AAL

37

American Airlines Group (AAL) Bankruptcy Hides Transition to a “New American” LONG, TP $46 (+30%) RESEARCH TEAM Parker Kim, Senior Director Mark Albin, Senior Analyst Charlene Shu, Junior Analyst Christopher Boyd, Analyst Daniel Chen, Analyst Karsic Ma, Analyst

-

Upload

usittech -

Category

Presentations & Public Speaking

-

view

2.448 -

download

1

Transcript of AAL

American Airlines Group (AAL)Bankruptcy Hides Transition to a “New American”LONG, TP $46 (+30%)RESEARCH TEAMParker Kim, Senior DirectorMark Albin, Senior AnalystCharlene Shu, Junior AnalystChristopher Boyd, AnalystDaniel Chen, AnalystKarsic Ma, Analyst

September 2014

Table of Contents

Investment ThesisParker Kim

Company OverviewDaniel Chen

Industry OverviewChristopher Boyd

Competitive OverviewKarsic Ma

Financial OverviewMark Albin

Risk OverviewCharlene Shu

Investment Thesis

September 2014

Investment ThesisInvestors Need More Evidence to be Convinced

AAL P/E Shows Underappreciation

Despite Becoming a Dominant Player

Why does AAL trade at discount to its peers despite having superior market

share and profitability?

We believe the market is holding American back

because they can’t let go of its turbulent

past and are waiting for merger execution.

September 2014

Investment ThesisThe “New American” Isn’t Just a Slogan

AAL Yields Have Grown the Most

Margins Closing in on “Best-in-Class”

Despite negative investor sentiment, we believe that

Network Quality+

Yield Growth+

Profitability GainsIndicate AAL both has

been and will continue to be successful in executing

the US Airways merger

Company Overview

September 2014

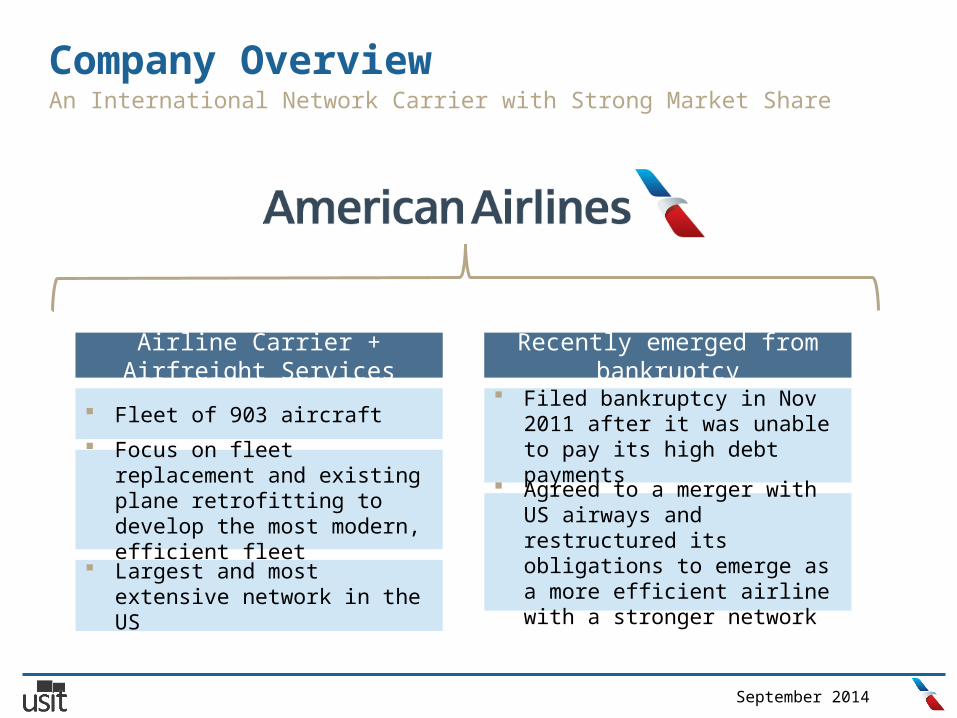

Company OverviewAn International Network Carrier with Strong Market Share

Airline Carrier + Airfreight Services

Recently emerged from bankruptcy

Fleet of 903 aircraft Focus on fleet replacement

and existing plane retrofitting to develop the most modern, efficient fleet

Largest and most extensive network in the US

Filed bankruptcy in Nov 2011 after it was unable to pay its high debt payments

Agreed to a merger with US airways and restructured its obligations to emerge as a more efficient airline with a stronger network

September 2014

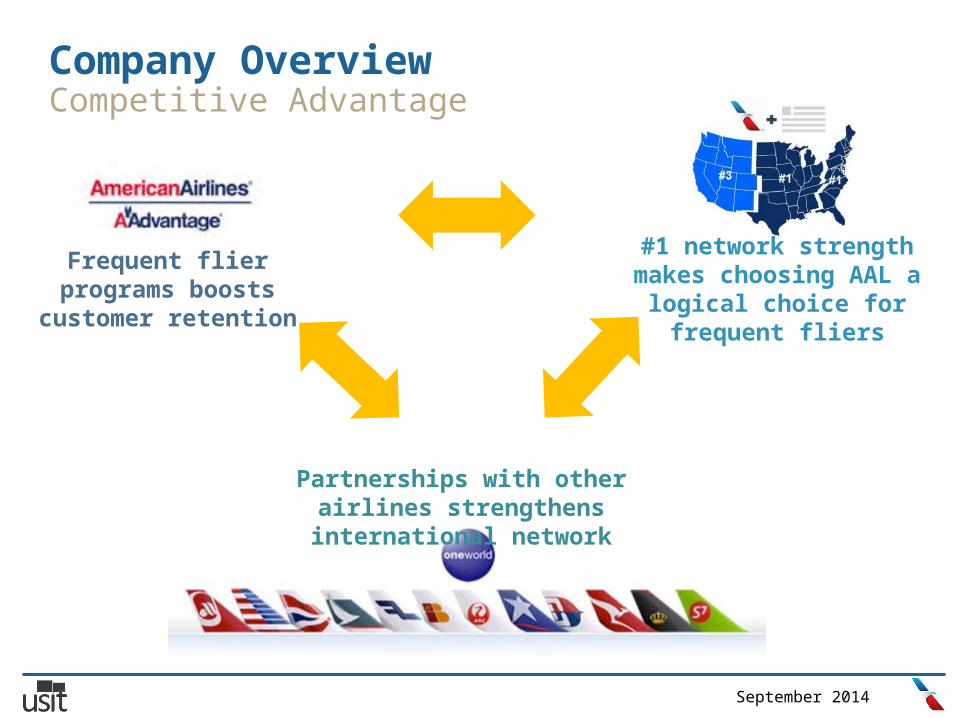

Company OverviewCompetitive Advantage

Partnerships with other airlines strengthens

international network

Frequent flier programs boosts

customer retention

#1 network strength makes choosing AAL a logical choice for

frequent fliers

September 2014

Company OverviewPost-Merger, US Airways Management Poised to Launch AAL

Doug ParkerChairman & CEO

Scott KirbyPresident

Derek KerrCFO

Experienced US Airways management team is key to executing on merger benefits

Synergy Targets: $1.4bn PwC Study: cost-cutting, increased efficiency, stronger

network Every performance metric has improved – approaching

#1 rank

September 2014

Company OverviewSWOT Analysis Indicates Opportunity in Pacific Markets

Strengths

Largest network Largest frequent flier

program Experienced management

team Excellent profitability

margins

Merger execution risk High leverage risk from

fleet improvements

Continued growth in disposable income

Increased business travel aligns with strong business traveler exposure

Increased demand for Pacific travel

Technology-based disruptions in business travel (ie. Skype)

Frequent-flier stealing programs

Opportunities

Weaknesses

Threats

Industry Overview

September 2014

Industry OverviewMarket Forces Make Airlines a Tough but Feasible Play

Large start up costs to purchase planes discourage new entrants

Regulatory issues and airport leasing process make the startup path difficult

Low switching costs and few variations between AAL/DAL/UAL make customer retention difficult

However, frequent flier programs offset this

Competition is based on price which forces razor-thin profit margins

Differentiation difficult, focus is on frequent flier programs + comprehensive network

Leisure carriers are the most susceptible to alternatives in domestic travel

Only 2 major suppliers: Airbus + Boeing Recently, AAL has begun purchasing planes

from Airbus (previously only Boeing) Despite duopoly, pricing power remains fair

HIGH

MODERATE

HIGH

LOW

MODERATE

Porter’s Assessment

Industry Dynamic Rationale

Barriers to Entry

Bargaining Power of Buyers

Intensity of Rivalry

Threat of Substitutes

Bargaining Power of Suppliers

September 2014

Industry OverviewPost-Consolidation, Pricing Power Should Improve

Favorable Industry Environment

The major US carriers should continue to benefit from a landscape where consolidation has optimized load factors.

Strong demand is producing record load factors. Revenue optimization initiatives combined with structural cost reductions should drive industry profitability up.

September 2014

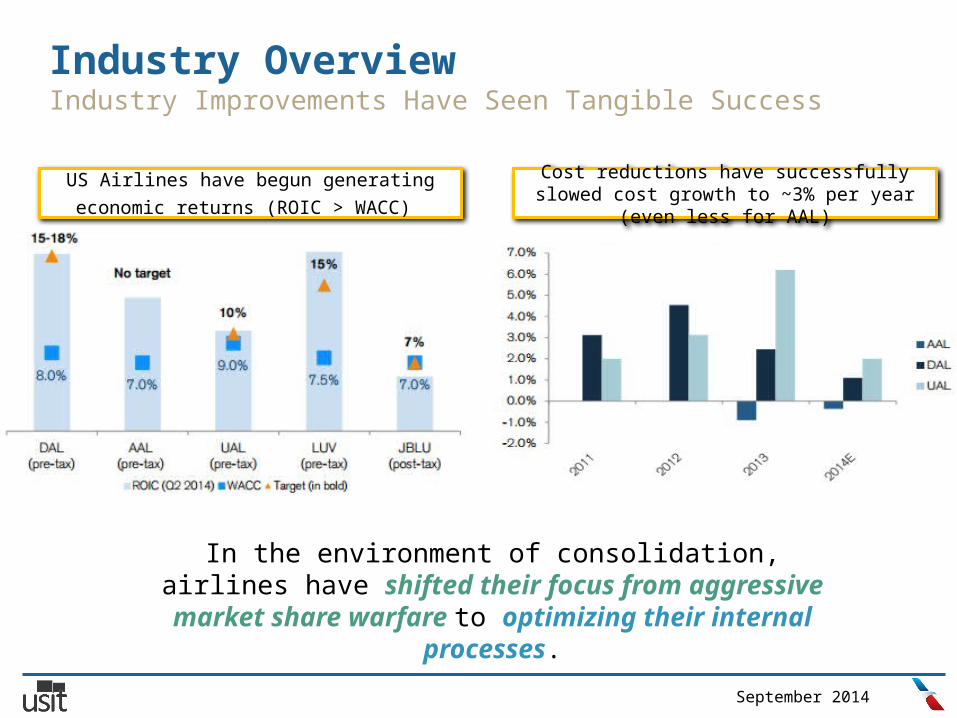

Industry OverviewIndustry Improvements Have Seen Tangible Success

US Airlines have begun generating economic returns (ROIC > WACC)

Cost reductions have successfully slowed cost growth to ~3% per year (even less for

AAL)

In the environment of consolidation, airlines have shifted their focus from aggressive market share warfare to optimizing their internal

processes.

Competitive Overview

September 2014

Competitive OverviewCompetitive Advantage leads to Revenue Success

AAL revenue per mile is continually growing and has recently moved to #2 in the

industry.

While its cost per mile has run in line with network operators.

American holds the most market share in the largest

market segment

September 2014

Competitive OverviewTarget Market

Who American targets relative to network, leisure

September 2014

Competitive OverviewAAL’s Network Leads in Market Share

Financial Overview

September 2014

Financial OverviewSeemingly Riskier Balance Sheet is not as Bad as Perceived

We project AAL’s total liquidity position ex-RCF to be between $10-12bn for 2014-2016

...but we forecast Debt / EBITDAR levels to normalize as cash flows mature and debt is

paid down.

Liquidity as a % of LTM Revenue has topped the industry for the last year

AAL does have the largest debt position of its network peers…

September 2014

Financial OverviewSeemingly Riskier Balance Sheet is not as Bad as Perceived

Free cash flow levels should begin to normalize to begin funding capital structure changes.

September 2014

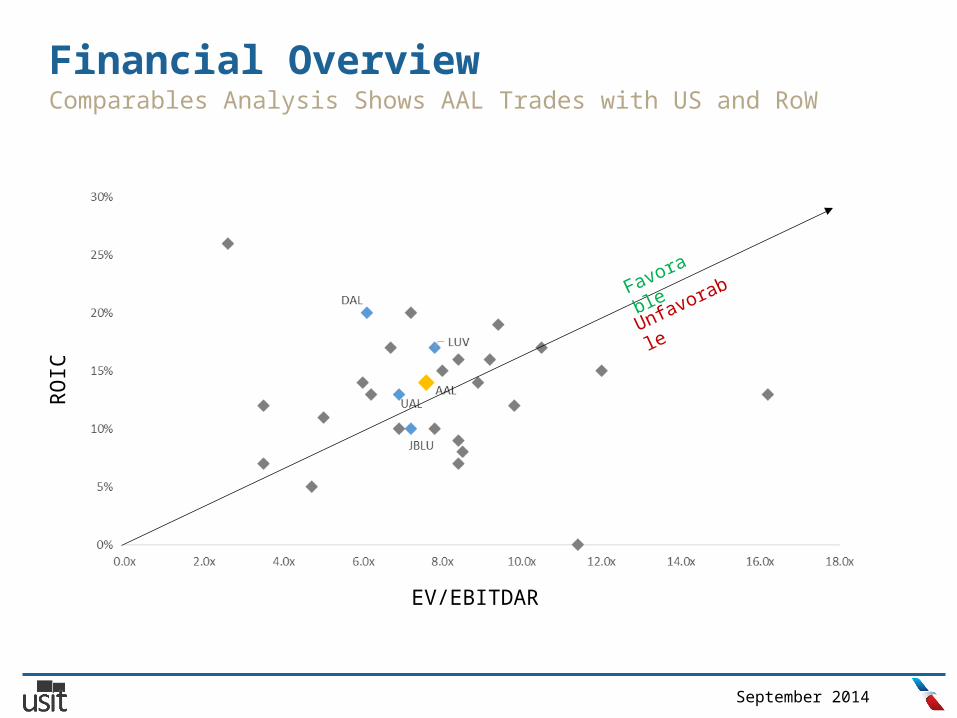

Financial OverviewComparables Analysis Shows AAL Trades with US and RoW

Global Average: 7.8x

US Average: 7.1x

AAL7.6x

September 2014

Financial OverviewComparables Analysis Shows AAL Trades with US and RoW

EV/EBITDAR

ROIC

Favorab

leUnfavorabl

e

September 2014

Financial OverviewAAL Represents Strong Upside Despite Negative Sentiment

2013A 2014E 2015E 2016EEBITDAR, adj 5,744 7395 8779 9678

% Margin 14.2% 17.2% 19.4% 20.4%

Taxes -107 363 20 25NOPAT 5,851 7,032 8,759 9,653

Capex -2,143 -2,813 -3,438D&A 1,132 1,272 1,307 1,344Change in NWC -150 -200 -300Unlevered FCF 6,011 7,053 7,259

PVFCF 5,869 6,261 5,858

Projected Period EV 17,988Terminal EV @ 4.7x 36,707Enterprise Value 54,695

Less: Debt 22627Plus: Cash 1140Equity Value 33,208Fully Diluted Shares Outstanding 720.5

Share Price $46.09

Blended UAL/DAL 2015E EV/EBITDAR, current EV/EBITDAR: 7.1x

Consensus estimates for EBITDAR

+30% upside

September 2014

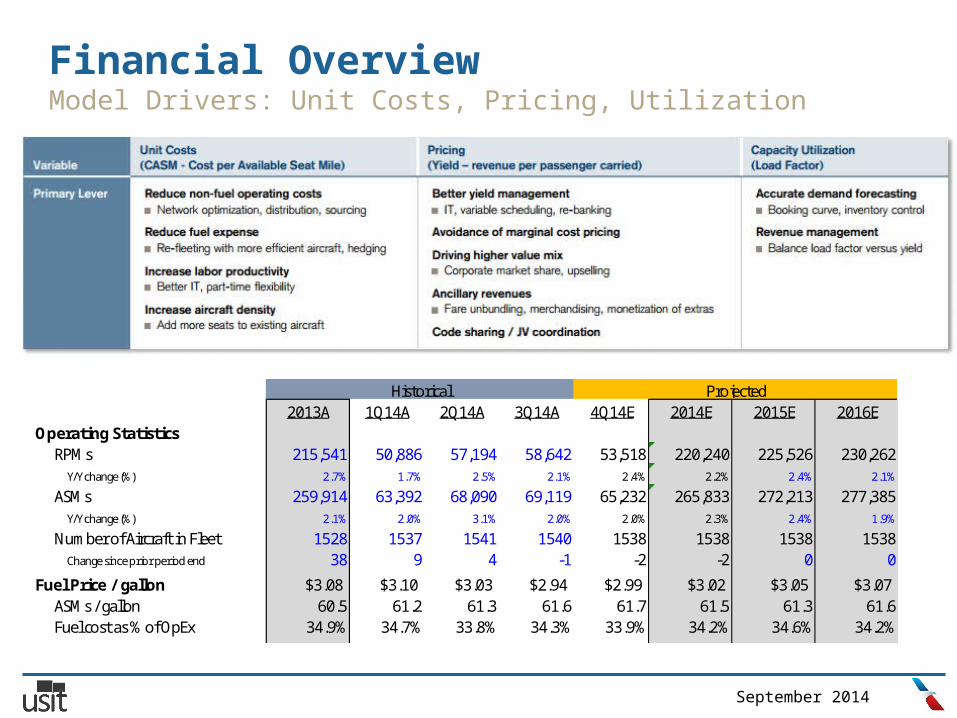

Financial OverviewModel Drivers: Unit Costs, Pricing, Utilization

2013A 1Q14A 2Q14A 3Q14A 4Q14E 2014E 2015E 2016EOperating Statistics

RPMs 215,541 50,886 57,194 58,642 53,518 220,240 225,526 230,262Y/Y change (%) 2.7% 1.7% 2.5% 2.1% 2.4% 2.2% 2.4% 2.1%

ASMs 259,914 63,392 68,090 69,119 65,232 265,833 272,213 277,385Y/Y change (%) 2.1% 2.0% 3.1% 2.0% 2.0% 2.3% 2.4% 1.9%

Number of Aircraft in Fleet 1528 1537 1541 1540 1538 1538 1538 1538Change since prior period end 38 9 4 -1 -2 -2 0 0

Fuel Price / gallon $3.08 $3.10 $3.03 $2.94 $2.99 $3.02 $3.05 $3.07ASMs / gallon 60.5 61.2 61.3 61.6 61.7 61.5 61.3 61.6Fuel cost as % of OpEx 34.9% 34.7% 33.8% 34.3% 33.9% 34.2% 34.6% 34.2%

Revenue & Costs / ASMYield (cents) 16.49 17.03 17.34 16.84 17 17.05 17.53 18.02

Y/Y change (%) 2.0% 3.2% 6.5% 2.0% 1.9% 3.4% 2.8% 2.8%PRASM (cents) 13.67 13.67 14.57 14.28 13.95 14.13 14.53 14.96

Y/Y change (%) 2.6% 2.9% 5.9% 2.2% 2.3% 3.3% 2.8% 3.0%CASM (cents) 9.13 9.75 9.31 9.15 9.46 9.46 9.38 9.57

Y/Y change (%) -2.5% 3.7% 2.4% 2.1% 2.1% 3.6% -0.8% 2.0%Margins

8.1% 5.9% 14.5% 14.3% 10.6% 11.3% 13.8% 15.0%Y/Y change (bps) 443bps 294bps 456bps 327bps 274bps 274bps 250bps 120bps

EBITDAR Margin 14.2% 12.2% 20.1% 20.0% 16.9% 17.2% 19.4% 20.4%Y/Y change (bps) 459bps 294bps 415bps 305bps 266bps 298bps 218bps 103bps

Historical Projected

Risk Overview

September 2014

Risk OverviewExecution Risk Limited- AAL Already Outpaces UAL and DAL

September 2014

Risk OverviewGeneral Risk Overview

Union Integration Fuel Price Risk Labor Cost Control

Association of Professional Flight Attendants voted last Wednesday and reached a 5-year agreement with AAL.

Integration issues between LCC-AMR unions resolved with this.

AAL has invested in newer and more comfortable planes to keep up with competition and lower fuel consumption.

Fuel costs represent ~35% of OpEx but should approach 32-33% by 2016.

Contract lasting through 2019 to be signed in December- includes modest 2% pay raises and shortening of pay ladder.

Overall should improve quality of life for personnel.

September 2014

ConclusionInvestors aren’t Seeing the “New American”

Low Valuation

Strong operational

success

Profitability gains

Investors are waiting to buy

AAL because they are afraid its

recent merger will fail.

In reality, AAL has already begun to exhibit signs of merger success and could end up being the star of

the industry.

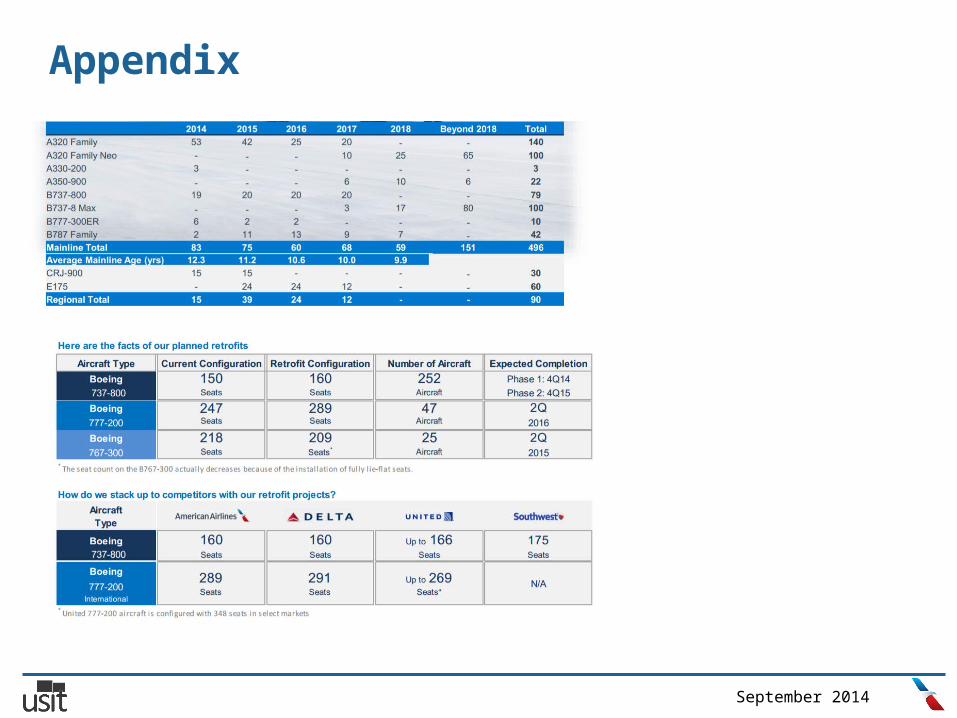

American Airlines Group (AAL)AppendixSeptember 30, 2014Research TeamParker Kim, Senior DirectorMark Albin, Senior AnalystCharlene Shu, Junior AnalystChristopher Boyd, AnalystDaniel Chen, AnalystKarsic Ma, Analyst

September 2014

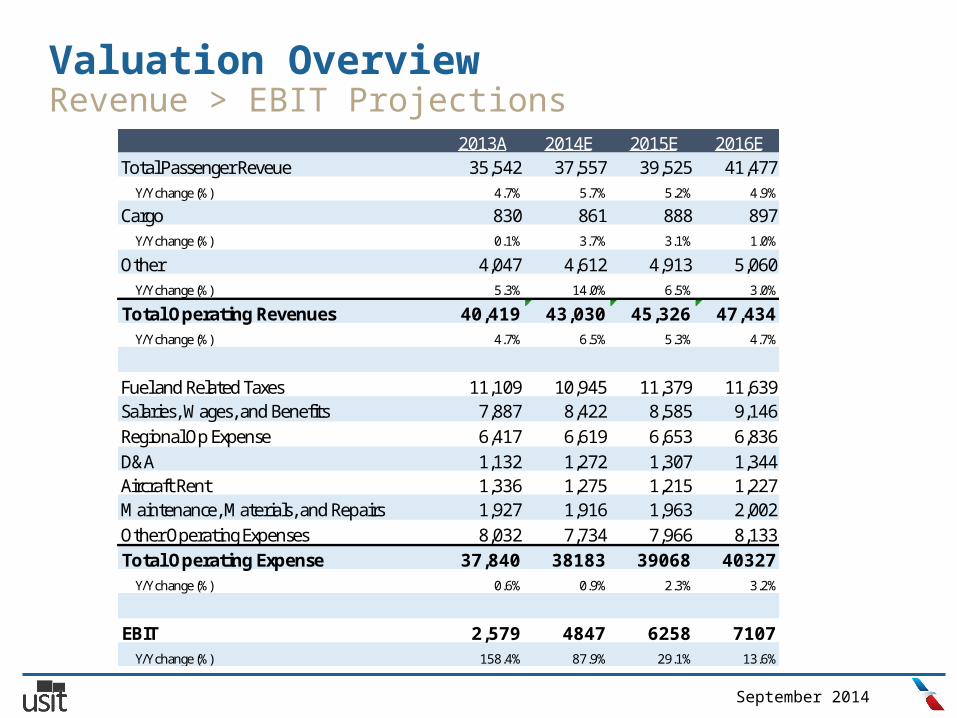

Valuation OverviewRevenue > EBIT Projections

2013A 2014E 2015E 2016ETotal Passenger Reveue 35,542 37,557 39,525 41,477

Y/Y change (%) 4.7% 5.7% 5.2% 4.9%Cargo 830 861 888 897

Y/Y change (%) 0.1% 3.7% 3.1% 1.0%Other 4,047 4,612 4,913 5,060

Y/Y change (%) 5.3% 14.0% 6.5% 3.0%Total Operating Revenues 40,419 43,030 45,326 47,434

Y/Y change (%) 4.7% 6.5% 5.3% 4.7%

Fuel and Related Taxes 11,109 10,945 11,379 11,639Salaries, Wages, and Benefits 7,887 8,422 8,585 9,146Regional Op Expense 6,417 6,619 6,653 6,836D&A 1,132 1,272 1,307 1,344Aircraft Rent 1,336 1,275 1,215 1,227Maintenance, Materials, and Repairs 1,927 1,916 1,963 2,002Other Operating Expenses 8,032 7,734 7,966 8,133Total Operating Expense 37,840 38183 39068 40327

Y/Y change (%) 0.6% 0.9% 2.3% 3.2%

EBIT 2,579 4847 6258 7107Y/Y change (%) 158.4% 87.9% 29.1% 13.6%

September 2014

Valuation OverviewRevenue > EBIT Projections

2013A 1Q14A 2Q14A 3Q14A 4Q14E 2014E 2015E 2016EOperating Statistics

RPMs 215,541 50,886 57,194 58,642 53,518 220,240 225,526 230,262Y/Y change (%) 2.7% 1.7% 2.5% 2.1% 2.4% 2.2% 2.4% 2.1%

ASMs 259,914 63,392 68,090 69,119 65,232 265,833 272,213 277,385Y/Y change (%) 2.1% 2.0% 3.1% 2.0% 2.0% 2.3% 2.4% 1.9%

Number of Aircraft in Fleet 1528 1537 1541 1540 1538 1538 1538 1538Change since prior period end 38 9 4 -1 -2 -2 0 0

Fuel Price / gallon $3.08 $3.10 $3.03 $2.94 $2.99 $3.02 $3.05 $3.07ASMs / gallon 60.5 61.2 61.3 61.6 61.7 61.5 61.3 61.6Fuel cost as % of OpEx 34.9% 34.7% 33.8% 34.3% 33.9% 34.2% 34.6% 34.2%

Revenue & Costs / ASMYield (cents) 16.49 17.03 17.34 16.84 17 17.05 17.53 18.02

Y/Y change (%) 2.0% 3.2% 6.5% 2.0% 1.9% 3.4% 2.8% 2.8%PRASM (cents) 13.67 13.67 14.57 14.28 13.95 14.13 14.53 14.96

Y/Y change (%) 2.6% 2.9% 5.9% 2.2% 2.3% 3.3% 2.8% 3.0%CASM (cents) 9.13 9.75 9.31 9.15 9.46 9.46 9.38 9.57

Y/Y change (%) -2.5% 3.7% 2.4% 2.1% 2.1% 3.6% -0.8% 2.0%Margins

EBIT Margin 8.1% 5.9% 14.5% 14.3% 10.6% 11.3% 13.8% 15.0%Y/Y change (bps) 443bps 294bps 456bps 327bps 274bps 274bps 250bps 120bps

EBITDAR Margin 14.2% 12.2% 20.1% 20.0% 16.9% 17.2% 19.4% 20.4%Y/Y change (bps) 459bps 294bps 415bps 305bps 266bps 298bps 218bps 103bps

Historical Projected

September 2014

Appendix http://

online.wsj.com/articles/american-airlines-flight-attendants-reach-tentative-agreement-1411164253 http://

www.dallasnews.com/business/airline-industry/20140919-american-airlines-reaches-tentative-agreement-with-flight-attendants-union.ece

https://www.iata.org/pressroom/facts_figures/fact_sheets/Documents/fuel-fact-sheet.pdf http://marketrealist.com/2014/07/why-american-us-airways-merger-was-conditional/ http://www.aa.com/i18n/amrcorp/corporateInformation/facts/measurements.jsp http://

phx.corporate-ir.net/External.File?item=UGFyZW50SUQ9MjI0MDU2fENoaWxkSUQ9LTF8VHlwZT0z&t=1 http://phx.corporate-ir.net/External.File?item=UGFyZW50SUQ9NTQyODc4fENoaWxkSUQ9MjMzMjk3fFR

5cGU9MQ==&t=1

http://phx.corporate-ir.net/External.File?item=UGFyZW50SUQ9NTQ2NTEwfENoaWxkSUQ9MjM4MDU0fFR5cGU9MQ==&t=1

http://phx.corporate-ir.net/External.File?item=UGFyZW50SUQ9NTU1MzM4fENoaWxkSUQ9MjUyMDU1fFR5cGU9MQ==&t=1

http://phx.corporate-ir.net/External.File?item=UGFyZW50SUQ9NTU1MzY0fENoaWxkSUQ9MjUyMDg4fFR5cGU9MQ==&t=1

http://aviationblog.dallasnews.com/2013/03/ceos-american-airlines-us-airways-will-bring-nothing-but-good-things.html/

September 2014

Appendix

September 2014

Appendix

September 2014

Appendix

September 2014

DO NOT WRITE OVER, TEMPLATE SLIDEDON’T EVEN THINK ABOUT IT MISTER