2009 10 NatGas Info

29

Oil & Gas Producers October 7 , 20 09 Calgary , Alberta Mark Leggett, CFA (403) 515-1508 [email protected] Associate: Jason Chang (403) 515-1527 [email protected] This report was prepared by an Analyst employed by a Canadian ailiate, BMO Nesbitt Burns Inc., and who is not registered as a research analyst under FINRA rules. For disclosure statements, including the Analyst’s Certifcat ion, please reer to pages 26 to 27 . PetroBakken Energy Ltd. (PBN – TSX) Stock Rating: Outperorm Industry Rating: Market Perorm Initiating at Outperorm; Leading the Canadian Bakken T echnology Evolution Price (5-Oct) $31.27* 52-Week High na Target Price $36.00 52-Week Low na (FY – Dec) 2008A 2009E 2010E CFPS na $2.89 $3.92 P/CFPS 10.8x 8.0x EPS na -$0.19 $0.85 P/EPS na 36.8x CF/boe na $32.25 $45.78 EV/EBITDA na 12.9x 9.1x ROCE na -2% 4% D/CF na 1.4x 1 .1x Dividend $0.96 Yield 3.1% Book Value $15.81 Price/Book 2.0x Shares O/S (mm) 171.9 Mkt. Cap ($mm) $5,374* Float O/S (mm) na Float Cap ($mm) na Notes: EPS (diluted), CFPS (diluted); *Implied share pr ice based on TOG closing price Highlights • PetroBakken’ slandholdingsofonemillionnetacres areunderpinned byitssignicantacreagepositionintheBakkenplayandcomplemented bythehigh-impactMontneyandHornRivernaturalgasshaleplays inNEBC.Petro BakkenwillbeledbyJohnD .Wright asChairman andCEO,andR.GreggSmithasPresidentandCOO.PetroBakken manag ement hasplayeda key rol e in pionee ringthe evo lutionof multi-sta gefracsintheB akkenpla yinsoutheastSaska tchewan.On arelativebasistoothersignicantoilplaysinWesternCanada,we estimatetheeconomicsoftheBakkenplayareunmatched. • Weproject 2009Eand2010ECFPSof $2.89and$3.92,respective ly . Ournancialestimatesarebasedon a ver age pr oduct ionof 42,15 8 boe/din2009Eand40,356boe/d(95%lightoil)in2010E.PetroBakken planstodiv est9,500boe/d andexit2009 at37,000boe/d. • Basedon TriSt ar’ sclosingprice,Petrobakk enshare sare tradingat animpliedvaluationof8.0xP/CFPSand9.1xEV/EBITDA*.Our targetpriceissupportedbyoursum-of-partsconsolidatedvalueof $35.72pershareusingaatlong-termCanadianparcrudepriceof $80/bblan dAECOnaturalgas priceassumptionof$6.00/Mcf .Our unbookeddrillingin ventoryvaluation isbased onthe detailedper well NPV(BT-10%)analysisofthecompany’sBakkenandConventional playsinSESaska tchewan,aswe llastheNEBCMontneyandHorn Riv erplays . Ourriske d anal ysissumsto tota l unbooked resourc e potentialof375MMboe. • Weareinitiatingcoverage withanOutperformratingandtargetprice of$36.PetroBakkensharesbegantradingonOctober6,2009,under thetickerPBNontheTSX.

Transcript of 2009 10 NatGas Info

8/3/2019 2009 10 NatGas Info

http://slidepdf.com/reader/full/2009-10-natgas-info 1/29

Oil & Gas

Producers

October 7, 2009Calgary, Alberta

Mark Leggett, CFA

(403) 515-1508

Associate: Jason Chang

(403) 515-1527

This report was prepared by an Analyst employed by a Canadian ailiate, BMO Nesbitt Burns Inc., and who is not registered as a researchanalyst under FINRA rules. For disclosure statements, including the Analyst’s Certifcation, please reer to pages 26 to 27.

PetroBakken EnergyLtd.(PBN – TSX)

Stock Rating: Outperorm

Industry Rating: Market Perorm

Initiating at Outperorm; Leading the

Canadian Bakken Technology Evolution

Price (5-Oct) $31.27* 52-Week High na

Target Price $36.00 52-Week Low na

(FY – Dec) 2008A 2009E 2010E

CFPS na $2.89 $3.92

P/CFPS 10.8x 8.0x

EPS na -$0.19 $0.85

P/EPS na 36.8x

CF/boe na $32.25 $45.78

EV/EBITDA na 12.9x 9.1xROCE na -2% 4%

D/CF na 1.4x 1.1x

Dividend $0.96 Yield 3.1%

Book Value $15.81 Price/Book 2.0x

Shares O/S (mm) 171.9 Mkt. Cap ($mm) $5,374*

Float O/S (mm) na Float Cap ($mm) na

Notes: EPS (diluted), CFPS (diluted); *Implied share pr icebased on TOG closing price

Highlights

• PetroBakken’slandholdingsofonemillionnetacresareunderpinned

byitssignicantacreagepositionintheBakkenplayandcomplemented

bythehigh-impactMontneyandHornRivernaturalgasshaleplays

inNEBC.PetroBakkenwillbeledbyJohnD.WrightasChairman

andCEO,andR.GreggSmithasPresidentandCOO.PetroBakken

management hasplayeda key role in pioneeringthe evolutionof

multi-stagefracsintheBakkenplayinsoutheastSaskatchewan.On

arelativebasistoothersignicantoilplaysinWesternCanada,weestimatetheeconomicsoftheBakkenplayareunmatched.

• Weproject2009Eand2010ECFPSof$2.89and$3.92,respectively.

Ournancialestimatesarebasedon average productionof 42,158

boe/din2009Eand40,356boe/d(95%lightoil)in2010E.PetroBakken

planstodivest9,500boe/dandexit2009at37,000boe/d.

• Basedon TriStar’sclosingprice,Petrobakkensharesare tradingat

animpliedvaluationof8.0xP/CFPSand9.1xEV/EBITDA*.Our

targetpriceissupportedbyoursum-of-partsconsolidatedvalueof

$35.72pershareusingaatlong-termCanadianparcrudepriceof

$80/bblandAECOnaturalgaspriceassumptionof$6.00/Mcf.Our

unbookeddrillinginventoryvaluationisbasedonthedetailedperwell

NPV(BT-10%)analysisofthecompany’sBakkenandConventional

playsinSESaskatchewan,aswellastheNEBCMontneyandHorn

Riverplays. Ourrisked analysissumsto total unbooked resource

potentialof375MMboe.

• WeareinitiatingcoveragewithanOutperformratingandtargetprice

of$36.PetroBakkensharesbegantradingonOctober6,2009,under

thetickerPBNontheTSX.

8/3/2019 2009 10 NatGas Info

http://slidepdf.com/reader/full/2009-10-natgas-info 2/29

8/3/2019 2009 10 NatGas Info

http://slidepdf.com/reader/full/2009-10-natgas-info 3/29

Table o Contents

ExecutiveSummary:SumofParts–NAVRoadMap................................................................................................... 2

TheBakkenPrize–SuperiorEconomics.................................................................................................................... 2

Operations:MultipleResourceGrowthPlatforms......................................................................................................... 3

LeadingtheCanadianBakkenTechnologyEvolution.................................................................................................. 4

HigherFracIntensityPerformance............................................................................................................................. 5

NorthDakotaOperationalTrends-TestingtheLimits.............................................................................................. 6

BakkenBilateralWellNPVAnalysis.......................................................................................................................... 8

EconomicsComparison.............................................................................................................................................. 9

Re-EntryOpportunities–CompellingLow-HangingFruit...................................................................................... 10

BakkenUnbookedDevelopmentProgramValuationSummary............................................................................... 12

IndustryBakkenSandbox–PeerComparables........................................................................................................... 13

BakkenComparables................................................................................................................................................ 14

BakkenInfrastructure.............................................................................................................................................. 14

SESaskatchewanConventionalInventory................................................................................................................... 15

NEBCShaleGas:MontneyandHornRiver............................................................................................................. 16

MontneyNPVAnalysis............................................................................................................................................ 17

HornRiver............................................................................................................................................................... 18

HornRiverNPVAnalysis........................................................................................................................................ 20

H2/09and2010Outlook.............................................................................................................................................. 21

PetroBakkenProle.................................................................................................................................................... 21

Management................................................................................................................................................................ 22

FinancialOutlook........................................................................................................................................................ 22

Valuation..................................................................................................................................................................... 24

InvestmentRisks.......................................................................................................................................................... 25

8/3/2019 2009 10 NatGas Info

http://slidepdf.com/reader/full/2009-10-natgas-info 4/29

Page 2 PetroBakken Energy Ltd.

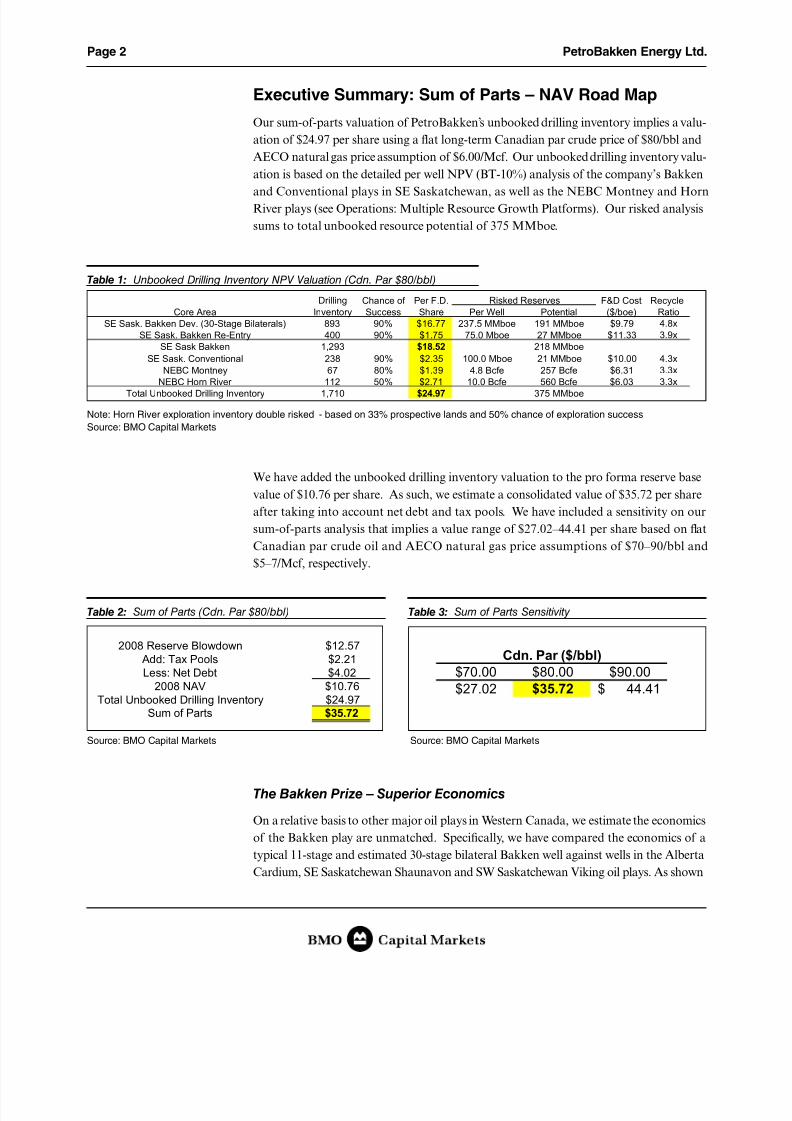

Executive Summary: Sum o Parts – NAV Road Map

Oursum-of-partsvaluationofPetroBakken’sunbookeddrillinginventoryimpliesavalu-

ationof$24.97pershareusingaatlong-termCanadianparcrudepriceof$80/bbland

AECOnaturalgaspriceassumptionof$6.00/Mcf.Ourunbookeddrillinginventoryvalu-

ationisbasedonthedetailedperwellNPV(BT-10%)analysisofthecompany’sBakken

andConventionalplaysinSESaskatchewan,aswellastheNEBCMontneyandHorn

Riverplays(seeOperations:MultipleResourceGrowthPlatforms).Ourriskedanalysis

sumstototalunbookedresourcepotentialof375MMboe.

Table 1: Unbooked Drilling Inventory NPV Valuation (Cdn. Par $80/bbl)

Drilling Chance of Per F.D. F&D Cost RecycleCore Area Inventory Success Share Per Well Potential ($/boe) Ratio

SE Sask. Bakken Dev. (30-Stage Bilaterals) 893 90% $16.77 237.5 MMboe 191 MMboe $9.79 4.8x

SE Sask. Bakken Re-Entry 400 90% $1.75 75.0 Mboe 27 MMboe $11.33 3.9x

SE Sask Bakken 1,293 $18.52 218 MMboe

SE Sask. Conventional 238 90% $2.35 100.0 Mboe 21 MMboe $10.00 4.3x

NEBC Montney 67 80% $1.39 4.8 Bcfe 257 Bcfe $6.31 3.3x

NEBC Horn River 112 50% $2.71 10.0 Bcfe 560 Bcfe $6.03 3.3x

Total Unbooked Drilling Inventory 1,710 $24.97 375 MMboe

Risked Reserves

Note: Horn River exploration inventory double risked - based on 33% prospective lands and 50% chance o exploration success

Source: BMO Capital Markets

Wehaveaddedtheunbookeddrillinginventoryvaluationtotheproformareservebase

valueof$10.76pershare.Assuch,weestimateaconsolidatedvalueof$35.72pershare

aftertakingintoaccountnetdebtandtaxpools.Wehaveincludedasensitivityonour

sum-of-partsanalysisthatimpliesavaluerangeof$27.02–44.41persharebasedonat

CanadianparcrudeoilandAECOnaturalgaspriceassumptionsof$70–90/bbland

$5–7/Mcf,respectively.

Table 2: Sum o Parts (Cdn. Par $80/bbl) Table 3: Sum o Parts Sensitivity

2008 Reserve Blowdown $12.57Add: Tax Pools $2.21Less: Net Debt $4.02

2008 NAV $10.76Total Unbooked Drilling Inventory $24.97

Sum of Parts $35.72

$70.00 $80.00 $90.00

$27.02 $35.72 44.41$

Cdn. Par ($/bbl)

Source: BMO Capital Markets Source: BMO Capital Markets

The Bakken Prize – Superior Economics

OnarelativebasistoothermajoroilplaysinWesternCanada,weestimatetheeconomics

oftheBakkenplayareunmatched.Specically,wehavecomparedtheeconomicsofa

typical11-stageandestimated30-stagebilateralBakkenwellagainstwellsintheAlberta

Cardium,SESaskatchewanShaunavonandSWSaskatchewanVikingoilplays.Asshown

8/3/2019 2009 10 NatGas Info

http://slidepdf.com/reader/full/2009-10-natgas-info 5/29

PetroBakken Energy Ltd. Page 3

below,weestimateBakkenwellshaveahigherNPVandIRRthanothermajoroilplays.

Additionally,Bakkenwellsoutperformtheseplaysonvariouseconomicmeasures,includ-

ingF&Dcost,payoutandrecycleratio.

Table 4: Single Well Economic Comparison o Various Oil Plays (Cdn. Par $80/bbl)SE Sask. SW Sask. Alberta Alberta

30-stage Bakken

Bilateral Long Hz Well

11-Stage Bakken Long Hz

Well

Shaunavon Hz

WellViking Hz Well

Cardium Hz Well Inc.

Incentives

Cardium Hz Well No

Incentives

Drill Cost Per Well $2.3 $1.7 $1.9 $1.7 $3.2 $3.2NPV (10%) Per Well ($ mm) $5.6 $2.8 $1.9 $1.1 $2.6 $2.0

IRR Per Well (%) 91% 64% 40% 29% 30% 23%

F&D Cost ($/boe) $9.79 $13.60 $15.20 $27.20 $18.29 $18.29Recycle Ratio 5.1x 3.9x 2.9x 2.1x 2.9x 2.7xPayout (years) 0.5 0.8 1.3 2.3 2.4 3.3

Companies In Play PBN PBN, CPG, NAE.UN, GLM PWT.UN, CPG PWT.UN, BTE.UN, CPG NAE.UN, PWT.UN NAE.UN, PWT.UN

SE Sask

Note: Based on operating netback to acilitate comparable analysis; Economic analysis or PBN within this report is based on cash fow netback.

Source: BMO Capital Markets, Company Reports

Operations: Multiple Resource Growth Platorms

PetroBakken’slandholdingsofonemillionnetacresareunderpinnedbyitssignicant

acreage positioninthe Bakkenplayandcomplementedby thehigh-impactMontney

andHornRivernaturalgasshaleplaysinNEBC.ThecompanyplanstosellAlberta

assetscomprisedof9,500boe/dand40.1MMboeto“wipetheslateclean”andfocuson

high-returnopportunitieswithinneighbouringprovinces(wehaveassumedsalemetrics

of$40,000/boe/dand$9.50/boeinQ4/09forthepurposesofourworkingmodel).

Chart 1: NPV Per Well and IRR (Cdn. Par Crude $80/bbl) Chart 2: F&D Cost, Payout (years) and Recycle Ratio

$0.0

$1.0

$2.0

$3.0

$4.0

$5.0

$6.0

30-stage Bakken

Bilateral Long Hz

Well

11-Stage Bakken

Long Hz Well

Shaunavon Hz Well Viking Hz Well Cardium Hz Well

Inc. Incentives

Cardium Hz Well

No Incentives

N P V P e r W e l l ( $ m m )

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

I R R ( % )

NPV Per Well($ mm)

IRR (%)

$0.00

$5.00

$10.00

$15.00

$20.00

$25.00

$30.00

30-stage Bakken

Bilateral Long Hz

Well

11-Stage Bakken

Long Hz Well

Shaunavon Hz Well Viking Hz Well Cardium Hz Well

Inc. Incentives

Cardium Hz Well

No Incentives

F & D C

o s t ( $ / b o e )

0.0

1.0

2.0

3.0

4.0

5.0

6.0

P a y o u t ( y e a r s ) / R e c y c l e R a t i o

RecycleRatio

Payout(years)

F&D Cost($/boe)

Source: BMO Capital Markets Source: BMO Capital Markets

8/3/2019 2009 10 NatGas Info

http://slidepdf.com/reader/full/2009-10-natgas-info 6/29

Page 4 PetroBakken Energy Ltd.

Leading the Canadian Bakken Technology Evolution

PetroBakkenmanagementhasplayedakeyroleinpioneeringtheevolutionofmulti-

stagefracsintheBakkenplayinsoutheastSaskatchewan,highlightedbythecompany’s

closerelationshipwithPackersPlus(#1customerstatus) 1.Theevolutionofhigherfrac

intensitytechnology(morefracswithinasinglewellbore)potentiallyindicateshigher

expectedultimaterecoveries(EURs)basedonearlydrillingresults.

Asshownbelow,drillingmethodshaveevolvedfromtheoriginal8-to11-stagefracswithin

alongwell(1,400metres)toshorterwells(600metres)usingthesamenumberoffracs

(8x2=16fracs),followedbybilateralshortwells(8x4=32fracs).Shortwellscontinueto

performgenerallyinlinewithlongwells,whichimplieshigherreserverecoverypotential

persectionofland.Morerecently,PetroBakkenannouncedthatitsrst long horizontal

well using 20-stage racs initiallytestedatmorethan400boe/d.Basedonthisinitial

success,thecompanyexpectstotestlong bilateral wells,representingthenextpotential

evolutionintheBakkenplay.Managementhasspokentoinitiallyexecuting15-stagefracsineachleg(15x2=30fracs).

Figure 1: CanadianBusiness Unit

Source: Company Reports

1 Dan Themig (President o Packers Plus Energy Services) is a director on PetroBakken’s board odirectors.

8/3/2019 2009 10 NatGas Info

http://slidepdf.com/reader/full/2009-10-natgas-info 7/29

PetroBakken Energy Ltd. Page 5

Bottomline,weexpectimprovedcapitalefcienciesondecliningFD&Ametrics,result-

inginhigherrecycleratiosonhigherbilateralEURs.Theeconomicbenetsofbilateral

drillingarefurtherhighlightedbycompellingeconomicsonthere-entryprogram(see

“Re-EntryOpportunities–CompellingLow-HangingFruit”).

Higher Frac Intensity Performance

Theapplicationofhigherfracintensitywithinalongerwellisstillearlydaysgiventhat

PetroBakkenhasonlyfourwellswithinitialdatapointstodate.Assuch,theproductiv-

ityofeachfracandEURisstilltobedeterminedbutdatatodateisveryencouraging.

Managementbelievesthefracperformancein20-stagelongwellsor30-stagebilateral

longwellsisnotnecessarilyalinearrelationshipduetothepotentialdepletionofenergy

withinthereservoirthatdiminishestheabilitytopushoiloutofthesystemovertime.

Thisspeakstothepotentialforasecondaryrecoverywateroodprograminthelongterm

tomaintainreservoirpressureandproduceremainingbarrels. However,PetroBakken

hasreported~12,000bblincumulativeproductionon20-stagelongwellsintherst35

days,whichiswellaheadofour11-stagelongwelltypecurveof~5,000bbloverthesame

timeperiod,potentiallyindicatinghigherperwellEURandassociatedrecoveryfactor

persectionofland.

Figure 2: Evolution o Technology in the BakkenPlay

•Original Development: Long Hz Wells (11 stages) •Evolution: Short Hz Wells (16 stages)

•Evolution: Short Bilateral Hz Wells (32 stages) •Evolution: Long Bilateral Hz Wells (30+stages)

•Original Development: Long Hz Wells (11 stages) •Evolution: Short Hz Wells (16 stages)

•Evolution: Short Bilateral Hz Wells (32 stages) •Evolution: Long Bilateral Hz Wells (30+stages)

Source: PetroBakken

8/3/2019 2009 10 NatGas Info

http://slidepdf.com/reader/full/2009-10-natgas-info 8/29

Page 6 PetroBakken Energy Ltd.

North Dakota Operational Trends - Testing the Limits

Furtheradvancementsinhigherfracintensitytechnologycanbeseensouthoftheborder

intherelativelydeeperNorthDakotaBakkenplay.Industrypeersintheplayhavealso

reportedearlydaysstronginitialsuccesswith20-stageintervalfracsandarenowtesting

28-stagefracsversus7-to12-stagefracsinprioryears.

Chart 3: Short Bilateral 91/02-10-009-10W2 Chart 4: 20-Stage Frac Wells

Source: Company Reports Source: Company Reports

Figure 3: North DakotaFrac Technology

Source: Brigham Exploration

8/3/2019 2009 10 NatGas Info

http://slidepdf.com/reader/full/2009-10-natgas-info 9/29

PetroBakken Energy Ltd. Page 7

TheoperationaltrendsinNorthDakotaprovideacomparable(albeitnotadirectcom-

parable)thatspeakstoimprovedEURsonhigherfracintensity.PetroBakkenplansto

replicatethisthemeofimprovedrecoveryfactors,resultinginlowerF&Dandrisingrecycle

ratios,asshownbelow.Clearly,industryplayerswillcontinuetotestreservoirlimitsto

optimizetheleveloffracintensitythatworksfortheBakkenplay,withPetroBakken

leadingthetechnicalevolutioninSESaskatchewan.Theimprovingcapitalefciencies

fromtheevolutionindrillingtechnologyarehighlightedbythedoublingofrecoveryfac-

torsfrom12%(11-stagelongwells)topotentially23%withthe30-stagelongbilaterals,

resultinginareductionofF&Dcoststo~$10/boefrom~$16/boe.

Chart 5: Recoverable Reserves per Section and F&D Trend

0

100,000

200,000

300,000

400,000

500,000

600,000

700,000

800,000

900,000

1,000,000

1,100,000

1,200,000

11-Stage Long 8-Stage Short 15-Stage Short Bilateral 20-Stage Long 30-Stage Long Bilateral

( b b l s )

$0.00

$2.00

$4.00

$6.00

$8.00

$10.00

$12.00

$14.00

$16.00

$18.00

( $ / b o e )

Rec. Reserves Per Section F&D

CAPITAL EFFICIENCIESRESERVE RECOVERY

11.9% RF

17.6% RF

22.6% RF 22.6% RF

17.6% RF

Note: Short well data based on company estimates

Source: BMO Capital Markets, Company Reports

Additionally,ContinentalResources(CLR-NYSE)hasreportedasuccessfulwellfrom

theSanishformationinNorthDakota(Mathistad2-35H–testedat995boe/d),which

initiallyindicatedaseparateproductivereservoirbelowtheBakkenformation(nocom-

municationbetweentheBakkenandThreeForks/Sanishreservoirs)2.Industryiscur-

rentlyexploringSanishpotentialinSESaskatchewanintheTablelandregion,whichmay

representexplorationopportunitiesinthelongterm.PetroBakkenalsoholdsmorethan

80,000netacresinMontana.

2 Continental Resources - The Mathistad 2-35H was drilled horizontally in the Middle Bakken (MB) zoneapproximately 50 eet above and essentially parallel to the horizontal o the Mathistad 1-35H.

8/3/2019 2009 10 NatGas Info

http://slidepdf.com/reader/full/2009-10-natgas-info 10/29

Page 8 PetroBakken Energy Ltd.

Bakken Bilateral Well NPV Analysis

Withtheevolutionofdrillingtechnologyandearlysuccesstodate,managementplans

toexecute30-stagelongbilateralwells(15fracsineachleg).Aspreviouslymentioned,

thefracperformancein bilateralwellsis unknownat this time andfracperformance

maynotbelinearduetodepletionofreservoirenergy.Assuch,wehaverunaNPVperwellsensitivityanalysisforthebilateralwellsusingvariousrecoverablereservescenarios.

Ourbilateralrecoverablereservescenariosarebasedonfracperformancethathasbeen

calibratedusingthefollowingassumptions:

• thepotentialfordecreasedfracperformanceoverthelifeof thewell(~6,700bbl/frac)

forrecoverablereservesperwellof200,000bbl(100,000bblperleg);

• PBN’simpliedfracperformanceon30-stagelongbilateralwells(~8,000bbl/frac)for

recoverablereservesperwellof237,500bbl(118,750bblperleg);and

• PBN’simpliedfracperformanceon20-stagelongwells(~9,250bbl/frac)forrecoverable

reservesperwellof277,500bbl(138,750bblperleg).

Referencingthetypecurvefor11-stagefraclongwellsspudsince2007frompubliclyavail-

abledata,wehaveprojectedaverage-typecurvesbasedontherecoverablereservescenarios

for30-stagelongbilaterals(15fracsineachleg)previouslymentioned(200,000–277,500

bbl).Webelievetheserecoverablereservescenariosprovidethegoalpostsforwhether

fracperformanceexceedsordoesnotmeetexpectations.OurNPVanalysisalsoassumes

drillingcostsof$2.3millionperwellandanall-incashownetbackbasedonvarious

assumptions, including operatingcosts of $5.75/boe and Saskatchewan’s incentivized

royaltyrateof2.5%ontherst37,500bblofproductionand25%thereafter.

Figure 4: Montana/NorthDakota Bakken ShaleCross-Section

Source: Continental Resources

8/3/2019 2009 10 NatGas Info

http://slidepdf.com/reader/full/2009-10-natgas-info 11/29

PetroBakken Energy Ltd. Page 9

WeestimateanNPVvaluerangeof$3.1–7.5millionperwellatvariousCanadianpar

crudeoilpricesandrecoverablereservescenarios.Oursum-of-partsvaluationanalysis

isbasedonarecoverablereservescenarioof237,500bblatCanadianparcrudeof$80/

bbl.Weestimatethebreakevencrudeoilpriceforthis30-stagelongbilateralwellis~$36/

bbl(IRR10%).PetroBakkenholdsanunbookeddrillinginventoryof893netBakken

locations.Assuch,weestimateanunbookeddevelopmentinventoryvaluationrangeof

$10.12–24.89(Table6),basedonaprojecteddrillingprogramoutto2017andarisked

chanceof success(COS)of 90%atvarious recoverablereserveandcommodityprice

scenarios.

Chart 6: PBN Bakken Well Profle Versus Long Bilateral Projected Production Profles

0

50

100

150

200

250

300

350

400

450

1 2 3 4 5 6 7 8 9 10 11 12

Month

b / d

PBN Bakken Well 200,000 bbls 237,500 bbls 277,500 bbls

Source: BMO Capital Markets, GeoScout

Table 5: 30-Stage (15 Per Leg) Bilateral NPV Per Well Sensitivity Matrix

Table 6: 30-Stage (15-Per Leg) Bilateral UnbookedInventory Valuation

Cdn. Par Crude Oil ($/bbl)$70.00 $80.00 $90.00

200,000 $3.1 $4.0 $5.0

237,500 $4.0 $5.1 $6.2

277,500 $4.9 $6.2 $7.5 R e c .

R e s .

( b o e )

$70.00 $80.00 $90.00

200,000 $10.12 $13.27 $16.42

237,500 $13.09 $16.77 $20.46

277,500 $16.34 $20.61 $24.89

Cdn. Par Crude Oil ($/bbl)

R e c .

R e s .

( b o e )

Source: BMO Capital Markets Source: BMO Capital Markets

Economics Comparison

BelowisasummaryoftheeconomicsforalongBakkenwellwithan11-stagefracand

s20-stagefrac,aswellasa30-stagelongbilateralwell(15fracsineachleg).Perwell

productivityleverageishighlightedgivena2:1relationshipbetweenincrementalreserve

recoveryversusincrementaldrillcosts,resultinginarisingIRRtrend.Specically,com-

paring11-stagewellsto30-stagewellsreectsa90%increaseinperwellreserverecovery

potentialversusa35%increaseindrillcostthatdrivesIRRupby25%to83%.

8/3/2019 2009 10 NatGas Info

http://slidepdf.com/reader/full/2009-10-natgas-info 12/29

Page 10 PetroBakken Energy Ltd.

Bottomline,theevolutionindrillingmethodsinSESaskatchewancontinuestoshow

a rising trendin theeconomics(NPV andrecycleratio), reecting improving capital

efciencies.PetroBakkencontinuestoleadthetechnicalevolutionintestingreservoir

productivitywhilemaintainingcapitalefcienciesintheplay.

Table 7: PBN BakkenEconomic Comparison(Cdn. Par $80/bbl)

11-stage Long Well 20-Stage Long Well 30-stage Bilateral Long Well

Drill Cost ($ mm) $1.7 $2.0 $2.3Reserves Per Well (Mboe) 125.0 185.0 237.5

Reserves Per Section (Mboe) 500.0 740.0 950.0Recovery Factor 11.9% 17.6% 22.6%

F&D Cost ($/boe) $13.60 $10.81 $9.79Recycle Ratio 3.6x 4.4x 4.8x

Payout (years) 0.9 0.6 0.5NPV (10%) Per Well ($ mm) $2.5 $3.9 $5.1

NPV (10%) Per Section ($ mm) $9.8 $15.6 $20.3

IRR Per Well (%) 58% 76% 83%

Note: Economics based on cash fow netback

Source: BMO Capital Markets, Company Reports

Chart 7: NPV Per Well and Recycle Ratio Trend

$0.0

$1.0

$2.0

$3.0

$4.0

$5.0

$6.0

$7.0

$8.0

11-Stage Long 8-Stage Short 15-Stage Short Bilateral 20-Stage Long 30-Stage Long Bilateral0.0x

1.0x

2.0x

3.0x

4.0x

5.0x

6.0x

7.0x

8.0x

NPV Per Well($ mm) Recycle Ratio

Note: Short well economics based on company estimates; NPV based on cash fow netbacks

Source: BMO Capital Markets, Company Reports

Re-Entry Opportunities – Compelling Low-Hanging Fruit

Pendingthesuccessofbilateraldrilling,PetroBakkenholdsapotentialinventoryof

400existingsingle-leghorizontalBakkenwellsthatcanbere-enteredtodrillaparallel

horizontalintheheelofthesewells.Thecompanyhasalreadytestedthisconceptwith

encouragingresultstodate,havingrecovered13,700bblinvemonths(73%ofEUR

fora125,000-bbl-typecurveoverthesametimeperiod)onare-entrydrilledwithonly

8fracs.

8/3/2019 2009 10 NatGas Info

http://slidepdf.com/reader/full/2009-10-natgas-info 13/29

PetroBakken Energy Ltd. Page 11

WehaverunaNPVanalysisontheBakkenre-entryopportunitiesthatimpliesanNPV

perwellrangeof$1.0–3.3million(Table8),basedonvariousrecoverablereservescenarios

andcommodityassumptions.Weestimatethecompany’sre-entryinventoryof400loca-

tionsisworth$1.31–4.40pershare(Table9),basedonaprojecteddrillingprogramoutto

2018andariskedchanceofsuccessof 90%atvariousrecoverablereserveandcommodity

pricescenarios.Oursum-of-partsvaluationanalysisisbasedonrecoverablereservesper

entryof75,000bblatCanadianparcrudeof$80/bbl.

Chart 8: Re-Entry -191/04-04-009-10W2

Source: PetroBakken

Table 8: Re-Entry Hz NPV per Well Sensitivity Matrix Table 9: Re-Entry Unbooked Inventory Valuation

Cdn. Par Crude Oil ($/bbl)$70.00 $80.00 $90.00

75,000 $1.0 $1.3 $1.6

100,000 $1.6 $2.0 $2.5

125,000 $2.2 $2.8 $3.3 R e c .

R e s .

( b o e )

$70.00 $80.00 $90.00

75,000 $1.31 $1.75 $2.19

100,000 $2.12 $2.71 $3.29

125,000 $2.93 $3.66 $4.40

Cdn. Par Crude Oil ($/bbl)

R e c .

R e s .

( b o e )

Source: BMO Capital Markets Source: BMO Capital Markets

Bottomline,asuccessfullow-riskre-entryprogramrepresentscompellinglow-hanging

fruitgivenimpliedF&Dandrecycleratiosof$11.33/boeand3.9x,respectively,basedon

recoverablereservesof75,000bbl.Wenotethatthesemetricsimprovesignicantlyto

$8.50/boeand5.2x,respectively,onhigherrecoverablereservesof100,000bbl.

8/3/2019 2009 10 NatGas Info

http://slidepdf.com/reader/full/2009-10-natgas-info 14/29

Page 12 PetroBakken Energy Ltd.

Bakken Unbooked Development Program Valuation Summary

PetroBakkenholdsanunbookedBakkendrillinginventoryof893netlocationsanda

re-entryinventoryof400locations.Inordertoestimatethevalueofthecompany’sun-bookedBakkeninventory,wehaveforecastdrillingprogramsoutto~2018.Aspreviously

mentioned,wehaveused237,500bbl(118,750bblperleg)onthe30-stagelongbilateral

wellsand75,000bblonthere-entryopportunities.Wehavealsoassumeda90%chance

of successoneach program. Assuch,we estimatethe company’sunbookedBakken

inventoryisworth$18.52pershareat$80/bblCanadianparcrude.

Table 10: Re-Entry Economic Summary (Cdn.Par $80/bbl)

Re-entryDrill Cost ($ mm) $0.9

Reserves Per Well (Mboe) 75.0

Reserves Per Section (Mboe) 300.0Recovery Factor +7.1%F&D Cost ($/boe) $11.33

Recycle Ratio 3.9x

Payout (years) 1.2NPV (10%) Per Well ($ mm) $1.3

NPV (10%) Per Section ($ mm) $5.3

IRR Per Well (%) 54%

Source: BMO Capital Markets

Table 11: Bakken Unbooked Drilling Inventory NPV Valuation (Cdn. Par $80/bbl)

Drilling Chance of Per F.D. F&D Cost RecycleCore Area Inventory Success Share Per Well Potential ($/boe) Ratio

SE Sask. Bakken Dev. (30-Stage Bilaterals) 893 90% $16.77 237.5 MMboe 191 MMboe $9.79 4.8x

SE Sask. Bakken Re-Entry 400 90% $1.75 75.0 Mboe 27 MMboe $11.33 3.9xSE Sask Bakken 1,293 $18.52 218 MMboe

Risked Reserves

Source: BMO Capital Markets

Aspreviouslyhighlighted,thereisadditionalincrementalreserveupsidewithinthe

bilateralandre-entryprogramsthatcouldwarranthighervaluations,pendingfurther

drillingsuccess.WehaveincludedanunbookedBakkeninventorydevelopmentvaluation

sensitivityusingvariousrecoverablereservescenarios,whichimpliesavaluationrange

of$15.02–24.28pershare.

Table 12: UnbookedBakken Inventory ValuationSensitivity Matrix (Cdn. Par $80/bbl)

200,000 237,500 277,500

75,000 $15.02 $18.52 $22.36

100,000 $15.98 $19.48 $23.32

125,000 $16.94 $20.44 $24.28

Bilateral Development Program

R e - E n t r y

P r o g r a m

R e c .

R e s .

( b o e )

Source: BMO Capital Markets

8/3/2019 2009 10 NatGas Info

http://slidepdf.com/reader/full/2009-10-natgas-info 15/29

PetroBakken Energy Ltd. Page 13

Industry Bakken Sandbox – Peer Comparables

Theemergenceofhorizontaldrillingandsubsequentevolutionsindrillingandcompletion

techniquespointstowardhigherrecoveryratesattheBakkenlightoilresourceplay.As

such,prospectiveBakkenacreagehasbeenrapidlyconsolidated,resultinginahandful

ofplayersinthearea.CrescentPointEnergyCorp.(CPG-TSX)isthelargestBakken

landholder,followedbyPetroBakkenwithmorethan210,000netundevelopedacresand

1,300drillinglocations(893unbooked)atfourwellspersection.

Figure 5: SE Saskatchewan Land Holdings

T1

T2

T3

T4

T5

T6

T7

T8

T9

T10

T11

T12

T13

T1

T2

T3

T4

T5

T6

T7

T8

T9

T10

T11

T12

T13

R30W1R31R32R33R34R1W2R2R3R4R5R6R7R8R9R10R11R12R13R14R15R16R17R18R19

R30W1R31R32R33R34R1W2R2R3R4R5R6R7R8R9R10R11R12R13R14R15R16R17R18R19

VIEWFIELD

PBN CPG CPG/PBN (TLM LANDS)Shelter Bay GLM PPY.A NAL

T1

T2

T3

T4

T5

T6

T7

T8

T9

T10

T11

T12

T13

T1

T2

T3

T4

T5

T6

T7

T8

T9

T10

T11

T12

T13

R30W1R31R32R33R34R1W2R2R3R4R5R6R7R8R9R10R11R12R13R14R15R16R17R18R19

R30W1R31R32R33R34R1W2R2R3R4R5R6R7R8R9R10R11R12R13R14R15R16R17R18R19

VIEWFIELD

PBN CPG CPG/PBN (TLM LANDS)Shelter Bay GLM PPY.A NAL

Source: GeoScout, Company Reports, BMO Capital Markets

First-monthIPratesforatypicalBakkenwellrangefrom150b/dto200b/dwithrecover-

ablereservesof125,000boeperwell(PBNtargeting150,000boebasedonresultstodate).PetrobankandTriStar’s(PetroBakken)Bakkenwellshaveconsistentlyshownhigherrst-

monthproductionratesversusCrescentPoint’sBakkenwellsoverthesametimeperiods,

basedonpubliclyavailabledata.Additionally,onacombinedbasisPetroBakkenhas

beengenerallymoreactivewiththedrillbit.Chart9highlightsthesetrends,particularly

overthepastfourquarters.

8/3/2019 2009 10 NatGas Info

http://slidepdf.com/reader/full/2009-10-natgas-info 16/29

Page 14 PetroBakken Energy Ltd.

Bakken Comparables

Ultimately,thedirectcomparableforPetroBakkenwillbeCrescentPointgiventheyare

thetwolargestlandholdersintheplay.Atcurrentimpliedtradingprices,PetroBakken

tradesslightlybelowandaboveCrescentPoint valuationsona 2010E P/CF andEV/

BOE/Dbasis,respectively.WebelievePetroBakken’soperationalleverageastheleader

ofthetechnologypushinSESaskatchewanwilljustifyhigherfuturerelativevaluations.AlthoughPetroBakkenandCrescentPointaredirectcomparables,theimportanttakeaway

isthattheybothholdcompellinglightoilassetbases.

Chart 9: Average BakkenFirst-Month ProductionRates and Activity by Spud Date

0

25

50

75

100

125

150

175

200

225

250

Q1/07 Q2/07 Q3/07 Q4/07 Q1/08 Q2/08 Q3/08 Q4/08 Q1/09 Q2/09

0

10

20

30

40

50

60

70

80

90

100

C PG # of W ells PBN # o f W ells

C PG M ont h One Prod. Adj PBN M ont h One Prod.

F i r s t M o n t h A v g . ( b

/ d )

N um b e r of W e l l s

Note: PBN production rates and activity are the results o PBG and TOG

Source: BMO Capital Markets, GeoScout

Table 13: BakkenValuation Comparable

Div. Unused Yield Line %

2009E 2010E 2009E 2010E 2009e 2009E 2009eCrescent Point CPG OP 36.55$ 5,475$ 9.0 8.8 176,071 146,182 7.6% 90% 26%Glamis GLM OP 1.73$ 490$ 20.0 8.5 319,180 122,249 0.0% 95% 42%Painted Pony PPY.A NR 4.35$ 123$ 12.1 5.4 na na 0.0% 55% naPetroBakken PBN OP 31.27$ 5,374$ 10.8 8.0 143,873 151,304 3.1% 85% 34%Bakken Peer Group Median 11.5 8.2 88% 34%

% OilPrice

5-OctRating

Mkt Cap

($ mm's)

P/CFPS EV/BOE/D

Note – PBN valuations using implied share price based on TOG closing price

Source: BMO Capital Markets, Company Reports

Bakken Infrastructure

ThesolidoilproductiongrowthproleoftheBakkenplayinSESaskatchewanhasled

tothestagedbuild-outofpipelinetakeawaycapacityintheregion.Enbridgealready

expandedpipelinecapacityby100,000b/din2008to255,000b/dandhasfurtherexpan-

sionplansforanadditional100,000b/dto355,000b/dby2011.Industryplayershave

8/3/2019 2009 10 NatGas Info

http://slidepdf.com/reader/full/2009-10-natgas-info 17/29

PetroBakken Energy Ltd. Page 15

reportedatemporaryuptickinoperatingcostswhenrequiredtotruckoilgivenpipeline

capacityconstraintsinprioryears.Thepositiveimpactfromtheslowdownindrilling

activitylevelsovertheH2/08toH1/09timeperiodishigherpipelinecapacityavailabil-

ity.However,weexpectindustrytorampupproductionandreachcapacitylimitsinthe

nearterm.Ofnote,thesimilarinfrastructurebuild-outthemehastranspiredinNorth

DakotaonrobustBakkenproductiongrowth.InChart11thebarsontherightrepresent

SaskatchewanpipelinecapacityandthebarsontheleftrepresentNorthDakota.

Chart 10: Average Throughput Chart 11: Williston Basin Pipeline Systems – EPSI(Saskatchewan) & EPND (North Dakota)

Source: Enbridge Source: Enbridge

SE Saskatchewan Conventional Inventory

PetroBakkenholdsacomplementaryinventoryofconventionaloilplayopportunities

inSESaskatchewan.Theseopportunitiesprovidequickpayoutsgivenlowdrillingcostswithfuturegrowthpotential throughinlldrilling. Currentproductionfromthe SE

Saskatchewanconventionalplaysis roughly 10,800 boe/d. We havecarried overour

NPVanalysisofTriStar’sconventionalopportunities,whichisbasedontheoperating

assumptionsshownbelow.

Table 14: SE Saskatchewan NPV Per Well Assumptions

Op Cost ($/boe) $6.00Royalty 25%Transportation ($/boe) $1.90

Drill Cost ($ mm) $1.0Discount Rate 10%Rec Reserves (mboe) 100.0Reserve Life (yrs) 8

Per Well Assumptions

Source: BMO Capital Markets

8/3/2019 2009 10 NatGas Info

http://slidepdf.com/reader/full/2009-10-natgas-info 18/29

Page 16 PetroBakken Energy Ltd.

PetroBakkenholds510,000netacresofundevelopedlandprospectiveforconventional

opportunities.Thecompanyestimatesanunbookeddrillinginventoryof238netlocations

asaresultoftheTriStaracquisition.Basedonourprojecteddevelopmentprogramout

to2015,weestimatetheunbookedconventionalinventoryisworth$2.35pershareata

Canadianparcrudeoilpriceof$80/bblandariskedchanceofsuccessof90%.

Table 15: SE Saskatchewan Conventional Unbooked Drilling Inventory NPV Valuation (Cdn. Par $80/bbl)

Drilling Chance of Per F.D. F&D Cost RecycleCore Area Inventory Success Share Per Well Potential ($/boe) Ratio

SE Sask. Conventional 238 90% $2.35 100.0 Mboe 21 MMboe $10.00 4.3x

Risked Reserves

Source: BMO Capital Markets

NEBC Shale Gas: Montney and Horn River

PetroBakken’sresourceportfolioincludesinterestsintheMontneyandHornRivershale

gasplaysinNEBC.Thecompany’sMontneylandsarelocatedintheMoniasarea,where

PetroBakkenholds17netsectionsoflandrepresentingapotentialdrillinginventoryof

67unbookedlocationsatfourwellspersectiontargetingtheUpperMontney.Canadian

NaturalResources(CNQ-TSX)andCrewEnergy(CR-TSX)havedrilledoffsettingwells

toPetroBakkenlandsintheSeptimusarea.

Figure 6: MoniasMontney Acreage

Source: GeoScout

8/3/2019 2009 10 NatGas Info

http://slidepdf.com/reader/full/2009-10-natgas-info 19/29

PetroBakken Energy Ltd. Page 17

Insupportoffuturedevelopment,PetroBakkenownsa5MMcf/dfacilitythatisexpand-

ableto10MMcf/d.Todate,thecompanyhasdrilledahorizontalwellwitha7-stage

frac.PetroBakkenisevaluatingthepotentialforhighdensityfracdevelopmentinthe

Montneyplay.ThecompanyhasdrilleditssecondMontneywellasahorizontalbilat-

eralwellwith33portsreadytobefraced,whichimpliescompellingoptionalityonour

NPVvaluation.Bottomline,theMontneyandHornRivergasplaysarecomplementary

high-impactresourceplaysthatcanbefundedbythecashowgeneratedbytheBakken

uponarecoveryinnaturalgasprices.

Montney NPV Analysis

GiventheearlydaysofPetroBakken’sMontneydrillingprogram,wehaverunaNPV

analysisofthecompany’sMontneywellsusinganindustrypeerproductionprole.

Basedonthisprole,wehaveprojectedanaverage-typecurvebasedonaveragereserve

bookingsof4.0Bcfperwellovera20-yearreservelife.OurNPVanalysisalsoassumes

drillingcostsof$5.0millionperwell,aliquidsratioof30bbl:1MMcfandanall-incash

ownetbackbasedonvariousassumptions.

Table 16: NEBC Montney NPV Per Well Assumptions Op Cost ($/boe) $6.50

Royalty 23%Transportation ($/boe) $1.50

Drill Cost ($ mm) $5.0Discount Rate 10%Rec. Reserves (Bcfe) 4.8Reserve Life (yrs) 20

Per Well Assumptions

Source: BMO Capital Markets, Company Reports

OurNPVanalysisimpliesavaluerangeof$3.3–8.4millionperwellatAECOnatural

gaspriceassumptionsof$5.00–7.00/Mcf.Ourestimatedbreakevennaturalgaspricefor

aMoniasMontneywellislessthan$4.00/Mcf(IRR10%),whichfurtherimproveson

theinclusionofroyaltyincentives.

Table 17: NEBC Montney NPV Per Well Summary $5.00 $6.00 $7.00

NPV (BT-10%) Per Well ($ mm) $3.3 $5.8 $8.4

IRR Per Well (%) 27% 42% 59%Payout (years) 2.5 1.6 1.1

AECO Natural Gas ($/Mcf)

Source: BMO Capital Markets

Basedonourprojecteddevelopmentprogramoutto2014,weestimatetheunbooked

Montneyinventoryisworth$1.39pershareatanAECOnaturalgaspriceof$6.00/Mcf

andriskedchanceofsuccessof80%.

8/3/2019 2009 10 NatGas Info

http://slidepdf.com/reader/full/2009-10-natgas-info 20/29

Page 18 PetroBakken Energy Ltd.

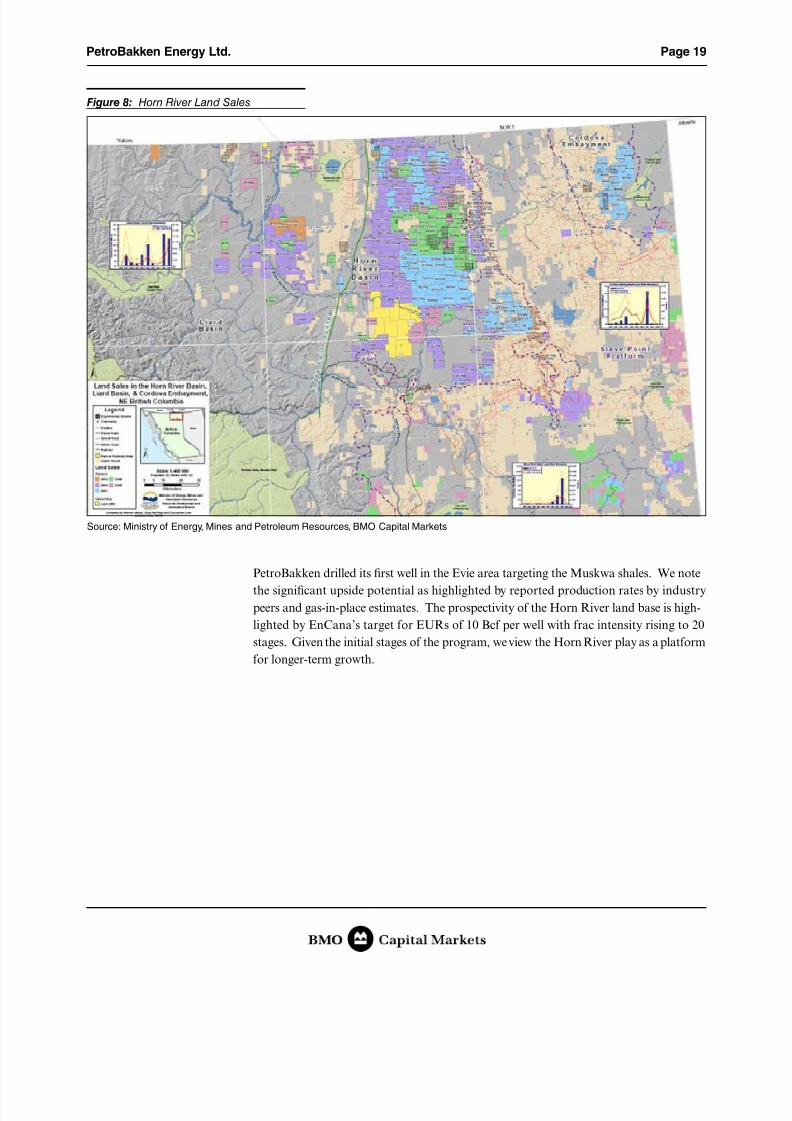

Horn River

PetroBakkenalsomaintainsaninterestintheHornRivershalegasplayinNEBCwhere

itholds84netsectionsof crownrightsintheEvie,SnakeRiverandJuliaarea.TheHorn

River’ssignicantresourcepotentialisduetothehighsilicaandorganiccontentfrom

theEvie,OtterParkandMuskwabasinalshales.

Table 18: Montney Unbooked DrillingInventory NPV Valuation(AECO $6/Mc)

Drilling Chance of Per F.D. F&D Cost RecycleCore Area Inventory Success Share Per Well Potential ($/boe) Ratio

NEBC Montney 67 80% $1.39 4.8 Bcfe 257 Bcfe $6.31 3.3x

Risked Reserves

Source: BMO Capital Markets

Figure 7: Middle andBasal Upper DevonianUnits o the Horn River Basin

Source: Ministry o Energy, Mines and Petroleum Resources

AsshowninFigure8,thesignicantresourcepotentialhasresultedinrecordlandsale

activitywiththebiggestinterestsheldbytheSeniorE&P’sincludingApacheCorp.

(APA-NYSE),DevonEnergyCorp.(DVN-NYSE),EnCanaCorp(ECA-TSX)andEOG

Resources(EOG-NYSE).

8/3/2019 2009 10 NatGas Info

http://slidepdf.com/reader/full/2009-10-natgas-info 21/29

PetroBakken Energy Ltd. Page 19

Figure 8: Horn River Land Sales

Source: Ministry o Energy, Mines and Petroleum Resources, BMO Capital Markets

PetroBakkendrilleditsrstwellintheEvieareatargetingtheMuskwashales.Wenote

thesignicantupsidepotentialashighlightedbyreportedproductionratesbyindustry

peersandgas-in-placeestimates.TheprospectivityoftheHornRiverlandbaseishigh-

lightedbyEnCana’stargetforEURsof10Bcfperwellwithfracintensityrisingto20

stages.Giventheinitialstagesoftheprogram,weviewtheHornRiverplayasaplatform

forlonger-termgrowth.

8/3/2019 2009 10 NatGas Info

http://slidepdf.com/reader/full/2009-10-natgas-info 22/29

Page 20 PetroBakken Energy Ltd.

Horn River NPV Analysis

Ouranalysisofthecompany’sHornRiverwellsarebasedonarecoverablereservesce-

narioof10Bcfovera20-yearreservelife.OurNPVanalysisalsoassumesdrillingcosts

of$10millionperwellandanall-incashownetbackbasedonvariousassumptions.

PetroBakkenholds84netsectionsofundevelopedHornRiveracreage.Giventheexplor-

atorynatureoftheland,wehaveheavilyriskedtheinventorybyassumingonlyone-third

isprospectivefortheHornRiver,whichimpliesadrillinginventoryof112locationsatfourwellspersection.Basedonourprojecteddevelopmentprogramoutto2016,we

estimatetheHornRiverisworth$2.71pershareataatAECOpriceof$6/Mcf anda

riskedchanceofsuccessof50%.

Figure 9: Horn River LandPosition

Source: PetroBakken

Table 19: Horn River Unbooked DrillingInventory NPV Valuation(AECO $6/Mc)

Drilling Chance of Per F.D. F&D Cost RecycleCore Area Inventory Success Share Per Well Potential ($/boe) Ratio

NEBC Horn River 112 50% $2.71 10.0 Bcfe 560 Bcfe $6.03 3.3x

Risked Reserves

Note: Horn River exploration inventory double risked - based on 33% prospective lands and 50%chance o exploration success

Source: BMO Capital Markets

8/3/2019 2009 10 NatGas Info

http://slidepdf.com/reader/full/2009-10-natgas-info 23/29

PetroBakken Energy Ltd. Page 21

H2/09 and 2010 Outlook

PetroBakkencompletedadrillingprogramof89wells(67.3net)consistingof71Bakken

developmentwells(51.4net)inQ3/09.Thecompany’sBakkendrillingprogramincluded

13longbilateralwells,fourofwhichhavebeentiedinwithincreasingproductionrates

andtheremainingwellsexpectedtobecompletedshortly.

PetroBakkencurrentlyhas12rigsoperatingintheBakkenwithsevenrigsexclusively

drilling30-stage(15fracsperleg)bilateralwellsandanotherrigdrillingre-entrywells.

Currentproductionis43,630boe/d.Aspreviouslymentioned,thecompanyexpectsto

sellAlbertaassetscomprisedof9,500boe/dand40.1MMboe.PetroBakkenexpectsto

executeacapitalprogramof$140millioninQ4/09tofund40Bakkenwellsprimarily

consistingofbilateralwells,aswellasninere-entrywells.Assuch,2009exitproduc-

tionisexpectedtobemorethan37,000boe/d(95%lightoil)aftertheplannedAlberta

dispostions.

For2010,PetroBakkenindicatedaninitialcapitalbudgetof$550million,basedona

WTIUS$75/bbloilprice.Thecompanyexpectstoexecuteadrillingprogramof110–130

bilateralBakkenwellswith10–12rigs.PetroBakkenintendstoadoptadividendpolicy

of$0.96perannum(~3%yield),payablemonthly,withtherstdividendtobepaidin

NovembertoshareholdersofrecordonOctober30,2009.

PetroBakken Profle

PetroBakkenwascreatedfromthecombinationofPetrobank’s(PBG-TSX)Canadian

BusinessUnitassetsandTriStarOil&Gas.Specically,PetroBakkenwascapitalized

withPetrobank’sCanadianBusinessUnitassetsalongwith$400millionincashinex-

changefor109.8millioncommonshares(64%ofoutstandingshares).PetroBakkenthen

completedtheacquisitionofTriStarOil&Gasfor$14.75cashor0.5350ofaPetroBak-kenshare.Assuch,theimpliedacquisitionmetrics(netofland)of theTriStardealare

roughly$118,700/boe/d(basedonQ1/09production)and$23.00/boe(2P–basedon2008

reservesandTalismanpropertyacquisition).Onacombinedbasis,PetroBakkenhasthe

followingattributes:

• 2009Eexitproduction of morethan 37,000 boe/d (net of theplanned Alberta

dispositions~9,500boe/d–BMOassumedQ4/09);

• greater thanone million net acresof land and morethan1,300 Bakkenlocations

complementedbyNEBCMontneyandHornRivernaturalgasexposure;

• a$1.05billioncreditfacility;and

• $1.9billionoftaxpools.

8/3/2019 2009 10 NatGas Info

http://slidepdf.com/reader/full/2009-10-natgas-info 24/29

Page 22 PetroBakken Energy Ltd.

Management

PetroBakkenwillbeledbyJohnD.WrightasChairmanandCEO,andR.GreggSmith

asPresidentandCOO.Mr.WrighthasbeenthePresidentandCEOofPetrobanksince

2000andisalsothePresidentandCEOofPetromineralesLtd.Mr.Smithhasbeen

theSeniorVicePresidentandCOO(Canada)ofPetrobanksinceNovember2008.The

seniormanagementteamisroundedoutbyCoreyRuttan(ExecutiveVicePresidentand

CFO),PeterHawkes(VicePresident,Exploration)andRichardPress(VicePresident,

LandandContracts).

TheboardofdirectorsofPetroBakkenconsistsofJohnWright(Chairman),CoreyRut-

tan,KennethMcKinnon,DanThemig,CraigLothian,BrettHerman,MartinHislop

andIanBrown.

Financial Outlook

Weproject2009Eand2010ECFPSof$2.89and$3.92,respectively.Ournancialestimates

arebasedonaverageproductionof42,158boe/din2009Eand40,356boe/d(95%light

oil)in2010E.Petrobakkenplanstodivest9,500boe/dandexit2009at37,000boe/d.Our

workingmodelassumesassetsaleproceedsof$380millionbasedonmetricsof$40,000/

boe/dand$9.50/boeinQ4/09,resultinginyear-endnetdebtof$679millionversusan

approvedcreditlineof$1.05billion.

Table 20: PetroBakken’sFinancial & OperatingSummary

2009E 2010E

EPS (Diluted Continuing) (0.19) 0.85

CFPS (Diluted ) 2.89 3.92

ROCE (%) - Continuing -2% 4%

Net L.T. Liabilities 20% 21%Net Debt/Cash Flow 1.4x 1.1x

Production:

Crude (b/d) 35,978 38,465

Natural Gas (mmcf/d) 37.1 11.3

Production (boe/d) 42,158 40,356

Percentage Gas 15% 5%

Commodity Assumptions:

WTI (US$/bbl) 59.00 70.00

AECO Gas (C$/Mcf) 3.33 4.12

Source: BMO Capital Markets

PetroBakkencurrentlyhas9%of2009Eoilproductionhedgedatanaverageoorand

xedpriceofroughly$75/bbl.For2010E,thecompanycurrentlyhas4%ofoilproduc-

tionhedgedatanaverageoorandxedpriceof$65/bbl.

8/3/2019 2009 10 NatGas Info

http://slidepdf.com/reader/full/2009-10-natgas-info 25/29

PetroBakken Energy Ltd. Page 23

Ourworkingmodelassumesplannedassetsalesof9,500boe/darecompletedinQ4/09,

resultingin year-endnetdebtof $691 millionversusan approvedcreditlineof $1.05

billion.

Table 21: PetroBakken’sIncome Statement

2009E 2010E

Gross Revenue 793.6 976.6

Realized Risk Management Gain/Loss 15.7 1.1

Unrealized Risk Management Gain/Loss (22.1) -

Interest Income 0.1 -

Royalty Expense (111.1) (117.2)

Net Revenue 676.3 860.5

Operating Expense 130.3 117.8

Transportation 15.4 14.7

G&A 32.3 29.5

Interest Expense 24.1 23.5

Stock Based Compensation 27.1 27.1

DD&A 492.4 441.9

Income Before Taxes (45.4) 205.9

Deferred Income Taxes (12.9) 58.5

Current Income taxes (0.1) 0.6

Income Taxes (13.0) 59.1

Net Income (32.3) 146.8

Source: BMO Capital Markets

Table 22: PetroBakken’sCash Flow Statement

2009E 2010E

Net Income (32.3) 146.8

Unrealized Gains/Losses on Derivatives 22.1 -

Stock Based Compensation 27.1 27.1

DD&A 492.4 441.9

Deferred Taxes (12.9) 58.5

Cash Flow from Operations 496.4 674.3

Net Change in Long Term Debt (293.9) 40.7

Dividends (82.5) (165.0)

Issue of Common Shares - -

Cash From Financing Activities (376.4) (124.3)

Expenditures on PP&E (500.0) (550.0)

Dispositions 380.0 -

Cash Outlays (Net Investment) (120.0) (550.0)

Increase/(Decrease) in Cash - -

Cash - Open 4.6 4.6

Cash - Close 4.6 4.6

Source: BMO Capital Markets

8/3/2019 2009 10 NatGas Info

http://slidepdf.com/reader/full/2009-10-natgas-info 26/29

Page 24 PetroBakken Energy Ltd.

Valuation

BasedonTriStar’sclosingprice,Petrobakkensharesaretradingat8.0xP/CFPSand9.1x

EV/EBITDA*.Ourtargetpriceissupportedbyoursum-of-partsconsolidatedvalueof

$35.72pershareusingaatlong-termCanadian.Parcrudepriceof$80/bblandAECO

naturalgaspriceassumptionof$6.00/Mcf.Ourunbookeddrillinginventoryvaluation

isbasedonthedetailedperwellNPV(BT-10%)analysisofthecompany’sBakkenand

ConventionalplaysinSESaskatchewan,aswellastheNEBCMontneyandHornRiver

plays.Ourriskedanalysissumstototalunbookedresourcepotentialof375MMboe.

Table 23: PetroBakken’sBalance Sheet

2009E 2010E

Cash 4.6 4.6

Financial Instruments 20.1 20.1

Accounts Receivable 113.3 113.3

Current Assets 138.0 138.0

Financial Instruments 1.7 1.7

Goodwill 839.9 839.9 Net Property, Plant & Equipment 3,122.3 3,230.4

Total Assets 4,102.0 4,210.1

Accounts Payable 233.2 233.2

Financial Instruments 9.9 9.9

Current Liabilities 243.1 243.1

Bank Debt 586.3 627.0

Deferred Taxes 494.7 553.2

Commodity Derivative Liability 3.6 3.6

Other 4.5 4.5

Site Restoration 53.7 53.7

Subtotal Liabilities 1,385.8 1,485.0

Equity Capital 2,568.1 2,568.1

Contributed Surplus 13.6 40.7

Other 0.5 0.5

Retained Earnings/(Deficit) 133.9 115.7

Subtotal Equity 2,716.1 2,725.0

Total Liabilities and Equity 4,102.0 4,210.1

Source: BMO Capital Markets

* Implied share price based on TOG closing price.

8/3/2019 2009 10 NatGas Info

http://slidepdf.com/reader/full/2009-10-natgas-info 27/29

PetroBakken Energy Ltd. Page 25

Table 24: Intermediate/Junior Oil & Gas Valuation Comparables

Price

Rating 5-Oct 2009E 2010E 2009E 2009E 2010E 2009E 2010E 2008 2009E

Anderson AXL Mkt 0.93 1.25 34% 140 5.3 3.4 0.5 8.8 5.1 28,846 25,134 $6.99 84%

Angle Energy NGL Mkt 5.02 5.50 10% 231 5.8 4.4 0.9 6.5 4.8 31,326 30,411 $9.44 57%Breaker WAV OP 5.33 7.00 31% 278 6.7 4.0 0.7 9.3 5.4 52,097 46,855 $11.36 55%Celtic CLT OP 18.93 23.50 24% 837 7.5 7.1 0.8 11.8 6.8 72,952 57,811 $12.36 73%Compton CMT R R R R R R R R R R R R R RCrew CR OP 8.83 10.00 13% 689 10.1 8.3 0.8 15.0 11.5 66,805 63,326 $10.77 65%Glamis GLM.A OP 1.73 2.75 59% 490 20.0 8.5 0.7 43.7 9.0 319,180 122,249 $10.43 5%Highpine HPX Mkt 7.19 7.00 -3% 482 4.7 4.5 0.9 6.0 5.1 33,267 36,749 $9.34 39%Iteration ITX Mkt 1.20 1.50 25% 253 7.2 3.8 0.4 10.6 6.1 29,435 32,850 $8.77 71%MGM Energy MGX Mkt(S) 0.13 na na 34 na na na na na na na na naNuVista NVA Mkt 12.89 11.00 -15% 1,136 6.0 5.9 0.9 8.8 7.5 57,776 53,903 $13.07 71%Orleans OEX OP 2.40 3.25 35% 149 10.3 6.1 0.6 15.5 7.1 46,886 40,118 $7.79 80%Paramount POU Mkt 14.90 10.25 -31% 1,009 8.0 6.7 1.2 39.6 18.1 65,067 67,442 $7.02 73%PetroBakken PBN OP 31.27 36.00 18% 5,374 10.8 8.0 0.9 12.9 9.1 143,873 151,304 na 15%

Progress PRQ R R R R R R R R R R R R R RStorm SEO OP 14.80 17.25 17% 689 19.5 12.4 0.8 22.3 13.7 98,543 91,523 $17.10 86%Vero VRO OP 4.00 5.00 25% 164 6.0 3.5 0.5 12.5 6.0 38,157 32,803 $11.99 81%

Peer Group Median 7.3 6.0 0.8 12.1 6.9 54,937 50,379 $10.43 71%2009 YTD Avg Transaction Metrics 51,829 $14.18

Most Recent Transaction Metrics - Daylight Resources Trust and Highpine Oil & Gas 37,606 $16.87

EV/BOE/D EV/2P (boe) % Gas

INTERMEDIATE/JUNIOR GROUP

Target ReturnMkt Cap

($ mm's)

P/CFPS P/NAV EV/EBITDA

Note – PBN valuations using implied share price based on TOG closing price

Source: BMO Capital Markets

Investment Risks

PetroBakken’snancialandoperatingresultscanbemateriallyimpactedbyunforeseen

geopoliticalevents,suchaswarorsevereeconomiccontractions,andprolongedextreme

weatherpatterns,whichcanhaveasignicantimpactonenergyprices.

PetroBakkenisalsoexposedtocapital,operatingmaintenanceandremediationexpen-

dituresasaresultof environmentallawsandregulations.Totheextentthatregulatory

requirementsandrelatedexpendituresarenotultimatelymetorprohibitexplorationand

developmentactivities,operatingresultswouldbeadverselyaffected.

Operationally,oilandgaspropertiesmayexperiencesteeper-than-forecastproduction

declines, encounter higher-than-expected water contentor be subjectto unforeseen

downtime,resultinginunscheduledmaintenance,whichcanhaveamaterialimpacton

thecompany’snancialandoperatingresults.

8/3/2019 2009 10 NatGas Info

http://slidepdf.com/reader/full/2009-10-natgas-info 28/29

Page 26 PetroBakken Energy Ltd.

Company Risk Disclosure

Inadditiontotherisksinvolvedininvestingincommonstocksgenerally,wealsohighlightthefollowingrisksthatpertaintothis

company.TriStar’snancialandoperatingresultscanbemateriallyimpactedbyunforeseengeopoliticalevents,suchaswarorsevere

economiccontractions,andprolongedextremeweatherpatterns,whichcanhaveasignicantimpactonenergyprices.TriStarisalso

exposedtocapital,operatingmaintenanceandremediationexpendituresasaresultofenvironmentallawsandregulations.Tothe

extentthatregulatoryrequirementsandrelatedexpendituresarenotultimatelymetorprohibitexplorationanddevelopmentactivities,

operatingresultswouldbeadverselyaffected.

Operationally,oilandgaspropertiesmayexperiencesteeperthanforecastproductiondeclines,encounterhigherthanexpectedwater

contentorbesubjecttounforeseendowntimeresultinginunscheduledmaintenance,whichcanhaveamaterialimpactonthecompany’s

nancialandoperatingresults.Wenotethatanyaccelerationorunforeseendelaysinwelltie-inscanmateriallyimpactproduction

giventherelativelysmallscaleofTriStar’soperationsfor2005.

Analyst’s Certication

I,MarkLeggett,CFA,herebycertifythattheviewsexpressedinthisreportaccuratelyreectmypersonalviewsaboutthesubject

securitiesorissuers.Ialsocertifythatnopartofmycompensationwas,is,orwillbe,directlyorindirectly,relatedtothespecicrecom-

mendationsorviewsexpressedinthisreport.

General Disclosure

TheinformationandopinionsinthisreportwerepreparedbybothBMONesbittBurnsInc.andBMONesbittBurnsLtée./Ltd.,col-

lectively(“BMONB”)andBMOCapitalMarketsLimited(U.K.),(“BMOCMLtd”).BMONBandBMOCMLtd.arenotsubjecttoU.S.ruleswithregardtothepreparationofresearchreportsandtheindependenceofanalysts.“BMOCapitalMarkets”isatrade

nameusedbytheBMOInvestmentBankingGroup,whichincludesthewholesalearmofBankofMontrealanditssubsidiariesBMO

NBinCanada,BMOCapitalMarketsLtd.intheU.K.andBMOCapitalMarketsCorp.intheU.S.BMOCapitalMarketsLtd.and

BMOCapitalMarketsCorp.areafliatesof BMONB.BankofMontrealoritssubsidiaries(“BMOFinancialGroup”)haslending

arrangementswith,orprovideotherremuneratedservicesto,manyissuerscoveredbyBMONBresearch.Asignicantlendingrelation-

shipmayexistbetweenBMOFinancialGroupandcertainoftheissuersmentionedherein.Theopinions,estimatesandprojections

containedinthisreportarethoseof BMONBandBMOCMLtd.asofthedateofthisreportandaresubjecttochangewithout

notice.BMONBandBMOCMLtd.endeavourtoensurethatthecontentshavebeencompiledorderivedfromsourcesthatwebelieve

arereliableandcontaininformationandopinionsthatareaccurateandcomplete.However,BMONBandBMOCMLtd.makeno

representationorwarranty,expressorimplied,inrespectthereof,takesnoresponsibilityforanyerrorsandomissionscontainedherein

andacceptsnoliabilitywhatsoeverforanylossarisingfromanyuseof,orrelianceon,thisreportoritscontents.Informationmaybe

availabletoBMONB,BMOCMLtdoritsafliatesthatisnotreectedinthisreport.Theinformationinthisreportisnotintended

tobeusedastheprimarybasisofinvestmentdecisions,andbecauseofindividualclientobjectives,shouldnotbeconstruedasadvice

designedtomeettheparticularinvestmentneedsofanyinvestor.Thismaterialisforinformationpurposesonlyandisnotanofferto

sellorthesolicitationofanoffertobuyanysecurity.Theresearchanalystand/orassociateswhopreparedthisreportarecompensated

basedupon(amongotherfactors)theoverallprotabilityofBMONB,BMOCMLtd.anditsafliates,whichincludestheoverall

protabilityofinvestmentbankingservices.BMONB,BMOCMLtd.,oritsafliatesexpecttoreceiveorwillseekcompensationfor

investmentbankingserviceswithinthenext3monthsfromallissuerscoveredbyBMONB.BMONB,BMOCMLtd.oritsafliates

willbuyfromorselltocustomersthesecuritiesofissuersmentionedinthisreportonaprincipalbasis.BMONB,BMOCMLtd.or

itsafliates,ofcers,directorsoremployeesmayhavealongorshortpositioninthesecuritiesdiscussedherein,relatedsecuritiesor

inoptions,futuresorotherderivativeinstrumentsbasedthereon.ThereadershouldassumethatBMONB,BMOCapitalMarkets

Ltd.,BMOCapitalMarketsCorp.,BankofMontrealortheirafliatesmayhaveaconictofinterestandshouldnotrelysolelyon

thisreportinevaluatingwhetherornottobuyorsellsecuritiesofissuersdiscussedherein.

Company Specic Disclosures

Disclosure3:BMONBhasprovidedinvestmentbankingserviceswithrespecttothisissuerwithinthepast12months.

Disclosure7:BMOCapitalMarketsCorp.oranafliatehasreceivedcompensationforinvestmentbankingservicesfromthisissuer

withinthepast12months.

Disclosure10A:Thisissuerisaclient(orwasaclient)ofBMONB,BMOCapitalMarketsCorp.oranafliatewithinthepast12

months:InvestmentBankingServices

Disclosure16:Aredacteddraftofthisreportwaspreviouslyshowntotheissuer(forfactcheckingpurposes)andchangesweremade

tothereportbeforepublication.

8/3/2019 2009 10 NatGas Info

http://slidepdf.com/reader/full/2009-10-natgas-info 29/29

PetroBakken Energy Ltd. Page 27

Distribution o Ratings (September 10, 2009)

Rating BMO BMO BMO Starmine

Category Rating Universe I.B. Clients* Universe**

Buy Outperform 36% 48% 48%Hold MarketPerform 55% 48% 44%

Sell Underperform 9% 4% 8%

* Reflects rating distribution of all companies where BMO Capital Markets has received compensation for Investment Bankingservices.

**ReectsratingdistributionofallNorthAmericanequityresearchanalysts.

Ratings Key

Weusethefollowingratingssystemdenitions:

OP=Outperform-Forecasttooutperformthemarket;

Mkt=MarketPerform-Forecasttoperformroughlyinlinewiththemarket;

Und=Underperform-Forecasttounderperformthemarket;

(S)=speculativeinvestment;

NR=Noratingatthistime;

R=Restricted–Disseminationofresearchiscurrentlyrestricted.

MarketperformanceismeasuredbyabenchmarkindexsuchastheS&P/TSXCompositeIndex,S&P500,NasdaqComposite,as

appropriateforeachcompany.PriortoSeptember1,2003,afourthratingtier—TopPick—wasusedtodesignatethosestockswe

feltwouldbethebestperformersrelativetothemarket.OursixTop15listswhichguideinvestorstoourbestideasaccordingtosix

differentobjectives(large,small,growth,value,incomeandquantitative)havereplacedtheTopPickrating.

Dissemination o Research

Ourresearchpublicationsareavailableviaourwebsitehttp://bmocapitalmarkets.com.Institutionalclientsmayalsoreceiveourresearch

viaFIRSTCALLResearchDirectandReuters.AllofourresearchismadewidelyavailableatthesametimetoallBMONB,BMO

CapitalMarketsLtd.,BMOCapitalMarketsCorp.andBMONesbittBurnsSecuritiesLtd.clientgroupsentitledtoourresearch.

Pleasecontactyourinvestmentadvisororinstitutionalsalespersonformoreinformation.

Confict Statement

AgeneraldescriptionofhowBMOFinancialGroupidentiesandmanagesconictsofinterestiscontainedinourpublicfacingpolicy

formanagingconictsof interestinconnectionwithinvestmentresearchwhichisavailableathttp://research-ca.bmocapitalmarkets.

com/Conict_Statement_Public.asp

Additional Matters

TOU.S.RESIDENTS:BMOCapitalMarketsCorp.and/orBMONesbittBurnsSecuritiesLtd.,afliatesofBMONB,furnishthis

reporttoU.S.residentsandacceptresponsibilityforthecontentsherein,excepttotheextentthatitreferstosecuritiesofBankof

Montreal.AnyU.S.personwishingtoeffecttransactionsinanysecuritydiscussedhereinshoulddosothroughBMOCapitalMarkets

Corp.and/orBMONesbittBurnsSecuritiesLtd.

TOU.K.RESIDENTS:IntheUKthisdocumentispublishedbyBMOCapitalMarketsLimitedwhichisauthorisedandregulated

bytheFinancialServicesAuthority.Thecontentshereofareintendedsolelyfortheuseof,andmayonlybeissuedorpassedonto,

(I)personswhohaveprofessionalexperienceinmattersrelatingtoinvestmentsfallingwithinArticle19(5)oftheFinancialServices

andMarketsAct2000(FinancialPromotion)Order2005(the“Order”)or(II)highnetworthentitiesfallingwithinArticle49(2)(a)to(d)oftheOrder(allsuchpersonstogetherreferredtoas“relevantpersons”).Thecontentshereofarenotintendedfortheuseof

andmaynotbeissuedorpassedonto,retailclients.

BMONesbittBurnsInc.andBMONesbittBurnsLtée/Ltd.areMembersofCIPF.BMOCapitalMarketsCorp.andBMONesbitt

BurnsSecuritiesLtd.areMembersofSIPC.

“BMOCapitalMarkets”isatrade-markofBankofMontreal,usedunderlicence.

“BMO(M-Barroundelsymbol)”isaregisteredtrade-markofBankof Montreal,usedunderlicence.

R38126