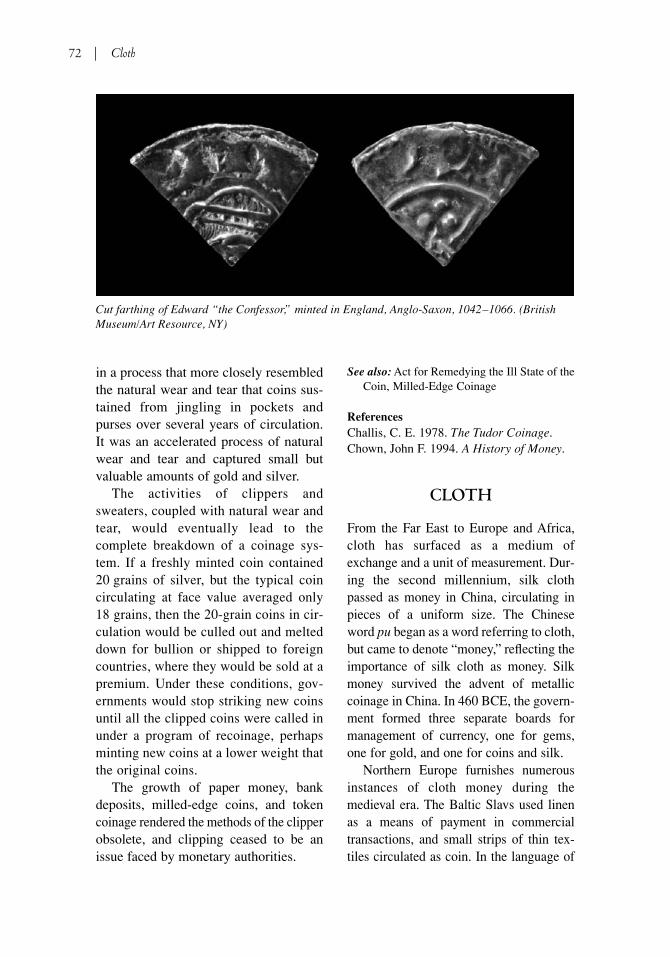

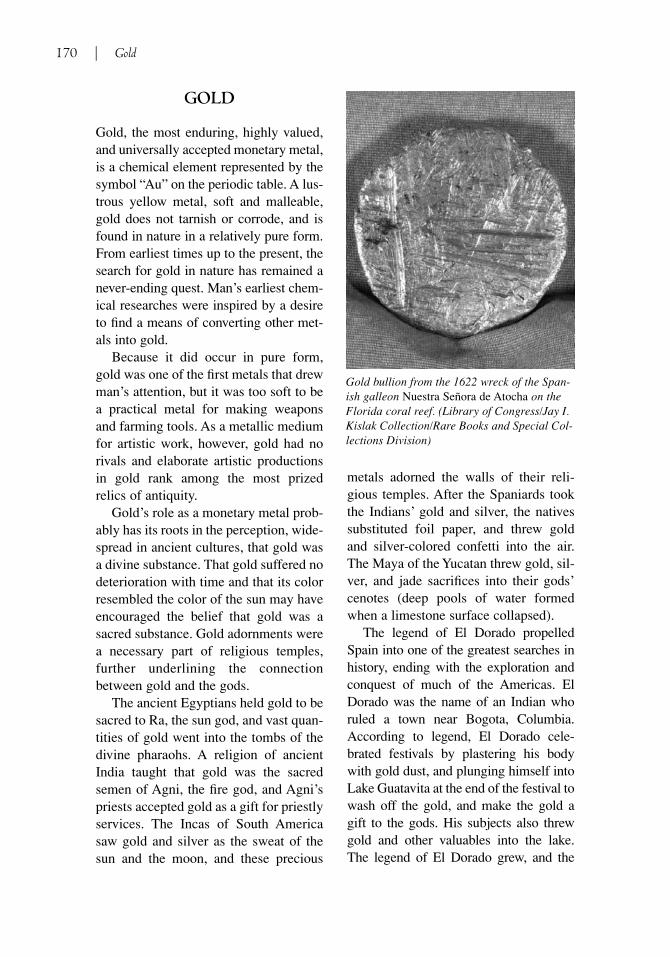

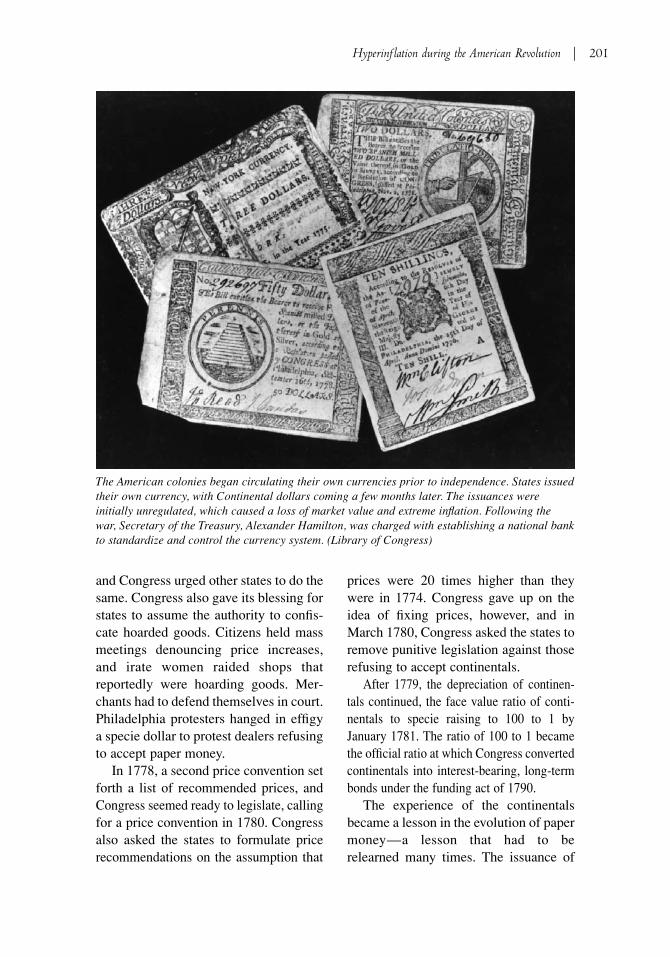

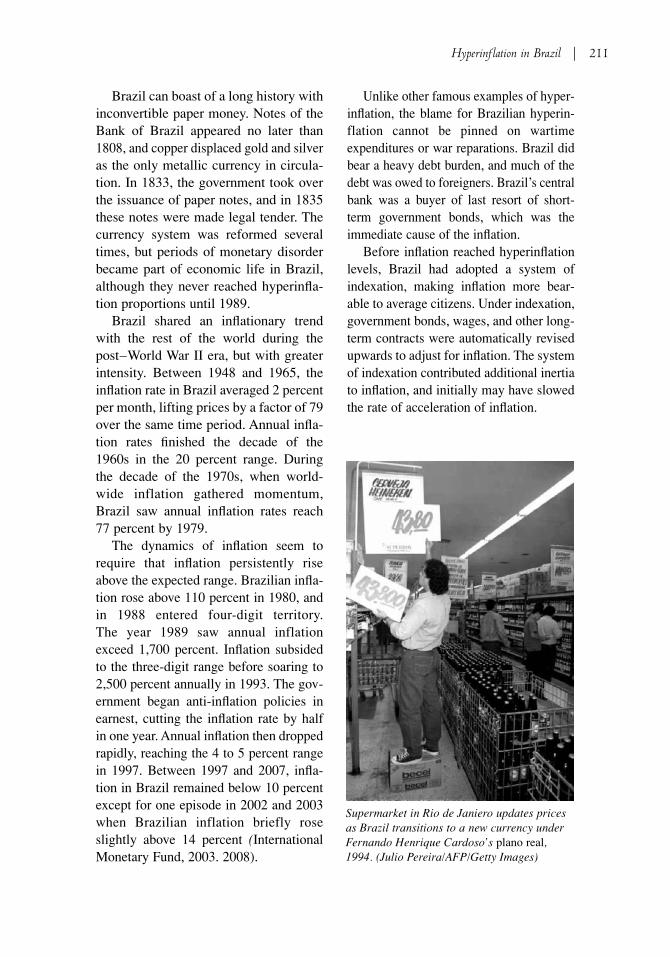

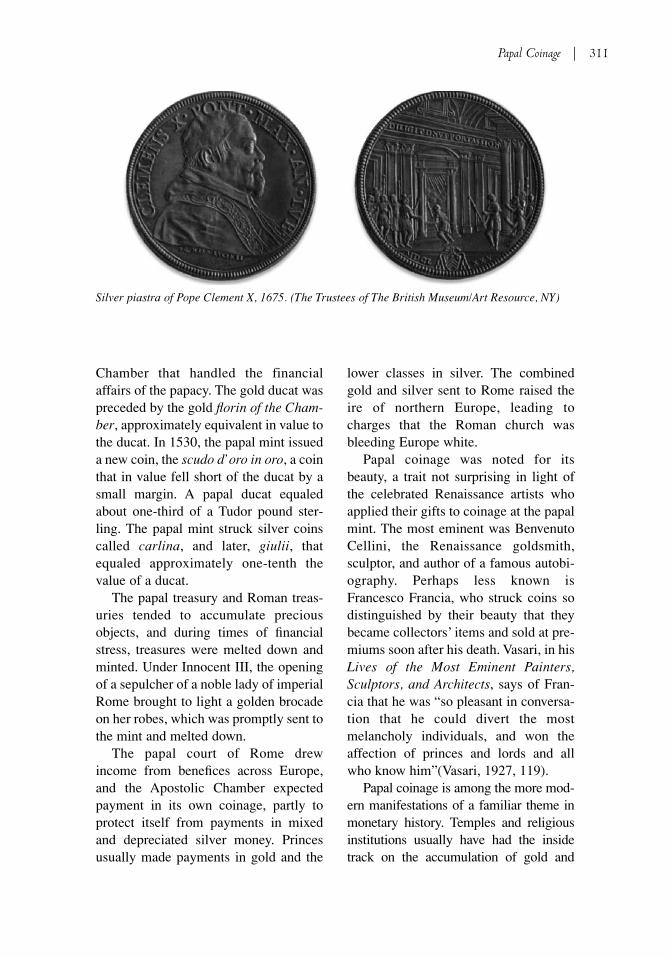

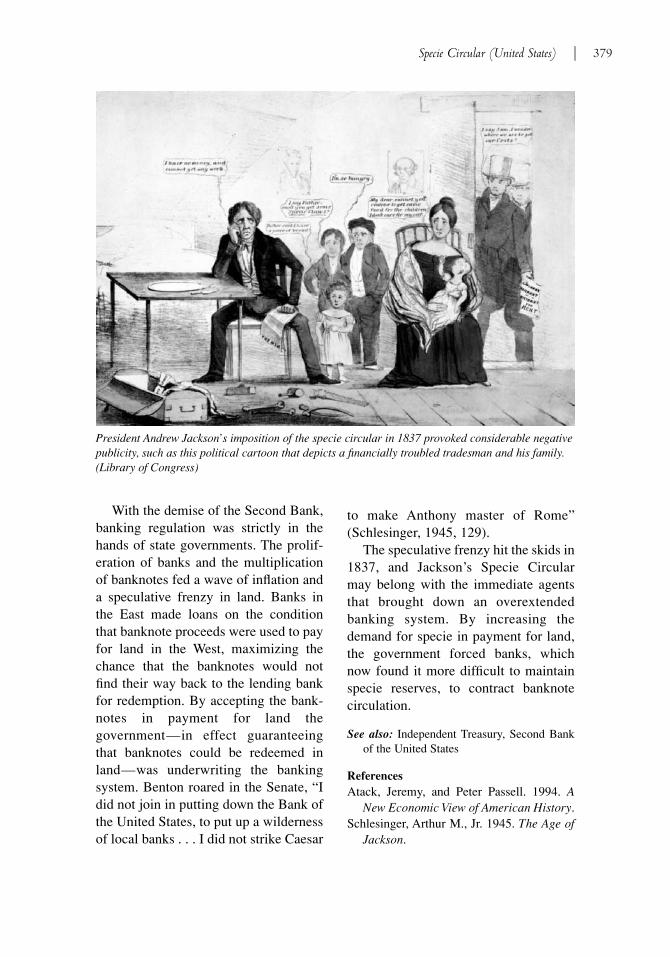

Современный бой. Оружие и тактика. Энциклопедия военного искусства.2003

description

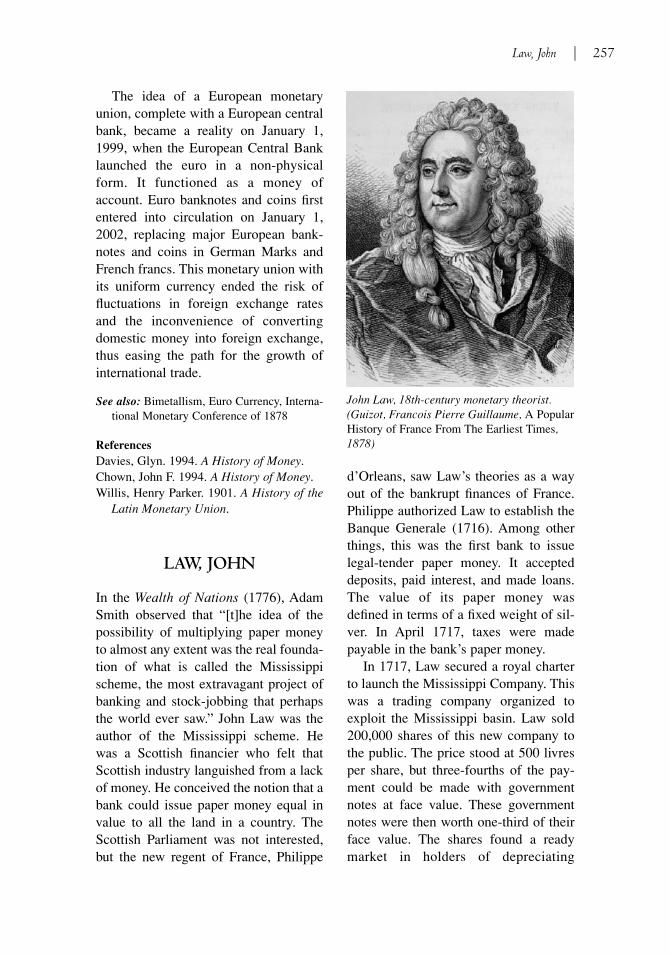

The Encyclopedia of Money

The Encyclopedia of Money

SECOND EDITION

Larry Allen

Copyright 2009 by ABC-CLIO, LLC

All rights reserved. No part of this publication may be reproduced, stored in a retrieval system, ortransmitted, in any form or by any means, electronic, mechanical, photocopying, recording, or oth-erwise, except for the inclusion of brief quotations in a review, without prior permission in writingfrom the publisher.

Library of Congress Cataloging-in-Publication Data

Allen, Larry, 1949-The encyclopedia of money / Larry Allen. — 2nd ed.

p. cm.Includes bibliographical references and index.ISBN 978-1-59884-251-7 (hard copy : alk. paper) — ISBN 978-1-59884-252-4 (ebook)

1. Money—Encyclopedias. 2. Monetary policy—Encyclopedias. I. Title. HG216.A43 2009332.403—dc22 2009035247

13 12 11 10 09 1 2 3 4 5

This book is also available on the World Wide Web as an eBook.Visit www.abc-clio.com for details.

ABC-CLIO, LLC130 Cremona Drive, P.O. Box 1911Santa Barbara, California 93116-1911

This book is printed on acid-free paper

Manufactured in the United States of America

v

Contents

List of Entries viiPreface to Second Edition xiIntroduction xiii

The Encyclopedia 1

Bibliography 447Glossary 475Index 481

vii

List of Entries

Act for Remedying the Ill State of the Coin(England)

Adjustable-Rate MortgagesAlchemyAmerican PennyAncient Chinese Paper MoneyAnnouncement EffectArgentine Currency and Debt CrisisAyr Bank

Balance of PaymentsBankBank Charter Act of 1833 (England)Bank Charter Act of 1844 (England)Bank Clearinghouses (United States)Bank for International SettlementsBanking Acts of 1826 (England)Banking and Currency Crisis of EcuadorBanking CrisesBanking SchoolBank of AmsterdamBank of DepositBank of EnglandBank of FranceBank of JapanBank of ScotlandBank of VeniceBank Restriction Act of 1797 (England)Barbados Act of 1706Barter

Beer Standard of Marxist AngolaBelgian Monetary Reform: 1944–1945Bills of ExchangeBimetallismBisected Paper MoneyBland–Allison Silver Repurchase Act of

1878Bretton Woods SystemBritish Gold SovereignByzantine Debasement

Caisse d’EscompteCapital ControlsCapital FlightCarolingian ReformCase of Mixt MoniesCattleCeltic CoinageCentral BankCentral Bank IndependenceCertificate of DepositCheckChilean InflationChinese Silver StandardClippingClothCocoa Bean CurrencyCoinage Act of 1792 (United States)Coinage Act of 1834 (United States)Coinage Act of 1853 (United States)

viii | List of Entries

Coinage Act of 1965 (United States)Commodity Monetary StandardCommodity Money (American Colonies)Commodity Price BoomComposite CurrencyCopperCore InflationCorso Forzoso (Italy)Counterfeit MoneyCredit CrunchCredit RatingsCrime of ‘73 (United States)Currency Act of 1751 (England)Currency Act of 1764 (England)Currency CrisesCurrency–Deposit RatioCurrency SchoolCurrency SwapsCurrent Account

De a Ocho Reales (Pieces of Eight)Debit CardDecimal SystemDepository Institution Deregulation and

Monetary Control Act of 1980 (UnitedStates)

Deutsche BundesbankDeutsche MarkDissolution of Monasteries (England)DollarDollar Crisis of 1971Dollarization

East Asian Financial CrisisEnglish PennyEquation of ExchangeEuro CurrencyEurodollarsEuropean Central BankEuropean Currency UnitExchequer Orders to Pay (England)

Federal Open Market Committee (FOMC)Federal Reserve SystemFinancial Services Modernization Act of

1999 (United States)First Bank of the United StatesFisher EffectFloat

Florentine FlorinFood StampsForced SavingsForeign Debt CrisesForeign Exchange MarketsForestall SystemFort KnoxFranklin, Benjamin (1706–1790)Free BankingFree Silver MovementFrench Franc

Generalized Commodity Reserve CurrencyGhost MoneyGlass–Steagall Banking Act of 1933

(United States)Global DisinflationGoat Standard of East AfricaGoldGold Bullion StandardGold DustGold Exchange StandardGold Mark of Imperial GermanyGold Reserve Act of 1934 (United States)Gold RushesGoldsmith BankersGold-Specie-Flow MechanismGold StandardGold Standard Act of 1900 (United States)Gold Standard Act of 1925 (England)Gold Standard Amendment Act of 1931

(England)Great Bullion FamineGreat DebasementGreek Monetary Maelstrom: 1914–1928Greenbacks (United States)Gresham’s LawGuernsey Market House Paper Money

High-Powered MoneyHot MoneyHouse of St. GeorgeHyperinflation during the American

RevolutionHyperinflation during the Bolshevik

RevolutionHyperinflation during the French RevolutionHyperinflation in ArgentinaHyperinflation in Austria

Hyperinflation in BelarusHyperinflation in BoliviaHyperinflation in BrazilHyperinflation in BulgariaHyperinflation in ChinaHyperinflation in GeorgiaHyperinflation in PeruHyperinflation in Post-Soviet RussiaHyperinflation in Post–World War I

GermanyHyperinflation in Post–World War I

HungaryHyperinflation in Post–World War II

HungaryHyperinflation in Post–World War I PolandHyperinflation in the Confederate States of

AmericaHyperinflation in UkraineHyperinflation in YugoslaviaHyperinflation in Zimbabwe

Inconvertible Paper StandardIndependent Treasury (United States)IndexationIndian Silver StandardInflation and DeflationInflationary ExpectationsInflation TaxInterest RateInterest Rate TargetingInternational Monetary Conference of 1878International Monetary FundIslamic BankingIvory

Japanese DeflationJuilliard v. Greenman (United States)

Labor NotesLand Bank System (American Colonies)Latin Monetary UnionLaw, JohnLaw of One PriceLeather MoneyLegal Reserve RatioLegal TenderLiquidityLiquidity CrisisLiquidity Trap

Liquor MoneyLiverpool Act of 1816 (England)Lombard BanksLondon Interbank Offered Rate

Massachusetts Bay Colony MintMassachusetts Bay Colony Paper IssueMedici BankMexican Peso Crisis of 1994Milled-Edge CoinageMissing MoneyMonetarismMonetary AggregatesMonetary Law of 1803 (France)Monetary MultiplierMonetary NeutralityMonetary TheoryMoneyerMoney LaunderingMoney Market Mutual Fund AccountsMughal Coinage

NailsNational Bank Act of 1864 (United States)Negotiable Order of Withdrawal AccountsNew York Safety Fund System

Open Market OperationsOperation BernhardOptimal Currency AreaOttoman Empire Currency

Pacific Coast Gold StandardPapal CoinagePig Standard of New HebridesPlaying-Card Currency of French CanadaPontiac’s Bark MoneyPostage StampsPotosi Silver MinesPound SterlingPOW Cigarette StandardPrice Revolution in Late Renaissance EuropePrice StickinessPrivate Paper Money in Colonial

PennsylvaniaProducer Price IndexPromissory Notes Act of 1704 (England)Propaganda MoneyPublic Debts

List of Entries | ix

Quattrini Affair

Radcliffe ReportReal Bills DoctrineRedenominationRentenmarkReport from the Select Committee on the

High Price of BullionRepurchase AgreementsResumption Act of 1875 (United States)Return to Gold: 1300–1350Rice CurrencyRiksbank (Sweden)Roman Empire InflationRossel Island Monetary SystemRoyal Bank of ScotlandRussian Currency Crisis

Salt CurrencySavings and Loan Bailout (United States)Scottish Banking Act of 1765Second Bank of the United StatesSecuritizationSeigniorageSeizure of the Mint (England)Sherman Silver Act of 1890 (United States)ShinplastersSiege MoneySilverSilver PlateSilver Purchase Act of 1934 (United

States)Slave CurrencySlave Currency of Ancient IrelandSnakeSocial Dividend Money of MarylandSpanish Inconvertible Paper StandardSpanish Inflation of the 17th CenturySpartan Iron CurrencySpecial Drawing RightsSpecie Circular (United States)SterilizationStop of the Exchequer (England)Suffolk SystemSugar Standard of the West IndiesSuspension of Payments in War of 1812

(United States)

Sweden’s Copper StandardSweden’s First Paper StandardSweden’s Paper Standard of World War ISweep AccountsSwiss BanksSwiss FrancSymmetallism

Tabular Standard in Massachusetts BayColony

TalerTallies (England)TeaTouchstoneTrade DollarTreasury NotesTrial of the Pyx (England)Troubled Asset Relief ProgramTurkish InflationTzarist Russia’s Paper Money

Universal BanksU.S. Financial Crisis of 2008–2009Usury Laws

Vales (Spain)Value of MoneyVariable Commodity StandardVehicle CurrencyVellonVelocity of MoneyVenetian DucatVirginia Colonial Paper CurrencyVirginia Tobacco Act of 1713

Wage and Price ControlsWampumpeagWendish Monetary UnionWhale Tooth Money in FijiWildcat Banks (United States)The Wizard of OzWorld Bank

Yap MoneyYeltsin’s Monetary Reform in RussiaYenYield Curve

x | List of Entries

xi

Preface to the Second Edition

The 2008–2009 financial crisis holds implications for the subject of money that makea new edition of The Encyclopedia of Money timely. A decade has elapsed since thefirst edition of The Encyclopedia of Money came off the press. In that decade, the setof money-related issues and problems underwent drastic change. The last centurydrew to a close with the widespread perception that inflation remained public enemynumber one where money was concerned. The decade of the 1970s had not only seenthe United States suspend the convertibility of dollars into gold, but it had also seenrampant inflation. Keeping inflation corralled became the preoccupation of monetaryauthorities around the world. The proper management of fiat monetary systems as apath to price stability became the central concern of economic research.

Experience with inflation exerts subtle influences on public policy. Inflation makesit easier to resell things at higher prices than were originally paid for them. As house-holds and businesses find it easy to sell things at a profit, they acquire greater confi-dence in free markets. Because government regulation is the greatest enemy of freemarkets, households and business are ready to do away with it. Government regula-tion becomes something that might hold a price below a market price, or subtract fromthe profits earned when assets are sold for a profit. Government regulation comes tobe viewed as a relic of Depression-era economics, as something that should be safelydismantled or ignored. Deflation has the opposite effect. Under deflation, few peoplewant to be left to the mercy of a market. Instead of seeing the market as their friend,households and businesses are more likely to view markets as the playground of cleverand sometimes unscrupulous intermediaries that know how to buy cheap and sell dear.Deflation leads to the perception that government regulations are needed to protect theless informed from the better informed.

As governments around the world exalted free markets, a less conspicuous trendwas also making itself felt. The worldwide average rate of inflation gradually subsidedin the 1990s. It was as if the war against inflation had succeeded all too well. By themid-1990s, Japan was reporting deflation. In 2008, U.S. monetary authorities gave

free reign to monetary growth, trying to prevent a recession from evolving into a trendof deflation. If fear of deflation replaces fear of inflation, the idea of policing marketswith government regulations may rise from the ashes and enjoy new prestige. Theabsence of inflation removes some of the fears of regulations and weakens confidencein free markets. A wave of failures in financial institutions suggests a need for stricterand more conscientious regulation.

Whether deflation develops in the United States remains to be seen. Certainly, fearof depression has led the U.S. monetary authorities to embrace Depression-era mone-tary policies.

In a nutshell, the focus of money-related issues shifted from the concerns associ-ated with rising inflation to the concerns associated with shrinking inflation, and fromthe concerns associated with shrinking inflation to the concerns associated with defla-tion. This new edition of The Encyclopedia of Money addresses these new issues intransparent language.

xii | Preface to the Second Edition

xiii

Introduction

Money serves four basics functions in an economic system. It acts as (1) a medium ofexchange, (2) a unit of measure, (3) a store of value, and (4) a standard of deferredpayment.

As a medium of exchange, money must be universally accepted in exchange. Itmust be something always accepted in trade. In prisoner-of-war camps, cigarettes haveserved as a medium of exchange, and in the northern reaches of the earth, furs havecirculated as a medium of exchange. Livestock and precious metals have a long his-tory of service as mediums of exchange.

Money must also act as a unit of measure, comparable to yards, gallons, tons, cubicfeet, or any other measure. British pounds sterling, U.S. dollars, Japanese yen, Germanmarks, and French francs all serve as units of measurement. A consumer can buy10 gallons worth of gasoline or $10 worth of gasoline. The Hudson Bay trading postsin Canada measured sales and profits in terms of beaver pelts, and Virginia colonistspriced goods in terms of pounds of tobacco.

Anything meeting all of the demands placed on money must be satisfactory as a storeof value. That is, it must preserve its value over a length of time. Perishable commodi-ties rarely serve as money because wealth stored in perishable commodities is doomedto extinction. Precious metals such as gold and silver, known for resistance to corrosionand natural deterioration, are the most prized as monetary commodities and have fewrivals as commodities that preserve value over time. Livestock reproduce, allowing themto preserve value over time, and even earn a form of interest. Inflation is the chief enemyof paper money because it renders the paper money useless as a store of value.

Money should also furnish society with a standard of deferred payment, enablingdebtors and creditors to negotiate long-term contracts. Creditors want assurance thatdebtors cannot legally discharge debts with money possessing less purchasing powerthan the money originally borrowed. An unanticipated depreciation of the currencyshortchanges creditors and gives debtors a windfall gain, arbitrarily redistributingincome from creditors to debtors.

On the other hand, if money becomes unusually abundant, debtors easily find themeans to repay debts, and creditors find the money repaid to them is worth less.Debtors are at risk if currency unexpectedly appreciates, increasing what debtors haveto repay creditors in real terms. Unexpected currency appreciation redistributes incomein favor of creditors over debtors. Because those who need to borrow money are usu-ally worse off than those who have money to lend, an income redistribution favoringcreditors is likely to cause hard feelings among those who already feel they get lessthan their share of income. Monetary issues are the focal point of a not-so-secret warbetween debtors and creditors.

Money falls within two broad categories, commodity money and fiat money. Com-modity money makes use of some commodity, such as tobacco, rice, gold, or silver,that has an intrinsic value, or market value independent of any government decreesanctioning the commodity as legal tender for payment of private and public debts.Commodity monetary standards may make use of tokens or paper circulating money,but the circulating money can always be redeemed in a monetary commodity at anofficial rate. Under the gold standard, the United States government committed itselfto selling gold for $35 per ounce. Fiat money has no intrinsic value; that is, it has nomarket value independent of a government decree establishing it as legal tender forprivate and public debts. Modern monetary systems are called inconvertible paperstandards, because the fiat money issued by these systems cannot be converted into acommodity at an official rate. Fiat money has value because governments give them-selves a monopoly on the privilege to issue fiat money, enabling them to limit its sup-ply, and governments use their power to adjudicate disputes to make the money legaltender for all debts. By limiting the supply and creating a need, the government con-fers value on paper money that has little or no intrinsic value.

Two commodities, gold and silver, have been promoted as the aristocrats of com-modity money. Until the 19th century, silver usually prevailed as the predominantform of commodity money, punctuated by intervals of bimetallism, which made useof both gold and silver and established a fixed ratio that set the value of each metal interms of the other. Aside from the Byzantine period, when gold reigned supreme, thehegemony of silver lasted from the time of Alexander the Great until the 19th century.

Historically, precious metals have had a funny way of showing up and disappear-ing as civilizations waxed and waned. The silver mines of Laurium helped finance thegolden age of Greece, and the decline of the Roman Empire coincided with theexhaustion of the silver mines in Spain and Greece. The stagnation of Western Europeduring the Middle Ages may be explained by the virtual disappearance of preciousmetals during that era. The economic expansion of Europe that led to the eventualworld dominance of European civilization in the 19th century followed the Europeandiscovery of vast precious metal deposits in the New World.

The much-vaunted gold standard, the demise of which is still mourned by a fewtrue believers, actually represents a relatively late development in monetary history.The gold standard is a recent upstart compared to silver and bimetallic standards. Onlyin the 50 years preceding World War I (1914–1918) did gold become the sole standardof purchasing power, completely eclipsing the role of silver in the world’s monetarysystem.

xiv | Introduction

The fascination with gold may be a relic of the awe that surrounded money in someprimitive societies. The word “taboo” originated from the sacred character and atmos-phere of mystery that surrounded primitive money in islands of the South Pacific. Inthe Fiji Islands, sperm whale teeth, called “tambua,” (of which “taboo” is a variant),acted as money and conferred social status on their owners. The power of a whaletooth guaranteed compliance with any request that accompanied it as a gift. On RosselIsland, some of the most valuable units of shell money could only be handled in acrouched position, and many of these units were thought to have been handed downfrom the beginning of time. In parts of the Philippines, women were not allowed toenter sacred storehouses where rice money was kept.

John M. Keynes, a famous British economist in the first half of the twentieth cen-tury, observed in volume two of his Treatise on Money (1930) that gold had“enveloped itself in a garment of respectability as densely respectable as was ever metwith, even in the realms of sex or religion” (259). Concerning the power that a rela-tively small amount of gold played in the world’s monetary affairs, Keynes wrote inthe same work that “[a] modern liner could convey across the Atlantic in a single voy-age all the gold which has been dredged or mined in seven thousand years” (259). Theworld’s supply of gold has increased since Keynes wrote these words, but the supplyremains small in comparison to the important role it has always played in monetaryaffairs. Even during Keynes’s time, monetary gold lay out of sight in the undergroundvaults of central banks, and gold transactions were conducted by paper notations (earmarking), rather than physically moving gold to different locations.

The strength of gold as a monetary commodity lay in the hold it commanded on thehuman imagination, but its weakness lay in its restricted supply, which failed to keeppace with the growth of trade. The gold standard forced the world’s economies tostruggle constantly against what today would be called a tight money policy. Althoughfresh supplies of gold occasionally burst forth, furnishing a brief respite from tightmoney, the long-term trend was one of deflation owing to the limited money supplies.

The world’s trading partners severed the connection between domestic money sup-plies and domestic gold reserves in the 1930s, hoping that more lax monetary policieswould reinflate the depression-ridden economies of that era. Under the Bretton Woodssystem of the post–World War II era, domestic currencies remained convertible intogold at the request of foreign central banks, but not at the request of private individu-als. During the Bretton Woods era, gold reserves failed to keep pace with the need formonetary growth, and by agreement of the members of the Bretton Woods system, aform of “paper gold” was created called “standard drawing rights.” Standard drawingrights are really only entries in accounting logs, but they act as reserves of gold or foreign currencies.

Since 1971, the world’s major trading partners have been on inconvertible paperstandards. The United States dollar and other major currencies became strictly fiatmoney, inconvertible into gold even at the request of foreign central banks.

The burst of inflation of the 1970s may have been due partially to a void in mone-tary discipline left by the departure from the last vestiges of the gold standard. Theexperience of Japan between 1999 and 2005, however, cautions against generaliza-tions about the inevitability of inflation under a fiat monetary system. Japan posted

Introduction | xv

consumer price deflation for seven consecutive years. Japan’s experience would nothave been unusual if Japanese authorities had induced deflation by a restrictive mon-etary policy and exorbitant interest rates. Before Japan’s episode of deflation, theworld’s monetary authorities had already learned how to restrict the rate of monetarygrowth to noninflationary levels. By the mid-1990s, inflation had subsided to insignif-icant levels virtually worldwide. Japan’s experience appeared unique because defla-tion persisted long after short-term Japanese interest rates fell to near zero levels.Japan’s deflation existed under conditions of relatively lax monetary policies.

In 2009, the United States is trying to formulate a policy in light of previous expe-riences with inflation and Japan’s recent experience with deflation. The outcomeshould reveal clues and hints that are even more interesting about the nature of money.

xvi | Introduction

The Encyclopedia of Money

1

A

ACT FOR REMEDYINGTHE ILL STATE OF THE

COIN (ENGLAND)

In 1696, Parliament enacted the Act forRemedying the Ill State of the Coin,after one of the famous currency debatesin history, which pitted those whofavored return to a historical currencystandard against those who favored rati-fying past depreciation.

Toward the end of the 17th century, theold hammered-silver coinage accountedfor the bulk of England’s circulatingcoinage. The coinage was worn andclipped, some dating back to Elizabeth I,effectively reducing the silver weight rel-ative to the face value of each coin.Freshly struck milled coins disappearedas fast as they left the mint as Gresham’slaw played itself out—bad money chas-ing out good. The milled coins, immunefrom clipping, enjoyed greater silvervalue and were far more beautiful.

Once the government committed itselfto recoinage, two schools of thought

arose about the principles that shouldguide it. John Locke, the famous philoso-pher who influenced the American Revo-lutionaries, stood firmly in favor ofmaintaining the historical weight stan-dard of English coins. Locke’s proposalrequired that the lost silver content ofworn and clipped coins be restored inrecoinage, substantially increasing thegovernment’s costs. William Lowndes,secretary to the treasury, proposedrecoinage at a lower silver content for agiven face value, bringing the silver con-tent of freshly minted coins into line withthe silver content of worn, clipped coins.Wear and clipping had on average costthe coinage 20 to 25 percent of silver con-tent. Supporting Lowndes’s proposalwere numerous historical precedents forstabilizing depreciated coins at currentlevels. Locke described the proposal toreduce the silver content relative to facevalue as “a clipping done by publicauthority, a public crime.” Locke was alsoconcerned that reducing the silver contentenabled the government to repay debtwith cheaper money.

Sir Isaac Newton, another toweringfigure who was a player in this drama,served as warden of the mint duringrecoinage. Newton appears to havefavored devaluation and apparently fore-saw that refusing to devalue wouldincrease the amount of silver each goldcoin would buy, increasing the value ofgold at home, causing gold to flow in andsilver to flow out.

Parliament sided with Locke, and theAct for Remedying the Ill State of theCoin, with minor exceptions, mirroredLocke’s views. The cost of the recoinage

surpassed all expectations, totaling £2.7 million, more than half of the gov-ernment’s revenue. In the spirit of theEnlightenment, the government enacteda tax on windows to help pay for therecoinage. In addition to the Tower mint,several branch mints were pressed intoservice, and the recoinage was com-pleted in three years.

The mechanics of the plan for callingin the old coinage caused no smallamount of discontent. For a certainperiod of time, the government acceptedat face value worn and clipped coins for

2 | Act for Remedying the Ill State of the Coin (England)

Woodcut illustrating the alchemical bonding of gold and silver, from Von dem grossen SteinUhralten, Strasbourg, 1651. (Jupiterimages)

the payment of taxes and governmentobligations. Landowners with propertytaxes to pay, and merchants with cus-toms’ duties to pay, benefited from theplan, buying up worn and clipped coinsat a discount and paying their taxes withthem. Wage earners and the poor hadless need of the money to pay taxes, andoften found the soon-to-be discontinuedmoney accepted only at a discount byshopkeepers.

The act struck a blow for upholdingthe sanctity of a monetary standard, evenat great expense, to protect the interest ofcreditors, especially when governmentwas a major debtor. Newton correctlyanticipated, however, that the act wouldput England on the road to the gold stan-dard. Gold flowed into England, where itcould purchase silver cheaply. The silverwas then sold abroad at a profit.

See also: Clipping, Great Debasement, PoundSterling

ReferencesChown, John F. 1994. A History of Money.Feavearyear, Sir Albert. 1963 The Pound

Sterling: A History of English Money,2nd ed.

Horton, Dana S. 1983. The Silver Pound andEngland’s Monetary Policy since theRestoration, together with the History ofthe Guinea.

ADJUSTABLE-RATEMORTGAGES

An adjustable-rate mortgage (ARM)provides for varying interest rates overthe life of the mortgage. It forces theborrower to shoulder some of the risksthat fixed-rate loans place on the lender.Key to the rationale for ARMs is thealmost one-to-one relationship between

short-term interest rates and inflationrates. Over the life of a 30-year, fixed-rate mortgage, inflation ranks among thebiggest enemies that a lender faces.Increases in the inflation rate reduce thereal (inflation-adjusted) rate of interestthat a mortgage pays to a lender. Higherinflation reduces the real purchasingpower of each monthly payment whilepushing up the real operating cost of alender. If the inflation rate happens torise above a mortgage interest rate, thelender ends up earning a negative realinterest rate.

The high inflation rates of the 1970staught lenders the damage that inflationcan wreak on the interest incomeearned from mortgages. Lenders begandemanding higher interest rates on 30-year mortgages as insurance againsta wave of inflation wiping out the prof-its and capital of mortgage holders.Adjustable-rate mortgages developedas a way to get home buyers intohouses without paying the high interestrates attached to 30-year, fixed-ratemortgages.

Under an ARM, the mortgage interestrate at any given time is linked orindexed to a short-term interest rate. Twoshort-term, benchmark interest ratescommonly used for setting ARM interestrates are the London Interbank OfferedRate (LIBOR) and the one-year, constantmaturity treasury bond rate. The interestrate on an ARM is adjusted periodicallyto reflect changes in a benchmark inter-est rate. The home buyer benefitsbecause short-term interest rates are usu-ally lower than long-term interest rates,since short-term rates have less inflationrisk. The disadvantage to the home buyerlies in the risk that short-term interestrates go up, probably because of risinginflation or anti-inflation policies. If

Adjustable-Rate Mortgages | 3

short-term interest rates go up, themonthly payments on ARMs go up. WithARMs, the burden of accelerated infla-tion is born by the borrower instead ofthe lender. In turn for bearing the risk ofaccelerated future inflation, the homebuyer stands a chance getting by withlower interest rates. If inflation neverdrives up short-term interest rates overthe life of the loan, the home buyercomes out ahead.

Adjustable-rate mortgages come inseveral varieties. In some mortgages, themonthly payment can change everymonth, depending on the benchmarkinterest rate. Other mortgages allowchanges in monthly payments as infre-quently as every five years. The timeframe between rate changes is called the“adjustment period.” A mortgage with aone-year adjustment period is called aone-year ARM.

Many ARMs put a cap on the amountthat a mortgage interest rate can changefrom one adjustment period to the next.This provision protects home buyers fromlarge jumps in interest rates and monthlypayments. Other contracts put a limit onthe amount that monthly payments canincrease from one adjustment period tothe next. If interest rate adjustments callfor a 10 percent increase in monthly pay-ments, but the contract only allowsmonthly payments to go up 5 percent,then the unpaid interest will be added tothe balance of the mortgage. By law,nearly all ARMs have a cap on how highinterest rates can go over the life of amortgage.

One version of the ARM allows the home buyer to pay an initial interestrate well below the benchmark interestrate used for setting an ARM interestrate. The home buyer enjoys the lowinterest rate, often called a teaser rate,

for an initial period, such as a year. Thenthe interest rate is adjusted upwardaccording to the indexing formula tiedto the benchmark interest rate. If short-term interest rates happen to be rising atthe same time that a homeowner is tran-sitioning from the teaser rate to the fullyindexed, benchmark rate, then the homeowner may experience “paymentshock.” The large increase in monthlypayment may leave a home ownerunable to make a house payment. Thepractice of offering teaser rates con-tributed to the severity of the subprimemortgage crisis in the United States.

See also: U.S. Financial Crisis of 2008–2009

ReferenceFederal Reserve Board. 2009. Consumer

Handbook on Adjustable-Rate Mortgages.

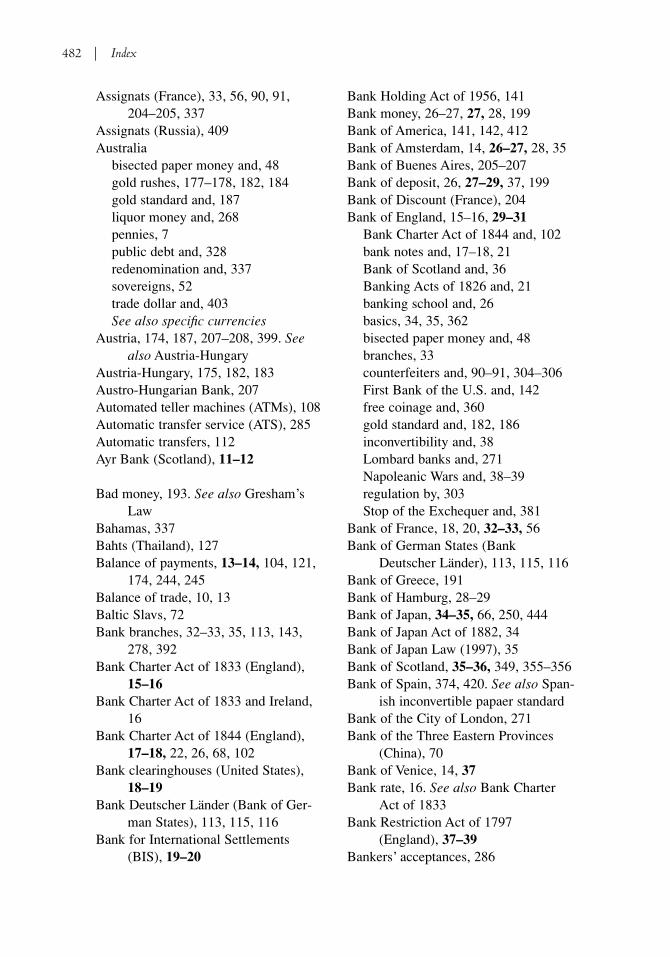

ALCHEMY

Alchemy was a pseudoscience that flour-ished during the Middle Ages. Its chiefaims were the transmutation of base met-als into gold and silver, and the discov-ery of an elixir of eternal youth. Thealchemists searched in vain for thephilosopher’s stone, a substance that, ifproperly treated, would allegedly trans-mute lead, iron, copper, or tin into goldor silver—but particularly gold.

Perhaps it is only coincidental that SirIsaac Newton, the master of the Londonmint from 1699 to 1726 and one of thetowering intellects in the history ofhumanity, spent years conducting experi-ments in alchemy, leaving behind manu-scripts of 100,000 words. Between 1661and 1692, experiments in alchemyaccounted for most of Newton’s labora-tory work. He experimented withalchemy while he was writing his

4 | Alchemy

masterpiece, Philosophiae NaturalisPrincipia Mathematica (MathematicalPrinciples for Natural Philosophy), alsoknown as the Principia.

The origins of alchemy stretch backinto the murky recesses of history. Onelegend suggests that Jason’s goldenfleece was actually a papyrus manuscriptdescribing the gold-producing secrets ofalchemy. Probably a combination ofGreek speculation, Eastern mysticism,and Egyptian technology conspired tomake Alexandria, Egypt, one of the firstcenters of alchemical studies in the West.The Roman emperor Diocletian orderedall Egyptian texts on alchemy destroyedafter crushing an Egyptian rebellion atthe end of the third century. Apparentlyhis action was taken only to punish theEgyptians. Evidence of alchemical stud-ies in China show up as early as the sec-ond century BCE, and India also boastsof an ancient tradition of alchemy.

The Arabs inherited both the easternand western traditions of alchemy, andmade advancements in the science ofchemistry while practicing alchemy. Thegreatest of the Islamic alchemists wasthe Great Geber, regarded in medievalEurope as the father of alchemy. To theArab alchemists we owe such terms as“alcohol,” “alkali,” “borax,” and “elixir.”

The study of alchemy passed from theArabs into Europe through Spain. In 1181the University of Montpellier wasfounded in southern France. It becamethe birthplace of European alchemy, pro-ducing in the 13th century several of themost famous alchemists, including Albertus Magnus and Roger Bacon, themost renowned of the medieval scientists.Another famous graduate, St. ThomasAquinas, also wrote about alchemy. Liketheir Arab predecessors, the Europeanalchemists believed that all metals were

constituted of varying proportions of twometals, mercury and sulfur. Much of theirresearch centered on the quest for an elusive elementary solvent with whichmetals could be broken down into thesetwo basic elements and then reconstitutedin different proportions, resulting in different metals.

It was with good reason that alchemistswere perceived as charlatans promisingmore than they could deliver, yet at thesame time they were suspected of being inleague with dark forces and, akin to sor-cerers, using black magic and charms.

The European monarchies also sus-pected alchemists of fraudulent andheretical practices, but were always in abind for money. Although fearingalchemists as potential counterfeiters,they could not resist the lure of thealchemists’ promise to convert lead andother base metals into gold. James II ofScotland is reported to have dabbled inalchemy himself. King Charles II ofEngland inherited a bare treasury andsought a solution to his fiscal problemsin the magic of alchemy. He built hisown laboratory for alchemical investiga-tions, connected to his bed chamber by asecret staircase. France also turned toalchemists to help finance wars withEngland, and both countries issued gold-colored currency as soldiers’ pay. In the20th century, Adolf Hitler is reported tohave sought the services of scientistsengaged in alchemical studies, hoping tobolster Germany’s gold reserves.

The famous English philosopher SirFrancis Bacon, in his book Advancementof Learning (1605), may have bestcaught the significance of alchemy whenhe wrote, “Alchemy may be likened tothe man who told his sons that he hadburied gold in the vineyard; where theyby digging found no gold but by turning

Alchemy | 5

up the mold about the roots of the vinesprocured a plentiful vintage.”

See also: Gold

ReferencesBacon, Sir Francis. 1625/1969. Advancement

of Learning.Cummings, Richard. 1966. The Alchemists.Marx, Jennifer. 1978. The Magic of Gold.

AMERICAN PENNY

The penny in the United States is a one-cent coin. Presently, the UnitedStates Mint strikes about 12 billion pen-nies annually, accounting for over one-half of all coins struck by the mint. If thepennies struck by the U.S. Mint since itsinception were lined up edge to edge, thepennies would roughly circle the earth137 times (www.penny.org).

Historically, the penny was a coppercoin. Copper coinage came slowly to theEnglish-speaking countries, perhapsbecause of its long association with cur-rency debasement. Early in the 17th cen-tury, Spain had debased its silver coinwith copper alloy, eventually strikingcoins that were virtually all copper withface values commensurate with high sil-ver content. The prevailing opinion inEngland was that only gold and silver metthe standard of a monetary metal. A short-age of small change among tavern keep-ers and tradesmen, however, prompted theintroduction of private tokens. To meetthe need for small change, the Englishgovernment in 1613 first struck coppercoins. Great Britain struck the first copperpennies for home use in 1797.

In 1681 New Jersey sanctioned as legaltender copper coins called Patrick’spence, after the Irishman who brought thecoins to the colonies. In 1722 the British

government authorized William Wood tomint pennies and halfpence for Irelandand the colonies. These pennies were amixture of copper, tin, and zinc, and had atouch of silver. Under the Articles of Con-federation, several states establishedmints that turned out copper coins. TheCoinage Act of 1792 established the centand the half-cent and set the weight of thecent at 264 grains of copper. The act madeno provision for the actual coinage ofcopper, and the legal tender provisions ofthe act failed to mention copper coins.Congress soon amended the act to pro-vide for the purchase of copper and fornecessary arrangements for the coinage ofcopper cents and half-cents. Congressalso began to think of the copper coinageas a fiduciary issue, and authorized thepresident to substantially reduce the copper weight of the cent and half-cent.

Congress also banned the circulationof foreign copper coins, a restriction thatdid not apply for foreign gold and silvercoins. The Spanish silver dollar circu-lated as clearly legal tender currencywhile the legal tender status of the coppercents and half-cents remained in doubt.After President Washington reduced thecopper content of the cent to 168 grains,the coinage of cents and half-cents accel-erated as a profit-making venture.

In 1857, Congress substantiallyincreased the seigniorage on the coppercoins. It abolished the half-cent andreduced the weight of the one-cent cointo 72 grains with 88 percent copper and12 percent nickel. In 1864, Congressagain changed the composition of thecent, raising the copper content to 95 percent with the remaining 5 percentzinc. Congress also made the one-centcoin legal tender.

In 1909, to mark the 100th year sincehis birth, Abraham Lincoln became the

6 | American Penny

first historical figure to adorn a UnitedStates coin. Fifty years later, an image ofthe Lincoln Memorial appeared on thereverse side, and today both sides of thepenny commemorate Abraham Lincoln.In 2009, the U.S. Mint will issue four dif-ferent one-cent coins to commemoratethe 200th anniversary of PresidentLincoln’s birth and the 100th anniversaryof the production of the Lincoln cent.

Rising copper prices in the 1970scaused a shortage of pennies, then worthmore as copper than as money. Pennieswere melted down for copper, and tokeep pennies in circulation the govern-ment reduced the penny’s copper con-tent to 2.5 percent, the remaining 97.5 percent was composed of zinc.

In the first decade of the new century,the penny’s future stands somewhat uncer-tain. Inflated price levels may have madethe penny coin obsolete, but proposals todiscontinue the penny have not met withwidespread approval. State and local gov-ernments claim the penny plays a neededrole in the collection of sales taxes appliedat percentage rates. Consumer groupsclaim abolishing the penny will mean thatprices will be rounded up a nickel insteadof a penny, leading to higher prices. Oppo-nents of the penny cite its insignificantpurchasing power, and the time andresources that households and businessesput into managing pennies. In 2001 and2006, bills came up in Congress to stopproduction of the penny, but the billsfailed to pass. The U.S. Mint contends thatcoinage of the penny is profitable to thegovernment, and other large major indus-trialized countries, including GreatBritain, Canada, Japan, Germany, France,and Italy, have kept the penny, or pennyequivalents, in production. Australia andNew Zealand have removed their pennyequivalent from circulation.

See also: Coinage Act of 1792, Copper

ReferencesCarothers, Neil. 1930/1967. Fractional

Money.Gadsby, J. William. 1996. Future of the Penny:

Options for Congressional Consideration.Hagenbauch, Barbara. “A penny saved could

become a penny spurned.” USA Today,July 7, 2006.

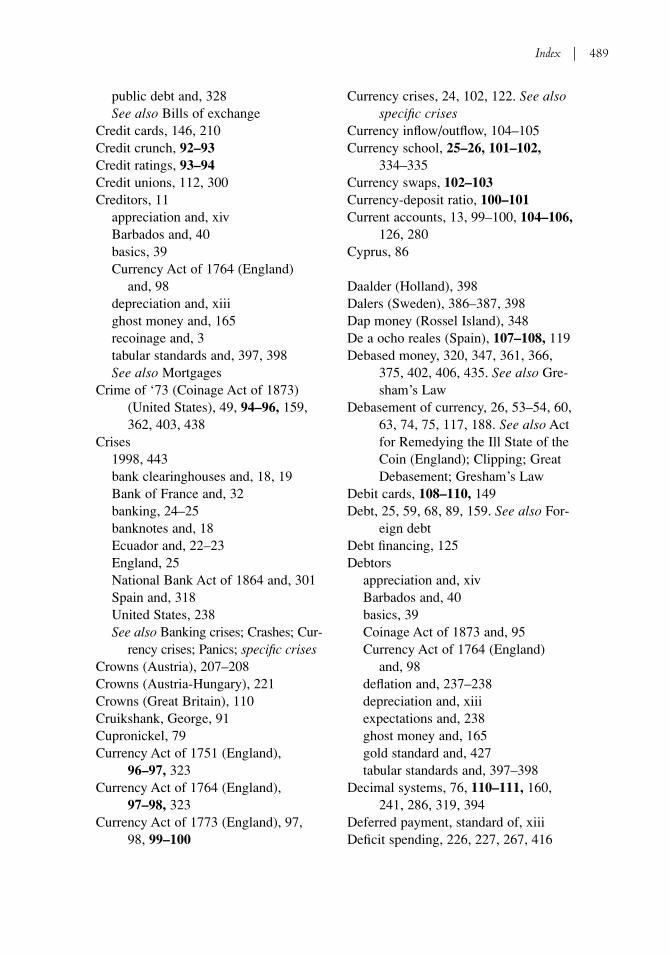

ANCIENT CHINESE PAPER MONEY

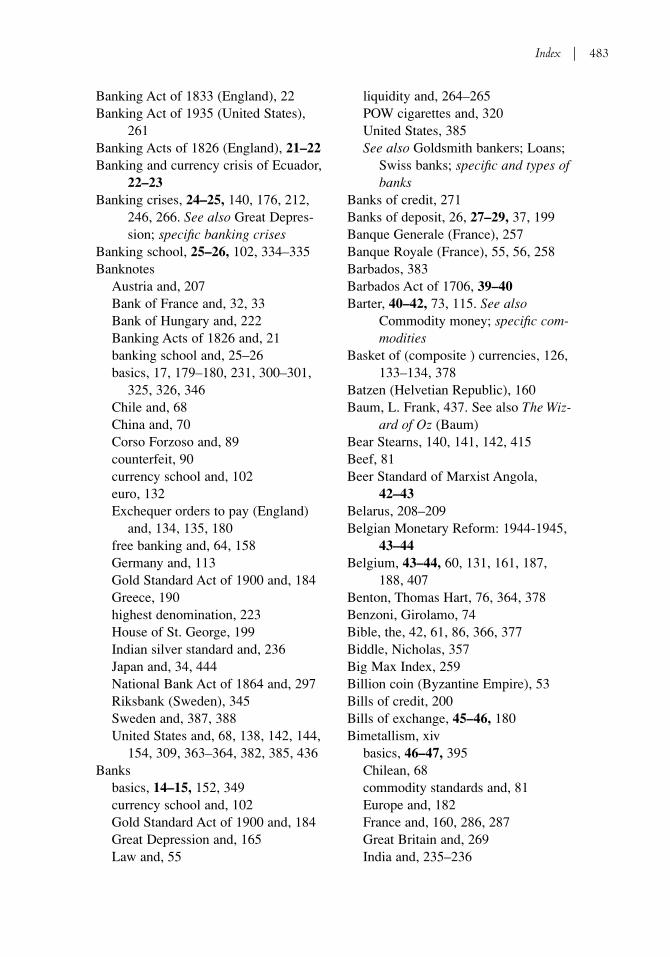

In the second book of The Travels ofMarco Polo, Chapter 18 is entitled: “Ofthe Kind of Paper Money Issued by theGrand Khan, and Made to Pass Currentthroughout His Dominions.” In thischapter, Marco Polo, who lived in Chinafrom 1275 to 1292, described the papermoney system as follows:

In this city of Kanbulu is the mint ofthe grand khan, who may truly besaid to possess the secret of thealchemist, as he has the art of pro-ducing money by the followingprocess. He causes the bark to bestripped from those mulberry-treethe leaves of which are used forfeeding silk-worms, and takes fromit that thin inner rind, which liesbetween the coarser bark and thewood of the tree. This being steeped,and afterwards pounded in a mortar,until reduced to a pulp, is made intopaper, resembling (in substance)that which is manufactured fromcotton, but quite black. When readyfor use, he has it cut into pieces ofmoney of different sizes, nearlysquare, but somewhat longer thanthey are wide. . . . The coinage ofthis paper money is authenticated

Ancient Chinese Paper Money | 7

with as much form and ceremony asif it were actually of pure gold or sil-ver; for to each note a number ofofficers, specially appointed, notonly subscribe their names, but affixtheir signets also; and when this hasbeen regularly done by the whole ofthem, the principal officer, deputedby his majesty, having dipped intovermilion the royal seal committedto his custody, stamps with it thepiece of paper, so that the form ofthe seal tinged with the vermilionremains impressed upon it, bywhich it receives full authenticity ascurrent money, and the act of coun-terfeiting it is punished as a capitaloffense. . . . nor dares any person, atthe peril of his life, refuse to acceptit in payment. When any persons

happen to be possessed of papermoney which from long use hasbecome damaged, they carry it tothe mint, where, upon the paymentof only three percent, they mayreceive fresh notes in exchange.Should any be desirous of procuringgold or silver for the purposes ofmanufacture, such as of drinking-cups, girdles, or other articleswrought of these metals, they in likemanner apply at the mint, and fortheir paper obtain the bullion theyrequire. (Polo, 1958, 153–155)

Marco Polo’s account of the papermoney system in China may have been abit optimistic. China had been issuingpaper money since 910 CE and hadalready suffered at least one round ofhyperinflation before Marco Polo’s visit.Around 1020, inflation and currencydepreciation became such a problem thatthe authorities resorted to perfuming thepaper money to make it more attractive.China seemed to have experiencedphases of reformed currencies, punctu-ated with bouts of inflation. By 1448, theMing note was worth only 3 percent ofits face value, and no further referencesto paper money are found after 1455.

Paper money lost its charm in Chinaowing to inflation, leading to its extinc-tion as a form of state-sponsored moneyin China until the 20th century. When theWestern world saw a renaissance of papermoney toward the end of the 17th century,inflation again reared itself as a rock ofdanger for any paper-money system.Despite the inflation dangers of papermoney, however, the societies experienc-ing the fastest economic developmentsince the beginning of the 17th centuryhave been those that learned to use papermoney.

8 | Ancient Chinese Paper Money

Banknote from Kublai Khan’s first issue ofbanknotes, 1260–1287. (The Bridgeman ArtLibrary)

See also: Leather Money

ReferencesHewitt, V., ed. 1995. The Banker’s Art.Polo, Marco. 1958. Travels of Marco Polo.

ANNOUNCEMENT EFFECT

Central banks publically announceintentions of maintaining a key policyinterest rate at a certain level called the“target rate.” The practice of announcingtargets is relatively recent, and repre-sents a sharp departure from the confi-dentiality and secretiveness that wasonce thought to be a necessary part ofmonetary policy and open market opera-tions. The “announcement effect” refersto a central bank’s ability to control a keyinterest rate merely by announcing itsintentions.

In the United States, the key policyinterest rate targeted by the central bankis the federal funds rate, and the centralbank is the Federal Reserve System. Thefederal funds rate is the interest rate atwhich commercial banks can borrowfunds from each other overnight. Thefederal funds rate reflects the markettightness for these funds. The FederalReserve can ease tightness in this mar-ket by purchasing U.S. governmentbonds, and can tighten this market byselling U.S. government securities. Buy-ing U.S. government securities injectsadditional funds into the banking sys-tem, allowing banks to increase lendingand enlarge the money supply in theprocess. Central bank purchases andsales of government securities are called“open market operations.” In the FederalReserve System, a policy-making groupcalled the Federal Open Market Com-mittee (FOMC) formulates the policyfor open market operations.

Until 1994, the Federal Reserve keptdirectives involving open market opera-tions a secret until 45 days after an FOMCmeeting, keeping current financial marketparticipants unaware of the FederalReserve’s policy stance at a given point intime. In 1976, the Federal Reserve suc-cessfully defended itself against aninquiry filed under the Freedom of Infor-mation Act to obtain copies of the min-utes of FOMC meetings without the45-day delay. Federal Reserve cited an“announcement effect” that might lead tovolatility and uncertainty in financial mar-kets, and maintained that secrecy was anecessary part of monetary policy.

On 4 February 1994, the FOMC,amidst a two-day meeting, announced thatit planned to apply slight pressure to com-mercial bank reserve positions, and thatshort-term interest rates could be expectedto rise, breaking the Federal Reserve’slong stance policy of secrecy in these mat-ters. It was an experiment in clearly com-municating policy decisions to financialmarkets, and using public announcementsas a method of communication. Theexperiment had none of the dire conse-quences that the Federal Reserve cited inits 1976 defense against a Freedom ofInformation inquiry. The practice of publi-cally announcing policy decisions and tar-gets became a standard part of centralbanking in the United States and innumerous other countries. What becameknown as the “announcement effect”enabled central banks to control a targetedinterest rate with fewer interventions inthe open market. It gave central banks theability to control a targeted interest ratemerely by announcing its intentions andtaking little or no immediate action.

See also: Federal Open Market Committee,Open Market Operations

Announcement Effect | 9

ReferencesBelongia, Michael T., and Kevin Kliesen.

“Effects on Interest Rates of ImmediatelyReleasing FOMC Directives.” Contempo-rary Economic Policy, vol. 12, no. 4:79–91.

Demiralp, Selva, and Oscar Jorda. “TheResponse of Term Rates to Fed Announce-ments.” Journal of Money, Credit, andBanking, vol. 36, no. 3 (June 2004, part 1):387–405.

ARGENTINE CURRENCYAND DEBT CRISIS

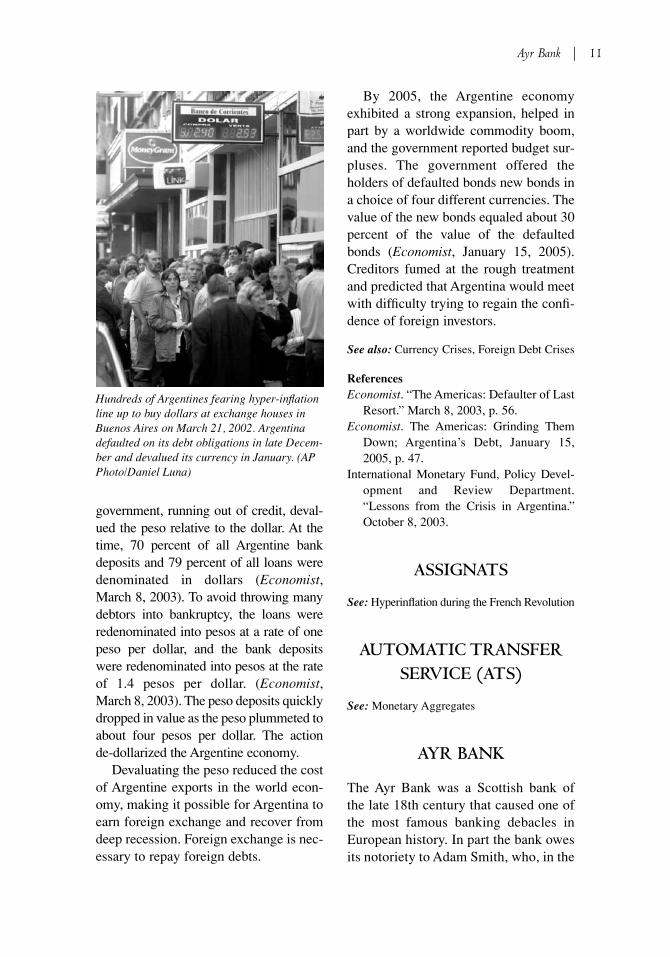

Between 2001 and 2002, Argentinaunderwent an episode of currency deval-uation and debt default that rocked inter-national financial markets and offeredfresh evidence of the varied economictrends that can lead to crises. TheArgentine crisis has been the topic ofwide discussion, partly because it wasborn of circumstances not normallyregarded as fertile ground for currencycrises. In the 1990s, Argentina boasted ofone of Latin America’s fastest growingeconomies and one of its staunches devo-tees to the gospel of free market reform.Part of the credit for economic prosperityseemed to lie with a successful monetaryreform that ended the hyperinflation ofthe 1980s. This monetary reform estab-lished a currency board that fixed thevalue of the Argentine peso at one peso toa U.S. dollar. One Argentine peso,exchangeable into dollars at any time,equaled one U.S. dollar. Argentine infla-tion subsided to low single-digit levels,output grew at a fast clip, and the econ-omy seemed resilient to external shocks.

The genesis of the crisis goes back to1998 when many of Argentina’s tradingpartners saw their currencies depreciate,

perhaps because of fallout to the EastAsian Crisis and the retreat of foreigncapital. The strong demand for U.S.financial assets keep the U.S. dollarstrong, which kept all currencies peggedto the dollar, including the Argentinepeso, strong. The strong Argentine pesomeant that Argentine exports went athigher prices in foreign markets, whileArgentine imports saw falling prices. Insummery, Argentina-produced goodsgrew costlier compared to goods pro-duced by Argentina’s major trading part-ners. Cheaper imports allowed Argentinato live beyond its means, while itsexports were over-priced in foreign mar-kets. To restore balance, Argentinaneeded to either devalue its currency asits trading partners had done, or undergodomestic deflation. Argentina did experi-ence some deflation, which is a charac-teristic that distinguishes the Argentinecrises from other crises. More often thesetypes of crises occur after governmentdeficits, financed by monetary growth,lead to inflation.

Government’s budget deficits weremodest, but were large enough to force agrowing reliance on foreign debt financ-ing. A small financial sector may sharethe blame for a dependence on foreigncapital to finance both private sector andpublic sector spending. The vulnerabilityof the system arose from the large shareof loans and mortgages denominated indollars while the income generated toservice these debts came in the form ofpesos. Once deflationary forces surfaced,output shrank, unemployment spiked,government deficits rose, and the gov-ernment proceeded to pile up foreigndebt. In December 2001, the governmentof Argentina defaulted on its public debt.

After more than three years of reces-sion, in January 2002, the Argentine

10 | Argentine Currency and Debt Crisis

government, running out of credit, deval-ued the peso relative to the dollar. At thetime, 70 percent of all Argentine bankdeposits and 79 percent of all loans weredenominated in dollars (Economist,March 8, 2003). To avoid throwing manydebtors into bankruptcy, the loans wereredenominated into pesos at a rate of onepeso per dollar, and the bank depositswere redenominated into pesos at the rateof 1.4 pesos per dollar. (Economist,March 8, 2003). The peso deposits quicklydropped in value as the peso plummeted toabout four pesos per dollar. The action de-dollarized the Argentine economy.

Devaluating the peso reduced the costof Argentine exports in the world econ-omy, making it possible for Argentina toearn foreign exchange and recover fromdeep recession. Foreign exchange is nec-essary to repay foreign debts.

By 2005, the Argentine economyexhibited a strong expansion, helped inpart by a worldwide commodity boom,and the government reported budget sur-pluses. The government offered theholders of defaulted bonds new bonds ina choice of four different currencies. Thevalue of the new bonds equaled about 30percent of the value of the defaultedbonds (Economist, January 15, 2005).Creditors fumed at the rough treatmentand predicted that Argentina would meetwith difficulty trying to regain the confi-dence of foreign investors.

See also: Currency Crises, Foreign Debt Crises

ReferencesEconomist. “The Americas: Defaulter of Last

Resort.” March 8, 2003, p. 56.Economist. The Americas: Grinding Them

Down; Argentina’s Debt, January 15,2005, p. 47.

International Monetary Fund, Policy Devel-opment and Review Department.“Lessons from the Crisis in Argentina.”October 8, 2003.

ASSIGNATS

See: Hyperinflation during the French Revolution

AUTOMATIC TRANSFERSERVICE (ATS)

See: Monetary Aggregates

AYR BANK

The Ayr Bank was a Scottish bank ofthe late 18th century that caused one ofthe most famous banking debacles inEuropean history. In part the bank owesits notoriety to Adam Smith, who, in the

Ayr Bank | 11

Hundreds of Argentines fearing hyper-inflationline up to buy dollars at exchange houses inBuenos Aires on March 21, 2002. Argentinadefaulted on its debt obligations in late Decem-ber and devalued its currency in January. (APPhoto/Daniel Luna)

Wealth of Nations, devoted a good bit ofspace to describing its story.

The Ayr Bank, more accurately calledthe firm of Douglas, Heron, and Com-pany, came into being in November1769. It was founded along the lines ofthe land bank schemes suggested by JohnLaw, but unlike Law’s schemes, it was apurely private initiative without officialbacking. As a copartnership, rather thanan incorporated business, its owners werefully liable for all the debts of the busi-ness. Its founders were landowners of thefirst order, one of whom, the Duke ofBuccleuch, had accompanied AdamSmith on a tour of Europe and had thebenefit of the famous economist’s advice.Land owned by the founders was the ulti-mate security for the bank’s notes.

The Ayr Bank burst on the scene whenthe Scottish economy was in a contrac-tion and many observers felt that a short-age of circulating money acted as a dragon the Scottish economy. According toSmith, writing in the Wealth of Nations:

This bank was more liberal than anyother had ever been, both in grantingcash discounts, and in discountingbills of exchange. With regard to thelatter, it seems to have made scarceany distinction between real andcirculating bills, but to have dis-counted all equally. It was theavowed principle of this bank toadvance, upon any real security, thewhole capital which was to beemployed in those improvements ofwhich returns are the most slow anddistant, such as the improvements toland. (Smith, 1952, 135)

The liberal lending policy of the bankled to a rapid expansion of bank notes,greater than what the bank’s resources

could support. The Ayr Bank expansionof credit found its way into speculationin real estate and the London stock mar-ket. Bank notes were redeemed withbills of exchange drawn on Londonbanks in amounts that exceeded thebank’s London resources. In 1772, aLondon-Scottish banking house withclose connections with the Ayr Bankfailed, and the Ayr Bank’s house of cardscollapsed. Scotland’s public banksrefused to grant credits to the failingbank. The bank was liquidated, and theincome from the land was pledged to theredemption of outstanding bank notes.The founders of the bank lost everything,some of whom were apparently unawarethat their liability was unlimited.

The failure of the Ayr Bank was prob-ably due more to mismanagement thanto faults in the land bank principle. Thebank may have actually spurred the eco-nomic development of Scotland, but itsfailure weakened public confidence inland-banking schemes, leaving gold andsilver as the most acceptable security forbank notes. The bank’s history showshow easily an expansion of bank notesleads to a speculative bubble that ends incollapse. History has continued to repeatitself, with Tokyo being the last scene ofa speculative bubble fed by overly gener-ous credit policy.

See also: Bank of Scotland, Free Banking, LandBank System, Scottish Banking Act of 1765

ReferencesCheckland, S. G. 1975. Scottish Banking

History: 1695–1973.Kroszner, Randy. 1995. Free Banking: The

Scottish Experience as a Model forEmerging Economies.

Smith, Adam. 1776/1952. An Inquiry into theNature and Causes of the Wealth ofNations.

12 | Ayr Bank

13

B

BALANCE OF PAYMENTS

The balance of payments for a countrysummarizes all the international transac-tions that involve either an outflow or aninflow of money. It is composed of threemajor elements: (1) the current account,(2) the capital account, and (3) the offi-cial reserves transactions account. Theofficial reserves transactions accountreflects the official transactions betweencentral banks that must occur when thecombined balance of the current andcapital accounts is in either the deficit orsurplus column.

Transactions that lead to an outflow ofmoney are registered as a debit in the bal-ance of payments, and are entered with anegative sign. Transactions that lead to aninflow of money are registered as acredit, and are entered with a plus sign.Imports of foreign goods cause an out-flow of money, entering with a negativesign in the balance of payments. Exportsof domestic goods to foreign buyers leadto an inflow of money, registering as acredit with a plus sign. The balance oftrade is total exports minus total imports.

A balance of trade deficit causes a netoutflow of money, and a surplus causes anet inflow of money. Income earnedfrom foreign investments, money trans-ferred between citizens of differentcountries, can also influence the balanceof payments. When these types of flowsare figured into the balance of trade, theoutcome is the balance on currentaccount.

Capital flows between countries showup in the balance of payments on the cap-ital account. When domestic investorspurchase financial or nonfinancial assetsin foreign countries, capital flows out,and money also flows out, registeringwith a negative sign on the balance ofpayments. When U.S. citizens purchasestock on the Tokyo stock exchange, dol-lars flow out, just as when U.S. citizenspurchase a Toyota. When foreigninvestors purchase financial or nonfinan-cial investments in the domestic econ-omy, capital flows in, and money flowsin, registering as a positive sign in thebalance of payments. The sale of U.S.government bonds to Japanese investorscauses dollars to flow into the United

States. If a domestic seller exports goodsabroad on credit, the sale of goods isentered as a plus sign in the balance ofpayments, and the grant of credit is a cap-ital outflow, entered with a negative sign.

Capital flows often offset imbalances inthe balance of trade, as can be observed inthe bilateral relationship between theUnited States and Japan. U.S. exports toJapan fall well short of U.S. imports fromJapan, contributing to a deficit on the bal-ance of trade, and an outflow of dollars. Inturn, Japan invests significantly in theUnited States, building factories, and pur-chasing real estate and U.S. governmentbonds. Japan earns dollars by sellinggoods in the United States, and investsthose dollars back in the United States,causing dollars to flow out on the currentaccount and flow in on the capital account.

If the outflow of money exceeds theinflow of money, the central banks mustsettle accounts by compensating adjust-ments in holdings of gold, foreignexchange, or other reserve assets. Anexcess of money outflow over moneyinflow will draw down the reserves ofthe domestic central bank, whereas anexcess of money inflow over money out-flow will build up reserves of the domes-tic central bank. An excess in the outflowof money leaves foreigners with a claimon domestic resources; excess in theinflow of money has the opposite effect.

Persistent deficits or surpluses on thecombined current and capital accountscause changes in the value of domesticcurrency in foreign exchange markets. Adeficit causes supplies of domestic cur-rency to build up in foreign exchangemarkets, and the domestic currency willlose value. As the currency loses value,imports become more expensive, andexports become cheaper in foreignmarkets. Together these forces will

remove the deficit. A surplus causesdomestic currency to gain value in for-eign exchange markets, making importscheaper and exports more expensive inforeign markets. These forces act toremove the surplus.

See also: Foreign Exchange Markets, Gold-Specie-Flow Mechanism

ReferencesAppleyard, Dennis R., and Alfred J. Field,

Jr. 1992. International Economics.Daniels, John D., and David Vanhoose. 1999.

International Monetary and FinancialMonetary Economics.

BANCO DEL PIAZZA DELRIALTO, IL

See: Bank of Venice

BANK

The term “bank” apparently owes its ori-gin to the bank (or bench) used by themoneychangers during the Middle Ages.Historically, some banks were calledbanks of deposit, and mainly helddeposits of foreign and domestic curren-cies and arranged payment in foreigntrade transactions. The Bank of Amster-dam was a bank of deposit.

Other banks created deposits that actedas a circulating medium of money in asociety. One of the earliest banks in thiscategory, the Bank of Venice, was formedwhen a group of the government’s credi-tors combined and began using govern-ment debt as a means of payment in trade.The famous merchant bankers, such asthe Rothschilds, acted largely as brokersmarketing government and corporatesecurities to wealthy patrons.

14 | Bank

Central banks are bankers’ banks, andthese banks trace their history from theBank of England. These banks buy gov-ernment debt, have a monopoly on theissuance of paper money, and often actas a lender of last resort to commercialbanks. In current times, the term “bank”refers to a commercial bank.

Commercial banks in modern capital-ist societies act as financial intermedi-aries, raising funds from depositors andlending the same funds to borrowers. Thedepositors’ claims against the bank, theirdeposits, are liquid, meaning banks areexpected to redeem deposits on demand,instantly. Banks’ claims against their borrowers are much less liquid, givingborrowers a much longer span of time torepay money owed banks. Because abank cannot immediately reclaim moneylent to borrowers, it may face bankruptcyif all its depositors simultaneously with-draw all their money. Protecting banksand bank customers from bank failures ofthis sort is the aim of much governmentbanking regulation.

The principle of fractional reservebanking lies at the heart of the moderncommercial banking system. During agiven period of time a bank will receivefresh deposits while existing deposits arewithdrawn. Normally the fresh depositsand the withdrawn deposits cancel eachother out. Despite daily deposits and with-drawals, a bank maintains an average levelof deposits that represents funds the bankcan largely keep loaned out. For safety,banks hold back a certain fraction ofdeposits, called “reserves” (thus fractionalreserve banking) to cover themselves overperiods of time when withdrawn depositsexceed fresh deposits. Because thesereserves earn no interest, banks aretempted to cut the margin of reserves a bitthin. If adequate, these reserves enable a

bank to weather a crisis of confidencewhen masses of people suddenly with-draw deposits out of fear.

When a bank fails, the bank’s cus-tomers, the depositors, suffer as much ormore than the bank’s owners. Thismakes the banking industry an excellentcandidate for government regulation.Bank lending policy can also aggravatethe business cycle. During an economicdownswing, banks can become overlycautious, restricting the availability ofloans and sending the economy into asteeper downward spiral. On theupswing, however, banks lose their cau-tion, generously granting loans and pro-pelling the economy into an inflationaryboom. Government regulation strives toprotect bank depositors from bank fail-ures and to encourage banks to become astabilizing force in the economy.

See also: Bank of Amsterdam, Bank of England,Bank of Venice, Central Bank, DepositoryInstitution Deregulation and Monetary Con-trol Act of 1980, Goldsmith Bankers,Glass–Steagall Banking Act, Medici Bank,Swiss Banks, Wildcat Banks, World Bank

ReferencesBaye, Michael R., and Dennis W. Jansen.

1995. Money, Banking, and FinancialMarkets: An Economics Approach.

Richards, R. D. 1929/1965. The Early His-tory of Banking in England.

BANK CHARTER ACT OF1833 (ENGLAND)

With passage of the Bank Charter Act of1833, Parliament renewed the Bank ofEngland’s charter until 1855. The actalso included provisions thatstrengthened the bank as the prime note-issuing institution in England, an impor-tant step toward giving a single

Bank Charter Act of 1833 (England) | 15

institution a monopoly on the privilegeof issuing bank notes (paper money).

In 1832, Parliament formed a com-mittee of inquiry to look at variousissues from all sides, including the Bankof England’s monopoly on joint-stockbanking within 65 miles of London. Thelaw forbade incorporated banks withmore than six shareholders from engag-ing in London’s banking business. Otherjoint-stock banks wanted to enter theLondon market, and existing law seemedto suggest that other banks were free toset up business in London as along asthey did not issue bank notes. The Bankof England hotly contested this view-point, and Parliament made timely use ofthe expiration of the Bank of England’scharter to review the matter.

One outcome of the inquiry was arecommendation that did not make itinto the law, but nevertheless repre-sented an important principle. HorselyPalmer, governor of the bank, formu-lated the principle that all demanddeposits and bank notes, that is “all lia-bilities to pay on demand,” should bebacked by gold reserves equaling one-third of such liabilities. The remainingtwo-thirds could be invested in securi-ties. The gold reserves were necessaryto ensure the convertibility of banknotes and other bank liabilities. Parlia-ment failed to act on Palmer’s recom-mendation, but the quantification of areserve policy remained an importantissue in banking.

One provision of the act stated “thatany Body Politic . . . consisting of morethan six persons may carry on the Tradeof Business of Banking in London, orwithin sixty five miles thereof providedthey did not issue notes.” The forbiddennotes were notes payable on demand orwithin less than six months. Other banks

could open for business in London, butthe Bank of England held a monopoly onthe privilege of issuing bank notes.

The act also made Bank of Englandnotes for more than £5 legal tender inEngland and Wales but not in Scotlandand Ireland. These notes were legal ten-der everywhere except at the Bank ofEngland. This provision enabled countrybanks to hold Bank of England notes asreserves in lieu of gold, reducing thedrain on gold reserves in times of con-traction, and centralizing gold reservesin the vault of the Bank of England.

Another important provision lifted the5 percent usury ceiling on bills ofexchange payable within three months.This provision was the beginning of thefamed “bank rate” that became a power-ful policy instrument for the Bank ofEngland. If gold began to flow out,threatening England’s gold reserves, thebank raised the bank rate, attractingfunds from abroad and ending the out-flow.

With the Bank of England’s growingpower came responsibility for public dis-closure of activities. The act required theBank of England to begin sendingweekly statistics on notes issues and bul-lion reserves to the treasury, and monthlysummaries were to be published in theLondon Gazette.

The Act of 1833 was important in thehistory of money because it made Bankof England notes legal tender duringpeace time, it effectively made the Bankof England the custodian of England’sgold reserves, and it gave the Bank ofEngland the bank rate with which to con-trol the inflow and outflow of gold. It laidin place principles fundamental to theoperation of England’s 19th-century goldstandard, a standard that ruled the mone-tary world by the end of the century.

16 | Bank Charter Act of 1833 (England)

See also: Bank Charter Act of 1844, Bank ofEngland, Central Bank

ReferencesChown, John F. 1994. A History of Money.Roberts, Richard, ed. 1995. The Bank of

England: Money, Power, and Influence,1694–1994.

BANK CHARTER ACT OF1844 (ENGLAND)

The English Bank Charter Act of 1844represents an important step in the evo-lution of the Bank of England as a cen-tral bank with a monopoly on theissuance of bank notes (paper money),one of the defining characteristics of acentral bank. Today all moderneconomies have central banks with amonopoly on the issuance of bank notes,the Federal Reserve System in theUnited States being a good example. Inthe early 1800s a multitude of commer-cial banks issued their own bank notes inEngland, France, the United States, andother countries.

Sir Robert Peel, who was prime min-ister when Parliament passed the BankCharter Act of 1844, shared with thefamous economist David Ricardo theview that the issuance of currency shouldbe a government monopoly with theprofits accruing to the government. Peelconsidered establishing a new system ofcurrency, with a board independent ofgovernment but responsible to Parlia-ment, charged with the issue of paper,convertible into gold, and valid as legaltender. In reality, Peel chose a moremoderate course that made use of exist-ing institutions. Important provisions inthe Bank Charter Act are paraphrased asfollows:

1. The note issuing department of theBank of England became separateand distinct from other depart-ments. The bank removed it to adifferent building.

2. The Bank of England was requiredto hold gold bullion equal in valueto the volume of its bank notesissued in excess of £14 million.The government debt secured mostof the first £14 million.

3. The Bank of England was requiredto stand ready to redeem its banknotes into gold at the rate of £317/9 (3 pounds, 17 shillings, and 9pence) per ounce of gold.

4. The creation of new banks with theprivilege to issue bank notes wasprohibited.

5. Banks currently issuing bank notescontinued to issue notes as long astheir total notes in circulationnever exceeded their average forthe 12 weeks preceding April 27,1844.

6. If a bank became insolvent, it lostthe right to issue bank notes.

7. If a bank stopped issuing notes forany reason, it could never again putnotes into circulation.

8. If two or more banks combined andended up with more than six part-ners, the new bank could not issuebank notes.

9. The Bank of England was allowedto issue new bank notes backed bysecurities up to two-thirds of thevalue of discontinued country banknotes.

The act had the desired effect. Theissuance of bank notes gradually becamethe exclusive privilege of the Bank of

Bank Charter Act of 1844 (England) | 17

England, which by World War I had madeits monopoly complete. By monopolizingthe issuance of paper money, the Bank ofEngland was able to limit the money sup-ply, helping to maintain its value, which isequivalent to avoiding inflation. The acthelped bring stable prices, but its restric-tions on the issuance of bank notes ham-pered the Bank of England’s ability to actas a lender of last resort.

The government was forced to suspendthe convertibility of Bank of England notesinto gold during major financial crises. Thefinancial crises of 1847, 1857, and 1866 allsaw suspensions of convertibility.

The Bank of France has enjoyed amonopoly on the issuance of bank notessince 1848, and the Federal ReserveSystem, established in 1914, has alwayshad a monopoly on the issuance of banknotes. With the demise of the gold stan-dard in the 1930s, the practice of main-taining the convertibility of bank notesinto gold disappeared, giving central

banks more freedom to inject liquidityinto a financial system during a crisis.

See also: Bank Charter Act of 1833, Bank ofEngland, Central Bank

ReferencesDavies, Glyn. 1994. A History of Money.Powell, Ellis. 1915/1966. The Evolution of

the Money Market: 1385–1915.Roberts, Richard, ed. 1995. The Bank of

England: Money, Power, and Influence,1694–1994.

BANK CLEARINGHOUSES(UNITED STATES)

In the United States, bank clearinghousespartially fulfilled the functions of a cen-tral bank before the establishment of theFederal Reserve System. Bank clearing-houses facilitated interbank settlement ofaccounts, a necessary part of check clear-ing processes. Also, during financialcrises, when currency and coin werescarce, bank clearinghouses issued cer-tificates representing claims on bankassets. These certificates replaced cash inthe interbank settlement of accounts andinfused additional liquidity into the bank-ing system, allowing banks to survive theoutflow of currency and coin typical offinancial crises. On rare occasions thesecertificates circulated as currency.

New York City banks established thefirst clearinghouse in 1853. Two yearslater, the concept spread to Boston, andsoon all the nation’s largest cities hadbank clearinghouses. The New Yorkclearinghouse remained the most impor-tant because of New York’s (WallStreet’s) strategic role as the financialnerve center of the United States.

Under a bank clearinghouse system,an individual bank, Bank A, presents all

18 | Bank Clearinghouses (United States)

Robert Peel, prime minister of Great Britainfrom 1834 to 1846. (Library of Congress)

its claims against other banks (depositedchecks written on other banks) to theclearinghouse each day. The clearing-house credits Bank A’s clearinghouseaccount accordingly. All other banks thathave received deposits of checks writtenon Bank A will take these checks to theclearinghouse also, and Bank A will findits clearinghouse account debited to payfor these checks. Whatever discrepancyexists between debits and credits is set-tled with cash. The clearinghouse systemsubstantially reduces the amount of cashthat changes hands in the check clearingprocess.

Banks operate on the principle that,despite daily withdrawals and newdeposits, the average level of depositsat a bank remains steady during normalbusiness conditions, and thereforebanks can keep the vast proportion (80to 95 percent) of customer depositsloaned out. Banks keep reserves, suchas vault cash, for those periods of timewhen withdrawals exceed newdeposits. Sound banks, however, oftenfell prey to their own success by loan-ing out too much of depositors’ moneyand coming up short of reserves toredeem deposits during a financial cri-sis. Bank clearinghouses help banksresist the temptation to overextendloans by forcing banks to speedilyhonor checks written on their accounts.Also, the New York clearinghouserequired weekly reports from associ-ated banks showing customer deposits,assets, and reserves.

The New York clearinghouse issuedcertificates against bank assets to substi-tute for cash in interbank settlements dur-ing financial crises when acceleratedwithdrawals of deposits often left bankswithout cash reserves. The clearinghouseissued certificates against a bank’s assets

when a bank put up 100 percent collateraleither in bonds, or short-term commercialloans rated at 75 percent of face value. Ina financial crisis, a bank experiencing adrain on reserves could use certificates tosettle with the clearinghouse. The use ofclearinghouse certificates was not legallysanctioned until 1908, but certificateshelped ease the strain in every financialcrisis from 1873 until 1914. The clear-inghouse was essentially serving as alender of last resort, one of the importantfunctions of a central bank.

Although clearinghouses werestrictly private organizations, acting onprivate rather than public initiatives,they met some of the regulatory needs ofthe banking system before the UnitedStates turned to central banking in 1914with the establishment of the FederalReserve System.

See also: Central Bank, Federal Reserve Sys-tem, National Bank Act of 1864

ReferencesGorton, Gary. 1984. Clearinghouses and the

Origin of Central Banking in the U.S.Hepburn, A. Barton. 1924/1967. A History of

Currency in the United States.Myers, Margaret G. 1970. A Financial His-

tory of the United States.

BANK FORINTERNATIONALSETTLEMENTS

The Bank for International Settlements(BIS) acts as a bank for central banks,holding deposits of and providing abroad array of services to central banks.It accepts deposits in currencies andgold, mostly from central banks. By June1994, 100 central banks kept deposits atthe BIS (Siegman, 1994). Central banks

Bank for International Settlements | 19

can borrow from the BIS. Money marketinvestments account for a large share ofBIS assets.

The BIS has also grown into animportant forum for facilitating interna-tional monetary cooperation, consulta-tion, and exchange of informationbetween central banks. The BIS con-ducts research on monetary, economic,and financial issues and serves as agentor trustee for international financial set-tlements. The bank is headquartered inBasel, Switzerland.

The BIS was established in 1930 tohandle the coordination of Germany’sWorld War I reparation payments. Theterm “settlements” came from the roleof war reparations in its original mis-sion. Aside from the temporary issue ofwar reparations, the bank’s primaryobjective from the beginning lay inpromoting cooperation among centralbanks and providing added facilities forinternational financial operations.

At its inception, the central banks inEurope and the United States wereinvited to purchase a share of the totalcapital subscription of BIS. The UnitedStates elected not to subscribe to itsshare, and the Bank of France and theNational Bank of Belgium purchasedonly a portion of the issues representingtheir share. J.P. Morgan and Company,the First National Bank of New York,and the First National Bank of Chicagopurchased the U.S. part of the capitalsubscription. Private investors also pur-chased shares originally intended forthe Bank of France and the NationalBank of Belgium. In 2008, centralbanks owned 100 percent of BIS stock(www.bis.org).

The United States was slow to rec-ognize BIS as a necessary and usefulpart of the international monetary