2011 Chicago Ebig Mtg Staneski

54

Equity-Based Insurance Guarantees Conference November 14-15, 2011 Chicago, IL The Risk-Neutral World Paul Staneski

-

Upload

abhishek-puri -

Category

Documents

-

view

5 -

download

0

Transcript of 2011 Chicago Ebig Mtg Staneski

Equity-Based Insurance Guarantees Conference November 14-15, 2011

Chicago, IL

The Risk-Neutral World

Paul Staneski

1

The Risk-Neutral WorldThe Risk-Neutral WorldThe meaning of risk-neutral valuation and what it says about risk-neutral scenarios.

P l G St ki Ph DPaul G. Staneski, Ph.D.Managing Director, Credit SuisseChicago, November 14, 2011 (1500 Hrs – 1545 Hrs)

2

Q ti f SOA M bQuestion from SOA Member

2

2

3

Q tiQuestion

The 3m 185 Call on IBM is priced at $9 Is thisThe 3m 185 Call on IBM is priced at $9. Is this …

• A. The risk-neutral price?

B The real world (risk averse) price?• B. The real-world (risk-averse) price?

• C. Huh? I thought this was a wine-tasting event!

3

3

4

B t d th B tBeauty and the Beast

The risk-neutral valuation argument for derivatives isThe risk neutral valuation argument for derivatives is both a beautiful and powerful result.

That said its sheer brilliance (like that of the Sun) blinds That said, its sheer brilliance (like that of the Sun) blinds us to some deeper truths and beauty (like the Sun’s Corona).

… and often leads us astray as well!

4

4

5

St k PStock Process

A stock is priced at 90 and in one year will be either 120A stock is priced at 90 and in one year will be either 120 or 80, with probabilities p = 70% and 30%, respectively.

12070%

90

8030%

Assume interest rates and dividends are both zero.

80

5

5

6

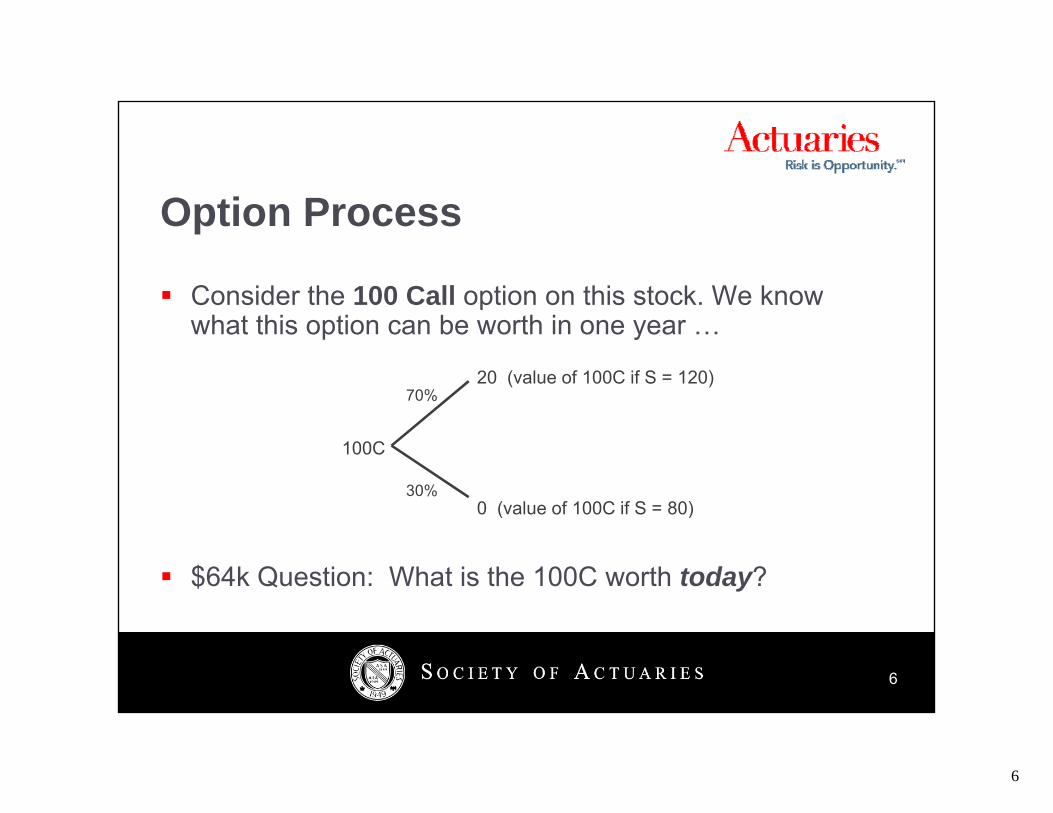

O ti POption Process

Consider the 100 Call option on this stock. We knowConsider the 100 Call option on this stock. We know what this option can be worth in one year …

20 (value of 100C if S = 120)70%

100C

0 (value of 100C if S = 80)30%

$64k Question: What is the 100C worth today?

0 (value of 100C if S = 80)

6

6

7

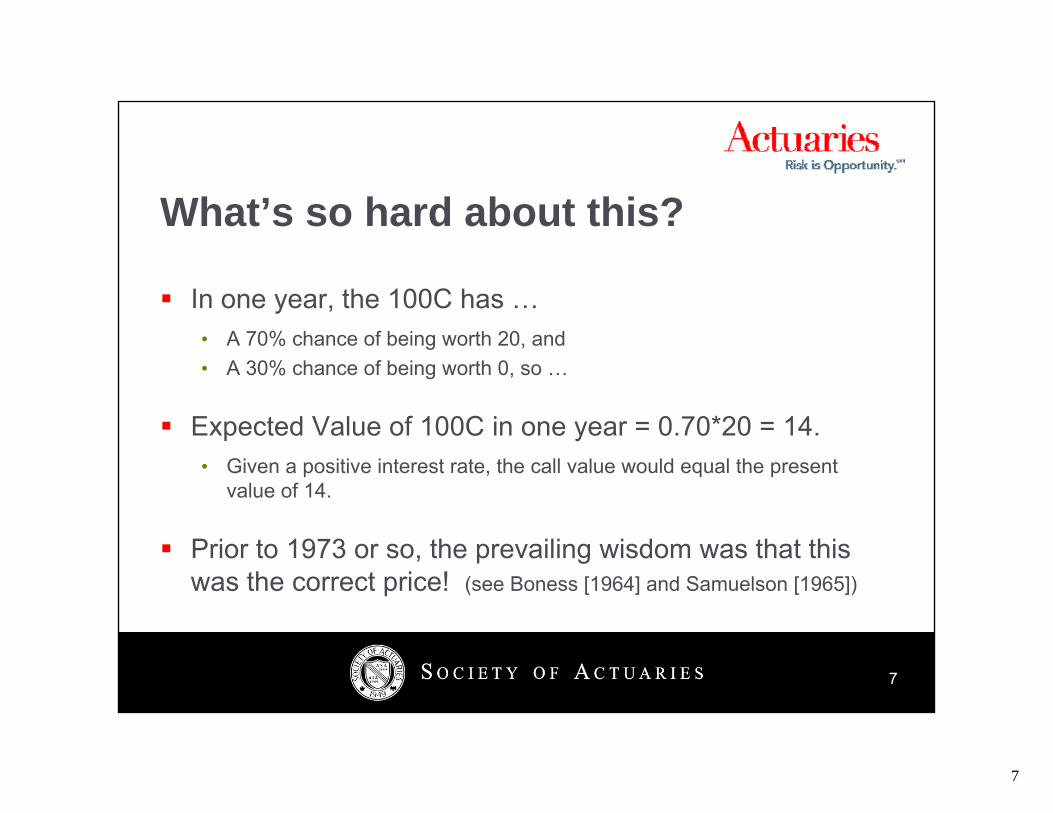

Wh t’ h d b t thi ?What’s so hard about this?

In one year the 100C hasIn one year, the 100C has …• A 70% chance of being worth 20, and• A 30% chance of being worth 0, so …

Expected Value of 100C in one year = 0.70*20 = 14.• Given a positive interest rate, the call value would equal the present

value of 14.

Prior to 1973 or so, the prevailing wisdom was that this was the correct price! (see Boness [1964] and Samuelson [1965])

7

7

8

L t’ t dLet’s trade

I’ll sell you the 100C for 10I ll sell you the 100C for 10.

Do you want to buy it?

Of course you do – I’m selling it “cheap” !

8

8

9

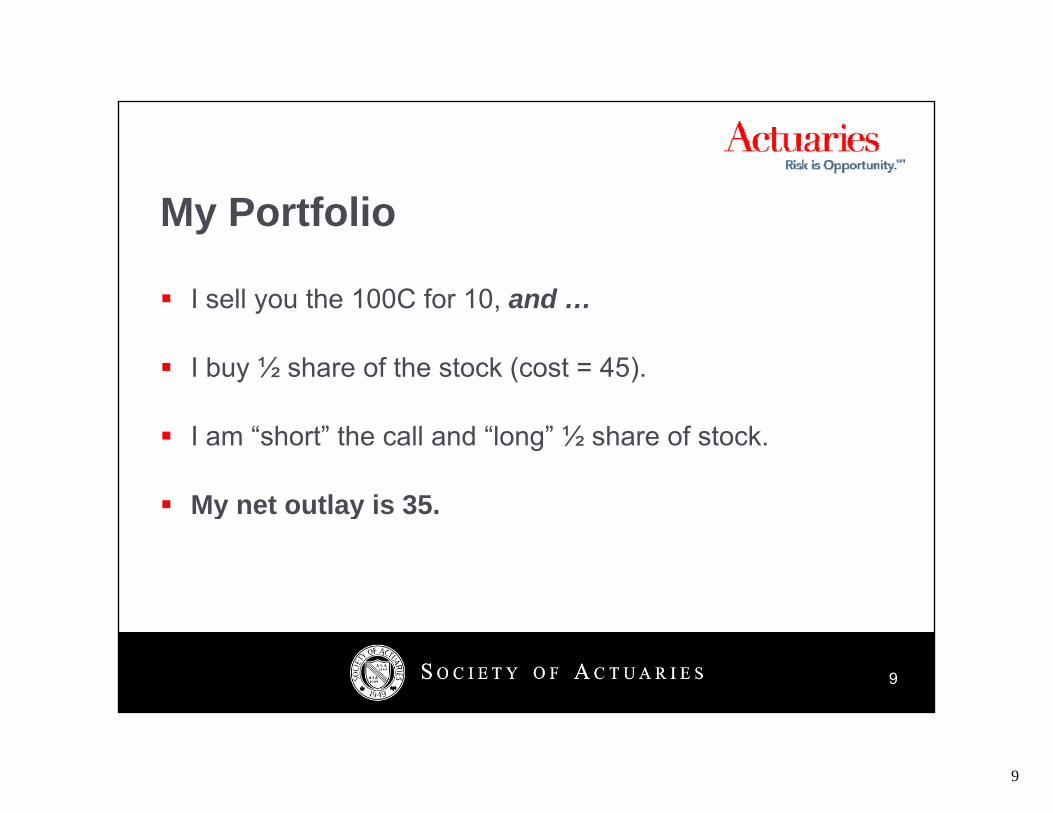

M P tf liMy Portfolio

I sell you the 100C for 10 and …I sell you the 100C for 10, and …

I buy ½ share of the stock (cost = 45).

I am “short” the call and “long” ½ share of stock.

My net outlay is 35My net outlay is 35.

9

9

10

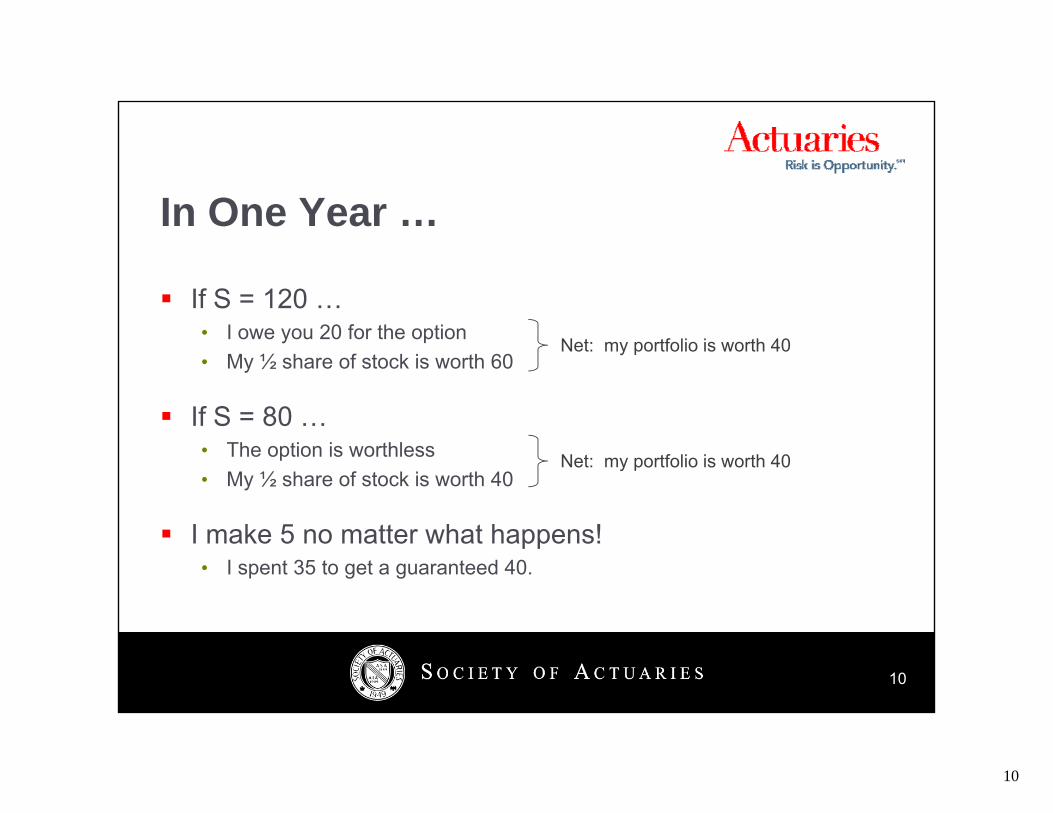

I O YIn One Year …

If S = 120If S 120 …• I owe you 20 for the option• My ½ share of stock is worth 60

If S 80

Net: my portfolio is worth 40

If S = 80 …• The option is worthless• My ½ share of stock is worth 40

Net: my portfolio is worth 40

I make 5 no matter what happens!• I spent 35 to get a guaranteed 40.

10

10

11

O ti V lOption Value

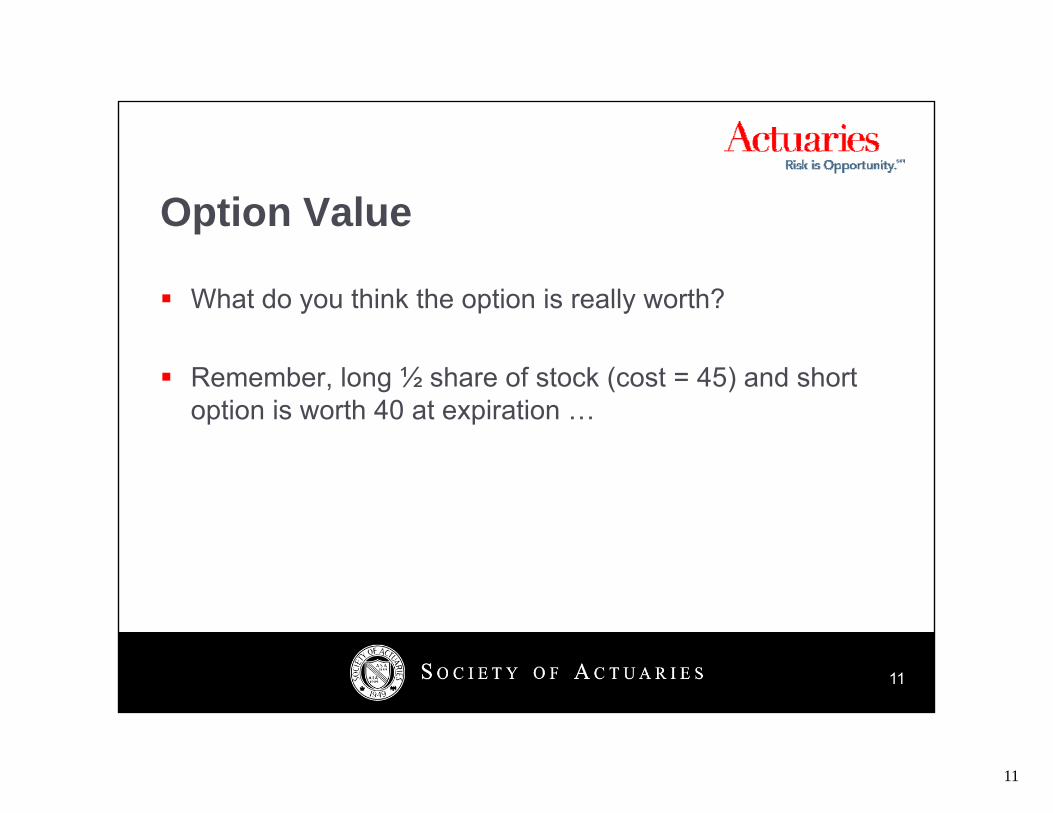

What do you think the option is really worth?What do you think the option is really worth?

Remember, long ½ share of stock (cost = 45) and short option is worth 40 at expirationoption is worth 40 at expiration …

11

11

12

N A bit P iNo-Arbitrage Price

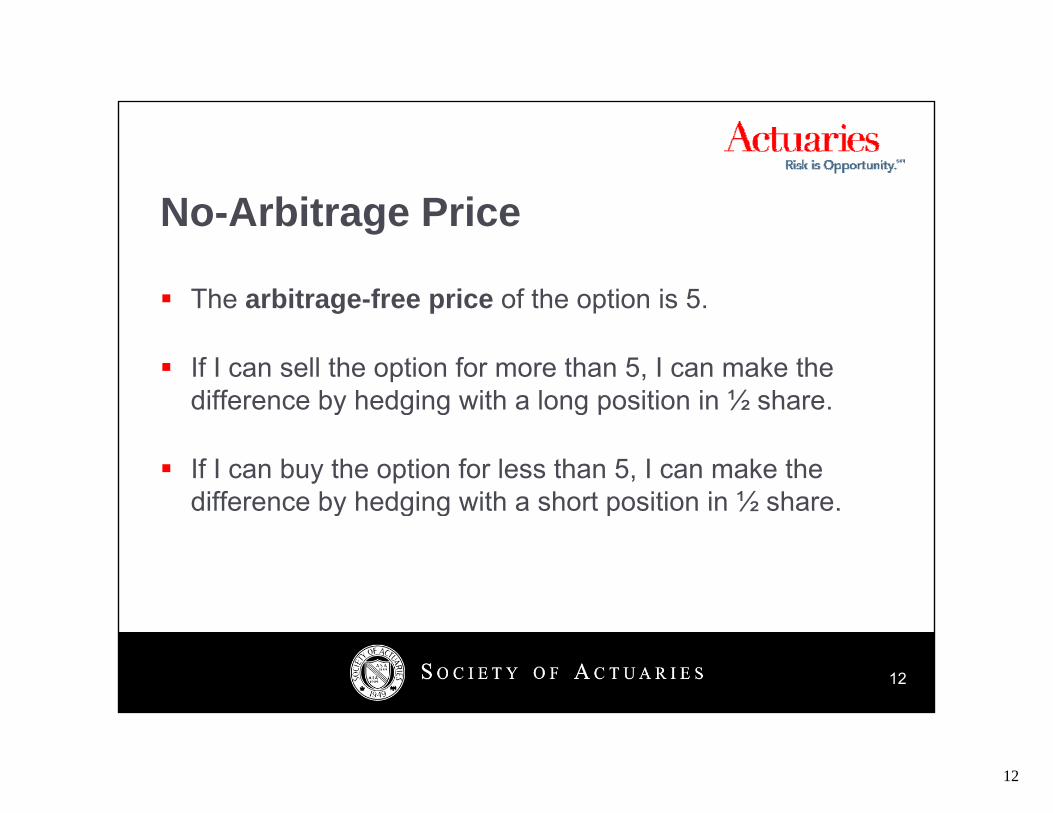

The arbitrage-free price of the option is 5The arbitrage free price of the option is 5.

If I can sell the option for more than 5, I can make the difference by hedging with a long position in ½ share.difference by hedging with a long position in ½ share.

If I can buy the option for less than 5, I can make the difference by hedging with a short position in ½ share.difference by hedging with a short position in ½ share.

12

12

13

Ri k F P tf liRisk-Free Portfolio

A portfolio that is short the option and long ½ share ofA portfolio that is short the option and long ½ share of stock is certain to be worth 40 at expiration …

60 – 20 = 40

Value of portfolio today = 45 – C

40 0 40

The value today must = 40 45 – C = 40 C = 5.

40 – 0 = 40

13

13

14

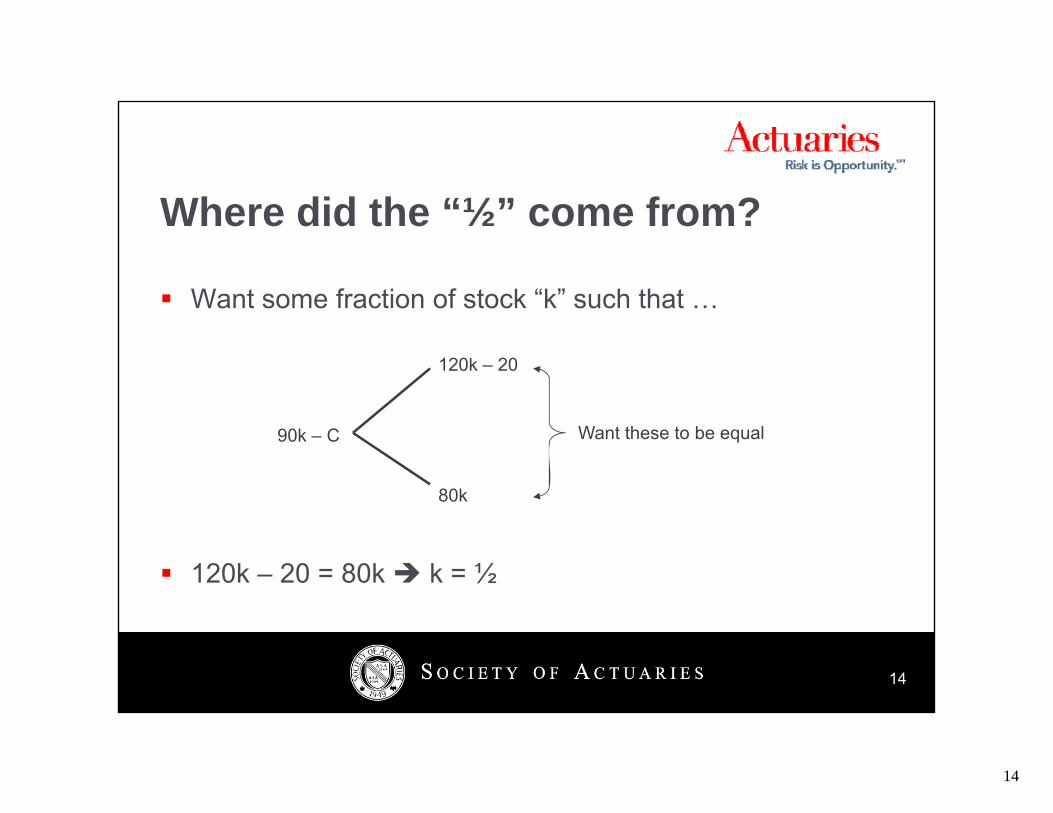

Wh did th “½” f ?Where did the “½” come from?

Want some fraction of stock “k” such thatWant some fraction of stock k such that …

120k – 20

90k – C

80k

Want these to be equal

120k – 20 = 80k k = ½

14

14

15

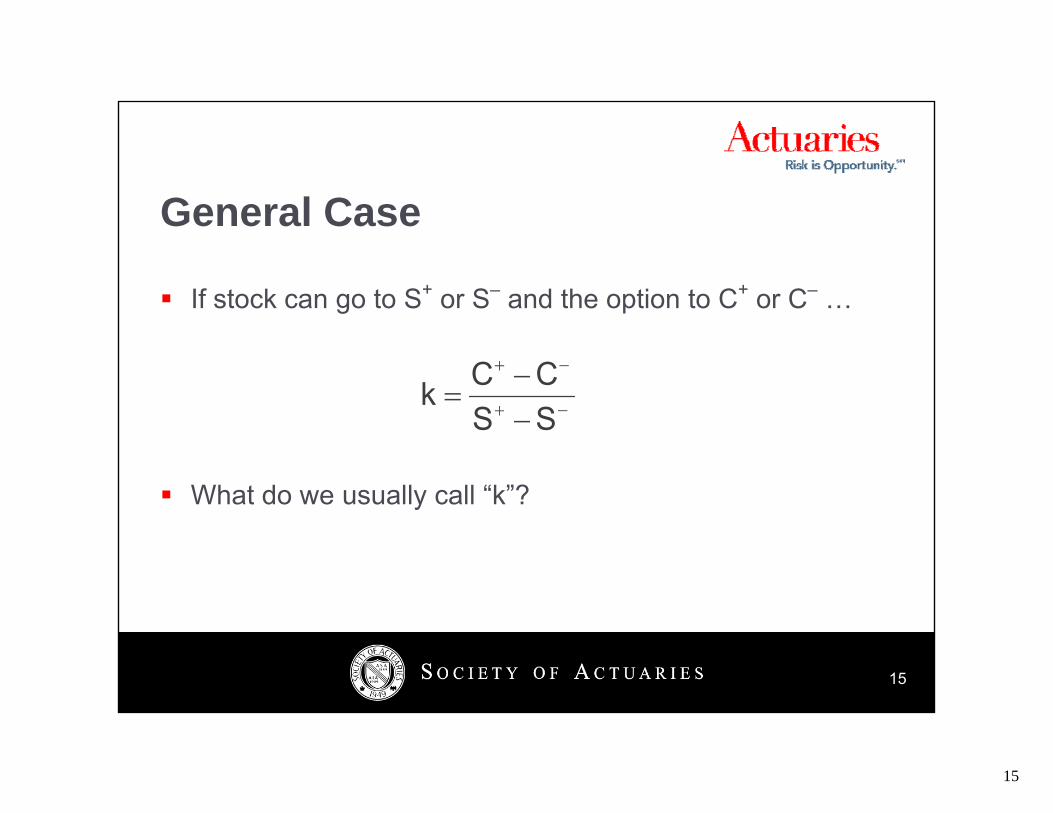

G l CGeneral Case

If stock can go to S+ or S– and the option to C+ or C–If stock can go to S or S and the option to C or C …

SSCCk

What do we usually call “k”?

SS

y

15

15

16

T A i Ob tiTwo Amazing Observations

1 We arrived at the 5 call value without using the 70%1. We arrived at the 5 call value without using the 70% probability; in fact, we get 5 regardless of the probability “p” that stock goes up!• That is the expected growth rate of the stock is immaterial to the valueThat is, the expected growth rate of the stock is immaterial to the value

of the option.

2 We also made no appeal to (or use of) the risk2. We also made no appeal to (or use of) the risk preferences of the investor.

16

16

17

Bl k S h l i N t h llBlack-Scholes in a Nutshell

17

17

18

Wh t t id !What a great idea!

Ed Thorp (b 1932 Ph D mathematician gambler andEd Thorp (b. 1932, Ph.D. mathematician, gambler, and hedge fund manager extraordinaire) first derived this “hedging” result in the mid 60s.

• See “Beat the Market” by Thorp & Kassouf (1967)

• Read “Fortune’s Formula” by William Poundstone.

18

18

19

BSMBSM

Robert Merton Fischer Black and Myron ScholesRobert Merton, Fischer Black, and Myron Scholes derived the call value in the early 70s.• Explicitly made the risk-free rate the appropriate discount rate.• Did not fully appreciate the hedging arguments embedded in theirDid not fully appreciate the hedging arguments embedded in their

“mathematical” result.• Fischer Black and Myron Scholes, “The Pricing of Options and Corporate

Liabilities”, Journal of Political Economy, 81, (May-June 1973), pp. 637-659.659.

• Scholes and Merton win 1997 Nobel Prize in Economics (Black died in 1995).

19

19

20

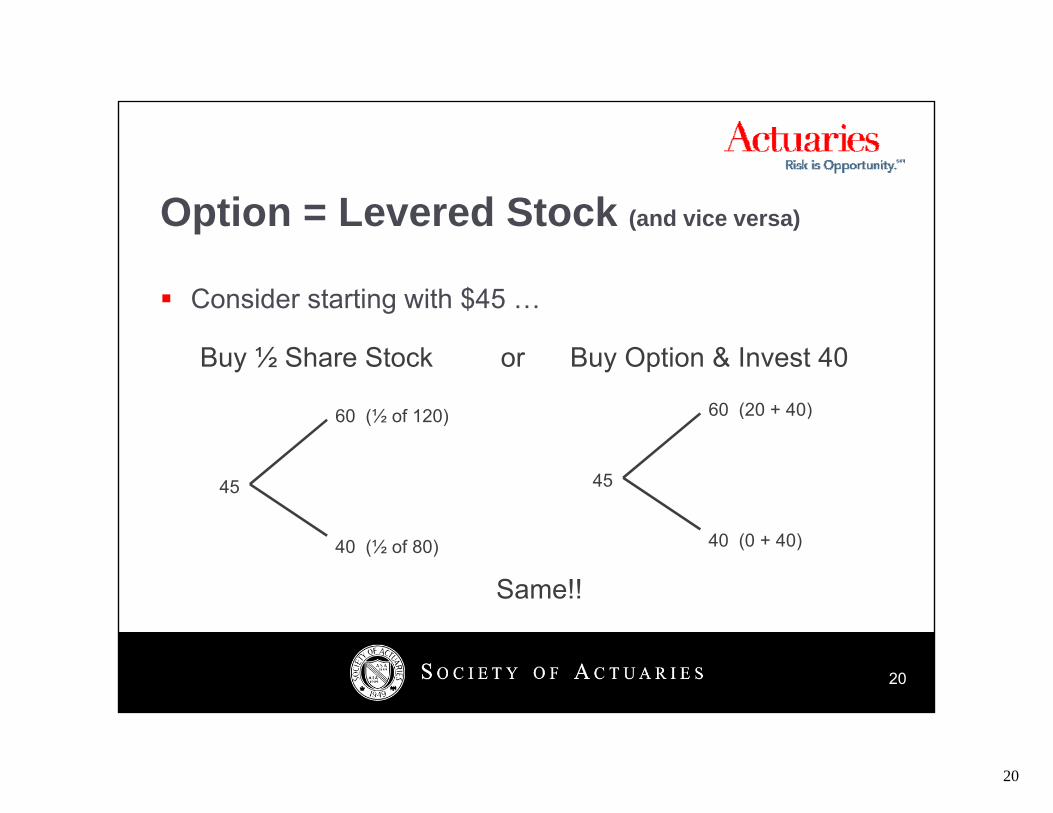

O ti L d St kOption = Levered Stock (and vice versa)

Consider starting with $45Consider starting with $45 …

Buy ½ Share Stock or Buy Option & Invest 40

60 (20 + 40)

45

60 (½ of 120)

45

60 (20 + 40)

40 (½ of 80) 40 (0 + 40)

Same!!

20

20

21

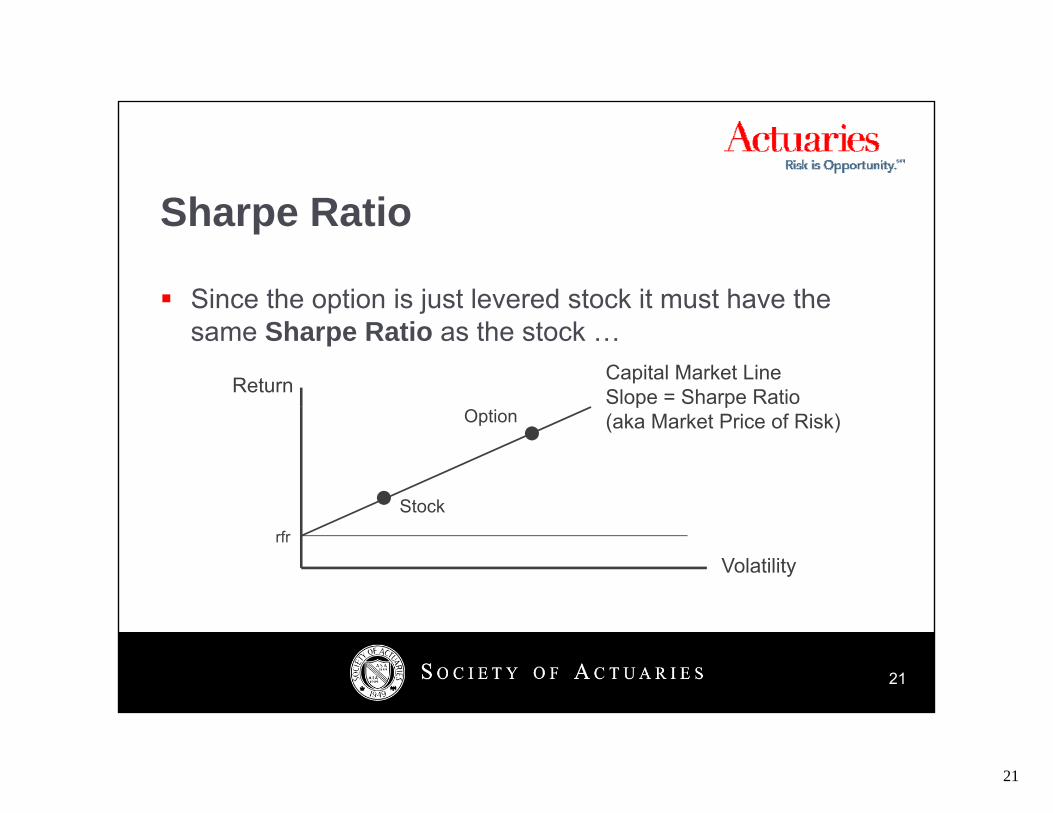

Sh R tiSharpe Ratio

Since the option is just levered stock it must have theSince the option is just levered stock it must have the same Sharpe Ratio as the stock …

Return Capital Market LineSlope = Sharpe Ratiop p(aka Market Price of Risk)

••

Stock

Option

Volatilityrfr

Stock

21

21

22

Sh R ti O ti V lSharpe Ratio Option Value

It is simple enough to solve for the value of the optionIt is simple enough to solve for the value of the option that has the same Sharpe Ratio as the stock.

• In our example, the Sharpe Ratio of the stock is 0.98.

• This implies the 100C must be worth 5.

22

22

23

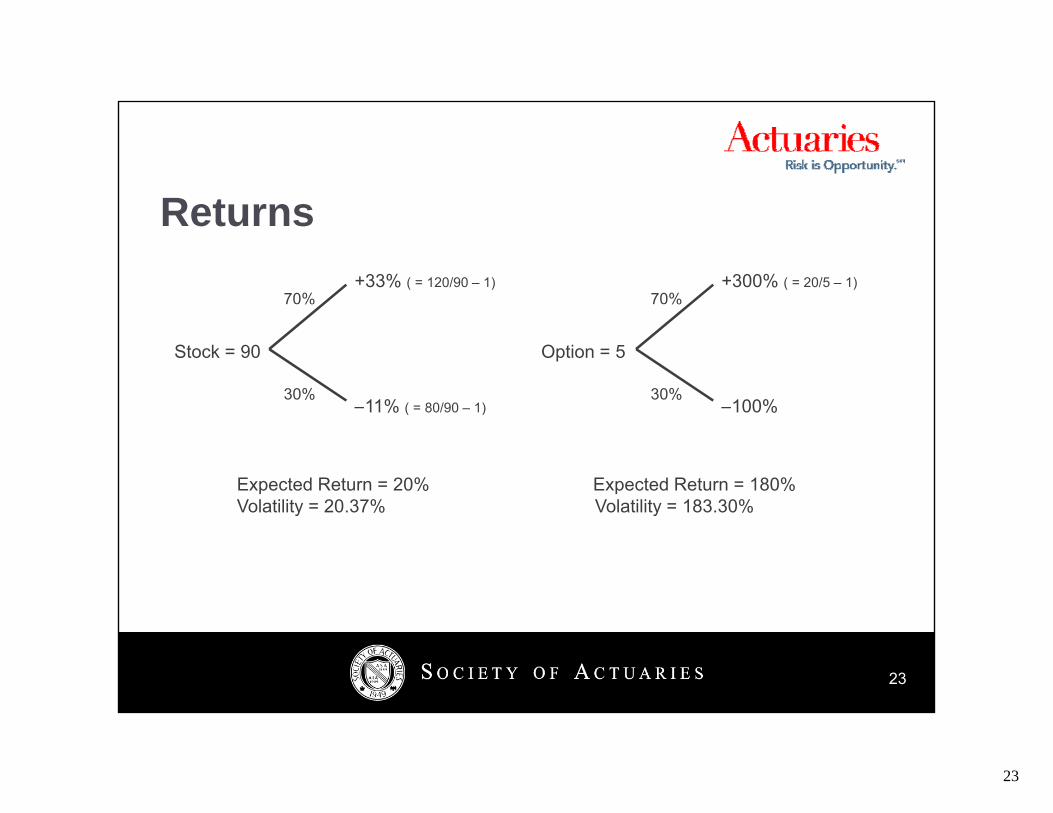

R tReturns+300% ( = 20/5 – 1)

70%+33% ( = 120/90 – 1)

70%

Option = 5

100%30%

Stock = 90

11% ( = 80/90 1)30%

–100%–11% ( = 80/90 – 1)

Expected Return = 20% Expected Return = 180%Volatility = 20 37% Volatility = 183 30%Volatility 20.37% Volatility 183.30%

23

23

24

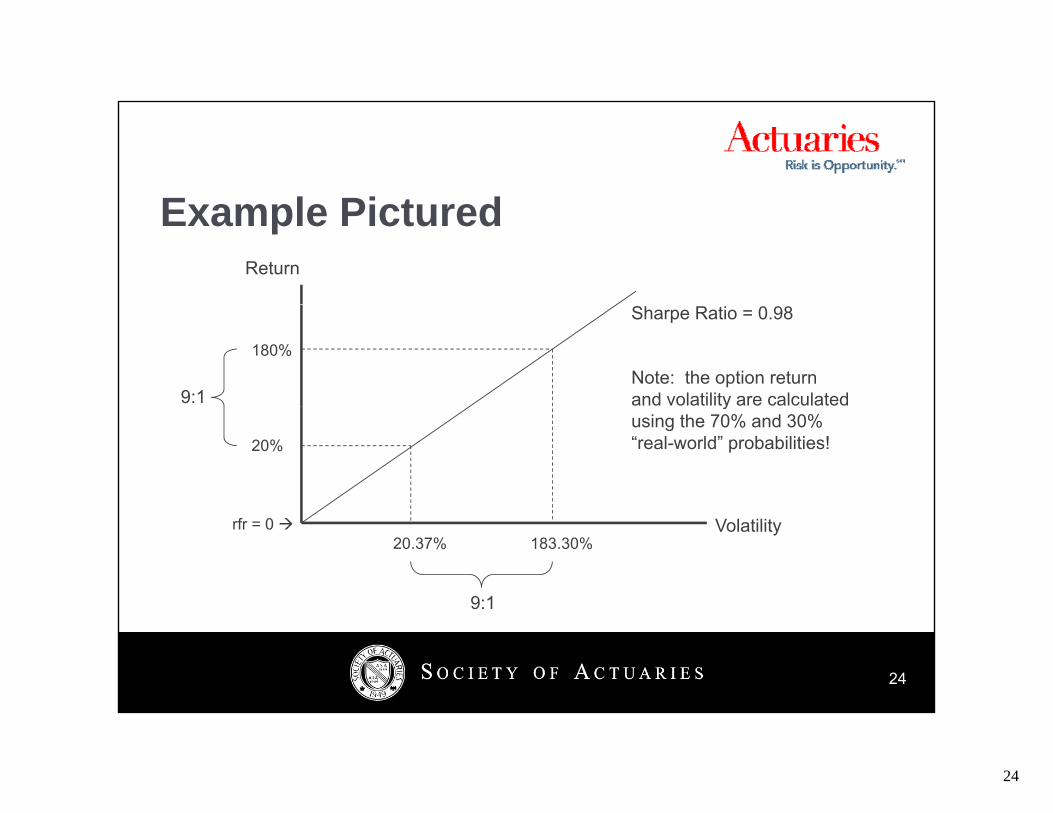

E l Pi t dExample PicturedReturn

180%

Sharpe Ratio = 0.98

Note: the option returnand volatility are calculated9:1

20%

yusing the 70% and 30%“real-world” probabilities!

Volatility20.37% 183.30%

rfr = 0

9:1

24

24

25

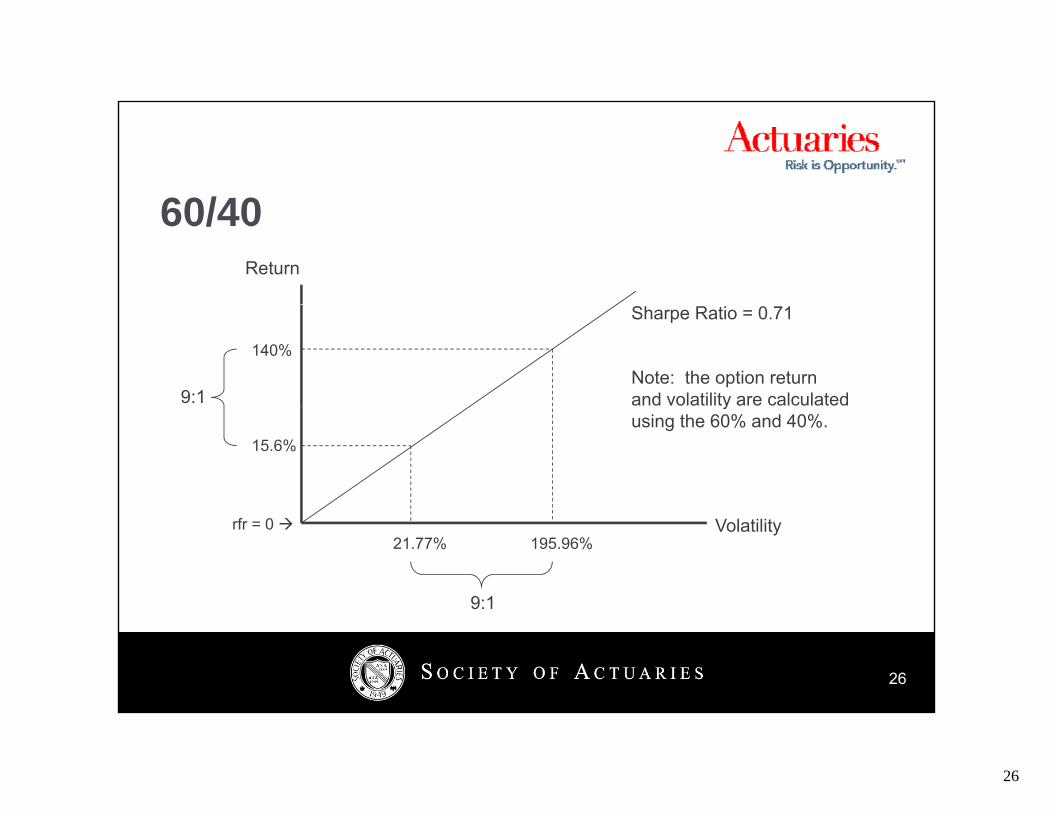

Diff t P b bilitiDifferent Probabilities

What if the probabilities were 60% and 40% (instead ofWhat if the probabilities were 60% and 40% (instead of 70 and 30) …

12060%

90

60%

40%80

0%

25

25

26

60/4060/40Return

140%

Sharpe Ratio = 0.71

Note: the option returnand volatility are calculated9:1

15.6%

yusing the 60% and 40%.

Volatility21.77% 195.96%

rfr = 0

9:1

26

26

27

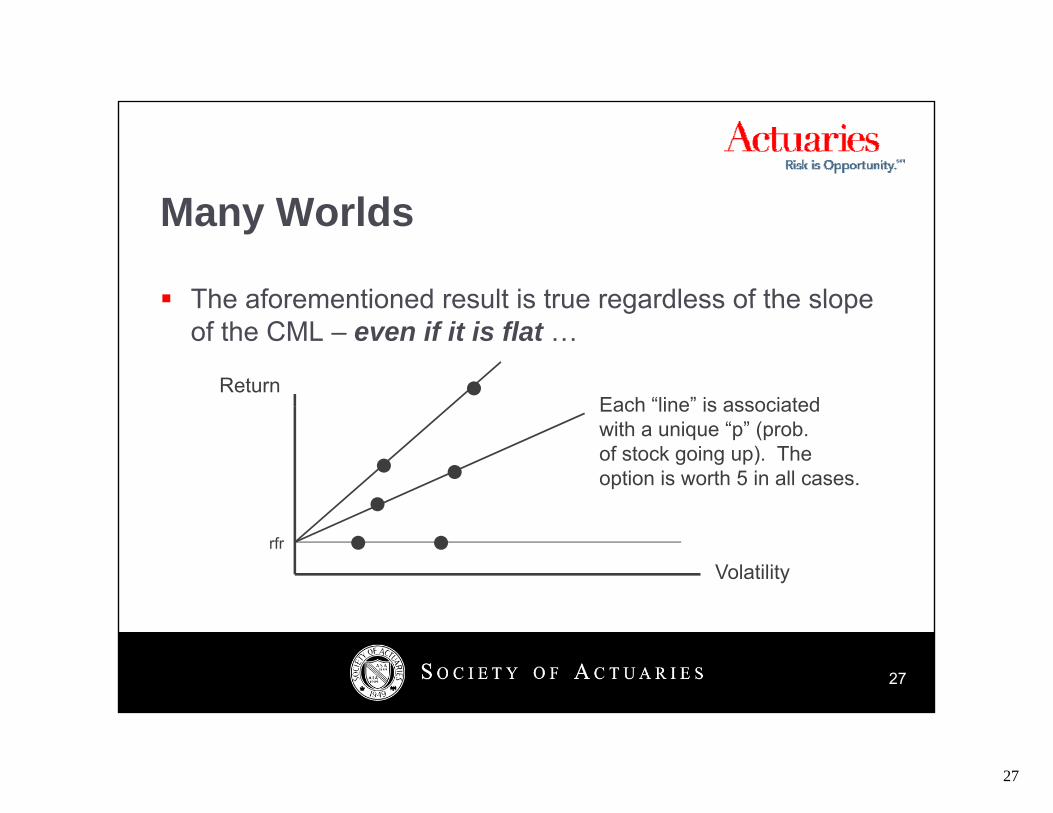

M W ldMany Worlds

The aforementioned result is true regardless of the slopeThe aforementioned result is true regardless of the slope of the CML – even if it is flat …

Return • Each “line” is associated

• ••Each line is associatedwith a unique “p” (prob.of stock going up). Theoption is worth 5 in all cases.

Volatilityrfr

•• •

27

27

28

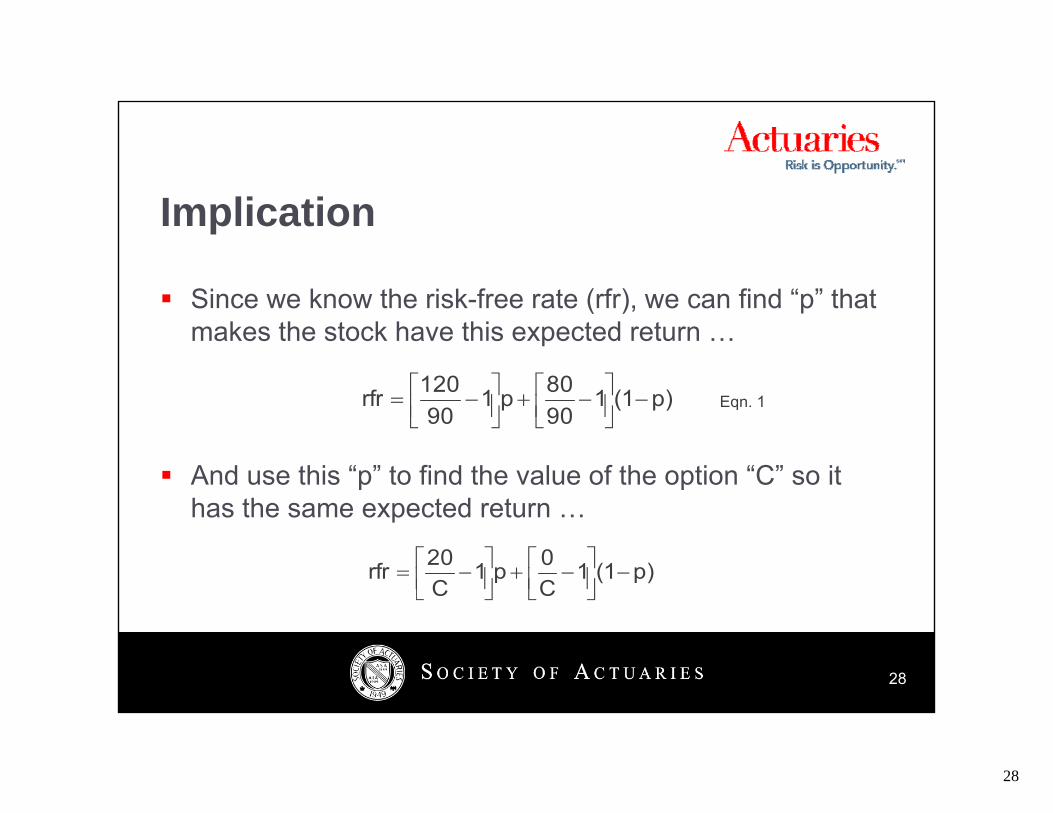

I li tiImplication

Since we know the risk-free rate (rfr) we can find “p” thatSince we know the risk free rate (rfr), we can find p that makes the stock have this expected return …

p)(1180p1120rfr

Eqn. 1

And use this “p” to find the value of the option “C” so it has the same expected return

p)(90

p90

Eqn. 1

has the same expected return …

p)(11C0p1

C20rfr

28

28

29

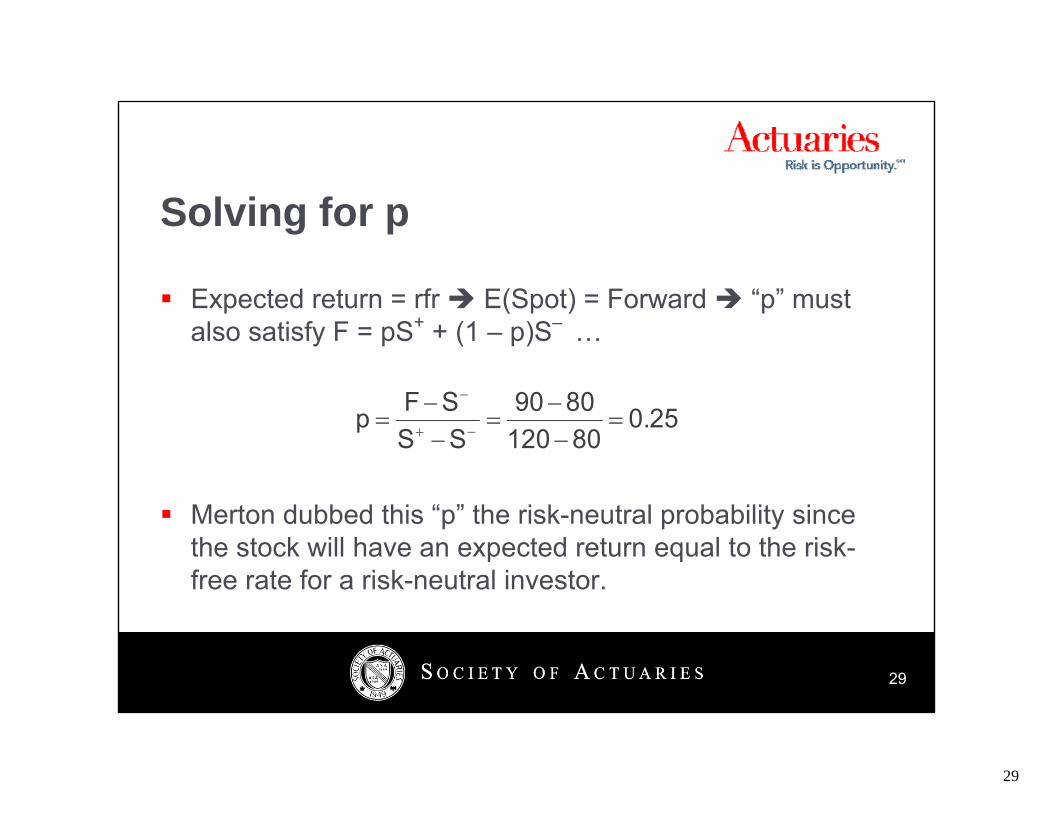

S l i fSolving for p

Expected return = rfr E(Spot) = Forward “p” mustExpected return rfr E(Spot) Forward p must also satisfy F = pS+ + (1 – p)S– …

8090SF

M t d bb d thi “ ” th i k t l b bilit i

0.25801208090

SSSFp

Merton dubbed this “p” the risk-neutral probability since the stock will have an expected return equal to the risk-free rate for a risk-neutral investor.

29

29

30

Ri k N t l P b bilitRisk-Neutral Probability

The “risk-neutral probability” is just one of an infiniteThe risk neutral probability is just one of an infinite number of choices that can be used to value the option.

It’s a convenient choice since we can derive it upon pobserving the risk-free rate.

But it also leads to a deeper observation But it also leads to a deeper observation …

30

30

31

Ri k P iRisk Premium

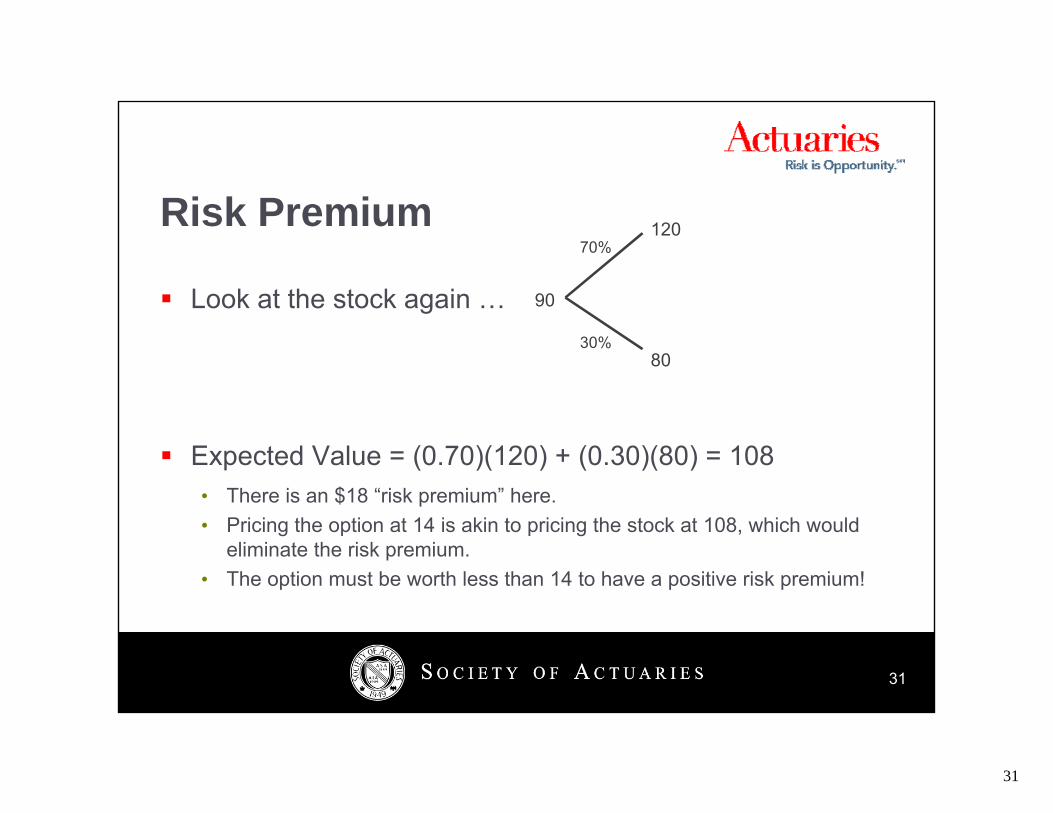

Look at the stock again 90

12070%

Look at the stock again … 90

8030%

Expected Value = (0.70)(120) + (0.30)(80) = 108• There is an $18 “risk premium” here.• Pricing the option at 14 is akin to pricing the stock at 108, which would

eliminate the risk premium.• The option must be worth less than 14 to have a positive risk premium!

31

31

32

P i d P b bilitiPrices and Probabilities

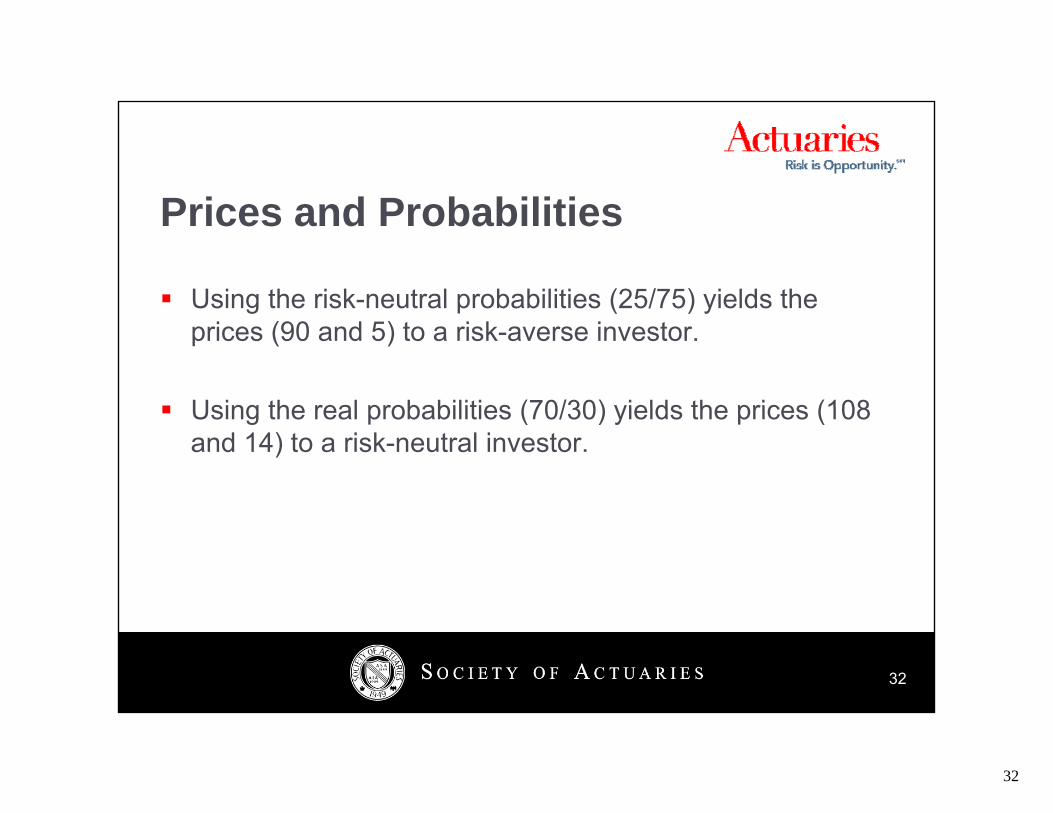

Using the risk-neutral probabilities (25/75) yields theUsing the risk neutral probabilities (25/75) yields the prices (90 and 5) to a risk-averse investor.

Using the real probabilities (70/30) yields the prices (108 Using the real probabilities (70/30) yields the prices (108 and 14) to a risk-neutral investor.

32

32

33

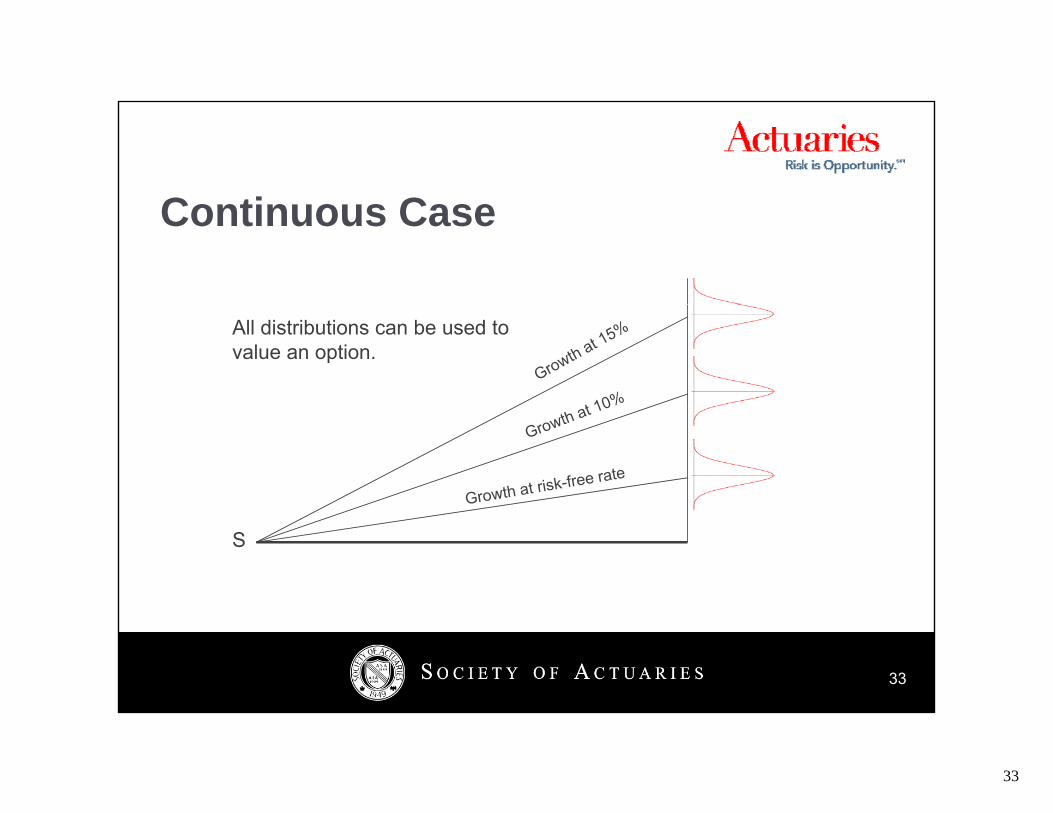

C ti CContinuous Case

All distributions can be used tovalue an option.

S

33

33

34

A th E lAnother Example [chosen with a method to the madness!]

Consider the following stock and optionConsider the following stock and option …

1.25 0

1.11

0.8333

1 Put

0.1667

Again, assume rates and dividends are zero.

34

34

35

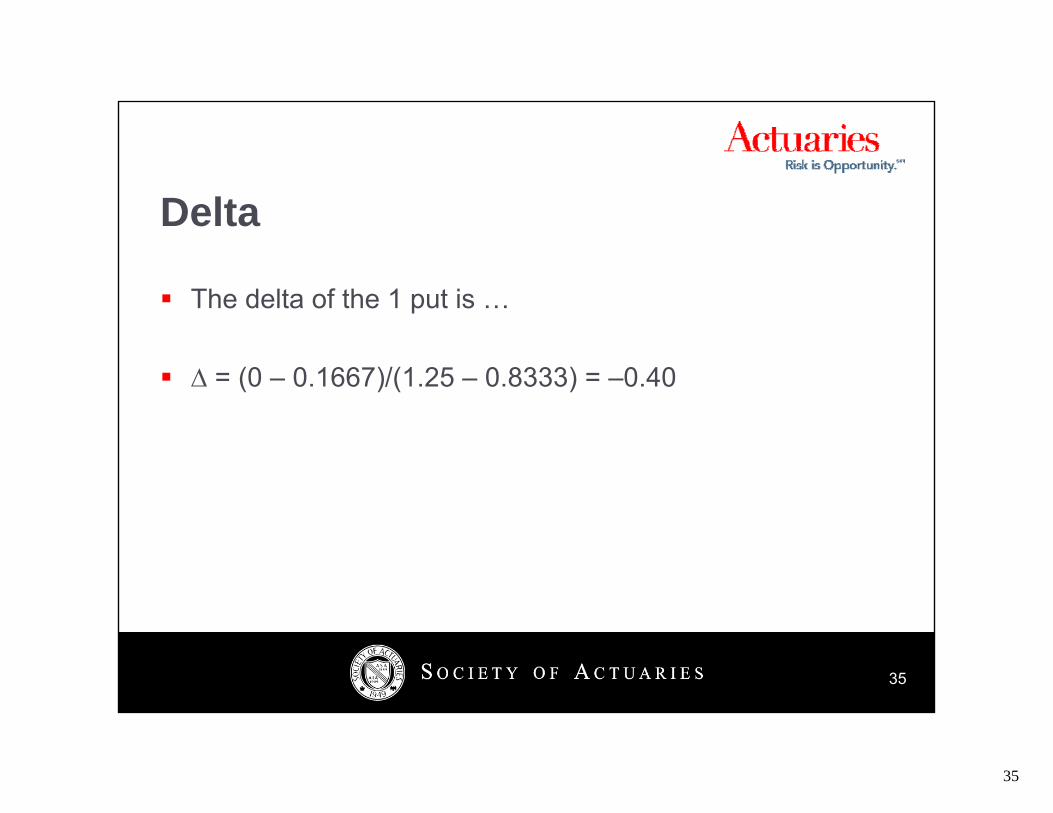

D ltDelta

The delta of the 1 put isThe delta of the 1 put is …

∆ = (0 – 0.1667)/(1.25 – 0.8333) = –0.40

35

35

36

P t V lPut Value

Risk-free portfolio: Long Put + Long 0 40 SharesRisk free portfolio: Long Put + Long 0.40 Shares …

• Stock up: (0.40)(1.25) = 0.50 (put worthless)• Stock down: (0.40)(0.8333) + 0.1667 = 0.50

Equal

Put + (0.40)(1.11) = 0.50 Put = 0.50 – 0.4444 = 0.0556

36

36

37

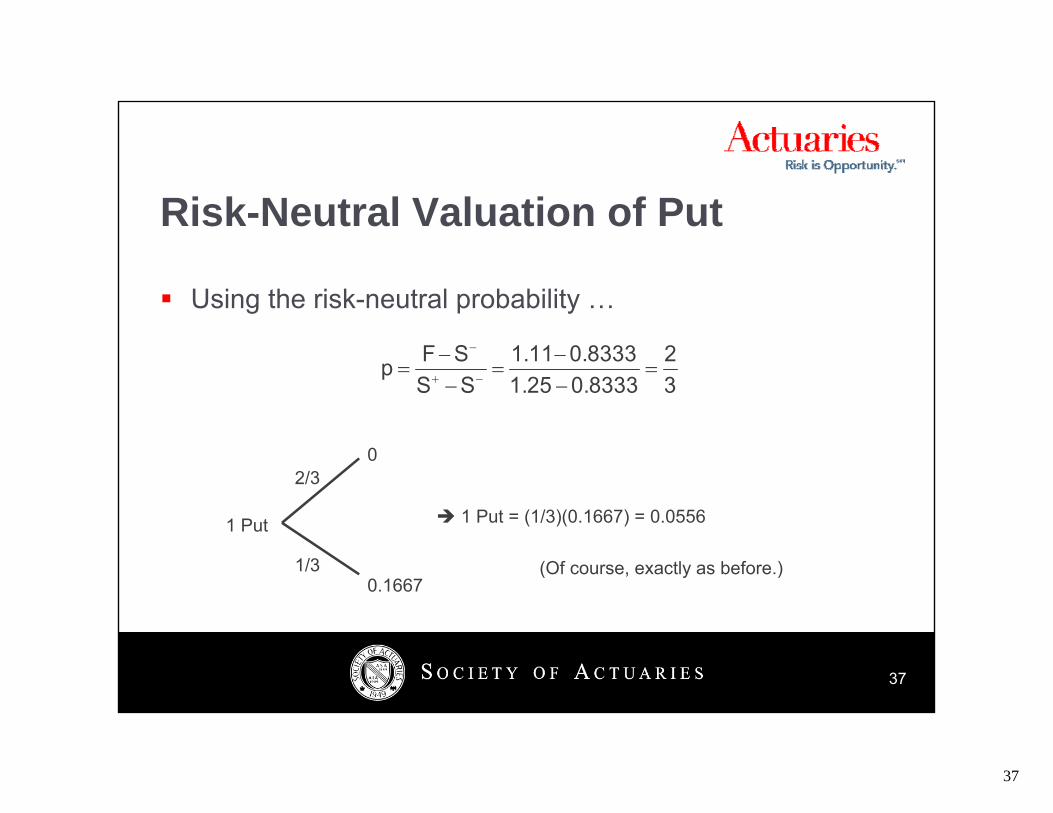

Ri k N t l V l ti f P tRisk-Neutral Valuation of Put

Using the risk-neutral probabilityUsing the risk neutral probability …

32

0.83331.250.83331.11

SSSFp

02/3

1 Put

0.16671/3

1 Put = (1/3)(0.1667) = 0.0556

(Of course, exactly as before.)

37

37

38

“Th ll t t lik hi k ”“They all taste like chicken”

The use of the terms “Call” and “Put” is really just aThe use of the terms Call and Put is really just a convenience, rooted in long-held tradition (especially in equities).

In fact, every call is a put and vice versa: every option is a contract to exchange two assets at a fixed ratio.

Thi i t b i i FX• This is most obvious in FX.

38

38

39

Th 100C? O th 1 h P t?The 100C? Or the 1-share Put?

The 100C that we valued can thusly be viewedThe 100C that we valued can thusly be viewed …

You Market$100

You Market1s Stock

You are long a call in one “currency” and long a put in another “currency”.

39

39

40

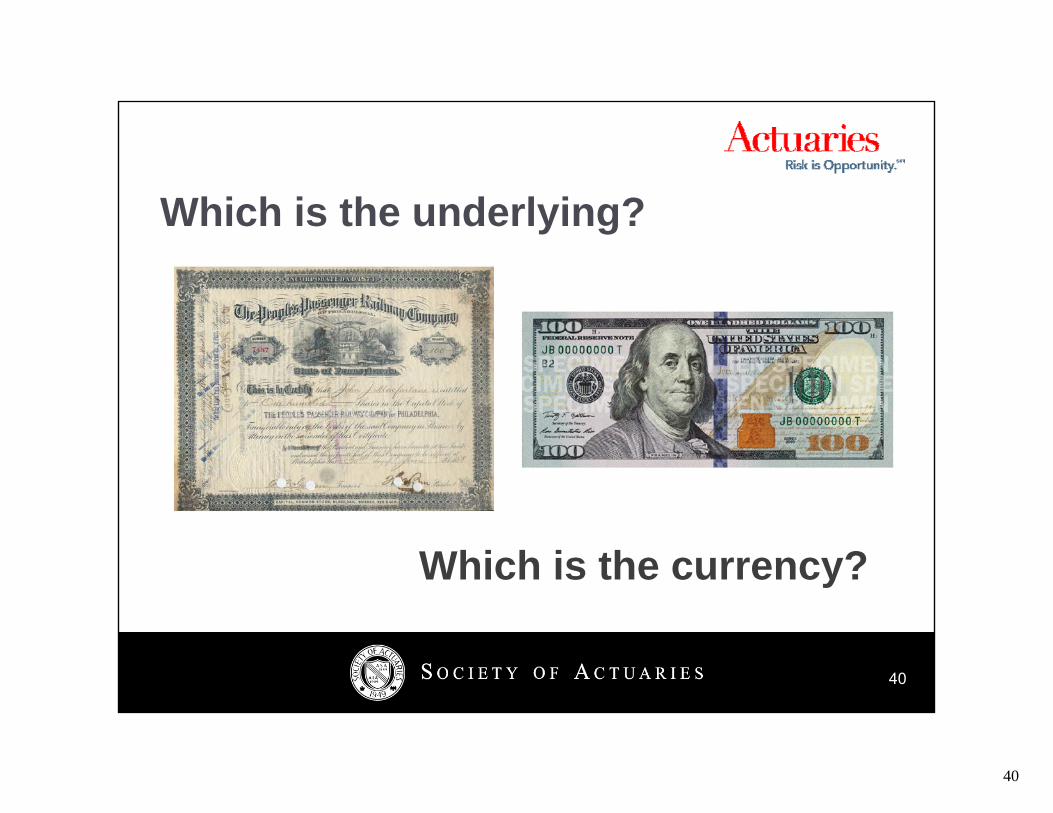

Whi h i th d l i ?Which is the underlying?

Which is the currency?

40

40

41

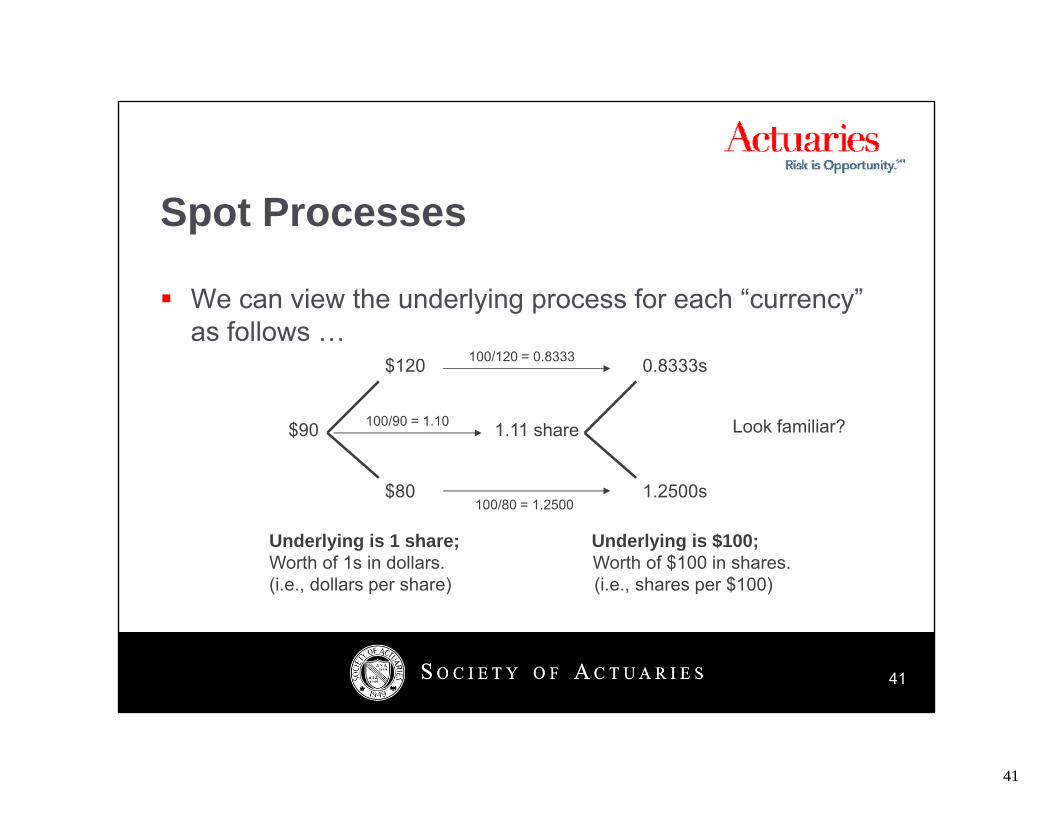

S t PSpot Processes

We can view the underlying process for each “currency”We can view the underlying process for each currency as follows …

$120 0.8333s100/120 = 0.8333

$90

$80

1.11 share

1.2500s100/80 = 1.2500

100/90 = 1.10 Look familiar?

Underlying is 1 share; Underlying is $100;Worth of 1s in dollars. Worth of $100 in shares.(i.e., dollars per share) (i.e., shares per $100)

100/80 1.2500

41

41

42

O ti P (1 Sh P t)Option Process (1 Share Put)

The process for the 1s put (put $100 for 1 share) isThe process for the 1s put (put $100 for 1 share) is …

0

1s Put

0.1667s

We’ve seen this before too!

42

42

43

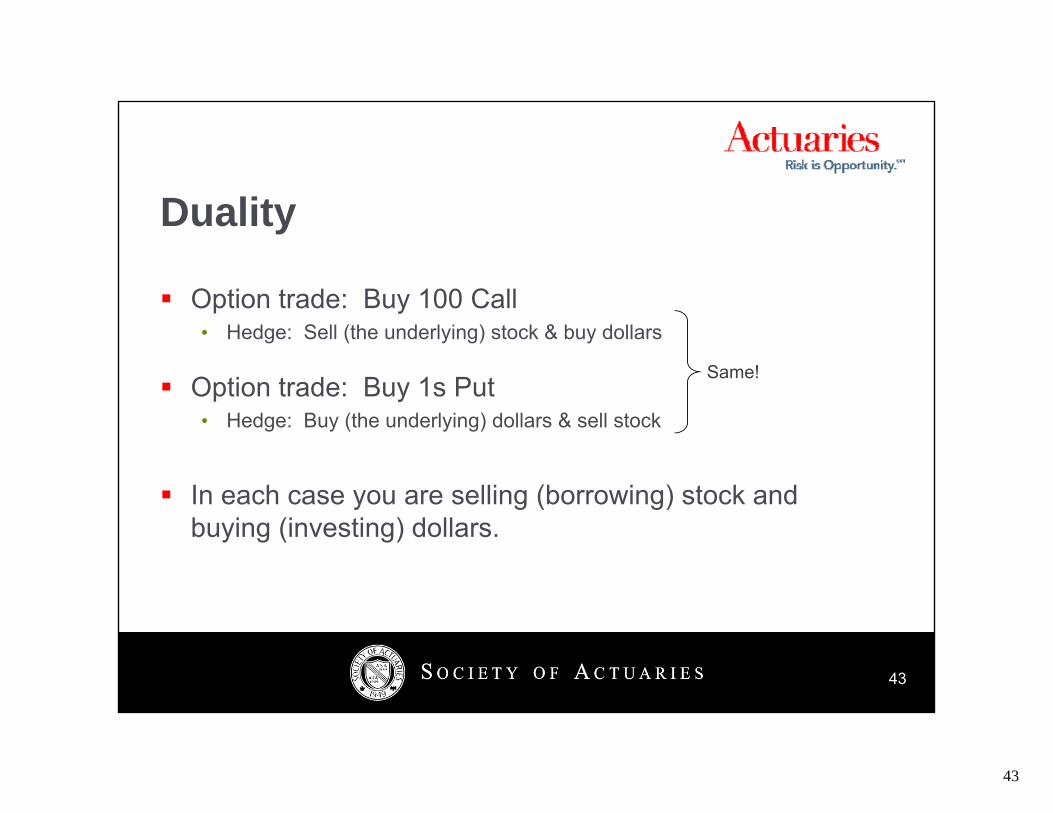

D litDuality

Option trade: Buy 100 CallOption trade: Buy 100 Call• Hedge: Sell (the underlying) stock & buy dollars

Option trade: Buy 1s PutSame!

• Hedge: Buy (the underlying) dollars & sell stock

In each case you are selling (borrowing) stock and y g ( g)buying (investing) dollars.

43

43

44

Ri k F P tf liRisk-Free Portfolio

Recall: for the 100C we had: $45 – C = $40Recall: for the 100C we had: $45 C $40. • [value of ½-share hedge in dollars] – [value of call in dollars] = [value of

portfolio in dollars at expiration]

For the one share put we have: 0.4444s + P = 0.50s.• [value of $40 hedge in shares] + [value of put in shares] = [value of

portfolio in shares at expiration]

• $40 buys 40/90 = 0.4444s at $90/s today.

44

44

45

V l f 1 P tValue of 1s Put

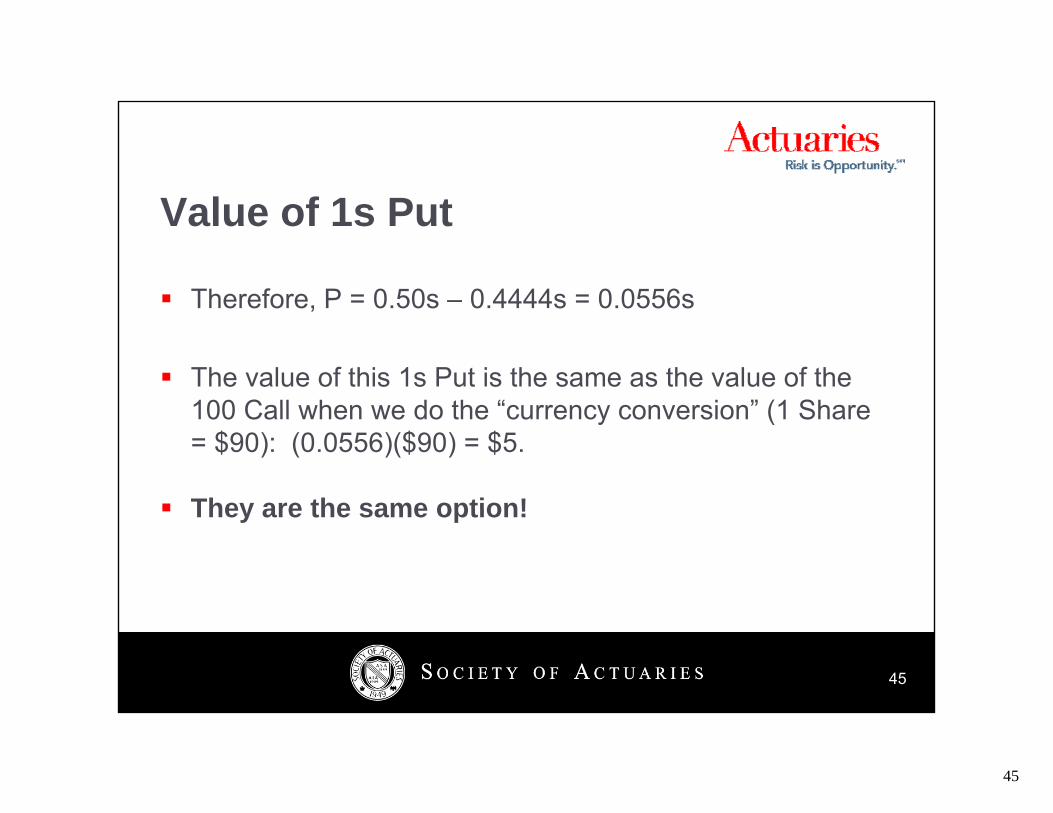

Therefore P = 0 50s – 0 4444s = 0 0556sTherefore, P 0.50s 0.4444s 0.0556s

The value of this 1s Put is the same as the value of the 100 Call when we do the “currency conversion” (1 Share100 Call when we do the currency conversion (1 Share = $90): (0.0556)($90) = $5.

They are the same option! They are the same option!

45

45

46

Ri k N t l “P b biliti ”?Risk-Neutral “Probabilities”?

The risk-neutral probability that 1s = $120 was found toThe risk neutral probability that 1s $120 was found to be 1/4.

The risk neutral probability that $100 = 0 8333s was The risk-neutral probability that $100 = 0.8333s was found to be 1/3.

But these are exactly the same event! • How can this event have 2 different “probabilities”?

46

46

47

P b b(ilit) NOT!Probab(ilit)y NOT!

The “risk-neutral probability” is not a probability at all inThe risk neutral probability is not a probability at all, in the sense that it describes the probability of some event in the real world.

47

47

48

“U i ” Ri k N t l P b biliti“Using” Risk-Neutral Probabilities

“Testing techniques and forecasting ability of FX Options Implied Risk Neutral Densities”, Oren Tapiero, European Central Bank, 2004.

48

48

49

“I li d P b biliti ”“Implied Probabilities” …

49

49

50

C ti f I f tiConservation of Information

The very fact that an option is nothing more than aThe very fact that an option is nothing more than a levered position in the underlying belies the belief that any information about the future probability distribution of the underlying can be derived from option prices. y g p p

50

50

51

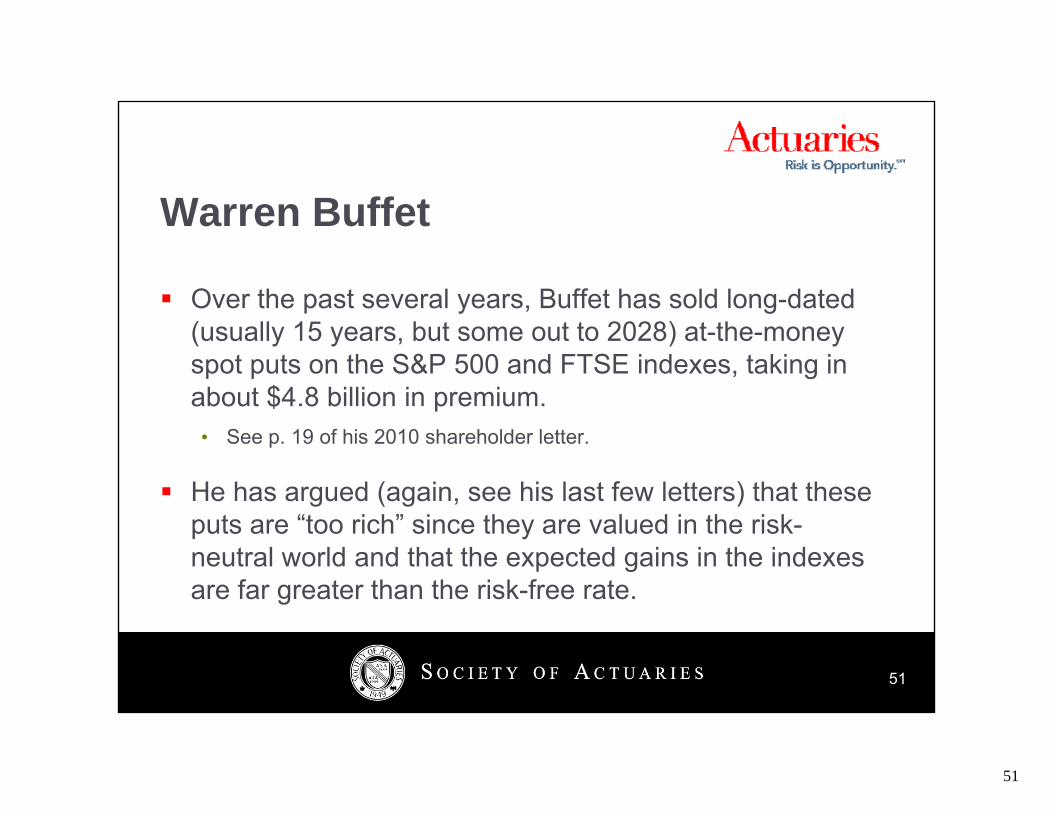

W B ff tWarren Buffet

Over the past several years Buffet has sold long-datedOver the past several years, Buffet has sold long dated (usually 15 years, but some out to 2028) at-the-money spot puts on the S&P 500 and FTSE indexes, taking in about $4.8 billion in premium.$ p• See p. 19 of his 2010 shareholder letter.

He has argued (again, see his last few letters) that these puts are “too rich” since they are valued in the risk-neutral world and that the expected gains in the indexes are far greater than the risk-free rate.

51

51

52

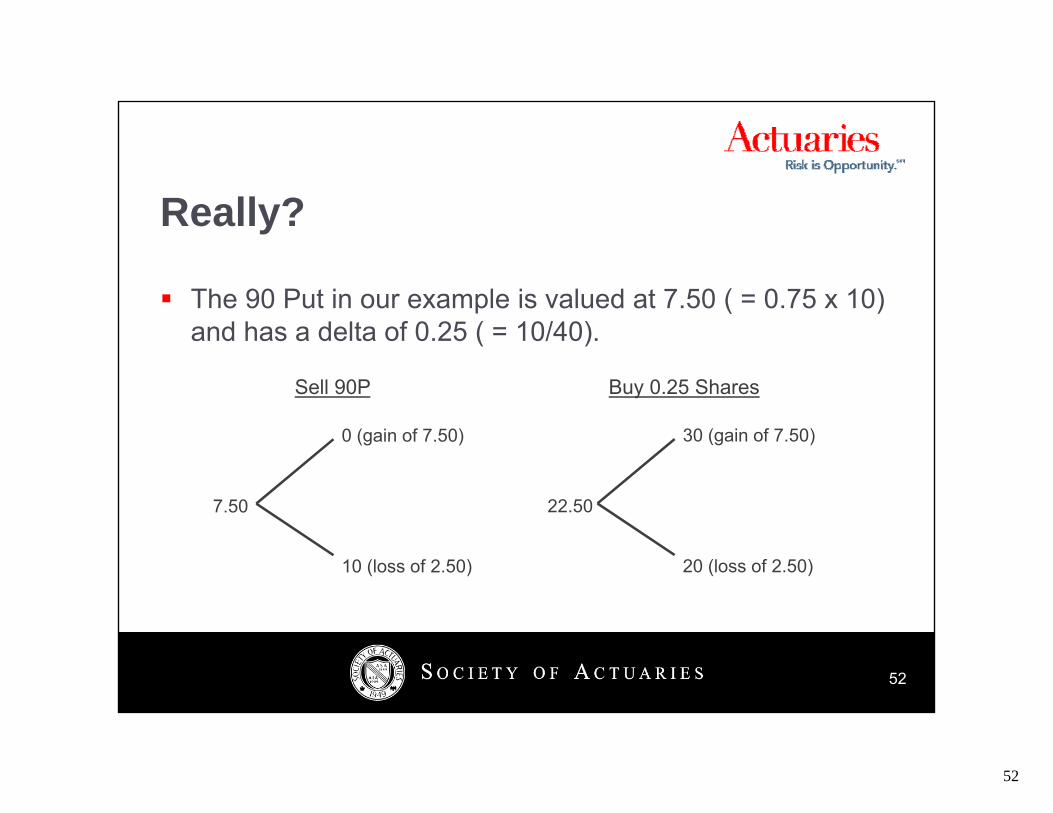

R ll ?Really?

The 90 Put in our example is valued at 7 50 ( = 0 75 x 10)The 90 Put in our example is valued at 7.50 ( 0.75 x 10) and has a delta of 0.25 ( = 10/40).

Sell 90P Buy 0.25 Shares

7 50

0 (gain of 7.50)

22 50

30 (gain of 7.50)

7.50

10 (loss of 2.50)

22.50

20 (loss of 2.50)

52

52

53

C t t I f tiContact Information

P l G St ki Ph DPaul G. Staneski, Ph.D.Credit SuisseManaging Director212 325 [email protected]

53

53