Innovation opportunities from a transition to low carbon ...

10

Innovation opportunities from a transition to low carbon prosperity ECO-Innovation Summit March 23, 2010 CONFIDENTIAL AND PROPRIETARY Any use of this material without specific permission of the European Climate Foundation is strictly prohibited

Transcript of Innovation opportunities from a transition to low carbon ...

Innovation opportunities from a

transition to low carbon prosperity ECO-Innovation Summit

March 23, 2010

CONFIDENTIAL AND PROPRIETARY

Any use of this material without specific permission of the European Climate Foundation is strictly prohibited

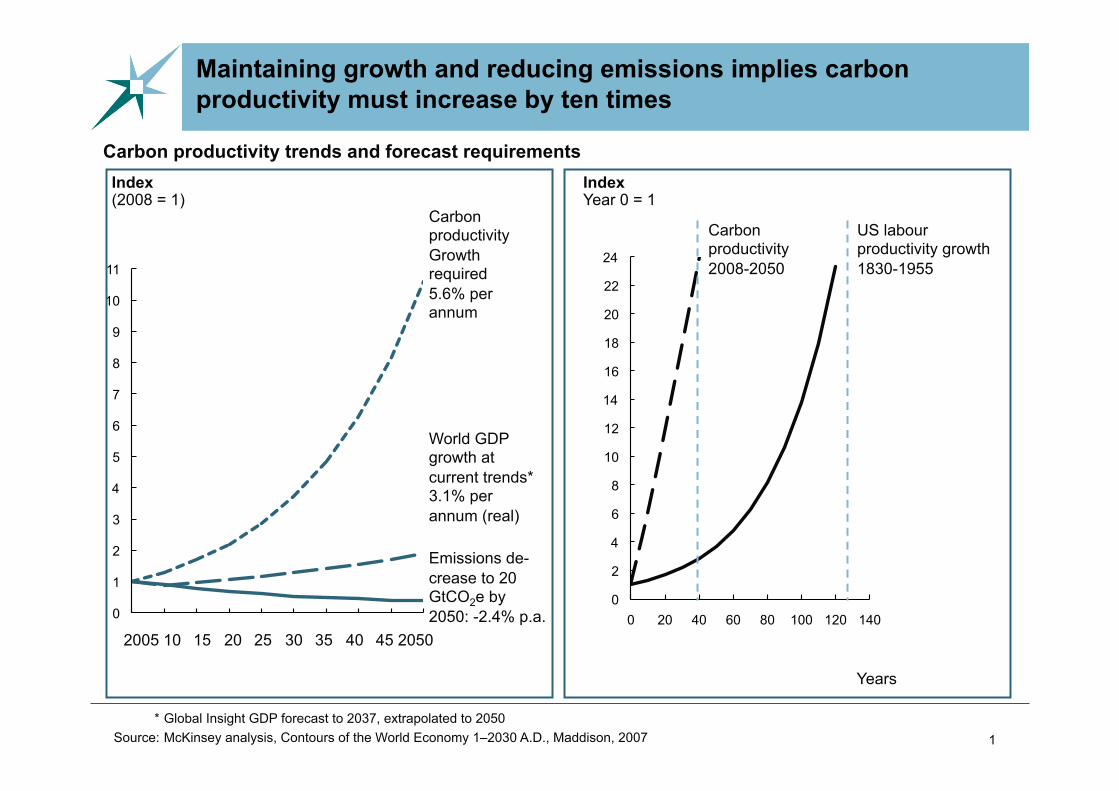

Maintaining growth and reducing emissions implies carbon

productivity must increase by ten times

1

0

1

2

3

4

5

6

7

8

9

10

11

Carbon productivity trends and forecast requirements

Index (2008 = 1)

Carbon productivity

Growth required

5.6% per annum

World GDP growth at

current trends* 3.1% per

annum (real)

Emissions de-

crease to 20 GtCO2e by

2050: -2.4% p.a.

2050 45 40 35 30 25 20 15 10 2005

0

2

4

6

8

10

12

14

16

18

20

22

24

0 20 40 60 80 100 120 140

Index Year 0 = 1

Years

* Global Insight GDP forecast to 2037, extrapolated to 2050

Source: McKinsey analysis, Contours of the World Economy 1–2030 A.D., Maddison, 2007

Carbon productivity

2008-2050

US labour productivity growth

1830-1955

2

EU-27 total GHG emissions GtCO2e/yr

SOURCE: McKinsey Global GHG Abatement Cost Curve; IEA WEO 2009; US EPA; EEA; Team analysis

Sector

Power

Road transport

Industry

Buildings

Agriculture

Waste

Air & sea transport

Forestry

Abatement

95% to 100%

95%

40%

95%

20%

100%

50%

-0.25 GtCO2e

An 80% GHG reduction could be achieved by maximum abatement

within and across sectors

1990

0.4

0.1

0.2

0.1

2050

5.4

0.3

0.3 0.2

1.0

0.9

0.6

0.9

1.0

0.7

0.9

5.2

2010

1.2

1.0

1.2

0.9

1.1

0.5

2030

5.3

0.5

0.1

1.2

0.3

0.9

2050 abated

-0.3

0.6

0.4

5.9

1.2

-80%

The pathways cover a wide range of technology mixes and are

assessed based on set criteria

3

Security of energy supply and technology risk

Economic impact Sustainability

System reliability

Decarbonization pathways

60% RES

20% Nuclear

20% CCS

40% RES1

30% Nuclear

30% CCS

80% RES

10% Nuclear

10% CCS

100% RES

SOURCE: ECF Roadmap 2050

4

80% RES: DSM reduces transmission requirements

with 24%

80% RES, 20% DSM

Iberia

France

UK &

Ireland

Nordel

Benelux &

Germany

Italy &

Malta

South East

Europe

Central Europe

Poland &

Baltic

5GW

7GW 14GW

46GW

3GW

8GW

7GW

10GW

12GW

12GW

4GW

Centre of gravity

SOURCE: ECF Roadmap 2050

Half of the capex is required for wind and solar PV up to 2050 for a

60% RES decarbonized pathway

60% RES PATHWAY Capex by technology by decade, EUR billions

SOURCE: ECF Roadmap 2050

EXAMPLE

0

100

200

300

400

500

600

700

2010-2020 2020-2030 2030-2040 2040-2050

Wind

Solar PV

Other RES

Non RES

396

637 619

545

Grid

investments 19 25 19 9

Key low carbon technologies

6

On- / Offshore wind Solar PV / CSP Automotive power train Energy Efficiency

Super / Smart Grid Biomass & -fuels CCS

To achieve this, the EU is facing large challenges over the next

years

7

•! Drive faster investment in cost-effective measures to reach 20%

end-use efficiency improvement by 2020 and continue efficiency

gains beyond 2020

Energy

Efficiency

Power

Markets

•! Ensure timely retirement of existing high-carbon resources

•! Drive commercialization and deployment of critical low-carbon

technologies

•! Create a durable business case for investment in long-lived, capital-

intensive low-carbon resources needed to meet load growth

Grid

Expansion

•! Timely delivery of the required expansion in inter-regional power

transfer capability

•! Create a business case for appropriate load mgmt/smart grid

investments

SOURCE: ECF Roadmap 2050

Opposing voices Supporting voices

8

Opposing and supporting voices are quoted

“A 30 per cent reduction by 2020 would be physically impossible”, F.

Conti, CEO Enel

“EU must not increase in any way its 20 per cent commitment without a full

global deal “, BusinessEurope

Source: Financial Times, the Economist

“The green revolution has started and by 2020, green technology will have

surpassed the car industry as well as the engineering sector in Germany”, P.

Löscher, CEO Siemens

“[…] we must rely much more on renewable energy, which is clean, safe

and make us more independent”, N. Röettgen, Germany’s environment

minister

“Europe’s competitiveness vs. the US is at risk [with ambitious climate

targets]”, F. Sijbesma, CEO DSM

““Whoever is first to conquer green-tech markets will have an enduring export

advantage and create jobs” Angela Merkel

“““The private sector can and will make GHG reductions” J. vd Veer on behalf

of ERT

9

Incumbents’ voices have traditionally been much louder than

the new industry’s

* Estimate

Source: Burson Marsteller, Guide to Effective Lobbying 2009; European Commission Register of interest representatives

70

7

0 20 40 60 80

Car industry*

European

Federation for

Transport and Environment

Number of lobbyists