND

12

INDEPENDENT AUDITORS’ REPORT

to the Board of Trustees ofSOCIAL ACTION TRUST FUND (SATF) – (Continued)

Opinion

In our opinion, the financial statements, give a true and fair view of the financial position of the Company as of 31 December 2006, and of its financial performance and its cash flow for the year then ended in accordance with International Financial Reporting Standards.

Report on other legal and regulatory requirements

These financial statements comply with the Societies Ordinance of 1954.

Ernst & Young Joseph SheffuCertified Public Accountants Partner

Dar es Salaam

SOCIAL ACTION TRUST FUND

13

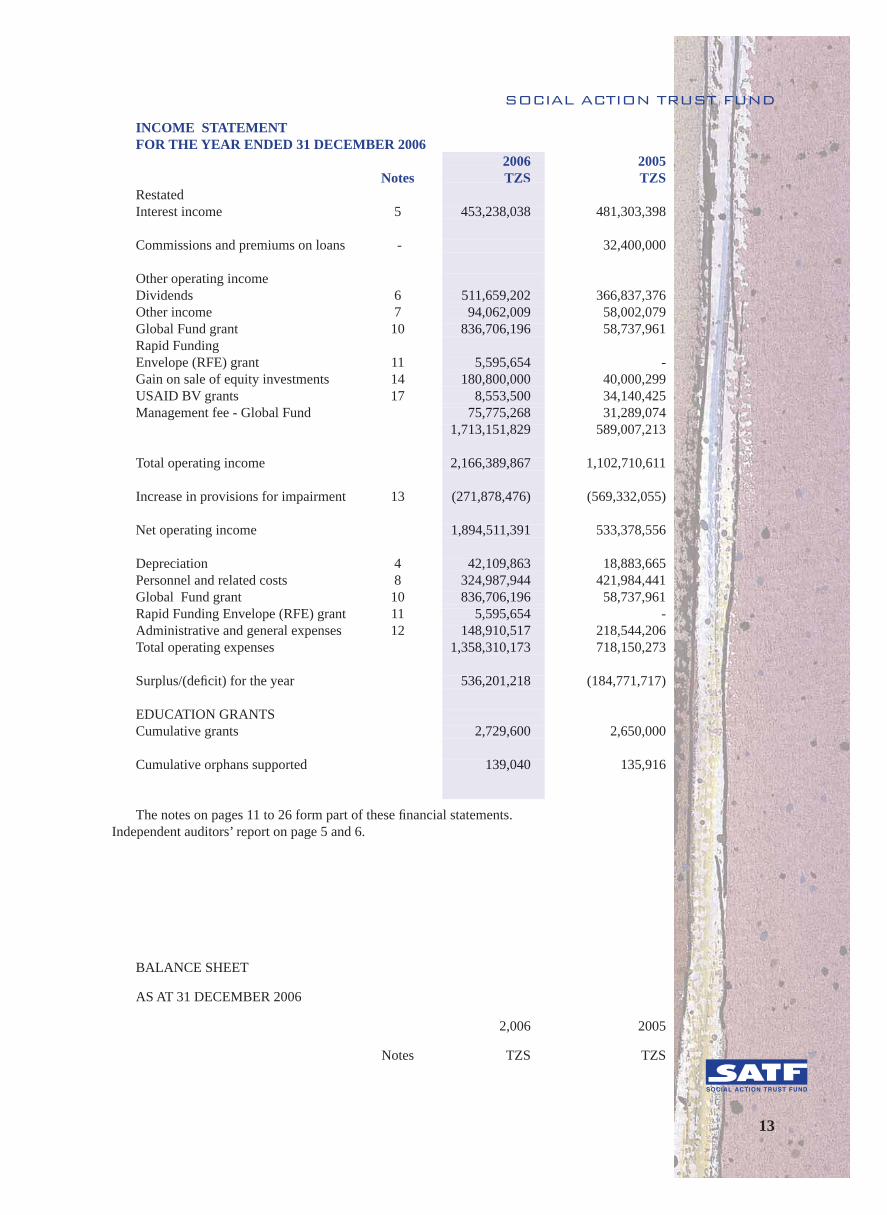

INCOME STATEMENT FOR THE YEAR ENDED 31 DECEMBER 2006 2006 2005 Notes TZS TZS Restated Interest income 5 453,238,038 481,303,398 Commissions and premiums on loans - 32,400,000 Other operating income Dividends 6 511,659,202 366,837,376 Other income 7 94,062,009 58,002,079 Global Fund grant 10 836,706,196 58,737,961 Rapid FundingEnvelope (RFE) grant 11 5,595,654 - Gain on sale of equity investments 14 180,800,000 40,000,299 USAID BV grants 17 8,553,500 34,140,425 Management fee - Global Fund 75,775,268 31,289,074 1,713,151,829 589,007,213 Total operating income 2,166,389,867 1,102,710,611 Increase in provisions for impairment 13 (271,878,476) (569,332,055) Net operating income 1,894,511,391 533,378,556 Depreciation 4 42,109,863 18,883,665 Personnel and related costs 8 324,987,944 421,984,441 Global Fund grant 10 836,706,196 58,737,961 Rapid Funding Envelope (RFE) grant 11 5,595,654 - Administrative and general expenses 12 148,910,517 218,544,206 Total operating expenses 1,358,310,173 718,150,273 Surplus/(deficit) for the year 536,201,218 (184,771,717) EDUCATION GRANTS Cumulative grants 2,729,600 2,650,000 Cumulative orphans supported 139,040 135,916 The notes on pages 11 to 26 form part of these financial statements.

Independent auditors’ report on page 5 and 6.

BALANCE SHEET

AS AT 31 DECEMBER 2006

2,006 2005

Notes TZS TZS

2006 TZS

453,238,038

511,659,202 94,062,009

836,706,196

5,595,654 180,800,000

8,553,500 75,775,268

1,713,151,829

2,166,389,867

(271,878,476)

1,894,511,391

42,109,863 324,987,944 836,706,196

5,595,654 148,910,517

1,358,310,173

536,201,218

2,729,600

139,040

SOCIAL ACTION TRUST FUND

14

ASSETS

Restated

Cash in hand 9 69,624 823,672

Bank balances 9 421,255,798 417,152,923

Fixed deposits with banks 9 1,969,555,257 1,018,586,881

Loans and advances 13 2,158,701,596 3,152,933,442

Equity investments 14 5,480,653,028 4,480,739,419

Other assets 15 105,291,581 193,303,063

NGOs’ clearing account 16 37,552,452 12,952,452

Plant and equipments 4 123,111,222 31,040,251 TOTAL ASSETS 10,296,190,557 9,307,532,101

RESERVES AND LIABILITIES

RESERVES

Trust investment fund 6,318,675,000 6,318,675,000

RMPS fund 1,325,360,000 1,325,360,000

RMPS accumulated losses (528,558,664) (528,558,664)

Available-for-sale reserve 1,150,544,177 (28,685,173)

Retained income 1,623,810,375 1,087,609,157 9,889,830,888 8,174,400,320 LONG TERM LIABILITIES

Provisions for employee benefits 59,322,464 59,322,492 CURRENT LIABILITIES

Accrued expenses 61,511,181 89,447,125

Deffered income 17 285,526,024 984,362,164

347,037,205 1,073,809,289 TOTAL RESERVES AND LIABILITIES 10,296,190,557 9,307,532,101

The notes on pages 11 to 26 form part of these financial statements.

Independent auditors’ report on page 5 and 6.

These financial statements were approved by the Board of Trustees for issue

on _________________________, and were signed on their behalf by:

SOCIAL ACTION TRUST FUND

15

STATEMENT ON CHANGES IN EQUITY

FOR THE YEAR ENDED 31 DECEMBER 2006

Trust RMPS

Investment RMPS Accumulated Retained Available-for-

Fund Fund Losses Income sale reserve Total

TZS TZS TZS TZS TZS TZS

At 01 January 2005 6,318,675,000 1,325,360,000 (528,558,664) 1,772,380,874 - 8,887,857,210

Deficit for the year - - - (184,771,717) - (184,771,717)

Net loss on available-

for-sale financial assets - - - 0 (28,685,173) (28,685,173)

Donation paid - - - (500,000,000) - (500,000,000)

At 31 December 2005 6,318,675,000 1,325,360,000 (528,558,664) 1,087,609,157 0 (28,685,173)

8,174,400,320

At 1 January 2006 6,318,675,000 1,325,360,000 (528,558,664) 1,087,609,157 (28,685,173) 8,174,400,320

Surplus for the year - - - 536,201,218 - 536,201,218

Net gain on available-

for-sale financial assets - - - - 1,179,229,350 1,179,229,350

Prior year Adjustment - - - - - 0

At 31 December 2006 6,318,675,000 1,325,360,000 (528,558,664) 1,623,810,375 1,150,544,177 9,889,830,888

Available-for-sale reserve is made upof Unit Trust of Tanzania units, TZS 517,870,925 and other equity investments TZS 813,013,312. The notes on pages 11 to 26 form part of these financial statements. Independent auditors’ report on page 5 and 6.

SOCIAL ACTION TRUST FUND

16

CASH FLOW STATEMENT

FOR THE YEAR ENDED 31 DECEMBER 2006

2006 2005 Note TZS TZS OPERATING ACTIVITIES Surplus/(deficit) for the year 536,201,218 (184,771,717)

Increase in provisions for impairment 271,878,476 569,332,055

Depreciation 42,109,863 18,883,665

Gain on sale of plant and equipment - (1,124,606)

Gain on sale of equity investments (180,800,000) (40,000,299)

Increase in provision for gratuity - 8,219,060

Grant taken to income (850,855,350) (92,978,735)

Increase in NGO’s clearing accounts (24,600,000) (555,000,000)

Decrease in other liabilities (27,935,944) 39,982,039

Decrease/(increase) in other assets 88,011,483 (160,044,542)

Decrease in loans and advances 722,353,370 682,897,449

Decrease in treasury bills - 976,500,000

Net cash out flow on operating activities 576,363,115 1,261,894,369

INVESTING ACTIVITIES

Purchase of equity investments (106,145,609) (1,686,403,501)

Recapitalisation of dividends (64,285,678) -

Purchase of plant and equipment (134,180,835) (20,733,930)

Proceeds from disposal of plant and equipment - 1,550,000

Proceeds from sale of equity investments 530,547,000 245,272,899

Net Cash Flow on Investing Activities 225,934,878 (1,460,314,532)

FINANCING ACTIVITIES

Grant received (RFE/Global Fund) 152,019,210 981,305,896

Net increase in cash and cash equivalent 954,317,203 782,885,734

Cash and cash equivalents at 01 January 1,436,563,476 653,677,742 Cash and cash equivalent

at 31 December 9 2,390,880,679 1,436,563,476

The notes on pages 11 to 20 form part of these financial statements.

Independent auditors’ report on page 5 and 6.

SOCIAL ACTION TRUST FUND

17

NOTES TO THE FINANCIAL STATEMENTS FOR

FOR THE YEAR ENDED 31 DECEMBER 2006(Continued)

4 EQUIPMENTS

Motor Computers Office Office

vehicles & accessories equipment furniture Total

TZS TZS TZS TZS TZS

31 December 2006

Cost

At 01 January 2006 34,628,450 30,244,143 17,734,902 23,780,500 106,387,995 Additions 87,547,194 12,110,940 34,190,701 332,000 134,180,835

At 31 December 2006 122,175,644 42,355,083 51,925,603 24,112,500 240,568,830

Accumulated depreciation

At 01 January 2006 25,971,339 21,903,279 11,982,000 15,491,126 75,347,744

Charge for the year 26,967,713 7,452,539 6,255,758 1,433,853 42,109,863

At 31 December 2006 52,939,052 29,355,818 18,237,758 16,924,979 117,457,607

Net book value

At 31 December 2006 69,236,591 12,999,265 33,687,845 7,187,521 123,111,222

31 December 2005

Cost

At 01 January 2005 34,628,450 19,576,217 14,656,822 18,068,500 86,929,989

Additions - 11,943,850 3,078,080 5,712,000 20,733,930

Disposal - (1,275,924) - - (1,275,924)

At 31 December 2005 34,628,450 30,244,143 17,734,902 23,780,500 106,387,995

Accumulated depreciation

At 01 January 2005 17,314,226 16,338,023 10,130,672 13,531,688 57,314,609

Charge for the year 8,657,113 6,415,786 1,851,328 1,959,438 18,883,665

Disposal - (850,530) - - (850,530)

At 31 December 2005 25,971,339 21,903,279 11,982,000 15,491,126 75,347,744

Net book value

At 31 December 2005 8,657,111 8,340,864 5,752,902 8,289,374 31,040,251

Available-for-sale reserve is made upof Unit Trust of Tanzania units, TZS 517,870,925 and other equity investments TZS 813,013,312. The notes on pages 11 to 26 form part of these financial statements.

Independent auditors’ report on page 5 and 6.

SOCIAL ACTION TRUST FUND

18

NOTES TO THE FINANCIAL STATEMENTS FOR

FOR THE YEAR ENDED 31 DECEMBER 2006(Continued)

2006 2005 TZS TZS

5 INTEREST INCOME

Interest from loans 332,012,040 427,047,907

Interest on treasury bills - 13,945,055

Bank deposits and others 121,225,998 40,310,436

453,238,038 481,303,398

The substantial amount of interest income is accrued from Tanzania Pharmaceutical Industries Ltd, Foot Loose Limited and Walkgard Westland Hotel &Tours Limited.

6 DIVIDEND

Tanzania Breweries Limited 264,662,480 290,396,956

Swissport (Tanzania) Limited 24,343,554 18,725,811

Tanga Cement Limited 92,796,038 57,714,609

Unit Trust of Tanzania 129,857,130 -

511,659,202 366,837,376

7 OTHER INCOME

Gain on disposal of plant and equipment 1,124,606

Gift/donation received 598,965 -

Recoveries of RMPS debts 5,260,000 -

Gain on fluctuation of foreign currency 47,785,416 26,641,300

Miscellaneous income 40,417,628 30,236,173

94,062,009 58,002,079

8 PERSONNEL EXPENSES

Salaries and allowances 239,012,836 271,198,513

Gratuity 38,837,542 44,540,273

Social security contribution 23,087,973 25,997,402

Medical expenses 2,372,189 3,887,375

Leave expenses 19,351,917 4,314,000

Staff recruitment 1,155,000 4,031,655

Staff welfare 1,170,487 8,219,061

Gratuity - 59,796,162

324,987,944 421,984,441

9 CASH AND CASH EQUIVALENT

Cash in hand 69,624 823,672

Cash at bank 421,255,798 417,152,923 Fixed deposits: Exim Bank 1,850,129,386 1,018,586,881

Citibank 119,425,871 -

2,390,880,679 1,436,563,476

SOCIAL ACTION TRUST FUND

19

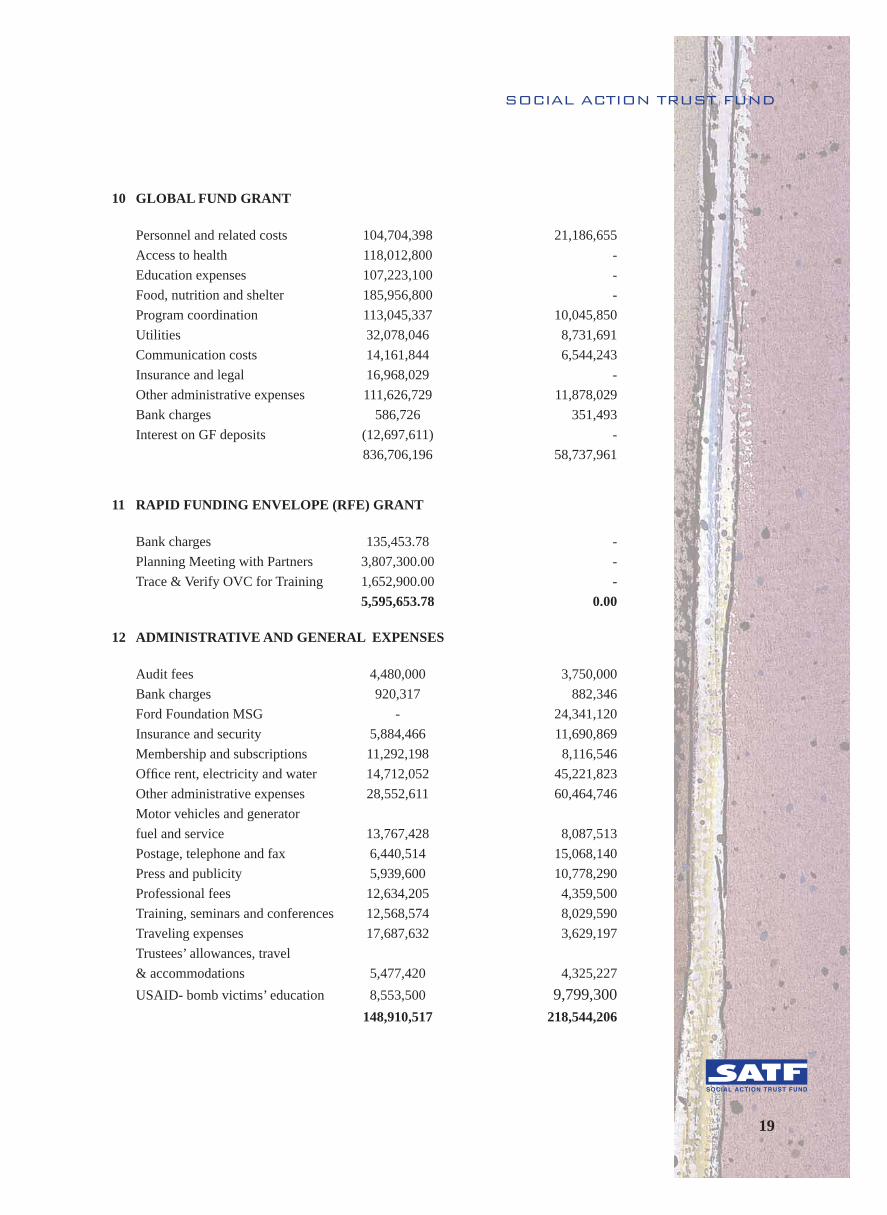

10 GLOBAL FUND GRANT

Personnel and related costs 104,704,398 21,186,655

Access to health 118,012,800 -

Education expenses 107,223,100 -

Food, nutrition and shelter 185,956,800 -

Program coordination 113,045,337 10,045,850

Utilities 32,078,046 8,731,691

Communication costs 14,161,844 6,544,243

Insurance and legal 16,968,029 -

Other administrative expenses 111,626,729 11,878,029

Bank charges 586,726 351,493

Interest on GF deposits (12,697,611) -

836,706,196 58,737,961

11 RAPID FUNDING ENVELOPE (RFE) GRANT

Bank charges 135,453.78 -

Planning Meeting with Partners 3,807,300.00 -

Trace & Verify OVC for Training 1,652,900.00 -

5,595,653.78 0.00

12 ADMINISTRATIVE AND GENERAL EXPENSES

Audit fees 4,480,000 3,750,000

Bank charges 920,317 882,346

Ford Foundation MSG - 24,341,120

Insurance and security 5,884,466 11,690,869

Membership and subscriptions 11,292,198 8,116,546

Office rent, electricity and water 14,712,052 45,221,823

Other administrative expenses 28,552,611 60,464,746

Motor vehicles and generator

fuel and service 13,767,428 8,087,513

Postage, telephone and fax 6,440,514 15,068,140

Press and publicity 5,939,600 10,778,290

Professional fees 12,634,205 4,359,500

Training, seminars and conferences 12,568,574 8,029,590

Traveling expenses 17,687,632 3,629,197

Trustees’ allowances, travel

& accommodations 5,477,420 4,325,227

USAID- bomb victims’ education 8,553,500 9,799,300 148,910,517 218,544,206

SOCIAL ACTION TRUST FUND

20

2006 2005 TZS TZS

13 LOANS AND ADVANCES

Past due loans

Tanzania Pharmaceutical

Industries Limited 279,892,116 419,838,172

Bob Investments Limited 17,532,733 52,598,203

Twiga Feed Limited 382,400,000 382,400,000

Laureate International School 69,428,573 138,857,144

Foot Loose Tanzania Limited 8,333,335 25,000,001

Imra Holding Limited - 136,687,587

Walkgard Westland Hotel

&Tours Limited 354,605,760 504,605,760

Total past due loans 1,112,192,517 1,659,986,867

Current loans and advances 3,691,954,698 3,980,427,024

4,804,147,215 5,640,413,891

Less: Provision for impairment (2,645,445,619) (2,487,480,449)

Total loans and advances 2,158,701,596 3,152,933,442

Movement in provision for bad debts

At 01 January 2,487,480,449 2,078,192,937

Charge during the year 271,878,476 569,332,055

Bad debts written off against provision (113,913,306) (160,044,543)

At 31 December 2,645,445,619 2,487,480,449

Loan receivable amount includes the following:

i} Debtor under receivership

Happy Sausages Limited (HSL)- On 10 November 2006, the court case against HSL was adjourned to July 2007. Trustees believe that a ruling will be made to enable SATF to recover the loan by selling the assets pledged as collateral. The assets are worth TZS 750 million, while the amount due is 643.5 million and has been fully provided for in the books.

ii} Debtors under court decrees

a) Kays Hygiene Products Limited- KHP has continued to service the loan as per court decree, with an outstanding amount of TZS 329,833,505.48 at the end of the period.

b) Trade Goods Limited with Tsh. 125.6 million outstanding, this receivable amount was fully provided.

SOCIAL ACTION TRUST FUND

21

13 LOANS AND ADVANCES

iii} Bank of Tanzania Guarantee Musoma Dairies Limited (MDL)- The three lenders to MDL, i.e. East African Development Bank (EADB),

Preferential Trading Area (PTA) Bank and SATF are at an advance stage on a turnaround strategy for the project, having already committed the necessary working capital for the project and identified a new management team. The Bank of Tanzania Guarantee is in its final stage, the receivable amount of TZS 969.4 million was fully provided.

14 EQUITY INVESTMENTS

No. of Cost/Share Value/Share shares

Tanzania Oxygen Limited 954,834 250.00 330.00 315,095,220 238,708,500 76,386,720

Tanzania Breweries Limited 1,430,871 1,256.00 1,580.00 2,260,360,640 1,797,491,025 463,602,204

Tanzania Tea Packers 876,868 440.00 440.00 385,821,920 387,392,433 0

Tanga Cement Limited 1,139,164 850.00 960.00 1,093,597,440 849,758,278 125,308,040

Dar es Salaam Handling

Cargo Limited 328,523 600.00 680.00 223,395,640 197,112,283 26,281,840

Unit Trust of Tanzania (UTT) 10,032,050 70.00 108.75 1,091,031,588 1,010,276,900 388,741,938

Tanzania Portland

Cement Company Limited 168,713 435.00 660.00 111,350,580 - 37,960,425

La Fleur D’ Afrique 745,900,000 745,900,000 1,118,281,166.50 6,226,553,028 5,226,639,419 32,263,011

Less: Provision (745,900,000) (745,900,000) 5,480,653,028 4,480,739,419

180,800,000.00

During the year 5,000,000 units of UTT investments were sold.

at a price of TZS 106.16 per unit. These were originally purchased at TZS 70 per unit.

2006 2005

TZS TZS 15 OTHER ASSETS Sundry debtors 105,291,581 56,196,418 Prepayments - 137,106,645

105,291,581 193,303,063

16 NON-GOVERNMENTAL ORGANISATIONS’ (NGO)

CLEARANCE ACCOUNT

Receivable from NGOs’ 164,600,000 555,000,000

Payable to NGOs’ (127,047,548) (542,047,548)

37,552,452 12,952,452

SOCIAL ACTION TRUST FUND

22

17 DEFERRED INCOME

USAID Bomb Victims Program

This is an education grant (US$96,870) for 16 orphans of the United States Embassy bomb

victims received from the United States Agency for International Development (USAID) in October 2002.

At 01 January 61,794,229 71,593,529

Amount spent during the year (8,553,500) (9,799,300)

At 31 December 53,240,729 61,794,229

Global Fund for Malaria, Tuberculosis and HIV/AIDS

SATF is a sub-recipient of funds for orphans and vulnerable children (OVC) interventions

under the Global Fund Round 4 for Malaria, Tuberculosis and HIV/AIDS. During the year

a disbursement of US$ 866,879 (TZS 981,305,896 equivalent ) was received for program

activities covering the period from 1st July 2005 to 31 March 2006.

At 01 January 922,567,935 981,305,896

Interest on GF deposits 12,697,611 -

Amount spent during the year (849,403,807) (58,737,961)

At 31 December 85,861,739 922,567,935

Management fees charged by SATF is equivalent to 10% of quarterly budget approved by

Global Fund.

Rapid Funding Envelope (RFE) for HIV/AIDS

This is RFE Impact Mitigation of the effects of HIV/AIDS- OVCs Vocational Education

Support Programme (TZS 263,447,310), the first disbursement of TZS 152,019,210 was

received in November 2006.

At 01 January 0 -

Received during the year 152,019,210 -

Amount spent during the year (5,595,654) -

At 31 December 146,423,556 0

Total grants 285,526,024 984,362,164

SOCIAL ACTION TRUST FUND

23

18 RELATED PARTY TRANSACTIONS

Trustees remuneration and allowances 5,477,420 4,325,227

Key management salaries and allowances 200,482,069 246,683,707

Post employment benefits 30,835,463 20,048,207

Other long term employment benefits 34,476,840 51,979,806

271,271,791 323,036,948

These are remuneration to the Chief Executive Officer, Finance & Administration Manager,

Grants Manager and Investments Manager.

Apart from key management remuneration, there are no other related party transactions.

19 CONTINGENT LIABILITIES AND COMMITMENTS

Legal claims

Civil case No.76 of 1998 at Tanzania high court in Dar es salaam , Tairo Urassa versus SATF.

In this matter Tairo Urassa, ex-SATF Chief Executive Officer is claiming TZS 400,000,000/=

being general damage for wrongful termination of employment contract. The organisation has

been advised by its legal counsel that it is possible, but not probable, that the action will succeed

and accordingly no provision for any liability has been made in these financial statements.

Commitment

There were no capital commitments at the year end.

SOCIAL ACTION TRUST FUND

24

NOTES TO THE FINANCIAL STATEMENTS FORFOR THE YEAR ENDED 31 DECEMBER 2006(Continued)

23 LIQUIDITY RISK

At 31 December 2006 Up to Up to Up to Up to Up to

1 month 3 months 6 months 12 months 5 years Total

TZS TZS TZS TZS TZS TZS

Assets

Cash in hand 69,624 - - - - 69,624

Bank balances 421,255,798 - - - - 421,255,798

Fixed deposit

with banks 1,169,555,257 200,000,000 600,000,000 - - 1,969,555,257

Loans and advances - - - 2,158,701,596 - 2,158,701,596

Other assets - 30,292,822 4,000,000 70,998,759 - 105,291,581

NGOs’ clearing account - - 37,552,452 - - 37,552,452

Equity investments - - 385,821,920 - 5,094,831,108 5,480,653,028

Plant and equipments - - 123,111,222 - - 123,111,222

Total assets 1,590,880,679 230,292,822 1,150,485,594 2,229,700,354 5,094,831,108 10,296,190,557

Liabilities

Provisions for employee benefits - - - 59,322,464 - 59,322,464

Accrued expenses - 61,511,181 - - - 61,511,181

Deferred income - 142,763,012 142,763,012 - - 285,526,024

Total liabilities 0 204,274,193 142,763,012 59,322,464 0 406,359,669

Net liquidity gap 1,590,880,679 26,018,629 1,007,722,582 2,170,377,890 5,094,831,108 9,889,830,888

As at 31 December 2005

Total assets 1,438,121,498 208,179,697 1,040,013,930 2,015,600,577 4,605,616,400 9,307,532,101

Total liabilities 569,617,503 398,093,902 165,420,376 0 0 1,133,131,781

Net liquidity gap 1,438,121,498 (361,437,806) 641,920,028 1,850,180,200 4,605,616,400 8,174,400,320 24

INTEREST RATE RISK

The table below summarises the exposure to interest rate risks.

SOCIAL ACTION TRUST FUND

25

NOTES TO THE FINANCIAL STATEMENTS FORFOR THE YEAR ENDED 31 DECEMBER 2006(Continued)

24 INTEREST RATE RISK

The table below summarises the exposure to interest rate risks.

At 31 December 2006 Up to Up to Up to Up to Up to

1 month 3 months 6 months 12 months 5 years Total

TZS TZS TZS TZS TZS TZS

Shs’000

Assets

Cash in hand 69,624 0 0 - - 69,624

Bank balances 421,255,798 0 - - 0 421,255,798

Fixed deposits with banks 1,169,555,257 200,000,000 600,000,000 - - 1,969,555,257

Loans and advances - 2,158,701,596 - - 2,158,701,596

Other assets - 30,292,822 4,000,000 70,998,759 105,291,581

NGOs’ clearing account - 37,552,452 - - - 37,552,452

Equity investments - - 385,821,920 5,094,831,108 5,480,653,028

Plant and equipments - - - - 123,111,222 123,111,222

Total assets 1,590,880,679 230,292,822 1,027,374,372 2,229,700,354 5,217,942,330 10,296,190,557

Liabilities

Provisions for employee benefits - - - 59,322,464 - 59,322,464

Accrued expenses - - - 61,511,181 - 61,511,181

Deferred income - 142,763,012 142,763,012 - - 285,526,024

Total liabilities 0 142,763,012 142,763,012 120,833,645 0 406,359,669

Interest sensitivity gap 1,590,880,679 87,529,810 884,611,360 2,108,866,709 5,217,942,330 9,889,830,888

At 31 December 2005

Total assets 1,590,880,679 230,292,822 1,027,374,372 2,229,700,354 5,217,942,330 10,296,190,557

Total liabilities 0.00 0.00 142,763,012.03 0.00 142,763,012.03

120,833,645

0.00 0.00 0.00 406,359,669

Interest sensitivity gap 1,590,880,679 87,529,810 884,611,360 2,108,866,709 5,217,942,330 9,889,830,888

SOCIAL ACTION TRUST FUND

26

CURRENCY RISK The various currencies to which SATF is exposed at 31 December 2006 are as shown

below:

TZS US$ Total

Assets

Cash and bank balances 309,430,589 111,894,833 421,325,422

Loans and advances ̀2,158,701,596 - 2,158,701,596

Equity investments 5,480,653,028 - 5,480,653,028

Fixed deposits with banks 1,784,981,081 184,574,176 1,969,555,257

Other assets 105,291,581 - 105,291,581

NGOs’ clearing account 37,552,452 - 37,552,452

Plant and equipments 123,111,222 - 123,111,222

9,999,721,548 296,469,009 10,296,190,557

Reserves and liabilities

Reserves

Trust investment fund 6,318,675,000 - 6,318,675,000

RMPS fund 1,325,360,000 - 1,325,360,000

RMPS accumulated losses (528,558,664) - (528,558,664)

Available-for-sale reserve 1,150,544,177 - 1,150,544,177

Retained income 1,623,810,375 - 1,623,810,375

9,889,830,888 0 9,889,830,888

Liabilities

Provisions for

employee benefits 59,322,464 - 59,322,464

Accrued expenses 61,511,181 - 61,511,181

Grants 285,526,024 - 285,526,024

406,359,669 0 406,359,669

Total reserves and

liabilities 10,296,190,557 0 10,296,190,557

SOCIAL ACTION TRUST FUND

27

NOTES TO THE FINANCIAL STATEMENTSFOR THE YEAR ENDED 31 DECEMBER 2006

1. BASIS OF PREPARATION

The financial statements have been prepared on a historical cost basis and are presented in Tanzanian Shillings (TZS).

Statement of compliance

The financial statements of Social Action Trust Fund (SATF) have been prepared in accordance with International Financial Reporting Standards (IFRSs).

2. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

The principal accounting policies adopted, which have been consistently applied from previous years, are set out below.

Revenue recognition

Revenue is recognised to the extent that it is probable that the economic benefits will flow to the Fund and the revenue can be reliably measured. It comprises interest received from loans issued, dividends received from equity investments, management fees, grant income and income from short term fixed deposits.

Interest income is recognised in the income statement for all instruments measured at amortised cost using the effective interest method. The effective interest method is a method of calculating the amortised cost of a financial asset or a financial liability and of allocating the interest income over the relevant period.

Management fee is recognized on accrual basis. Income from short term fixed deposits is recognized when realized.

Cash and cash equivalents

Cash and bank balances in the balance sheet comprise cash at banks and in hand and short-term deposits with an original maturity of three months or less. For the purpose of the cash flow statement, cash and cash equivalents consist of cash and cash equivalents as defined above, net of outstanding bank overdrafts.

Employee benefits

The organisation operates National Social Security Fund (NSSF) contribution scheme to which both the employee and employer contributes. The organisations’ contributions to NSSF are charged to the income and expenditure statement in the period to which they relate.

SOCIAL ACTION TRUST FUND

28

NOTES TO THE FINANCIAL STATEMENTSFOR THE YEAR ENDED 31 DECEMBER 2006 (Continued)

2. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (Continued)

Plant and equipment

Plant and equipment is stated at cost less accumulated depreciation and any accumulated impairment losses. Cost comprises of expenditure that is directly attributable to the acquisition of the items. Subsequent costs are included in the asset’s carrying amount or recognised as a separate asset, as appropriate, only when it is probable that future economic benefits associated with the item will flow to the Trust and the cost of the item can be measured reliably. All other repairs and maintenance are charged to the income statement during the financial period in which they are incurred.

Depreciation is calculated on a straight-line basis over the useful life of the assets.

The carrying values of plant and equipment are reviewed for impairment when events or changes in circumstances indicate that the carrying value may not be recoverable. An item of plant and equipment is derecognized upon disposal or when no future benefits are expected from its use or disposal. Any gain or loss arising on derecognition of the asset is included in the income statement in the year the asset is derecognized.

The asset’s residue values, useful lives and methods are reviewed, and adjusted if appropriate, at each financial year.

The current useful lives in use are: Years

Motor vehicles 4 Computers and accessories 3Furniture, fittings and office equipment 8

Foreign currency translations

Transactions in currencies other than Tanzania Shillings are recorded at rates prevailing at the transactions dates. Monetary assets and liabilities that are denominated in foreign currencies are translated into Tanzania Shillings at rates prevailing at the balance sheet date. The resulting differences from conversion and translation are dealt with in the income statement.

Provisions

Provisions are made when the Trust has a present obligation, as a result of past events where it is probable that an outflow of resources embodying economic benefits will be required to settle the obligation and a reliable estimate can be made for the amount of the obligation.

SOCIAL ACTION TRUST FUND

29

NOTES TO THE FINANCIAL STATEMENTSFOR THE YEAR ENDED 31 DECEMBER 2006 (Continued)

2. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (Continued)

Investments and other financial assets

Financial assets in the scope of IAS 39 are classified as either financial assets at fair value through profit or loss, loans and receivables, available-for-sale and held-to-maturity investments as appropriate. When financial assets are recognised initially, they are measured at fair value plus directly attributable transaction costs. The Fund determines the classification of its financial assets after initial recognition and, where allowed and appropriate, re-evaluates this designation at each financial year-end.

Available-for-sale financial assetsAvailable-for-sale financial investments are those which are designated as such or do not qualify to be classified as designated at fair value through profit or loss, held-to-maturity or loans and advances. They include equity instruments, investments in mutual funds and money market and other debt instruments. After initial measurement, available-for-sale financial investments are subsequently measured at fair value. Unrealised gains and losses are recognised directly in equity in the “Available-for-sale reserve”. When the security is disposed of, the cumulative gain or loss previously recognised in equity is recognised in the income statement in ‘Other operating income’ or ‘Other operating expenses’. Where the Fund holds more than one investment in the same security they are deemed to be disposed of on a first-in first-out basis. Interest earned whilst holding available-for-sale financial investments is reported as interest income using the effective interest rate. Dividends earned whilst holding available-for-sale financial investments are recognised in the income statement as ‘Other operating income’ when the right of the payment has been established. The losses arising from impairment of such investments are recognised in the income statement in ‘Impairment losses on financial investments’ and removed from the available-for-sale reserve.

Held-to-maturity investmentsNon-derivative financial assets with fixed or determinable payments and fixed maturity are classified as held-to-maturity when the Fund has the positive intention and ability to hold to maturity. Other long-term investments that are intended to be held-to-maturity, such as bonds, are subsequently measured at amortised cost. This cost is computed as the amount initially recognised minus principal repayments, plus or minus the cumulative amortisation using the effective interest method of any difference between the initially recognised amount and the maturity amount. For investments carried at amortised cost, gains and losses are recognised in income when the investments are derecognised or impaired, as well as through the amortisation process.

Loans and receivablesLoans and receivables are non-derivative financial assets with fixed or determinable payments that are not quoted in an active market. Such assets are carried at amortised cost using the effective interest method. Gains and losses are recognised in income when the loans and receivables are derecognised or impaired, as well as through the amortisation process.

SOCIAL ACTION TRUST FUND

30

NOTES TO THE FINANCIAL STATEMENTSFOR THE YEAR ENDED 31 DECEMBER 2006 (Continued)

2. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (Continued)

Impairment of financial assets

The Fund assesses at each balance sheet date whether a financial asset or group of financial assets is impaired.

Assets carried at amortised costIf there is objective evidence that an impairment loss on receivables carried at amortised cost has been incurred, the amount of the loss is measured as the difference between the asset’s carrying amount and the present value of estimated future cash flows discounted at the financial asset’s original effective interest rate. The carrying amount of the asset is reduced either directly or through use of an allowance account. The amount of the loss is recognised in profit or loss. The Fund assesses whether objective evidence of impairment exists individually for financial assets. If, in a subsequent period, the amount of the impairment loss decreases and the decrease can be related objectively to an event occurring after the impairment was recognised, the previously recognised impairment loss is reversed. Any subsequent reversal of an impairment loss is recognised in the income statement, to the extent that the carrying value of the asset does not exceed its amortised cost at the reversal date.

Impairment of tangible assets

The Fund assesses at each reporting date whether there is an indication that an asset may be impaired. If any such indication exists, or when annual impairment testing for an asset is required, the Fund makes an estimate of the asset’s recoverable amount. An asset’s recoverable amount is the higher of an asset’s or cash generating unit’s fair value less costs to sell and its value in use and is determined for an individual asset, unless the asset does not generate cash inflows that are largely independent of those from other assets or groups of assets. Where the carrying amount of an asset exceeds its recoverable amount, the asset is considered impaired and is written down to its recoverable amount.

Trade and other payables

Liabilities for the trade and other amounts payable are carried at cost which is the fair value of the consideration to be paid in the future for goods and services received, whether or not billed to the SATF.

Comparatives

Where necessary, comparative figures have been reclassified to conform to the presentation in the current period.

SOCIAL ACTION TRUST FUND

31

NOTES TO THE FINANCIAL STATEMENTSFOR THE YEAR ENDED 31 DECEMBER 2006 (Continued)

2. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (Continued)

Grants

Grants are recognised where there is reasonable assurance that the grant will be received and all attaching conditions will be complied with.

When the grant relates to an expense item, it is recognised as income over the period necessary to match the grant on a systematic basis to the costs that it is intended to compensate.

Where the grant relates to an asset, the fair value is credited to a deferred income account and is released to the income statement over the expected useful life of the relevant asset by equal annual instalments.

3. SIGNIFICANT ACCOUNTING JUDGEMENTS AND ESTIMATES

The Fund makes estimates and assumptions that affect the reported amounts of assets and liabilities within the next financial year. Estimates and judgments are continually evaluated and are based on historical experience and other factors, including expectations of future events that are believed to be reasonable under the circumstances.

(a) Impairment losses on loans and advancesThe Fund reviews its loan portfolios to assess impairment at least on annual basis. In determining whether an impairment loss should be recorded in the income statement, the Fund makes judgments as to whether there is any observable data indicating that there is a measurable decrease in the estimated future cash flows from a portfolio of loans before the decrease can be identified with an individual loan in that portfolio. This evidence may include observable data indicating that there has been an adverse change in the payment status of borrowers in a group, or national or local economic conditions that correlate with defaults on assets in the group. Management uses estimates based on historical loss experience for assets with credit risk characteristics and objective evidence of impairment similar to those in the portfolio when scheduling its future cash flows.

(b) Held-to-maturity investmentsThe Fund follows the guidance of IAS 39 on classifying non-derivative financial assets with fixed or determinable payments and fixed maturity as held-to-maturity. The classification requires significant judgement. In making this judgement, the Fund evaluates its intention and ability to hold such investments to maturity. If the Fund fails to keep these investments to maturity other than for the specific circumstances – for example, selling an insignificant amount close to maturity – it will be required to reclassify the entire class as available for sale. The investments would therefore be measured at fair value and not amortised cost.

SOCIAL ACTION TRUST FUND

32

NOTES TO THE FINANCIAL STATEMENTSFOR THE YEAR ENDED 31 DECEMBER 2006 (Continued)

20. TAXATION

Social Action Trust Fund is exempted from all taxes and levies on income as provided for under Article (3) of the Trust Deed.

21. FINANCIAL RISK MANAGEMENT The Fund’s activities expose it to a variety of financial risks, including the effects of changes in debt and equity market prices, foreign currency exchange rates and interest rates. The Fund’s overall risk management programme focuses on the unpredictability of financial markets and seeks to minimize potential adverse effects on the Fund’s financial performance. The Board provides written principles for overall risk management, as well as written policies covering specific areas, such as foreign-exchange risk, interest-rate risk, credit risk, and liquidity risk.

Liquidity risk

Liquidity risk is termed as a risk arising when the Fund is unable to meet its obligations from maturing commitments due to insufficient fund. The Fund has set the finance department which among other functions, it monitors the maturity gap of the Fund’s assets against maturing liabilities.

Foreign exchange risk

The Fund operates internationally and is exposed to foreign exchange risk arising from various currency exposures, primarily with respect to the United States Dollar (US$). Management monitors the foreign exchange risk of the Fund.

Interest-rate risk

The Fund’s income and operating cash flows are substantially independent of changes in market interest rates. The interest rates of loans and advances are fixed at the commission of the loan or at the time of renewal.

Credit risk

The Fund assumes risks in order to realize returns on its investments, however assumed risk may result into potential losses to the Fund. In order to minimize this risk the Fund monitors the credit risk at management level and board level in accordance to procedures, limits, and Fund laid down by the credit policies and the investment policies.

22. COUNTRY OF INCORPORATION

The Fund is incorporated in Tanzania under the Societies Ordinance of 1954 and domiciled in Tanzania.

SOCIAL ACTION TRUST FUND

Muccadam Building,Ali Hassan Mwinyi RoadP. O. Box 10123,Dar es Salaam,TANZANIA

Tel: +255 (0) 22 2118740 +255 (0) 22 2118742Fax: +255 (0) 22 2118741

Email: [email protected]

Web: www.satf.org