09.10.2011 What opportunities exist for private equity investors within Mongolia, Masa Igata

14

I N T R O D U C T I O N T O M O N G O L I A Securities Discover Mongolia’s investment opportunities 1 1 December 8 – 9, 2011 By Masa Igata, Founder & CEO Frontier Securities M O N G O L I A I N V E S T M E N T S U M M I T 2 0 1

-

Upload

the-business-council-of-mongolia -

Category

Business

-

view

230 -

download

0

Transcript of 09.10.2011 What opportunities exist for private equity investors within Mongolia, Masa Igata

I N T R O D U C T I O N T O M O N G O L I A

Securities

Discover Mongolia’s investment opportunities

2 0

1 1

December 8 – 9, 2011

Discover Mongolia’s investment opportunitiesBy Masa Igata, Founder & CEO Frontier Securities

M O

N G

O L

I A

I N

V E

S T

M E

N T

S

U M

MI T

2

0 1

1

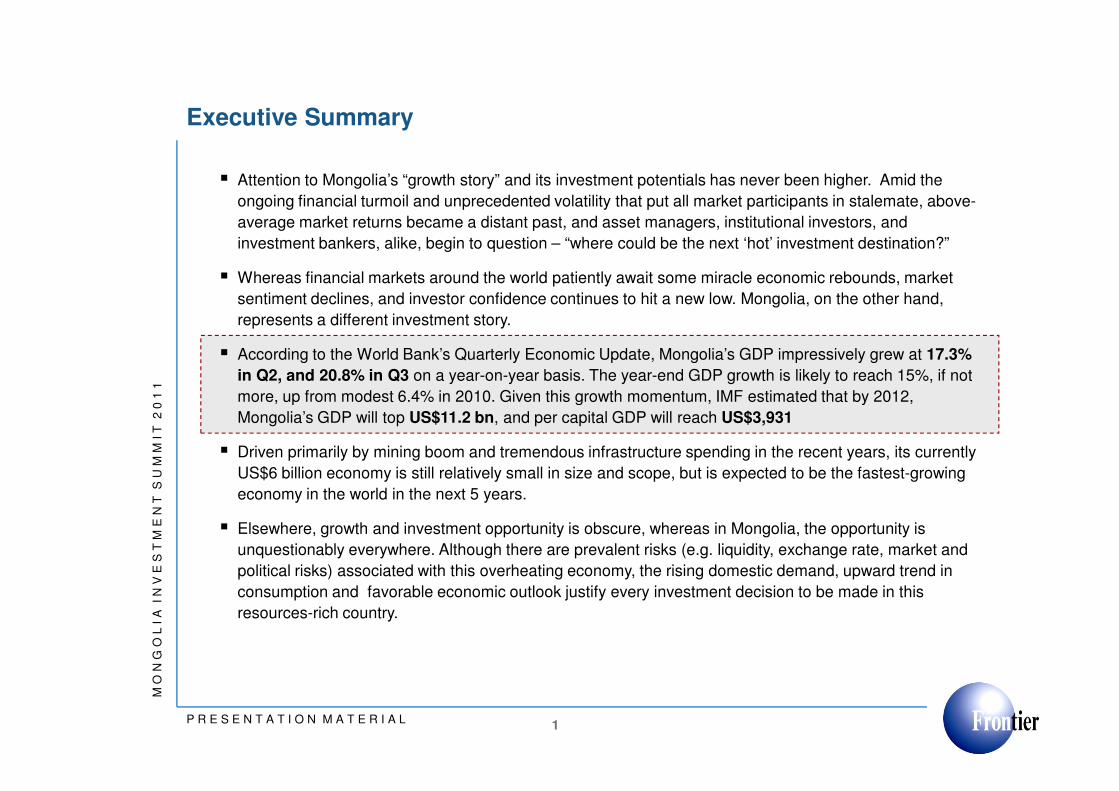

Executive Summary

� Attention to Mongolia’s “growth story” and its investment potentials has never been higher. Amid the

ongoing financial turmoil and unprecedented volatility that put all market participants in stalemate, above-

average market returns became a distant past, and asset managers, institutional investors, and

investment bankers, alike, begin to question – “where could be the next ‘hot’ investment destination?”

� Whereas financial markets around the world patiently await some miracle economic rebounds, market

sentiment declines, and investor confidence continues to hit a new low. Mongolia, on the other hand,

represents a different investment story.

� According to the World Bank’s Quarterly Economic Update, Mongolia’s GDP impressively grew at 17.3%

in Q2, and 20.8% in Q3 on a year-on-year basis. The year-end GDP growth is likely to reach 15%, if not

more, up from modest 6.4% in 2010. Given this growth momentum, IMF estimated that by 2012,

2 0

1 1

1

more, up from modest 6.4% in 2010. Given this growth momentum, IMF estimated that by 2012,

Mongolia’s GDP will top US$11.2 bn, and per capital GDP will reach US$3,931

� Driven primarily by mining boom and tremendous infrastructure spending in the recent years, its currently

US$6 billion economy is still relatively small in size and scope, but is expected to be the fastest-growing

economy in the world in the next 5 years.

� Elsewhere, growth and investment opportunity is obscure, whereas in Mongolia, the opportunity is

unquestionably everywhere. Although there are prevalent risks (e.g. liquidity, exchange rate, market and

political risks) associated with this overheating economy, the rising domestic demand, upward trend in

consumption and favorable economic outlook justify every investment decision to be made in this

resources-rich country.

P R E S E N T A T I O N M A T E R I A L

M O

N G

O L

I A

I N

V E

S T

M E

N T

S

U M

MI T

2

0 1

1

Mongolia: country profile1

Young, democratic and resources-rich country sandwiched by Russia and China

Territory: 19th largest country - 1,565,000 km2Population: 135th in the world3.1 millions (July 2011 est.)1.8 people/km2 on average180 people/km2 in the capital, Ulaanbaatar cityTerrain: Vast semi-desert and desert plains, grassy steppe, mountains in west and southwest; Gobi Desert in south-centralLandlocked; strategic location between China and Russia

2 0

1 1

2P R E S E N T A T I O N M A T E R I A L

Russia

Political structure: Parliamentary democracy from 1991, 2 large parties (MPP and Democratic Party)Current Prime Minister: S. Batbold (MPP), 2008 election results: MPP 46, DP 27, others 3Current President: Ts. Elbegdorj (nominated from DP) in office since 2008Next Elections: June 2012

Main Religions: Buddhist (90%), Muslim (5%), Shamanist and Christian (5%)Life expectancy: Men – 66 years old, Women – 71 Literacy rate: 97.8%

Currency: Tögrög (1,315₮ = US$1 as of Nov 18th, 2011)Inflation: 11.9% (as of Sept 2011)GDP*: US$6.24 bn (2010, IMF)Growth rate: 20.8% yoy (Q3:2011)Per capita GDP*: $2,267 (2010, IMF)No capital controls, free press and internet

Source: 1) Unless stated otherwise, all economic figures are obtained from the World Bank’s Mongolia Quarterly Update (October 2011)

Note: “GDP” and “Per capita GDP” statistics are in current prices

M O

N G

O L

I A

I N

V E

S T

M E

N T

S

U M

MI T

2

0 1

1

Mongolia’s GDP surged 20.8% yoy in Q3:2011, and robust growth is expected to continue

With OT and TT operating at full capacity, Mongolia is the fasting-growing economy in the next 5 years

0

5

10

15

20

25

4,000

5,000

6,000

7,000

8,000

9,000

10,000

%MNT bn 1990 – 2016F real GDP (constant price of 2005) and GDP growth

Inception of OyuTolgoi

Tavan Tolgoi at full capacity

2 0

1 1

3P R E S E N T A T I O N M A T E R I A L

Source: IMF estimates (September 2011)

-15

-10

-5

0

0

1,000

2,000

3,000

GDP (MNT bn) % GDP growth

2008 2009 2010 2011F 2012F 2013F 2014F 2015F 2016F

Mongolia % GDP Growth

8.9% -1.3% 6.4% 11.5% 11.8% 19.3% 14.8% 9.3% 15.6%

M O

N G

O L

I A

I N

V E

S T

M E

N T

S

U M

MI T

2

0 1

1

GDP breakdown by sector: 2009 vs 2010

While mining sector is the main driving force, emerging opportunities in other sectors exist

164

369

51

68

206

240

95

21

19

455

Financial and insurance activities

Real estate activities

Professional, scientific and …

Administrative and support …

Public administration and …

Education

Human health and social work …

Arts, entertainment and recreation

Other service activities

Net taxes on products

2009 GDP by sectors at current pricesUS$5,070 mm*

122

394

54

77

232

266

107

24

21

771

Financial and insurance activities

Real estate activities

Professional, scientific and …

Administrative and support …

Public administration and …

Education

Human health and social work …

Arts, entertainment and recreation

Other service activities

Net taxes on products

2010 GDP by sectors at current pricesUS$6,350 mm*

I T

2

0 1

1

4P R E S E N T A T I O N M A T E R I A L

Source: National Statistics Office (NSO) – Macroeconomic Statistical Indicators

Note: * Exchange rate attributes to discrepancy in GDP figures (US$ = 1,300 MNT).

� Mining sector contributes to nearly 20% of the country’s GDP composition

� Non-mining sectors, especially services industry, are also gaining momentum in the recent years

906

989

327

121

20

66

333

421

34

166

164

0 500 1,000 1,500

Agriculture, forestry and fishing

Mining and quarrying

Manufacturing

Electricity, gas, steam and air …

Water supply; sewerage, waste …

Construction

Wholesale and retail trade; …

Transportation and storage

Accommodation and food …

Information and communication

Financial and insurance activities

US$ mm

1,010

1,385

410

153

25

82

458

517

42

201

122

1,500

Agriculture, forestry and fishing

0 500 1,000

Manufacturing

Electricity, gas, steam and air …

Water supply; sewerage, waste …

Construction

Wholesale and retail trade; …

Transportation and storage

Accommodation and food …

Information and communication

Financial and insurance activities

US$ mm

M O

N G

O L

I A

I N

V E

S T

M E

N T

S

U M

MI T

2

0 1

1

Mongolian exports resume its upward trend after 2009 recession

Resources-driven economy of Mongolia is vulnerable to commodity prices volatility

1%

4%26%

11%

51%

1%

2%4%

US$3,190 mm in Mineral Exports (2011 I-X)

Refined copper & Copper alloysZinc

Copper

Iron

Bituminous coal

Molybdenium

Fluor spar

1%

5%

35%

11%

35%3%

8%

US$1,837 mm in Mineral Exports (2010 I-X)

Refined copper & Copper alloysZinc

Copper

Iron

Bituminous coal

Molybdenium

Fluor spar

2 0

1 1

5P R E S E N T A T I O N M A T E R I A L

Source: National Development and Innovations Committee (NDIC) & National Statistics Office (NSO) – Sept 2011 Bulletin

51%Gold

35%

2%

3% Gold

127

1394

68 14767

2466

83 14259

3430

78 76

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

UK China Russia Canada

US$ mmMongolia’s major exports destinations

2009 2010 2011 (I-X)

0

500

1,000

1,500

2,000

2,500

3,000

3,500

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

US$ mmMining equipment and fuel imports contribute

to the surge in Mongolia’s trade deficit

Exports Imports

M O

N G

O L

I A

I N

V E

S T

M E

N T

S

U M

MI T

2

0 1

1

Inflation and currency outlooks

Annualized inflation is 10.8% with upside risk

� Generalized wage and price pressures from a booming economy, expansion in fiscal expenditures, and large government cash handout contribute to rising inflation.

� Given the overheating economy (20%+ GDP growth), rising policy rate measure (currently at 12.5%) is implemented to curb price increases.

� Yet, inflation is expected to reach 13% by 2011 year-end. Double-digit inflation is likely to prevail at least until 2013.

� BOM combats against inflationary pressure by 0

5

10

15

20

25

30

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

% Percentage change in average consumer prices(2005 – 2016F)1

Annualized inflation

Upward trend in inflation

2 0

1 1

6P R E S E N T A T I O N M A T E R I A L

Source: 1) IMF estimates (September 2011)

2) Bank of Mongolia, Exchange Rates Statistics

� BOM combats against inflationary pressure by tightening monetary policy to ensure economic stability.

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

1,000

1,100

1,200

1,300

1,400

1,500

1,600

1,700

2/1/2006 2/1/2007 2/1/2008 2/1/2009 2/1/2010 2/1/2011

MNT per US$ MNT vs USD (2006 – 2011)2

MNT vs US$

MNT – 13% appreciation against US$ in 2010, the world’s second best performing currency

Capital inflows and exports drive MNT

� Rising domestic consumption and demand for raw materials from industrialized countries contribute to MNT appreciation

� In 2010, coal exports increased 2.3 times to 16.6 mm tons, and iron exports increased 2.2 times to 3.5 mm tons.

� Further mild appreciation or FX stability is expected due to large capital inflows for major mining projects.

� With continued high real GDP growth, the real exchange rate will have to adjust, either through nominal appreciation or through inflation.

M O

N G

O L

I A

I N

V E

S T

M E

N T

S

U M

MI T

2

0 1

1

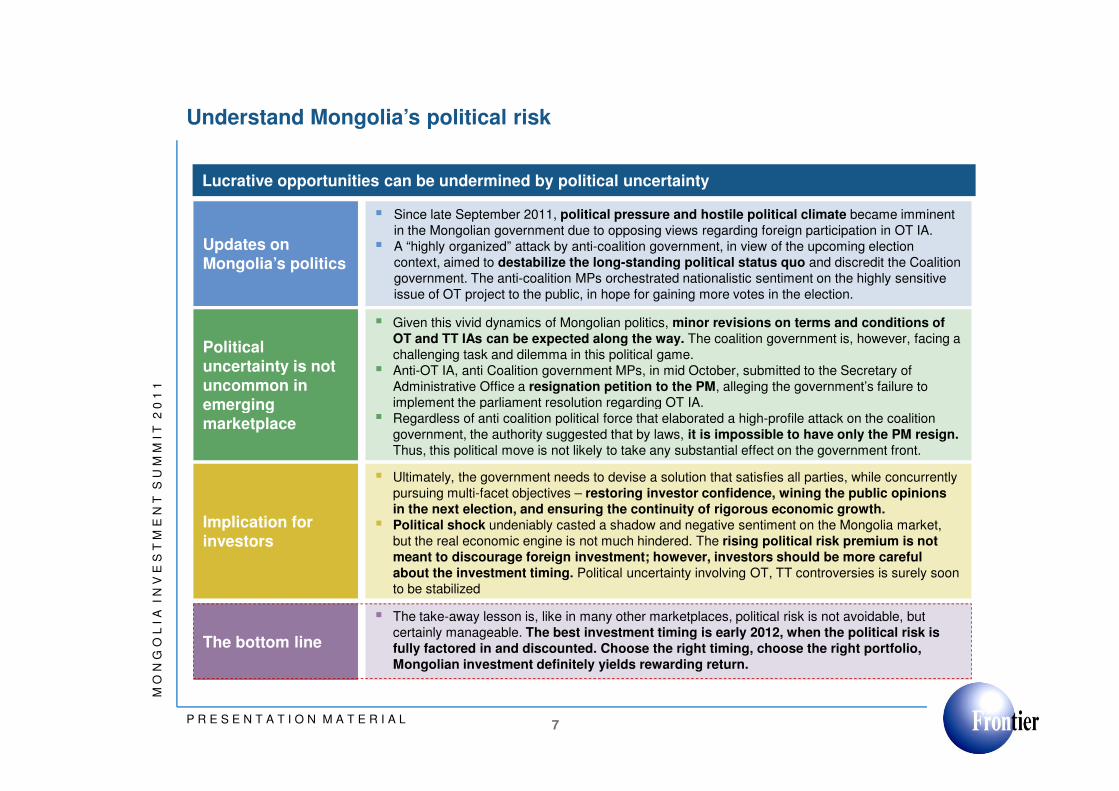

Understand Mongolia’s political risk

Lucrative opportunities can be undermined by political uncertainty

Updates on Mongolia’s politics

Political uncertainty is not uncommon in emerging

� Since late September 2011, political pressure and hostile political climate became imminent in the Mongolian government due to opposing views regarding foreign participation in OT IA.

� A “highly organized” attack by anti-coalition government, in view of the upcoming election context, aimed to destabilize the long-standing political status quo and discredit the Coalition government. The anti-coalition MPs orchestrated nationalistic sentiment on the highly sensitive issue of OT project to the public, in hope for gaining more votes in the election.

� Given this vivid dynamics of Mongolian politics, minor revisions on terms and conditions of OT and TT IAs can be expected along the way. The coalition government is, however, facing a challenging task and dilemma in this political game.

� Anti-OT IA, anti Coalition government MPs, in mid October, submitted to the Secretary of Administrative Office a resignation petition to the PM, alleging the government’s failure to implement the parliament resolution regarding OT IA.

2 0

1 1

7P R E S E N T A T I O N M A T E R I A L

emerging marketplace

implement the parliament resolution regarding OT IA. � Regardless of anti coalition political force that elaborated a high-profile attack on the coalition

government, the authority suggested that by laws, it is impossible to have only the PM resign. Thus, this political move is not likely to take any substantial effect on the government front.

Implication for investors

� Ultimately, the government needs to devise a solution that satisfies all parties, while concurrently pursuing multi-facet objectives – restoring investor confidence, wining the public opinions in the next election, and ensuring the continuity of rigorous economic growth.

� Political shock undeniably casted a shadow and negative sentiment on the Mongolia market, but the real economic engine is not much hindered. The rising political risk premium is not meant to discourage foreign investment; however, investors should be more careful about the investment timing. Political uncertainty involving OT, TT controversies is surely soon to be stabilized

The bottom line

� The take-away lesson is, like in many other marketplaces, political risk is not avoidable, but certainly manageable. The best investment timing is early 2012, when the political risk is fully factored in and discounted. Choose the right timing, choose the right portfolio, Mongolian investment definitely yields rewarding return.

M O

N G

O L

I A

I N

V E

S T

M E

N T

S

U M

MI T

2

0 1

1

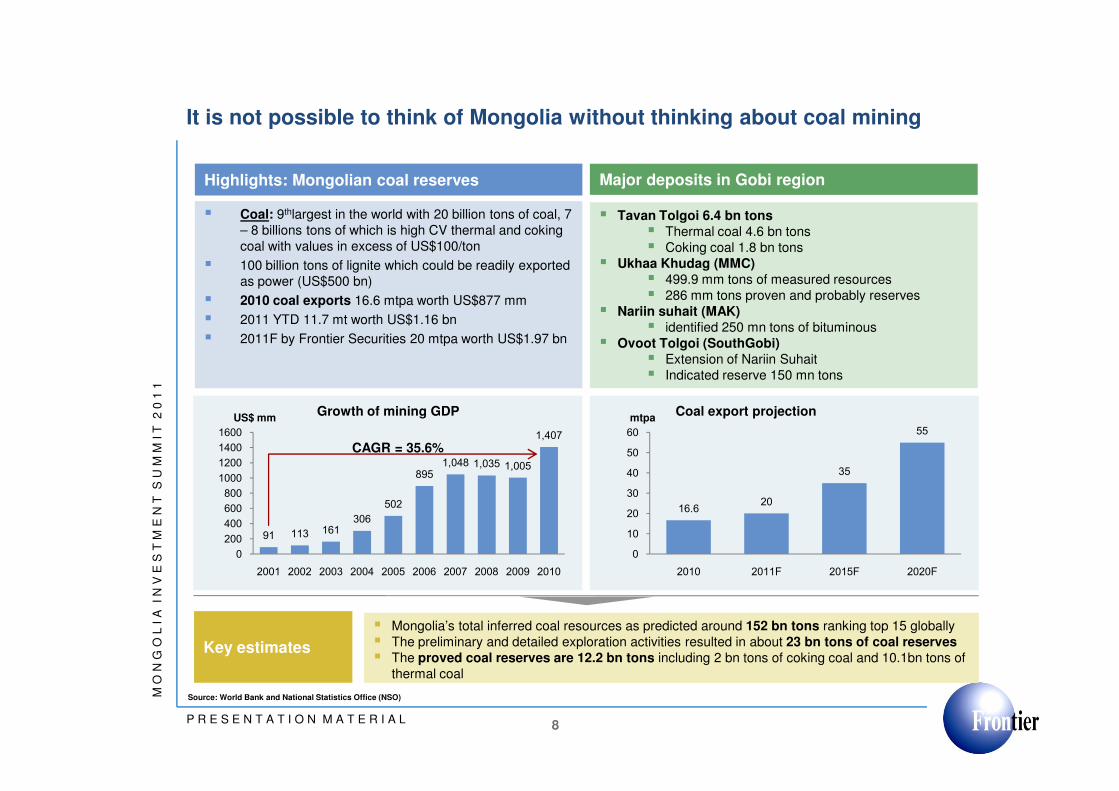

It is not possible to think of Mongolia without thinking about coal mining

Major deposits in Gobi region

� Tavan Tolgoi 6.4 bn tons � Thermal coal 4.6 bn tons� Coking coal 1.8 bn tons

� Ukhaa Khudag (MMC)� 499.9 mm tons of measured resources� 286 mm tons proven and probably reserves

� Nariin suhait (MAK)� identified 250 mn tons of bituminous

� Ovoot Tolgoi (SouthGobi)� Extension of Nariin Suhait� Indicated reserve 150 mn tons

Highlights: Mongolian coal reserves

� Coal: 9thlargest in the world with 20 billion tons of coal, 7 – 8 billions tons of which is high CV thermal and coking coal with values in excess of US$100/ton

� 100 billion tons of lignite which could be readily exported as power (US$500 bn)

� 2010 coal exports 16.6 mtpa worth US$877 mm

� 2011 YTD 11.7 mt worth US$1.16 bn

� 2011F by Frontier Securities 20 mtpa worth US$1.97 bn

2 0

1 1

8P R E S E N T A T I O N M A T E R I A L

Key estimates

� Mongolia’s total inferred coal resources as predicted around 152 bn tons ranking top 15 globally� The preliminary and detailed exploration activities resulted in about 23 bn tons of coal reserves� The proved coal reserves are 12.2 bn tons including 2 bn tons of coking coal and 10.1bn tons of

thermal coal

Source: World Bank and National Statistics Office (NSO)

16.620

35

55

0

10

20

30

40

50

60

2010 2011F 2015F 2020F

mtpaCoal export projection

91 113 161306

502

895

1,048 1,035 1,005

1,407

0

200

400

600

800

1000

1200

1400

1600

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

US$ mmGrowth of mining GDP

CAGR = 35.6%

M O

N G

O L

I A

I N

V E

S T

M E

N T

S

U M

MI T

2

0 1

1

Mineral assets’ geographical locations: an ultimate blessing

Mining sector is the driving force of resources-rich Mongolia

2 0

1 1

9P R E S E N T A T I O N M A T E R I A L

Coking coal Bituminous coal Sub-bituminous coal Lignite

Most developments located hereMost mining developments are located in South Gobi area

Source: The Mineral Resources Authority of Mongolia (MRAM)M O

N G

O L

I A

I N

V E

S T

M E

N T

S

U M

MI T

2

0 1

1

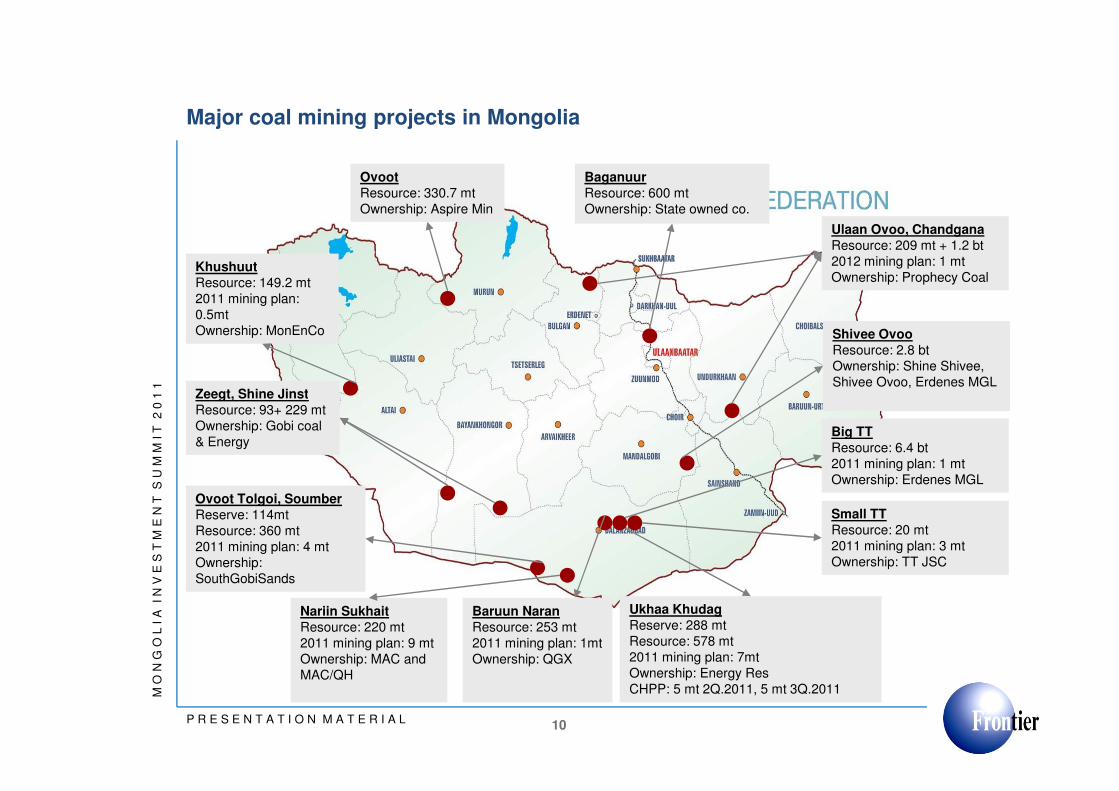

Major coal mining projects in Mongolia

KhushuutResource: 149.2 mt2011 mining plan: 0.5mtOwnership: MonEnCo

Zeegt, Shine Jinst

OvootResource: 330.7 mtOwnership: Aspire Min

Ulaan Ovoo, ChandganaResource: 209 mt + 1.2 bt2012 mining plan: 1 mtOwnership: Prophecy Coal

Shivee OvooResource: 2.8 btOwnership: Shine Shivee, Shivee Ovoo, Erdenes MGL

BaganuurResource: 600 mtOwnership: State owned co.

2 0

1 1

10P R E S E N T A T I O N M A T E R I A L

Zeegt, Shine JinstResource: 93+ 229 mtOwnership: Gobi coal & Energy

Ovoot Tolgoi, SoumberReserve: 114mtResource: 360 mt2011 mining plan: 4 mtOwnership: SouthGobiSands

Nariin SukhaitResource: 220 mt2011 mining plan: 9 mtOwnership: MAC and MAC/QH

Baruun NaranResource: 253 mt2011 mining plan: 1mtOwnership: QGX

Ukhaa KhudagReserve: 288 mtResource: 578 mt2011 mining plan: 7mtOwnership: Energy ResCHPP: 5 mt 2Q.2011, 5 mt 3Q.2011

Small TTResource: 20 mt2011 mining plan: 3 mtOwnership: TT JSC

Big TTResource: 6.4 bt2011 mining plan: 1 mtOwnership: Erdenes MGL

M O

N G

O L

I A

I N

V E

S T

M E

N T

S

U M

MI T

2

0 1

1

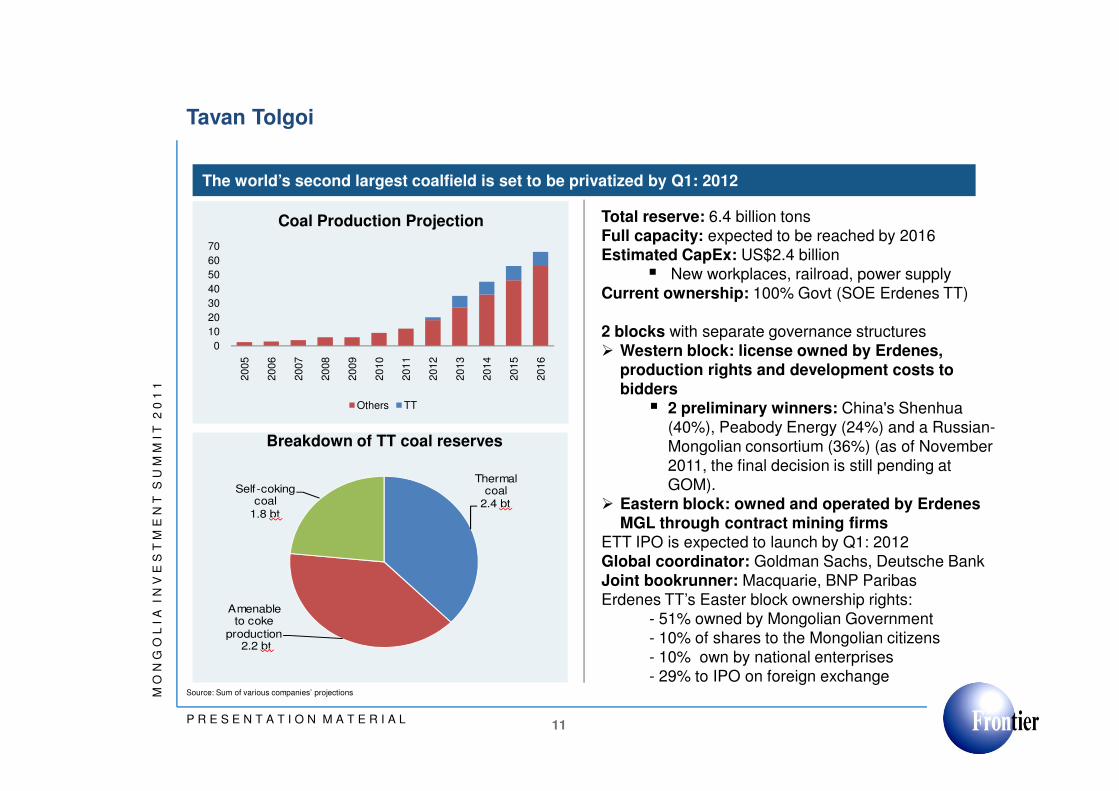

Tavan Tolgoi

The world’s second largest coalfield is set to be privatized by Q1: 2012

Total reserve: 6.4 billion tonsFull capacity: expected to be reached by 2016Estimated CapEx: US$2.4 billion

� New workplaces, railroad, power supplyCurrent ownership: 100% Govt (SOE Erdenes TT)

2 blocks with separate governance structures� Western block: license owned by Erdenes,

production rights and development costs to bidders

�

0

10

20

30

40

50

60

702005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

Coal Production Projection

0

10

20

30

40

50

60

702005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

Coal Production Projection

2 0

1 1

11P R E S E N T A T I O N M A T E R I A L

bidders� 2 preliminary winners: China's Shenhua

(40%), Peabody Energy (24%) and a Russian-Mongolian consortium (36%) (as of November 2011, the final decision is still pending at GOM).

� Eastern block: owned and operated by ErdenesMGL through contract mining firms

ETT IPO is expected to launch by Q1: 2012Global coordinator: Goldman Sachs, Deutsche BankJoint bookrunner: Macquarie, BNP ParibasErdenes TT’s Easter block ownership rights:

- 51% owned by Mongolian Government - 10% of shares to the Mongolian citizens- 10% own by national enterprises- 29% to IPO on foreign exchange

Thermal coal

2.4 bt

Amenable to coke

production 2.2 bt

Self-coking coal

1.8 bt

Source: Sum of various companies’ projections

Others TT

Breakdown of TT coal reserves

Others TT

M O

N G

O L

I A

I N

V E

S T

M E

N T

S

U M

MI T

2

0 1

1

Oyu Tolgoi (66% owned by Ivanhoe Mines)

0

0.2

0.4

0.6

0.8

1

1.2

Ou

nces (

Mil

lio

ns)

OT Gold Production Projection

0

200

400

600

800

1000

1200

1400

1600

1800

Lb

s. (M

illi

on

s)

OT Copper Production Projection

I T

2

0 1

1

12P R E S E N T A T I O N M A T E R I A L

Source: Ivanhoe Mines IDP-10 & Frontier Securities’s projections

Total Reserve: 81 billion lbs. of copper, 46 million oz of goldExpected production: 2013 Projected investment: US$4.6 billion in pre-production capitalNPV at today’s metal prices: US$15 billionBenefits/contribution to Mongolian economy:� average 34% increase in real GDP over 30 years� average 71.6% increase in export� average 10.3% increase in employment� up to 48 thousand new workplaces over the project life

time

Oyu Tolgoi Investment Agreement (In full legal effect since March 2010)� Integrated Development Plan is released� Stabilized custom regime� Abolishment of Windfall tax� Government ownership 34% � Private investment in auto roads� Loss rollover period of 4-8 years� Stabilized tax regime� 95% Mongolian employees

OT has the mineral resources to become one of the world’s top 3 copper-gold producers

M O

N G

O L

I A

I N

V E

S T

M E

N T

S

U M

MI T

2

0 1

1

Disclaimer

Information in this presentation does not constitute invitation or application or investment advice or service provisionfor sale and purchase of any stock, future, option or other financial product by Frontier Securities and its relatedcompany. This presentation is not the recommendation to make a specific trade and guarantee for a specific productwhether it is appropriate or adequate for buyers. Also, although this presentation is prepared from the variousinformation sources we deem reliable, we shall not guarantee their accuracies and rightness. Moreover, pastperformances do not suggest or guarantee for the future results. Thus, the Company shall not take responsibility forthe loss out of the decision based on its content. When making a contract on trades using the information in thispresentation, please consult with your business advisor, lawyer, tax & accounting advisor about investment productprices, compatibility, value or other items beforehand. Information and services in this presentation and its provision orusage shall not contradict to the applied laws and work guidelines or regulations of self regulating organization or shallnot be provided in the legal frame which does not admit such information and its provision; in the legal frame naturalperson or legal body shall not use those information and service. Some of the products and services in thispresentation may not be applied for all the legal frames or not all customers may not use. Also, the Company may

2 0

1 1

P R E S E N T A T I O N M A T E R I A L

presentation may not be applied for all the legal frames or not all customers may not use. Also, the Company maychange or delete information or others items in this presentation without previous notice.

Contact:Frontier SecuritiesEmail: [email protected]: +976-70119999Address: #705, Blue Sky TowerPeace Avenue 17, 1st khorooSukhbaatar, District,Ulaanbaatar, Mongolia

M O

N G

O L

I A

I N

V E

S T

M E

N T

S

U M

MI T

2

0 1

1