AA stable Banco Santander, S.A. · UK and in Brazil, Santander is the largest foreign private bank....

16

27034/RB/1.0/1/20190527 © GBB-Rating / confidential Page 1/16 Based on the information available, the financial standing of Banco Santander, S.A. (hereinafter referred to as "Santander" or "Group") is again evaluated as high. GBB- Rating confirms the rating result of AA- as well as the stable outlook. The rating reflects Santander's very high financial standing, which is underpinned by its high level of profitability and the low risk business profile focused on retail and commercial banking. The Group's broad geographical diversification is a major advantage over most competitors, as its strong presence in Latin America (especially in Brazil) provides access to markets with comparatively high interest rates and sufficient growth potential. Santander has a leading market position in retail lending in most of its core markets. The marked increase in client numbers in recent years (144 million at year-end, 2017: 133 million) is partly due to the acquisition and integration of Banco Popular (Spain, Portugal), but it also stems from substantial investments in digitalization and the expansion of online services. According to the updated mid-term plan, Santander plans to invest about EUR 20 billion in digitalization and technology over the next four years. Furthermore, the Group plans to cut EUR 1.2 billion of annual costs, largely in Europe. Overall, Santander has a sound and sustainable business model. In 2018, Santander reported an operating profit before tax of EUR 14.2 billion compared to EUR 12.1 billion in 2017. The main reason for the increase in profit was the significant decline in provisions and impairments on non-financial assets, in particular on intangible assets (EUR 0.1 billion, 2017: EUR 1.1 billion). The Group's net interest income as the main source of earnings remained almost at prior year's level (EUR 34.3 billion) whilst net commission income slightly decreased (-1 %). Administrative expenses (EUR 20.4 billion) remained stable. Consequently, Santander's earnings indicators remain at a high level. Based on GBB-Rating's profitability ratios, return on equity improved to 13.3 %, compared to 11.5 % in 2017. The cost income ratio (without provisions for credit risks) remains on an exceptionally low level of 49.6 % (2017: 51.9 %). In Q1 2019, attributable profit to the parent declined by 10.4 % compared to Q1 2018 as lower earnings in AA- stable Rating Committee: 05/27/2019 Strengths/Opportunities: High profitability and efficiency in a peer group comparison; strategic targets set in 2015 were met Sound and sustainable strategy Updated mid-term plan: focus on substantial investments in digitalization and cost savings Strong position in its core markets Broad geographical diversification Resilient structure of financially autonomous subsidiaries Balanced funding profile and comfortable liquidity position Weaknesses/Threats: CET1 ratio (fully loaded) remains on a comparatively low level NPL ratio declining, yet elevated in some regions (e. g. Brazil, Spain, Portugal) Ongoing low interest rate environment in advanced economies Deteriorating economic outlook particularly in Europe Financial data: (in EUR m) 2018 2017 Adjusted gross profit 45,966 44,325 Operating result 14,201 12,091 Net income 9,315 8,207 Total assets 1,459,271 1,444,305 CET1 capital ratio* 11.5 % 12.3 % Total capital ratio* 15.0 % 15.0 % Leverage Ratio* 5.2 % 5.3 % LCR 158 % 133 % NSFR 114 % 105 % * phased-in Analysts: Daniel Sebastian Bittner + 49 221 912 897 254 [email protected] Angelika Komenda + 49 221 912 897 248 [email protected] Banco Santander, S.A. Rating result

Transcript of AA stable Banco Santander, S.A. · UK and in Brazil, Santander is the largest foreign private bank....

27034/RB/1.0/1/20190527 © GBB-Rating / confidential Page 1/16

Based on the information available, the financial standing of

Banco Santander, S.A. (hereinafter referred to as

"Santander" or "Group") is again evaluated as high. GBB-

Rating confirms the rating result of AA- as well as the stable

outlook.

The rating reflects Santander's very high financial standing,

which is underpinned by its high level of profitability and the

low risk business profile focused on retail and commercial

banking. The Group's broad geographical diversification is a

major advantage over most competitors, as its strong

presence in Latin America (especially in Brazil) provides

access to markets with comparatively high interest rates and

sufficient growth potential. Santander has a leading market

position in retail lending in most of its core markets. The

marked increase in client numbers in recent years (144

million at year-end, 2017: 133 million) is partly due to the

acquisition and integration of Banco Popular (Spain,

Portugal), but it also stems from substantial investments in

digitalization and the expansion of online services. According

to the updated mid-term plan, Santander plans to invest

about EUR 20 billion in digitalization and technology over the

next four years. Furthermore, the Group plans to cut EUR 1.2

billion of annual costs, largely in Europe. Overall, Santander

has a sound and sustainable business model.

In 2018, Santander reported an operating profit before tax of

EUR 14.2 billion compared to EUR 12.1 billion in 2017. The

main reason for the increase in profit was the significant

decline in provisions and impairments on non-financial

assets, in particular on intangible assets (EUR 0.1 billion,

2017: EUR 1.1 billion). The Group's net interest income as

the main source of earnings remained almost at prior year's

level (EUR 34.3 billion) whilst net commission income slightly

decreased (-1 %). Administrative expenses (EUR 20.4

billion) remained stable.

Consequently, Santander's earnings indicators remain at a

high level. Based on GBB-Rating's profitability ratios, return

on equity improved to 13.3 %, compared to 11.5 % in 2017.

The cost income ratio (without provisions for credit risks)

remains on an exceptionally low level of 49.6 % (2017:

51.9 %).

In Q1 2019, attributable profit to the parent declined by

10.4 % compared to Q1 2018 as lower earnings in

AA-

stable Rating Committee: 05/27/2019

Strengths/Opportunities:

High profitability and efficiency in a peer group comparison; strategic targets set in 2015 were met

Sound and sustainable strategy

Updated mid-term plan: focus on substantial investments in digitalization and cost savings

Strong position in its core markets

Broad geographical diversification

Resilient structure of financially autonomous subsidiaries

Balanced funding profile and comfortable liquidity position

Weaknesses/Threats:

CET1 ratio (fully loaded) remains on a comparatively low level

NPL ratio declining, yet elevated in some regions (e. g. Brazil, Spain, Portugal)

Ongoing low interest rate environment in advanced economies

Deteriorating economic outlook particularly in Europe

Financial data:

(in EUR m) 2018 2017

Adjusted gross profit 45,966 44,325

Operating result 14,201 12,091

Net income 9,315 8,207

Total assets 1,459,271 1,444,305

CET1 capital ratio* 11.5 % 12.3 %

Total capital ratio* 15.0 % 15.0 %

Leverage Ratio* 5.2 % 5.3 %

LCR 158 % 133 %

NSFR 114 % 105 %

* phased-in

Analysts:

Daniel Sebastian Bittner + 49 221 912 897 254 [email protected]

Angelika Komenda + 49 221 912 897 248 [email protected]

Banco Santander, S.A.

Rating result

Banco Santander, S.A.

Rating report per 05/27/2019

27034/RB/1.0/1/20190527 © GBB-Rating / confidential Page 2/16

Continental Europe and in the UK and extraordinary effects

(net capital losses, restructuring costs) more than

outweighed the strong increase in earnings in Latin America.

In a peer comparison, Santander's capital ratios stand at a

relatively low level. At Q1 2019, the Group's CET1 capital

ratio was 11.2 % (phased-in and fully-loaded), well above the

minimum regulatory requirement of 9.7 %. Given

Santander's retail-focused, low-risk business model (low

earnings volatility, limited dependency on individual markets

and regions) the Group's capital resources are assessed as

adequate, further underpinned by the results of the "2018

EU-wider Stress Test Exercise".

The Group's funding plan has focused on TLAC/MREL

eligible instruments in recent years. Current MREL

requirements are already being met.

The quality of the loan portfolio has improved significantly in

recent years. This is reflected in the decline of the NPL ratio

in most regions. However, the NPL ratio remains high in

some core markets (Spain, Brazil). Despite the NPL's

sensitivity to any adverse economic downturn, the recent

improvement of the quality of the loan book indicates an

adequate risk management. In conjunction with modest

market and operational risks and with regard to the Group's

comfortable liquidity position, Santander's risk profile is

assessed as adequate.

Rating drivers

Santander's rating result strongly reflects the high level of

profitability. The rating would stabilize in a consistent profit

situation, and it would benefit from further sustainable in-

creases in capital and earnings.

The rating could be adversely affected by a global economic

slowdown, with negative consequences on consumer

confidence and on credit demand by enterprises and

households. A weaker economy would usually deteriorate

asset quality and increase loan-loss provisions.

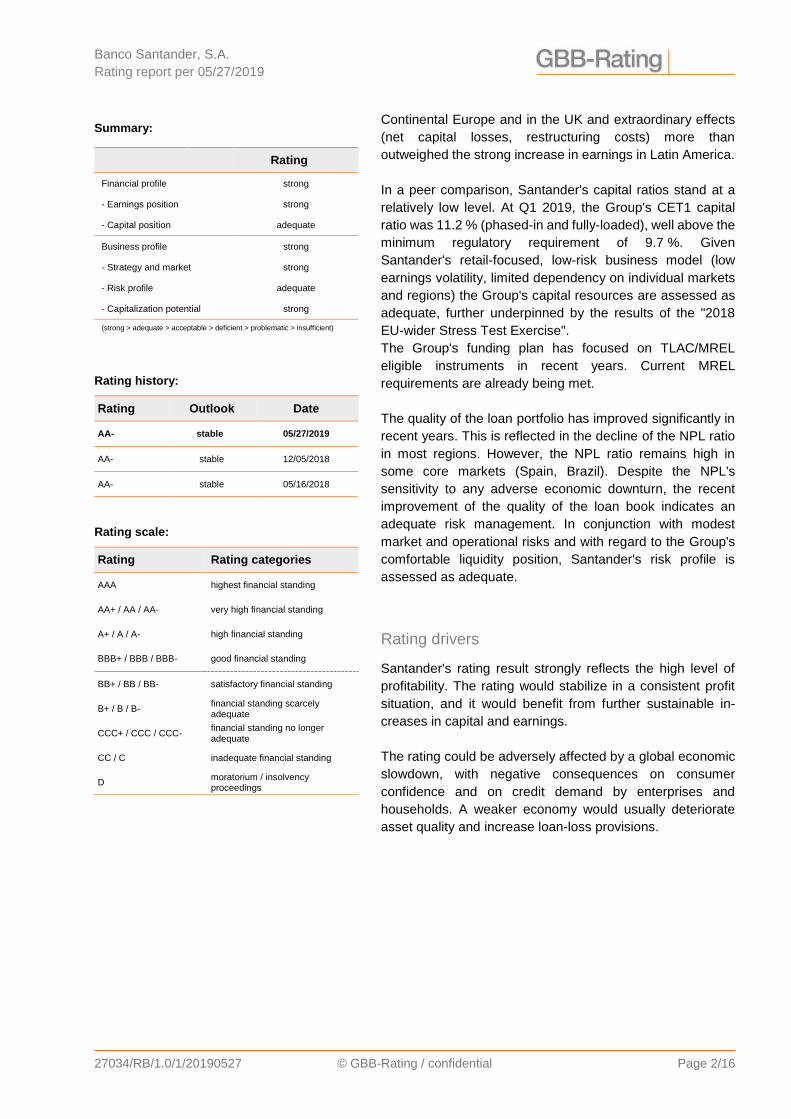

Summary:

Rating

Financial profile strong

- Earnings position strong

- Capital position adequate

Business profile strong

- Strategy and market strong

- Risk profile adequate

- Capitalization potential strong

(strong > adequate > acceptable > deficient > problematic > insufficient)

Rating history:

Rating Outlook Date

AA- stable 05/27/2019

AA- stable 12/05/2018

AA- stable 05/16/2018

Rating scale:

Rating Rating categories

AAA highest financial standing

AA+ / AA / AA- very high financial standing

A+ / A / A- high financial standing

BBB+ / BBB / BBB- good financial standing

BB+ / BB / BB- satisfactory financial standing

B+ / B / B- financial standing scarcely adequate

CCC+ / CCC / CCC- financial standing no longer adequate

CC / C inadequate financial standing

D moratorium / insolvency proceedings

Banco Santander, S.A.

Rating report per 05/27/2019

27034/RB/1.0/1/20190527 © GBB-Rating / confidential Page 3/16

Strategy and market

Strategy

Santander has a sound and sustainable strategy, focused on retail and commercial banking. The

Group's retail banking, which accounts for 88 % of total gross income in 2018, comprises a

comprehensive range of lending and deposit products, including residential mortgages, vehicle

financing and SME finance. Further business activities include wealth management (private banking,

asset management) and corporate & investment banking (wholesale banking business), which have

been established in recent years. Measured by their profit contribution, both divisions are of minor

importance.

The Group's business approach is characterized by broad geographical diversification and its model

of autonomous subsidiaries. Santander's core markets as measured by attributable profits and the

number of customers are Brazil, Spain, the United Kingdom (UK) as well as Central and Northern

Europe (Santander Consumer Finance). The geographical reach in both developed, generally low

interest rate markets and in emerging, relatively high interest rate markets helps to reduce

Santander's sensitivity to economic downturns in individual regions.

Santander defined a number of main strategic targets, comprising qualitative as well as quantitative

objectives (e. g. increase in customer satisfaction, growth in customer numbers, target ranges for

profitability and efficiency). GBB-Rating attests an efficient strategic management with view to the

following objectives:

The medium-term targets set in 2015 were all met in 2018.

The return on tangible equity (RoTE) increased to 11.7 % in 2018 from 10.0 % in 2015. The cost-

to-income ratio remained below 50 % during this period, considerably lower than the sector

average.

In 2018, the number of customers grew in all target markets (144 million, 2017: 133 million). The

rise was particularly pronounced in Spain, Brazil and Mexico. Furthermore, the number of clients

who consider Santander their main bank ("loyal customers") increased by 15 %. Since 2015, the

number of "digital" customers (commercial banking customers who used online/mobile banking

in the last 30 days) rose by 93 %.

Santander has a leading market position in retail lending in nearly all of its core markets. In the

UK and in Brazil, Santander is the largest foreign private bank. In Brazil, the Group's subsidiary

is the only foreign bank with a significant market share (about 9 %). In Spain and in Portugal,

Santander benefited from the takeover of Banco Popular Español S.A. (Banco Popular) in 2017

(lending share of 18 % in both markets).

Santander's management updated the mid-term plan and strategic targets in April 2019. Over the

next four years, Santander plans to invest about EUR 20 billion in digitalization and technology, in

particular in digital global payment solutions. The growth in digital offerings includes the launch of

open market apps for international payments in European core markets. It also includes the

expansion of "GetNet", a subsidiary of Santander Brazil which provides payment transactions with

cards and terminals, in Latin America and Europe. Santander plans to cut roughly EUR 1.2 billion of

Banco Santander, S.A.

Rating report per 05/27/2019

27034/RB/1.0/1/20190527 © GBB-Rating / confidential Page 4/16

annual costs, largely in Europe. The updated target range for the underlying RoTE (13-15 %)

appears to be ambitious but achievable.

Market

The macroeconomic environment deteriorated in 2018 in view of downward revisions of growth

forecasts for advanced economies, the economic slowdown in the Eurozone, and the (post-) Brexit

uncertainty. Global trade volumes plummeted in Q4 2018 and industrial production sharply

decreased in advanced economies and in China except for the USA. Nevertheless, consumer

confidence remains on a very high level on a worldwide scale.

In 2018, GDP of the Eurozone rose by 1.8 % (2017: 2.4 %). In response to the slowdown, the

European Central Bank adjusted its forward guidance and is likely to maintain the low level of interest

rates until at least 2020. The OECD and IMF revised growth forecasts for the Eurozone down to just

over 1 % in 2019. For the USA, the IMF also lowered the expected 2019 growth rate to 2.3 % (2018:

2.9 %).

Growth will remain considerably higher in emerging and developing economies than in advanced

economies. According to current forecasts, growth in Latin America is projected to recover in 2019

and 2020, mainly driven by Brazil and Mexico.

Albeit Brazil's GDP increased by 1.1 % in 2018, it fell short of forecasts (about 2 %), and grew only

marginally in Q4 2018. 2019 and 2020 forecasts predict some moderate growth of around 2 % and

2.5 %, respectively. The unemployment rate remains elevated and volatile, standing at 12.7 % in

March 2019. The weaker than expected labor market and the rising inflation (March 2019: 4.6 %)

may impede the recovery in purchasing power. On the other hand, the Brazilian banking system is

highly profitable with a double-digit average return on equity. As in other Latin American countries,

the financial system in Brazil is quite resilient to external shocks due to its experience in managing

volatility (economic development, foreign exchange risks) during the past decades. It should also be

noted that the number of problem assets of private banks have decreased considerably in the past

years, and the reduction of the loan-loss provision was a main driver for the increase in profitability.

The implementation of the pension reform remains uncertain but is likely to have a positive impact

on the economy.

In 2018, real GDP in Spain grew by 2.5 % (2017: 3.0 %) and above the Eurozone average (1.8 %),

driven by consumer spending and investment. In the wake of the positive economic environment in

recent years, the unemployment rate fell to 14.5 % in Q4 2018, the lowest level since the beginning

of the 2008 Financial Crisis. According to current predictions, growth momentum will slightly fade to

2.2 % in 2019 with view to potential impacts from a slowing global economic environment, the UK's

withdrawal from the EU and increasing protectionism. The NPL ratio in Spain developed favorably

in recent years to 3.7 % in Q4 2018, however, it still remains above the EU average (3.2 %). Demand

for consumer credits should be supported by robust growth of the Spanish economy and should

remain at high levels, despite a dip in Q1 2019 and tightened credit standards.

The economic development in the United Kingdom is strongly influenced by political uncertainty on

the withdrawal from the European Union. At this stage, the EU delayed Brexit until the end of October

2019. In the past two years, investment fell behind the OECD average and consumer confidence

Banco Santander, S.A.

Rating report per 05/27/2019

27034/RB/1.0/1/20190527 © GBB-Rating / confidential Page 5/16

declined. The short-term projection for GDP growth stands at 1.0 % to 1.5 %, primarily based on the

stable inflation, the robust labor market and growing wages. The fundamental data of the UK's

banking sector are sound with historically low NPL ratios and an average CET 1 ratio (fully loaded)

of 15.1 % as of Q4 2018, close to the EU average. According to recent stress test results conducted

by the British banking supervision (assumptions: "hard" Brexit, recession lasting several years), the

long-term fundamental position of British banks may worsen, however, they show a high level of

resilience and have sufficient leeway in an adverse economic scenario. Retail Banking is dominated

by four large domestic banks (Lloyds, Barclays, RBS, HSBC) and Santander UK. Consumer lending

grew strongly in recent years, albeit credit growth slowed down to about 8 % between Q3 2017 and

Q3 2018. Positively, mortgage lending increased at about 3 % in the same period. Growth rates are

expected to remain at this level in 2019.

Strong long-term earnings position

Santander's long-term earnings position is assessed as strong. The Group's profitability, which is

already at a very high level, continued to improve in 2018. According to GBB-Rating's calculation

method (see appendix), the return on equity rose to 13.3 % compared to 11.5 % in 2017. The cost

income ratio remains at a remarkably low level in comparison to peers and stood at 49.6 % in 2018

(2017: 51.9 %). Taking into account impairment losses ("cost-income ratio I", see appendix), the

ratio also improved to 66.4 % from 67.8 %.

The improvement in the profitability and cost indicators stems mainly from the increase in adjusted

gross profit and operating profit which are primarily due to the significant decline in impairment losses

on intangible assets to EUR 0.1 billion (2017: EUR 1.1 billion) and lower provisions of EUR 2.2 billion

(2017: EUR 3.1 billion). The Group's net interest income as the main source of earnings was virtually

unchanged (EUR 34.3 billion). The net commission income slightly decreased (-1 %), mainly due to

higher commission expenses. The result from categories of financial instruments rose by EUR 0.9

billion to EUR 2.8 billion, partly due to higher gains on financial assets and liabilities held for trading.

The positive developments in provisions and impairments and in the result from categories of

financial instruments more than outweighed the losses on exchange differences of EUR 0.7 billion

(2017: gain of EUR 0.1 billion) and the sharp decline in gains on non-financial assets to EUR 0.0

billion from EUR 0.5 billion due to the sale of Allfunds Bank in 2007. Overall, the adjusted gross profit

rose by nearly 4 %.

Administration costs remained almost unchanged at EUR 20.4 billion as the decrease in staff costs

was offset by the rise in IT expenditures. Impairment of financial assets measured at amortized costs

further decreased by nearly 3 % to EUR 9.0 billion. As a result, profit before tax grew by EUR 2.1

billion to EUR 14.2 billion.

Banco Santander, S.A.

Rating report per 05/27/2019

27034/RB/1.0/1/20190527 © GBB-Rating / confidential Page 6/16

Interim result as of 31 March 2019

In comparison to Q1 2018, total income declined by 0.5 %. Whilst net interest income increased by

2.7 %, it was offset by lower gains on financial transactions and exchange differences, primarily due

to higher costs of foreign currency hedging. Compared to Q4 2018, total income was 3.6 % lower,

mainly due to weaker net interest income (-4.2 %) from the impact of the revised IFRS 16 and fewer

days in the quarter.

Operating expenses stayed flat in comparison to Q1 2018 and declined by 3.0 % compared to Q4

2018.

Falling total income was compensated by a further decline in loan-loss provisions (-4.8 % compared

to Q1 2018). As a result, underlying profit before tax was just 0.1 % below the level of Q1 2018, and

higher than in Q4 2018 (+3.9 %).

The attributable profit to the parent (-11.0 % compared to Q4 2018; -10.4 % compared to Q1 2018)

was negatively affected by a higher tax on profit, restructuring costs (Poland, UK) and capital losses

due to property sales.

In Continental Europe, underlying profit before tax fell by 3.4 % compared to Q1 2018, with a marked

decline in Spain (-10.5 %, mainly due to lower gains in financial transactions). In the UK, profit before

tax declined sharply by 16.8 % since total income was negatively impacted by competitive pressure,

lower mortgage margins and lower gains on financial transactions; the attributable profit was even

36.0 % lower than in Q1 2018 because of restructuring costs (branch closures). In contrast, profit

before tax rose by 5.5 % in Latin America, with substantial profit growth in Brazil (+8.4 %) and Mexico

(+20.0 %).

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

50,000

2018 2017 2016

Adjusted gross profit

Administration costs

Development of adjusted gross profit and administration costs (EUR m)

7%

8%

9%

10%

11%

12%

13%

14%

15%

2018 2017 2016

Return on equity (%)

Banco Santander, S.A.

Rating report per 05/27/2019

27034/RB/1.0/1/20190527 © GBB-Rating / confidential Page 7/16

Interim Results* (EUR m) Q1 2019 Q4 2018 Q1 2018

Net interest income 8,682 9,061 8,454

Net fee income 2,931 2,956 2,955

Total income 12,085 12,542 12,151

Operating expenses -5,758 -5,936 -5,764

Net operating income 6,327 6,606 6,387

Net loan-loss provisions -2,172 -2,455 -2,282

Underlying profit before tax 3,684 3,546 3,689

Underlying profit from continuing operations 2,358 2,369 2,409

Attributable profit to the parent 1,840 2,068 2,054

* Based on Santander's interim accounts without GBB-Rating adjustments

In consequence of the lower attributable profit, the Group's RoTE dropped by 0.8 percentage points

to 11.3 % compared to Q4 2018 but remains on a high level. The cost-to-income ratio maintains a

comparatively low level (47.6 % in Q1 2019).

Adequate sustained capital position

As of 31 March 2019, Santander's CET1 ratio stood at 11.3 %, both on a phased-in and on a fully-

loaded basis; the leverage ratio was 5.1 %. The Group targets a CET 1 capital ratio (fully-loaded)

between 11 % and 12 % in the medium term. On a fully-loaded basis, total capital increased to EUR

90.0 billion in Q1 2019 (compared to EUR 87.5 billion as of 31 December 2018). The Group applies

the transitional arrangements of IFRS 9 according to Article 473a of the CRR, mitigating the impact

of the new impairment regime. According to Santander, the fully loaded CET1 ratio would decrease

to 11.0 % with full implementation of IFRS 9 (as of March 2019).

Santander's capital ratios clearly exceed the regulatory minimum requirements of 13.2 % for the total

capital ratio and 9.7 % for the CET 1 capital ratio (as of March 2019), with a Pillar 2 requirement of

1.5 % and a combined buffer requirement of 3.7 %. In Q1 2019, the buffer to the Maximum

Distributable Amount (MDA) was 1.6 percentage points and therefore quite comfortable.

Selected data: Capital structure (EUR m) 03/31/2019 Phased-in

03/31/2019 Fully-loaded

12/31/2018 Phased-in

12/31/2018 Fully-loaded

Common equity tier 1 capital 68,230 68,230 67,962 66,904

Tier 1 capital 77,705 75,826 77,716 75,838

Total capital 90,141 89,983 88,725 87,506

Risk-weighted assets 606,300 606,300 592,319 592,319

CET1 capital ratio 11.25 % 11.25 % 11.47 % 11.30 %

Tier 1 capital ratio 13.05 % 12.91 % 13.12 % 12.80 %

Total capital ratio 14.87 % 14.84 % 14.98 % 14.77 %

Compared to its peers, Santander's capital ratios are on a comparatively low level. This is also

reflected in the results of the "2018 EU-wide Stress Test" which ranks Santander's fully-loaded CET1

Banco Santander, S.A.

Rating report per 05/27/2019

27034/RB/1.0/1/20190527 © GBB-Rating / confidential Page 8/16

capital ratio lower than those of all other 47 participants. However, the stress test indicated that the

adverse scenario resulted in one of the exercise's most contained negative impacts on the fully-

loaded CET1 capital ratio between 2017 and 2020, reflecting the Group's sound risk profile.

Santander was also one of few participants that were able to generate a cumulative profit in a three-

year adverse scenario.

MREL/TLAC

In recent years, Santander's funding plan has focused on MREL/TLAC eligible instruments as part

of the resolution strategy. Since the TLAC requirement is requested at each resolution entity,

Santander's operating model of legally independent subsidiaries renders multiple points of entry. In

consideration of Santander's minimum TLAC requirement of 16.0 % of resolution group RWAs, the

G-SIB buffer (1.0 %) and the capital conversation buffer (2.5 %), the Group's TLAC requirement is

19.5 % of RWA as of January 2019.

Santander received formal notification of the MREL requirement in May 2018 for the Banco

Santander S.A. Resolution Group at a sub-consolidated level; the minimum required eligible liabilities

were set at EUR 114.5 billion, representing 24.35 % of the Resolution Group’s risk-weighted assets.

These current requirements are met by Santander.

In order to comply with the TLAC/MREL requirements, on a Euro-basis, the Group issued EUR 13.5

billion of eligible instruments (2017: EUR 19.8 billion). This issue volume is dominated by senior non-

preferred and other senior debt (EUR 10.3 billion). In Q1 2019, Santander issued TLAC eligible

preferred debt in the amount of EUR 1.1 billion.

Strong capitalization potential

In light of Santander's strong earnings position, the Group has a strong and sustainable internal

financing capacity. Since 2009, the Group's net operating income never fell below EUR 20 billion,

illustrating the sustainability of the bank's profits and its relatively low susceptibility to earnings

volatility.

Santander's ability to strengthen its capital resources by way of capital market issues is assessed

as strong (see "sustained capital position"). In order to strengthen AT1 capital, the bank recently

issued CoCo bonds (February 2019: USD 1.2 billion; March 2018: EUR 1.5 billion).

By market capitalization, Banco Santander is the largest bank in the Eurozone, although the bank's

share price fell by more than 27 % in 2018 (market capitalization: EUR 64.5 billion as of 31 December

2018; 2017: EUR 88.4 billion). The decline was in line with the poor general market trend in 2018.

At the end of 2018, Santander had about 4.1 million shareholders. Institutional investors held about

59 % (2017: 61 %) of the share capital; nearly 40 % (2017: 38 %) of Santander's share capital were

in the hands of retail investors. The majority of the share capital (> 75 %) is located within Europe.

As in previous years, no shareholder (with the exception of custodians) had an ownership interest

greater than 3 %. Due to the diversified ownership structure, a shareholder's support in case of need

is considered unlikely.

Banco Santander, S.A.

Rating report per 05/27/2019

27034/RB/1.0/1/20190527 © GBB-Rating / confidential Page 9/16

Risk profile

Credit and counterparty risk

The main geographical markets in terms of total lending are Spain, the UK, Brazil and the United

States. More than half of the lending volume accounts for secured loans (e. g. mortgage loans).

Over the past few years, the credit quality improved to a significant extent as reflected in the steady

decline of the NPL ratio in most markets. As of Q1 2019, the overall NPL ratio amounted to 3.6 %

(Q1 2018: 4.0 %). In the same period, the volume of non-performing loans fell by 4.9 % to EUR 35.6

billion. In line with the overall trend, the NPL ratio continuously decreased in Continental Europe in

recent years (Q1 2019: 5.2 %; Q1 2018: 5.8 %). However, it remains elevated in Spain (Q1 2019:

6.2 %; Q1 2018: 6.3 %) due to the acquisition of Banco Popular in 2017 and despite the sale of

Banco Popular's real estate business; excluding Popular's portfolio, the NPL ratio stood at just 4.7 %

at the end of 2017. In the UK, the NPL ratio remains on a considerably lower level (Q1 2019: 1.1 %).

Until now, negative impacts on the NPL of the impending Brexit have not been discernible. In the

United States, the NPL ratio stayed on an acceptable level (Q1 2019: 2.4 %; Q1 2018: 2.9 %). In

Brazil, which is the Group's key market in Latin America, the NPL ratio remains high (Q1 2019: 5.3 %,

at previous year's level). The same applies to the cost of credit which dropped to 3.9 % in Q1 2019

(Q1 2018: 4.4 %), but remains high compared to the Group level.

As to the coverage ratio, there was a downward trend in Continental Europe over the past years (Q1

2019: 52.1 %; 2015: 64.2 %), whereas it increased in Latin America (Q1 2019: 97.7 %). In the USA,

the ratio remained well above 100 %. In Spain and in the UK, the coverage ratio remains low (44.1 %

and 31.0 %, respectively) as a result of the dominant mortgage portfolios. In this context, it should

be noted that more than 80 % of the residential mortgage portfolio in Spain has an LTV below 80 %;

in the UK, the average LTV is about 40 %.

In view of the bank's progress in credit risk mitigation, GBB-Rating evaluates the risk management

and risk monitoring systems to be appropriate and effective. Nevertheless, it remains to be monitored

how a possible economic downturn may effect credit quality.

Market risk

The Group faces limited interest and exchange rate risks arising from the banking book; market risks

resulting from trading activities are of minor importance.

In line with the BCBS standards for Interest Rate Risks in the Banking Book (IRRBB), Santander

conducts six interest rate scenarios, measuring the interest rate risk on both economic values (EVE)

and earnings (NII). As in the previous year, a parallel downward shock would have the most severe

impact on the change in economic value of equity (EUR 8.0 billion as of 31 December 2018);

however, the "early warning signal" according to the IRRBB guidelines released by EBA (threshold:

decline in economic value greater than 15 % of Tier 1 capital) is not exceeded.

A rise in interest rates would have opposite effects in the Group's core markets: in Europe and in the

USA, where interest rates are at a very low level, a rise in interest rates would positively affect net

interest income and the economic value of equity; in Latin America, earnings and economic values

would decrease.

Banco Santander, S.A.

Rating report per 05/27/2019

27034/RB/1.0/1/20190527 © GBB-Rating / confidential Page 10/16

Since the structural VaR was considerably higher than the trading risk VaR (EUR 568.5 million vs

EUR 9.7 million as of 31 December 2018), the main drivers for market risks derive from the banking

book. Regarding Santander's capital base and its profitability, market risks are deemed manageable.

Funding and liquidity

The majority of Santander's total assets account for net loans to customers with a long-term maturity;

the Group's funding is based on predominantly short-term customer deposits and, to a lesser extent,

medium- and long-term financial instruments. Due to the high extent of retail and commercial

banking, the Group has a sufficiently large and stable base of customer deposits.

As of 31 December 2018, the LTD ratio was at 113 % (2017: 109 %; target: below 120 %), well in

line with the European average1.

The regulatory liquidity ratios indicate a comfortable liquidity position. As of end-2018, the Group's

LCR stood at 158 % and the NSFR was at 114 %. In all legal entities, both ratios were above 100 %.

In view of the sound balance sheet structure, the diversified funding structure and the robust liquidity

ratios, the Group has in place a sound and effective liquidity risk mitigation.

Operational and legal risks

The provisions for customer remediation account for 12 % of total provisions for taxes and other

legal contingencies and mainly include the estimated redress payments relating to the sale of

Payment Protection Insurance (PPI) policies in the UK. The deadline for PPI complaints is 29 August

2019. With respect to the mis-selling of PPI, Santander UK plc raised provisions of EUR 275 million

for PPI and EUR 406 million for related costs.

Provisions for employment-related proceedings in Brazil amount to EUR 859 million at year-end

2018. These legal proceedings have been mainly initiated by trade unions, associations and former

employees to claim overtime pay, retirement benefits and compensation associated with other

employment rights. Such proceedings are common practice in Brazil, and provisions are similarly

high as in previous years.

Further legal risks may arise from the acquisition of Banco Popular, which had concluded a high

number of transactions with floor clauses ("Clausula Suelo"). In the past years, resulting from several

rulings of the EU Court of Justice and of Spanish courts, borrowers have been able to lodge

complaints for overpaid amounts due to the floor clauses. Provisions used for refunds in 2017 and

2018 amounted to EUR 357 million. As of end-2018, provisions amount to EUR 104 million.

As the successor entity to Banco Popular, Santander is exposed to legal risks resulting from claims

of investors of Banco Popular against the EU’s Single Resolution Board (SRB) decision (resolution

of Banco Popular, redemption and conversion of capital instruments). Santander estimates

compensation payments to shareholders at EUR 680 million.

1 According to EBA, the EU average for the LTD ratio for households and non-financial corporations was 117 % (Dec. 18)

Banco Santander, S.A.

Rating report per 05/27/2019

27034/RB/1.0/1/20190527 © GBB-Rating / confidential Page 11/16

In 2018, about 60 % of net losses resulting from operational risks refer to the risk category "practices

with customers, products and business practices", which include customer complaints for improper

marketing and inaccurate information on products. In addition, external fraud, in particular the

fraudulent use of debit and credit cards and incidents related to the execution, delivery and process

management are of relevance. By geographical distribution Brazil accounts for 45 % of net losses,

employee litigation not included.

Banco Santander, S.A.

Rating report per 05/27/2019

27034/RB/1.0/1/20190527 © GBB-Rating / confidential Page 12/16

Appendix

Assets – selected data (EUR m) 12/31/2018 12/31/2017 12/31/2016

Cash and cash balances at central banks 113,663 110,995 76,454

Financial assets held for trading 92,879 125,458 148,187

Financial assets at fair value through profit or loss 68,190 34,782 31,609

Financial assets at fair value through other comprehensive income

121,091

Financial assets available-for-sale 133,271 116,774

Financial assets at amortized cost 946,099

Loans and receivables 903,013 840,004

Investments held-to-maturity 13,491 14,468

Hedging derivatives 8,607 8,537 10,377

Fair value changes of the hedged items in portfolio 1,088 1,287 1,481

Investments accounted at equity / in associates 7,588 6,184 4,836

Intangible assets 3,094 2,914 2,697

Goodwill 25,466 25,769 26,724

Tangible assets 26,157 22,974 23,286

Assets held for sale 5,426 15,280 5,772

Tax assets 30,251 30,243 27,678

Other assets 9,672 10,107 8,778

Total assets 1,459,271 1,444,305 1,339,125

Liabilities – selected data (EUR m) 12/31/2018 12/31/2017 12/31/2016

Financial liabilities held for trading 70,343 107,624 108,765

Financial liabilities designated at fair value through profit or loss

68,058 59,616 40,263

Financial liabilities at amortized cost 1,171,630 1,126,069 1,044,240

Hedging derivatives 6,363 8,044 8,156

Fair value changes of the hedged items in portfolio 303 330 448

Provisions 13,225 14,489 14,459

Tax liabilities 8,135 7,592 8,373

Other liabilities 13,853 13,708 11,722

Equity 107,361 106,833 102,699

Total liabilities and equity 1,459,271 1,444,305 1,339,125

Banco Santander, S.A.

Rating report per 05/27/2019

27034/RB/1.0/1/20190527 © GBB-Rating / confidential Page 13/16

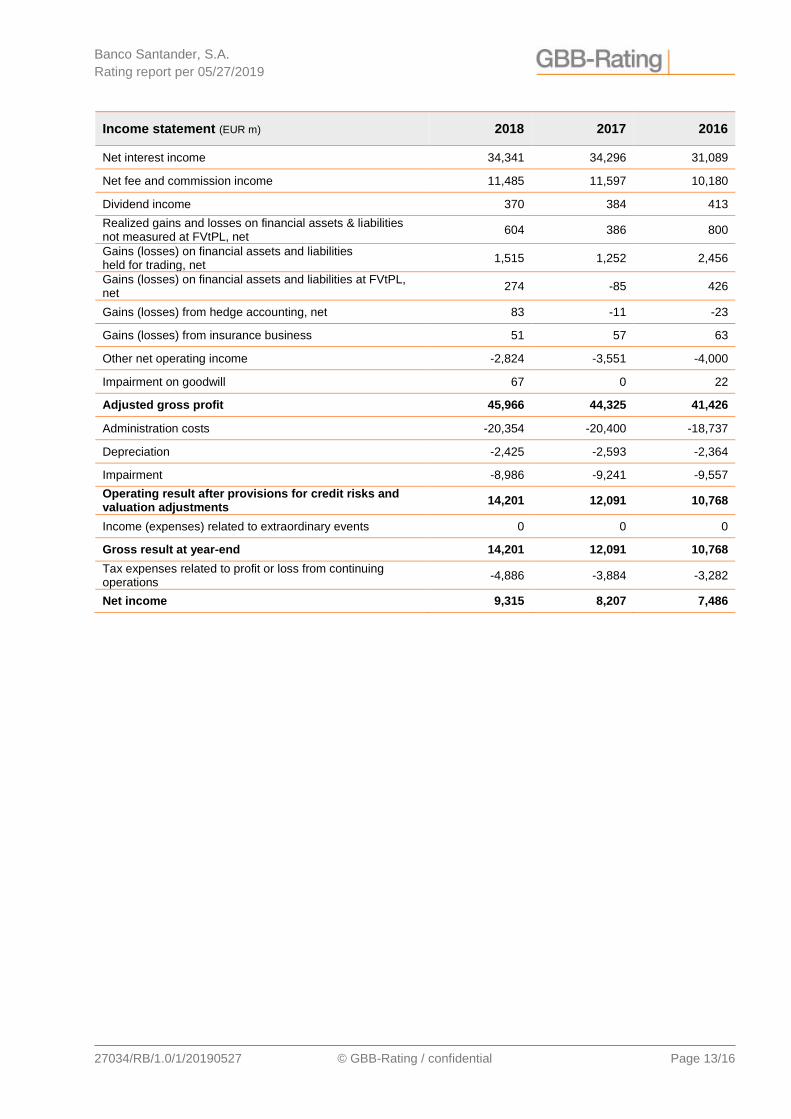

Income statement (EUR m) 2018 2017 2016

Net interest income 34,341 34,296 31,089

Net fee and commission income 11,485 11,597 10,180

Dividend income 370 384 413

Realized gains and losses on financial assets & liabilities not measured at FVtPL, net

604 386 800

Gains (losses) on financial assets and liabilities held for trading, net

1,515 1,252 2,456

Gains (losses) on financial assets and liabilities at FVtPL, net

274 -85 426

Gains (losses) from hedge accounting, net 83 -11 -23

Gains (losses) from insurance business 51 57 63

Other net operating income -2,824 -3,551 -4,000

Impairment on goodwill 67 0 22

Adjusted gross profit 45,966 44,325 41,426

Administration costs -20,354 -20,400 -18,737

Depreciation -2,425 -2,593 -2,364

Impairment -8,986 -9,241 -9,557

Operating result after provisions for credit risks and valuation adjustments

14,201 12,091 10,768

Income (expenses) related to extraordinary events 0 0 0

Gross result at year-end 14,201 12,091 10,768

Tax expenses related to profit or loss from continuing operations

-4,886 -3,884 -3,282

Net income 9,315 8,207 7,486

Banco Santander, S.A.

Rating report per 05/27/2019

27034/RB/1.0/1/20190527 © GBB-Rating / confidential Page 14/16

Credit and Counterparty risk cluster 2018 2017 2016

Gross profitability 1 Adjusted gross profit / Average Total assets

3.2 % 3.2 % 3.1 %

Gross profitability 2 Net interest income and net credit risk provisions / Average risk-weighted exposure amounts 1)

5.0 % 4.8 % 4.4 %

Net profitability 1 Operating result after provisions for credit and valuation adjustments / Average total risk exposure amount

2.4 % 2.0 % 1.9 %

Net profitability 2 Gross annual profit / Average adjusted total assets 2)

0.9 % 0.8 % 0.8 %

Return on equity 1 Operating result after provisions for credit risks and valuation adjustments / Average total capital

13.3 % 11.5 % 10.7 %

Return on equity 2 Gross annual profit / Average total capital

13.3 % 11.5 % 10.7 %

Cost income ratio 1 Administration costs and provisions for credit risks / Gross profit

66.4 % 67.8 % 69.4 %

Cost income ratio 2 Administration costs / Adjusted gross profit

49.6 % 51.9 % 50.9 %

Financial data (EUR m) 12/31/2018 12/31/2017 12/31/2016

Net interest income 34,341 34,296 31,089

Net interest income and net provisions for credit risks 25,355 25,055 21,532

Gross profit 47,845 47,575 44,178

Adjusted gross profit 45,966 44,325 41,426

Administration costs -22,779 -22,993 -21,101

Administration costs and provisions for credit risks -31,765 -32,234 -30,658

Operating result after provisions for credit risks and valuation adjustments

14,201 12,091 10,768

Gross annual profit 14,201 12,091 10,768

Average risk-weighted exposure amounts1) 509,390 525,926 493,548

Average total risk exposure amount 593,822 613,714 581,748

Average total assets 1,451,788 1,391,715 1,339,693

Average adjusted total assets2) 1,616,153 1,463,661 1,407,942

Average total capital 107,097 104,766 100,726

1) Risk weighted exposure amount for credit, counterparty credit and dilution risks and free deliveries 2) Comprises on-balance sheet total assets, contingent liabilities and loan-loss allowances

Banco Santander, S.A.

Rating report per 05/27/2019

27034/RB/1.0/1/20190527 © GBB-Rating / confidential Page 15/16

Indicators of sustained capital position 12/31/2018 12/31/2017 12/31/2016

Total capital ratio Own funds / Total risk exposure amount

15.0% 15.0% 14.7%

Tier 1 capital ratio Tier 1 capital / Total risk exposure amount

13.1% 12.8% 12.5%

Common equity Tier 1 ratio Common equity tier 1 capital / Total risk exposure amount

11.5% 12.3% 12.5%

Financial data (EUR m) 12/31/2018 12/31/2017 12/31/2016

Own funds 88,725 90,706 86,337

Tier 1 capital 77,716 77,283 73,709

Common equity Tier 1 capital 67,962 74,173 73,709

Total risk exposure amount 592,319 605,064 588,088

Banco Santander, S.A.

Rating report per 05/27/2019

27034/RB/1.0/1/20190527 © GBB-Rating / confidential Page 16/16

Regulatory disclosure requirements

Name and function of the analysts:

Daniel Sebastian Bittner, Lead Rating Analyst GBB-Rating, Cologne Angelika Komenda, Rating Analyst GBB-Rating, Cologne

Company address:

GBB-Rating Gesellschaft für Bonitätsbeurteilung mbH, Kattenbug 1, 50667 Cologne

Members of the Rating Committee:

Stefan Koll, Manager GBB-Rating, Cologne Christina Weymann, Senior Manager GBB-Rating, Cologne Volker Jindra, Senior Manager GBB-Rating, Cologne

Date Rating Commitee Notification Issue

First rating 12/19/2013 12/20/2013 02/26/2014 Current rating 05/27/2019 05/27/2019

Validity:

Rating: 12 months Outlook: 24 months

Subsequent rating changes after notification to client:

Major sources of information for the rating:

Annual report as at 12/31/2018 Quarterly Report Q1 2019 Conference calls Further disclosures and company specific information

Statement about the quality of information available (including potential restrictions):

The quality and extent of information (interviews and documents) were suitable to obtain a comprehensive picture of the bank and to assign an objective, transparent and professional credit rating

Applicable rating methodology, rating type and release:

Solicited rating Methodology for Rating 3.0.03 Banks – credit and counterparty credit risk (CCR) www.gbb-rating.eu/de/presse/eu-veroeffentlichungen/Seiten/default.aspx

Meaning of the rating category:

www.gbb-rating.eu/en/ratings/ratingskala/Pages/default.aspx

Business relationship:

Besides the rating mandate there are further business relationships within the group

Legal remarks

GBB-Rating Gesellschaft für Bonitätsbeurteilung mbH does not make any guarantees regarding the accuracy, completeness or timeliness

of the present rating or the data, values and other information presented (including ERI) or the eligibility of this information for specific

purposes nor for losses arising from the use of the information or in confidence in the information. The current rating report is not an

investment recommendation.

Future events are uncertain. Ratings are based on predictions of these and thus inevitably rely upon estimates. Therefore they solely

represent statements of opinion rather than statements of fact or investment advice.

Credit ratings are performed with proficiency and due professional care. Ratings are based on the data and

information provided by the applicant. This information is used in reaching an opinion about the future viability as

well as the strengths and weaknesses of the rated company as of the date of rating issuance.

GBB-Rating puts focus on sustainability and is a signatory of the UN Global Compact since 2018. We

support the 10 principles of the UN Global Compact relating to human rights, labor standards, the

environment and anti-corruption.