An Introduction to System of National Accounts – … V Part 1 Production and Generation of Income...

51

Lesson: V Part 1 Production and Generation of Income Accounts An Introduction to System of National Accounts – Integrated Transaction Accounts Third Intermediate-Level e-Learning Course on 2008 System of National Accounts May - July 2014 SIAP 1

Transcript of An Introduction to System of National Accounts – … V Part 1 Production and Generation of Income...

Lesson: V Part 1 Production and Generation of Income Accounts

An Introduction to System of National Accounts – Integrated Transaction Accounts

Third Intermediate-Level e-Learning Course on 2008 System of National Accounts

May - July 2014

SIAP 1

Contents 2

Production and production process Production account and Generation of Income

account

SIAP

Lesson Objectives 3

At the end of the lesson, participants are expected to Describe the concept of production and compile output

using SNA principles Compile production account and compute value added Identify components of intermediate consumption Describe components and compile the generation of

income account

SIAP

4

Production and Production Process

SIAP

5

Concept of Production 1993 / 2008 SNA: “ ... an activity in which an

enterprise uses inputs to produce outputs.”

OR an economic activity that

creates (produces) goods and / or services

from inputs of raw materials and other intermediate products,

using (human) labour and available productive resources like machinery, buildings and land.

Production and Production Process

SIAP

6

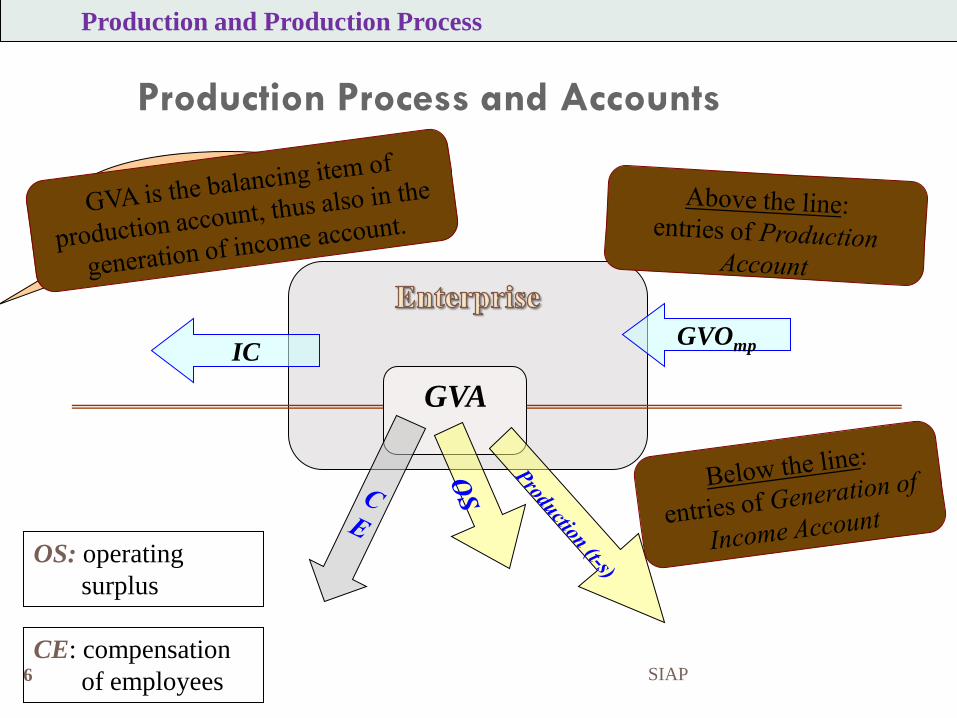

Production Process and Accounts

GVA

CE: compensation of employees

OS: operating surplus

Production and Production Process

IC GVOmp

These are the money flows involved

SIAP

7

IC or CE or OS? – A Simple rule

Production and Production Process

Enterprise’s expenses

For produced or

non-produced resources?

whether entirely used up?

Capital formation

no

yes IC

Whether for human resources?

produced non-produced

IC CE yes

no

Capital formation

OS

SIAP

8

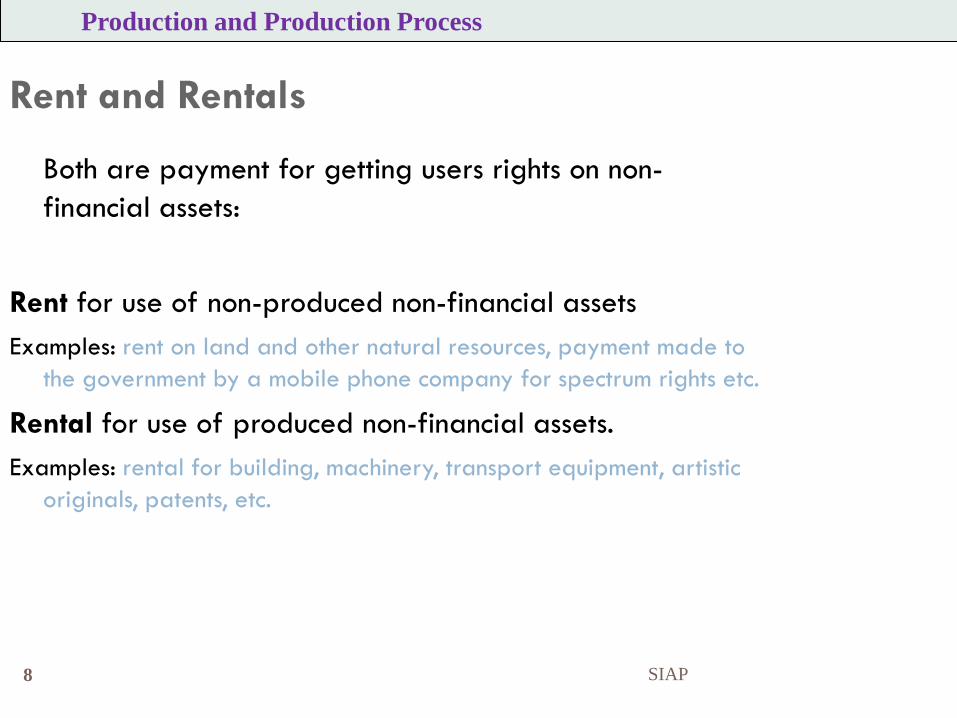

Rent and Rentals

Both are payment for getting users rights on non-financial assets:

Rent for use of non-produced non-financial assets Examples: rent on land and other natural resources, payment made to

the government by a mobile phone company for spectrum rights etc.

Rental for use of produced non-financial assets. Examples: rental for building, machinery, transport equipment, artistic

originals, patents, etc.

Production and Production Process

SIAP

9

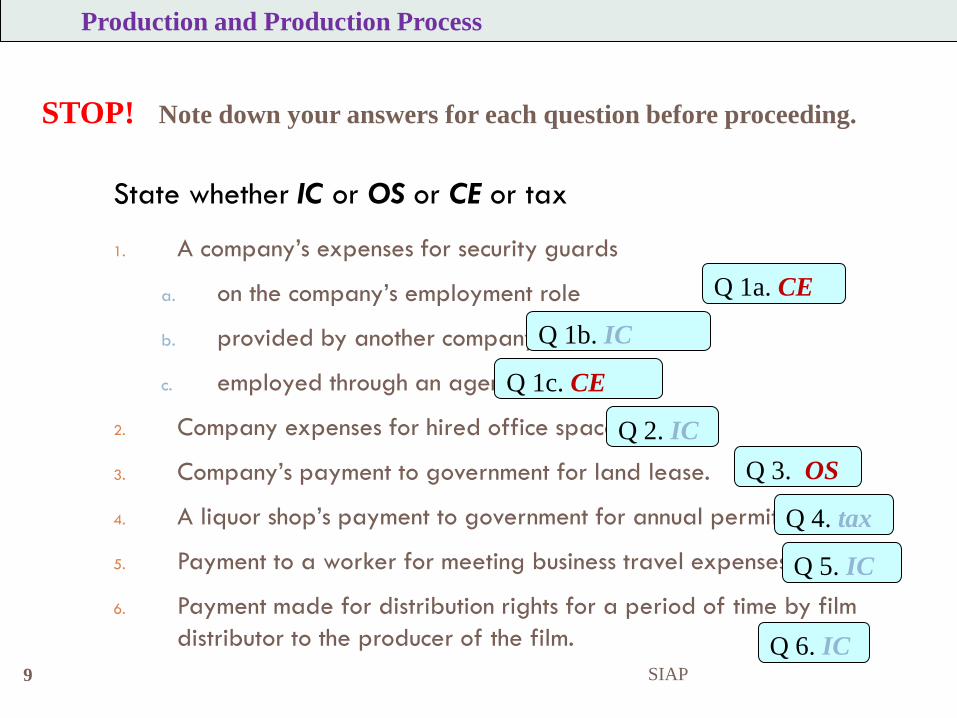

State whether IC or OS or CE or tax 1. A company’s expenses for security guards

a. on the company’s employment role

b. provided by another company

c. employed through an agent

2. Company expenses for hired office space.

3. Company’s payment to government for land lease.

4. A liquor shop’s payment to government for annual permit.

5. Payment to a worker for meeting business travel expenses.

6. Payment made for distribution rights for a period of time by film distributor to the producer of the film.

Q 1a. CE

Q 1b. IC

Q 1c. CE

Q 2. IC Q 3. OS

Q 4. tax

STOP! Note down your answers for each question before proceeding.

Production and Production Process

Q 5. IC

Q 6. IC SIAP

10

Production Account and Generation of Income Account

SIAP

11

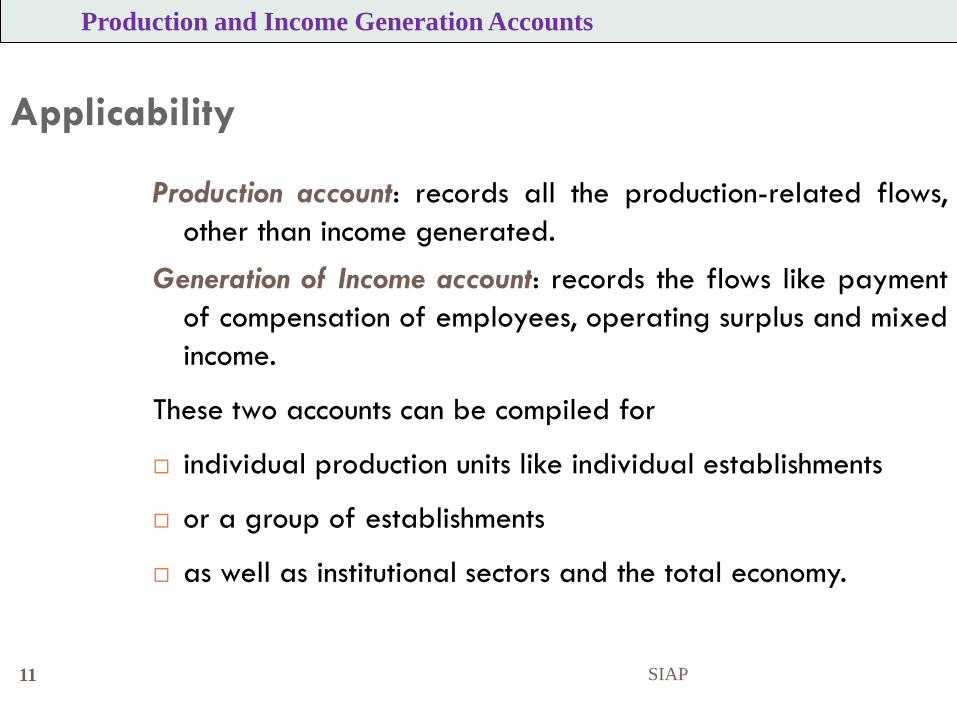

Applicability

Production account: records all the production-related flows, other than income generated.

Generation of Income account: records the flows like payment of compensation of employees, operating surplus and mixed income.

These two accounts can be compiled for

individual production units like individual establishments

or a group of establishments

as well as institutional sectors and the total economy.

Production and Income Generation Accounts

SIAP

12

Underlying Identities

For total economy Production account:

GDPmp≡ GVObp – IC + product (t-s) + (t-s) on imports. Generation of Income account:

GDPmp ≡ (CE + OS & MI) generated in resident enterprises + production (t-s) + (t-s) on imports.

Production and Income Generation Accounts

SIAP

13

Accounts Structure

Production and Income Generation Accounts

Uses Resources Production Account

Intermediate consumption GVObp Market output (at basic price) For own use Non-market (t-s) on products & import duties

B.1g GDP CFC B.n1 NDP

Generation of Income Account B.1g GDP B.1n NDP

Compensation of employees Product & import (t-s) Other Production (t-s) B.2g & B.3g OS+MI (gross) B.2n & B.3n OS+MI (net)

SIAP

14

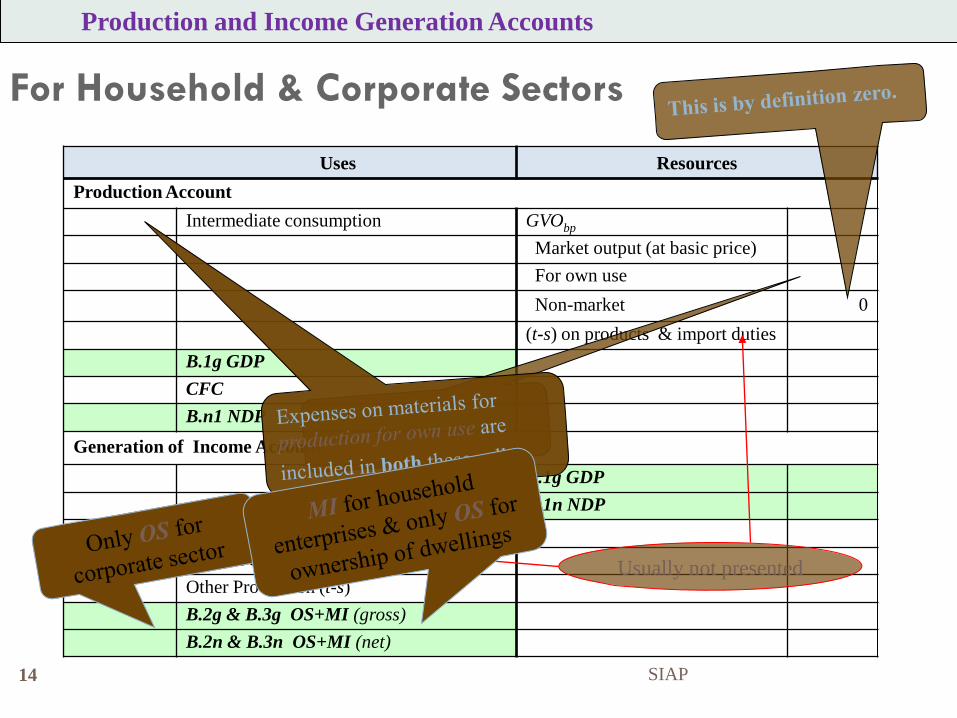

For Household & Corporate Sectors

Production and Income Generation Accounts

Uses Resources Production Account

Intermediate consumption GVObp Market output (at basic price) For own use Non-market 0 (t-s) on products & import duties

B.1g GDP CFC B.n1 NDP

Generation of Income Account B.1g GDP B.1n NDP

Compensation of employees Product & import (t-s) Other Production (t-s) B.2g & B.3g OS+MI (gross) B.2n & B.3n OS+MI (net)

Usually not presented

SIAP

15

For General Government & NPISHs Sectors

Production and Income Generation Accounts

Uses Resources Production Account

Intermediate consumption GVObp Market output (at basic price) 0 For own use Non-market (t-s) on products & import duties

B.1g GDP CFC B.n1 NDP

Generation of Income Account B.1g GDP B.1n NDP

Compensation of employees Product & import (t-s) Other Production (t-s) B.2g OS (gross)

0 B.2n OS (net)

SIAP

16

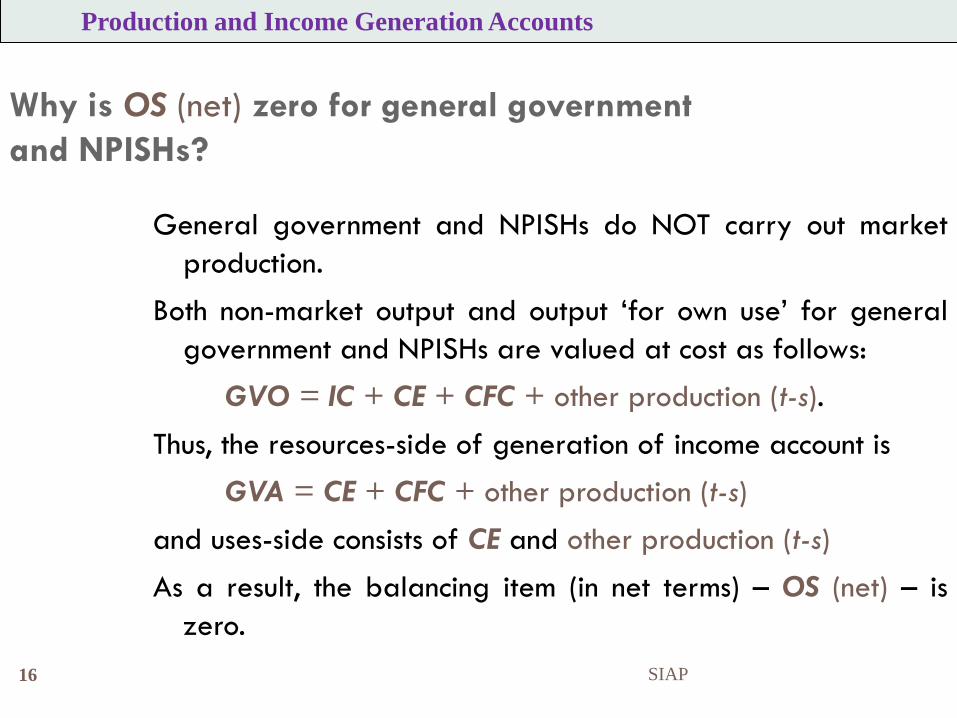

Why is OS (net) zero for general government and NPISHs?

General government and NPISHs do NOT carry out market production.

Both non-market output and output ‘for own use’ for general government and NPISHs are valued at cost as follows:

GVO = IC + CE + CFC + other production (t-s).

Thus, the resources-side of generation of income account is GVA = CE + CFC + other production (t-s) and uses-side consists of CE and other production (t-s)

As a result, the balancing item (in net terms) – OS (net) – is zero.

Production and Income Generation Accounts

SIAP

17

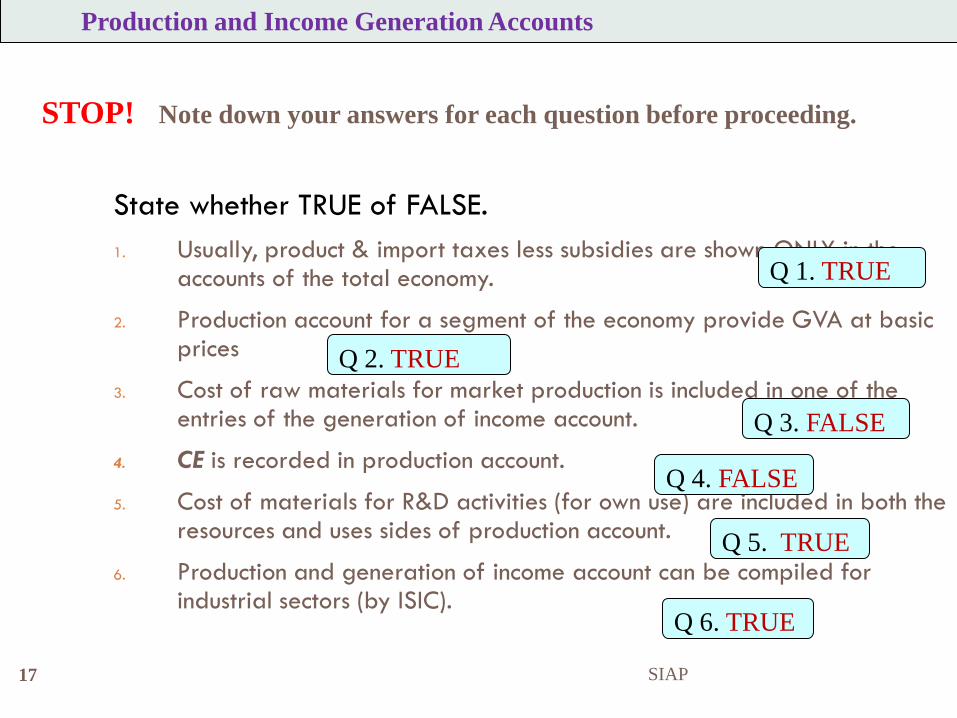

State whether TRUE of FALSE. 1. Usually, product & import taxes less subsidies are shown ONLY in the

accounts of the total economy.

2. Production account for a segment of the economy provide GVA at basic prices

3. Cost of raw materials for market production is included in one of the entries of the generation of income account.

4. CE is recorded in production account.

5. Cost of materials for R&D activities (for own use) are included in both the resources and uses sides of production account.

6. Production and generation of income account can be compiled for industrial sectors (by ISIC).

Q 1. TRUE

Q 2. TRUE

Q 3. FALSE

Q 4. FALSE

Q 5. TRUE

Q 6. TRUE

STOP! Note down your answers for each question before proceeding.

Production and Income Generation Accounts

SIAP

18

End of Part-1

Lesson V

SIAP

Lesson: V Part 2 Production and Generation of Income Accounts

An Introduction to System of National Accounts – Integrated Transaction Accounts

Second Intermediate-Level e-Learning Course on 2008 System of National Accounts

May - July 2014

SIAP 19

20

Measuring Output

SIAP

21

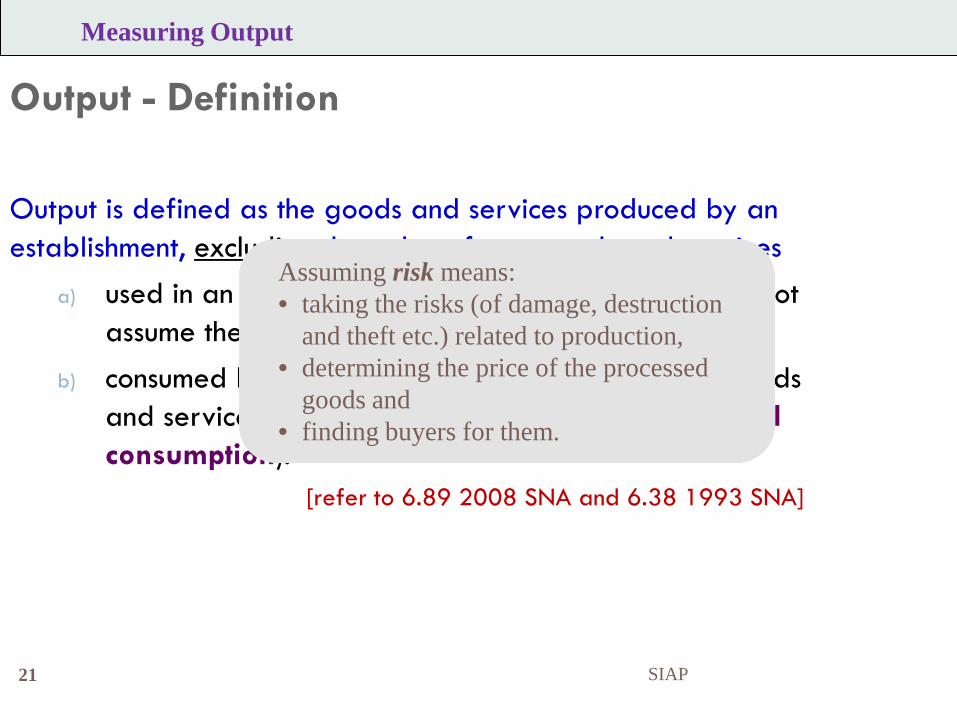

Output - Definition

Output is defined as the goods and services produced by an establishment, excluding the value of any goods and services

a) used in an activity for which the establishment does not assume the risk of using the products in production,

b) consumed by the same establishment (except for goods and services used for capital formation or own final consumption).

[refer to 6.89 2008 SNA and 6.38 1993 SNA]

Measuring Output

Assuming risk means: • taking the risks (of damage, destruction

and theft etc.) related to production, • determining the price of the processed

goods and • finding buyers for them.

SIAP

22

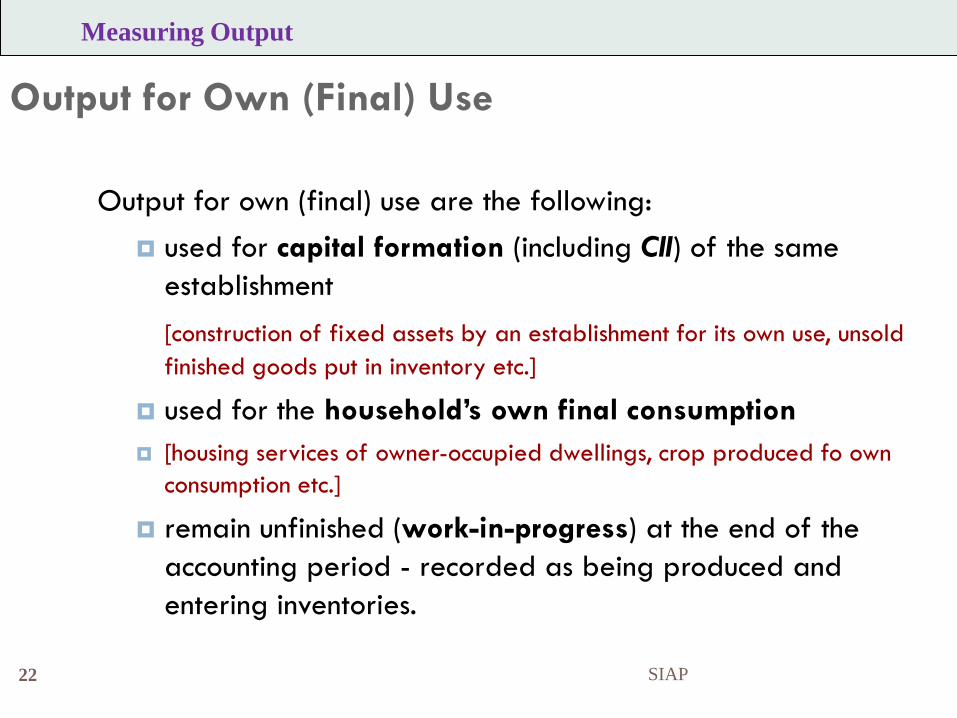

Output for Own (Final) Use

Output for own (final) use are the following: used for capital formation (including CII) of the same

establishment [construction of fixed assets by an establishment for its own use, unsold

finished goods put in inventory etc.]

used for the household’s own final consumption [housing services of owner-occupied dwellings, crop produced fo own

consumption etc.]

remain unfinished (work-in-progress) at the end of the accounting period - recorded as being produced and entering inventories.

Measuring Output

SIAP

23

Economic Ownership

The principle of change of ownership is central to recording of transactions in goods, services and financial assets.

From an economic view point, a change in ownership represents transfer of all the associated risks, rewards, rights and responsibilities.

Economic ownership takes account of where the risks and rewards of ownership lie.

Measuring Output

SIAP

24

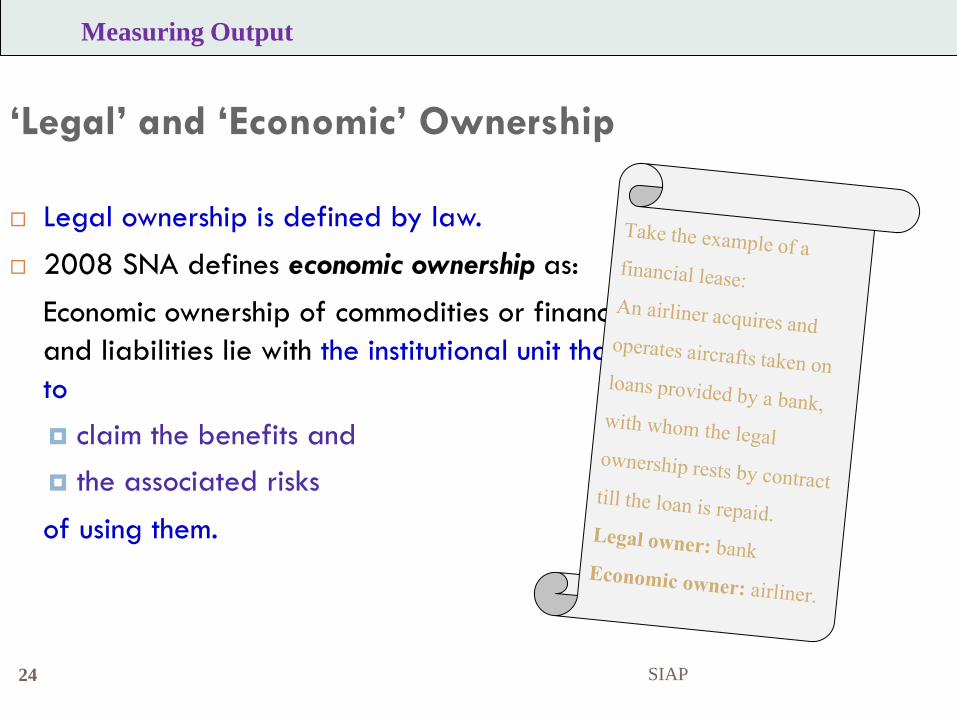

‘Legal’ and ‘Economic’ Ownership

Legal ownership is defined by law. 2008 SNA defines economic ownership as: Economic ownership of commodities or financial assets

and liabilities lie with the institutional unit that is entitled to claim the benefits and the associated risks

of using them.

Measuring Output

SIAP

25

Principle of Recording Transactions

The 2008 SNA recommends that transactions in services be recorded when they are

provided; transactions in goods be recorded when there is a

change in economic ownership rather than the legal ownership; and

assets be recorded on the balance sheets of the economic owner rather than the legal owner.

Measuring Output

SIAP

26

Recording within-enterprise Transactions

For internal within-enterprise transactions, goods delivered from one establishment to other

do not involve change in legal ownership

but possibly a change in economic ownership.

Measuring Output

SIAP

27

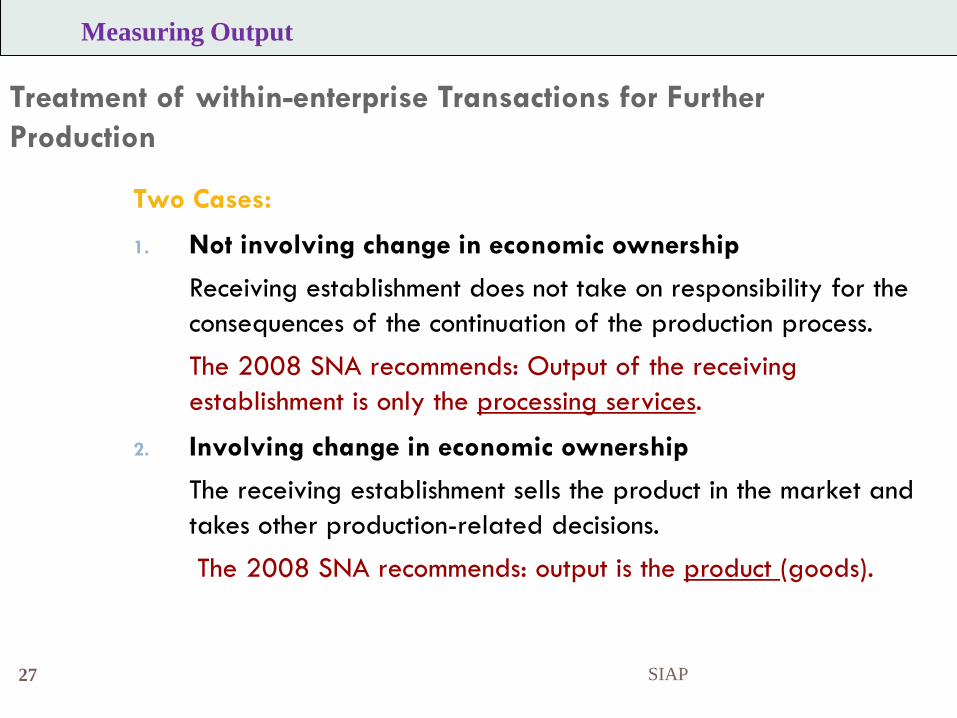

Treatment of within-enterprise Transactions for Further Production

Two Cases:

1. Not involving change in economic ownership

Receiving establishment does not take on responsibility for the consequences of the continuation of the production process.

The 2008 SNA recommends: Output of the receiving establishment is only the processing services.

2. Involving change in economic ownership

The receiving establishment sells the product in the market and takes other production-related decisions.

The 2008 SNA recommends: output is the product (goods).

Measuring Output

SIAP

28

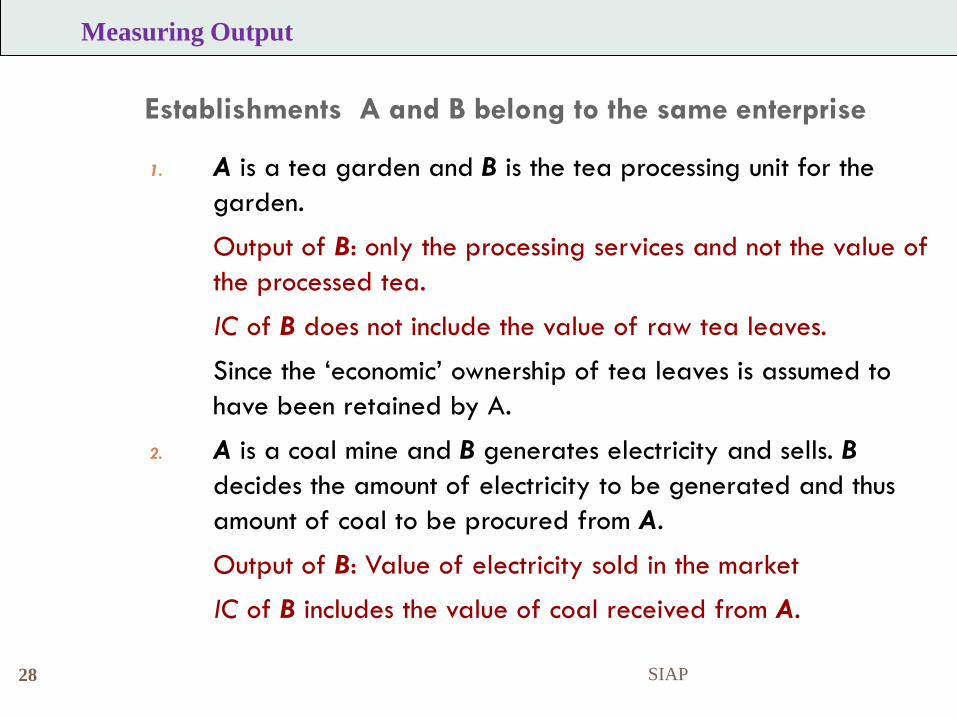

Establishments A and B belong to the same enterprise

1. A is a tea garden and B is the tea processing unit for the garden.

Output of B: only the processing services and not the value of the processed tea.

IC of B does not include the value of raw tea leaves.

Since the ‘economic’ ownership of tea leaves is assumed to have been retained by A.

2. A is a coal mine and B generates electricity and sells. B decides the amount of electricity to be generated and thus amount of coal to be procured from A.

Output of B: Value of electricity sold in the market

IC of B includes the value of coal received from A.

Measuring Output

SIAP

29

Recording of Output

Output is recorded if the goods and services being produced are provided (sold or given free) to other institutional units are used for capital formation of the same establishment;

enter inventories even if eventually are withdrawn from inventories for use as

intermediate consumption in the same establishment in a later period;

Measuring Output

SIAP

30

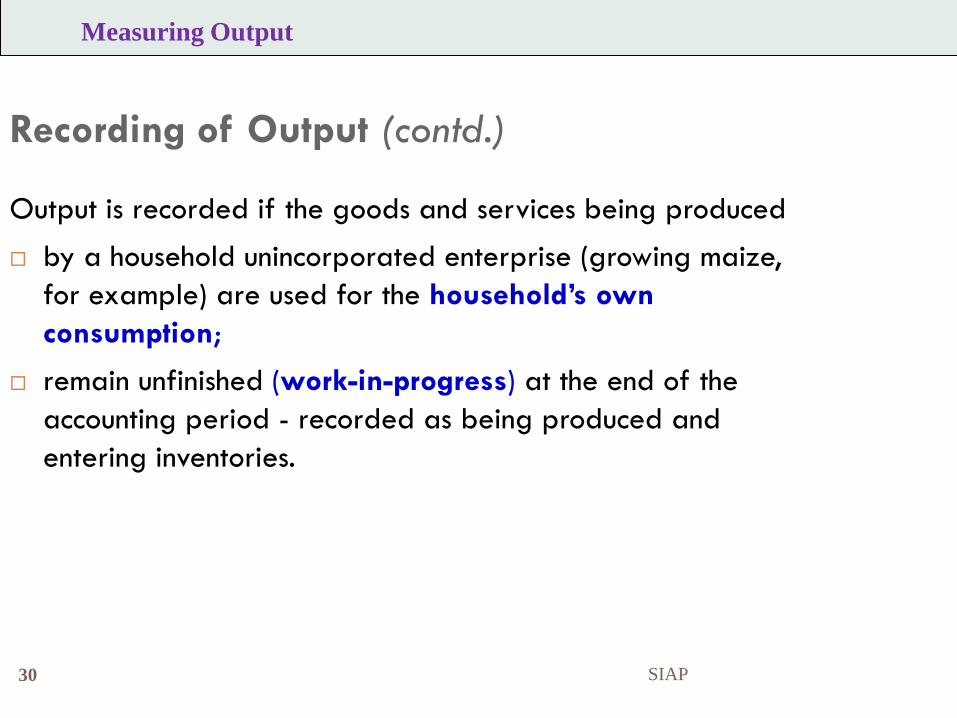

Recording of Output (contd.)

Output is recorded if the goods and services being produced by a household unincorporated enterprise (growing maize,

for example) are used for the household’s own consumption;

remain unfinished (work-in-progress) at the end of the accounting period - recorded as being produced and entering inventories.

Measuring Output

SIAP

31

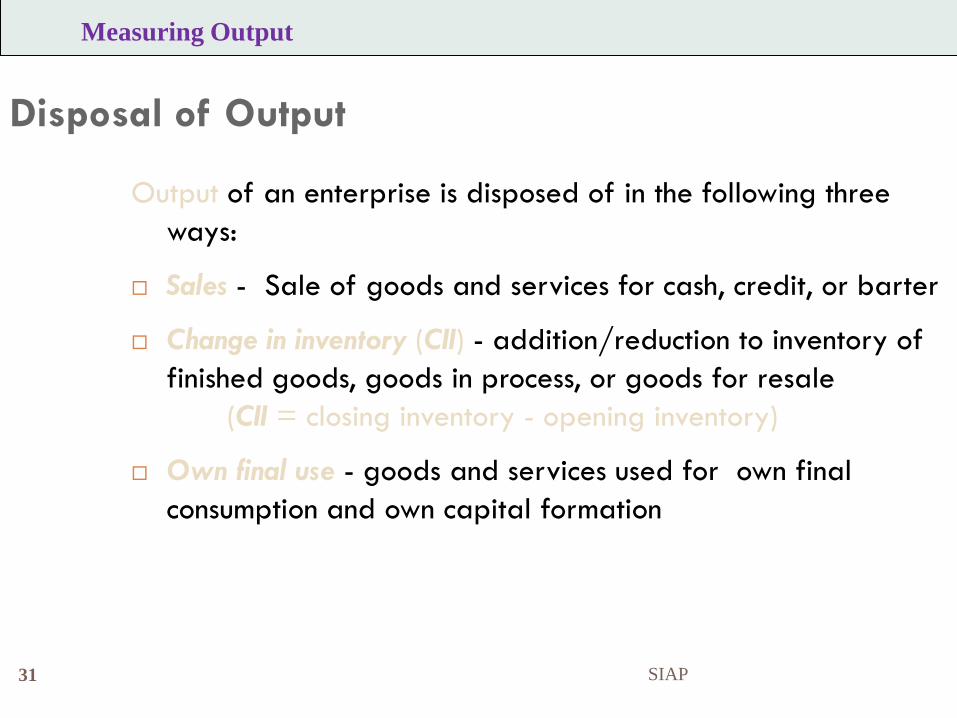

Disposal of Output

Output of an enterprise is disposed of in the following three ways:

Sales - Sale of goods and services for cash, credit, or barter

Change in inventory (CII) - addition/reduction to inventory of finished goods, goods in process, or goods for resale

(CII = closing inventory - opening inventory)

Own final use - goods and services used for own final consumption and own capital formation

Measuring Output

SIAP

32

Goods for Processing

Goods for processing: goods owned by one enterprise sent for processing to another enterprise.

The receiving establishment (for example an independent tailor working for a garment making enterprise) does NOT take on the responsibility of disposal of the finished product.

The output of the receiving establishment: processing services.

Measuring Output

SIAP

33

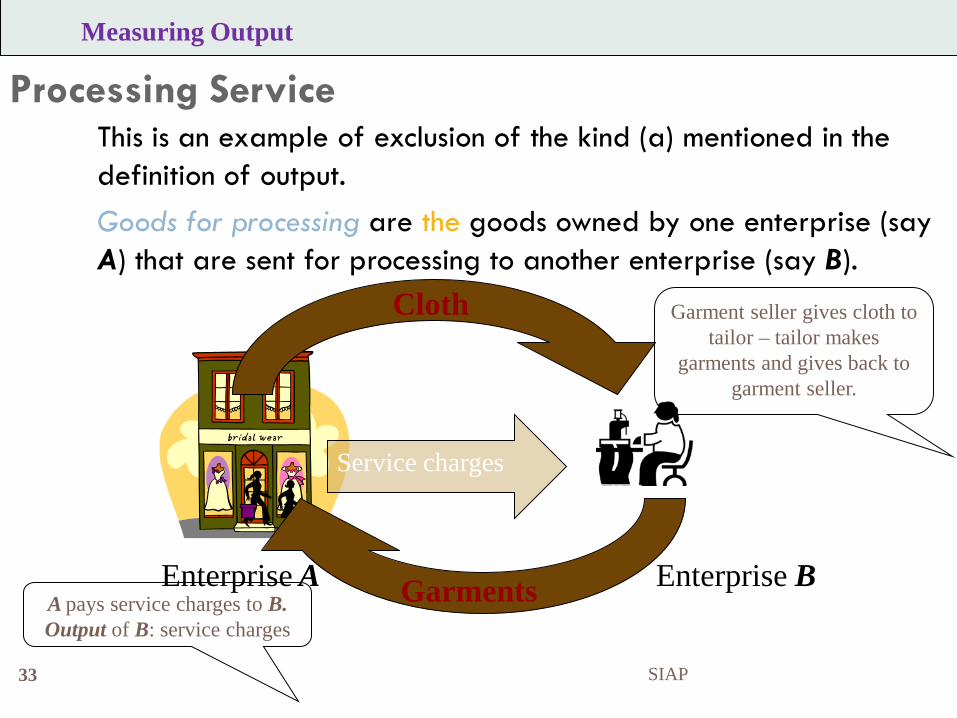

Processing Service This is an example of exclusion of the kind (a) mentioned in the definition of output. Goods for processing are the goods owned by one enterprise (say A) that are sent for processing to another enterprise (say B).

Enterprise B Enterprise A

Garments

Cloth

Service charges

Measuring Output

Garment seller gives cloth to tailor – tailor makes

garments and gives back to garment seller.

A pays service charges to B. Output of B: service charges

SIAP

34

Output - Processing Service

The receiving enterprise B (for example an independent tailor working for a garment-seller) does not take on the responsibility or the risk of disposal of the finished product.

The enterprise A (garment-seller in the example) owns both the raw materials (cloth) sent for processing as well as the finished product (garments).

Gross value of output:

GVO of A: value of garments

GVO of B: processing services it receives from A.

Measuring Output

SIAP

35

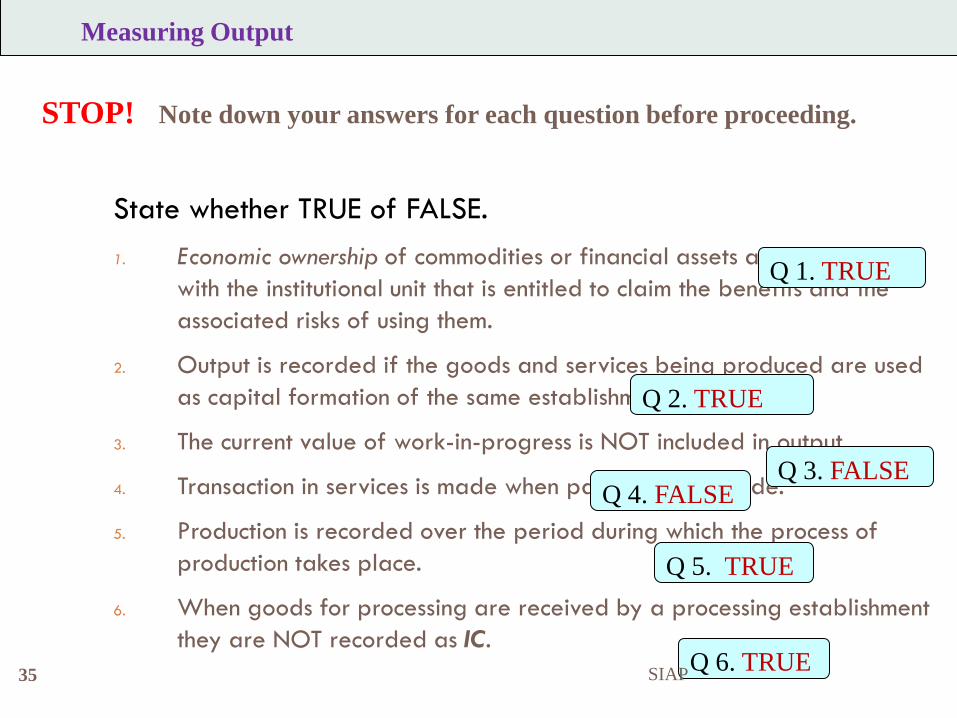

State whether TRUE of FALSE. 1. Economic ownership of commodities or financial assets and liabilities lie

with the institutional unit that is entitled to claim the benefits and the associated risks of using them.

2. Output is recorded if the goods and services being produced are used as capital formation of the same establishment

3. The current value of work-in-progress is NOT included in output.

4. Transaction in services is made when payments are made.

5. Production is recorded over the period during which the process of production takes place.

6. When goods for processing are received by a processing establishment they are NOT recorded as IC.

Q 1. TRUE

Q 2. TRUE

Q 3. FALSE Q 4. FALSE

Q 5. TRUE

Q 6. TRUE

STOP! Note down your answers for each question before proceeding.

Measuring Output

SIAP

36

End of Part-2

Lesson V

SIAP

Lesson: V Part 3 Production and Generation of Income Accounts

An Introduction to System of National Accounts – Integrated Transaction Accounts

Second Intermediate-Level e-Learning Course on 2008 System of National Accounts

May – July 2014

SIAP 37

Contents 38

Measuring Intermediate consumption

Compensation of Employees Data Needs

SIAP

39

Measuring Intermediate Consumption

SIAP

40

Intermediate Consumption (IC)

IC is recorded when it is actually used in the process of production.

Thus, the entire purchase of raw materials is not always included in IC.

IC of raw materials is measured as:

purchases less CII of raw materials.

Measuring IC

SIAP

41

IC in Goods for Processing

When goods are sent for processing from a unit A to unit B

IC of B does NOT include ‘goods received for processing’,

but, IC of A includes ‘goods sent for processing’.

Measuring IC

SIAP

42

R&D and Mineral Exploration

The output of mineral exploration and R&D activities are capitalised, i.e. treated as capital formation.

The output of such activities are mostly valued at cost. Thus, expenditures on goods & non-factor services for own-

account capital formation, such as mineral exploration,

R&D and

constructions for own use

are included in IC, GVO and GFCF.

Measuring IC

SIAP

43

Military Inventories

Military weapon systems are classified as fixed assets. Single-use items, such as ammunition, missiles, rockets,

bombs, etc., are treated as military inventories These form part of IC when put to use.

Measuring IC

SIAP

44

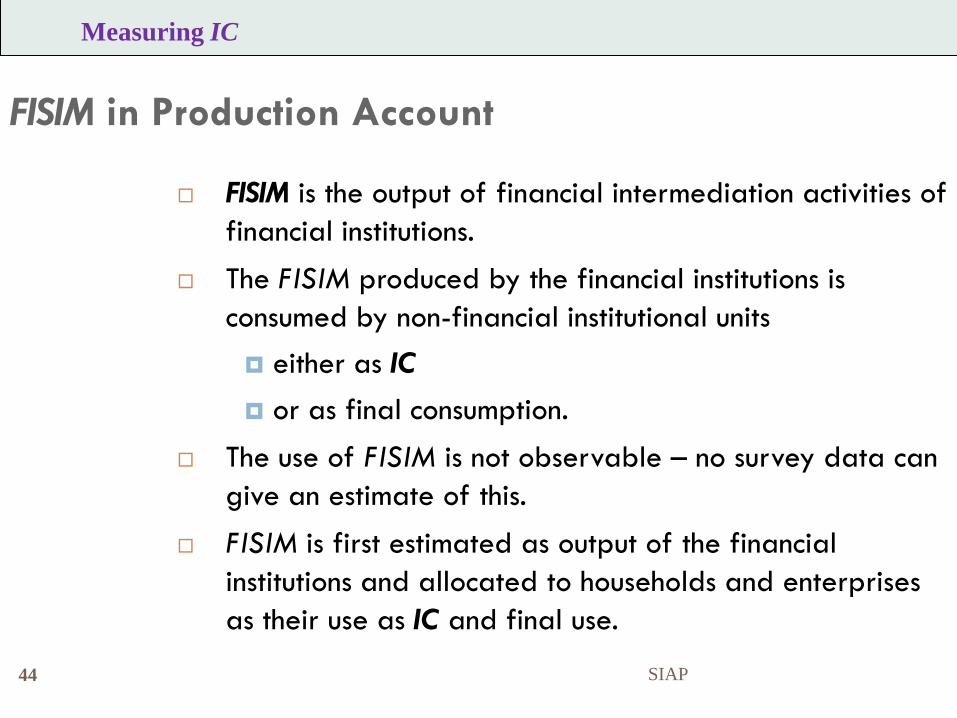

FISIM in Production Account

FISIM is the output of financial intermediation activities of financial institutions.

The FISIM produced by the financial institutions is consumed by non-financial institutional units either as IC

or as final consumption. The use of FISIM is not observable – no survey data can

give an estimate of this.

FISIM is first estimated as output of the financial institutions and allocated to households and enterprises as their use as IC and final use.

Measuring IC

SIAP

45

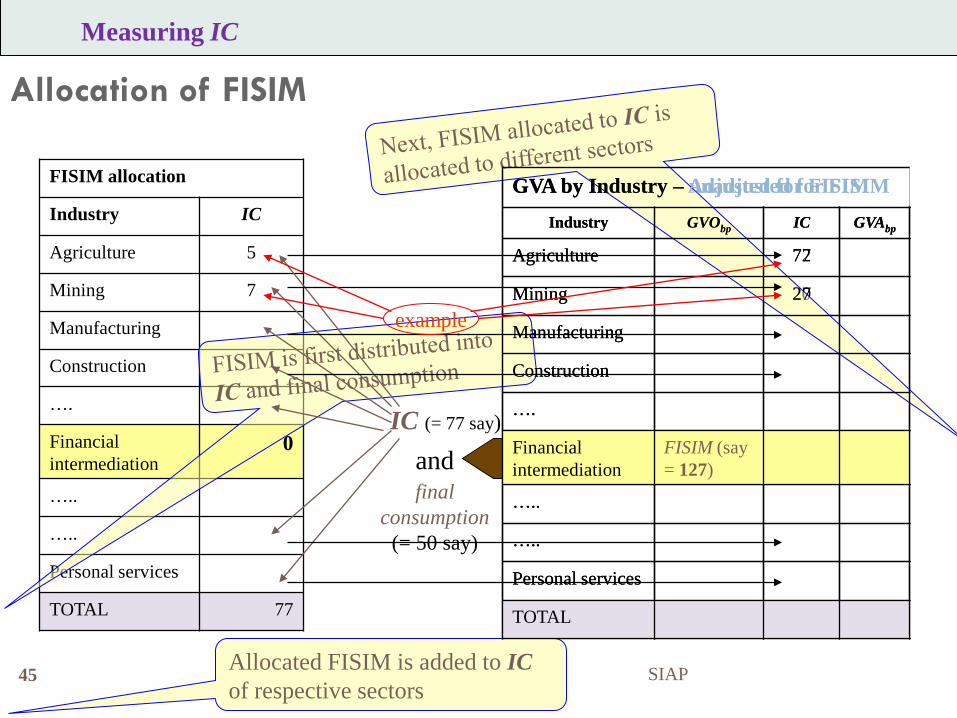

Allocation of FISIM

Measuring IC

GVA by Industry – unadjusted for FISIM Industry GVObp IC GVAbp

Agriculture 72

Mining 20

Manufacturing

Construction

….

Financial intermediation

FISIM (say = 127)

…..

…..

Personal services

TOTAL

FISIM allocation

Industry IC

Agriculture 5

Mining 7

Manufacturing

Construction

….

Financial intermediation

0

…..

…..

Personal services

TOTAL 77

allocated to

IC (= 77 say)

and final

consumption (= 50 say)

Allocated FISIM is added to IC of respective sectors

GVA by Industry – Adjusted for FISIM Industry GVObp IC GVAbp

Agriculture 77

Mining 27

Manufacturing

Construction

….

Financial intermediation

FISIM (say = 127)

…..

…..

Personal services

TOTAL

example

SIAP

46

Rearranged Transaction in SNA In the SNA, often a single monetary transaction taking place

between institutional units is decomposed to more than one transactions.

The values of certain transactions in business accounts are thus rearranged.

Three kinds of rearrangements of transactions partitioning, rerouting and reallocating

often involve a component of IC.

Measuring IC

SIAP

47

Measuring Compensation of Employees

SIAP

48

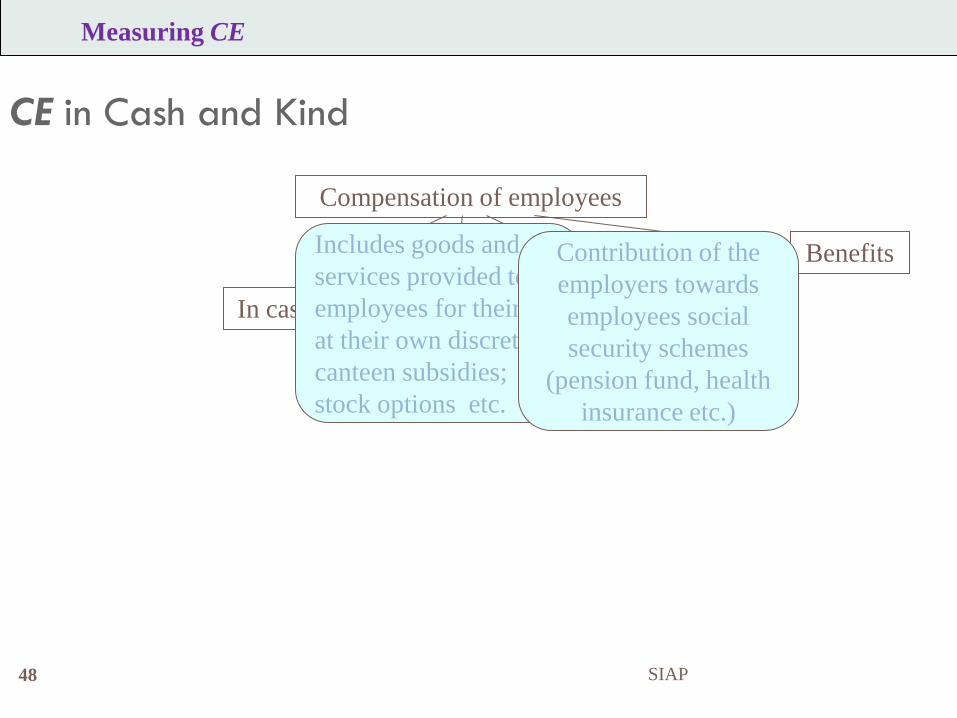

CE in Cash and Kind

Measuring CE

Compensation of employees

In cash In kind Employers’ social contribution

Benefits Includes goods and services provided to employees for their use at their own discretion; canteen subsidies; stock options etc.

Contribution of the employers towards employees social security schemes

(pension fund, health insurance etc.)

SIAP

49

Rerouting Employers’ Social Contribution

Social Security Agency

Employee Employer

CE

Contribution

Contribution

Measuring IC

SIAP

50

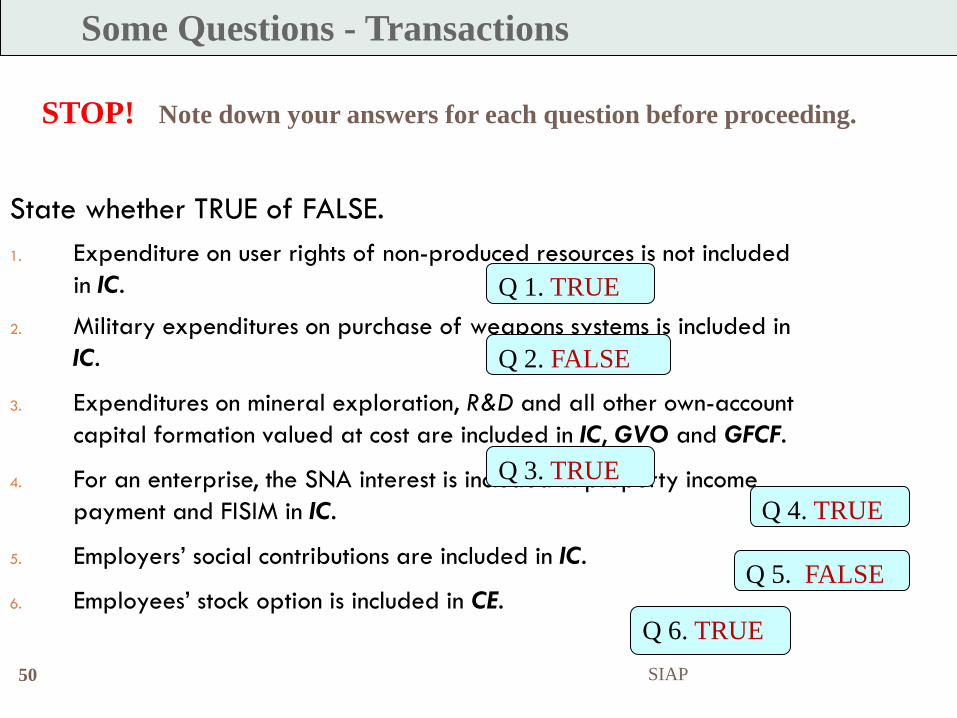

State whether TRUE of FALSE. 1. Expenditure on user rights of non-produced resources is not included

in IC.

2. Military expenditures on purchase of weapons systems is included in IC.

3. Expenditures on mineral exploration, R&D and all other own-account capital formation valued at cost are included in IC, GVO and GFCF.

4. For an enterprise, the SNA interest is included in property income payment and FISIM in IC.

5. Employers’ social contributions are included in IC.

6. Employees’ stock option is included in CE.

Some Questions - Transactions

Q 1. TRUE

Q 2. FALSE

Q 3. TRUE Q 4. TRUE

Q 5. FALSE

Q 6. TRUE

STOP! Note down your answers for each question before proceeding.

SIAP

End of Lesson V

51

SIAP