2 CHAPTER COST BEHAVIOR AND COST ESTIMATION photo: © Tischenko Irina/Shutterstock.

36

2 CHAPTER COST BEHAVIOR AND COST ESTIMATION p hoto : © Tisc henk o I rina /Shu tter stoc k

-

Upload

sybil-mosley -

Category

Documents

-

view

223 -

download

0

Transcript of 2 CHAPTER COST BEHAVIOR AND COST ESTIMATION photo: © Tischenko Irina/Shutterstock.

2CHAPTER

COST BEHAVIOR ANDCOST ESTIMATION

photo: © Tischenko Irina/S

hutterstock

2

UNIVERSAL SPORTS’ INCOME STATEMENT

Sales $ 1,039,500

COGS 769,230

Gross Profit $ 270,270

Selling and administrative expense 230,370

Operating income $ 39,900

Tax expense (30%) 11,970

Net Income $ 27,930

What would Universal Sports’ net income be if it met the original sales volume projection?

COST BEHAVIOR PATTERNS

Unit 2.1

21.Unit 2.2 Unit 2.3

© Tom

wang112 / iS

tockphoto

2

4 TYPES OF COST BEHAVIOR

► Variable► Fixed► Step-Variable► Mixed

2

IT’S TIME FOR A STUDY BREAK!

You’ve been studying for several hours and are getting ready to take a study break, so you break open a nice cold can of soda. Just then the doorbell rings and in come three friends.

2

HERE’S THE DRINK BILL

Friends Cost per can Total cost

1 $0.75 $0.75

2 $0.75 $1.50

3 $0.75 $2.25

4 $0.75 $3.00

2

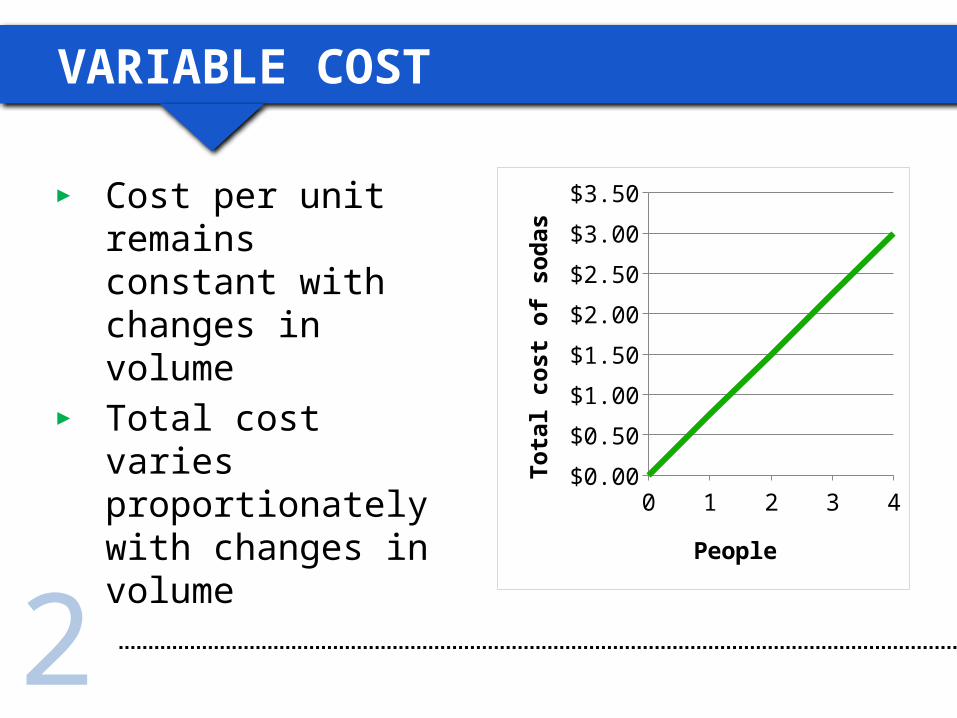

VARIABLE COST

0 1 2 3 4$0.00

$0.50

$1.00

$1.50

$2.00

$2.50

$3.00

$3.50

PeopleTo

tal c

ost o

f sod

as

► Cost per unit remains constant with changes in volume

► Total cost varies proportionately with changes in volume

2

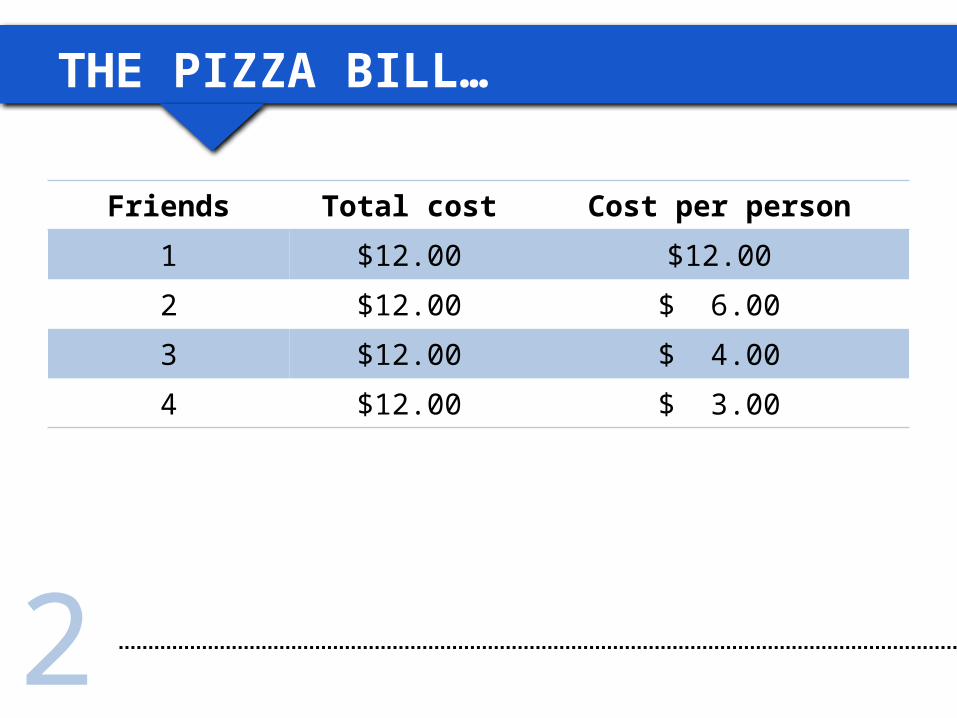

LET’S ORDER PIZZA!

The soda didn’t do the trick, so you order a $12 large pizza from your favorite pizza place.

2

THE PIZZA BILL…

Friends Total cost Cost per person

1 $12.00 $12.00

2 $12.00 $ 6.00

3 $12.00 $ 4.00

4 $12.00 $ 3.00

2

FIXED COST

► Total cost remains constant with changes in volume

► Unit cost changes inversely with changes in volume

► Fixed relationship only holds over the relevant range

0 1 2 3 4$0.00

$2.00

$4.00

$6.00

$8.00

$10.00

$12.00

$14.00

PeopleTo

tal c

ost o

f piz

zas

2

REMEMBER TO KEEP IT CONSTANT

Friends Cost per can Total cost

1 $0.75 $ 0.75

2 $0.75 $ 1.50

3 $0.75 $ 2.25

4 $0.75 $ 3.00

Friends Cost per person Total cost

1 $12.00 $12.00

2 $ 6.00 $12.00

3 $ 4.00 $12.00

4 $ 3.00 $12.00

Variable Cost

Fixed Cost

2

COMMITTED VS. DISCRETIONARY

► Depends on the time frame over which the costs are incurred and fixed.

10-year factory lease

COMMITTED6-month advertising

DISCRETIONARY

CAUTIONWhat effect will reducing the cost to $0 have on the long-term health of the company?

2

STEP-VARIABLE COST

0501

10011501

2001$0

$70,000

$140,000

$210,000

$280,000

$350,000

$420,000

Enrolled Students

Tota

l Cos

t

► Cost remains fixed in total over small range of volume or activity

► These small ranges are smaller than the relevant range of fixed cost

2

MIXED COST

► Cost contains both fixed and variable components

► Total cost AND unit cost varies with changes in volume

0 25 50 75 100$0

$200

$400

$600

$800

$1,000

$1,200

$1,400

GuestsTo

tal c

ost o

f ban

quet Meals = $10 per person

Room rental = $200

Meals are a variable cost

Room rental is a fixed cost

2

Friends Total cost (room and meal) Cost per guest

25 $ 450 $18.00

50 $ 700 $14.00

75 $ 950 $12.67

100 $1,200 $12.00

MIXED COST EXAMPLE

► Variable cost = $10 per person► Fixed cost = $200.00

COST ESTIMATION

Unit 2.1

22.Unit 2.2 Unit 2.3

© Tom

wang112 / iS

tockphoto

2

REVISITING COST BEHAVIOR

How do we break a mixed cost into its fixed and variable components?

$

Activity Level

Slope = variable cost p

er unit

Y-intercept = total fixed cost

2

MIXED COST REALITY

2

WHICH LINE BEST ESTIMATES TOTAL COST?

2

THE SCATTERGRAPH METHOD

2

MIXED COST FORMULA

Where:► y is total cost► m is the variable cost per unit► x is the level of activity (number of units)► b is total fixed cost

y = mx + b

2

THE SCATTERGRAPH METHOD

$4,000 – $2,6002,500 – 1,500

= 1.4

b = $500

y = $1.40x + $500

2

THE HIGH-LOW METHOD

► This is an algebraic method to break out the fixed and variable components of a mixed cost

► Based on two extreme points during a period – the highest activity level and the lowest activity level

2

THE MECHANICS OF HIGH-LOW

► STEP 1: Find the high and low points in terms of activity level

► STEP 2: Compute the variable cost per unit► STEP 3: Calculate the fixed cost using either the

high point or the low point.► STEP 4: Complete the cost equation y = mx + b.

2

$4,800 = $1.50(2,800) + FC

FC = $600.00

DO THE HIGH-LOW# of

DeliveriesTotal Delivery

Cost

Jan 2,000 $3,650

Feb 985 $1,875

Mar 1,500 $2,600

April 2,500 $4,000

May 800 $1,400

June 600 $1,500

July 2,800 $4,800

Aug 1,200 $2,125

Sept 1,350 $2,200

Oct 725 $1,600

Nov 1,850 $3,050

Dec 2,200 $3,400

$4,800 - $1,500

2,800 - 600= $1.50 / Delivery

LOW

HIGH

Total cost = ($1.50 × Number of deliveries) + $600.00

2

WHAT IS THE ESTIMATED TOTAL COST AT 1,500 DELIVERIES?

Why is this different from the $2,600 total costs actually incurred in March?

($1.50 x 1,500) + $600 = $2,850

2

THE HIGH LOW IS JUST AN ESTIMATE

March

2

REGRESSION ANALYSIS

► Statistical technique to calculate variable and fixed components of mixed costs

► Gives the “best” line that fits a set of cost points► Easy to do with Excel

2

REGRESSION WITH EXCEL – VARIABLE COST

2

REGRESSION WITH EXCEL – FIXED COSTS

CONTRIBUTION MARGINANALYSIS

Unit 2.1

23.Unit 2.2 Unit 2.3

© Tom

wang112 / iS

tockphoto

2

WHAT IS “CONTRIBUTION MARGIN”?

► Sales Revenue – Total Variable Expenses► Contribution margin is the revenue remaining to

cover fixed expenses and provide profit after variable expenses have been covered

► Contribution Margin Ratio =Contribution Margin

Sales Revenue

2

CONTRIBUTION INCOME STATEMENT

Sales Revenue

- Variable Expenses

= Total Contribution Margin

- Total Fixed Expenses

= Operating Income

2

LET’S BUILD A CM INCOME STATEMENT

2

HERE IT IS…

2

A BETTER FORMAT