ADVERTISEMENT SUPPLEMENT DAWN THURSDAY FEBRUARY … · improving quality of life. FMFB’s prime...

1

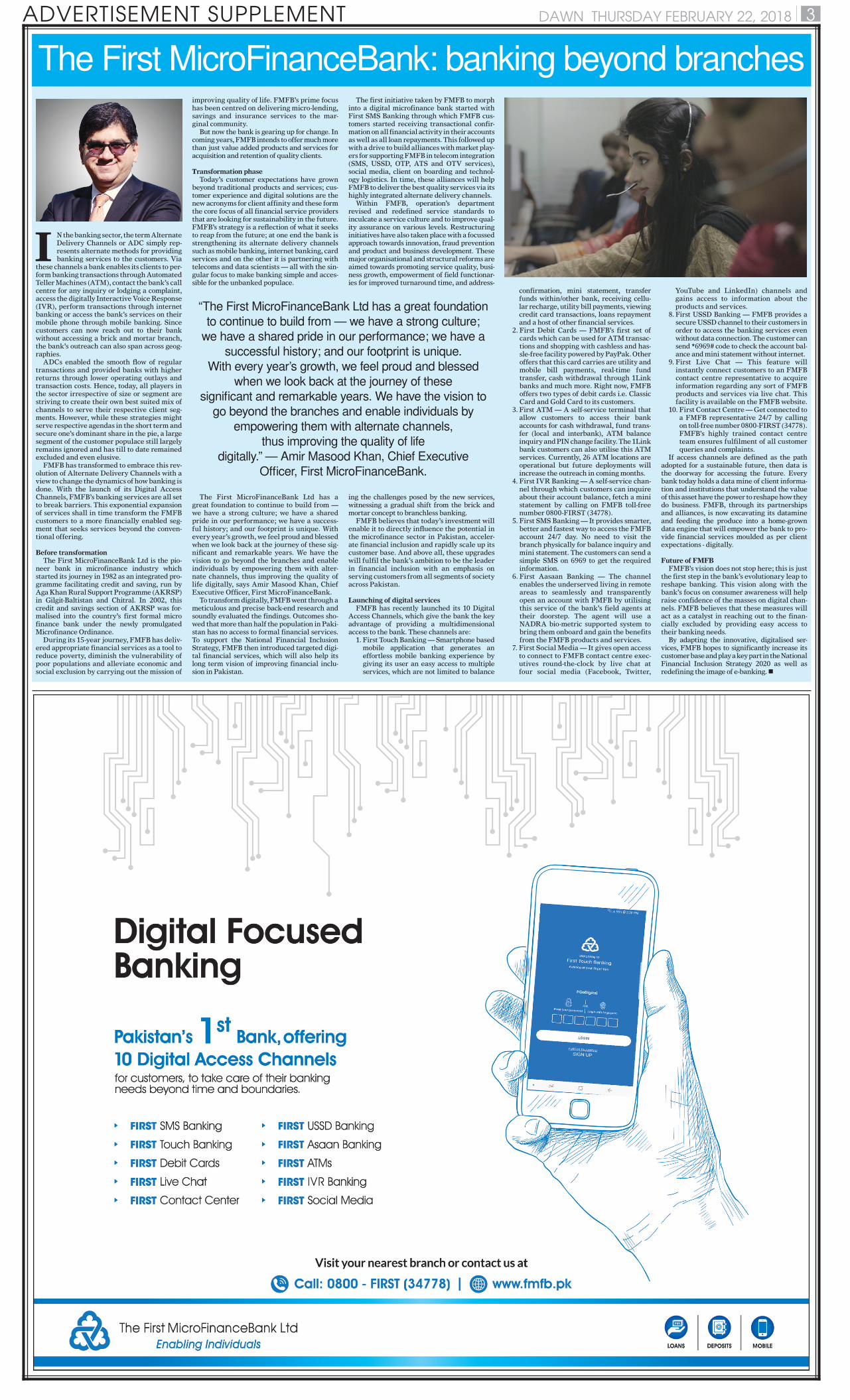

ADVERTISEMENT SUPPLEMENT 3 DAWN THURSDAY FEBRUARY 22, 2018 I N the banking sector, the term Alternate Delivery Channels or ADC simply rep- resents alternate methods for providing banking services to the customers. Via these channels a bank enables its clients to per- form banking transactions through Automated Teller Machines (ATM), contact the bank’s call centre for any inquiry or lodging a complaint, access the digitally Interactive Voice Response (IVR), perform transactions through internet banking or access the bank’s services on their mobile phone through mobile banking. Since customers can now reach out to their bank without accessing a brick and mortar branch, the bank’s outreach can also span across geog- raphies. ADCs enabled the smooth flow of regular transactions and provided banks with higher returns through lower operating outlays and transaction costs. Hence, today, all players in the sector irrespective of size or segment are striving to create their own best suited mix of channels to serve their respective client seg- ments. However, while these strategies might serve respective agendas in the short term and secure one’s dominant share in the pie, a large segment of the customer populace still largely remains ignored and has till to date remained excluded and even elusive. FMFB has transformed to embrace this rev- olution of Alternate Delivery Channels with a view to change the dynamics of how banking is done. With the launch of its Digital Access Channels, FMFB’s banking services are all set to break barriers. This exponential expansion of services shall in time transform the FMFB customers to a more financially enabled seg- ment that seeks services beyond the conven- tional offering. Before transformation The First MicroFinanceBank Ltd is the pio- neer bank in microfinance industry which started its journey in 1982 as an integrated pro- gramme facilitating credit and saving, run by Aga Khan Rural Support Programme (AKRSP) in Gilgit-Baltistan and Chitral. In 2002, this credit and savings section of AKRSP was for- malised into the country’s first formal micro finance bank under the newly promulgated Microfinance Ordinance. During its 15-year journey, FMFB has deliv- ered appropriate financial services as a tool to reduce poverty, diminish the vulnerability of poor populations and alleviate economic and social exclusion by carrying out the mission of improving quality of life. FMFB’s prime focus has been centred on delivering micro-lending, savings and insurance services to the mar- ginal community. But now the bank is gearing up for change. In coming years, FMFB intends to offer much more than just value added products and services for acquisition and retention of quality clients. Transformation phase Today’s customer expectations have grown beyond traditional products and services; cus- tomer experience and digital solutions are the new acronyms for client affinity and these form the core focus of all financial service providers that are looking for sustainability in the future. FMFB’s strategy is a reflection of what it seeks to reap from the future; at one end the bank is strengthening its alternate delivery channels such as mobile banking, internet banking, card services and on the other it is partnering with telecoms and data scientists — all with the sin- gular focus to make banking simple and acces- sible for the unbanked populace. The First MicroFinanceBank Ltd has a great foundation to continue to build from — we have a strong culture; we have a shared pride in our performance; we have a success- ful history; and our footprint is unique. With every year’s growth, we feel proud and blessed when we look back at the journey of these sig- nificant and remarkable years. We have the vision to go beyond the branches and enable individuals by empowering them with alter- nate channels, thus improving the quality of life digitally, says Amir Masood Khan, Chief Executive Officer, First MicroFinanceBank. To transform digitally, FMFB went through a meticulous and precise back-end research and soundly evaluated the findings. Outcomes sho- wed that more than half the population in Paki- stan has no access to formal financial services. To support the National Financial Inclusion Strategy, FMFB then introduced targeted digi- tal financial services, which will also help its long term vision of improving financial inclu- sion in Pakistan. The first initiative taken by FMFB to morph into a digital microfinance bank started with First SMS Banking through which FMFB cus- tomers started receiving transactional confir- mation on all financial activity in their accounts as well as all loan repayments. This followed up with a drive to build alliances with market play- ers for supporting FMFB in telecom integration (SMS, USSD, OTP, ATS and OTV services), social media, client on boarding and technol- ogy logistics. In time, these alliances will help FMFB to deliver the best quality services via its highly integrated alternate delivery channels. Within FMFB, operation’s department revised and redefined service standards to inculcate a service culture and to improve qual- ity assurance on various levels. Restructuring initiatives have also taken place with a focussed approach towards innovation, fraud prevention and product and business development. These major organisational and structural reforms are aimed towards promoting service quality, busi- ness growth, empowerment of field functionar- ies for improved turnaround time, and address- ing the challenges posed by the new services, witnessing a gradual shift from the brick and mortar concept to branchless banking. FMFB believes that today’s investment will enable it to directly influence the potential in the microfinance sector in Pakistan, acceler- ate financial inclusion and rapidly scale up its customer base. And above all, these upgrades will fulfil the bank’s ambition to be the leader in financial inclusion with an emphasis on serving customers from all segments of society across Pakistan. Launching of digital services FMFB has recently launched its 10 Digital Access Channels, which give the bank the key advantage of providing a multidimensional access to the bank. These channels are: 1. First Touch Banking — Smartphone based mobile application that generates an effortless mobile banking experience by giving its user an easy access to multiple services, which are not limited to balance confirmation, mini statement, transfer funds within/other bank, receiving cellu- lar recharge, utility bill payments, viewing credit card transactions, loans repayment and a host of other financial services. 2. First Debit Cards — FMFB’s first set of cards which can be used for ATM transac- tions and shopping with cashless and has- sle-free facility powered by PayPak. Other offers that this card carries are utility and mobile bill payments, real-time fund transfer, cash withdrawal through 1Link banks and much more. Right now, FMFB offers two types of debit cards i.e. Classic Card and Gold Card to its customers. 3. First ATM — A self-service terminal that allow customers to access their bank accounts for cash withdrawal, fund trans- fer (local and interbank), ATM balance inquiry and PIN change facility. The 1Link bank customers can also utilise this ATM services. Currently, 26 ATM locations are operational but future deployments will increase the outreach in coming months. 4. First IVR Banking — A self-service chan- nel through which customers can inquire about their account balance, fetch a mini statement by calling on FMFB toll-free number 0800-FIRST (34778). 5. First SMS Banking — It provides smarter, better and fastest way to access the FMFB account 24/7 day. No need to visit the branch physically for balance inquiry and mini statement. The customers can send a simple SMS on 6969 to get the required information. 6. First Aasaan Banking — The channel enables the underserved living in remote areas to seamlessly and transparently open an account with FMFB by utilising this service of the bank’s field agents at their doorstep. The agent will use a NADRA bio-metric supported system to bring them onboard and gain the benefits from the FMFB products and services. 7. First Social Media — It gives open access to connect to FMFB contact centre exec- utives round-the-clock by live chat at four social media (Facebook, Twitter, YouTube and LinkedIn) channels and gains access to information about the products and services. 8. First USSD Banking — FMFB provides a secure USSD channel to their customers in order to access the banking services even without data connection. The customer can send *6969# code to check the account bal- ance and mini statement without internet. 9. First Live Chat — This feature will instantly connect customers to an FMFB contact centre representative to acquire information regarding any sort of FMFB products and services via live chat. This facility is available on the FMFB website. 10. First Contact Centre — Get connected to a FMFB representative 24/7 by calling on toll-free number 0800-FIRST (34778). FMFB’s highly trained contact centre team ensures fulfilment of all customer queries and complaints. If access channels are defined as the path adopted for a sustainable future, then data is the doorway for accessing the future. Every bank today holds a data mine of client informa- tion and institutions that understand the value of this asset have the power to reshape how they do business. FMFB, through its partnerships and alliances, is now excavating its datamine and feeding the produce into a home-grown data engine that will empower the bank to pro- vide financial services moulded as per client expectations - digitally. Future of FMFB FMFB’s vision does not stop here; this is just the first step in the bank’s evolutionary leap to reshape banking. This vision along with the bank’s focus on consumer awareness will help raise confidence of the masses on digital chan- nels. FMFB believes that these measures will act as a catalyst in reaching out to the finan- cially excluded by providing easy access to their banking needs. By adapting the innovative, digitalised ser- vices, FMFB hopes to significantly increase its customer base and play a key part in the National Financial Inclusion Strategy 2020 as well as redefining the image of e-banking. The First MicroFinanceBank: banking beyond branches “The First MicroFinanceBank Ltd has a great foundation to continue to build from — we have a strong culture; we have a shared pride in our performance; we have a successful history; and our footprint is unique. With every year’s growth, we feel proud and blessed when we look back at the journey of these significant and remarkable years. We have the vision to go beyond the branches and enable individuals by empowering them with alternate channels, thus improving the quality of life digitally.” — Amir Masood Khan, Chief Executive Officer, First MicroFinanceBank.

Transcript of ADVERTISEMENT SUPPLEMENT DAWN THURSDAY FEBRUARY … · improving quality of life. FMFB’s prime...

ADVERTISEMENT SUPPLEMENT 3DAWN THURSDAY FEBRUARY 22, 2018

I N the banking sector, the term Alternate Delivery Channels or ADC simply rep-resents alternate methods for providing banking services to the customers. Via

these channels a bank enables its clients to per-form banking transactions through Automated Teller Machines (ATM), contact the bank’s call centre for any inquiry or lodging a complaint, access the digitally Interactive Voice Response (IVR), perform transactions through internet banking or access the bank’s services on their mobile phone through mobile banking. Since customers can now reach out to their bank without accessing a brick and mortar branch, the bank’s outreach can also span across geog-raphies.

ADCs enabled the smooth fl ow of regular transactions and provided banks with higher returns through lower operating outlays and transaction costs. Hence, today, all players in the sector irrespective of size or segment are striving to create their own best suited mix of channels to serve their respective client seg-ments. However, while these strategies might serve respective agendas in the short term and secure one’s dominant share in the pie, a large segment of the customer populace still largely remains ignored and has till to date remained excluded and even elusive.

FMFB has transformed to embrace this rev-olution of Alternate Delivery Channels with a view to change the dynamics of how banking is done. With the launch of its Digital Access Channels, FMFB’s banking services are all set to break barriers. This exponential expansion of services shall in time transform the FMFB customers to a more fi nancially enabled seg-ment that seeks services beyond the conven-tional offering.

Before transformationThe First MicroFinanceBank Ltd is the pio-

neer bank in microfi nance industry which started its journey in 1982 as an integrated pro-gramme facilitating credit and saving, run by Aga Khan Rural Support Programme (AKRSP) in Gilgit-Baltistan and Chitral. In 2002, this credit and savings section of AKRSP was for-malised into the country’s fi rst formal micro fi nance bank under the newly promulgated Microfi nance Ordinance.

During its 15-year journey, FMFB has deliv-ered appropriate fi nancial services as a tool to reduce poverty, diminish the vulnerability of poor populations and alleviate economic and social exclusion by carrying out the mission of

improving quality of life. FMFB’s prime focus has been centred on delivering micro-lending, savings and insurance services to the mar-ginal community.

But now the bank is gearing up for change. In coming years, FMFB intends to offer much more than just value added products and services for acquisition and retention of quality clients.

Transformation phaseToday’s customer expectations have grown

beyond traditional products and services; cus-tomer experience and digital solutions are the new acronyms for client affi nity and these form the core focus of all fi nancial service providers that are looking for sustainability in the future. FMFB’s strategy is a refl ection of what it seeks to reap from the future; at one end the bank is strengthening its alternate delivery channels such as mobile banking, internet banking, card services and on the other it is partnering with telecoms and data scientists — all with the sin-gular focus to make banking simple and acces-sible for the unbanked populace.

The First MicroFinanceBank Ltd has a great foundation to continue to build from — we have a strong culture; we have a shared pride in our performance; we have a success-ful history; and our footprint is unique. With every year’s growth, we feel proud and blessed when we look back at the journey of these sig-nifi cant and remarkable years. We have the vision to go beyond the branches and enable individuals by empowering them with alter-nate channels, thus improving the quality of life digitally, says Amir Masood Khan, Chief Executive Offi cer, First MicroFinanceBank.

To transform digitally, FMFB went through a meticulous and precise back-end research and soundly evaluated the fi ndings. Outcomes sho-wed that more than half the population in Paki-stan has no access to formal fi nancial services. To support the National Financial Inclusion Strat egy, FMFB then introduced targeted digi-tal fi nancial services, which will also help its long term vision of improving fi nancial inclu-sion in Pakistan.

The fi rst initiative taken by FMFB to morph into a digital microfi nance bank started with First SMS Banking through which FMFB cus-tomers started receiving transactional confi r-mation on all fi nancial activity in their accounts as well as all loan repayments. This followed up with a drive to build alliances with market play-ers for supporting FMFB in telecom integration (SMS, USSD, OTP, ATS and OTV services), social media, client on boarding and technol-ogy logistics. In time, these alliances will help FMFB to deliver the best quality services via its highly integrated alternate delivery channels.

Within FMFB, operation’s department revised and redefi ned service standards to inculcate a service culture and to improve qual-ity assurance on various levels. Restructuring initiatives have also taken place with a focussed approach towards innovation, fraud prevention and product and business development. These major organisational and structural reforms are aimed towards promoting service quality, busi-ness growth, empowerment of fi eld functionar-ies for improved turnaround time, and address-

ing the challenges posed by the new services, witnessing a gradual shift from the brick and mortar concept to branchless banking.

FMFB believes that today’s investment will enable it to directly infl uence the potential in the microfi nance sector in Pakistan, acceler-ate fi nancial inclusion and rapidly scale up its customer base. And above all, these upgrades will fulfi l the bank’s ambition to be the leader in fi nancial inclusion with an emphasis on serving customers from all segments of society across Pakistan.

Launching of digital servicesFMFB has recently launched its 10 Digital

Access Channels, which give the bank the key advantage of providing a multidimensional access to the bank. These channels are:

1. First Touch Banking — Smartphone based mobile application that generates an effortless mobile banking experience by giving its user an easy access to multiple services, which are not limited to balance

confi rmation, mini statement, transfer funds within/other bank, receiving cellu-lar recharge, utility bill payments, viewing credit card transactions, loans repayment and a host of other fi nancial services.

2. First Debit Cards — FMFB’s fi rst set of cards which can be used for ATM transac-tions and shopping with cashless and has-sle-free facility powered by PayPak. Other offers that this card carries are utility and mobile bill payments, real-time fund transfer, cash withdrawal through 1Link banks and much more. Right now, FMFB offers two types of debit cards i.e. Classic Card and Gold Card to its customers.

3. First ATM — A self-service terminal that allow customers to access their bank accounts for cash withdrawal, fund trans-fer (local and interbank), ATM balance inquiry and PIN change facility. The 1Link bank customers can also utilise this ATM services. Currently, 26 ATM locations are operational but future deployments will increase the outreach in coming months.

4. First IVR Banking — A self-service chan-nel through which customers can inquire about their account balance, fetch a mini statement by calling on FMFB toll-free number 0800-FIRST (34778).

5. First SMS Banking — It provides smarter, better and fastest way to access the FMFB account 24/7 day. No need to visit the branch physically for balance inquiry and mini statement. The customers can send a simple SMS on 6969 to get the required information.

6. First Aasaan Banking — The channel enables the underserved living in remote areas to seamlessly and transparently open an account with FMFB by utilising this service of the bank’s fi eld agents at their doorstep. The agent will use a NADRA bio-metric supported system to bring them onboard and gain the benefi ts from the FMFB products and services.

7. First Social Media — It gives open access to connect to FMFB contact centre exec-utives round-the-clock by live chat at four social media (Facebook, Twitter,

YouTube and LinkedIn) channels and gains access to information about the products and services.

8. First USSD Banking — FMFB provides a secure USSD channel to their customers in order to access the banking services even without data connection. The customer can send *6969# code to check the account bal-ance and mini statement without internet.

9. First Live Chat — This feature will instantly connect customers to an FMFB contact centre representative to acquire information regarding any sort of FMFB products and services via live chat. This facility is available on the FMFB website.

10. First Contact Centre — Get connected to a FMFB representative 24/7 by calling on toll-free number 0800-FIRST (34778). FMFB’s highly trained contact centre team ensures fulfi lment of all customer queries and complaints.

If access channels are defi ned as the path adopted for a sustainable future, then data is the doorway for accessing the future. Every bank today holds a data mine of client informa-tion and institutions that understand the value of this asset have the power to reshape how they do business. FMFB, through its partnerships and alliances, is now excavating its datamine and feeding the produce into a home-grown data engine that will empower the bank to pro-vide fi nancial services moulded as per client expectations - digitally.

Future of FMFBFMFB’s vision does not stop here; this is just

the fi rst step in the bank’s evolutionary leap to reshape banking. This vision along with the bank’s focus on consumer awareness will help raise confi dence of the masses on digital chan-nels. FMFB believes that these measures will act as a catalyst in reaching out to the fi nan-cially excluded by providing easy access to their banking needs.

By adapting the innovative, digitalised ser-vices, FMFB hopes to signifi cantly increase its customer base and play a key part in the National Financial Inclusion Strategy 2020 as well as redefi ning the image of e-banking.

The First MicroFinanceBank: banking beyond branches

“The First MicroFinanceBank Ltd has a great foundation to continue to build from — we have a strong culture;

we have a shared pride in our performance; we have a successful history; and our footprint is unique.

With every year’s growth, we feel proud and blessed when we look back at the journey of these

signifi cant and remarkable years. We have the vision to go beyond the branches and enable individuals by

empowering them with alternate channels, thus improving the quality of life

digitally.” — Amir Masood Khan, Chief Executive Offi cer, First MicroFinanceBank.