3 CHAPTER COST-VOLUME-PROFIT ANALYSIS AND PRICING DECISIONS photo: © Tischenko Irina/Shutterstock.

34

3 CHAPTER COST-VOLUME-PROFIT ANALYSIS AND PRICING DECISIONS p hoto : © Tisc henk o I rin a/S h u t t er sto ck

-

Upload

lonnie-legate -

Category

Documents

-

view

222 -

download

2

Transcript of 3 CHAPTER COST-VOLUME-PROFIT ANALYSIS AND PRICING DECISIONS photo: © Tischenko Irina/Shutterstock.

3CHAPTER

COST-VOLUME-PROFIT ANALYSISAND PRICING DECISIONS

photo: © Tischenko Irina/S

hutterstock

3

MARKETING WANTS ANOTHER $50,000

► What will they do with it?► How will it affect sales volume?► What is the impact on our bottom line?

© Tom

wang112 / iS

tockphoto

BREAKEVEN ANALYSIS

Unit 3.1

31.Unit 3.2 Unit 3.3 Unit 3.4

3

WHAT DOES IT MEAN TO “BREAK EVEN”

► Total revenues = total expenses► Profit = $0► There is one sales volume at which this

relationship is true► This is called the “breakeven point”

3

TO CALCULATE THE BREAKEVEN POINT

► Use the equation approach

• Solve for units sold, which equals the breakeven point• Why is profit set to $0?

Sales Revenue – Variable expenses – Fixed expenses = Operating income

(SP×units sold) – (VC×units sold) – FC = $0

[(SP – VC)×(units sold)] – FC = $0

(CM/unit×units sold) – FC = $0

$20x - $16x - $168,000 = $0

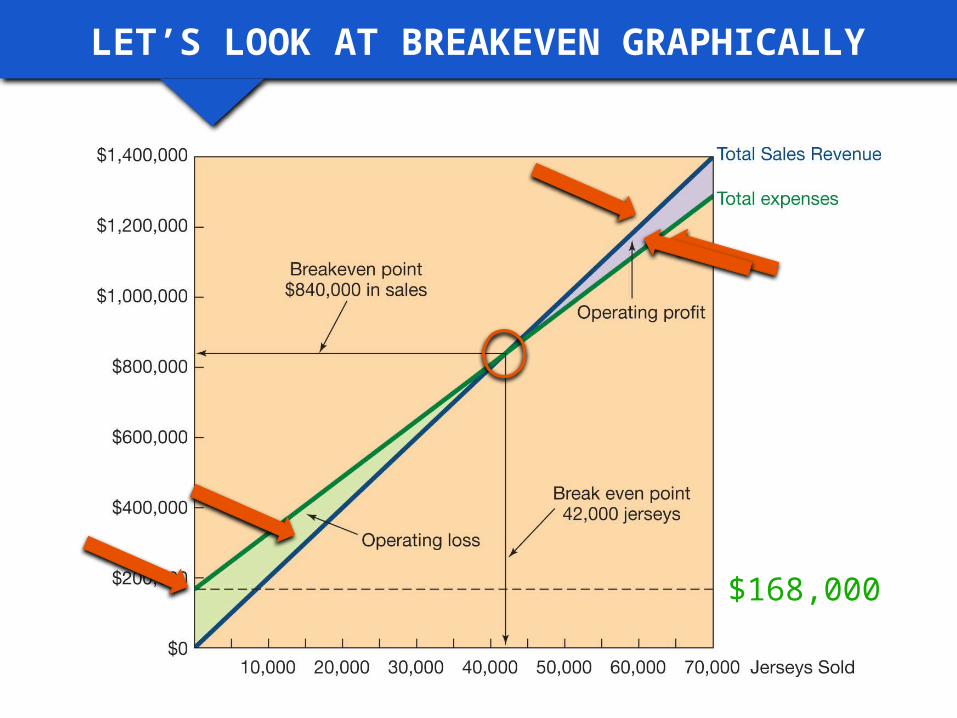

x = 42,000 jerseys

BREAKEVEN POINT FOR UNIVERSAL SPORTS EXCHANGE

$4x - $168,000 = $0

BREAKEVEN POINT FOR UNIVERSAL SPORTS EXCHANGE

3

FCCM/Unit

= Breakeven in units

SHORTCUTS…

$168,000

$4= 42,000 jerseys

3

SHORTCUTS…

FCCMR

= Breakeven in sales $

$168,000

0.2= $840,000

LET’S LOOK AT BREAK EVEN GRAPHICALLY

$168,000

LET’S LOOK AT BREAKEVEN GRAPHICALLY

3

Current sales – Breakeven sales

MARGIN OF SAFETY

What does this mean?

$1,050,000 – $840,000 = $210,000

52,500 – 42,000 = 10,500 jerseys

© Tom

wang112 / iS

tockphoto

C-V-P ANALYSIS

Unit 3.1

32.Unit 3.2 Unit 3.3 Unit 3.4

3

LET’S REVIEW THE PROFIT EQUATION

– VC×(units sold)SP×(units sold) – FC = OI

3

HOW MUCH DO I HAVE TO SELL TO MAKE $X?

► This is called the “target income” question► Use the profit equation

► Use the breakeven formula and treat your target pretax income as additional fixed costs

FC + Target Income

CM / unit = required sales volume

To find the sales dollars required to attain the target income, use the CMR rather than the CM / unit.

(SP×units sold) – (VC×units sold) – FC = $X

3

WHAT ABOUT TARGET NET INCOME?

► You must adjust net income to pretax income► Divide target net income by (1 - tax rate)► Solve as before

Total FC +

= required sales volumeCM / unit

Target net income

1 – tax rate

3

CVP ANALYSIS

► Stands for cost-volume-profit► A tool to determine the impact of changes in sales

volume, costs, or sales mix on net income► Useful for evaluating decision alternatives

3

THREE APPROACHES TO CVP

► Prepare a contribution format income statement before and after implementing the changes

► Prepare a partial contribution format income statement that includes only those items that change (called the “incremental approach”)

► Compare the current total contribution margin with the proposed total contribution margin, then adjust for changes in fixed expenses

3

CVP AND THE SUPPLY CHAIN

► How do the CVP decisions of supply chain partners affect each other?

► For example, consider the jerseys that Universal Sports Exchange purchases from C&C Sports.• What happens if C&C Sports increases the selling

price?• What happens if Universal Sports Exchange decides

to use a cheaper supplier?

3

OPERATING LEVERAGE

► Firms sometimes have the option to trade fixed costs for variable costs

► Higher levels of fixed costs introduce higher levels of risk

► Measures the magnitude of change in operating income for a given percentage change in sales revenue

Degree of operating leverage =Contribution margin

Net operating income

WHY DO WE CARE ABOUT OPERATING LEVERAGE?WHY DO WE CARE ABOUT OPERATING LEVERAGE

© Tom

wang112 / iS

tockphoto

MULTIPRODUCT C-V-P ANALYSIS

Unit 3.1

33.Unit 3.2 Unit 3.3 Unit 3.4

3

MULTIPRODUCT CVP

► Rarely does a company produce a single product► Since not every product will have the same

contribution margin, we have a problem when more than one product is produced

3

WHAT IS “SALES MIX”?

► The “bag” or “package” of goods sold► For example:

• For every dining room table sold, the company also sells 4 chairs

• For every computer sold, the company also sells a monitor and a printer

• For every pair of athletic shoes sold, Landon Sports sells 4 baseball jerseys

3

USE THE PROFIT EQUATION…WITH ADJUSTMENTS

CM(jerseys) + CM(shoes) – FC = OI

Product PriceVariable

CostContribution

Margin

Jerseys $20 $16.00 $4.00

Shoes $45 $38.70 $6.30

3

DETERMINE THE SALES MIX

$4.00(4x) + $6.30(x) – FC = OI

ProductContribution

Margin Sales MixAdjusted

Contribution Margin

Jerseys $4.00 4x $16.00x

Shoes $6.30 1x $ 6.30x

$16x + $6.30x – FC = OI

Jerseys Shoes4 1:

3 $22.30x = $178,400

$16x + $6.30x – $178,400 = $0

CALCULATING THE BREAKEVEN POINT

ProductContribution

Margin Sales MixAdjusted

Contribution Margin

Jerseys $4.00 4x $16.00x

Shoes $6.30 1x $ 6.30x

x = 8,000 shoes 4x = 4(8,000) = 32,000 jerseys

3

LIMITING ASSUMPTIONS OF CVP ANALYSIS

► All costs can be divided into fixed and variable components

► All cost and profit functions are linear throughout the relevant range

► Sales mix will remain constant

3

CHANGES EXAMINED USING CVP

► Change in sales price► Change in sales volume► Change in variable costs per unit► Change in fixed costs► Change in sales mix► Any combination of the above

Remember to always use “constant” forms – SP/unit, VC/unit, Total FC – when doing CVP analysis

© Tom

wang112 / iS

tockphoto

PRICING DECISIONS

Unit 3.1

34.Unit 3.2 Unit 3.3 Unit 3.4

3

ECONOMICS OF PRICE

Market equilibrium

3

COST-PLUS PRICING

► Start with the cost to produce the product► Add a markup to the cost to arrive at price► Be clear about what cost you use in the markup

calculation

Product Cost+ Markup= Sales Price

3

CALCULATING MARKUP PERCENTAGE

Sales price – Cost

Cost= Markup %

$20.00 - $14.80

$14.80= 35%

3

$36.00 + $12.60 = $48.60

CALCULATING PRICE USING MARKUP %

Cost

$36.00 + ($36.00 × 35%) = Price

Markup amount

+ (Cost × Markup %) = Price

3

ISSUES WITH COST-PLUS PRICING

► What if customers are willing to pay more than the calculated price?

► Cost-plus pricing does not recognize the value provided to the customer; it recognizes a return to the seller

► The costs of the seller’s inefficiencies are borne by the customers

3

TARGET COSTING

► Start with an estimate of the price customers will pay• Subtract the desired markup• The result is the target, or maximum, product cost

► This is calculated before the product is designed and manufactured

► If you can produce the product for the target cost, go forward

![Shutterstock 288500075 [Converted]](https://static.fdocuments.in/doc/165x107/56d6bf4b1a28ab301695ab2f/shutterstock-288500075-converted.jpg)