2013 SEMA Annual Market Report · 2013 SEMA Annual Market Report 1 Three years of positive results...

83

2013 SEMA Annual Market Report

Transcript of 2013 SEMA Annual Market Report · 2013 SEMA Annual Market Report 1 Three years of positive results...

2013 SEMA AnnualMarket Report

2013 SEMA Annual Market Report

11

Three years of positive results point to a renewed growth trend for the Specialty Equipment Market. Overall, specialty equipment industry sales in 2012 climbed 4% to over $31 billion.

Fueled by a rebirth of the muscle car, street performance products lead the growth of the industry. Models such as the Mustang, Camaro, and Challenger are sparking increased passion for performance products. The Camaro and Mustang were the most commonly displayed cars at the 2012 SEMA Show, indicating the industry’s focus on the new muscle. But, muscle cars aren’t the only ones getting the industry excited, a newcomer, the Scion FR-S, was also one of the most common 2012 SEMA Show booths vehicles.

The truck market continues to rebound, both in terms of new-vehicle sales and specialty equipment sales. Sales of specialty equipment for light trucks grew 1% in 2012 to reverse a declining trend that was set off by the recent recession. New pickup truck sales are up for the third year, climbing 6.4% in 2012. With GM and Ford due to release major redesigns to their flagship pickups in the next couple models years, the truck sector looks like it should continue a slow recovery.

The off-road market continues to be solid, with the Wrangler continuing as one of the most popular booth vehicles at the 2012 SEMA Show. With the Wrangler Unlimited accounting for nearly half of the Jeep vehicles in SEMA Show booths, the industry sees a lot of possibility for the four-door off-road sector.

Industry optimism continues to build. The 2012 SEMA Show brought in a record attendance and the 2013 Show is shaping up to be even bigger. SEMA industry research shows that most companies are reporting sales are up over the last year and they expect growth going forward. More than 40 companies recently attended a new product development conference sponsored by SEMA. And in anticipation of further growth opportunities for members, SEMA is opening a new product development facility, the SEMA Garage – Industry Innovations Center.

Most economic indicators are showing positive signs, resulting in GDP growth and lower unemployment rates. Forecasters are generally predicting moderate, but increasing growth for the US economy over the next few years. While we aren’t returning to the free spending days of the past decade, positive eco-nomic growth combined with the rebound in new-vehicle sales point to continued positive results for the specialty equipment market.

For the first time, the 2013 SEMA Annual Market Report includes sales estimates for a separate product category, Suspension. This gives us the opportunity to track an important industry product group which hasn’t been reported as a separate category previously. In addition, the Q1 2013 SEMA Market Update is integrated into the Annual Market Report to provide additional updates on economic and industry trends.

Think of this report as a starting point for the information that SEMA can provide to help your business. We encourage you to take advantage of its findings as well as all of the research reports available on our website, www.SEMA.org .

As always, if you have any questions or require assistance with the data or information in this report, please let us know.

Gavin Knapp Senior Manager, Market Research

Introduction

2013 SEMA Annual Market Report

22

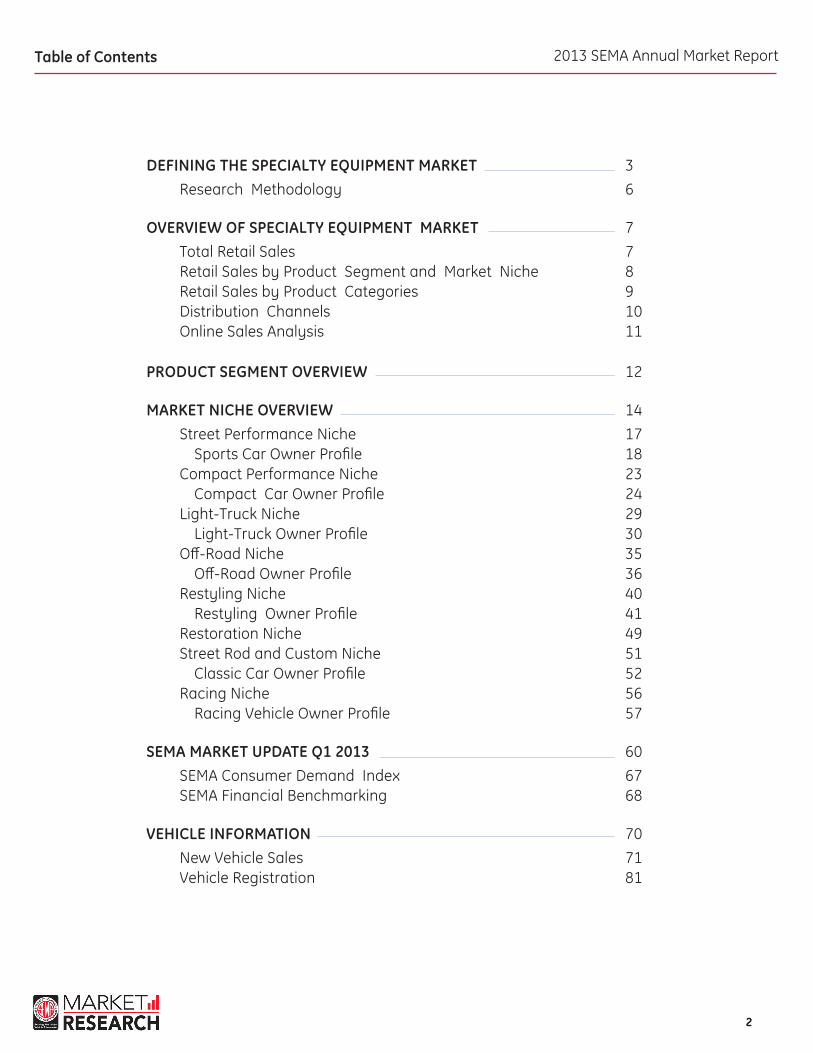

DEFINING THE SPECIALTY EQUIPMENT MARKET 3 Research Methodology 6

OVERVIEW OF SPECIALTY EQUIPMENT MARKET 7 Total Retail Sales 7 Retail Sales by Product Segment and Market Niche 8 Retail Sales by Product Categories 9 Distribution Channels 10 Online Sales Analysis 11

PRODUCT SEGMENT OVERVIEW 12

MARKET NICHE OVERVIEW 14 Street Performance Niche 17 Sports Car Owner Profile 18 Compact Performance Niche 23 Compact Car Owner Profile 24 Light-Truck Niche 29 Light-Truck Owner Profile 30 Off-Road Niche 35 Off-Road Owner Profile 36 Restyling Niche 40 Restyling Owner Profile 41 Restoration Niche 49 Street Rod and Custom Niche 51 Classic Car Owner Profile 52 Racing Niche 56 Racing Vehicle Owner Profile 57 SEMA MARKET UPDATE Q1 2013 60 SEMA Consumer Demand Index 67 SEMA Financial Benchmarking 68

VEHICLE INFORMATION 70 New Vehicle Sales 71 Vehicle Registration 81

Table of Contents

2013 SEMA Annual Market Report

33

Defining the Specialty Equipment Market

DEFINING THE SPECIALTY EQUIPMENT MARKETThe specialty equipment market includes parts and accessories that are manufactured, sold and distributed for cars, light trucks, and other passenger vehicles (motorcycles, ATVs, UTVs, boats, etc.). These products are designed to customize or enhance the performance, handling or appearance of new or used vehicles. The market does not however include direct repair or replacement parts intended to replicate factory specs (except in the case of restoration parts for older vehicles). The specialty equipment market is often described as the parts you want rather than those you need. Some examples of products that fall into the specialty equipment market include exhaust kits, suspension kits, custom wheels, stereo systems and engine modifications to increase horsepower.

Throughout this report, SEMA tracks two broad types of sub-groups within the specialty equipment market: Product Segments and Market Niches.

PRODUCT SEGMENTSSEMA defines three product segments to include everything in the specialty equipment market: accessory and appearance products; performance products; and wheels, tires and suspension. These segments are made up of groups of products that serve similar functions and are generally added for the purpose of comparison.

Accessory and appearance products include interior trim and accessories; restyling and appearance products; specialty waxes and chemicals; graphics and decals; sunroofs; and others. This segment has a broader range and larger number of products than the other latter two segments. These products are often a non-enthusiast’s initial contact with the automotive specialty equipment industry. Many consumers keep coming back and, in the process, escalate their involvement with other industry products along the way.

The second product segment is performance products, which includes internal engine, drivetrain, exhaust system, fuel system and ignition components designed to improve performance through increased durability, capability or dependability. This “go-fast” segment has long been thought of as the heart of the specialty equipment market.

The third product segment in the specialty equipment industry is wheels, tires and suspension. Wheels, tires and suspension components include specialty shocks, struts, lowering packages, lift kits, custom wheels, performance tires and performance brakes. Custom wheels have become the most visible item in this product mix, though suspension upgrades are also common for performance and off-road enthusiasts.

2013 SEMA Annual Market Report

44

SEMA defines eight primary and one miscellaneous market niche, each of which includes the three product segments. Each of these market niches is centered around a vehicle type, how the vehicle is used or the type of components involved in the vehicle use. The three product segments detailed in the previous section are sold and installed in each of the niches.

Four major types of information are combined to determine the size of each of the eight primary specialty equipment markets: product information, vehicle information, distributor/retailer/installer information and parallel research. For some niches, market size is determined by a combination of factors.

For example, defining the light-truck market and off-road market volumes involves determining the nature of the vehicle on which the products are used [truck versus SUV/CUV versus car, etc.] and examining the nature of the product and its design purpose. Such definitions also involve combining information about product volume through particular retailers and distributors as well as specific outlets or installers where the products were purchased. For example, products designed for the trail [even if used on-road] would be allocated to the off-road market.

The nine niches SEMA recognizes are: Street Performance Market Compact Performance Market Light-Truck Market Restyling Market Restoration Market Off-Road Market Street Rod and Custom Market Racing Market Other

MARKET NICHES

Defining the Specialty Equipment Market

2013 SEMA Annual Market Report

55

Light-Truck Market The Light-Truck Market involves all products used to modify the performance, appearance, and/or handling of light trucks (pickups, vans, and sport utilities) for street use. This category excludes products designed specifically for off-road use.

Off-Road Market The Off-Road Market consists of all products used to modify the appearance, performance, and/or handling of light trucks, all-terrain vehicles, and other power units specifically for off-road use.

Street Performance Market The Street Performance Niche includes all products (engine, handling, appearance) used to modify light vehicles for street use that would be considered “performance vehicles”, such as sports cars and muscle cars. This category does not include light trucks or any passenger cars that are not typically designed for performance (i.e. compact cars).

Compact Performance Market The Compact Performance Market includes all products used to modify the performance, handling and appearance of compact size cars for street use.

Racing Market The Racing Market includes all products used in vehicles and power units engaged in all types of off-street, professional and amateur racing and performance competition.

Restoration Market The Restoration Market consists of all products used in returning vehicles to their condition as originally manufactured. There are four primary segments to the vehicle restoration market: antiques prior to 1920s; domestic vehicles 1920 to World War II; domestic vehicles post-World War II; and foreign vehicles.

Restyling Market The Restyling Market comprises all products used to modify vehicles that are not specifically included in other segments of the Specialty Equipment market. Traditionally, this category has focused more on interior and exterior accessories than performance.

Street Rod and Custom Market The Street Rod and Custom Market encompasses all products used in the construction and operation of street rods and customs. Street rods are highly modified vehicles based on body types from 1920 to 1948 for street use and show. Customs are vehicles from 1949 through the late 1960s that are modified in various aspects (particularly appearance) for street use and show.

MARKET NICHE DEFINITIONS

Defining the Specialty Equipment Market

2013 SEMA Annual Market Report

66

RESEARCH METHODOLOGY

The 2013 SEMA Annual Market Report was compiled utilizing a variety of data sources, including interviews with industry sources, consumer surveys, secondary data sources and published government statistics. The main data was provided by:

Lang Marketing Resources: Retail and Manufacturer Sales; Retail Sales Channels Information was gathered on 2012 specialty equipment market volume for retailers, jobbers and warehouse outlets; sales by product segment; and product sales by eight market niches. The data was collected through telephone interviews, mailed questionnaires, Internet questionnaires and parallel research.

SEMA Consumer Segmentation: Vehicle Owner Profiles; Consumer Data The study surveyed 3,000 people across the U.S. who spent more than $100 per year modifying or accessorizing their vehicles. This study represents the buying habits of a large cross-section of specialty equipment buyers. The full SEMA Consumer Segmentation report is available for download from the SEMA website (sema.org/research), but pertinent details from the research were used in preparing this 2013 SEMA Annual Market Report.

Ward’s Auto: New-Vehicle Sales Information was collected from Ward’s online data library at www.wardsauto.com.

Experian: Vehicle Registrations The data collected covered vehicles registered through the 2012 calendar year.

U.S. Census Bureau; Federal Reserve; Bureau of Economic Analysis; U.S. Energy Information Administration: National Economic Trends Data was collected from published government statistics.

Defining the Specialty Equipment Market

2013 SEMA Annual Market Report

77

OVERVIEW OF SPECIALTY EQUIPMENT MARKET

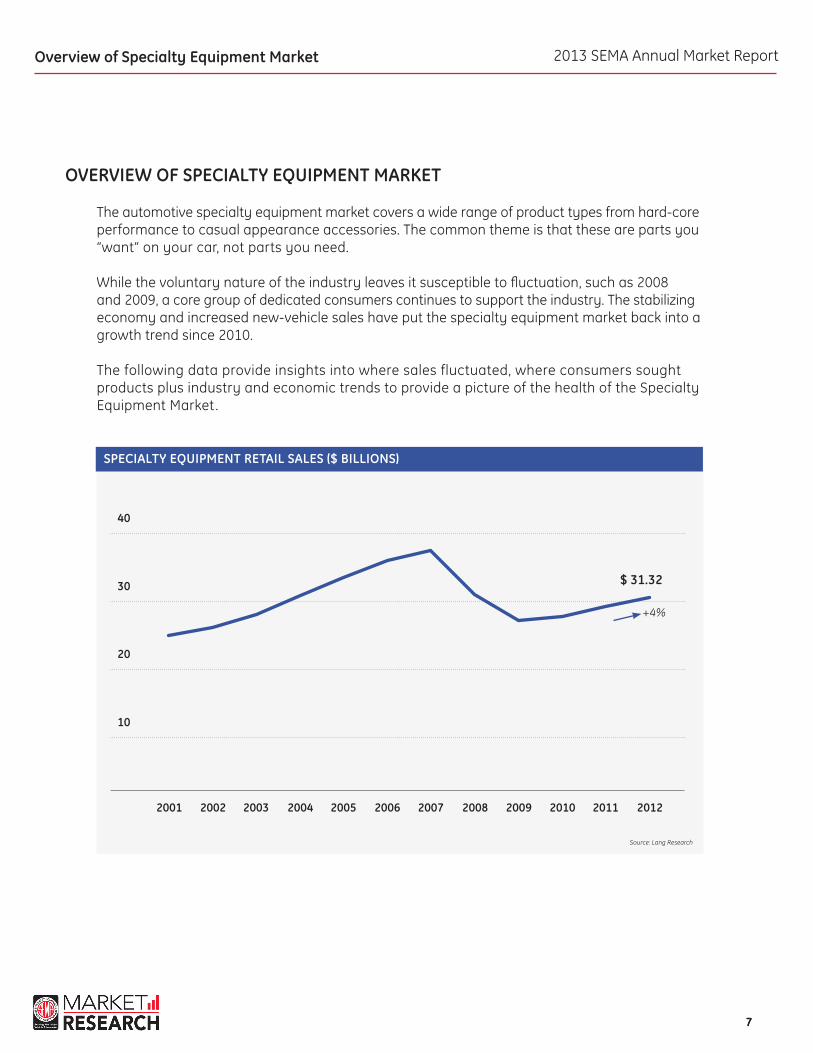

The automotive specialty equipment market covers a wide range of product types from hard-core performance to casual appearance accessories. The common theme is that these are parts you “want” on your car, not parts you need.

While the voluntary nature of the industry leaves it susceptible to fluctuation, such as 2008 and 2009, a core group of dedicated consumers continues to support the industry. The stabilizing economy and increased new-vehicle sales have put the specialty equipment market back into a growth trend since 2010.

The following data provide insights into where sales fluctuated, where consumers sought products plus industry and economic trends to provide a picture of the health of the Specialty Equipment Market .

Overview of Specialty Equipment Market

SPECIALTY EQUIPMENT RETAIL SALES ($ BILLIONS)

2001 2005 20092003 2007 20112002 2006 20102004 2008 2012

40

20

30

10

$ 31.32

+4%

Source: Lang Research

2013 SEMA Annual Market Report

88

Overview of Specialty Equipment Market

2012 RETAIL SALES BY SEGMENT ($ BILLIONS)

2012 RETAIL SALES BY NIChE ($ BILLIONS)

0

0($ BILLIONS)

($ BILLIONS)

5

1

15

3 4 5 6 7 8

10

2

Accessory and Appearance Products

Street Performance

Off-Road

Light-Truck

Racing

$ 8.18

$ 10.61

$ 5.04

$ 4.23

$ 1.20

$ 4.65

$ 1.31

$ 1.46

$ 1.19

$ 12.52

$ 7.47

+5.7%

+2.7%

+3.0%

+5.6%

+5.9%

+1.0%

+2.0%

+5.2%

+5.2%

+4.9%

+15.3%

Percent Change from 2011

Percent Change from 2011

Wheels, Tiresand Suspension

Compact Performance

Restoration

Restyling

Street Rod & Custom

Performance Products

Source: Lang Research

Source: Lang Research

2013 SEMA Annual Market Report

99

Overview of Specialty Equipment Market

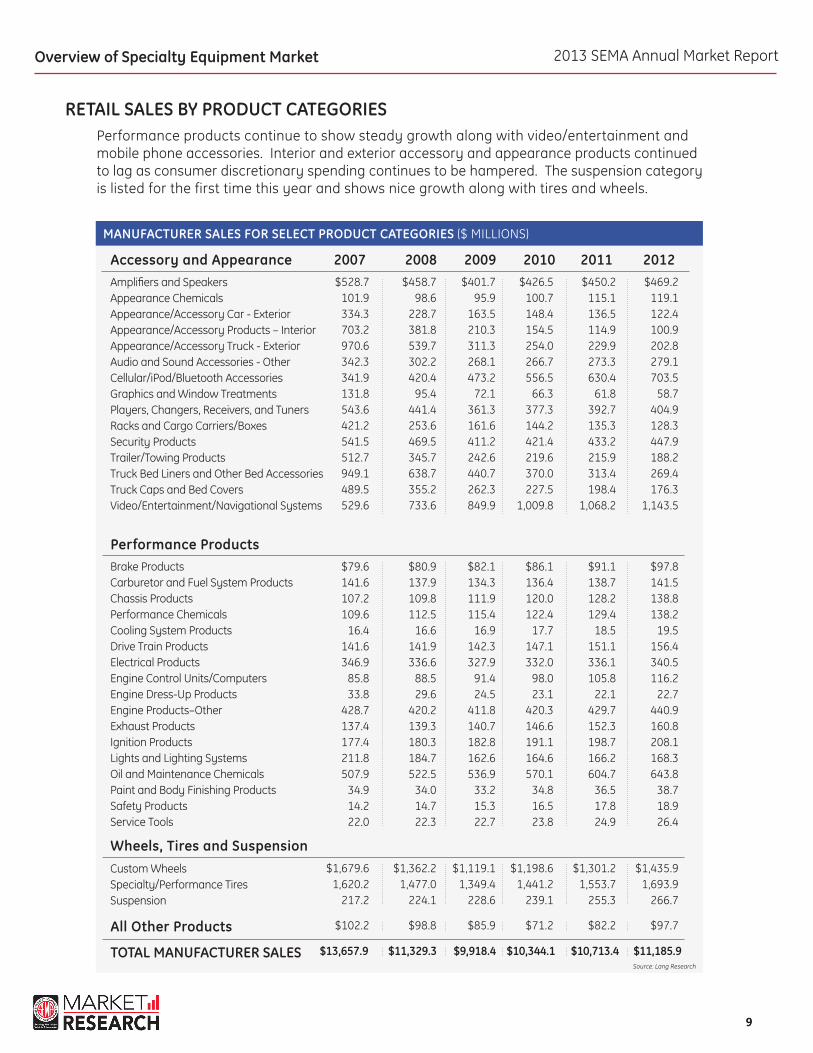

RETAIL SALES BY PRODUCT CATEGORIESPerformance products continue to show steady growth along with video/entertainment and mobile phone accessories. Interior and exterior accessory and appearance products continued to lag as consumer discretionary spending continues to be hampered. The suspension category is listed for the first time this year and shows nice growth along with tires and wheels.

MANUFACTURER SALES FOR SELECT PRODUCT CATEGORIES ($ MILLIONS)

Accessory and Appearance 2007 2008 2009 2010 2011 2012

Performance Products

Wheels, Tires and Suspension

All Other Products

TOTAL MANUFACTURER SALES

Amplifiers and SpeakersAppearance ChemicalsAppearance/Accessory Car - Exterior Appearance/Accessory Products – InteriorAppearance/Accessory Truck - ExteriorAudio and Sound Accessories - OtherCellular/iPod/Bluetooth AccessoriesGraphics and Window TreatmentsPlayers, Changers, Receivers, and TunersRacks and Cargo Carriers/BoxesSecurity ProductsTrailer/Towing ProductsTruck Bed Liners and Other Bed AccessoriesTruck Caps and Bed CoversVideo/Entertainment/Navigational Systems

Brake ProductsCarburetor and Fuel System ProductsChassis ProductsPerformance ChemicalsCooling System ProductsDrive Train ProductsElectrical ProductsEngine Control Units/ComputersEngine Dress-Up ProductsEngine Products–OtherExhaust ProductsIgnition ProductsLights and Lighting SystemsOil and Maintenance ChemicalsPaint and Body Finishing ProductsSafety ProductsService Tools

Custom WheelsSpecialty/Performance TiresSuspension

$528.7 101.9 334.3 703.2 970.6 342.3 341.9 131.8 543.6 421.2 541.5 512.7 949.1 489.5 529.6

$458.7 98.6

228.7 381.8 539.7 302.2 420.4

95.4 441.4 253.6 469.5 345.7 638.7 355.2 733.6

$401.7 95.9

163.5 210.3 311.3 268.1 473.2

72.1 361.3 161.6 411.2 242.6 440.7 262.3 849.9

$426.5 100.7 148.4 154.5 254.0 266.7 556.5

66.3 377.3 144.2 421.4 219.6 370.0 227.5

1,009.8

$450.2 115.1 136.5 114.9 229.9 273.3 630.4

61.8 392.7 135.3 433.2 215.9 313.4 198.4

1,068.2

$469.2119.1122.4100.9202.8279.1703.5

58.7404.9128.3447.9188.2269.4176.3

1,143.5

$79.6 141.6 107.2 109.6

16.4 141.6 346.9

85.8 33.8

428.7 137.4 177.4 211.8 507.9

34.9 14.2 22.0

$80.9 137.9 109.8 112.5

16.6 141.9 336.6

88.5 29.6

420.2 139.3 180.3 184.7 522.5

34.0 14.7 22.3

$82.1 134.3 111.9 115.4

16.9 142.3 327.9

91.4 24.5

411.8 140.7 182.8 162.6 536.9

33.2 15.3 22.7

$86.1136.4 120.0 122.4

17.7 147.1 332.0

98.0 23.1

420.3 146.6 191.1 164.6 570.1

34.8 16.5 23.8

$91.1 138.7 128.2 129.4

18.5 151.1 336.1 105.8

22.1 429.7 152.3 198.7 166.2 604.7

36.5 17.8 24.9

$97.8141.5138.8138.2

19.5156.4340.5116.2

22.7440.9160.8208.1168.3643.8

38.718.926.4

$1,679.6 1,620.2

217.2

$1,362.2 1,477.0

224.1

$1,119.1 1,349.4

228.6

$1,198.6 1,441.2

239.1

$1,301.2 1,553.7

255.3

$1,435.91,693.9

266.7

$102.2 $98.8 $85.9 $71.2 $82.2 $97.7

$13,657.9 $11,329.3 $9,918.4 $10,344.1 $10,713.4 $11,185.9Source: Lang Research

2013 SEMA Annual Market Report

1010

Overview of Specialty Equipment Market

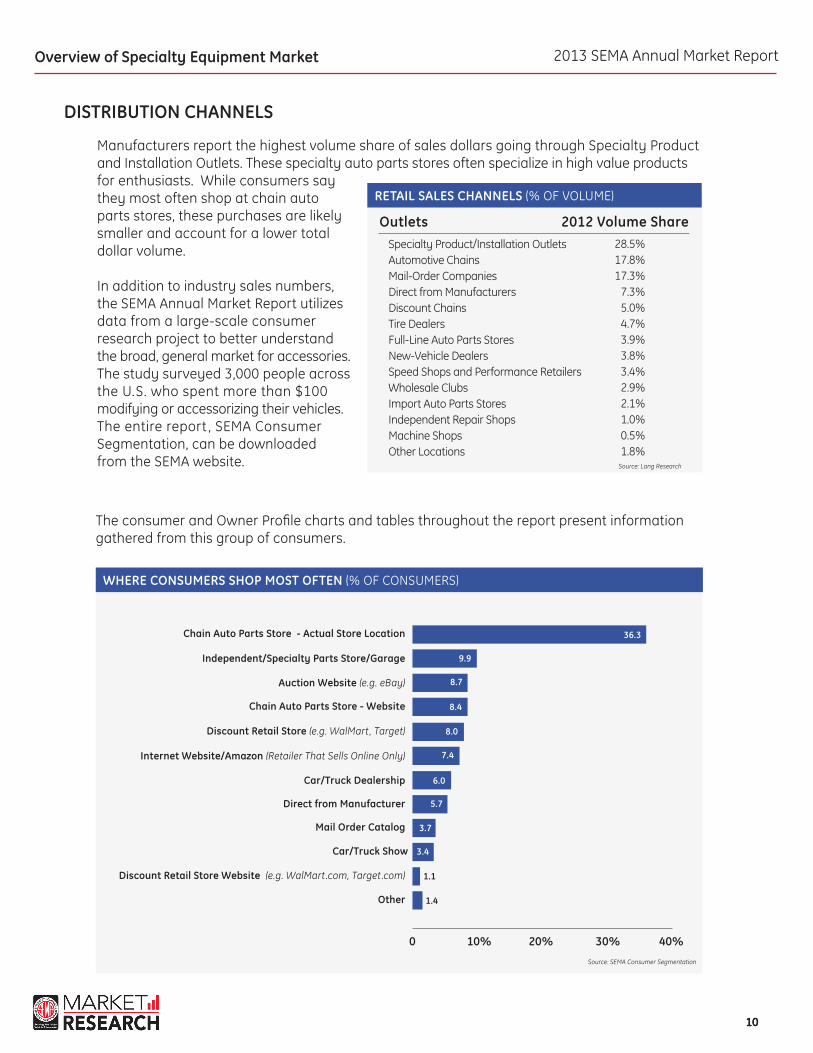

DISTRIBUTION ChANNELS

Manufacturers report the highest volume share of sales dollars going through Specialty Product and Installation Outlets. These specialty auto parts stores often specialize in high value products for enthusiasts. While consumers say they most often shop at chain auto parts stores, these purchases are likely smaller and account for a lower total dollar volume.

In addition to industry sales numbers, the SEMA Annual Market Report utilizes data from a large-scale consumer research project to better understand the broad, general market for accessories. The study surveyed 3,000 people across the U.S. who spent more than $100 modifying or accessorizing their vehicles. The entire report , SEMA Consumer Segmentation, can be downloaded from the SEMA website.

The consumer and Owner Profile charts and tables throughout the report present information gathered from this group of consumers.

RETAIL SALES CHANNELS (% OF VOLUME)

Outlets 2012 Volume ShareSpecialty Product/Installation OutletsAutomotive ChainsMail-Order CompaniesDirect from ManufacturersDiscount ChainsTire DealersFull-Line Auto Parts StoresNew-Vehicle DealersSpeed Shops and Performance RetailersWholesale ClubsImport Auto Parts StoresIndependent Repair ShopsMachine ShopsOther Locations

28.5%17.8%17.3%

7.3%5.0%4.7%3.9%3.8%3.4%2.9%2.1%1.0%0.5%1.8%

Source: Lang Research

Source: SEMA Consumer Segmentation

WHERE CONSUMERS SHOP MOST OFTEN (% OF CONSUMERS)

0 10% 30% 40%20%

Chain Auto Parts Store - Actual Store Location

Discount Retail Store (e.g. WalMart, Target)

Mail Order Catalog

Independent/Specialty Parts Store/Garage

Internet Website/Amazon (Retailer That Sells Online Only)

Car/Truck Show

Auction Website (e.g. eBay)

Car/Truck Dealership

Discount Retail Store Website (e.g. WalMart.com, Target.com)

Chain Auto Parts Store - Website

Direct from Manufacturer

Other

36.3

8.0

3.7

8.7

6.0

1.1

9.9

7.4

3.4

8.4

5.7

1.4

2013 SEMA Annual Market Report

1111

Overview of Specialty Equipment Market

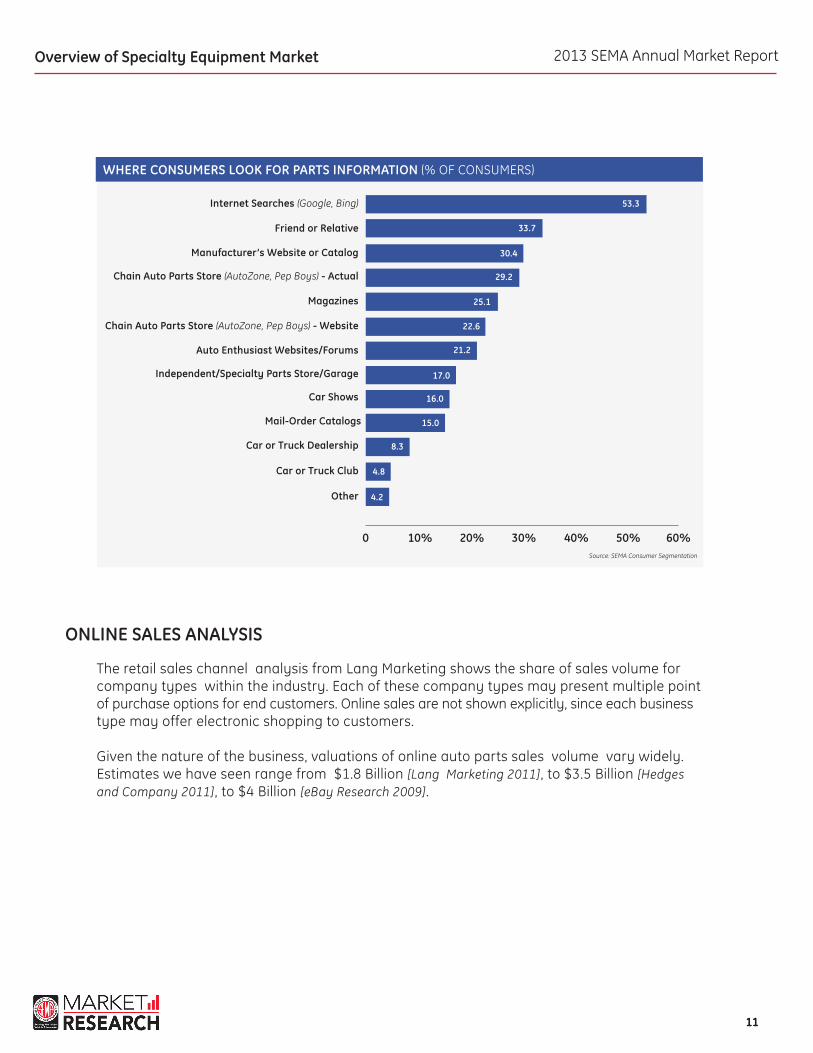

ONLINE SALES ANALYSIS

The retail sales channel analysis from Lang Marketing shows the share of sales volume for company types within the industry. Each of these company types may present multiple point of purchase options for end customers. Online sales are not shown explicitly, since each business type may offer electronic shopping to customers.

Given the nature of the business, valuations of online auto parts sales volume vary widely. Estimates we have seen range from $1.8 Billion [Lang Marketing 2011], to $3.5 Billion [Hedges and Company 2011], to $4 Billion [eBay Research 2009].

Source: SEMA Consumer Segmentation

WHERE CONSUMERS LOOK FOR PARTS INFORMATION (% OF CONSUMERS)

0 10% 30% 40% 50% 60%20%

Internet Searches (Google, Bing)

Magazines

Car Shows

Friend or Relative

Chain Auto Parts Store (AutoZone, Pep Boys) - Website

Mail-Order Catalogs

Manufacturer’s Website or Catalog

Auto Enthusiast Websites/Forums

Car or Truck Dealership

Car or Truck Club

Chain Auto Parts Store (AutoZone, Pep Boys) - Actual

Independent/Specialty Parts Store/Garage

Other

53.3

22.6

15.0

29.2

17.0

4.8

30.4

33.7

21.2

8.3

25.1

16.0

4.2

2013 SEMA Annual Market Report

1212

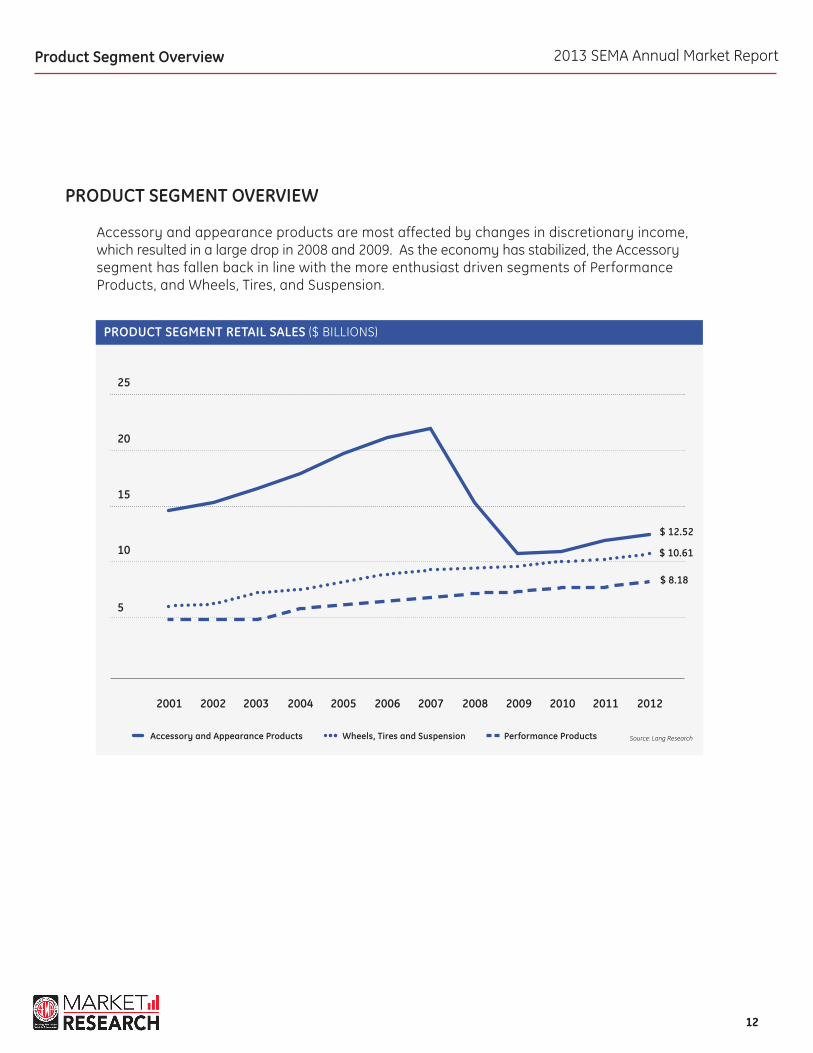

PRODUCT SEGMENT OVERVIEW

Accessory and appearance products are most affected by changes in discretionary income, which resulted in a large drop in 2008 and 2009. As the economy has stabilized, the Accessory segment has fallen back in line with the more enthusiast driven segments of Performance Products, and Wheels, Tires, and Suspension.

Product Segment Overview

PRODUCT SEGMENT RETAIL SALES ($ BILLIONS)

2001 2005 20092003 2007 20112002 2006 20102004 2008 2012

10

15

20

25

5

$ 12.52

$ 10.61

$ 8.18

Source: Lang ResearchWheels, Tires and SuspensionAccessory and Appearance Products Performance Products

2013 SEMA Annual Market Report

1313

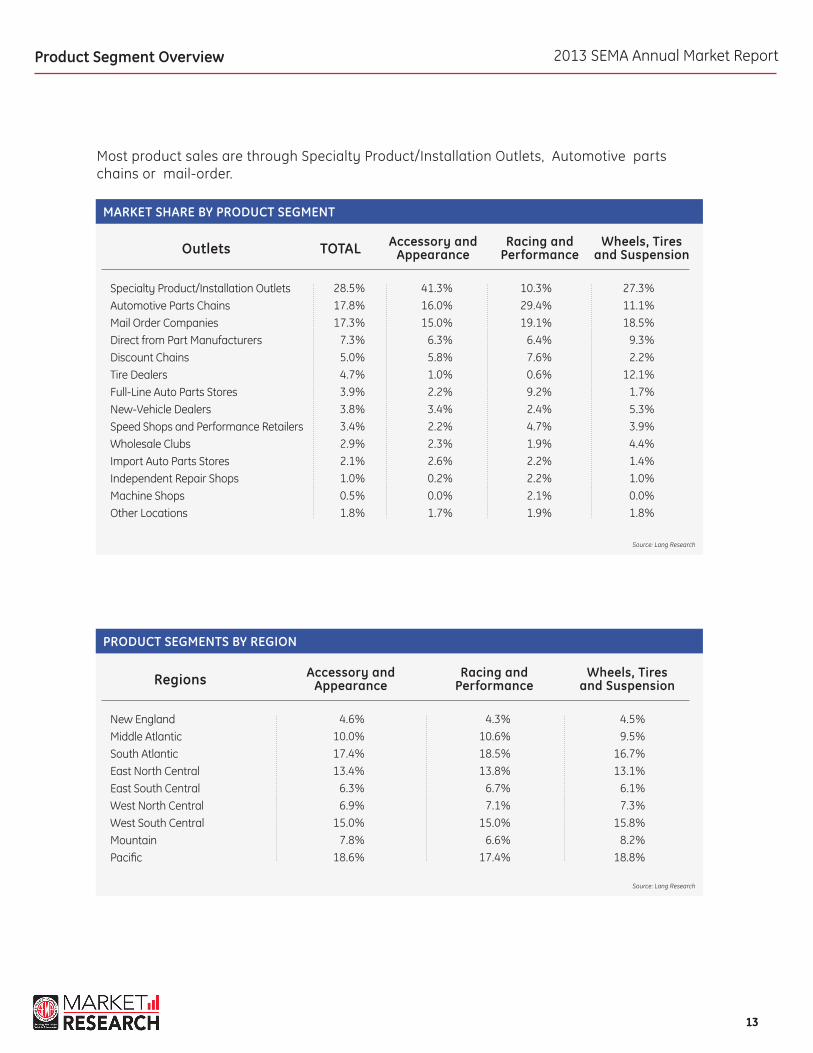

MARkET ShARE BY PRODUCT SEGMENT

PRODUCT SEGMENTS BY REGION

Outlets

Regions

TOTAL Accessory and Appearance

Accessory and Appearance

Racing and Performance

Racing and Performance

Wheels, Tires and Suspension

Wheels, Tires and Suspension

Specialty Product/Installation Outlets Automotive Parts Chains Mail Order Companies Direct from Part Manufacturers Discount Chains Tire Dealers Full-Line Auto Parts Stores New-Vehicle Dealers Speed Shops and Performance Retailers Wholesale Clubs Import Auto Parts Stores Independent Repair Shops Machine Shops Other Locations

New EnglandMiddle AtlanticSouth AtlanticEast North CentralEast South CentralWest North CentralWest South CentralMountainPacific

28.5%17.8%17.3%

7.3%5.0%4.7%3.9%3.8%3.4%2.9%2.1%1.0%0.5%1.8%

4.6%10.0%17.4%13.4%

6.3%6.9%

15.0%7.8%

18.6%

41.3%16.0%15.0%

6.3%5.8%1.0%2.2%3.4%2.2%2.3%2.6%0.2%0.0%1.7%

4.3%10.6%18.5%13.8%

6.7%7.1%

15.0%6.6%

17.4%

10.3%29.4%19.1%

6.4%7.6%0.6%9.2%2.4%4.7%1.9%2.2%2.2%2.1%1.9%

27.3%11.1%18.5%

9.3%2.2%

12.1%1.7%5.3%3.9%4.4%1.4%1.0%0.0%1.8%

4.5%9.5%

16.7%13.1%

6.1%7.3%

15.8%8.2%

18.8%

Product Segment Overview

Most product sales are through Specialty Product/Installation Outlets, Automotive parts chains or mail-order.

Source: Lang Research

Source: Lang Research

2013 SEMA Annual Market Report

1414

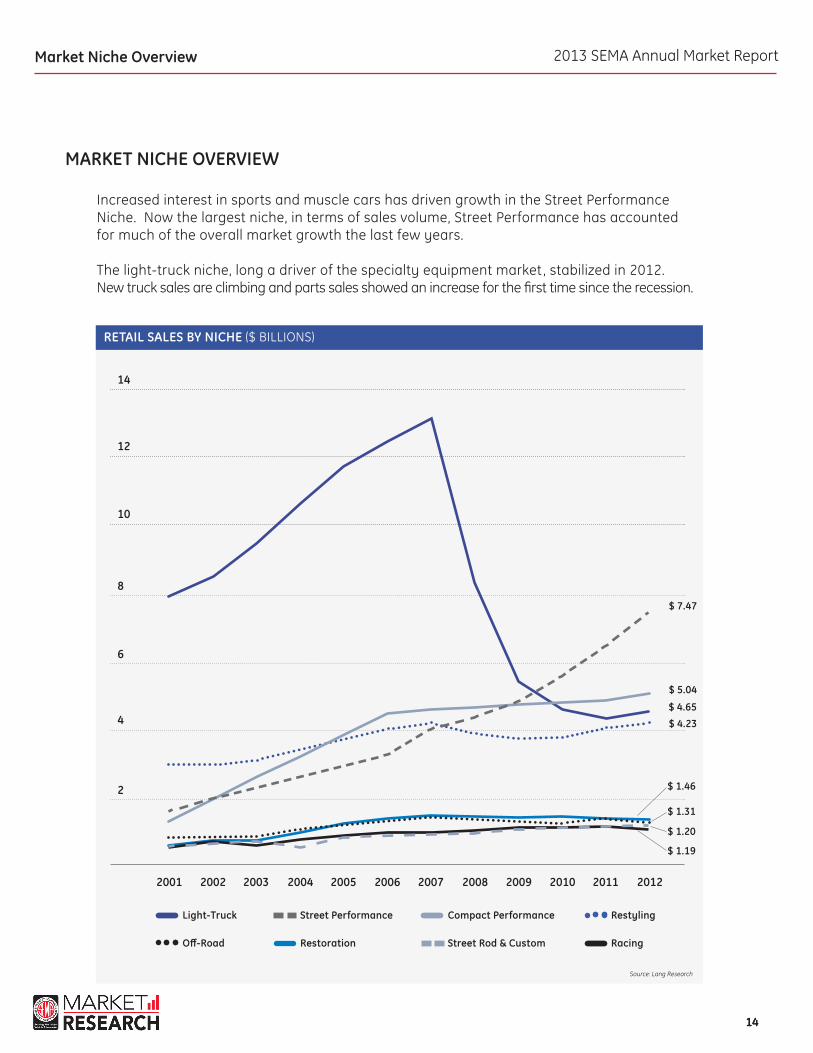

MARKET NICHE OVERVIEW

Increased interest in sports and muscle cars has driven growth in the Street Performance Niche. Now the largest niche, in terms of sales volume, Street Performance has accounted for much of the overall market growth the last few years.

The light-truck niche, long a driver of the specialty equipment market , stabilized in 2012. New truck sales are climbing and parts sales showed an increase for the first time since the recession.

Market Niche Overview

RETAIL SALES BY NIChE ($ BILLIONS)

2001 2005 20092003 2007 20112002 2006 20102004 2008 2012

4

6

8

10

12

14

2

$ 7.47

$ 4.65

$ 5.04

$ 4.23

$ 1.31

Source: Lang Research

Restyling

Off-Road

Light-Truck Compact Performance

Restoration Street Rod & Custom Racing

Street Performance

$ 1.46

$ 1.19

$ 1.20

2013 SEMA Annual Market Report

1515

Specialty Product/ Installation Outlets

Automotive Chains Mail Order CompaniesDirect from Manufacturers Discount Chains Full-Line Auto Parts Stores Tire Dealers Speed Shops & Performance Retailers

New-Vehicle Dealers Wholesale Clubs Import Auto Parts Stores Independent Repair Shops Machine Shops Other Locations

SALES ChANNELS BY NIChE (%)

RacingStreet Performance

Compact Performance

Light- Truck Off-Road Restyling Restoration Street Rod

& Custom

25.9%

19.4%17.7%

7.1%5.4%4.8%4.2%3.7%

3.5%2.9%1.8%1.4%0.4%1.8%

29.3%

16.9%17.2%

6.8%4.0%4.2%3.9%3.4%

5.8%1.8%3.3%1.2%0.4%1.8%

29.0%

17.8%16.5%

7.7%4.7%3.4%5.4%3.3%

4.1%3.4%1.7%1.1%0.2%1.7%

28.4%

15.5%17.7%

8.1%4.2%3.2%6.4%3.5%

4.3%3.6%1.6%1.2%0.4%1.9%

33.4%

17.0%16.6%

6.8%5.7%3.3%3.2%3.2%

3.5%3.1%1.9%0.7%0.2%1.4%

28.6%

17.7%17.3%

7.4%5.3%4.1%4.5%3.4%

3.6%3.0%1.8%1.2%0.6%1.5%

23.4%

15.5%18.3%

9.4%5.6%5.7%4.3%4.0%

3.3%2.8%2.0%1.6%2.6%1.5%

25.0%

19.4%17.8%

7.3%5.4%4.7%4.4%3.5%

3.8%3.0%1.7%1.4%0.8%1.8%

Market Niche Overview

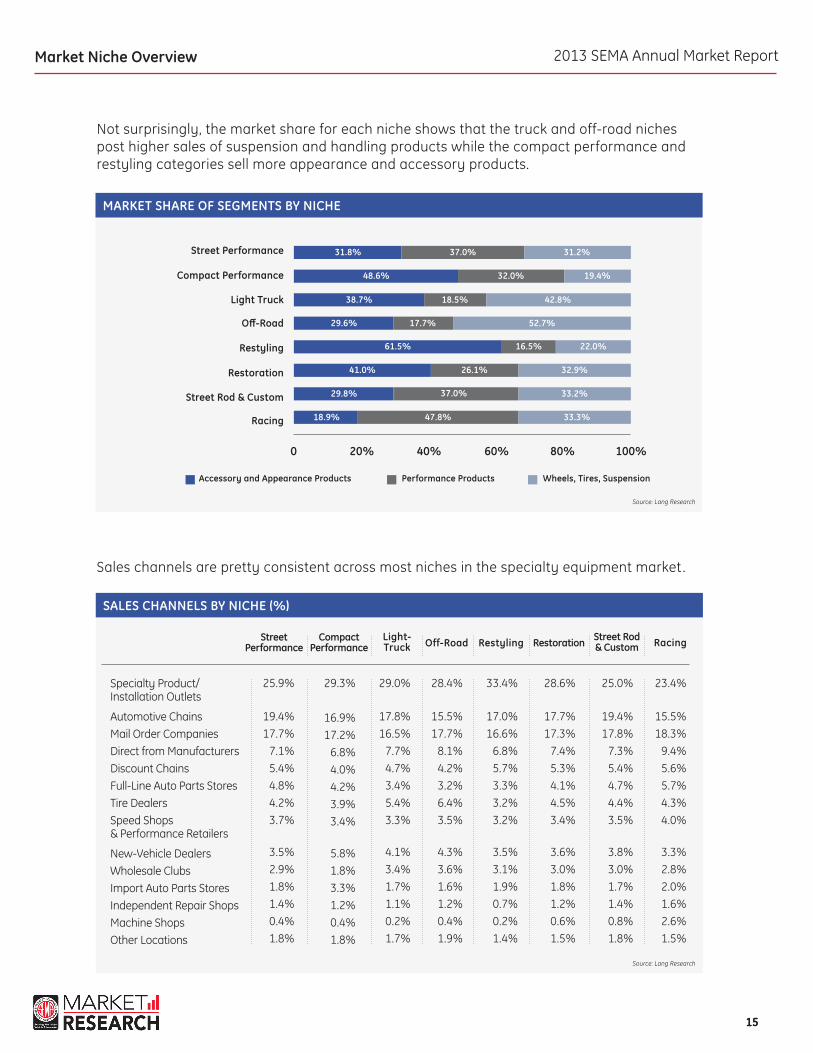

Not surprisingly, the market share for each niche shows that the truck and off-road niches post higher sales of suspension and handling products while the compact performance and restyling categories sell more appearance and accessory products.

Sales channels are pretty consistent across most niches in the specialty equipment market .

Source: Lang Research

Source: Lang Research

MARkET ShARE OF SEGMENTS BY NIChE

0 20% 60% 80% 100%40%

Street Performance

Restyling

Compact Performance

Restoration

Light Truck

Street Rod & Custom

Off-Road

Racing

31.8%

48.6%

38.7%

29.6%

61.5%

41.0%

29.8%

18.9%

37.0%

32.0%

18.5%

17.7%

16.5%

26.1%

37.0%

47.8%

31.2%

19.4%

42.8%

52.7%

22.0%

32.9%

33.2%

33.3%

Performance Products Wheels, Tires, SuspensionAccessory and Appearance Products

2013 SEMA Annual Market Report

1616

Sports car and classic car owners showed a higher propensity to perform engine, chassis and intake/ exhaust modifications than some of the other niche enthusiasts. Passenger car owners [midsize, fullsize, and luxury] were less likely to perform such “hard parts” modifications but were interested in performing interior and electrical modifications and in using chemical products.

TYPES OF MODIFICATIONS (% OF OWNERS)

Luxury Sports Car

Pickup Truck

Midsize Car

Street Performance

Restyling

Light-Truck

Compact Performance

Street Rod & Custom, Restoration

Sports Car

SUV/CUV

Large/ Fullsize Car

Small/Compact Vehicle

Van/Mini Van

Luxury Car Classic/Pre-1973

EngineChassisIntake/Fuel/ExhaustElectrical (e.g. Audio, alarm, GPS)Drivetrain (e.g. Clutch, shifter, transmission)Chemicals (e.g. Fluids, cleaners)Lighting (e.g. Exterior/Interior)Interior (e.g. Mats, safety gear) Exterior (e.g. Decals, paint, racks, truck shell, hitch) Other

EngineChassisIntake/Fuel/ExhaustElectrical (e.g. Audio, alarm, GPS)Drivetrain (e.g. Clutch, shifter, transmission)Chemicals (e.g. Fluids, cleaners)Lighting (e.g. Exterior/Interior)Interior (e.g. Mats, safety gear) Exterior (e.g. Decals, paint, racks, truck shell, hitch) Other

EngineChassisIntake/Fuel/ExhaustElectrical (e.g. Audio, alarm, GPS)Drivetrain (e.g. Clutch, shifter, transmission)Chemicals (e.g. Fluids, cleaners)Lighting (e.g. Exterior/Interior)Interior (e.g. Mats, safety gear) Exterior (e.g. Decals, paint, racks, truck shell, hitch) Other

41.9%38.1%45.6%56.9%22.5%40.0%49.4%50.6%38.8%

4.4%

24.7%29.0%35.5%33.4%11.6%44.0%22.8%46.3%57.5%

8.3%

20.3%22.6%26.6%40.3%10.5%46.1%26.1%46.6%32.4%

8.4%

43.0%40.8%51.5%41.3%25.0%42.5%31.3%51.8%42.5%

6.5%

17.8%23.6%26.8%42.3%

7.5%45.7%27.5%47.7%43.8%

9.0%

33.3%39.8%34.9%40.9%15.6%48.9%32.8%39.8%36.6%

8.6%

23.0%26.3%32.6%42.9%15.8%39.5%30.3%48.7%35.3%

6.9%

23.2%16.8%22.4%32.8%11.2%42.4%25.6%44.0%30.4%14.4%

28.5%29.5%29.5%44.4%15.0%39.1%28.5%48.8%37.7%

5.8%

60.2%55.6%61.7%39.3%36.7%42.9%27.6%50.0%42.3%

6.6%

Source: Lang Research

Market Niche Overview

2013 SEMA Annual Market Report

1717

STREET PERFORMANCE NICHE

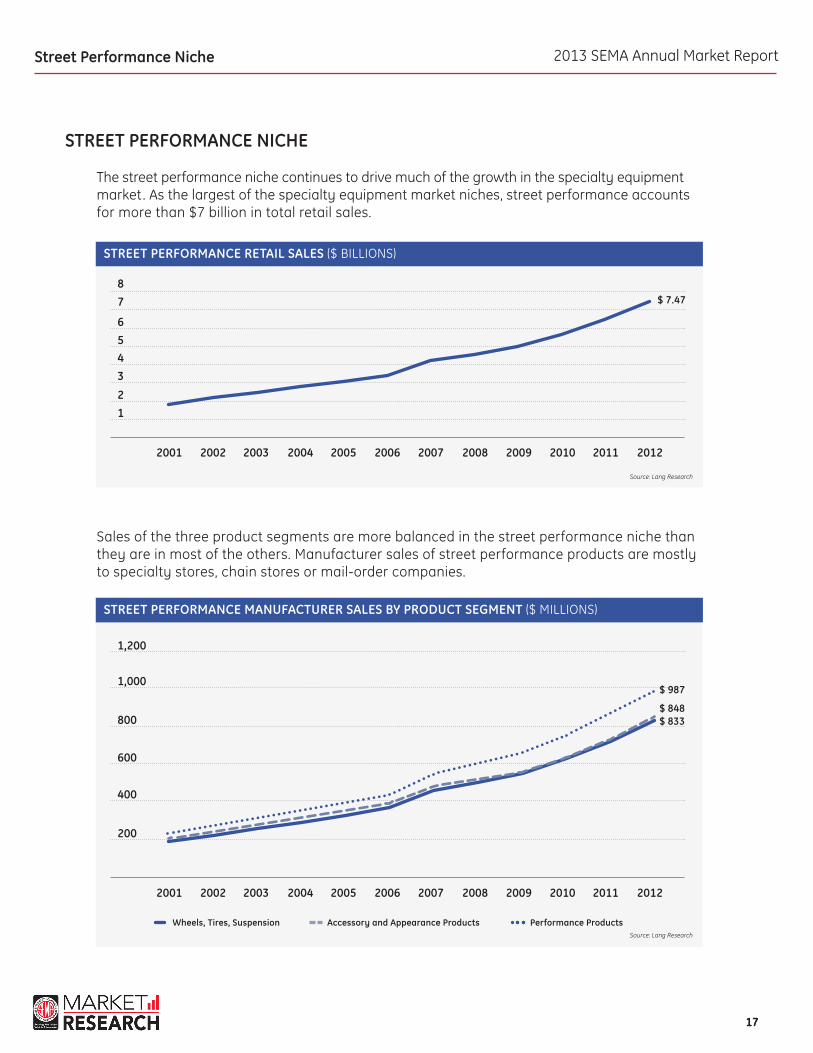

The street performance niche continues to drive much of the growth in the specialty equipment market. As the largest of the specialty equipment market niches, street performance accounts for more than $7 billion in total retail sales.

Sales of the three product segments are more balanced in the street performance niche than they are in most of the others. Manufacturer sales of street performance products are mostly to specialty stores, chain stores or mail-order companies.

Street Performance Niche

STREET PERFORMANCE RETAIL SALES ($ BILLIONS)

STREET PERFORMANCE MANUFACTURER SALES BY PRODUCT SEGMENT ($ MILLIONS)

2001

2001

2005

2005

2009

2009

2003

2003

2007

2007

2011

2011

2002

2002

2006

2006

2010

2010

2004

2004

2008

2008

2012

2012

2

4

6

8

1

200

400

600

800

1,000

1,200

3

5

7 $ 7.47

$ 833$ 848

$ 987

Source: Lang Research

Source: Lang Research

Performance ProductsWheels, Tires, Suspension Accessory and Appearance Products

2013 SEMA Annual Market Report

1818

SPORTS CAR OWNER PROFILE

The profile of the street performance consumer was comprised of data on the owners of sports cars and luxury sports cars. Among those owners, nearly one-third use auto-enthusiast websites and forums as a primary source for information on specialty equipment parts.

STREET PERFORMANCE SALES CHANNEL (% OF VOLUME)

Specialty Product/Installation Outlets Automotive Chains Mail-Order CompaniesDirect from Manufacturers Discount Chains Full-Line Auto Parts Stores Tire Dealers Speed Shops and Performance RetailersNew-Vehicle Dealers Wholesale Clubs Import Auto Parts Stores Independent Repair Shops Machine Shops Other Locations

25.9%19.4%17.7%

7.1%5.4%4.8%4.2%3.7%3.5%2.9%1.8%1.4%0.4%1.8%

Source: Lang Research

Source: SEMA Consumer Segmentation

SPORTS CAR - SOURCES OF INFORMATION (% OF OWNERS)

0 10% 30% 40% 50% 60%20%

Magazines

Chain Parts Stores (e.g. AutoZone, Pep Boys) - Actual Store

Manufacturer’s Website or Catalog

Car or Truck Club

Auto Enthusiasts Websites/Forums

Chain Parts Stores (e.g. AutoZone, Pep Boys) - Website

Car or Truck Dealership

Friend or Relative

Mail Order Catalogs

Other

Car Shows

Internet Searches (e.g. Google, Bing)

Independent/Specialty Parts Store/Garage

32.9

23.9

35.0

8.6

28.8

20.0

32.0

22.3

7.7

5.2

27.1

48.9

19.6

Street Performance Niche

2013 SEMA Annual Market Report

1919

Source: SEMA Consumer Segmentation

Source: SEMA Consumer Segmentation

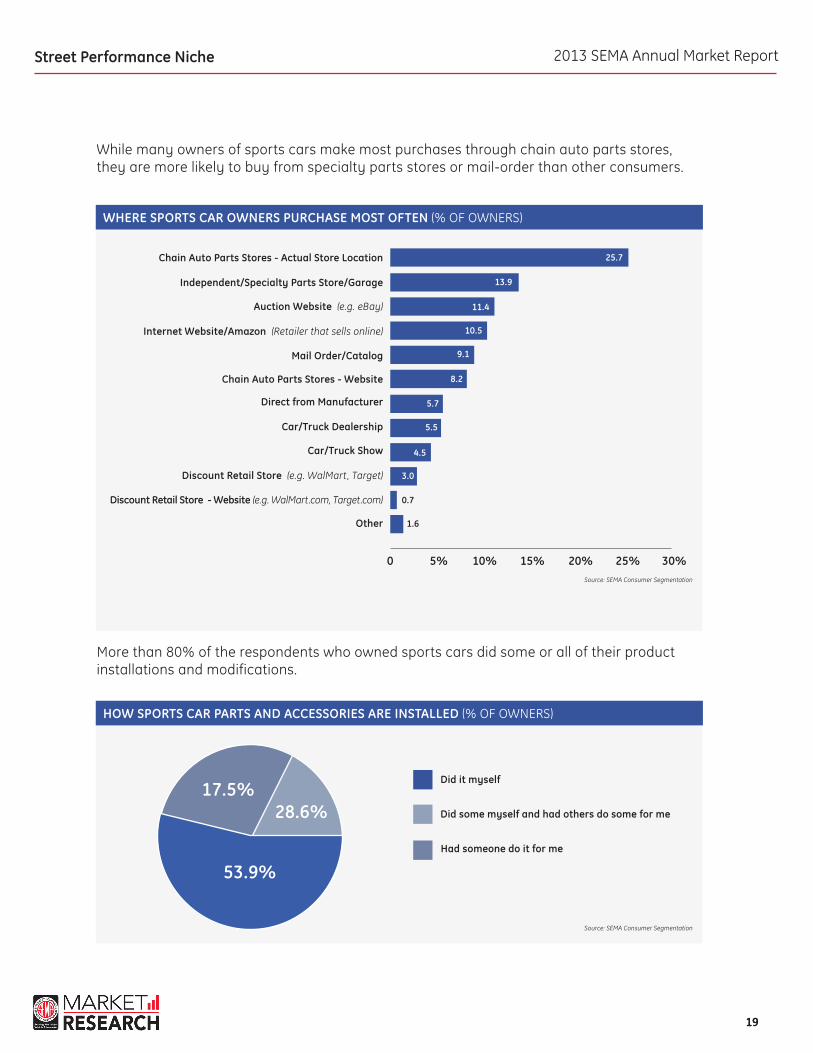

WHERE SPORTS CAR OWNERS PURCHASE MOST OFTEN (% OF OWNERS)

HOW SPORTS CAR PARTS AND ACCESSORIES ARE INSTALLED (% OF OWNERS)

0 5% 15% 20% 25% 30%10%

Auction Website (e.g. eBay)

Car/Truck Show

Independent/Specialty Parts Store/Garage

Car/Truck Dealership

Internet Website/Amazon (Retailer that sells online)

Discount Retail Store (e.g. WalMart, Target)

Mail Order/Catalog

Discount Retail Store - Website (e.g. WalMart.com, Target.com)

Chain Auto Parts Stores - Website

Other

Chain Auto Parts Stores - Actual Store Location

Direct from Manufacturer

Street Performance Niche

While many owners of sports cars make most purchases through chain auto parts stores, they are more likely to buy from specialty parts stores or mail-order than other consumers.

More than 80% of the respondents who owned sports cars did some or all of their product installations and modifications.

11.4

5.7

13.9

0.7

9.1

4.5

10.5

5.5

1.6

8.2

25.7

3.0

17.5%28.6%

53.9%

Did some myself and had others do some for me

Did it myself

had someone do it for me

2013 SEMA Annual Market Report

2020

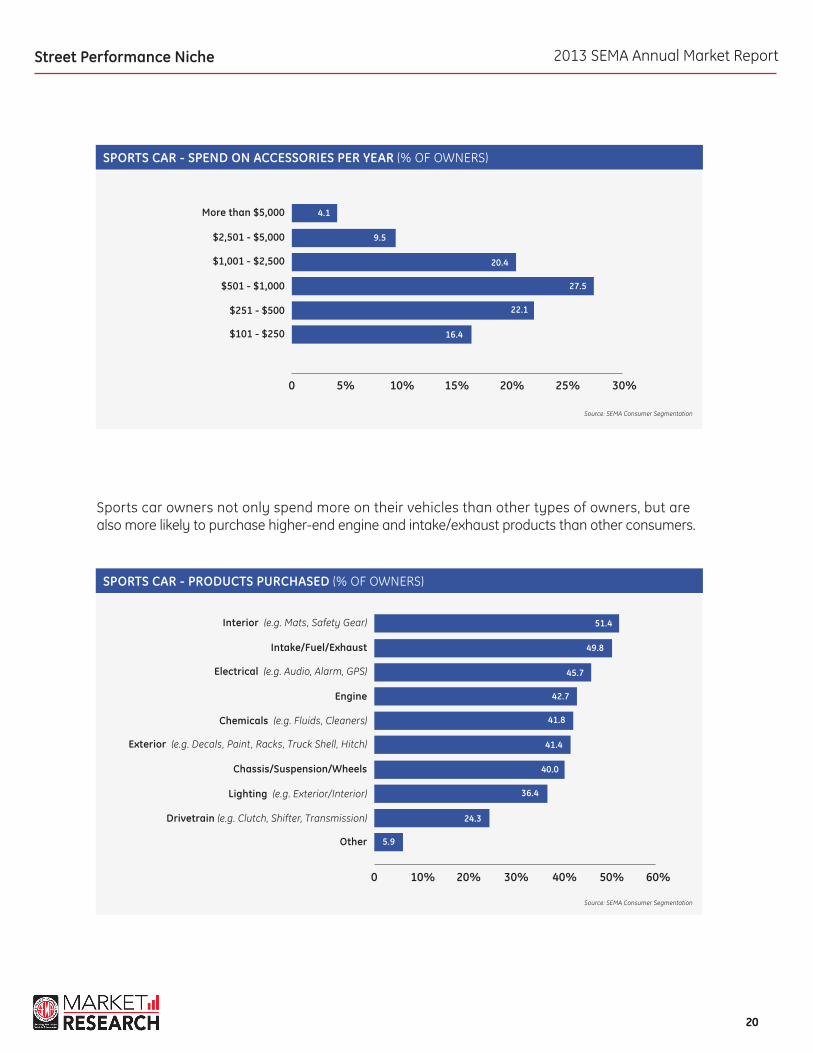

SPORTS CAR - SPEND ON ACCESSORIES PER YEAR (% OF OWNERS)

0 5% 15% 20% 25% 30%10%

$1,001 - $2,500

$2,501 - $5,000

$501 - $1,000

$251 - $500

$101 - $250

More than $5,000

20.4

9.5

22.1

27.5

16.4

4.1

Street Performance Niche

Sports car owners not only spend more on their vehicles than other types of owners, but are also more likely to purchase higher-end engine and intake/exhaust products than other consumers.

Source: SEMA Consumer Segmentation

Source: SEMA Consumer Segmentation

SPORTS CAR - PRODUCTS PURChASED (% OF OWNERS)

0 10% 30% 40% 50% 60%20%

Electrical (e.g. Audio, Alarm, GPS)

Chassis/Suspension/Wheels

Intake/Fuel/Exhaust

Engine

Lighting (e.g. Exterior/Interior)

Chemicals (e.g. Fluids, Cleaners)

Drivetrain (e.g. Clutch, Shifter, Transmission)

Exterior (e.g. Decals, Paint, Racks, Truck Shell, Hitch)

Interior (e.g. Mats, Safety Gear)

Other

45.7

40.0

49.8

41.8

24.3

42.7

36.4

41.4

51.4

5.9

2013 SEMA Annual Market Report

2121

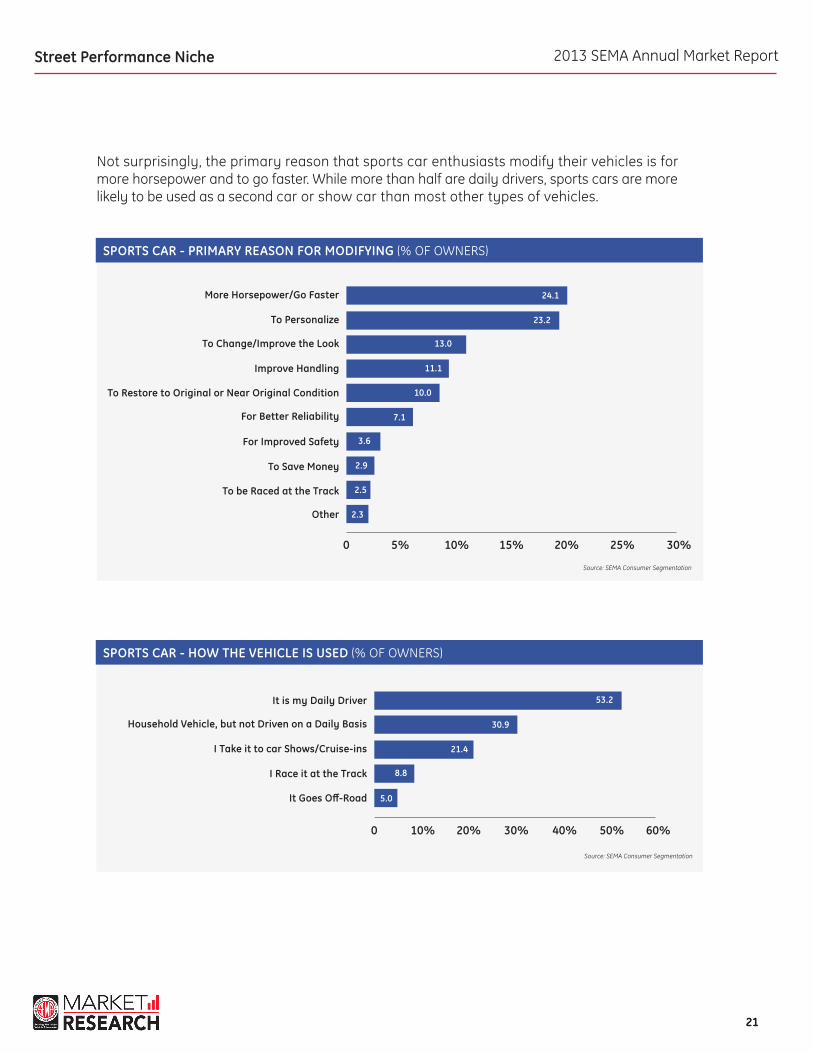

SPORTS CAR - PRIMARY REASON FOR MODIFYING (% OF OWNERS)

0 5% 15% 20% 25% 30%10%

To Change/Improve the Look

For Improved Safety

To Personalize

Improve handling

To Save Money

To Restore to Original or Near Original Condition

To be Raced at the Track

For Better Reliability

Other

More horsepower/Go Faster

23.2

7.1

11.1

2.9

2.3

24.1

10.0

13.0

3.6

2.5

Street Performance Niche

Not surprisingly, the primary reason that sports car enthusiasts modify their vehicles is for more horsepower and to go faster. While more than half are daily drivers, sports cars are more likely to be used as a second car or show car than most other types of vehicles.

Source: SEMA Consumer Segmentation

Source: SEMA Consumer Segmentation

SPORTS CAR - hOW ThE VEhICLE IS USED (% OF OWNERS)

0 10% 30% 40% 50% 60%20%

I Take it to car Shows/Cruise-ins

I Race it at the Track

It is my Daily Driver

It Goes Off-Road

household Vehicle, but not Driven on a Daily Basis

21.4

53.2

5.0

8.8

30.9

2013 SEMA Annual Market Report

2222

Acura TLAcura TSXAudi A4Audi A5BMW 3-SeriesBMW 5-SeriesBMW 7-SeriesChevrolet CamaroChevrolet CorvetteDodge ChallengerDodge ChargerDodge DartFord MustangHyundai GenesisInfiniti GInfiniti MMercedes SLMercedes SLKMitsubishi LancerNissan 370ZPorsche 911Scion FR-SSubaru LegacyVolkswagen GTI

ExAMPLES OF CURRENT STREET PERFORMANCE VEHICLE SALES

2008 2009 2010 2011 2012

46,76631,99843,344

6,282112,464

45,91512,276

--26,97117,42397,367

--91,251

6,16764,18115,618

5,4644,941

27,861--

8,324--

22,61412,232

33,62028,65037,070

9,80090,96040,109

9,25461,64813,93425,85260,651

--66,62321,88947,174

8,5014,0252,566

20,1179,2426,839

--30,974

7,932

34,04932,07634,67216,379

100,91039,48812,25381,29912,62436,79175,397

--73,71629,12258,14314,618

2,3851,980

21,41610,215

5,737--

38,72513,755

31,23730,93535,23415,38594,37151,49111,29988,24913,16439,53470,089

--70,43832,99858,24610,818

1,4493,220

19,8747,3286,016

--42,40116,867

33,57228,86535,41517,27099,60256,79811,09884,39114,13243,11982,59225,30382,99533,97359,844

9,1304,8994,595

16,4267,3388,528

11,41747,12716,314

Sources: Ward’s Auto, SEMA

STREET PERFORMANCE VEHICLE SALES

SEMA SHOW STREET PERFORMANCE VEHICLE DATAMost of the top models displayed at the 2011 SEMA Show remained in the top five in 2012. The Scion FR-S displaced the Dodge Charger from the top five positions and was the third most displayed model among the street performance cars.

Sports cars and muscle cars are the top-selling vehicles that are considered part of the street performance niche. Note also that this study places all sports cars—foreign and domestic— in this niche rather than in compact performance.

SEMA ShOW VEhICLES—STREET PERFORMANCE

2010 2011 2012

Ford MustangChevy CamaroDodge ChallengerChevy CorvetteDodge Charger

Chevy CamaroFord MustangDodge ChallengerChevy CorvetteDodge Charger

Ford MustangChevrolet CamaroScion FR-SChevrolet CorvetteChallenger, BMW 3-series,Porsche 911, Genesis

177135

454012

11699352622

7473532214

Source: SEMA

TOP 5 MODELS

Note: The method of counting SEMA Show display vehicles changed between years.

Street Performance Niche

2013 SEMA Annual Market Report

2323

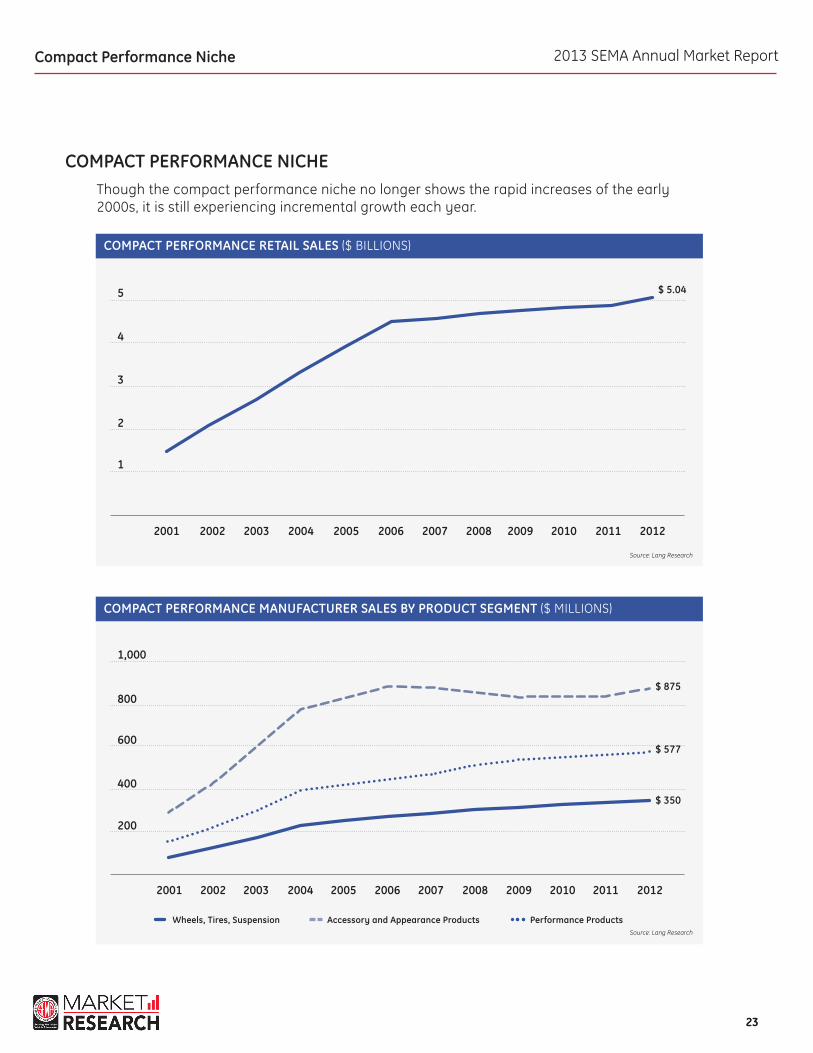

COMPACT PERFORMANCE NICHEThough the compact performance niche no longer shows the rapid increases of the early 2000s, it is still experiencing incremental growth each year.

Compact Performance Niche

COMPACT PERFORMANCE RETAIL SALES ($ BILLIONS)

COMPACT PERFORMANCE MANUFACTURER SALES BY PRODUCT SEGMENT ($ MILLIONS)

2001

2004

2005

20092008

2009

2002

2003

2006

2007

2011

2011

2001

2002

2005

2006

2010

2010

2003

2004

2007

2008

2012

2012

2

4

1

200

400

600

800

1,000

3

5 $ 5.04

$ 350

$ 577

$ 875

Source: Lang Research

Source: Lang Research

Performance ProductsWheels, Tires, Suspension Accessory and Appearance Products

2013 SEMA Annual Market Report

2424

COMPACT CAR OWNER PROFILE

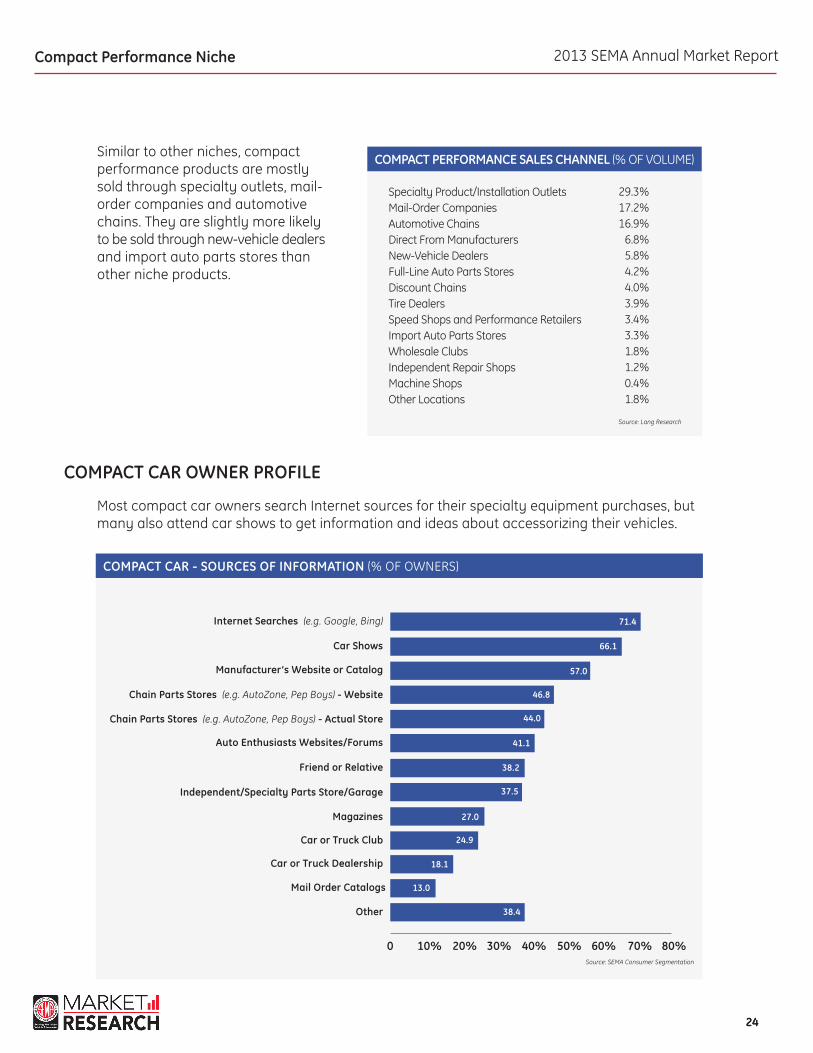

Most compact car owners search Internet sources for their specialty equipment purchases, but many also attend car shows to get information and ideas about accessorizing their vehicles.

Similar to other niches, compact performance products are mostly sold through specialty outlets, mail-order companies and automotive chains. They are slightly more likely to be sold through new-vehicle dealers and import auto parts stores than other niche products.

COMPACT PERFORMANCE SALES CHANNEL (% OF VOLUME)

Specialty Product/Installation Outlets Mail-Order CompaniesAutomotive Chains Direct From Manufacturers New-Vehicle Dealers Full-Line Auto Parts Stores Discount Chains Tire Dealers Speed Shops and Performance RetailersImport Auto Parts Stores Wholesale Clubs Independent Repair Shops Machine Shops Other Locations

29.3%17.2%16.9%

6.8%5.8%4.2%4.0%3.9%3.4%3.3%1.8%1.2%0.4%1.8%

Source: Lang Research

Source: SEMA Consumer Segmentation

COMPACT CAR - SOURCES OF INFORMATION (% OF OWNERS)

0 10% 30% 40% 50% 60% 70% 80%20%

Manufacturer’s Website or Catalog

Friend or Relative

Car Shows

Car or Truck Dealership

Chain Parts Stores (e.g. AutoZone, Pep Boys) - Website

Independent/Specialty Parts Store/Garage

Mail Order Catalogs

Chain Parts Stores (e.g. AutoZone, Pep Boys) - Actual Store

Magazines

Other

Auto Enthusiasts Websites/Forums

Internet Searches (e.g. Google, Bing)

Car or Truck Club

57.0

38.2

66.1

18.1

44.0

27.0

46.8

37.5

13.0

38.4

41.1

71.4

24.9

Compact Performance Niche

2013 SEMA Annual Market Report

2525

Source: SEMA Consumer Segmentation

Source: SEMA Consumer Segmentation

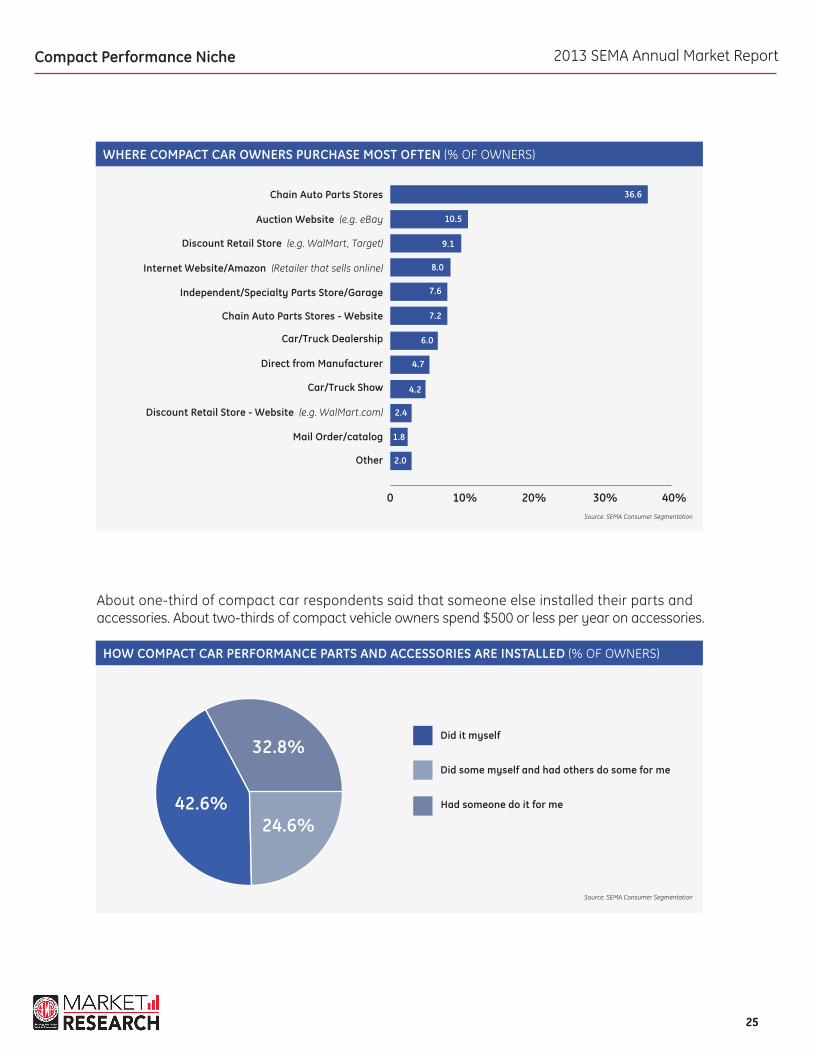

WHERE COMPACT CAR OWNERS PURCHASE MOST OFTEN (% OF OWNERS)

HOW COMPACT CAR PERFORMANCE PARTS AND ACCESSORIES ARE INSTALLED (% OF OWNERS)

0 10% 20% 30% 40%

Discount Retail Store (e.g. WalMart, Target)

Car/Truck Show

Auction Website (e.g. eBay

Direct from Manufacturer

Internet Website/Amazon (Retailer that sells online)

Discount Retail Store - Website (e.g. WalMart.com)

Independent/Specialty Parts Store/Garage

Mail Order/catalog

Chain Auto Parts Stores - Website

Other

Chain Auto Parts Stores

Car/Truck Dealership

Compact Performance Niche

9.1

6.0

10.5

1.8

7.6

4.2

8.0

4.7

2.0

7.2

36.6

2.4

24.6%

32.8%

42.6%

Did some myself and had others do some for me

Did it myself

had someone do it for me

About one-third of compact car respondents said that someone else installed their parts and accessories. About two-thirds of compact vehicle owners spend $500 or less per year on accessories.

2013 SEMA Annual Market Report

2626

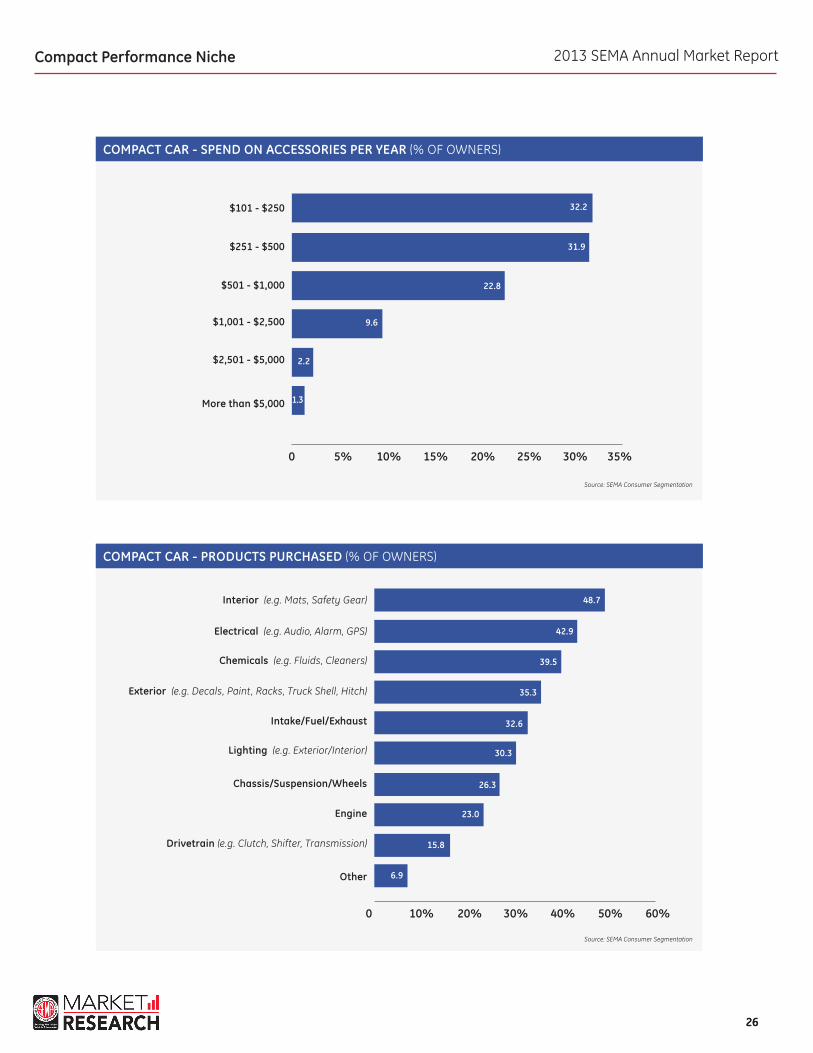

COMPACT CAR - SPEND ON ACCESSORIES PER YEAR (% OF OWNERS)

0 5% 15% 20% 25% 30% 35%10%

$501 - $1,000

$251 - $500

$1,001 - $2,500

$2,501 - $5,000

More than $5,000

$101 - $250

22.8

31.9

2.2

9.6

1.3

32.2

Compact Performance Niche

Source: SEMA Consumer Segmentation

Source: SEMA Consumer Segmentation

COMPACT CAR - PRODUCTS PURChASED (% OF OWNERS)

0 10% 30% 40% 50% 60%20%

Chemicals (e.g. Fluids, Cleaners)

Chassis/Suspension/Wheels

Electrical (e.g. Audio, Alarm, GPS)

Exterior (e.g. Decals, Paint, Racks, Truck Shell, Hitch)

Engine

Intake/Fuel/Exhaust

Drivetrain (e.g. Clutch, Shifter, Transmission)

Lighting (e.g. Exterior/Interior)

Interior (e.g. Mats, Safety Gear)

Other

39.5

26.3

42.9

32.6

15.8

35.3

23.0

30.3

48.7

6.9

2013 SEMA Annual Market Report

2727

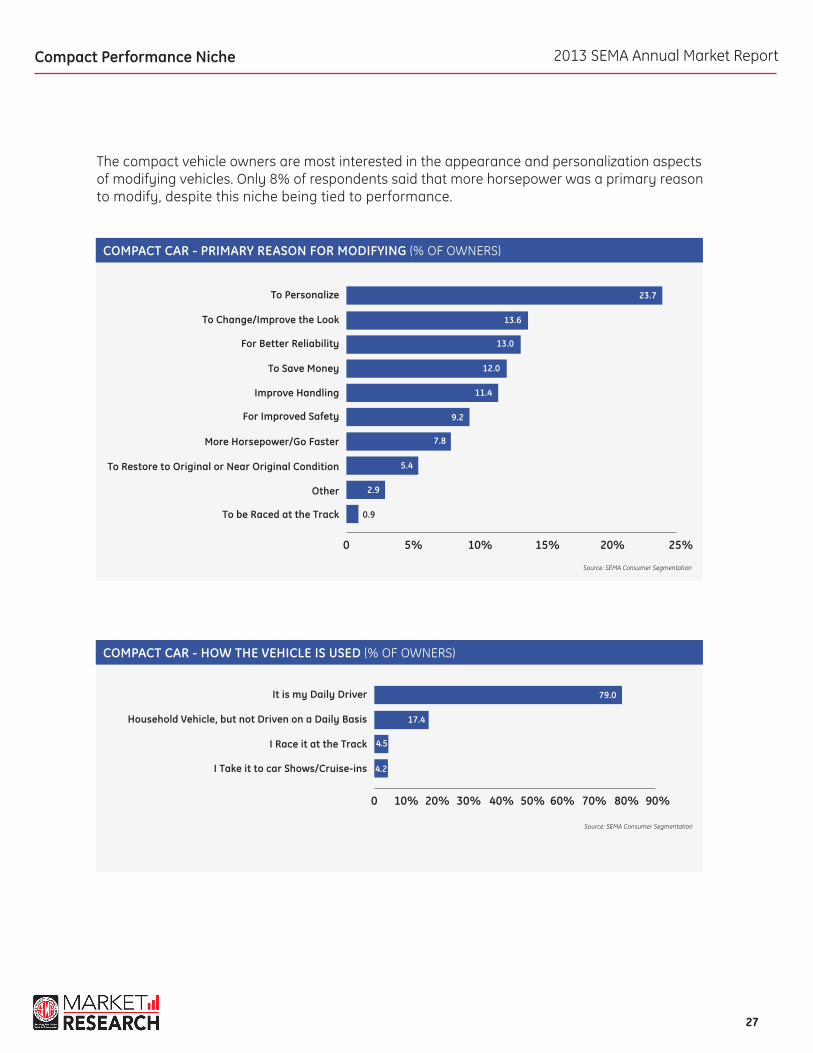

COMPACT CAR - PRIMARY REASON FOR MODIFYING (% OF OWNERS)

0 5% 15% 20% 25%10%

For Better Reliability

More horsepower/Go Faster

To Change/Improve the Look

To Save Money

To Restore to Original or Near Original Condition

Improve handling

Other

For Improved Safety

To be Raced at the Track

To Personalize

13.6

9.2

12.0

5.4

0.9

23.7

11.4

13.0

7.8

2.9

Compact Performance Niche

The compact vehicle owners are most interested in the appearance and personalization aspects of modifying vehicles. Only 8% of respondents said that more horsepower was a primary reason to modify, despite this niche being tied to performance.

Source: SEMA Consumer Segmentation

Source: SEMA Consumer Segmentation

COMPACT CAR - hOW ThE VEhICLE IS USED (% OF OWNERS)

0 10% 30% 40% 50% 60% 70% 80% 90%20%

household Vehicle, but not Driven on a Daily Basis

I Race it at the Track

I Take it to car Shows/Cruise-ins

It is my Daily Driver

17.4

4.2

4.5

79.0

2013 SEMA Annual Market Report

2828

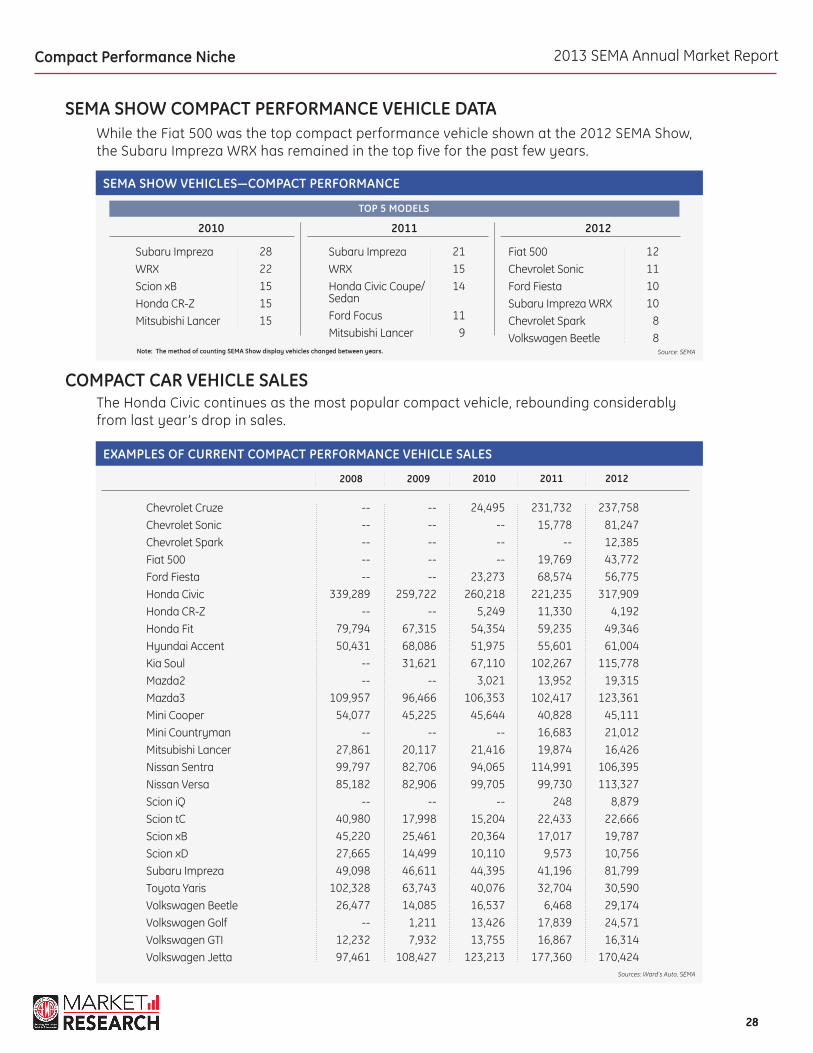

Chevrolet CruzeChevrolet SonicChevrolet SparkFiat 500Ford FiestaHonda CivicHonda CR-ZHonda FitHyundai AccentKia SoulMazda2Mazda3Mini CooperMini CountrymanMitsubishi LancerNissan SentraNissan VersaScion iQScion tCScion xBScion xDSubaru ImprezaToyota YarisVolkswagen BeetleVolkswagen GolfVolkswagen GTIVolkswagen Jetta

ExAMPLES OF CURRENT COMPACT PERFORMANCE VEHICLE SALES

2008 2009 2010 2011 2012

----------

339,289--

79,79450,431

----

109,95754,077

--27,86199,79785,182

--40,98045,22027,66549,098

102,32826,477

--12,23297,461

----------

259,722--

67,31568,08631,621

--96,46645,225

--20,11782,70682,906

--17,99825,46114,49946,61163,74314,085

1,2117,932

108,427

24,495------

23,273260,218

5,24954,35451,97567,110

3,021106,353

45,644--

21,41694,06599,705

--15,20420,36410,11044,39540,07616,53713,42613,755

123,213

231,73215,778

--19,76968,574

221,23511,33059,23555,601

102,26713,952

102,41740,82816,68319,874

114,99199,730

24822,43317,017

9,57341,19632,704

6,46817,83916,867

177,360

237,75881,24712,38543,77256,775

317,9094,192

49,34661,004

115,77819,315

123,36145,11121,01216,426

106,395113,327

8,87922,66619,78710,75681,79930,59029,17424,57116,314

170,424Sources: Ward’s Auto, SEMA

COMPACT CAR VEHICLE SALES

SEMA SHOW COMPACT PERFORMANCE VEHICLE DATAWhile the Fiat 500 was the top compact performance vehicle shown at the 2012 SEMA Show, the Subaru Impreza WRX has remained in the top five for the past few years.

The Honda Civic continues as the most popular compact vehicle, rebounding considerably from last year’s drop in sales.

SEMA ShOW VEhICLES—COMPACT PERFORMANCE

2010 2011 2012

Subaru Impreza WRXScion xBHonda CR-ZMitsubishi Lancer

Subaru Impreza WRXHonda Civic Coupe/SedanFord FocusMitsubishi Lancer

Fiat 500Chevrolet SonicFord FiestaSubaru Impreza WRXChevrolet SparkVolkswagen Beetle

2822151515

211514

119

12111010

88

Source: SEMANote: The method of counting SEMA Show display vehicles changed between years.

TOP 5 MODELS

Compact Performance Niche

2013 SEMA Annual Market Report

2929

LIGhT-TRUCk NIChE

The SEMA definition of the light-truck niche includes a combination of pickups, SUVs, CUVs and vans. This market was particularly hard hit by the recession that began in 2008 as well as the escalation of fuel prices in the last few years. Light-truck accessory sales plummeted from their peak in 2007 but now seem to be leveling out . The downward trend has begun to improve slightly in 2012 by gaining almost 1% from the previous year.

Light-Truck Niche

LIGhT-TRUCk RETAIL SALES ($ BILLIONS)

LIGhT-TRUCk MANUFACTURER SALES BY PRODUCT SEGMENT ($ MILLIONS)

2001

2004

2005

20092008

2009

2002

2003

2006

2007

2011

2011

2001

2002

2005

2006

2010

2010

2003

2004

2007

2008

2012

2012

10

5

200

400

600

800

15

$ 4.65

$ 307$ 643$ 712

Source: Lang Research

Source: Lang Research

Performance ProductsWheels, Tires, Suspension Accessory and Appearance Products

2013 SEMA Annual Market Report

3030

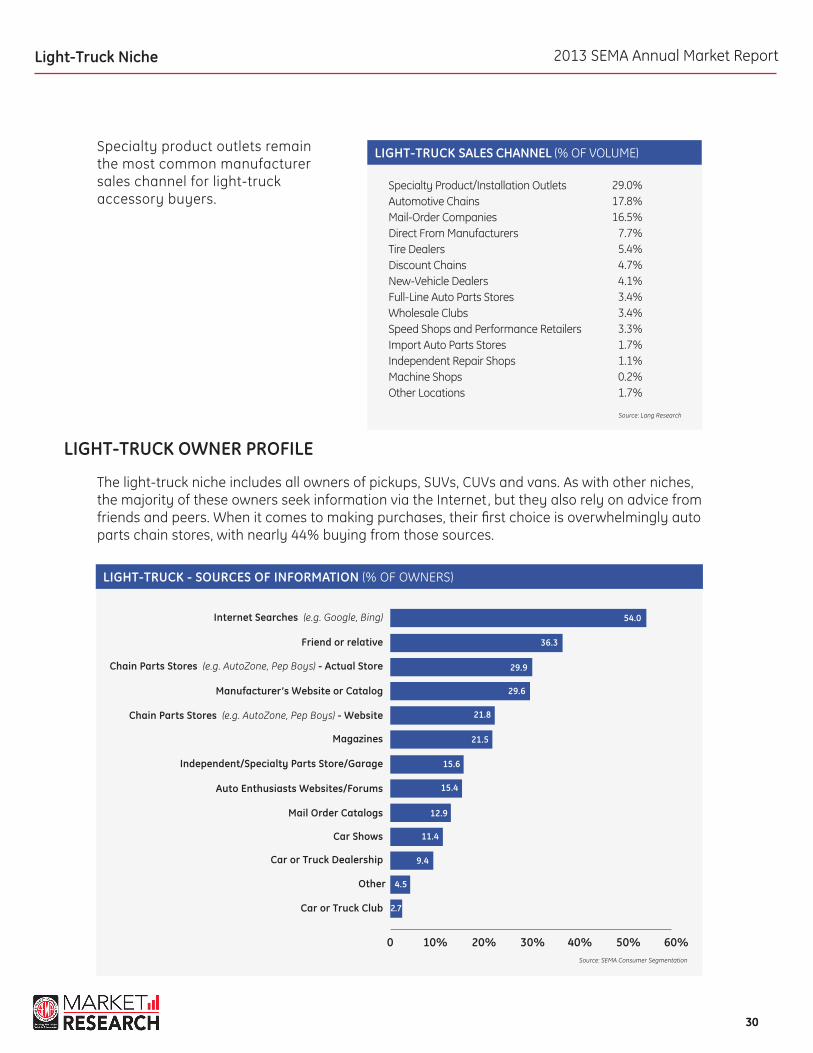

LIGhT-TRUCk OWNER PROFILE

The light-truck niche includes all owners of pickups, SUVs, CUVs and vans. As with other niches, the majority of these owners seek information via the Internet, but they also rely on advice from friends and peers. When it comes to making purchases, their first choice is overwhelmingly auto parts chain stores, with nearly 44% buying from those sources.

Specialty product outlets remain the most common manufacturer sales channel for light- truck accessory buyers.

LIGhT-TRUCk SALES ChANNEL (% OF VOLUME)

Specialty Product/Installation Outlets Automotive Chains Mail-Order CompaniesDirect From Manufacturers Tire Dealers Discount Chains New-Vehicle Dealers Full-Line Auto Parts Stores Wholesale Clubs Speed Shops and Performance RetailersImport Auto Parts Stores Independent Repair Shops Machine Shops Other Locations

29.0%17.8%16.5%

7.7%5.4%4.7%4.1%3.4%3.4%3.3%1.7%1.1%0.2%1.7%

Source: Lang Research

Source: SEMA Consumer Segmentation

LIGhT-TRUCk - SOURCES OF INFORMATION (% OF OWNERS)

0 10% 30% 40% 50% 60%20%

Chain Parts Stores (e.g. AutoZone, Pep Boys) - Actual Store

Independent/Specialty Parts Store/Garage

Friend or relative

Car or Truck Dealership

Manufacturer’s Website or Catalog

Auto Enthusiasts Websites/Forums

Other

Chain Parts Stores (e.g. AutoZone, Pep Boys) - Website

Mail Order Catalogs

Car or Truck Club

Magazines

Internet Searches (e.g. Google, Bing)

Car Shows

29.9

15.6

36.3

9.4

21.8

12.9

29.6

15.4

4.5

2.7

21.5

54.0

11.4

Light-Truck Niche

2013 SEMA Annual Market Report

3131

Source: SEMA Consumer Segmentation

Source: SEMA Consumer Segmentation

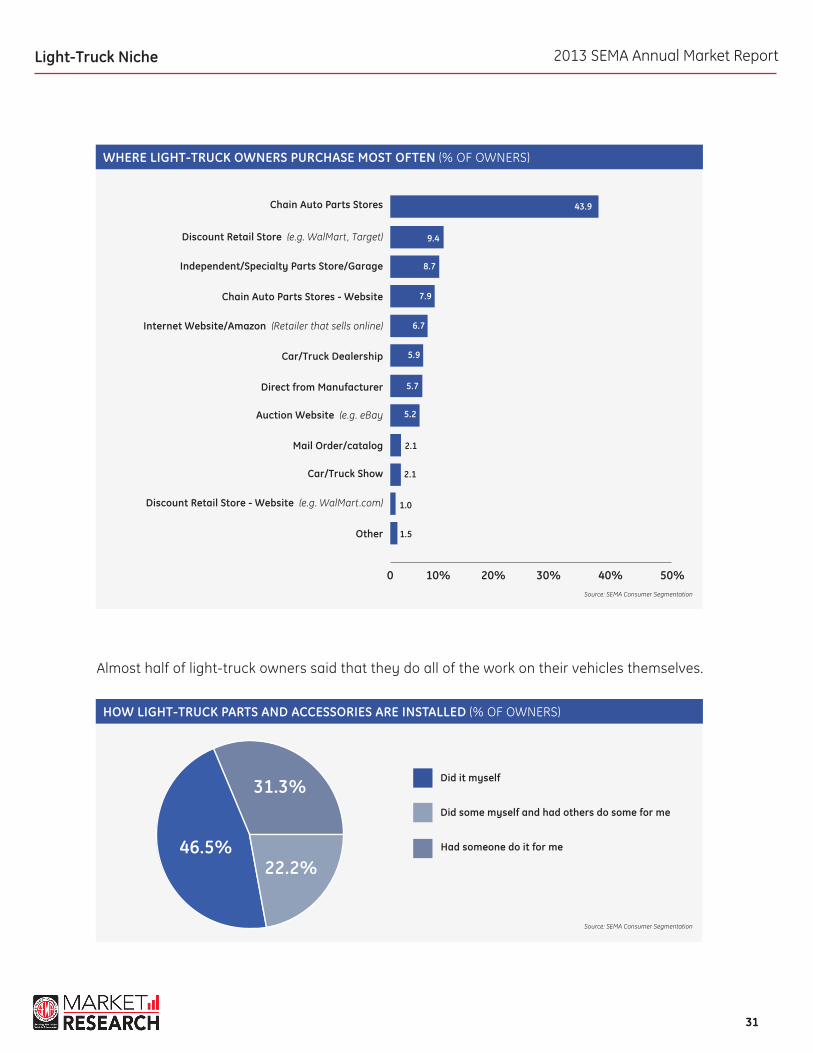

WhERE LIGhT-TRUCk OWNERS PURChASE MOST OFTEN (% OF OWNERS)

hOW LIGhT-TRUCk PARTS AND ACCESSORIES ARE INSTALLED (% OF OWNERS)

0 10% 20% 30% 40% 50%

Independent/Specialty Parts Store/Garage

Mail Order/catalog

Discount Retail Store (e.g. WalMart, Target)

Auction Website (e.g. eBay

Chain Auto Parts Stores - Website

Car/Truck Show

Internet Website/Amazon (Retailer that sells online)

Discount Retail Store - Website (e.g. WalMart.com)

Car/Truck Dealership

Other

Chain Auto Parts Stores

Direct from Manufacturer

Light-Truck Niche

8.7

5.7

9.4

1.0

6.7

2.1

2.1

7.9

5.2

1.5

5.9

43.9

22.2%

31.3%

46.5%

Did some myself and had others do some for me

Did it myself

had someone do it for me

Almost half of light-truck owners said that they do all of the work on their vehicles themselves.

2013 SEMA Annual Market Report

3232

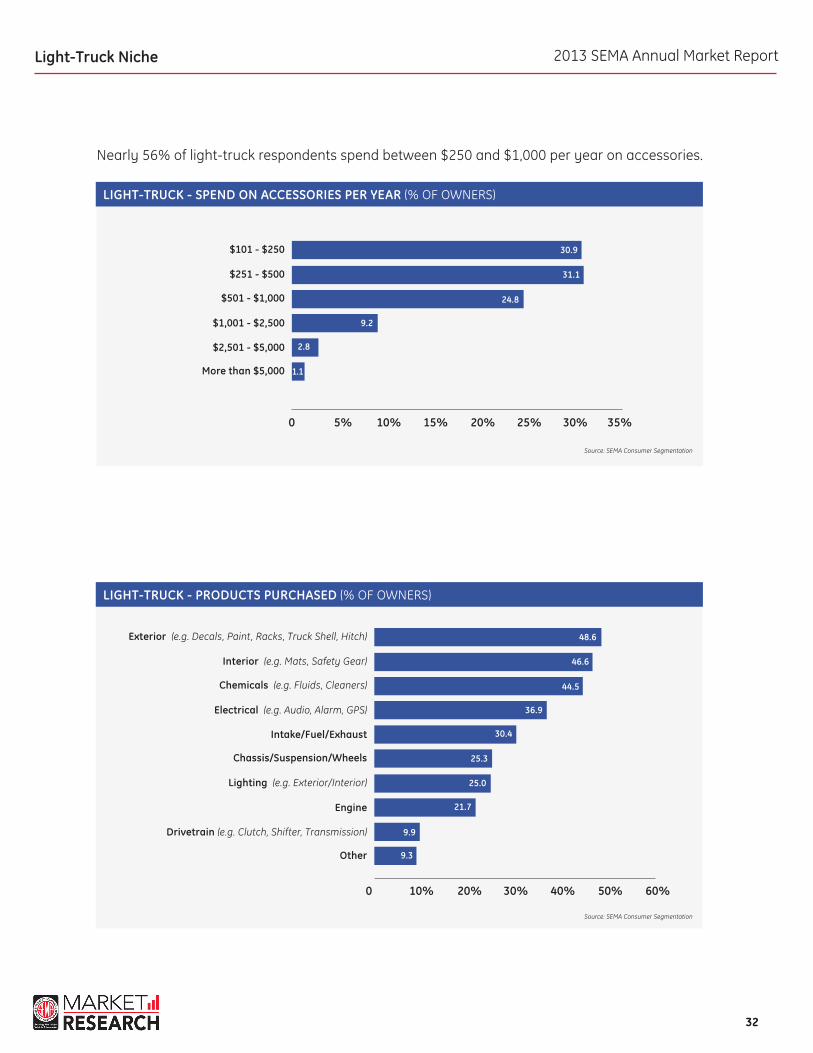

LIGhT-TRUCk - SPEND ON ACCESSORIES PER YEAR (% OF OWNERS)

0 5% 15% 20% 25% 30% 35%10%

$501 - $1,000

$251 - $500

$1,001 - $2,500

$2,501 - $5,000

More than $5,000

$101 - $250

24.8

31.1

2.8

9.2

1.1

30.9

Light-Truck Niche

Source: SEMA Consumer Segmentation

Source: SEMA Consumer Segmentation

LIGhT-TRUCk - PRODUCTS PURChASED (% OF OWNERS)

0 10% 30% 40% 50% 60%20%

Chemicals (e.g. Fluids, Cleaners)

Lighting (e.g. Exterior/Interior)

Interior (e.g. Mats, Safety Gear)

Electrical (e.g. Audio, Alarm, GPS)

Engine

Intake/Fuel/Exhaust

Drivetrain (e.g. Clutch, Shifter, Transmission)

Chassis/Suspension/Wheels

Exterior (e.g. Decals, Paint, Racks, Truck Shell, Hitch)

Other

44.5

25.0

46.6

30.4

9.9

36.9

21.7

25.3

48.6

9.3

Nearly 56% of light-truck respondents spend between $250 and $1,000 per year on accessories.

2013 SEMA Annual Market Report

3333

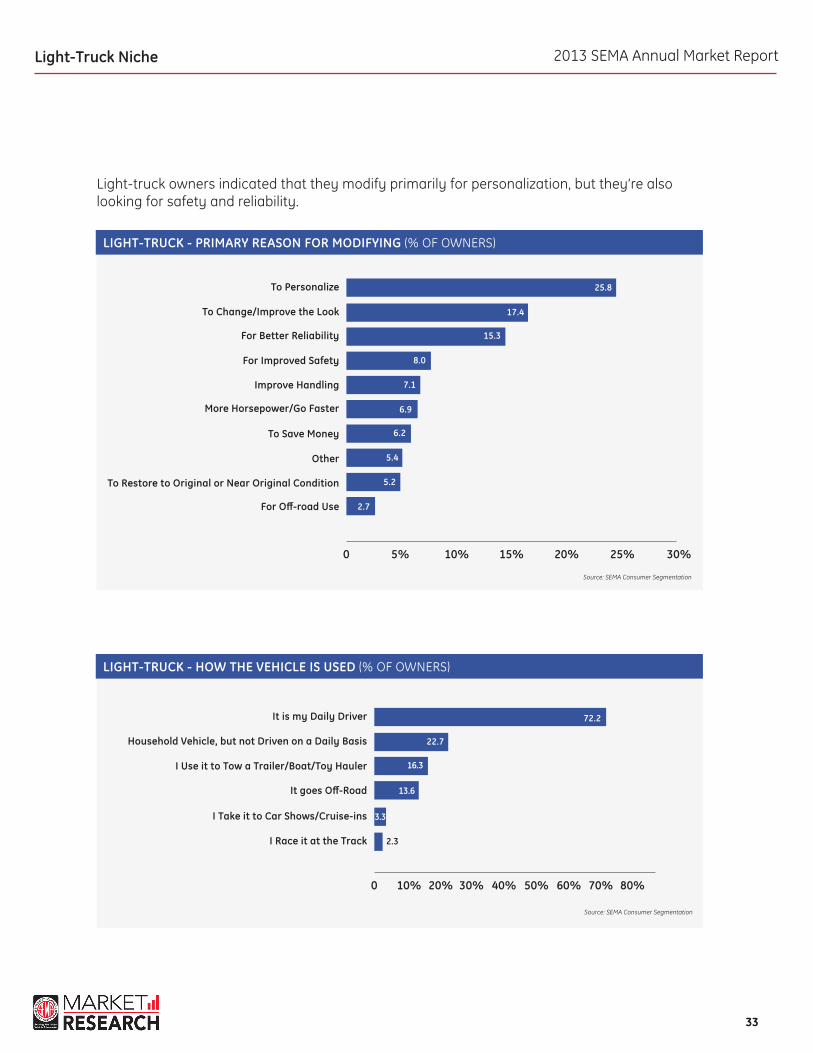

LIGhT-TRUCk - PRIMARY REASON FOR MODIFYING (% OF OWNERS)

0 5% 15% 20% 25% 30%10%

For Better Reliability

To Save Money

To Change/Improve the Look

For Improved Safety

Other

Improve handling

To Restore to Original or Near Original Condition

More horsepower/Go Faster

For Off-road Use

To Personalize

17.4

6.9

8.0

5.4

2.7

25.8

7.1

15.3

6.2

5.2

Light-Truck Niche

Light-truck owners indicated that they modify primarily for personalization, but they’re also looking for safety and reliability.

Source: SEMA Consumer Segmentation

Source: SEMA Consumer Segmentation

LIGhT-TRUCk - hOW ThE VEhICLE IS USED (% OF OWNERS)

0 10% 30% 40% 50% 60% 70% 80%20%

household Vehicle, but not Driven on a Daily Basis

I Race it at the Track

I Use it to Tow a Trailer/Boat/Toy hauler

It goes Off-Road

It is my Daily Driver

I Take it to Car Shows/Cruise-ins

22.7

2.3

13.6

16.3

72.2

3.3

2013 SEMA Annual Market Report

3434

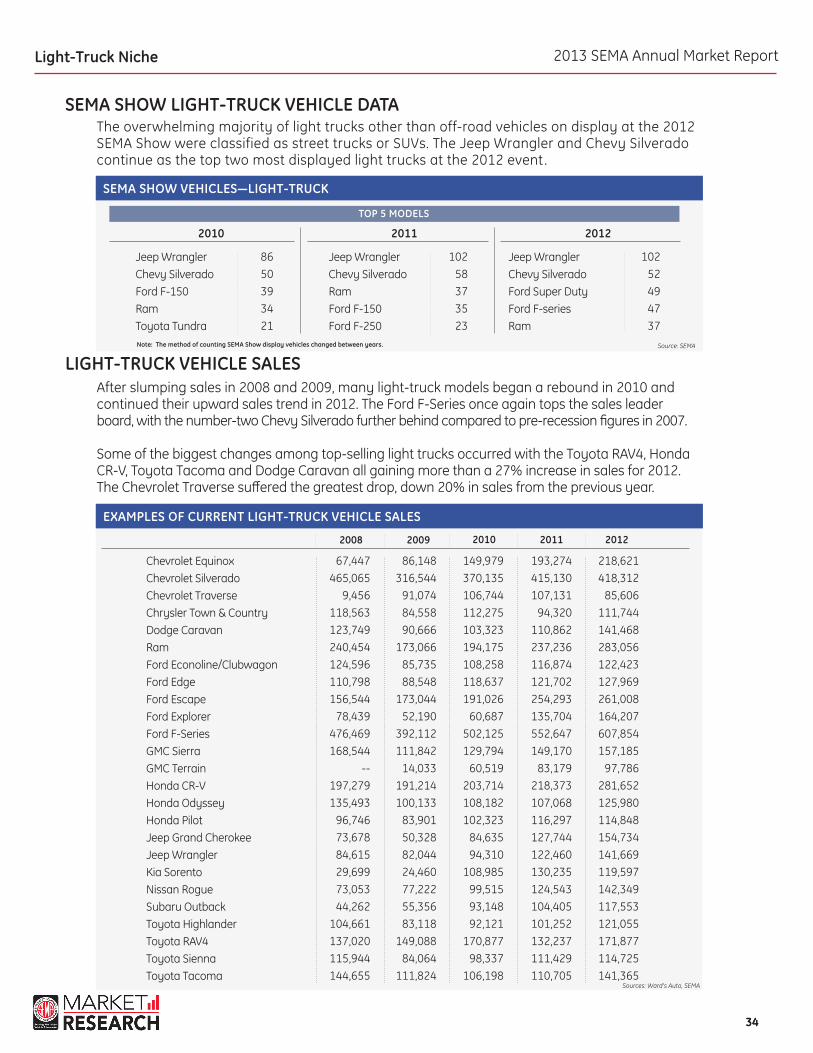

SEMA ShOW LIGhT-TRUCk VEhICLE DATAThe overwhelming majority of light trucks other than off-road vehicles on display at the 2012 SEMA Show were classified as street trucks or SUVs. The Jeep Wrangler and Chevy Silverado continue as the top two most displayed light trucks at the 2012 event .

SEMA ShOW VEhICLES—LIGhT-TRUCk

2010 2011 2012

Jeep WranglerChevy SilveradoFord F-150RamToyota Tundra

Jeep WranglerChevy SilveradoRamFord F-150Ford F-250

Jeep WranglerChevy SilveradoFord Super DutyFord F-seriesRam

8650393421

10258373523

10252494737

Source: SEMA

TOP 5 MODELS

LIGhT-TRUCk VEhICLE SALESAfter slumping sales in 2008 and 2009, many light-truck models began a rebound in 2010 and continued their upward sales trend in 2012. The Ford F-Series once again tops the sales leader board, with the number-two Chevy Silverado further behind compared to pre-recession figures in 2007.

Some of the biggest changes among top-selling light trucks occurred with the Toyota RAV4, Honda CR-V, Toyota Tacoma and Dodge Caravan all gaining more than a 27% increase in sales for 2012. The Chevrolet Traverse suffered the greatest drop, down 20% in sales from the previous year.

Chevrolet EquinoxChevrolet SilveradoChevrolet TraverseChrysler Town & CountryDodge Caravan Ram Ford Econoline/ClubwagonFord EdgeFord EscapeFord ExplorerFord F-SeriesGMC SierraGMC TerrainHonda CR-VHonda OdysseyHonda PilotJeep Grand CherokeeJeep WranglerKia SorentoNissan RogueSubaru OutbackToyota HighlanderToyota RAV4Toyota SiennaToyota Tacoma

ExAMPLES OF CURRENT LIGhT-TRUCk VEhICLE SALES

2008 2009 2010 2011 2012

67,447465,065

9,456118,563123,749240,454124,596110,798156,544

78,439476,469168,544

--197,279135,493

96,74673,67884,61529,69973,05344,262

104,661137,020115,944144,655

86,148316,544

91,07484,55890,666

173,06685,73588,548

173,04452,190

392,112111,842

14,033191,214100,133

83,90150,32882,04424,46077,22255,35683,118

149,08884,064

111,824

149,979370,135106,744112,275103,323194,175108,258118,637191,026

60,687502,125129,794

60,519203,714108,182102,323

84,63594,310

108,98599,51593,14892,121

170,87798,337

106,198

193,274415,130107,131

94,320110,862237,236116,874121,702254,293135,704552,647149,170

83,179218,373107,068116,297127,744122,460130,235124,543104,405101,252132,237111,429110,705

218,621418,312

85,606111,744141,468283,056122,423127,969261,008164,207607,854157,185

97,786281,652125,980114,848154,734141,669119,597142,349117,553121,055171,877114,725141,365

Sources: Ward’s Auto, SEMA

Note: The method of counting SEMA Show display vehicles changed between years.

Light-Truck Niche

2013 SEMA Annual Market Report

3535

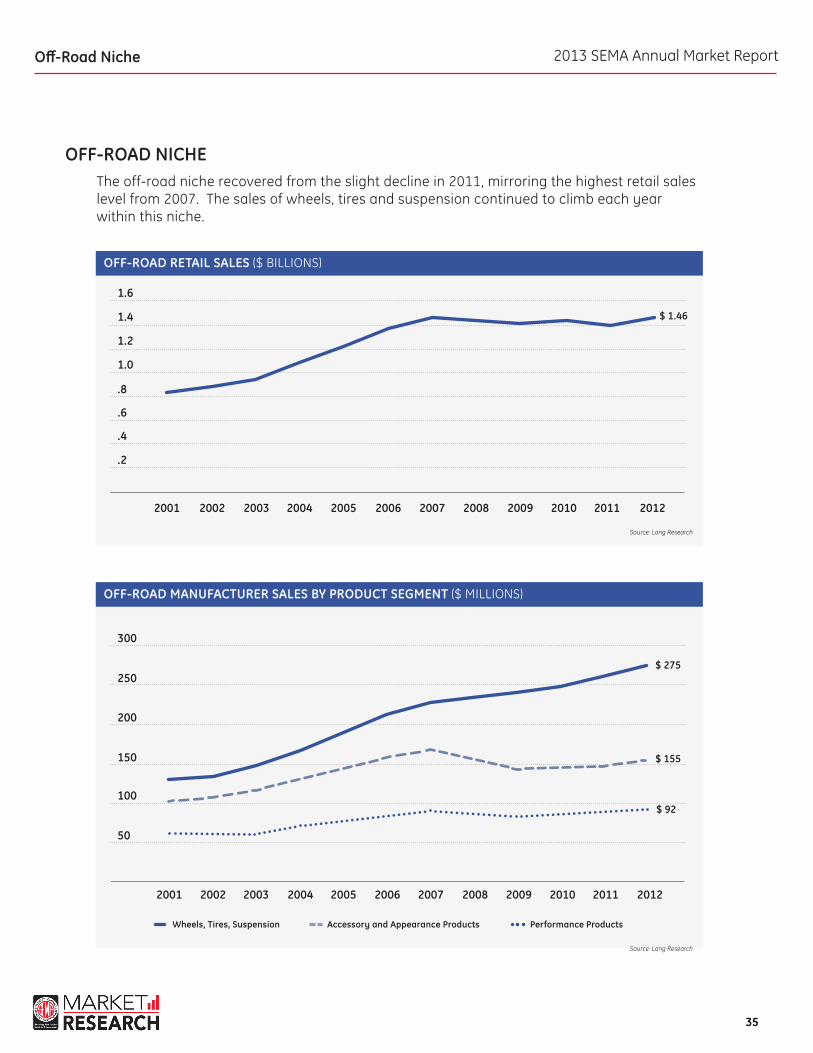

OFF-ROAD NIChEThe off-road niche recovered from the slight decline in 2011, mirroring the highest retail sales level from 2007. The sales of wheels, tires and suspension continued to climb each year within this niche.

Off-Road Niche

OFF-ROAD RETAIL SALES ($ BILLIONS)

OFF-ROAD MANUFACTURER SALES BY PRODUCT SEGMENT ($ MILLIONS)

2001

2004

2005

20092008

2009

2002

2003

2006

2007

2011

2011

2001

2002

2005

2006

2010

2010

2003

2004

2007

2008

2012

2012

.2

.4

.6

.8

1.0

1.2

1.4

1.6

50

100

150

200

250

300

$ 1.46

$ 92

$ 155

$ 275

Source: Lang Research

Source: Lang Research

Performance ProductsWheels, Tires, Suspension Accessory and Appearance Products

2013 SEMA Annual Market Report

3636

OFF-ROAD SALES ChANNEL (% OF VOLUME)

Specialty Product/Installation Outlets Mail-Order CompaniesAutomotive Chains Direct from Manufacturers Tire Dealers New-Vehicle Dealers Discount Chains Wholesale Clubs Speed Shops and Performance RetailersFull-Line Auto Parts Stores Import Auto Parts Stores Independent Repair Shops Machine Shops Other Locations

28.4%17.7%15.5%

8.1%6.4%4.3%4.2%3.6%3.5%3.2%1.6%1.2%0.4%1.9%

Source: Lang Research

Source: SEMA Consumer Segmentation

OFF-ROAD - SOURCES OF INFORMATION (% OF OWNERS)

0 10% 30% 40% 50% 60%20%

Chain Parts Stores (e.g. AutoZone, Pep Boys) - Actual Store

Chain Parts Stores (e.g. AutoZone, Pep Boys) - Website

Manufacturer’s Website or Catalog

Car or Truck Dealership

Magazines

Car Shows

Car or Truck Club

Friend or relative

Mail Order Catalogs

Auto Enthusiasts Websites/Forums

Internet Searches (e.g. Google, Bing)

Independent/Specialty Parts Store/Garage

38.7

27.7

40.3

12.6

30.3

22.7

37.8

24.4

5.9

30.3

54.0

20.2

Off-Road Niche

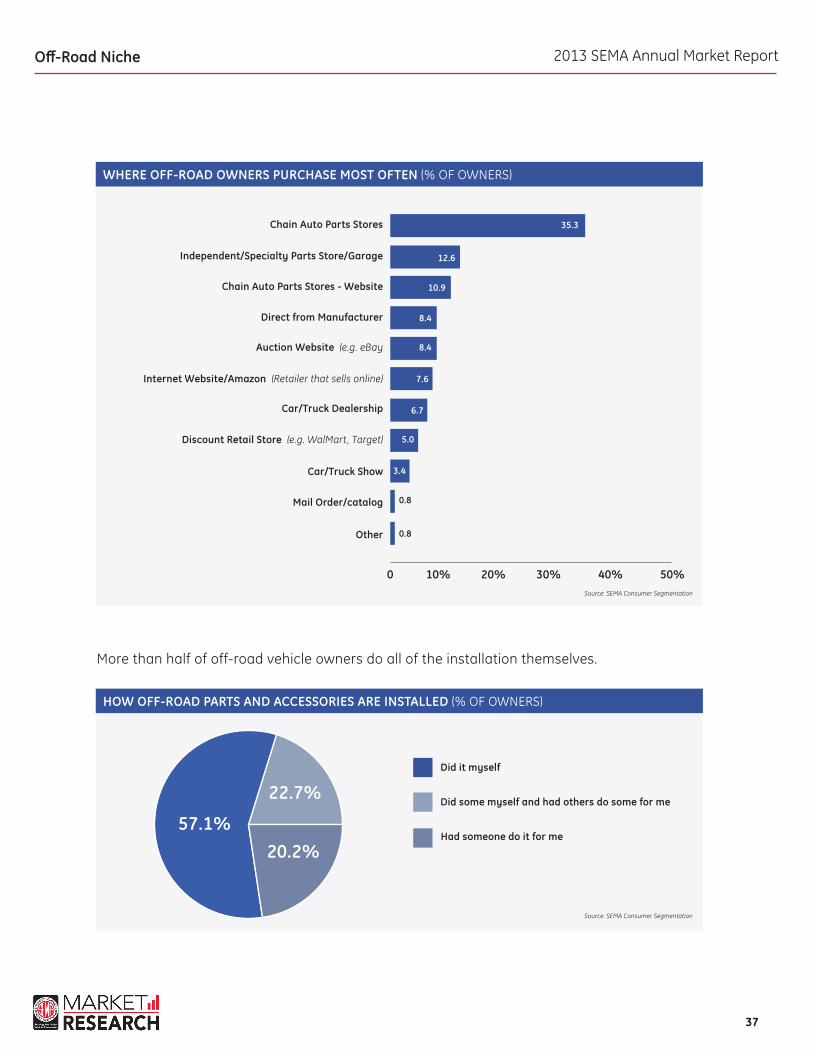

OFF-ROAD OWNER PROFILEThe results tabulated in the following section include data from only consumers who indicated that they used their vehicles off-road. Like most others, off-road owners are likely to look to the Internet for information about customization.

2013 SEMA Annual Market Report

3737

Source: SEMA Consumer Segmentation

Source: SEMA Consumer Segmentation

WhERE OFF-ROAD OWNERS PURChASE MOST OFTEN (% OF OWNERS)

hOW OFF-ROAD PARTS AND ACCESSORIES ARE INSTALLED (% OF OWNERS)

0 10% 20% 30% 40% 50%

Chain Auto Parts Stores - Website

Car/Truck Show

Independent/Specialty Parts Store/Garage

Discount Retail Store (e.g. WalMart, Target)

Direct from Manufacturer

Mail Order/catalog

Auction Website (e.g. eBay

Other

Internet Website/Amazon (Retailer that sells online)

Chain Auto Parts Stores

Car/Truck Dealership

Off-Road Niche

10.9

6.7

12.6

8.4

3.4

0.8

0.8

8.4

5.0

7.6

35.3

20.2%

22.7%

57.1%Did some myself and had others do some for me

Did it myself

had someone do it for me

More than half of off-road vehicle owners do all of the installation themselves.

2013 SEMA Annual Market Report

3838

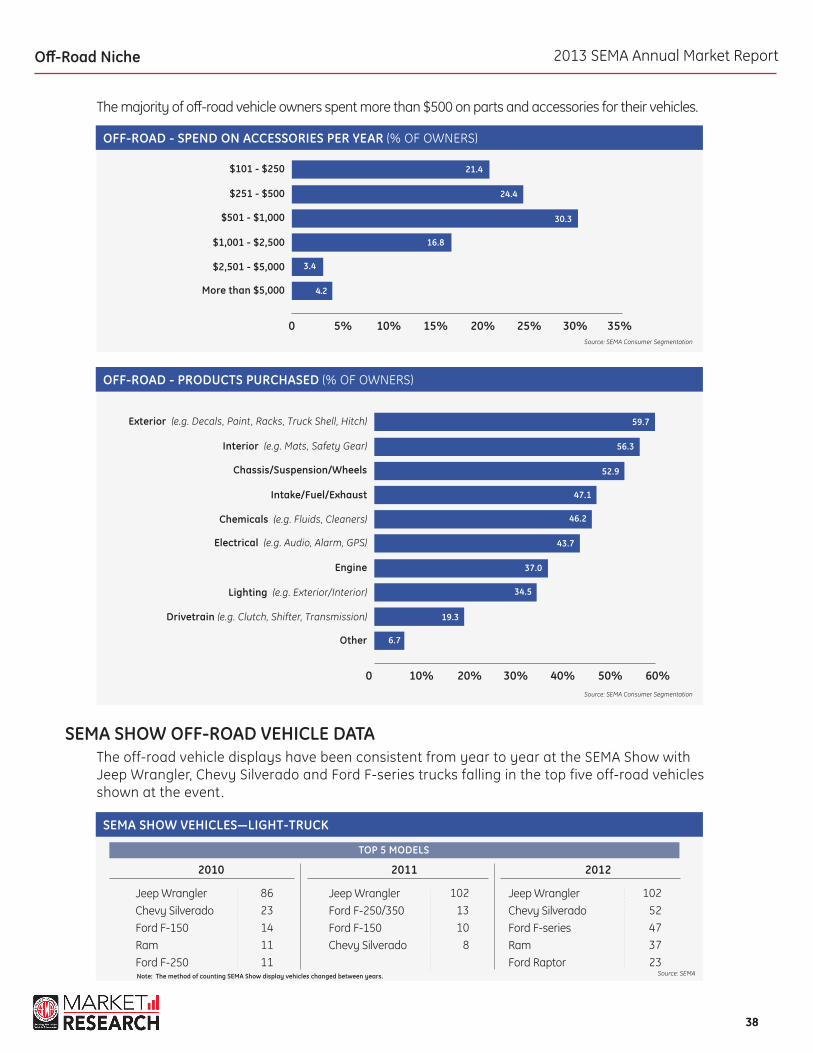

SEMA ShOW OFF-ROAD VEhICLE DATAThe off-road vehicle displays have been consistent from year to year at the SEMA Show with Jeep Wrangler, Chevy Silverado and Ford F-series trucks falling in the top five off-road vehicles shown at the event .

SEMA ShOW VEhICLES—LIGhT-TRUCk

2010 2011 2012

Jeep WranglerChevy SilveradoFord F-150RamFord F-250

Jeep WranglerFord F-250/350Ford F-150Chevy Silverado

Jeep WranglerChevy SilveradoFord F-seriesRamFord Raptor

8623141111

1021310

8

10252473723

Source: SEMA

TOP 5 MODELS

Note: The method of counting SEMA Show display vehicles changed between years.

OFF-ROAD - SPEND ON ACCESSORIES PER YEAR (% OF OWNERS)

0 5% 15% 20% 25% 30% 35%10%

$501 - $1,000

$251 - $500

$1,001 - $2,500

$2,501 - $5,000

More than $5,000

$101 - $250

30.3

24.4

3.4

16.8

4.2

21.4

Off-Road Niche

The majority of off-road vehicle owners spent more than $500 on parts and accessories for their vehicles.

Source: SEMA Consumer Segmentation

Source: SEMA Consumer Segmentation

OFF-ROAD - PRODUCTS PURChASED (% OF OWNERS)

0 10% 30% 40% 50% 60%20%

Chassis/Suspension/Wheels

Engine

Interior (e.g. Mats, Safety Gear)

Intake/Fuel/Exhaust

Lighting (e.g. Exterior/Interior)

Chemicals (e.g. Fluids, Cleaners)

Drivetrain (e.g. Clutch, Shifter, Transmission)

Electrical (e.g. Audio, Alarm, GPS)

Exterior (e.g. Decals, Paint, Racks, Truck Shell, Hitch)

Other

52.9

37.0

56.3

46.2

19.3

47.1

34.5

43.7

59.7

6.7

2013 SEMA Annual Market Report

3939

Chevrolet AvalancheChevrolet ColoradoChevrolet SilveradoChevrolet SuburbanChevrolet TahoeDodge Ram DakotaRamFord ExpeditionFord F-SeriesFord RangerGMC CanyonGMC SierraGMC YukonGMC Yukon XLHonda RidgelineJeep Grand CherokeeJeep WranglerLand Rover LR4Land Rover Range RoverLand Rover Range Rover SportNissan FrontierNissan TitanNissan XterraToyota 4RunnerToyota FJ CruiserToyota Land CruiserToyota TacomaToyota TundraVolkswagen Touareg

ExAMPLES OF CURRENT OFF-ROAD VEhICLE SALES

2008 2009 2010 2011 2012

35,00354,346

465,06554,05891,57826,044

240,45455,123

476,46965,87214,974

168,54439,06426,40433,87573,67884,615

--8,393

11,66844,99734,05333,57947,87828,668

3,801144,655137,249

6,755

16,43232,413

316,54441,05573,25410,690

173,06631,655

392,11255,60010,107

111,84229,41116,81916,46450,32882,044

8677,312

11,36428,41519,04216,45519,67511,941

2,261111,824

79,3854,392

20,51524,642

370,13545,15275,67513,047

194,17537,336

502,12555,364

7,992129,794

28,78123,79716,14284,63594,310

7,1228,746

12,34740,42723,41620,52346,53114,959

1,807106,198

93,3094,713

20,08831,026

415,13049,42780,52712,156

237,23640,499

552,64770,832

9,590149,170

34,25025,223

9,759127,744122,460

7,9839,761

15,33351,70021,99418,22144,31613,541

1,662110,705

82,9087,535

23,99536,840

418,31248,11668,904

490283,056

38,062607,854

19,3668,735

157,18527,81823,42714,068

154,734141,669

7,3167,843

16,49155,43521,57617,22248,75513,656

2,895141,365101,621

10,553

Sources: Ward’s Auto, SEMA

OFF-ROAD VEhICLE SALESAmong vehicles often accessorized for off-road use, the Toyota Land Cruiser, Volkswagen Touareg and Honda Ridgeline experienced the largest gain in sales in the past year. Sales for the Ford Ranger and Ram Dakota declined drastically in 2012 as the vehicles are being discontinued.

Off-Road Niche

2013 SEMA Annual Market Report

4040

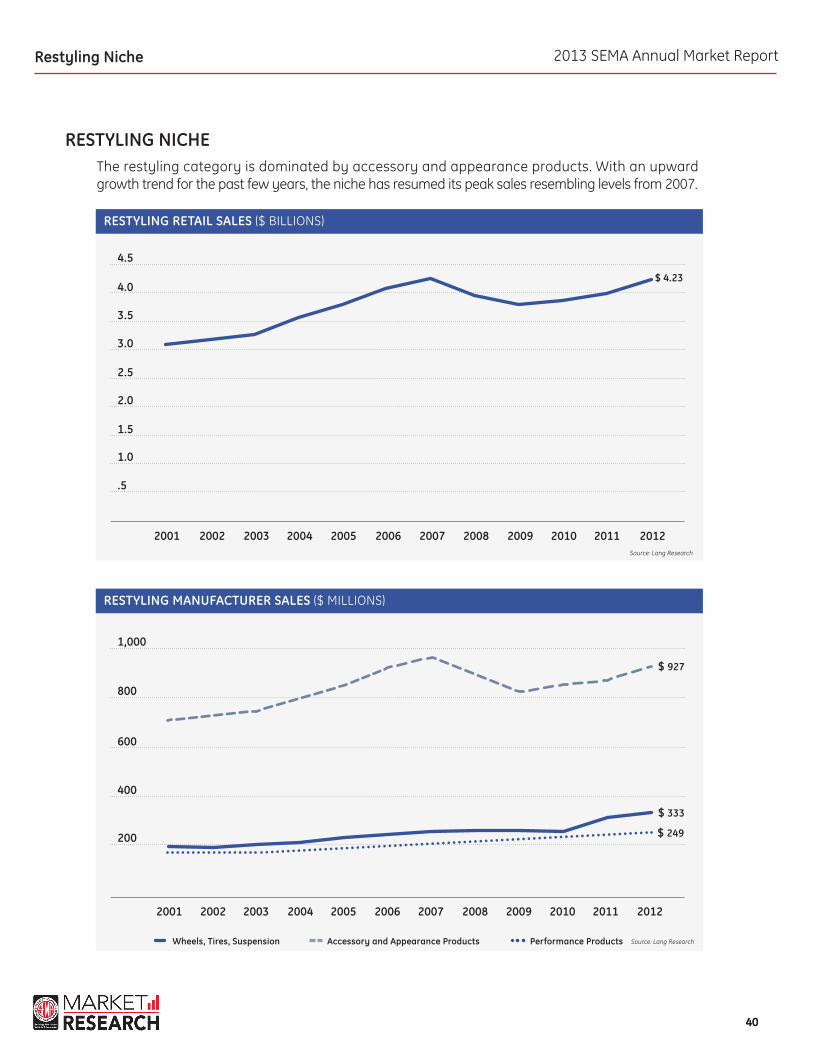

RESTYLING NICHEThe restyling category is dominated by accessory and appearance products. With an upward growth trend for the past few years, the niche has resumed its peak sales resembling levels from 2007.

Restyling Niche

RESTYLING RETAIL SALES ($ BILLIONS)

RESTYLING MANUFACTURER SALES ($ MILLIONS)

2001

2004

2005

20092008

2009

2002

2003

2006

2007

2011

2011

2001

2002

2005

2006

2010

2010

2003

2004

2007

2008

2012

2012

.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

200

400

600

800

1,000

$ 4.23

$ 249

$ 333

$ 927

Source: Lang Research

Source: Lang ResearchPerformance ProductsWheels, Tires, Suspension Accessory and Appearance Products

2013 SEMA Annual Market Report

4141

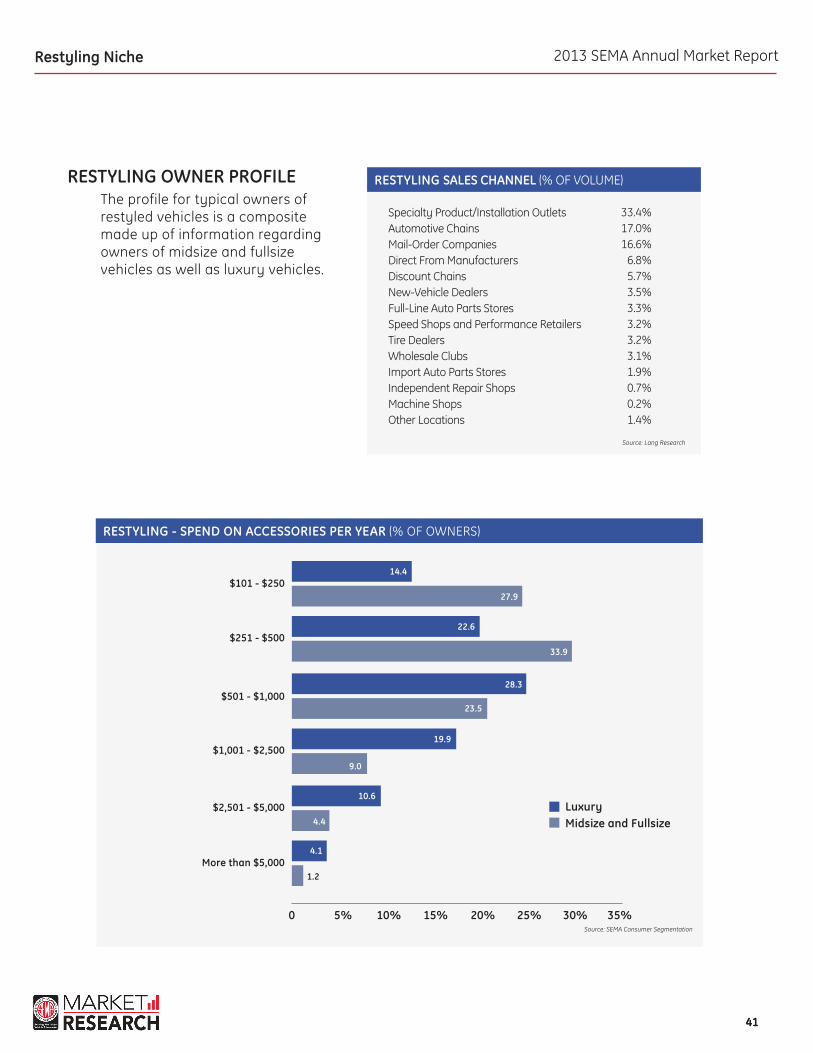

Restyling Niche

RESTYLING OWNER PROFILEThe profile for typical owners of restyled vehicles is a composite made up of information regarding owners of midsize and fullsize vehicles as well as luxury vehicles.

RESTYLING - SPEND ON ACCESSORIES PER YEAR (% OF OWNERS)

0 5% 15% 20% 25% 30% 35%

LuxuryMidsize and Fullsize

10%

$501 - $1,000

$251 - $500

$1,001 - $2,500

$2,501 - $5,000

More than $5,000

$101 - $25014.4

28.3

10.6

22.6

19.9

4.1

27.9

23.5

4.4

33.9

9.0

1.2

Source: SEMA Consumer Segmentation

RESTYLING SALES CHANNEL (% OF VOLUME)

Specialty Product/Installation Outlets Automotive Chains Mail-Order CompaniesDirect From Manufacturers Discount Chains New-Vehicle Dealers Full-Line Auto Parts Stores Speed Shops and Performance RetailersTire Dealers Wholesale Clubs Import Auto Parts Stores Independent Repair Shops Machine Shops Other Locations

33.4%17.0%16.6%

6.8%5.7%3.5%3.3%3.2%3.2%3.1%1.9%0.7%0.2%1.4%

Source: Lang Research

2013 SEMA Annual Market Report

4242

Source: SEMA Consumer Segmentation

RESTYLING - SOURCES OF INFORMATION - LUxURY VEhICLES (% OF OWNERS)

0 10% 30% 40% 50% 60%20%

Auto Enthusiasts Websites/Forums

Friend or relative

Manufacturer’s Website or Catalog

Car or Truck Dealership

Chain Parts Stores (e.g. AutoZone, Pep Boys) - Actual Store

Car Shows

Car or Truck Club

Chain Parts Stores (e.g. AutoZone, Pep Boys) - Website

Mail Order Catalogs

Other

Magazines

Internet Searches (e.g. Google, Bing)

Independent/Specialty Parts Store/Garage

30.8

23.7

38.4

9.5

28.1

19.3

30.5

20.7

8.2

3.3

27.5

47.1

19.3

Restyling Niche

Source: SEMA Consumer Segmentation

RESTYLING - SOURCES OF INFORMATION - MIDSIzE AND FULLSIzE (% OF OWNERS)

0 10% 30% 40% 50% 60%20%

Chain Parts Stores (e.g. AutoZone, Pep Boys) - Actual Store

Auto Enthusiasts Websites/Forums

Friend or relative

Car or Truck Dealership

Manufacturer’s Website or Catalog

Car Shows

Car or Truck Club

Magazines

Independent/Specialty Parts Store/Garage

Other

Chain Parts Stores (e.g. AutoZone, Pep Boys) - Website

Internet Searches (e.g. Google, Bing)

Mail Order Catalogs

30.9

19.4

36.6

9.2

26.8

15.1

28.3

15.9

4.8

3.0

24.0

57.8

14.4

While both groups use the Internet as a primary source for information, the owners of midsize and fullsize vehicles are more likely to also seek information from family and friends.

2013 SEMA Annual Market Report

4343

Source: SEMA Consumer Segmentation

Source: SEMA Consumer Segmentation

WhERE RESTYLING OWNERS PURChASE MOST OFTEN - MIDSIzE AND FULLSIzE (% OF OWNERS)

WhERE RESTYLING OWNERS PURChASE MOST OFTEN - LUxURY VEhICLES (% OF OWNERS)

0

0

10%

10% 15% 25%5%

20%

20%

30%

30%

40% 50%

Chain Auto Parts Stores - Website

Chain Auto Parts Stores - Website

Mail Order/Catalog

Discount Retail Store (e.g. WalMart, Target)

Discount Retail Store (e.g. WalMart, Target)

Auction Website (e.g. eBay

Direct from Manufacturer

Internet Website/Amazon (Retailer that sells online)

Independent/Specialty Parts Store/Garage

Independent/Specialty Parts Store/Garage

Car/Truck Show

Mail Order/Catalog

Auction Website (e.g. eBay

Direct from Manufacturer

Discount Retail Store - Website (e.g. WalMart.com)

Discount Retail Store - Website (e.g. WalMart.com)

Car/Truck Dealership

Car/Truck Dealership

Other

Other

Chain Auto Parts Stores - Actual Location

Chain Auto Parts Stores - Actual Location

Internet Website/Amazon (Retailer that sells online)

Car/Truck Show

Restyling Niche

10.2

11.4

5.7

6.5

10.6

13.9

0.5

0.8

8.8

8.2

3.0

5.2

2.3

3.0

10.1

9.5

4.9

5.2

0.9

0.8

6.2

7.6

36.7

27.8

2013 SEMA Annual Market Report

4444

Source: SEMA Consumer Segmentation

Source: SEMA Consumer Segmentation

hOW RESTYLING PARTS AND ACCESSORIES ARE INSTALLED - LUxURY VEhICLES (% OF OWNERS)

hOW RESTYLING PARTS AND ACCESSORIES ARE INSTALLED - MIDSIzE AND FULLSIzE (% OF OWNERS)

Restyling Niche

24.8%

23.1%

25.6%

33.6%

49.6%

43.3%

Did some myself and had others do some for me

Did some myself and had others do some for me

Did it myself

Did it myself

had someone do it for me

had someone do it for me

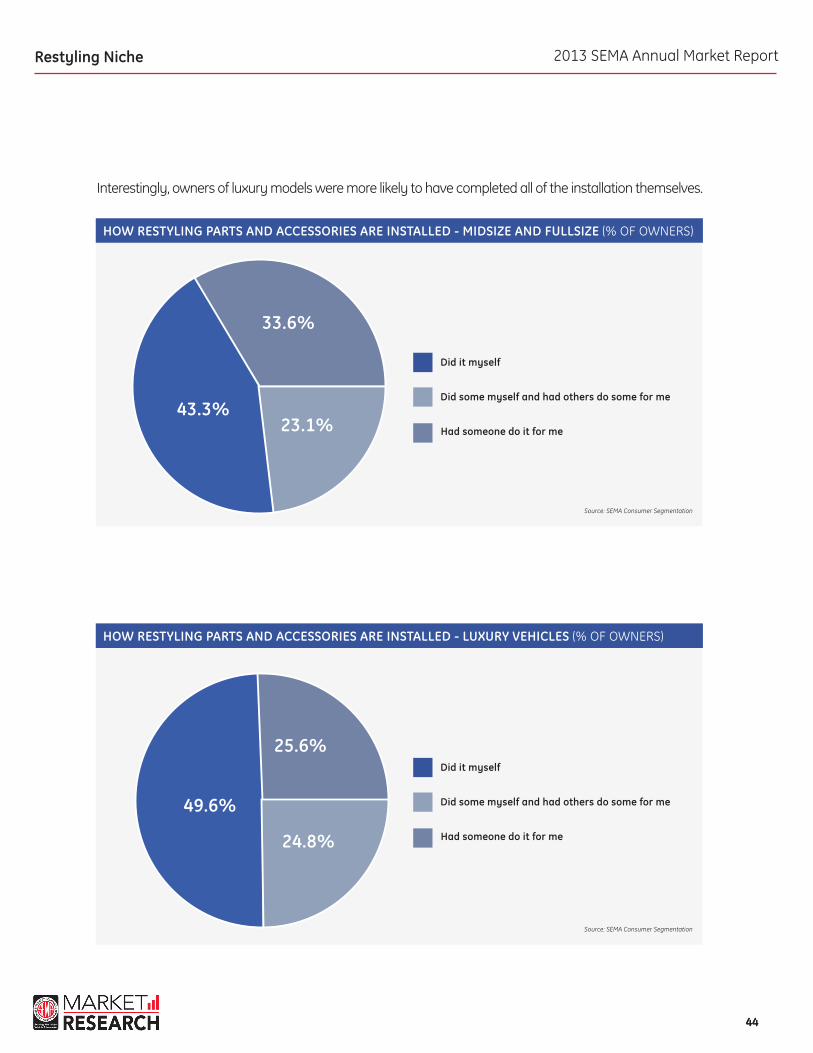

Interestingly, owners of luxury models were more likely to have completed all of the installation themselves.

2013 SEMA Annual Market Report

4545

Restyling Niche

Source: SEMA Consumer Segmentation

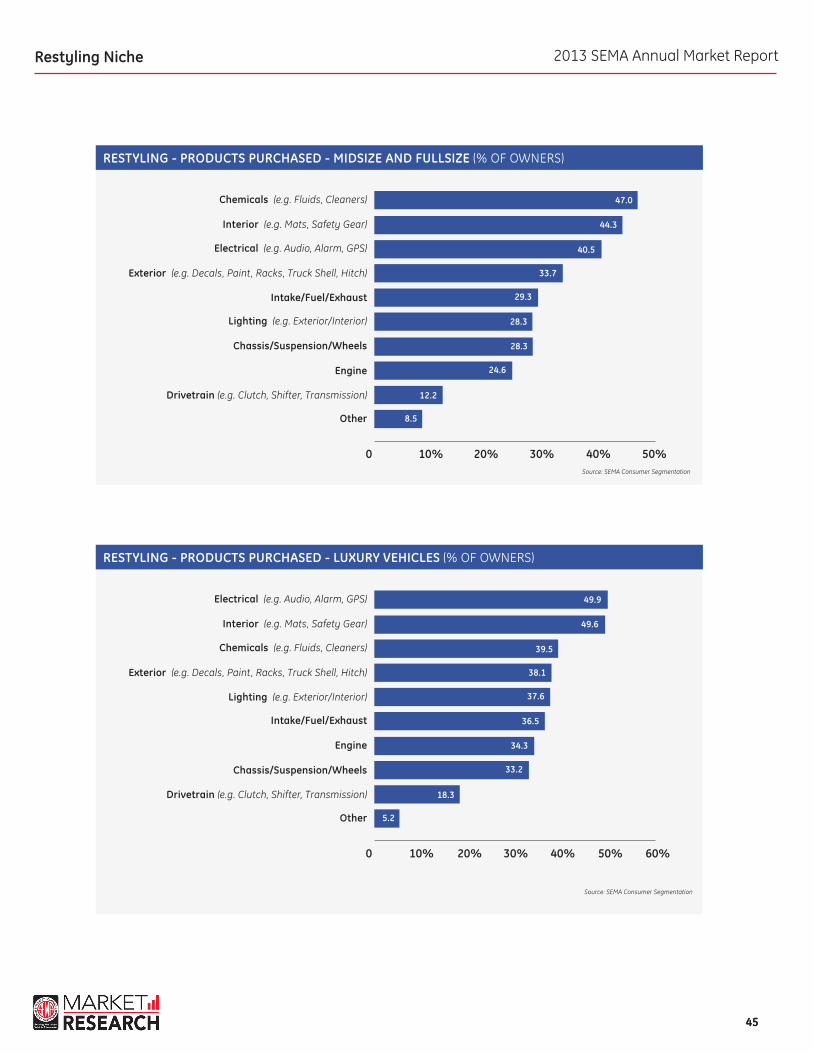

RESTYLING - PRODUCTS PURChASED - MIDSIzE AND FULLSIzE (% OF OWNERS)

RESTYLING - PRODUCTS PURChASED - LUxURY VEhICLES (% OF OWNERS)

0

0

10%

10%

30%

30%

40%

40%

50%

50% 60%

20%

20%

Electrical (e.g. Audio, Alarm, GPS)

Chemicals (e.g. Fluids, Cleaners)

Chassis/Suspension/Wheels

Engine

Interior (e.g. Mats, Safety Gear)

Interior (e.g. Mats, Safety Gear)

Exterior (e.g. Decals, Paint, Racks, Truck Shell, Hitch)

Exterior (e.g. Decals, Paint, Racks, Truck Shell, Hitch)

Engine

Chassis/Suspension/Wheels

Intake/Fuel/Exhaust

Lighting (e.g. Exterior/Interior)

Drivetrain (e.g. Clutch, Shifter, Transmission)

Drivetrain (e.g. Clutch, Shifter, Transmission)

Lighting (e.g. Exterior/Interior)

Intake/Fuel/Exhaust

Chemicals (e.g. Fluids, Cleaners)

Electrical (e.g. Audio, Alarm, GPS)

Other

Other

40.5

39.5

28.3

34.3

44.3

49.6

29.3

37.6

12.2

18.3

33.7

38.1

24.6

33.2

28.3

36.5

47.0

49.9

8.5

5.2

Source: SEMA Consumer Segmentation

2013 SEMA Annual Market Report

4646

RESTYLING - PRIMARY REASON FOR MODIFYING - MIDSIzE AND FULLSIzE (% OF OWNERS)

RESTYLING - PRIMARY REASON FOR MODIFYING - LUxURY VEhICLES (% OF OWNERS)

0

0

5%

5%

15%

15%

20%

20%

25%

25% 30%

10%

10%

To Change/Improve the Look

More horsepower/Go Faster

To Restore to Original or Near Original Condition

To Save Money

For Better Reliability

Improve handling

For Improved Safety

To Change/Improve the Look

More horsepower/Go Faster

To Restore to Original or Near Original Condition

Improve handling

For Better Reliability

Other

Other

To Save Money

For Improved Safety

To Personalize

To Personalize

15.2

19.6

8.7

11.8

11.2

6.9

4.4

20.3

24.0

10.4

8.4

8.4

14.8

15.3

8.0

6.8

3.4

0.5

Restyling Niche

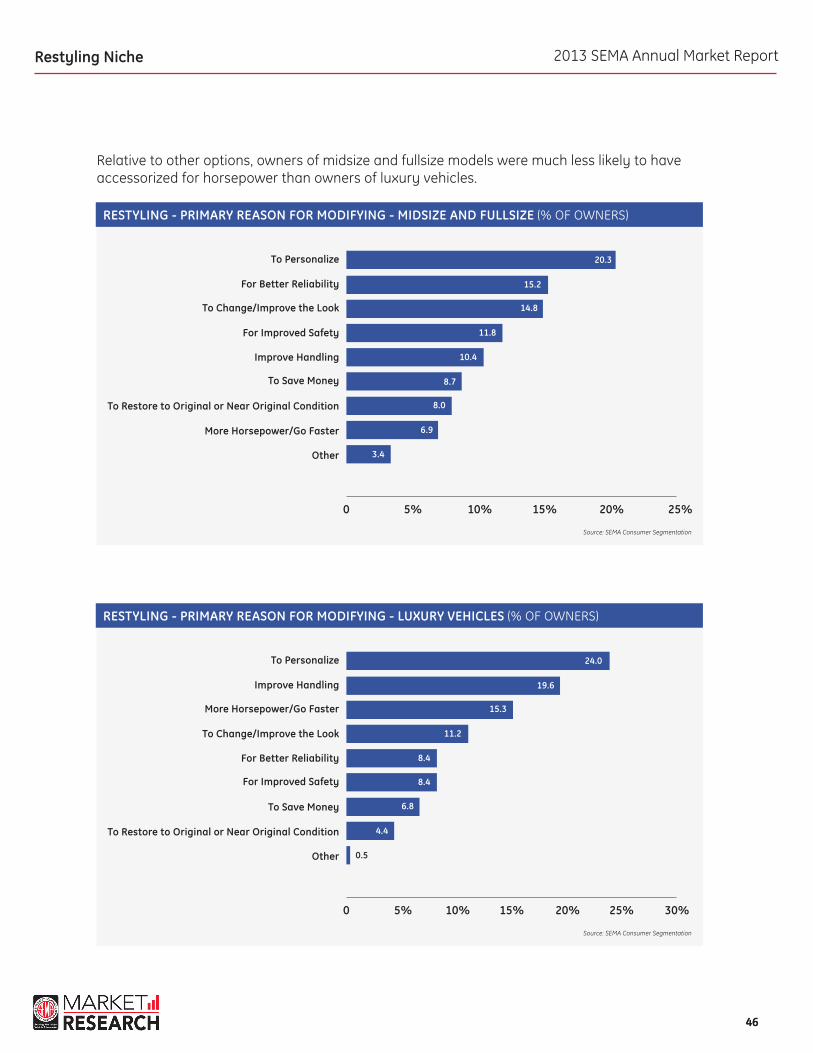

Relative to other options, owners of midsize and fullsize models were much less likely to have accessorized for horsepower than owners of luxury vehicles.

Source: SEMA Consumer Segmentation

Source: SEMA Consumer Segmentation

2013 SEMA Annual Market Report

4747

SEMA ShOW VEhICLES—RESTYLING

2010 2011 2012

BMW M3BMW 3-SeriesBentley ContinentalLamborghini GallardoBMW M5

Bentley ContinentalLexus ISMercedes Benz CLLexus GSLamborghini Murcielago

Mercedes-Benz C-ClassChrysler 300Ford FocusFord FusionCadillac CTS

8650393421

116655

17151210

9Source: SEMA

TOP 5 MODELS

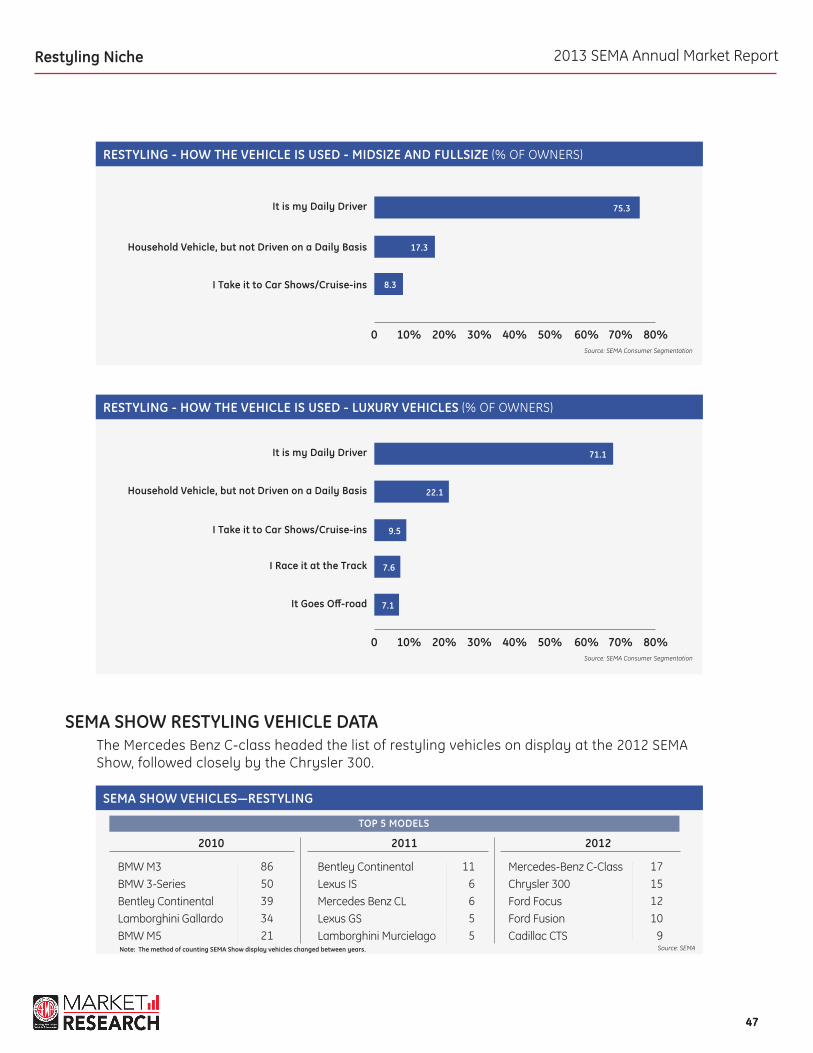

SEMA SHOW RESTYLING VEHICLE DATAThe Mercedes Benz C-class headed the list of restyling vehicles on display at the 2012 SEMA Show, followed closely by the Chrysler 300.

Note: The method of counting SEMA Show display vehicles changed between years.

Restyling Niche

Source: SEMA Consumer Segmentation

Source: SEMA Consumer Segmentation

RESTYLING - hOW ThE VEhICLE IS USED - MIDSIzE AND FULLSIzE (% OF OWNERS)

RESTYLING - hOW ThE VEhICLE IS USED - LUxURY VEhICLES (% OF OWNERS)

0

0

10%

10%

30%

30%

40%

40%

50%

50%

60%

60%

70%

70%

80%

80%

20%

20%

household Vehicle, but not Driven on a Daily Basis

household Vehicle, but not Driven on a Daily Basis

It Goes Off-road

It is my Daily Driver

It is my Daily Driver

I Race it at the Track

I Take it to Car Shows/Cruise-ins

I Take it to Car Shows/Cruise-ins

75.3

71.1

7.6

17.3

22.1

7.1

8.3

9.5

2013 SEMA Annual Market Report

4848

Acura TLAcura TSXAudi A3Audi A6Audi A8BMW 1-SeriesCadillac CTSChrysler 300 SeriesFord FocusFord FusionHonda AccordHyundai SonataInfiniti GInfiniti MLexus ESLexus GSLexus ISLexus LSMazda6Mercedes C-ClassMercedes CLSMercedes E-ClassMercedes S-ClassNissan AltimaNissan SentraToyota Camry

ExAMPLES OF CURRENT RESTYLING VEHICLE SALES

2008 2009 2010 2011 2012

46,76631,998

4,75911,956

2,82512,01858,77462,352

195,823147,569372,789117,357

64,18115,61864,13515,75949,43220,25552,59072,471

5,77538,57617,787

269,66899,797

436,617

33,62028,650

3,8746,7861,463

11,18238,81738,606

160,433180,671287,492120,028

47,1748,501

48,4857,430

38,07711,33434,86652,427

2,52743,07211,199

203,56882,706

356,824

34,04932,076

6,5588,6751,521

13,13245,65637,116

172,421219,219282,530196,623

58,14314,61848,652

7,05934,12912,27535,66258,785

2,13560,92213,608

229,26394,065

327,804

31,23730,935

6,56111,124

5,7008,832

55,04236,285

175,717248,067235,625225,961

58,24610,81840,873

3,74629,669

9,56835,71169,314

5,66562,73612,258

268,981114,991308,510

33,57228,865

7,20518,998

6,0027,689

46,97970,747

245,922241,263331,872230,605

59,8449,130

56,15822,16027,708

8,34533,75681,697

8,06565,17111,794

302,934106,395404,886

Sources: Ward’s Auto, SEMA

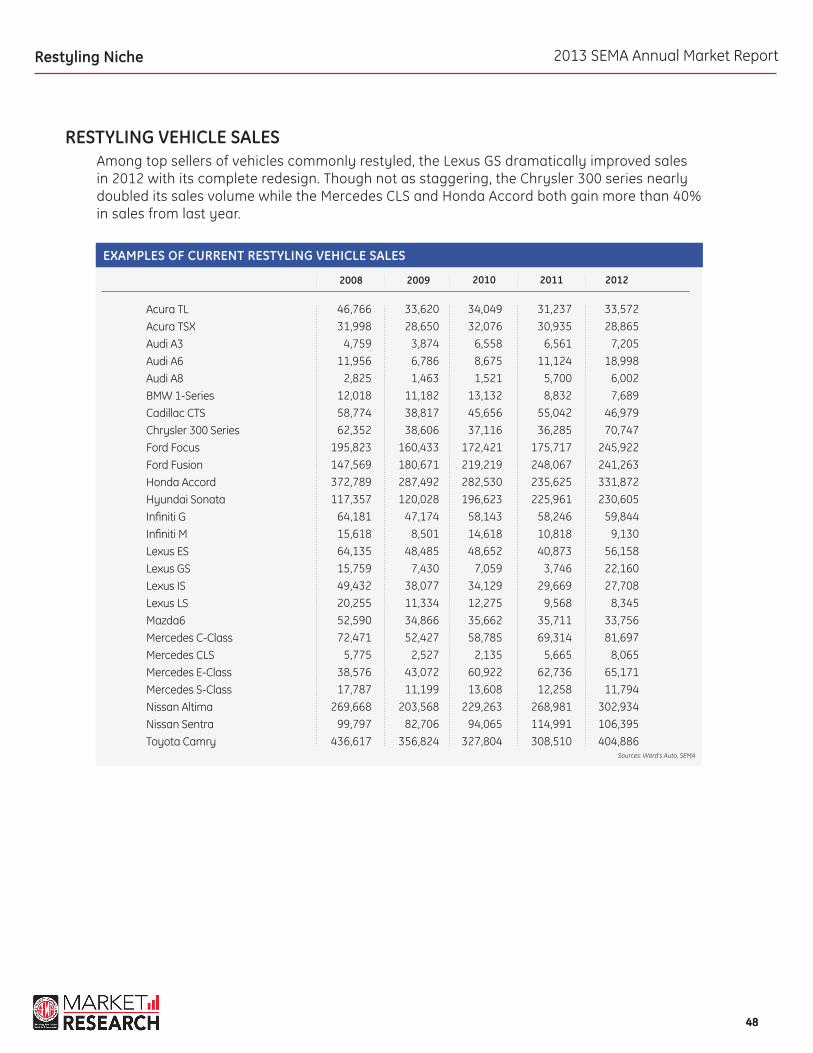

RESTYLING VEHICLE SALESAmong top sellers of vehicles commonly restyled, the Lexus GS dramatically improved sales in 2012 with its complete redesign. Though not as staggering, the Chrysler 300 series nearly doubled its sales volume while the Mercedes CLS and Honda Accord both gain more than 40% in sales from last year.

Restyling Niche

2013 SEMA Annual Market Report

4949

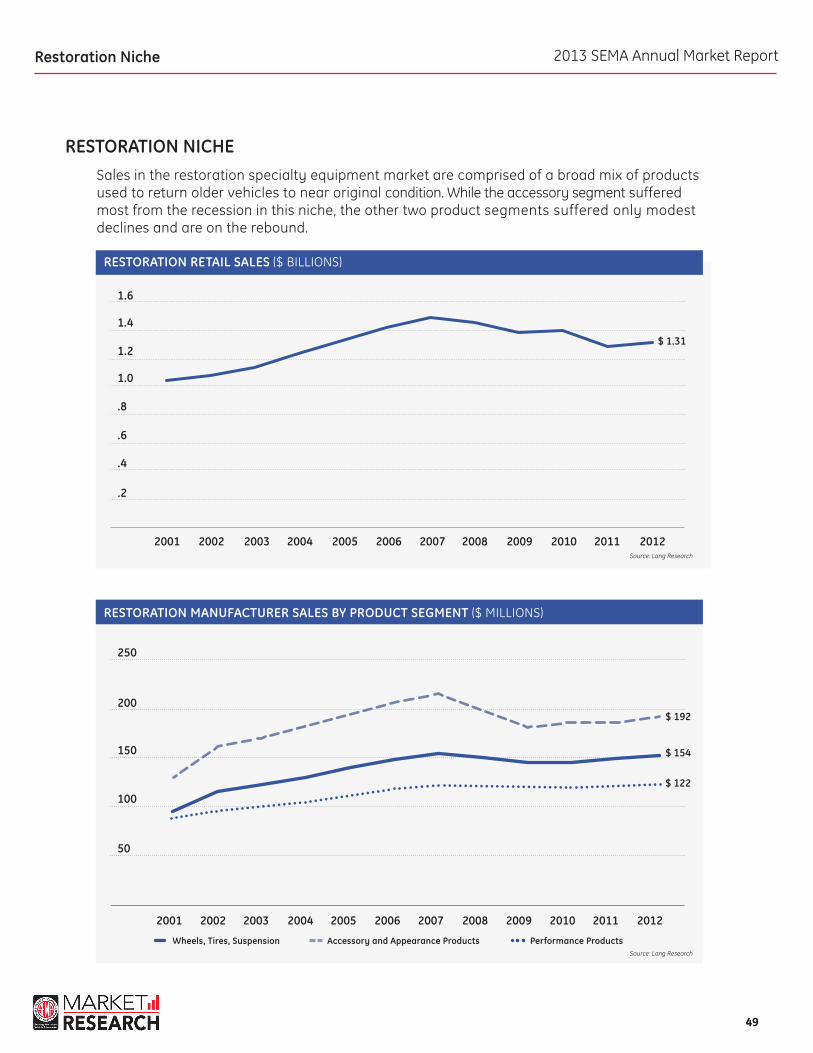

RESTORATION NICHESales in the restoration specialty equipment market are comprised of a broad mix of products used to return older vehicles to near original condition. While the accessory segment suffered most from the recession in this niche, the other two product segments suffered only modest declines and are on the rebound.

Restoration Niche

RESTORATION RETAIL SALES ($ BILLIONS)

RESTORATION MANUFACTURER SALES BY PRODUCT SEGMENT ($ MILLIONS)

2001

2004

2005

20092008

2009

2002

2003

2006

2007

2011

2011

2001

2002

2005

2006

2010

2010

2003

2004

2007

2008

2012

2012

.4

.8

.2

50

100

150

200

250

.6

1.0

1.2

1.4

1.6

$ 1.31

$ 122

$ 154

$ 192

Source: Lang Research

Source: Lang Research

Performance ProductsWheels, Tires, Suspension Accessory and Appearance Products

2013 SEMA Annual Market Report

5050

Restoration Niche

RESTORATION SALES CHANNEL (% OF VOLUME)

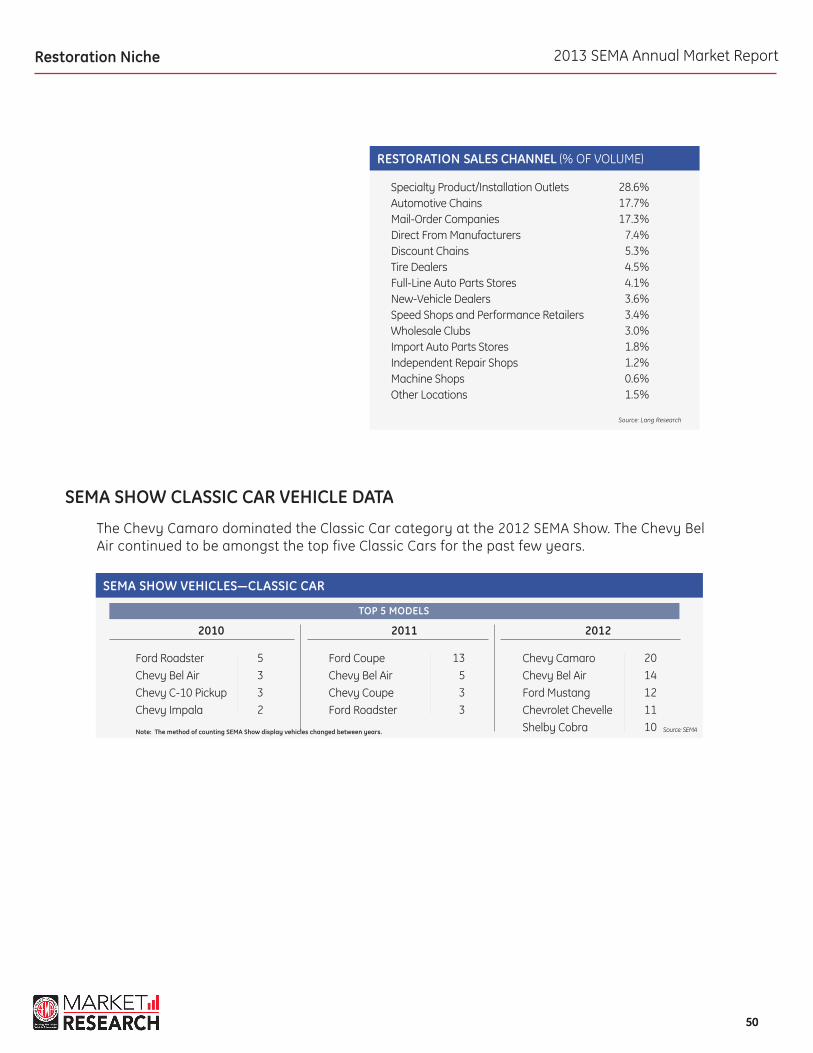

Specialty Product/Installation Outlets Automotive Chains Mail-Order CompaniesDirect From Manufacturers Discount Chains Tire Dealers Full-Line Auto Parts Stores New-Vehicle Dealers Speed Shops and Performance RetailersWholesale Clubs Import Auto Parts Stores Independent Repair Shops Machine Shops Other Locations

28.6%17.7%17.3%

7.4%5.3%4.5%4.1%3.6%3.4%3.0%1.8%1.2%0.6%1.5%

Source: Lang Research

SEMA SHOW CLASSIC CAR VEHICLE DATA

The Chevy Camaro dominated the Classic Car category at the 2012 SEMA Show. The Chevy Bel Air continued to be amongst the top five Classic Cars for the past few years.

SEMA ShOW VEhICLES—CLASSIC CAR

2010 2011 2012

Ford RoadsterChevy Bel AirChevy C-10 PickupChevy Impala

Ford CoupeChevy Bel AirChevy CoupeFord Roadster

Chevy CamaroChevy Bel AirFord MustangChevrolet ChevelleShelby Cobra

5332

13533

2014121110 Source: SEMA

TOP 5 MODELS

Note: The method of counting SEMA Show display vehicles changed between years.

2013 SEMA Annual Market Report

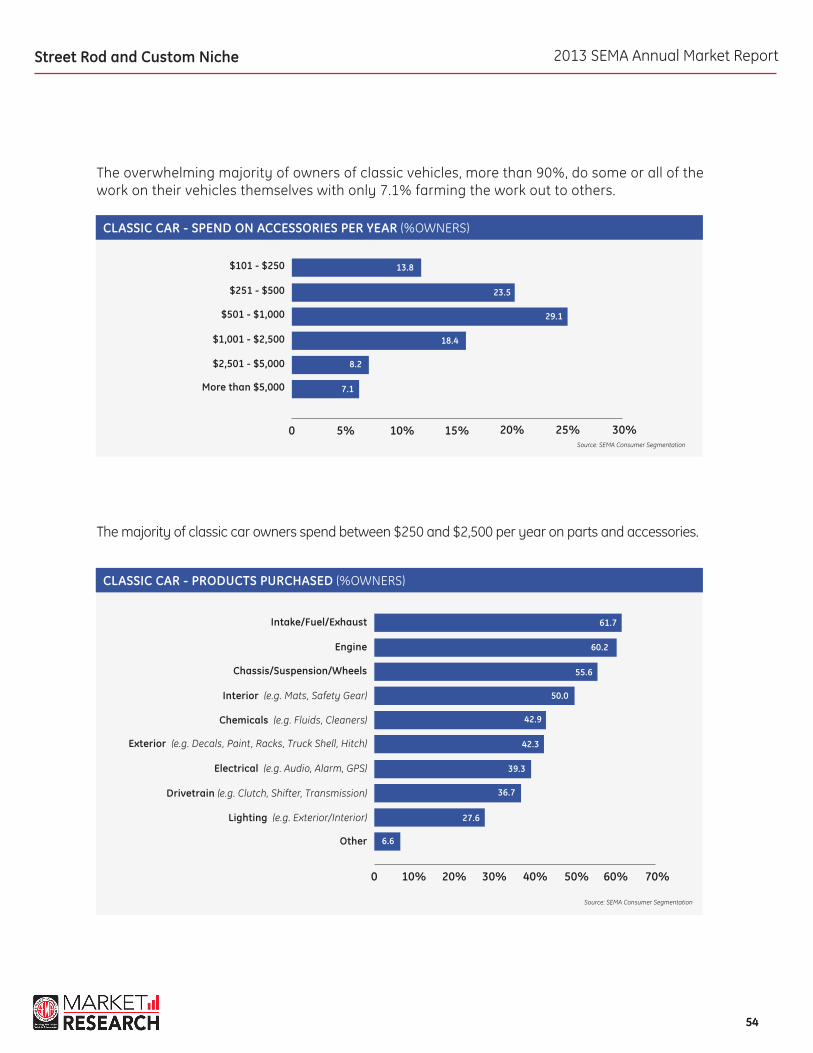

5151

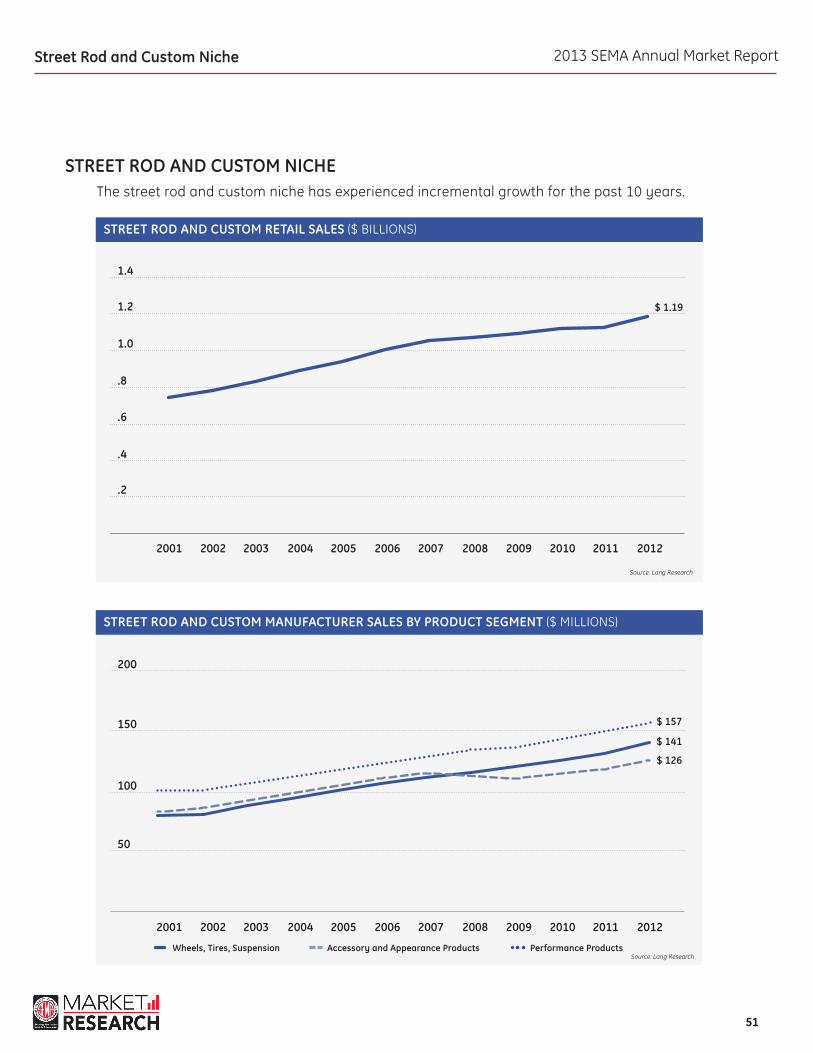

STREET ROD AND CUSTOM NICHEThe street rod and custom niche has experienced incremental growth for the past 10 years.

Street Rod and Custom Niche

STREET ROD AND CUSTOM RETAIL SALES ($ BILLIONS)

STREET ROD AND CUSTOM MANUFACTURER SALES BY PRODUCT SEGMENT ($ MILLIONS)

2001

2001

2005

2005

2009

2009

2003

2003

2007

2007

2011

2011

2002

2002

2006

2006

2010

2010

2004

2004

2008

2008

2012

2012

.4