A sustainable & secure transition to a low carbon future sustainable & secure transition to a low...

22

© OECD/IEA 2017 A sustainable & secure transition to a low carbon future Dr. Fatih Birol The Round Table for Studying Energy Situations, METI , Tokyo, 27 February 2018 IEA Executive Director, International Energy Agency Document 5

Transcript of A sustainable & secure transition to a low carbon future sustainable & secure transition to a low...

© OECD/IEA 2017

A sustainable & secure transition to

a low carbon future

Dr. Fatih Birol

The Round Table for Studying Energy Situations, METI , Tokyo, 27 February 2018

IEA

Executive Director, International Energy Agency

Document 5

© OECD/IEA 2017

Tipping the energy world off its axis

• Four large-scale upheavals in global energy :

- The United States is turning into the undisputed global leader for oil & gas

- Solar PV is on track to be the cheapest source of new electricity in many countries

- China’s new drive to “make the skies blue again” is recasting its role in energy

- The future is electrifying, spurred by cooling, electric vehicles & digitalisation

• These changes brighten the prospects for affordable, sustainable energy &

require a reappraisal of approaches to energy security

• There are many possible pathways ahead & many potential pitfalls if

governments or industry misread the signs of change

1

© OECD/IEA 2017

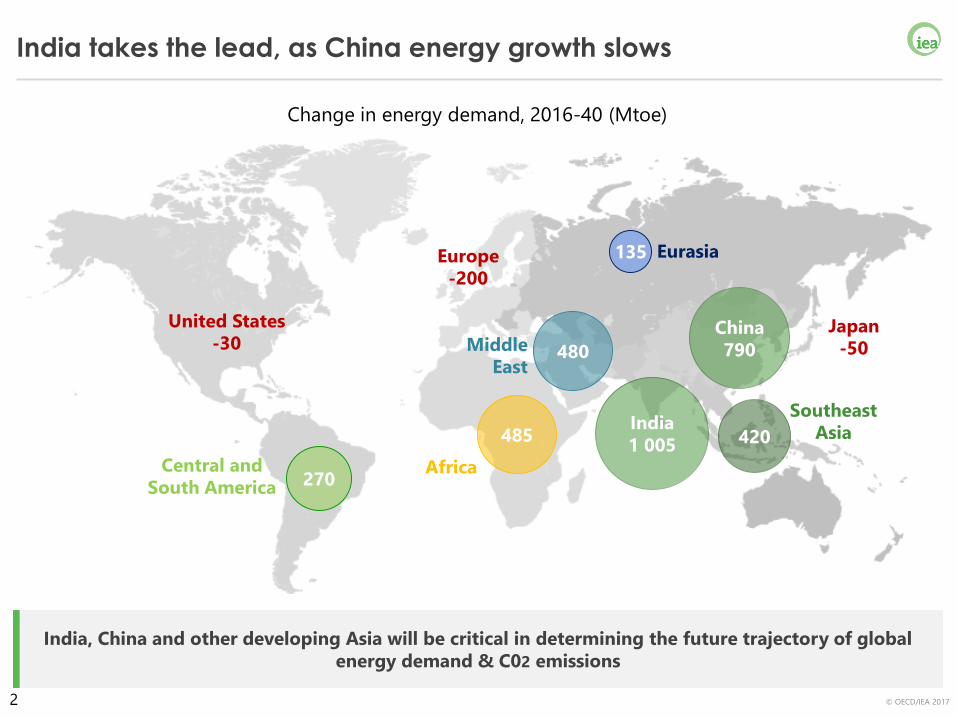

India takes the lead, as China energy growth slows

India, China and other developing Asia will be critical in determining the future trajectory of global

energy demand & C02 emissions

Change in energy demand, 2016-40 (Mtoe)

India

1 005 420

Southeast

Asia

China

790

United States

-30Japan

-50

Europe

-200

270Central and

South America

485

Africa

135 Eurasia

480Middle

East

2

© OECD/IEA 2017

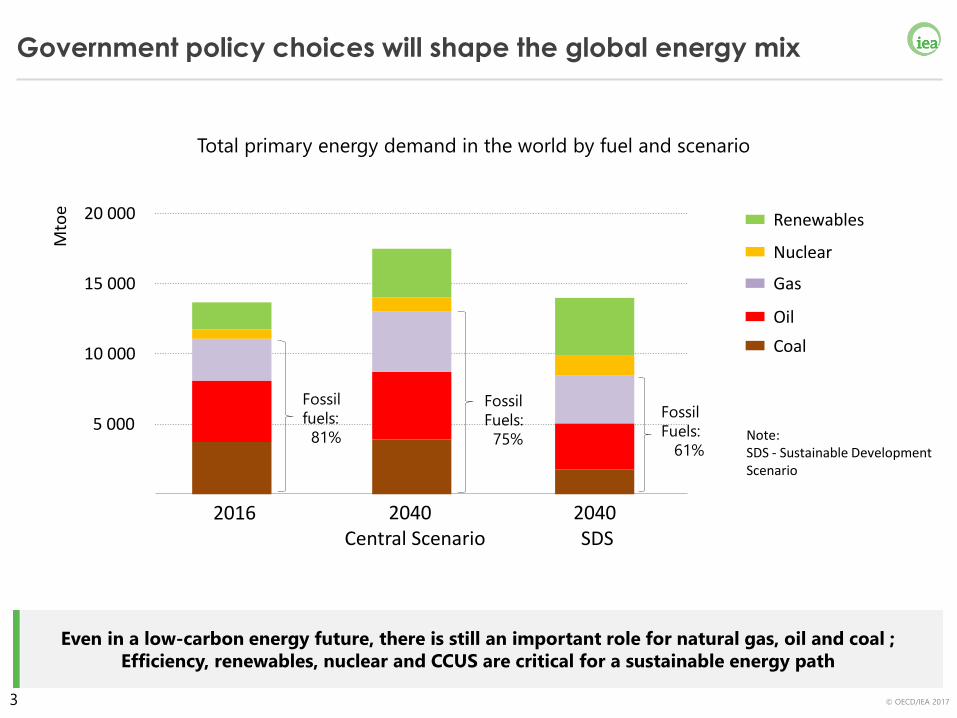

Government policy choices will shape the global energy mix

Even in a low-carbon energy future, there is still an important role for natural gas, oil and coal ;

Efficiency, renewables, nuclear and CCUS are critical for a sustainable energy path

Total primary energy demand in the world by fuel and scenario

5 000

10 000

15 000

20 000

2016 2040 Central Scenario

2040 SDS

Mto

e

Renewables

Nuclear

Gas

Oil

Coal

Note:SDS - Sustainable DevelopmentScenario

Fossil

fuels:

81%

Fossil

Fuels:

75%

Fossil

Fuels:

61%

3

© OECD/IEA 2017

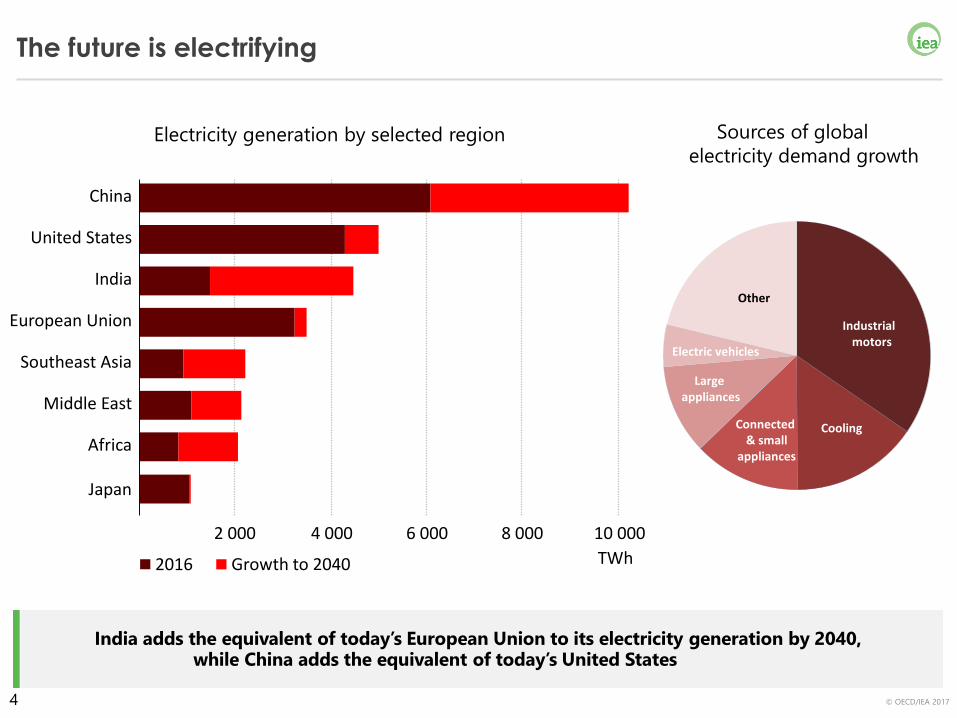

The future is electrifying

India adds the equivalent of today’s European Union to its electricity generation by 2040, while China adds the equivalent of today’s United States

Electricity generation by selected region

Middle East

2 000 4 000 6 000 8 000 10 000

Africa

Southeast Asia

European Union

India

United States

China

TWh2016 Growth to 2040

Sources of global

electricity demand growth

Industrial motors

Cooling

Large appliances

Connected & small

appliances

Electric vehicles

Other

Japan

4

© OECD/IEA 2017

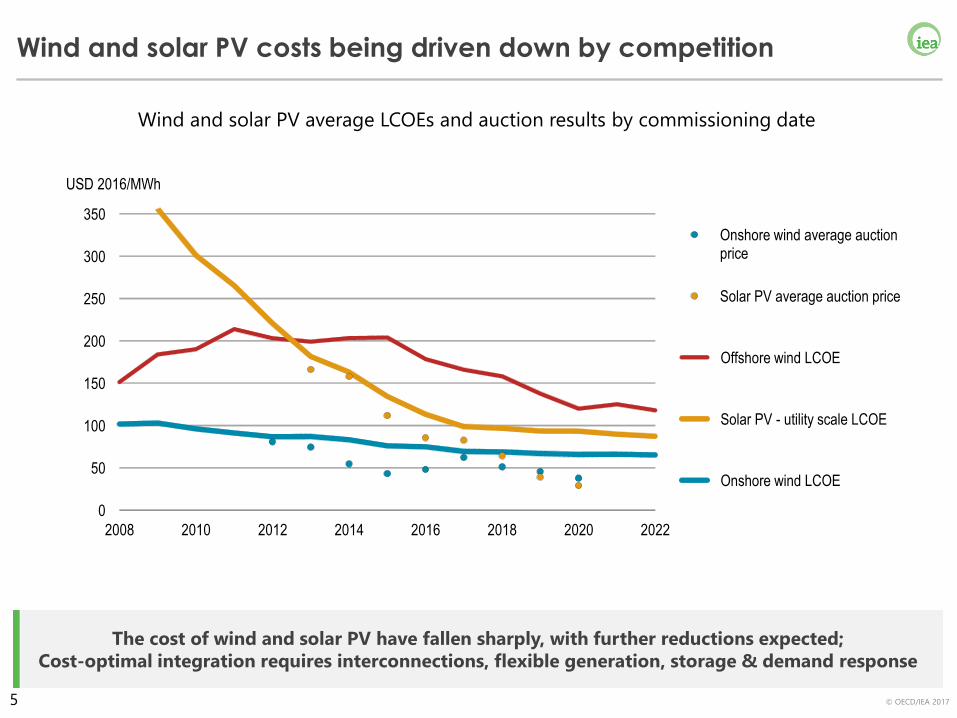

The cost of wind and solar PV have fallen sharply, with further reductions expected;

Cost-optimal integration requires interconnections, flexible generation, storage & demand response

Wind and solar PV average LCOEs and auction results by commissioning date

Wind and solar PV costs being driven down by competition

0

50

100

150

200

250

300

350

2008 2010 2012 2014 2016 2018 2020 2022

USD 2016/MWh

Onshore wind average auctionprice

Solar PV average auction price

Offshore wind LCOE

Solar PV - utility scale LCOE

Onshore wind LCOE

5

© OECD/IEA 2017

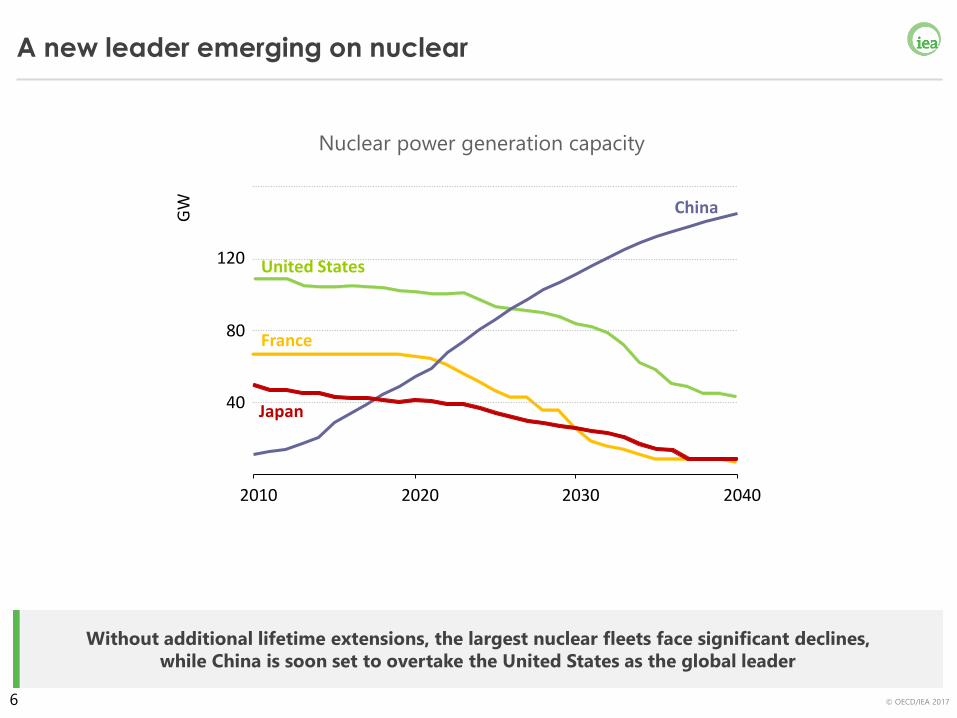

A new leader emerging on nuclear

Without additional lifetime extensions, the largest nuclear fleets face significant declines,

while China is soon set to overtake the United States as the global leader

Nuclear power generation capacity

40

80

120

2010 2020 2030 2040

GW

United States

China

France

Japan

6

© OECD/IEA 2017

The potential of clean energy technology remains under-utilised

Despite good progress in some areas, many technologies still need a strong push to achieve their full

potential and deliver a sustainable energy future

Energy storage Solar PV and onshore wind

Electric vehicles

●Not on track ●Accelerated improvement needed ●On track

Building energy efficiency Transport biofuels

Carbon capture and storage More efficient coal-fired power

Nuclear Transport – Fuel economy of light-duty vehicles

Lighting, appliances and building equipment Energy efficiency in industry

Hydrogen and Fuel Cells

7

© OECD/IEA 2017

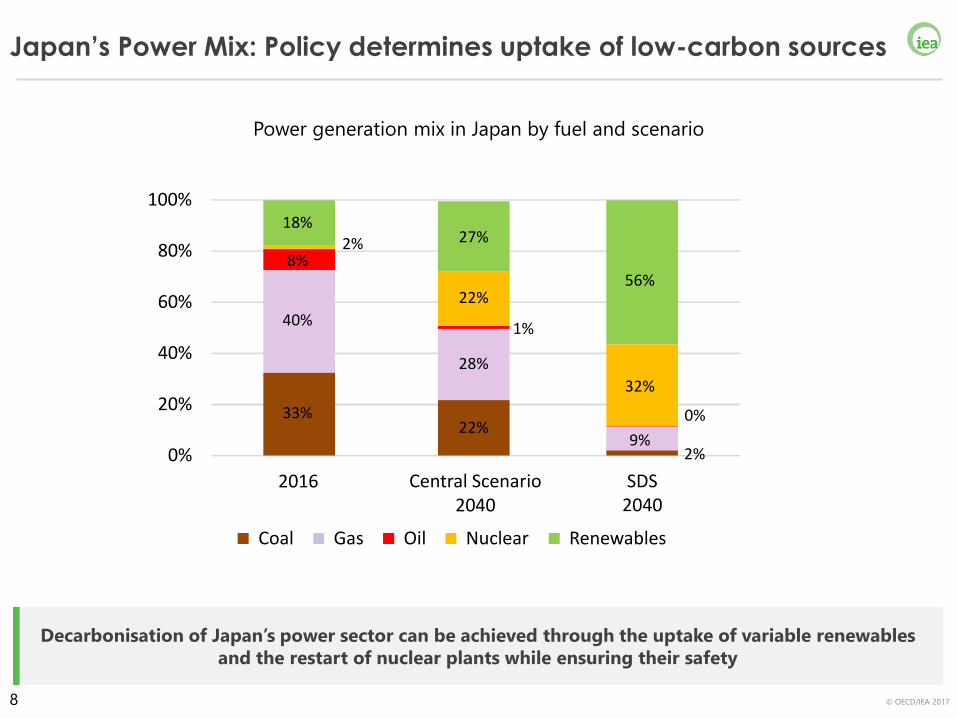

Japan’s Power Mix: Policy determines uptake of low-carbon sources

Decarbonisation of Japan’s power sector can be achieved through the uptake of variable renewables

and the restart of nuclear plants while ensuring their safety

Power generation mix in Japan by fuel and scenario

0%

20%

40%

60%

80%

100%

2016 Central Scenario2040

SDS2040

Coal Gas Oil Nuclear Renewables

33%

40%

8%2%

18%

22%

28%

1%

22%

27%

2%9%

0%

32%

56%

8

© OECD/IEA 2017

Recommendations for Japan

• Enhance energy security and resilience by taking an “all fuel” and “all technology“

approach to energy policy

• Continue to adjust renewable support policies in line with falling costs & ensure

there is adequate system flexibility including interconnections

• Pursue all low carbon options, including efficiency, renewables, nuclear (with

maximum safety), to decrease emissions in a cost-optimal way

• Continue to be a leader in global energy technology R&D and innovation

• Take advantage of the opportunities that digitalization is creating in the energy

sector, while being mindful of the associated risks

• The IEA stands ready to support the clean and secure energy transition in providing

cutting-edge technical advice to governments

9

© OECD/IEA 2017

www.iea.org

IEA

10

© OECD/IEA 2017

低炭素社会への持続的かつ確実な転換

ファティ・ビロル

エネルギー情勢懇談会 経済産業省(東京) 2018年2月27日

IEA

IEA 事務局長

仮訳資料5

© OECD/IEA 2017

エネルギー業界を根底から覆す

• 世界のエネルギーにおける4つの激変

- 米国が石油・天然ガス分野において、確固たるグローバル・リーダーへと変わる。

- 太陽光発電は、多くの国において最も安価な電源になりつつある。

- 中国は「青空を再び」というメッセージの下、エネルギー分野における役割を再構築

している。

- 冷房需要、電気自動車、デジタル化などによって電化社会の到来。

• こうした変化により、安価で持続可能なエネルギーの見通しは明るくなると同時にエネルギー安全保障に向けた取組みを再評価する必要性も出てくる。

• 今後、取り得るべき道程は数多く存在するが、政府や産業が変化の兆しを読み間違えれば、落し穴に落ちる可能性も十分にある。

1

仮訳

© OECD/IEA 2017

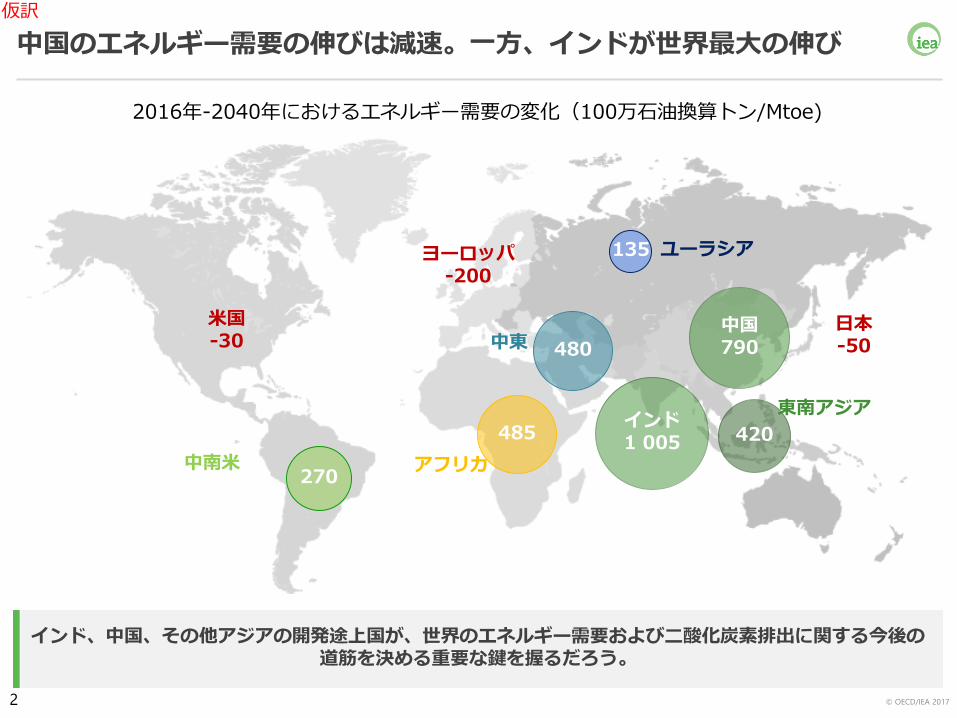

中国のエネルギー需要の伸びは減速。一方、インドが世界最大の伸び

インド、中国、その他アジアの開発途上国が、世界のエネルギー需要および二酸化炭素排出に関する今後の道筋を決める重要な鍵を握るだろう。

2016年-2040年におけるエネルギー需要の変化(100万石油換算トン/Mtoe)

インド1 005 420

東南アジア

中国790

米国-30

日本-50

ヨーロッパ-200

270中南米

485

アフリカ

135 ユーラシア

480中東

2

仮訳

© OECD/IEA 2017

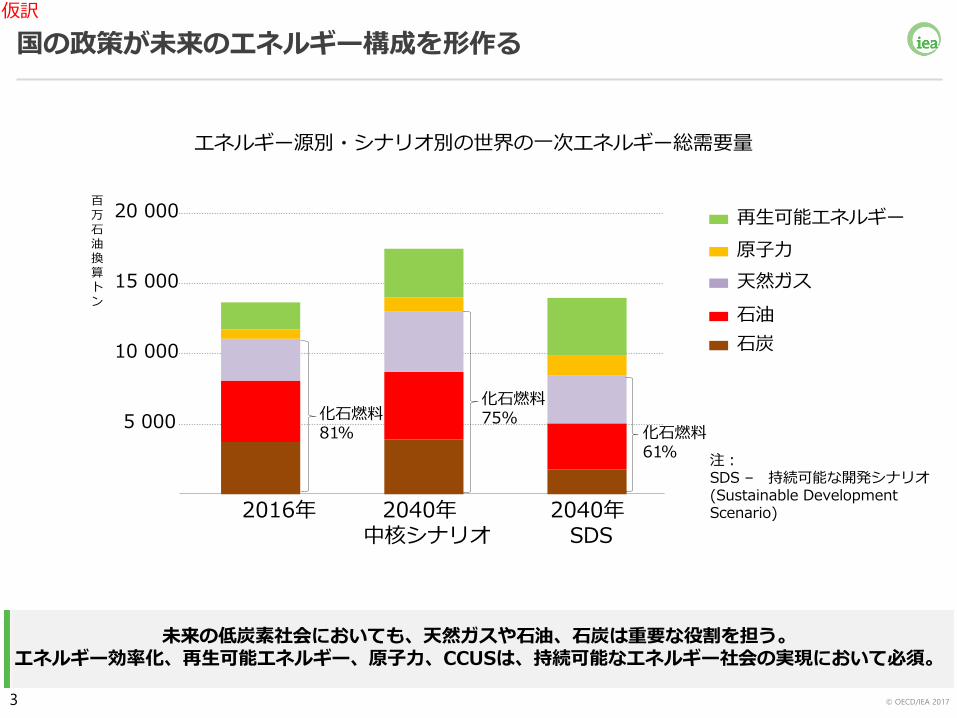

国の政策が未来のエネルギー構成を形作る

未来の低炭素社会においても、天然ガスや石油、石炭は重要な役割を担う。エネルギー効率化、再生可能エネルギー、原子力、CCUSは、持続可能なエネルギー社会の実現において必須。

エネルギー源別・シナリオ別の世界の一次エネルギー総需要量

5 000

10 000

15 000

20 000

2016年 2040年中核シナリオ

2040年SDS

百万石油換算トン

再生可能エネルギー

原子力

天然ガス

石油

石炭

注:SDS – 持続可能な開発シナリオ(Sustainable DevelopmentScenario)

化石燃料81%

化石燃料75%

化石燃料61%

3

仮訳

© OECD/IEA 2017

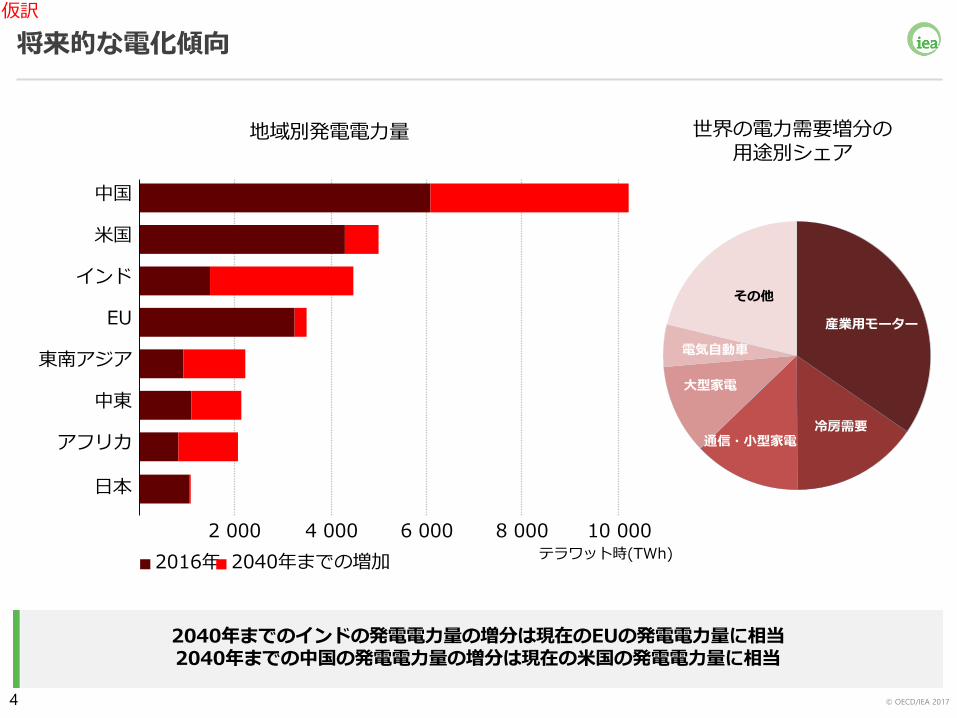

将来的な電化傾向

2040年までのインドの発電電力量の増分は現在のEUの発電電力量に相当2040年までの中国の発電電力量の増分は現在の米国の発電電力量に相当

地域別発電電力量

中東

2 000 4 000 6 000 8 000 10 000

アフリカ

東南アジア

EU

インド

米国

中国

テラワット時(TWh)2016年 2040年までの増加

世界の電力需要増分の用途別シェア

産業用モーター

冷房需要

大型家電

通信・小型家電

電気自動車

その他

日本

4

仮訳

© OECD/IEA 2017

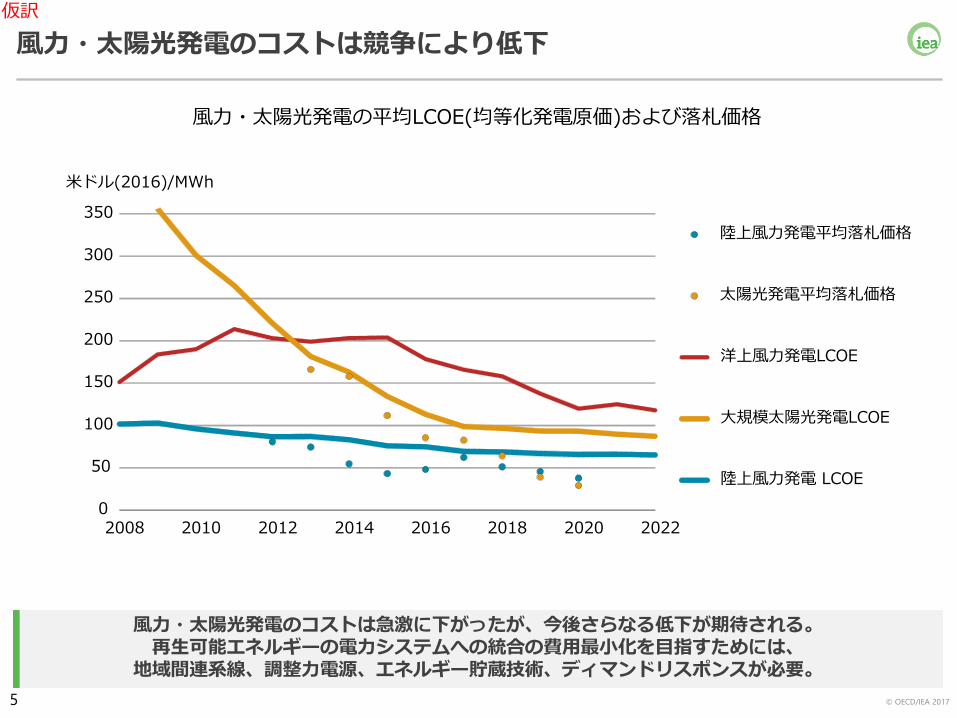

風力・太陽光発電のコストは急激に下がったが、今後さらなる低下が期待される。再生可能エネルギーの電力システムへの統合の費用最小化を目指すためには、

地域間連系線、調整力電源、エネルギー貯蔵技術、ディマンドリスポンスが必要。

風力・太陽光発電の平均LCOE(均等化発電原価)および落札価格

風力・太陽光発電のコストは競争により低下

0

50

100

150

200

250

300

350

2008 2010 2012 2014 2016 2018 2020 2022

米ドル(2016)/MWh

陸上風力発電平均落札価格

太陽光発電平均落札価格

洋上風力発電LCOE

大規模太陽光発電LCOE

陸上風力発電 LCOE

5

仮訳

© OECD/IEA 2017

原子力における新リーダー出現

既設炉の運転延長が行われない場合、原発大国の発電量は大幅に減少する一方で、中国が近い将来、業界のリーダーとして米国に取って代わる。

原子力発電所発電量

40

80

120

160

2010年 2020年 2030年 2040年

GW

(ギガワット)

米国

中国

フランス

日本

6

仮訳

© OECD/IEA 2017

クリーンエネルギー技術は、さらなる活用が可能

進展した分野がある一方、多くの技術では、そのポテンシャルを最大限に活かし、持続可能なエネルギー社会を達成するための継続的かつ強力な後押しが必要である。

エネルギー貯蔵

太陽光・陸上風力発電

電気自動車

●不調 ● 更なる改善が必要 ●好調

民生部門のエネルギー効率化(省エネ)輸送用バイオ燃料

二酸化炭素回収・貯留

高効率石炭火力発電

原子力

運輸部門 – 普通乗用車の燃費

照明、家電、業務用機器

産業部門におけるエネルギー効率化(省エネ)

水素・燃料電池

7

仮訳

© OECD/IEA 2017

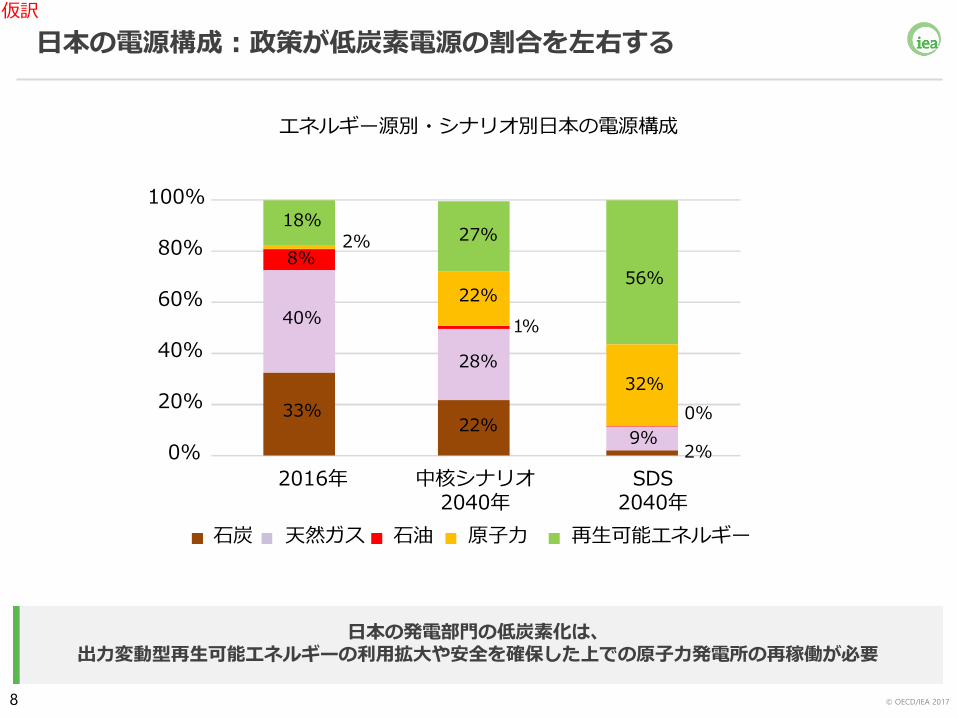

日本の電源構成:政策が低炭素電源の割合を左右する

日本の発電部門の低炭素化は、出力変動型再生可能エネルギーの利用拡大や安全を確保した上での原子力発電所の再稼働が必要

エネルギー源別・シナリオ別日本の電源構成

0%

20%

40%

60%

80%

100%

2016年 中核シナリオ2040年

SDS2040年

石炭 天然ガス 石油 原子力 再生可能エネルギー

33%

40%

8%2%

18%

22%

28%

1%

22%

27%

2%9%

0%

32%

56%

8

仮訳

© OECD/IEA 2017

日本への提言

• エネルギー政策において「あらゆる燃料」、「あらゆる技術」を視野に入れたアプローチを取り入れ、エネルギー安全保障やレジリエンスを向上させる。

• 再エネコストの低下傾向を踏まえた再エネ導入支援策の継続的な調整が必要。また、地域間連系線拡充を含む適切な電力システム柔軟性のあり方の検討が必要。

• 費用最適な二酸化炭素排出削減の実現に向け、エネルギー効率化、再生可能エネルギー、原子力(世界最高の安全基準)など全ての低炭素技術を活用し続ける。

• 世界のエネルギー技術の研究開発・イノベーション分野でリーダーであり続ける。

• デジタル化によるリスクにも対応しつつ、エネルギー産業にもたらされる新たなチャンスを活用する。

• IEAは、各国政府へ最新の技術的助言を提供することでクリーンで安全なエネルギーへの転換を支援できる体制にある。

9

仮訳

© OECD/IEA 2017

www.iea.org

IEA

10

仮訳